More people, more workers, more income, more debt.

By Wolf Richter for WOLF STREET.

The summary could go something like this in terms of the past three years: More workers (employment +7.79 million, or +5.0%, BLS data), earning more money (average hourly earnings +13.4%), boosted total disposable income (+20%, BEA data). And over these three years, these workers added to their debts but at a slower pace (+13.8%) than their income grew (+20%). So the overall burden of their debts in terms of their income declined even further. This is not to say that subprime – a small subset that is always in trouble, which is why it’s called “subprime” – isn’t, as always, in trouble.

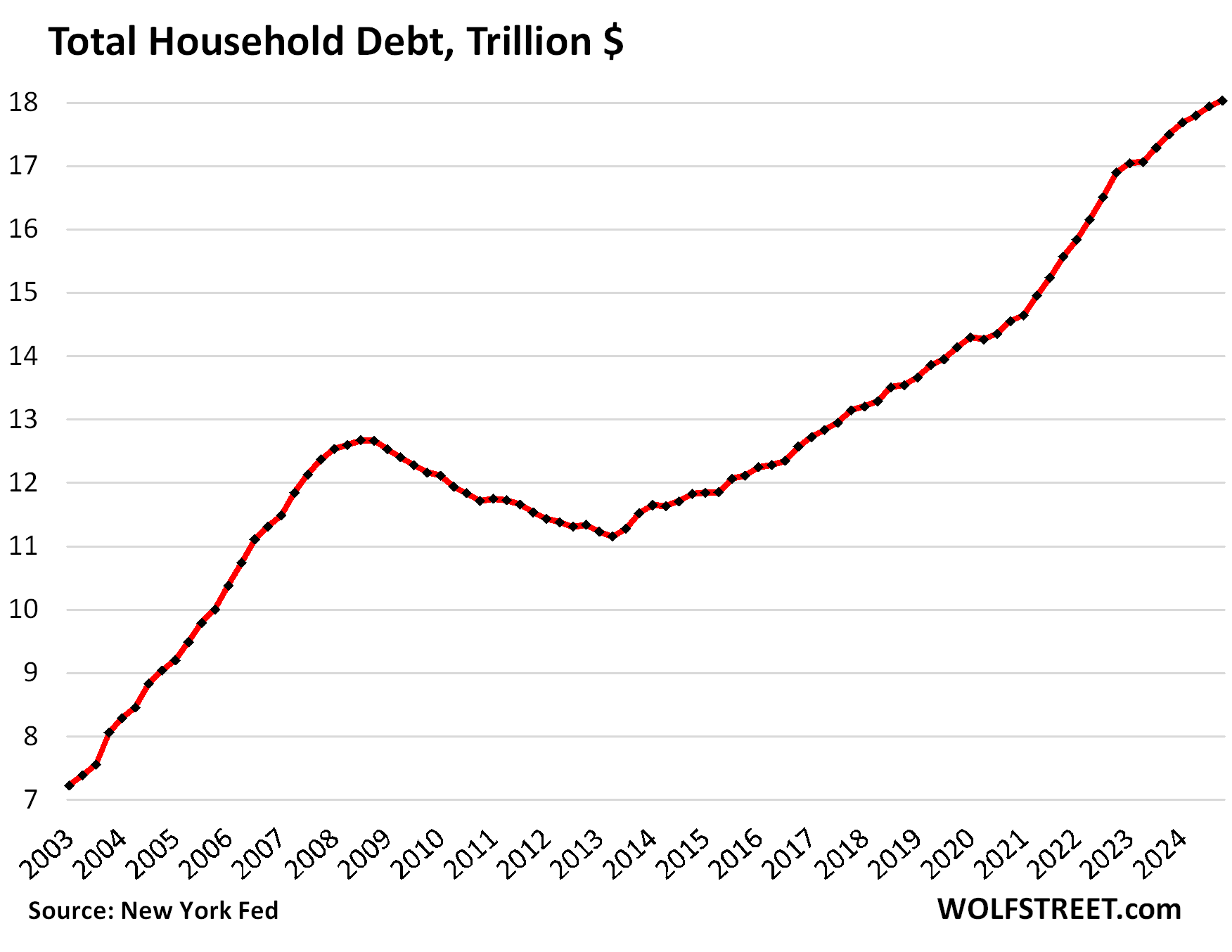

Total household debt outstanding inched up by $93 billion in Q4, or by 0.5%, from Q3, to $18.0 trillion, according to the Household Debt and Credit Report from the New York Fed today. Year-over-year, total household debt grew by 3.0%:

Each category of household debt – mortgages, HELOCs, auto loans, credit cards, other revolving credit (including BNPL), and student loans – increased in Q4, some of it barely. We’ll get into the weeds of each category in separate articles over the next few days. Today, we look at the overall debt, its burden, delinquencies, collections, foreclosures, and bankruptcies.

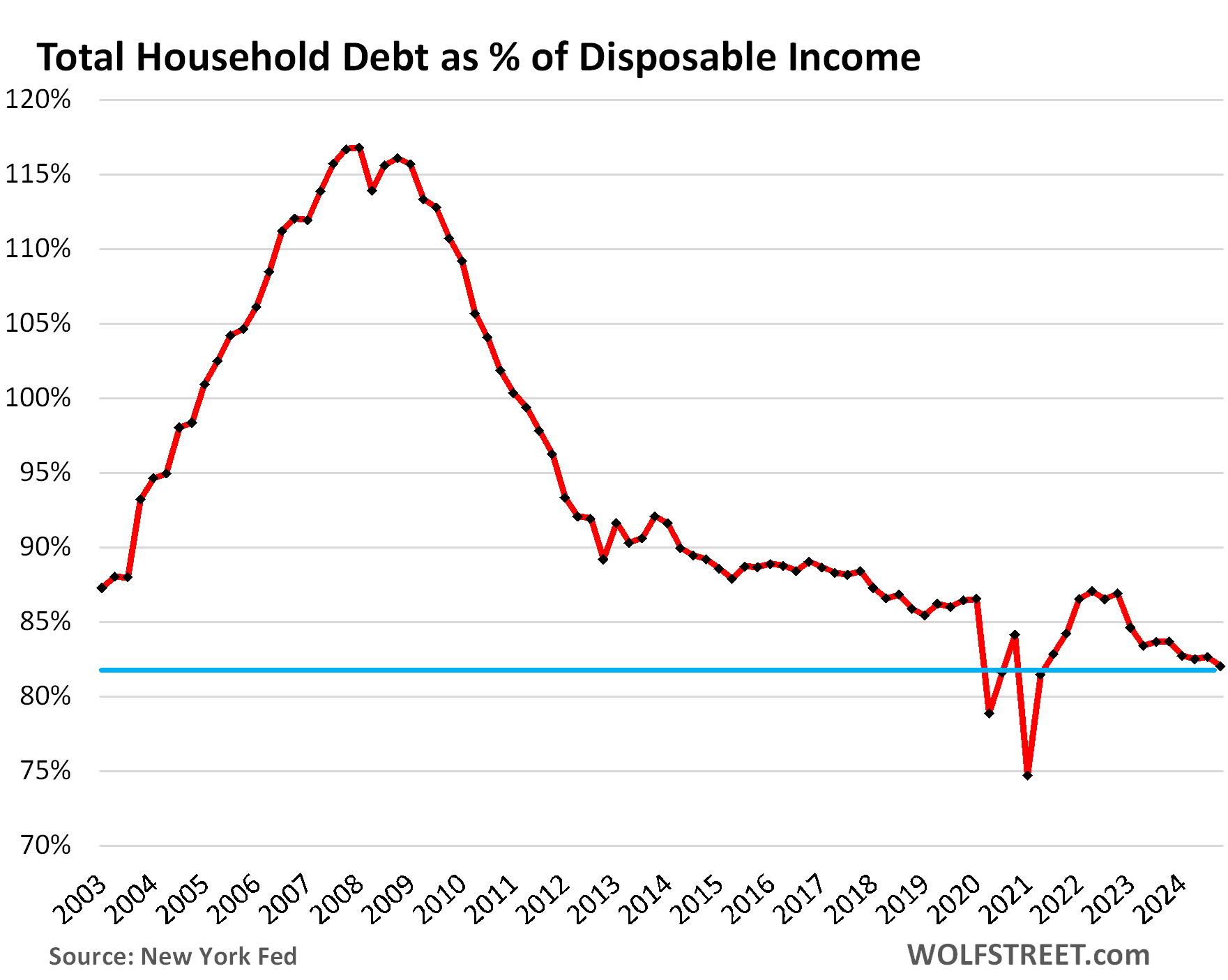

The burden of household debt: Debt-to-income ratio.

To view the overall burden of debt on households, while accounting for more workers and higher incomes, we use the debt-to-disposable-income ratio.

Disposable income, released by the Bureau of Economic Analysis, is household income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. This is essentially the cash that consumers have available to spend on housing, food, toys, debt payments, etc. And what they don’t spend, they save.

- From Q3 to Q4, disposable income +1.3%, total debts +0.5%.

- Year-over-year, disposable income +5.1%, total debts +3.0%.

So quarter-over-quarter and year-over-year, disposable income rose at a faster pace than household debts, and the burden of the debt on households declined further. We wish that were true for the federal government’s finances.

The resulting debt-to-income ratio of 82.0% in Q4 was the lowest ratio in the data going back to 2003, except for a few quarters during the free-money-stimulus era that had briefly inflated disposable income beyond recognition.

So the aggregate balance sheet of consumers is in good shape. The heavily leveraged economic entities in the US are the federal government and businesses, not consumers. This balance-sheet strength of consumers — 65% own their own homes, over 60% hold equities, and their debt burden is relatively low — explains in part why consumer spending has been so strong, despite the higher interest rates.

This wasn’t always so. In the early 2000s, households piled on huge debts in relationship to their incomes, and their debt-to-disposable-income ratio spiked in five years from 88% in 2003 to 117% in 2007. That this wasn’t going to work out should have been clear. And it didn’t work out, and it contributed to blowing up the financial system that had provided this debt.

But our Drunken Sailors, as we lovingly and facetiously have come to call them, have learned a lesson and have become a sober bunch, most of them, not all.

Free-Money is over.

Subprime means bad credit, not low income. A small subset of our Drunken Sailors has subprime credit scores because they’ve been behind with their payments, have defaulted on their debts and other obligations, etc. But low-income people cannot borrow at all or only very little. It’s the people with higher incomes that have access to lots of credit that get into it over their heads and fall behind. People with good incomes early on in their careers fall into this trap easily, and eventually get out of it again.

Subprime isn’t a permanent condition, but a phase that consumers move into and out of: Some people get into trouble, and fall behind on their payments, and their credit scores drop to subprime, while others are curing their credit problems and are working their way out of a subprime credit rating. It’s in constant flux.

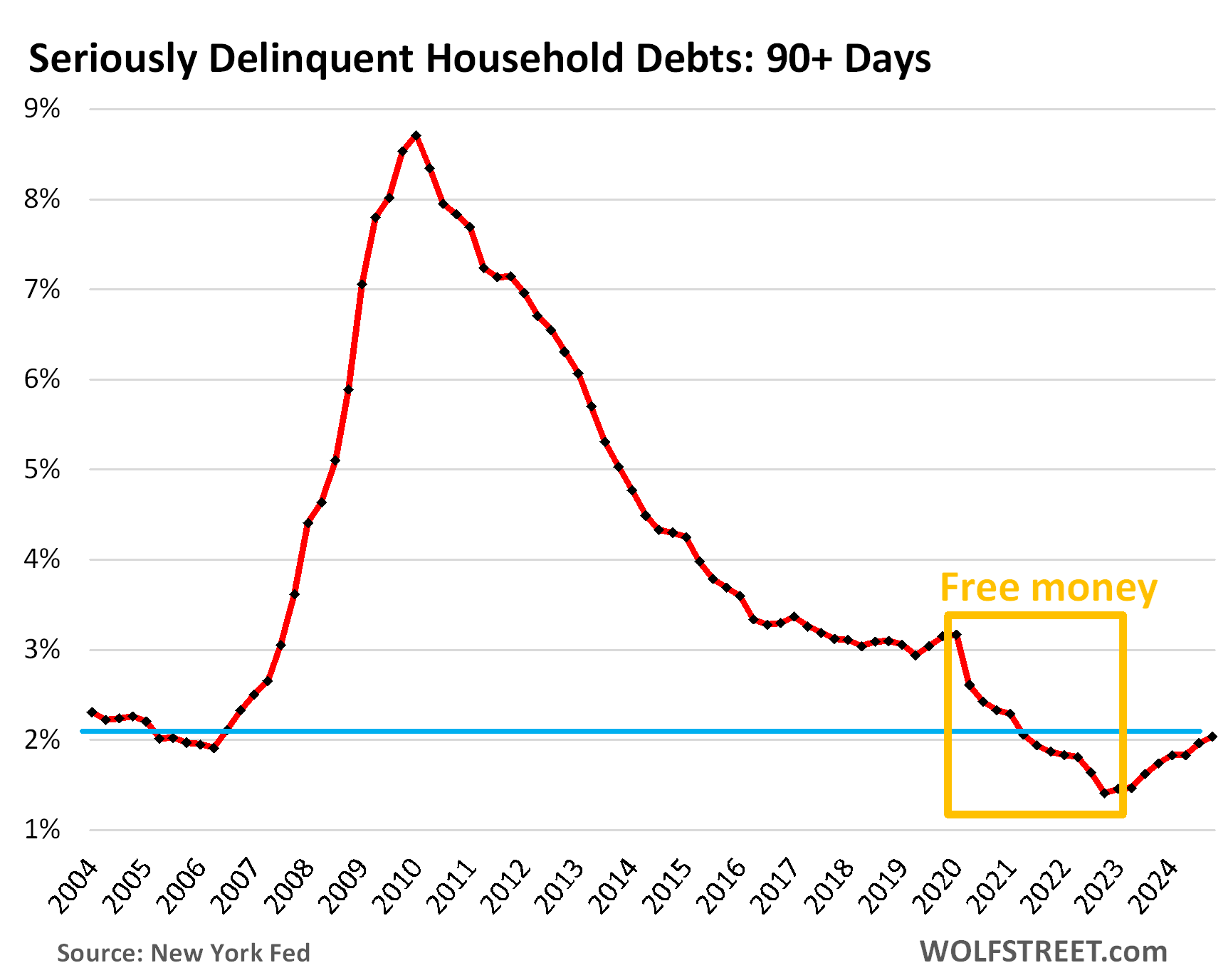

Serious delinquencies after Free-Money: Household debts that were 90 days or more delinquent by the end of Q4 inched up to 2.0%. Beyond the Free-Money era (gold box), we have to look back nearly 20 years to see a similarly low rate.

In the Good Times of 2018-2019, before Free-Money, the serious delinquency rate was about 3%.

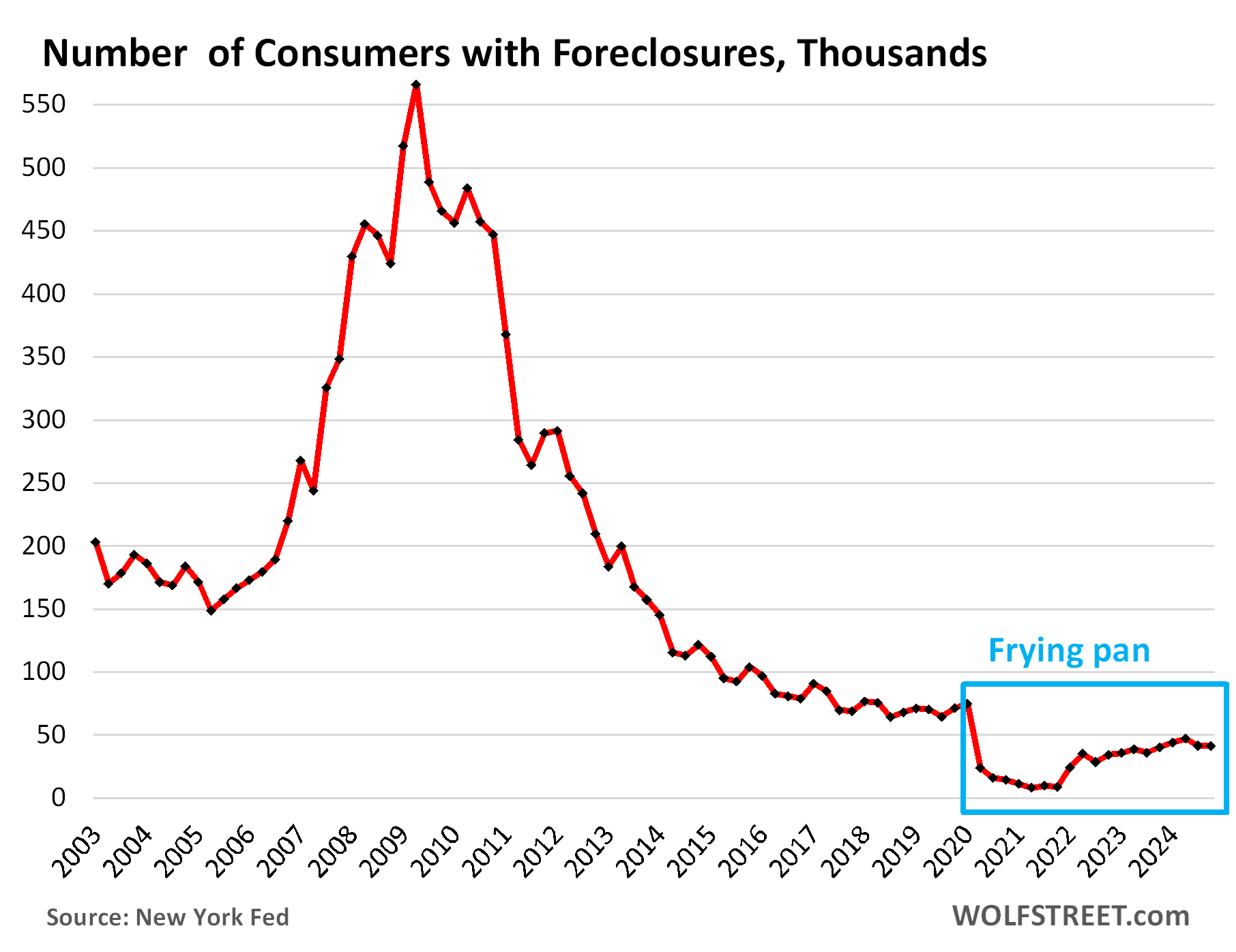

The foreclosures frying-pan pattern. The number of consumers with foreclosures in Q4 dipped to 41,220, the second months in a row of declines and at ultra-low levels, compared to 65,000 to 90,000 in the Good Times of 2018-2019.

During the Free-Money era, which included government-sponsored mortgage-forbearance programs under which foreclosures were essentially impossible, the number of foreclosures fell to near zero.

What is keeping foreclosures so low currently is that, after years of ballooning home prices, most strung-out homeowners can sell their home for more than they owe on it, pay off the mortgage, and walk away with some cash, and their credit intact.

It’s only when home prices spiral down for years that foreclosures can become a problem, if it coincides with big job losses.

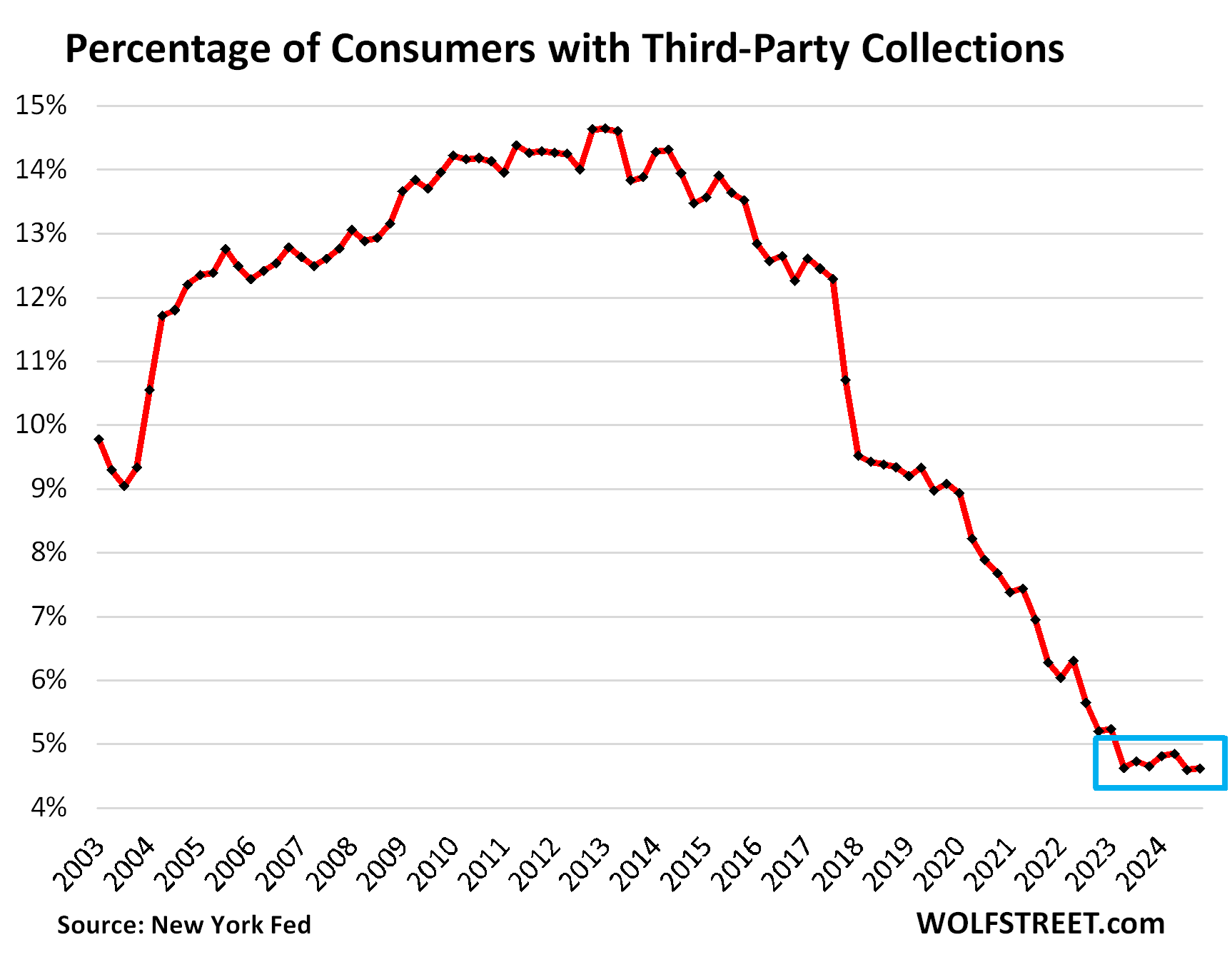

Third-party collections still at rock bottom. A third-party collection entry is made into a consumer’s credit history when the lender reports to the credit bureaus, such as Equifax, that it sold the delinquent loan (for cents on the dollar) to a collection agency. The New York Fed obtained this data on third-party collections in anonymized form through its partnership with Equifax.

The percentage of consumers with third-party collections has been at the record low level of around 4.6% for nearly two years:

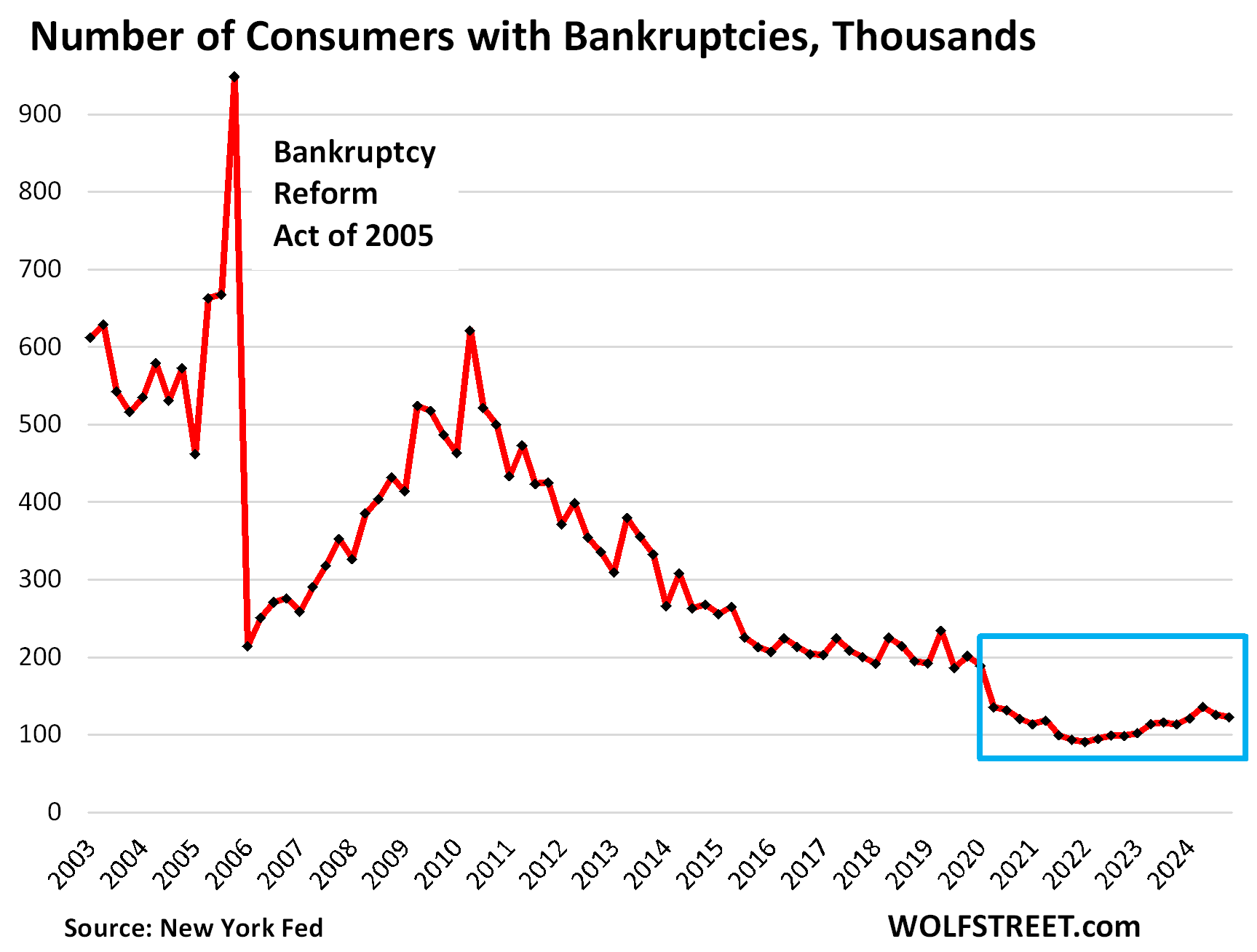

The consumer bankruptcies frying-pan pattern. The number of consumers with bankruptcy filings dipped to 122,660 in Q4, the second quarter in a row of declines, and lower than any time before Free-Money. During the Good Times before the pandemic, the number of consumers with bankruptcy filings ranged from 186,000 to 234,000, which had also been historically low.

An odd-looking frying-pan pattern with a short handle.

We’re going to get into the weeds of housing debt, credit card debt, and auto debt in separate articles over the next few days. Next one up is housing debt. So stay tuned.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So despite $10 per dozen eggs (and rising), $100k pickup trucks, and $500k shacks on grass, consumers are doing gangbusters. Let the good times roll!

Can’t wait to see how wild the party gets when we reach $20 eggs, $250k pickup trucks, and $2 million shacks on grass.

In terms of eggs, that’s the effect of the avian flu that’s causing chicken flocks to get wiped out across the country. So there’s now a huge shortage of eggs. When the avian flu is over, egg production will begin to soar, and prices will collapse. We went through this before, periodically. This happens every few years.

Side 1: Quick, shut down the barbershops. If a chicken gets a haircut we’ll all be infected overnight!

Side 2: Nonsense. Let them develop natural immunity by gathering on the beaches. They can always drink an Ajax solution for extra protection.

Side 3: Buy more Birdcoin!

Side 4: Cancel my agricultural college loans!

Side 5: Where’s my egg stimulus money?

I would think if they would just mask & booster

it would be a happy hen house.

The corner stone, “Total household debt outstanding” seems to be in good shape as you demonstrated in your narrative and presentation of figure 5.

America’s wealth has always been opportunity of the good life for the median bloke. The young people are tired of waiting for the prices to fall from their preposterous asking price to a more realistic selling price.

Wolf after being off the website for awhile and not reading comments, I consume other forms of information. Just to see other stuff. It’s all the same garbage. You are showing the math and data, the arguments that you get dragged into is time consuming. $20 per dozen, it will happen not at this time. It can happen with another outbreak, but not through dumb reasons. Last time I checked the world is not ending and these people that say stupid sh!+ are delusional. I was reading the data prior to all the fixes and the oppsies, it looked bad. I was really thinking recession, even everything was indicating recession. It was technical by definition a recession, Gov said not a recession so all good. I don’t believe it still, but real jobs not exactly crap jobs are still hiring. Cheers with a mug of brew, but tell them to show you the data and math.

I bought two dozen of eggs this week for 3.50 a dozen. It matters where you shop .

Does life really go totally to hell without eating eggs? The pain of this part of a lifestyle reduction must be agonizing.

Ts and Ps for those going thru it.

I haven’t ate an egg since I was two years old. I hate the taste of eggs.

Basic capitalism 101. Astounds me that people can even begin to believe or wants a president to control prices. Especially the side which screams Communists are hiding everywhere wanting some sort of, hmmm, central committee?, to set prices.

…as the supply/demand prices of things are

merely symptomatic of our too-slow/unwitting/relentless understandings/neglects/poisonings of our spacecraft’s overall maintenance functions and stores production capabilities…

may we all find a better day.

Silly Sacks,

$35 Trillion and Freidman will tell you otherwise.

Since you have no idea what communism is, that’s how you think.

The American people are tired of the old presidents.

Obama’s father was a proud Socialist, you have no idea what that is.

Do us all a favor and figure out what that is. The idea is an illusion and it all turns into a dictatorship.

There will never be a socialist utopia, once you realize that you can free your time on more productive means and do well for yourself. Good luck

Firing millions of public workers – they’re just starting with federal workers, but it will work its way down to states and localities – should be great for real estate and overall demand, as well.

The Overclass, via entities like PE, have been stripping private aggregate wealth for decades; now it’s time to strip the State.

…well, when our nicely-suited financial/business managements have exhausted any pretense of conducting genuinely-productive/profitable operations, the new clothing budgets will have to be borne by someone else…

may we all find a better day.

As a renter, this article makes me want to move to another country. I’ll be dead before the collapse comes.

SOL, I hope your crystal ball shows a truer picture than mine. I’m seeing the collapse as coming by this time in 2026.

There is no collapse coming. The working people desperately need deflation – an actual drop in prices across the board – but this would be devastating for wealthy asset holders who control the politicians and government, so this will never, ever be allowed. The notion of a collapse is particularly laughable when you consider the current president and his obsession with the stock market.

We have been shown the path. It is money printing. They have chosen to steal the value of labor by destroying the US dollar and every other currency in the world in order to artificially manufacture not only a floor under asset prices, but an ever higher ceiling.

The greed of the billionaires knows no bounds. They will push until they have taken everything way too far, and then it is too late. Their rapacious greed will be their downfall. Prepare for more inflation, measured in perhaps decades, not years. We are in uncharted territory, and it is global.

If people only buy want they need and not what they want prices will come down.

Rick,

In general, I agree but with the post-2020 housing inflation (the primary driver of overall inflation because it is – by far – the largest component of the total HH expenditure bucket) I think there are multiple factors at work – and it is not all McMorons lusting after McMansions (this time…).

The G encouraged pretty-close-to-unprecedented levels of illegal immigration (how many millions revised upward are we this week?) at the same time multiple factors (many pretty illegitimate – political zoning restrictions, possible landlord collusion via RealPage, etc.) were reining in housing supply well below what it might otherwise have been.

(I know the housing supply was soaring for a while…but it is slowing down a lot now…and it could have soared a lot more earlier…you don’t get 25% rent hikes in 1-2 years unless something is interfering with the supply response.).

Supply and demand *are* adjusting but slowly. And a lot of misery has been inflicted upon third parties thanks to the agendas of others.

So Depth Charge, regarding the stock market, are you all in? You make arguments that the Fed will always bail out the stock market and Trump is obsessed with the stock market. If I believed all that, I would be 100% invested in equities.

Do you realize how devastating deflation is? It was deflation, not inflation, that contributed to the depression.

Rural America will never get it. Yes, your cost of living is lower. But that’s because your poverty rate is 30% and unemployment rate is 9%. When a population has less money to spend, things cost less: But most of the time the poverty-stricken people there can’t even afford the lower cost items anyway.

Low unemployment, higher wages = higher prices

High unemployment, lower wages = lower prices

Prices would not be what they are if the average American couldn’t afford to pay these prices. When demand drops, they lower prices. In four years, they haven’t. They keep going up – because Americans can, and are paying these prices.

Good lord, and this is why we’re all screwed. Rural America voted in someone who virtually handed them a recipe for a depression, and they were like, “Sounds great!”

Mass deportation (leveling the farming industry and causing American layoffs as well), tariffs, huge budget cuts, deregulation, more unemployment = recession or depression

In the last 36 years, there have been 4 republican terms. All 4 terms ushered in a recession. This is why. These bumpkins do not understand a developed economy. In undeveloped economies, prices are low but wages are also so low you can’t afford what they’re selling. Russia and Afghanistan are undeveloped. They have very low prices. Would you want to live there? In more developed economies, there will always be a low bottom… but everyone else is doing fine.

@Wbrab,

The business cycle doesn’t have a whole lot to do with which party holds the Presidency at any given moment. There are 3 branches of the Federal government, and the Federal Reserve policies have more bearing than any other single factor on the short term economic outcome. It’s pretty hard for a recession to occur, for example, when the Fed floods the economy with Trillions of dollars, as it did from 2009 to 2021 ish intermittently. The real question is what happens when QT is wound back and there is another shock. Will they start up QE again? This is orders of magnitude more important economically than which party holds the Presidency.

There are lots of interesting statistics as to which cities are a better buy, rent v. own.

Maybe Wolf can address this.

We sold the house and moved overseas. Trump will crash the economy, again.

You must still receive your NY Times, WaPost or, is it The Guardian ! lol

Ever heard the saying “you are too close to the (big) picture”

Breathe, Think, take a time out and you will find that you screwed yourselves.

Remember Enter the Dragon?

Hans to Saxon “you will reach a point of NO return “

Good luck to you in a society that is monstrously divided.

WaPost is owned by Bezos. Yes, the Guardian is independent. You must consume the alternative: Fox State Media! lol

Europe is splitting in half as well, if you’ve been following national elections there.

What the Orville Redenbacher guy said in 1980.

What the Guy With The Big Ears and Funny Voicesaid in 1992 and 1996.

He also knew a bit about computers/data, too. Prob like –

How many duplicate numbers?

How many 000-00-0000 ?

How many no numbers?

How many y’all over 100 years old so I can personally deliver a birthday card?

The y = e to the x power hockey stick curve had gone way up the shaft by this time.

What do you mean “again”? There was a very brief downturn in stocks during the pandemic, but no economic crash from 2016-2020. The last 4 years also no “crash”, just above average inflation and a strong economy. I don’t think either President had much to do with any of that. The Fed sure did though, if they hadn’t gone nuts with unnecessary QE in 2021, we would probably have had very little inflation. The Fed probably did more to influence the 2024 election than anyone else by stoking inflation that made be voters look for an alternative, although I am sure this wasn’t their intention with the QE.

That is always an option. There are plenty of countries with a higher quality of life than this one.

It’s stunning how cheap it is to live in smaller cities in countries like Italy and Brazil. You barely need any money at all. I was just looking at rents in Chicago and couldn’t believe my eyes, it’s almost as expensive as California now

You money doubles about every 5 years in Brazil as long as the currency stays stable.

My son lives in Chicago, it’s way less expensive than comparable cities in CA, like 40% at least for comparable neighborhoods.

It depends on where in California. Fresno? San Francisco? San Diego? San Bernardino? Huge differences in rents.

The problem with the countries you mention is finding a job. It’s great to have made your money in the US and then move somewhere cheap. Living there the whole time, not so much.

Oh yeah, thankfully I put a new roof on and painted the house before our loss with the deportation policy.

I live almost in Mexico and have the most pleasant feelings towards my neighbors.

At the same time, the romance of Mexico has been defiled by their complicity with the cartels.

There are a number of asset bubbles that are inflated when compared to historic measurements. No one knows how the obvious incongruity will resolve itself.

Great stats Wolf…the media presents a very contrary view. But,at least to this point your overwhelming data settles the qwuestion..for now. Let’s not forget though,we have a 2.5 trillion a year shimmy out there providing a floor for this superstructure. And,the wind has shifted.

This data helps illustrate why the US continues to be a destination country…

Super off topic but if Trump goes with reciprocal tariffs and it escalates into a full blown trade war then how is that good for anyone? Obviously would have to look at specifics but seems like that could have significant ripple affect and drive inflation up further. Other countries may choose to just do business elsewhere which hardly is good for the jobs picture. Obviously this could be an attempt by the administration to negotiate tariffs with countries but my experience is much of the world, or the West anyway, already finds the US a necessary but difficult ally.

Well evidently our drunken sailors are cruising around just fine!

Looking forward to your upcoming piece on housing debt. There has been a huge wave of seller financing deals since rates went up. The wholesalers and seller finance investors have way more technology to enable their crafts than ever before. They wrap the mortgages and rescue homeowners with notices of default, or they offer to buy the homes and then assign the the contracts to real estate investors. The seller finance investors catch them up on their past due payments, and they never reach foreclosure. The wholesalers sell them “off market” to real estate investors. These types of seller finance deals and off market wholesale deals are not tracked anywhere. I wonder how many pre-foreclosures are rescued by seller finance deals, or by wholesalers, and thus never go to foreclosure? This may be a comment for the upcoming piece on housing debt, not relevant here.

“These types of seller finance deals and off market wholesale deals are not tracked anywhere.”

That’s not correct. All real estate transactions, after they close, are entered into the public records (taxes) and are tracked by the likes of Zillow, the credit bureaus, such as Equifax on whose data the housing debt article is based, and others.

All mortgages, first-lien and second-lien loans, and HELOCs are tracked in a variety of ways, including by the credit bureaus such as Experian.

What is not tracked in terms of off-market is the off-market for-sale inventory. But that’s not even part of the discussion of housing debt.

All closed transactions and all secured housing debt is tracked and part of the data.

Wolf, a typical seller-financed mortgage involves the seller negotiating a note under which the buyer must keep making payments to the seller or the seller will foreclose and take the property back. While many of these deals will be recorded, they never touch a bank and don’t run credit, and they may not even be reported to the MLS. In some instances, they may not even involve public recording of the transaction details until after the mortgage is satisfied. This might happen depending on state law or local practice, but it would be especially motivated in “wraparound” transactions where sellers are keeping their old mortgage with a due-on-sale clause, making payments on that, and then carrying additional debt from the new buyer. Some of these deals are scheduled to run for a long time, although many also have balloon payments 5-10 years after closing.

Something tells me the outstanding debt from a seller-financed mortgage won’t show up in credit bureau data, although if it’s structured as a wraparound, the seller’s existing mortgage will continue to show up in the statistics. And while sale transactions that are publicly recorded may show up in sales data, it generally won’t reflect the ongoing mortgage payments.

I personally believe seller-financed mortgages are a tiny fraction of overall housing transactions, but it seems entirely plausible that they won’t be reflected properly in the data. I’m not sure you’ve really sat down and thought that out, Wolf.

NOTE: this data from Equifax/NY Fed, including for the housing-debt article to come, has nothing to do with the MLS. This is public records and credit reporting data.

Any housing debt that is secured by the property — lien on the property! — shows up in the figures. That’s what a lien does. Period!

Seller financed mortgages mean that there is a recorded property sale (public records and tax records) and a recorded lien on the property for to give the seller right to the collateral if the buyer defaults. And that makes both the transaction and the loan part of the data, whether you like it or not.

If it’s just a signature loan, like mom lends the son $100k to buy a house, it does not show up in the data, but then the lender has zero collateral, it’s an unsecured loan, and the lender has to sue in case of default, and this cannot involve a foreclosure because the lender doesn’t have the right to get the property because the seller didn’t put a lien on the property!

So that may be ok for mom. But NO professional investor and no seller with a brain would lend unsecured funds on a property. So it’s just nonsense to claim that seller-financed debt doesn’t show up in the housing debt that Experian/NY Fed provide. You’re just making up stuff.

Same with all property transactions that have any legal validity: the property deeds are recorded and are part of the data. You’re just making up stuff again.

Robert Allen – No Money Down book about ~ 45 years ago. All that possible now, technically, but it’s a much “lower trust society” now. Prob work for close relationships. non-arms length transactions, sweetheart deals.

I’d have to check to see what shows up now on some transactions I know of a couple of years ago: print classified ad in paper, no realtor, no MLS, no loan. But as Wolf says, even that goes to county records.

Hello Wolf, You missed a very important factor when doing your analysis on the strength of the US consumer. The amount of debt vs the disposable income is not what gives strength or liquidity to the consumer. It is the cost of that debt that matters. I always think of economic models in their extreme to make them clearer. Take the same amount of debt at 2% interest and than at 20% interest. Those extremes will have a very different impact on the consumer. We have seen a real application of this over the past 5 years. Mortgage rates went from 5% in 2019 to 2.5% by the end of 2020. That helped to drive up home prices. The fact that they had not increased much for 10 years also helped. We are now in a very different environment. Mortgage rates are in the 7s and home prices increased significantly in the past 5 years. They have doubled or more in a lit of places. The cost to the consumer for a home in 2020 vs today has to take into account not only the selling price but the delta in interest rates, the increase in property taxes and the increased insurance costs. I was an economics major and have been writing mortgages for almost 40 years. I’m on the front line. I can tell you right now the consumer is getting squeezed. Even those with big incomes.

But no…

1. 30-year mortgages don’t change their interest rates during their 30-year term. So the people with their below-4% mortgages still have below 4% mortgages until they pay them off. That’s the majority of the debt. In 2022, 65% of mortgages had below-4% rates. Some of them have gotten paid off by now, including by people who now no longer have mortgage debts at all. Currently 55% of all mortgages are below-4% mortgages.

The 6%-plus mortgages whereof you speak only matter to the relatively small number of people who have those mortgages. Currently only 17% of all mortgages have 6%-plus rates, and even fewer have 7%-plus rates.

I covered this here, including charts:

https://wolfstreet.com/2025/01/20/locked-in-homeowners-nevertheless-pay-off-below-4-mortgages-and-their-share-of-all-mortgages-outstanding-drops-to-55-lowest-since-q1-2021/

2. Mortgage rates are now about back where they used to be at the left side of the chart. The 6-7% mortgage is nothing new. The below-4% 30-year fixed mortgage was a new phenomenon, and it didn’t last very long.

3. Debt to income ratio is a classic measure of the ability to deal with the burden of debt and of credit-worthiness, for example when you personally apply for a loan.

Personally I’m in a decent financial position, and that’s because I just don’t make huge purchases (aside from the house).

So I have tried my best to put myself in other voters shoes.. especially when so many quoted the “economic outlook” as their primary motivator to vote for the current administration

I’m sure some are struggling, but based on the data those people would be in the minority.

So where is their huge concern coming from, I know they aren’t worried about the US deficit (not on a personal level). Did people just forget what the world was like before the free money era?

The numbers tell the story of the average or median, consumer/ houshold.

Especially inflation is sumthing thats a very subjective experience as the official number is comprized of 80 000 items and their wheighting is subject to some debate.

It gives a consistend number thats compareable to the past.

It does not show how the bottem 20-50% experience inflation.

There is e.g. the “real living cost” calculated by the LISEP that tries to observe price changes in necessities.

It calculated the inflation experienced at 9.4% for “minimum adequat needs” for the year 2023 vs the CPI of 4.1%.

If you check out their website it has thei methodology and whitepaper, I found it interesting.

They see higher cost rises in medical, housing, and especially technology where the CPI uses hedonic adjustments to reduce the cost of accessing your email and buying a telephone but fails at adequatly pricing the costs of smartphones and streaming subscriptions.

They have similar numbers for childcare and food but lower for transportation as they use a lower yearly milage as “minimum adequat needs”

Those inflation numbers are important if one tries to understand how different people experience inflation and why so many people don’t seem to share the same experience in the best economy of all times.

The LISEP institute also has numbers for income and “functionally unemployed”.

If policiy is created based on the big CPI and other numbers but polici makers don’t understand how those numbers are calculated there will be a disconnect. Especially if the top income and bottom income percentiles drift further appart, numbers based on average or median don’t tell the whole story.

Very personal anecdote: I am also fairly well off and retired early. Not wealthy, but debt free with solid investments. My youngest sister has lived on disability for a decade as the result of a pretty horrific bout with breast cancer. My mother and stepfather live with her for two reasons: 1. to pay her rent and help her out and 2. because they sold the house they inherited to pay off my stepfather’s ridiculous debts and so he could buy a new Ford F-150 to be mobile when global cooling would drive northerners to invade Florida (where we live). I also have an old high-school buddy hanging on by the skin of his fingers, because he spent most of his life as a construction worker, spending any extra income on weed. Millions of folks are like this. And the economy is horrible. Because they are not where they thought they would be at this point in their lives, and someone else is to blame.

@Kent

I’m at the highest earning point in my career. If it was 2020 I’d own a nice house and be comfortable until retirement.

Instead housing prices doubled from 2020-2022 and it looks like I will never own a home. I did everything right. I stayed out of debt, saved lots of my income, and still can’t own a home because the gov’t and fed printed massive amounts of money and gave it away. I have multiple people that work for and make way less than me but own a nice place because they bought during the QE era.

And people may ask why I didn’t buy earlier. I was stationed overseas with the military. I came back to the states in 2022 and homes and inflation has made my return miserable.

The young people who work for me decided they’ll never own a home and gave up caring about saving money. The economy sucks for lots of people. Not everyone was just irresponsible and are looking for someone to blame. If you were under 30 then you’d think the world was against you.

All of the people I mentioned already own a mortgaged house and the economy still sucks for them. My 26 year old nephew just got a job as a cop making $42k per year here in Florida. That’s not enough to buy a house in this city. So he bought a quarter acre of land about 15 miles outside of town next to cattle pasture, and he’s building a small house. The total cost will be about $185k. With 20% down, he’s still financing too much IMHO, but the bank doesn’t care. Lots of people in expensive areas plan on renting their whole lives. It’s a choice to live in a super expensive area, or buy a house from a previous owner or developer.

I don’t mean to sound callous, but you know what else sucks? Stretching to buy a house for $850,000 and paying $50k/year for the mortgage, insurance and taxes. And then watch your “investment” fall to $500k over the next 5 years. That’s about to happen to millions of people to one degree or another, all by their choices.

kent, there is a segment of people who, rightly or wrongly, believe congress and the fed will step in before that $850k can get anywhere near $500k.

that is what is keeping assets levitating, the belief that the fed will bail them out. after the past 15 years, it’s not an awful assumption.

Hey Young People,

Relax and don’t drink the kool-aid. Keep doing what you are doing and always put money away. You can never afford to buy a home “where you live”. One day, maybe decades from now. You can pack your sh×t and move just about anywhere in flyover country and buy a home. There are plenty of cheap homes, go to realtor.com and search any state for 200k or less. You will be amazed at what lovely homes you can buy in beautiful cities. Some snobs just think if they aren’t in some happening hub it’s just all hillbilly sh×tholes out there. Don’t believe it.

You’ll be able to buy a house.

The reality is you’re basing your assumptions on current market conditions, and they’re VERY abnormal – the the article displays.

If you plan on ‘buying the dip’ – and pretty much nobody can accurately time that to buy at the bottom on purpose – you can do it.

That means leveraging a ‘fortune favors the prepared’ mentality, that requires you be disciplined and keep saving.

All 3 of the houses I’ve purchased were ‘bought in the dip’. Two were for residences, one was a rental (sister and kids were homeless, so we used retirement savings to buy it).

Plan for this:

1. gubmint spending has a very large impact on the economy – the velocity of money is why.

2. Large cuts to spending AND workforce reduce both nominal inputs, but also velocity of the dollar in our economy.

3. Tariffs increase prices, which reduce demand.

4. Fed policy takes 6 months to 2 years to see full effect.

5. Reducing the size of the workforce (immigration enforcement without intelligent reform) has the potential to create a harsh supply-shock, causing prices to spike (just like 2021-2023).

The net effect of the U.S. fiscal policy – especially with the stated intent to redistribute wealth to the already rich (reduction in velocity) – will result in a recession within the next 6 months to a year.

IF implemented. Argentina’s recession from doing much of the same is a current, salient example.

If you’re a social-media consumer who groupthinks what uneducated, sparsely experienced people tell you to believe: Yes, you’ll never be able to buy a house.

If you learn very little about economics (like I have), you will be able to successfully plan and purchase a house.

Here’s my final word of advice: The economy ALWAYS sucks for most people. Except if you’re very, extremely lucky, or born into money (the reality is that most of the self-made people you read about were born into upper-middle class to upper-class families, with a LOT of exposure to entrepreneurs and policy-makers).

If you can’t figure out how to make lemonade from the lemons most of us are handed – and that takes sacrifice, discipline, and long-term hard work – you will never benefit from a ‘good’ economy.

I was born into a petroleum construction family, and every Christmas was a welfare Christmas from ’74 through ’87. I retired at 49 and live mostly off my investments.

This is achievable. It takes DECADES if you weren’t born into money.

What part of florida are you in? Panhandle?

put yourself in the shoes of the 35% who don’t own their homes, and it’s easy to see.

The silent killer here is real inflation for middle and lower “class” families. I run a small business so we track everything and we are in the food industry so I see how “manipulated” that sector can be … sure canned goods, processed food or off brand bad bread is only up 1% but raw ingredients that are anything close to wholesome are all up last year 18% and to start 2025 cocoa, wheat and rice for example are all up on average of 12% just this month … sure there are swings with these and it is a game of wack a mole to try to figure out which “basket” to use and track BUT the fed does a horrible job at looking at raw ingredients (and hence why it is a bit harder to “game” PPI and Core which are harder to manipulate). On another note all of my utility costs are 25% the last 2 years as they catch up with their increased costs … so while they make many categories cheaper (have you bought an appliance lately they are junk from even 5 years ago) the real costs for many Americans when it comes to their disposable income are way up (even if they have 8% more over the last 2 years).

Anthony Ace

The CPI for food at home (bought at grocery stores) has shot up by 28% since 2020. The CPI pretty much nailed it. People should read my CPI articles and look at the charts before they spread BS about CPI. SO READ THIS CAREFULLY:

https://wolfstreet.com/2025/02/12/beneath-the-skin-of-cpi-inflation-worst-month-to-month-acceleration-of-cpi-since-aug-2023-on-spikes-in-used-vehicles-non-housing-services-food-energy/

also, put yourself in the shoes of people who spend a high percentage of their income on the cpi basket that has gone up way more than the average, like child care, health care, dental care, and education, and it’s very easy to see why 70% of americans were unhappy with the economy

Yes, and the are going to be REALLY unhappy with the eCONomy moving forward. Especially of Trump and Liz get lower rates!

another part of the problem is that people gauge their own situation not in absolute terms, but relative to others. the sky high wealth stratification created by the fed is amplifying this program.

Troy-a big source of generational disconnects/dissatisfactions/disruptions: significant demographic groups who didn’t live, at least, a young adult’s life in the ‘before (fill in the blank) era’. Even if in the now-unlikely scenario of having an interest in legitimate history and senior family members who could honestly inform-recount the times they lived through, the experience of those times will largely remain in the abstract, and with it, how the present is dealt with (or not) by a younger demographic’s own life experiences. So rhymes the eccentric on the rolling wheel…

may we all find a better day.

Secretary of Treasury, Scott Besset, says, “within 12 months we will monetize the asset side of the balance sheet.” Any thoughts on what the plan is?

1. “Bessent.” With an n

2. He was talking about the creation of the US sovereign wealth fund that Trump wants. And he was talking about the federal government’s balance sheet where this wealth fund would reside as a big asset. There are other assets on this balance sheet, such as the federal student loans, LOL. On the liability side of this balance sheet is the $36.1 trillion in Treasury debt, plus other debts. This has nothing to do with the Fed, in case you’re wondering.

Wolf,

Would love an article on the SWF if/when it becomes a thing.

I don’t want to read anyone else’s opinion on it haha.

1:04 PM 2/13/2025

Dow 44,711.43 342.87 0.77%

S&P 500 6,115.07 63.10 1.04%

Nasdaq 19,945.64 295.69 1.50%

VIX 15.06 -0.83 -5.22%

Gold 2,957.60 28.90 0.99%

Oil 71.40 0.03 0.04%

“The heavily leveraged economic entities in the US are the federal government and businesses, not consumers.”

This suggests that consumers are isolated from the debt of the federal government and businesses. The debt still needs to be paid down. For example, if the federal government decided to make housing free and paid down everyone’s mortgage, and took on all mortgage debt, the debt would not go away, magically giving consumers a huge amount of disposable income relative to debt–the federal government would turn around and manage the debt by placing the burden back on consumers, one way or another. “There’s no such thing as a free lunch” would seem to apply here. I guess the concept here is that consumers feel like they are unburned by debt and can spend, because the debt has been shifted out of sight and out of mind; it is not directly allocated to them, but they will still be impacted by it and should pay attention to what they will eventually be on the hook to pay down.

And yet this hidden debt has been rising for decades and just the opposite has happened: the burden of paying it down has been repeatedly reduced with tax cuts. And the House is getting ready to ensure those tax cuts are made permanent. So when is the debt burden going to rear it’s ugly head and force a reversal in the general standard of living? How is it that we can go not months or years, but decades with it not being a problem?

I don’t think the burden of paying off the debt has been reduced, only selfishly, ignorantly delayed, as it puts the debt on people that didn’t overspend to accumulate it, and it could make the burden end up a lot bigger than what it would have been if we’d been responsible and gradually started paying it down when it was more moderate, because the US might lose control of the games it plays to keep it going, and there could be big sudden dollar devaluation leading to increase in inflation. I think the right way to fix things would be large spending cuts, tax hikes, and a deflation of the stock and real estate bubbles. If housing expenses weren’t so high here, and if stock buybacks were illegal, more companies could pay the wages to manufacture here, so we quit the periodic money printing insanity where a lot of money gets sent to manufacturing overseas. And quit the periodic rate suppression that wastes money on RE and other asset gambling.

yes, the debt has been transferred to the federal government’s balance sheet. the politicians have decided that there is no limit to what the u.s. can borrow, and so far, they’re right.

Wolf (or anyone)-

Slightly off topic, but in line with Kent and Frank G comments: does the concept of “fiscal dominance” carry any weight in discussion of “heavily leveraged economic entities” as mentioned in the article?

[Respected analysts argue the US is already in fiscal dominance, defined as “an economic condition that occurs when a country’s debt and deficit levels are sufficiently high that monetary policy can no longer effectively control inflation.” from Doomberg, Feb 13, 2025, The US Is Not Broke]

Does spiraling debt service (as percent of tax receipts) eventually cancel the Fed’s ability to control rates, leading to Kent’s premonition of a reversal of living standards.

Thanks.

While it’s not exactly what you were asking – I’d argue the previous Treasury admin was engaging in a form of easing by shifting the tenor of bond issuance towards shorter maturities.

Bessent seems like he wants a more normal auction schedule – i.e. fewer bills and more coupons. But this would have the effect of increasing supply of coupons, which could drive down their price (and push up yields).

The whole concept of fiscal dominance as an option is nonsense. All it would do is create hyperinflation.

I was thinking of “fiscal dominance” as more of a condition than an “option.” The onset of the condition having to do with a normalization of significant and chronic budget deficits resulting in a dramatic and ongoing increase of federal debt. The hyperactive debt growth then undermines the efficacy of monetary policy through a mistrust of the monetary authority.

I agree that fiscal dominance could easily end in hyperinflation, as depicted by Costantino Bresciani-Turroni in his 1931 classic description of Weimar Republic money meltdown 102 years ago: The Economics of Inflation.

Not meaning to sound hyperbolic, but on federal and corporate debt, this might be the road we’re on.

…since ‘TBTF’ seems to have worked seamlessly for certain entities, why not take THIS Kabuki off the road and put it on Broadway?

may we all find a better day.

The consumers in the #1 consumption economy in the world are doing extremely well. Hard to believe that any of our trade partners are going to walk away from US consumers? What market or where on earth are their bigger consumers who will purchase all their crap? The world stage if under pressure as no one knows what Trump will on any given day he walk into the Oval Office. $DOGE is keeping many politicians occupied, and Americans are loving the deep dive into where our money has been spent. One thing is for sure, the sheer number of individuals throwing money at political campaigns will suffer going forward. The sky is falling scenario and the price of eggs has gotten to be old news. There is no magic wand to wave for 1980 prices due to inflation. Americans always purchase what they want be their needs.

Everybody talks about the government’s debt, but are they taking into account everything arguably on the other side of the national “balance sheet” — public goods like freeways, the dollar’s reach, our Internet and banking choke-points dominance, the military, etc.? Forgive my ignorance for asking.

And BTW, it seems completely logical that a government would be running some deficit, with future taxation to ideally equalize that. A government is not a for-profit business. Successful nations have been the fiscal states — taxing and spending — for several centuries now. Otherwise you have no global heft, such as a military, or public infrastructure. I always hear these geniuses righteously griping about government while heedlessly riding on public streets or walking on public sidewalks, talking on publicly regulated bandwidths, etc.

do you realize just how little as a percentage u.s. federal spending goes to roads and the internet?

Phleep,

It may not be for profit but it has plenty of policies, especially foreign, that ensure American companies significantly profit. The constant conflict in the Middle East but you would be hard pressed to find a country not in NATO that we haven’t interfered with to advance its interests. It is a big reason behind our massive war machine, that and defense industry is hugely profitable and of course it is profitable in a world always at war somewhere which is why those lobbies are so strong.

“public goods like freeways”

How much do you think the Grand Canyon is worth?

Unfortunately most government spending is for social programs not hard goods like roads and infrastructure.

Did they make a change to calculate debt to disposable income from 2008 – today.

“they?” LOL, conspiracy theories coming out of every wormhole? Nope. I, me, and myself (the “they”) calculated that ratio via a spreadsheet, just a basic division, which is what spreadsheets are for, and I, me, and myself didn’t change the calculation from 2008 to today.

Howdy Folks. “But our Drunken Sailors, as we lovingly and facetiously have come to call them, have learned a lesson and have become a sober bunch, most of them, not all. ”

Some of US will continue to spend what we want, when we want, no matter the want. Signed A very sober sailor.

It is becoming easier and easier to get some fast cash for the consumers. Look at the stocks like Affirm (buy now pay later) and Upstate (Get an instant loan for about any purpose). Customers and Sales are growing fast.

For the first time in 25 years I am seeing the rental market soften and vacancies go up. This is a survey of three local property owner/operator operations. Probable 200 units between us all. Banks hate deflation, but the three of us definitely see this as an opportunity to dump the poorer-performing units and upgrade/purchase better properties.

Howdy WB. The Lonewolf charts have stopped showing real estate peaks?

Hopefully, the real estate bubble they created, keeps hissing and deflates.

I’ll keep my comments limited but two points of note. First, the charts as presented by WR are generally positive (over the past four years), especially the debt to disposal income. I’m not playing politics here but this clearly occurred during the Biden Administration so I’m wondering where the Trump Administration goes from here.

Second, today’s retail sales report for January 2025 (multiple sources) was poor, I believe down .9% with almost all retail classes reflecting sales decreases. Of course the excuses (or should I say BS) are starting to fly including weather, CA fires, economic uncertainty, inflation, hell, maybe someone will even blame it on mass deportation (which is not even a rounding error yet). I’m sure a 3 or 6 month moving average will tell a more accurate picture but this is something to keep an eye on as if the US consumer catches a cold, a more dangerous flu may spread.

In terms of retail sales, in the headline figure, you’re seeing huge seasonal adjustments in December and January. You’re not seeing actual retail sales.

Year-over-year, not seasonally adjusted, retail sales jumped by 4.8%; and seasonally adjusted, by 4.2%, strong year-over-year growth in January. But January always sucks, as sales collapse from December, which is the best month of the year, and so huge seasonal adjustments are used to lower December sales and raise January sales, and the thus constructed difference is what you see in the headlines.

Article coming shortly, a fun, geeky, and exciting romp through seasonal adjustments?

Wolf,

I think I’ve asked this before, but can’t remember your response. Gift cards don’t count towards retail sales, correct?

Gift cards are very often “sold” in December and redeemed in January. But it’s really the redemption that should count as a sale.

Census Bureau:

“How are gift certificates/cards treated? Following generally accepted accounting principles, sales from gift certificates are included in the retail sales of firms at the time the gift certificate is redeemed.

https://www.census.gov/retail/mrts_general_faqs.html

Sounds exciting and probably better than the Super Bowl last Sunday. Man, I must be getting old if data, information, and facts are more interesting than an over-hyped sporting event.

Here it is. Have fun:

https://wolfstreet.com/2025/02/14/about-that-plunge-in-retail-sales-a-romp-through-the-massive-seasonal-adjustments-this-time-of-the-year/

It would be interesting to see a chart showing the ratio of interest paid (rather than debt) to income. Those with adjustable mortgages or HELOCs may have seen interest rates rise from 2% to 8% in three short years.

Yeah, well, a record 40% of homeowners have no mortgage and no interest expense, and a big portion that do have mortgages have 3% rates.

Everyone has choices. Some people buy fancy Raptors, and Dura max +80k trucks so that they can go to the grocery store and buy 10$ a dozen eggs. Others buy used ford f150’s go to costco and buy $8 per flat.

Some people spend their money to show off. Others save and invest, and retire well.

Most ecomic compainers blame everyone but themselves. Want to blame someone, Look in the mirror!

Love it!

Know the difference between living rich and being rich? (You just described it.)

Average millionaire drives a Chevy, works 80+ hours a week, and looks “middle class”.

That being said, I am buying that solid-gold riding lawn mower for my .0056 acre strip of grass. Can’t let the neighbors think I’m POOR!!! ;)

Retail sales jumped as big box stores continued to collapse. 1000’s of store closings planned for this year. Is everyone working for Amazon?

All big-box store chains have HUGE ecommerce divisions. Walmart has seen 20%-30% growth year-over-year in ecommerce sates. What keeps Walmart’s stores open are grocery sales. Walmart is the largest grocery store in the US. Americans still like to buy (part of their) groceries at the store.

Macy’s is a huge ecommerce operator. As are others. They’re closing their stores, hundreds every year, and shift sales to ecommerce. That has been going on for many years.

there’s a lot of clickbait about well to do customers trading down to walmart. and while it is true that walmart is doing well among the upper income crowd, in my anecdotal experience, it’s that those people are using walmart+ and ordering online for delivery, not going to the stores. a lot of amex cards come with walmart+ for free.

I shop at Walmart using Instacart (Walmart+ is also available for home delivery). I would never think to step into a Walmart store anymore (it’s like going to the zoo where there are no cages or fences). Walmart does have the lowest prices for just about everything. But I buy fresh vegetables and fruit using Instacart at Sprouts. I would never buy fresh vegetables or fruit in a Walmart. I buy almost everything else from Amazon. I have a service that delivers my meds for free (Walgreens stores are disgusting where I live). I think the last time I was in a brick and mortar store was over five years ago, when I said to myself, fk this, I’m buying online and getting stuff delivered to my door.

I’m pretty sure there’s a more sophisticated spending dynamic at play than is being presented.

I know wealthy-ish people who buy non-perishable and quality-unimportant goods at Walmart/other discount retailers.

They buy high quality perishable goods, shoes, and other things where quality matters from retailers that offer premium goods.

@thurd2 The Walmarts and other stores I’ve shopped at in TX are pretty quiet and the people are laid back, very few incidents. And Walmart’s produce is just fine. Where are these crazy stores you’ve been in?

1234, the Bay Area in northern California. Glad to hear things are better in other parts of the country.

I was under the impression that the Fed was de facto unconcerned about inflation because the excessive debt load on private individuals would slow down the economy on its own. I remember reading about “secular stagnation” some years ago and thought that was a thing and it too would slow down the economy. Apparently none of that is true.

So I’m guessing it’s back to my other hypothesis – that the medicine for inflation is so bitter that the powers that be do not wish to administer it and the populace does not want to take it until inflation is much more severe and sustained.

Alpha chicken-

Sort of like institutional sins of omission and sins of commission.

It’s not just what the banking institution (in this case the banks linked together by the regulatory apparatus under Fed leadership) does, but what it doesn’t do, or prevents from happening, that leads to destabilizing imbalances. Like setting rates and disallowing market volatility.

Outside of economics, ground fuel policy in California is like that: neglect the prescribed burn and eventually you face a hellish price in fire and mudslides. Error of omission.

Or, try to control the flow of the Mississippi and eventually New Orleans pays the price with catastrophic flooding. Error of commission.

(Both examples described four decades ago in John McPhee’s fascinating book The Control of Nature)

Thanks for the thoughtful comment.

2nding your comment

&adding: Over the last 15-17 years, we’ve seen mythological government intervention in the ‘behind the curtains’ financial sector.

The bailouts, interest rates, ‘quantitative easing’, and fiscal stimulus since the Great Recession have never been done before.

They haven’t been wound down, either.

“A rising tide raises all boats.”

However, while that tide does make the boats rise, it takes a LOT of time to pump that high tide back out of your basement.

I think secular stagnation may come about, but an unprecedented dollar value still has to be bled out of the system.

For reference: The average (western economy) person is vastly richer now than ever before in history.

I mean, the middle class never really existed 300 years ago. We have ~5000 years of recorded history. The middle class has existed for 6% of human history.

The rest of the time, there were the rich and the poor.

It will be interesting to see what the mass firing of govt employees does to these numbers and the reduction in govt spending that will flow through NGOs and private corporations ultimately leading to layoffs.

Also its tale of 2 economies, if you’re someone who bought before 2018 you’re in great shape financially. Those who didn’t, will struggle to buy because Salaries did not keep up with housing inflation.

That being said at least in CO rent prices are dropping both month over month and year over year and supply is up significantly over 2019 levels, and there’s a net outflow of people. Tourism is down. And lastly weed tourism is down and weed businesses are going bankrupt left and right (supposedly they bought up a lot of real estate because they couldn’t keep money in banks back in 2015 and 2016) so all things point to real estate deflation here if these trends continue….we might just be the next Austin 🤞🤞🤞

Compound that with large-scale return to office mandates.

All the people buying ‘country homes’ with the idea the ‘new normal’ was going to be remote work are in for some trouble.

…definitely the ones who didn’t anticipate having to move back, and so sold high, bought high, and now must sell low and buy high…

I dont think the population doesn’t want to stop debasing the dollar. It’s the businesses that want the consumer flush with cash that don’t want to reduce deficit spending. Theyre the ones that are giving the campaign donations to keep the spending going. But I think inflation is and will lead more people to cut discretionary spending out of concern for not being be to afford necessities down the road, so I think discretionary sector businesses such as restaurants should support govt restraint and balanced budgets so people feel more confident if stable future prices in basic needs.

How does the debt to income ratio look if you eliminate the top 1% or 5% of earners from the equation?

has little or no impact because CAPITAL GAINS are not included in disposable income (RTGDFA), and capital gains from investments is WHY the rich are rich and how they got rich.

Mick mentioned top earners and should’ve said those with the highest level of disposable income. Semantics aside, this data would be interesting and would likely tell a somewhat different story. Income/debt of those with very high disposable income has little impact on defaults and foreclosures, which is the heart of this dataset’s analysis. Trimming off 20% or 50% from the top would be interesting.