Last time, $840 billion got sucked out in 5 months, all from excess cash in ON RRPs. But after $2.26 trillion of QT, ON RRPs are nearly gone.

By Wolf Richter for WOLF STREET.

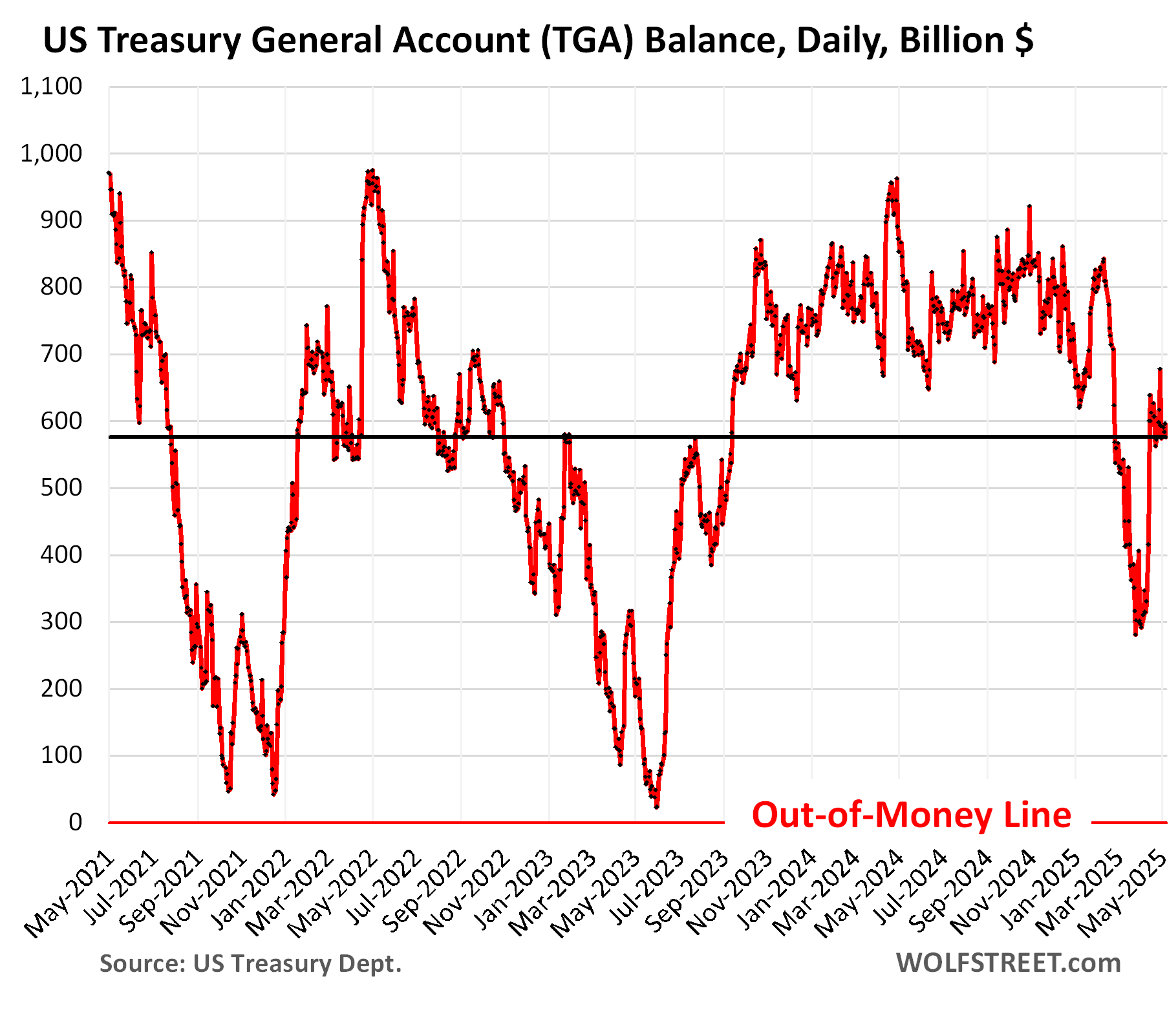

Back on April 3, 2025, cash in the government’s checking account, the Treasury General Account (TGA) at the Federal Reserve Bank of New York, had plunged to $296 billion, from over $800 billion in mid-February. Then came the flood of tax receipts, and by April 16, the TGA balance had shot up to $639 billion, and by April 30, to $678 billion. Then, the balance began to decline again.

On May 8, the closing balance was already down by $100 billion, to $576 billion, according to the Treasury Department. The flood of tax receipts likely moved the out-of-money date into August. The balance of the TGA got pretty close to zero during the prior debt-ceiling farces, which is about when Congress agrees to lift/suspend the debt ceiling. The TGA is cash parked at the Fed and is a liability on the Fed’s balance sheet. Draining the TGA pulls that cash from the Fed and throws it into the markets. That’s what we’re seeing now.

But note what happened the last two times after the debt ceiling was lifted or suspended: the TGA balance exploded.

The balance in the TGA is determined by the cash inflow from issuance of Treasury debt and collections from taxes, fees, and tariffs, minus the cash outflow to pay for daily outlays and to pay off maturing Treasury securities. The daily inflows and outflows can be huge.

The desired level of cash in the TGA is $800 billion to accommodate those huge daily flows, according to the Treasury Department. Once the debt ceiling is lifted/suspended, the TGA will be refilled pronto.

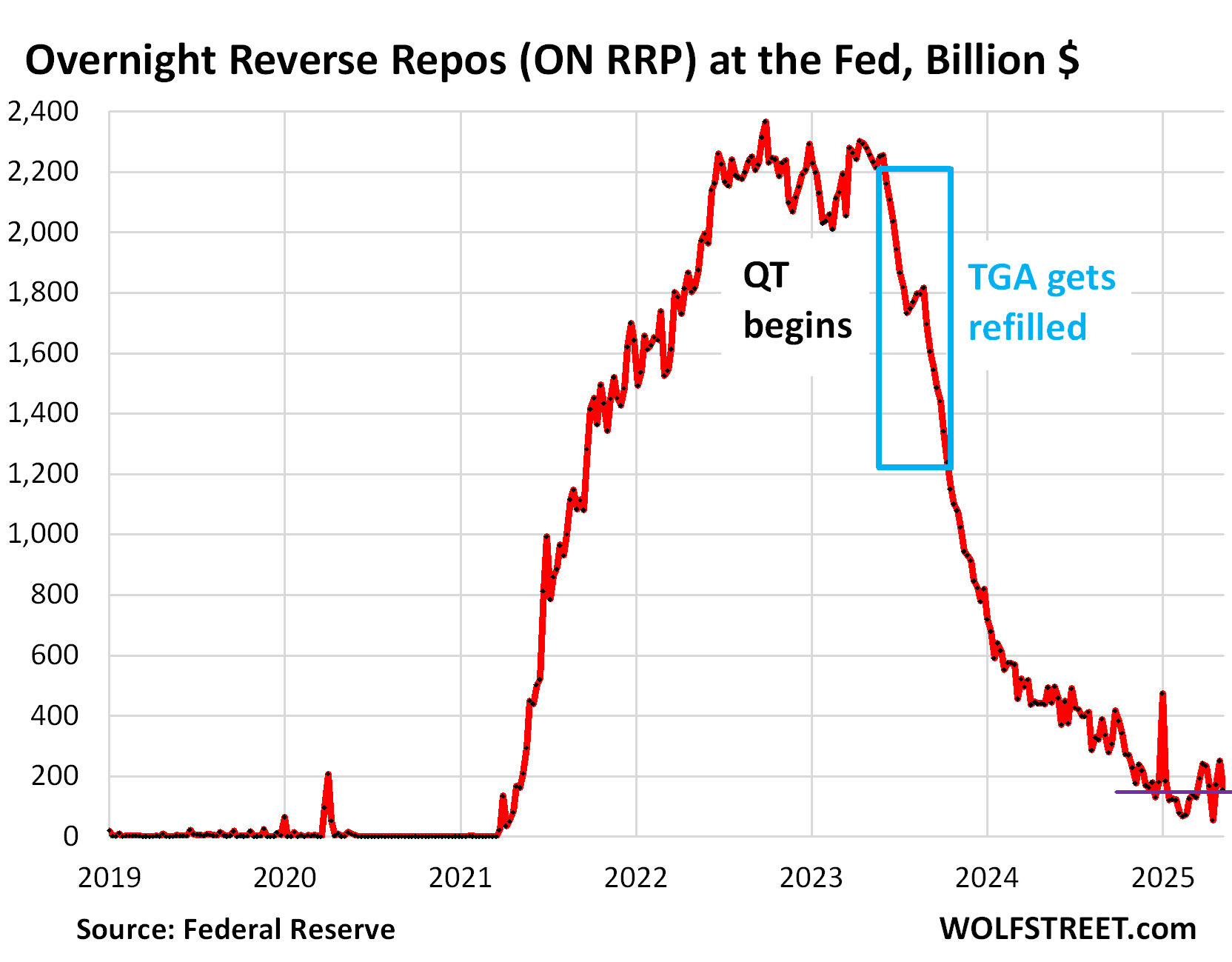

In 2023, in the six weeks between June 1 and July 11, the government sucked $520 billion in liquidity back out of the financial markets to refill the TGA by issuing huge amounts of T-bills on top of the long-scheduled regular auctions. Then over the next 3.5 months, it sucked another $320 billion out of the markets, $840 billion in total in less than five months.

But back then, that cash came entirely out of the cash that money market funds had parked at the Fed via overnight reverse repos (ON RRPs). ON RRPs essentially represent cash that money market funds don’t know what to do with, and so they place it at the Fed and collect interest.

ON RRPs plunged by $1 trillion in less than five months as money-market funds bought the T-bills that the government issued and paid for them with the cash from unwinding their ON RRPs at the Fed.

Last time when the debt ceiling was suspended, on June 3, 2023, money market funds had $2.2 trillion in excess liquidity parked in ON RRPs at the Fed, some of which they deployed to buy those T-bills that the government issued to refill the TGA.

ON RRPs are a liability on the Fed’s balance sheet, like the TGA. And the cash to refill the TGA essentially came from ON RRPs at the Fed via money market funds and T-bill issuance. From the Fed to the Fed. And markets barely noticed.

This time around, the Fed’s $2.26 trillion in QT has whittled down that excess liquidity in ON RRPs to just $142 billion. And if the TGA gets drawn down to near-zero again, and if Treasury then issues $800 billion in additional T-bills over a few months later this year and early next year, ON RRPs can only provide a small portion of that cash, and the rest of the cash to buy those T-bills will come from the financial markets and the banking system’s reserve balances at the Fed.

That’s what is different this time, compared to the last two times. This time, financial markets are going to notice that $800 billion in liquidity getting sucked out in a short time.

Buying a little bit of time: The large inflow this year by Tax Day pushed out the TGA’s out-of-money day. The tax haul was driven in part by massive capital gains taxes. The S&P 500 gained 26% in 2024 after having already gained 21% in 2023. Investors who sold winners in 2024 had to pay capital gains taxes by April 15. Payroll taxes were also strong, driven by record employment and record high wages. And then in April, $17 billion in tariffs washed into the TGA, up by 81% from March.

All this bought a little bit of time before the liquidity drain on the financial markets begins – assuming that Congress waits again till the last minute to raise/suspend the debt ceiling, rather than doing it, like, right now.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Congress should just make a permanent flexible debt ceiling, rather than these continual confrontations we have over them in the political arena, a game of chicken between Republican and Democrat that happens every few years.

Doesn’t a “permanent flexible debt ceiling” just mean no debt ceiling? I’m fine with getting rid of this political farce, but we should just say we’re ending the debt ceiling.

The debt ceiling is there to make the politicians think about how much they’re spending beyond their means. It doesn’t actually stop any of them, preferring to kick the can down the road, but at least it keeps the idea of a balanced government alive,

Brian is 100% right.

The debt ceiling is a failure as an actual *impediment* to the endless accumulation of federal debt. Because the legislature (for decades) has been willing with flirt with ruin in order to more easily resolve spending conflicts of the day (by borrowing – really printing – more money rather than hashing out a way to live within the means of tax revenue – at whatever level of taxation).

*But* – without the periodic chaos and rancor of official debt ceiling hikes, pathological legislative dysfunction would be made *easier* – 100% guaranteeing the pathologies would explode.

You don’t normalize/hide addiction – otherwise you get more addiction.

Brian and cas127,

The problem with these debt ceiling farces was the point of this article. Excess liquidity in markets now to be drained rapidly when the ceiling is inevitably lifted. Since these farces don’t really produce balanced government and the addiction is already normalized, I don’t think adding market instability to the mix of negative outcomes is productive.

Until we get the beautiful bill signed,Ha, it’s a game of chicken between republicans and republicans with the debt ceiling vote. Unfortunately…..RIP tea party,

Very useful and easy to understand article! As TGA is drawn down to near ZERO over the next three months, and with ample bank reserves at a stable 3.2 trillion, there is a very high chance that RRP balances will begin to increase by large amounts over the next three months. I think we have seen the bottom in RRP at around 40 billion dollars a few weeks ago. If I am right, and the RRP increases by 200 or 300 billion before the Congress

raises or abolishes debt limit, this increase in RRP may mitigate the pressure on the system when the Treasury refills the TGA. So, keep an eye on the daily RRP balance!

What if banks hold more T Bills instead of reserves or RRPs?

It is my belief that the money market funds are the big players in RRP. They cannot find a suitable place to invest the marginal dollars elsewhere and the big banks do not want MMF deposits because it causes a diminishing or even a negative return for the money center banks. So, the MMFs park the money at the Fed.

Bobber,

Banks don’t hold ON RRPs. They put their cash in their reserve accounts at the Fed because reserves pay more interest than ON RRPs.

Banks already hold T-bills. But there are regulatory differences between reserves and T-bills.

Reserves going down is exactly what refilling of the TGA will do, that’s where part of the cash will come from because reserves are cash from bank customers, and if they buy T-bills with their cash, the banks end up with less customer cash, and their reserves will drop. That’s exactly what we mean when we say “refilling the TGA sucks liquidity out of the financial system.”

but arent bank reserves also created using QE? and isnt the Fed doing stealth QE, through SOMA buys at auction? and isnt global liquidity rising, while CBs ex BOE drop interest rates? TGA sucks with a straw, while the global firehose keeps things wet and wonderful.

You smoked way too much pot this morning. I will just single out this one:

“…isnt the Fed doing stealth QE, through SOMA buys at auction?”

This “stealth QE” is ignorant BS spread by people who don’t understand what a bond is.

Bonds are not like stocks. Bonds mature at the maturity date and the holder gets the face value of the bond paid back in cash. So if you manage a big portfolio, there are always securities that mature all the time, and you get your money back. T-bills mature in 1 month, in 2 months, in 3 months, etc. up to 1 year, and everyone that has held them on auto rollover knows exactly what happens: every three months when your 3-month T-bill matures you get your money back plus interest, and then at the next auction, you buy the next batch of 3-month T-bills, and that money gets sucked out of your bank account. Lots of people here are doing this and understand how this works.

So if you hold a 10-year note, on maturity date you get you money back, and if you want to maintain your portfolio, rather than sit on this cash, you have to buy a new issue of a 10-year note.

The Fed has a $4.2 trillion portfolio of Treasury securities, and so lots of securities mature every single month. The way it does QT is by not rolling over all maturing securities. Those that it doesn’t roll over, “roll off” its balance sheet, and its balance sheet declines by that amount. It replaces the rest of the maturing securities by rolling them over. The roll-off is capped. That is the amount of QT, that’s by how much its balance sheet declines.

You have obviously never ever read a single one of my Fed balance sheet articles, or else you wouldn’t spread this ignorant BS that you picked up in an internet garbage dumpster.

“You smoked way too much pot this morning”

:”D

“You smoked way too much pot this morning”

😂

Does the Treasury have to refill the TGA quickly? Like a statutory requirement or something?

Or could they do it slowly, say over 12 months? Or not at all, and simply run with the TGA at close to zero?

Or could the Treasury do it with 2-7 year coupon bonds in the “belly” of the yield curve?

Bessant seems like a guy who might think outside of the box on something like this if it’s likely to cause an actual liquidity squeeze. Or is a liquidity squeeze not such a big deal, and the Administration is likely to let it simply happen?

The Treasury likes to keep a balance of 700 to 800 billion dollars. Remember that the US annual budget is around 7 trillion dollars. It is similar to keeping one or two months of your annual expenses in your checking account.

There is no legal reason. They have to refill it very quickly up to a fairly decent level because it’s super risky to not have enough cash balances to be able to pay off maturing bonds while a bunch of other things need to get paid the same day, and for some reason, revenues are a little slow, for example. That account needs to have a huge cushion to avoid a potential fiasco. That $800 billion is the desired level. They can operate with a lower balance. But it gets riskier the lower the balance goes. It cannot operate with just $40 billion in that account. It would have to kite checks to do that, and that’s hard to do today with electronic payments.

There exists the “Unclassified” line item, the last line item, in fact, in the TGA, both on the deposit and withdrawal side of the leger. The deposit side, FYTD, is tiny, at $3.2 billion. However, on the withdrawal side, FYTD, it stands at $168 billion. Any idea what “unclassified” entails and why such a large imbalance? Hookers ‘n blow for the congress, fed, and POTUS on the withdrawal side, perhaps?

In the Daily Treasury Statement you’re referring to, deposits and withdrawals are classified by department or entity, such as DOD, NASA, SSA, SBA, OPM, Legislative Branch, GSA, FTC, public debt, etc.

There are also deposits and withdrawals that are not classified by department, so “unclassified.” But they are MINUSCULE, less than 1%, of the inflows and outflows. It’s a catch-all, such as “miscellaneous” or “other,” for stuff that’s too small to bother with on a published report.

YTD total:

Deposits: $22,608 billion

of which “unclassified” $3 billion = 0.01% 🤣

Withdrawals: $22,918 billion

of which “unclassified” $168 billion = 0.7% 🤣

Note that the biggest part of the deposits and withdrawals is the cash flow around the public debt, paying off maturing Treasury securities and issuing new Treasury securities.

Paying off maturing government bonds would be a predictable amount and should be covered by issuing new bonds at a higher interest rate than those maturing.

Paying off old debt with new and increasing debt at a higher interest rate without cutting expenditure would to my mind be rapidly becoming unsustainable. The so-called debt ceiling in reality does not exist as it is always ignored. Time for congress to cut military and other unnecessary expenses The US faces no risk of invasion by foreign forces

So, best to anticipate a big stock market drop later in the year?

Is there a legal requirement that says the TGA can’t go negative (overdrawn)? It’s not like the Sheriff is going to show up at the front door at the White House. We’ve lost any semblance of fiscal responsibility with overspending and massive tax cuts, not to mention this farce of a debt ceiling and the Fed buying treasuries, why not just take that last step to moral decrepitude? Maybe say it’s for the children or something…

“The last step to moral decrepitude” Are referring to a massive default or just inflating the debt away slowly and hoping that nobody notices?

That’s always the hope – that they can inflate it away slowly, with nobody noticing. Like a lot of things in life, that works until one day it doesn’t. Then the @#% hits the fan.

From a trader / investor perspective, the problem is that we have no realistic way to predict when that one day will occur.

INFLATION. Huge amounts of inflation.

That’s always the result sooner or later when a central bank funds government spending. See Argentina, they have this system.

But how does Japan get away with a debt of 256 percent of GDP? Why can’t we do this?

They didn’t get away with it. it just took a while.

They now also have inflation, quite a bit more than in the US, and rising, 3.6% overall.

And their currency crashed against the USD by 30%. So Japanese people stopped traveling overseas because they cannot afford it anymore, and they’re paying out of their nose for imports, which they stopped buying when possible, because they cannot afford them anymore.

Japan is also a credit nation, which helps them out.

“The data add to signs that Japanese households are shifting their long-held stance of holding deposits or cash, a strategy enabled by more than a decade of deflation.”

At one time “Japanese households have 52% of their money in currency & deposits, vs 35% for people in the Eurozone and 14% for the US.”

A rise in the demand for money slows the circuit income velocity of funds. So, the BOJ was able to monetize and sterilize more funds.

Isn’t most of that debt held by their national bank? I haven’t checked the numbers.

If you consider the national bank to be part of the government, which I do, much of the government debt cancels out. What matters more is the portion of debt held by the public.

90 days until China tariff issues kick off again.

90 days until T bills need selling to stay solvent.

Could get interesting?

Only $17B in tariff income? I thought we were all going to be rich?

Rich??

I thought the world was supposed to end.

Tariffs were going to take us back to the stone age. We would revert to hunters and gatheres. Even the Amish would suffer.

Oh well just fueled up the work equipment for 2.75 gallon.

The next stone age will be different with Bitcoin around.

BitCON and “crypto” are the biggest financial scam in history. Rich people created a fake product and are making mountains fleecing the suckers, like southeast Asians toiling away in rice paddies while pouring all their wages and life savings into it.

We can criticize Bitcoin, but there are lots of things in this world that have value due to faith and tradition, some more lasting than others. Religion, marriage, government, family, gold, monetary stability, law and order, etc.

If enough people continue to believe in it, it will sustain, and there’s no set time limit for human irrationality and group think.

I do not hold any Bitcoin or crypto garbage.

Caveat emptor. An old friend tried to buy bitcoin through a 3rd party and ended up losing all of his money.

Stone Age (next one) = NO INTERNET. No internet = NO BITCOIN!

Tariffs are not going to end. I look forward to more crazy swings after the 90 days are up. Maybe even before the 90 days are up.,,,,because markets will be moving on the whims of one country’s leader.

Hmmm….USA pays 30%, Chinese 10%. Best businessman ever, eh ?

I doubt it. Many things were never discussed such as China increasing US imports or rare earth minerals. Trump’s strategy right now is to not lose the midterms as almost all 2nd term Presidents are lame duck in last two years, even if they control Congress. Our election cycles are so long that everything is aligned to who is next president

Source? Trust me bro

old ghost,

Your numbers are backwards

Oops never mind!

Eric86 wants a Source ?

Google Reuters, or CNBC.

Or were you asking for the definition of a tariff ?

It should be US importers and Chinese manufacturers pay

30%. Whether they can pass those costs onto the consumer, we’ll see. If some production moves back to the US, that’s a win.

“Google Reuters, or CNBC”

LMFAO. Fake news central…

Thanks for the update Wolf. Personally, I no longer lend the government money for anything less than 5% interest…

Looking forward to a complete treasury analysis. If I remember correctly, there is a fair amount of debt that needs to be rolled over this year…

Hey Wolf,

Any thoughts on how the US government plans to refinance the 7.8 trillion in debt coming due this year? I believe that the majority of this is shorter duration, but I am sure you can correct me if I am wrong.

https://www.treasurydirect.gov/auctions/upcoming/

So, it’s hard for me to assess whether or not you think ON RRPs dropping really close to zero is going to be an issue. I guess you’re saying it matters more how much of the reserves the Fed allows to be used that matters?

Sitting behind all of this, I assume, is the very real possibility that the Fed is forced into real QE again, if reserves drop below that ~ $6T’ish threshold that I think you’ve talked about occasionally?

O/N RRPs were misclassified. The draining of the O/N RRPs increased both the supply of money and the supply of loanable funds.

Aug, 9 WSJ:

“In their Aug 6. letter in response to our op-ed “How the Fed Is Hedging Its Inflation Bet” (Aug. 2), John Greenwood and Steve Hanke argue that the Fed’s sale of a trillion dollars of reverse repos does not in and of itself reduce the deposit liabilities of banks and money-market mutual funds, and that the money supply is unaffected. By that logic, none of the monetary tools of the Federal Reserve Bank would affect the money supply.”

1. ON RRPs are normally at zero, and it’s not an issue. And they’ll go back to zero as QT drains more liquidity. But the debt ceiling causes massive liquidity flows, first into the markets (right now), and then out of the markets after it’s lifted.

2. Before 2008, the Fed’s balance sheet has always grown in line with its liabilities (mostly cash in circulation at the time). At some point in the future, the Fed will end QT, and at that point, the balance sheet will remain flat (it did that in 2014-2017). But remaining flat in a growing economy and with inflation devaluing its dollar holdings, it means that in relationship to the economy, the balance sheet is still shrinking. This was a mild form of QT in 2014-2017, before actual QT started. And it’s going to do that again in the future. Then when the balance sheet in relationship to the economy is deemed low enough (reserves), the Fed will let the balance sheet grow as it had done before 2008. There is a lot of BS being circulated around out there.

Hi Wolf,

Possible typo:

‘ if Treasury then ‘

My best wishes to you..

Thank you. But actually no typo. In the quaint manner of US gov speech, gov departments don’t get an article.

For example, from the horse’s mouth:

“The report builds on Treasury’s work on AI-related cybersecurity risks in the financial sector…”

https://home.treasury.gov/news/press-releases/jy2760

Same with all departments, such as CIA et al.

From CIA’s “Ask Molly” (Googling is hilarious):

“I’ve worked at CIA for a long time, and I can honestly say…”

https://www.cia.gov/stories/story/ask-molly-may-12-2021/

Wolf,

From your last article titled “10-year Treasury Yield Back at 4.39%, Yield Curve Steepens at Long End, Mortgage-Rate Spread Remains Historically Wide”, the fifth figure shows the Treasury Yield curves for May 9th and other dates. When the refilling process begins in earnest, will that tend to cause upward pressure on TIP rates? I have some money in 1 month t-bills. I have been following your data, and I can’t fathom why anyone would loan money to the Treasury for a longer time at a lower interest rate, hence my refusal to put it into 3 mo, 6 mo, or longer t-bills. At some point, that curve has to start to de invert across the spectrum, and interest rates increase across the board. Thoughts?

The refilling takes place by issuing large amounts of T-bills. Later some of the T-bills will be replaced by increasing the issuance of notes and bonds. When that happens, there should be upward pressure on longer-term yields.

And if the TGA gets drawn down to near-zero again, and if Treasury then issues $800 billion in additional T-bills over a few months later this year and early next year, ON RRPs can only provide a small portion of that cash, and the rest of the cash to buy those T-bills will come from the financial markets and the banking system’s reserve balances at the Fed.- Wolf

That assumes that reserves are earning less than T-bills. Do you see the yield of T-bills going up again to find demand if Reserves reach that level that the Fed finds sufficient? I mean, the idea is that Reserves can’t go down to near zero like ON RRPs so finding demand might be a problem?

Reserves cannot go to near zero. Each bank has a reserve account at the Fed, it’s how banks pay each other every day. Huge volumes go through these reserve accounts every day, from your mortgage payment to payments needed to buy stocks and entire companies. The reserve accounts at the Fed are the central core of the US payments system. So banks have to have enough cash in their reserve accounts, and still they have to manage the timing of when they send out their payments, but other banks do that too, so it gets very complicated daily. The Fed allows banks to overdraw their reserve accounts for very short periods, such as minutes or a few hours when payments go out before a big chunk of payments come in. So there will always be a substantial amount of cash in those reserve accounts. But it could be a lot less than $3 trillion (currently).