HELOC balances surged, mortgage balances barely budged: More households, more income, more housing debt.

By Wolf Richter for WOLF STREET.

Mortgage balances barely edged up in Q4, by just $15 billion, or by 0.1%, from Q3, the smallest percentage increase since the dip in Q2 2023, to $12.6 trillion, as demand for mortgages has plunged, because sales of existing homes have plunged to the lowest since 1995, though there is plenty of inventory for sale. But demand for new single family houses has held up, as homebuilders cut prices and threw big incentives at the market, including mortgage-rate buydowns, to move the glut of new completed single-family houses they have for sale. At the same time, more people who could buy are renting – the “renters of choice” – to benefit from an arbitrage between two similar products with very different prices.

Year-over-year, mortgage balances rose by 2.9%, or $353 billion, the smallest year-over-year increase since Q1 2019, according to the Household Debt and Credit Report from the New York Fed, based on Equifax credit report data.

The increases over the years were driven by higher prices and thereby larger amounts financed, topping out with a year-over-year increase of 10% in Q1 2022.

But here come the HELOCs.

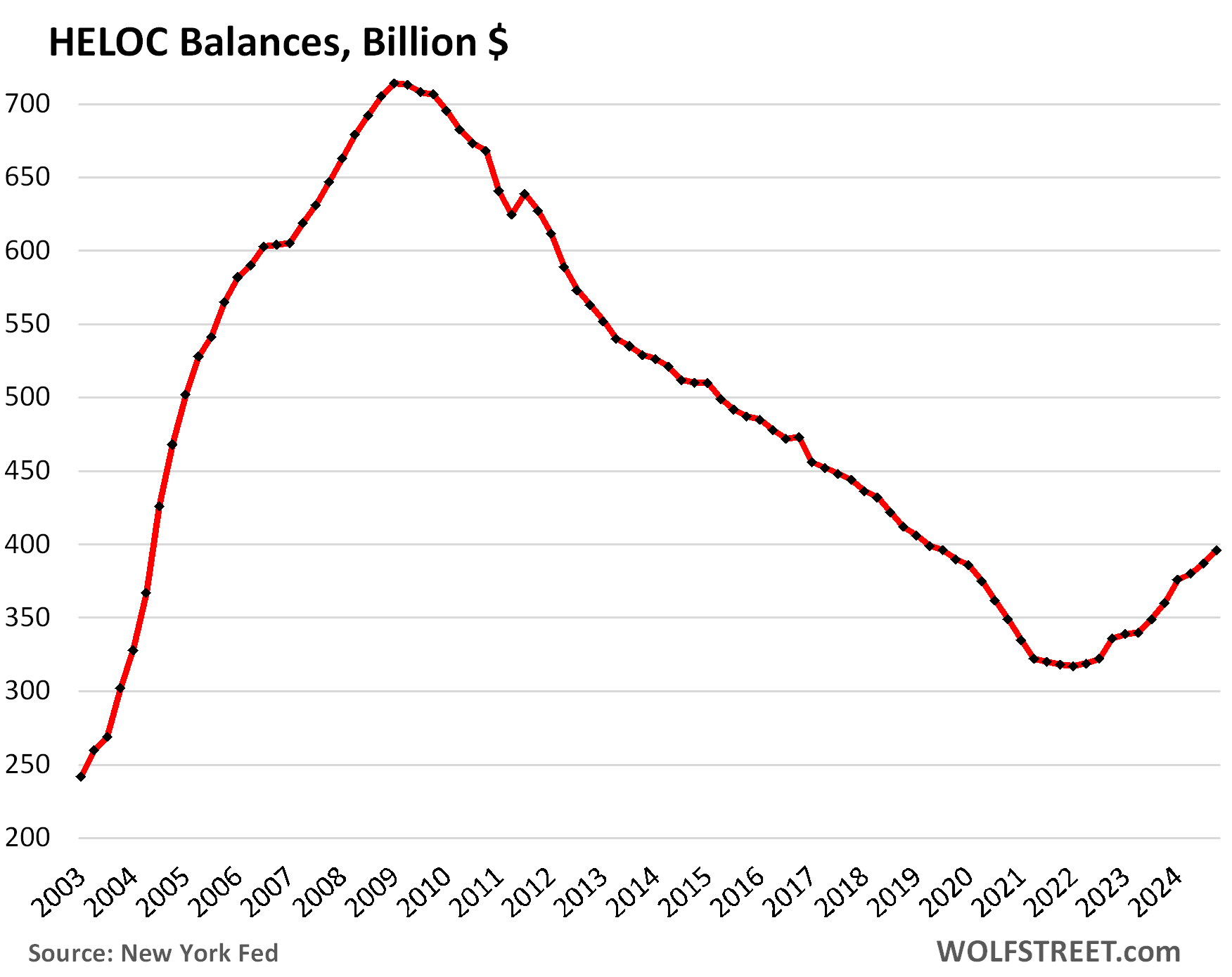

Balances of Home Equity Lines of Credit jumped by 2.3% in Q4 from Q3, and by 10.0% year-over-year, to $396 billion. In less than three years since the low point in Q1 2022, HELOC balances have surged by 25%.

People are doing the math: Cash-out mortgage refinancing activity has collapsed due to the higher mortgage rates. If homeowners need cash for a remodeling project or a wedding or whatever, it can be less costly for them to take out a HELOC at the higher rates that HELOCs come with, and not cash-out-refinance an existing 3% mortgage where they would end up with a bigger mortgage at a 7% rate on the entire mortgage. In addition, HELOCs are lines of credit; only the actual balance drawn on it incurs interest.

Despite the 25% surge in less than three years, HELOC balances remain historically low after 13 years of incessant declines coming out of the Housing Bust. These are the actual balances drawn on HELOCs.

In terms of size, nearly half of all HELOCs recently originated had credit limits between $50,000 and $150,000, according to an earlier report from the New York Fed. About 28% had credit limits below $50,000, and 25% had credit limits of $150,000 to $650,000. Only 1% had credit limits of over $650,000.

HELOCs turned into an additional risk for homeowners during the Housing Bust, including in the 12 non-recourse states – more details and list of nonrecourse states here – because lenders of second-lien mortgages could sue the borrower for the deficiency, while first-lien lenders got the house in a foreclosure and then, in non-recourse states, could not sue for a deficiency judgement.

In addition, in all states, the lender of a defaulted HELOC could foreclose on the home even if the borrower was up-to-date with the payments on the first-lien mortgage. There were a lot of lessons learned back then – by both lenders and borrowers.

Burden of housing debt: Debt-to-Income Ratio

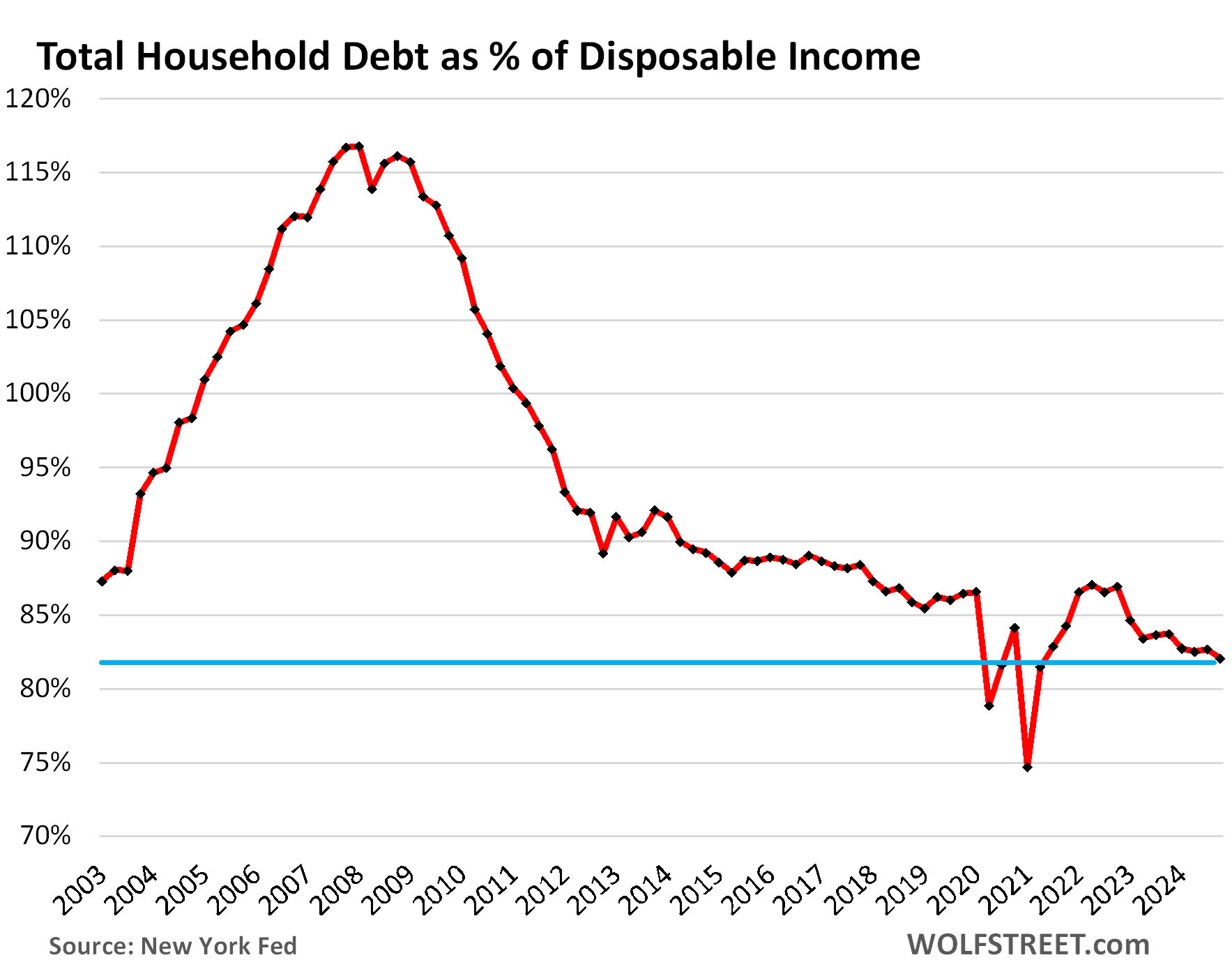

To view the burden of total housing debt – mortgage debt plus HELOC debt – on households, while accounting for more homes and higher incomes, we use the housing-debt-to-disposable-income ratio.

The debt-to-income ratio is a classic measure of the borrowers’ creditworthiness, their ability to deal with the burden of debt.

We use disposable income (by the Bureau of Economic Analysis) because it represents an after-payroll-tax cashflow from all income sources, not just wages: Household income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. This is the cash that consumers have available every month to spend on housing, food, and other daily expenses, debt payments, etc. What they don’t spend, they save.

- In Q4 from Q3: housing debt +0.2%, disposable income +1.3%.

- Year-over-year: Housing debt +3.1%, disposable income +5.1%.

With disposable income rising faster than housing debt in 2024, the burden of the housing debt on households, in terms of the debt-to-income ratio, declined further, to 59.1% in Q4, the lowest in the data except for a few quarters during the Free-Money era when stimulus payments from the government inflated disposable income beyond recognition.

The 50% spike of the ratio in the four years before it all blew up should have scared the bejesus out of everyone. When borrowers massively defaulted on this debt – $10 trillion in housing debt at the time – the financial system began to implode.

Today, the debt is bigger, but there are a lot more households, and they make a lot more money, so the burden of the debt is lower.

Higher mortgage rates impact only a small portion of borrowers: A 30-year fixed-rate mortgage, the benchmark mortgage in the US, doesn’t change its interest rate and payments during its entire 30-year term.

So homeowners with below-4% mortgages will have below-4% mortgages until they pay them off. That’s the majority of the debt even today. In 2022, 65% of mortgages had below-4% rates. Some of them have gotten paid off by now, including by people who no longer have mortgage debts at all. Currently 55% of all mortgages are below-4% mortgages (see our discussion and charts of the slowly fading “locked-in effect” here).

The 6%-plus mortgages only matter to the relatively small number of people who have those mortgages. Currently only 17% of all mortgages have 6%-plus rates, and even fewer have 7%-plus rates.

In addition, mortgage rates are now about back where they had been at the left side of the chart. The over-6% mortgage is nothing new. The below-4% 30-year fixed mortgage was a new phenomenon, and it only lasted a few years, during which everyone refi’ed into them.

Who is on the hook this time? Not the banks. The government guarantees the majority of residential mortgages, and those have been packaged into MBS and sold to investors, and it’s the taxpayer, not the banks and not these investors, that would eat the losses from mortgage defaults – one of the huge changes that came out of the Financial Crisis. Even those mortgages that the government doesn’t guarantee have largely been packaged into “private label” MBS and sold to investors, and it’s the investors that carry the credit risk. Banks keep only a relatively small portion of mortgages on their books.

So far, so good.

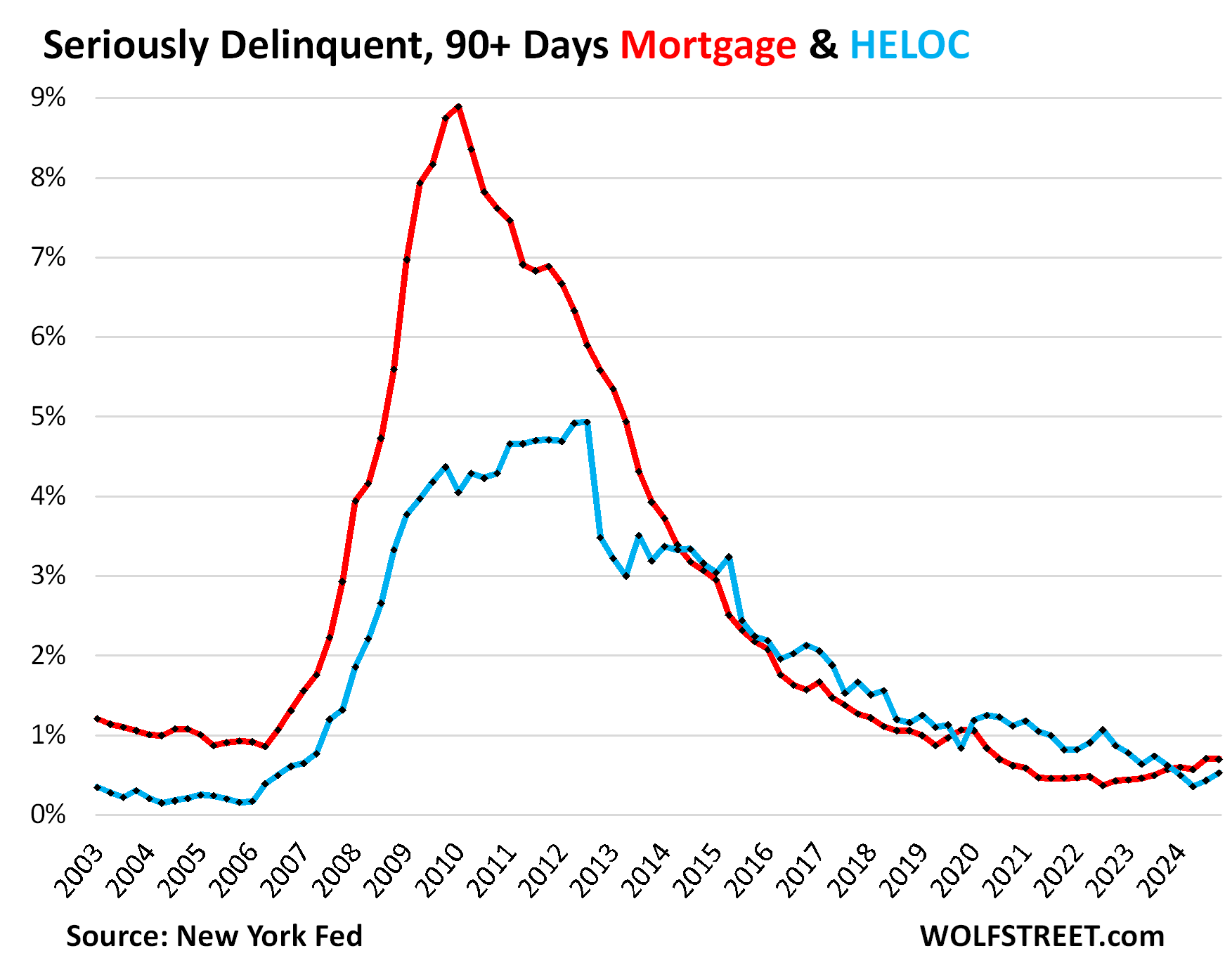

Serious delinquencies remain low. Mortgage balances that were 90 days or more delinquent remain very low, at 0.70%, down a hair from Q3 (0.71%), and well below the range during the Good Times of 2018-2019 and before the Financial Crisis of around 1% (red line in the chart below).

HELOC balances that were 90 days or more delinquent ticked up to 0.53%, also very low (blue).

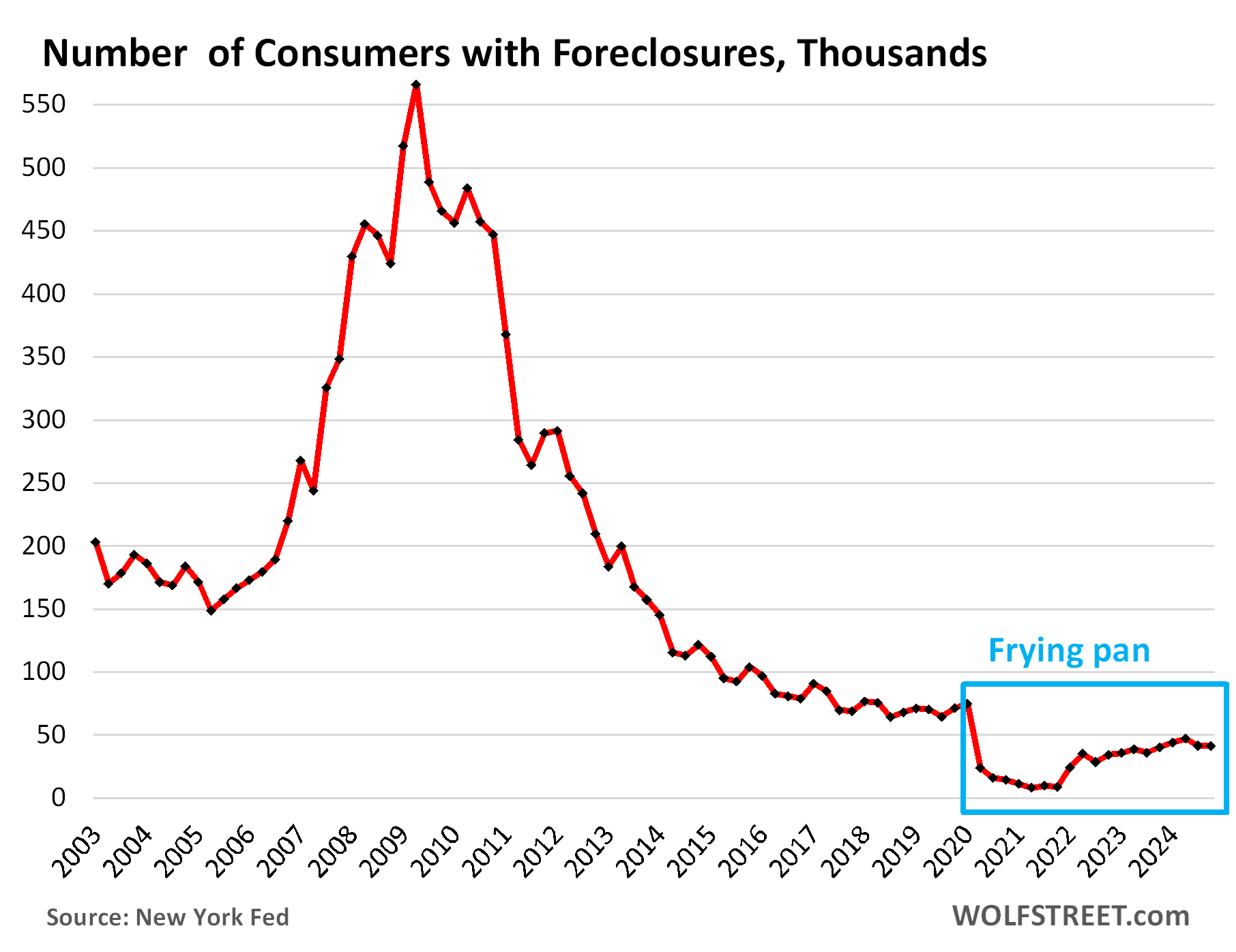

Foreclosures are ultra-low. The number of consumers with foreclosures in Q4 declined to 41,220, the second month in a row of declines, and at ultra-low levels, compared to 65,000 to 90,000 in the Good Times of 2018-2019.

The mortgage forbearance programs and foreclosure bans during the pandemic essentially made foreclosures impossible. They have risen since then but remain well below the prior all-time lows.

We have come to call the “frying pan pattern” is now cropping up in other credit metrics of the pandemic and its aftermath.

What’s keeping mortgage problems so low? After years of ballooning home prices, most homeowners that get into some kind of trouble, such as losing their jobs, can sell their home for more than they owe on it, pay off the mortgage, thereby avoid or cure a delinquency, and walk away with some cash, their credit intact.

Mortgages don’t get in serious trouble on a large scale until home prices crater, at which point homeowners who can no longer make the mortgage payments cannot sell their homes for enough to pay off the mortgage.

And in case you missed it on Thursday: Household Debts, Debt-to-Income Ratio, Serious Delinquencies, Collections, Foreclosures, Bankruptcies: Our Drunken Sailors’ Debts in Q4 2024

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In answer to your question toward the end of the article: “What’s keeping mortgage problems so low?”—

In addition to rising home prices, isn’t the low unemployment rate another important factor, and a somewhat fickle one at that?

True, though time will tell how fickle it really is. It’s been below 5% for 9 years now, except for the pandemic spike. For reference, from 1970-2015 it was only below 5% for 8 out of those 45 years, and now it’s been below that number for 8 of the last 9.5 years.

Could change at any time, of course.

Well, no. So for example, you bought the house five years ago in an area where prices soared by 50% over that period, and then you lose your job and remain without a job for long enough that you’re low on cash. So you just sell the house, pay off the mortgage with the proceeds, and have a bunch of cash left over. You rent until you find a job and get your feet back on the ground. This huge pile of home equity is why serious delinquency rates (90+ days) are so low. Job losses don’t matter until home prices tank enough to where the people that lost their job have negative equity in their homes, and then they cannot get out of them by selling them, they’re stuck, and they cannot make the payments, and that starts the process of delinquency.

This huge price surge in recent years has created a very peculiar housing market, and one of the peculiarities is this low delinquency rate.

However, there are already some cities with big home price drops from their peaks several years ago, and people that bought 4 years ago with only a 10% downpayment might now be underwater. So we should see delinquency rates rise in those cities (but I don’t have geo data for delinquency rates). Here are the biggest cities with big drops.

https://wolfstreet.com/2025/01/19/the-big-cities-with-the-biggest-price-declines-of-single-family-houses-or-condos-from-their-peaks-from-9-to-21/

sure, but this assumes that the person who lost his job is not part of a trend of millions of others also losing their jobs, in large enough numbers that it affects the housing market, lowers sale prices, and reduces the pile of home equity.

Like I said, it boils down to home prices tanking. Last time, home prices tanking came first, and caused the financial crisis which caused the Great Recession and the layoffs. Delinquencies started taking off when home price tanked in 2006 while the economy was still doing fine, and 2 years before job losses began to pile up massively in 2008.

agreed. but i don’t see any reason it couldn’t happen in reverse order next time. unless i’m missing something?

“unless i’m missing something?”

Respectfully, re-read Wolf’s comment:

IF someone loses their job, AND their house is still worth more than they paid, they just sell the house and rent with the cash from the sale. It wouldn’t trigger a foreclosure.

I guess if someone lost their job, but refused to sell, and then their home price tanked in value later, the same result could occur, but seems less likely.

respectfully, please re-read mine.

i’m not talking about one person losing his job. i’m talking about enough people losing their jobs in mass, such that the total demand for houses drops, and sale prices drop. if everyone who loses their job puts their houses on the market at the same time, you’d see a drop.

Thanks for the input. I see from Frank G and ShortTLT interchange that I was confusing the subject of “mortgage problems” with falling home prices.

Related but distinctly different data points…

But the demand for home prices has *already* dropped. See any of Wolf’s recent articles on home sales – new homes are doing ok (in markets that have them) but overall the housing mkt is still pretty frozen.

“But the demand for home prices has *already* dropped.”

I respectfully disagree. The demand for homes is there, it’s the affordability at these prices that has dropped… Dropped negligibly from nosebleed highs, and only in select markets. You can frame it as prices being down 10% if you want. If prices somehow doubled for a month then came back down to these levels, you could say “home prices are down 110% from their peaks!”. The peaks don’t matter unless you’re using that to tell a story. What’s relevant is the 200-300% price increases over a few decades, often averaging out to 10% home price appreciation (inflation) a year.

Franz is correct. One *possible* scenario would be if enough people lost their jobs then it would impact the supply/demand aspect of the housing market enough to make prices drop.

Right now prices are not dropping because, even though there is record low demand, we also have record low supply (of pre-existing homes) keeping prices roughly in equilibrium.

Whatever changes this ratio first likely determines what happens next.

I understand what you’re saying, but another effect of drop in employment is a probable drop in inflation and therefore a drop in interest rates. So, there is normally a natural offset.

Granted factors like tariffs may mean we’re in a non-normal situation whereby falling unemployment is not associated with falling inflation.

How about the fact that 60 percent of all mortgages are under 4 percent, that too with 2019-2020 prices and 2024-2025 wages,also many more percentage of US homes are owned outright compared to 2008, I just don’t see a cratering of the market unless there is some big bump/crash in numbers such as employment or confidence such US defaulting on interest payments or a china war on Taiwan or the coming demographic crisis. Correct me if I am being too optimistic.

is that relevant though? prices are set at the margins. your numbers just mean a sudden, large crash isn’t likely, but a slow, gradual reduction in prices seems likely as sellers realize they’re not getting their peak 2022 prices, and to get out while they can.

sellers aren’t going to hold out indefinitely, not if they want to move or need to move.

we’re continuing to see huge numbers of for sale homes

it’s funny to watch as so many are pulled from market for 30days before being re-listed ‘like new’

lots of smaller reductions, lenders want top $$$ for their foreclosed fixups

stopped wasting time for now

planning on summer were we’re gonna buy something as we just sold our 5th wheel

wife wants newer one and permanent location in 55+ resort

either way not going to be cheap

joedidee,

yes, exactly. that’s the part where i think the housing shills are wrong. a lot of people want to sell for a variety of reasons, so the “low inventory” meme is complete bullcrap. they just don’t want to sell for less than they think it’s worth, and they think it’s worth what it was in february of 2022, three years ago, when mortgage rates were 3%.

a lot of people held out waiting for the fed to drop rates and mortgage rates to drop from 7% back to 4%, and all would be right in the world again. but that didn’t happen. when the fed dropped rates, the mortgage rates went up. so after that, they clung to the fantasy that ten million immigrants were going to keep housing propped up, because we all know that impoverished migrants are buying 4 br houses in the suburbs.

now that that been exposed, as migration has slowed dramatically, their fantasy is that younger people having families is going to prop it up and that they’re going to be willing to pay these top 2022 prices for good schools, work remote, or whatever.

anecdotally, i have heard of several people who bought in 2023 or 2024 at peak pricing but with 7% interest rates. they figured they would struggle financially for a year or two and then refinance into a more reasonable 4-5% rate. now seem of them are legitimate worried.

housing prices are simply too high for the 7% mortgage rates, and there is no evidence rates are coming back down any time soon. you won’t start seeing foreclosures in mass and crashing prices without job losses, but it’s not hard to see how the $300k house from 2019 that peaked at $600k in 2022 could easily sell for $575, then $550k, then $525k, and all the way down until it’s at something closer to $300k.

every seller who is tired of paying the carrying costs on a house they don’t need will drop over time. enough people do this, and the comps start gradually dropping. that’s already happening in a lot of markets.

“housing prices are simply too high for the 7% mortgage rates”

FACTS.

Tim, I agree that analyzing the rate of change of existing mortgage rates is key. From Wolf last month: “The share of mortgages with rates below 4% has dropped to 55.2% of all mortgages outstanding at the end of Q3 2024, from the high of 65.1% in Q1 2022… Conversely, the share of mortgages outstanding that have rates of 6% and higher has more than doubled to 17.2% at the end of Q3 2024, the highest since Q3 2016, from a share of 7.3% at the low point in Q2 2022.”. A massive change in a few years, that will only continue to shift, accelerated by any job churn (federal layoffs or otherwise). I’d love to see more data on these shifts and other mortgage ranges.

https://wolfstreet.com/2025/01/20/locked-in-homeowners-nevertheless-pay-off-below-4-mortgages-and-their-share-of-all-mortgages-outstanding-drops-to-55-lowest-since-q1-2021/

The mortgage problems will make themselves known in good time. It is too early in the cycle to look at them as an indicator. The importaint indicators to look at right now are credit card balances. Some people try to say that increasing credit card balances are a sign of strong consumer spending but that is not the case. In reality, credit card spending has changed significantly over the past decade because now most people pay their insurance, HOA fees, and even property taxes on their credit cards where as 10 years ago they paid those bills with checks. The massive increases in insurance, taxes, and HOA fees are pushing up credit card balances as homeowners go into debt to pay them.

People keep conveniently forgetting that there are lots more workers with lots more income to spend a lot more money. And higher balances reflect higher purchases by more workers with higher incomes. See consumer spending data. And since credit cards are the universal payment method in the US, most get paid off by due date and don’t accrue interest, people just collect their 1% or 2% cash back. And therefore lower burden. Article coming:

It seems to me the average American learned a hard lesson about debt during the GFC. This trend of keeping debt low makes the average American more resilient financially. My guess is that is why the housing market is still holding onto the ridiculous price gains(or at least a partial reason).

“Lots more workers” is debatable. The tech sector is shedding jobs at unprecedented rates, much like the manufacturing jobs we sent to Asia in the 80s. “Unemployment rate” is a misnomer, because it only counts those collecting UI, not those whose payments have expired yet they are still not employed.

PART of the tech sector is shedding employment, but that’s a small sector. The other part of the tech sector is adding employment (AI and related).

Here are the job gains:

https://wolfstreet.com/2025/02/07/huge-upward-adjustment-of-employment-labor-force-as-wave-of-immigrants-is-finally-included-unemployment-drops-wage-growth-accelerates-the-annual-revisions-are-here/

Any mortgage in default that historically would have been a foreclosure in many cases today are not being defined as being in foreclosure when they are in Forbearance which is hiding the volume. Many go into loan modifications and fail multiple times and still not being called a foreclosure. The CFPB has alot of responsibility on this and creating a false market signal.

I’ll just repeat it here:

Only 0.5% of all the Fannie and Freddie mortgages are in forbearance, most of them due to natural disasters and other temporary reasons. The Covid forbearance is nearly gone.

Most of the mortgages in Covid forbearance were modified and payments resumed or payments resumed without mortgage modification. In a small number of instances, the people sold the home, paid off the mortgages, and walked away with some cash. There is only a minuscule number of mortgages still in Covid forbearance problems (blue in the chart).

The number of mortgages in natural disaster forbearance has surged with the hurricanes in the 2024. The Los Angeles fire forbearance figures are not yet shown, but they will show up too over the next few months. Other temporary hardship forbearance is shown in gray.

The chart (via Mortgage Bankers Association) shows the percentage share among the 0.5% of Fannie and Freddie mortgages in forbearance.

HELOC’s typically have an initial “teaser rate” (ie. 2.99%) for the first 6-12 months or so, before re-setting to the fully indexed rate. Monthly payments are also “interest only” during the draw-down period (which can be as long as 5-10 years), thus the monthly payments are initially quite a bit lower than a mortgage re-fi’d at today’s prevailing rates.

But problems can crop up at the end of the draw-down period, when principal gets added to the monthly payment. It can increase dramatically at that point.

barely closed on my heloc end of dec at 8%

by Jan 5th it was raised to 8.25%

no hurry – just getting liquid for when time is right

If you do a HELOC, and then borrow but pay it back within e.g. a couple days or a week, do you still accrue interest? Or is it like a credit card, where you can get an interest-free loan by paying off the full balance by the due date?

I’d guess the former but never inquired.

Hey Wolf,

Secretary of the Treasury Bessent stated that he plans to monetize the fixed asset side of the USA balance sheet. With $4.7 Trillion of MBS on its balance sheet, Fannie Mae appears to be near the top of the list.

Can you take a look at what privatizing Fannie Mae might do to the mortgage market?

One concern I have is that without the explicit government guarantee to cover a mortgage default, the US could pretty much kiss a reasonable 30 year fixed rate mortgage goodbye.

The US government should have never ever purchased, guaranteed, or insured mortgages. It has taken all the risks of these risky 30-year mortgages, which contributed to the inflation of the housing market. Then the Fed stepped in with its MBS purchases in 2009 and made the whole thing worse. I cannot wait for mortgage insurance and securitization to be entirely privatized, and get the government out of it.

The only problem I have with the privatization scenario is the problem of bailouts. If mortgages blow up again, there is a chance the government/Fed will step in again and bailout those investors, thereby continuing the process of privatizing the gains (during the good years) and socializing the losses when it blows up.

FNMA stock up 600% since Nov 5.. good for investors. May go up a lot more.

Privatization means more lender risk, therefore higher interest rates.

Mortgage borrowers will need to compete for capital against other borrowers.

Initially volatile marketplace likely.

Home prices likely adjust downward.

In theory taxpayer off the hook (but we have seen this story before).

Agree?

Any privatization would impact only new mortgages and new MBS, not the existing ones that are already guaranteed by the government.

There is nothing to say that the government guarantee of existing mortgages will not be removed by privatization. We will have to see.

What do you think the odds are that the administration and friends loaded up on that stock prior to the announcement?

Privatizing gains and socializing losses. USSA. But its ok because we are the greatest flawless nation in the world.

“Historically, the political left has seen oligarchy as an outcome of unfettered private markets, while the political right has seen it as an outcome of an unfettered state. In truth, however, the defining feature of oligarchy is not the balance between the market and the state. Its defining feature is the highly unequal distribution of wealth and power. If purchasing power and political power are concentrated in the hands of a few, it doesn’t matter whether we have a “free-market” economy or a state-run economy: the result will be unhappy outcomes for most of the people and for the planet, too.”

MEGA oligarchy is becoming ridiculously obvious, it has NOTHING to do with capitalism or study/discussion thereof, it is obvious, and I wish I had the verbal ability to write the above, and to to dispense with this “state/private” bickering that may have ONCE meant something and been worth studying.

Well said! 👏🏼

Excellent as always Wolf. Contrasting with Canada it’s almost the opposite probably in most of those categories and especially probably soon on foreclosures/powers of sale if prices go down anymore.

So much for the crashing real estate theory folks who missed the 10 year bull market have been pushing.

Lower, yes. Crash, no.

ahh, yes, so judgmental of people who were 14 years old or in the military stationed overseas when this “bull market” was taking place.

Ah, yes, the “bull market” of the Fed printing $2.8 trillion to directly buy mortgage loan products, which by itself can almost fully explain the ballooning of prices.

yes. i’ve seen his other comments. cccb is the type that got lucky for being in the right place at the right time and thinks he’s brilliant. you see that also with people who bought s&p indexes throughout the 80s and 90s and now think they’re brilliant.

Whereas most everyone else’s money here (besides CCCB’s) was “hard earned”…..as the common saying goes…..

A most excellent comment, Franz G…….I didn’t learn anything, but excellent, nonetheless.

I just wish I had your skill set.

10 years? Try 40 – Basically since rates started declining in the 80s.

Some of us just never realized what a huge government assistance program real estate would turn out to be.

In the first crash, I understood the banking laws and the problems with the mortgage is the world and I had been calling that one – I initially made some good money with a real estate shorting index. Then the government came in, changed all the banking rules, and I got out at about breakeven…

Also didn’t occurr to me that they would force interest rates lower for such a long time. Silly me, I didn’t realize it was one big government handout to people that had real estate investments.

There have been a lot of other factors (airbnb, fer instance), but it’s ironic to me that some of the people who are most against government handouts are often some of the biggest recipients in a lot of instances.

Whatever, this may not even have been what you were talking about, but I’m making spaghetti and I had a few minutes to kill…. :-)

“ some of the people who are most against government handouts are often some of the biggest recipients in a lot of instances.”

Nobody is against the hand out, once it’s “in-hand.”

The HNW and corporate types that receive them don’t consider them handouts, but rather their “earned partnership” with the government, for putting their capital “at risk.”

Whether it is a favorable monetary policy, tax break, credit or whatever they call it, the individual/ organization that gains an advantage is considered “smart” and “contributing” by the system and therefore has earned it.

Contrast that with a veteran who has their mental health destroyed by the ravages of military service or war? They were weak, and they already have a host of “handouts” waiting for them at the VA et al.

Similar analogies exist for other impoverished, sick or just plain “unsuccessful” folk who were sold on the idea of “hard work.”

In some cities you could ague there has been an actual crash, e.g. Florida, where you can find condos listed for less than what they were worth 10 years ago.

With the purges taking place in the Federal government employment, I could see Northern Virginia real estate taking a big hit price wise as many leave the area for other employment. Thoughts?

It’s incredible to see the Seriously Delinquent mortgage chart. Smooth sailing in 2006 then bam a steep increase in 2007-2010.

Helloc interest rates are not deductable unless the proceeds are used for home improvement. Hellocs are like a second trust without the benefits.

Standard deduction on taxes is so high now that only about 10% of taxpayers are doing itemized deductions schedule A… so deductibility is not important to most people..

What happened to the cares act forebearance? Was that all wiped out or still carried on the mortgages?

Of all the Fannie and Freddie mortgages, only 0.5% are in forbearance, most of them due to natural disasters and other temporary reasons. The Covid forbearance is nearly gone.

Most of the mortgages in Covid forbearance were modified and payments resumed or payments resumed without mortgage modification. In a small number of instances, the people sold the home, paid off the mortgages, and walked away with some cash. There is only a minuscule number of mortgages still in Covid forbearance problems (blue in the chart).

The number of mortgages in natural disaster forbearance has surged with the hurricanes in the 2024. The Los Angeles fire forbearance figures are not yet shown, but they will show up too over the next few months. Other temporary hardship forbearance is shown in gray.

The chart (via Mortgage Bankers Association) shows the percentage share among the 0.5% of Fannie and Freddie mortgages in forbearance.

I think you’re asking what happened to the balances that weren’t paid during forbearance. They were not wiped out. When a borrower exits COVID-19 forbearance, the unpaid principal and interest is packaged up into a secondary loan. It accrues no interest and requires no payments until the primary mortgage is paid off, at which point the entire thing is due at once.

In addition to selling the house as Wolf mentioned, some people refinanced. I believe this forbearance program was only available to borrowers with FHA/VA/USDA loans, which usually (always?) carry mortgage insurance payments that can only be removed by refinancing. The rise in prices would have given these borrowers enough equity to do that, and with the rock bottom interest rates, it was a no-brainer IF you could take advantage.

Wolf, you pointed out one of the key factors helping mortgage burden for millions: The inflation impulse from COVID has raised (and continues to raise albeit more slowly) wages and salaries while their debt has remained fixed. This one factor is the primary reason why inflation is so important in debt financed economies. Unfortunately, folks on the lower income spectrum aren’t owners anyway, and the inflation hurts them in an opposite way; rent goes up and their small wage increases barely help. All of this additional income has helped shore up discretionary spending in the economy too.

DM: Washington DC housing market crashes as DOGE lays off thousands of federal workers and bureaucrats bail out of ‘swamp’

Home prices in Washington, DC, have plummeted since the Trump administration and the Department of Government Efficiency began discussing layoffs. Since Donald Trump took office, Elon Musk’s Department of Government Efficiency (DOGE) has fired thousands of federal workers in a push to reduce spending. In the wake of those layoffs, droves of former federal employees have packed up their bags and put their homes on the market, causing the average listing price to sink, The Kobeissi Letter (TKL) reported. In November, the median home in the nation’s capital was worth $699,000, according to Redfin. By February, the median home value dropped 20 percent, bringing the price down to $560,000.

i’m not overly surprised. d.c. is a transient town, in that a lot of people move there solely for their government jobs. if they no longer have those jobs, a lot of them have no reason to stick around and will move elsewhere.

Those houses were overpriced and due for a correction.

All interesting thoughts here…one data point I’d like to hear thoughts on impact to homes sales market is renting. Since financial crisis, mid 2000’s, rental vacancies have plummeted as people moved from owning to renting…..ripple effects have continued as more people have come of age where they wanted to step up from renting to buying….market supply to buy was already low going into covid, rental vacancies was also low….covid supercharged those numbers lower as there was a massive surge of people choosing to move, despite financial costs…

Seems to me, any conversation about where homeownership is currently, and where it’s going, should benefit from looking at apartment rental vacancies….and average rent versus mortgage payment…

I’m in Vermont where we have the highest percentage increase, nationally, of home prices going up, in part due to our limited construction season, higher average cost to build, as well as limited land to build on and higher costs all around due to climate (energy, insulation, etc).

Due to fires in California and hurricanes in east, building materials will continue to rise. My guess is labor expense will continue to rise as the pressure relief valve for the labor market (construction workers from outside of US will diminish substantially under current political administration.

I’m a realtor and I’m seeing lots of first time home buyers who aren’t happy about interest rates but are doing the math and are seeing homeownership as a better financial decision than paying crazy rent for a less than desirable apt…to them, a 6-7 % interest rate isn’t harder to swallow than the crazy rent with annual, significant increases…these buyers have never had the benefit of a 3-4 % interest rate so they don’t have that psychological hurdle….they are looking at high rent costs with no equity being built…and wanting to move on with there lives….another strong motivator I have noted from many covid and post-covid buyers….we all lost a year or two of moving forward in our lives and are ready to get back moving forward….financial costs are less of a decision making data point to them, or , it’s different than a current homeowner….high rent, low rental vacancy (choice) is a motivating factor for buyers….like others have said, the underlying support for continued activity in home sales, despite all of these high living expenses prices, is a strong jobs market….keeping an eye on that amongst the many white collar jobs going away in news….as well as significant government, and government supports (through programs being doge-d)….interesting times indeed.

My best case scenario is a slow, steady unwinding of housing expense for owners and renters….high hopes but hedging my best….

Good luck all..

What are you talking about? It’s down 8.6% year over year. I just got that straight from Redfin. Stop “spreading b.s.” as WR likes to say.

$699,000 – $560.000 = Down $121, 000 which is 19.8% not 8.6% and that number is from November 2024 until February 2025.

I’m not sure what numbers the article was referring to. I cannot get any of these numbers on Redfin. I get different numbers.

However here is a chart with data from Realtor.com about the listing price you mentioned. You can see that it has been going down for years. But on a per-square-food basis, it actually ticked up in January, while per-home it fell, which points at a shift in the mix in January.

Anyway, not looking rosy here over the past few years but I don’t see a crash in January yet.

DC is on my list of the cities with the biggest price drops. So here are the sold prices, down 9% from the peak in 2022.

https://wolfstreet.com/2025/01/19/the-big-cities-with-the-biggest-price-declines-of-single-family-houses-or-condos-from-their-peaks-from-9-to-21/

Howdy Prisoners. Another great LoneWolf article how to un cuff yourself. Now lets say you still plan on keeping your job and spouse and house? Rental property is a great way to build wealth. HELOC that 2 % mortgaged home and build real estate wealth. Become an entrepreneur and make your dreams come true. Too scared? Bet the youngins are…..

Rental property is a great way to build wealth as long as you’re not buying at peak bubble prices.

Personally, I’ve chosen income-based funds which avg 10% yoy return, and require absolutely zero work to maintain, unlike being a landlord and dealing with tenants.

I think timing can be pretty tricky in those high income funds. The assortment of CEFs and mREITs I have are all down because in hindsight, I bought when they were pretty high/rates were artificially low, so it was a lesson for me. Not that I think it’s a good time to be a landlord.

Personally I’m not touching anything that says REIT with a 50 foot pole.

I have mostly specialty credit funds – think sr. secured loans, BDCs, things like that. A couple covered call funds and one microcap oil producer that pays 15-25% in dividends annually.

A couple funds did go down in NAV as rates went up, but overall I held up well.

Right now, my estimated interest/dividend income for 2025 is about 11% of the portfolio’s starting balance for the year.

From a housing standpoint the USA is largely in a solid place. The metrics shown above are quite promising. The other benefit most don’t discuss, is that house prices have largely either stagnated or declined since 2022, making cash based affordability better, and similar to bonds, bringing the prices more in line with rates. Wages have continued to rise since the price stagnation/decline, further increasing affordability.