January was up-revised to worst increase since August 2023, PPI inflation doubling in 12 months. February unchanged, waiting for up-revision.

By Wolf Richter for WOLF STREET.

It happened again. We’ve been discussing this issue here for many months: It’s the up-revisions of the prior months that are largely driving the PPI higher, and that was the case today too.

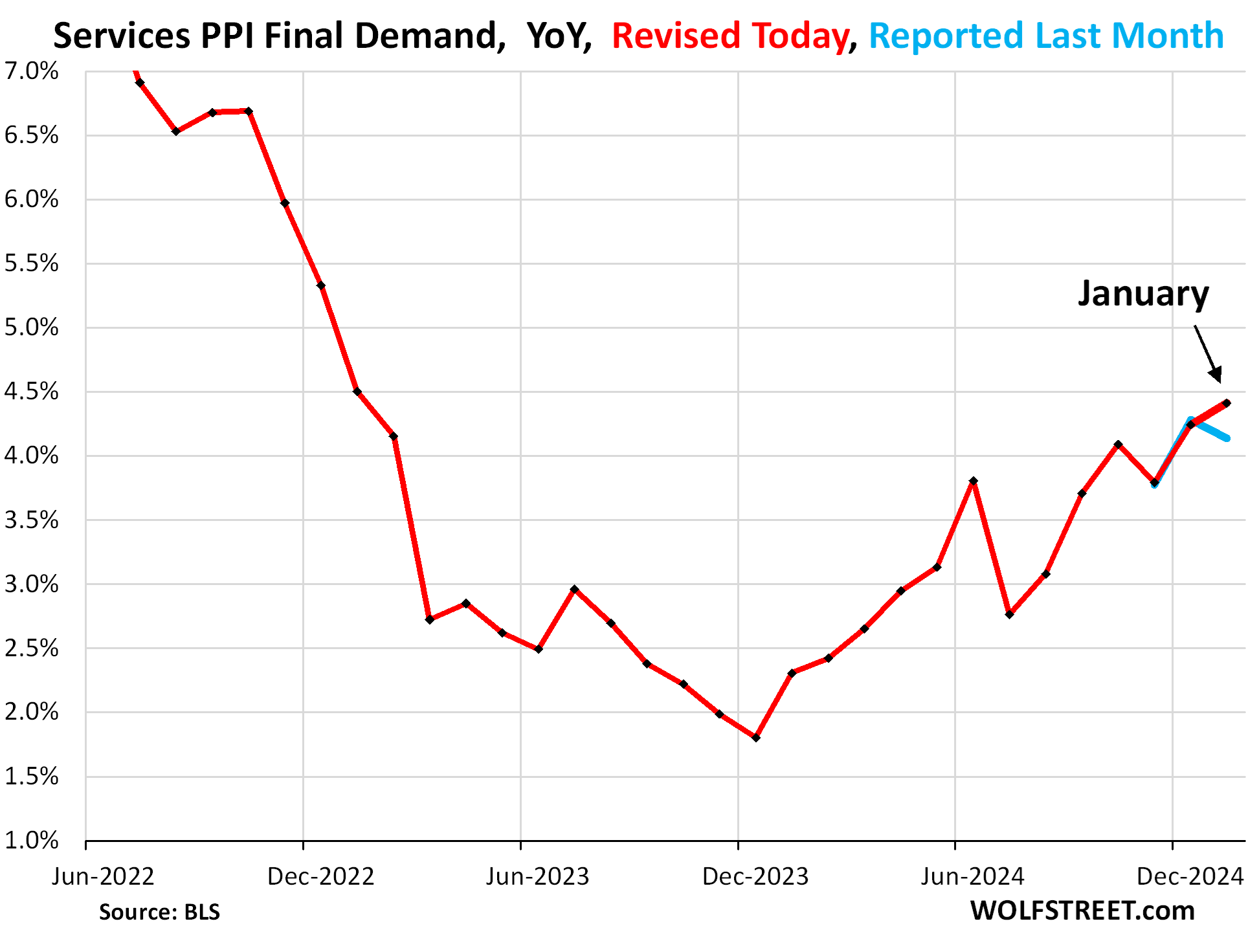

Today’s Producer Price Index for February once again included up-revisions of the data for the prior month, driven by a big up-revision for the services PPI that doubled the month-to-month increase, which flipped the previously reported year-over-year “cooling” in January to “continued heating” in January.

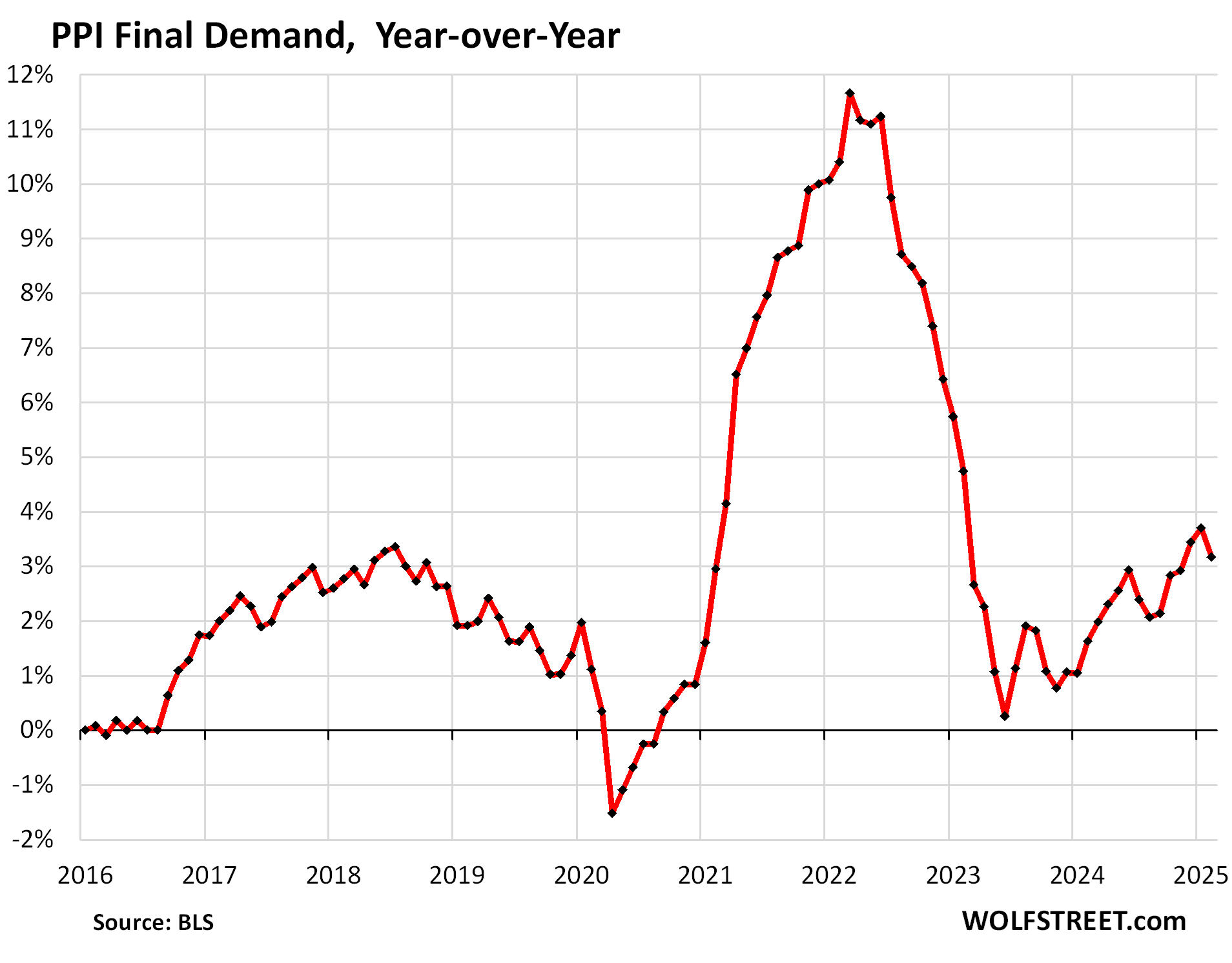

Overall PPI up-revisions: The month-to-month increase of the PPI for January was revised up by 21 basis points, to +0.61% (+7.6% annualized), the biggest increase since August 2023, from the previously reported +0.40% (+4.9% annualized).

The year-over-year increase of the PPI for January was revised up by 19 basis points, to +3.70%, the biggest increase since February 2023, from the previously reported +3.51%.

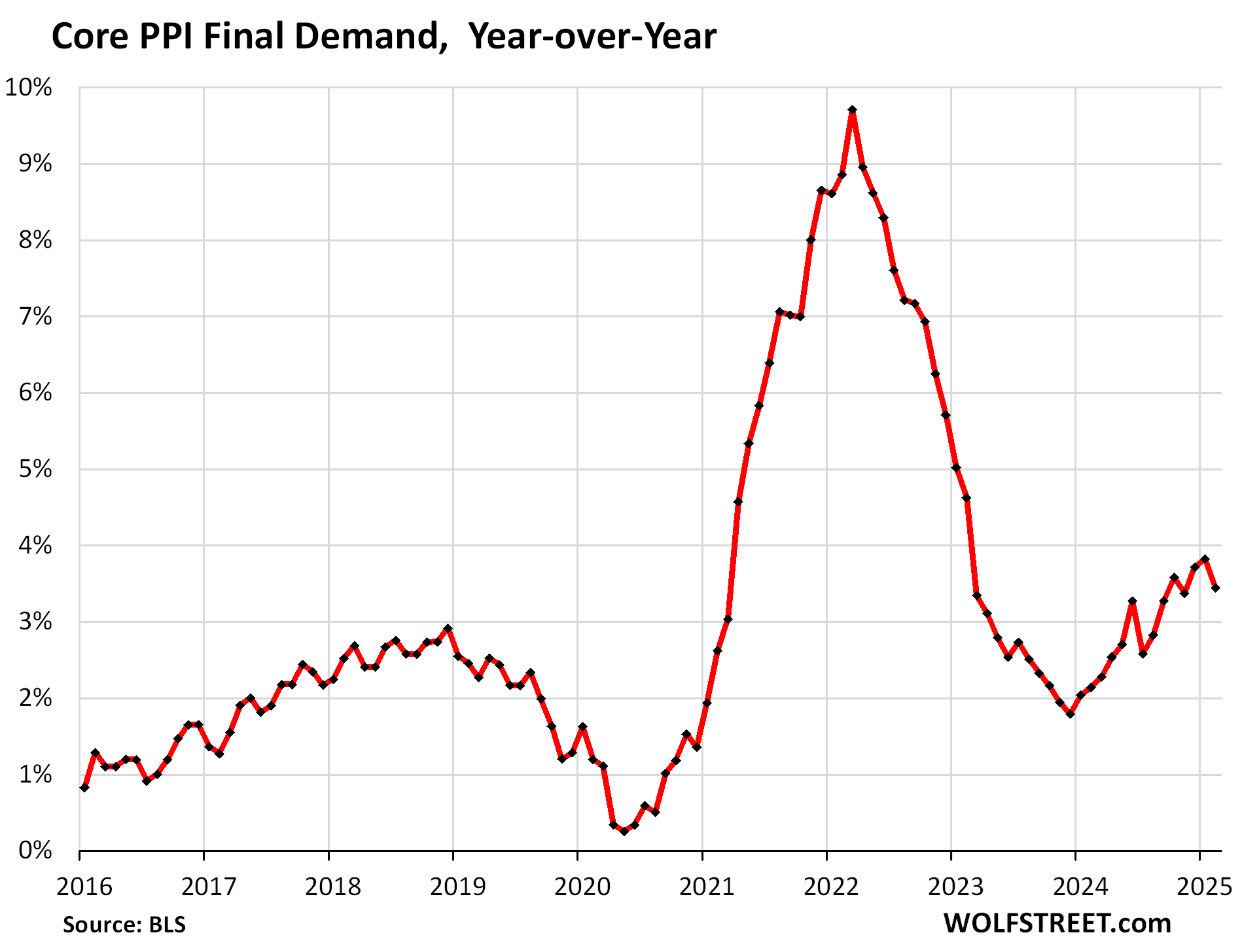

Core PPI up-revisions: The month-to-month increase of the “core” PPI for January was revised up by 23 basis points, to +0.51% (+6.3% annualized), the biggest increase since June 2024, from the previously reported +0.28% (+3.4% annualized).

The year-over-year increase of the core PPI for January was revised up by 22 basis points, to +3.83%, the biggest increase since February 2023, from the previously reported +3.61%. This up-revision to +3.83% flipped the January data point from being lower (cooling) than December (3.72%) to being higher (re-heating) than December.

Services PPI up-revisions: The month-to-month increase of the services PPI for January was revised up by 29 basis points, nearly doubling it, to +0.61% (+7.6% annualized), the biggest increase since June 2024, from the previously reported +0.32% (+3.9% annualized).

Services account for 67.5% of the overall PPI. It’s these big up-revisions in services that trigger the up-revisions in the core PPI and the overall PPI.

The year-over-year increase of the services PPI for January was revised up by 27 basis points, to +4.41%, the worst increase in two years, from the previously reported +4.14%. This up-revision to +4.41% flipped the January data point from being lower than December (+4.24%) to being higher than December.

To illustrate the impact of the revisions, here is the chart of the year-over-year services PPI through January with the revised data as reported today (red) and originally reported data (blue). January flipped from cooling (blue) to heating (red). Since these types of up-revisions have been happening nearly every month since PPI inflation began reheating last summer, we see a good chance that today’s February data (more in a moment) will be up-revised too.

These up-revisions are a substantial part of what drives the PPI higher, but they don’t show up in the headlines reporting on the month-to-month data.

The PPI for February.

The overall PPI for February (to be upwardly revised next month?) was essentially unchanged from the upwardly revised January, which had been the biggest increase since August 2023.

This unchanged February caused the year-over-year increase to decelerate to +3.2% from the upwardly revised increase in January of 3.7%.

So far, powered by the up-revisions, it’s a trend of zig-zagging higher from the low point of near 0% in June 2023.

The PPI tracks inflation in goods and services that companies buy and whose higher costs they ultimately try to pass on to their customers.

Energy prices dropped in February (-1.2% month-to-month), after several month-to-month increases. Gasoline prices dropped by 4.7% at the wholesale level. Year-over-year the energy PPI fell by 3.7%.

Food prices jumped by 1.7% in February from January, after the 1.0% jump in January. The avian flu’s impact on egg production played a role, as egg prices jumped 54%. Year-over-year, food prices at the wholesale level increased by 5.9%.

Without food & energy: “Core” PPI for February (to be upwardly revised next month?) declined by 0.6% in February from the upwardly revised January, which had been the biggest increase since June 2024.

Year-over-year, core PPI rose by 3.45%, a deceleration from the upwardly revised January reading.

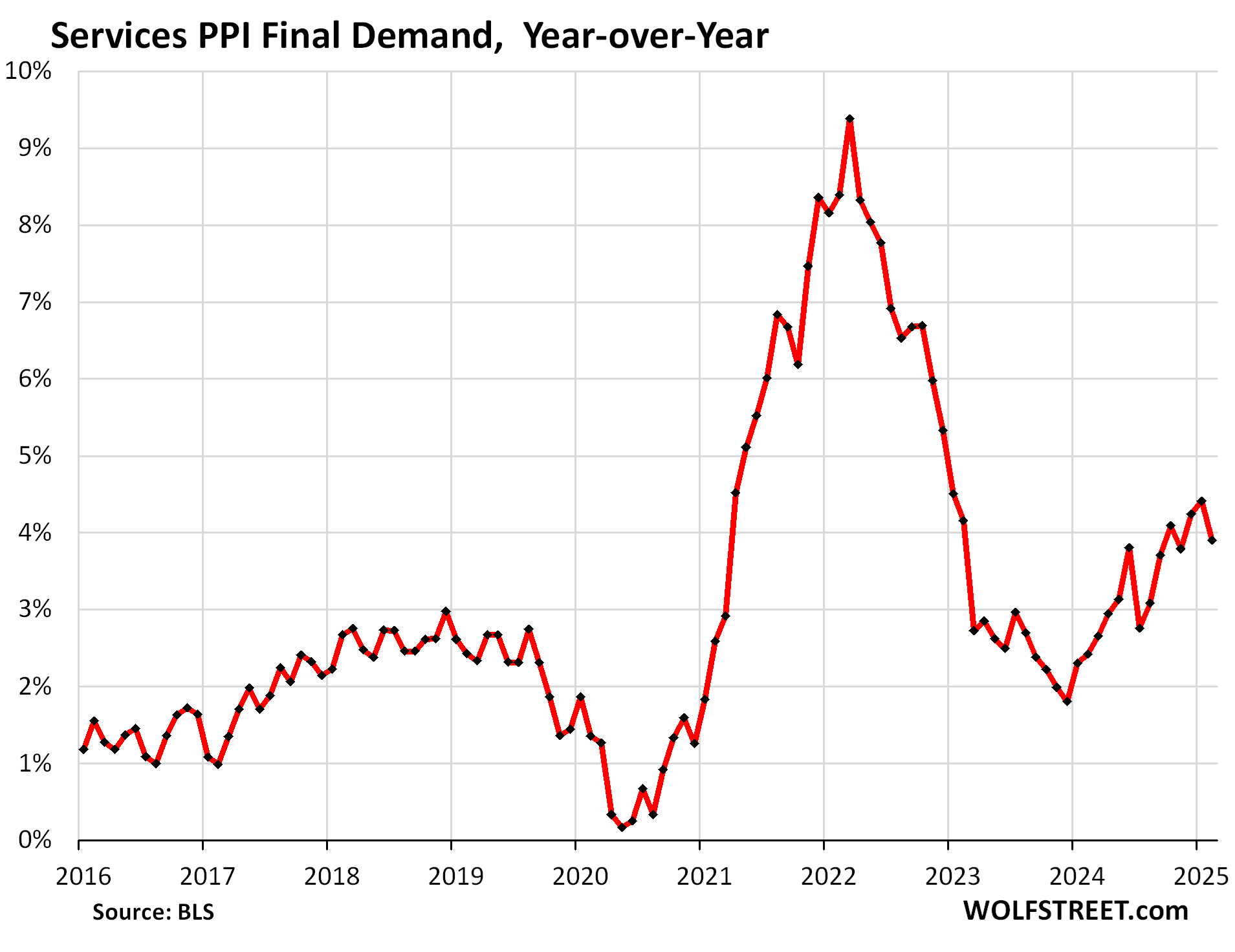

The services PPI, which accounts for 67.5% of the overall PPI but excludes energy services, declined by 0.16% in February from the upwardly revised January.

The month-to-month decline was driven by margins for trade services, which dropped by 1.0% (the trade PPI tracks changes in margins received by wholesalers and retailers). Without trade, transportation, and warehousing, services rose by 0.2% in February from January.

Year-over-year, services PPI rose by 3.9%, a deceleration from the upwardly revised January reading that flipped from the previously reported decline to the hottest increase since January 2023 (see first chart above with the blue and red lines):

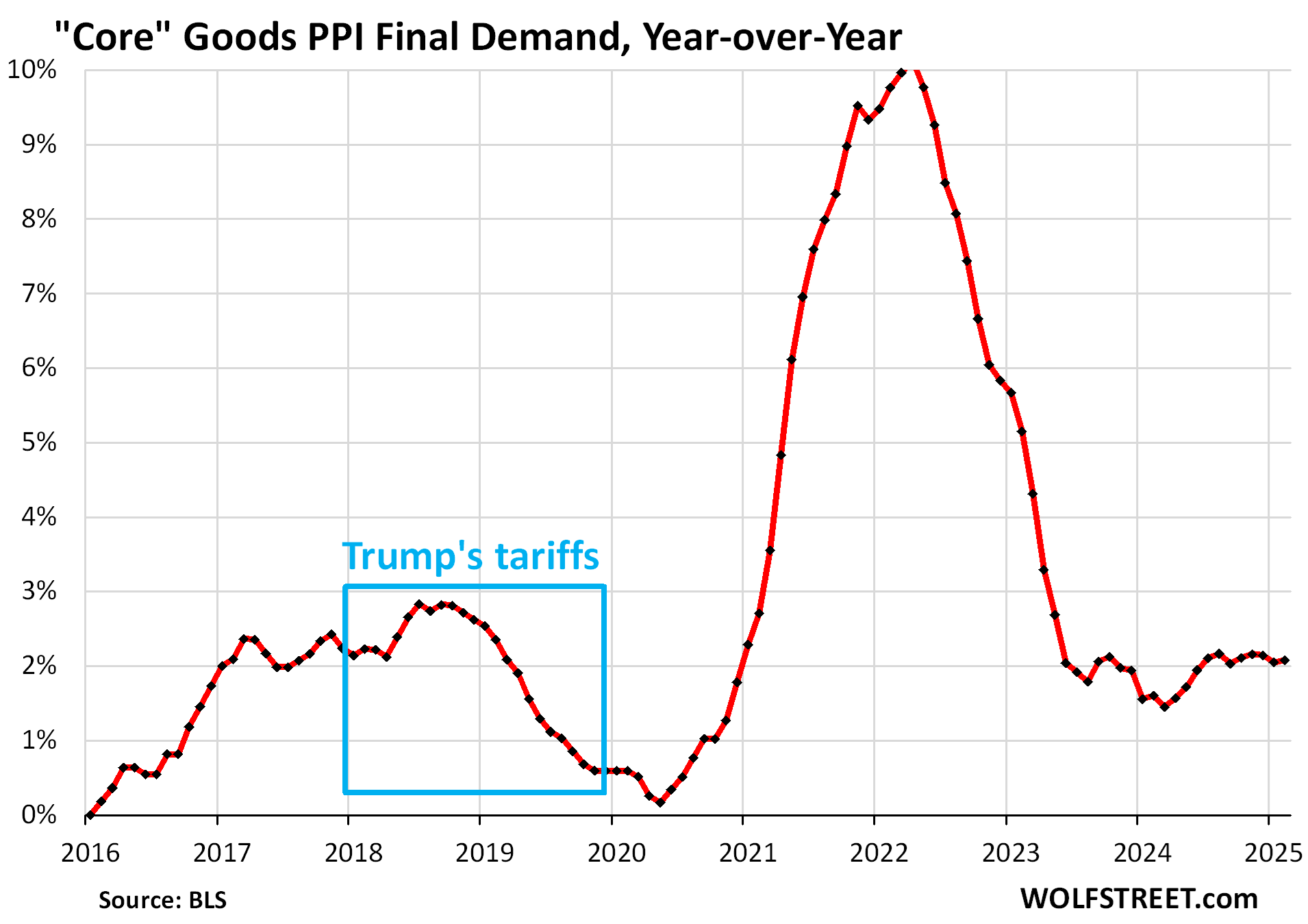

The “core goods” PPI was revised up by only 4 basis points for January (to +0.17% from +0.13%). But in February, it jumped by 0.35% (+4.3% annualized), the biggest increase since January 2023.

Year-over-year, it rose by 2.1%, in the same 2%-plus range of increases for the eighth month in a row. The PPI for “core goods” covers goods that companies buy but excludes food and energy products.

This is where tariffs would show up if they get passed on this far. Last time, there was a little bump in early to mid-2018, even though the final tariffs weren’t implemented until later in 2018 (blue box).

But companies could not pass on the price increases overall to consumers, and consumer price inflation for durable goods, where tariffs would have hit the most, remained negative (in deflation) throughout that time (PCE price index charts for durable goods and all goods, and article). This time, it’s different?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, any systemic reasons for the constant revision upward of the PPI?

The PPI data pile is gigantic. It goes deep into all industries and way up into the pipelines of products and services all the way to raw materials. The BLS publishes a detailed report every month on the PPI. Here is February, 352 pages of detailed tables!

https://www.bls.gov/web/ppi/ppi_dr.pdf

The up-revisions became a big thing last summer when the PPI inflation started to re-accelerate. So the original reporting lags, and revisions are used to catch up. And it’s mostly in services.

I’m fine with this, that’s how it is with these huge amounts of data that they’re trying to release as soon as possible before they have all the data.

But I don’t like the month-to-month reporting of it. If they report three-month averages, the last two revisions would be included, and two-thirds of the problem would go away. If they report three-month averages with a one-month lag, nearly all of the revisions would go away. So today, they would report the three-month average of November, December, and January. But then people complain that the data is too late, though it would be a lot more accurate. So we rather get advance data that is highly volatile and subject to big revisions – and can thereby be misleading if you cite it out of context. But the media doesn’t care, it comes up with its headlines and washes its hands off it. And that’s the problem.

I’m all for quarterly reporting with a one month lag. The more this can be firmed up the less it can be politicized, adulterated and misunderstood.

EXACTLY! MSM economic reporting – and the ever present Village Idiot brokerage firm self proclaimed “experts” (they NEVER, and r incapable of citing ACTUAL DATA like our BELOVED WOLF 😊👍👍🙏🙏 Many thanks Wolf 🐺) spew inane ridiculous BS, maintaining the faux ideation that random events and POTUS administration policies r the key drivers of the markets

Wolf, if the reporting were unbiased, we’d expect to see frequency of up/down revisions fluctuating randomly (think coin-flip).

Looking backward, are you observing that?

Steve,

As I said, the PPI is an enormously complex huge pile of data into all industries and up the pipeline all the way to raw materials, and the data collection is lagging, and the revisions supply the lacking data later. It’s just that this is now a fast-moving train, and the additional data is mostly in the direction of the fast-moving train.

I started discussing the up-revisions with the September 2024 PPI (released in October).

https://wolfstreet.com/2024/10/11/after-large-upward-revisions-core-core-services-ppi-inflation-not-benign-at-all-whole-scenario-changed-for-the-worse/

PPI often has pretty big revisions, but in normal times, they’re kind of random, up and down, and so I didn’t pay that much attention to them. But last fall, I took notice, and I started saving the old unrevised data, starting with the September PPI, rather than overwriting it with the new data in my spreadsheet. And so I was able to track the revisions better, and go back to the original data, several months back if I have to. This provided a lot of clarity.

Hasn’t anyone created the Inflation Revisions Volatility Index Numbers Gauge (IRVING)? We need another dorky measure of hot air to increase employment in the consultants and advisors sector. Slight of hand stageshows are all the rage, The Way We Live Now.

Your article made me think about the inaccuracies of preliminary data and whether it was politically motivated or just a random reading.

yes

The economy was rolling over before the pandemic. The fact that services is above pre-covid betrays the inflationary bias. (Labor weighted) When you mix inflation with a recession you get stagflation.

The pandemic was more serious economically because of the anti-viral measures taken to slow the spread of the disease. If we had simply accepted that Covid would take out the old and the compromised immunologically we would have been in better shape in dollars and cents ways. But such brutality is not to be countenanced, supposedly…

It did not threaten the young and healthy in any way, and those are who should be protected – the future. Instead, a bunch of old billionaires panicked when they thought that a new plague with a penchant for killing olds was going to separate them from their precious lucre, so they destroyed countless lives instead, thinking only of themselves.

Huh? The hospitals filled up with social distancing. Without distancing, there would have been alot more suffering. Are you fine with watching people gasping for air on the streets?

People were learning as time went on. There were alot of unknowns. If you’re going to worry about billionaires, now is the time to do that. They’re trying to decimate the government, and what little remaining safety nets that are in place. I don’t think anyone wants to go back to the days of watching suffering old people picking through trash cans.

I worked in a major inner city level 1 trauma center as an ICU nurse on the COVID unit. I personally took care of people in their 30’s to 50’s who died from COVID.

Which is exactly the apparent call to arms against the concept of an un-taxed billionaire class imposing their will on a subservient, throw away American.

The best thing about Americans is that they’re Americans.

I was just remembering today a family friend pumping gas for a living and the elevator operators whose jobs must have been boring but honorable.

Ambrose Bierce

The economy “rolling over” before the pandemic is fantasy nonsense. The 15-year average growth rate of real GDP in the US is 2.0%. This is what the economy did before the pandemic, in real GDP growth:

2018

Q1: 3.3%

Q2: 2.1%

Q3: 2.5%

Q4: 0.6%

2019

Q1: 2.5%

Q2: 3.4% (hot)

Q3: 4.8% (HOT)

Q4: 2.8%

“It did not threaten the young and healthy in any way”

FALSE

The young and healthy, as with most diseases, had FEWER life-threatening infections, not none.

And then they brought the disease to their parents.

Prevention methods make for fewer infections which makes for less transmission which eventually halts the spread of the disease. Which is the point.

I think you are brave in the sense that what you are describing is the chaotic state of society that actually existed.

Your conclusion, ” take out the old and the compromised immunologically ” seems familiar like a passage from Hitler’s manifesto.

The cure is …….

YUP!! And that’s EXACTLY where we’re at/headed! 👍👍

Yes the economy was rolling over, with Trump on the phone to Yellen to reinstate QE or he would replace her. Which he did with the right aligned Powell who reinstated QE, before the covid panic saved them, as I recall.

Yellen was out in Feb 2018, not 2019. Powell was in on Feb 5, 2018. And the economy was not “rolling over” in 2019. See my GDP figures above.

I offer as evidence your chart of Core Final Demand with the blue box Trump Tariffs.

Ambrose Bierce

That’s a PRICE/inflation chart (“PPI Final Demand,” the last stage of the four stages of PPI price indexes), not an economic growth chart. Good grief?

We are definitely not going towards a recession. We will either have infaltionary growth or stagflation.

Or maybe a new term; economic malaise

Wolf,

Thank you as always for these articles. A few thoughts and questions from me. First, is there a time limit for when data is not revised anymore (i.e. a month, a quarter, or only when materially different)?

Second, I like the highlights you have done with Trump 1 tariffs, but I would like to delve deeper. This stuff gets complicated pretty quick so trying to really understand it.

First set of questions around PPI specifically (the last chart in the article – Core Goods PPI Final Demand YoY). One, while it does appear to trend towards 0 pre-covid, technically since this is a YoY % change, that means PPI is still higher than the previous year, just not as much (i.e. the number would need to be negative to show actual reduction in PPI prices, just not less steep increases)? Two, as you point out tariffs should show up here, regardless if the producer ultimately passes on prices (that would be CPI/PCE correct?), but tariffs would not show up here if the importer of the good prior to the producer ate the tariff cost (ex: producer tells steel supplier that they will not pay tariff cost, so steel supplier gets less money for product since they pay tariff, assuming no change in price otherwise)?

Finally, this is in relation to the PCE chart you linked in the last paragraph. With a focus on the Durable good category again during Trump 1 tariffs, while the overall durable goods index is negative, it is moving more positive (less negative up until covid – where it does a nice fake-out lower before shooting for the moon!). So would this not show some small impact of tariffs, since they are generally going to be on durable goods and less so on services? Again, overall the amount is still negative, but the YoY % gets less negative, so that would show things still being cheaper than a year prior, just less cheap than in years past?

Thanks, and I always appreciate these articles.

I’ll just pick one question to answer:

“With a focus on the Durable good category again during Trump 1 tariffs, while the overall durable goods index is negative, it is moving more positive (less negative up until covid – where it does a nice fake-out lower before shooting for the moon!). So would this not show some small impact of tariffs....”

Year-over-year percentage change charts can get you lost in the weeds, which is also why I often post price-level charts. So here is the price level of durable goods. You can see that prices were relatively flat with a slight downward bias in 2028-2019, and there was no visible impact from tariffs:

Excellent thank you

Yes, Price Level. Just another example why we come to Wolfstreet. from 105 ro 120+ is what people “know” is true. Thank you.

Sounds like time for a FED rate cut. /s

Nah, upward revisions are transitory

Question:

Do CPI trend typically follow PPI trend? If so, how much lag is there?

These revisions are just another reason not to get too excited about a single month-to-month change in and of itself. Some indicators are worse than others as far as revisions go. A list of “the most likely to be revised and by how much” might be interesting.

I am a big advocate of data being supplied to two decimal places, as Wolf sometimes does when appropriate. A .4% increase could be anything from .35% to to .44% because of rounding, which is a pretty big range.

Good stuff as usual, Wolf. Why aren’t you working for Goldman or Blackrock or some other crooked investment firm and raking in the big bucks? Is it because they are crooked? Or maybe you prefer your freedom? Maybe altruism?

i work for a small T1 autosuplier. just 3 days of 25% nafta tariff last week cost the company $350,000. that’s pure profit up in smoke in a razor margin thin industry… after 1 year highering freeze due to EV pullbacks. If that nafta tariff comes back April 2 there are a lot of companies that won’t last long at all. Nissan, Stellantis? These companies are already on the edge with soft sales.

All part of the plan.

The cruelty of micro economic realities as collateral damage to the tectonic shifts in the macro economic equilibrium.

What you think your Elon Musk, America’s most flamboyant welfare queen. Well you aren’t. You are insignificant enough the the police will apply all the current technology on you.

I’d like to see Stellantis and all their crappy (mid-life crisis) vehicles finally go away completely.

The second wave of inflation is coming (baked-in etc.). It’s our spring of 1979. As a surfer, I can tell you that waves are very predictable if you know the intensity and the period of the wave. The larger the period, the more intense the set of waves will be. Get it over with already, stop stalling and let the second wave come. The longer we try to manipulate the data, the worse it will be.

I think you meant to describe in two dimensions the period and the amplitude, rather than intensity. Just a matter of vernacular, not a diss.

Do surfers live both longer and better than someone that has spent their lives mostly unaware of the ocean ?

That’s some amazing inflation! A quick 20% rise during 2020-mid 2024, followed by annualized increases of 3-6%.

1:04 PM 3/13/2025

Dow 40,813.57 -537.36 -1.30%

S&P 500 5,521.52 -77.78 -1.39%

Nasdaq 17,303.01 -345.44 -1.96%

The meltdown continues….

It’s not melting down fast enough. We need an entire week of days with the circuit breakers triggered. 1%? 2%? That’s nothing. Let’s see a week of solid 7% down days. One third melted away would be a good start.

Circuit breakers themselves are the real problem. By applying the rational stops to a panic state, you further encourage the irrational pie-in-the-sky to the “gotta get in there now” mindset at the other end. If you want to curb gambling, you’ve got to commit to breaking gamblers’ knuckles so that can’t sign those IOU’s.

Yeah about that. I think that the stock market is just as likely to erupt to the upside, a furious 6 pct rally in a couple of days. In a typical manner as the previous pattern of deflation of over inflated asset price bubbles.

What do they call it ? A suckers rally.

It’s crazy when you look at the charts and see the entire stock market doubled since 2020.

None of it seems to be based on any sort of logic or fundamentals.

it nearly doubled from the pre-march 2020 meltdown. it tripled from the march low.

I expect Elon will have people at the BLS replaced who compute increases in the inflation rate. What I am surprised about is that the 10 Year Treasury has trended downward. Wall Street wizards have a history of being complacent.

Wolf, does super easy government lending sponsored programs influence cpi or ppi rates down the road? During the pandemic we saw some of these programs…. Just wondering the correlations if any…with easy money….thru lending.

Yes, I think the huge inflation pulse we saw in 2021-2022 was a product of a lot of simultaneous factors, including the whole basket of “free money” — PPP loans, student loan forgiveness, mortgage forbearance (borrowers didn’t have to make payments for a while and could spend this money), eviction bans (the government paid landlords not to evict, and tenants had this extra money to spend), ultra-low borrowing rates all around, all kinds of government giveaways to companies and consumers, including all kinds of tax credits, the Fed’s QE-inflated assets bubble that made lots of people a lot richer, and they went on to spend some of this money… you name it we had it. Tbh, I’m glad we didn’t get away with it.

when you say “get away with it,” i assume you mean do so without consequences, i.e. inflation?

if so, i agree. otherwise all governments would be tempted to do this again, every year.

Bet they will anyway. Ours, at least.

This may seem like some mundane article about PPI, but Wolf Richter has distilled the data, purifying it and giving it to us for …… free.

I cannot find a more elegant, timely, accurate, unbiased, blatantly truthful view and assessment of this PPI data anywhere. It is like he is handing out gold coins. He has earned our respect and admiration.

A day with Wolfstreet ensures enlightenment.

Howdy Harry. A day without the Wolfman is a day without sunshine…

Howdy Folks. Wallstreet, RE, bubbles are hissing. Will inflation follow the trend? Keep the popcorn handy, a long way to go…….

Dips are still buying. Barely a blip off all-time highs….

Howdy DC. YEP, The Golden Age could happen. Millions and millions of new Drunken Sailors and private sector bubbles everywhere. Life is Good if you plan ahead……

An acquaintance of mine, with a gambling tendency, pinning their hopes on the long shot. The only bet he could afford.

All the while, 30 million people in California have chosen to ignore the LA fault which is overdue for a 8 Richter shrug from the universe.

In that context, perhaps who cares if one loses one’s bet than to the equally vacuous result. Winning.

I think they’re just moving money around, for now.

Who would ever think that ‘The Goose that Laid the Golden Egg’ would be a reality some day?They seem to cost that much! They hen owners must feel like their hens are money producers these days!

Hold on ! Not everyone is competent in producing their own eggs. The concept underlying the basis of the assertion that productivity is enhanced through the lens of the division of labor basis.

I can’t wait to see what tariffs does to this. You know, if they actually stick. I just wonder how long it will take to see them show up.

Howdy Folks. Let me know when Buffett sells his T Bills and starts buying stocks again?????

By the time you hear about that, it will be too late.

R&T: BMW Promises to Protect 2 Series, 3 Series Buyers from Tariffs, But Not Forever

The carmaker says it’ll temporarily “price-protect” the Mexican-made models.

From Reuters a few hours ago:

CEO Oliver Zipse said, “BMW expects trade tariffs to cost the carmaker 1 billion euros this year,” factoring in EU duties on its China-made EV and newly imposed U.S. tariffs which are upending global trade.

The 1 billion euro provision in the group’s earnings was “conservative”, with possible further tariffs to come from the European Union and United States.

Still, executives did not expect all the tariffs in place so far, which include 25% tariffs on steel and aluminum and on BMW’s vehicle imports to the U.S. from Mexico, to remain in place for the whole year, Zipse said.

“If the situation changes, so does our outlook,” CFO Walter Mertl added.

Here’s a nice tidbit from the Reuters report: BMW’s U.S. plant in South Carolina exports cars worth over $10 billion, making the company the largest U.S. automotive exporter by value, according to Zipse.

Prairie Rider

Thanks for citing BMW to confirm what I have said forever: Tariffs are a tax on profit margins of importers, not on consumers, because it’s hard to pass on tariffs in the current climate, or most any climate, where the company would lose sales if it hikes prices to pass on the tariffs. Automakers will eat those tariffs. And that’s good.

Automakers have huge profit margins that got big and fat during the pandemic. BMW said that its profit margin might shrink by 1 percentage point because of the tariffs. So no biggie.

This is precisely what occurred last time: no impact on goods inflation but stocks got hit.

https://wolfstreet.com/2025/02/03/what-trumps-tariffs-did-last-time-2018-2019-had-no-impact-on-inflation-doubled-receipts-from-customs-duties-and-hit-stocks/

Wolf,

I enjoyed my ’16 M4 yesterday for the first time since winter and road salt hit the Twin Cities. Damn, that car is a joy to drive. And, with the tire pressure and temperature readings on the center console display, you know the temp, and therefore the stickiness of the tires.

A fresh set of Michelin Pilot Super Sport went on last April. Of course, I got ’em up to temp and used every bit of stick they had yesterday.

And a thanks goes out to you, Wolf. As a reader of WOLF STREET, I learned that the used car market was very soft in the immediate time after Covid hit in March 2020. So at the absolute market bottom, I picked up my ride (a 3 year lease-back from Atlanta) on 2 May ’20.

All BMWs are a joy to drive! Glad you enjoy your M4!

Shows how much markup there is.

DM: Trump’s tariffs have caused the 7th fastest stock market slump on record… leaving 401(K)s ravaged

Wall Street´s sell-off hit a new low Thursday after President Donald Trump´s escalating trade war dragged the S&P 500 more than 10 percent below its record – set just last month.

The S&P 500 is down ONLY 10%, and still up yoy, LOL. What kind of spoiled brats are these?

The S&P 500 was down 50% in 2002. And it was down 50% again in 2009. And the Nasdaq was down 78% in 2002. So 10% is nada. These kids have no idea.

10% corrections happen at an average interval of 13 months. One year pre pandemic, either 2018 or 2019, had two different 10% corrections.

The sky is not falling. This happens almost every year.

Right. And new highs always follow these brief dips. These crybabies deserve an 80% correction to put them in an extended time out, because that’s how crybabies should be treated.

these people believe markets have a right to hit new records every few months.

Biden was giving money away after Trump got elected, are we seeing the repercussions of those actions to sabotage his presidency?

Weirdo.

Following DOGE daily. You would think congress…regardless of the D or R in front of their name would be ashamed & in hiding to the absolute fleecing of America.

Maybe you should look into the actual reality of their “cuts”.

I did not mention “cuts”.

My comment is the actual REALITY of what was funded.