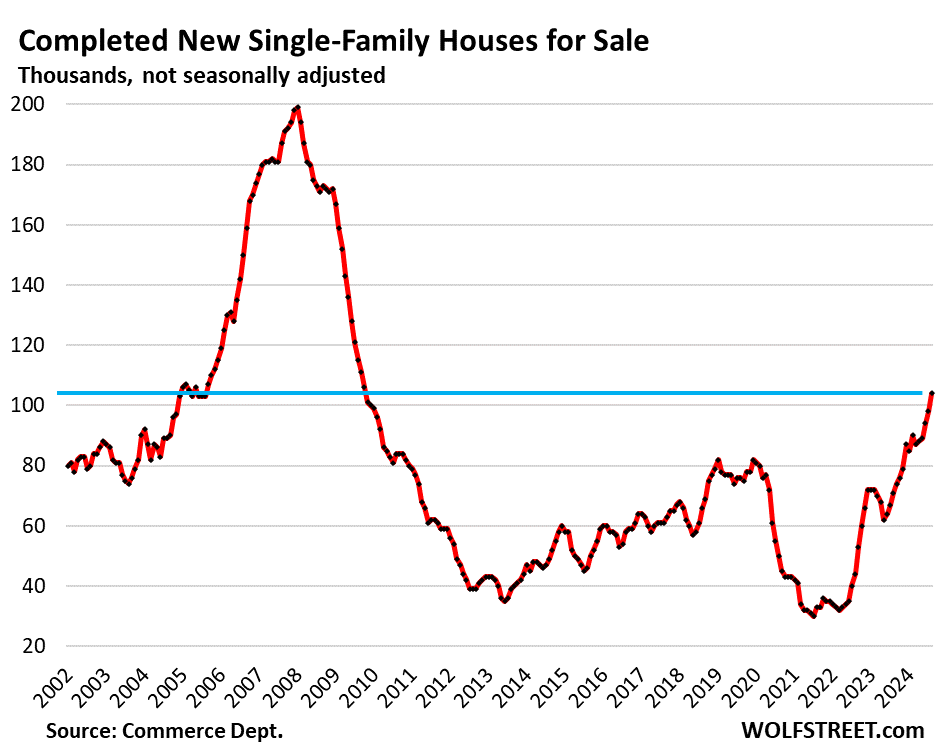

This buildup of completed single-family houses is a factor in resolving the price dislocations of the overall housing market.

By Wolf Richter for WOLF STREET.

Inventory of new completed houses jumped by 46% year-over-year, and by over 200% since mid-2021, to 104,000 houses in August, the highest since November 2009, according to Census Bureau data today.

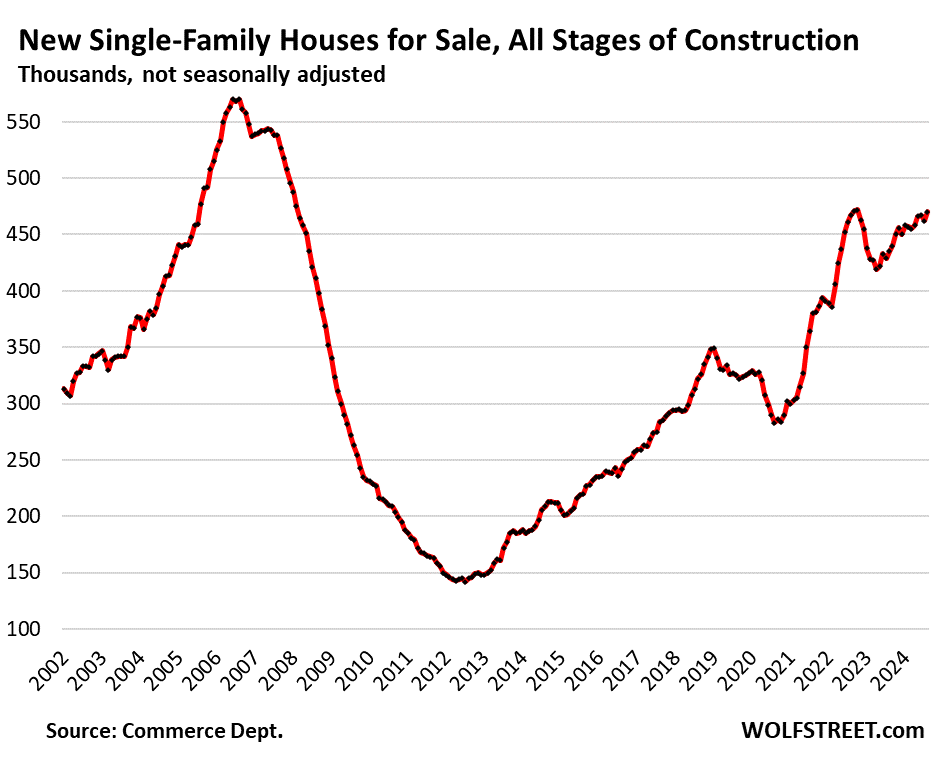

About half of all new houses sold are in various stages of construction currently, many of them in the early stages of construction or even before construction begins, and buyers have to wait for (sometimes many) months before they can move in. Finished houses are essentially move-in ready. But builders have tied up a lot of capital in them, and they have to be sold quickly. Inventory of completed houses encourages builders to make deals.

This buildup of spec houses is what the overall housing market needs the most, and it will help resolve the massive dislocations in prices that have befallen the housing market years ago.

Inventories of houses at all stages of construction – from not yet started to completed – rose to 470,000 houses, right up there with August-October 2022, and they’re all the highest since 2008. Supply rose to 8.2 months.

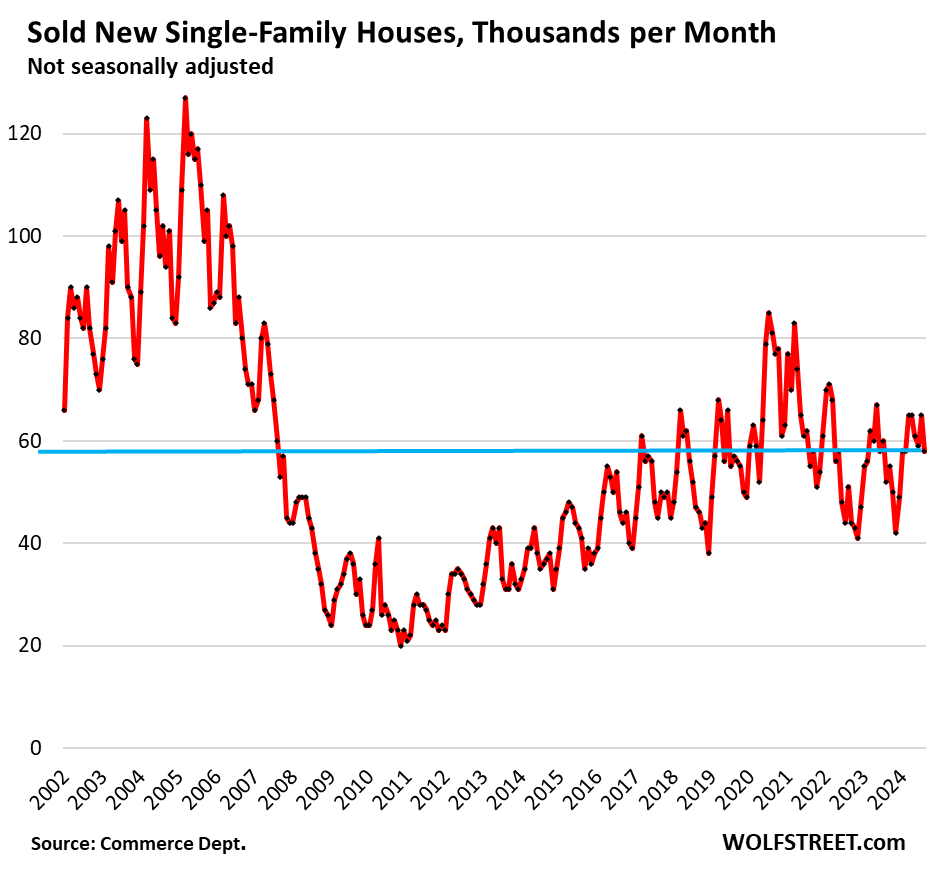

Sales of completed houses jumped by 53% year-over-year to 29,000 houses, not seasonally adjusted. Even at this brisk rate of sales, supply of unsold inventory of completed houses rose to 3.6 months. Rising inventory and supply are good – they’re what this housing market needs the most. Potential sellers of existing homes (the homeowners) need to compete with new houses.

Sales of houses at all stages of construction rose by 11.5% year-over-year to about 58,000 in August, not seasonally adjusted. This was up by 4% compared to August 2019.

By comparison, sales by homeowners of existing homes have collapsed to the worst levels of the Housing Bust, even as supply has spiked. Homebuilders are taking advantage of homeowners’ refusal to adjust their price expectations to reality.

Prices of new houses have dropped to prices of resale houses.

Contract prices of new single-family houses at all stages of construction dropped in August from July, are down by 4.6% from a year ago, and are down by 8.8% from the peak in October 2022.

However, these contract prices do not include the substantial costs of mortgage-rate buydowns, which have become the primary incentive that big builders are using to make deals. For example, Lennar disclosed in its Q2 filings that mortgage-rate buydowns cost $47,100 per house on average.

Homebuilders are also building houses at lower price points – smaller, less fancy houses with less fancy appliances and finishes – and they’re adding incentives, such as free upgrades.

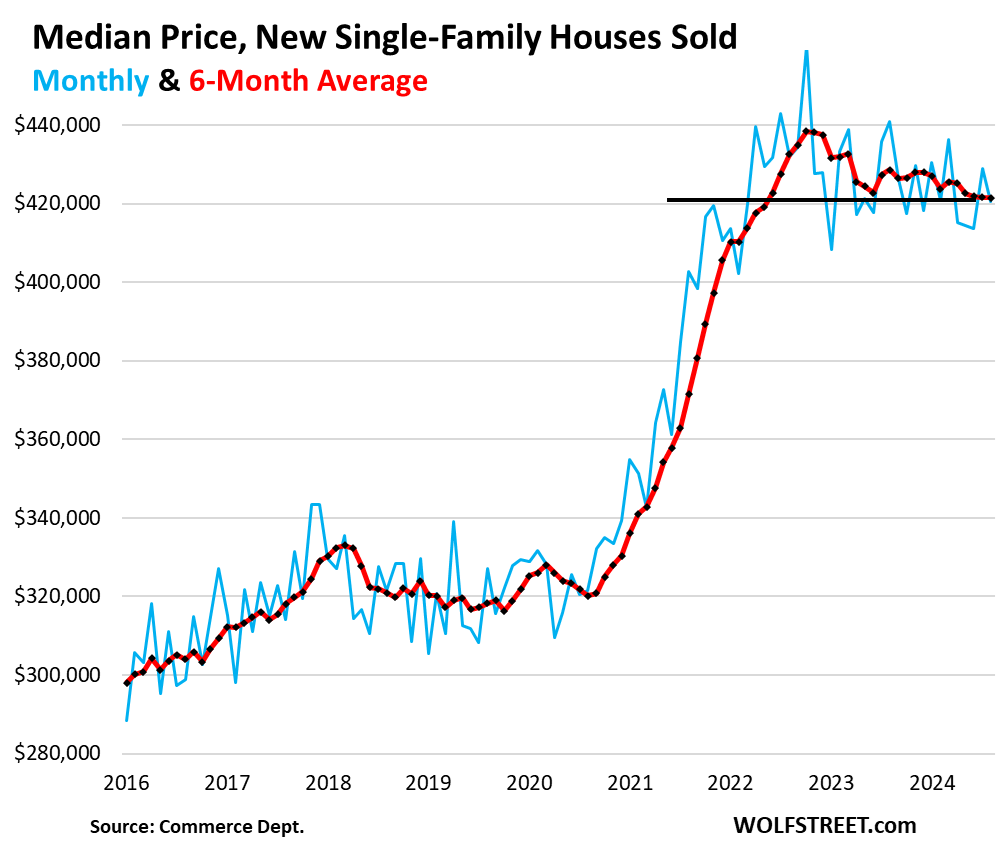

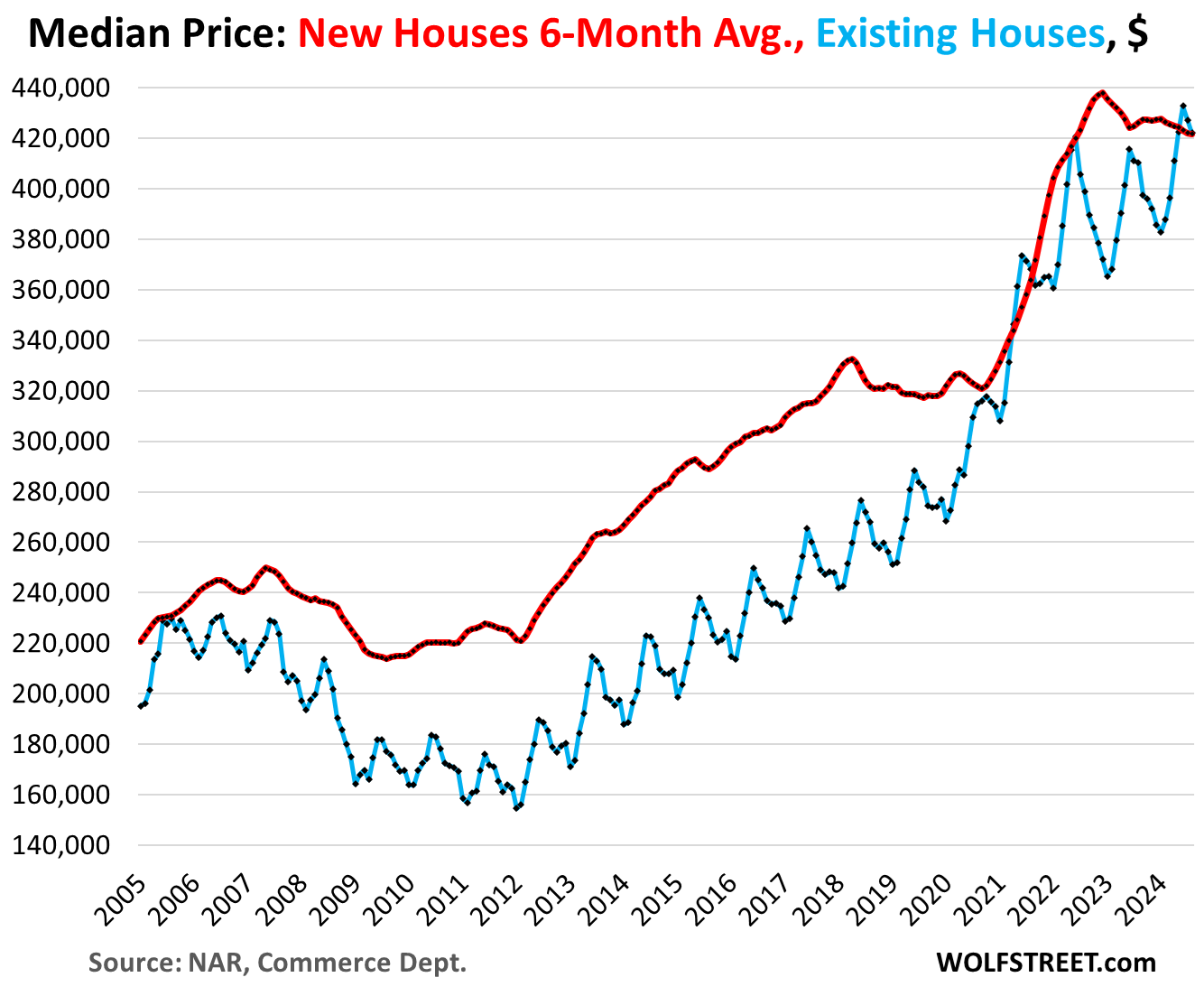

The median price of new houses (based on contract prices) is subject to large monthly up-and-down squiggles that are often heavily revised, so we focus on the six-month moving average of the median price, which includes all prior revisions, and irons out the monthly squiggles.

This six-month average of the median price declined to $421,553 in August, down by 1.6% year-over-year, down by 3.8% from the peak in October 2022, and below where it had been in June 2022. But remember, the costs of mortgage-rate buydowns are not included here:

New-house prices have dropped roughly to the level of existing-house prices – not even including the costs of mortgage-rate buydowns.

The six-month-average median price of new houses (red in the chart below) dropped to $421,533 while existing-house prices dropped $422,100 in August (blue):

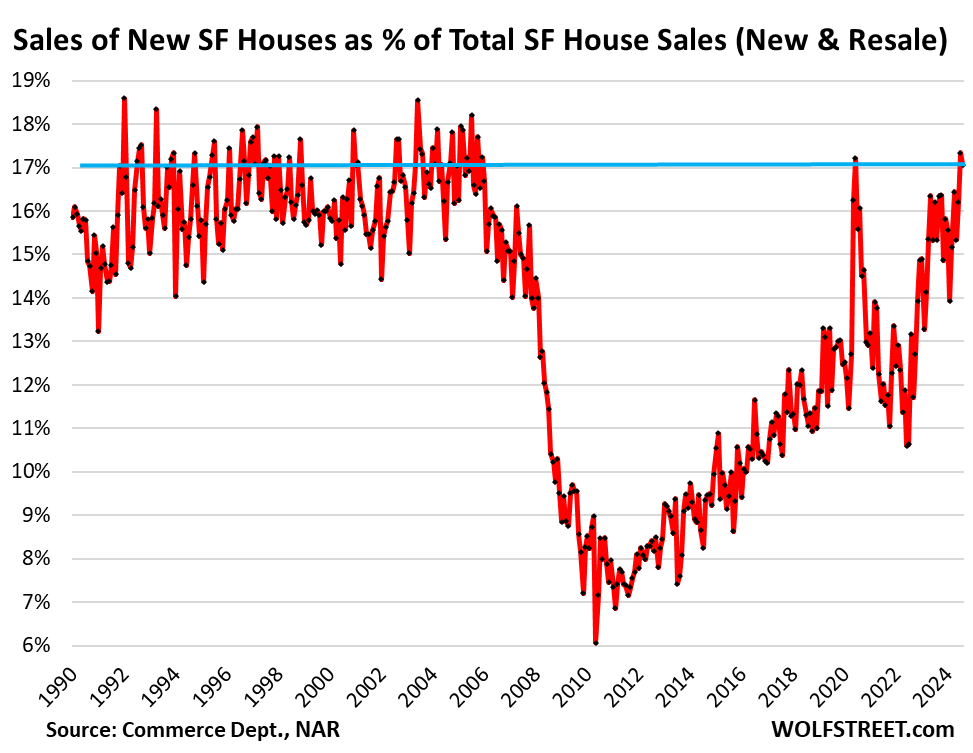

Homebuilders take an ever-larger share from homeowners.

Sales of new single-family houses as a percentage share of total single-family house sales (= new + existing) have been above 17% in July and August. This is the share that new single-family houses used to have in the decades before the Financial Crisis, but haven’t had since (except for June 2020).

The big homebuilders, the pros in the housing market, have figured out how to deal with this market and make deals. Unlike homeowners sitting on vacant houses waiting for whatever, they have to build and sell houses to keep their revenues flowing and to keep their businesses growing, and they’re doing that.

This aggressiveness by homebuilders to supply the market with competitively priced houses, and then to push sales with mortgage-rate buydowns and other incentives to make deals will help resolve the pricing dislocation that has befallen the housing market years ago.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Homebuilders are also building houses at lower price points – smaller, less fancy houses with less fancy appliances and finishes – and they’re adding incentives, such as free upgrades.”

Yea, that’s my new house bought in 2023. The builder threw in over $5K upgrades. I had to wait two months for it to be finished.

They are all sold around here now.

New bedroom communities are popping up on farmland that were sprayed with pesticides and herbicides that cause cancer and birth defects.

This is the kind of timely, pertinent and hard hitting analysis on the housing market that I come to Wolf Street for.

🤣RFLMAO🤣

Builders scrap off all the rich topsoil and sell it, then use cheap clay and sand mixture for the new home owners. No issues!!

Lake Elmo, Minnesota has a very large number of recently built, and new homes under construction. This is between St. Paul and Wisconsin. It is also not far from 3M’s headquarters.

Two problems though. First, the aquifer that supplies the city’s wells can’t keep up with the new development’s demand for tap water. Second, the entire region has PFAS, or per- and polyfluoroalkyl substance in its aquifers. Although this contamination is scattered around somewhat in terms of how concentrated it is; it did come from 3M and has been there for decades.

New methods of filtration and treatment are being tried and experimented with to address this problem.

A friend of mine and his family live in a new home in Lake Elmo. They use a reverse osmosis filter system for their drinking and cooking water.

Exactly the problem a lot of Delaware communities deal with.

Do not consume the soil you should be fine.

Why buy house?? Wasteful expensive capex

Meta is releasing Orion smart glasses

If you want house just wear those. Then you can live anywhere and save $$$

Guess what? Powered by NVDA (and MU)

Is your love bot powered by an NVDA chip too? Or do you handle that with Orion smart glasses as well?

My wife uses those Orion glasses. Says she likes to put me in “George Clooney mode”, whatever that means. It seems to get the job done.

Nope these posts are all 100% free range human!

My portfolio on the other hand…. :]

C’mon Wolfie, enjoy the economy! Being pouty is bad for your blood pressure…..

I’m enjoying the economy — the economy is doing pretty good, I’ve been saying it for two-plus years — as you can see if you ever read any of my articles, including this one here! I’ve been one of the most vocal recession-deniers here for two years, LOL!

🤣🤣🤣

I highly respect the home builders. They are generating “value” for the soeciety. They are also a remedy against “homes are buying, not for selling” cult, those who buy homes repeatedly but never sell.

I think only limiting factor for construction in my area is land availability. I wish local administrations would allow more land for construction. The problem would definitely ease.

I got buildable land on a golf course in Florida for sale. We never had a housing problem. Just buy a small home made in China on the internet. Not big enough? My first home was a 1000.sq foot. Why should our kids start with.more? They need incentive just like we did.

Of course. Spend that 50k on a gutted singlewide from 1972 and a tenth an acre and put in the labor. DIY’ers dream! Investor special!

But in all seriousness there is demand for smaller homes, but the ones on market in “livable” condition are limited and not everyone wants to or can afford to rehab a property, even the 203(k) rehab loan is only 35k max, while also paying rent. Builders have a market but the costs per sqft are astronomical for a single story sub-1000sqft home compared to the average 2 story tract at 1300-1500sqft.

Andrew: That’s the problem. There is scarcity of land that is permitted for construction. It may have worked for you, but in most places, converting a golf course to a residential zone is almost impossible. Otherwise, constructors would build a lot.

I live in north east and know about a big construction project for which the houses that will be completed in about 5 years are already sold. And there is scarcity of residential land there.

A cult?

Maybe it’s just financially advantageous to them? Do you sell assets that benefit you more by holding them?

“Homebuilders are also building houses at lower price points…”

But so far it is trivial relative to the insane price inflation powered by demented ZIRP.

Going from 440k to 420k is a tiny step in the right direction.

But ZIRP madness drove median new home prices from 220k in 2012 to 440k in 2023 – nothing in the real economy drove the component costs of homebuilding anywhere *remotely* near that much.

(What was the median in 2000, before all the arrogant ZIRP insanity (Helicopter Ben)? Perhaps 150k?)

As with the insanity of 2002-2006, homebuilders squeezed every possible cent out of the naivete/foolishness of buyers – using ZIRP to double prices…rather than halving monthly payments (affordability).

And the Fed stood there…watching (actually, creating.)

It is basically inexcusable that the Fed fueled essentially the same madness *twice* (actually, *three times* including the pandemic bubble).

The standard excuse is that “we only have one interest rate” for everything from new product invention/development to rank SFH real estate speculation.

But the Fed has plenty of regulatory tools (and statutory input) that the worst of the (repeated) excesses could have been tacked against.

Apparently the key policy makers at the Fed believe that doomed asset bubbles/wealth effects somehow contribute anything other than destruction to the US.

Those people are how countries die.

The Fed wants asset prices high. There’s no real way to deny it anymore with a straight face. As long as they can set a floor under asset prices while keeping CPI inflation low, they’re happy.

But those asset prices are incredibly fragile because most/all professionals know they are 90%+ propped up by printed money (past and future) – which inescapably creates inflationary problems the G can no longer frame innocent private actors for (thank you, Internet…and the homebuilders weren’t innocent actors…much closer to co-conspirators…).

When you have nation-sized companies at the Top of the SP 500 trading for PE multiples that are 2.5 to 3 *times* historic norms (suggesting a price normalization might see an SP 500 drop of 50-65% extremely quickly…a la Internet Bubble, Housing Bubble 1.0, etc.) that is the definition of phony wealth, wholly a product of ZIRP depredations.

And the housing market?

Post unZIRP, transactional volumes are off by 2.5 million or well over 33%.

Without historically unprecedented for-sale inventory starvation, home prices would have already cratered – just as they did in RE Bubble 2008 (LA prices off 50%, etc.).

Yeah, the changes in median price chart going back to 2005 was eye opening for me too.

You should see the one that starts in 2001…

There’s no law saying Americans have to be able to own single-family homes. In most first world countries it is a luxury, and people live in apartments.

Volpe – you’re not wrong, but strongly-fixed in our national psyche (especially post WWII), is the ‘exceptional’ ideal of home ownership as one of the foundation blocks of the oft-mentioned (but always-unwritten) ‘American Dream’. Given recent years of ravages from unbridled domestic housing speculation plus a massively-increased world population always desiring an ‘improved’ (and always more planetary land/resource-consumptive) living standard, we may be forced to acknowledge that even more of our ‘1st-world luxuries’ (so often perceived as ‘rights’) are not guaranteed …

may we all find a better day.

We are doing a lot of condos that have been recently renovated by big investors and just put on the market. The market is booming for these renovated entry level condos, even in marginal neighborhoods. The sale prices are up slightly but not anything remarkable. Some of the existing condo spec homes by mom & pop investors are not doing well at all. They are unloading them for what they can get, sometimes for a loss. Looks like the big guys are getting out while they can and the little guys will be left holding the bag like 2006/2007.

smart money/pro-investors are exiting markets even though they may have to sell for a small loss as they are not really emotionally attached to their houses unlike mom and pop landlords.

I know few homes in FL owned by BlackRock subsidiary sold for loss and these were bought just couple of years back.

From BlackRock to BlackStone (I’m looking for *any* angle to get this story in…).

Blackstone just sold Motel 6 for $525 million.

Blackstone paid *$1.9 billion* for them in 2012 (the, ahem, borrow of the 1st RE bust…).

Despite desperate happy talk in the Blackstone press release, that is an *enormous* loss (well over 66%).

It is incredible to me that nobody is talking about this massive hit (apparently the Blackstone pr Jedi mind trick is working so far).

1) This is a measure of just how huge losses can be in leveraged real estate,

2) Despite buying at the supposed “bottom” of a bust,

3) By one of the “smartest” and biggest buyers out there.

This Motel 6 transaction is crying out for a post, Wolf.

Hotels have been in trouble, and there have been a bunch of huge defaults and losses. So this fits right in.

But it’s hard to tell how much Blackstone lost, if any, and it could have made a lot of money on this deal, because:

– it was a leveraged buyout and they could have paid themselves big dividends and fees.

– Blackstone then leveraged the real estate, and cash-out borrowed against it, and that debt is now in CMBS, and Oyo has to deal with it, and the cash is Blackstone’s.

– Blackstone also sold some of the motel properties over the years.

So Blackstone could have made money on this deal overall, but it’s mostly private info and I have trouble getting it. I only got bits and pieces, not enough to string it together, and missing are things like how much Blackstone cashed out when it issued the debt, how many properties it sold for how much in total, etc.

Wolf,

That is definitely the line the Blackstone press release is taking and I don’t discount PE firms’ ability to extract profits in all sorts of more obscure ways.

But…historically PE firms did all that *and* sold for multiples of the purchase price…not 35% of purchase price.

And, yeah, lodging has been under a lot of pressure (although, whither the much ballyhooed post-pandemic travel boom?) but the Motel 6 transaction is a high-profile comp-setting type deal.

And 65% off ain’t chicken-feed for a national chain. One off office buildings have been taking big hits…but again, Motel 6 is a ntl chain with well over 1000 units.

I do think the business press should be doing more digging and less PR retailing….

Yes, I’m pretty sure they expected a better outcome — another Hilton, maybe. In 2007, Blackstone bought Hilton in an LBO, spun off its hotel properties into a REIT and sold it via IPO to the public, and sold the hotel operations separately via IPO to the public. And it may have separated and sold another entity. It made a total absolute killing on Hilton. So maybe it was trying to do the same thing with Motel 6 and didn’t quite make it to the IPO exit before the pandemic tangled everything up.

Word on the swamp (instead of street), lol. Yeah, Ray Charles can see what’s coming.

Oddly enough, a lot of the bitcoin to 100k or even 1M crowd are guys that went BK in the 2008 RE crash. Same as it ever was.

Wolf, can you do an article on how much of the funds for the chips act, inflation reduction act, EV charger and rural broadband bills have actually been spent? You’ve touched on at least some of them before but I think it would be interesting to view them altogether, along with any other spending bills like covid or disaster funds. I just heard there were unspent disaster funds from a bill passed before 2012 per the speaker of the house. Are we paying interest on trillions that aren’t being used?

I know the chip funds are very slow in being disbursed because of the due diligence involved and the phased releases. This will be spread out over years. I don’t think the dollars have started flowing yet.

The media has misreported on this, such as Intel “received $8.5 billion” — as if it were cash — when in fact it was “awarded a grant,” which then started the process of due diligence. So the awards are still being announced, but the cash will take time to flow.

Do the likes of Intel wait for the funds? Or do they just go ahead and complete the project from existing resources while they wait?

I don’t think there is any waiting going on. These fabs take years to plan, build, equip, and get going. And they started these massive project well before the CHIPS act was even passed.

“And they started these massive project well before the CHIPS act was even passed.”

If that is accurate, isn’t the CHIPS act less of an incentive than a pre-emptive bailout?

You can’t incentivize a project that has already started.

Add to that a lot of grants and tax breaks at all levels generally have milestone requirements before any payout happens. Easiest example being a local municipality giving a tax break to an incoming business, but that break doesn’t happen unless the business employees X number of people in a certain time frame. (I use the tax example because it gets reported in much the same manner as grants by the media)

Random50,

No, they do not wait. I’m in the construction industry and we have been involved in the early phases of this process. Preliminary design, site selection, budget analysis, etc. This has been happening for years. The money from the feds will come whenever, but these companies are spending their own cash (CapEx) to secure their future.

Interest cost of Land/house in 2021 was 3%. Today it’s 8%/10% bc Land isn’t a good collateral. The cost of Land/apt is much cheaper.

If there will be a systemic change from buying houses to buying apt

home prices will dive.

So with the recent drop by Feds on short term rates how will that translate into the economic spending by the folks that have been enjoying the 5 percent plus MM cash flow that has contributed to the drunken sailor at port for the last several years . This could also have a dramatic negative effect on sales as the cash flow drops from the Fed QT rate hikes .

I’m retired living off SS and interest income. I dread when my CDs reach maturity next July if the Fed continues rate cuts. My savings account has already emailed me about a half point cut. I was never a drunken sailor and have no mortgage or car payments but still I’m figuring out what else to chop. Frankly, my biggest monthly expense is Comcast if you want to watch SF Giants games. I’m thinking of going the illegal streaming route. PG&E bills are running $400 a month in the California central valley frying pan. Hope my teeth hold out!

Sorry, my biggest expense is property tax!

@Bongo sorry to hear that times are tough, Google “California Property Tax Postponement”. My brother’s mother-in-law had a paid off home but not a lot of monthly income and was able to qualify to “postpone” paying her property tax until she died. I’m pretty sure they had to pay off the taxes + 5% interest but it seemed like a good deal to me.

@Apartment Investor

That is kind of you. I may end up applying for that, only there is a limited amount of funding every year so it’s first come first serve. I would prefer not to have a lien on the house when I croak since my adult child with disabiiities won’t have to deal with that. We should be okay, it’s just that the interest rates gave us a little cushion to enjoy a few indulgences and now, not, lol.

@Bongo: Sorry to hear that. The Fed has been trying to keep the economy afloat on the backs of retirees and people relying on their savings. In a humanistic society, this would be considered a crime.

Bongo – I don’t know if this would fit you, but I have a MYGA (insurance company version of a CD called Multi-Year Guaranteed Annuity). They are not FDIC insured but some states insure them up to 250k. A 3 year term MYGA pays above 5% from several companies and you can withdraw interest monthly from some of them, and get your principle back at the end of the term. Minimum to put in is 20k on most companies. This is better than most CD’s I’ve seen. Otherwise, it’s Tbills for shorter duration for fixed income.

Shasta,

“The Fed has been trying to keep the economy afloat on the backs of retirees and people relying on their savings.”

Golly, only from 2002-2007 and 2011 to 2022.

Think of all the *much* more important drivel that flooded the “news” networks during those years…and how many times they ever covered the perversions of ZIRP.

^^^ This right here. This why they should have delayed cutting. The fed is neglecting those on a fixed income by allowing their monthly expenses to increase (inflation) and then lowering their return on their savings (lower interest rates).

Sorry you’re dealing with that. Also if this helps at all, I have found lots of ways to stream stuff for free. Additionally a lot of the services like Hulu and Amazon allow you to pay additional to add specific channels which I think ends up being cheaper than Comcast. Also you can easily activate and deactivate the channels when you no longer need them, i.e. only pay for football season not a full year. A lot of these accounts can also be shared with family, albeit for a slightly higher price but if you’re splitting it with friends or family that helps split up the cost. Personally I split a number of accounts with various family and friends.

The Fed as much as admitted the point was to force people to buy stocks.

Bongo – Have you looked into a reverse mortgage?

Reverse mortgages to pay for relentlessly inflating property taxes built on the back of the ZIRP’ed retirees/savers.

Are you that mayor in Maine?

I’d look into the MLB streaming and a VPN. The ability to stream all year from MLB.TV is like $200 annually; however, that’s only for out of market games. In order to get those, you’ll need a VPN to make MLB think you’re out of the Giant’s viewership area.

@Bongo For free streaming, be careful not to click on any websites you’re not familiar with because there’s a lot of viruses out there. But sites like YouTube, local tv channels websites, espn.com and what not should most likely be legitimate. I typically find a way to stream march madness for free every year and same with the Denver Nuggets games when they were in the playoffs. Locally you can’t get Denver Nuggets games, but with that it was a trick of logging in through a vpn (~$10/month) so it didn’t think you were in Colorado. If you know someone tech savvy they can help you figure out how to legally stream most things for free. No need to go to sketchy illegal streaming websites. Then just hook your computer up to your TV and you can watch everything there :)

Thanks to everyone for their sympathy and suggestions, what a great commentariot!

I’m not surprised new home builders are more successful at selling homes than those trying to sell used homes. I’ve been observing used homes for sale in the New England area. Most are coming on the market and sitting for months without selling, even with $100k price reductions. They start out too high and make only small decreases in prices over time.

What are you seeing for new spec builds in New England? The only ones I see are modular homes (why I asked about them below). There isn’t really space for entire new subdivisions like you see in flyover country.

In my town there are new builds that aren’t modular, but they’re all $1M+ McMansions, not starter homes.

ShortTLT,

I’m seeing new spec homes (not modular) in the Bangor, Maine area and also in and around Torrington, CT. They’re priced under 500k.

Interesting – Bangor is a small city and I didn’t see any listed on Zillow, but maybe they’re still under construction.

I was up in Skowhegan this past weekend – driving up 201 from Waterville, the road is dotted with ‘showrooms’ for modular & manufactured homes. It seems like this is the only affordable housing in the area.

Amazing that home prices are nuts even in the middle of nowhere.

@ShortTLT

Maine housing has been absolutely bonkers since the pandemic. Houses on Mount Desert Island doubled. Everyone is buying up 2nd and retirement homes.

Not surprising that Bar Harbor and anywhere along the coast) would be a popular retirement destination.

But it’s crazy that even going inland – with so much buildable land – the only affordable options are manufactured and modular homes.

It seems more and more like New England won’t see the same price pressures as markets like the sunbelt (entire new subdivisions being built) or Florida (and their ‘condopocalypse’ with all the HOA reassessing causing sales).

Wolf, does this data include manufactured homes?

no, manufactured (mobile) homes are not part of this data. The houses here have to be site-built, though they can use prefabricated walls that are assembled on site, etc.

I’m not a fan of “manufactured homes communities” (aka “mobile home parks”) but it seems like the people that complain the most about the “lack of affordable housing” are the ones that work the hardest to stop any from getting built in CA. New parks where people can own the land under theit own “multi-sectional home” (aka “double wide”) are not where I would want to live, but I bet that pelenty people would love to live in one (and not worry about annual rent increases) if they had the choice.

In my area, the issue with mobile home parks is, ironically, affordability. They all have HOA fees that run hundreds of $$$/mo – some of them nearly as much as my mortgage. Many come with amenities such as a pool.

In rural Maine, it’s common to see manufactured homes along the side of state roads – not in parks, but rather sitting on big parcels of land.

I think they’re a good idea for affordabilty and they seem to meet many folks’ needs. Personally, I prefer having a basement.

In Mohave county where I live, lake Havasu, bullhead city area, mobile homes spread about sitting next to site built homes, double wides, single wides ‘not’ mobile home parks, you own the land. A retirement/ snowbird type of town, quiet, low taxes.

Check out the area, buy a lot, make sure it’s zoned for mobiles.

All the mobiles for sale on Zillow are older, don’t think I’ve seen one for sale that wasn’t over 20 yrs old…strange.

Re; Factory built homes, many more pre fab stick construction parts, very weak building codes (last of gov’t interference…oh joy!), etc.

Salton Sea was a fairly famous and similar retirement/vacation/snowbird place when I was a kid. Couldn’t just walk out into it because of sharp barnacles, (old tennis shoes, flip flops was option) but could float on belly and hold head up in 1 ft of water or when barnacles stopped maybe 3-5 ft depth plus..(a VERY OLD guess)..but was even better floating than at Great Salt Lake.

Had showers all over for when you got out.

(Still bet a lot of heart prob types went into bad V-fib and died while there.)

Sure is a mess now, from what I hear, although I also hear this “Slab City” homeless place with “homes” is pretty wild life style.

Not for old folks like us, although hear some hard core boomers are there.

As usual most anyone with “good business acumen” involved in the development got filthy rich and cleared out….my relevant point to article which I read with mixed feelings.

“(a VERY OLD guess)..”

Look up on Wikipedia when the modern Salton Sea was created (1905), how, and by whom. Interesting story.

Too bad there’s a much smaller share of new home build in somewhat desirable parts of SoCal (without driving into the middle of nowhere) which means it won’t put pricing pressure on delusional home sellers around this neck of the wood anytime soon…

Guess I just have to put up with seeing funny listings like the one I just saw in my inbox from Redfin, a new listing of low low price of $739K asking for a 730 sq ft house in a sketchy part of Long Beach…what a joke..

Why are prices in cali so out of touch with reality?

Southern California and Bay Area much different than slightly North. Prices are still high but 650K will get you a 2500 sqft house in a decent area. Plenty of new housing going up as well. We did get a lot of Bay Area transplants when companies went telework but they has mostly ended. Summers can be hottish but electricity rates are some of the best in the state. Highest bill ever was $200 and that was this last July which was a cooker.

I left North CA because of housing costs. What area “slightly North” are you referring to?

Prices are out of touch everywhere. Even the modular homes you referred to in an earlier comment are ridiculously high. I don’t mean “manufactured” homes (trailers). I’m talking about modular homes. There’s a modular home company in Ellsworth, Maine that’s charging as much as builders of stick built homes. Builders of modular and stick built homes are also having trouble finding enough employees. My spouse and I spoke with a builder in Belfast a few weeks ago who said there’s a 2 year wait list for stick built homes due to labor shortages. You can find spec homes in Maine, but they are few and far between.

I got buildable land on a golf course in Florida for sale. We never had a housing problem. Just buy a small home made in China on the internet. Not big enough? My first home was a 1000.sq foot. Why should our kids start with.more? They need incentive just like we did.

Depends where in Cali. IMO Redding is cheap vs. San Diego. Or even the new houses being built off the 41 on the outskirts of Fresno. But as far as San Diego is concerned – high paying jobs lead to high cost of living and there’s a fair amount of high paying industries here from tech, chips, pharm, biotech, and med. tech. Also, look at how little land is available to actually build on vs. what’s been built on already. If you have the means to do it, you can tear down a crap shack in North Park and build a brand new house and sell it for well over a million (have had coworkers do it).

“you can tear down a crap shack in North Park and build a brand new house and sell it for well over a million”

Uh, aren’t the crap shacks a mil? I’d think more like $2m breakeven to buy one and rebuild.

Wolf- Do you have historic data that goes back further? Wondering if the ratio of new home sales price vs existing home sales price swings on a cyclical basis. A long term ratio chart of the two would be interesting to see. You’d think new (on average) would always be higher than used (on average)- improvements do depreciate…

Her you go:

How much could the median price decline in the next two years? Do you have any guesstimates? Take a SWAG.

I’ll guess 10%.

Lots of hopeful peeps will be pissed.

@Phoenix_Ikki I just looked on Zillow and there are about a dozen “mobile homes” in Malibu for sale with list prices from $1mm to $5mm (and monthly pad rent/HOA fees higher than the average monthly mortgage payment in the US).

Yup sounds about right….hence why it’s such a joke in SoCal, a cruel joke that doesn’t seem to have any end in sight..at least those prices is for a view in Malibu but when I see $1M for ordinary house in Chino with cow dung smell for free…that’s another hilarious joke in itself

Why is it a joke? Supply/demand. You’ve mentioned delusional sellers. If any are selling, albeit slowly, they aren’t delusional. It’s buyers that are idiots!

I saw those – I wondered what the fire insurance would run. Perhaps the buyers are only there 5 and a half months, or maybe they are unaware of living in the west.

I like Malibu but the people, that’s up for debate.

Thanks for the great articles. Not only are new homes 47k cheaper once you factor in buydowns, they also don’t require the ~25k for new roof and maintenance that so many existing homes I’m seeing need. Sellers in NW PA are still in denial, and unfortunately, anything nice still seems to go for outrageous markups…too much stupid money out there still.

Assuming the builder honors the warranty.

See also: DR Horton

Bought a new house for retirement in FL about 11 months ago. Drove the entire coastline of FL looking at existing houses for sale last year. We ended up buying a new house far from the coast because the coastal homes are way overpriced especially for the small lots they are built on (and the dogs would be pissed). Got a lakefront single story 1900 square feet home on 1.25 acres for mid 400K. A new home today costs less to operate, a lot less maintenance than the old model, and homeowners insurance is way cheaper.

@David Metheny glad to hear you (and your dogs) found a home you like, but new homes are like new cars and have less problems for a while, but due to a combination of “more things to go wrong” and “they don’t make things like they used to” I have more problems with my newer property and newer cars than the older ones. My 1960’s apartments have the least problems and of all my cars and SUVs my 1996 Landcruiser (that I have owned since 2000 and is pushing 300K) is the most dependable. My wife’s (still under warranty) Lincoln Navigator has the most problems ($2K+ sunroof problem and $2K+ “cam phaser” problem just this year) and my newest property (2 units that I built in 2022) has had the most problems related to the $100K high tech sprinkler system monitoring and just this week I found out that some microwaves just don’t work with the fancy new AFCI Breakers in the new unit (the electrician told me to just buy my tenants a different microwave).

Smart electrician 😂. Sad for you how many microwaves will that be? Can you just get some air fryers instead?

@Wolf if we continue the trend out a year or two is there any precendent of similar events in thr past and if so what was the price drop/effect on the single family homes prices nationwide?

I like to go to new developments to see what is new and talk to the real estate folks. I went to a Lennar development out in the suburbs from a tech hub. Decent size of about 120 homes and about 50% sold/built and rest slowly released. Houses range from about 2500-3500 sqft, but mostly in the 2500 sqft range.

Compared to where I live in the “city” and the new development, they get about the same size of house for half the price, but brand new. In other words, this house would cost twice what they are currently selling if it were in my area. Almost all of the buyers are tech people with obligatory 1-2 Telsas. The sales folks were saying the price is all inclusive, no hidden charges. You could upgrade if you ask early enough, but pretty much as is.

They are also adding mortgage buy downs as a bonus. But you can tell they are cutting out the fat, like no EV chargers. So, brand new neighborhood with similar social economic class folks within driving distance at half the price and mortgage buydowns. Fucking no brainer, folks. I wouldn’t mind living there, if I had kids and starting out.

Then, I drive around the neighborhood and see if I can find a comp.

These poor folks trying to sell and to complete with these brand new homes. Yes, bigger yards, but 20+ year old homes versus brand new, no real maintenance for at least 10 years. That is why their house is on the market for 60+ days or second listing.

I confirmed it with another smaller developer of homes in the area. It is about twice compared to my area. So, if you want to get under the skin of a seller’s agent of a used home and there are brand new homes nearby and similar prices, poke the bear and get a better price.

Good luck.

I would say those new homes are junk, but….the 20 year old stuff is even worse (generally).

Good article Wolf. After-all, why overpay for time capsule, when you can get a new, up to code modern home. In a lot of cases, location is just as good, because builders buy up old tiny houses to tear down and build new construction. You can’t just remodel your house, while “Working from home” as easy anymore either.

Last two or so years, i’ve been reading comment sections here and other websites as to how builders won’t build new construction, because of higher interest rate. This was laughable. I’ve been saying, that builders are in business to build and they will figure out the way, otherwise they go out of business.

For me, the new homes are built with inferior materials. Vinyl siding instead of brick. Vinyl wood look flooring instead of real wood. It goes on and on.

Wolf, are you aware that Seeking Alpha has taken your content and put it behind a paywall? They are “seeking profit” from your work. I hope they are at least giving you a cut.

I’ve sent them a “strongly worded letter” indicating my feelings about this borderline unethical practice.

Anyhoo, nice work and I am grateful for your blog, where I can read insightful analysis like this without having to pay a middleman who adds no value.

ChrisFromGA: You should email this to Wolf I doubt he’s reading comments on this post at this point…

1stTDinvestor,

I read every single comment, no matter when it was posted. I’m in my commenting software that shows comments in reverse chrono order, the most recently posted comment on top, no matter what article they were posted on.

ChrisFromGA.

Seeking Alpha has had my permission to republish my content for many years. I don’t think it’s a “paywall.” But you have to log in to read them – or to read anything on SA. Setting up a basic account on SA is free. But they have “premium” accounts that are not free.

Thanks for the reply. It actually is behind a paywall, because I have an account there and was logged in when I was surprised to see them trying to charge for content you provide for free (thanks again.)

Recently they started putting almost everything there behind a “premium” paywall including even basic “rip and read” news items that can be easily found on CNBC, CNN, or Reuters.

I am not sure what is going on but I think it could be a sign they’re hard up for cash.

Thanks.

Paywalls are the future. Internet advertising – thanks to Google largely, which now got sued over it — has deteriorated to the point where publishers can no longer survive, with Google and big tech taking the majority of the money that advertisers spend. Paywalls solve that problem. More and more publishers are doing it because advertising is no longer working for publishers, and many fairly successful publishers (in terms of readership) have collapsed. I have long struggled with it too, but chose to ask for donations instead of putting up a paywall so that all my content remains available for all to read. That also works.

The problem with new houses is that in most populated areas they are on the far outskirts. New home sellers talk of the “easy drive to major employers and attractions” but over the years that 45+ minute commute wears on a person. A used house may need a roof but your job is ten or fifteen minutes away.

This new home builder supply will help as long as investors don’t start buying it all up.

Big investors are building their own “build to rent” communities, entire subdivisions. Build-to-rent is a huge thing now, and it makes sense because these communities have hundreds of houses all in one place and come with a leasing and maintenance office and common amenities. This is much more profitable to manage than buying hundreds of scattered houses here and there. The biggest single-family landlords have started selling their individual houses as they pivot to rental subdivisions.

Some of the biggest single-family landlords have their own homebuilding divisions; others work with homebuilders.

Build-to-rent adds supply of single-family houses. Build-to-rent subdivisions offer a great option for people wanting to live in a nice new house and save $1,000 to $2,000 in monthly expenses. There is a lot of demand for them. These people are arbitraging the ridiculous home prices (high mortgage payments, insurance, property taxes, and maintenance) and much lower rents for the same type of home.

Also, multifamily apartments. Lennar has stated that prior to 2016, most apartments buildings they built they would sell after completion. (someties as individual condos). Since then, they been keeping many of these multi-family units and are now landlords.

GSE backing these mortgages makes it a now brainer for the big landlords.

I’ve noticed something very interesting politically about those build to rent housing developments. The very same politicians who want to rezone existing neighborhoods to allow duplexes or even small multiple apartment buildings on formerly single home lots are very much against new single homes built on new land to specifically be rented. If these were apartment complexes with the walls touching they’d have no problem with this construction, but if you separate the rentals by 8 to 10 feet and put some landscaping in between suddenly the builder and investors have performed some sacrilege against the American Dream.

Some people will never own a stand alone house, especially in California or New England. They might have owned a condo when they were single or will end up in one late in life. So to have these rental neighborhoods exists gives them an option during the child raising years.

One political side seems to want to control and manipulate every aspect of housing and zoning and investing and history shows that leads to nothing but shortages and workarounds. For instance, if a $25k “first time buyer” government credit ever gets passed (doubtful) I think you’ll see all prices jump by $25k, and some sellers offering “second and third time buyer” discounts..of $25k. Nobody is going to leave “free” government money on the table.

I’ve wondered why there aren’t more small (e.g. <1000 sqft ranches) homes available as rentals. I assumed it was just inefficient use of the space.

If people want to rent less than 1,000 sf, why don’t they rent a nice apartment of that size? They can probably rent a 1,200 sf apartment and still come out ahead. Well, actually, that’s what they’re doing.

Personally I have a really big stereo, which is why I’m glad I don’t share a wall with any neighbors (for their sake). But I also wouldn’t want to buy in the current market, with prices sky-high.

I love my little 960sqft ranch, it’s exactly what I need and nothing more.

Unemployment claims drop to 210……sure glad that emergency cut was in time. Pure sarcasm,

Disney cutting several hundred white collar……what does this mean in a company of 220,000 employees…..

Jim the boss calls Joe the underboss and say let 300 go…….Joe whines and cries mostly because his empire is being reduced so his income will probably need to be trimmed…….but……Joe quickly calls in HR and explains that the 150 folks in the x department that were never hired because that project never was funded are now gone from the chart……the 100 slots that are empty in T department will not get filled……..the 100 in the R department will now be called full time/part time.

Another day of sweat by Joe as he tells the Times about how times are tough. So much pain.

At one time I was a person running HR in a major company for a short period of time….this is how it works in the larger companies……until the unemployment rate gets up to 6 to 7 percent.

From Invitation Homes Investors presentation.

“We focus on high-growth markets and infill neighborhoods with proximity to jobs, transportation, and schools”

So if you are not looking for a home with good schools and close to hot jobs then your probably are not competing for the same home. So look at places the big landloards are not to find good deals. ;)

/sarc

Such as neighborhoods with bad schools and long distances from work.

Mr Powell at the FED makes around 200k a year. And I am sure he works hard and is worth that. However, he is priced out of what was a middle class suburb here pre pandemic.

I hope they are happy with the results – starter homes are 700k and that’s a townhouse. And they, at least until perhaps right now, have been selling left and right.

Burn the excess inventory…Alan Greenspan solution to the housing bubble…The joker burned the money…what this empire needs is a better set of crooks…by hook or crook…Thomas crooks, lol…clown show empire…scripted by the numbers…