Active Listings compared to April 2019: Jacksonville +23%, North Port-Sarasota +29%, Tampa +31%, Orlando +40%, Cape Coral-Fort Myers +42%, Lakeland-Winter Haven +71%.

By Wolf Richter for WOLF STREET.

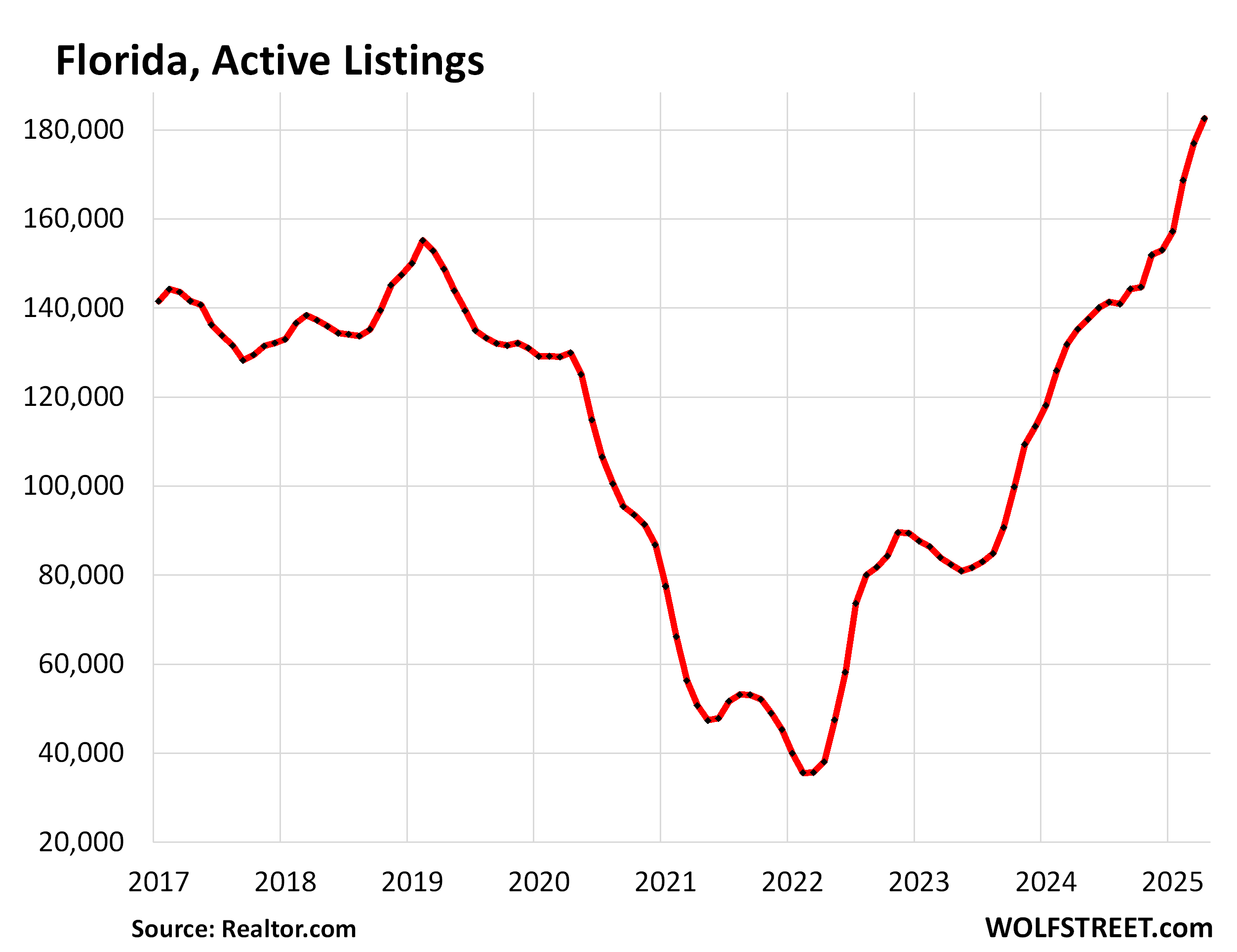

Unsold inventory of existing homes for sale is piling up in Florida at a stunning rate. Active listings jumped by 35% year-over-year in April, to 182,589 homes, by far the highest in the data from realtor.com going back to 2016, and was 23% higher than in April 2019. There’s a housing shortage until there suddenly isn’t.

The month-to-month surges in February, March, and April were particularly spectacular. It seems sellers have lost patience with “this too shall pass,” in terms of the 6%-plus mortgage rates, and have started to put their homes on the market in larger numbers, and leave them on the market when they don’t sell, instead of pulling them off the market within a short time. But buyers are on strike.

So inventory has been piling up because sales plunged. Lots of supply, little demand. Why? Because prices are far too high after the price explosion since 2020, and those too-high prices have triggered demand destruction, one of the most fundamental economic dynamics.

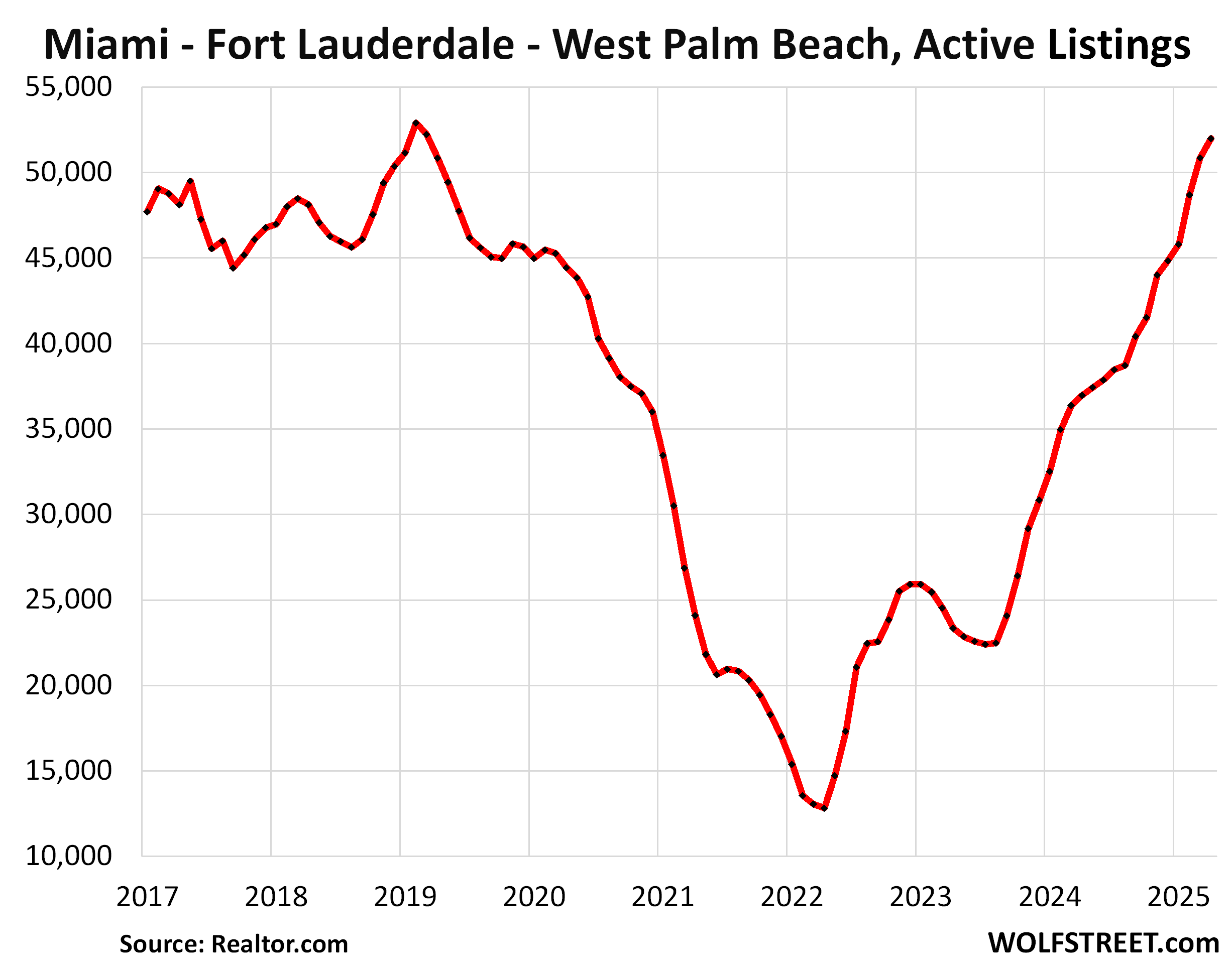

Miami-Fort Lauderdale-West Palm Beach metro: Active listings jumped by 41% year-over-year in April, to 51,987 homes, the third-highest in the data, behind only February and March 2019. Compared to April 2019, inventory was 2% higher.

The Miami metro is still a little behind the other big Florida metros, in terms of the inventory pile-up, but it’s coming right along now:

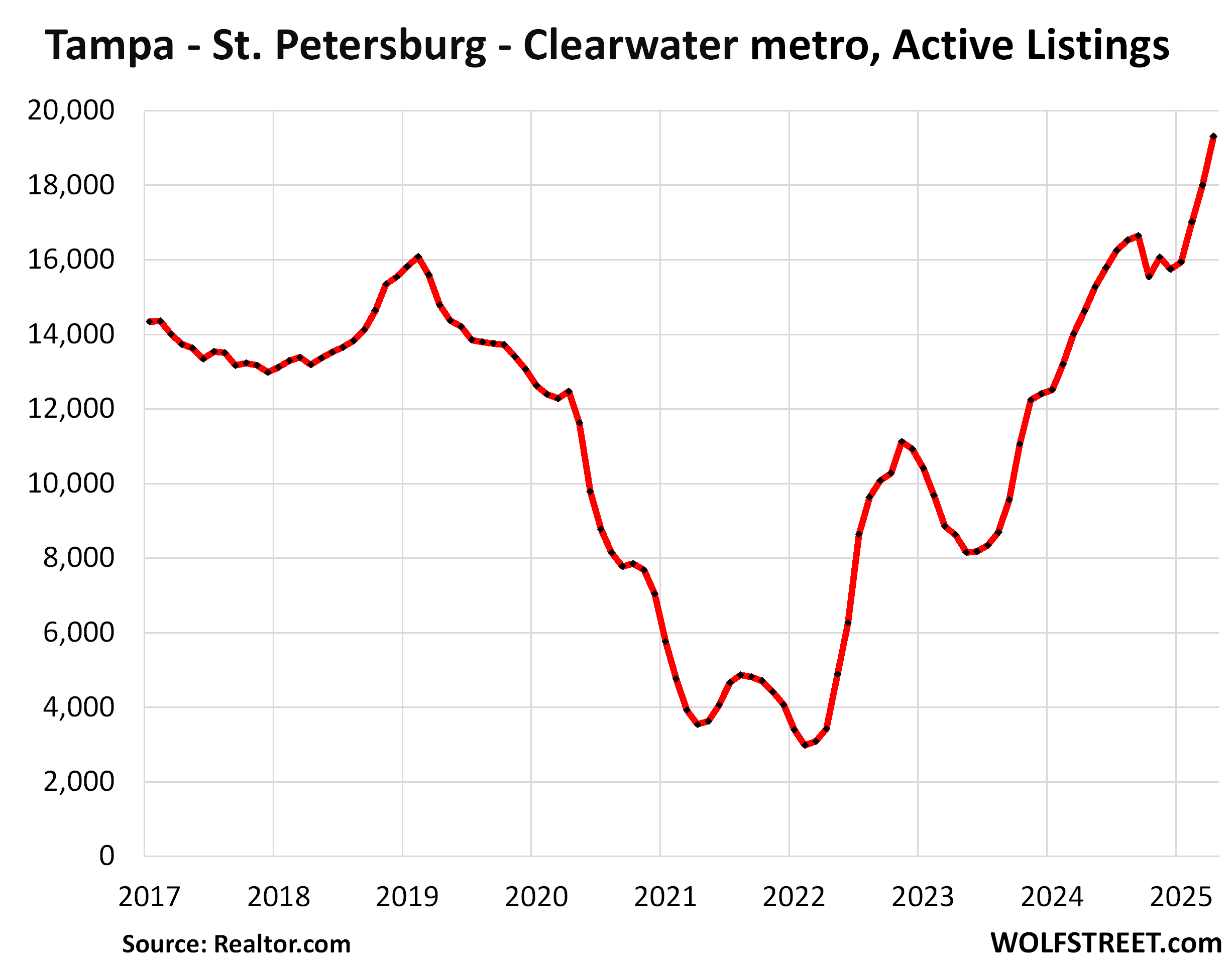

Tampa-St. Petersburg-Clearwater metro: Unsold inventory jumped by 32% year-over-year in April, after three majestic month-to-month jumps in a row totaling 21%, to 19,310 homes, the highest in the data from realtor.com going back to 2016. Unsold inventory was 31% higher than in April 2019.

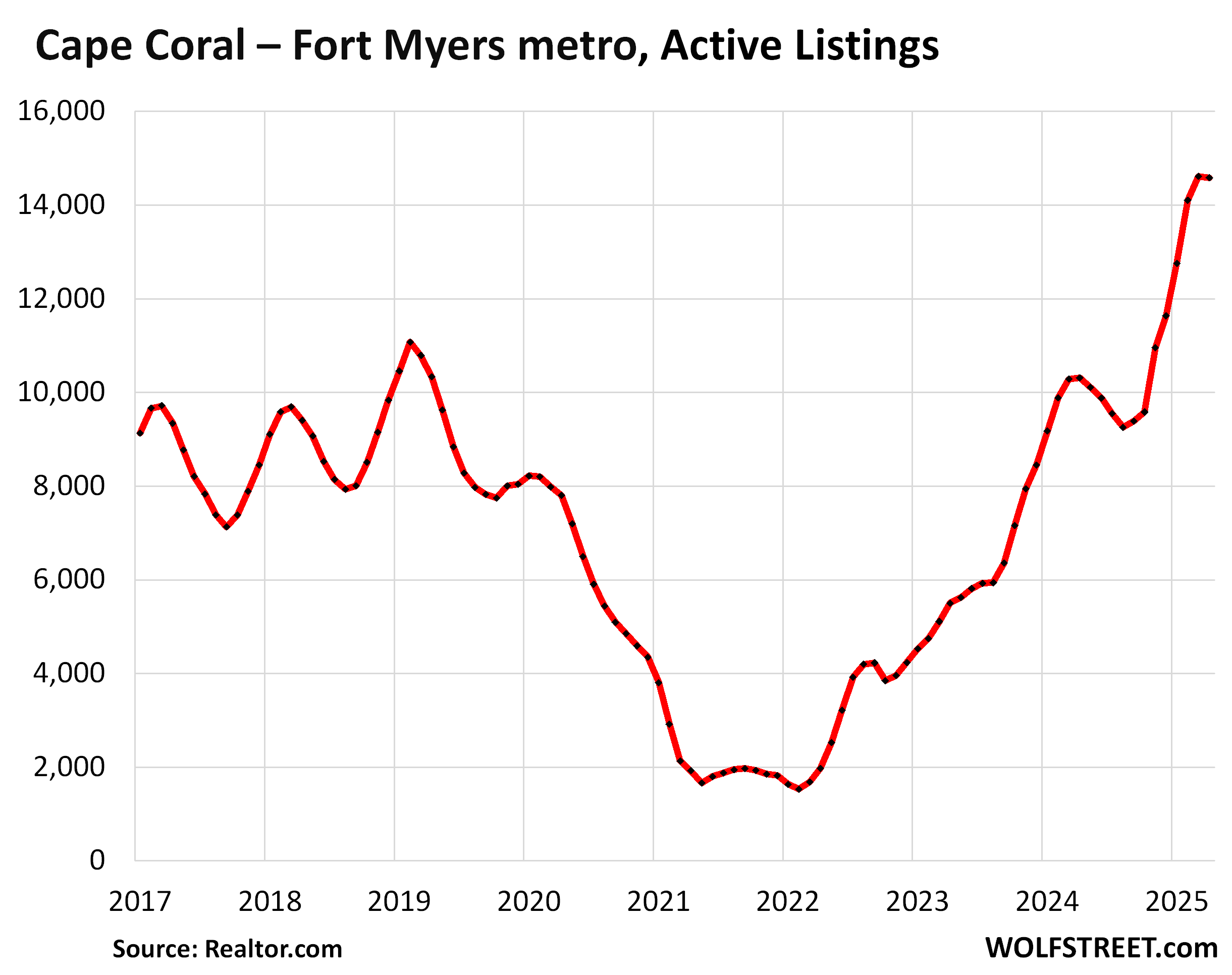

Cape Coral-Fort Myers metro: Active listings spiked by 41% year-over-year in April, to 14,580 homes, along with March the highest in the data from realtor.com going back to 2016, and 42% higher than in April 2019.

There is some pre-covid seasonality in the metro where March marked the high point, and then inventory fell in April and continued falling till about September. But this year, instead of falling in April, inventory was essentially unchanged. The same occurred during the inventory surge a year ago.

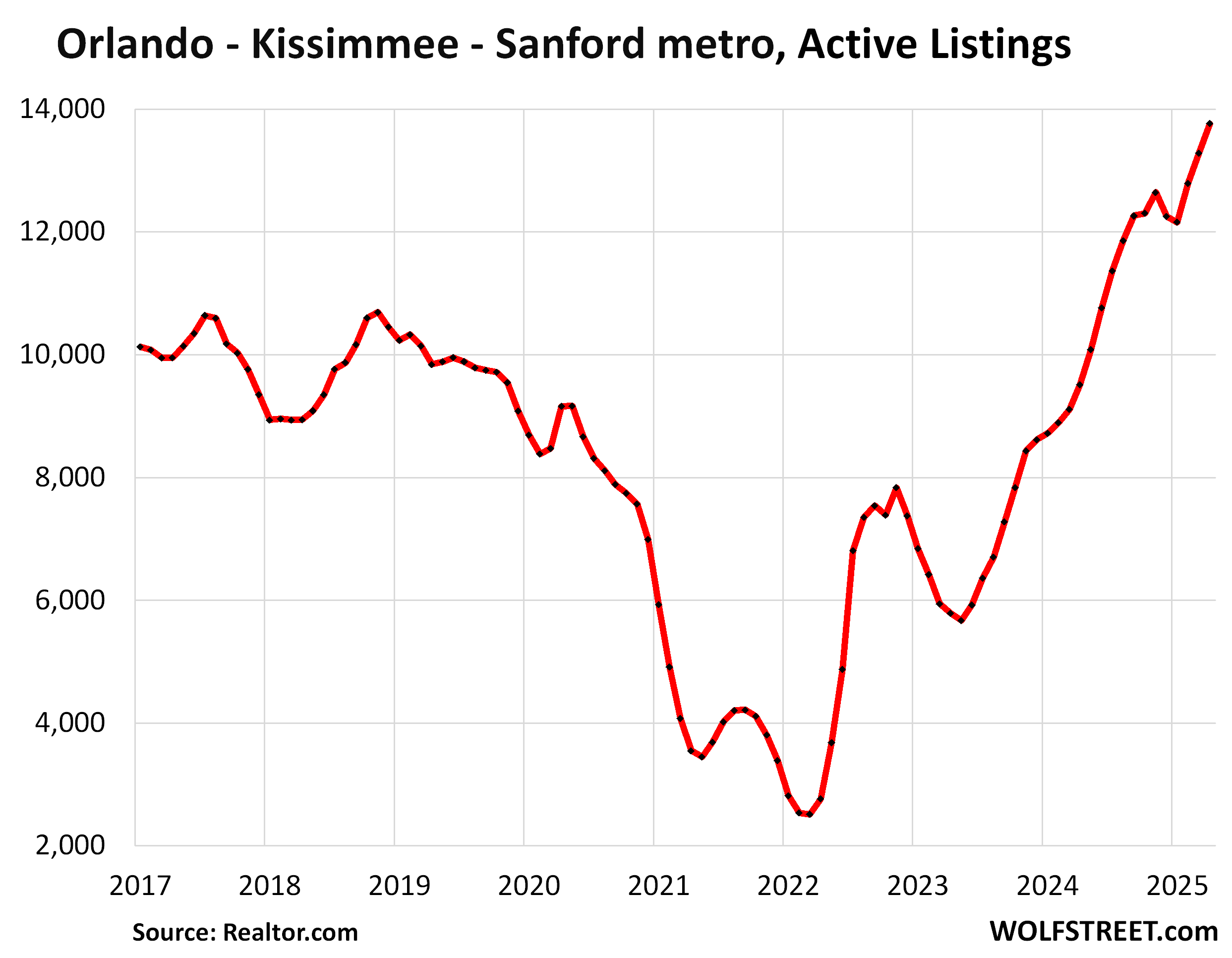

Orlando-Kissimmee-Sanford metro: Active listings spiked by 45% year-over-year in April, to 13,765 homes, by far the highest in the data from realtor.com going back to 2016, and up 40% from April 2019:

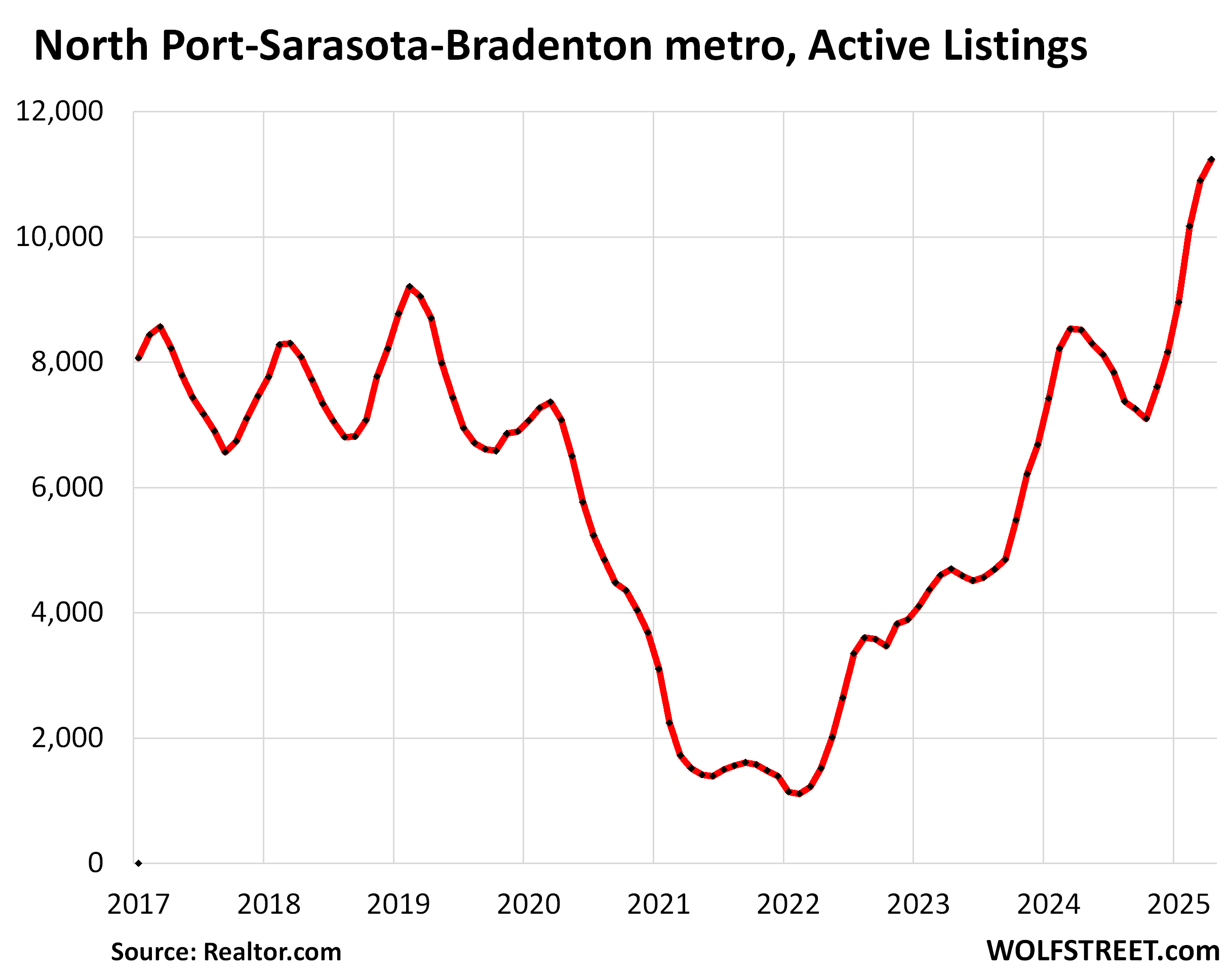

North Port-Sarasota-Bradenton metro: Active listings spiked by 32% year-over-year in April, after six majestic month-to-month jumps in a row totaling 58%, to 11,234 homes, the highest in the data from realtor.com going back to 2016, and up 29% from April 2019.

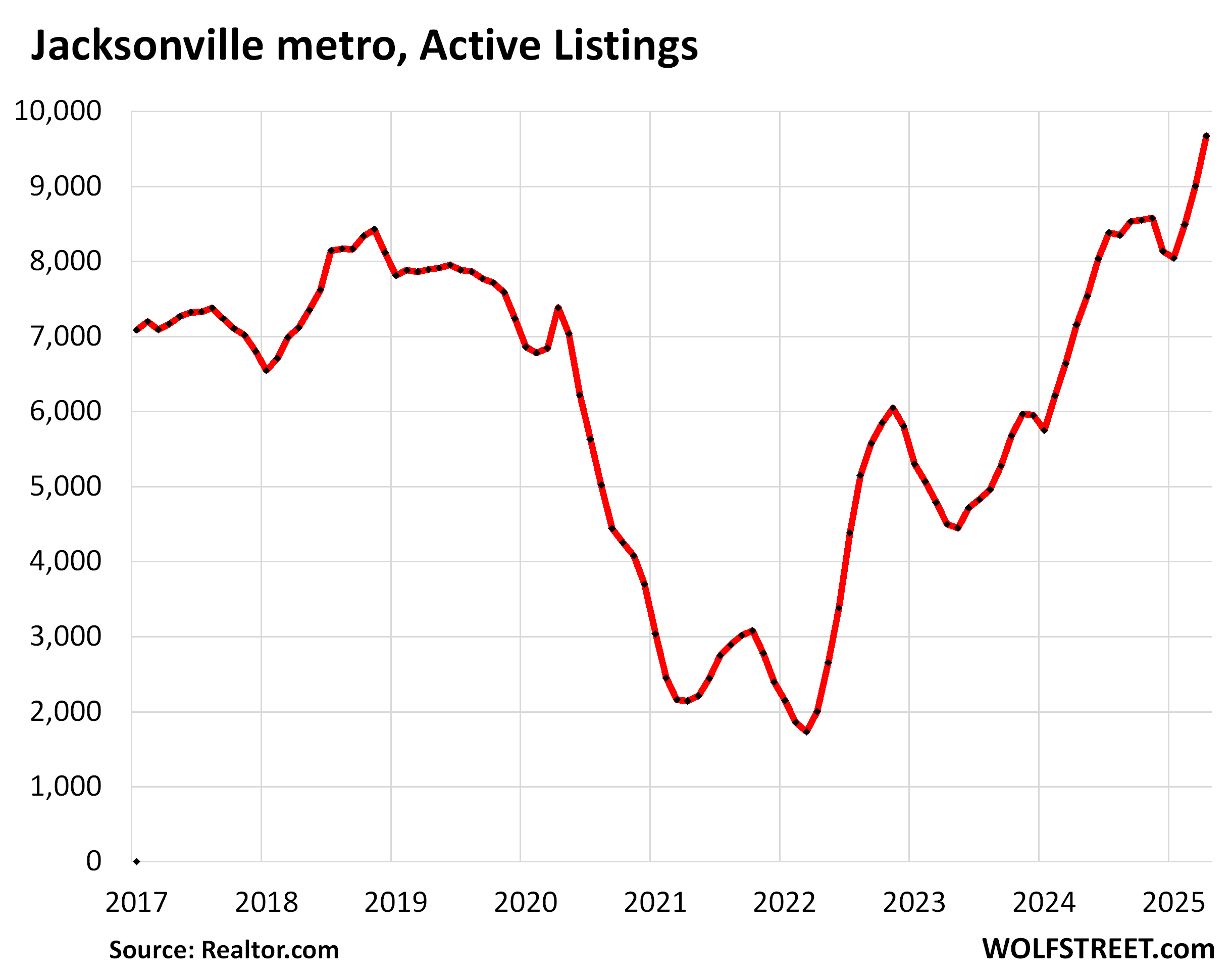

Jacksonville metro: Active listings spiked by 35% year-over-year in April, after three majestic month-to-month jumps in a row, similar what we’ve seen in the other metros, totaling 20%, to 9,676 homes, the highest in the data from realtor.com going back to 2016, and up 23% from April 2019.

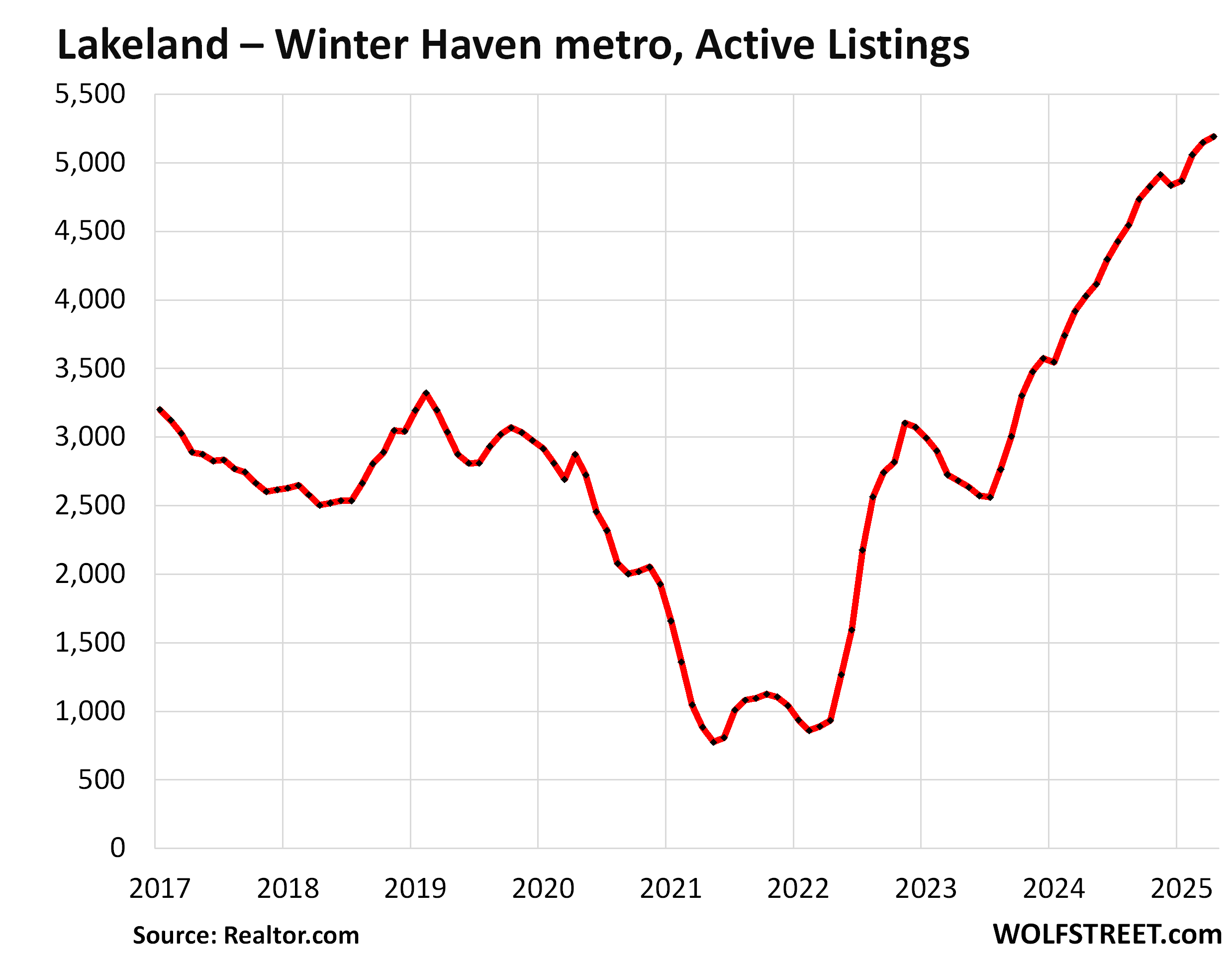

Lakeland-Winter Haven metro: Unsold inventory jumped by 29% year-over-year in April, to 5,191 homes, by very far the highest in the data from realtor.com going back to 2016. It was 71% higher than in April 2019, and 107% higher than in April 2018. Showing signs of a glut:

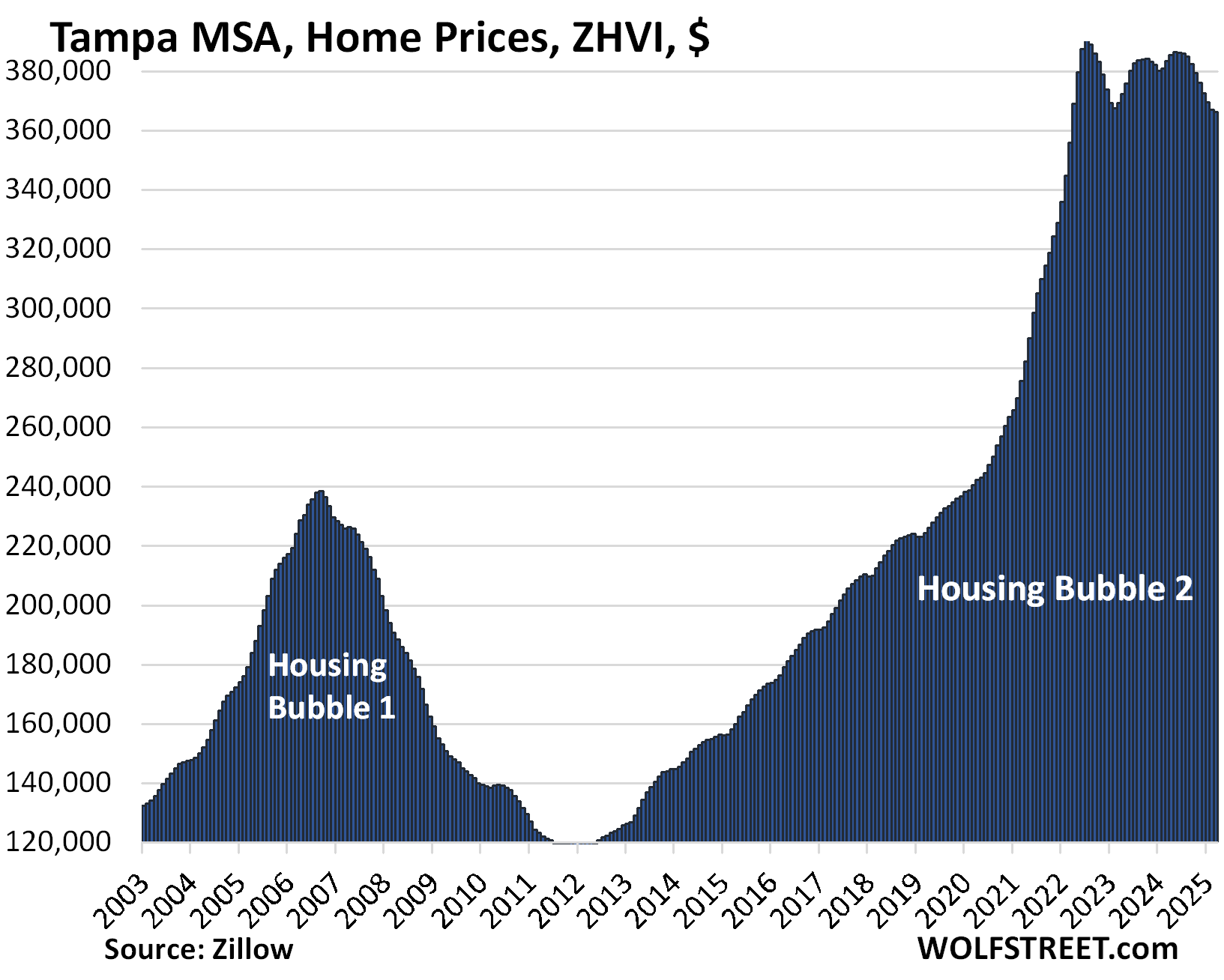

Prices have shot up way too far: For example, the prices of mid-tier homes in the Tampa metro spiked by 60% from 2020 to the peak in mid-2022. That’s what triggered demand destruction, one of the most fundamental economic dynamics:

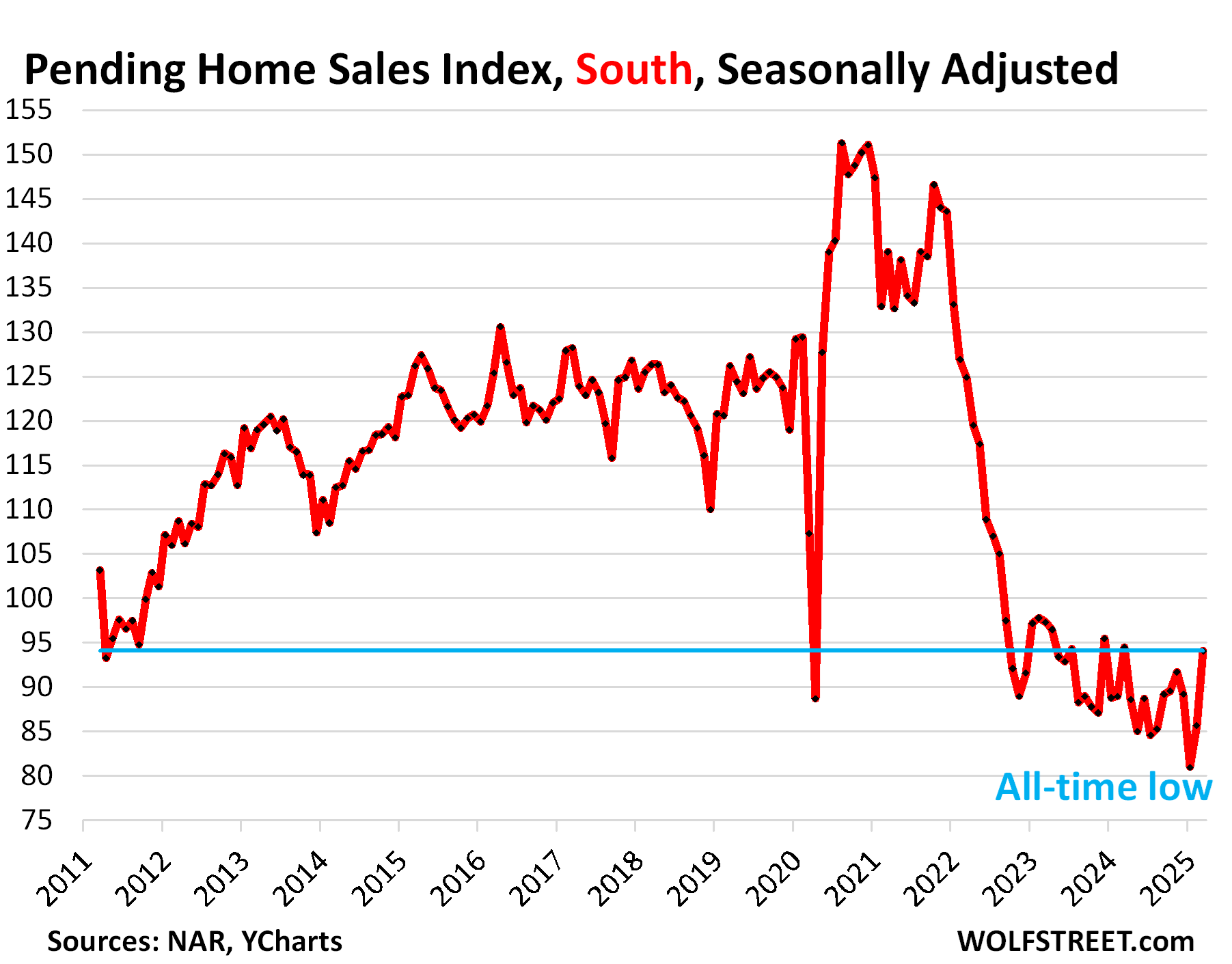

Demand destruction: In the South, pending sales of existing homes were again down year-over-year in March, and marked the worst March in the data from the National Association of Realtors going back to 2011, though they rose from February, seasonally adjusted. Compared to March 2019, pending sales were down 25%.

And that’s the problem: At these way-too-high prices, result of the massive price-spike since 2020, demand destruction has set in, which is why inventory is piling up. But there is a classic cure for any demand destruction – there always is: substantially lower prices.

Home prices have started to move lower in many metros, including in Florida: The Most Splendid Housing Bubbles in America, March 2025: The Price Drops & Gains in 33 of the Largest Housing Markets

Condos are making particularly sharp moves: In 15 Bigger Cities, Condo Prices Already -10% to -22%, 5 Are in Florida with Accelerating Drops. Absurdity Comes Unglued

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interestingly, today’s bubble peak, inflation adjusted, is about the same as the 2007-8 bubble peak. If history follows, we may be looking at some bargains in the near future.

Let’s hope so. At a minimum, let’s hope high mortgage rates stay around for at least 2-3 more years. That may be just enough time to get a very broad 20% or so decline existing home prices.

To want mortgage rates to stay high for 2-3 more years means you don’t give a flying fck about the millions of people who have not bought a home before and are desperately trying to escape rent slavery. Flat out un-American in my view. You want people to spend more money just for the essentials in life. This world doesn’t revolve around you and your own self-centered ideals. Think about the whole, not just yourself.

AverageCommenter

Mortgage rates are fine. Prices are too high. What you people have to do is get on a buyers strike and stay on it for years and let boomers sell their homes to the angels in the sky. Prices will come down, they’re already coming down in lots of markets, and your income will rise, and it’ll work out eventually with normal mortgage rates, such as now. But as long as you’re feverishly trying to buy, you’re just driving up prices and letting boomers lock in their profits. And the buyers strike is already in full swing, as you can see from the sales volume, which has collapsed.

Talk about a myopic view of things..as Wolf already point out interest rates isn’t the problem, the high price is the culprit. If you need more proof, check out in the 80s when interest rates was double digits and what home price was like even when accounted for inflation compare to current prices, you can see the glaring issue right there..

Of course, people already have a stake in the market or trying to push a narrative will only harp on interest rates and completely ignoring the ridiculous price relative to what you get . Yeah I am not buying a freaking Corolla for $100k even if I can finance it for 0% for 10 years because no sane person would think a normal Corolla is worth $100K, apparently this logic cannot be apply to housing for some reason because everyone and their mom is convinced my house will double in price in 10 yrs so better get in at all cost now..

High mortgage rates? Try 18%! I had a mortgage with that rate and I was darned happy to have it. So much whining!

On Old Highway 98 in Miramar Beach there is a stretch of beautiful three story beach homes built in the early 2000’s for a couple of million $ each. In 2008-2009 almost every one was for sale…for 600-700k. Recently they were back up to $3+ million. Since the first Florida real estate boom of the 1920’s it has proven to be an extremely volatile market.

If price discovery in housing, an illiquid asset, were ever allowed to happen, it would crash below the 2012 bottom, nominally. But instead, it’s rigged by the government.

For context, how does inventory of 182K listings compare to the depths of the financial crisis?

Miami is still a good long-term bet for housing. The booming Sun Belt won’t die down in population for decades to come, and everyone needs a place to live.

Doesn’t Miami have a serious problem with sea level rise? I’m thinking here mostly of the consequences for its water table and public works (water and sewer) rather than outright inundation on its perimeter).

Correct. Described by Jeff Goodell in his book “The Water Will Come”.

Wonder if most of the RE agents are having any honest conversation with their sellers like lower your price to move those supply and stop hanging onto 2022-23 prices or they are still selling BS narrative like oh rate is going to get cut soon and floods of demand will pile up again or telling them one of area is still having bidding wars..etc.

Anecdotally, been seeing way more email blasts on houses for sale from Redfin in SoCal compare to last 6 months, now daily I get about 4-5 a day on areas I searched before, probably doesn’t mean anything. It’s still funny to see some gem from these ads though, hopium is still around and once in a while you’ll still see sold with price increase and the original price wasn’t cheap to begin with..like the gem below.

$690,000

2 Beds · 2 Baths · 862 Sq. Ft.

Laguna Niguel, CA

Phoenix Ikki, that’s not a bad price for a property in Laguna Niguel. I wonder if it is a tear-down, right next to the freeway, or maybe the seller is low-balling the price.

Hmm, did you see the sq footage? The place is a shoebox size condo with a large HOA monthly. Location matters but not at these kind of pricing and without an ocean view

Phoenix, 862 sq ft is the size of a decent two bdrm apartment. Not a shoebox. The cheap price is because it is a condo with HOA bs.

@thurd2 yeah no, 862 sqft condo is small, especially for that price . The value proposition simply isn’t there….unless you’re talking about a place in Hong Kong, then perhaps 862 sq ft is consider decent. Also this place isn’t anywhere near the beach nor is it a stylish cottage but to each its own…the craziness of people still buying in SoCal is not over so I am sure someone will buy it and try to make it work or rent it out.

If they are renting it out, I doubt they can get the a good cap rate out of it under current interest rates, plus HOA, insurance..etc.

I thought the same thing. Not Laguna Beach but not far off either. Those size houses if habitable rent for lots of money. My friend rented a 2 bedroom 1 bath small house for a bit with no view years ago and 4K a year, not counting some of the most expensive electricity rates that exist. The owners gave it good price since they owned for generations, but that changed as family members wanted a cut via inheritance.

Thurd:

862 square feet is not a good sized condo.

That is stinky, small sized living space.

For one person it might be barely ok. For two people, no way.

This is exactly what I have been telling sellers. Drastically reduce the price or it will sit and rot on the market. Most sellers just don’t want to have that Come to Jesus moment unfortunately.

John in Florida many homeowners took on heloc’s, and can’t sell for a profit anymore, and therefore are unwilling to sell having to bring money to the table at closing. Gotta keep up with the joneses you know at all cost.

People are still in la la land here. I see it everywhere here in tampa. At least the few left here that still speak english as a primary language. I believe we are in the early stages of a huge decline in prices with so many houses going back to the lenders because of all the under water heloc’s and hurricane damaged homes that were not insured. And its gonna be like deja’ vu all over again. What I can’t figure out is who pays off all those delinquent mbs monthly coupons that pensioners need for their fixed incomes throughout the world because as we all know these days banks are nothing more than loan originator conduits that jobbed off these loans to wallstreet for that quick buck.. Perhaps this is a question for the wolfman.

The other issue with a “too high” price is that most buyers will not even bother with an offer.

A quick case in point of a listing I just viewed – built in 1986 is good shape (from the pix) but a very ordinary house. Sold in May 2014 for $380k. Sold in July 2021 for $920k. Listed in Oct 2024 for $999k; relisted in May 2025 for $989k. Seller is trying to “get out whole” – cover their selling expenses and getting what they paid. Problem is that they WAY overpaid in July 2021 (probably looking at the monthly at 3% which on a 800k mortgage was about $3,400/month. At current rate of 7% $3,400 will cover a $500k mortgage.

So realistically, the fair number on the house is probably somewhere around $600-650k. But the seller can’t take that loss. And a serious buyer isn’t going to bother with an offer that’s 30 to 40% less than asking.

Price dreamers who bought prior to 2017-8 will not get what they want but can sell. But individuals who overpaid due to the low mortgage rates, especially between 2020 and 2023, are in for a world of pain. The latter just needs to love the house, because they’re not going to be selling for what they want anytime soon.

Funny, the price between 2014 to what the seller is trying to unload for sure do remain me of MO of Ponzi or Crypto rugpull .. Get out and find the next bag holder..

Another one I saw listed in SoCal, buyer bought couple of months ago for one million, now trying to list at 1.25m. Yup, couple of months used and all of a sudden it’s worth 25% more.. You can’t make this crap up.. The level of greed would make Gordon Gekko blush..

Excellent piece, Wolf. The national implications are definitely something to watch. Your work, as always, delivers just the facts – a true Dragnet for our times.

Wolfman, there is no mention of the Florida panhandle :-(

I’m not surprised Florida will be the first to drop in price due to the housing bubble, as its always been more of a speculative state for real estate and a lot more pro-real estate developer than California and other states.

The Panama City Beach area is still growing because of tourism (within a 14 hour drive of Chicago and 5 hours of Atlanta) and other industries like Eastern Shipyard, Kraton Chemical Plant, SeaPort of Panama City, Berg Pipe, Miller Marine custom boats construction, Trane HVAC manufacturing, the new teaching hospital and medical research facility run by Florida State University, as well as the Coast Guard base, the Naval Station Panama City and Tyndall Air Force Base.

Also Panama City Beach is becoming popular for off season or non beach weather (December 1-February 28) tourism with different types of major events and conventions.

1. “there is no mention of the Florida panhandle”

The metros here are the largest metros in Florida. They’re just not in the Panhandle.

2. The Panama City Beach area is still growing because of tourism …

what’s growing is inventory, LOL. In the Panama City-Panama Beach metro, inventory is double of where it was in April 2019. It’s among the worst in Florida:

As you say Wolf, prices have to be come down to clear inventories, but the part I don’t understand is, with such high inventories in Florida, what is keeping prices so high, as if they defy economic gravity.

Prices ARE coming down, they’re just very sticky, nothing moves fast in RE. I included the Tampa price chart in the article. Have a look.

There is an entire government system designed to maintain and boost real estate prices. Fannie, Freddie, Ginnie, targeted tax breaks, FHA, VA, USDA, and a myriad programs at the state and local levels designed to inject money into the real estate market, and remove risk from lenders. Add to that, the Federal Reserve system, designed to protect the financial system in the case of widespread poor judgment, has shown it can and will suppress interest rates and sequester vast amounts of mortgage debt on its books, further boosting the real estate market.

It seems to me that system has been a resounding success for what it was meant to do – remove risk from mortgage lenders and keep money flowing into mortgage loans regardless of price (see conforming loan), which boosts real estate prices. Inflation expectations in the housing market are “entrenched”, about as entrenched as can possibly be. Additionally people see that the wealthy often have multiple properties (and this includes legislators and financial system members), and they will not take actions that harm themselves.

tl;dr: people have been conditioned to believe home prices only go up; and that the government will intervene in the case of widespread real estate price declines. There is a great deal of government money available to buy houses at all price points (conforming loans) and all that support puts brakes on price declines and shapes people’s future expectations.

Good of you to add reference to what some of us old and older folx born and raise in the flower state usually label as LA, which is this case means “Lower Alabama” rather than SoCal.

Other name, of many, some not family friendly, for the area is ”Red Neck Riviera”…

In any case or name, it really is a beautiful area with the best season far into warmer months than ”Florida” and IF I had my wish, we would absolutely have a home about 50+ miles from the coast up there for our summer home,,,

Unlikely due to my better half being born and raised in the Saintly Part of the TPA bay area, with tons of family local.

Wolf, do you have any data on Ormond Beach?

All these markets in Florida look kind of the same, some a little ahead, others a little behind:

A D, do you work for the Panama City Chamber of Commerce?

Typo. It’s AI not AD.

It’s “just a 14-hour drive from Chicago” said no family with three kids ever.

Ya really have to learn how to drive with kids HD:

leave in the afternoon, with some thing, games or whatever to amuse the kids,,, then drive through the night.

Next day, if driving across USA, go to motel at earliest check in time!

Sleep while kids are in pool, etc., then have a really great meal and drive all night, then repeat…

My kids loved it, and slept all night in the ”camper shell” while I drove, alone most of the time, but sometimes with a partner who drove while I napped,,,

(BTW, have driven all the way across USA many dozens of times,,, sometimes just because of the really incredible beauty of our country, which is still there.)

Bingo! Exactly what we did with our four children. We would put the seats down and make a big bed for them to stretch out on and drive until the wee hours when we would stop at a motel. We even backpacked with the four of them, carrying the baby and a toddler on our backs along with our camping gear.

If the Fed cuts mortgage rates increase.

Jay’s favorite past time is painting himself into corners.

Powell is doing the best he can (not a compliment). But he is probably doing a “good enough” job since almost everybody hates him now. Of course almost everybody will love him when he caves to Wall Street and Wall Street’s political puppets and lowers rates, like last year when he cut 50 basis points based on employment data that turned out to be wrong.

The 12 member FOMC makes any and all interest rate policy decisions at the Federal Reserve, not Jerome Powell personally.

Who is placing these properties on the market? What percentage are those middle income earners that where convinced by ads to have a holiday home in the sun, just like the mega-rich? Then finding out about all the hassle of maintaining at far away place and now even more expensive to do so. Or is it old men not being able to find a member of an all girl swing band?

Howdy Youngins. JFYI. A 6 – 7 % percent Mortgage rate is really kinda normal. A Bubba Believe it or not.

Right Bubba! In the 7 houses I have owned since 1980 I have never had a mortgage rate that low. Lowest was 8%.

With you, like totally dude!!

That was also for me the lowest! Hi est was 18%, for my first owned House, as opposed to land…

Price of that house was $40K, and after serious upgrades, we sold it for $105, with $16K invested including labor and materials,,, that house sold recently for $800K.

Cannot blame young folx wondering how to proceed.

Cannot suggest anyone buy any RE, seems clear enough that the continuing degradation of USD will continue to make ALL assets equally degraded.

But, in reality, ”who knows” is most likely, as always…

We are living parallel lives! I fondly remember my 18% mortgage!

I remember my 18% mortgage in California in 1981 also!

What is a ‘normal’ interest rate? The most common? If so 2.5-5% is clearly the most common of the last 30 years. If you want to go back further it’s still probably the most common. Interest rates have been dropping for the last 50 years. There is no ‘normal’ interest rate. Given the global increase in lending liqudity and general decrease in risk now compared to decades past, there really is no reason to expect those rates would make sense today. Is it your belief there is just a platonic, normal rate and all others are ‘wrong’? In 1000 years we’d still be at the same rate regardless of economic conditions? I’m gonna go with believe it not.

https://wolfstreet.com/2025/04/18/spread-between-10-year-treasury-yield-mortgage-rates-is-historically-wide-and-widened-further-some-thoughts/

Just in case you want to check if anything you wrote is true.

Average mortgage rate over the last 30y is 5.5%, median is 5.8%.

The 40y average is 6.5%.

https://fred.stlouisfed.org/series/MORTGAGE30US#

The only way it’s going back to ~3% is another major economic crisis.

There’s a concept called r*, which represents the “neutral” rate of interest, neither stimulative or restrictive. There is active debate about what really is. I have no idea what it would be.

Note that despite the massive increase in inventory, seasonally-adjusted prices have barely budged. Many, many homes in Florida are siting unsold for 90-180 days. If you look at the stats you’ll see that new listings in most metros in the state are being priced at a higher median sales price than ever before (both sales price and per square foot). Basically, sellers continue to be completely delusional with respect to price and this is the primary cause of the massive buildup in inventory… as one can see that more aggressively-priced properties seem to sell briskly.

While you do see a lot of sellers reducing prices, it’s by small amounts which aren’t making much of a difference. You also see quite a few sellers re-listing their properties with a different agent, as if that’s somehow going to sell the house without substantially changing the sales price also. What that does do is though is reset the property ID in the MLS which then resets the property’s unsold days on market so the actual days on market is actually quite a bit worse than the stats imply.

Annually, sales peak around June 1. I pity the fools who do not sell by then. They could easily tag on another 180 days on market since after that date demands naturally falls substantially due to seasonal factors.

I predicted this inventory situation was going to happen in another comment on this site early this year and so far things are working out about as I expected. It is definitely going to be a very interesting time this summer in the real estate market in the South and Florida in particular!

Love your handle and hopefully it’s in reference to that Simpson episode…

Speaking of The Simpsons, feels like the last couple of years a lot of people Homer Simpsons their way into this housing market…

I knew a number of Canadians that went to Florida to buy a winter home back in the 2010-12 time frame, and bought two because they were so cheap. They can definitely afford to sell 30% down from the peak, those post covid buyers will definitely feel the pain

On the Florida resale housing, did I miss your comment on the effects of insurance costs contributing to more houses on the market.

A good barometer for “core” causes of “buyers on strike” is watching the large new home builders. They have the wherewithal (and are not emotional about it) to push sales. What are they doing in these same markets? Price discounts? Probably not so much (can’t really look at the price as they can reduce that by building smaller and/or removing features). They buy down rates to make the payments lower. They have been successful with this; but now – not as much. What’s changed? Insurance costs (and perhaps people’s understanding that the insurance companies aren’t making them whole after a hurricane) – this is maybe a combination of monthly payment cost but also fear/uncertainty – emotions that say “wait”. And one other factor in FL – the resale condo association fees (again uncertainty for new buyers but also a contributor in seeing more listings of resales).

I think the new normal in home buying in many markets is much higher home insurance costs and the uncertainty that the insurance companies are going to make the homeowner whole (not to mention the effects of FEMA cost cutting).

Just watch what the giant builders do in these markets to see what solutions evolve

This one reason for the huge increase in condos for sale in Waikiki – increase in insurance costs raising the carrying costs of the real estate.

Another is the continuous erosion of property rights by the government there.

Last month the government there again passed a law restricting the ability of people to rent out their property for less than 90 days.

There used to be a large inventory of condos that could be rented for less than 30 days. That had been gradually reduced by regulation, taxation and fees, and sales of those units. The then short term limit was moved to 30 days with more taxes and fees.

The new law will greatly restrict the number of vacation condos for rent. The idea is to force people into hotels which can get higher room rates because of scarcity. (There are numerous reports of connections between people in government and the hotel industry)

I don’t know how many people can afford to take a vacation in Waikiki for three months.

Of course, the new law will again be challenged in court and people will have to wait to see if the law gets an injunction like last time, but that doesn’t help people that need income from rental procedes in the mean time.

Florida needs to be experienced in July – September for the full effect.

😂😬😂😬😂😬

In addition to high prices, a FL buyer also has two wild card factors that make settling on a sales price anything more than speculation: insurance and HOA. With HOA and/or insurance fees exploding, how does one calculate the property value?

In the short 3 mile drive to my inlaws from my house here in Tampa, there are now 4 new for rent signs and half a dozen for sale.

For years after the pandemic there were zero. It is finally exploding visually roadside.

Same here in my small ‘hood in the Saintly part of the TPA bay area that the boss and I walk daily:

After the ‘canes last fall, nothing at all for sale or rent, including two under construction sold the day they were listed; now OTOH, two new for sale at $1.6 and 1.3 MM, and half a dozen others for sale or for rent and none of them moving 30+ days after listed…

Others sitting empty, which is not unusual for this time of year when many of our seasonal residents have already gone north to avoid the wicked heat…

As someone commented above, ya really gotta experience FL in the summer BEFORE moving here, and keep in mind summer sometimes starts in January,,, LOL

Have to assume insurance in many areas significant. I pay about $2,000 a year for homeowners ($1,200 for HO) and about $800 for optional flood insurance (mandatory if had mortgage). I think some people don’t calculate the full cost of living somewhere, where even electricity rates can vary significantly town to town. I drive twenty minutes north or south and electricity is double(SMUD versus PG&E).

The next hurricane that hits Florida and causes serious property damage and insurance losses will mark the end of the real estate boom. People won’t be just lowering their prices to get rid of their properties. They will be walking away from them in droves.

“Prices ARE coming down, they’re just very sticky, nothing moves fast in RE.” -Wolf.

Stickiness is an interesting concept in economics. In the past (before 1850) nominal wages of laborers were sticky. We see nowadays that home prices are sticky. I’d like to see a decent book or article that explores “stickiness”. I wonder if there is a way to exploit stickiness, as it seems like an economic inefficiency.

Can anybody suggest a way to short the price of single family units, especially by state, e.g., Florida, California, Texas? By city would be better but that is asking too much.

Inventory flooding Las Vegas Valley’s home market with no buyers in sight: Zillow

Article from LVRJ 5-1-2025

So with unemployment at 4.2% do people have to sell is the question?

I wonder if a lot of stickiness has to do with people being able to pull their property off the market instead of cut price by 20%.

Seeing a similar trend here in the Denver suburbs. Inventory is up. No one is buying. Rent prices are falling. Tourism is down. Population growth is non existent. But single family homes are still being listed at delusional all time high prices.

I remembered Big Shorts movie where Steve is going in Realtor’s with his co-workers. Realtor saying Market is facing itsy bitsy gully right now. Then goes on how crazy market was and this Seller is motivated. That Seller is motivated. Steve Carrel says oh wow lot of motivated Sellers. Oh thats just golly thats all.

For me that movie and scene stuck in mind. May be it always start with Florida. Sure there were 20% down-payment loans and all. But Prices went crazy in 2020 boom. Life happens for the Owners too as it happens to Renters. But Renters can just move or downgrade. So how long Owners can hold only time will tell.

Now Govt owns all those Fannie Mae & Freddie Mac and what not. Will FED and Govt allow serious Market corrections? Only time will tell.