I watched this stuff last time, amazed by the lack of inflation. Sure, “This time it’s different,” but those are the four most costly words on Wall Street.

By Wolf Richter for WOLF STREET.

President Trump has now started implementing his promise to impose new or additional tariffs on goods from various countries, starting with China, Canada, and Mexico. Trump already imposed tariffs in 2018 against various countries. Now, once again, the media are all over how prices are going to jump for consumers because tariffs are a “regressive consumption tax,” and how tax receipts from tariffs won’t go up, etc. etc.

Now we’ll look at what tariffs did and didn’t do last time. One, they didn’t trigger inflation, which stayed below the Fed’s target. Two, they more than doubled tax receipts from customs duties. And three, they hit stocks, and the S&P 500 tanked 20% in 2018.

Sure, “This time it’s different” – but those are the four most expensive words on Wall Street.

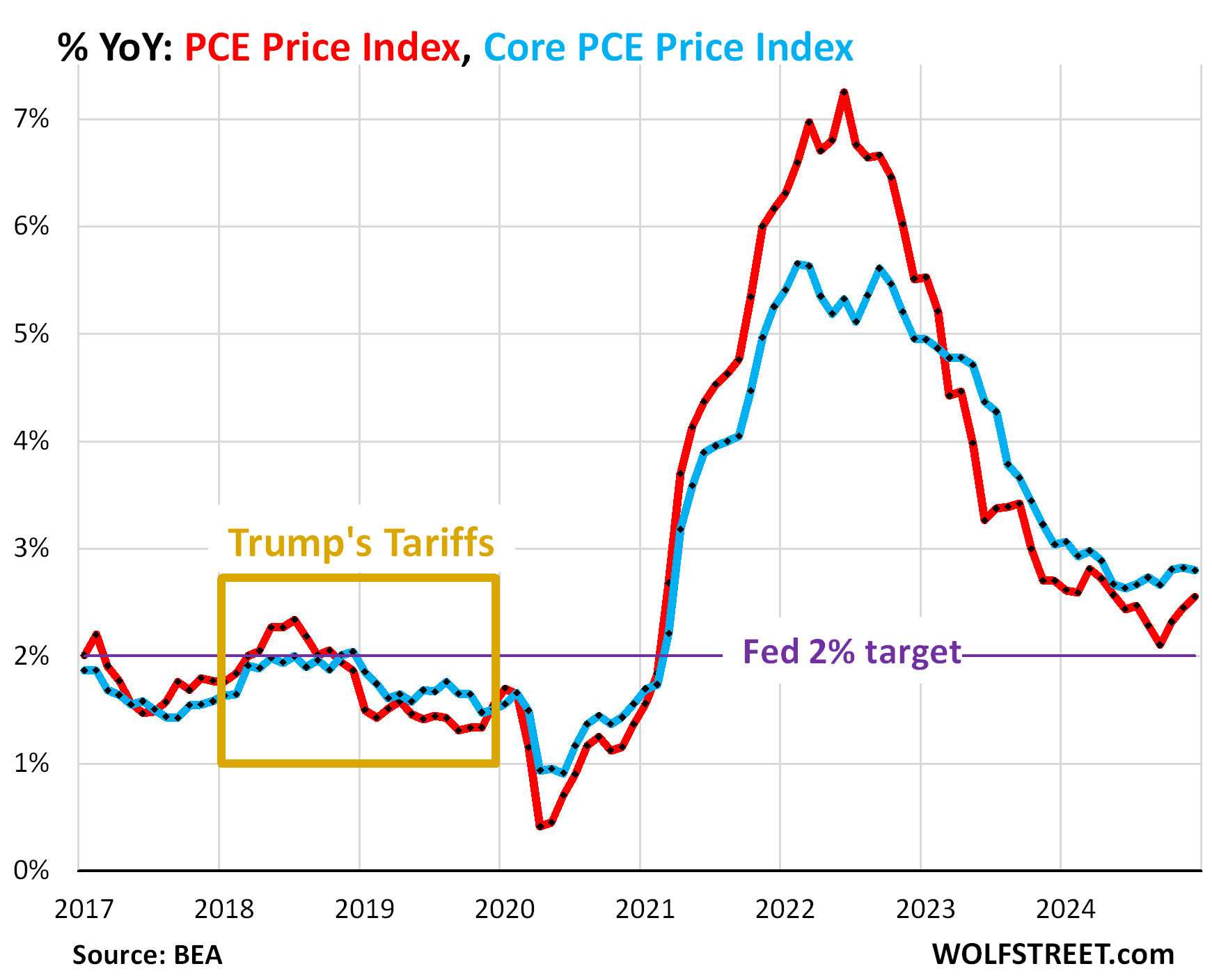

Inflation did not accelerate.

We reported on the tariffs back then, also expecting price increases, thinking that companies would be passing on their increased costs. But that didn’t happen. They tried, but couldn’t. And the Fed-favored “core” PCE price index (blue) remained below the Fed’s 2% target and then decelerated further.

The reason that inflation remained cool and cooled off further in 2018-2019 was that durable goods inflation was essentially zero.

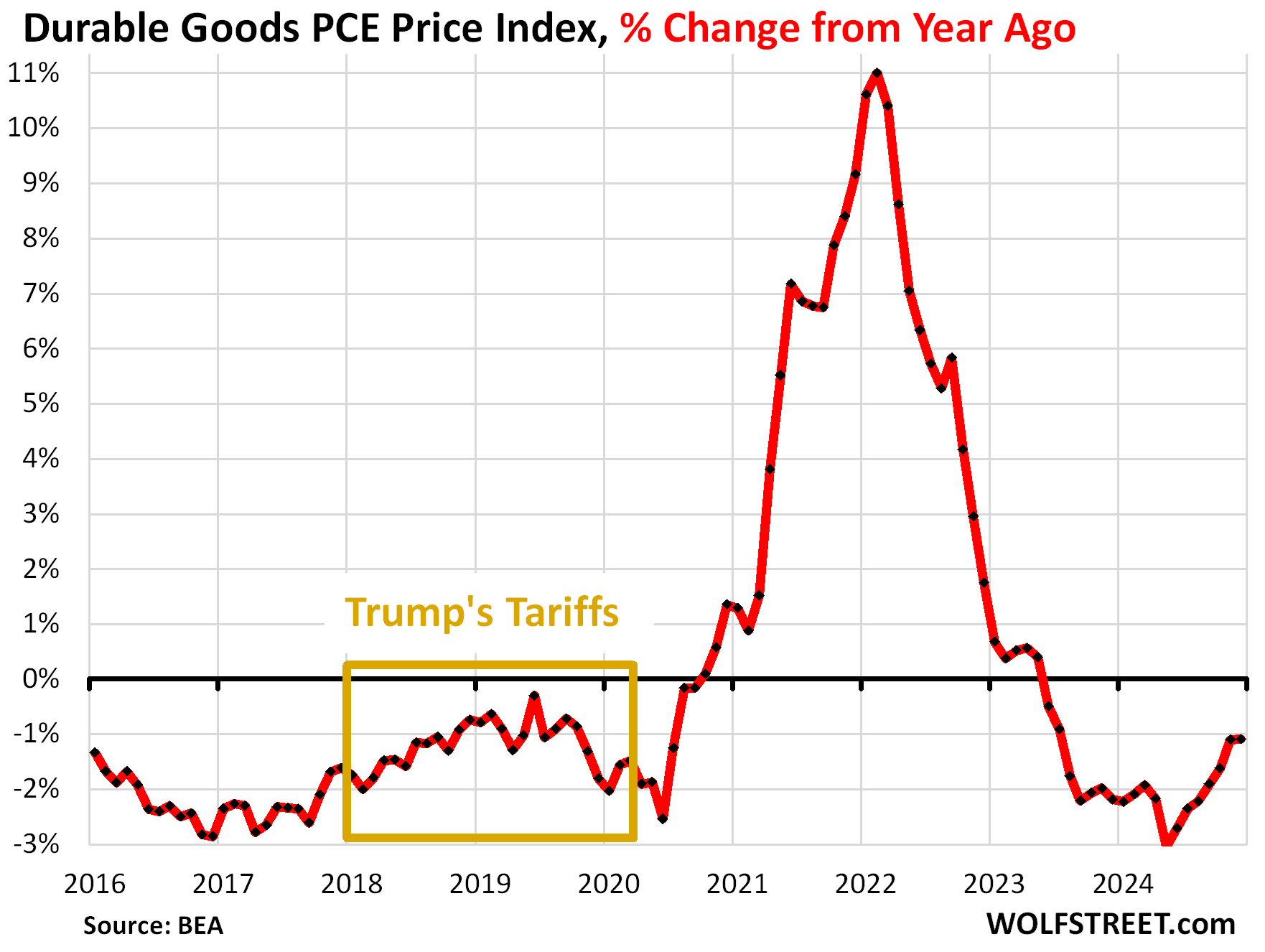

Tariffs are not applied to imported services; they’re applied only to imported goods. And those tariffs should have shown up in durable goods inflation because a lot of durable goods are imported, or their components are imported, and were tariffed.

The PCE price index for durable goods remained negative throughout that time…

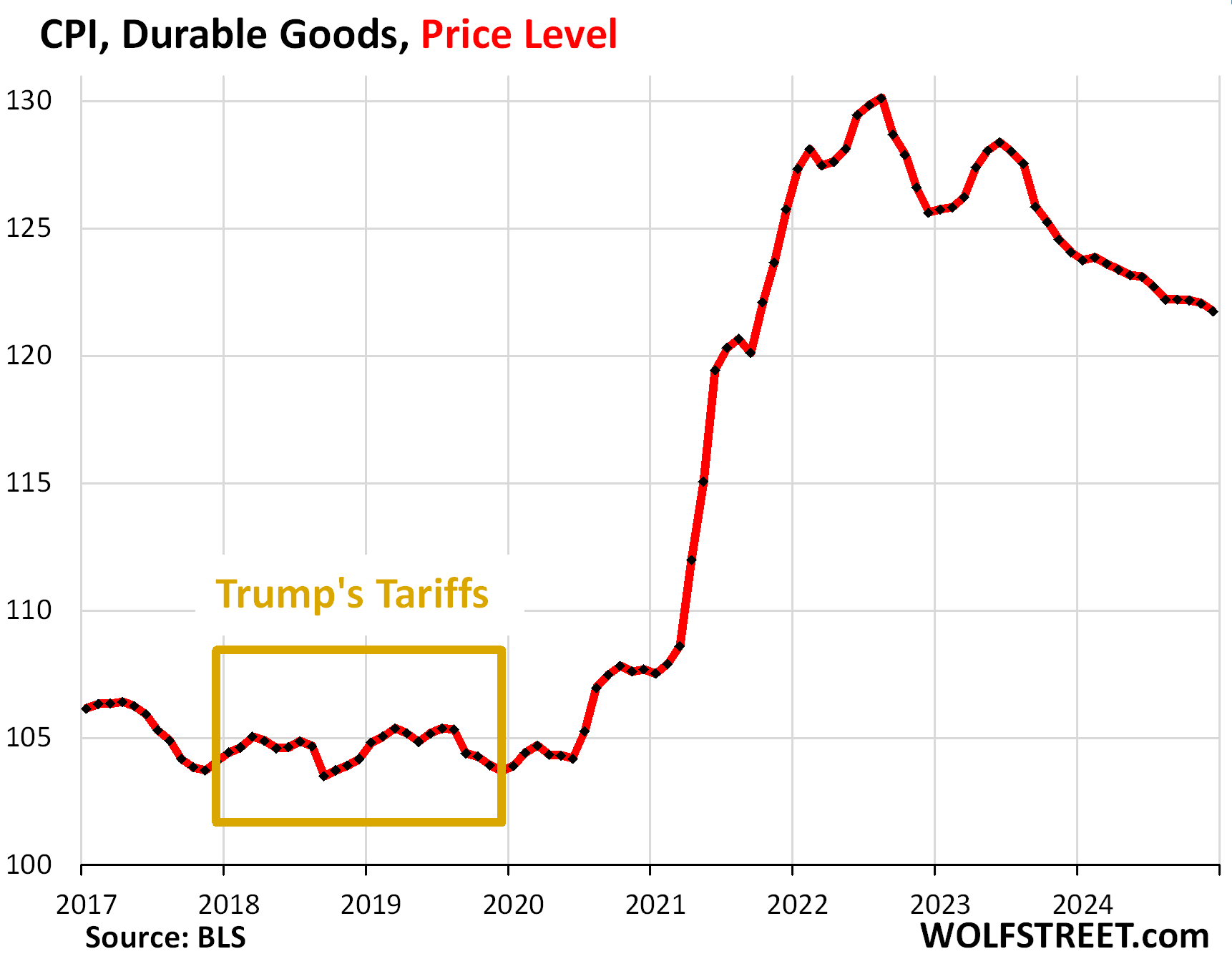

…while the CPI for durable goods – CPI usually tracks a little higher than the PCE Price index – moved in a range of -2% to +1% year-over-year. The chart below shows the price level, not the year-over-year change, and it’s a little clearer about there essentially not being any inflation in durable goods at that time:

This lack of inflation in durable goods despite the tariffs throughout the period until the pandemic price spike surprised many of us observers. But there are reasons for it.

It’s hard for companies to raise prices and not lose sales. There is lots of competition in the US, including from domestic production. Companies, including retailers, raised their prices, but then lost sales and couldn’t sell at those prices, and their inventories piled up because Americans hate, hate, hate higher prices, and then these companies had to roll back their price increases in order to salvage their revenues. And in doing so, the companies and their suppliers ate those tariffs lock, stock, and barrel.

Customs duties more than doubled in less than two years.

Tax receipts from tariffs soared to a seasonally adjusted annual rate of $80 billion in Q3 2019, from under $40 billion before 2018. The pandemic with its shortages and import hang-ups then mucked things up, but by Q1 2021, when Biden took over, customs duties were back at $80 billion and continued to rise through Q2, 2022, reaching nearly $110 billion.

This chart shows two things: One, the surge of customs duties under Trump. And two, it’s not something Trump invented. Customs duties had been collected before, and Trump just added to them, and they continued to be collected under Biden. Now the new tariffs will add to those customs duties already being collected.

We don’t know how much in customs duties the new tariffs will add to the existing customs duties, and the current amounts are not huge by government-deficit standards, but with the huge US government deficit, every $100 billion counts.

The stock market tanked in 2018. Tariffs are good for the US economy because they change the math for domestic production, and the primary, secondary, and tertiary effects of producing in the US are great for employment, tax receipts, household incomes, etc. But tariffs are not good for the S&P 500. Stocks got hit last time.

The reason why tariffs can hit stocks is because tariffs are a direct tax on Corporate America’s gross profit margins on imported goods.

But even for the S&P 500, new tariffs are just a one-time hit. So if the new tariffs cause a company’s gross profit margins to decline from 20% to 19% in 2025-2026, that’s it; they would not decline every year, but just once after tariffs are implemented, and then remain stable.

It’s not the end of the world for stocks. Crazy overvaluation is a far bigger problem for stocks. In 2018, QT-1 was also beginning to bite, and the Fed was nudging up its policy rates at snail’s pace. A mix of things came together in 2018, and the S&P 500 tanked 20%. But it didn’t last long.

Some basics about tariffs.

I posted this list before. But it’s important, so here it is again:

- Tariffs have two roles: raising taxes (which the US desperately needs); and changing the economic math for domestic production.

- US “trading partners” have used tariffs extensively to raise taxes and to protect and support their own industries at the expense of US production and exports. The US has used tariffs, they all have used tariffs to raise taxes essentially since the beginning.

- Tariffs are applied to the cost for the importer. If a big US retailer buys T-shirts by container loads from a factory in Bangladesh that it intends to retail in the US for $9.99 each, and if the tariff on this product is 25%, the importer (the retailer) is going to have to pay 25% in taxes on the cost from the factory. If the factory charges $1 per T-shirt, the tariff amounts to 25 cents.

- Tariffs are a direct tax on the profit margins of foreign producers and US importers. Whether or not they can charge more for their products without gutting their sales to pass on the tariffs is decided by the market. And if they can pass on a portion or all of the tariffs, it would be a one-time bump.

- Companies are already charging the maximum amount they can and still obtain their sales goals. If they raise prices to pass on the tariffs, sales may fall. Whether or not the retailer can raise the price of the T-shirt to $10.24 without pulling the rug out from under the desired sales volume is decided by the market, not by the retailer, and the retailer may find that it has to eat the tariffs.

- US importers may negotiate the purchase price to where the foreign factory eats part of the tariff, in which case foreign producers pay the taxes to the US government.

- Domestic production reduces transportation expenses, loss of Intellectual Property (a huge issue in China), supply-chain uncertainty and lead times (catastrophic issues during the pandemic), and other costs and risks. Tariffs tilt the balance further in favor of domestic production.

- Foreign manufacturers can avoid tariffs by producing in the US. All major foreign automakers that sell in the US already manufacture vehicles in the US. In terms of “US content,” Honda models are right behind Tesla on top of that list. Tariffs will further encourage US production, including of components and assemblies.

- Many producers have cut prices in the US over the past two years, either directly or through incentives to reach their sales goals, including automakers (here) and homebuilders (here). In this environment, they will eat 100% of any tariffs because they cannot pass on any additional costs.

- Industrial robots cost about the same anywhere. Products can be and are manufactured in the US price-competitively when advanced automation reduces the labor-cost component. Tariffs add some pluses to that math.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

But aren’t these tariffs much larger and wide ranging this time? And aren’t we going see the same in kind from Mexico and Canada? And won’t this cause unemployment to go up on both sides of the border, at least in the short term, as demand falls and companies try to sure up margins?

1. The US had the biggest trade deficits in 2023 with China, then Europe, then Mexico — TRADE DEFICITS. In 2018, the trade deficit with China was even bigger. Imports from China got slammed by tariffs, so some of the trade was then routed through Vietnam by 2023 as you can see in the chart below.

2. “Trading partner” is a commonly used BS term that adds imports and exports together, but what matters are imports, and the trade deficit with each country (exports MINUS imports).

3. The principles are the same?

— No/little impact on inflation because Americans hate, hate, hate price increases, and they’re stick and tired of them, and companies that try to raise their prices will watch their sales plunge.

— Receipts from customs duties will soar, thank you!

— Stocks will tank? (Don’t look now)

https://wolfstreet.com/2024/02/08/us-trade-deficit-in-2023-dropped-19-as-goods-deficit-with-china-plunged-29-imports-exports-of-goods-services/

“Receipts from customers duties will soar, thank you!”

—“Customs duties”?

Illuminating article.

Thanks, fixed. It was kind of late when I wrote that comment. Should have gone to bed instead of posting comments in the middle of the night, LOL

Illuminating colors too. Southern Pacific Daylight red and orange. You’d almost think Wolf’s been in Sunnee Caleeforneeuh for so long that he’s beginning to see things like a true native. Now hum along, “Way down yonder on the Indian nation, ridin’ my pony on the reservation, in those Oklahoma hills a’ way back home. Way down yonder on the Indian nation, the horse traders life was my occa-u-upation, in those Oklahoma hills a’ way back home.”.

Standard internet colors that display properly in your browser. Fancy colors that are not part of the standard colors might look different on different devices and browsers. The internet is a strange place.

“because Americans hate, hate, hate price increase”

They’re also used to them now which may make a difference. Time will tell.

That’s kind of what I’m thinking, Covid changed that equation and price increases can just be blamed on Trump, letting the sellers get of free.

Never let a good crisis go to waste, and all that.

Sandy,

That’s not how prices work. It doesn’t matter what the price tag says. Someone has to BUY that product at that price for the price to become effective. If no one buys it at that price, the price doesn’t actually exist. It’s just a number on a tag. Might as well be smiley face. Consumer aren’t going for price increases anymore. They’ve had it. How are automakers going to increase prices, when their inventories are piling up, and they’re having to cut prices to sell this stuff, and their sales are still well below where they had been in 2019? Any automaker that tries to increase prices now will lose sales, and inventories pile up further.

Was this sarcasm? I thought Wolf explained things quite clearly. President Trump may be annoying, undiplomatic and rude in many ways. But his opposition is distorting these tariffs a little.

I’ve seen examples of a $1,000 television going to $1,500 due to tariffs. The tax is on the import cost, not the retail cost. So maybe $50 on a $1,000 television. A pair of Gap jeans (if still made in China) might have a $1.30 added. But since the cost difference between making those jeans overseas is currently only about $2-$3 per pair, it brings businesses closer to deciding to reshore jobs. Logistics and supply chain became huge problems recently and these tariffs may help sway some companies back here.

I do worry that produce from Mexico will hurt- those tariffs will likely be more noticeable and painful as grocer margins are miniscule. But the general idea of using tariffs as a business and policy strategy is what our competitors have been doing for decades.

Good points. My friend who grows avocados in California has been struggling to compete against Mexico avocados. Tariffs are good for him and better yet he is an American tax payer. Go figure. Somebody is looking out for these people for once? He makes more money, hires more people, and pays more taxes. Win-Win

I was a kid in Fallbrook, CA in the 60’s. “Avocado Capital of he World,” it billed itself. Avocado Festival, Avocado Queen. Classic small-town agricultural culture.

And now you pay more for avocados and you can feel good paying more for avocados since you know that it benefits your friend growing those avocados. Win-Win for you.

Meanwhile Loss-Loss for everyone else in the world. Loss for all of us who aren’t friends and have to pay $2 an avocado instead of $1. Loss in sales of avocados in the US at grocery stores which now have to also let go of people and make less money. Loss for the farmers in Mexico now selling less avocados in the US. Loss for the farmers in Mexico who now makes less money, loss for the farmers in Mexico who have to let go of people cause can’t sell as many avocados, loss for Mexico on taxes because sells less.

which is why targeted tariffs more sensible than blanket – possible to predict the consequences; and, avocado here avocado there – but the Trump blanket tariffs will have unforeseen and hard to predict consequences as USA does not necessarily have the factory today that offshore currently supplying (takes years to locate/build/launch said factory).

Michoacan has the best avocados, period.

I like buying local when possible, put CA isn’t local to me anyway.

This idea that working age Americans will go back making jeans is at the root of the boomer misunderstanding. You can barely get gen z to do office work–they are absolutely not going to move to a semi-rural area and make jeans on third shift without wages 10-20x foreign ones. You would need tariffs in the 100s of percent. And even then, why exactly do we want an economy with more low-skill manufacturing. We moved past that.

William McDonald,

This is the same thoughtless anti-tariff propaganda BS copied-and-pasted everywhere!!! You have a brain, so USE IT before you post! AUTOMATION. INDUSTRIAL ROBOTS. Ever heard of it? That’s what manufacturing in the US is all about, not sweatshop labor. Walmart is now buying USA-made T-shirts and hoodies, but they’re largely made by automated equipment. Most of the products made in the US are and will be high-value products in plants that are largely automated, such as motor vehicles, semiconductors, batteries, electrical equipment of all kinds, other equipment of all kinds, including for oil and gas drilling, steel products, etc. That’s just in terms of durable goods. The US is already a huge manufacturer of petrochemical products, food products, construction materials, etc. All of this production is largely automated, and the labor it does require is highly qualified, including tech people.

Much larger and wide ranging? The 2018 tariffs on Canada were on steel and aluminium. The 2025 tariffs are on everything. So that is wider ranging.

The impact on the auto biz will be interesting. As in ‘just in time’ parts supply. They aren’t stacked in warehouses around the assembly lines.

“The impact on the auto biz will be interesting.”

Anecdotally: most parts I order are located in domestic warehouses when I order, even aftermarket parts made overseas. And the rare “made in Japan” Honda parts are usually in stock at my dealer’s parts dept or can be brought in next day on their truck.

I do suspect many aftermarket parts will get a bit more expensive – but they are already so much cheaper than OEM. For example: local dealership wanted $350+ each for lower control arms; name-brand aftermarkets were less than a third in price at $100 each. Even if I had to pay 50% more it still would have been a deal vs OEM.

NB: all my oils and fluids are already made in USA.

An individual’s need for parts is not quite the same as the supply for a moving assembly line. A co not using ‘just in time’ could not compete financially in a field with fewer survivors every year.

BTW: Wells Fargo figures their earnings forecast for GM, Ford, and Stella for 25 will be lowered to zero. That is just based on the extra 25% for parts…not however long they get held up, if they do. Another giant parts outfit, Liminar, figures some lines will shut down in a week.

One thing about this most integrated industry, where thousands of parts come together to become an auto in a very short time, it is complex, not simple.

Sorry, realise you were just commenting anecdotally.

Moving on…suppose it was determined that all car parts should be made in US. OK but how about giving the industry some more time than a week. How about phasing tariffs in, maybe beginning at 1 % and rising 1% every month. This would be considered very fast in the old normal universe of a few days ago.

Indeed this is just my perspective as a single person with a single 14 y/o car. N=1, mileage = 193k.

But I have been buying quite a bit of parts lately for a front suspension, drivetrain, and power steering rebuild. And with the talk of tariffs, taking note of what is made where.

A significant % of OEM Honda parts are made in USA, as Wolf correctly notes. Every now and then I get little stuff with made in Japan on the sticker – recently a pair of front wheel bearing snap rings, for example.

All my fluids – Honda OEM and 3rd party – are made in USA.

Most aftermarket parts are made overseas tho.

Thank you, I understand tariffs much better since I read your blog.

The big problem is that people who are attacking tariffs AND who defend tariffs in the media/ social networks etc. are missing that point. If Trump would communicate half as coherent as you do I suspect people would have much less proplems with it.

And the trade balance didn’t get better 2018-2019 and it won’t be getting better this time around. It can’t as long as the deficit is as it is.

The trade balance didn’t improve because Corporate America tried by hook or crook to subvert the tariffs, and they lobbied mightily to get exemptions, and were given exemptions, they routed trade through Vietnam to get around the China tariffs, etc. etc. Corporate America hates tariffs, billionaires hate tariffs, the billionaire-owned media hate tariffs, such as Murdoch’s WSJ, Barron’s, MarketWatch, Fox, etc., Bezo’s WaPo, Buffett’s newspaper empire (20?), Sulzberger family’s NY Times, etc. They all fought and will fight Trump tooth and nail on tariffs. Some of those billionaires are in Trump’s inner circle now, so we can be assured that the new crop of tariffs will also be subverted.

… and those same billionaires, massive stockholders and their publications and political puppets will do their very best to spin this into positive news for the stock market soon. Too much is at stake there for their bank accounts.

Billionaire alchemy.

“Billionaire alchemy”

Great description. I’m stealing this!

“Some of those billionaires are in Trump’s inner circle now, so we can be assured that the new crop of tariffs will also be subverted.”

100 percent! However, my sense is Trump is doing this to get some small kernel of a “win”, cancel the tariffs and do a victory lap. Politics 101.

This would seem to be borne out by reported suspension of Mexico tariffs after a trifling gesture by Mexico.

“100 percent! However, my sense is Trump is doing this to get some small kernel of a “win”, cancel the tariffs and do a victory lap. Politics 101.”

THIS. Except it will be declared A BIG WIN.

Well look at that! First Mexico and now Canada avoiding tariffs. And sure enough Trump running some victory laps with multiple red caps flying off heads in wild applause!

you are psychic…just heard the news.

wonder if any insiders shorted , then bought at bottom

Your analysis doesn’t include retaliation from America’s trading partners.

1. They “retaliated” last time, and it’s included.

2. All countries ARE using tariffs, RTGDFA, and have been using tariffs against the US for eons.

3. China has big tariffs surrounding its protected industries, and US companies have to produce in China (in joint ventures and with required technology transfer and loss of IP) in order to sell in China. That’s how you develop and protect a manufacturing base.

4. The US has allowed its manufacturing base to be destroyed by globalization mongers for three decades. China has done the opposite, as have other countries, and now the US has a $1 trillion a year trade deficit, while the globalization mongers laughed all the way to the bank.

5. It’s a scandal what happened, three decades of connivance by the US government and Corporate America to destroy the manufacturing base so that corporate profit margins could fatten, while the most important economic sector – manufacturing – with its huge primary, secondary, and tertiary impact on employment, wages, household incomes, tax receipts, knowhow, infrastructure, etc. was shifted to overseas locations. That this was encouraged to happen was a huge scandal that spanned across both political parties. And those idiots are still spreading the same BS today.

Like I’ve asked before, in the case of peer countries like Canada or the EU, which are not really undercutting us on labor costs or regulation or whatever, the rational for trade seems to actually be comparative advantage. Are you saying that there’s some other reason that trade with those countries is hurting the US or are you just advocating for autarky?

It doesn’t matter one flip. The fact that both run big trade surpluses with the US, especially the EU (which has been engaging in industrial policy ever since its existence, following Germany’s industrial policy) is a sign that tariffs are needed to keep shift more US production to the US. Some of that has been happening without tariffs already.

wikipedia has a great list of 194 countries currently using tariffs.

Now if we could get a tariff placed on posting internet mis/disinformation we could slash the national debt overnight.

I remember when NAFTA was trotted out, students at the University of California Santa Cruz when balastic and said it would kill off blue color jobs in USA. For once I had to agree with them. To this day I wonder what professor at that uber liberal institution finally taught some sense.

Thank you, Wolf. This is precisely the issue:

“It’s a scandal what happened, three decades of connivance by the US government and Corporate America to destroy the manufacturing base so that corporate profit margins could fatten, while the most important economic sector – manufacturing – with its huge primary, secondary, and tertiary impact on employment, wages, household incomes, tax receipts, knowhow, infrastructure, etc. was shifted to overseas locations. That this was encouraged to happen was a huge scandal that spanned across both political parties. And those idiots are still spreading the same BS today.”

I still remember the early 2,000’s when I heard that Bush was reclassifying fast food workers as manufacturing workers. Funny if it wasn’t so sad. I don’t actually know if that stuck…?

That may have been an urban myth — or a dry joke. It’s not the case today, and it hasn’t been the case since I’ve been paying attention to this.

I don’t get the 10% on China, since that’s all the cheaply made garbage that can’t cost much to produce. Seems backwards. And China didn’t seem to even care that much. Canada, unless you count the things that they subsidize (health care), doesn’t have an unfair advantage on labor. Only thing that makes sense is that it generates attention and deal making – Getting to play host to all kinds of groveling sleezebag business owners who want exemptions. And now, since sitting presidents can’t be prosecuted, and because Congress is feckless, there are no restrictions on being openly transactional for personal gain. Maybe that’s all there is to it.

I suspect this leaves him room to negotiate and show force. If they retaliate, he can add 10 or 20% more for example. Of course, that is conjecture, but makes sense to me.

Correct. Remember, as “out there” as Trump appears, he is a businessman at heart and not a diplomat. He is indeed looking for the deal. I think he is “crazy as a fox” in that he will take risk (in the business sense) as a strategy, however in government there are many more variables which he cannot control. His leverage stops with congress and that part of the balance of power is not 100% lock in his favor. But hey, two out of three ain’t bad.

China doesn’t care, because even with an honest and sustained effort, enforcement would be difficult. They’re counting on shipping containers to intermediary countries and slapping a new label on them, and generally waiting things out until Trump declares victory, loses interest, and moves on to other things.

Read the US Customs and Border Protection website (cbp) for enforcement statistics. It’s a (bipartisan) joke.

Number of Enforcement Investigations per Year/Amount of lost revenue:

2018 – 7 investigations, $15 million

2019 – 31, $250 million

2020 – 64, $215 million

2021 – 48, $112 million

2022 – 35, $97 million

Maybe I’m missing something with the statistics, but there is no way everything else from China suddenly became compliant, with all duties paid. So, yeah, on paper we’ll get tariffs, but there will be leaks everywhere.

The 10% is on top of the tariffs that are already imposed on China-made goods.

China produces high end components just as much as cheap stuff in the electronics world. Cost savings on production don’t end at cheaply made stuff.

iPhones are made there as one high end example.

Well, maybe Apple should start making iPhones here instead of in China? We (the U.S.) could use the good jobs.

Apple has already been shifting production away from China long before this. They’ll get by fine continuing to do so

I started shopping for some hi fi equipment just before Trump imposed his first tariff on China. After that tariff was imposed, the prices of that equipment increased by several hundred dollars. Perhaps those price increases didn’t affect the official inflation calculation, but they were very annoying.

And then sales plunged, and those price increases were rolled back to increase sales. This happens in real time now. Companies always try to charge the maximum possible at which they can still achieve their sales goals, so they increase prices, and if sales slow, they roll back those increases. Happens every day all day long, even on Amazon by the minute.

I did not buy the equipment then because I hoped the tariffs would be lifted. I’m sad to report that the prices of hi fi equipment have not come down. In fact, they kept rising because of inflation. Of course, hi fi equipment is a niche market with relatively few brick and mortar stores.

Just buy some McIntosh gear from the 60s. Yes, they’re Veblen goods, but to my ears nothing sounds better and that stuff never dies.

Good stuff Wolf. Most anti-tariffs pictures do not understand tariffs and the after effects. Good example.

WSJ had a pretty good article on how the goal was to let China into the WTO and to get them to open their markets to U.S. companies. Well it backfired. What happened instead is very little except food and iPhones is sold to China. I don’t think we are selling TV there , or auto parts there , or computers there. But in the USA, many manufacturing towns have been hit hard since 2001.

————————

From WSJ:

The roots of the tension go back to 2001, when China joined the World Trade Organization, dropping many barriers to its exports around the world. Policymakers in the U.S. hoped China’s accession to the WTO would benefit U.S. consumers by giving them access to inexpensive goods and open the country’s markets to U.S. business while also nudging China toward democracy.

It didn’t work out that way. China was huge, its labor costs were extremely low, and its surge in exports took place over a matter of just years rather than decades. Many U.S. manufacturing towns couldn’t compete. Autor, along with the University of Zurich’s David Dorn and Harvard’s Gordon Hanson, released their first paper on the topic in 2011.

They showed, there and in subsequent research, how hard these towns were hurt. Those communities experienced higher unemployment, lower wages, higher use of food stamps, higher disability payments, higher rates of single parenthood and child poverty, and elevated mortality.

——————————————————-

Many people do not realize many industries in China are subsidized by their government in the purpose to take global market share. It is unfair practice.

Sure, a consumer may save 5% or 10% on some gadget now made in China but the middle class took the big hit. Who is the big winners from globalization. Walmart, Amazon, Target, etc.

The U.S. did fine prior to 2001 and before all the cheap stuff from came from China. Now anti-tariff people think the world is going to end because of some tariffs. Economically there is a term call substitution. If steak is to expensive then you eat Chicken.

LOL. So now after the tariffs one can only afford a 65 inch TV instead of a 75 inch TV.

If you paid attention during round one, clothes dryers increased in price with washing machines although there was not tariffs on clothes dryers.

Corporate America with use this confusion on tariffs to raise prices across the board.

But then people stopped buying those overpriced appliances, sales plunged, and prices were rolled back, at which point sales resumed. The media didn’t tell you about that. They only produced clickbait stores of how a specific retailer raised prices. But they failed to report, of course, that later, after sales had collapsed, the retailer was forced to roll back those price increases. The billionaire-owned media, including the NY Times, have been producing nothing but clickbait BS on this issue. And Americans ate it up because Americans love clickbait BS, which is why it is being produced.

It’s similar in the real estate market. Media reports home values going up while Zillow has price cuts galore.

Appliance prices have far more to do with consolidation than tariffs or inflation.

GE appliance was a leader in innovation design and US manufacture of appliances. They still remain top level in both, although they were purchased by the Chinese Haier company in 2016. A sale of GE appliance to Swedish Electrolux was blocked by the US government in 2015.

Hmmm…

“Consumers have been gladly paying higher prices since the covid induced worldwide inflation.”

Speak for yourself. I stopped paying absurdly high prices for e.g. eating out, car repair, haircuts, and a bunch of other stuff. Now I do all these things myself, both to save money and protest higher prices.

I wonder if the reason corporate America absorbed the tariffs in 2018 and 2019 was because their margins had been inflated by near-zero interest rates on their borrowings. ZIRP gave them some fat to play with. With interest rates normalizing as fixed-rate debt starts to mature, that fat may not be available this time. Corporations could get hit with a double-whammy on their profit margins: increasing finance costs and increasing import duty at the same time.

“Corporations could get hit with a double-whammy on their profit margins: increasing finance costs and increasing import duty at the same time.”

Yes, kind of. But in a different place.

Tariffs are a tax on gross profit margin, they raise the cost of goods, and thereby reduce the difference between selling price and cost of goods = gross margin.

Financing costs are much further down on the income statement, often below Selling, General, and Administrative (SG&A) expenses. So gross profit minus SG&A expenses produces operating profit (Earnings Before Interest, Taxes, Depreciation, and Amortization, or EBITDA). Then, from this operating profit the interest and other non-operating expenses are subtracted. So the financing costs show up in net income, but generally not in operating profit.

Corporate earnings, at least the SP 500 which is included in the article, didn’t go down in 2018 or 2019. https://www.multpl.com/s-p-500-earnings

There are many flaws with this dumb tariff idea but the biggest one is what Wolf alluded to in one of the comments. Corporate America and the Stock Market demand that earnings go up forever. They aren’t going to settle for their margins going away, that’s not how this works. Either through exemptions, increasing prices, or using robotics to hire less people than the plant in China or Mexico or wherever used they will get their bag one way or another.

You’re NOT talking about gross margins (difference between cost of goods sold and selling price). You’re talking about earnings per share = net profit after all expenses, interest, and taxes, divided by the number of shares outstanding, the “earnings multiple” that your linked chart shows. This has nothing to do with gross margins. For example, a company can increase its earnings per share buy buying back its own shares even if its gross margin is shrinking.

In Your Deliberations You should incorporate that a big Chunk of US China Imports are imports from Companies owned by US ( and other Western and Japanese ) Companies ie is part of ” WESTERN ” PROFITS .. and the amounts are HUGE .. in reality reducing the TRUE TRADE Deficit with many many Billions.

The first part is correct and it’s included in the analysis and is part of the scandal of globalization.

The second part — “in reality reducing the TRUE TRADE Deficit with many many Billions” — is BS because corporate profits go to investors or stay in the company and have nothing to do with trade. yes, investors benefited hugely from this scheme, while manufacturing in the US got decimated.

I think this is a much different environment than previously. These tariffs are more wide spread and there appears to be more counter-tariffs coming in retaliation. So this could slow trade in all countries involved. And this in a world already stagnating. Second, due to the financialization of our economy, a 20% stock hit will lower consumer demand, especially in the top 20% who have been spending like drunken sailors due to the wealth effect. The market is wildly over-valued, and this may trigger a big sell off, and recession. And thirdly, consumers have become more used to price increases over the last three years so there will be less pushback. Where in 2018, most 50 year olds, and under, had never experienced an inflationary environment. This time is different 😉

The US has a $1-trillion-plus trade deficit in goods ever year (red line in the chart below). It’s a scandal that this was encouraged to happen by the globalization mongers in the US, and it was taken advantage of by other countries.

Other countries, including Canada and Mexico, hugely benefit from the US trade deficit, while US production got decimated. NAFTA should have never happened. Ross Perot nailed it when said that there would be a “giant sucking sounds of jobs going south.”

If the economy in those countries can only grow by ripping off the US with this one-way globalization, engineered by Corporate America to fatten up their profit margins, well then so be it, and they need to impose even bigger tariffs and start thinking about how to restructure their economy so it functions without sucking on the US. That gravy train should have never happened. And it should be stopped.

https://wolfstreet.com/2024/02/08/us-trade-deficit-in-2023-dropped-19-as-goods-deficit-with-china-plunged-29-imports-exports-of-goods-services/

People got used to price increases, then dug in their heels. Look at cars and houses. Volumes are down. In some cases, prices too.

I guess that the impact on inflation was limited last time exactly for the reason that Trump starts with tariffs on Mexico and Canada. Trade flows were just rerouted through these and a few other countries, including Vietnam, Thailand, India and others.

Do you think the planned tax cuts could alleviate the drop in corporate margins at the expense of higher government budget deficit? Or the receipts from tariffs will balance out the tax cuts?

Wolf, Thank you for being such an independent thinker!

The spectre of Depression era tariffs and their catastrophic effects is often raised by the advocates for free-trade.

How compelling are the alleged parallels?

There was Smoot-Hawley and at the same time there was wild speculation in stocks fueled by debt from unregulated banks. The wild speculation and debt is the immediate cause of the Great Depression. Did Smoot-Hawley kick-off the loss of confidence that caused the meltdown? I don’t think anyone knows. But it is a good boogeyman for the free trade crowd.

The “parallel” is pure BS. And only anti-tariff propaganda pushers spread that comparison. There is no “parallel.”

1. Back then, the US was the largest exporter in the world; and now it is the largest importer. 180-degree different, the opposite. If countries want to retaliate, fine, let them, and they should. Everyone should use tariffs to raise some taxes, and nearly all countries already do, particularly China.

2. Tariffs are already widely in use by all countries, and have been in use forever. Tariffs are very high in China against protected products.

3. The Great Depression wasn’t caused by tariffs. People who say that propagate anti-tariff BS. It was caused by a mix of factors, including the collapse of massive speculation on everything, entailing the total collapse of the stock market, and the collapse of the banking system where money in bank accounts just vanished when the bank collapsed, and companies couldn’t make payroll anymore because their money was gone, triggering huge unemployment, but without unemployment insurance, and so people stopped spending because they ran out of money even if their bank hadn’t collapsed, and it turned into a vicious self-propagating cycle. That’s why we have backstops today, such as backstops for banks (deposit insurance, the Fed’s liquidity tools, strict regulations, etc.), unemployment insurance, a retirement system, etc. Most of these things came out of lessons learned from the Great Depression.

I appreciated how thorough this article was. One aspect I thought should have been included is: Where does the rare earth mineral conversation come into play? Other countries are buying up deposits of lithium, cobalt, etc needed for production of EV and other tech. Hard for domestic production to win if competitors get monopolies on strategic resources, and a tit for tat raising the stakes.

The US has huge lithium deposits and there are now large-scale investments underway to extract the lithium. In the US, these investments (in California, Arkansas, and other states) focus on pulling up the lithium rich brine deep underground and extracting the lithium, then pumping the brine back down. Hot lithium-rich brine has been used in CA for decades to generate geothermal power, and the investments underway now focus on extracting lithium from this brine before pumping it back down.

This is a very different technology than the vast lithium ponds you see in Chile, etc. Exxon is deploying its fracking knowhow to extract the lithium brine in Arkansas. It started drilling the first lithium wells in 2023. These are huge investments, the involve US knowhow, and they’re great to see.

In terms of rare earths, they aren’t rare, there is a lot of it in the US, but they’re messy to mine, refine and process. The US produces about 15% of global rare earths in one location (the Mountain Pass mine in CA), but the mine used to ship it to China for refining. But now refining has started at the mine, production is increasing, and lots of investments are being made. This should have happened a long time ago. But it’s finally happening now.

Essentially, the cause was a lack of regulation. Which Republicans are arguing for now.

We have lithium in East Texas, too, though southern Arkansas has received more of the media attention.

Excerpts from the October 2024 issue of Texas Monthly:

Chemist John Burba developed … direct lithium extraction, in 1995. In DLE, brine is pumped through cylinders made of a fiber-reinforced polymer and filled with crystalline granules slightly larger than grains of sand. Lithium ions get stuck, much like contaminants in an ordinary water filter, but the granules release the prized metal when the cylinder is flushed with fresh water. The process takes less than an hour to extract lithium that would otherwise take months or years to mine or to concentrate through evaporation, and it doesn’t ruin large stretches of land or pollute millions of gallons of water.

In the nineties, Burba designed and built the first DLE plant, in a place ominously called Hombre Muerto, in Argentina. The plant remains in operation today, although DLE didn’t immediately take off because global lithium demand at the time was satisfied by existing mines and evaporation ponds. But as the need for batteries has soared, so has interest in new lithium sources. Last year the financial giant Goldman Sachs called DLE “a potential game changing technology.”

Over the years, to test his invention, Burba has evaluated brine samples from fifty locations around the world. “Most are crap,” he says, relaxing in jeans and black alligator boots in a large house with vaulted ceilings outside Atlanta, a small town a thirty-minute drive south of Texarkana. The brine containing the most lithium he’s found in North America, rivaling the best in the world, lies beneath a one-hundred-mile swath of northeast Texas and southern Arkansas.

Don’t forget the ‘Climate Change’ 1930’s ‘Dust Bowl’.

Bravo. This great depression nonsense is spread through academia as gospel. It’s amazing how corrupt these institutions continue to pedal these lies to support a political viewpoint, not a historical one.

I am not surprised that inflation did not accelerate with the last tariffs.

But costs to many of us went up signficantly. The city of Huntsville was building a new branch library and when the tariffs came out they had to stop for 6 months to go looking for more money to pay the increased cost of the steel in the roof beams. Alabama was extending the limited access section of highway through Huntsville, and the state had to stop that effort for some months and go look for more money to pay for the beams that support the overpasses.

The cost of the steel angle that is used to hang garage door openers went up as well. It was almost as expensive as the garage door opener. Socket wrenches went up and I paid an eye watering price for a replacement aluminum ladder.

I’m sure inflation will not go up again, especially with the new administration telling the FED what inflation numbers to publish. But if the cost increases are anything like last time and spread across a wider array of goods than just metals, a lot of us are in real trouble.

Your comment is BS.

1. Commodity prices are NOT consumer prices. Consumers don’t buy rebar.

2. Commodity prices spike and plunge all the time, they did before tariffs and after tariffs. That’s what commodities do, DUH. Look at the charts of commodities before you post this BS.

For example, steel rebar prices soared from 2016-2017 and fell back in 2018 after the tariffs were implemented, then spiked in 2020-2021, then plunged, and today, and today are about where they had been in 2017.

Alabama has a LOT of steel mills. Why were they buying foreign steel and transporting it across the world instead of locally and across the state?

❤️👍

If you have a look at steel prices (I focus on flat products e.g. HRCb or CRC) and compare ex-works prices in the US with prices in China, Europe or world export you will see a HUGE difference over the last 10 years. Might tariffs have anything to do with US steel mills demanding up to 2 x the world export prices ?

[data from steelbenchmarker]

@Wolf: keep up the good work – very well appreciated!

Yes. More steel is bought locally. Then the steel company hires more people. Then more people are working the district and the local government receives more tax revenue to pay for the increase cost of the steel for the library.

Plus it reduces government cost of unemployment, food stamps, and other entitlements.

Tariffs cause minimal inflation because all goods are already priced to compete with the cheapest producer. You can find a manufacturer of nearly anything in the US – be it lumber, steel, widgets, etc. – and their prices will be competitive with China’s, Canada’s, Mexico’s, etc.

These US manufacturers do it out of necessity. Afterall, you can only charge what someone is willing to pay for a product.

They get away with it by running lean. They’re almost always small-medium sized private businesses with little to no marketing budget.

My company ran into this during Covid. Freight prices and lead times skyrocketed, so we turned to domestic sources for a lot of goods. We were building medical diagnostic workstations at the time and ended up sourcing 100% USA casters, power cords, ethernet cables, etc. The prices were very comparable; it just took more effort to find the suppliers because they’re not household names.

Whether or not these new tariffs will cause inflation will be a matter of our domestic supply capacity, I think. Our domestic sources should be able to ramp up SPF and oil production just fine. Fruits and Vegetables, combined with deportations, will probably see a rise.

Exactly.

Our border hopping competitor lives in one of the most expensive zip codes in the country and flies freely on a private jet. I live in a corn field and drive a 10-year-old pickup truck. I mow my own grass but hope not to someday.

I am debating if we can provide raises this year. Why? Because we have no pricing power. I have to find the money to do it because it is not hanging out at the bottom line. We have similar product designs, and similar machinery (some of ours is actually newer and more efficient).

American producers exist on razor thin margins because it is all we can do. We gobble up the crumbs falling on the floor at the import feast. Eventually the math just doesn’t work, and we close up shop. That’s the game.

A 10-15% tariff levels the playing field. 25% tips the scales slightly in our favor.

Another piece people just don’t consider: Businesses like ours prop up the healthcare system in our rural area. Hospitals can’t make ends meet serving only folks on Medicare and Medicaid. The reimbursements are low. Another 1/3 of patients are underemployed and uninsured, so they become a write off. Doctors roll out the red carpet when our employees hand them the Blue Cross card. We don’t mind carrying that societal burden if we can pass the cost onto customers. That cost is between 4 and 10% of top line revenue! We still provide a really good plan… maybe because we are stupid, or we feel it is the right thing to do.

Bingo.

Border hoppers have won big in the truck equipment world but we domestic producers still have enough capacity to soak up the market share with the scales tipped slightly back in our favor. No price increases necessary. The additional fixed cost absorption of being much busier may actually allow us to cut prices.

I am trying to not get too excited but cannot overstate how big of a deal a 25% tariff on Mexico is for our domestic manufacturing operation. It is absolutely massive.

Assuming they stick, we will be investing in machinery and hiring for living-wage jobs in small town USA at an aggressive pace this spring.

This is a great result.

There’s a piece missing in this article that I don’t understand. If prices are already the maximum they can be without causing demand destruction, then the inflation rates from 2021 – 2023 should not have happened the way it did. One would expect inflation from the COVID supply chain disruptions and free money from Trump and Biden. But the expectation would be a short bump in prices on domestically produced products that had little to no supply chain issues and a return to prior prices. That didn’t happen. Many companies simply took advantage of the expectation of higher prices, raised them, and saw corporate profits go through the roof.

“One would expect inflation from the COVID supply chain disruptions and free money from Trump and Biden.”

Yes, that was part of it. The other part of it was $4 trillion in money printing by the Fed in three years. So those are among the triggers.

Inflation in durable goods then vanished, with many prices plunging starting in mid-2022 because, as you say, demand destruction from high prices, see new and used vehicles, computers, etc., triggering large-scale deflation in durable goods, see the charts in the article. So in terms of goods — which is what tariffs are applied to — it was a “short bump” (18 months), as you said. So that is what happened, and your statement, “That didn’t happen,” is the only part you got wrong, while nailing just about everything else.

The first sticker shock will show up in food and energy. People are still reeling from those recent inflationary price hikes. You can expect a loud whaling that will make the politicians sweat.

Ignorant BS. The US is the largest energy producer in the work and the biggest exporter of natural gas in the world and large exporter of petroleum and petroleum products (gasoline, diesel., etc.).

The US is a huge food producer and exporter, and sure people like to drink French wines and Mexican beers, but they can buy much better US wines and US craft brews.

That kind of ignorant BS is part of the anti-tariff bullshit being spread around. Don’t do it here, spread this BS somewhere else.

All energy is not the same. All crude oil is not the same. Typically, refineries are tailored to certain kinds of crude oil (eg heavy sour crude or light sweet) so the tariffs may increase some regional fuel prices until either new flows of inputs into the refineries are established and/or the refineries are modified to take different crudes.

Good. So prices go up short term. Then the refineries make adjustments for local crude types. Now, after the tariffs are over, they will still need local crude because the refineries cannot accommodate Canadian crude.

Good for the local oil companies as they need to produce more oil and good for the local refineries as they do not have to worry about future trade wars anymore.

“All energy is not the same. ”

Absolute BS. All hydrocarbons are fungible because they serve the same purpose: creating energy through combustion in order to do work.

You’re so wrong that not only is all oil interchangeable, but oil is even interchangeable with other types of hydrocarbons such as natural gas. Look at how China is switching their long-haul trucks from diesel to CNG as Exhibit A.

“until either new flows of inputs into the refineries are established and/or the refineries are modified to take different crudes”

In other words – until the market arbitrages away the price difference, which is INEVITABLE when different hydrocarbons diverge significantly in price.

In time, things that do the same thing will eventually sell for the same price.

Sounds like we have an economics major on our hands here.

“In time”, perhaps, but in the short term, no. For heavier crudes you need extra cracking equipment, for sour crudes you need more hydrogen production to remove the sulfur, etc. That takes time to build. In the meantime the refineries either reduce production or pay more to get similar crudes from other places.

BTW, if you go to https://oilprice.com/oil-price-charts/ you can see that Brent crude, for example, always sells for a premium over WTI crude.

Nit picking the differences between various grades of crude is irrelevant when oil in general is 3-4x more expensive than natural gas on an energy-equivalent basis.

Natural gas is also cleaner burning than gasoline/diesel etc. And it’s easy to design an engine that can run on both.

All hydrocarbons are fungible. You can’t ignore natural gas – it’s now another type of oil.

We don’t have retail distribution infrastructure for CNG for vehicles, so, no.

But stationary engines can easily be switched to burn CH4 or C3H8. And there are chemical techniques for refining straight-chain hydrocarbons into those found in liquid fuels.

Anything is possible when the price difference is big enough.

Efficiency and optimization SHOULD cause the price of durable goods to go down over time. Henry Ford did it in the 1910s – Musk should be able to do it now. A Tesla model 3 should cost HALF as much over time. Why not? A Model 3 at $19,999 would probably fend off BYD quite well.

During Trump’s first term we saw a nice flat or slightly declining DG price level. Services – that is the cost of PEOPLE – should rise slightly if low inflation is indeed desirable. 1-2% a year. People increase their value beyond that with experience and quality so a worker should see larger pay improvements for productivity.

What I think we all really do want – and what Trump is trying to force after three decades of decline – is for the “bicycle factory in Ohio” that had 900 workers and moved to China in 1998 to move BACK to Ohio in 2025 and now have 150 workers and a lot of robots, powered by abundant US energy. 150 higher paying factory jobs is better than zero. This isn’t going to happen overnight but it could happen in a year or two. Multiply this by a thousand different products and that’s a lot of jobs back in the US. I’d like to hear the argument of why it’s better to employ four million Chinese workers building things by hand vs. a quarter million Americans running automated factories here.

+1

We have been re-engineering a flagship product for the last two years to wring out manual labor and make it “robot friendly”. It’s the only way we see to survive in the truck equipment industry from a US manufacturing base.

We have plowed the entirety of our free cash flow for the last three years back into capital (mostly robotics) investment. Hoping to take a breather from that plan this year. My truck is getting tired, and the garage roof needs to be replaced.

There is minimal grunt work left in the product. Most of it is now loading fixtures, metals, and programs into CNC machinery and hitting go. The fit and finish is better than ever. We shaved about 10% from unit cost last year, with a goal of another 10% this year.

We can pay our people well if their labor is well-utilized.

A tariff on foreign imports would be icing on the cake we’ve been baking for a while now.

It IS different this time. Last time the Trump tariffs were not focussed on Canada. We have decades of cooperation between the two countries due to our proximity and the ease of transport across the border. Businesses like the auto industry are highly integrated, and are facing major disruption.

And Canadians, except for oil, buy more durable goods from the USA than the other way around.

My Canadian friends are pissed and worried by the new tarrifs. Trust is being eroded. My mail box is full of suggestions on how to avoid buying American made. “Made in USA” is now a dirty word with the friends I talked to. People will shift to buying Canadian, Chinese and EU products where they can.

And moving production to avoid tariffs works two ways. This happened a lot in Canada in the 1900’s when tariffs were higher. Many companies moved at least part of their production to Canada to avoid tariffs.

“Buy Canadian” was never a huge thing here. People were barely aware of the difference between buying Canadian or US goods. They are now.

Canadas politicians are now facing pressure to reduce shipments of resources to the USA. Short term, Trump will see a blip in tariff revenue, and will take the credit. But now Canada is highly motivated though economics and anger to build long term infrastructure like pipelines and refineries to be better able to ship our resources to Asia and the EU, and even from West to Eastern Canada. The US has been buying oil at a discount from Canada, and then selling gasoline back to Canada for decades. Now there is the political will to put an end to that.

Yep, tariff inflation is a one time thing, but the damage to Canada’s economy and the the loss of exports to Canada, and the increased cost of resources could be felt for decades.

What about effects on energy/oil(gasoline) prices? Things that the consumer can’t really control with our demand.

The US is the largest energy producer in the work and the biggest exporter of natural gas in the world and large exporter of petroleum and petroleum products (gasoline, diesel., etc.). Much of the oil being imported is refined and processed, the resulting value added products (gasoline, diesel, petrochemical products, etc.) are sold to other countries.

Gasoline prices spiked and plunged for all kinds of reason and just pure speculation, but not because of tariffs, LOL

And we can easily extract and refine significally more if regulations are changed. Penty of domestic energy supply just waiting to be utilized…

So f the end is near with these evil tariffs.

Please benchmark the dollar this past friday with the countries who

we increased tariffs on. Track it and lets see how it plays out.

Will it be a repeat of his 1st term.

Everyone should support tariffs and the rebuilding of USA’s industrial base. The country was being taken advantage of by the rich through outsourcing everything for cheap labor. Make things in America!

The stock market is not the economy. It doesn’t need to go up 25% per year. I support Trump on this one.

Then why did Trump just delay the Mexican tariffs for one month all due to fentanyl? Does not appear it was EVER about raising tariff revenue..

The billionaires win again, as I pointed out, and now they’re running the show. They have always subverted Trump’s tariffs. Musk was planning to build a Tesla factory in Mexico to produce the lower-end EV. Musk imports components from China, Mexico, and other countries for US assembly. So he hates tariffs. That said, and to Musk’s credit, Teslas have the most US content of any models sold in the US. Honda models are closely behind.

GM is the worst. It’s barely a US automaker anymore. It builds almost 30% of its US vehicles in Mexico, it builds vehicles in Canada and imports them, it builds cars in China and imports them (Buick Envision). It imports components from China, Mexico, Canada, and other parts of the world to assemble in the US. Tariffs would change the math for GM and push it to follow Musk’s lead and produce more in the US, which is the purpose of tariffs. Maybe GM should quit incinerating cash on buying back its own shares, and instead investing it in top-notch production facility in the US, no?

but is it really so wrong for trump to use tariffs as a stick and carrot for something completely unrelated? The situation at the border is unacceptable for a variety of reasons. mexico showing good faith there is a decent reason to give them something on something else.

Wolf, your annoyance over GM’s shifting production of finished vehicles as well as the purchase of parts (content) is shared by a columnist in a Detroit online news aggregator https://www.deadlinedetroit.com/articles/32777/starkman_anti-maga_mary_barra_slashed_u_s_parts_content_of_gm_s-mexican_made_2025_evs_subsidized_by_u_s_taxpayers . Per the column, the Mexican built 2025 Chevy EV Blazer and EV Equinox will have only 12% parts manufactured in the U.S. and Canada, compared with 62% percent of the 2024 models. The vehicles are still eligible for the $7,500 consumer tax credits. The vehicles had 18% Chinese-made parts in 2024, will only have an “insignificant” number of parts in 2025. In 2025, Mexico and South Korea content will be 46% and 20% respectively. The total domestic content of GM’s vehicles fell to 54% in 2024 from 66% in 2015. Per Bloomberg, in 2022, there were 33 auto parts makers registered in Mexico and 18 of these exported parts to the U.S.

The 2024 Cars.com American-made index had no GM or Ford vehicles in its top 20. Tesla had three and Stellantis had two.

Most GM cars sold in Mexico are imported from China.

“The billionaires win again”

Exactly. The stock market was going to dump, and all crypto, so it was called off. Trump will NEVER allow an asset price correction.

When trade is an exchange of steel for copper, or apples for bananas, or coal for grain, the transaction is a net benefit. Both parties get something they want that they didn’t have before. That is a good trade.

The billionaires and the politicians in their pockets don’t want you to think of it this way, but when trade is one side’s standard of living versus the other side’s standard of living, the whole thing is a raw deal for whoever lives better. This force has wrecked the American rust belt for the last few decades to the point that millions of people are angry enough to vote for you know who.

We in the American Midwest are not asking for handouts or welfare. We want to build things, and we are pretty good at it. We want to trade that value-creating activity for a reasonable standard of living. Our people are underemployed. We are far better off running CNC machinery or assembling equipment than working at the counter at Arby’s or Dollar General.

When given the choice between buying from the American Midwest or a from some town south of the border, the people on the coasts simply choose whatever is cheaper. They don’t realize that they are often shooting themselves in the foot in doing so. They should consider buying from the people who share their national debt!

It should come as no surprise that private union membership has cratered, and the middle class continues to fade. Workers have no bargaining power against a foreign workforce and the constant threat of plant closures. Local manufacturing is a foundational piece of a healthy middle class.

I swear the concept of value-creation has been purposely deleted from our national conversation. Value creation is what generates our standard of living. We cannot all just kick back, drink wine, and sell each other insurance!

“We in the American Midwest are not asking for handouts or welfare. We want to build things, and we are pretty good at it. We want to trade that value-creating activity for a reasonable standard of living. Our people are underemployed. We are far better off running CNC machinery or assembling equipment than working at the counter at Arby’s or Dollar General”

Amen.

Looking at the gross margins and net margins of some large U.S. companies, including the Mag7, they certainly have some room to absorb tariffs without raising prices. Maybe they will have to reduce their stock buybacks, reduce wasteful spending, and slightly reduce executive bonuses to look good.

How the stock markets react will be interesting. If the market is radically overpricing the value of a company on historical P/E terms pre-tariffs, will the market continue to overprice the value those stocks post-tariffs? And by how much?

Don’t confuse irrational markets with the actual economy.

Not sure if any of the MAG7 will be effected much? Meta, Google, Microsoft, and Amazon (AWS) make most of their money selling services. Maybe Tesla if they import but don’t they try to make cars in the U.S. or the local countries? NVDIA may take a hit but they only have $130 billion in sales a year. Total revenue of all companies in the SP500 is 16 trillion. So NVDA is not going to move any needle as their revenue is only .8% of the entire SP500 revenue.

Imports are not a very big percentage of the US GDP. Plus companies that produce locally will see margin increase. So that will be a positive impact? Plus, because of COVID, there has been an onshoring trend recently.

7:07 AM 2/3/2025

Dow 43,930.06 -614.60 -1.38%

S&P 500 5,932.17 -108.36 -1.79%

Nasdaq 19,186.47 -440.97 -2.25%

VIX 19.26 2.83 17.22%

Gold 2,870.00 35.00 1.23%

Oil 72.98 0.45 0.62%

You are going to have to update your daily cut and paste to real time updates , because the markets are already walking back those numbers.

Buy the dip doesn’t wait for the next day.

MW: Barron’s Tesla Stock Is Plunging. Both Trump Tariffs and Canada’s Response Will Hurt.

MW: Dow slumps 550 points as S&P, Nasdaq drop after Trump announces tariffs. Dollar soars, bitcoin slumps.

10 year barely moved today.

1 year still pricing in a rate cut or two.

These clickbait articles freaking out about inflation are a joke. Where were these people for the last 3+ years???

Then everything reversed, including the tariffs.

I would have said “indirect tax on the profit margins of foreign producers”. Direct tax sounds like the foreign producer is transferring money to the US gov. Only the importer pays directly.

Tariffs last time were also on specific HTS codes, not as broadly applied. The first few tranches did not include many consumer product (e.g., the t-shirt used as an example in the article above), but mostly inputs to products (e.g., steel and aluminum) that have multiple inputs (so the impact on total price was smaller). The tariffs on HTS codes related to a broader range of consumer products only started to kick in right as COVID shut down the world. Prices went up in the year after COVID due to the combination of higher costs (from tariffs, transportation, shipping contain shortage, etc.) and we saw inflation at that point in time.

It isn’t really an apples to apples comparison to look at the tariffs from 2018-2020 and say, oh, they didn’t meaningfully impact inflation so this time it won’t either, given the vast differences in what is being tariffed, the speed with which tariffs are being implemented this time, and the fact that we aren’t currently in the middle of a global pandemic. The fact that the stock market was so negatively impacted last time should scare people even more this time, as companies will have even less ability to absorb the costs this time around, both due to the nature of the products being tariffed and the speed with which these are being put into place (limiting their ability to renegotiate prices and find alternate sources of supply).

I’m skeptical but learned from your post and will try to keep an open mind. Namely, this is a powerful statement that I and many others may not factor heavily enough: “Tariffs are good for the US economy because they change the math for domestic production, and the primary, secondary, and tertiary effects of producing in the US are great for employment, tax receipts, household incomes, etc.”

That said, a few things come to mind.

1. There are just too many variables to conclude that tariffs didn’t negatively impact inflation in 2018-2019. Just because durable goods inflation stayed low, doesn’t mean it wouldn’t have been lower otherwise. It happened when inflation was very reasonable, so whatever negative impact it had (if any) may not have mattered as much or got much attention, compared to if it has an impact now.

2. “But even for the S&P 500, new tariffs are just a one-time hit. So if the new tariffs cause a company’s gross profit margins to decline from 20% to 19% in 2025-2026, that’s it; they would not decline every year, but just once after tariffs are implemented, and then remain stable.” I may be missing something but unless these tariffs are short-lived, the price increases will continue to impact business margins indefinitely. What will cause the impact to go away after the initial adjustment?

3. While the impact on consumers may not be as huge as anticipated because they may choose not to spend more on things, it will still cause a fair amount of small businesses that import products to go under. Yes, it’s a risk of operating a business, but it couldn’t have been foreseen a few years ago, and it’s still sad.

4. This time, it sounds like the tariffs could hit fruits and veggies pretty hard. When combined with climate issues in CA/the south, that could be very impactful and hard to avoid, even though we hate, hate, hate price increases.

5. These tariffs seem more widespread and impactful. I expect this to be more of a “shock and awe” type of negotiating tactic and he will find a middle ground, but this seems more extreme than the previous tariffs.

Thanks as always for the in-depth analysis.

This is very much along the lines of what I’ve been thinking.

Tariffs may turn out to be a net positive, but I think there’s going to be a fair amount of nuance here.

And maybe the increase in manufacturing will help us to offsets the medium-longer-term impacts of lost jobs from AI in the future… talking to a friend in the IT world the other night, he’s been tinkering with a lot of AI stuff on the side, and he sees it crushing a lot of developer/coding jobs. And that’s only one sector…

“….the tariffs could hit fruits and veggies pretty hard.”

LOL, where did you hear this BS? In anti-tariff clickbait producing billionaire-owned media?

I admit, i was curious about potential impact, so i googled and found some clickbait articles. But another quick search makes this seem like a legit concern. Source: USDA.gov chart 107008

“Between 2007 and 2021, the percent of U.S. fresh fruit and vegetable availability supplied by imports grew from 50 to 60 percent for fresh fruit and from 20 to 38 percent for fresh vegetables (excluding potatoes, sweet potatoes, and mushrooms)”

“In 2022, Mexico and Canada supplied 51 percent and 2 percent, respectively, of U.S. fresh fruit imports, and 69 percent and 20 percent, respectively, of U.S. fresh vegetable imports in terms of value”

Great synopsis, Wolf, makes perfect sense, thank you for it.

You must not have been around when the deindustrialization of the US started. It was a real sight to see large steel mills shutting down and thousands of people losing their jobs. My dad included. The cities went to hell, too. But that’s ok as WAL-MART and Kmart came in a provided great jobs for these poor folks.

Who famously said we are becoming a nation of shopkeepers?

Sorry John, this above post was aimed at the person above you.

I’ve seen “a nation of shopkeepers” used many times over the years, always referring to the Brits, sometimes contemptuously.

This time may be a bit different, but the the data outlined here clearly shows that there was very little impact last time. Just the same, I am definitely increasing my own production of avocados and citrus. Based on the producers I know personally, there will be significant price increases here, not just from the tariff, but the labor costs as well.

Glad to see that this article, and the comments, made it to Google News (scroll down a little), with the first chart displayed.

that link shows multiples for me

Scroll down until you see my chart on the left. Then click on it, which takes you to my article. New articles are being posted in this feed all the time, and older stuff moves down. By now it’s near the bottom of the feed.

Thanks Wolf for this clear-eyed assessment of the effects of Trump’s tariffs. There is another factor in this hullabaloo over tariff’s on Mexico and Canada is their failure over the past decade to more effectively deal with the illegal drug manufacturing going on in their countries using smuggled chemicals from China. A few years ago, Sam Cooper, a Canadian journalist wrote a book, Willful Blindness, that documented China’s underground banking empire and how they use it to support the drug trade. Ed D’Agostino recently did an excellent interview with Cooper on MauldinEconomics.com about this.

The US economy is primarily a service based economy now. If this is (partially) about protecting US job against off shoring perhaps there should be some sort of tax on outsourced labor as well. Recently what I’ve seen in a lot of white color jobs in tech, engineering and finance is the laying off US workers to then turn around and hire in Indian. Taxing that would also bring a lot of extra tax money.

Or, with the H1B visa, drives me nuts when I see people say that we need to bring people from other countries because they have skills that are not available here.

If that’s the case, prove it and make them get paid at least the same amount as the comparable US worker. Stop under cutting US wages by 20% or whatever they are discounting.

Heck, there should actually be a premium paid for H1B visas – why shouldn’t the US worker have an even playing field or even a slight advantage over the imported worker?

Very compelling analysis, thank you!

Joe Biden put a 100% tariff on Chinese EVs in 2024, for exactly the reasons you state.

I feel that most people who have done any decent amount of reading on tariffs are aware that they are a reasonable economic tool for specific goals. Tariffs as a concept are neither good nor bad, but as a tool they can be used in both good and bad ways.

One area that seems to be missed in the analysis of the article, is how much workforce capacity does the US have to ‘re-shore’ all these jobs? For things like steel, I imagine there is a good amount of skilled capacity available. For things like oranges and limes, perhaps not so much? My understanding is that US employment levels are historically high. Also, protecting high paying skilled jobs makes sense, but low paying unskilled jobs not so much.

“…how much workforce capacity does the US have to ‘re-shore’ all these jobs?”

1. There are currently 7 million people in the US without a job that are actively looking for a job (the narrowest definition of “unemployed”). There are many more that would like a job but haven’t actively looked for a job in the 30-day reference period.

2. Modern day manufacturing in the US would be largely automated, with jobs for highly qualified workers and tech people. It’s no longer the simple manual labor of yore. That’s why US production is so important because automation (industrial robots) is a high-end technology, and the US needs to be the leader in it, but has given up this role because manufacturing was offshored to China.

Change can happen very quickly.

Mexico agreed to use troops to help to stop the drug trafficking, and supposedly the tariffs are suspended for now.

Avocado toast and tequila shots for everyone!

I don’t believe anyone said tariffs won’t increase prices. The market will determine if the retailers can pass on some or all of the additional cost as discussed in the article in items 4 and 5 under “Some basics about tariffs.” Thus, the entire premise upon which you’re playing devil’s advocate (“If Tariffs won’t increase prices, and only eats into the profits of companies importing goods…”) is flawed because it mischaracterizes what the article actually says.

This article is pure gold.

Per your tariff comment in point 3: Your example shows a 90% margin for a $9.99 T shirt??

Holy cow– that seems like an amazingly high margin. Are they really typically that high? No wonder T shirts aren’t made in the USA. And no wonder a 25% tariff won’t show up in retail cost.

You’re looking at the difference in the purchase price of a T-shirt in bulk from a factory in Bangladesh and retail price at a big-box store the US. These is a lot of stuff in between that needs to be paid for, from transportation to running the entire operation that come with distribution and retail, including the costs of returns, wages and salaries, fuel, buildings, etc. Everyone needs to make money in these operations. Retail is expensive. If there are more middlemen involved, such as a small retailer would have, then the price of the T-shirt would have to be much higher. If the small retailer buys the T-shirt for $10 from a distributor, they’re going to charge $20 retail price to survive.

Honestly, this is not a topic that I care about at all. I know it affects me but I have no interest in trying to unravel the hows, whens, and whys of the matter. I’d rather read some Hammett.

But then I wake up to a fresh Wolf Street posted ~3 AM followed immediately by some insightful commentary from our host. Then he’s back at in 5 hours later correcting uninformed perspectives – clearly this is something he’s passionate about.

I guess I’m gonna have to study up, because if it gets Wolf this excited there’s probably something to it.

You got that right!

Great article. Lots to think about. Another thing to remember is USD exchange rates. For example I think CAD has lost 15% or 18% against USD in the last 12 months. A declining currency will probably also increase CAD costs to a degree, but I notice tariff announcements also sparked a strengthening of USD. Many countries will allow their currencies to weaken and that will absorb some of the tariff impact.

It will be interesting to see if, perversely for Trumps state desire for lower rates, that the impact will be higher rates. If Tariffs work it seems like that should contribute to a lower flow of USD overseas and thus if foreigners are going to buy Treasuries with precious USD, those rates will have to go up.

Generally I think we have to be a little humble in our thinking that we can predict what is going to happen. The system is vastly complex and more and more artificial. Our normal understanding of cause and effect may not operate as we think.

I did read an interesting article that focused in on the elimination of the exemption rule that allowed packages of less than 800 USD value to transit tariff free. The Trump executive orders, specifically cancelled those exemptions. The article stated that the USD volume involved was 48 Billion/year.

“I did read an interesting article that focused in on the elimination of the exemption rule that allowed packages of less than 800 USD value to transit tariff free. The Trump executive orders, specifically cancelled those exemptions. The article stated that the USD volume involved was 48 Billion/year”