Inflation-adjusted consumer spending jumped. They splurged on durable goods. And still saved some. In response, the Atlanta Fed’s GDPNow jumped.

By Wolf Richter for WOLF STREET.

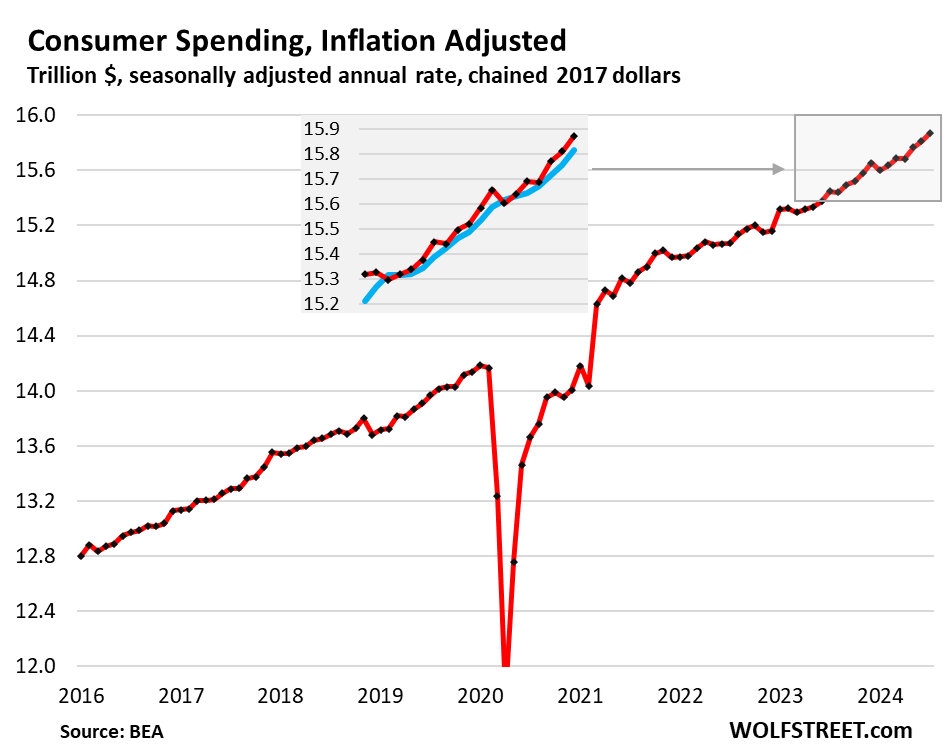

Consumer spending, adjusted for inflation, rose by 0.39% in July from June. Spending growth in May and June had also been strong, and the three-month average growth also jumped by 0.39%, the highest growth since February 2023, and the second highest since November 2021, according to data from the Bureau of Economic Analysis today. On an annualized basis, that pace of growth over the past three months, adjusted for inflation, was 4.8%!

Year-over-year and adjusted for inflation, consumer spending rose by 2.7%, similar as in May and June. All three months had been the largest year-over-year growth rates since November 2023, and before then since February 2022. (In the chart below, the insert shows the three-month average in blue).

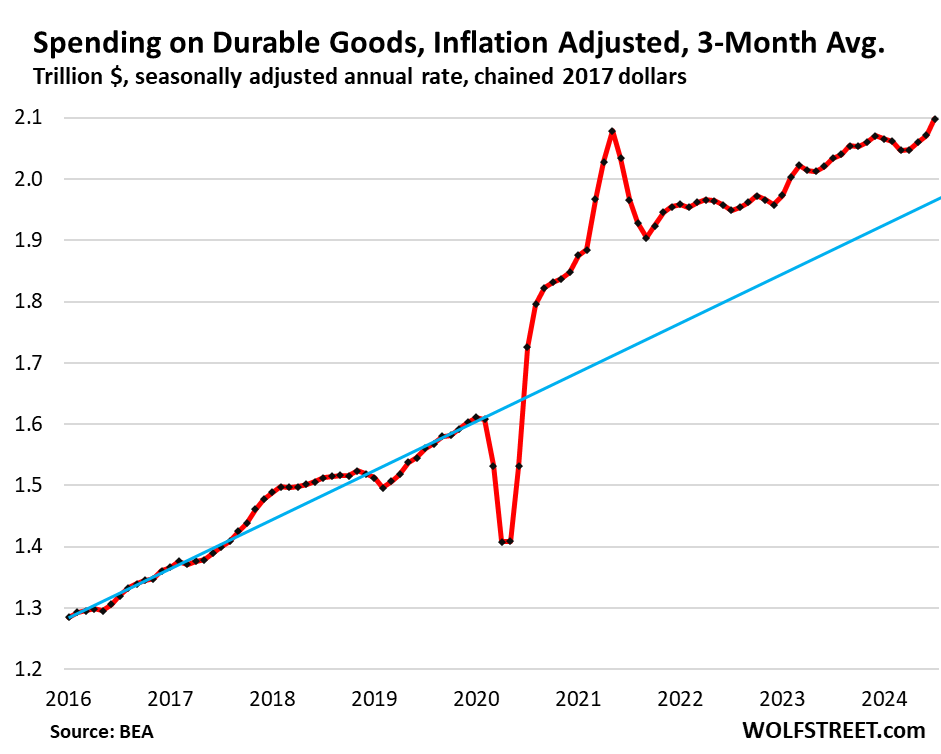

What was particularly fascinating was the inflation-adjusted surge in spending on durable goods over the past three months, where a slowdown had taken place earlier in the year. But starting in May, our Drunken Sailors, as we’ve come to call them lovingly and facetiously, returned to the punch bowl.

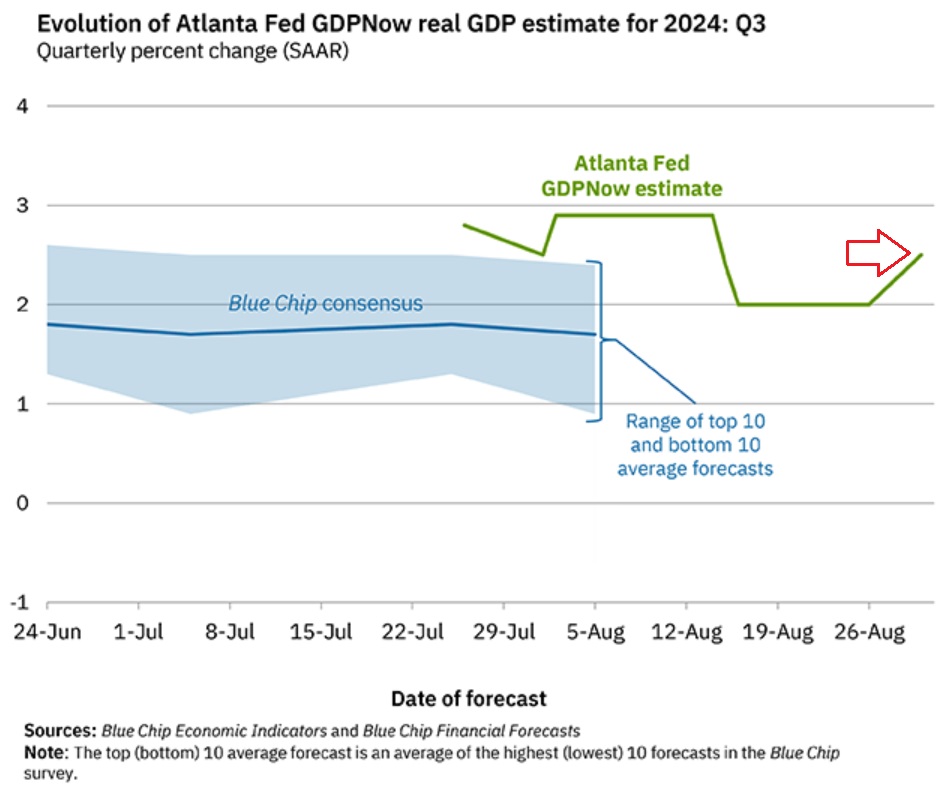

Upon the release of this data, the Atlanta Fed’s GDPNow, which attempts to estimate Q3 growth of real GDP, jumped to 2.5% growth, up from 2.0%. The 10-year average real GDP growth for the US is about 2.0%.

Spending on durable goods, adjusted for inflation, jumped by 1.7% in July from June. Given the big monthly squiggles in this metric, we look at its three-month average, which jumped by 1.3% in July. That’s an annualized growth rate of 16.8%!

You can see the slowdown in spending earlier this year through April, and then over the past three months, the return to the punchbowl.

In 2021, we expected that spending would eventually revert to prepandemic trend (blue line), and it tried for a little while, but then just stayed well above it. At this point, it seems to be permanently above the old trend, possibly establishing a new trend line. This kind of shift in demand from trend is just amazing:

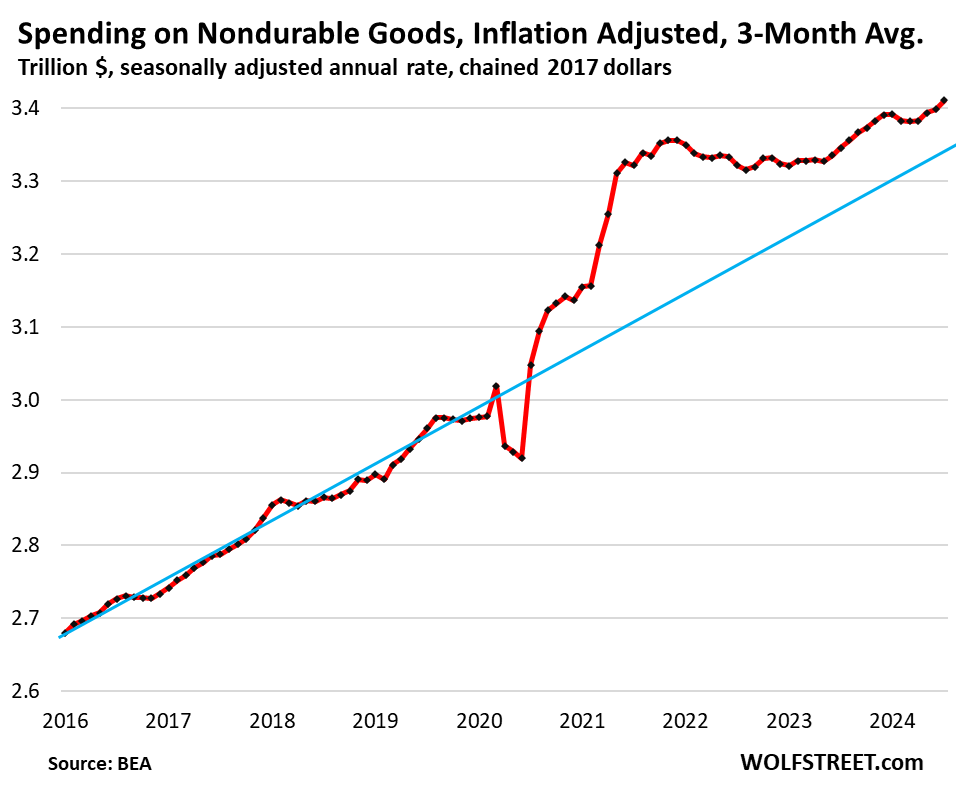

Spending on nondurable goods, adjusted for inflation, rose by 0.24% in July from June. The three-month average rose by 0.36%, or about 4.4% annualized, the highest growth rate since February 2023, and beyond that, the highest growth rate since October 2021. Year-over-year, spending rose by 1.8% adjusted for inflation.

Spending on these items, adjusted for inflation, has also not returned to prepandemic trend. Nondurable goods are dominated by food, gasoline, apparel, footwear, household supplies, etc.:

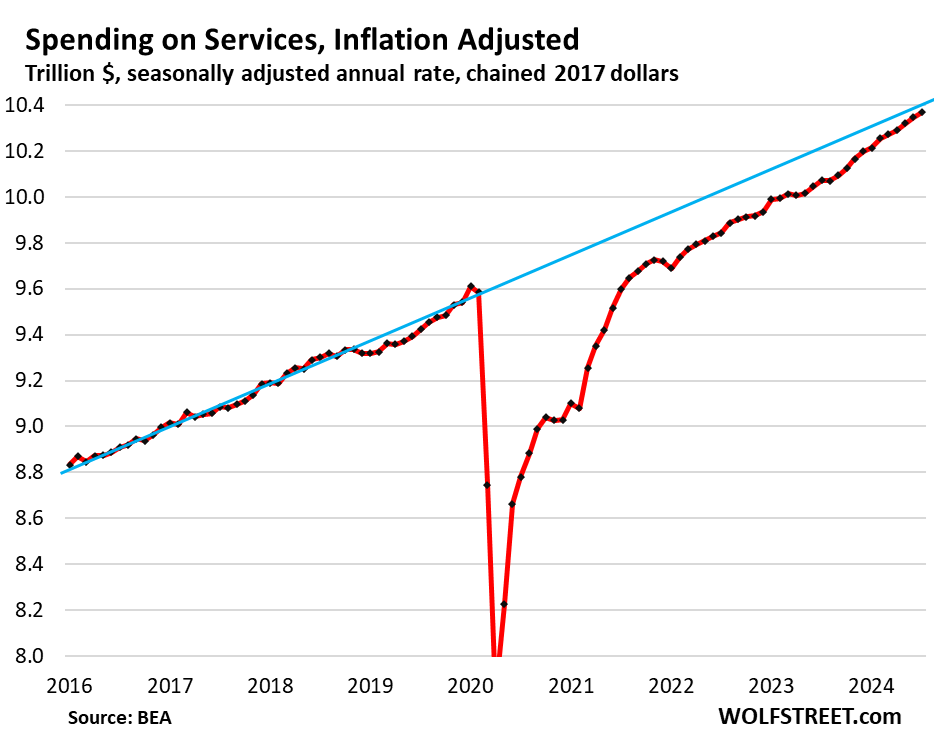

Spending on services, adjusted for inflation, rose by 0.20% for the month (2.4% annualized) and by 2.9% year-over-year.

Spending on services accounts for 65.5% of total consumer spending. It includes rents, utilities, insurance, streaming, broadband, cellphone services, entertainment, healthcare, airfares, lodging, rental cars, memberships, etc.

Spending on services still hasn’t quite reverted to prepandemic trend but is now getting close to it.

Where did our Drunken Sailors get this money?

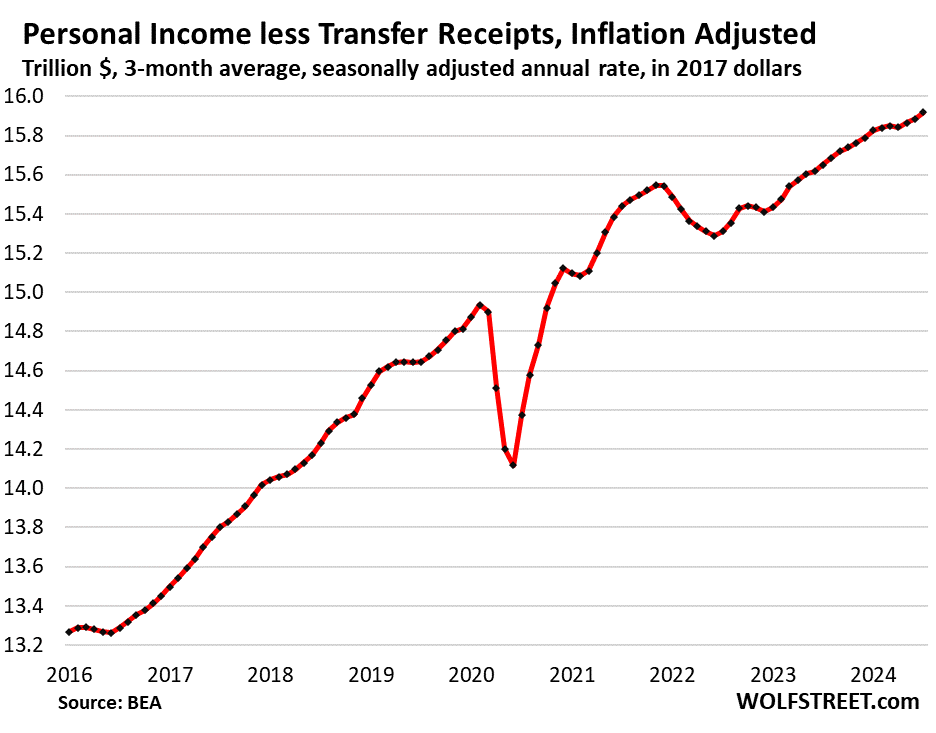

Personal income without transfer receipts – income from wages, salaries, interest, dividends, rental properties, farm income, small-business income, etc., but excluding Social Security and other transfer payments – and adjusted for inflation, rose by 0.16% in July from June. The three-month average rose by 0.22%. Year-over-year, it grew by 1.7%. This is by how much our Drunken Sailors out-earned inflation.

But during the inflation surge in 2021 through mid-2022, inflation outran wage increases. It took consumers until April 2023 to catch back up with what they’d lost to inflation through mid-2022.

This income growth is a function of employment growth, rising wages, higher dividend and interest incomes, higher rental incomes, etc. About 11 million single-family rental houses are owned by mom-and-pop landlords with 1-9 rentals.

Transfer receipts are dominated by Social Security benefits that grow with more retirees receiving them, and with rising benefits that are adjusted to inflation. Transfer payments also include VA benefits, unemployment benefits, welfare benefits, etc.

During the pandemic, transfer payments were dominated by stimulus checks, unemployment benefits, extra unemployment benefits, and other pandemic payments made to consumers.

This chart shows both personal income without transfer receipts (red) and transfer receipts (blue).

![]()

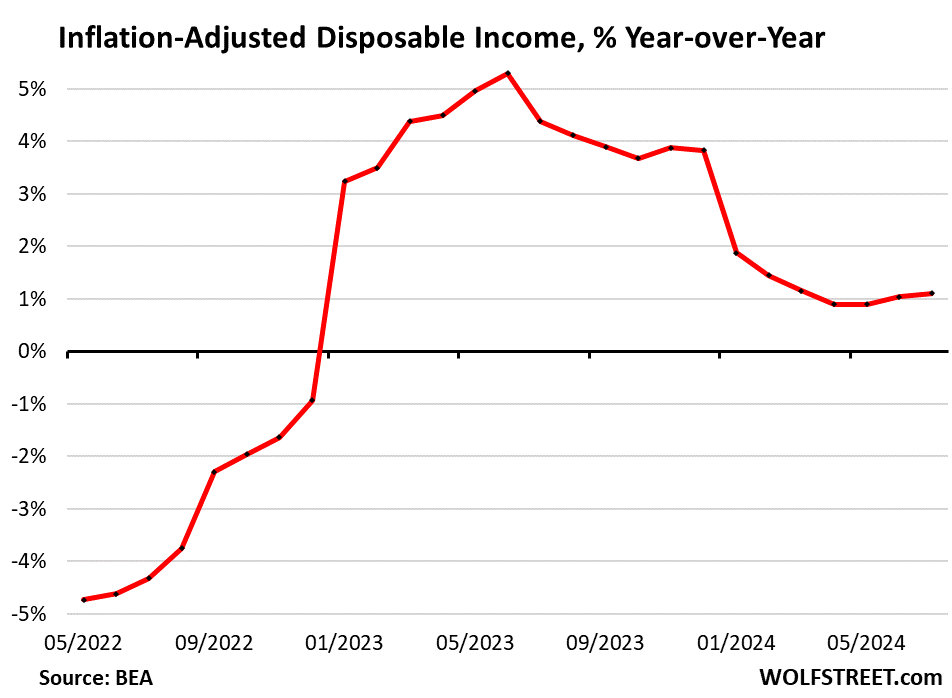

Disposable income, adjusted for inflation, grew 0.11% in July from June. The three-month average grew by 0.17%.

Year-over-year, disposable income after inflation grew by 1.1%, marking the 19th month in a row when disposable income outran inflation on a year-over-year basis, after having taken a hit from early 2021 through mid-2022, when the explosion of inflation overpowered wage increases.

Disposable income is income from all sources minus income taxes and social insurance payments. It’s what consumers have left to spend on goods and services and to save.

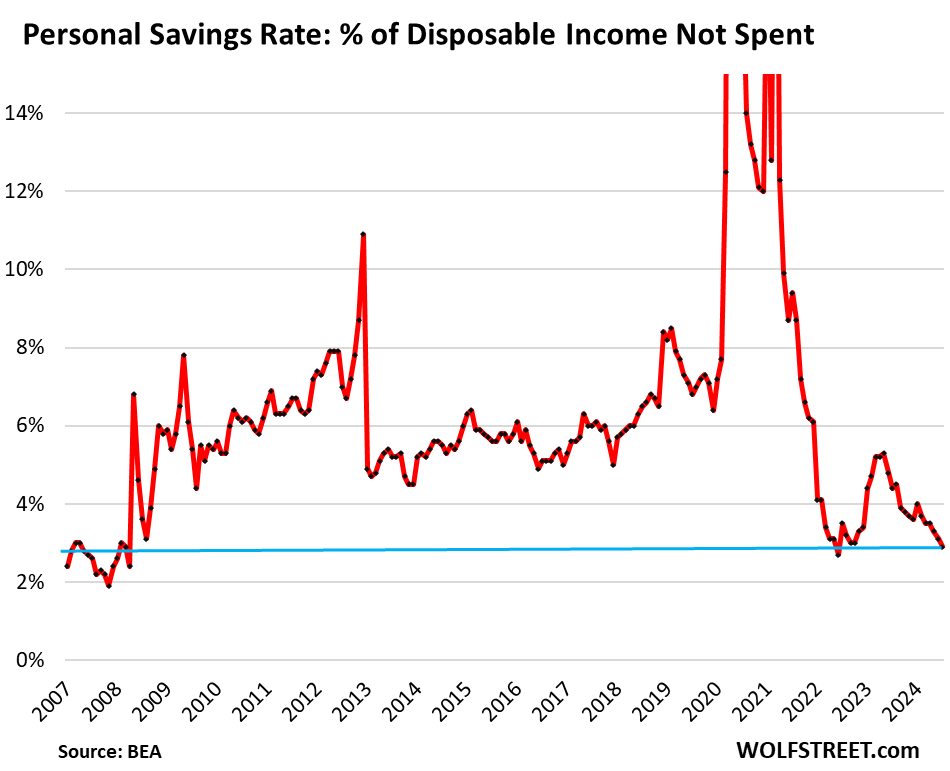

And people still spent less than they earned, and they added the remainder to their savings, but they did so at a slower rate.

The savings rate dipped to 2.9%, so they’re adding to their savings at the slowest pace since June 2022.

This is the portion of their disposable income that they didn’t spend. It doesn’t mean that they put it into savings accounts. They might have bought stocks, CDs, or money market funds with it, or left it in their checking account, or used it to pay down credit cards, or whatever.

The surge in home prices (65% of households are homeowners), stock prices, and other assets have caused many Americans to feel confident enough to spend a little more and save a little less. And yet, they’re still adding to their savings.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

That’s with continual decline in durable good prices. Gasoline just cratered as well so people are going to be Splurging going into Halloween.

Gas was $5.99/gallon at the Truckee Chevron tonight (a little lower than July, but I would not say the price “cratered” (it is down less than 10% in the Bay Area).

I hardly think Truckee is a good barometer of fuel prices in America. I know in San Antonio we’re at the lowest per gallon price since coming out of the pandemic, and that’s without considering inflation. With inflation accounted for, I think we’re probably at a 10-year low.

$3.27 at Costco Scottsdale. Not my fault you get gouged. BTW, $3.92 in Palm Springs. YMMV. Gas is cheap. And commodity food prices are dropping, sooooo inflation beyond our lovely monopsony paradises will fall.

As for housing. Expensive until we have enough empty ones available for rent. And with the tide of suckerz quitting the short term market… well the Fed is going to drop rates

Just filled up at $2.91/gal here in NC.

I just want to confirm what you wrote. You’re saying you pay basically six dollars a gallon in the in the san francisco area for gas?

Lake Tahoe area, up at 6,000 feet altitude, in one of the wealthiest vacation-home spots. Everything is expensive up there. Gasoline has to be trucked up from God knows where.

Even our gas station from hell here in San Francisco is at $4.xx

I have not paid less than $5 for premium at any time since mid 2021. San Jose, California. Low of $5.10 to high of $5.90 the last two years depending on various factors. But no $4.XX.

Find a different gas station. You’re getting ripped off.

Average price in CA is $4.32 (EIA), and we’re paying more than average.

Move to the east coast. BJ’s gas is $3.79 for 93 and name brand (Mobil etc.) is around $4.29 in the Boston commuter suburbs.

Gasoline here in Wisconsin is $3.12 today, down from $3.19 on Monday. But we don’t have those sky high wages and real estate prices that California does.

Might CaRFG (state-mandated formulation regulations for gasoline) be part of the huge differential?

And I’d guess that local and state taxation policies play a part.

Of course California hydrocarbon distribution has always been a unique challenge (though maybe not that far east?)

Did I hear Chevron is moving some operations out of state…

California is its own ecosystem but the commodity price fell by 15 cents on Friday to 2.10 a gallon. When the hits gas stations the national average will move below 3.00 a gallon and we’re still not in the winter blend.

Gasbuddy has an excellent blog on this topic.

Here in California we pay 76 cents per gallon in gas taxes (57 cents state, 19 cents federal). So our gas prices are too damn high!

1.76 /liter here in British Columbia. Works out to 6.68/gallon CAD. About $5 USD/Gal. Diesel is $2.00/liter

Actually total Federal, State etc. tax on gasoline in California is $1.18 a gallon

Just google ktla california total california gasoline prices

Here is the breakdown from that article and I think they are going up another 2 cents a gallon soon.

Earlier this year, an analysis by Irvine based researchers Stillwater Associates found Californians were paying at least $1.18 cents per gallon in taxes and fees alone. That number fluctuates by a few cents depending on sales tax calculations, which vary by city.

Here is a full breakdown of the added cost:

Taxes:

Federal Excise Tax: 18 cents per gallon

State Excise Tax: 51 cents per gallon

Sales Tax (estimated): 10 cents per gallon

Fees:

Low Carbon Gas Programs: 22 cents per gallon

Greenhouse Gas Programs: 15 cents per gallon

Underground Tank Storage: 2 cents per gallon

California has the highest gas prices in the nation, according to AAA.

This will end badly. We are going to shoot past a recession and jump into a depression if people do not start acting like responsible adults. This is an indicator of a generation of people who never learned responsibility and the word no.

Who says they aren’t? They’re still flush with money-printer-go-brrrrrrrr cash and they’re enjoying it before it depreciates any further. Read Wolf’s articles about consumer debt. These people aren’t going in hock to do this stuff.

Splurging everywhere on everything and to top it all off everyone and his dog is screaming that the Fed just has to cut rates now. I suppose after all bonuses depend on the S&P being at 7000 by Christmas and all those animal spirits pushing everything to the moon and beyond. Color me a cynic but if the Fed does cut then one could easily make the argument that the 2 percent inflation target is a complete fiction and that the real target is somewhere between 3 and 4 percent. Now if that is really what the Fed is trying to jam down our collective throats riddle me this….why would anyone buy a government bond with a maturity greater than 2 years? Now if that is the case then shouldn’t the yield curve start to go vertical here?

Unfortunately I agree – the Fed’s unspoken policy is letting inflation run above target to help the gov’t with its debt problem…

the Fed’s unspoken policy is letting inflation run above target to help the gov’t with its debt problem…”

I don’y buy that. All that would do is accommodate even more debt, rather than just keep current debt more affordable. Congress will spend and spend until it becomes too expensive too do so.

We desperately need a rate cut yesterday in order to support new all-time highs…OR ELSE. Our economy cannot function without new all-time highs. That’s the Wharton dood says. Santa might stay away.

Some folx on here make comments about how stupid consumers are, but the chart of personal savings sure looks otherwise:

GFC when RE prices were crashing, savings went up, then back down when economy began at least leveling off…

Covid and the chicken littles screaming world coming to end, savings went WAY up; then again, when world calmed down savings ”normalized” …

Seems that a lot of saving from covid era still around and folx either upgrading or replacing a lot of fridges, etc.

Good stuff Wolf,, thanks

“Seems that a lot of saving from covid era still around”

I think even the Fed’s measure of Pandemic era “excess savings” (that evil…) indicates said “excess savings” ran out in March/April of this yr.

1) The granular calculation of “excess savings” during the Pandemic should probably be reflected upon, since while I can understand that certain categories of outflow/spending certainly dropped (cruise/airline trips, for example), plenty of inflow/earnings categories also got the hell beat out of them during the Pandemic (18 months of hugely reduced economic activity/work).

How that nets out to trillions in Pandemic “excess savings” doesn’t seem like a slam dunk to me, unless somebody steps through it in much finer detail than has been publicized.

2) On a broader, related note, this brings up the ostensibly “evil” role savings (especially “excess savings”) get cast as in the Keynesian worldview. Keynesians seem to mostly view savings as sub-optimal “leakage” out of their perfectly meshed, perpetually recycling economic machine (actually a *model* of a machine…).

But if that Keynesian “machine” is doing something stupid/counterproductive/largely contingent upon borrowed external resources, then its “optimal operation” is not a win, and savings are not a sin/”leakage”, but the necessary margin for reconsidering/reconstructing a very flawed machine.

That theory of “excess savings” is BS. The fake theory was formed by a fresh-out-of-college staffer at the SF Fed, and that paper went viral. If you want to look at the actual savings, look at money market funds ($6 trillion), CDs and savings deposits ($10 trillion), checking accounts, T-bill holdings, stock holdings, bonds holdings, etc. That’s where people but their “excess” money, LOL.

S/B…”put” their excess money….they but(t) it over in the frozen desserts aisle.😂

Wait and see.

Lacy Hunt is quite adamant that looking at GDP at inflection points is misleading. We should be looking at GDI (Gross Domestic Income), which is dropping and much lower at 1%. This is the same pattern we see in every recession.

GDI has been revised up HUGELY last year, which destroyed the recessionistas argument, so they switched to something else. Now they switched back to GDI? LOL

GDI quarter to quarter is HUGELY volatile, so it increased by 3.6% in Q4.

And in Q2, year-over-year, GDI increased by 2.0%, adjusted for inflation, so that’s pretty good.

It’s the same BS day after day from those recessionistas that have said for two years that we’re either already in a recession or on the verge of a recession. GDI announced the recession in 2022, and it never came, LOL

Nah not high enough, we need an emergency rate cut now to juice these numbers even higher…/s

Here’s another data point why we don’t need a rate cut in Sept. Who knows, maybe Pow Pow miss Wolf calling him the most reckless FED ever and want that title back..

He’s has no chance of losing that title. He’s a hero for asset holders — nobody else matters.

Bernanke was worse.

I posted this another article. But it perfectly fits in here. Sorry for the repeat.

In 2023, all the MSM was talking about soft landing vs hard landing. Now we are living the third scenario: No landing: Ultra-inflated asset prices and crazy spending. There is little incentive for saving where asset prices are continuously (and artificially) fueled.

The drunkest sailor is the federal govt. FED cannot fight the prices alone with reckless govt spending. Stabilizing prices requires not only discipline in both monetary (reducing balance sheet) policy and but also fiscal (reducing budget deficits). There is absolutely zero intention about it. So, we have to live with reckless spending, increasing asset prices and increasing wealth disparity.

I think the sailors might be sober. Extra jingle in their pockets, locked in 3% real estate deals preventing moving, might as well upgrade the durable goods.

HELOCS are up and while the debt numbers seem to not show it, people ate spending money they do not have. Check your mail and spam. Notice the huge increase in approved loan offers and credit cards? There are indicators that people do not pay attention to but they matter.

If you get a HELOC and spend that money, you’re spending your OWN money (home equity), but you have to pay Wall Street to get access to your OWN money. When people are spending their own wealth, they’re spending their own money. What else are they supposed to do with their wealth? Take it with them?

Certainly don’t save anything for the grandkids!

Equity?

Like the equity homeowners had in 2005 right before the housing market collapsed?

Spending that ‘equity’ will turn you into a renter.

Yes, in a leveraged bet — stocks on margin or housing with mortgages — this can and does happen. It is now standard practice in CRE where landlords just hand over the buildings to lenders, or they’re taken from them via a foreclosure. Wealth is not forever. It can slip through your fingers like desert sand.

The sailors are definitely not sober. I just saw the captn crack a beer in the wheelhouse.

What, me worry?

I think the sailors are psychologically exuberant.

They have their low 3% loans on houses they mostly purchased over 5 years ago at low low prices (even though 2019 were high prices at the time)

Homeowners sleep easy at night knowing their beds are sitting on 100’s of thousands, if not millions of dollars in equity. That builds courage to spend like a drunken sailor, so they do with their higher wages.

If they were knowledgeable enough 10 years ago, they moved their savings from low interest savings accounts to boring stock index funds and made at least 500% return.

The responsible ones contributed to their 401Ks and also grew 500%. Retiring early is no longer a dream.

The future is so bright, you gotta wear shades.

The people who missed out were the people 10 years ago who couldn’t buy a house, invest in a 401K, or buys stocks. They suffered for 10 years with low wages and 0.01% savings accounts. Blame the Fed? How many people does this affect? 20-30%? They are in psychological despair with high inflation and higher rents.

It remains to be seen if the people coming of age now who buy a house, and invest in stocks will have the same outcome. I think they will but it may be 15-20 years before they see the same return. They’ll need patience and a lot of hard work to get there.

Unlike 2008, the economy is still driven by exuberance. Nobody has lost 50% on their house or stocks yet.

Not yet, but I am counting on it.

The stock market is bigger than the actual economy now. So, the performance of the stock market determines what happens to the actual economy. Tail wagging the dog. But this is the what we have now thanks to the Fed.

yes. people like to say “the stock market is not the economy,” but now it literally is. the entire economy is based on inflated asset prices. if asset prices correct, the u.s. is in deep trouble, as consumers spending would drop like a rock.

If this happens and the stock market reverts to mean, then even the partially deaf will hear the wallets snap closed. Nothing changes but the old circus tricks of QE and ZIRP would be like torpedoes through the US navy’s best ships.

exactly. so basically the wealth effect is holding up american spending, and making wealth inequality and social unease worse than ever.

The majority of Americans do not invest in the stock market.

What a lovely picture painted, everybody and everything are high as kites.

As long as the tax receipts in the US can keep up with our 35 trillion in debt we can “pork out” for a bit longer, but….no butts, from here on out drinks for everyone…

What a splendid crash it will be. Soon wolf can start a series of articles called “What happened to all my “g-d” money”.

@Home Toad,

“What a lovely picture painted, everybody and everything are high as kites.”

And it is *real* this time. In Orange County, California where I live, only 9% of the *households*, not individuals, have an income high enough to qualify for a home mortgage in the county. That’s according to The California Association of Realtors. And just about all the people with that income level already own at least one home.

Correction. 9% in Mono county, 15% in Orange county. My comments still hold. 85% of *households* don’t bring in enough income to qualify for a mortgage.

Apple – 61% of Americans own stocks. That’s a majority.

shorttlt, a good percentage of that 61% is due to an arcane provision of erisa that incentivizes employers to set 401k participation on automatic, meaning you’d have to opt out.

don’t think that 61% of americans are benefiting when stocks are pumped up. most of them don’t have enough to move the needle.

Yep.

Stock market capitalizations have nothing at all to do with the Federal Reserve and its policy decisions.

Hello SoCalBeachDude,

Pardon my polite incredulity. Is your comment “tongue-in-cheek”?

–Geezer

No.

SCBD, you’ve stated this before.

Have you ever looked to see who owns major positions in almost all stocks, macrocaps down to small positions in micro-caps – across the board? It’s all the banks, insurance companies, private equity firms, brokerages, pension funds… If the market cracks, so do these institutions.

Do you think the Fed ignores this?

Couple the above with the fact that the top 10% own 93% of all stock market wealth in the U.S., and the top 10% account for 2/3rds of the overall wealth in the U.S. It’s not hard to see there will likely be no recession without a stock market drawdown. Quite the upside down world the Fed has created.

The Federal Reserve has nothing whatsoever to do with the prices of stocks in the stock markets.

You always forget the /sarc tag!

Exactly what I stated is 100% correct. The ONLY thing that pushes stock prices up to absurd PE levels is mindless manic speculation in defiance of all reason.

SoCalBeachDude,

We have an entire generation raised on 0% interest rate “free money” magical thinking. Where do you think it came from?

Andy, that came from the bond markets, particularly the US Treasuries markets and is a thing of the crazy irrational past which was only around for a very short time.

US treasuries that THE FED, and other central banks bought, YES.

it’s not fed policies at this point, but investor belief that the fed will ride in to rescue any drop.

it’s not an unreasonable belief given americans’ belief in the magical money tree.

@Wolf

My questions would be so what if the spending continues if the inflation is coming down, has come down to 2 6%? We need to worry if the spenders are going to pass on the bill to the savers which according to this article is not. But perhaps savers do pay in one way because all these are possible due to free govt. spending via deficits, money printing of various forms by FED that has enormouslyboosted asset prices. Or savers can wonder if this inflation data is invalid because it doesn’t include data pertaining to inability to own a house, some stocks etc. If the FED reduces IR, it is going to make the hedge funds thriving on shadow banking system to go ballistic and cause more harm eventually but common person’s fate is sealed by the use of skewed or colored inflation metric.

LOL @ Drunkin’ Sailors.

Maybe: Stupid is as Stupid Does.

It’s a good metaphor. Sailors drinking on their boat is a stereotype for a reason just as American consumer spending is.

I see both all the time on my boat – sailors drinking, and passengers buying overpriced food & drink in the galley for a 90 minute ferry ride.

I feel a lot of the spending while drunken is also folks preparing for harder times/supply chain interruptions again ect.,i.e. prepping.

But by doing the “prepping” spending, they are making the hard times not come! That is good for all the “non-preppers”.

Jorge,as having personally gone thru a few natural disasters trust me,always good to prep.,even if needed only short term.

All the talk about birdy flu/monkey pox/new covid(flu strains)could easily see another lock down for our health and safety.

J

Lock downs are over…..for good.

Stop fighting the last war.

Lock downs are over?

People voluntarily lock themselves up in their homes/appt. (No need for a mandate). The kids stay in the room, locked up doing whatever. No need to go out…order it online…3 large pizzas with a soda. Then to top it off, without proper exercise and sunshine, we’ve become flabby, self-imposed “locked down porkers”. Over 40% of Americans are obese, let alone overweight.

But on a the bright side we got some money so we’re “drunken porkers”, splashing in the mud.

Apologies to those who are not porkers.

Hell Guys,

Right now lot of money is locked in Money Market, T Bills . short term bonds etc etc since the yields are good, above 5%.

If the FED is going to start cutting rates, won’t these money come out of the above instruments seeking yield , and get into asset markets thus increasing the asset market valuation ?

Right now, there is an argument when it comes to real estate investment that if one can get 5% plus in T Bills risk free, then why to buy houses for rent since cap rate does not make sense.

But with FED cutting rates, this risk free 5% t bills wont be available anymore.

And the insurance on your house and/or rental property doubled, as you or others pointed out — if you can even get insurance. RE has a lot of carrying costs. T-bills don’t. Here’s an example what can happen to house prices that cannot happen to T-bills:

Still taxed as ordinary income. You’re barely beating inflation.

If the price of your asset goes down, you’re not EVEN beating inflation. Inflation is a bitch. You get double-whammied, first by price declines then by inflation.

Put another way, about 50 years ago, I bought some BRK.A stock. it sits in an envelope, the same size envelope it came in. I would call it an investment. About the same time i bought a house; the deed sits in an envelope. however, there is a large box associated with that deed. Endless insurance bills, tax bills, repairs such as new roofs, new siding, new windows, new carpet, other flooring, drapes, landscaping etc. Endless costs associated with that second envelope. I call that my money pit. yes, one might make money on houses flipping them, might make it via prime rental property with the associated work and risk. For most folks, they are a losing proposition. But, still, a place to live.

Your paper stock certificate doesn’t keep you warm in the winter. It doesn’t keep you dry when it rains. A house does.

And that falling home is was very likely some bank(s) collateral/asset value and therefore some bank saver(s) account balance safety margin…(referencing the debate above).

BS. Most of these loans have been securitized into MBS and are held by investors not banks. And most of the MBS are guaranteed by the government, so it’s the taxpayers that are on the hook. Private label MBS are just a small portion, and they’re held by investors, not banks.

This bank-deposit fear-mongering is just stupid BS. Go do that on X.

I wonder, as a percentage of internet correspondence, “fear mongering” amounts to? 75%? Higher?

I wonder what… (left “what” out).

As Wolf mentioned, this is exactly why I’m not buying any more rental properties. Zero point in paying these sky-high prices when I can make more in cash flow each month than my rents after HOA fees, taxes, vacancy costs, repairs, insurance, etc. with essentially zero risk to principal right now. I would love to buy a few more rental properties, but it just doesn’t make any economic sense when I can park the money in ST bills. If money market rates comes down, then maybe I re-evaluate, but I need to see a corresponding drop in home prices.

I make more money each month selling covered calls on my portfolio than my buddy does in real estate, and that includes estimated RE appreciation. I spend maybe 3 hours a week and he spends 20..basically a second job maintaining three homes.

Not sure what he spends 20 hours a week on for only 3 properties. I might spend 5 hours a month on my properties.

the difference is he’s working and you’re gambling. it’s worked out for you so far, but eventually you’ll lose.

It’s nice to hear from a RE investor with an understanding of alternative asset classes and opportunity cost.

I think you are correct. I have a lot in 5% money markets right now and if rates drop below 4 then i will sell it all and look for yield. I know several friends who think the same thing.

With every asset class at inflated levels, where do you go for “yield”? When the Fed repressed rates, money poured into equities and real estate, chasing yield and appreciation.

Those prices haven’t declined much.

What’s for dinner, Grandpa?

In July from June, spending in the USA on durable good, nondurable goods and services all increased. No doubt about it.

Wolf, in your discussion with Adam Taggart, posted 26 August, you brought up the number of immigrants that have come into the US. This number, while somewhat of an unknown, could perhaps be 4% of the total population added into in the last couple of years (13.4 divided by 335 = 4%).

Is their a cause and effect from immigration to what we see in July’s spending numbers that would help explain this?

Granted, this immigration didn’t just happen from June to July, but these people are working and spending, no?

So the number I mentioned from the CBO was less than half that, 6 million in 2022 and 2023, which would be less than 2% of the population.

As Adam and I discussed more people means more spending, and it means more jobs, and more income, etc. But the new immigrants are generally neither big spenders nor big earners, so their contribution is at first marginal. Later, years down the road, they’ll be bigger earners and bigger spenders, but not yet.

Even if the new immigrants spent on average the same as the rest of the population, it would still be the same result: consumer spending growth. It doesn’t matter for the economy who does the spending.

What a lot of people don’t realize is that they are getting debit cards pre-loaded with taxpayer funds in the many thousands of dollars. This is yet another form of government stimulus, but largely hidden.

Source?

Depth charge was being generous and kind in only bringing up that small piece of apple pie given to the migrants, after all, they are valuable in many ways…

Is there a breakdown on this spending by income group? Something isn’t adding up to me. If people have all this money to spend and save at the same time, why are housing sales lagging even if prices are elevated?

Use your brain and it’ll add up:

“why are housing sales lagging even if prices are elevated?” should read “housing sales are lagging BECAUSE prices are elevated.” with elevated being the understatement of the year. This is not rocket science.

Sales of existing houses plunged because prices are way too high as potential sellers are clinging to those prices and are trying to wait this out.

Sales of NEW houses, sold by homebuilders, are BOOMING because builders have cut prices and they buying down mortgage rates, and they have figured this out.

https://wolfstreet.com/2024/08/23/inventory-of-new-completed-houses-surges-to-highest-since-2009-triple-from-2-years-ago-exactly-whats-needed-to-bring-down-prices-across-the-housing-market/

Here’s what I’m getting at, are the people that are priced out from buying a home not even saving for one and spending money on other things instead? These people most likely being 25 to 40.

Yes.

For the most part, they can’t save fast enough to even get closer to the target. So go buy stuff and pretend you don’t care about not owning.

OMG, YES!!! Look at food, energy and services (insurance) inflation!

PRICES ARE TOO DAMN HIGH, and STILL GOING UP BY AN AVERAGE OF 3% (CPI).

The average Joe/Jane needs DEFLATION.

The media (propagandists) want you to celebrate a 3% RATE OF CHANGE….

WTF? UNAFFORDABLE prices means people CANNOT buy. Nevermind unaffordable prices going up by 3%!!!

Prices need to return to pre-pandemic, but they will not.

Interesting times.

Where does it say income is down? I had to go back and read it again but I’m not seeing it

Yep immigration tbill interest stock cap gains house equity falling durable goods all lead to more spending !! My neighbors just purchased a new Ford Class B conversion camper van . They picked it up at factory and paid 165k not sure about taxes etc, They are 72

Their next of kin will be selling it for $75K in a year or two.

Also not sure that as retirees get a bit older and are in the 65-75 age range spending accelerates if they have the cash !

Are you serious? I am 70 and I spend less than I ever did. I have everything I need in the way of material possessions. My spending is limited to food and utilities along with insurance and property taxes. My property taxes are $400 and the condo insurance is $500. A year.

Wow.. that’s cheap

I wonder where do you live 🤔

I live a minimalist life so my expenses are low as well

I have no desire to prove anything to anyone

No desire to impress anyone and this saves money and give me freedom

Jon, I think yours is a geezer’s mind-set: frugality because you don’t really give a s**t what others say. Personally, I find it very gratifying to be stuck in traffic with a Lamborghini standing stationary, right next to my car.

ESCIERTO., At 70 you are still young yet. Your spending on health care is set to increase in 5..4..3..2…..

Oh, and Social Security adjustments do not come close to matching the ever onward march of inflation. And medicare does not cover everything.

Most medical spending occurs in the last month of life.

Actually, when you’re retired and you’ve been frugal, it’s HARD to get yourself or your spouse to just go out and spend money.

So our expenses are less.

Not paying for work lunches or dinners. Not paying for nice ‘working’ clothes.

Yes, our healthcare costs have gone up. But Medicare and Medicare supplements pays almost all of that. Our total monthly healthcare insurance premiums are less than what we paid for our company plans.

We do spend more money spoiling our adult children and especially spoiling our grandchildren.

Obviously … YMMV.

Wolf,

Why not set a trend line for personal income? That would also be interesting to see. I can pretty much guess where it is, not pretty.

I would like to see the spending and income statistics per capita.

Wolf,

Thank you for another report on facts. It is painful to see our country on this path.

Would you Pls consider a report outlining countries with lowest debt, budget deficits, positive trade balances?

If this is outside your scope, can your Pls recommend good sources where I can find this info with hopefully reliable/objective analyses?

Thank you & pls keep up your good work

Was this posted under the wrong article?

Because I don’t get this comment. Why is “painful to see” that Americans are making and spending money? What else should they do? Not make money? Not spend money?

What they should do is to not spend more money than they can pay in full in a reasonable and prompt term of time and they should not waste time trying to ‘make more money’ without careful consideration of the costs and risks of doing so.

it’s painful to see things that are unsustainable.

What’s unsustainable? That Americans are making more money than they’re spending?

Franz may be referring to the continually rising debt-to-GDP ratio.

It begs the question – what would current economic growth be if the country were forced to keep debt growth in line with GDP growth.

Also, what will society be like in 10 years if wealth concentration continues at its current pace?

Spend it before it’s worthless.

How much of this spending is by the boomer generation? My wife and I are retired and while we are not rich we were able to retire with sufficient retirement funds. We have our house with a smaller mortgage at a low rate. We do notice the increase in services but our retirement funds are growing at a faster pace. We have commented that it would be difficult to be raising a family in this inflationary environment.

The big earners and big spenders are the Millennials (biggest generation ever) and GenZers that are equipping their new homes, buying stuff, starting families (very expensive!), going on fancy “experiences” for vacations, etc. That’s the driving force in the housing market, ecommerce, motor vehicle sales, etc. all of it.

Howdy Lone Wolf. Drunken Sailor Articles make some of US so proud. Squirrels are loving life, still saving more $$$ than they spend, still making more $$$ than last time, still spending more than last time. YEP, no matter what they try and do to Squirrels, we keep living the dream……

Does the savings rate include pension/401K savings?

The savings rate is the difference between disposable incomes (incomes after taxes and social contributions) and personal consumption expenditures. I’m not 100% sure about pre-tax savings deductions, such as HSAs and 401ks. Disposable income is supposed to reflect a version of take-home pay.

What are the chances CPI-U comes in hot in September

Pretty good.

Are you referring to the August report that will be released a few days before the FOMC?

Yes

So spending on durable goods and nondurable goods remains above the pre-pandemic trendline, and spending on services is finally catching up to trendline. Meanwhile, personal income less transfer receipts is beginning to take a hard right on the graph above, falling increasingly below the pre-pandemic trendline. More and more spending, and less saving. I don’t see how anything could possibly go wrong if we keep this overall trend going.

“If the homework brings you down, then we’ll throw it on the fire, and take the car downtown” — David Bowie, Kooks

Well, it’s a good thing the Fed is here to tamp down on the exuberance by clearly signaling rate cuts soon!

America’s Navy of Drunken sailors is the best in the world. Armed with credit cards, HELOC’s, 96-month truck loans and cash-out refi’s, they have proved to the world they are masters at ignoring reality.

Maybe the USA’s sailors have grown to implicitly (if not even consciously) expect a bailout? By government, or sheer luck, or divine favor?

How are buy-now-pay-later sales accounted for in retail sales?

If the sales prices are being booked as earned revenue this may be significantly distorting the view.

I just read somewhere that credit card companies are refusing to allow their cards to be used to pay for BNPL purchases, because they are a stealth path to going beyond the credit card balance limits.

1. This is consumer spending (personal consumption expenditures), from the consumers point of view; not retail sales, which is from the retailers’ point of of view.

2. Consumer spending has zero to do with how it’s paid for — whether with crinkled dollar bills, debit cards, credit cards that are paid off by due date, check, money order, BNPL…. You’re talking about a “payment method,” not spending.

Everything is up and people are having a gala time. But then there are a few of us, who got a steady job but haven’t seen any of these great richness. We struggle managing our finances. It appears that feds intervention following the financial crisis were a master stroke, eventhough some of us are still struggling. But majority of people are doing good and there is no financial downfall in near sights. Still doesn’t understand how government’s manage to intervene and still leave the financial sector without any significant negative impact in long-run.

As long as enough people are doing OK, that would seemingly be the sign of a successful economy? And if it all tips over, as it did in 2008, I note that, back then, though I’m not in the rich financiers’ club, I had a 30-year mortgage in a market more or less held above a certain floor by government, and the spending that was done seemingly kept my job going (despite my losses on stocks, which in fairness I could expect). If it all tips over, the spending trough would be re-opened, and most of us would presumably not starve, as we didn’t, that time. Yes, I am being very careful with money, but I don’t see unfairness in that. It helped me focus on a healthier better diet and lose 25 lb.s this summer! I have no jealousy of people blowing the money they have.

The key problem is financial authorities currently don’t care about the dispersion of income and wealth. They care only about the aggregate economic result.

Take the savings rate of 3%, for example. Very few people save 3%. The bottom 50% likely has a negative savings rate (spending more than they earn) while the top 10% might have a 40% savings rate (just guessing).

Wealth concentration is at all-time highs and getting worse, and that is a major source of social discontent and bewilderment. It gives many people the feeling that something is rigged. They wonder who has the financial capability to buy these things. They are repeatedly told the economy is fine, and they see shiny new cars and trucks all over the place, but their individual circumstances might have deteriorated significantly, particularly if they are renters or new owners of an overpriced home.

Home Toad had a few interesting facts (hopefully, they’re “facts”): That a small percentage of the residents of some heavily populated counties in California can actually afford the median home price in those counties. Even here, in NC, there are many, many multimillion dollar houses – near lakes, the coast, views of various types, major metros.

With AI likely to take out most “analytical” jobs (accounting, consulting, even IT and software developers, for e.g.), who the hell is going to keep these inflated home prices aloft?

was/were…got/have…good/well…sight/sights….

exactly how are you struggling?

would americans be making more than they’re spending if the government wasn’t pumping $2 trillion of deficit spending into the economy every year? how much of that ultimately ends up in the hands of consumers to juice spending and gdp?

The economy has normalized, yet we need $2T deficits to maintain employment. Artificial monetary and fiscal stimulus is here to stay, along with elevated inflation. There is a need for political cover, so elevated inflation may come in the form of periodic step ups in response to crisis, like we witnessed during the pandemic.

This bubble is much bigger and longer lasting than past bubbles. Why? Markets now know that QE and money printing have been used to avoid recession. These tools weren’t imaginable in past bubbles.

Bernanke changed the world by reneging on long-standing social and economic contracts.

agree with this. americans wouldn’t tolerate 5% inflation every year, so instead it’ll be 2-3% most years with a few years of 8-10% during every self-interested fed emergency. look how many people say that powell and lagarde “saved the world.”

people actually believe this crap. that must be why there are so many investors willing to buy long treasuries.

The good news is they likely only have a few bullets left in the QE gun. After 2008 and 2020, bullets are running low. I assume investors who lost 40% on long bonds during the pandemic will be less willing to buy them in the future. Even diversified investors might choose to hold fewer long bonds.

I definitely will not be holding any long bonds for anything more than a short term purpose. Even then, I’d have to think hard about it.

The level of risk thrust on the economy by monetary and fiscal authorities is mind boggling. They are pushing it to the brink. At some point, there will be a massive deflationary event. The question is how much inflation they hand us in the meantime.

Speaking of people believing crap…

“Bernanke changed the world by reneging on long-standing social and economic contracts.”

That oaf got the Nobel to show for it too!

No. All of it.

Rough TA of both durable and non-durable goods is a “rising wedge” reversal pattern. Stocks look like they’re gonna implode and the longest negative yield curve in human history is consolidating to finally go positive. As The Big Good Wolf tells us ☺️, Real estate is in a massive bubble. Oil is forming a hard bottom – in spite of gas prices not coming down concomitantly. We’re I’m unprecedented conditions, and unprecedented conditions create unprecedented corrections/crashes.

For your speakers : Mendelssohn violin concerto , Maxim Vengenrov, Antonio Pappano, Rome.

Thanks, Michael.

If this ends up without a cut on Sept 17, I will be eating a lot of crow.

That would be hilarious. It would be a worldwide crow-eating party. All of Wall Street would stand in line for days and weeks to eat truckloads of crow. There would be such huge demand for crow that the world would run out of it, and there’d be a worldwide crow shortage.

It’s hard to believe there’s any left considering what has already been eaten this year. There is a reasonable chance of no September cut. Even a broken clock is right twice a day.

Not to worry. I’m sure there’ll be a technical fix for the shortage: Impossible Crow.

Ethereum crash alert: Why ETH might plunge to $1800 soon

November 5th results and the hype-meister loses?

BC has been stuck around sixty K for a while but a ponzi or chain letter has to grow, it can’t just sit.

As for a store of value the old ‘shiny rock’ has done better YTD. BTW: the Bank of International Settlements recognizes gold as a ‘tier one asset’ It’s not just money it’s a super money.

Saw a bit about banks waiting for a new coin?? Aren’t there already a bunch? No point waiting for a new precious metal. They are elements. But plutonium is a precious metal and an element created in reactors, so it’s a relatively new PM. Has a nice glow to it, literally.

I have a buyer if you have some.

– Whether or not an economy is in a “recession” can be very easily seen. Then one simply has to look at what happened with the total amount of debt. Don’t look whether or not the total amount of debt grows or shrinks but look by how the growth rate of debt grew or shrank. E.g. when in one quarter (total) debt grew by say $ 10 billion and the next quarter debt grows by say $ 18 billion then that is a sign an economy is growing. If in that next quarter the debt grows by “only” $ 5 billion then that economy is “contracting”.

Nah, the debt is a result of issuance of new debt minus maturing old debt. The debt is predictable on a quarter-to-quarter basis because the Treasury Department releases its plans on issuing new debt; and we know from the maturity schedule what’s maturing and coming off the debt.

During the debt ceiling period, the debt doesn’t grow at all for months, and then when the debt ceiling is suspended, the debt suddenly spikes.

None of this says anything about a recession.

The flat parts are the debt-ceiling periods: