Despite the rumors during bond turmoil, foreigners kept buying Treasuries and the “basis trade” didn’t blow, but the “swap spread trade” made a mess.

By Wolf Richter for WOLF STREET.

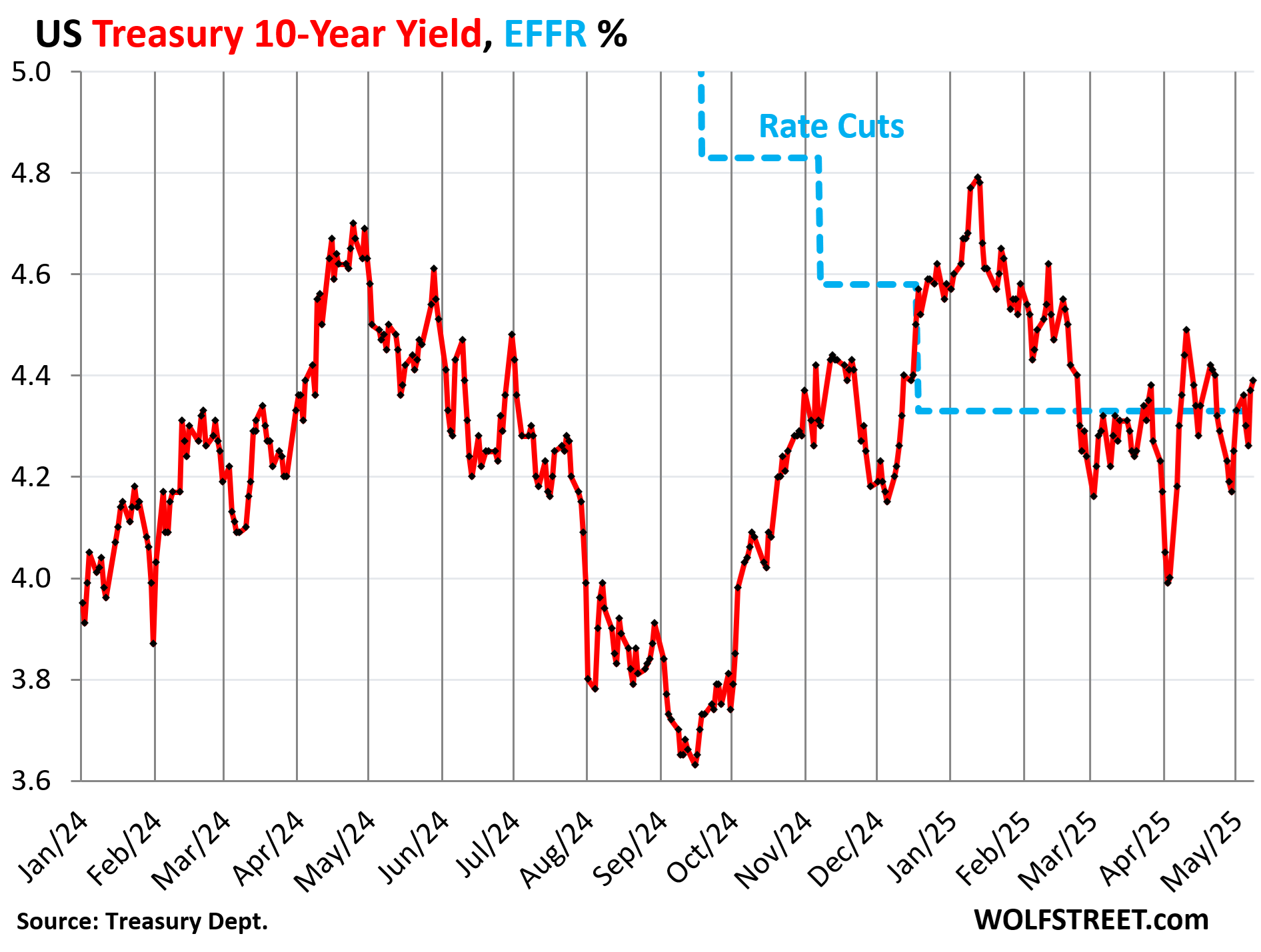

The 10-year Treasury yield rose to 4.39% today and is now back in the middle of the range of the past two-plus years, despite the gyrations in between, having brought behind it the deep plunge to 3.99% (bond prices soared) in late March and early April, followed by the brutal re-spike to 4.49% (bond prices dropped) after the announcement of the new tariffs on April 2.

But now the yield has calmed down at 6 basis points above the Effective Federal Funds Rate (EFFR), a short-term money-market rate that the Fed tries to keep locked in place with its policy rates.

Spikes followed by plunges, and vice versa, in an always edgy bond market are part of the deal and don’t indicate long-term trends.

Everyone from Bessent on down loved the big plunge to 3.99% because everyone loves low long-term interest rates because they matter for the economy, and the real estate industry was salivating about mortgage rates falling below 6% or whatever because the 10-year Treasury yield is hugely important for mortgage rates.

But when the 10-year yield re-spiked in early April, it unleashed all kinds of rumors in the media about foreigners refusing to buy Treasuries to punish the US government, and about the “basis trade” blowing up, and both turned out to be wrong. But there was a highly leveraged Treasury trade that soured when yields re-spiked, and unwinding that souring trade exacerbated the yield-spike further, and we’ll get to all those in a moment.

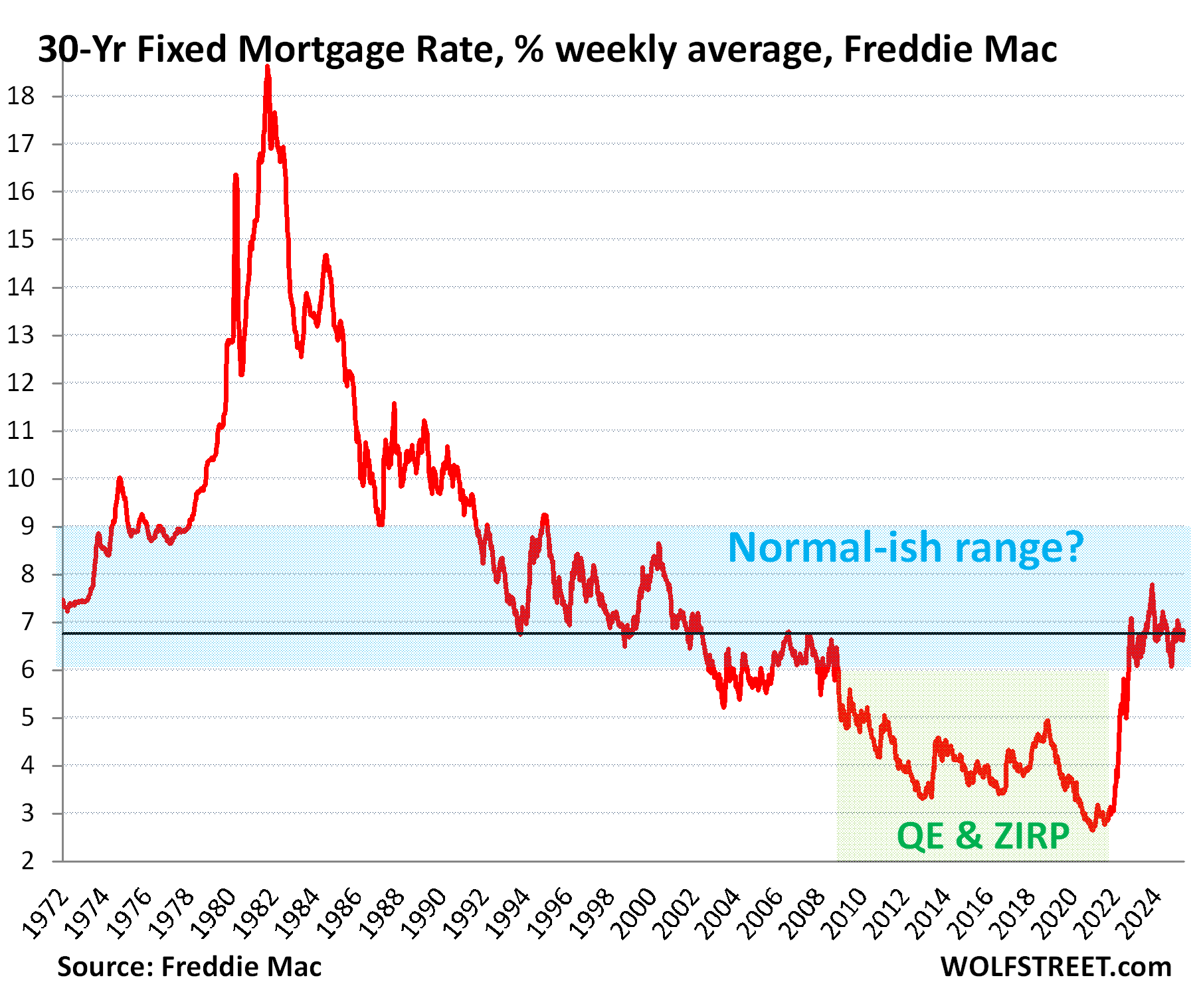

Mortgage rates remain near 7%.

The average 30-year fixed mortgage rate was unchanged at 6.76% for the second week, according to Freddie Mac on Thursday. They’ve been north of 6% since September 2022.

Historically, the average 30-year fixed mortgage rate didn’t drop to 5% until the Fed started QE in 2009, which included the purchases of ultimately trillions of dollars of mortgage-backed securities, which helped push down mortgage rates and was part of the Fed’s scheme of interest-rate repression and asset-price inflation.

But when raging consumer-price inflation broke out in 2021, the Fed eventually put an end to buying MBS, and since mid-2022 has been shedding them. And mortgage rates have been in what we might call the historically normal-ish range since September 2022 of above 6%.

The 3% mortgage rates were a brief aberration that created massive distortions in the US housing market and were the final act of the 40-year bond bull market.

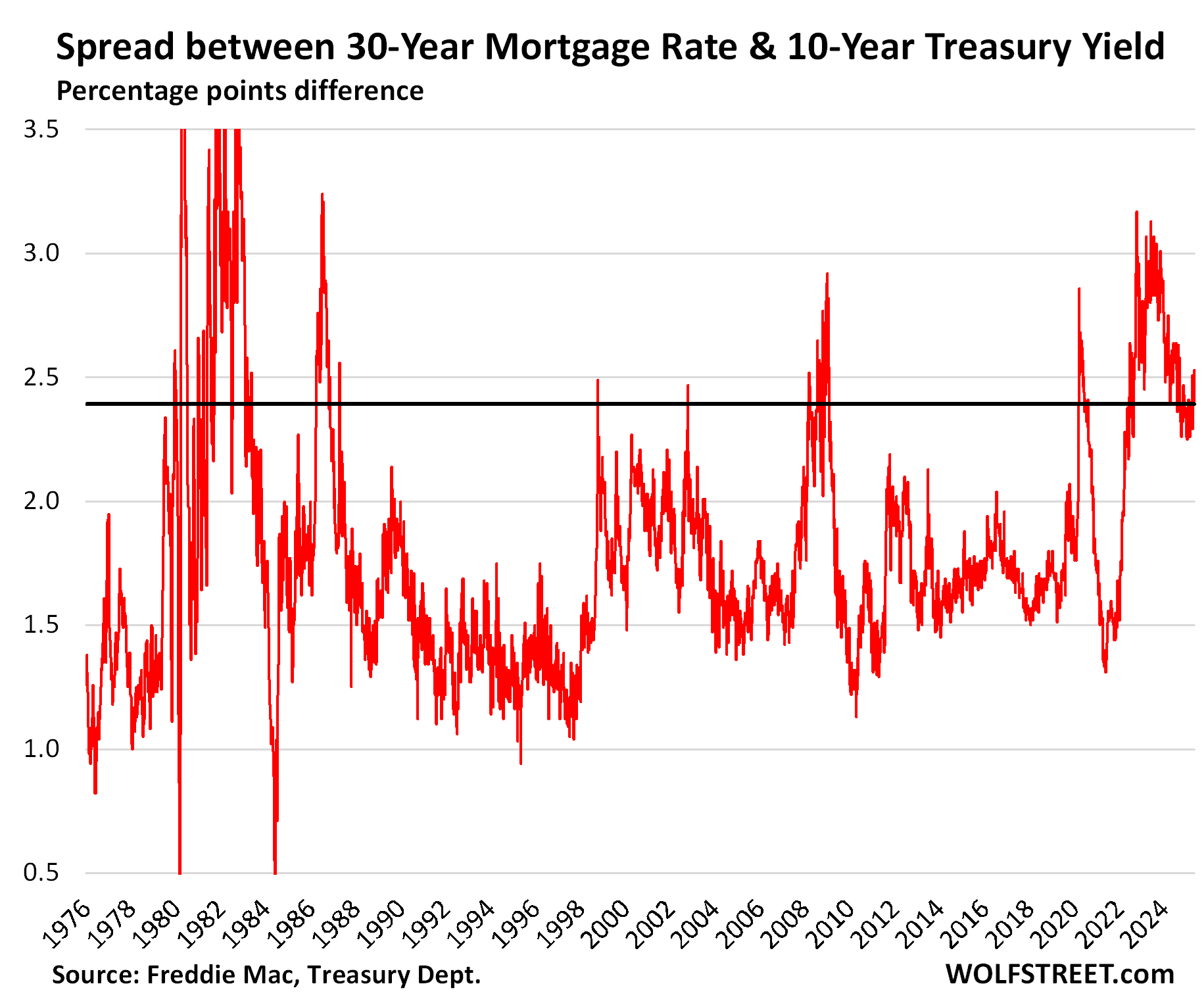

The spread matters. Mortgage rates track the 10-year Treasury yield, but are higher, and this spread varies but is currently relatively wide at about 2.4 percentage points, keeping mortgage rates relatively high with respect to the 10-year Treasury yield.

Over the past 50 years, there were not many years when that spread was wider. My thoughts about this phenomenon here.

The Fed’s new mantra: “Wait and see.”

At the Wednesday press conference after the FOMC meeting, Powell kept getting bombarded with the same questions about rate cuts.

But Powell, with super-human patience, kept giving the same answer: The Fed will “wait and see,” he said 11 times. “Uncertainty is extremely elevated,” he said, and the Fed is well-positioned to “wait and see.” 11 times. It has become a mantra.

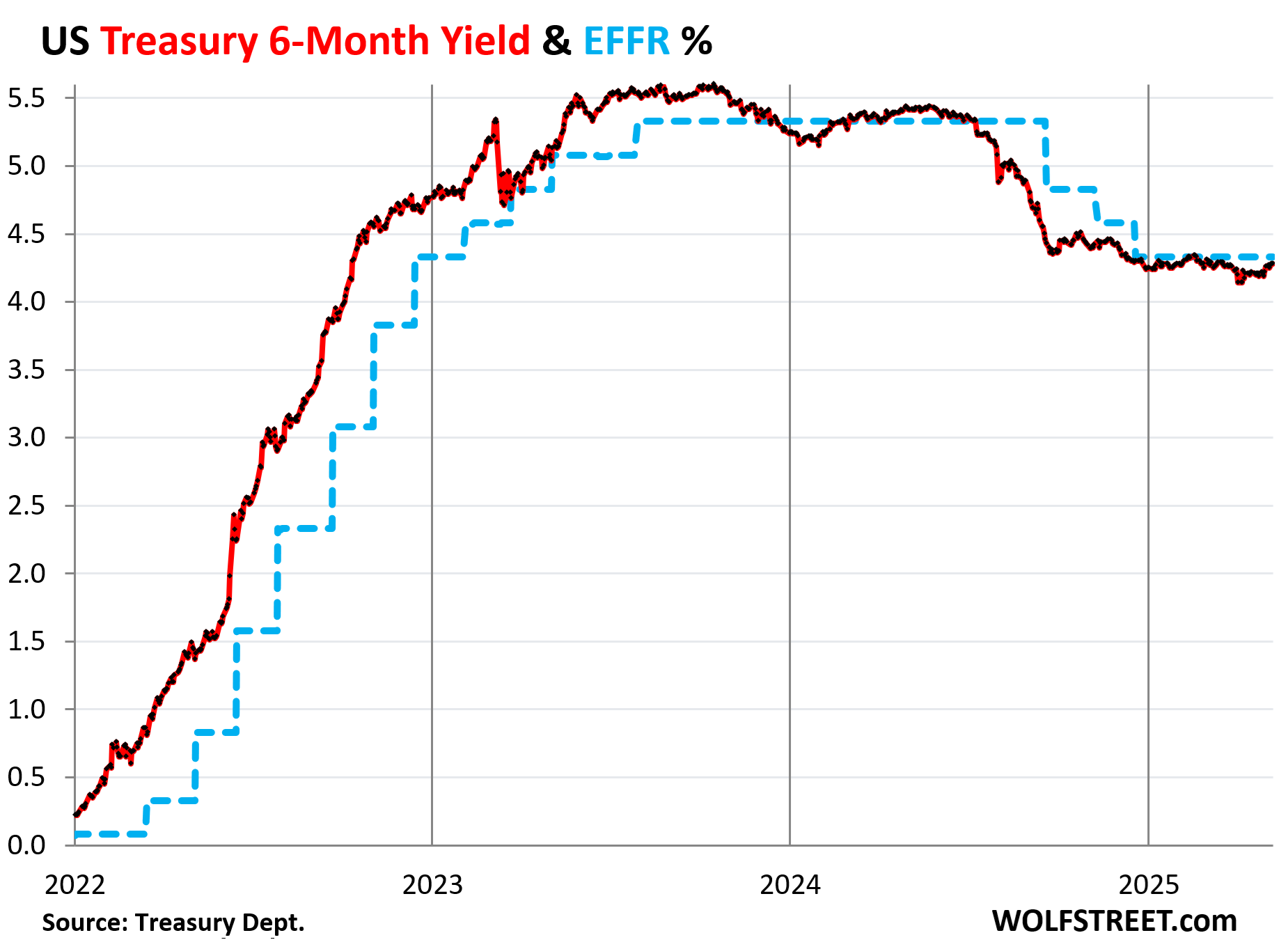

The six-month Treasury yield has taken rate cuts off the table within its window. It has edged higher since March, approaching the EFFR from underneath:

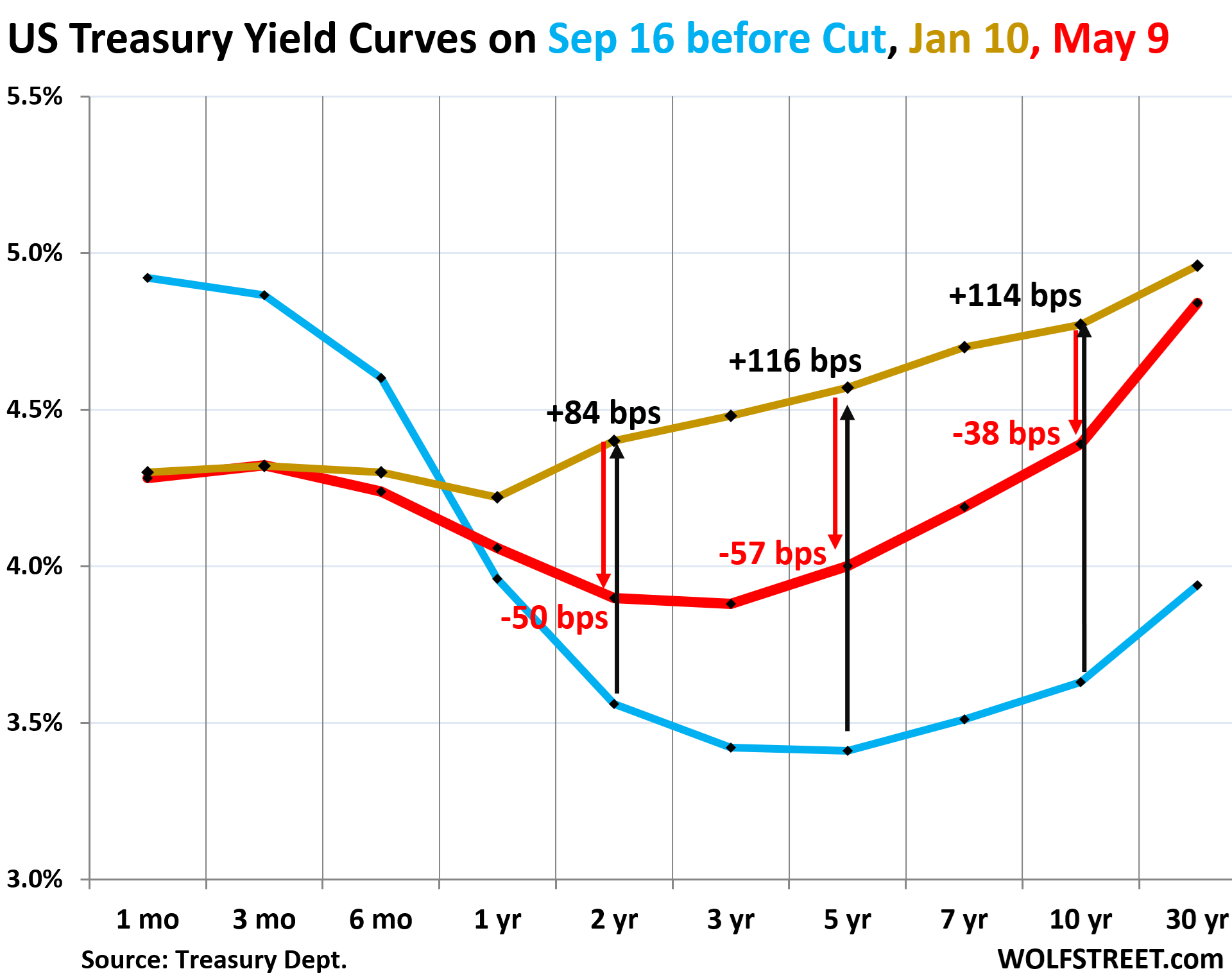

The yield curve steepened at the long end.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, before the Fed pivoted to wait-and-see.

- Red: Today, May 9, 2025.

- Blue: September 16, 2024, before the Fed’s monster rate cut.

Amid the mantra of wait-and-see, short-term yields from 1-6 months haven’t moved much and remain near the EFFR. The sag in the middle got a little shallower, as those yields rose.

Long-term yields have snapped back from the early-April lows, with the 10-year and longer-dated yields higher than 1-to-6-month yields. That part of the yield curve has un-inverted, if only by a hair.

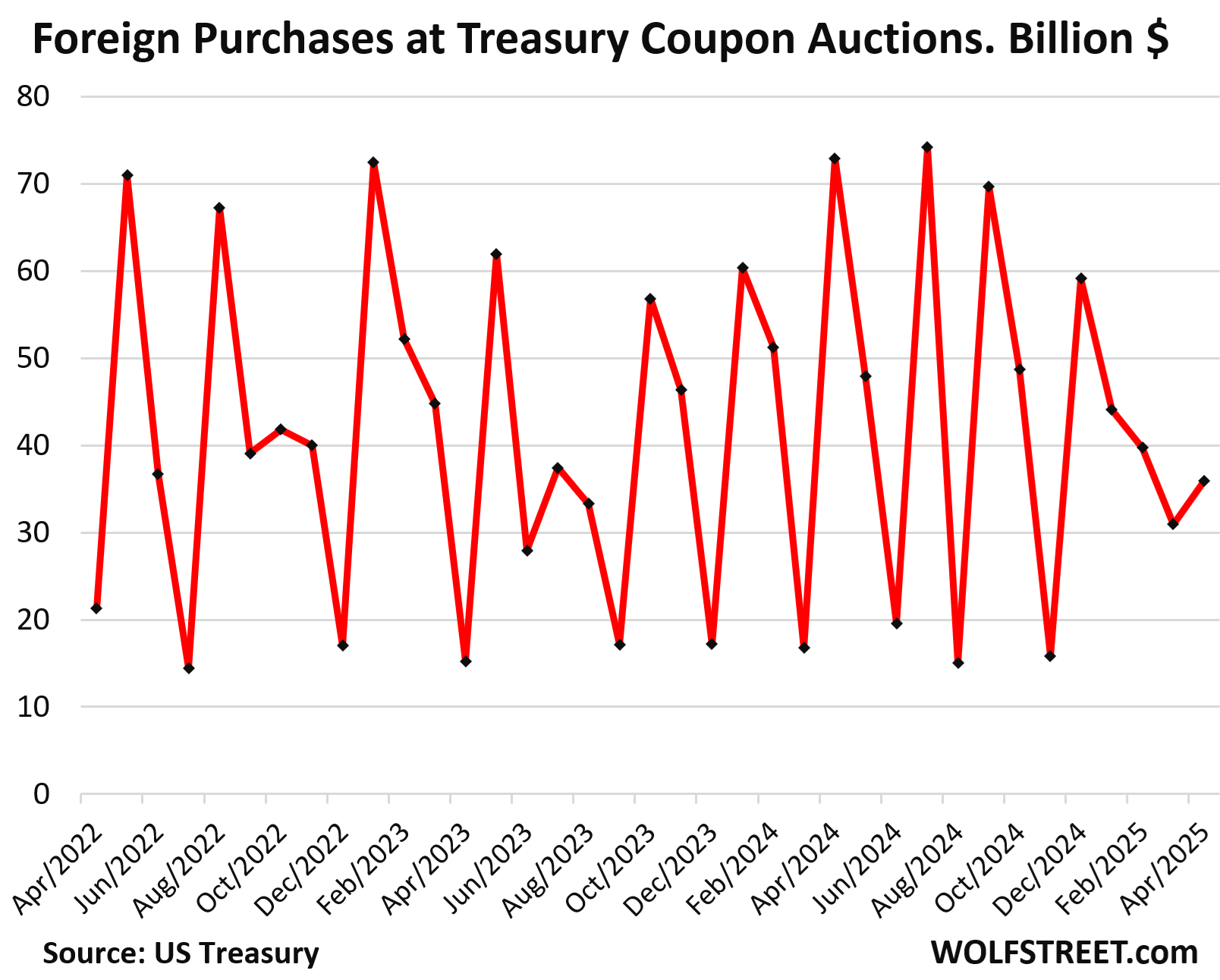

Foreigners kept buying at Treasury auctions, no problem.

When yields spiked in early April, rumors raged that foreigners were punishing the US government for the tariffs by not buying at the Treasury auctions.

That turned out to be just another rumor that was fun to spread, as we now know from the Treasury Department’s Treasury Auction Allotment Reports, released twice a month, with detail as to who bought what.

In April, foreign investors bought $36.0 billion in 2-year to 30-year Treasury securities, up from March ($31 billion) and within the range. The large month-to-month variations are in part a result of the large variations in the amounts of securities sold in various months.

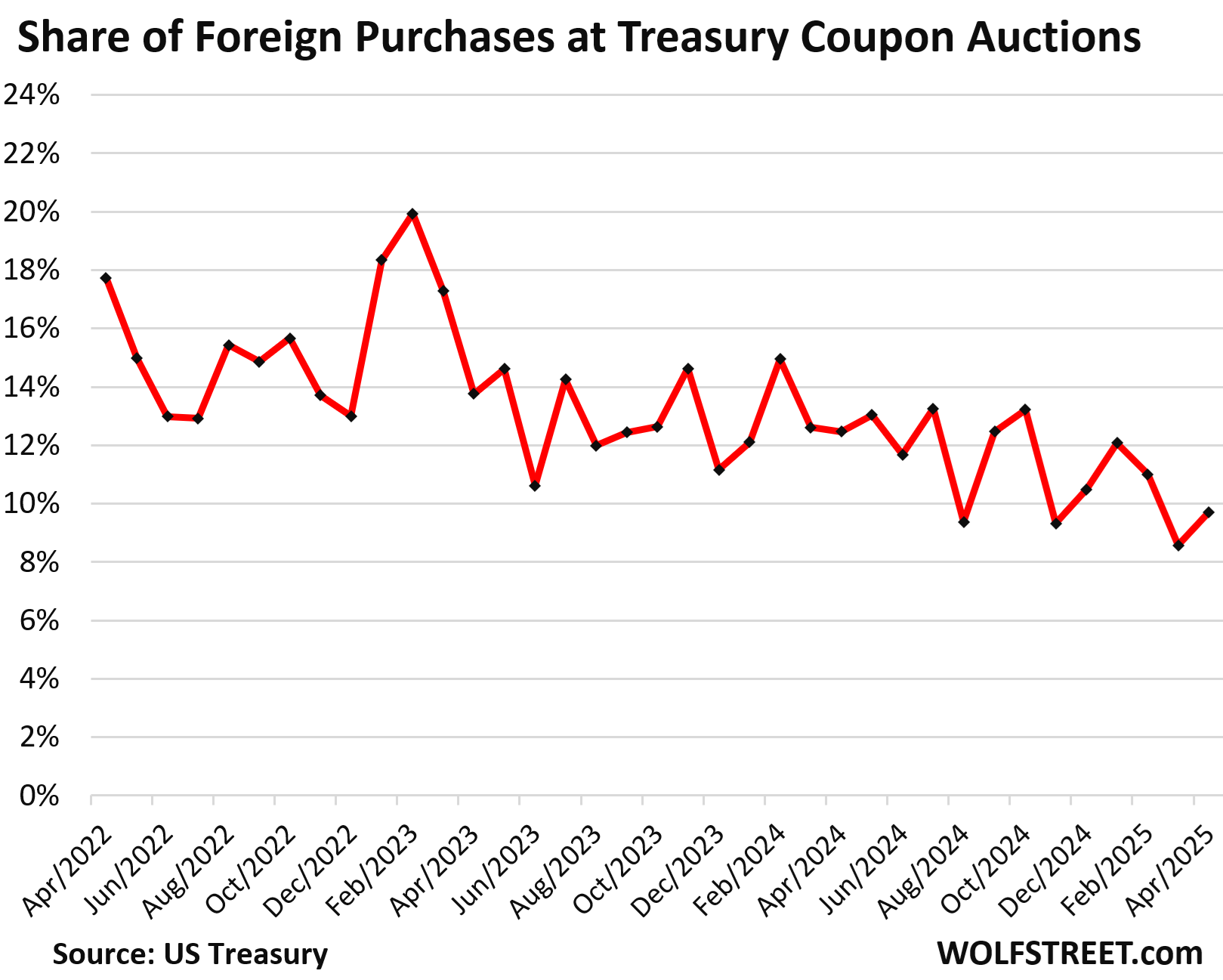

Over the years, foreign purchases have increased in dollar amounts, but the US debt has grown so fast that foreign buyers have lost share, and domestic buyers have picked up those securities. This also shows up at the auction, where foreign purchases have not kept up with the increasing auction sizes. But the process has been slow.

In April, the share of foreign purchases of total securities sold (Fed purchases excluded) rose to 9.7%, which was a higher share than in March (8.6%). But we can see the longer-term trend that their buying is not keeping up with the increasing auction sizes due to the ballooning debt and deficits:

“No Evidence” the basis trade blew, but the “swap spread trade” made a mess.

There is “no evidence” of an unwind of the Basis Trade, said Roberto Perli, Manager of the System Open Market Account (SOMA) at the New York Fed, in a long speech today on the Treasury market events in late March through mid-April that had caused such consternation.

He estimated the notional value of the basis trade to be about $1 trillion. He said:

“One factor that could lead to a rapid unwind of the basis trade is substantial repo rate volatility or a persistent increase in repo rates, which could in turn increase the cost of financing the position and therefore make it unprofitable.

“But this by and large did not happen in April since repo rates were fairly stable and dealers remained willing and able to intermediate. As a result, according to Desk staff’s estimates, the basis remained relatively stable.

“This stands in sharp contrast to March 2020, when the basis jumped by about 100 basis points and the unwinding of basis trades was likely an important contributor to the sharp dislocation in the Treasury market we observed at that time.”

But the “so-called swap spread trade” made a mess, as the 10-year yield was snapping back in early April, exacerbating the spike in the yield. Perli said:

“Reportedly, many leveraged investors were positioned to benefit from a decrease in Treasury yields of longer maturity relative to equivalent-maturity interest rate swaps, partially due to the expectation for an easing of banking regulation that would bolster bank demand for Treasuries.

Since swap spreads are defined as the swap rate minus the Treasury yield, leveraged investors were making a directional bet that swap spreads would increase.

“However, on the heels of the tariff announcement, swap spreads started to decline and made the swap spread trade increasingly unprofitable.

“Because this trade is usually highly leveraged, prudent risk management dictated that the trade should be quickly unwound, which is what appears to have happened. The unwinding involved selling longer-term Treasury securities, which likely exacerbated the increase in longer-term Treasury yields.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As the USS Dollar continues to go boldly where no one has gone before.

Dollar Index [DXY] at 100.4:

Uh, according to Wolf’s chart, we’ve been here before. The sky is not falling.

It’s boldly hanging to the 50 year norm…

🤣 One of the reasons to come to the comments is for the humor. Never a dull moment in this joint.

Jeff, have you been watching too many old Star Trek reruns?

Acknowledged, but the return to 4.39% suggests everyone knows where we are going ultimately. It’s like we’ve seen this show before and we know the dollar is drifting further and further away from 1971.

Lol, 10/10, no notes.

Yes, I acknowledge that you completely disproved my statement with a single graph, but I still feel I’m right.

The hardest part for dollar obsessives is the that any correlation between dollar strength and anything meaningful is moderate at best. When are the economic glory days we’re supposed to be shooting for? The late 90s, when we had some of the highest employment rates in history? Well, the dollar index was almost exactly at 100 then. The Trump years that everyone seems to be pining for? Same.

Late 90s when oil crashed to 8 usd in 1998/9 after staying low for almost a decade . USA thrives on low oil prices however I worked for an upstream oil company and we had massive layoffs in 1999 . Mergers layoffs etc . Not a pretty sight

We’re not seriously suggesting the basis trade didn’t try to unwind? Does no one care about being gaslit anymore?

Sorry to disappoint you. It would have been so much fun if the basis trade had blown up. It did blow up in March 2020 though. But do read the stuff about the basis trade in the article, not just the subtitle. It tells you what unwound.

I miss the RTGDFA’s

Where, pray tell, is that which everyone knows is where we are going ultimately ?

Good article, Wolf. Definitely described the known parameters of the 10 year. The interpretation of the facts is an individual prerogative. For instance I think your statement :

“Everyone from Bessent on down loved the big plunge to 3.99% because everyone loves low long-term interest rates ”

Which I think is accurate. The market reacted in a mindless fashion indicating confusion which was subsequently verified to the retracement that we are currently experiencing.

The reasons for a market driven decline in the rate complex are, outside of QE which artificially suppresses the complex, not a sign of robust demand.

The direction which everyone knows we are going is: the USD is worth less. Ultimately? Completely worthless.

We can measure the over 99% reduction in purchasing power of the USD since the establishment of the Fed.

Not that it’s the fault of the institution, it’s just the inevitable outcome of all “fiat” or arbitrarily created “store of value.”

It’s true for all currencies, companies and empires. The feature of technology and communication is that this process is now accelerated!

Rome lasted for 1000+ years in power, Britain couldn’t survive half that, and now the US may spend less than half that in the driver’s seat?

BTC will not feed my children and neither will gold. The stuff of life is not produced by any company or currency, but these things are established to create (a concept of) power and control OVER the stuff of life.

This is not a trade or investment advice. Arable farmland is an eternally increasing asset, especially compared to an inflating currency and degradation of “land formerly known as farmland.”

Vertical/ indoor farming and modern agricultural methods are more valuable than financial assets, but the rules of the game are against basic survival and are centered around excess consumption.

TLDR: The fate of everything considered “wealth” is the same as that of you and I: going to 0. Remember your Mother this weekend!

…Struggler-ALWAYS good to remember every one of us, from the mighty on down, are only the current crew on this spacecraft, and will only occupy that position as long as those basic planetary systems that brought us here continue to be available and functioning at species-friendly levels. (reminder: ‘saving the planet’ is a null term, it cares not what ‘rules’ it’s surface…).

may we all find a better day.

All stores of value only have meaning until they don’t. Because value is in the eye of the beholder and changes with time, society, technology, and human beliefs. That’s not something magical about fiat currency, it’s true about gold, shells, cars, Bitcoin, houses, horse-drawn carriages, canoes, and every single “permanent” store of value ever invented.

Numbers:

Of all those items you mentioned only one is false.

Gold has not only maintained is store of value, but sometimes increased it.

True for the last 100 years, 200 years and even longer.

Better in some countries’ currencies as well.

Golden Dragon:

It’s possible to test your argument by plotting how many loaves of bread one could buy with an ounce of gold in the US over 200 years. Pay close attention to times of war.

Our communist containment deficits were responsible for 1971 – along with the E-$. The private sector was running surpluses. Today, we have 750 foreign military bases. Our trading partners have yet to become sated with dollar denominated assets.

Yeah, base number 461, an antenna with an associated power source in Japan is a real concern….

That number, 750, is so fake that people who repeat it have no idea at all.

128 foreign military bases maybe. But it has hundreds of “installations,” which can be as small as a building under the control of the military.

Gee, ~5% for 30 year UST risk. Nah. Pass.

I’m a fairly smart guy, I have a finance degree, I’m a decent investor, I make nearly a million bucks a year. However…

Yield curves and rate spreads over time coupled with basis trades, reverse repo implosions and the other myriad 3rd derivative terms make my brain hurt. I buy undervalued equity, and I sell over valued equity. That’s all I do, it’s all I can really understand.

As Warren Buffett (the soon-to-be-retired Warren Buffett) would say, stick to your circle of competence. If you don’t understand obscure transactions, eschew them. There’s no shame in that whatsoever.

That’s like telling someone something Einstein said to make stupid people feel better.

Just say “well you’re no Warren buffet THATs for sure!”

Rip the band aid right off. Lol

But spreads have lower margin requirements.

I first read this as “…margarine requirements.” LOL!

Another great article Wolf. You are covering issues that aren’t addressed in the regular media and I thank you for that. I doubt most reporters have the bandwidth or expertise to cover these complex issues. Your explanation of the spread between MBS and Treasuries makes perfect sense. (Yes, I read the GDFA) Do you think this also impacts ICE credit vhttps://fred.stlouisfed.org/series/BAMLH0A0HYM2 spreads?

Perhaps your readers would find your take on credit spreads (similar to MBS/Treas spreads) very compelling. I certainly would. TY

I talk about junk bond credit spreads quite a bit, most recently on April 21:

https://wolfstreet.com/2025/04/21/despite-turmoil-in-stocks-financial-conditions-financial-stress-and-junk-bond-spreads-still-in-la-la-land-or-barely-exiting/

Wait and See…Isn’t that what they did 4 years ago and let inflation run wild? Oh, it’s transitory they said, we don’t need to raise rates.

Opposite. Fed rates are now well above CPI, not far below CPI, and the wait-and-see is before CUTTING rates (though it could be before hiking rates further if inflation serves up a really bad deal).

There ain’t no “cutting rates” coming until AFTER more rate HIKES. The current admin is going to blow the biggest, mother of all mother everything asset price bubbles you’ve ever seen. All that money sloshing around is going to drive inflation into double digits, and soon.

Things are absolutely bananas out there right now. The money is sloshing everywhere, and durable goods prices (not just autos) are ramping massively again. BitCON and all cryptos are in lalaland, and those gamblers spend those gains like it’s free water. This shit show is just getting started.

I’ve been saying that Volker type FFR is in the cards. We are still in an inflationary expansion. It will take more than “wait and see” to fix this.

There have been seismic shifts in the money markets. MMMFs have exploded.

Powell eliminated the 6 withdrawal restrictions on savings accounts, aka, 1981 NOW accounts, destroying deposit classifications, which previously isolated money intended for spending, or means-of-payment money, from the money held as savings, or the demand for money (reciprocal of velocity).

“Standing Repo Facility, or SRF, operations will be made available in the morning as well as the afternoon in the “not-too-distant future.”

The Keynesian economists have achieved their objective, that there is no difference between money and liquid assets.

That’s not Keynesian. Without new technology to build assets, markets will struggle. Its why they have since the mid 2000’s. Monetarism is the word your looking for. Dollar globalism games.

Would have finance capitalism ever came into existence without the industrial Revolution??? My view…no.

April 7 and 8th, something broke, maybe basis trade melt down, but something broke on those trading days. Huge risks off in equities and we had yield exploding higher on the 10 UST, not too common. But the rare and scary thing on the 7th and 8th, when trillions of dollars worth of stocks and bonds are being sold the $USD dollar always gets a bid from the functional outcome; the trade is settled in $USD, the fact that the $USD sold off on big $ asset liquidation days was something non of us have seen in our lifetime, It definitely scared Bessent enough to talk some sense into his boss. Will it happen again? That’s the 100 trillion dollar question. Definitely a warning shot over the bow. Danger ‼️

The article TOLD YOU WHAT BROKE.

No disrespect, :) I was referring to the $usd price action as what broke on liquidation day, not bond yield on those days. Yes, I am here because I agree with you. Confirmation bias keeps me reading your every article. Thanks

I posted a long-term chart of the dollar above. Look at it. It didn’t break, LOL.

You make me laugh. Stocks drop 10% during normal times (no Fed put) several times a decade. 20% at least twice a decade and 50% on occasion. This isn’t even in the top 10 financial turmoil events of my lifetime.

Give it 2 years or 3 years. The multi decade secular bull market in $UST has changed to a secular bear market, when the $tnx gets above 5.4%,( I am buying at 5.2% for a trade) the hurt will set in. Smart people believe Yield control will happen before that, we will see how liquidity flows. Thanks 🙏

Bubble asset prices deflating is a good thing, not a bad or a danger. The problem is what has already happened and is here now, the creation and existence of the bubbles. Yield curve control would be another foolish attempt hide problems and would only lead to more of an inevitable reckoning down the road. People need to realize this supposed wealth is an illusion and can’t be propped up.

The S&P500 is only down 4% this year. This is a very minor correction.

Correct, technically the SP 500 is in bear market rally until it makes a new highs or it runs out of gas, reverses and makes new lows, if or when we make new lows this happens~The Kiss of Death is a sell signal in the S&P 500 that occurs when the index drops from an all-time high, falls below its monthly 21 exponential moving average (EMA), bounces back above the 21-EMA, and then drops below its recent low. I am guessing mid June to mid July we make new lows and get positive confirmation. I am in good company with that call Paul Tudor is waiting for new lows and Buffet is not sitting on 331B in cash because he is expects new highs. Yes SP is down 4% $sox is down 10.3% $trans are down 11.7% and only 50% of the SP 100 are trading above their 200DMA, the last fact is super bearish!!! ‼️

Japan and China, big holders of Treasuries, are not going to binge sell Treasuries. They would just be screwing themselves by driving prices down. They will have to find other ways to screw America, if that is what they want to do. I can’t think of any right now. I expect they will roll over on Trump’s tariff deals. They need us a lot more than we need them.

I wouldn’t be so sure about any of this.

China has plenty of leverage in these negotiations and it wouldn’t surprise me to see them use the economic turmoil to move into Taiwan.

The Treasury nuke is a last resort I’m sure but if the US says we’re gonna freeze all your assets I.E. Russia then why not sell treasuries. Even the threat of selling US debt or the US threatening to not pay it could send yields higher.

Mix in higher inflation expectations and lowering growth expectations and I’d say the hot seat will be in the oval office.

Why would Japan and China even want to “screw America”. Most people want their biggest customer to get even richer so they can buy even more of their stuff, especially the more profitable stuff. Japan and China love the trading relationship with the USA, and love a healthy USA.

The USA is not rich. We owe $107,600 per citizen. It is being and will continue to be paid for by all in many ways. Seems like most people haven’t noticed yet, though.

Were rich in dollars. Its what drives the game. We owe nothing until called. You don’t get the game.

thurd2,

The idea they need us more than we need them is a dated idea. The percentage of exports is 13% and of course slightly lower recently. That is not insignificant but they also have other markets to tap into. Sure, they want to be in the US market but have both the patience and stable leadership to not compromise. They won’t make emotional deals to win elections but ones in the best interests of their population. If the US decides to move from globalization/neoliberalism to economic isolationism then say goodbye to most manufacturing. When China, South Korea and Japan sit at the same table discussing trade that shouldn’t go unnoticed as not exactly bridge partners!

I think the worry for the Chinese is that

tariffs increase among all nations, not just the US. The EU will surely increase tariffs to protect key industries. So they may be inclined to make a few big short term concessions .

People forget about something called margin and profit at the micro level when talking about aggregate macro statistics.

That amount may “only” be 13% at the macro level, but at the micro level it may be the only things keeping a company is business and being able to pay their debt and interest.

Take away the US international export market and the company goes bankrupt.

Same with countries as well. You just can’t find new markets right away for many products if your main market disappears.

For example, right hand left handed cars….

“Patient and stable leadership”? China?

Xi is a dictator and will be gone in an instant if his credibility falters amongst the ruling kleptocracy. Their government is stable only on the surface. Under the sheen there is a titanic battle for power that none of us can see, people falling out of favor and vanishing, being sent to jail for “corruption”, etc. I wouldn’t call it “stable”.

“Patient” is true to some degree, but if the average working person is having a hard time finding employment, they will move heaven and earth and burn all their seed corn to buy a few months of fake prosperity. Not that our government is patient either, but there are at least some means to push back against an autocracy here, none in China except burning everything down.

I’m not concerned about Japan and China thinking of ways to “screw America”. The real danger is how many Americans consciously profit from America being “screwed” and spend their waking hours inventing new exotic positions to facilitate it.

I can’t see how Japan or China are cheating us by being willing to give us stuff in exchange for paper ?

“everyone loves low long-term interest rates”

They most assuredly DO NOT.

Borrowers sure do.

Everyone with money is moving to Mexico. That should tell everyone about low interest rates. Low interest rates are good for nobody.

Actually, they are not.

Movement of people with millionaire and billionaire status to certain countries is well known and Mexico is not on the list.

The US, UAE, Singapore, Australia, and Canada along with Switzerland are the top destinations.

Any insight into the ADR markets? I have been trying to find a source of both Sponsored and Unsponsored ADR market cap. Curious if this has been expanding recently .

Additionally, I have not seen recent estimates on cover-carry trade volumes. With the Euro supposedly joining the Renminbi & Yen as a funding currency, I am also interested in this impact with respect to current market conditions.

If I remember correctly we are out of the waiting period for enforcement of the HFCAA. Which if it is ever actual enforced, might have some interesting effects on the markets.

Interested to see where it goes as still have 50% of my portfolio in short term treasuries/money markets and 50% in equities in various indexes. If rate cuts do show up later this year and equities are sitting where they are at, short term rates look less and less attractive. I don’t buy/sell based on random WH tweets and decisions which seem to be the biggest movers of markets but don’t want to get locked into low rates. Given strong auction demand doesn’t feel like longer term rates will move up to where locking in that rate is worth the relatively low return. Obviously individual opportunities exist but I’m not that type of investor and given the unclear direction of tariffs feels like a bit of dice rolling in any event. I assume many people are in the wait and see more but perhaps I am missing something obvious?

In both 2000 and 2008, the Fed cut interest rates and equities still went down more before finding bottom.

To give my money to the US government for 10 years, I’d need at least an 8% return. The dollar will probably see average inflation over 4% per annum during that period (possibly over 6%), and US Congress has proven they won’t cut social programs despite the desperate need. If the US government balances the budget, then current rates are reasonable if you just need to park some cash. Given the excessive social programs and deficit spending, 8% should be a minimum.

Luke,

I always find your type of comment

fascinating unless of course you are not a US citizen. Don’t you see buying US treasuries as supporting the choices of your democratically elected leaders trying to do good for the long term outcome of it citizens?

No, me neither. I view the US as a place as a place where I was born and currently choose to live and work and the government as one of my investment options! Just interesting how people see their elected government from my perspective.

What other investment are you making that will double your money in 10 years instead then?

MW: How an obscure bet on bonds almost crashed the $29 trillion Treasury market

Yes, I described that “bet” in the article but without this ridiculous clickbait title. It didn’t “almost crash” the Treasury market. It caused the 10-year yield to rise maybe an additional 20 basis points to where it had been a little while earlier. No biggie.

6.76% mortgage rate quoted by FreddieMac is for folks with a plus 800 fico score (only 20% of folks are over an 800 fico).

Looking at Bankrate and similar, folks with a fico in the 750 range can expect to see a mortgage rate in the 7.25% – 7.50% range for a 30-yr fixed.

Risk is being repriced around the world. I expect this spread to worsen. The Fed also knows full well that interest rates are going up, they have no credibility, and would only have less (if that’s even possible) if they cut rates now.

The Lowest Comfortable Level of Reserves (“LCLoR”) is a joke.

Dr. Daniel L. Thornton, May 12, 2022:

“However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1.”

https://fred.stlouisfed.org/series/TOTBKCR

Commercial bank credit, where loans/investments equal deposits

The banks, REITs, and hedge funds that we place commercial real estate loans with are all becoming more cautious. With few exceptions, the banks are tightening up their underwriting criteria. Assuming the trend continues, this will reduce liquidity and it will eventually lead to more defaults and lower prices. CRE is already in a world of hurt due to retail and office market meltdowns. Best guess, the next CRE asset classes to take gas will big box logistics and IA buildings.

New Trump Budget Bill allows for an increase of $4T to the debt ceiling.

Party on Garth!

2 and 3 month bill yields are rising past the 1 month now.

Up up and away with interest rates the gov is adding and extra 600 billon maybe more in interest payments than 3 years ago into the system fueling inflation and that will only go up. This will get interesting.