Quantitative Tightening accelerated further. With its bank stocks gone, the BOJ may start selling its equity ETFs soon.

By Wolf Richter for WOLF STREET.

Quantitative tightening, in terms of the Bank of Japan’s vast holdings of Japanese Government Bonds, picked up speed in Q2 2025. The BOJ also continued to shed its loans – the other big method with which it conducted QE. Its holdings of commercial paper and corporate bonds continued to plunge and hit the lowest level since 2013. The BOJ sold its holdings of bank stocks down to near-zero. Only its small holdings of equity ETFs and Japanese REITS have been unchanged at peak level since Q4 2023. But they may be next.

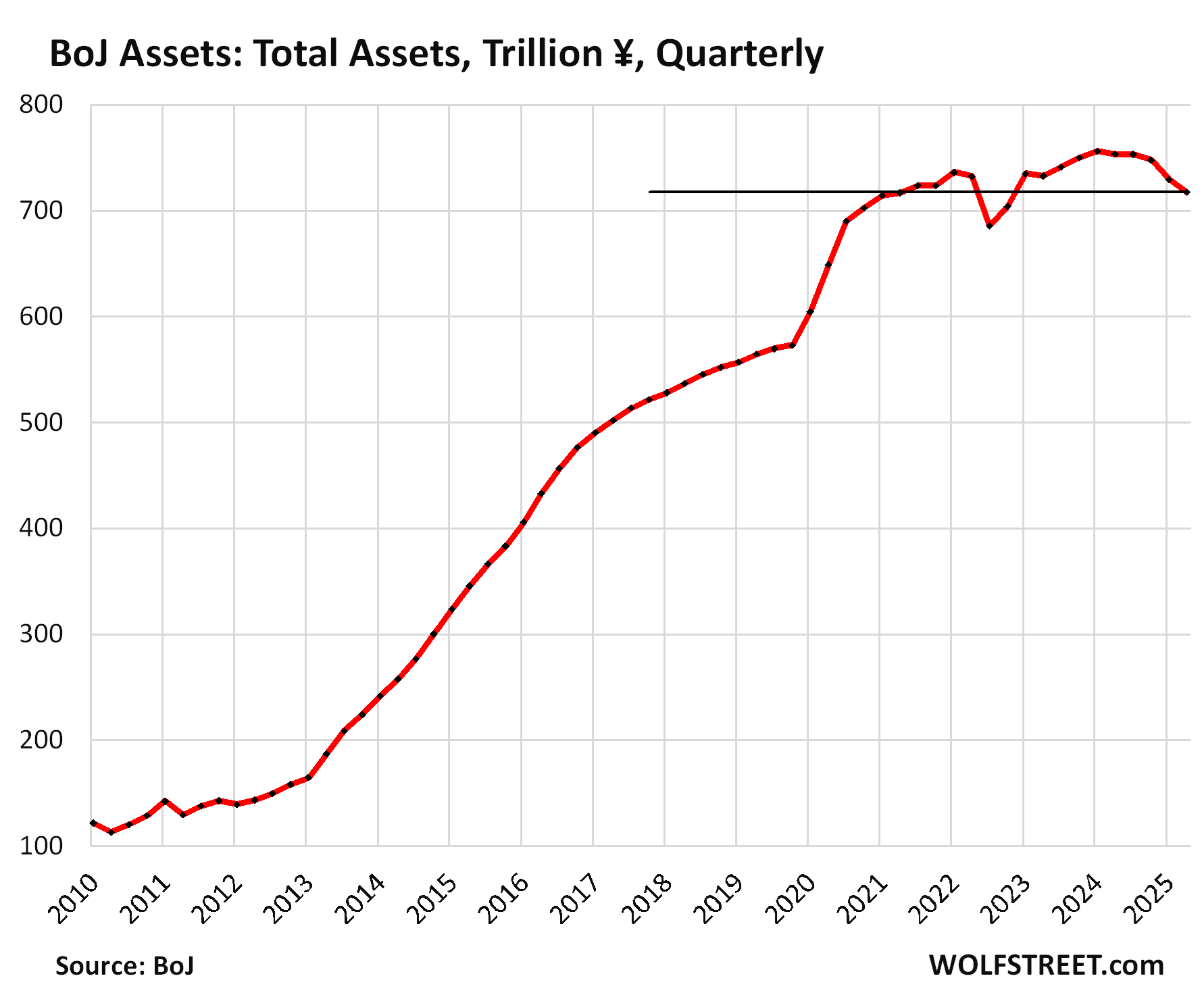

Total assets at the end of Q2 fell quarter-over-quarter by ¥12.3 trillion ($84 billion), and year-over-year by ¥36.2 trillion ($248 billion), according to the Bank of Japan’s balance sheet data.

Since the peak in Q1 2024, total assets have fallen by ¥38.9 trillion ($267 billion), or by 5.1%, to ¥717 trillion ($4.92 trillion), the lowest since Q4 2022, and back to about where they’d first been in Q2 2021.

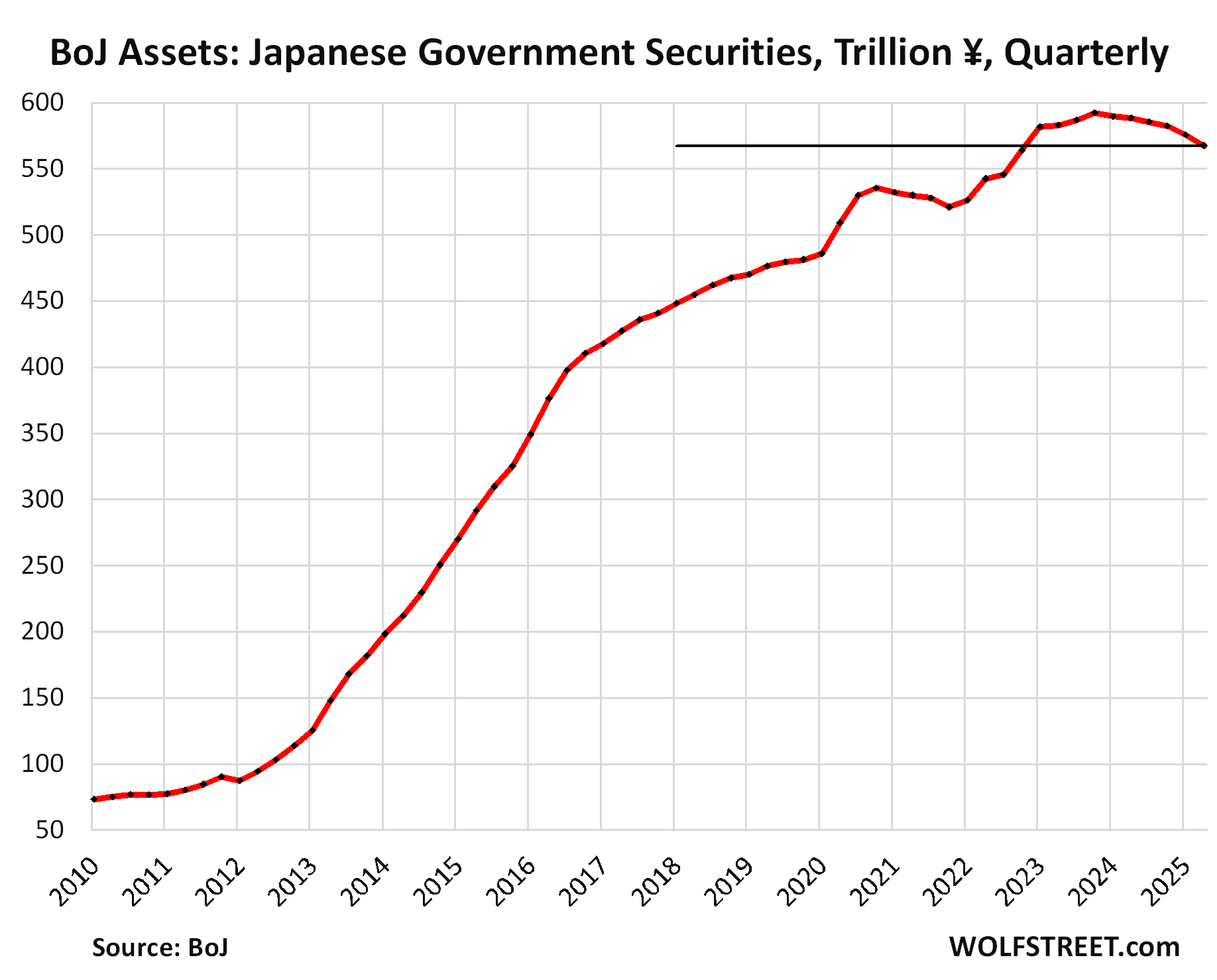

Japanese government securities declined quarter-to-quarter by ¥8.4 trillion, to ¥567 trillion ($3.88 trillion), the lowest since Q1 2023. They amount to 79% of its total assets.

Nearly all of them are longer-term Japanese Government Bonds (JGBs); its holdings of short-term Japanese Government Treasury Bills were unchanged at just ¥1.7 trillion ($12 billion).

Year-over-year, its holdings of Japanese government securities fell by ¥21.0 trillion. Since the peak in Q4 2023, they fell by ¥24.8 trillion, or by 4.2%.

On July 31, 2024, when the BOJ announced details of its QT process, it also laid out a plan for accelerating QT in 2025, and this acceleration is now taking place.

In terms of the pace of quarter-over-quarter declines, Q2 was the fastest so far:

- Q2 2025: -¥8.4 trillion

- Q1 2025: -¥6.4 trillion

- Q4 2024: -¥3.1 trillion

- Q3 2024: -¥3.0 trillion

- Q2 2024: -¥1.2 trillion

- Q1 2024: -¥2.6 trillion

- Q4 2023: end of QE

Note: To reduce the complexity here, all quarters here are calendar quarters; but the BOJ operates on fiscal quarters, with its fiscal Q1 being the March to June quarter (Q2 here).

The BOJ’s government securities holdings move in three-month cycles due to the timing of when long-term bonds mature and when they’re replaced with newly issued bonds of the same type. The BOJ also makes quarterly data available and refers to quarterly data in its balance sheet discussions, which iron out the three-month cycles.

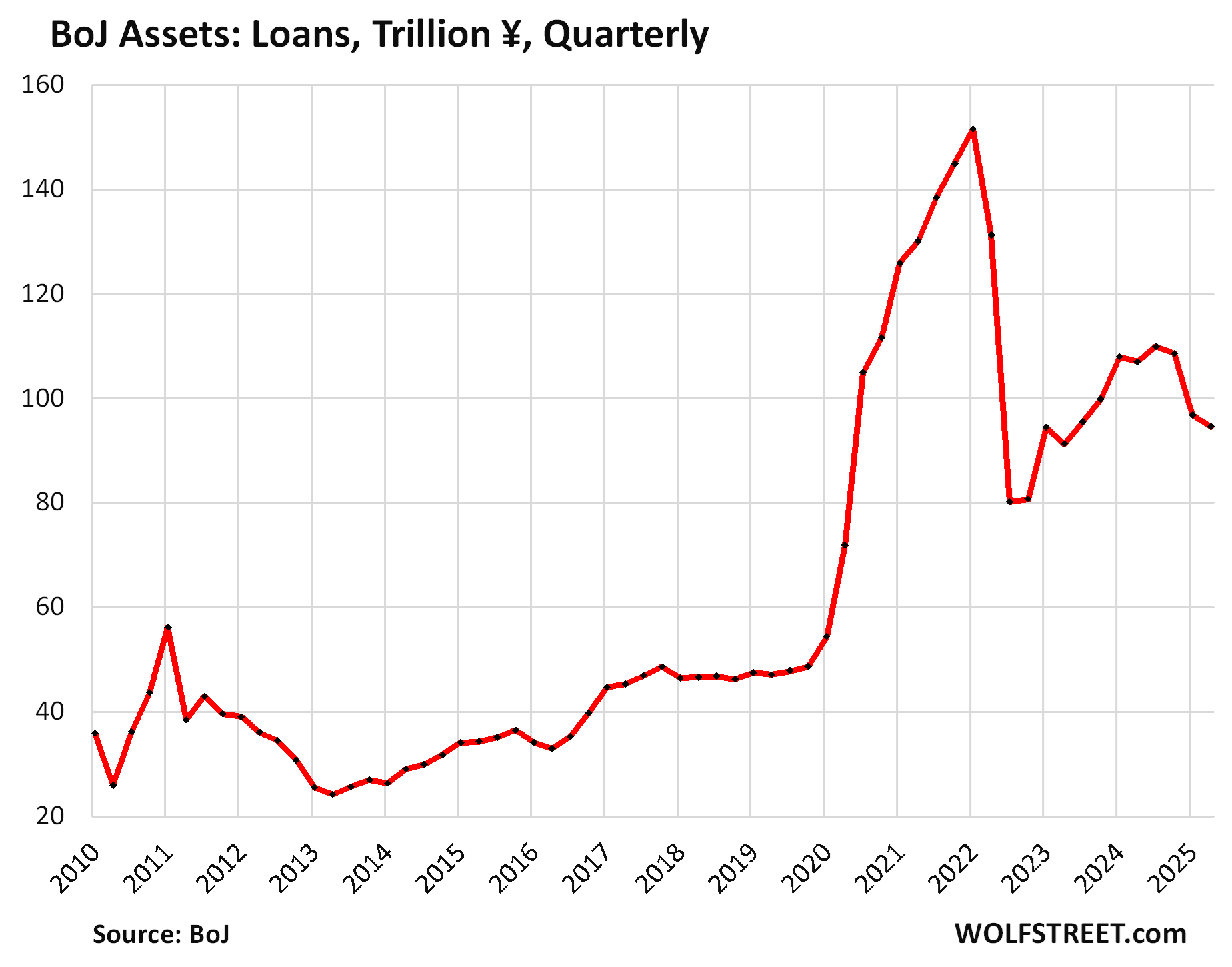

Loans declined by ¥2.2 trillion in Q2 from Q1, and by ¥12.4 trillion year-over-year, to ¥94.6 trillion ($648 billion), first seen in Q3 2020

Since the peak in Q1 2022, the outstanding balance has fallen by ¥57.0 trillion, or by 37%.

These loans accounted for 13% of the BOJ’s total assets in Q2. The BOJ provided loans to banks and other entities under several programs, including the pandemic-era loans that caused the total amount of loans outstanding to more than triple in two years:

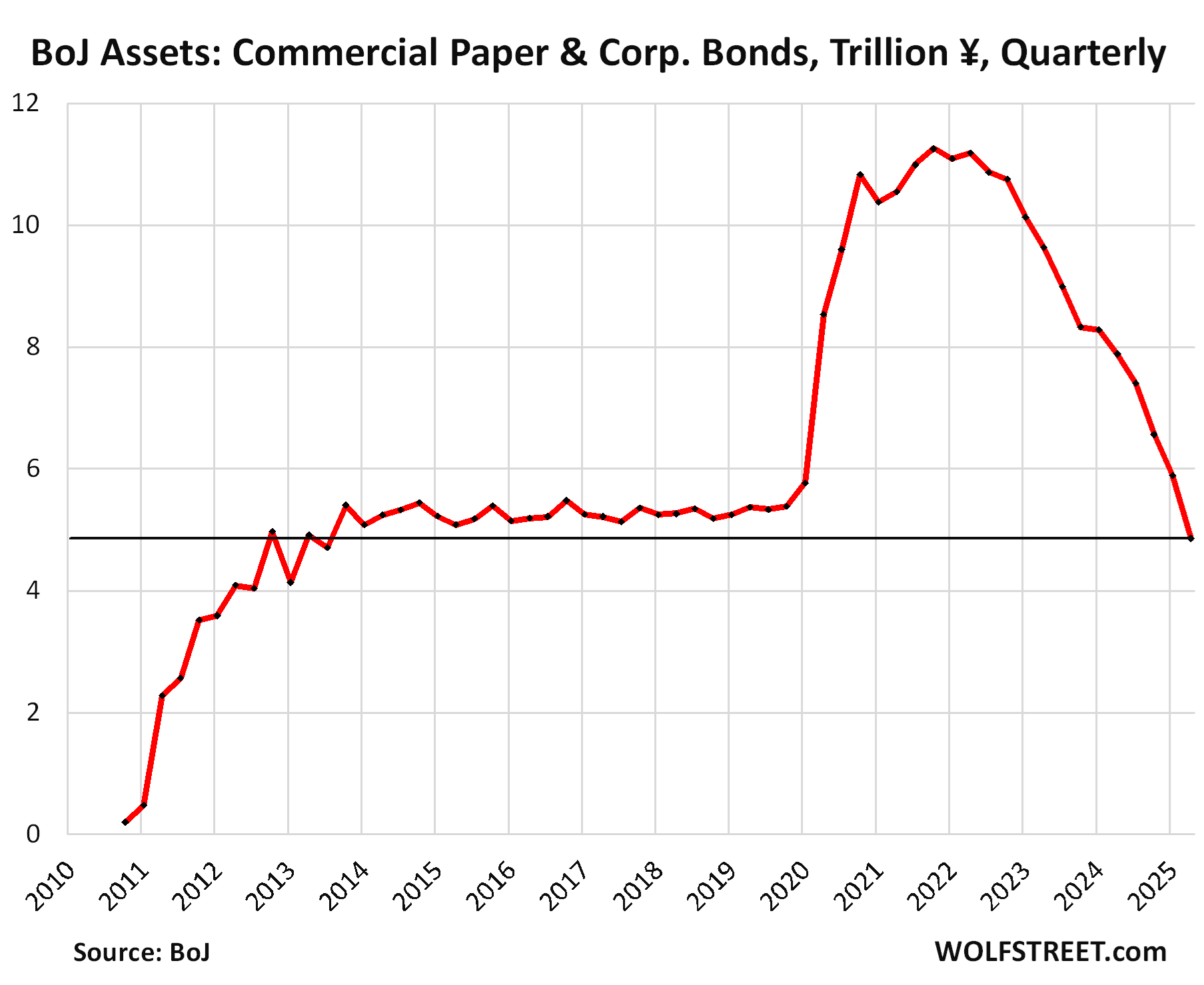

Commercial paper and corporate bonds fell by ¥1.0 trillion in Q2 and by ¥3.0 trillion year-over-year, to just ¥4.9 trillion ($33 billion), the lowest since 2013.

Since the peak in Q4 2021, they have plunged by 57%. The BOJ stopped buying commercial paper and corporate bonds in early 2022, and its holdings have been running off the balance sheet as they mature.

While hyped endlessly in the QE-promoting media at the time, along with the BOJ’s purchases of equity ETFs, they were never a significant part of the BOJ’s QE operations. At their peak in Q4 2021, they accounted for only 2.2% of the BOJ’s total assets, and their share is now down to just 0.7%.

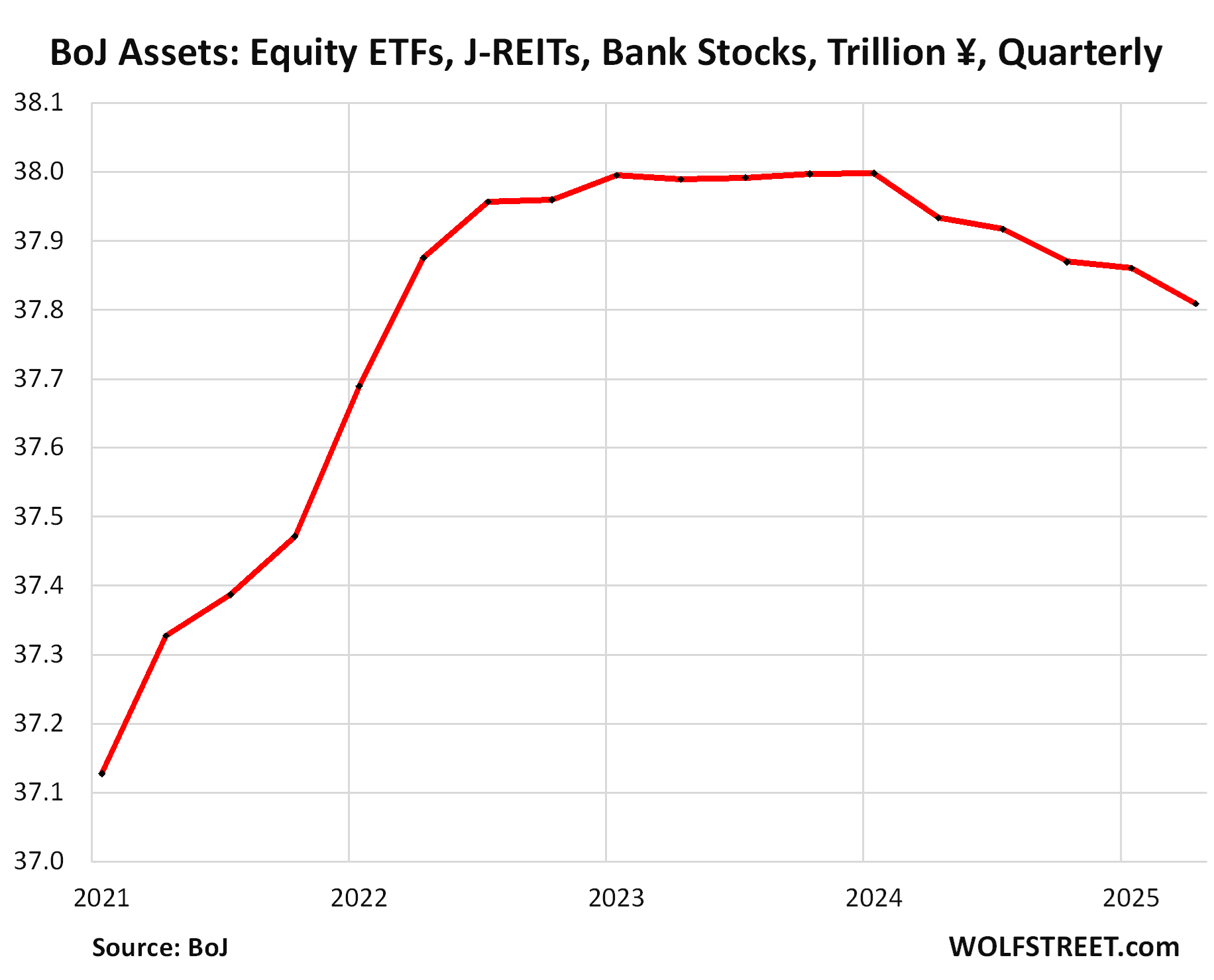

Equity ETFs, Japanese REITs, and bank stocks, which are traded in the stock market, have to be sold to come off the balance sheet – since they don’t mature, unlike the above assets.

In terms of the equity ETFs and Japanese REITs, the BOJ has not yet started selling them, but has been talking about selling them.

But it has been selling the stocks of Japanese banks that it purchased in the early 2000s and then again in 2009. The purchases of bank stocks ceased in 2010. In 2016, the BOJ started selling these stocks, in a process that it said would take 10 years to complete through March 2026.

The fear in the market is that once those stocks are gone, the BOJ would then begin selling its equity ETFs and J-REITs ever so slowly. And these bank stocks are now nearly gone.

The BOJ’s holdings of bank stock dropped to just ¥2.5 billion ($17 million), and at the recent pace of selling them, they will be gone in a few weeks.

The BOJ started buying ETFs in 2012 and stopped buying them in Q4 2023. It carries them at acquisition cost, not at market value. If market values fall substantially below acquisition cost, the BOJ would write them down. But the BOJ doesn’t write them up when market values rise.

Since reaching peak in Q4 2023, equity ETFs and J-REITs have been at ¥37.2 trillion ($260 billion) at acquisition cost, or just 5.0% of the BOJ’s total assets. They were always only a small part of the BOJ’s QE operations.

To shed them, the BOJ has to sell them outright in the market. Obviously, the BOJ doesn’t want to rattle the Japanese stock market. But with the bank stocks now sold down to near-zero, the ETFs are likely next.

The BOJ’s total stock-market-traded assets combined – bank stocks, equity ETFs, and J-REITs – have been declining due to the decline in its bank-stock holdings, but at a microscopic pace. Since the peak in Q4 2023, they have inched down by 1.0% to ¥37.84 trillion as bank stocks are in the process of vanishing from the balance sheet.

Looking at them under the microscope:

In case you missed it: Fed Balance Sheet QT: -$13 Billion in June, -$2.31 Trillion from Peak, to $6.66 Trillion. New Milestone: 3 Years of QT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The BOJ’s sharemarket holdings might be small relative to its enormous balance sheet but they’re still extremely significant. Bloomberg reported that the BOJ owns approximately 7% of the entire market via its ETF holdings.

To make matters worse, rather than just buying the market cap weighted Topix ETF, the BOJ bought the price weighted Nikkei 225 ETF and the JPX 400 ETF which has a bizarre weighting scheme based on ROE. As a result, its ownership percentage of different companies varies significantly. As an example, the BOJ owns approximately 12% of Fast Retailing (the owner of Uniqlo) via its ETF holdings.

If the BOJ sells its ETF holdings it will have to do it very slowly. It’s the ultimate whale and it could easily spook investors.

I think the game is almost over for Japan (over the next 5-10 years). I don’t think that the JCB can buy JGB (long term Japanese government bonds) at low interest rates since the wolf is at the door for the Japanese government, with its mountain of debt, primarily to the JCB. The low rate era for long term bonds is over. Inflation has started to be normal at over 2%. So not many want to buy long term Japanese bonds for cheap. So the spending spree for the Japanese government by selling bonds to the JCB is over. There are many elderly, requiring services and retirement income. I expect social stress, more inflation, and government change within a few years. Japan imports most of its raw materials including energy since shutting down many of its nuclear facilities. Japan is perhaps a decade or so ahead of what is in store for the USA. jmo

Energy and raw resources underpin everything, without these you just have an agrarian economy. As you say Japan is lacking in these. This is the reason why Japan invaded the rest of Asia prior to WW2. USA should be okay for now, it is still rich in energy and to a lesser extent raw materials.

True-ish but in the end political sociopathy can stunt/destroy the most richly endowed of nations.

If natural endowment were fate, Russia and Argentina would have much, much more successful economies.

As for the US, after decades of using the dollar/savings as a crutch to empower political pathology/dementia, Americans are going to have to learn to live in a world where printing-at-will comes with dire consequences (that’s why few countries try it and even fewer successfully navigate it).

100%. Assets are all priced as they are because people are convinced there will be more printing. I think however without COVID as a cover, the rest of the world will not take kindly to more deranged printing, and the long end of the treasury curve will react accordingly.

Japan’s been a slow-moving trainwreck now for decades. ~9.5 million 50-54 yo’s, 6 million 25-29 yo’s, 4.9 million 0-4 yo’s. Their largest population cohort was in their early twenties when the asset bubble burst in ~’90 and they never had enough kids to replace themselves. The Lost Decades included many aspects of life.

The US is dealing with a shrinking birthrate, but we still have a fairly wide population peak in the 22-44 range and decent immigration. And the 0-4 cohort is only down ~15% from our peak compared to Japan’s 50%. We can manage a slow decline; it’s really hard to recover from halving the number of kids over forty years.

Broadly get your point but using population growth per se as the cure for an unhealthy economy/hallmark of a healthy one is mistaken in my opinion.

Slowing/declining of the domestic birth rate is a natural response a sick economy – and likely a predicate for its return to health (providing time/resources to rethink macro policies gone wrong, economic margin to less painfully adjust those policies).

And businesses/politicians engaging in mass human trafficking across borders with an eye to providing a sugar-rush boost to stagnating economies (aggregate GDP “growth” through stacking bodies) has worked pretty damn poorly for the US/Europe since at least the late 1980’s.

I can’t see how it’s that dire.

No one who sells raw materials is likely to cut off the supply to Japan. Australia, Canada, the US, New Zealand, the Middle East, South America, etc. All are perfectly happy to sell exports of raw materials to Japan.

Very few nations are going to restrict the flow of Japanese-manufactured goods exports. From Toyota trucks to Mitsubishi Shipbuilding, or the subcomponents for so many items, they’re often cornerstones for much of the global industry.

If Japan’s trade and industrial policies aren’t ridiculous, they should always have enough currency to buy their energy and raw material needs. After that, the ship isn’t going to sink, so everything else is just getting the chairs arranged correctly. That’s not exactly trivial, but it’s also not an end-of-days crisis.

“so everything else is just getting the chairs arranged correctly.”

Hmm…if it were that easy, then why have the chairs been left in disarray for decades (see, also, US – including Big Baloney Bill of last week…).

At some point in time, deteriorating macro stats have to make you ask if the disordered chairs are in fact deck chairs on the Titanic.

Great article! Thanks Wolf!

I’m long the Yen. Most FX traders are looking for a major step, like a rate hike. But the BOJ is plodding along with its QT slowly and deliberately.

I see the following major factors:

Bull (for Y/$):

– rate normalization over long term

– upcoming Fed rate decreases (so rate divergence)

– “safe haven” currency (main risk being China; away from Middle east & Russia-Ukraine)

– restarting reactors will lessen dependence of energy imports

Bear:

– Debt/GDP is twice that of the US (wow!)

– aging population

– tariffs (perhaps short-term problem)

Any comments anyone?

Wolf?

[I’m already on your email list. Thank you.]

What if those upcoming rate cuts don’t materialize? Or they do, but the 10yr Treasury goes up in yield instead of down?

The Fed has been out-hawking the BOJ by a significnt margin for a couple years now.

Japan has two huge factors working against it: 1) The demographic shortfall due to the serious drop in birth rate and cultural rigidity against diversity/immigration, and 2) China.

While China has “saddled up” with Japan through inclusion in the ASEAN trading pact, it’s all a “wolf in sheeps clothing” (Sorry Wolf, not you). That is to say, I believe China has a deep seated but well concealed goal of crushing Japan economically.

More importantly, crushing Japan also involves continued bleeding of America (increased military budget and federal deficits) until the debt crisis hits (another long term China/BRICS goal). The entire Taiwan “game” is nothing more than China’s effort to bleed America dry through military overexpenditure with all the veiled threats. And of course, we are stupid enough to fall for it…..You know, “democracy” in every pot.

In the long run, Japan will not likely do well based on the above.

I can understand why a central bank would want to keep interest rates at some “normal” rate to be able to lower OR raise it as needed. And I get why QE happened when they couldn’t lower rates to less than 0. But I wonder if central banks will permanently keep a QE balance sheet above zero to be able to have yet another tool besides interest rate.

“… keep a QE balance sheet above zero”

This BS needs to stop NOW. Assets on any balance sheet MUST BE ABOVE ZERO at all times or else there is no balance sheet, and no nothing there, you goofballs.

Any central bank has a balance sheet with assets above zero even on its first day of existence.

If you don’t know what a balance sheet is, go attend the first few days of a basic accounting course at your community college.

Even Bookkeeping 101 at night school will do the trick Wolf!

Been there, did that, as my B.A. didn’t help at all when I started working for myself 45 years ago, and realized how many legal deductions I could take with proper paper backup.

I am still of the mindset that Japan’s bond market is the first domino. Time will tell. Interesting times just the same.

Appreciate the international perspective Wolf, and I apologize in advance for going off topic, but Argentina’s been pretty interesting lately.

Granted, it’s a Poland sized economy, and no one cares except those of us partial to the cono sur, but if there are lessons to be learned you’re just the guy to tease them out.

I’ve written about Argentina plenty of times but stopped years ago because the lesson has invariably and always been the same forever: NO ONE should ever lend any money to Argentina, period. Argentina’s foreign currency bonds are just a Wall-Street-Argentina-hedge-fund collusion scheme to extract fees, make huge profits, and rip off retail investors that buy emerging market bond funds or global bond funds.

And now (as of a day ago) Japan along with South Korea is looking at a 25% tariff. Unless maybe this won’t happen. Got a coin?

That should have happened a long time ago. They’re among the most protected markets. Why were all the US governments asleep for 40 years????

”Why were all the US governments asleep for 40 years????”

”Bribery will get you everywhere/anything.”

Was and still is the methodology of most parents and (maybe almost) all politicians, just as it always has been and likely to continue.

Probably because of geopolitics. The plan to turn Japan into an ally has been very successful, and the US needs Japan in order to have a strong presence in Asia. If Japan were to join the BRICS coalition, it would be a disaster for US power projection.

This is an argument against tariffs if, of course, you care about this sort of thing.

I think it was Reagan that did crack down a little in the 1980s, and threatened tariffs on Japanese imports. And that was resolved, but not by Japan opening up its market to US cars. It refused to do that and continued to impose administrative barriers that are impossible for mass-market lower-priced cars to overcome because the auto industry is sacred in Japan and must be protected at all costs. Instead, Japanese automakers committed to build plants in the US and manufacture most of their popular models in the US. As a result, many of the Hondas and Toyotas that you can buy today in the US are assembled in the US and have among the most US content.

But GM is the worst. These tariffs hit GM the most and Honda and Tesla the least.

Wolf: Biggest issue is American cars will never sell in Japan unless US automakers make cars the Japanese actually want. They have little roads and expensive gas- they want small, efficient cars. Instead we keep pumping out SUVs and trucks. Good luck navigating the neighborhood back roads in a Suburban or F-150. I hear Jeep (as in Wranglers) sells the best now, but I think Tesla has a chance. Historically, there have also been quality issues. Japanese cars are just made better.

There is a rice crisis going on right now, so I think pushing American rice and ag more generally could be a good strategy.

“American cars will never sell in Japan unless US automakers make cars the Japanese actually want.”

Ridiculous BS that has been regurgitated brainlessly for decades, including by the very Japanese government officials, to justify blocking those cars from entering Japan as to prevent the Japanese from deciding for themselves.

The Toyotas and Hondas and Nissans in Japan are the same size and quality as here — including minivans and SUVs. Neighborhoods are full of these vehicles, including one parked at the carport of my in-laws house.

The only thing they have in Japan in terms of size that we don’t have in the US is Kei cars (not street-legal in the US). But they’re not highway-legal in Japan either, and only of limited use.

Look at Japanese medium-duty and heavy-duty trucks. Those are big vehicles, just as big as in the US, and they get around just fine. In fact, they sell their medium-duty trucks in the US.

Japan will make a deal with Trump. It just has to wait until after the election.

Although this is somewhat off topic, I think the possibility that Japan may slow down QT and adapt to new tariff dynamics, sets up crazy outcomes ahead.

The tariffs impact Yen and their economy in complex ways, but there is a chance they reduce US Treasury holdings, helping to increase our supply and helping to keep our yields higher for longer.

It’s interesting to note: By the end of 2025, the projected cost of servicing the US Treasury debt is estimated to be around $952 billion. This figure represents a significant increase compared to previous years and is projected to reach 3.2% of the nation’s GDP

That, against this today by our guru at Treasury:

US Treasury Secretary, Scott Bessent, has stated that tariffs could raise more than $300 billion in revenue by the end of 2025

I think that actually provides Japan with leverage to push back on tariffs and scratching my head on QT???

What is the plan going forward? Will BOJ continue to accelerate QT?