The bond market’s reaction to the inflationary environment, to fears of a lax Fed, and to a Mississippi River of new debt.

By Wolf Richter for WOLF STREET.

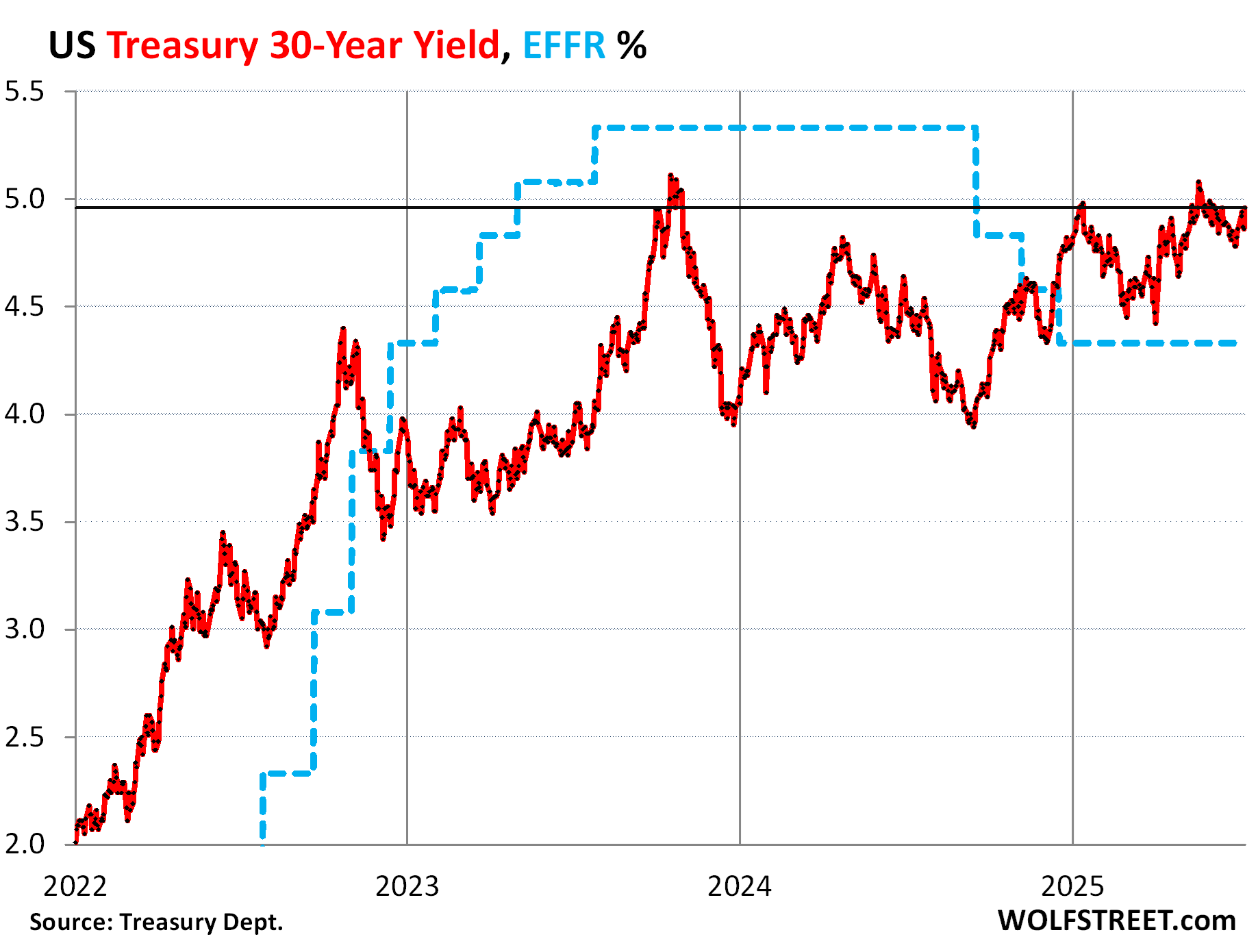

The 30-year Treasury yield rose by 10 basis points on Friday to 4.96%, despite a 30-year Treasury auction on Thursday that was described as “solid” and “strong,” where the government sold $22 billion of 30-year bonds at a yield of 4.89%.

So far in July, the 30-year yield has risen by 18 basis points. It is now 63 basis points above the effective federal funds rate (EFFR), which the Fed targets with its monetary policy rates (blue in the chart).

This increase in yield came despite the government’s assurances that it would only slowly replenish its checking account, the Treasury General Account – which had been partially drained during the debt-ceiling period – by taking it easy on issuance of long-term notes and bonds, and by slowly increasing the issuance of short-term T-bills, all in order to defuse the pressures around long-term yields, while short-term yields are bookended by the Fed’s policy rates and expectations of those policy rates over the near term.

So, since the Fed cut by 100 basis points starting in September (dotted blue line), the 30-year yield (red line) has risen by 102 basis points!

The 30-year yield is a thermometer of the bond market’s current fears about:

- Inflation over the long term

- A lackadaisical Fed in face of this inflation

- And a Mississippi River of new Treasury debt flowing into the market.

That the 30-year yield is back near 5% amid all these efforts to keep it from going there is quite something.

This reaction – rate cuts of 100 basis points lead to a 102-basis-point increase of the 30-year yield – raises the secret question: How many more rate cuts would it take to drive the 30-year yield to 6%?

Cutting policy rates in an inflationary environment has turned out to be a very tricky thing. Bessent may have had this type of conversation with Trump, but it likely went in one ear and out the other.

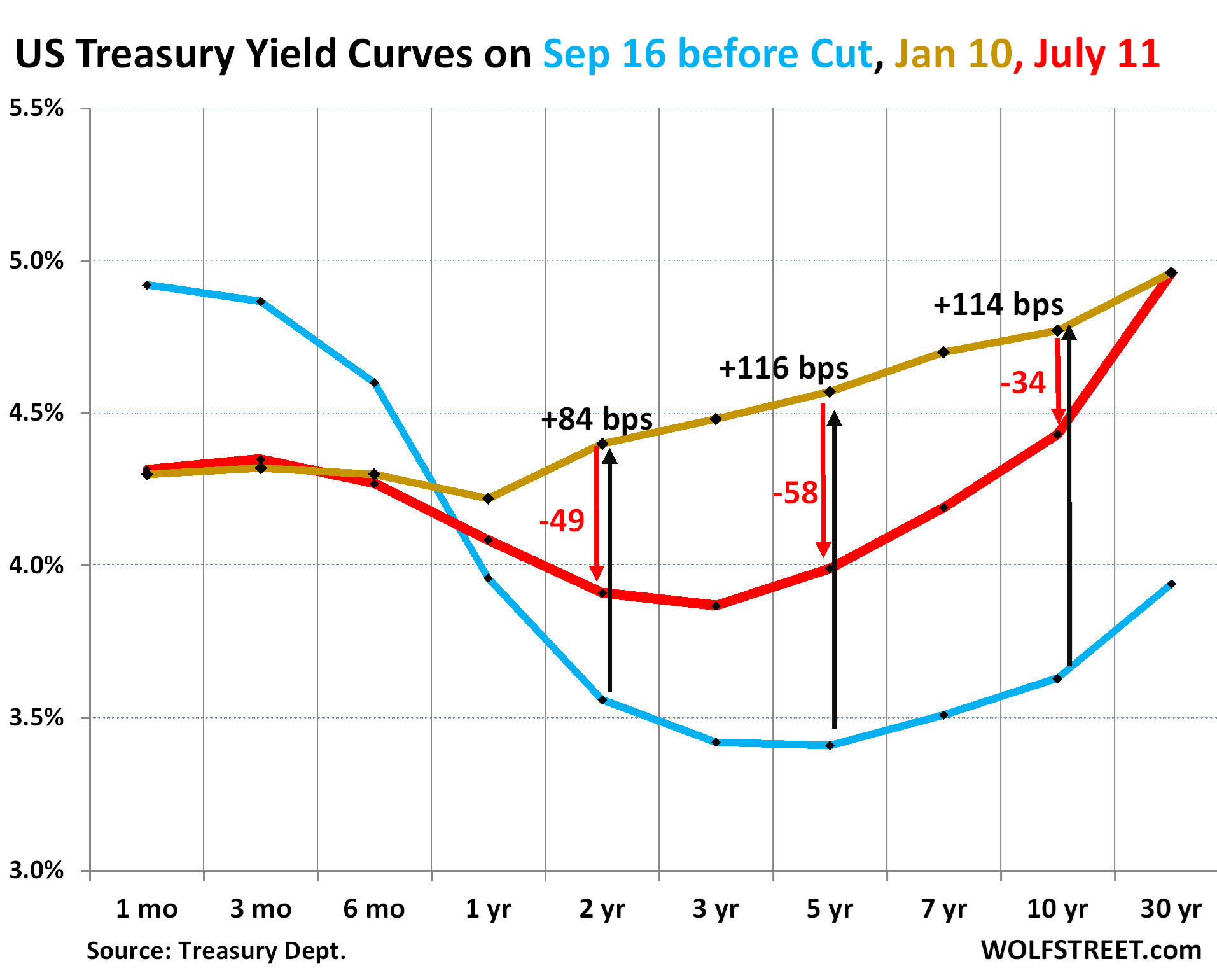

The yield curve: bond anxiety.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Red: Friday, July 11, 2025.

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

With rate cuts still on ice, short-term yields up to six months haven’t budged much and remain glued to the EFFR of 4.33%. But rate-cut expectations have pushed down yields over six months and into the five-year range.

What is pushing up long-term yields are the other factors: inflation expectations over the long-term, concerns over a lackadaisical Fed in face of this inflation, and a Mississippi River of supply flowing into the market that has to be absorbed by additional buyers that may have to be enticed with higher yields.

So, at the long end, the yield curve has steepened. The 10-year yield is higher than all yields shorter than 10 years:

- Between 8-16 basis points higher than 1-6-month yields

- About 52 basis points higher than the 2-year yield

- About 56 basis points higher than the 3-year yield

And the 30-year yield is right back where it had been on January 10, just a hair below 5%.

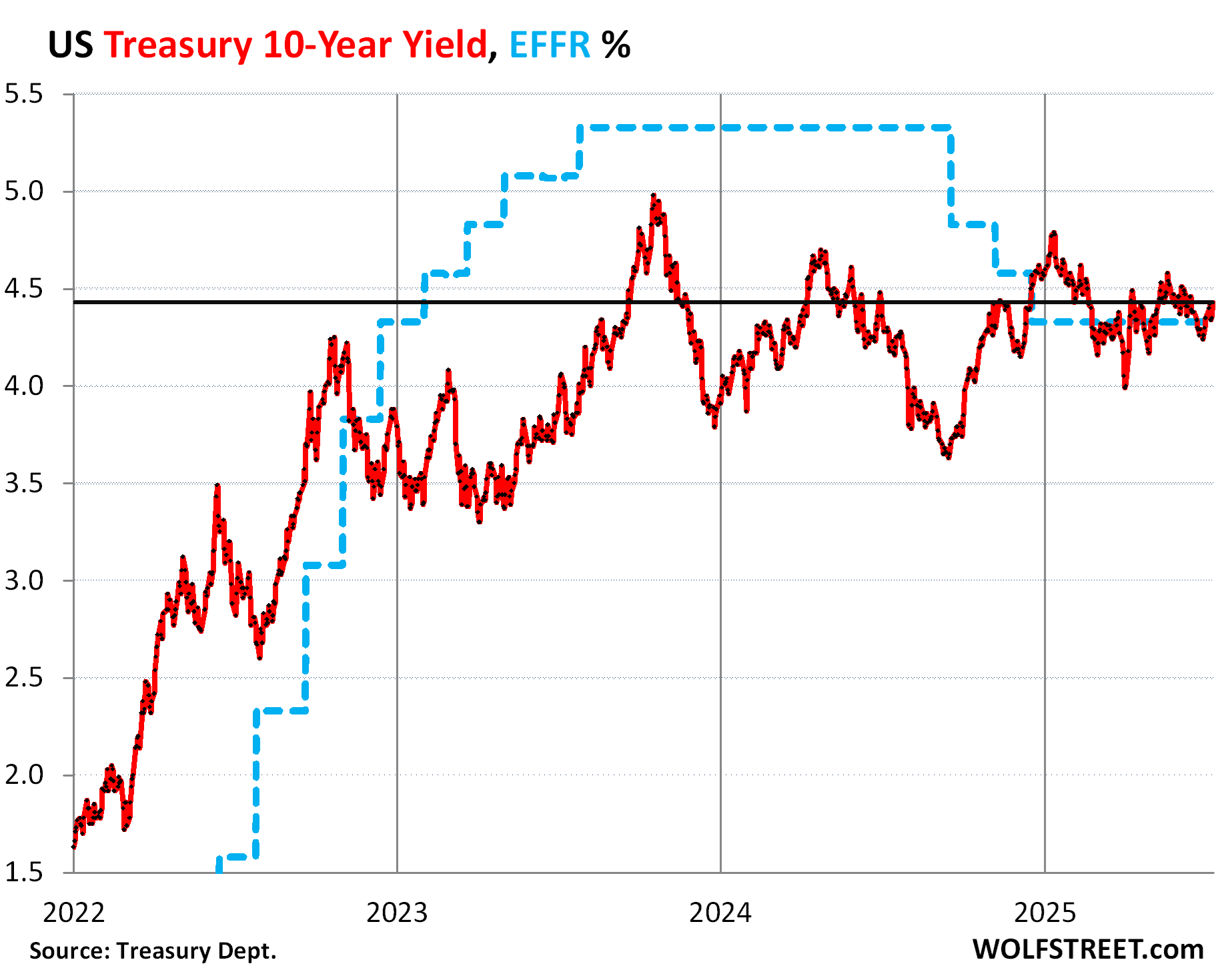

The 10-year Treasury yield has been hovering near the EFFR for months. But it too has risen: by 8 basis points on Friday, by 19 basis points so far in July, and by 80 basis points since the eve of the Fed’s rate cuts.

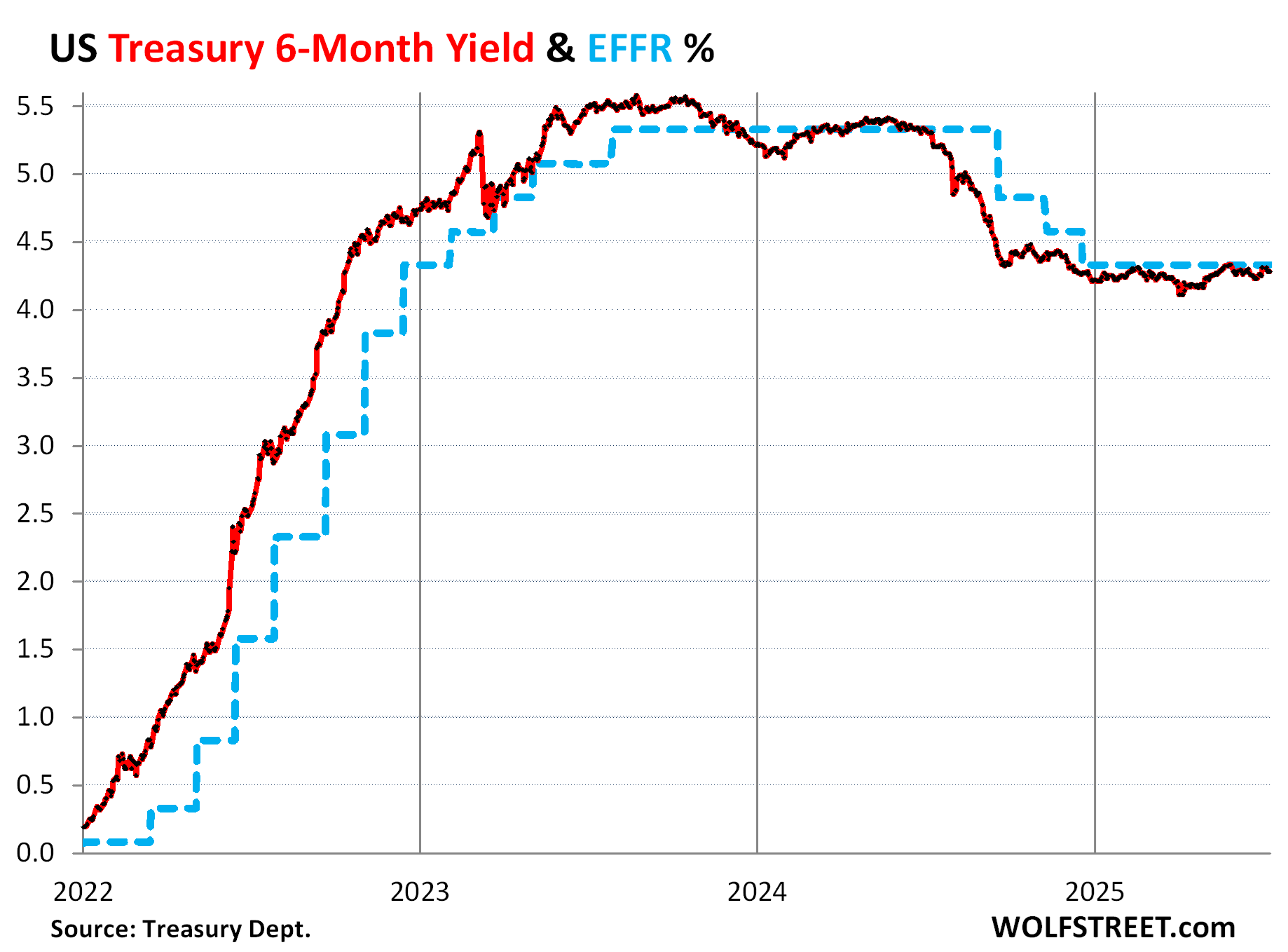

The six-month yield, which is a good indication of market expectations for cuts within 2-3 months, has been glued to the underside of the EFFR and is thereby not yet predicting rate cuts within 2 to 3 months.

The FOMC’s September meeting, with a rate decision to be announced on September 17, is just on or beyond the outer edge of the 6-month yield’s vision. So going forward, we’ll watch the 6-month yield for indications of a September rate cut.

But there is now substantial disagreement among the FOMC members about rate cuts. The CPI report next week may shift their rate cut rhetoric into one or the other direction, and the 6-month yield would then begin to react to it.

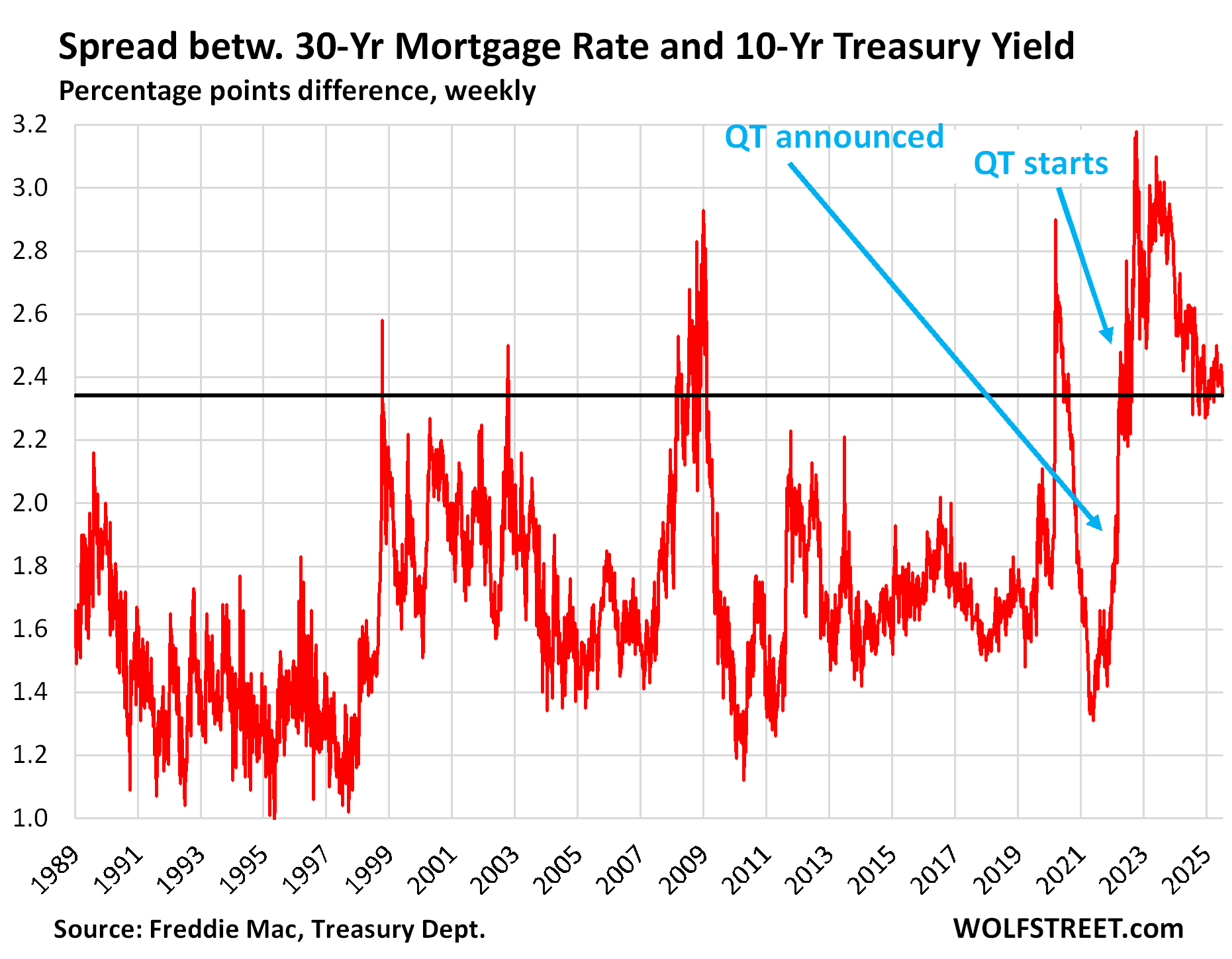

For 30-year fixed mortgage rates, the 10-year yield and the spread matter.

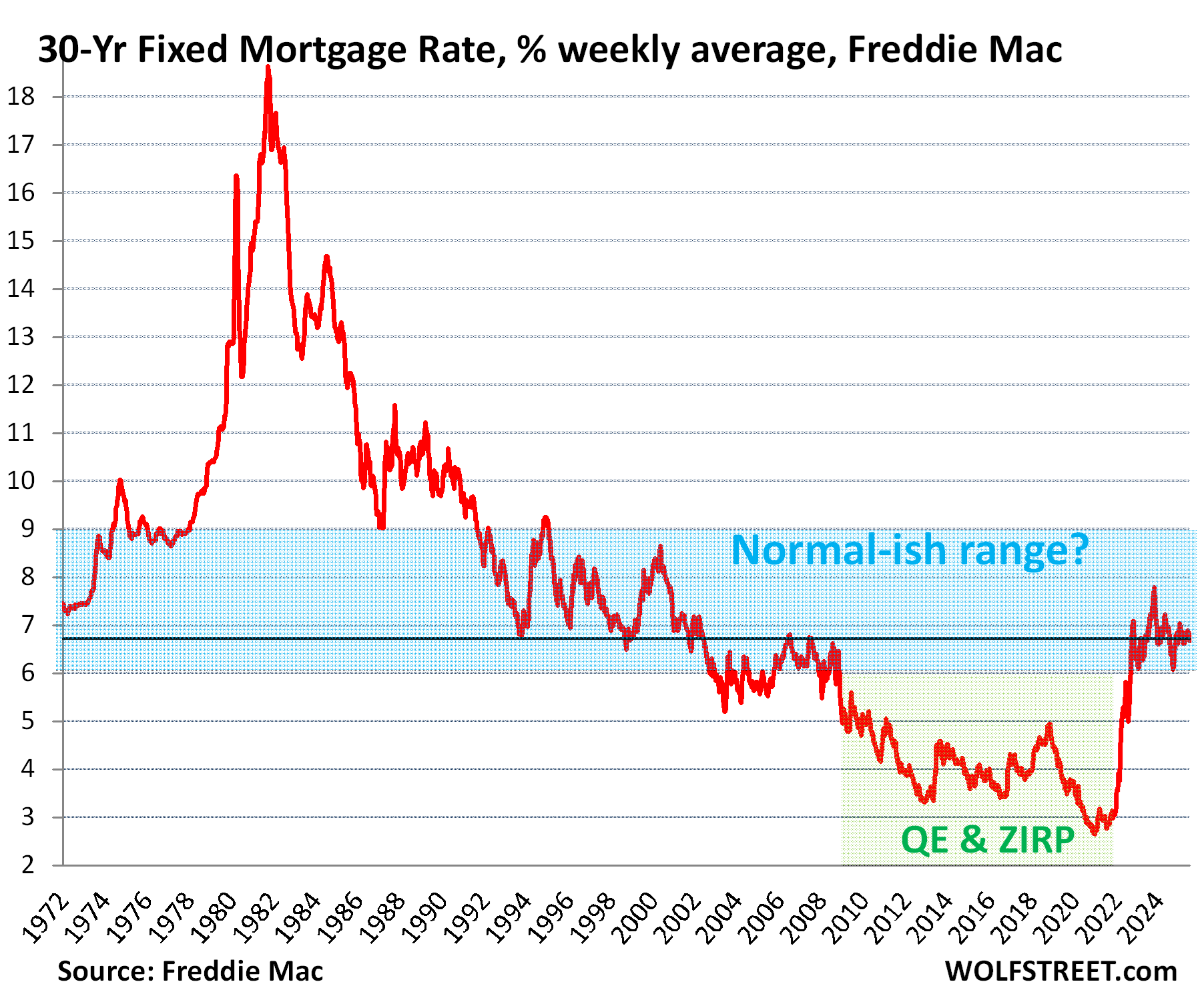

The average 30-year fixed mortgage rate has been above 6% since September 2022 and has stuck fairly closely to either side of 7%.

In the latest reporting week, which does not yet include the rise of the Treasury yields over the past few days, the average 30-year fixed mortgage rate ticked up to 6.72%.

It didn’t drop to 5% until the Fed started QE, including buying trillions of dollars of MBS, from early 2009 on, which helped push down mortgage rates. But the consumer price inflation that broke out in 2021 put an end to it.

The spread between the average 30-year fixed mortgage rate and the 10-year yield has been fairly wide since the Fed ended QE and thereby stopped buying MBS, and then started QT in the second half of 2022, thereby starting to unload its MBS. It has by now unloaded over $600 billion of its MBS, and has said many times that it wants to get rid of its MBS entirely, and only hold Treasury securities on its balance sheet.

The spread between the weekly average 30-year mortgage rate and the weekly average 10-year Treasury yield was 2.34 percentage points. Over the past four decades, that happened only four times, twice very briefly just before and at the end of the Dotcom Bust, and twice during two panics, when the 10-year yield plunged amid massive QE, and mortgage rates were slower to follow. Now there is no panic, the 10-year yield is near 4.5%, and the Fed is doing QT..

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Long term bonds still don’t pay enough. Interest rates are too low which is why capital is flowing to stocks and bitcoin. RIP Treasurys.

Exactly right. Risk assets still the best way to butter your bread. I’d say a relatively risk free 5% is alright if you’re already rich looking for somewhere to park your money. But for the rest of us treasuries make 0 sense.

Except that it only works if stocks can continue expanding based on multiples. At some point, there will be a change in psychology, and those risk assets will plummet.

Someone who gets it. A rare instance these days. The only thing keeping risk assets levitating….the very fact that there’s very few left who think anything could drop in value.

“I’d say a relatively risk free 5% is alright if you’re already rich looking for somewhere to park your money. ”

What would say “rich” is?

Harvey,

From your prior posts, I think I am fiscally conservative like you. You have a very good question on what is rich .

I consider rich in retirement as making enough to live comfortably for 30 years after I retire.

If I had a million dollars saved, could I live for 30 years at 5% (50K/year) in a very safe investment? Add in SS and it would be 75k per year. If I had no debt or mortgage, that should be doable. I eat less every year.

Eventually, inflation would eat away at the buying power of that 50K per year so I’d have to start taking principal from somewhere else since that million is locked up in a 30 year treasury. I’d wait until 10 year treasuries reached 5-6% so I could re-evaluate at age 75 a and maybe consider taking some principal to get me through my remaining 20 years(if I’m lucky).

That’s my conservative view on being rich. If I had a million dollars and inflation stayed below 5% I could live a comfortable life.

Your results may vary.

@BobE,

Thanks for the response. As a 62-year-old, these kinds of topics are on my mind all the time.

Horrible advice.

Crypto is rat poison. Treasurys are exactly what you want in a recession

10-year treasury is not “relatively risk-free” when your principal could go down in value significantly…

I agree if you are trading bonds or have a situation where you have to sell the bonds at whatever the going bond price. Similar to the difference in investing in a house vs living in a house. If I live in a house or own a bond to maturity, I have much less worry.

I view bonds as an investment that I will hold to maturity. You get exactly what you were promised. 5% for 30 years and then you get all of your principal back.

That’s why bonds won’t be attractive to me until rates increase more. Then I will collect the cash every 6 months, pay my bills, and live a very comfortable life (well, unless inflation is higher than 5% and I have to cash out my bonds at a loss to pay my bills.) No worries about 20-30% stock market or housing crashes.

In fact, if housing crashes 30%, I’d likely pay less in insurance and property taxes.

I envy my silent generation parents who purchased 10 or 30 year Treasuries in the early 80’s at a 15-16% rate. They lived well and slept well at night.

That stuff only happens to SVB bank. Don’t you worry about long bonds.

I consulted with the “Oracle of Omaha” & he said any bad mouthing of Treasuries is Blasphemy.

Wolf will back me up on this…. maybe.

Duration can make sense. I own a couple CDs and agencies with 10-15 years till maturity in my 401(k) portfolio.

I’m just saying it’s not accurate to call it “relatively risk-free” especially when interest rates are marching higher.

Yes, you need high 10-year real-rates of interest. At 1.87 interest rates on 2025-06-01, interest rates yield less than can be found in too many other areas.

The correct measure is to lower FDIC insurance rates, aka, the “taper tantrum” driven from the drop from unlimited transaction accounts to $250,000 limits.

Trump gonna need a super volcker not petty powell

Any Chairman of the Federal Reserve becomes just one of the twelve members of the FOMC which establishes policy interest rates – all of which are short term interest rates.

Say what you will about Powell. He certainly isn’t perfect. But he has been sticking to QT when he had many opportunities to revert back to QE before inflation really bit hard. After Helicopter Bernanke and Yellen, he’s relatively decent.

Powell destroyed the housing market. Even someone as clueless as me was left in amazement as he kept pumping the housing market a full year after housing reached all time highs. Kept interest rates at zero, kept buying mbs. How could that not be intentional if someone like me can see that?

Good night. Housing is 40% more expensive in most of the country compared to 2019. Powell had one job. He failed.

We need to raise Volcker from the grave.

Dig up his grave. Get his DNA. Start cloning an army of Volkers.

That’s my idea. Not your idea. Don’t take credit it for it.

On another matter, I’ve stated before that I’m the dumbest man on this comment section. But if buying T-bills is good enough for buffet, then it’s good enough for me.

Bitcoin still hasn’t made a new high priced in euros. It has in yen and Canadian dollars. Capital flows, risk has been back on. However, The USA stock market hasn’t made new highs in any currency but $USD. The ROW haven’t seen new highs in the US stock market once they convert back into their homeland currency!! If the USA has the reserve currency we also have a reserve asset Destination for surplus capital being invested USA equities. When will the ROW bail on their USA assets holdings? When they do Americans won’t be able to keep the risk on party going. Technically, damage was done in the April sell off and the $USD weakness is the only reason we are sitting at all time highs right now, priced in a world currency basket we are 4% below all time highs that were made in Dec 2024.

@Joseph

Correct. I expect long-term inflation to be 6%, which means that current T-Bond rates are WAY too low.

Of course, I remember the 1970s very well. . .

So you could either have your money 100% secured in a treasury making 2% after inflation, for a real return.

OR

Wait for Bitcoin to crash and moan with the rest of the losers?

look up bimetaliasm from over 100 years ago, see how that worked out. Lol

Cool, rooting for 6% or higher soon, so I can eventually just park most of my money there, despite the short term cut soon and Tbill will be not as attractive. Sure is nice if we don’t go back to any TINA environment and force to buy stock in these ridiculous valuation now.

On the hand, the mortgage spread sure is nice to see, hopefully it will hold. Nothing better than to see that to use it as a STFU to all the genius and RE agents brain deadly repeating cutting short term rates will mean lower mortgage rates..so date that rates now…

Always liked the longtime real estate agents using pictures from their Junior Prom.

Phoenix_Ikki,

We all have hope.

The wildcard would be if our leader decides any new Fed chief should start QE again by buying MBS’s, CMBS’s, and 10 and 30 year Treasuries to flatten the yield curve and drive up RE prices. Wealthy people are on the hook these days and not banks. They want to be paid.

That would make life interesting but anything is possible these days.

I don’t think anything the Fed does right now can reassure the market with the chaotic policies coming from Pres tirade tariff. No one knows what is coming tomorrow and that’s what is showing. The constant undermining of the Fed isn’t helping anything either.

The tariffs brandished by Trump like a sword will not always be there. They are primarily a negotiating tool used by the Donald to get a better deal for his own country. Trump often goes on the offensive when he senses he has the upper hand, and for him America’s wealth and absorption of foreign goods means the U.S. has the firm upper hand.

Trumps tariffs and threats random are disingenuous and thus ineffective ,and other countries know it. To think countries won’t offer a strong response to his nonsensical actions is naive

What will they do? Raise their prices and incentive us to produce our own goods here?

@Blake, that’s just naive. There’s a myriad of ways blocks like the EU could pressure the US economically. They are not doing it because they know this temper tantrum of an admin will pass and they have long-term stakes in strong trans-atlantic collaboration. Doesn’t even have to be the EU, individual countries could take steps as well if the sentiment sours.

Regardless of the patience of our partners, some of the damage is already done, as evidenced by the article above. Money talks.

Jorg,

“the patience of our partners, some of the damage is already done, as evidenced by the article above. Money talks.”

I assume you mean Europeans not buying Treasuries? Not happening, except in your wishful thinking. I posted this already below in reply to another comment, but here it is again:

@Wolf,

In light of your article the ‘damage done’ refered to the bond market reacting to the mounting uncertainty. I’d say these yields are not going to lower anytime soon given that the german debt ceiling is gone and that eurobonds is no longer a forbidden word thanks to the 5% on defense man. But yeah, I stand by my argument that there’s many more ways to exert pressure apart from raising the prize on Ozempic.

It’s not wishful thinking btw, just thinking, I have no stake in it. Just pointing out a fallacy.

Personally I think all the hate for Powell and saying he needs to cut rates is PR for his fan base. He’s a real estate guy which means he should understand the bond market, cutting in this environment seems unlikely to lower the 10 year rates or mortgage rates. Cutting isn’t going to fix the demand issues for CRE – with buildings vacant there’s still going to a be a large risk premium built into any refi.

What I think cutting short term rates will do is prop up the stock market and the economy because below 4% (basically 3% after taxes) it makes no sense to have money parked there so instead people will spend or invest in the stock market

“He’s a real estate guy which means he should understand the bond market….”

LOL! He’s a real estate SALES guy. Giant difference.

The question is not what Powell will do, it’s whether the FOMC members as a whole can withstand domination by Trump. So far, Congress and SCOTUS have not.

If FOMC capitulates and puts Trump over inflation and employment, we’re in for a wild ride.

Admittedly that would be a wild ride.

But what would you call the inflation of 2021-2023? Hard to imagine it being as wild as that Fed self inflicted disaster.

That’s a fact!

Does the US $ dropping %18 against the Euro affect bonds?

If anything, it would make them more attractive to euro-based investors, and so they would bid up their price (push down their yields). Some of this is happening for whatever reason, because US Treasuries are immensely popular with EU investors (red line), but not so much with Chinese investors (blue).

Is it a problem for organisations that owned bonds when the dollar was strong?

For new euro investors, the drop in the dollar is an opportunity because those bonds are now cheaper for euro investors.

For euro-investors that have owned these bonds for a while, the drop in the dollar means lower euro-value of those bonds.

This assumes that they’re not hedged.

The same with yields: when yields drop, existing investors make money. When yields rise, existing investors lose money.

But for new investors rising yields (lower price) are more attractive.

Keep it coming! I want the 18% mortgages we’ve heard SO much about. That’s how a generation learns the value of hard work and to pull themselves up by the bootstraps, right?

Bring it on.

I had one. It was not fun, but we got through it.

Similar to AA, we had a mortgage at that rate in 1979,,, but, and it’s a huge butt, the house cost $40K, and with 20% down payments were quite affordable.

Last time I looked, that house sold for $800K, and now valued over a million.

Everyone needs to read this comment over and over again until they understand.

I sure hope so. I’d rather buy an affordable home like the boomers got to in the 70s and 80s that I can make balloon payments against than to pay half a million for a crappy median priced home at a 7% rate.

Literally the greatest leg-up a generation ever received

The reason homes are selling for “half a million” is because BUYERS were eager to pay that much for them — they trampled all over each other to pay that much for a “cappy” home. QUIT BUYING HOMES, let boomers sell their homes to the angles in the sky, and prices will come down. It’s BUYERS who drove up prices, not sellers.

And a large number of people has quit buying homes, so that’s step in the right direction.

Incomes are a LOT higher than they were back then, and they continue to grow, so home prices don’t need to fall back to price levels of the 80s to make sense today, but they do need to fall.

Institutional investors, like private equity took the crown as the majority home purchaser from 2021 to 2023. It’s not a people buying houses problem. Normal people got trampled by rich people bidding up houses over others as an investment, driving up the prices.

18% mortgages would be fine if a $500k house suddenly became sellable for $200k.

Some group is going to get hurt and some group may benefit.

Have you seen credit card rates? Like 27.99%

I remember when 9.99% was punishing.

There’s no way you can get out from under 25,000$ at 27.99%. I bet a lot are figuring this out atm

I was told we would be greating again, not suffering our way to virtue.

Apparently it is “exact maximum pain”

I dunno if that was the plan all along, it’s def not an effective campaign slogan.

“We’re going to just do everything bad and painful to anyone not extremely wealthy.”

It just does not propel people to the polls on your side.

Luckily they waited until the election was over to show the cards.

I mean otherwise not very smart the other way.

1969 all over again? Bessent the next Burns?

1969 was a good year as I began my career in oil and doubled my wages.

You mean Powell the new Burns. This guy waited too long to raise rates while at the same time Yellen didn’t change the stance of debt rollover to long term bonds when the 30 year was down.

Now, I am not an economist, but we’re about 50bps out of bounds on the funds rate. Yields are meant to be linear, however the 2 year lags. 30 year resurfaced for many reasons as mentioned above. One particular I’d note would be the paltry 5 billion a month of QT we are doing. Again another Powell disaster. Bessent received a disaster of an issue made by Yellen. Yellen worst treasury secretary in my lifetime.

I think Yellen knew she couldn’t sell the long term debt,and Bessent found that out about April 4

I’m not sure why when the 30 was low in 2021. Even government could have inserted at that low rare if buyers didn’t want it.

Now, we have a debt to gdp at 125%. Who would want long term debt.

Give Bessent the rest of his term …..

That can’t and won’t be done. Obviously. Bessent is an imbecile.

Are you too young to be alive during the tenure of the architect of monetary bubbles: Alan Greenspan?

Not suprised with the misallocation of funds all these years. Expect 10 year at 5% and 30 year at 6% shortly. Debt hasn’t been serviced in a long time and people want more return on investment with debt to GDP at 125%.

The US debt is ALWAYS services all the time. The only question is at what price. It is dangerous for it to be so heavily reliant on short-term rates versus long-term rates as it makes the cost of servicing it much more unpredictable and volatile.

In the past 30 years the USD has lost more than half its value. What you could buy for a $1 in 1995 now costs $2.11. In these circumstances what idiot would buy 30 year bonds paying 5%? The rate should be at least two or three times that to compensate.

A 30-year bond that pays 5% in interest pays $50 a year in interest on a $1,000 bond. Over a period of 30 years, that’s $1,500 in interest. And if you run a bond portfolio, you reinvest the interest in new bonds, the interest on the interest compounds for 30 years, and gains are far larger. If compounded semiannually at 5% for 30 years, you would end up after 30 years with the $1,000 bond, paid off in cash, plus about $3,400 in compounded interest, for a total of $4,400.

TIPS rate is 2.63%. Incredibly low still.

That’s actually pretty good because you also get the inflation protection added to the principal. The inflation protection is based on CPI and changes with CPI.

Yeah and you 100% of your principal back.

Even in worst case scenario.

The 5 year auction is in October I think.

I like the rule of 72 for quick math to show capital doubling. Divide 72 by 5(% return) and it takes 14.4 years to double your money. Obviously, no inflation adjustments in the simple rule of 72. The Nikkie was under its high mark set in 89/90 for ~3 decades, risk carries risk.

Think about it though, it’s 5% for 30 years.

The stock market won’t even be that consistent.

And at any time the stock market can lose 80% of its value.

The law of randomness

Once rates go down everyone will dream of 5% for 20 years

Is there another high volume financial asset that is guaranteed to the same degree as treasuries?

Not any $USD assets — treasuries are called “the risk free rate” for a reason.

They are guaranteed in US dollars. As WR has said many time a sovereign can’t default in its own currency, because it can just print it.

PS: if you are looking for a guarantee of purchasing power that is a different animal.

Well if you watch CNBC, it’s probably Nvidia #!@&*%!!!

The United States spends more on defense than all the other countries in the world combined. There is nothing more safe.

“spends more on defense than all the other countries in the world combined.”

That’s not correct. The US spends about as much as the next 9 biggest spenders combined. It spends about 3x as much as #2 China. So it still outspends everyone else by a wide margin, but it doesn’t outspend all of them combined.

The U.S. government’s interest expense is in the process of passing up the U.S. Defense spending.

A “solid” auction yet an increasing yield. Please correct me if I am wrong.

This, imho, sounds like a contradiction. For a solid auction there should be high demand with prices rising and yields falling.

Also interesting that the Chinese have lost their appetite for US treasuries. Maybe another reason for higher yields.

Andre-

It’s in the by-line: “Mississippi River of new debt.”

“Solid auction” demand is counterbalanced (and then some) by bulge in supply… thus long end prices decline marginally.

This is what “grinding higher” treasury yield market looks like. Expect about 40 years of “two steps forward, one step back” for long bond rates, in keeping with Homer and Sylla’s History of Interest Rates.

Thanks John “Grinding higher”,I like it. The Fed may drop interest rates but the market will ignore it. True rates will reign

Andre, my understanding of what the Fed considers a “solid” auction is one which results in a certain amount (I don’t know the quanta) of bidders left empty-handed — which is to say that the auction is “overbid.” Now, there is some question as to whether or not the structure of the auction itself is designed such that there will always be “overbidding” given that the primary dealers (and no, I don’t know how many of them there are) are REQUIRED by regulation to submit bids.

So presumably if a large enough number of primary dealers are submitting high enough bids, still not all of them will get allocations, resulting simultaneously in higher yields and what the Fed calls a “solid” auction.

If I have not made this clear, please let me know. Also, if I am just outright wrong about the auction process, I also welcome correction — I don’t like to remain ignorant if I can possibly help it.

Everyone does rate cut or increase analysis but they forget the every increasing debt to 40T within a few years will create havoc in markets in ways that you cannot forecast, including servicing this debt with 1T+ mandatory payments, if Democrats get elected in 2028 their policies will accelerate debt, no one wants to increase taxes

If Democrats ever get control of anything again, ALL Republicans will instantly convert from crazed spenders and debt-doesn’t-matter promoters to fiscal hawks, and they will try to block all spending.

Yes. The whole charade is really tiresome to those of us older than 24 who have seen this stupid game time and time again.

Yup

except military and foreign aid.

Re: If Democrats ever get control of anything again

Republicans are acting like they have no re-election concerns — even in the face of polls that show their constituents are not supportive of their legislation.

Is that over confidence, arrogance, ignorance — or a red flag that the republicans won’t cede power?? There is a reckless willingness to redefine the Constitution or rewrite it — which worked well for Putin and other dictators.

Except polls show the Democrats are doing worse among their constituents

Are you seriously comparing Republicans to Putin?

Wolf,

Well said!!! So next time democrats come in power they need to double down on cuts and increase taxes for rich. Give what republicans want when they are not in power. At some point we the people (idiots) will finally see the difference between 2 parties. 2 party system is a joke.

If you can’t block a tax bill with a vote of 51-50 then good luck blocking Anything in the future.

Just so you are aware, with the Bush tax cuts, the occupation of Afghanistan and Iraq, the Trump 1 tax cuts and the Big Beautiful Bill, the Republicans have been responsible for 4 of the 5 biggest deficit increases in the last 26 years. The only other was the IRA.

COVID spending was excessive under both Trump and Biden.

I am not a fan of either party and I find both the party to be fiscally irresponsible.

I love this response

It’s like saying I don’t like the bank robbers or the old lady who takes up the line at the bank depositing her dime collection.

A relevant article on Bloomberg says:

“…The Committee for a Responsible Federal Budget decomposed the increase in debt [since 2000] and apportioned it out: Some 28% of the increase is due to legislation and programs enacted in response to recessions. Some 33% can be attributed to increases in spending. And the largest share — 37% — is due to tax cuts.

In other words, tax cuts are the single largest contributor to the increase in debt of the last quarter century. This accomplishment is all the more remarkable considering that those years include two multitrillion-dollar wars in Iraq and Afghanistan, an unfunded expansion of Medicare, and the two worst economic downturns since the Great Depression.”

This is not accurate.

If you look at debt as a percentage of GDP, there were two massive spikes in the last 30 years, one from 2008 to 2012, partly under Bush and partly under Obama, and one that kicked off in 2020 during the pandemic continuing to 2025 under Trump, then Biden, and now Trump again.

The biggest common denominator isn’t tax cuts or war spending, it’s GDP decline during recession, increased spending related to economic downturn (including the COVID blowout of 2020).

So economic cycles are more important than tax cuts and war spending, and in the short-term, social program spending.

The post pandemic blowout started by Biden and largely continuing with Trump is a whole different animal, just a massive festival of spending above revenue during peacetime that doesn’t have a precedent.

But it’s not at all accurate to pin it more on one party or the other.

The NIMs of large banks typically ranges from 2.5 to 3.5 percent. It’s higher for smaller banks, 3.5 to 4.5%. But with the IOR at 4.4 percent, there’s not much reason for expanding commercial bank credit.

QT, while paying interest on interbank demand deposits at the FED, has heretofore restricted the growth of the money stock. Powell needs to hold his ground. The longer the FED remains tight, the lower interest rates will go.

And the administration ramped up attacks on Powell.

How much abuse can a man take before it’s not worth it. I guess consensus is yield will rise if he’s fired or forced to resign.

The role of the Fed chairman is to be bad cop and take abuse.

Designated scapegoat…

No. That is certainly not the job of the Federal Reserve Chairperson.

Dude just wants to get out without breaking anything.

He’s said as much many many many times.

The guy loves public service and being in the middle of important stuff.

He’s def not an economist but he listens closely to them.

It’s stupid to want anyone else other than Powell

“Now there is no panic, the 10-year yield is near 4.5%, and the Fed is doing QT..”

Maybe you have identified a leading indicator. The yield curve was also uninverted a few months ago as well.

We didn’t see the Dotcom or two panics coming. CNBC was a lot like it is now. It was Overwhelmingly positive and everyone, even people with no clue, were investing.

The tariff rate is as high right now as the 1930s, and we are getting $30B per month. He didn’t TACO, and someone is losing money right now. He is doubling down. I am pretty leery as this is what drives credit crunches and freezes.

They’re estimating that tariffs will bring in about $300 billion a year in revenues, and companies pay that out of their nearly $3 trillion in annual profits that have exploded during the high-inflation years. So what’s the big deal suddenly?

https://wolfstreet.com/2025/06/26/the-corporate-profit-explosion-stalls-in-q1-on-the-eve-of-the-new-tariffs/

I don’t think it’s a problem, except for the bloated stock valuations.

Exactly right!

The 30-year yield is a thermometer of the bond market’s current fears about:

Inflation over the long term

A lackadaisical Fed in face of this inflation

And a Mississippi River of new Treasury debt flowing into the market.

Wolf

You’ve said (sorry for paraphrasing) that the way the President is handling tarrifs is not a big risk to inflation. And yet the market is indicating as you say.. fears about inflation over the long term.

Do you think the market is worrying about inflation for the wrong reasons?

Tariff-based inflation fears have not shown up in bond yields yet. Bond yields are not even as high as they were before tariffs were a thing. The bond market is not yet worrying about tariff-based inflation. It’s worried about services inflation, and services are not tariffed, and they’re 65% of the inflation basket. If there is a big bout of long-term inflation, it would come from services.

Is a price rise because of a tariff inflation or just a tax increase?

If the latter, there is no reason for the Fed to adjust monetary policy since the price rise would have a real (not monetary) cause and would be a one off effect and not the start of an ongoing inflationary cycle.

technically tariff won’t cause inflation because inflation is a continuous process while tariff is an one-off event. Prices will be higher one time. There might be a feedback loop of higher and higher prices triggered by tariff but as long as Trump caves rapidly, the risk of inflation is low.

Monetary theory says that inflation is only the result of more money supply, not supply shock or taxes. The real risk of inflation is the ever larger debt. The only cure to debt is inflation. It is hard to resist the temptation to use inflation to reduce debt. Musk hates the idea. Trump wants it and he wants it now — willing to fire Powell to get his way. If Powel is fired, I suspect the 30 year rate will jump.

Ok so tariffs could cause a one time effect, but the echos from that one time affect could be around for awhile. If steel is 50 percent more expensive, causing American cars to be 15 percent more expensive, causing unions to need higher wages …etc. it’s still a highly undesired situation no matter what you call it. I’m not even going into the whole subject of American expor competitiveness.

Mitchv

“If steel is 50 percent more expensive, causing American cars to be 15 percent more expensive, causing unions to need higher wages…”

OK, serial BS overload.

1. Automakers can buy from US steel mills, no problem, and their production is NOT tariffed. End of your silly story.

2. Enough healthy competition in the US will see to it that steel prices remain within the normal range over the longer term. The US has plenty of modern steel mills and can build more.

3. Hyundai already announced that it would build a steel mill in the US (the Hyundai group is a huge steel maker in Korea, they know how to do this) to serve its auto production in the US, and I assume other customers too. That’s the result of tariffs.

4. Some basic math, using your wrong assumptions: An average car contains about 1,000 pounds of steel. So that might run about $7,000 in costs for the automaker. To use your figure, if the cost of steel for the automaker that refuses to buy USA-made steel rises by 50%, then it would add $3,500 to the cost of the vehicle for the automaker. The average transaction price retail is now nearly $50,000. To use your ridiculous assumption that this automaker is able to pass on the entire cost increase (while its competitors buy non-tariffed USA-made steel and there don’t have that cost increase), then the retail price of the vehicle would rise by about 7%, not 15%.

Hi Wolf

Lol. Ok agreed some off the cuff serial BS. But your theory that all the companies will absorb all their tarrifs or find cheap alternatives in the US is wishful thinking. Steel mills and copper mines don’t get built and up to speed overnight. And some companies might absorb price increases but they obviously can’t all do that.

“all the companies will absorb all their tarrifs or find cheap alternatives in the US”

You’re lying about what I said. I never said that.

What I always said is that:

1. Tariffs are a tax on gross profits, and whether or not companies can pass them on to the consumer depends on market conditions.

2. Companies can and will dodge SOME of the tariffs by shifting production to the US (and they’re already doing that).

Howdy Teach Its more like The Great Lakes of Debt to me or Ocean of debt. This is the first time I disagree with you… HEE HEE

The expression is: “a Mississippi River of NEW debt”

The existing debt might be an ocean or the Great Lakes. But the NEW debt that is being issued to fund the current and future deficits is a massive flow that has to be absorbed by the market — hence the Mississippi River, and then it becomes part of the overall debt.

If we’re really going to quibble over details, the existing debt would be where the Mississippi River flows into, Lake Pontchartrain and then the Gulf of Mexico LOL.

Gulf of Mexico? Isn’t that now called the Gulf of America :-)

The Gulf of Debtxico!

Oh, by the way, the auto ad system keeps giving me big pictures of Che Cuevera…is that following just me or does everyone get it?……I’m like Bernie, actually…would TRY to make it work. Key is just MORE taxes well spent like FDR did.

The Mississippi River does not empty into Lake Pontchartrain. This fact detracts from an otherwise clever analogy.

The Bonnet Carre spillway is rarely used and doesn’t count.

Sell the naming rights for sponsorship….Gulf of AMEXico. “Debt. Don’t leave home without it!”

Wolf, just a note to thank you for all your economic analysis. I struggle with these kind of things, but am getting a little more knowledgeable. Thanks for explaining difficult economics in a way I can understand it.

@wolf I know you mention the spread between the 10yr and mortgage rates only happening 4 times before, what do you make of it?

Also things typically revert to the mean, so does that mean mortgage rates are likely coming down or 10yr rates are likely going up? I.e. which rate is the one that’s slow to react? Or do you think the split this time around is more of a risk premium (instead of just one rate being slower to react) because real estate valuations are too high and there is downside risk in the underlying assets backing the mortgages?

I think the wide spreads are currently driven by MBS QT. What is interesting: the Fed has essentially been unanimous in saying that it wants to get rid of all its MBS, and will continue to shed them even after QT ends, likely replacing them with T-bills. This will take years, even if the Fed sells MBS outright, in addition to the pass-through principal payments of about $15-20 billion a month. So all this is just standard every-day operations, and there is no panic, and the spread is wide because mortgage rates are higher; in the prior four occasions, the spread was wide because the 10-year yield plunged and mortgage rates didn’t follow as quickly. Those a very different mechanics.

Love your line…

This reaction – rate cuts of 100 basis points lead to a 102-basis-point increase of the 30-year yield – raises the secret question: How many more rate cuts would it take to drive the 30-year yield to 6%?

Trump wants lower rates to finance the debt and stimulate the economy. He’ll try to inflate away the debt. Inflation he’ll get. Lower rates? Nowhere but short term.

And Wolf, start a new acronym for tariffs, USBIT. US Business Import Tax.

Wolf, Kevin Warsh may be the likely next Fed Chairman. In a recent interview with Hoover Institute he suggested reducing the balance sheet while simultaneously reducing short term rates.

It seems this would “raise” long term borrowing rates, rather than lowering them, which is the opposite of what Trump wants.

Am I missing something, can you explain?

Warsh quit the Fed’s Board of Governors under Bernanke because he vigorously opposed Bernanke’s QE2 at the time. Warsh thought QE1 was OK, but once the crisis was over, it was time to stop QE, and get the balance sheet back down. Bernanke forced through QE2 against quite a bit of resistance, including from Powell – but Powell soldiered on, while Warsh quit, and Hoenig retired. Warsh wrote about his opposition to QE2 and his decision to quit later, and Bernanke also made reference to it in his book.

So speeding up the balance sheet reduction would fit into Warsh’s history. But he used to be a higher-rate kind of guy also and has meanwhile changed his tune to even be considered for the job. He wouldn’t be too bad as chairman, which is why I don’t think he’ll get the job.

On the other hand, during my occasional fits of delusions, I think Trump might want to pull another Powell: get a mild hawk to keep a lid on inflation, but bash him over the head on a daily basis during the week and keelhaul him on weekends, and blame him for everything that goes wrong. That would make sense for Trump to do. I don’t know how many humans can endure this kind of stuff from Trump, but these critters are tough.

To respond to your question: speeding up QT could reduce inflation, and could persuade the bond market that the Fed is serious about inflation, and it might have the effect of keeping a lid on long-term yields. That may be Warsh’s calculus.

Not that I was asked, but, imho, the delicate balance of threading a needle by speeding up QT and reducing short term rates, goes against the aggressive tantrum uncertainty and chaos this administration is famous for — a new Fed chair will likely not get easy consensus with policy strategy — and if anything, I think we’ll end up seeing a large uptick in overall mkt volatility (stocks & bonds).

Right or wrong, Powell has been a steady hand and FOMC has rarely dissented — so, if the ships new captain projects a drunken path of instability, the little people will want more yield premium.

He wouldn’t be too bad as chairman, which is why I don’t think he’ll get the job.

Fair enough. I guess that is the world we live in.

Wolf, do you know where can you find some info about inner politics of Fed and ECB? Not formal stuff that is in the minutes but stuff like this.

We’ll see if crowding out the private sector leads to higher interest rates.

https://fred.stlouisfed.org/series/W068RCQ027SBEA

Total government spending is out of control! That’s what leads to crowding out.

$22BB wont even keep the Gov running for a minute. I wonder why they even bothered with the bond sale?

“Roughly $9.2 trillion in Treasuries mature in 2025 and with a $1.9 trillion deficit, total issuance tops $10 trillion, most of it front-loaded in the first half.” (fistnational.ca)

This could become a problem if trade negotiations go badly (i.e. inflation higher than anticipated)

“Roughly $9.2 trillion in Treasuries mature in 2025”

Seems you misunderstand what that means. The vast majority of that maturing $9 trillion are T-bills (securities of 1 month, 2 months, 3 months, etc. to 1 year) that constantly mature and get rolled over. There are over $6 trillion in T-bills outstanding, and they constantly mature and get rolled over. A 1-month T-bill matures in one month, and that happens 12 times a year. If you have a 1-month T-bill, you get paid the face value when it matures in one month, and just then there is another 1-month T-bill auction, and you can auto-rollover your T-bills. It’s very smooth, almost like a savings account. Lots of people and companies do that. Your $9.2 trillion includes $6 trillion in T-bills that are constantly maturing and are getting rolled over multiple times per year.

So don’t get distracted by the “$9.2 trillion” – the thing you need to look at is the INCREASE in the debt.

That’s why they want an interest rate cut, otherwise they’re looking at rolling it over at a higher rate. Lower short term yields?

Consensus estimates show a big increase in Core CPI on Tuesday. 20 and 30 year Treasury bond traders are aware of this, which is why yields are rising. If the consensus estimates are correct, 20 and 30 year Treasury yields should jump past 5% on Tuesday. Trump will continue his whining about rates, not realizing that 20 and 30 year Treasury yields are set by the market, not by the Fed.

Tech bubble update: Combined market capitalization of Nvidia and Microsoft is now almost $8 trillion, which is equivalent to $1000 for every man, woman and child on the planet. JUST THOSE TWO COMPANIES.

$8,000,000,000,000 (!!!!!)

If you could build a stack of ONE trillion dollars in THOUSAND dollar bills it would reach an altitude of 65 miles. That is higher than where Jeff Bezos’ spaceship goes.

The chart of the 30 year yield shows higher highs and higher lows and has formed an ascending triangle. I have no idea what the implications are, but the next 3 1/2 years should be interesting.

And that will be less than the increase in federal debt from Trump. LoL

It’s just more paper

But then there would be no stocks

So how would we make money?

By starting a new stock exchange?

And think of the insane inflation on everything once you unleash that much cash to the world.

4.96% per annum to hold onto HORSE CRAP for 30 years? I’d rather spend it on call girls and cocaine. At least that way you get something in return. At 4.96%, you’re losing your shirt.

The Fed’s acknowledged mission is to slice AT LEAST 2% a year off the purchasing power of the dollar.

How far we have strayed from “stable prices”

Remarkable, and strangely accepted in toto without debate or concern

Hookers and blow!

A solid investment in your at the moment in life happiness!

As a long term investment I would need to think on it a bit.

I know it’s not a consensus view but I think 30-year treasuries yielding 5% are a great buy. The likelihood that inflation will be anywhere near 5% per annum over this time frame is extremely remote. It would require severe interest rate suppression and debt monetisation for this to occur, and the likelihood of this happening is remote. A positive real return over 30 years looks attractive compared to other risk assets which are priced to perfection. For the first time in many yields, treasures offer a decent yield and are an attractive investment.

You need to include the value of the dollar! Its value is not just a chart somewhere. It is about trust.

The midterms could be a huge turnimg point. Much of TACO’S base have had enough of daily drama showmanship.

Best advice. Don’t tie yourself to long term rates until after mid terms.

The decline in the dollar makes treasuries more unattractive, and thus the market demands a higher rate of return.

Forcing the Fed to cut is an absurd idea, suggested by those who wish to manipulate rather than obey and respect market forces. IMO

A past decline in the dollar doesn’t make treasuries less attractive. It’s the belief that the decline will continue that makes them less attractive.

But the decline MADE the treasuries unattractive…

that was my time frame.

Enjoy yours

Of course. The point I was trying to make is that, if a foreign investor was assured that the value of the dollar relative to his currency would stay stable, the only thing he’d care about is the dollar’s yield. He’s not going to be concerned with a past decline in the value of the dollar against his currency.

The reason a European investor is less interested in the dollar when it’s 0.86 euro (today) versus 0.96 back in January is that he’s worried he’ll buy into a dollar denominated asset today and have it be worth 0.76 tomorrow. It’s the trajectory he’s concerned with.

Trump’s close pal Epstein described the president as being functionally innumerate and unable to read a spreadsheet, which might help explain some of the policies coming out of this administration.

Phil, at that level, they have people read the spreadsheets for him. Do you think Biden would have been able to read one, or even know what a spreadsheet was?

Joe couldn’t even get in bed w/o help, much less spred his sheet

Great site Wolf – keep it up!

A few weeks ago, someone said it’s the 2nd after Zerohedge, but I dispute that. ZH has developed into a woke haven. Yes, being anti-woke is also woke to me. On top of it, their finest articles are now behind a paywall, but you can read all the outrage about whether Macron’s wife is a man, AOC calling Trump a racist etc… I DO NOT CARE! ZH was great during the EU debt crisis, but it’s a sad site.

Alas, I have my eyes on the long end only – that is where the action is going to be. Sure, new ATH daily due to the AI craze. I do see a mini dot.com implosion coming, as not all these AI firms will last and sentiment will change.

The 30 yr is almost back at 5%… but is it? Now that I am educated enough I feel like it’s in fact way higher already. Only due to the Fed’s bond holdings is it at 5%….

The Fed buying bonds, is like a parent buying a kid’s lemonade at his lemonade stand and then claiming that demand is high and thus prices need to be high (and yields low). It’s FAKE demand. The Fed should be forbidden from doing any QE.

“Yes, but then rates would be too high”… Too high? No!!! There is simply too much supply. Reign in the supply of treasuries.

Disclosure: cash, gold, pslv.

I stopped reading ZH altogether when they paywalled their daily market recaps – which was the only thing I had been going there for in recent years.

It’s a complete dumpster fire of a site now… very thankful for Wolf’s wisdom here.

A really wild issue unfolding here, is the overall juxtaposition in the 30yr headed higher, and absolute disconnect with asset valuations — and future value.

This blows my mind:

“Citing data from Bitbo, The Kobeissi Letter also pointed out that the S&P 500 has dropped a staggering 99.98% against Bitcoin since 2012”

It’s also insane that Nividia is $4 trillion+ — we’re basically seeing a shift from a post WWll global economy, that used finance to build productive output, like GDP stuff — used debt, like treasuries to finance big projects that were generally focused on creating things for society. AI seems destructive versus constructive — it helps do what???

Now, we’re pulsing forward with laser focused speculation, in a nano -second basis — completely oblivious to the old realty — where antiquated, dinosaur-like 30 year treasuries don’t play a role, except to act as tool for Treasury to use to measure the disconnect from monetary reality, as Trillions compound ….

The bottom line is to ponder what use, worthless govt paper serves, in a future world where a 5% yield has no meaning — what purpose will worthless Zimbabwe toilet paper serve in a pension portfolio, or as a safety net?

The instability unfolding is profound, as Baby Boomer wealth, smashes into the gravity of super nova speculation — Neutron star merger and black hole extinction — YOLO!!

I use “worthless” government to buy goods and services all the time. I even invest some “worthless” government paper in other “worthless” government paper and collect still more “worthless” government paper with which I buy more goods and services. I don’t, however, buy Zimbabwe toilet paper or have a pension, so that’s not a problem for me.

Regardless of what the Fed does, RISK is being repriced, globally. As it turns out, our oligarchs are just as corrupt as their oligarchs…

As the saying goes; Full FAITH and Credit.

America is no longer the cleanest dirty shirt, but rather just another dirty shirt, hedge accordingly.

I wouldn’t be surprised if the “way out of this” is to significantly increase the social security payroll tax from both worker and employer – and put it into a surplus that is invested solely in T bonds. It will be sold as “shoring up your SS benefits” but will also serve to absorb this river. Combined with a cap increase that might be a half a trillion dollars of SS Trust Fund Bucks buying automatically at 5%. They did something like this in the 1980s.

I think at this point the system needs 5% 30s, 4.5% ten years, and 6-6.5% mortgages to survive. Lower would be “better” but higher might be fatal.

Wolfe:

How is the interest rate determined in these auctions?

Do buyers bid the rate up until all the notes are sold?

I am clueless on all of this.

Thank you sir!

https://www.treasurydirect.gov/auctions/how-auctions-work/

In a nutshell – You bid the price, which determines the yield. Coupon is fixed.

President calls for 1% even 0% interest rates

Spoken like a person who was put out of business by the Fed in 1981 and runs a business that constantly borrows.

Free money is the best money.

Yield goes up on 30y T-bill could largely affected by current geo-political situation. Loss of confidence in a sovereignty is a very important reason. Get real info on what is going on around the world. Of course never forget about the manipulators who purposely “create” certain market conditions.

Meanwhile, in the far East:

“ “If the opposition parties win, the government deficit will see a huge expansion,” Chiba said. “The JGB yield curve will steepen by a lot.”

Mkt votes for higher 30y

5.011

Obviously rates and yields, deficits and zombies are irrelevant — we need to see 6%!!!

Me hopes Wolf writes a post on the inflation increase due to the tariffs. He is pretty sure, based on much of his writting, that the companys will absorb tarrifs or they can get US replacments. I would say, and time will tell, that either way the price will be higher and will be sent along to the consumer. This is also due to the lack of competition in most businesses. For example my friend with glass installer business has a 25% increase accross the board for his window products coming. I have suppliers adding tarriff costs to there bills now. I will be passing them along.

“Me hopes Wolf writes a post on the inflation increase due to the tariffs.”

LOL, inflation reheated in services, which are not tariffed, while prices durable goods, apparel and footwear (which are tariffed) remained cool, you lying, ignorant, manipulative goofball.

“While pundits looked with their magnifying glasses for tariffs in consumer goods prices, it was in services, which are not tariffed, where inflation took off again. Shocker? No”

https://wolfstreet.com/2025/07/15/feds-nightmare-cpi-inflation-in-services-reheats-not-tariffed-while-inflation-in-durable-goods-apparel-footwear-tariffed-remains-cool/

The tariffs resulted in a 27b surplus in June. The O/N RRP facility still has 218b in it.

We’ve got a blue line going down and a red line going up, up, up. what to think?