Quantitative Tightening shed 44% of Pandemic-QE assets. Fed’s share of the ballooning US national debt dropped to the lowest since 2019.

By Wolf Richter for WOLF STREET.

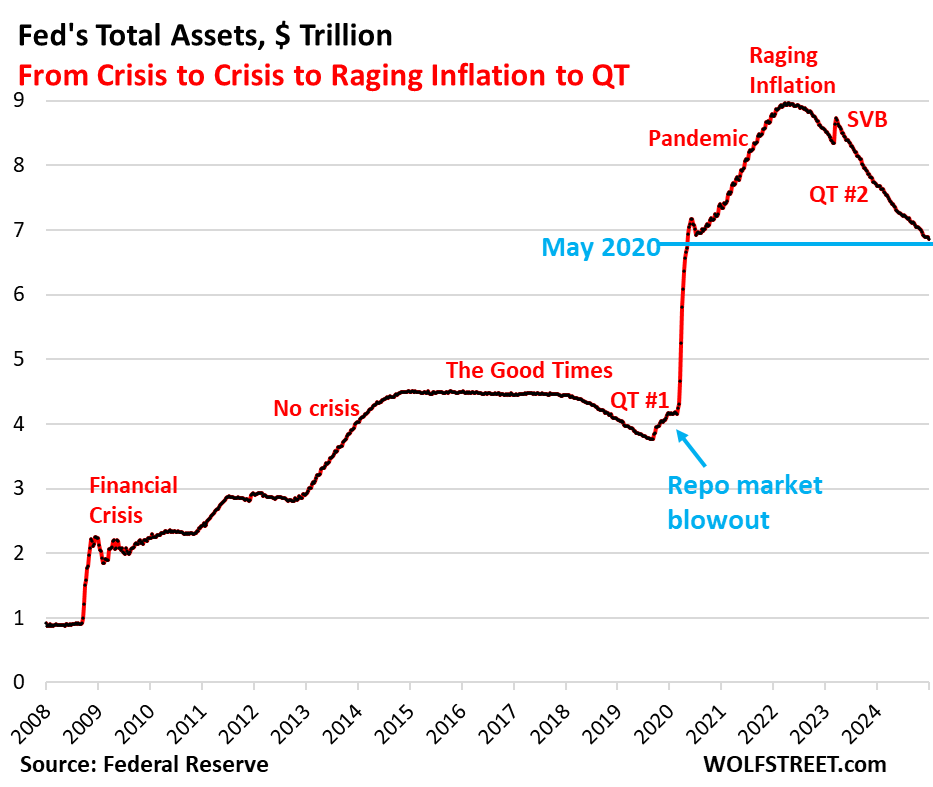

Total assets on the Fed’s balance sheet declined by $43 billion in December, to $6.85 trillion, the lowest since May 2020, according to the Fed’s weekly balance sheet today.

Since the end of QE in April 2022, the Fed has shed $2.11 trillion, or 23.6% of its assets.

In terms of the $4.81 trillion piled on the balance sheet during pandemic QE from March 2020 through April 2022, the Fed has now shed 44% of that.

QT assets by category.

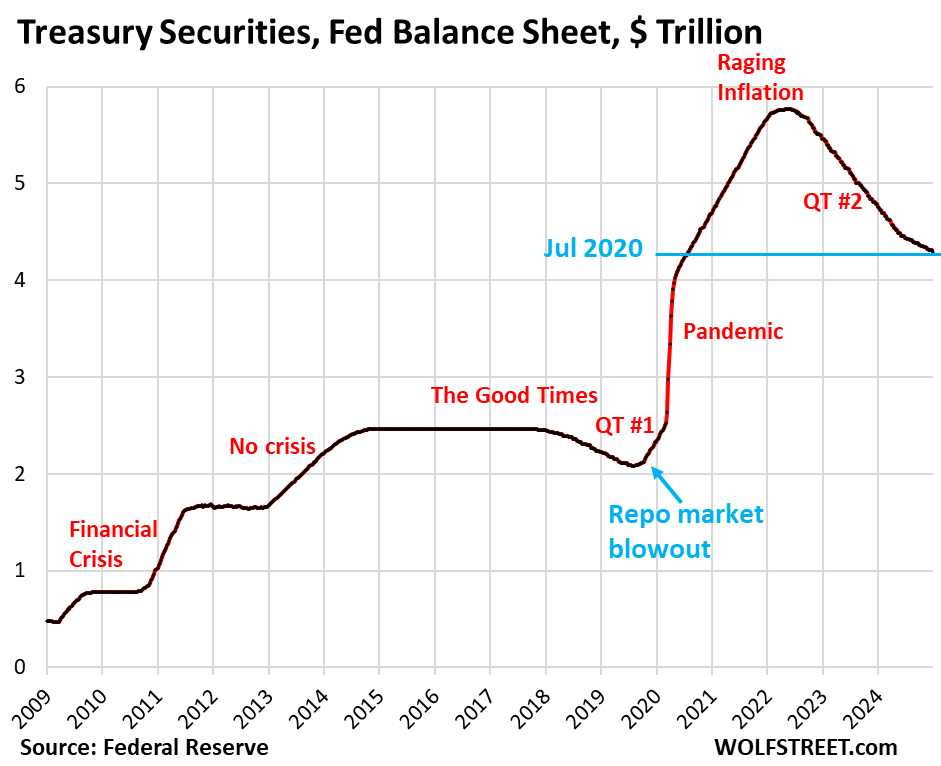

Treasury securities: -$24.5 billion in December, -$1.48 trillion from peak in June 2022, or -26% since the peak, to $4.29 trillion, the lowest since July 2020.

In terms of the $3.27 trillion in Treasuries piled on the balance sheet during pandemic QE, the Fed has now shed 45% of it.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. Since June, the roll-off has been capped at $25 billion per month. About that much rolled off in December, minus the amount of inflation protection the Fed earns on its Treasury Inflation Protected Securities (TIPS) that was added to the principal of the TIPS.

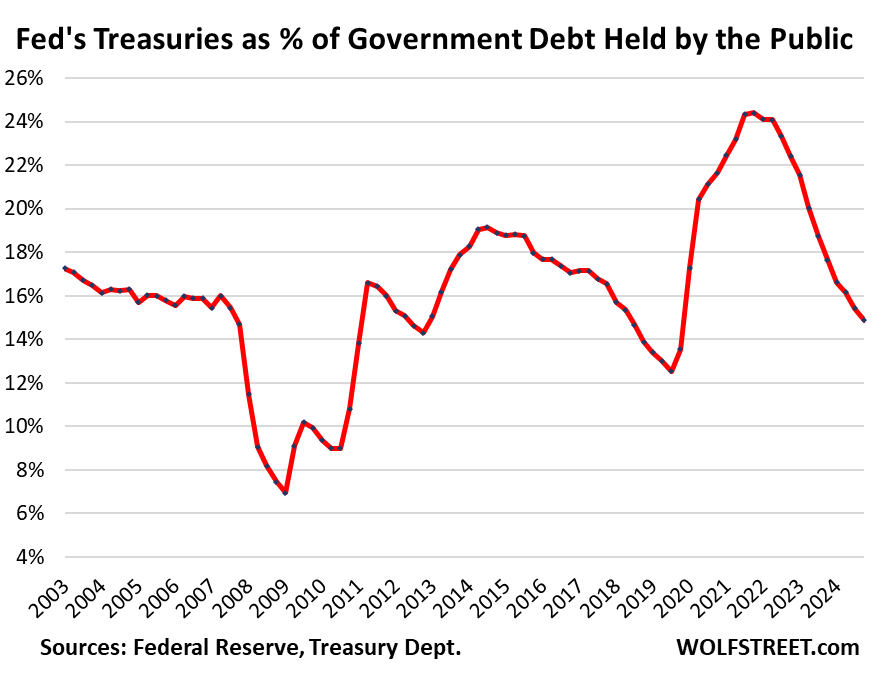

The Fed’s share of the “Debt held by the public” has been declining sharply since mid-2022, as the US national debt has surged at a mindboggling pace, while the Fed started cutting its holdings at the same time. Investors in the US and around the globe have stepped in to buy what the Fed has walked away from.

Of the $36.1 trillion US national debt, $7.30 trillion are held by various federal government pension funds, military pension funds, the Social Security Trust Funds, Medicare Trust Funds, etc.

The remaining $28.87 trillion are “held by the public,” including by the Fed, foreign investors, banks, individuals, etc., and we have laid out these investors by category here.

The Fed’s Treasury holdings of $4.29 trillion amount to 14.9% of the “debt held by the public,” the lowest since Q4 2019.

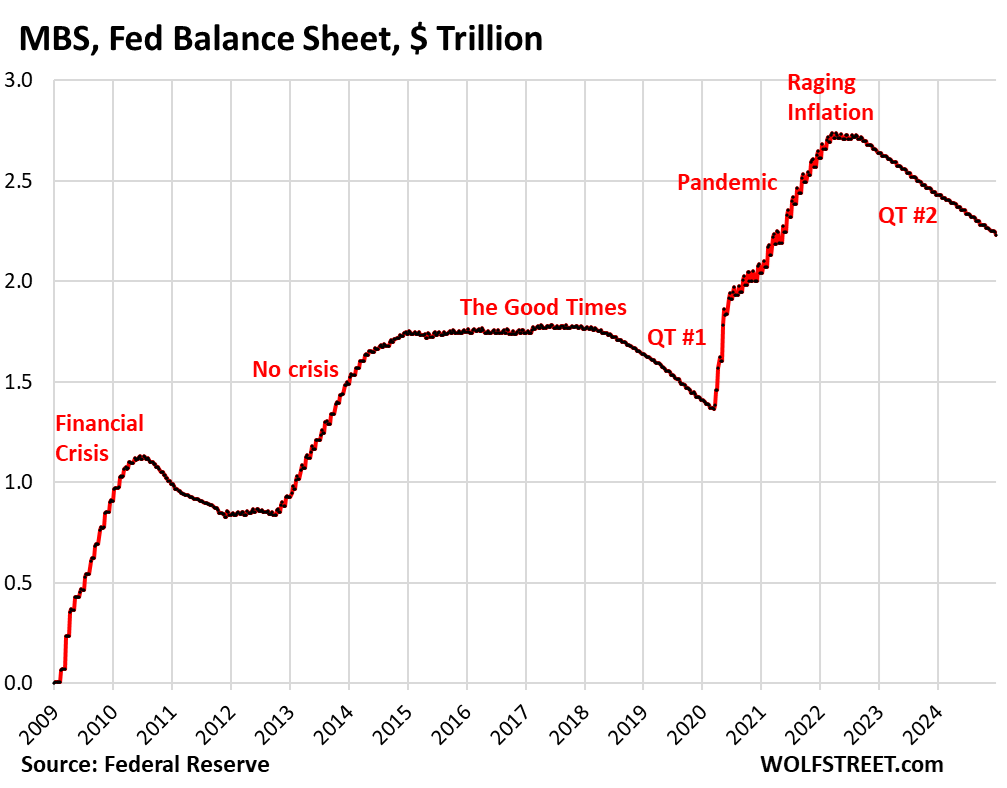

Mortgage-Backed Securities (MBS): -$15.7 billion in November, -$507 billion from the peak, to $2.23 trillion, the lowest since May 2021. The Fed has shed 18.5% of its peak holdings in April 2022.

In terms of the $1.37 trillion in MBS that the Fed added between March 2020 and April 2022, it has shed 37% of it.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But sales of existing homes in 2024 have plunged to the lowest since 1995 and mortgage refinancing has collapsed, and therefore far fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have become a trickle. As a result, MBS have come off the Fed’s balance sheet at a pace that has been below $20 billion in most months.

There has been some discussion at the Fed, including in October by Dallas Fed President Lorie Logan, about outright selling MBS to speed up the process of getting rid of them, and getting rid of all of the MBS even after QT ends, and replacing them with Treasury securities. But the Fed doesn’t seem to be in a hurry to tackle this topic.

The Fed only holds “agency” MBS that are guaranteed by the government, and is therefore not exposed to losses if borrowers default on mortgages; the taxpayer would pick up those losses, not the Fed.

Bank liquidity facilities.

The only two bank liquidity facilities that currently have a balance that’s above zero or near-zero are the Discount Window and the Bank Term Funding Program (BTFP). The other bank liquidity facilities that were heavily used after the SVB collapse are either at zero or near zero:

- Central Bank Liquidity Swaps ($1 billion)

- Repos ($0)

- Loans to the FDIC ($0).

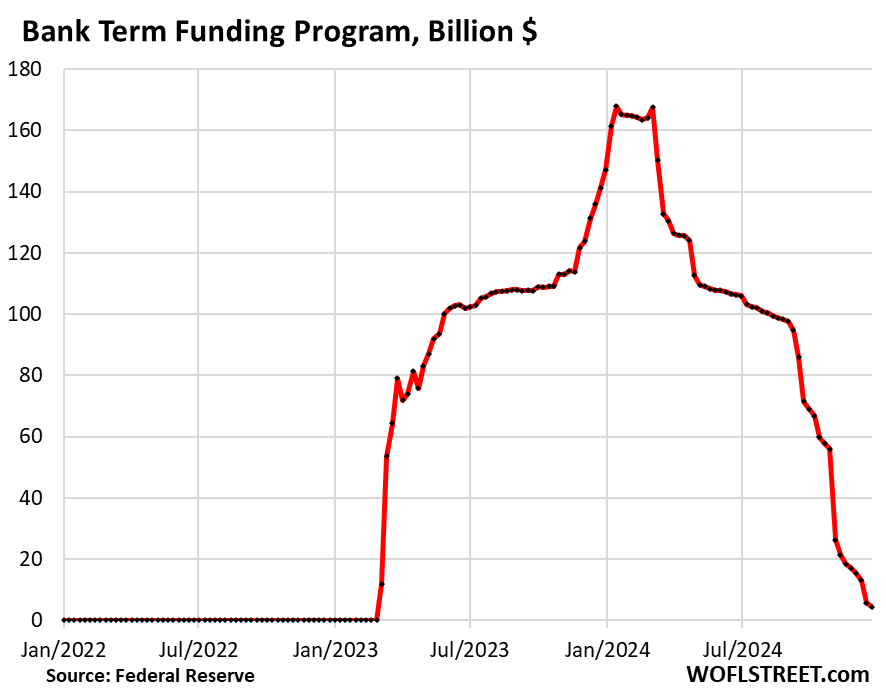

Bank Term Funding Program (BTFP): -$13 billion in December, to $4 billion, -97% from the peak ($168 billion).

The BTFP had a fatal flaw when it was conceived in March 2023 after SVB had failed: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed’s policy rates were unchanged, including the 5.4% the Fed paid banks on reserves at the time. Some banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion.

The Fed shut down the arbitrage in January by changing the rate and decided to let the BTFP expire on March 11, 2024, and no new loans could be taken out since then. Any remaining loans, which had a maximum term of one year, will be paid off by March 11, 2025, and the balance will go to zero.

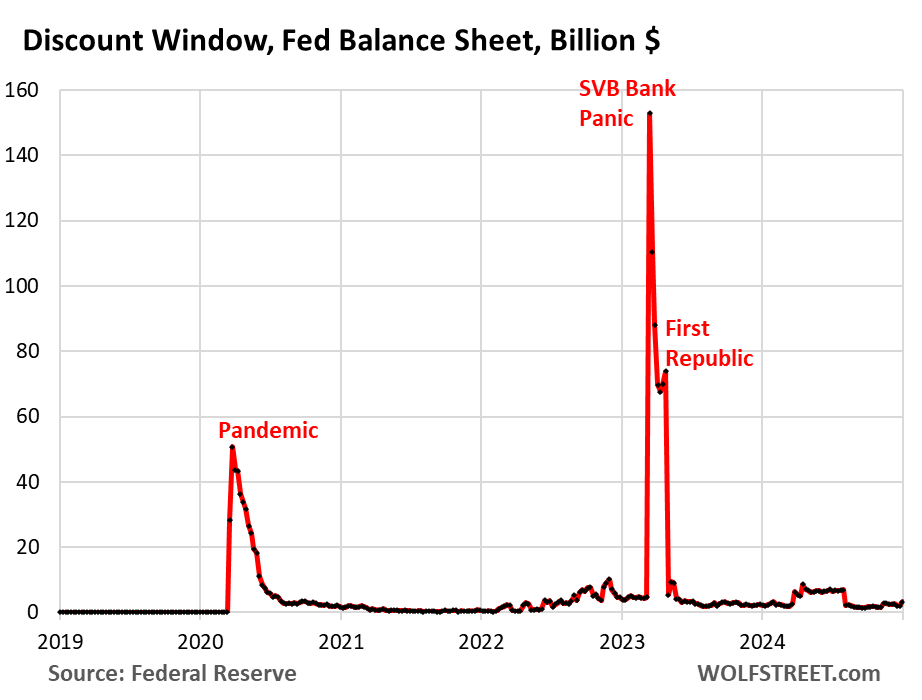

Discount Window: +$800 million in December, to $3.2 billion. During the bank panic in March 2023, loans had spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. As of the rate cut in December, the Fed charges banks 4.50% in interest on these loans and demands collateral at market value, which is expensive money for banks.

In his efforts to water down the stigma attached to borrowing at the Discount Window, Powell has been exhorting banks to use this facility more often, and practice using it with small-value exercise transactions, and to even get set up to use it, which many banks apparently are not, and to pre-position collateral so that they can use it when they need to.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks Wolf.

Now the BTFP is almost zero. Because of housing Market is slowed down, only Pass thru payments and because no sales/refinance, MBS is way lower than FED limits. Only 25 Billions in treasuries will go on till FED says otherwise.

I guess balance sheet reduction will slow down. Is that fair understanding?

May be FED should bring back discussion on Selling MBS sooner than later.

“I guess balance sheet reduction will slow down”

That’s the explicit statement the Fed made in May, when it reduced the cap for Treasury runoff to $25 billion a month, starting last June, and that’s what it has been every month. However, it removed the cap of the MBS runoff. MBS runoff is determined by mortgage payoffs, so refis and sales.

Go slower to go further — that’s explicit and official Fed motto here. It wants to keep QT going for as long as possible without blowing anything up, and going slowly will do the trick.

Great to see where fed has progressed without blowing up anything.

Have you missed them blowing up The Everything Bubble? They literally call it the everything.

I think SC73 was referring to the rapid, often explosive, deflation of a Fed fueled over-inflation of available reserves to the point that they have to pay the perps interest so they don’t drive inflation too high. A hypothetical scenario.

A definition of a bubble, as an engineer, requires dimensions as well as an impeccable standard for comparison.

I think the Fed is doing well in a damage control situation. QE, the untested economic plan that was implemented has been shown to be destructively wrong and now they have the unwind to deal with.

The AI machine society, Big Brother, that big tech is cravenly gravitating to the defense and homeland security agendas.

Best wishes

By doing insane un needed QE, with financial conditions never too tight, with already high costs, locking out generation of Americans from housing market by buying MBS, with ever increasing wealth gap, I already see things blown up by FED to the advantage of asset holders.

But this is just my opinion.

I guess, by FED blowing up, you guys meant rich getting tiny less richer because of lowered asset prices.

Well I suggest that it only requires the will of the people, which is what America has always claimed to be sacred.

When the government itself over throws democracy, that is, perhaps, the end of the experiment. The corruption of the Supreme Court is all it took.

Blowing things up… It’s a long fuse, give it time.

I think I’ll go hang out at the discount window, that’s where all the rich people go to get their food stamps, maybe do some begging….

I’m thinking about getting a red pen like Wolf has, and making some charts of my own.

I would like to announce the passing of another GI today. He was old and always salty. May we all want too live so long.

Mr Wolf writes: “…getting rid of all of the MBS even after QT ends, and replacing them with Treasury securities. But the Fed doesn’t seem to be in a hurry to tackle this topic.”

Seems like the Fed will try and sell MBS even at a loss in order to have the funds to buy up deficit debt.

LOL, no. The Fed creates and destroys money (“funds”) every day as a matter of routine. It doesn’t need to sell something to raise the “funds” to buy something because it just creates the funds to buy something, just like it destroys the funds when it sells something. That principle is at the core of a central bank.

And that’s why losses don’t matter to the Fed.

At the current pace the MBS should be gone in ten years plus or minus. Since they presumably pay far under current MBS rates the Fed would be sort of foolish to try to force them out the door early. Probably best to just leave that pile in the corner and let time take care of it. -15 to 20B a month as the Fed is repaid is going to be almost imperceptible in a $30 trillion economy.

The loss is the same whether they realize by selling or holding aAnd taking over time. If long term rates move up, then losses increase. If long term rates move down, then the losses in FEDs portfolio go down. If rates stay flat, losses are the same whether sold and loss is lump sum, or retained and taken daily in the form of lower returns.

How secure are agency bonds issued by FHLB, FFCB, and FHLMC?

The thing to worry about with agency bonds is that they’re callable, which is a nasty feature. And they do get called.

The Fed should never have bought a penny of MBS in the first place.

What’s next? Buying 10% of the stock market like Japan’s central bank? Or crypto? Where does the absurdity end?

Every nation seems to have a central bank. Every central bank seems to be that main villain in the story.

This QT series you run is my favorite.

The Fed never should have done QE in the first place, MBS or otherwise.

now now – and let few banksters feel pain back in 2009-2013

and paying interest on repo’s

stealing in so many ways

that’s what govts do

Yellin did say the Fed could do the same as the BoJ buying up equities…she left the door open to it for sure. Which means it probably will happen if we get a repeat of 2000. I guess the moral is, only poor people should feel pain

“only poor people should feel pain”

This is exactly right, basically the whole point of the fed’s existence.

The dual mandate – privatize the gain, socialize the loss.

Sarc, sort of.

Agreed, the FED should never have bought MBS securities. I think even most of the FED board would agree with this in retrospect.

However, they did. Right or wrong, it happened.

The question is, since we cannot go back and change the past, what is the best path forward from where we are at right now?

Right now, I am fairly certain the FED is generally following the best path forward. They are slowly trying to correct the mistakes of the past so that there isn’t another catastrophe that requires extraordinary measures.

So many people get hung up on the mistakes of the past. They literally cannot get past those mistakes. They rant and have about them and have them dominate their thoughts that they cannot see the best path forward.

“So many people get hung up on the mistakes of the past.”

Not only that, they ignore what DIDN’T happen because of those “mistakes”. The GFC didn’t become Great Depression 2.0. The pandemic didn’t cause a huge economic crash. The list goes on.

A lot of good things happened during Great Depression. Insolvent businesses closed their doors, and the middle class started a 45-year winning streak. We’ll get a worse version of all the bad things the Fed “prevented” when the market takes away the printing press.

Homelessness and debt defaults are the new Great Depression. We are there. The assets owned by the ultrarich will contract, the economy will leave Wall Street and return to Main Street. The economy will gradually recover when the Fed is disempowered.

“The GFC didn’t become Great Depression 2.0.”

You obviously don’t live in the U.K! Potholes in the roads so deep you could lose a child in one. Crumbling pavements , broken streetlights that are never repaired. Rubbish is everywhere and anything that can be reached has graffiti on. Oh and did a mention the stench of cannabis everywhere you go?

It’s Impossible to see a Dr or dentist. People can’t afford to put the heating on and my weekly shop is up 15% since December 2024.

JimL

If a surgeon removes a body part of yours by mistake, are you going to hire him for your next operation?

To sound rational, you need to make a case the Fed did not error. Good luck.

This isn’t a kids’ tee ball game.

Well limiting themselves at 10 pct of the stock market was insufficient at the time because the stock market was down 60 pct or so at the time.

Liquidity from the Fed has dominated the market price of credit in support of a financial regimen. The Fed balance sheet is morbidly obese. They are still paying a certain group of obviously good people that had the misfortune of placing a leveraged bet on a losing horse, interest on reserves that the Fed is forcing to hold. wink wink

So to summarize:

– Pandemic response: $4.8trn QE + 150bp Fed funds cut corresponded to CPI rising from 2.5% to 9.1%

– Inflation response: $2.1trn QT + 525bps Fed funds hike corresponds to CPI declining to 2.4% by Sep 2024

– Easing: Fed can only cut by 100bps before CPI starts rising again and 10y yield blows out by 100bps

– Conclusion: the remaining $2.7trn of QE got leveraged into asset price support/expansion, a significant portion of which (real estate, corporate debt etc.) cannot economically be funded based off a 4.25-4.75% treasury curve

What if inflation is rising and falling independent of the Fed’s interest rate changes?

Correct. The QE had too much time to absorb and inflate, so now it’s a permanent feature. Under current central bank policy, inflation is a ratchet. Nothing corrects, it only absorbs.

Unfortunately, this creates depressions and system destroying events.

Haven’t there been depressions throughout history? Maybe credit, leverage and speculation are just human nature.

Credit, leverage and speculation are policy at the Fed, dating back to 1987 (Greenspan). There is no excuse.

What do these post-pandemic actions by the Fed i.e. QT,

do to M2?

Ed, Wolf has discussed M2 in length on other monthly FED/QT updates like this article. Do a keyword search for “M2” and look for Wolf’s comments.

The more months I read Wolf’s QT update, the more I appreciate Wolf as also a patient gardener. M2 crops up in the comment section like weeds do in a garden. The gardener dutifully tends to his garden by addressing the weeds. One cannot fault the weed for sprouting, for it is in its nature to do so.

You have to dissect M2. Savings/investment accounts growing as a percentage of the total figure, signifies contraction. Dr. Philip George has an explanation for it. He called it The Riddle of Money Finally Solved.

ed domovitch

M2 is a nonsense measure these days as the financial flows have changed over the decades (if it ever meant anything before my time). M-2 tries to measure the cash that is ready to be spent. But it doesn’t do that. It doesn’t measure money supply. For example, M-2 includes CDs of less than $100k, but excludes CDs of over $100k. So if someone has a CD of $120k that matures, and the cash goes into a bank account, or into to two $60k CDs, then money supply increases. There are other problems with M-2, including how ON RRPs are handled. M-2 is meaningless, which is why I don’t cover it, and why the Fed no longer mentions it.

A growing economy with profitable businesses naturally creates money, and that’s not the problem. A sharply declining economy where businesses lose money and a bunch of them collapse destroys money. That’s natural.

The problem is central-bank-created money. Which is what you see here in this article.

Monetarists believe that inflation is caused by money supply increases. If you don’t believe that M2 represents money supply, what punlished numbers are the best measure of money supply?

Re-read the last two paragraphs of my comment that you replied to.

At what level does the fed hit bone? 5.5 trillion? 6 trillion? Should it aim for a balance sheet level it was before the pandemic + inflation? Will going below that be deflationary?

In theory, the Fed could revert to its old way of doing things, changing from its “ample reserves” to a “scarce reserves” regime, and it created the means to revert to that system by reviving its old Standing Repo Facility in July 2021 before it even started QT. The Fed will release its 5-year “framework” later this year, and it might spell something out to that effect, and it might not. The last framework was released in 2020.

Assuming that the Fed sticks to its “ample reserves” regime, I would say it could do another $1 trillion in QT at the most, so to about $5.8 trillion at the most. The bottom is formed by the Fed’s liabilities:

– reserves

– cash in circulation

– the government’s checking account (TGA)

– RRPs.

Cash in circulation ($2.4 trillion), the TGA (average $800 billion), and Foreign official RRPs ($300-$400 billion) are not determined by the Fed. They’re demand-based. So that’s $3.6 trillion, and they grow over time.

But overnight RRPs (ON RRPs) are liquidity that the Fed drains, and they’re well on their way to zero.

So that leaves reserves, which are now about $3.1 trillion. Under the ample reserves regime, they might drop closer to $2 trillion and still be “ample,” but barely.

Here are the numbers for the calculation:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

So under the current “ample reserves” regime, the lowest possible level would be about $5.8 trillion.

If something blows up or gets close to blowing up beforehand, the Fed will stop. Withdrawing liquidity is very risky. Last time the Fed did QT, something did blow up – the repo market in the fall of 2019. Which is why the Fed has slowed QT last June. In addition, it has the Standing Repo Facility again that it didn’t have in 2019, which will help forestall blowups, presumably.

Realistically speaking, getting the balance sheet to $6 trillion by the end of 2026, so shedding close $1 trillion more, on top of the $2.1 trillion it already shed, will be a big improvement, meaning that the Fed’s balance sheet will by then have shed over $3 trillion, assuming that nothing blows up along the way.

The Fed’s balance sheet has always grown, even before 2008, as a function of currency in circulation. In 2009, the government’s checking accounts were moved from JPMorgan and other banks to the New York Fed (a liability for the Fed), so that also means a permanent increase of the assets that have to balance it.

Here are total assets and currency in circulation (liability) before 2009 QE

The FED’s Lowest Comfortable Level of Reserves (“LCLoR”) was c. 3.T.

Now we are below that number.

1. That’ll jump back up next week. That was a one-day thingy on Dec 31 for year-end regulatory purposes, and ON RRPs briefly rose about that much. Look at the weekly average, also listed on the balance sheet, and that’s about $3.1 trillion. ON RRPs have already dropped again today. So by next week, this whole thing will be reversed. This is the same thing every year at year end.

2. “Lowest comfortable level of reserves” is NOT the Fed’s level. It’s the banks’ level. Each bank has its own figure for itself. And each bank changes that figure depending on some factors, including the amount of deposits the bank has (more deposits moves up the LCLR). The Fed collects some data on it via its Senior Financial Office Survey. They’ve been doing that for two years.

3. So I looked this up. The LCLR used to be MUCH lower when reserves were only “ample.” In August 2019’s Senior Financial Office Survey of 80 bigger banks, combined holding 3/4 of total banking system reserves, came up with an LCLR of $650 billion, and that was down from $700 billion in the prior survey:

https://www.federalreserve.gov/data/sfos/aug-2019-senior-financial-officer-survey.htm

4. The reason why reserves are still so huge is because there is still such a huge amount of liquidity in the banking system. As that liquidity gets drained out via QT, you will see that the LCLRs will fall too because banks needs less in reserves because they have less in deposits.

Interestingly, that balance sheet reduction is not hitting the over 10 year maturities, those are actually increasing slightly.

https://fred.stlouisfed.org/seriesBeta/TREAS10Y

5 to 10 years are down

https://fred.stlouisfed.org/seriesBeta/TREAS5T10

As are lower durations

https://fred.stlouisfed.org/release/tables?eid=840849&rid=20&form=MG0AV3

But it looks like QT by itself is not responsible for the recent increase in long term yields.

I recall reading that they were going to try to rebalance the duration of the remaining assets, when will they start doing that, as presumably that will result in an even steeper yield curve.

If they don’t start doing that soon they are going to left with a very unbalanced duration porfolio, and I know long term they want it rebalanced to be mostly short term so they can do another operation twist when they need to.

So just for everyone:

This is a function of how the Fed replaces maturing securities with like securities. So when a 10-year note matures, the Fed replaces that with a new 10-year note bought at auction.

But in the years before the 10-year note that rolled off, it was no longer a 10-year maturity. A 10-year note with five years left has a 5-year maturity. A 10-year note with three months left trades like a 3-month T-bill.

Since that 10-year note that rolled off in December didn’t count as a 10-year maturity in 2024, but as an under-1-year maturity on the maturity schedule you linked, replacing it with a new 10-year note replaces a 1-year maturity with a 10-year maturity and lifts the average maturity profile at the Fed.

This is why the Fed is talking about changing how it may replace maturing notes and bonds with T-bills, which would bring the overall balance sheet duration down. Before 2008, the Fed carried mostly T-bills, and it might be angling back into that direction.

Make sure you understand that the number of 10-year notes and 30-year bonds on the Fed’s balance sheet has been declining with QT. So there are now FAR FEWER 10-year notes and 30-year bonds on the Fed’s balance sheet than before, but a FEW of the maturing ones (when over the cap) were replaced with new ones. So on the maturity schedule you linked, a less than 1-year maturity (such as a 10-year note maturing in 8 months) was replaced with a new 10-year note or 30-year bond. But most of the others rolled off without replacement. So this caused the dollar amounts with 10-year plus duration to inch up a little, but not the number of 10-year notes and 30-year bonds.

This is complicated bond math. I’m not sure I explained this well enough to make it comprehensible.

That is the most comprehensive and understandable explanation I have ever seen for this topic. Thx.

It seems odd that they would do it that way and seemingly not have specific duration goals for the portfolio. However, I’ve heard Treasury people talk about how they want to offer things the market wants in enough quantity to maintain that market, even if it doesn’t seem like the optimal move as a debtor. Maybe the Fed has some kind of market support for specific categories it’s doing like that.

Cervantes,

“and seemingly not have specific duration goals…”

The Fed had specific goals. The Fed’s duration goal during QE was to have a portfolio that is roughly similar in structure as total Treasuries held by the public. And that worked during QE, but it’s getting distorted during QT through the mechanism I explained.

Now the Fed is discussing going back to its preference for T-bills, which eliminate the risk of unrealized losses as rates change. That’s why they will soon decide to replace maturing notes and bonds that are over the cap with T-bills, and then after QT stops, to replace many or all maturing notes and bonds and MBS with T-bills. This will get them slowly back to a portfolio of mostly T-bills, which is where they used to be before 2009.

Wolf,

Slightly off-topic, but do you have any SOFR data that goes past the 31st?

Seems like we got thru year-end without any major funding shortages, and the SRF & PCF worked as intended… but I can’t find any SOFR vs EFFR charts that go beyond year-end.

SOFR and the other rates are published the next day. So this morning, we got yesterday’s SOFR: 4.40% with a range between 4.28% and 4.56%. On December 31, it was 4.49% with a range of 4.36% and 4.75%.

Yesterday’s TGCR (Tri-Party General Collateral Rate) was similar: 4.36%, with a range from 4.20% to 4.50%.

The EFFR barely budged.

This shows only minuscule year-end liquidity pressures.

The SRF stayed at zero throughout, which is where banks would have gone for funding if they’d needed it or wanted it to supply funding to the repo market and profit from the spread. But nothing, meaning that there was not enough spread in the repo market to profit from.

ON RRPs jumped, showing the opposite – excess liquidity that banks needed to temporarily move aside for regulatory purposes, in line with the drop in reserves at year-end.

The Fed had announced a couple of weeks before year-end, that it would conduct two daily auctions at the SRF through the year-end period, instead of the customary one auction, because banks face two daily waves of funding pressures, one in the morning to settle securities transactions, and one in the afternoon for everything else. But there were no takers. So still more than “ample” liquidity in the banking system, and more QT coming.

“ON RRPs jumped, showing the opposite – excess liquidity”

Interesting – and that’s despite the extra 5bps reduction in RRP yield.

I agree there’s no evidence of funding stress here, which is a good thing.

It seems reasonable to assume Treasury bonds will continue to rise in yield in the next 6-12 months. Persistent inflation, reduced Fed buying of Treasury bonds, and the massive government spending (monthly debt incurred) will push Treasury rates over 5%.

5-5.5% Treasury bonds are very attractive and will be tempting to “lock in” to provide credit-risk-free income. Expect money market flight and taking of stock market gains by investors who have enjoyed recent market gains.

Money market flight will not happen. Some investors were arbitraging the inverts yield curve when T-Bills were paying more than long-term bonds. But most people using short-term accounts will continue doing so. Basic savings can sit in a money market account. It shouldn’t move to long-term bonds where the value can decline if interest rates were to head even higher.

Wolf,

On the Reverse Repo, and TGA, can/should the Fed change the interest rates paid?

IE instead of paying 4.3%, pay less? Maybe 4%, or 0%? I know they’re reduced the interest rates for the reverse repos. I can’t find any discussion about doing this more.

Would that change the demand for them? I would assume the Treasury and the MMFs would react moving their money out of the FED, and into the world, allowing for more QT? For the Reverse Repo that almost doesn’t matter, but for the TGA that’s a significant amount of money.

The Fed doesn’t pay interest on the TGA.

The Fed already lowered the ON RRP rate by 5 basis points more than its other rates. So it’s now at the bottom of the target range. ON RRPs aren’t the issue anymore, they’re going to zero or near zero.

The Fed uses these 5 policy rates to bracket short-term funding rates. That’s how it controls short-term rates these days, and you can see that in the EFFR, which is super-well controlled compared to how it used to zigzag up and down.

Thank you,

I just can’t see the advantage to the Treasury in holding it’s funds in the TGA during the era of QT.

If the Fed doesn’t pay interest on the TGA, why wouldn’t the Treasury save the government some money, and move the money in the account back to the “Treasury Loan and Note Accounts” with commercial banks?

This shift to the Fed was done during the financial crisis when there were concerns that banks could collapse, and the Fed cannot collapse. Can you imagine that the government’s money is tied up in a collapsed banks that the FDIC, a government agency, is trying to deal with? So that would be unfunny.

Banks don’t pay interest either on commercial checking accounts with that kind of huge volume of payments going through — and they charge a bunch of fees. So for the government, it’s probably a better deal.

Wolf, would you please define ‘Roll Off’ once and for all for me. In the above comment you stated a ‘few’ were replaced but ‘most’ were allowed to roll off without replacement. When these roll off without replacement isn’t it an indication that there are no buyers? If this is the case aren’t we saying that the US is in default on this debt. It doesn’t matter whether the Fed is holding these securities at maturity or the public or China, it is still default. Please elaborate.

1. When a security that the Fed holds matures, the Fed gets paid cash for its face value, plus the remaining interest. The securities disappear, the Fed destroys the cash, and the Fed’s balance sheet declines (= “roll off”)

2. If the Fed didn’t replace any of the maturing securities with new securities, its balance sheet would decline more quickly than now, and the Fed would destroy more cash, and the pace of QT would be faster.

3. But the Fed capped the pace of QT for Treasury securities at $25 billion a month. So when $50 billion mature in one month, the Fed gets paid $50 billion for those securities, plus the remaining interest. It then destroys $25 billion of that cash (= QT) and buys $25 billion of new securities at auction, thereby replaces $25 billion in maturing securities with $25 billion of new securities (= “roll over”) to keep the Treasury QT under the cap of $25 billion.

4. There are no buyers involved in any of this.

5. investors have to pick up the amounts that the Fed rolls off because the government refinances all maturing securities with new securities (pays off maturing securities with funds raised by selling new securities). So investors have to pick up these amounts that the Fed sheds, and they’re doing it, and there’s lost of demand at current yields, and auctions are oversubscribed, with more buyers than there are securities for sale.

So this is the reply to your first sentence. The rest of your comment is a compilation of BS statements with questions marks attached to the end. And I’m not going to waste my time responding to that.

I am pretty sure you have borrower and lender backwards here.

The Fed is not the US treasury. The US treasury is the borrower. The Federal reserve is a lender. At maturity the Treasury repays the loan. The Fed re-loans part of the loan payment back the the Treasury. Other investors step up to loan the rest.

The Fed can’t default on this arrangement – it is the creditor, not the borrower.

Yes, The Fed is a “creditor” using counterfeit “money” created from nothing. They cannot go “bankrupt” because there is no real value in their debt-based paper/digits. The true creditors are the producers. Precisely why gold and silver are constitutional money. Real wealthy/value is in creation and they ability to produce/innovate.

Thank you for documenting the Fed’s criminal activities. Specifically with the purchase of MBS and CMBS. The Fed was never given the authority to touch these financial “products” of mass destruction. The very creation of MBS and CMBS was illegal in terms of 150+ years of contract law, and the bankers and financial fuckers that created these things should have gone bankrupt and to prison (capitalism and rule of law). The very fact that the Fed bailed out these criminals should tell us all who they truly serve. None of this changes until these criminals start losing their heads. May I suggest we start with Hank Paulson…

LOL.

It is a good (no it is great actually) that you don’t get to determine what is legal and illegal.

It is clear you like to declare things illegal and call for imprisonment when you are unhappy. Rule of law doesn’t work that way.

Reading comprehension is not your strong suit. I am not declaring anything, but simply pointing out the obvious. The law was broken (you admit as much), and no one was prosecuted. When there is no law, people will take matters into their own hands. History is very clear on this.

Another corrupt banker. You give yourself away troll.

In other words, I hate Facist A-holes like you. Rule of law should matter. Not some idiot declaring someone a criminal and beheading them.

So you applauded TARP when Wall St. was bailed out in the trillions while 7 million people lost their homes…and not one bankster or FED criminal even indicted?

How is that “rule of law”?

As I understand it, Treasury has been concentrating most issuance on the short end of the market in TBills etc. Consequently during 2025, 7 or 8 trillion will come due and have to be re-borrowed. This along with the probable new issuance needed to cover the 2025 deficit of 2 trillion means 9 trillion of new issuance in 2025.

Is that considered to be a lot of issuance in the Treasury market ? Will the market have any trouble absorbing that supply at current or declining rates or is that a significant amount of new issue that will tend to push rates higher to enable the markets to digest it ?

It seems like much of the existing holders, will simply roll old debt into new ? Not sure how “hot” this short term money is. It also seems like the ease with which the market can absorb Treasury issuance depends on liquidity generally ?

I’ve read a couple reports that the Chinese are using some of the USD reserves to issue USD denominated loans ? It’s only been 2 Billion thus far, but what does it mean if China moves to recycle USD that accumulates into it’s own loans rather than into Treasury purchases ?

So many moving parts and unknowns in 2025. Since nothing else seems to work, the US seems intent on increasing the weaponization of currency, sanctions, trade and economics against all of our “enemies”. This seems easy for the US since there are no body-bags, but the costs and risks are real just the same.

T-bills as percent of Treasury securities held by the public:

With inflation rising, see Cleveland FEDs nowcast

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

versus more net private savings of households and institutions being absorbed by our fiscal deficits

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

interest rates have nowhere to go but up:

date;

10/1/2013 2462.787 680… 3.622

10/1/2014 2847.983 485… 5.872

10/1/2015 3162.291 442… 7.155

10/1/2016 2984.788 585… 5.102

10/1/2017 3366.586 665… 5.063

10/1/2018 3986.622 779… 5.118

10/1/2019 4712.634 984… 4.789

10/1/2020 10636.04 3132. 3.396

10/1/2021 8382.799 2772. 3.024

10/1/2022 2264.383 1376. 1.646

10/1/2023 3868.898 1684. 2.297

The deficits are absorbing more and more of all savings.

hmm but throughout this brave process of tightening, over the last four years, the 10 year treasury yield has been going up.. and the dollar has been going down.

10 year USA treasuries at 4.6%.

Also these prices (not unusually) are set at the margin its not necessarily clear that the fed can exit, and until it does, the fed is paying printed money interest on printed money deposits. The reason its going slow is because at any moment they may cross some invisible line in the market.

Look at what happens after the “good times” in all the charts.

people talk about meme stocks, but the entire market is a meme stock. look at tsla. it drops 6% yesterday because it missed deliveries, and now it’s up 8% based on nothing.

We are buying 10 and 30 year treasuries with Treasury Direct.

Hopefully we will be able to sell them at market value before they mature through Treasury Direct.

Transfer them

Did you check the website to see if that’s even possible? I kinda doubt it.

“Hopefully we will be able to sell them at market value before they mature through Treasury Direct.”

You’re buying 30 year bonds for personal use? I was under the impression that only pensions, insurance companies and maybe entities like States and Municipalities went that long on duration. Interesting.

I buy ten years through TD. You can transfer them out to a brokerage account then sell at current market value. But in that case it probably would have made sense to buy a shorter Note or Bill and just get the interest expected on time.

I have a 10y bought in early 2024 that yields ~4.1%. It’s now worth less than I paid for it, however that interest is rolled into Bills paying closer to 4.5. I have no plans to transfer and sell that particular note at a loss over the next nine years. In my view Treasuries should be the “foundational” paper assets for most people, and could make up maybe 5% of your portfolio in your 20’s and perhaps 50% in your 80’s. A big pile of cash loaned to the last entity you’d expect to miss a payment before the lights go out. Once you have a TD account you realize that all the money market and bank CD stuff chasing another 0.1% isn’t worth it. I’ve been very happy doing this online myself for over twenty years now. The last CD I had was with Countrywide back in 2007. I got my money back with around 7% interest just before THEIR lights went out.

The Fed’s existing MBS consist of low interest rate mortgages, and because interest rates have risen, presumably the market values of the Fed’s MBS are lower than the MBS book values. The Fed’s sale of MBS would result in a loss. What happens to this loss; would it be charged to the Treasury?

And if the Fed sold MBS at a loss, would it need to mark-to-market its remaining MBS inventory?

Losses don’t matter to the Fed or any other central bank that creates and destroys money as a matter of routine every day when it pays for something or gets paid for something.

Here is something you should read about the Fed’s losses — including its “unrealized losses” when it values its securities at market prices.

https://wolfstreet.com/2024/11/23/operating-losses-and-unrealized-losses-of-the-federal-reserve-in-q3-2024/

Thanks for the reference. If the Fed sells MBS, the unrealized loss becomes an actual loss, which disappears as a matter of routine. But why would the Fed sell MBS? If MBS are held, then the Fed receives its full value and the treasury continues to receive interest payments. For the banks and issuing agencies, buying MBS at a significant discount to book value would seem to offer windfall profits.

The Fed doesn’t really care about making money. But MBS are complicated for monetary policy purposes for two reasons, according to the Fed’s logic for getting rid of them:

1. They’re unpredictable. They come off the balance sheet mostly via passthrough principal payments, and those are unpredictable.

2. They show a preference by the Fed for some private sector debt — for example, MBS instead of corporate bonds — that it wants to avoid.

I know, I know, they shoulda thought about it beforehand. And they did, and they’d already decided to get rid of their first generation of MBS, and were already replacing these MBS with Treasuries in 2019 and 2020 through February, when Covid knocked on the door, and they panicked and started all over again.