The 10-year yield surged by 60 basis points in five weeks but may run out of steam by about right now.

By Wolf Richter for WOLF STREET.

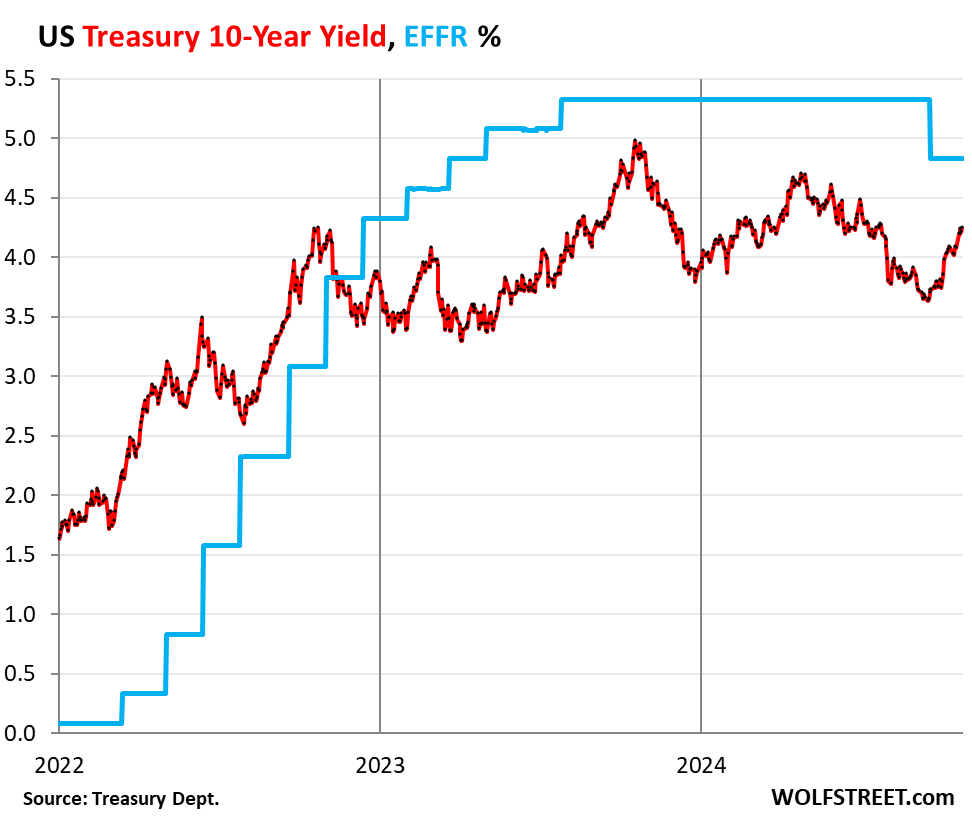

The 10-year Treasury yield rose to 4.25% on Friday, up by 60 basis points from the day before the Fed’s monster rate cut (when the 10-year yield was 3.65%), and up by 5 basis points from a week ago. This 4.25% is a milestone of sorts.

The 10-year yield has now reached the highest point since July 25. What a three-month round trip! On July 25, longer-term yields began to speed up their decline as the bets on Fed rate cuts kept gaining momentum on less-than-hot labor market data and cooling inflation, and kept declining until the Fed actually cut by 50 basis points on September 18, at which moment, to the surprise of many, particularly in the home sales industry, longer-term yields headed higher, instead of dropping further.

And about two weeks after the rate cut, the series of large everything-up-revisions started arriving, one after the other, a stronger labor market and higher and rising inflation. And yields spiked (blue = effective federal funds rate which the Fed targets with its headline policy rate):

But short-term yields have continued to decline, pricing in at least one 25-basis point cut this year, but are unconvinced about a second 25-basis point cut. Mega-cuts are off the table. And they’re pricing in cuts next year, but more slowly than a couple of months ago.

The “yield curve” has continued the process of un-inverting amid the simultaneous rise of longer-term yields and decline in short-term yields.

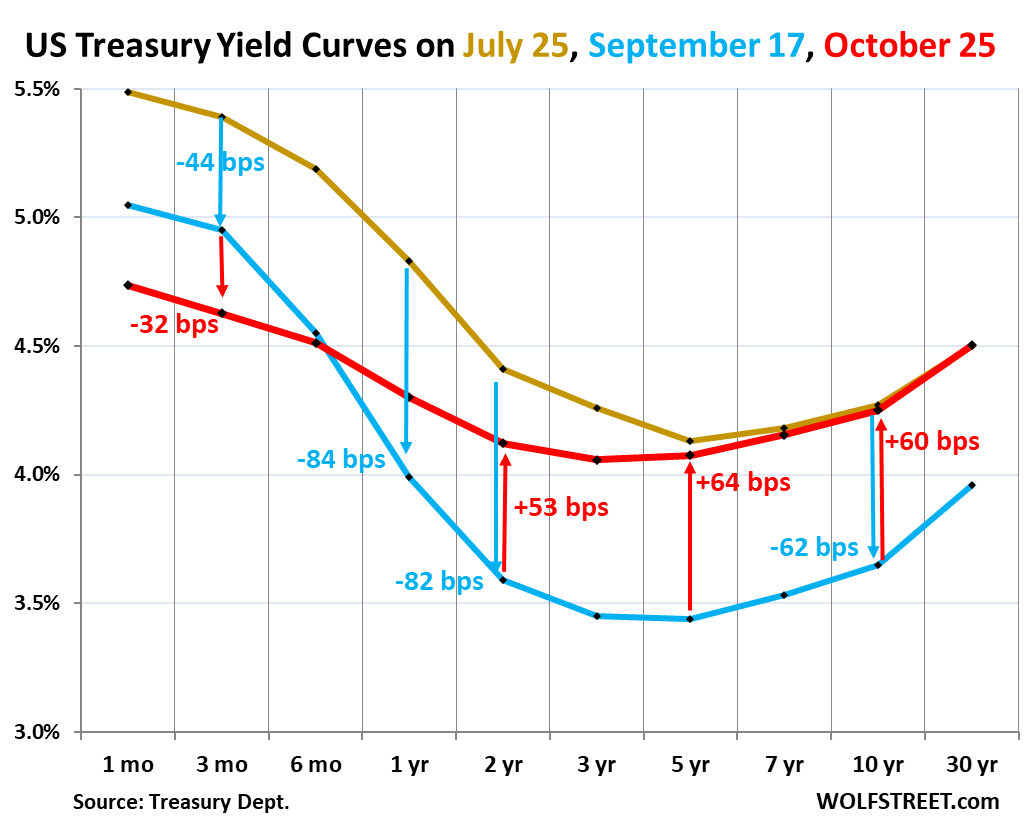

The normal condition of Treasury yields is that longer-term yields are higher than short-term yields. The yield curve is considered “inverted” when longer-term yields are below short-term yields, which started happening in July 2022 as the Fed rapidly hiked policy rates, pushing up short-term Treasury yields, while longer-term yields also rose but more slowly. The yield curve is now in the process of normalizing.

The chart below shows the “yield curve” with Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 25, 2024, before the labor market data went into a tailspin.

- Blue: September 17, 2024, the day before the Fed’s mega-rate cut.

- Red: Friday, October 25, 2024.

Yields from 7-year maturities on up are now (red) about where they’d been on July 25 (gold). This is the milestone.

And note by how far those yields have risen since the day before the rate cut (blue line). Everything from 3-years through 20-year yields has risen by 60 basis points or more. This was a big fast round trip, going down in two months, going back up the same distance in one month amid a lot of volatility in the Treasury market.

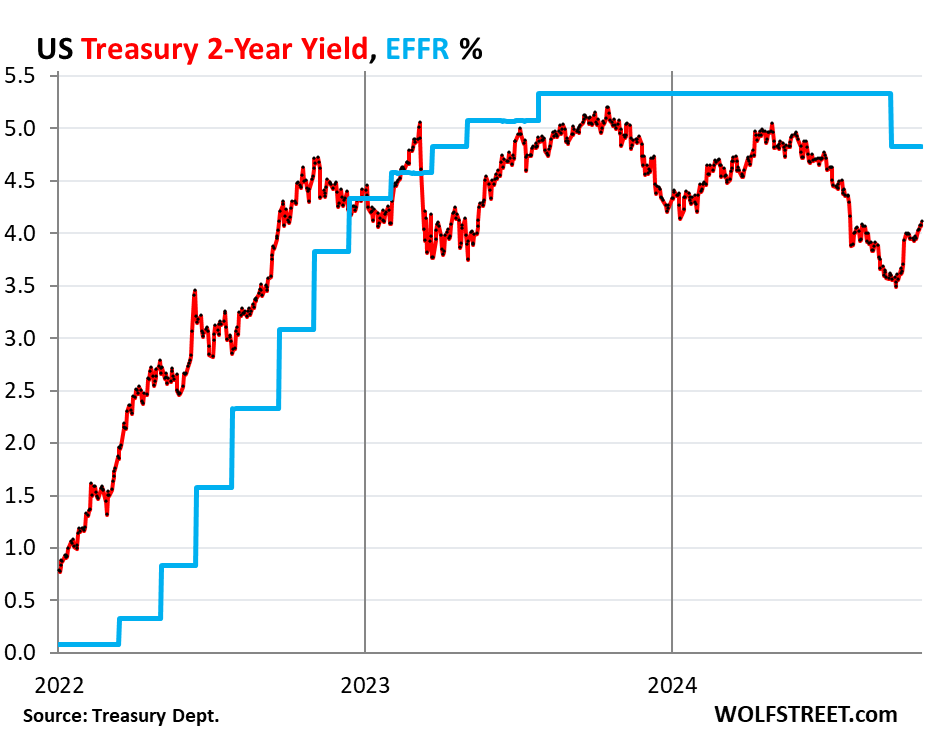

The two-year Treasury yield has been above 4% the entire week and on Friday closed at 4.11%, the highest since August 1. It has come up in part because the aggressive rate-cut expectations have been dialed back after the series of everything-up-revisions.

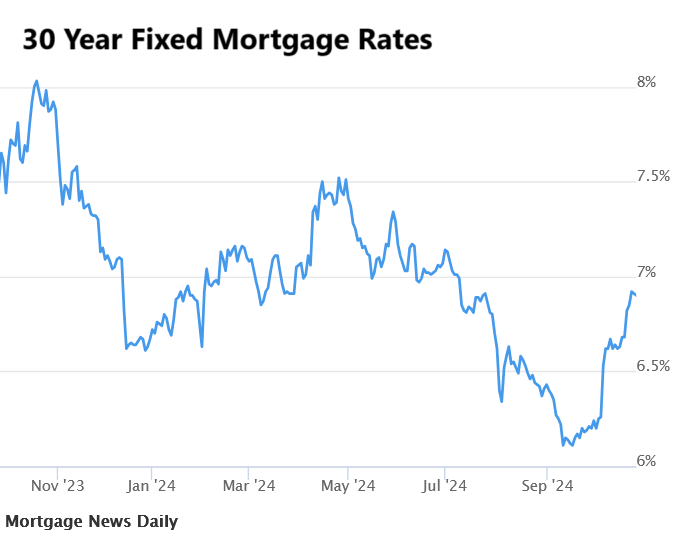

Mortgage rates, which roughly parallel the 10-year yield but higher, have spiked from the low-point just before the rate cut. The daily measure of Mortgage News Daily for the 30-year fixed rate mortgage has gone in a little over one month from the low of 6.11% on the eve of the rate cut to 6.90% now.

Mortgage rates in the decades before QE were normally above 6%, and for long periods above 7% to 8%, and there were years with much higher rates (chart via Mortgage News Daily).

For the real estate industry, this turn of events was very much unexpected. They promised buyers and sellers that mortgage rates, which had already plunged from near-8% a year ago to near-6% by mid-September without even a single rate cut, just on a wing and a prayer, would continue to plunge, and there was talk of 4% rates or whatever.

Despite the plunge in mortgage rates from the end of October 2023 through September 17, sales volume of existing homes wilted – because prices are too high. And over the past few weeks, sales volume has deteriorated further, as we can see from the drop in mortgage applications.

The problem with the housing market today – sales of existing homes in 2024 are on track to plunge to the lowest volume since 1995 – isn’t mortgage rates; they’re back to normal. It’s that home prices exploded, including by 50% or more in many markets in less than three years during the free-money era of the pandemic, in many cases on top of already precariously high prices.

These prices are too high, they’re not economically feasible, they don’t make sense. Seeing this, many buyers have gone on strike. But mortgage rates are now back in the normal range.

The drivers…

Longer-term yields, especially 10 years and longer, are driven by projections of inflation over the life of the security and by projections of supply of new Treasury securities to fund the huge deficits.

Inflation fears are big motivators. No investor wants to end up holding a Treasury security with 10-year left to run, and with a yield as purchased of 3.6%, when the average inflation rate over the life of the security is 4% or 5% or 6%.

A tsunami of supply of new Treasury securities is currently washing over the land every week to fund the deficits, and there is nothing to indicate that Congress and whoever is in the White House are even willing to have a serious conversation with the American people about this issue. So the debt has been ballooning recklessly, and bond investors aren’t seeing any relief on the horizon.

The Fed’s QT, a third factor that drives longer-term yields to some extent. The Fed switched to QT in 2022, after reckless rounds of trillions of dollars of QE, which had repressed longer-term yields and mortgage rates to record lows and had caused all kinds of mega-problems, including the crazy spike in home prices. By now, the Fed has shed nearly $2 trillion from its balance sheet. And QT continues despite rate cuts.

How much further can the 10-year yield go?

The 10-year yield has come up a lot, and fast, and our gut feeling is that it will run out of steam about right now.

If the next few inflation readings are benign, and the labor market data re-weakens, in that kind of scenario, the 10-year yield will likely back off.

But core CPI inflation has accelerated for the third month in a row on a month-to-month basis, and if it squiggles higher over the next few months, powered by continued strong demand and a solid labor market, the 10-year yield might try to climb up the steps some more, which would push mortgage rates back over 7%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What’s your take Wolf on T-bill and chill still or at 4.25%, good time to jump into some 10 year T notes? The delta is much smaller than before and if FED will once again cut before end of this year and then some more next year, current rates aren’t bad at all. Just curious, since I do have some Tbill near maturity end of Nov..and not quite sure I want to move it over to Index funds since the market is still pretty overvalue overall.

I’m not jumping into duration at this point. But some other people do. Which is what makes a market.

Keep an eye out for 10-year agencies. Some of them pay quite a bit higher than the 10y note and are effectively risk-free.

I have some FHLB bonds with a 5.75% coupon. 9 ish years left till maturity.

Some (many, actually) agency bonds are callable, including bonds issued by FHLB. So make sure to check. Callable bonds trade with a higher yield due to this feature.

Indeed. I had some 5.98% Fed Farm bonds called earlier this year.

I’m surprised my FHLB bonds haven’t been called yet tbh.

Hahahaha my FHLB bonds got called this morning.

Sorry to hear.

Some commenters here have been through this with their CDs. You’re not alone! I hate callable bonds. But you had a good run while it lasted.

Just bought 90 day bank CD at 4.55% in a Roth. Why risk 10 years when you can run a ladder of short CD’s for a greater return?

On the positive side at least there aren’t any major world events that will drive up spending, but I suppose one could argue that even significant deficit spending is a good economic catalyst. No chickens returning to the roost for the time being.

I hate to say it but you are right. The markets do not seem to be as worried about it as I am.

I know Wolf doesnt like too much political stuff so I will just say that how we vote on Nov 5 seems like it will have deeper consequences than the last few elections.

How do you figure? Both political parties are in favor of warmongering. It doesn’t make much of a difference which one you choose if you are antiwar, as there is no party for you.

Conquer and pillage, always good….juicy steak afterwords.

No one’s in the mood for a war, we can just spend our way to forever, watch the faces of the poor people as they chew their dog food.

Does a new world war drive up military spending or do nukes “level the field” and consumers, with those surviving needing clean water and low radiation eggs?

Persp – mebbe reexamine the Soviet-era quote that lead to The Grateful Dead’s choice of moniker…

may we all find a better day.

The Fed probably jumped the gun on rate reductions. I’m not seeing all the expertise of the “experts”.

In the future, if there’s a look back in the history book and people want to wax poetry on Pow Pow’s legacy and the great job he did…etc. They need to make sure not to leave this part out and put it front and center…the amount of damage it has done to future generation…pricing out millions from homeownership. Under no circumstances is this kind of home price growth is consider normal or healthy despite people that already got theirs before this boom or NAR/RE would like to tell you.

” It’s that home prices exploded, including by 50% or more in many markets in less than three years during the free-money era of the pandemic, in many cases on top of already precariously high prices”

And all idiot buyers from the North East coast continue to buy in South Florida.

Following in their parents footsteps!

Maybe of interest to people here: the Florida comments keep reminding me of this paper from last December where they did anonymous interviews with 76 members of various levels of government involved in South Florida, regarding climate change and the viability of the real estate market there. Most of them said that people are going to have to move and that they aren’t prepared for it because everyone currently has an interest in ignoring the problem to preserve property values and such.

There was one quote from a member of the Federal government regarding the financial situation there that was interesting:

“I think that the potential to have a financial collapse driven by the impacts to the coastal real estate market and how that could cascade to the mortgage industry, that is so scary for folks that it’s hard to talk about. The finance conversation is starting and the new administration is trying to spur that conversation. You see that in executive orders, right? You see that in conversations that are now being had in the financial sector. I think there’s a growing recognition of these issues amongst the reinsurers we’re sort of first, but now insurers are also concerned, and lenders are starting to be concerned. There’s a lot of talk about disclosure, right? I think we’re starting to have the finance conversation, but it’s probably not, I don’t know that that’s happening at the regional level, although we can be sure that financial interests are thinking about South Florida and the implications of that. Players like Fannie and Freddie are also looking at the risk to their portfolios and their mortgages and what that could mean for low income owners and those sorts of issues. There’s more and more happening on the finance realm, but I feel like we’ve been slow to get there.”

https://doi.org/10.1093/oxfclm/kgad015

Everywhere in FL Joe, not just South part…

Our hood has seen prices for same place go from around $100/SF to $400, and that’s for the old and older ”tearer downer” types that have been torn down and replaced by usually much larger houses selling rapidly for $500/SF and up.

Our little hood had no flooding, but huge old trees did come down, many still do not have internet three weeks after milty…

Not just Powell, but it goes back to Yellen and Bernanke keeping ZIRP way too long. Rates should have started to back up by 2012.

Agree, if we want to go back just a little further I would pin it to Greenspan for starting us down this road. That guy did more damage than most people realized and I really hope they don’t look at that vulture look a like fondly in the history book.

Phoenix,

From 1968 to 1998, 10 yr Treasuries rarely (if ever) went lower than 5.5%.

From 2011 to 2022, 10 yr Treasuries spent 99% of the time *below* 3% (close enough to half of the 68-98 era, considering just how long T rates really were for how long).

*And* that 2011-2022 period saw massively higher Federal Debt – to – US GDP ratios (making the Feds a much worse risk – despite paying much lower T rates…thanks to Fed money printing).

The T rate history is available, fascinating, and ugly as hell.

It is the daily/annual record of a nation/economy in corrupt decline.

i wouldn’t even use their terminology. “price growth” is only said by real estate shills who want to pretend that it’s a good thing. say price inflation.

by the same ”token” FG,,, price inflation is just another cover up for the reality of currency degradation that is SO obviously happening,,,

the meme that USD is the ”cleanest dirty shirt” while mostly true,,, does NOT excuse the massive degradation of our savings in US dollars, in spite of the equally massive propaganda trying to convince us otherwise…

SHAME on our PUPPETs, AKA political panderers,,

This is a nail bitter in terms of where 10Y goes, it’s recent accent above 4% was unexpected, but that’s what makes markets fun. The main attraction I’m curious about, is the fairly recent resurgence of inflation that’s been kept alive by resilient growth, which is a nonstop narrative which has killed recession narratives for almost three years,

Hence, if we’re certainly not going into a recession and growth is strong, and we just had a monster rate cut and an exploding ongoing non-ending deficit expansion, with massive upward revisions, then there’s a decent chance that a rising 10Y with a rising term premium is a trend that doesn’t just suddenly exhaust itself.

I’m rooting for it and pounding my cane with great force and enthusiasm!

From Trowprice, a few days ago:

“ Breakeven inflation rates1 are the best measure of market‑implied inflation forecasts. On September 20, the day after the Fed’s rate cut, 10‑year inflation breakevens jumped around seven to eight basis points2 higher, likely in response to the size of the rate cut. After the previous two inflation breakeven moves of that magnitude, the nominal3 10‑year Treasury yield increased by about 100 basis points within three months. This pattern indicates that inflation expectations could likely contribute to a higher 10‑year term premium over the next few months.”

“ Dollar emerged as the unequivocal winner in the currency markets last week. Both Dollar Index and 10-year US Treasury Yield surged through their respect technically significant 55 W EMA resistance.”

“ The dollar has also benefited from a rise in market expectations for a victory next month by Republican candidate and former U.S. President Donald Trump, which would likely bring about inflationary policies such as tariffs.”

I was shocked to recall that the 10y had fallen to the 1.5% area in August 2019 — primarily because of tariff shock:

“ The yield on the benchmark 10-year Treasury note fell to its lowest level since 2016 on Thursday after President Donald Trump announced new tariffs on Chinese goods.”

I am not sure if I understood….why should tariff related inflation reduce bond yields? Should they not result in higher yields?

Yes, they should. It’s also unclear how increased likelihood of Trump bringing inflationary policies into office is good for the dollar. There were multiple aspects of that quote that didn’t make sense to me.

Aman,

As I was looking at break even stuff at Fred, I saw a very weird trend anomaly and then searched news to see what was going on August 2019 — and it was tariff shocks.

I included that, but failed to put into perspective how YUGE new tariffs next year will likely upset the yield apple cart, the Dollar apple cart and world stability — not there’s a great deal of stability now, but more like chaos ahead.

I guess that’s part of maga, to disrupt functionality — but maybe that’s six months away.

In that light, one has to look at the potential gift of higher 10Y yields within the next several months and then ponder how that plays out long term — and obviously that’s very confusing and potentially risky.

Grabbing the 10Y on its way a bit higher, may be a reasonable idea, if we’re headed for substantially lower yields during another MAGA episode — but locking up funds for 10 years with anticipated tariff and tax cut inflation doesn’t seem productive.

I kinda think there’s a chance we go back to the 2019 great days that everybody wants to relive, with low rates and a fight to take the Fed rate to zero — and crash the dollar.

As I recall, that was an incredibly awful time to have cash or treasuries — but apparently, as corporate earnings yields are headed lower— stocks will make everyone happy (if we collectively ignore truthful valuations).

I can’t help ranting after I drink my mocha…

Oh yah, yah gotta thing about the high end of R* which is maybe 3.5% as some ghost-like neutral rate cap — which probably makes my 5% 10T Dream sketchy — but the deficit may still play a starring role in the perception of how far the banana republic stupidity can be extended.

Even the break even rates top out at 3%. All in all, even with pandemic, the dollar hasn’t swung significantly since 2016 and treasury rates have gone up since being zero — so maybe even with a political shift, there’s probably an insignificant middle ground that will evolve?

My hope is for the 10Y going above 5% and crushing exuberance — but I’m starting to doubt that’ll happen — I think we’ll end up going into hyper-exuberance and entirely detach from any hint of reality — which ironically may be an excellent case for buying a cheaply priced 10Y — lol.

The 2016 level was achieved by a 2-year tight money policy beginning January 2014. I count that as the end of the long-standing bull market in bonds.

“I count that as the end of the long-standing bull market in bonds.”

Not the end of 2020 when the 10-year hit half a %?

The yields inversion was the #1, cited by many, reason for incoming recession. I guess at this point we can say that this rule of thumb is not solid…

Another cited reason for a doom was Buffet going cash, a long time ago. Since then the market has gone up by >20%?

Then Buffet selling Apple many months ago, losing a lot of upside. Both flops, if applied to a normal investor.

How to live without the thumbs and gurus? /s

It is the un-inversion, not the inversion of the yield curve that historically predates/predicts recessions. And there is typically a lag of some months. So a recession in early 2025 would qualify.

Personally, I think monetary and fiscal policy may pump liquidity to try to delay it further.

100%, the 10 year vs the 3 month 👍🏻

John Daniels,

And if there is no recession by Q2 2025, will this endless recession mongering here finally stop??

MaddieB,

Here is your “pump liquidity” by monetary policy (BTW, fiscal policy doesn’t “pump liquidity,” it spends money in the economy, which creates demand not liquidity, and this demand is inflationary)

A bear steepener?

I mean the longest time between inversion and recession was 1966 and it took around 37 months. That would put us at September 2025.

Granted we were still on the gold standard then.

I’m not betting on a recession but I do think about that. If it’s not here (or spooky) September I’ll just move on with my life.

Even if we hit recession Sept 2025 how one can “prove” that related to yields? How about idea that inversion prevents recession? It is just all too random / limited sampling to make a rule.

I’m not trying to “prove” anything.

I just care about a slow burn where zombie companies have an opportunity to amend the errs of their ways and SOME asset price stability that meets rising wages within the next five years.

Wages as percentage of mortgage payment have me concerned. Every indicator I watch tells me housing is still wayyyyy too hot. PE valuations are the same.

I certainly hope they can pull off all this chicanery and nothing breaks.

Recessions are a thing of the past thanks to gov’t spending. Without it we would have probably bad in 2023 and be outta this mess by now

There are three conditions that always happen prior to recession, One is peaking of interest rates, the second is the falling of rates from the peak, and the third is the inversion and then subsequent un-inversion of the yield curve. There has never been an example of those three things happening without a corresponding recession, and we have now had all three occur.

This is not my opinion. It is a fact which can be verified by looking at the FRED’s own charts. If you doubt it, just look for yourself.

Yawn. I’ll keep buying NVDA enjoy your chart astrology

I think that the key here is the reason for the falling of the rates. If because of inflation down then no recession. If because of a major drop in employment and profits then recession. All sorted now :)

It is not astrology, it is history, and those who forget it, are doomed to repeat it….

Yawn. I’ll keep buying TLT puts. Enjoy being unable to make >1000% ROI on your NVDA shares.

I own NVDA so I love this optimism. I’m riding the wave too. But it makes me nervous. I see this going the way of tesla – so it’s ride the hype but just know when to get out. I have to wonder why more companies aren’t using google tensor chips like apple? From what I can tell they’re faster and cheaper.

Recessions generally occur when the economy is overheated – i.e., everything is great, no one is expecting a recession.

If everyone is expecting a recession, they will act with caution, and a recession will not occur.

That’s exactly how recessions occur because people stop spending when they’re cautious

Past performance does not guarantee future results.

Economists have successfully predicted nine of the last five recessions. Clearly you have a background in econ.

They are in Florida enjoying the sun, drinking a cool swamp monster slush.

Nothing wrong with them spending their money in Florida…or Arizona where I live.

It’s government spending that is the killer, not the old turds in Florida.

Yields will go higher due to several forces. I fully expect to see the 10-year yielding 4.5% before too much longer.

Agree. And mortgage rates will be near, if not above, 8% by mid 2025. Yellen is funding the govt primarily with ST paper, she needs lower ST rates for that to work. Powell is accommodating. But Powell needs to counterbalance the inflationary effect of lower ST rates and out of control govt spending. Enter higher LT rates, which dampen down demand for mortgages, HELOCs, auto loans, expensive big ticket consumer discretionary, etc.

And there is the specter of bond traders waking up from a 40 year nap.

Agree with you both.

I think the Fed wants to uninvert the yield curve because the bond market is more liquid when volitility is low. Sinc the Fed started hiking rates in 2022, the MOVE index has been significantly elevated.

QT = letting the market digest new debt, ergo long term rates rise. A rate cut or two = bringing policy rates down below rates on duration.

Thanks Wolfe.

—-

The 10-year yield has come up a lot, and fast, and our gut feeling is that it will run out of steam about right now.

If the next few inflation readings are benign, and the labor market data re-weakens, in that kind of scenario, the 10-year yield will likely back off.

——

FED can also influence by aggressively reducing the rates. I understand 10 year yield went up even FED cut 50BP. But as some FOMC members cautioned against aggressive cuts, Market has dialed down future rate cut mania. If FED becomes dovish, it will surely bring down 10 yr yield. As of now QE is very very distant possibility but FED can slow down or stop QT if new President forces them. We can see in Refunding Announcements that slowing QT helped US Treasuries to borrow less from Market.

Lorie Logan told us ON RRP will become nearly zero. It will become eventually but as of now that drop has slowed down a lot from May. If they were dead serious about QT, they should NOT have slowed QT and wait until ON RRP are near zero. Some movement in ON RRP this month but still some distance to go before becoming nearly zero.

re: “As of now QE is very very distant possibility”

The markets can’t digest 1 trillion in debt every 100 days.

Nonsense. The market is “digesting” them just fine, which is why longer-term yields are still so low because there’s huge demand for this stuff.

If the market had indigestion, longer term yields would be 10%.

This silly QE-mongering gets old.

Some mixed up stuff in there (starting with my name).

In terms of your ON RRP comment, here are ON RRPs, they’re already down by over 90%, not much left, just $227 billion, compared to $3.2 trillion in reserves:

Wolf,

I recently read the theory that the RRP won’t go to exactly zero. The speculation was that some MMFs aren’t setup to lend in certain private repo mkts with higher yields, so they still lend cash to the Fed instead.

In that context, very low RRP balances (<$500B?) could be considered effectively drained in the context of capital flows.

BS no?

The common lingo is “zero or near-zero” and the Fed speakers use that phrase or something similar. And it doesn’t matter whether it’s zero or $156 or a few billion $. If you look at the balances in the past, small amounts (that you now cannot see because the scale has gotten so large) come and go all the time, interrupted by periods of actually zero balances. But $500 billion is not “near zero.” Even $200 billion is not “effectively drained.” When it gets down to $10 billion or $20 billion or so, I would consider it effectively drained.

Thanks for clarifying, Wolf. I hadn’t noticed the “near-zero” part of the lingo.

McService Job Nation was created with endless Fed Puts, Wealth Effects and Wall Street Bailouts.

The US stock market for some reason reminds me of the Japanese stock market during the 1990’s…hope we don’t repeat their lost decades.

The Japanese stock crash had a lot to do with a quirk of financial engineering. Companies were able to book unrealized gains on real estate as profit (GAAP doesn’t allow this in the US).

As a result Japanese companies used the “profits” from sharply rising real estate prices to buy more real estate at even higher prices.

This worked wonderfully for a few years. Then it stopped working in spectacular fashion. Guess what happens when you get to start booking losses on unrealized gains when the real estate goes down? The highly-leveraged bubble deflated rapidly.

Leverage and bubbles work together like hand and glove.

Do you think it had anything to do with the uneven playing field in the country? Our tax system is absurd.

Elon Musk is the wealthiest person in America and has come from nowhere to that position in the last 15 – 20 years. Yet it is likely that most auto workers, teamsters, electricians, and carpenters have paid more in federal tax than he has over that time.

Didn’t Musk have to pay tens of billions in Federal tax when he sold Tesla stock to buy Twitter?

JimL,

That’s nonsense. The guy paid astronomical taxes when he’s sold stocks.

The Fed includes tariffs in inflation measurements and certainly it’s very possible that Trump will win, so I wonder what happens about that.

As in, you wouldn’t include additional taxes on income in inflation measurements, but they are when fixed to prices. Which would mean that the Fed will have to abandon the rate cuts you would imagine.

Tariffs. Perspective here.

Trump will barely enact any tariffs. He’ll use the threat ersatz negotiating points, and announce that he’s made great trade deals that obviate the need for tariffs. Basically, it’s another “…and Mexico will pay for it” thing. Anyone pricing in higher inflation for that reason is going to be….sad.

You seem to be engaging in the long time history of Trump supporters attempting to normalize his behavior.

While I agree that it is impossible to know what exactly Trump will do, he promises one thing today and the opposite tomorrow, it should be noted that even if he doesn’t completely enact his promised tariffs (he does them “barely” as you try to waive them away), he has already initiated/raised tariffs more than anyone other president in 40+ years when he was in office.

Furthermore, it is quite clear he is looking to cut taxes drastically, that lost revenue will either drive up the deficit or have to be made up elsewhere. Tariffs are the only place he has mentioned so far.

And I guess he will take over the Fed to start QE and enrich himself. Inflation follows, for that reason at least.

If prices were indeed too high, then builders could build with higher margins.

Their margins are still very high, just down a little from the greed phase in 2021 and 2022. They cut their margins a little to make deals that take market share from sellers of existing homes. You can see that because sales of existing homes have collapsed while sales of the now very competitive new homes are very solid.

It’s mostly due to inflation expectations, and somewhat due to oversupply. I doubt QT is a factor – https://fred.stlouisfed.org/series/TREAS10Y

By supporting your statement with the link you posted, you show that you’re utterly clueless about QT and the Treasuries the Fed holds.

Your link says that $1.5 trillion in Treasuries mature in 10 years or later. But the Fed holds $4.4 trillion in Treasuries now. Even under the old roll-off cap of $60 billion a month, more matured every month than the cap, and the Treasury QT was $60 billion every month. And now under the new cap of $25 billion a month, a lot more Treasuries mature every month than the new cap, and the Treasury QT is $25 billion every month. The Treasury QT will run at the maximum allowed by the cap until the Fed decides to end it which will be long before the Treasury holdings go down to $1.5 trillion. All you have to do is look at the maturity schedule to see the pile that is maturing at mid-month and at the end of the month. Or you can save yourself the trouble and just read my balance sheet articles:

https://wolfstreet.com/2024/10/03/fed-balance-sheet-qt-66-billion-in-sept-1-92-trillion-from-peak-to-7-05-trillion-back-to-may-2020-below-7-trillion-in-1-2-months/

Please, bear with me. I may not understand this as well as you do, but I understand just fine how well QT has progressed so far and how well it’s ongoing. I’m not one of those QT-deniers.

I just meant to say, on a net basis QT seems to be happening in shorter duration Treasuries while the holdings of longer duration Treasuries are … changing in a way inconsistent with the rise in bond yields.

No, that’s not how it works. QT happens when securities mature. So a 30-year bond matures and comes off the balance sheet, and that’s QT. And there are lots of these bonds issued a long time ago that the Fed bought in the market in 2020-2022 with only a few years left to run at the time, and those are coming off now during QT, and they will continue to do so.

What the Fed has been doing every month: it replaced the maturing securities that are in excess of the cap with new securities of the same maturity.

So under the new cap of $25 billion a month, if a $10 billion issue of 30-year bonds matures, along with a $10 billion issue of 10-year notes, along with a $10 billion issue of 5-year notes, so a total of $30 billion matures in one month, then $25 billion will mature without replacement and come off the balance sheet, and that’s QT. The remaining $5 billion will be replaced with securities of the same maturities. So at the next auctions, the Fed will buy $1.7 billion of each, 30-year, 10-year, and 5-year securities. So now $30 billion in old securities are off the balance sheet, and $5 billion in new securities are on the balance sheet, and those $1.7 billion in newly issued 30-year bonds and $1.7 billion of newly issued 10-year notes are added to the total of “matures in 10 years or more.” That’s why that total has been stable.

The Fed has said that it will change this method of replacement like-for-like by shifting to a system where it will replace maturing longer-term securities with T-bills, at least to a large extent, thereby no longer adding longer-term maturities, but replacing what comes off in excess of the cap with T-bills. The Fed has only $195 billion in T-bills. Before 2008, the Fed’s Treasury holdings were mostly T-bills. That will address the issue of the remaining securities being all longer-term. Logan explained that again, and that’s a sign that the FOMC will start discussing this officially, and we’ll see it crop up in the minutes over the next few months.

Thanks for that explanation. I think I understand the mistake I was making. A Treasury that was issued a long time ago and now close to maturing, already got off that chart ten years ago. So it’s not “removed” now when it matures. But its replacement (minus the cap) that the Fed now buys is “added” to that chart. This is the asymmetry which makes that chart useless in understanding QT, right?

Correct.

Ah Mr.Bridger…if you’re still under the illusion that the Republicans are fiscally conservative, I have a lot of bridges that I can sell you…LOL

As usual, good talking points Wolf! I’d say we keep the politicians out of the monetary policies and leave it to the bankers at the Federal Reserve.

When the politicians run their mouths they foul up the free market!

@Slick. The free market is only in theory.

For a market to operate freely, it needs a number of players on both sides to create a balance of power.

The Fed is a unilateral agency that operates at the behest of banksters and oligarchs with no concern for average citizens.

In our corporate market, endless and unchecked consolidation of companies have resulted in a handful of companies holding all the power. Though (with branding), the companies make it appear that the markets are competitive.

So free markets hardly exist. The government typically (typically left-wing) has had its hands tied when it comes to antitrust because there is a right-wing chorus against “regulation” and for “allowing free markets to operate”.

This has been to the benefit of corporations, oligarchs, and the 1%-ers and the detriment of average citizens.

The United States started out as a republic, a rule of law, a limited government. I don’t know what the answer is but it definitely seems like both sides are getting more extreme.

I agree about the corporate consolidation, here’s a great picture that shows just how much consolidation is happening.

https://nutritionstudies.org/wp-content/uploads/2022/11/consolidation-in-the-food-system-graph2.jpg

A great kids movie shows this in extreme, is called Wall-E

Both sides?

In my mind, the consolidations make sense, and periodically get dismantled by force, fall, or farce.

Billions in profits can’t sit idle, so a guy like Gates has to put it somewhere other than software. He’s already tapped out in that market.

So he does, and makes more money that also has to be put to work, but now his cycle is larger than before.

Productive money buys productive assets. I suppose they could just “give the excess away” but guess what? They don’t! Neither do their competitors or any of us.

The system can’t stay closed, it must grow. so inflation of money supply creates all the extra cash flowing around while simultaneously debasing its purchasing power for the common man.

They’re structured for growth. So grow they must. No matter what. Sure greed is a factor, but it’s not the only one.

The “common man” as I define him, exists paycheck to paycheck supplementing his lifestyle with credit card debt. All he sees is their greed.

He cannot understand both Buffet and the homeless man have money problems. One has none, the other has to keep it moving or it’s destroyed by taxes and inflation.

Yes, I understand this isn’t truly accurate. It’s an attempt to help think outside a locked bias box. It’s complicated, and working people are easily influenced.

No matter how many times Wolf calmly explains the Fed, most commentators keep seeing it the same as they did before.

That about sums it up @seanshasta !

I would bet a lot of money you could not define a “free market” if your life was on the line.

I fine most people who advocate for free markets are people who have the least understanding of them.

In reality there is absolutely no such thing as a free market. Once you introduce the most basic anti-fraud law it isn’t a free market. Almost every single law inhibiting free markets are some sort of anti-fraud law.

The closest we can get to a free market is the dark web (which is a sewer filled with con artists and such), and even that market there are costs to avoiding government interference through anti-fraud laws.

there’s a big difference between regulation designed to protect against theft and regulation designed to fix prices.

in the final analysis, most of what central bankers do, outside of regulation of member banks, is designed to distort the free market price of capital.

The other night I drove my buddy home from the bar and he gave me a few bucks for gas.

People do free markets all the time – most of us just aren’t thinking about it.

In regards to mortgage rates, how long until there is fallout in the RE industry from the lack of sales?

I can’t imagine a commission based industry can sustain itself with nothing selling. Do RE agents start telling people to lower their price? I know everyone claims they’d never sell their low rate house but sometimes you don’t have a choice. Return to office, job loss, divorce, need more space, retirement are all things that you can’t just put off.

This isn’t the first time the real estate market has been in an ‘ebb’ phase that has lasted. It will eventually flow again and of course likely just be normalizing that a 3% 30 Year mortgage isn’t in the near term cards. I only know a real estate agents and they either got into it in retirement as more a hobby and are fine with pension, or did it successfully for a long time and own multiple properties and income from those sources. Fortunately a lot of employment opportunities to fill in the gaps. At least in California we have massive substitute and other teachers shortages so can make $260 a day and down in LA

make $35/hour. That is double what I made back in 2013 where it marginally wasn’t worth it but helped offset the outflow while I found a permanent position back in IT. Obviously those anecdotes aren’t representative but they are also buckets as well. Unclear how the larger real estate companies are doing but guessing they are built for ebb and flow.

“At least in California we have massive substitute and other teachers shortages so can make $260 a day”

LMAO. Imagine trying to live off $1,300 a week gross with median house prices of $900k.

It’s easy….you just need a dozen or so people living in the same 1.300 sq. ft. house earning that money.

I live in the Coachella Valley, and here the price of middle class homes and rental rates has doubled in the past 4 years. No person in the lower 50% of earners can remotely afford what they took for granted just 4 years ago. Of course, the price of groceries and energy haven’t helped either. No wonder there is a lot of discontent with voters.

Depth….

You don’t buy a median house on that income.

Gattopardo – tell me something I don’t already know…

Renter,

“I can’t imagine a commission based industry can sustain itself with nothing selling”

Nothing? Sales are down, what, 30% from peak? 70% od previous peak sales still sounds like a decent number to me. Definitely not “nothing”. Now factor in that of the 70% that are selling, those values are at least 50% higher than a few years ago, so the commission income in total isn’t down THAT much. What this probably means is income is more concentrated among a small # of agents/brokers.

38% from 2021. 29% from 2019. Pretty terrible numbers when you consider existing homes for sale is much higher than 2021 and close to the same level for 2019. And these numbers are before rates went back up last month. So expect the next data set to be worst.

-38% is still very far from nothing. Prices are up close to that much, so again, the total commissions income isn’t down much.

Also a flexible work force. Many are licensed but in a “deadpool” that comes on line when sales volume is way up.

Correct Gatto…

Long term agents that have invested wisely in real estate are fine. These are the agents maintaining their share of current sales volume. It’s called “Real” Estate” for a reason. Which is why monetarily successful folks own a lot of it.

If real estate crashed 90%, buying a home will be the least of anyone’s worries.

Factoid:

Next to no one is going to abandon their 3% 30 year fixed rate mortgage with rents at the current level.

I recently bought a house (in January in Las Vegas). We used a real estate agent (best money ever spent for a multitude of reasons, but that is a different discussion). The real estate agent was really good. Worked hard and tirelessly as we were a very picky buyer thay he had to work extra for.

Anyway, we still keep it touch. Recently we heard from him. He worked on an office that at it’s peak had almost 40 agents. A few were part time, but most were full time. They are down to 15 agents. All but one are full time (the one part timer he wouldn’t really consider a real estate agent, it is more of a hobby). The 15 left are generally the hardest workers.

Combine the slowdown in sales with the recent fallout from the lawsuit and it has gotten way harder to make money in real estate. Everyone is making far less money. The best are still making a decent wage, but nothing like it was before.

He is still holding out because it is a good fit for him. He enjoys what he does, but he admitted that it is getting close to the point where he can probably make more money elsewhere. Not quite, but close.

that’s always been the problem with the real estate agent industry. very few barriers to entry combined with a lot of people who are just greedy and want a commission for the least work possible.

during the bubble days of 2021 and 2022, a $1 million house could be listed on tuesday and be under contract by thursday. there’s nothing you could say that would convince me that the two realtors involved did $60k worth of work.

now there are much fewer, they are selling less, and there is more pressure on commissions. it’s a different story now.

“there’s nothing you could say that would convince me that the two realtors involved did $60k worth of work”

You should have tried being an agent in 2009-2012. Cash flowing homes far below replacement value couldn’t be sold to a Buyer with a shotgun to his head.

But it’s all the agents’ fault. It has nothing to do with greedy sellers and FOMO buyers.

First thing I learned in real estate:

Buyers are liars and sellers are worse.

after a decade in the business I extended that to include:

Trust another agent and get yourself a curse.

10% of the real estate agents sell 90% of the properties. Experienced agents most definitely advise their seller clients to price their homes to sell. They use local data which is timely and persuasive. While 2024 may be historic in the lower number of closed transactions; 4,000,000 closed sales = 456 houses sold eveery hour of the day = 10,958 houses sold per day. Our industry NEEDS to reduce the number of practioners who work part time or as a hobby so that clients ALL received the professional service only experienced veterans can deliver.

Wolf,

If the Fed replaces long duration treasuries with T-bills, what do you think the net effect will be on rates on longer duration Treasuries?

Do we have a good way of estimating how rates would be different if the Fed had never bought long duration Treasuries and had continued in their tradition of buying T-bills?

Great questions. I’ll address just one of them. Just a gut feeling that this type of reverse Operation Twist will elevate long-term yields. But it could be very disruptive if done too fast — both on the long end and at the T-bill end. That’s a lot of T-bills the Fed would have to put on its balance sheet. But the government has been increasing the amount of T-bills outstanding, and that would make the T-bill end easier for the Fed.

Logan said that this whole thing would be complex and would require a lot of thinking. So that tells me that they’re not going to be brutal. They’re going to do this carefully. They’re going to try to not blow up the Treasury market with this.

I’m also convinced they’re discussing the technical aspects of this issue with Treasury, which might be one of the reasons why Treasury is now issuing a lot more T-bills so that there will be enough T-bills outstanding so that the Fed can buy a few trillion $ in T-bills over time to replace a few trillion $ of long-dated bonds.

The problem is that the amounts involved in the Fed’s portfolio are so huge. If the Fed today replaced all its Treasuries with T-bills, it would hold about 67% of all T-bills outstanding.

When the Treasury says it is going to issue T-Bills instead of longer term bonds, are they talking about for all or even a majority of debt issuance, or are they talking about just a portion?

I’m trying to think through the implications of this. If they drastically reduce long term bond issuance, then wouldn’t the supply dry up, and excess demand would put downward pressure on rates?

But, can you imagine the quantity of short-term T-bills being issued every month in just a few years time? Not only would they have to issue for the new deficit spending for that period, but they would be issuing many times that amount to refinance existing debt.

Unless the Fed is willing to step in and buy all unsubsubscribed bills, couldn’t it cause short term rates to disconnect from the Federal Funds Rate? And if they do buy all supply in excess of market demand, doesn’t that put pressure on the dollar, and indirectly increase inflation?

It just seems like this plan invites the potential for severe risk of instability in financial markets.

It seems like it might be better to go out to a duration period at which they would not really be competing directly against private capital needs, like 100 year bonds.

Right now, $6 trillion of the $27.7 trillion in publicly traded debt are T-bills. That’s 22%, which is relatively high.

The government issues a lot of debt in all maturities. But the proportion of T-bills has increased with regards to notes and bonds.

And yes, you’re correct about the future size of the T-bill auctions. they’re already huge, and they will get huger. But it’s a well-oiled machine that’s running pretty well, much of it automated, such as auto-rollovers.

If the Fed starts buying lots of T-bills to replace maturing longer-term debt, there are now plenty of T-bills out there to get that started. But over the years, Treasury will likely issue more T-bills if the Fed starts buying them. So I doubt we’ll see a big disconnect in terms of rates.

It seems that the FOMC 50 basis point rate decrease (Treasury Bills short term maturity) may have been to help out the US Treasury’s interest expense.

I think this paper attempts to answer some of your questions.

https://www.kansascityfed.org/research/economic-bulletin/considerations-for-the-longer-run-maturity-composition-of-the-federal-reserves-treasury-portfolio/

Chart 2 shows that buying long duration treasuries vs T-bills reduced rates by 1 to 1.5%.

My take from that article is that long term rates are going back to at least pre 2008 levels and staying there once this replacement of long duration with T bills happens.

But as Wolfe kindly replied to me on the article preceding this one, that is going to be a very slow gradual process over many years, they are not actively going to sell their long duration bonds like the Bank of England are doing. I guess the impact will be more immediate though as one buyer for long duration treasuries will disappear once this new policy gets implemented.

What this does to the pricing of other assets like house prices and the stock market that seem to think we are about to see reduced rates to justify their excess valuations remains to be seen.

I’m Canadian invested in USA stock. I see an interesting play being exposed to both economies. For instance at this stage it seems to me that Canada is on a path of low growth, low inflation. USA quite opposite. Now, the USA inflation should have 66%? positive impact on stock prices. But living in Canada with limited inflation makes the both of the two worlds.

There are similar plays regarding currencies. The bigger mess in the world, the higher US dollar, pushing the investments in CAD up.

Too bad I cannot edit my posts. So many grammar errors. I just see them right after posting…

“Too bad I cannot edit my posts. So many grammar errors. I just see them right after posting…”

Ditto

…the ghost of Prof. ‘iggins walks forever among us…

may we all find a better day.

The last time I checked, every major currency was down when priced against gold. I can’t remember another time when every major currency was down at the same time. Gold has not become more valuable, the major currencies have become less valuable. In other words, there was a coordinated effort between the central banks to debase their respective currencies.

No. That just tells you how out of line the price of gold is priced in every currency and should give you a clue as to how far it has to fall from its manic unsupportable speculative highs now.

Meth for dinner again, huh?

Both can be true.

Gold’s price rise could be from a mix of inflation / sovereign debt fears (gold as USD CDS) and

FOMO buying behavior / excess liquidity chasing assets.

NB: I own a little gold, but don’t like holding a lot of non-yielding assets in an inflationary environment.

“In other words, there was a coordinated effort between the central banks to debase their respective currencies.”

Right. And look at the net worths of the people in charge who made those decisions – they have skyrocketed way beyond the pace of inflation. Coincidence? I think not….

“In other words, there was a coordinated effort between the central banks to debase their respective currencies.”

Wow. Where are you getting all this wealth of knowledge?

One day we will see a Hollywood action movie about it?

The curious thing about a 10y treasury, is pondering holing to maturity.

With AI and ongoing hyper expansion of financial innovation, including the realms of crypto and MMT — there’s an increasingly wide divide between a 10Y fixed rate and the deposit liquidity of an SVB deposit rate at a bank — I’m referring to the speed of transfer, between a digital deposit versus holding to maturity.

“In 2015, 1.4239 billion smartphones were sold worldwide.”

“The global smartphone market is expected to grow in 2024, with shipments reaching 1.23 billion units”

Hmm?

The intended point, is that smartphone ubiquity and omnipresence is a dominant reality — but the functionality in ten years will probably be disturbingly profound and mind-altering.

Between geopolitics and demographic shifts, it doesn’t seem far fetched to imagine that a traditional bond will go through some significant changes in 10 years — and a 30 year mortgage may eventually be a far different looking animal than what grandma has today.

It’s possible that people won’t have a way to value the future value of money and the role of banks will be far different in 10 years — just as the role of governments evolve.

10 years is forever and change is inevitable.

I recently found this dude to be very entertaining and enlightening:

“In a note for Macquarie Capital, Shvets wrote that investors may be better off ignoring most macroeconomic narratives – whether that’s people saying the U.S. dollar DXY is doomed or that out-of-control spending implies higher rates. In Shvets’ twilight world, the way these narratives play out is never as drastic as they’re made out to be. Investors may be better off weathering the gentle storm.“

Perhaps, what he was trying to say was that only gamblers should feel comfortable in this market with the never ending bid.

How is that any different than the past 30 years?

30 years ago people shopped in malls and online shopping was almost unheard of. People used physical maps to get around (map quest was still a few years away). If you wanted to look up a tidbit of information you went to the library. Many cars still had manually roll up windows and it wasn’t unreasonable for people to change their own oil. On a financial front, CDS were unheard of. There was still laws dividing invest banks from comercial banks

Point is, the world is always changing. Yes, AI is going to make drastic changes to the way we live. So did the rise of computers and the internet.

Things change.

JimL, to your concluding sentence-usually just when one is ready to relax a bit, enjoy the ‘rewards’, and congratulate themselves of their successful navigation of the preceding changes…

may we all find a better day.

Yields on the long end of US treasuries are heading higher, not lower. Between the massive deficits and increasing pressure on debt service, a huge increase in supply, plus political unrest, all indicate greater risk for investors. Greater risk always demands higher reward, in this case higher yields.

“On July 25, longer-term yields began to speed up their decline as the bets on Fed rate cuts kept gaining momentum ”

IMHO, the 10 year is at least 100 bps under priced. As the glow of the pre and post election dims, fiscal concerns will drive the 10 year more toward what I interpret as an equilibrium at 5.25. Which I consider as a only a whistle stop. Great article.

More importantly, vote for democracy.

everybody votes for democracy. people just don’t agree on what that means.

Yields have nothing to do with any election results.

Not quite “uninverted” yet, with the 4-week T-bill reluctantly dropping. Moreover, how is CONgress going to service that debt with a truly uninverted yield curve if the short end stays around four percent?

Interesting times.

The past 20 years of experience gives us the answer to that question.

No, because the debt wasn’t that bad until the last few years.

The new answer is: Inflation.

Besides gold and silver, commodity prices in grains are at 4 year lows and basically back to 2020 or 2021 prices.

Oil has dropped below $70. Nat gas is low.

So on the bright side. That is sort of good news to help keep inflation down for food and transportation? It could be worse if those items had seen the same inflation increases as housing, rent, services and goods.

Inflation is NOT down in food prices. I’m now doing more and more shopping at a high end grocery store. Reason: the quality of food and service at my former chain, Giant Food, which was a home grown chain for 80 years, was outsourced to a foreign company, and they couldn’t care less about their community customers or loyalty. All that matters is the bottom line. They now push frozen fish imported from China, and are discontinuing fresh unfrozen fish. I told them they were losing customers, like myself because of this policy and they couldn’t care less. Just paid $20/lb for some fresh thick Icelandic Cod at my new high end store. It tasted great on my outdoor grill. So we now how a society where the rich get to eat good quality, healthy food and the poor eat unhealthy crap food from food deserts, which makes them sicker with more medical problems in the future. No one is talking about this. What a disgrace! This is America in the 21st Century.

1. Inflation = rate of change. High prices that are not rising anymore are not “inflation”; they’re “high prices.” But when those high prices rise further, then that’s “inflation.”

2. Costco has a decent selection of not-frozen fish of all kinds from black cod (“butterfish”) to wild king salmon. Their farmed salmon trout is delicious and last time was around $8 a pound. The only thing is the packages are big, and you end up freezing some of it.

BTW, nearly all fish you can buy was at some point frozen, unless you buy the daily catch from local fishermen off the boat or in special stores by the dock, which is possible/legal in a few places in the SF Bay Area. You may have that too, being close to the coast. Truly fresh never-frozen-fish is different, it’s nice.

“BTW, nearly all fish you can buy was at some point frozen”. Yep, true but I like the fresh fish much better as you said. I have fish 3 to 4 times a week.

You cannot freeze fish that has been previously frozen. It also says that on the label. Packages are required by law here in Maryland to be marked previously frozen when they have been frozen in shipment and defrosted at the supermarket. My local supermarket discontinued the fresh Icelandic fish that was NOT frozen. It cost more but was well worth the price. Now I go to the high end store which still sells the same unfrozen Cod at $20/lb. I pay the price because I can certainly tell the difference and can afford it. Also, I cut it up into smaller pieces and freeze small portions for future meals. Not as good as when it’s completely unfrozen, but still satisfactory. They must ship it in by air freight from Iceland.

Inflation is NOT coming down in housing prices here in the heart of the Swamp. Today we’re doing another property in a crime infested neighborhood in the far reaches of Capitol hill in a neighborhood called Trinidad. A few years ago police had to wall off streets there because there was so much violent crime in these streets. People had to show an ID just to get to their homes. Now, these recently renovated properties that were bought by investors during the pandemic are coming on the market for prices of $1.3 million and up. They are being snapped up by eager buyers as soon as they hit the market. 7% interest rates are no problem for these buyers.

VA interest rates are 6.25%.