Bring on the supply. Homebuilders may need to do some serious price cutting to move their inventory.

By Wolf Richter for WOLF STREET.

Big homebuilders cannot sit out this market, they have to do what it takes to build and sell homes to keep their businesses intact and keep their shares from tanking. So they’re building at lower price points, buying down mortgage rates, and throwing in other incentives at a substantial expense to them. Though that may not have been enough.

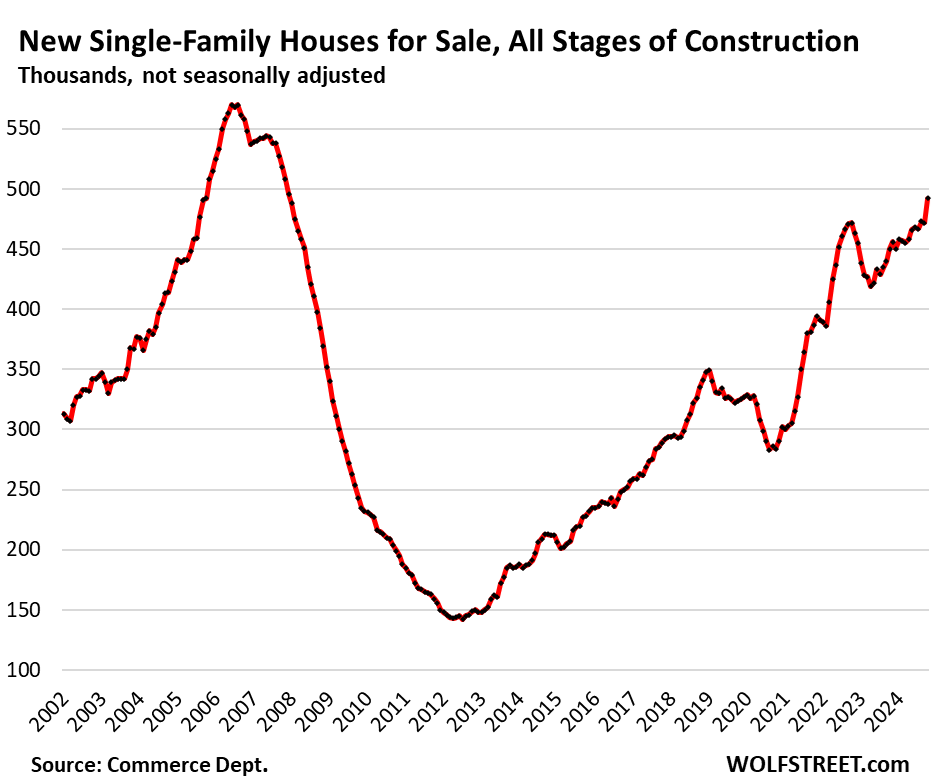

Some demand has shifted to new houses from existing houses whose sales have plunged to the lowest levels since 1995 because their too-high prices have triggered large-scale demand destruction. But inventories of new houses have been piling up, and then there’s this sales issue in October with spec houses.

Unsold inventories of new single-family houses at all stages of construction – from not yet started to completed – jumped by 9.3% year-over-year to 492,000 houses, not seasonally adjusted, the highest since December 2007, according to Census Bureau data today. That’s getting on up there. Supply rose to 8.2 months.

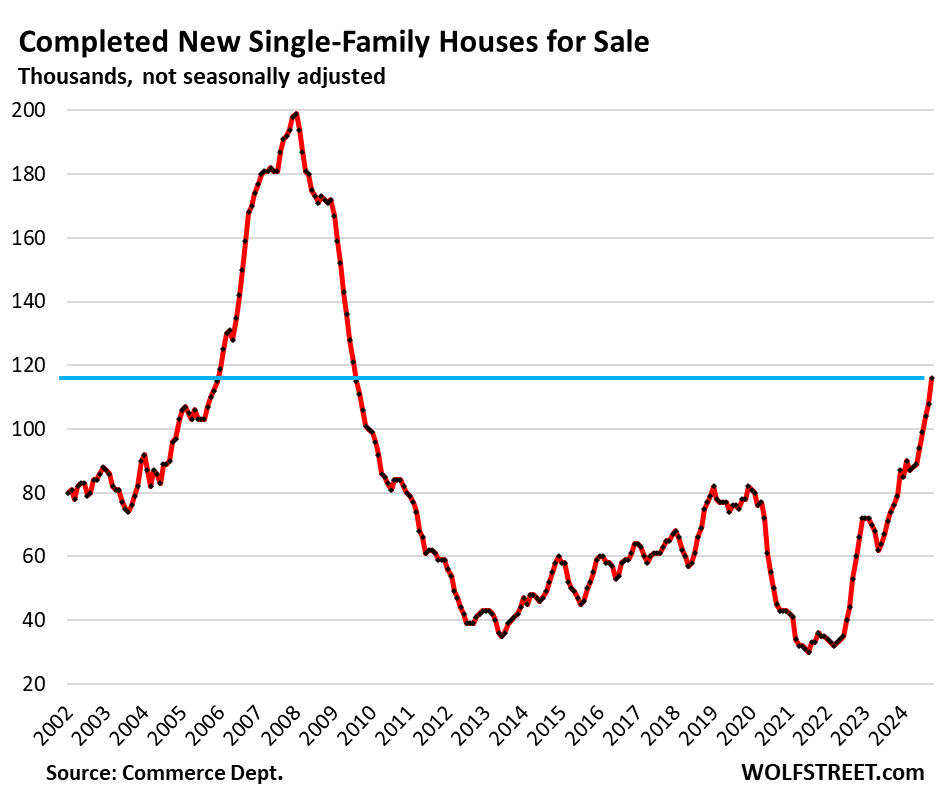

Unsold inventory of completed new houses spiked by 53% year-over-year to 116,000 houses, the highest since July 2009 during the depth of the Housing Bust when homebuilders were trying to survive.

These completed “spec houses” are essentially move-in ready. But builders haven’t found buyers for them yet — and they will need to pretty quickly because they have sunk a lot of capital into these completed houses.

The surge in inventory is a good thing for the housing market. Since builders have tied up a lot of capital in spec houses, they have to sell them quickly. Rising inventory of completed houses encourages builders to lower prices and offer deals, which will help resolve the mindboggling dislocations in prices that we’ve seen across the housing market.

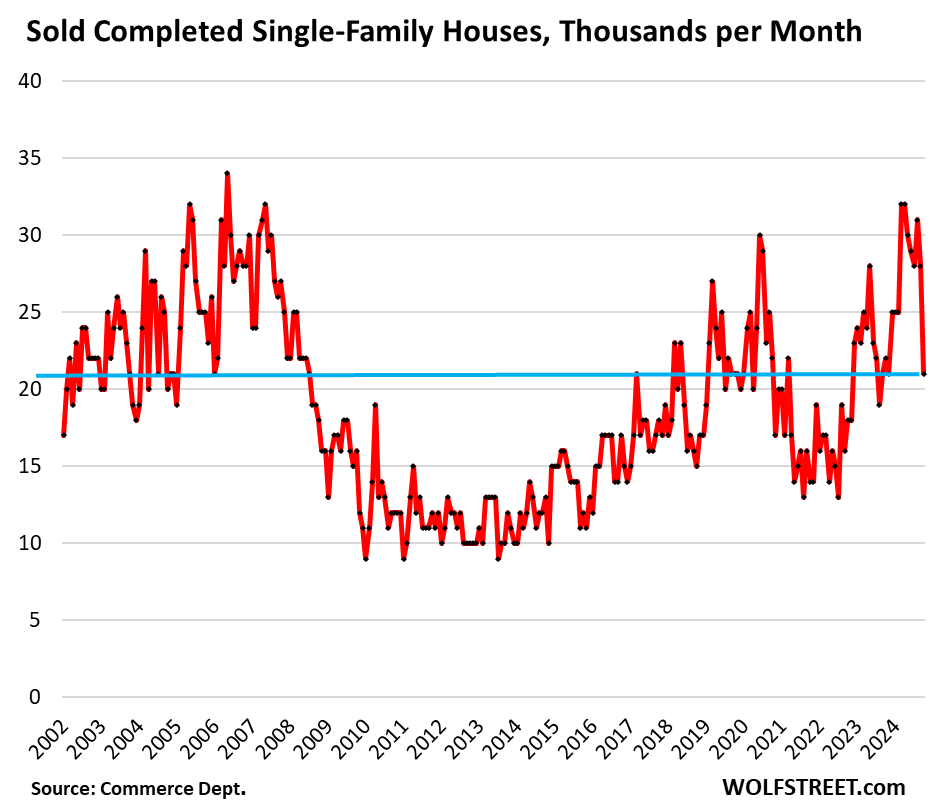

Sales of completed houses plunged 25% month-to-month in October to 21,000 houses, from 28,000 in September, and from 31,000 in August, a huge outlier, perhaps hurricane-related in the crucial South.

If this doesn’t reverse over the next few months, homebuilders will need to start some serious price cutting to get their inventory moving. Year-over-year, sales fell by 4.5%.

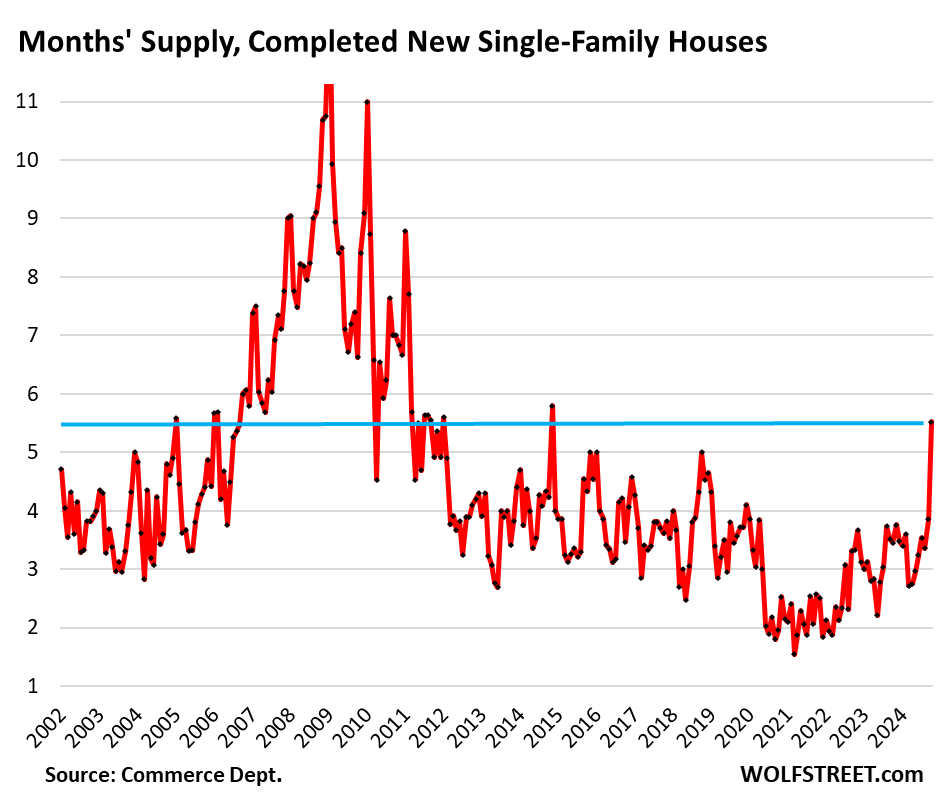

Months’ supply of completed houses spiked to 5.5 months at the current rate of sales, the highest supply since November 2014, and before that since 2012. Supply spiked because sales plunged and inventory surged. This level of supply of spec houses provides a strong motivation for homebuilders to offer deals:

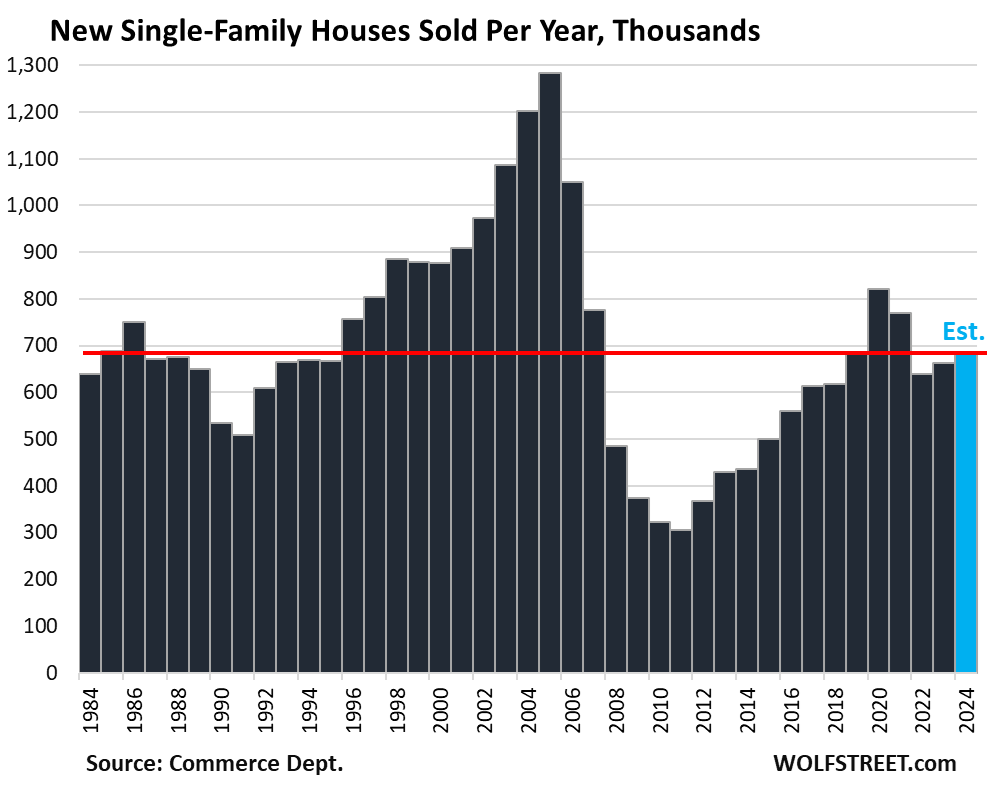

Sales of new single-family houses at all stages of construction, not seasonally adjusted, inched up to about 59,000 in October from 57,000 in September and were up by 7.3% year-over-year, despite the plunge in completed houses. Compared to October 2019, sales were up 18%. So outside of spec houses, sales in October held up.

Year-to-date, sales of new houses at all stages of construction rose by 3.3% from the same period in 2023. On this basis, we estimate that sales for the whole year will come in at 686,000 houses, about level with 2019.

Prices, mortgage-rate buydowns, and incentives.

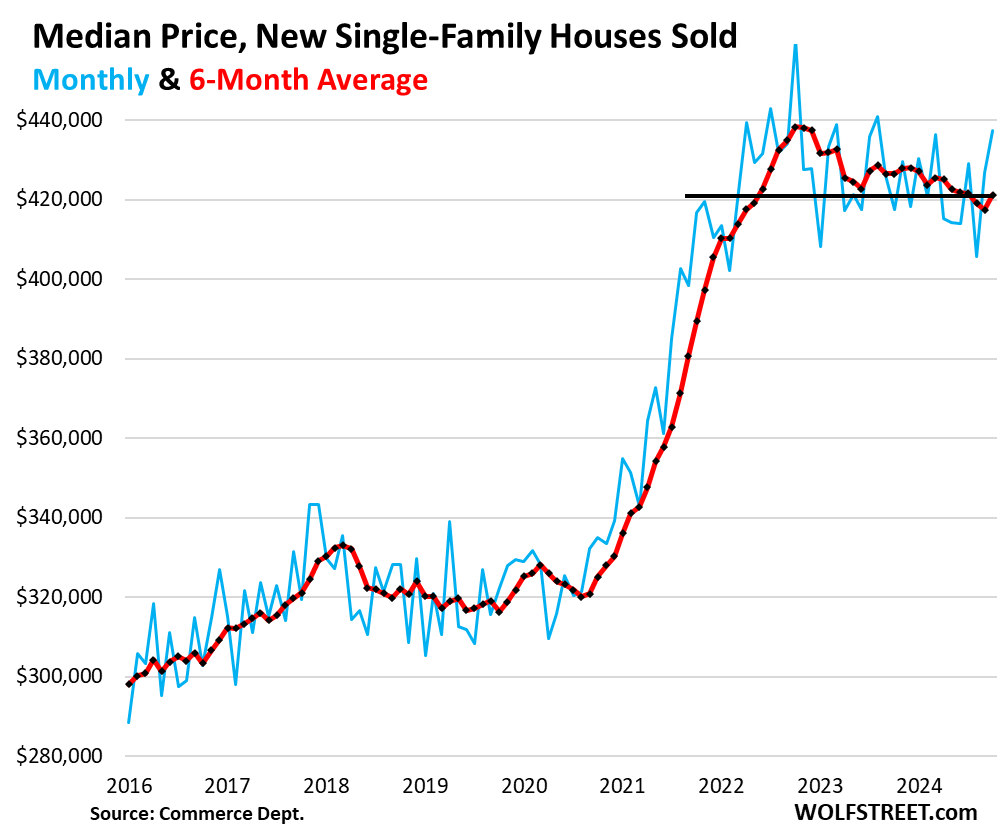

The median contract price of new single-family houses at all stages of construction spikes and plunges month to month in a random non-seasonal way, and it comes with big revisions after the fact (blue in the chart below).

In October, it spiked to $437,300. We had a similar spike in October 2022 to the all-time high of $460,300, after which it plunged.

The six-month average, which irons out much of the month-to-month volatility, ticked up to $421,000, down by 3.9% from its peak in October 2022.

Note that these contract prices do not include the substantial costs to homebuilders of mortgage rate buydowns and other incentives.

For example, Lennar disclosed that in Q3, the costs of its mortgage-rate buydowns and other incentives, such as free upgrades, jumped by 32% year-over-year to $48,100 per house it sold in Q3, which amounted to 10.2% of revenues. So this median price is only a partial measure of the pricing of new houses:

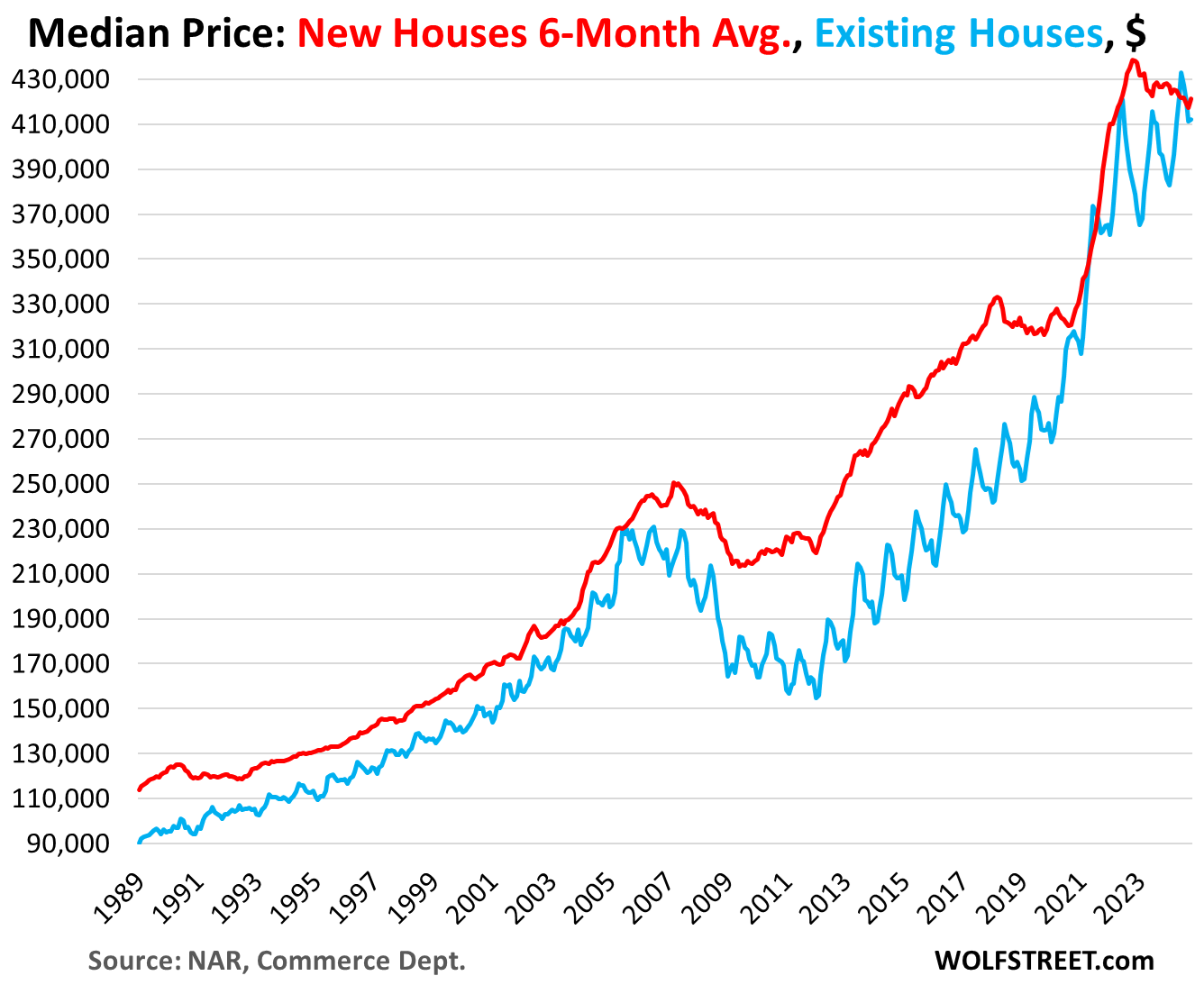

Prices of new houses versus existing houses.

Over the past four decades, the median contract price (six-month average) of new houses exceeded the median price of existing houses nearly all of the time. For most of that time, new houses were between 10% and 30% more expensive than existing houses. This changed in 2021 and then again this year, a very unusual situation.

With mortgage-rate buydowns and other incentives (which are not included here), new houses on a monthly payments basis are out-competing existing houses, which is why a portion of demand has shifted from existing houses to new houses, which is why sales of new houses have largely held up, while sales of existing houses have plunged to levels not seen since 1995.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yet another excellent update!

The housing market seems to be taking on a 2006-2007 vibe…. Some regional markets and housing types have started falling – faster – while others are still holding up.

It’s not so obvious in last 5 years but it looks like there used to be a seasonality in months’ supply prior to the GFC. Be interesting to see how much of the current spike “sticks” and where the next low is.

We are on our sailboat near Myrtle Beach for the winter. The amount of new construction in the area is beyond description. Single family. Multi family. Condos. There are over 2000 new build listings and 1000s more under construction. And yesterday we drove by a new build site that will have 300+ homes where they are just starting to clear the land.

Wilmington NC is the same.

I was just in the Wilmington and Wrightsville Beach area. My cousin works for a large drywall supply company. He said they’re slammed. My question is…

Do you feel this coastal area is overheated?? I know you mentioned a lot of listings, but our properties selling? The prices seem a lot more affordable per square foot versus Austin, TX (where I’m from).

3 years QT burrows it’s way through our economy.

The mantra of the natives is “Watch for the lag effect”

I can see why they thought in July 1929 that it was impossible for the stock market to ever go down again. I understand why bears capitulate at the very end.

I think there is a “retirement economy” which is almost independent from the general economy. Many retirees are sitting pretty— with bloated retirement account balances and paid-off homes which have had massive appreciation. And they are also getting decent interest on their cash holdings. So places like Myrtle Beach and other vacation/retirement communities may continue to grow and outperform everywhere else.

Valid point, Tony.

The outperformance you mention may continue until a stock market correction interrupts the pretty resting place retirees currently occupy.

As the late Marty Zweig pointed out in the 1990’s, over the (then) prior 100 years, 40%+ corrections in the Dow Industrials Average occur about every 10 years.

Perhaps that pattern is history, but I wouldn’t count on it. Into every retirement some rain must fall…

OR perhaps it continues until more hurricanes trash the place.

AuHound-

Yes. Either way, retirees will feel the generational need to “batten down the hatches!”

You should run with that concept of a “Retirement Economy!” I think you are spot on. There has probably always been a “Retirement Economy,” but the current one seems to be in fantastic financial shape.

This appears to be part of what’s keeping condo prices from falling very much in our region — there’s a steady increase in aging retirees who are moving out of their single family homes in favour of condos. I don’t know what the average stay for them in a condo is before they either die in place or are forced into a second move to a care facility, but there is some sort of regular turnover of this sort if my mother’s building is any indication. At least in our region (Ontario Golden Horseshoe) these buyers don’t seem to be terribly price sensitive and the turnover seems to be driving a thriving condo renovation (I mean individual units, not entire buildings) industry.

GOOD ONE Tony,

And I agree with your thesis re best or better locations.

While I am not much of an investor in RE as I was formerly, just enjoying the results for now in my 9th decade.

It certainly appears that we are in another vast and vastly different ”bubble” of RE,,,

OF COURSE it IS different THIS time,,, until, as WR has said many times, IT ISN’T…

Wilmington sorta makes sense – especially given the increasing Florida blowback (basically FL prices got way too high, too fast – again).

People/developers are looking for semi-nice winter weather (not Florida nice but not NYC/Boston crappy) at a price point that won’t cripple them financially.

So interest is going incrementally north from Florida.

Saw it with the incredible 2022-2023 surge in Charleston, SC.

But with the internet, newbie RRE speculators burn out individual emerging markets very quickly (far overpay, far in advance). Then have to try and sell at much, much less appealing prices.

Charleston is a prime example of this – so is Austin (in a different context).

Expert tip – if the appeal of your emerging mkt is that it is 25-33% the cost of CA or NYC/Boston…don’t bid prices up so that the local market is just 50%-65% of CA or NYC/Boston…you destroy most of the point of people relocating.

People/businesses want to *save* money by relocating…not just get almost-as-ripped-off-in-a-somewhat-less-ideal-place.

So Wilmington makes sense – I don’t think it has *ever* seen much of a relocation boom, so prices are still attractive.

But the truth is there are still multiple GA/SC/NC coastal sites (and, my god, slightly inland ones) that can provide excellent value with much better weather than NYC/Boston.

So long as RRE newbies don’t go from paying 1x to 1.5-2x in the span of a month.

>But the truth is there are still multiple GA/SC/NC coastal sites

cas127, please, don’t give them more ideas!

Four years ago I moved away from Northeast, as I thought I found a quiet and peaceful spot 40 min from Raleigh NC and bought a house in a development literally in between corn and tobacco fields. Four years later we have traffic backed up for half a mile in some spots and construction on every corner (and even more construction planned on paper for 2025-2030).

This is not even remotely what I’ve been picturing in my mind four years back.

Many of my friends in NC/SC have the same sentiment. A lot of folks jokingly see Wake county turning into “mini-NJ”, both from the pricing point and from the overall vibe. Just yesterday my former coworker who I haven’t spoken to in ages l, told me she can’t keep up with the development and is already eyeing more rural areas with acreage for when her kids are done with school in 4-5 years.

As a Raleigh native I’ve heard this story so many times. What did you think the corn and tobacco fields wouldn’t be developed? I remember when Crabtree was in the outer suburbs! Briar Creek was all hunting land and farms. And your friend. It’s just gonna do the same. Development will continue to get pushed out. Why the shock?!

540 is like being in the nascar 500 at Daytona. Cars come in on the right and immediately want to pass everyone on the left and do 110 mph, not to mention ride your bumper the whole way.

“Expert tip – if the appeal of your emerging mkt is that it is 25-33% the cost of CA or NYC/Boston…don’t bid prices up so that the local market is just 50%-65% of CA or NYC/Boston”

Do you believe there is some central authority controlling real estate prices in Charleston?

If we instead take the premise that Charleston has thousands of individual, self-interested sellers, then your pro-tip is essentially “throw a bunch of money out the window so the stranger buying your home gets an even bigger cost-of-living cut”.

i am not sure what would motivate Charleston sellers to forego a large sum like that.

You need to create a chart showing the price of new houses with all discounts in there. The true price of a new house is actually probably closer to 370k and shows the true value of new house over existing and accentuates the unreasonable price levels of existing homes.

The problem is where they are and how unwilling younger generations are to endure the shortest of commutes. See the huge rise is delivery meal services justified on the back of “not wasting time” and “finding time in hectic schedules) aka playing videogames.

WTH? Meal delivery services do save time. I can make a lot more money doing my job as a car & truck accident lawyer than shopping for groceries. And I wouldn’t say I’m particularly younger, either.

Plus, my money, my business.

My partner pays someone to walk his dog, drive him longer distances, run any and all errands, etc.

And when I’m going for a walk, then watching television with my husband at night, instead of shopping for groceries, that’s well-earned and necessary relaxation time.

You are so wrong. The younger generation requires two incomes and works longer hours than any other generation just to get by. Throw a young child in the mix and they literally have more hectic schedules.

Agreed.

Idiotic, doomed levels of housing inflation have badly hurt younger generations financially.

There have been similar bad times in the past (1979-82) but they weren’t as desperately, blindly engineered as purposefully by the Fed/DC (the 2004-2022 Long Night of ZIRP).

Older SFH owners have almost entirely *benefitted* from this – so they are eagerly blind to the harm/anger caused.

DC policy has turned the housing market into a manic-depressive casino for the last 20 years.

Glad to see the pushback on Billy McD’s non-sequitur of a reply to Adam’s very good suggestion on the chart with incentives. Even if it’s a squishy dashed line on that other chart as an estimate, it would still be helpful to gauge.

I generally find these sorts of personal critiques unhelpful and kind of cringe, and the only reasonable response is the classic, “ok, boomer.”

Nah, William is correct. So many people have so much free time on their hands, but refuse to do anything useful with it that they sit around doom scrolling or thinking about the (lack of) meaning of life, getting depressed , deleting themselves.

Where I work, the younger people make all kinds of money, inflation-adjusted, compared to what we did, waste it on total garbage, and then act like they’re poor and have been wronged.

Always exceptions of course. And everyone always thinks they are one. But whatever you think is fine.

That is very much “an old man yelling at clouds” comment.

Just tell them to get off your lawn.

I am the younger generation he’s talking about, and I can tell you that, as a whole, we are worthless, useless, brainless trash that couldn’t start a fire with a match and a full can of gas. Our helicopter parents made us this way. We are entitled, don’t know how to save, let greedy corporations take advantage of us, don’t fight back, and freak out and cry when things don’t go our way. We can’t form good relationships with the opposite sex because we have so much hate for anyone who thinks slightly different than us, even if we claim to be inclusive of others who are physically different. We lie on social media to show off or else we feel pathetic for not keeping up with those who do. We get investing advice from insurance hawkers on TikTok and don’t realize that’s wong. We don’t know how to cook, and would be too lazy to do so if we could, so we eat complete trash, often paying more for the delivery service than the food because we’re just that lazy. Sometimes we even let the food sit in the lobby of our apartment building because we’re too depressed and mortified to be seen by ourselves out fetching it like a loser. The only way we can leave the house is in Pajamas and Crocs, preferably with a man-bun, and with our only friend, Fido, who we don’t pick up after, and often just let him go in the house because we’re bored with walking him, and don’t care about his well being.

I could go on, but this is starting to feel…unhealthy.

The mortgage rate buy-downs negate the effect of interest rate increases, leaving the selling price unchanged, and thus not impacting inflation numbers, while reducing profit to the builder. Why not just drop the price? Presumably builders would prefer to hold their apparent selling prices and pay for incentives rather than drop prices then raise them again when rates fall. The unsold housing inventory may be getting too big to sustain this strategy.

Some builders around here (south Texas) have dropped prices 10% across the board, AND are still offering financing incentives. These are “starter” SFH’s that sell for around $175/sq. ft.

Once significant price drops are implemented, the whole thing begins a repricing downward spiral. They want to avoid that at all costs.

Similar to comps in a neighborhood. If I sell my house 30k under market to move it, that affects what everyone else does.

It’s like a bad AI headline: The One Trick Builders and Realtors Hate

“Once significant price drops are implemented, the whole thing begins a repricing downward spiral.”

This.

By obscuring the true transaction price, it is much easier for the builders to try and BS the *next* potential buyer to pay the phony “market” price.

See also, price discrimination in college tuitions…

Offering incentives rather than a lower price makes it harder for the buyer to become a seller and thereby compete with the builder. The incentives go away upon resale while the higher mortgage balance inhibits price cutting upon resale.

That is a really good insight that I hadn’t thought of before.

Sounds extremely similar to new car “incentives”.

Boy, using financing to,

1) Jack up primary transaction prices up by manipulating monthly payments down and

2) also restricting secondary mkt supply by retroactively jacking prices up (financing incentives go bye bye)

is some master villain level planning.

From an accounting perspective it might also be that the rate buydowns are an incentive expense whereas a reduction in selling price could impact the value of the inventory (e.g. houses) on the company’s balance sheet. Maybe Wolf accounting extraordinaire could correct this assertion?

Inventory is carried at cost, not at sales price, and sales prices don’t impact inventory unless sales prices plunge below inventory cost, which would trigger a write-down, but we’re far from that. Builders are still making gross margins of 20%. So it makes no difference on the inventory valuation whether the builder gives a discount on the sale or throws in a freebee.

Builders take the upgrades they give away (incentives) to the construction costs of the house. By installing nicer counter tops, they put more money into the house, and therefore make a smaller profit on the sales price. These upgrades (incentives) are just part of the construction costs of the house. But builders track them separately for memo purposes so they know, and some break them out on their quarterly financials, like Lennar did.

The costs of the mortgage rate buydowns, including the costs of the hedges that are involved, are taken straight against the gross profit margin. This is how DR Horton described the accounting during the earnings call, when asked, after their hedges had blown up a year ago and trigged a substantial charge (write-down of the hedges).

I know that where I live San Francisco, I will never be able to own a home. Even if I had an income of $225K/yr. Maybe a very small condo with no parking or someplace in city limits where I would need to drive to get basic necessities. Those are not really something I would invest in long term. Rent is outrageous for a place with a washer and dryer and a parking space. Hardly anything left over for bills, let alone a down payment on a house. Meanwhile in my building I would guesstimate half if the condo units are completely empty some having not been occupied for years. Wall Street vultures having snapped them up long ago. Politicians say we need more “affordable” housing but I don’t qualify for any of that. Rent for life I guess!!

Yeah you should be aiming for an affordable subsidized condo if you are making under 200k and you can only afford a 5 figure DP. Need to make >200k, with 400k saved for DP to get decent market rate condo. And 500k min. to afford a SFH, with 0.8~1.2mil DP. Of course if you have that much for a DP why you wouldn’t keep it in the stock market and make some sweet dividends is beyond me. I presume lots of marriages have issues only resolved with remolding projects to keep the mind occupied.

Welcome to the Bay, if you don’t like it, I guess you can move to Chico and get your yard.

There’s a development near me in San Diego starting at $2.3M for a normal 5 bedroom home. At current rates that would be around ~$20K per month.

I rent a house right next to the development for $4600. The new homes are nice but Lennar is smoking crack thinking people will pay that much for a tract home in the SD desert.

“Normal 5 bedroom home”??

I don’t think a 5 bedroom home is “normal”. Maybe I am missing something?

Agreed. No one needs 5 bedrooms. That’s crazy. In SD, new 3-4 bedroom homes with small yards start at $1.4M+. Townhouses with 3-4 bedrooms start at $1.25M.

“No one needs five bedrooms”

Five bedrooms might sound like overkill until you do the math. Master bedroom for us, 2 kids bedrooms, spare bedroom (all our family is out of town and they don’t like sleeping on couches), and our 5th bedroom is my office (full time WFH).

Of course, we live in Jacksonville not San Diego. Probably half the houses in our neighborhood have 4 or 5 bedrooms.

@Duck – you like the extra 3 bedrooms but by prior generations’ standards, none are essential… you just proved Randy’s point.

BG- by prior generations standards most of the conveniences we have today are not essential. Prior generations of my family were proud that their children had more than they did. I will feel the same for my kids.

As for what is “essential” that is decided by each person individually according to their circumstances. The statement “no one needs five bedrooms” is provably false. Plenty of us have decided that we do – regardless of whether others think it’s really necessary or that we could probably get by with less.

Agreed…the median family size in the US for a long time was 2.6 people – so 2 or 3 bedrooms got the job done.

And birth rates have been cratering post Housing Implosion 1.0/Baby Boom retirements.

So we could see median household sizes of 2.0-2.2 (or lower if illegal immigration is dealt with at all after 40 years of “efforts”).

So 5 bedrooms doesn’t make a lot of sense…outside of the McMansions for McMorons trend of last 25 years.

A buddy in Chicago listed his 2 BR condo in the high $500s (record high for the building) over the weekend and has two competing all cash offers at or over list. Has nothing to do with single-family spec homes, but just making the point that even at nationally high inventory levels real estate is very local.

Daughter just sold a SFH home in IL for under $200M NE of St Louis metro. This was more than double what she paid some years past.

200 mill?

Chump change.

Lol jk

You’d think they’d want Malibu with that kinda cash ;)

Here in the western suburbs of Chicago we see lots of new construction going on.

Mostly, it seems, multi-family rentals or “Luxury” condos.

Not sure about what’s actually selling though.

Builders might have better luck selling if they wouldn’t build houses less than ten feet apart. I prefer not having a neighbor who can easily spit into my window from his window. I have more privacy in my apartment.

Local government allows close together houses since the tax revenue is increased for more homes on a large parcel. This works if infrastructure can handle it (water, sewer, etc).

You people don’t get it, do you? People complain all the time, and rightfully so, about home prices being unaffordable, and builders are trying to meet that demand by building at lower price points precisely to make homes more affordable, including smaller floorplates and smaller properties, and here you come, complaining about not enough space between houses.

People who want to spend extra money can always buy a house. But that’s not the problem this housing market has. The problem this market has is that houses have gotten too expensive.

Hey Wolf. At first I thought it was a typo but I’ve now seen you use the term “floorplate’ more than once. Is that spell check run amok or some term I’ve just never heard before?

just an RE expression. You can google it for a definition. It can be spelled with a space or as one word.

Nothing cures high prices like high prices! Patience is all it takes.

That’s not entirely true. What they are doing is trying to maximize profit given the available space to build. They are clearly not building for affordability by building the largest possible square foot structures on as small a plot as they can get away with.

If they were building to meet the demand of affordability they would build smaller homes on those small plots. 1000-1200 square foot homes would serve that demand better than 2000+ square foot homes.

Just read the quarterly earnings statements of the homebuilders. They’re talking about it. I linked Lennar’s in the article. You will see that Lennar’s average sales price dropped about 6% yoy, to $422,000 in Q3 2024 from $448,000 in Q3 2023 — smaller homes and cheaper finishes because that’s where the demand is.

Lennar’s gross margins dropped by nearly 2 percentage points in Q3 YOY, to 22.5% from 24.4%.

They’re in the business of selling homes. If they can’t sell because prices are too high, they have to sell at lower prices, and to get there, they’re building lower-priced homes, including smaller homes, that they can sell at lower prices, and they’re throwing incentives into the mix and giving up profit margin. But they HAVE to sell. That’s their business.

It is more than just maximizing profit. It is mixing profitability per square foot versus saleablity (how fast the houses were going to sell).

A perfect example to demonstrate this:

In the place with the new construction we were looking at there was a weird cross street at the back of the subdivision. It was a small street. When we first looked at it, it was divided up into 4 lots. They were bigger than average a d the builder was charging a big premium for the lots.

When we visited the second time. The same street was divided up into 5 smaller lots. Smaller than the average for the rest of the subdivision.

Initially the builder was trying to get premium money by offering bigger lots. When the market turned against them they adjusted and went to smaller lots for less. The builder probably makes a little less money overall (building an extra house costs a lot in upfront capital), but those 5 houses were more likely to move quicker than the 4 that would be built in the same space. Price point matters in this market so they adapted.

In Phoenix the infill boom has led to boxy two story houses shoehorned into odd “behind the gas station” corner developments where 15-20 houses sit arranged on maybe 3 acres (after room for a narrow road and “green space”), and the houses are literally 6 feet apart. The code must require 3 feet on each side for access. You can’t put a tree there, maybe a shrub near the block fence.

Really what these are are townhouses, with a minor gap to prevent sound transmission and give the appearance of SFHs. You’re not going to open your side window blinds for the view, or sit in your 8 foot deep back yard for any length of time. People buy these houses to live on the inside. Maybe they’ll change hands every 2-3 years as people try to move up the property ladder.

Do you think you are projecting your requirements on to others? I know lots of people who love on such homes for a long time simply because they do not care about the size of their yard.

Florida Home Sales Plunge As Sunshine State Becomes Less Desirable

We keep hoping beachfront prices will come in line with the risk of buying them now. Prices are coming down, but not fast enough. Many near the beach houses are still selling way too high. The few select beachfront houses we’ve been watching (and will continue only watching forever unless the prices massively drop) are just sitting there collecting dust with stubborn owners.

Make a reasonable offer. Worst case they say no, but that’s always possible.

I been saying the same thing for 4 years now. Prices are flat….but not dropping.

Lots of wealth still being generated in the U.S. via stocks and interest from treasuries. Plus who knows, maybe all those NIL millionaire college and football players are buying beach front property as investments. LOL

For my purposes, inventory is still zero because the new homes for sale are butt ugly (open concept, split entry and no basement in neighborhoods with small lots and on a flood plain). No thanks!

Recently I booked a new house with $285 sqft from builder. In same community, 4 years old homes are listing $325 sqft and above. Builder are giving lots of incentives to sell the houses. Existing home owners still in cloud.

Wolf – this data, is it available on a region by region basis?

Some. Not much. What’s available by regions are two things: “Sales at all stages of construction” and “Inventory at all stages of construction.”

But what I really want to know, and what I highlighted in this article, is “completed houses for sale” and “completed houses sold,” and that data is not available by region.

In addition, the sales figures are very small by region and rounded to the nearest 1,000. So in the Northeast, you will see 2 in October, 2 in September, etc. But that could be 1,501 or 2,499 houses, and so this sales data by region is useless.

This data set has enough problems on a national basis with revisions and random volatility. Subdividing it further makes these issues much worse. It’s just not the kind of data that’s useful for smaller geographic areas.

Hypothetically, if I went to Lennar and said:

“I’ll buy that house, and waive all the incentives/mortgage buydown/etc., if you sell it to me for $48k under asking”

Would they do it?

Lennar listed 1257K, i asked for 1150K. They agreed for 1167K.

90k off 1.257M = 7.2% discount. Not bad.

But I was thinking of 48k off a median 420k house – numbers pulled from the article, and an 11.4% discount.

Where was this? I can’t imagine them doing that in any place super desirable.

Lennar is doing this in all its markets. From Lennar’s quarterly report linked in the article:

Is there correlation with the location home builders are doing most of the new home building and where prices have fallen the most/fastest?

Great question. I bet your on to something. I bet if you look at the inventory and sales price for existing homes that are considered starter homes…. I bet there is not much if any price drops.

It looks bleak for the houses, a new mailbox, didn’t make a difference. Now what to do? I’ve dropped the price 3 times and nothing.

I think I’ll raise the price, two can play this game.

Does Wolf eat Shichimenco this time of year? ….just wondering.

We can wait an eternity. This issue is that after your three price drops, obviously the sales price is still way too high. Buyers look at everything in their price range, if your house doesn’t compare favorably, they will pass. And if everything is too high (it is), and they can afford to wait (most can), then they will wait.

For those who need mortgages, waiting isn’t an optional decision. They cannot get approved because the prices are currently WAY TOO HIGH based on nearly everyone’s income.

Prices need to drop 50% in most places. Bring back 2008 bc that’s what’s needed.

“Prices need to drop 50% in most places. Bring back 2008 bc that’s what’s needed”

So instead of “I got mine” now it’s “I’m gonna get mine”? Don’t worry about the massive amount of pain this would cause to millions of people who did nothing to cause the current mess. They have it, I want it, screw everyone else.

You need to bake cookies right before a showing. Hooks ’em every time.

For those wondering about “shichimencho” it means turkey in Japanese. The Japanese celebrate “kinro Kansha no Hi” every November 23, a holiday similar to our labor day. They don’t eat turkey like Americans do. So…..happy Kinro Kansha no Hi…

Why am I telling you about the Japanese?

Because…

Since buyers look to still be on strike as both prices and rates are still far too high, I would expect to see builders considering smaller, less expensive, and more energy efficient homes.

For example, a sub 1000 Square foot single family home meeting the German passive house energy efficiency standard would likely be quite attractive to singles and couples without children. Energy bills would be only a few hundred for an entire year or heating and cooling.

I’d certainly buy one of them.

That sounds horrible. A lot of builders need to go bankrupt or slash their profits and people who bought in the last several years need to lose a lot of money. Those who bought long ago need to give up their fantasy home values.

For those without cash, this is simple math. If they earn 100K per year, for example, then they qualify for whatever amount of mortgage. They don’t qualify for seller’s fantasy prices. That’s most people.

And those with cash mostly are being patient and have no need to buy. We want a vacation house and have cash. But there’s no way we are risking a purchase in what is obviously a declining market. We will air bnb forever if needed. That’s no problem either. Probably better in the long run bc we keep our options open.

We are also investors but today’s prices will not cash flow so that’s definitely out.

What Florida Coast and area are you looking in? All Florida coastal communities are not created equal. Insurances and taxes are a big deal.

Sales are still local.

That sounds horrible for you. Obviously they feel differently.

“ A lot of builders need to go bankrupt or slash their profits and people who bought in the last several years need to lose a lot of money.”

I hope we never have to live in the world you’re proposing. Let’s blow up the whole thing so you can “cash flow” that vacation house you always dreamed of? The tiny violins are deafening.

Probably not. The homebuilder monopolisation is going to enable higher prices for longer. See this substack by Matt Stoller to learn more.

Nonsense. It doesn’t matter what prices homebuilders want. It’s the buyers that set the transaction price. And homebuilders ran into that: buyers refused to buy at those prices in the second half of 2022, and those that already bought cancelled, and sales plunged and FORCED homebuilders to come down. Even if it’s just one nationwide builder, if they want to sell houses, they have to price them where demand is or they don’t sell houses. They can build houses, and pile up inventory, but they cannot sell if they don’t price them where demand is. That’s the situation the market is in now.

I have a different view. I have seen young buyers capitulate after several years of waiting for “normal” prices because their growing young families were bursting at the seams in their small apartments. Household formation can only be postponed for a short while, not forever. These are not buyers at any price or buyers by choice.

Housing is an essential commodity and I think the supply is managed pretty well by builders and other industry players.

Agreed that there are some areas which have high demand or limited land. But to have prices ratcheting up and then exploding across the entire country where there is no shortage of land like they have done since the GR, this is only possible if the supply was “managed” by industry players.

For a free market to operate in real estate, where there are a few million buyers every year, there should be at least a few thousand big builders. Instead, we have a handful of big builders like Lennar and maybe hundreds of really tiny ones. This is not a free market.

Your assumption is flawed. The market is manipulated, but free.

No one is forced to buy, ever. Builders are free to set prices, you’re free to respond.

They, and I, will set prices to the maximum every time. You would too.

Jump in the there and become a big builder. Should be easy if there’s a need for thousands.

Perhaps a loan of a few billion from one of the big builders would get you started?

Those buyers who capitulated for whatever reason are the problem.

In my market buyers want to capitulate and buy at these prices desperately.

The only problem is .. they can’t afford and on top of this they can rent the same home for 5k vs 10k to buy

Hence prices are going done with historically low volume and increasing inventory.

I don’t think most buyers are smart enough to see that prices are very high

They want to buy but can’t because they just can’t afford

@Pilotdoc:

You said: “The market is manipulated, but free.”

“Market manipulation is a type of market abuse where there is a deliberate attempt to interfere with the free and fair operation of the market.”

You don’t seem to know the very definition of a free market. Enough said.

I am going to ask you your definition of “free market”?

Any reasonable answer you come up with can easily be painted as a manipulated market. As the most basic example, should the government regulate fraud (i.e insuring one barrel of oil sold is 1 barrel of actual oil and not a 1/2 barrel of oil and 1/2 seawater)? If you believe i the government doing basic fraud regulation then you no longer believe in a free market.

Right now, the housing market in the U.S. is among the most absolutely free markets in the real world. Sure they might not meet some crazy ideological libertarian definition of a free market that doesn’t exist anywhere, but my point is to make it a real world discussion and not some theoretical how many angels are dancing on the head of a pin BS.

@ Pilotdoc –

you’ve been smoking what ????

a free market requires many buyers and sellers with no or low barriers to entry

People don’t realize that home builders are not really in the house selling business, they are in the transaction business. They need to move houses.

For them, the difference between 12% and 15% profit is not as important as time on market. Builders pay electricians, roofers, framers, etc up front and carry that cost until a house sells. Furthermore, it is very expensive for a builder to start and stop construction.

Ideally they want a backlog where they can have workers come in and always have something to do. If the back log dissappears, they have a choice of either telling the workers to stay home (meaning they might look for other jobs and never come back), or to start to build unsold lots where the builder carries the cost of construction until the eventual sale.

It is a tough balancing act. So when sales are slightly tight, they want to keep the workers on, so they will just sell lots for what they can get for them just to keep the line moving. The alternative is to tell workers to stay home and then not be available when times are better.

Keep the line moving is what the builders want to do in uncertain times like now.

I don’t think it’s fair that they can offer these high dollar incentives that aren’t reflected in the sales prices, it has kept new home sales prices artificially inflated. Anything to prop up those prices!

Exactly. They want to preserve the illusion of high prices so they can ratchet them up from that higher base as soon as they see some demand pick up.

A true free market with lots of suppliers/builders will make these tactics transparent.

Sean Shasta,

I made a comment above exploring the same thing. I think it’s about perception: builders want you to percieve that you’re getting a 420k house for “only” 372k with the incentives… but if they just lowered the price to 372k, then it’s no longer a 420k house…

Kind of like how electronics mfgrs never lower MSRP – they just put an item on perpetual rebate until it’s discontinued, and then release next year’s model at the same or higher price.

Perceive*

Forgot my “i before e except after c” rule…

Just like there’s a place to enter in concessions in the multiple listing service when a sale takes place, there needs to be a place to enter in “incentives/rate by downs” as a dollar amount.

Sean,

What is preventing you from buying land and becoming a home builder?

You literally do not understand what free market means. Rrgulstion is required unordered to bring about greater transparency in a free market, yet you most likely do not think regulation means a free market.

Besides, you are wrong in the basics. It is very clear and transparent what home builders (like Lenner) are doing from looking at their regulated SEC statements. It is clear they are using incentives to get higher sales prices. That is very clear.

This is not something homebuilders are doing, but how the Census Bureau collects the data. They collect the contract prices written into the sales agreements. That’s what the buyer pays for. The incentives come out of the profit margins of the builders, and you can see them on their financial statements. Each publicly traded builder in their quarterly earnings reports discloses all kinds of data on their sales, including average price, incentive levels, gross profit margins, etc. But the Census doesn’t collect that data. You can do that yourself, if you want to see it. For example, in this article I mentioned Lennar’s per-house incentive spend and linked their quarterly report.

No one, and I mean no one, cares about what you think is fair. It’s neither illegal nor immoral.

They do it, you’re obviously aware of it, so adjust accordingly. Fairness is irrelevant.

I don’t know how similar it is in other states, but in mine, prices rose until the median income qualified for a mortgage on the median house, with similar balance at the other percentiles. Then mortgage rates spiked and prices stayed where they were (actually, they’ve gone up slightly). Now you need more like a 75-80th percentile income for the median house, with similar imbalance across the spectrum. That’s just not sustainable, and incomes aren’t going up *that* fast. There was some pent up demand, but I think that’s now exhausted and the simple mathematics is starting to dominate. Either rates are going to have to come down or house prices are.

Rates are not coming down, at least not meaningfully.

Home prices will fall and rents will rise, as sure as the sun rising in the east.

I wouldn’t be so sure about rates. With Trump in office, absolutely anything is possible. He will push for control of everything and our institutions haven’t done a wonderful job so far of having a spine.

What implications for the housing market of Trumps projected policies such as mass deportations which will decrease demand and shrink the sectors labour market. Tariffs on cost of building supplies?

Actually, Govt/Trump/FED can’t really control the mortgage rates without any serious repercussions.

There is a reason, despite FED cutting rates by 75 bps so far, long rates have risen a lot.

I’m a landlord, with properties spread over 3 states. I raised rents in the late summer an average of 11%. No one moved.

DaveP,

How many illegal citizens do you think are buying houses?

Remember, buying a house requires a person to create a paper trail with the government and spend lots of money for an asset that could easily get taken away from them.

why do you think rents will rise?

how much?

I see the same thing. Rent and mortgage as % of median income on new transactions has spiked so that it is essentially @50-70% instead of the historical 30-35%.

Last time this happened was 2005-2008 where the sellers tried to hold the floor but it gave way. I don’t hope for things to swing one way or the other but it is interesting.

I realized I look old, weak, and vulnerable by the distribution of bids that I received too replace two air conditioner units, the 4 ton and a 2 ton.

The first bid by the TV recommended firm was $68000.

The next TV recommended came in at 48 grand.

Then the local face, offered to the job for 32 grand.

Finally we found an honest guy who did the job for a reasonable amount.

Why would you bother with TV recommended brands?

@Random50

You are correct about that 75-80th percentile.

Here in Utah the S.L. Tribune ran a story last week that showed unaffordability in very single county in the state. In no county could the median income family afford a median price home no matter how low the median was in some cow (or coal) counties.

Marriner Eccles, some would say was the father of the FDR New Deal. He was from SLC, Utah.

The retirement economy thought is interesting. With growing numbers of asset rich olds, one can make the argument that there is less sensitivity to price and rates. They can also hold houses that they want to sell on the market longer.

As one is delivered ever closer to the mortal coil. Money becomes less valuable in one’s personal list of accomplishments.

Perhaps

To what degree is this new housing coming up inside existing urban footprints vs just outside vs way outside?

There are home builders just outside the SF Bay Area building up a storm, for instance. These communities are relatively affordable, and seemingly well built, but at least 60-120 minutes by car to the major job centers.

I can only imagine what insurance or infrastructure limitations exist for these communities.

Are other new home communities around the country similar, or are they more closely integrated to the existing metro area?

The home builders should join the buyers strike. They have more too lose.

Building a spec house that won’t sell is expensive. The carrying cost is enormous. The builders pay for it.

Well the first step is to make all federally sponsored or guaranteed loans would be transferable to a new buyer.

a better step would be to get rid of all federally sponsored or guaranteed loans

Since C-19, the Case Shiller home price index has risen 53%. But disposable personal income has just risen by 32%. Homes have become less affordable along with lower inventories. Rent has yet to adjust.

Bernanke bankrupt half the home builders during the GFC creating this shortage. Powell has recently exacerbated this out-of-balance condition. Long-term money flows, the volume and velocity of money, bottomed in August.

You had me until you besmirched the evil genius of Bernanke whose hypothesis was imposed, suppression of the interest rate structure.

I submit that the housing price bubble is an artifact of ZIRP policy during which the federal reserve expanded their balance sheet with scant regard for the victims while bowing too the ……

Wolf,

I think there’s more factors needed to interpret those home inventory data.

US 2002 population: ~288 million

US 2024 population: ~341 million

~53 million people added over 22 years.

US 2002 home ownership rate: ~68%, ~195 million.

US 2024 home ownership rate: ~65%, ~221 million.

~26 million home owners added over 22 years.

I realize it might not make mathematical sense or be possible with available data to separate this group of “new” people into a separate statistic, however… I’m tempted.

Home ownership rate of added population : ~49%

I suspect that combination of data is saying something important.

Am I chasing ghosts?

You are chasing ghosts.

Unless you can prove that EVERY SINGLE HOUSE has only ONE occupant.

Aren’t we all, chasing ghosts. Some would say that is common too the looniest wild creature, humans.

Unaware of their place in the universe.

Six years ago I was interested in buying a 1,850 sq ft 3bd, 2bath, 2-car garage house that was listed for $320k. The exact same house is now on the market for $680k. The base monthly payment went from around $2,200 per month to $5,300. per month. Today’s lack of affordability is going to have a profound impact on our economy going forward.

6 years ago the S&P was about 2900 (before correcting to 2500) and is just under 6000 today.

Gold was about 1200-1300, and is 2600.

Either everything has been a great investment or the green pieces of paper are worth about half.

The discrepancy between the bid and the ask price of the asset, housing is highly irregular. The last time was a fiasco. Now is a fiasco caused by ZIRP.

Let’s see how they resolve it.

Bad shit happens when bubbles collapse.

I was just going to add that the health of the housing market is one symptom as to the overall health of the domestic economy, itself a component of the world economy.

Context matters when it comes to elections, I think. I’m probably wrong.

Too me, there is preternatural, hair standing up on the back of my neck feeling that every asset category is overpriced by a huge amount and the collapse of the edifice is likely too resolve in a manner that ordinary citizens pay the price, like last time.

The commenter who said no one cares about fairness is wrong on two counts: many, especially liberals, do highly prize fairness; and as for it not being immoral, if it’s unfair that’s usually the definition of immorality.

Fairness is so 1980’s….

Wolf,

This actually reinforced your overall point, but it needs to be pointed out.

New home inventory growing is indeed a dire situation. Homebuilders are very reluctant to lay out capital they do not need to. So when times are going good, they won’t build a house until they have a buyer for it. Their workers are busy elsewhere so there is no need to start a new house before it is sold.

As things slow down, the builders face a dilemma. Do they slow down the building of new homes (which means laying off workers which can make it harder to ramp up if demand picks up, or do they continue to build houses despite them yet being sold (keeping the workers busy)?

Obviously it is a mixture of both. You slow production by laying off your newest/worst workers, but you also continue to build homes hoping they will sell.

Builders absolutely, positively hate building a home without a buyer. Land maintenance costs are bad enough, but are generally tolerable to responsible builders. Floating the construction cost of a new home is brutal. They are paying labor with only hope of recouping it in the future. That can quickly get crazy expensive for a builder.

So the fact that inventory of new homes is jumping drastically should be a huge red flag for both investors and buyers of new homes. Unless things suddenly change (which there is no reason to think they will), homebuilders will probably soon drastically slow the building of new homes and look to dump existing inventory for whatever they can reasonably get. Homebuilders do not price anchor like homeowners do. They are a cash flow business. Better to get something better than holding a declining asset for years.

So the fact that new hime inventory is increasing is a huge red flag for existing home prices. People of existing homes who are motivated to sell are going to have a ton of competition from builders looking to dump houses at any price.

When we were looking at a house, one of the things that was important to is was high ceilings on the first level. We wanted 10 foot ceilings. The new houses we looked at had this as an option for an extra $15,000 – $20,000. If it would ha e been cheaper we might have bought there 9 months ago.

Now, when we stopped just for fun, the builder was offering 10 foot ceilings for free. Now, to a builder, the difference between the first floor having 8 foot versus 10 foot ceilings is negligible. Labor costs are near equal, material costs are very small. Two extra feet of studs, drywall, and some electrical piping. Likely hundreds, maybe a couple of thousands. The builders were making huge margins on those who wanted higher ceilings on the first floor. Now they are literally giving it away.

Homebuilders are not yet hurting, they are still positive, yet it is clear that they are doing everything they can to move product. However they are running out of tricks so the only thing left is margins.

Once the homebuilders surrender margins, look out below. They will try and dump whatever product they have built. That is going to have huge implications for the overall housing market.

I am part of the “Retirement Economy” looking to follow grandkids to the Austin Tx area, specifically Dripping Springs. Last week visiting we saw hundreds of new home construction projects. Can anyone comment on this particular regional situation?

Happening in the Houston area too. Lots of people moving to Texas.

Thank you Wolf. Love reading your articles and comments in the chat. Very helpful to understand the current situation as we are watching and will be moving mid next year. Selling then buying.

Just saw a posting of home with a total of 7 price reduction, 2 times removal of listing over last 7 months. The house is still unsold. Original posting had a listed price of ~$630k and current listed price is $505k. The house is in Coppell, TX.