Huge upward adjustment of total employment coming in February when the BLS incorporates the wave of immigrants into the data.

By Wolf Richter for WOLF STREET.

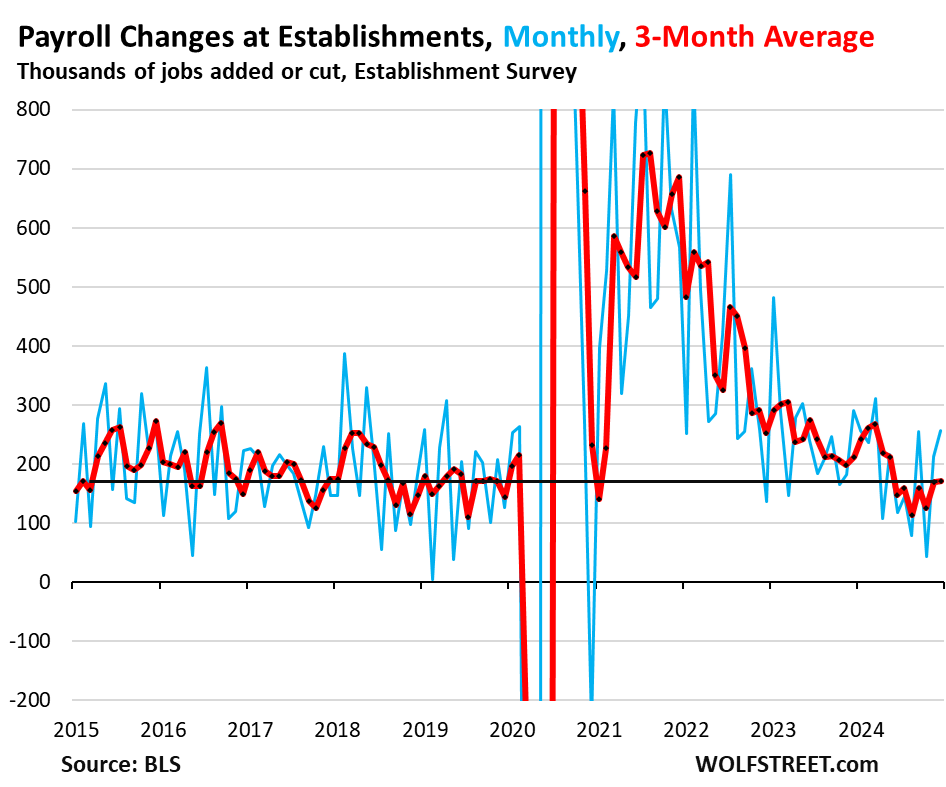

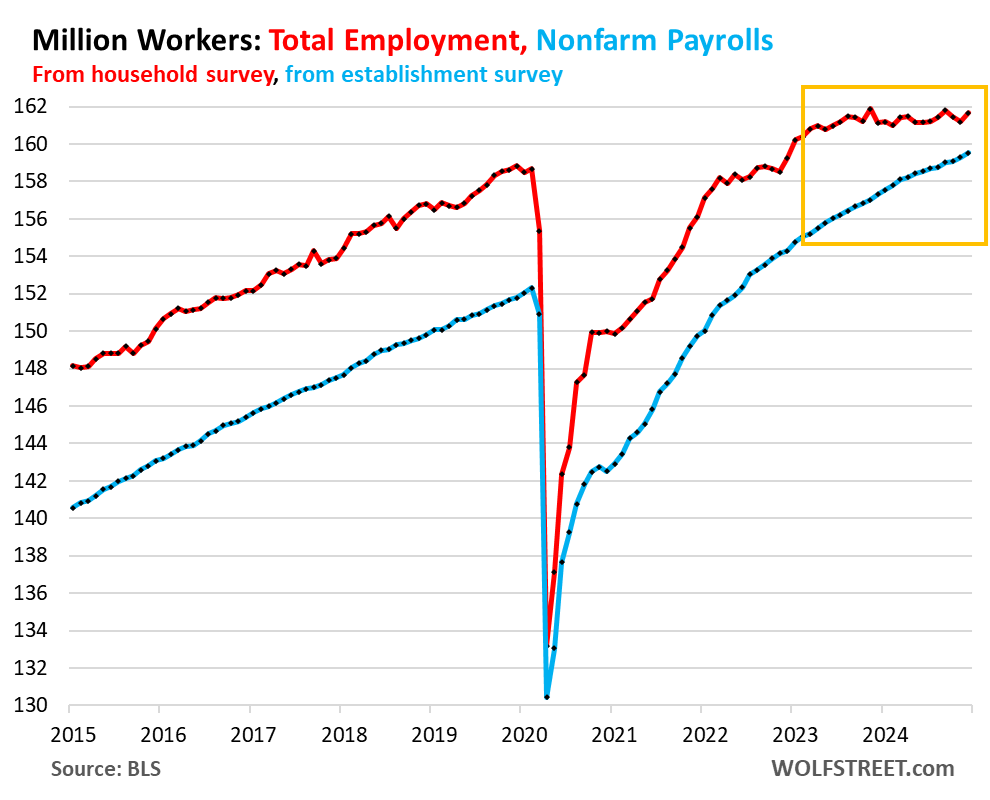

Nonfarm payrolls jumped by 256,000 in December, after having risen by 212,000 in November, to 159.5 million jobs, according to the Bureau of Labor Statistics today (blue in the chart below).

The three-month average rose by 170,000, same as in the prior month, and both had been the biggest increases since May (red). The three-month average irons out the month-to-month squiggles, including the effects of the Boeing strike and the hurricanes that had hammered down October’s job gains but were recaptured in the following months.

Over the past twelve months, employers added 2.23 million jobs, roughly 5% more than the three-year average before the pandemic. These are healthy job gains – in a way, surprisingly strong job gains, given the relatively high interest rates.

Fed rate cuts move further into the distance. The strength of this labor market and the growth of the economy that has been well above the 15-year average – despite the relatively high policy rates by the Fed – have led many to believe, including Fed governor Michelle Bowman yesterday, that the Fed’s policy interest rates are in fact already close to or at “neutral” and don’t need to be cut further to maintain solid economic growth and a healthy labor market.

And upside risks to the inflation outlook and the recent re-acceleration of inflation metrics have further darkened the future of any rate cuts. Powell himself had said at the press conference that “we still have work to do.” Maybe those 100 basis points in cuts is all the economy is going to get, as the Fed is gingerly shifting back into its wait-and-see mode.

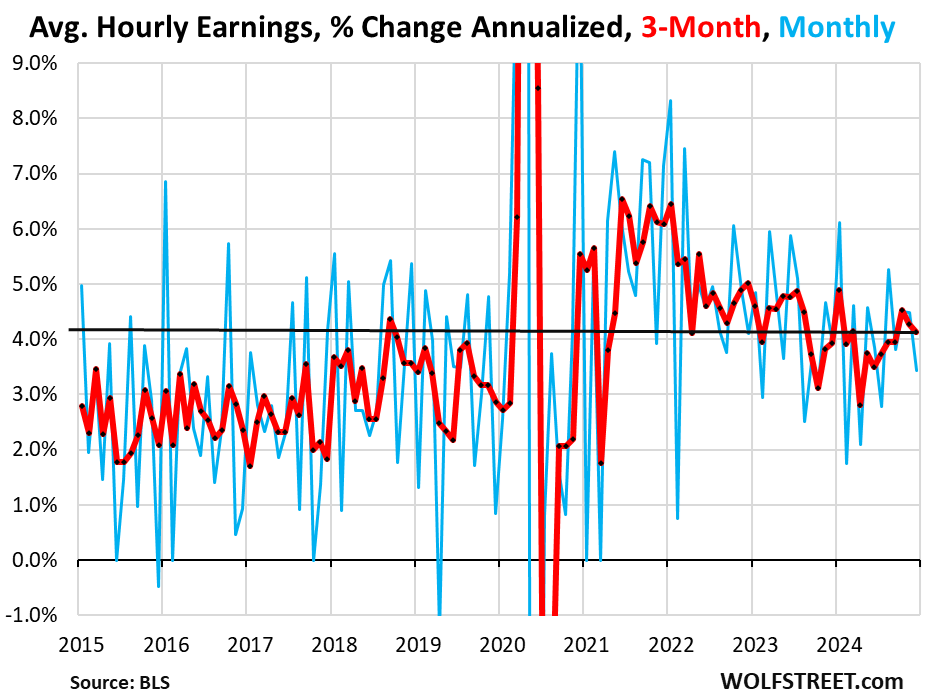

Average hourly earnings rose by 3.4% annualized in December from November, after two months in a row of 4.5% increases (blue line). The three-month average rose by 4.1% annualized in December from November (red).

Year-over-year, average hourly earnings rose by 3.9% in December, similar as in the prior two months. The job gains in those three months were the highest since May, and substantially above even the peaks of the 2017-2019 Good Times period.

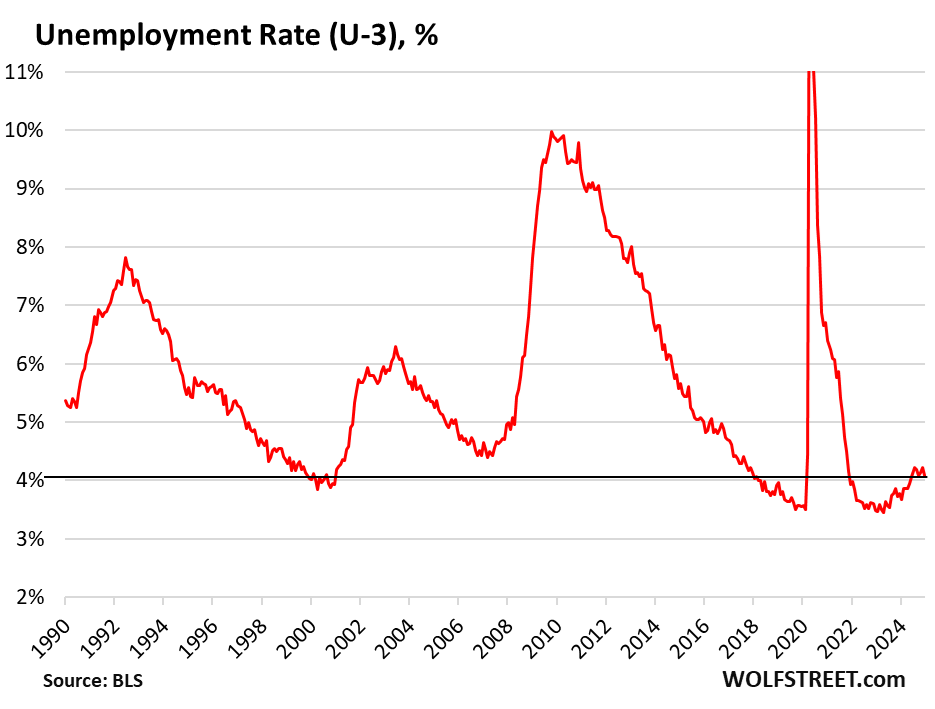

The headline unemployment rate (U-3), based on the survey of households, edged down to 4.1% in December from 4.2% in November. Unrounded, it was the lowest since June. Over the past seven month, the unemployment rate has averaged 4.1%, a historically low unemployment rate.

The unemployment rate = number of unemployed people who’d actively looked for a job over the past four weeks, divided by the labor force (number of working people plus the number of people actively looking for work).

December’s unemployment rate of 4.1% is below the Fed’s median projection for the end of 2024, which it had lowered to 4.2%, and is below the Fed’s median projection for the end of 2025 (4.3%), according to the Fed’s Summary of Economic Projections released at the December meeting.

In late 2023 and in the first half of 2024, the unemployment rate had zigzagged higher from record lows, and the trend was up, and by mid-2024, the Fed started projecting rising employment trends amid weak job creation.

But that up-trend of the unemployment rate broke in the second half. Job creation has stabilized at healthy levels, and the unemployment rate has stabilized around a historically low 4.1%, and the Fed’s projections have stabilized a well.

Employment to be adjusted in February for 8 million new legal and illegal migrants.

The BLS uses the Census Bureau’s population data to extrapolate the employment data from the household survey to the overall population. The household survey generates total employment, the labor force, unemployment, unemployment rate, etc.

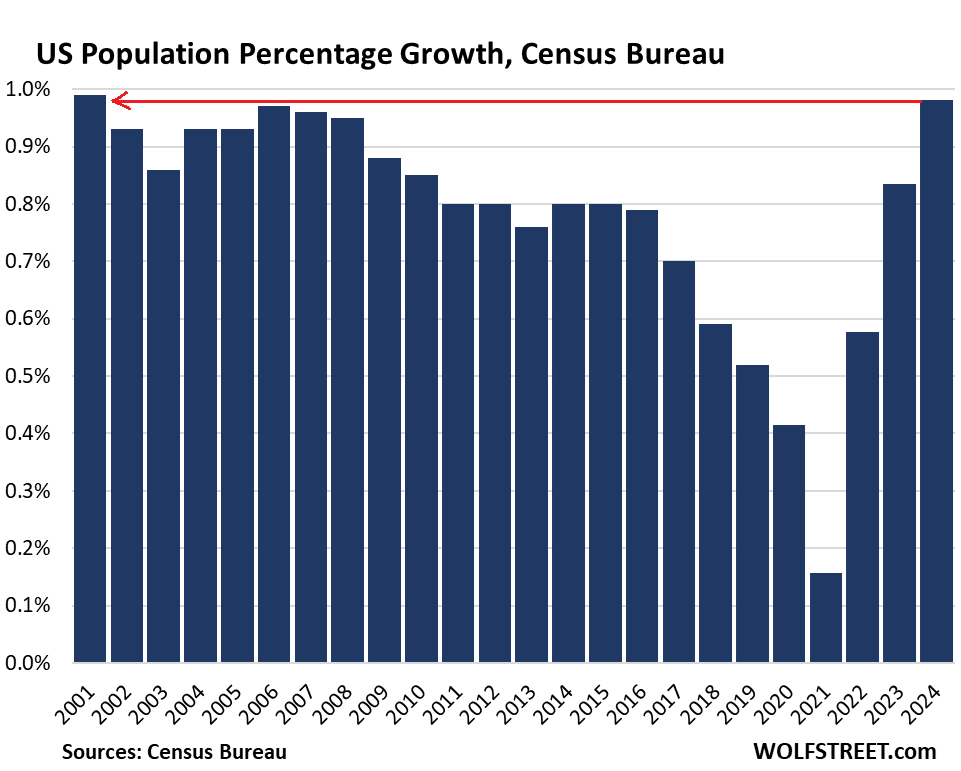

On December 19, the Census Bureau released its annual revision of the US population data, showing that the US population soared by 8.01 million people in the three years from July 2021 through July 2024, mostly from net-immigration, both legal and illegal. Many of these immigrants are already working, or are looking for work.

This population surge is not included in today’s employment data, but will be included in the employment data to be released in February, the BLS said today.

In percentage terms, the US population increased by nearly 1% in the 12 months through July 2024, the biggest increase in 23 years (we discussed this in detail here).

We expect large up-adjustments of employment, labor force, and related metrics. We expect to see a spike of the employment level for January that recaptures the entire adjustment for the three-year period (the BLS doesn’t revise the prior years with the population data, it does it all in one fell-swoop for the month of January).

So next month, the up-adjustment of total employment from the January household survey, plus the inclusion of the previously announced downward revisions of nonfarm payrolls from the establishment survey should re-establish the historic relationship between the employment level of the household survey and nonfarm payrolls from the establishment survey.

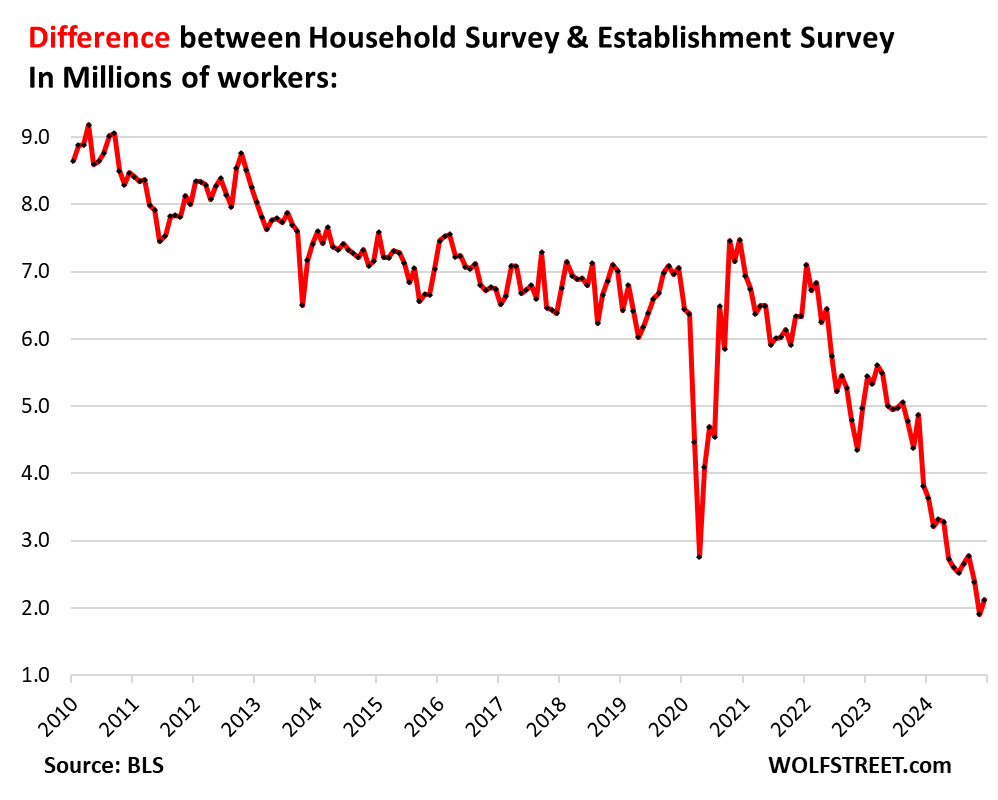

The household survey includes workers who are excluded from nonfarm payrolls reported by establishments, such as self-employed workers whose businesses are not incorporated, farm workers, and private household workers. So, total employment as depicted by the household survey is typically 6-8 million workers higher than nonfarm payrolls. But that difference has shrunk over the past two years and was just 2.1 million workers in December.

Total employment, lacking the new migrants who are working, has been relatively flat since mid-2023, and grew only slowly in the prior year (red), while nonfarm payrolls have continued to rise at a solid pace (blue).

We expect the population adjustment in February to create a spike in the red line for January; and we expect the inclusion of the benchmark revisions to lower the blue line somewhat; and the combination should re-establish the typical spread between the two:

This is how the spread between the employment level in the household data and nonfarm payrolls has shrunk from 6-7 million in prior years to 2.1 million in December. We should see a very sharp reversal next month back toward or over the 5-million line:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

MW: The Federal Reserve is seen as ‘very comfortable’ with rate-cut pause. But are hikes now on table?

So with the fires in socal, 100k+ people displaced what is the likely impact to the overall economy? Certainly certain industries will take a hit while other get a benefit. Given the size of the countries economy we seem to weather these things well.

with sabotage jerry in control count on OPPOSITE

What we see in Hurricane Country is that IMMEDIATELY after a major storm people have to spend on the lowest tier of Maslow’s Hierarchy… Food Clothing and Shelter. Some of that money comes from savings, some from insurance, and some from government intervention.

After that, the people who CAN rebuild start to do so. Not everyone can though (or wants to). IF (and it is a BIG if) you still have housing in your area following a storm then your personal situation can improve quite a bit because employers are desperate for workers.

Lots of very interesting developments possible with Trump coming in.

Very historical things to live through.

Good Health to all to sit back and watch for the full 4 years

Yeah, I am concerned negative things.

I think that Don Trump from Queens stands at a historic precipice that will either restore the rights of agency to every citizen for our persona, the foundation of what makes America the land of milk and honey.

AI is a Trojan Horse whose mission is too train the input set to minimize the sum of the squared error in attaining the desired outcome.

Best wishes to everyone

only few hundred land mines biden and company laid

Smile and wave boys. Smile and wave

Seems like “neutral” would be moving a quarter up. The push for lower rates is ridiculous.

They can bust the bubble by saying they are thinking about raising and watch the market blow up. And the new president have a meltdown.

This is an economy where you want to work, you got a job. There is opportunity.

With the higher prices on “everything” you better want to work. Got to have lots of money for the great future that awaits.

So…get up off your ass and go to work you lazy bum.

Nope. I’m downsizing and watching. Should be more interesting than the media, now with commercials on all the streaming services.

Quarter up sounds like the answer next go ‘round

yeah it’s an economy where you want to work, and you get a job. but the wages the job pays don’t buy you assets at reasonable valuations.

I may be wrong in my analysis but, I suggest, Trump is inheriting the maturation of the previous Trump economic agenda of tax cuts for the wealthy, especially real estate, capital gains, and carried interest loophole.

None of which applies too my taxes which have gladly paid for the past 60 years. Feeling that America has always been a social Democracy.

The everyday people are the spice.

dang, interesting thought, but hardly novel here at wolfstreet. Many commentators have opined that GDP has been goosed by deficit spending for years.

Had they waited in September, they would have fairly quickly seen.

Cutting 100 basis points, including 50 in Sept, was — even if they didn’t plan it this way — a pretty smart move: it caused longer-term yields to spike by over 100 basis points, and it caused mortgage rates to spike back over 7%, and corporate borrowing got a lot more expensive. The Fed’s short-term rates don’t impact much of the economy, but long-term rates do, they’re crucial, and those long-term rates are now FAR higher than they were just before the rate cut. Higher longer-term rates was what is really needed, and they delivered them (whether they planned it or not doesn’t matter)!! Kudos!!!

If “Cutting 100 basis points, including 50 in Sept was . . . a pretty smart move [because] it caused longer-term yields to spike by over 100 basis points,” shouldn’t the Fed continue cutting rates apace to spur more of the “pretty smart” results you listed — higher longer-term yields, higher mortgage rates, more expensive corporate borrowing — all of which in your view “is really needed” and was achieved thru Fed Fund rate cuts?

That would be a though-experiment you can play with. But we don’t want long-term rates to go too high. At some point, it would turn bad. So maybe just keep it there for a while and wait and see?

That is a hypothetical conjecture, almost worthy of derision in the sense that what might have been is not evidence.

Solving a problem by creating another problem doesn’t work so well. The problem in housing isn’t 7% mortgages, it is people sitting in homes with 3% mortgages.

Current rates don’t seem to be restricting .

the FED cuts have had a big impact on CD’s and savings rates…they were close to 5, now at 3.75 or so. That affects many folks trying to keep up with (ahem) 3% inflation without investing in the stock market ponzi scheme.

By the time your stuff matures, you may be able to invest the proceeds in 10-year Treasuries at over 5%, and not have to worry about it for 10 years. The 20-year Treasury yield is already over 5%. 30-year bonds were just sold at auction at a yield of 4.91%.

T-bills yield over 4%. Just today, 8-week T-bills sold at auction for a yield of 4.24%. You can set them up on automatic rollover and collect the interest every 8 weeks.

Money market funds yield 4.2%-plus currently.

Your bank is screwing you! It’s screwing you because you’re lazy and encourage it to screw you. Take your savings somewhere else. I just gave you some options.

Wolf said: “By the time your stuff matures, you may be able to invest the proceeds in 10-year Treasuries at over 5%, and not have to worry about it for 10 years.”

_____________________________

Only if inflation is tamed near zero. If you have to live on any significant portion of the interest, you are a tight dance. First you pay Federal tax on the interest. Look at 1 million in Treasuries at 5%. You earn $50,000. After tax, you have $40,000. If you need $40,000 to live on, with any inflation over zero you are moving backwards.

$40,000 doesn’t buy much.

I would be very nervous buying 10 year T-bills at 5% with the history of our FED, Bankers, GOV and inflation.

Would you buy 10 year Treasuries at 5%?

Inflation eats everything, from the purchasing power of your salary to the purchasing power of your home and your stock portfolio. You just hope that your salary and home price and stock value rise faster than inflation. But that’s not guaranteed. They can decline, and then on top of that decline, inflation eats the purchasing power of the remainder. With Treasuries at least, you know you get your money back when they mature, and interest every six months along the way. No one escapes inflation.

And with both moves, the yield curve uninverted. Again, maybe not on purpose, but a happy outcome.

Once the Mortgage rates get to 8% the housing market here will crash and burn if it hasn’t already. All the Dems that bought homes a few years back in DC and lose their jobs with the change over in administration will have some serious problems unloading their homes. Over 5,000 Presidential appointees will be affected. Most of the incoming staffers and appointees will chose to live in Northern Virginia verses DC. The crime in DC is completely out of control. It has descended into a 3rd world hellhole in the last 3 years.

Wolf said: “Higher longer-term rates was what is really needed”

—————–

Why? What does this fix?

An appropriate cost of capital fixes the free-money problem we have accumulated on a massive scale.

Wolf, you say cutting 100 Basis Points was a Smart Move ????

There Federal Reserve Credibility has taken a Big Hurt in Damage, but you know what…… the market has not even begun to price in the Credibility Damage, and when it does, Watch how things go Ballistic…………

Would you say Arthur Burns Cuts in the 1970’s was a smart move ??? i think not….

You just read the first sentence of my comment. You have NO IDEA what this was about because you didn’t read the rest of my comment. READ THE ENTIRE COMMENT, for crying out loud before you post BS.

The California fires will certainly have some impact on employment numbers, just like the hurricanes caused. It will be interesting to see how that plays out because of the different economic focus of the regions and the different types of jobs and how quickly they can recover.

The biggest concern for the rest of the country and the overall economy would probably be any disruption in the SoCal ports and shipping

Insurance rates certainly won’t get better.

The Southern California fires could cause a huge uptick in hiring in the construction industry as more than 10,000 structures have been leveled by the fires and most will be replaced. The ports are all way south of the fires along the coast below Palos Verdes Peninsula in LA/Long Beach and will be experiencing no affects from the fires at all. The areas affected by the fires are all residential with no manufacturing of any sort and a huge amount of stuff will have to be replaced due to loss in the fires which may cause a mini-boom in imports.

I think he’s referring to the possible labor strike at the ports??

There is no possible labor strike at the ports of Los Angeles and Long Beach. Wrong coast.

@SocalBeachDude

“The Southern California fires could cause a huge uptick in hiring in the construction industry as more than 10,000 structures have been leveled by the fires and most will be replaced.”

That is what I am thinking. My brother in-law has a drywall & plastering business. After the Northridge earthquake in 1994, he was swamped with work for the next several years.

Thank goodness for the Mexican construction workforce.

Exactly what I was thinking. As soon as FedGov adjusts the labor force and unemployment rates for immigration, tons of immigrants will get jobs rebuilding lost chunks of LA.

The So Cal fires will have very little impact on the US economy. Construction in the burn areas will get a boost, but after years of getting permits. Rents will rise somewhat faster in LA county. Lots of LA county officials will be voted out.

Good points BB:

Here in the saintly part of the TPA bay area, labor was definitely more expensive before the ‘canes hit us, but now almost impossible to find anyone to do anything.

New roof down the street had workers with trucks from NJ and MO as an example, and I think they were paid from FEMA funds as the roof was blue tarped since the storms.

GC friend can hardly pause to say hello, and he and his crews been working 7 days a week since October.

We can hope Trump and his crew can differentiate clearly between criminals and folx who WANT TO WORK,,, and proceed appropriately no matter what else, as USA clearly NEEDS WORKERS.

if america needs construction workers, it should bring in single men as it did in the 50s. not huge families and the associated costs.

No. Single men is what we don’t need.

I’m not racist or anti-immigration, but men are bad news in general. Single men the worst.

And for that matter, women are probably more likely to work, given the chance (and if they are culturally allowed, which in some cases is more likely once they get to the States). I do realize they are less likely to do construction work. But families make the most sense for that reason. Most dudes are about worthless without a woman to keep them in line.

(I was surprised, but interested, that someone commented exactly the opposite of what I thought everyone else thinks).

Of course, hope is never a plan. The reality is that Florida is facing it’s conservative self in the mirror. Crying out for the remedial emergency services they voted down.

@ VintageVNvet –

Is it that much harder to spell out Tampa than use the TPA acronym? Remember Wolf has a worldwide audience and some of us are acronym deficient.

Also, the USA HAS WORKERS. Let the internal market allocate where they go. Why pile in foreigner’s to continue the distortion?

Business likes immigration: a larger market of buyers and downward wage pressure.

Landlords like immigration: Higher rents.

“Is it that much harder to spell out Tampa than use the TPA acronym? Remember Wolf has a worldwide audience and some of us are acronym deficient.”

Where I live SD means South Dakota :)

Bob B

It destroyed mostly residential areas, plus some smaller commercial strips. From what I can tell, it didn’t get anywhere near the ports or other big elements of the transportation network and industrial parks. There’s going to be a surge of employment to clean up and rebuild.

The problem will be with getting homeowners’ insurance in CA. It’s already a fiasco, and this will make it an even bigger fiasco. It will make homeowners’ insurance across the state a lot more expensive and even harder to get, which will be another hit to the housing market.

Longer-term, it will encourage even more people to pack up and leave before their house too burns down, or because they cannot afford the insurance, and this may keep the population decline in the state going, which would be another hit to the housing market.

Will the destroyed SFH be replaced by multi family ?

I can see politicians pushing for it.

Mansions will be replaced by mansions. Smaller houses will be replaced by smaller houses. This isn’t an area for high-rise living. It’s not central LA.

In Oregon they push for MFH mixed in with SFH, and existing homeowners cannot stop it…and yes it does hurt property values despite what the internet claims.

Maybe the millionaires are just too rich and powerful to have it forced upon them. If so, that’s great, although tough to say after such a horrendous disaster.

The Southern California housing market NEEDS to take another hit (although I would’ve preferred it not happen because thousands of people lost their homes to devastating fires). Something has got to reset the prices here to something in the vicinity of affordable.

But in the short term, the rental market is already price-gouging. Rental homes that were languishing on the market for months are now re-listed at a monthly rent several thousand dollars higher, presumably because the owners think desperate people who need housing will pay any price. Whether those desperate people can/do remains to be seen. With respect to the Palisades fire, although some of those houses were owned outright and/or by rich people/celebrities, my uneducated guess is that just as many if not more were owned by well-paid working people with a high monthly mortgage, which mortgage still has to be paid whether the house is standing or not. Whether those people can afford to pay the mortgage AND a high monthly rent on another house while the rebuild remains to be seen.

“Rental homes that were languishing on the market for months are now re-listed at a monthly rent several thousand dollars higher, presumably because the owners think desperate people who need housing will pay any price.”

Don’t worry. NO ONE is going to rent these houses at overpriced rents. People who lost their home to a fire don’t have anything anymore, they lost everything they had. They have nothing left to move into a house. They need a furnished place, such as a hotel, extended-stay hotel, or vacation rental, or they move in with relatives. You can’t live in an empty house with nothing. They will live in this furnished place until they sort out what they’re going to do next. If they get insurance money pretty quickly, they’ll try to buy a house, maybe out of state because they don’t want it to burn down again, or because they can’t afford the insurance. So unfurnished rentals aren’t going to be in demand. Vacation rentals maybe. The RE trolls in the media are just hyping BS to pump up rents and prices.

SoCal Renter,

There will be those that take advantage of that is what happened with the Oakland fires so many years ago.

By the time the displaced have found places to live, I guess those incoming workers are going to have a hard time finding a place to live.

Don’t exaggerate. This is not a small town. 25 million people live in Southern California, that’s more than in all of Florida. LA County alone has a population of about 10 million people. Maybe 10,000 homes were destroyed.

Got it. thanks for clarification. I was thinking of smaller areas.

Good point WR.

I had a friend in LA county. Few years back, his neighborhood was impacted by wild fire, not his home. But after a year his property insurance shot up form 6K to 23K.

He sold his house and moved out of state.

I am finding it difficult to get property insurance in so cal. Looks like a lot of companies quit on so cal for property insurance.

About 12 Property & Casualty insurers stopped wring new dwelling or homeowner coverage but they are said to be as high as 85% of the market. The state DOI is now allowing future risk and other things to be considered a part of present rating and that decision was made just before the grand fires.

Where did this guy live? I mean, I’m not asking for his address but did he live in a more developed, sub/urban part of the county or up in the mountains or???

LA is hardly a sympathetic victim.

“LA is hardly a sympathetic victim.”

Wow, you’re a really charming person.

I can see Blackrock buying up the entire devastated area and putting up cheap rental housing, both single family and multifamily.

That would be a great thing. “Cheap rental housing” is exactly what this area needs the most. But not going to happen.

Not to worry Wolf

Gavin waived his executive order magic wand and everything will be fine:

“In exchange for underwriting riskier policies, companies will be permitted to use catastrophic modeling to set insurance rates, a practice Lara’s office did not previously allow. The companies will also gain the ability to pass reinsurance costs on to consumers.

Consumer Watchdog blasted the deal, saying Lara has “given into the industry’s demands,” and insurance companies will use the new modeling tools with “secret algorithms” to drive up consumer costs.

“The use of catastrophic modeling and adding of reinsurance costs to premiums has pushed Florida premiums up two to three times higher than California’s,” said Jamie Court, president of Consumer Watchdog, in a statement. “California is in danger of becoming Florida with these changes that mimic the failed strategies in the Florida.”

Generally speaking, pricing to risk is better for everyone. It SHOULD cost more to insure a structure that has a higher potential for loss. This is the same logic behind credit scores influencing loan availability/rate. It’s why auto insurance costs more for habitual traffic offenders. It’s the basis of the corporate bond market.

To do otherwise subsidizes building is places that shouldn’t be built on. Barrier islands, flood plains, volcanos, deserts, swamps, etc.

It’s socialism, plain and simple. I’m all for a little socialism here and there, but I don’t think it should be used to subsidize privledge. Disallowing ‘real’ risk premiums does just that for the most part.

I just spoke to a friend in San Diego last night who is having difficulty getting a loan because the VA (their originator) doesn’t think the HOA has enough insurance.

My friend has 2600 sq ft new home and his hoa and property insurance is almost 12k per year

He is not a happy camper as he pays 33k per year just for all free then mortgage

The SoCal ports aren’t disrupted in any way by the fires. The harbor area is quite significantly less affected by the high winds that are sparking these fires than any other area in greater Los Angeles. Wind maps over the last few days have consistently shown the area surrounding the joint port complex to be a sort of island of (relative) calm in a sea of terrifyingly high wind speeds. Most of the off-dock infrastructure–distribution centers, rail hubs, etc.–is similarly located in areas of relatively low fire hazard.

Any disruptions in the near future to the ports of LA/LB will almost certainly be caused by changes in the “rest of the country and the overall economy,” not the other way around.

You are almost certainly right about insurance rates. They will get worse, on top of eyewatering (14%) inflation in that particular sector.

Still talking STRIKE at the ports

No. The west coast ports employer group (PMA) and dockworkers union (ILWU) have a contract that has several more years to run. Any talk of a dock strike would concern the east and gulf coasts, which have an entirely different union (ILA) and employer group (USMX), and which are currently negotiating their contract (and have just recently announced a tentative deal).

The internet exists. You’re on it right now. You can use it to look this stuff up.

The California property taxes are limited by the Jarvis protocol.

1:04 PM 1/10/2025

Dow 41,938.45 -696.75 -1.63%

S&P 500 5,827.04 -91.21 -1.54%

Nasdaq 19,161.63 -317.25 -1.63%

VIX 19.62 1.92 10.85%

Gold 2,716.30 25.50 0.95%

Oil 76.60 2.68 3.63%

On a side note up in Canada the Bank of Canada must be worried about the Canadian dollar as the Canadian jobs figures had to be skewed heavily to the upside today to save the Canadian dollar from plunging.

LOL, companies finally hired some people, and you’re still not happy?

MW: Dow ends down almost 700 points as jobs report sparks jump in Treasury yields

i hope powell and co. are watching. the last all time high in the s&p was on 12/6. 35 days ago! investors in the u.s. stock market are entitled to get a new all time high every week, so if that isn’t happening, that means they need to start cutting rates and printing again.

their dual mandate is 1) inflate the u.s. stock market, and 2) inflate the real estate market.

anything less is a dereliction of duty.

That is not the way they see it. They see it as an accommodation to prevent the collapse of the QE asset bubbles.

The idea that QE is not inflationary is silly.

I would venture the events in LA will have a nationwide effect on inflation. Insurance seems obvious, supplies do to the rebuilding? Just seems unreal that so much could be lost, so quickly.

We all know that California is high cost due to regulations. Will lenders want to invest in areas seen as high risk and high cost. My homeowners insurance went up and I am more than a hundred miles from any of the headline flooding that happened in the last year.

I would guess banks and insurance companies will all be looking harder at risks of all types.

I agree. The LA fires will increase insurance rates unless the economy falters. The LA market is the market.

Mr. Wolf writes: “Maybe those 100 basis points in cuts is all the economy is going to get, as the Fed is gingerly shifting back into its wait-and-see.”

This seems like an excellent reason to adopt a two tier interest rate system; a higher rate to “skim” the population who obviously can afford it and a lower rate for the national debt. The lower rate for the national debt incorporates the reality of world dominance (empire) in the face of a world order turning into “survival of the fittest” with real pier adversaries. Of course inflation as an indirect tax is a given.

This two-tiered system you’re proposing has been in place forever, and very officially. The federal government borrows at far lower interest rates than consumers or businesses. This is not a conspiracy, but capitalism in that it puts a price on credit risk. The government cannot go bankrupt and, through the Fed if push comes to shove, is always able to service its debts. So the credit risk of its debt is zero (even if it causes inflation to soar), and investors know this, and if they seek investments with zero credit risk, this is the one, but because of it, it pays less interest. But consumers and businesses can and do go bankrupt, and their credit risk is rated. Consumers’ credit risks are rated by FICO scores (from subprime to super-prime), and businesses are rated by credit ratings agencies from deep-junk to triple-A investment grade. That credit risk determines at what cost they borrow. Risk has a price.

DON’T KNOW WHY PEA SEA doesn’t have a “Reply” available…but re his take on LA Ports…the problem with the recent union labor contract isn’t

the wage increase but the fact that the Union has nixed the idea of automation. This is going to be a problem going forward because as the union members want to “safeguard their jobs,” the overall productivity

of the ports (East coast & West coasts) will not improve!

LOL look at the new Chinese ports in Peru! _

You are very confused. The union representing the **EAST COAST** is currently negotiating a contract, with automation a contentious issue–but not so contentious that they weren’t able to reach a tentative agreement with the group representing East Coast employers. Neither side in a unionized industry is ever able to “nix” anything unilaterally. Ultimately both sides have to agree on a contract, and it looks, pending a vote, like they have done just that.

There is absolutely no talk, official or unofficial, of a strike on the west coast. The west coast union and the west coast employer group signed a contract in 2023; that contact will be in effect until 2028.

Again, if you can type on the internet you can use the internet to look up facts and learn things. Please, please do so. It costs you nothing.

I haven’t recognized a union since I was a Teamster in the 70’s. What were they supposed to do as the capitalists hired the CCP monopsonistic labor force to compete against the union contracts.

Inflation peaks in the 4th quarter of 2025:

08/1/2024 ,,,, 0.009

09/1/2024 ,,,, 0.029

10/1/2024 ,,,, 0.041

11/1/2024 ,,,, 0.055

12/1/2024 ,,,, 0.047

01/1/2025 ,,,, 0.064

02/1/2025 ,,,, 0.067

03/1/2025 ,,,, 0.057

04/1/2025 ,,,, 0.077

05/1/2025 ,,,, 0.081

06/1/2025 ,,,, 0.088

07/1/2025 ,,,, 0.086

08/1/2025 ,,,, 0.095

09/1/2025 ,,,, 0.098 peak

10/1/2025 ,,,, 0.092

11/1/2025 ,,,, 0.093

12/1/2025 ,,,, 0.070

Inflation is already baked in.

You have been QE-mongering for a long time now. Go somewhere else to spread this BS. I recommend X.

This site is a rare gem, and it’s great that there’s a conversation focused on was actually is rather than misinfo, conspiracy, and speculation which is pervasive these days. Thanks Wolf

I’m thinking of taking out flood insurance even though I am not in a flood zone. Those people in N Carolina didn’t have flood insurance because they were not in a flood zone, and look what happened. The rates are cheap if you are not in a flood zone. Look for all the relief money to go to the rich Los Angeles victims, while the poor victims in N Carolina are left living in tents forever.

I’m in a flood zone but not required to have it because no mortgage. Fortunately it is $600ish a year but rates vary dramatically in almost seemingly illogical ways. All depends on what price it would come out to and tolerance for risk. For me $600 is worth it but if it doubled I might pass, however illogical that might be.

I CANNOT RECCOMEND THIS HIGHLY ENOUGH!!!

My parents live on the Gulf Coast directly on a bayou… but their house is above the 14 foot flood insurance elevation requirement. After a hurricane in 1998 where the waters rose up to their driveway my mother called her insurance agent and found out that Flood Insurance was only $240 a year. “SIGN ME UP!!!”

Flash forward seven years and Hurricane Katrina hits. A house that had survived three decades of hurricane EYES passing overhead with barely a scratch now has major roof damage and floodwaters that were six feet high.

The BIG advantage to having flood insurance was that it limited the insurance company battle of “Wind versus Water” that hurricane survivors have to go through. The insurance appraiser came out… made his assessment… and they cut the check. If the Federal government wanted to battle the appraisal then that was done behind the scenes with the insurance company. There was no question that the damage was covered. My parents were among the first in the area to start rebuilding because they actually had the money in their account.

PS: After that my mom started paying the $50 per year for Earthquake insurance. We all laughed at her because the Gulf Coast doesn’t get earthquakes. A few years later there was a tremor near us and she just gave us that knowing little smile that mothers do.

PPS: According to FEMA 40% of flood insurance claims come from NON-high risk areas for flooding.

MW: Dow sees worst start to a year since 2016 as Fed rate-cut hopes fade for 2025

Nonfarm payrolls are mentioned, but I didn’t see anything about the “Usually Work Full-Time” numbers. I don’t know enough about it but that seems like an important metric, and it has languished over the last 2 years. I wonder if that isn’t a meaningful measure to the powers that be, or if it is being unwisely overlooked.

This is part of the household survey. What does the article say about the household survey? That it lacks the tsunami of immigrants, and that it will be updated with that tsunami of immigrants a month from now with the January jobs report, to be released in early Feb. All household survey data, from total employment down to full-time employment, will be revised up massively a month from now.

The Palisades fire is now moving east almost to the 405 freeway and if it jumps the freeway it is headed towards UCLA on Sunset and will pose a real threat to Bel Air and further east towards Beverly Hills. It is also moving northeast towards Tarzana, Encino, and Sherman Oaks and strong winds are expected to pick up again heading into the weekend. The total dollar damage is already estimated to be in the $135-150 billion range and could end up going much higher.

I suppose the next big dose of misery to be heaped onto LA (and the insurers) by the northern mountains will be mudslides, as poignantly explained by John McPhee back in the 1980’s (search New Yorker and LA Against the Mountains). The article is also included in his exceptional book: The Control of Nature.

When nature meets big policy failures, mayhem often ensues…

More of these events will just continue to happen and little investment will be done. Using positive discount rates is good for investments but less so for environmental impacts or human lives, where either zero or negative makes more sense. Unlikely climate change will ever get the money it needs if everything is ROI based. Asbestos company did the same thing with cancer and other diseases it caused and discounted a current human life from a million to $22,000. They knew the impacts, they didn’t care.