Our pantheon of Imploded Stocks is weighing down the Russell 2000 index.

By Wolf Richter for WOLF STREET.

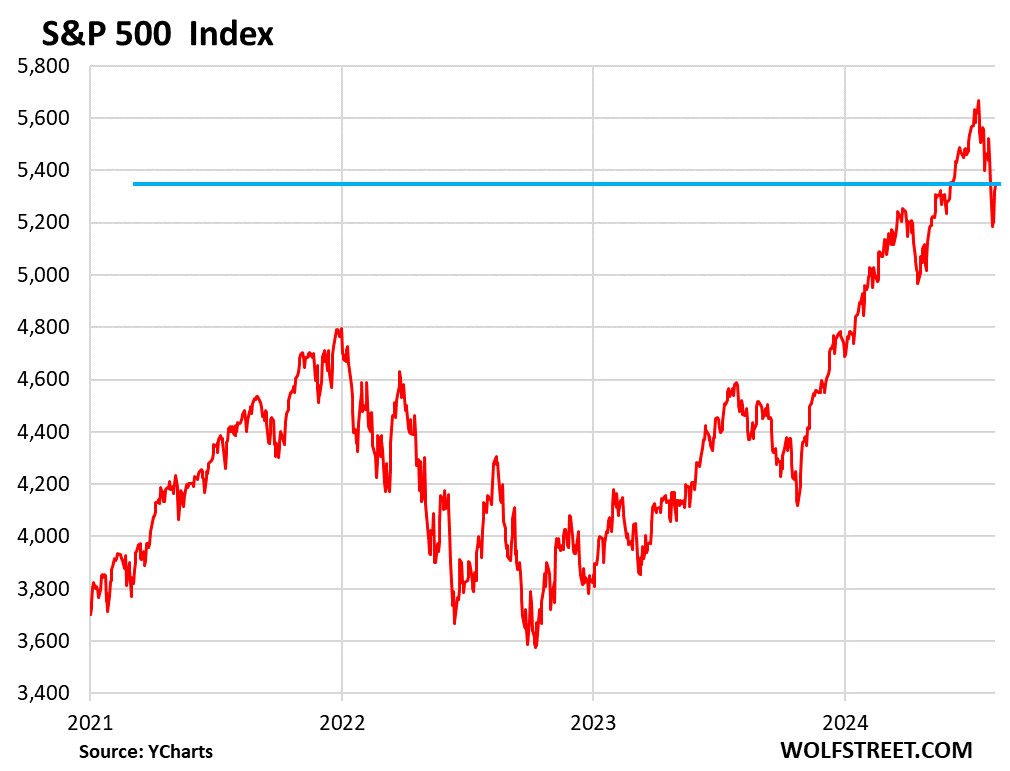

The S&P 500 ended where it had started out, and if you were away from the internet for those five days, you would have missed all the drama that had started out with the Nikkei plunging 12% on Monday, triggering a whiff of panic in the US markets that then quickly faded.

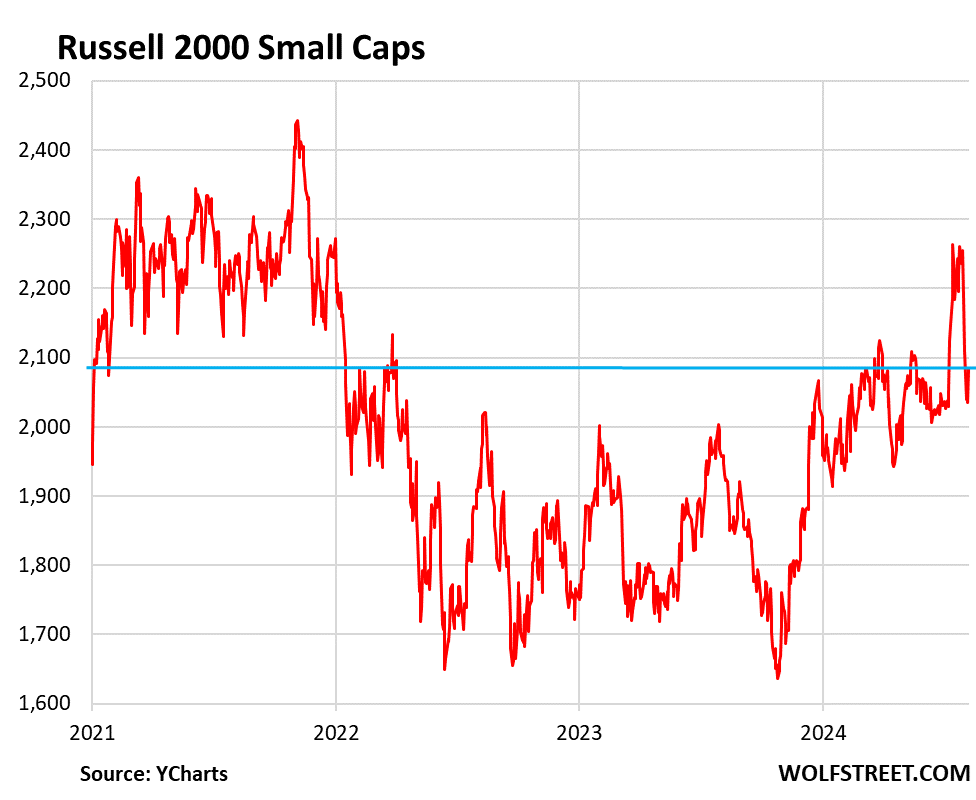

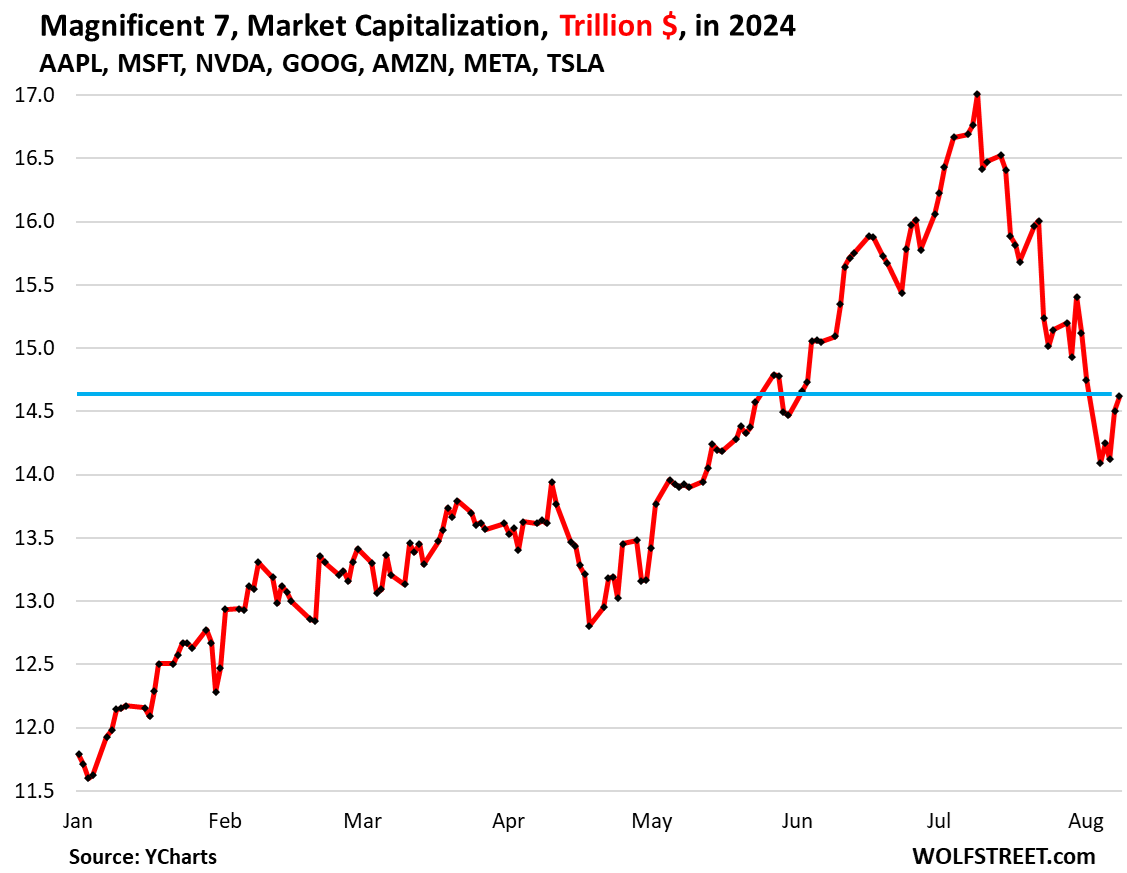

But not everything undid the Monday drop. For the week: The Russell 2000 small caps index -1.3%; at the other end, the Magnificent 7 (Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla) -0.9%. Meta had a great week, +6.1%. The Mag 6 without Meta: -1.5%, dragged lower by Tesla and Nvidia.

The S&P 500 Index, after all this drama, ended the week essentially unchanged at 5,344. Since the July 16 high, it has dropped just 5.7%, and it’s still up 12% year-to-date:

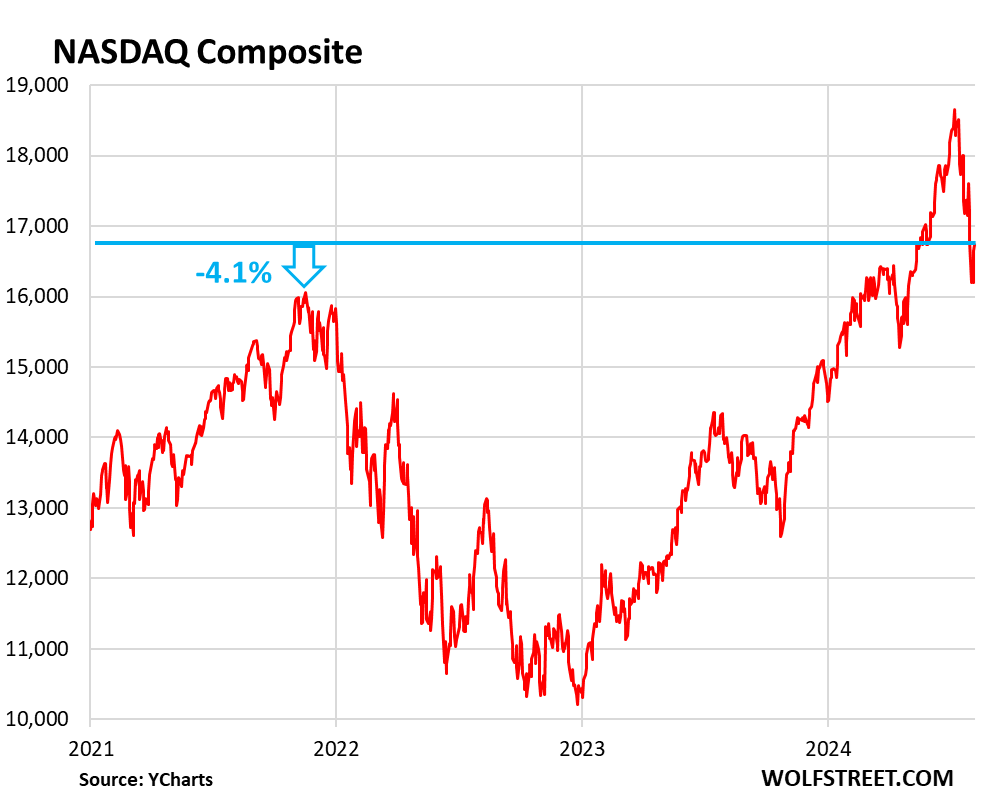

The Nasdaq Composite edged down just 0.2% for the week, to 16,745, which left it down 9.5% from the peak on July 10. Year-to-date, it’s still up 11.6%.

But the Nasdaq gives us a headache. If it drops by just 4.1%, it’s back where it had first been in November 2021, with a 36% plunge and a gigantic 81% rally to the all-time high in between. That sure was a lot of drama for nothing. T-bill and chill?

The Russell 2000, which tracks the 2000 smallest stocks in the Russell 3000, has been handicapped by the stocks that have collapsed since February 2021 – largely the super-hyped IPO and SPAC stocks that were born out of the pandemic and that are now packed like sardines into the cheap floor of our pantheon of Imploded Stocks.

Many of the stocks went from IPO or SPAC merger in the free-money era of 2020-2022 to zero or near zero by now. Many of them had valuations of billions of dollars or tens of billions of dollars, and there may be 1,000 of them by now that have collapsed by more than 80%, including such standouts as Blackstone’s epic pump-and-dump Bumble (-94%) or the winemaker PE-firm rollup SPAC that is now being liquidated in bankruptcy court (-100%).

Many of these stocks were in the Russell 2000, and their implosion – despite many other small caps doing well – is causing the Russell 2000 to be in such crappy shape, while the S&P 500 has soared and spiked from new high to new high – well until July 16 – because almost none of the imploded stocks ever made it into the S&P 500.

People have lost their shirts, trousers, and socks on these stocks when they emerged from Consensual Hallucination, as we’ve come to call the phenomenon. And those stocks have been weighing on the Russell 2000.

The Russell 2000 is now back where it had first been in early January 2021, so that’s 3.5 years ago. For the week, it was down 1.3%. That immensely hyped “rotation” into small stocks only lasted a few days:

At the other end, the Mag 7. Despite Meta’s great week (+6.1%), the bounce of the Mag 7 didn’t quite make it back to Friday’s close. But it was a good effort, thank you Meta [META].

Since the July 10 all-time high, the combined market capitalization has dropped by $2.34 trillion, or by 15%. They’re now back where they’d first been on May 24. That a $2.34 trillion plunge spread over just seven stocks sets them back only a few months is in itself astounding, and testimony of the crazy times, fueled entirely by the great AI bubble.

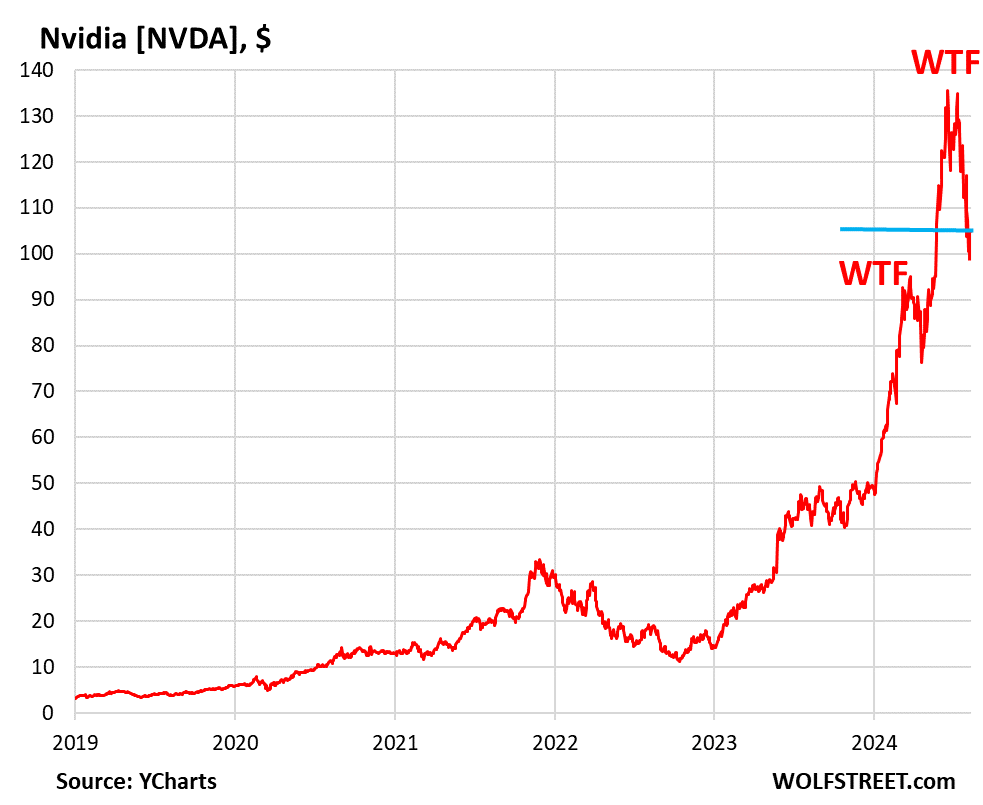

Nvidia [NVDA], briefly the most valuable company in the world, has now dropped by 22.3%, or by $741 billion in market cap, from the all-time high on July 10, and it is producing a fascinating chart.

Good lordy if Nvidia ever says anything about demand being somewhat “lumpy” – a term with which John Chambers, the CEO of Cisco – the first company that was supposed to reach a market cap of $1 trillion while riding up the dotcom bubble – had kicked off the dotcom bust. Cisco’s market cap is now just $183 billion.

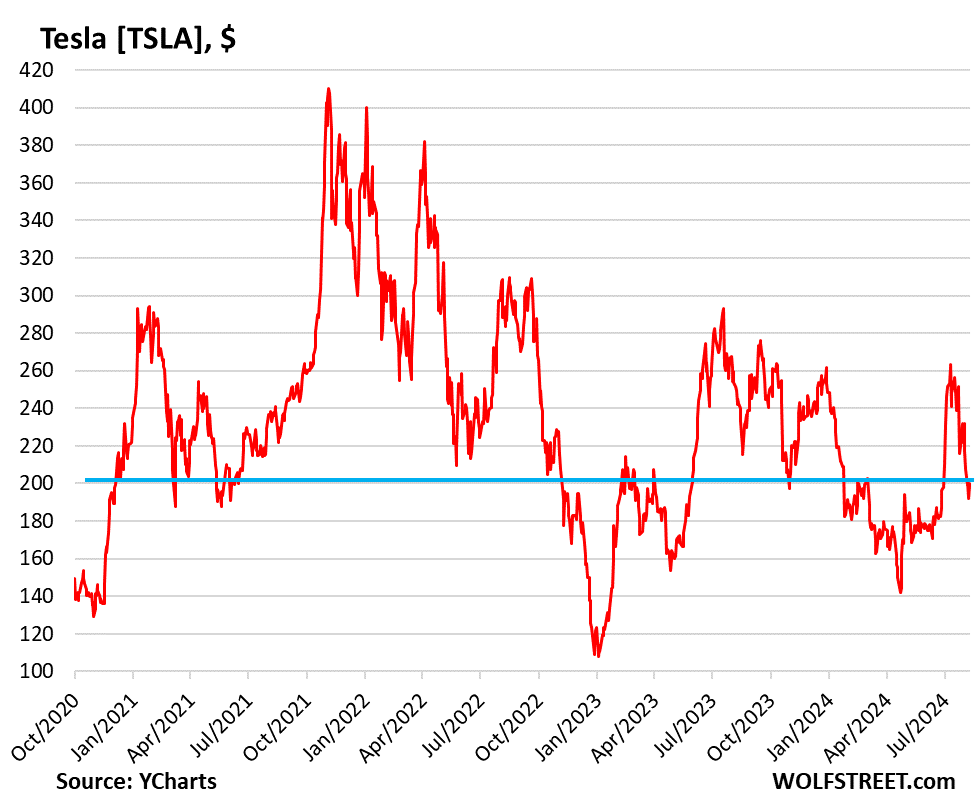

Tesla [TSLA] is at the other end of the Mag 7, in terms of the gain since December 2020, which is zero. From the peak in November 2021, Tesla has plunged by 51.7%. For the week, the stock dropped 3.7%. The little bounce over the past few days is barely visible:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

TBill and chill bro! lol

That needs to be a T-shirt.

Haha that is a great t-shirt idea, with a big wolf street logo on the back

Chill and t-bill, two alley cats in search of yield.

Doom and gloom, two other ally cats laying in wait.

Yep. I expect the uncertainty to continue until the “election”.

That’s funny…none of these charts shows the sky is falling to a point we need emergency rate cuts now…hmmm something doesn’t add up and I don’t smell what the Rock is cutting here /S

Btw, Nvidia is still a $2.5T company and this headline is still the reality in our sky is falling apart economy “$1 million starter homes are common in more than 100 towns in America, Zillow data shows” Let that sink in how out of whack things are..

If I could get a cool million for my newish south Texas starter home, I would be moved out by tomorrow.😊

Why? Getting a little warmer and wetter….or just bad neighbors?

I really couldn’t stop laughing early last week at the bozos coming out in the financial press saying the Fed needed to step in immediately for a 75 bps emergency rate cut.

The financial press is subtly (and not so subtly) influenced by megatrends that seem like revelations if you’re in the industry, voodoo if you’re not. They’ve probably consulted their crystal ball and gone aha! one time too many in a drunken stupor.

Just as realtors always say it’s a good time to buy, Wall Street always says it’s a good time for rate cuts. A stock market swoon, sunspots or Groundhog Day, any excuse will do.

If (when) Nvidia falls 70% from the top, it would qualify for Wolf’s Imploded Stocks list, and still be a Trillion dolllar company.

Well yes that would be interesting but it’s never going to happen. Nvidia is the key to everything. Sooo many mutual funds own 5% or more as their largest investment.

Microsoft is all in on Nvidia, heck even Palantir is loving Nvidia.

I see calls for it to go to $200 next.

I remember being at an annual family holiday gathering where the topic of conversation was how high Nortel would go. Almost everyone was in it, some in a big way, and it was about 60 at that time.

I said $2, and got The Dismissive Look.

At the next gathering they were at various levels of the 5 stages of grief.

Sell ’em when they’re yelling.

Buy ’em when they’re crying.

Words to invest/trade by…;)

I wish you could give us a timeframe for $200 print.

Microsoft loving NVDA?

I assume they are developing plans to replace them as we speak. Same with Google, Facebook, and Amazon.

There are no friends in business.

Young,

If we do not have a recession, I would say it hits it next year maybe late June?

A stable 200 base? Maybe 2027 in February.

Let see how this ages! Haha

Stock prices don’t care about love, they care about the growth rate of love.

If Microsoft and Palantir and others “Love NVDA” even 10% less next quarter than this quarter, what happens to NVDA’s stock price?

Patience. Don’t know about a 70% drop, but a 50% has a probability of 50:50.

I’ll bet there are some interesting options bets out there. It’s all a little too rich for my taste. I thought I could act like a trader. Once. I’m happy I just sat still this week.

Same. But even when I go to Vegas, I see some shows and do people watching on the gaming floors.

Since the July 16 high, it has dropped just 5.7%,

With “just” being the operative word, of course.

Howdy Folks. YEP 28 day TBills and watch the show. If and when the FED lowers, stay the course. Greenspan could re emerge.

DFB,

I think you should point out that the age of the investor is an important element of strategy. If a person is young, then dollar cost averaging in to an index fund is a better way to go to gain wealth.

Based on experts, such as Hussman, who analyze fundamentals or valuations, dollar cost averaging is not a good deal right now. Over the next 10 years, the probability is high that the big indexes that people DCA into, such as the spx, Dow, etc., will have a very low or even negative return, similar to the period after 1929 or from the mid 1960s to the early 1980s, but his articles explain it a lot better than me. I think this should be communicated to employees automatically contributing into 401k target date funds.

It’s great this guy has a crystal ball that shows him the future and he’s willing to give this knowledge away for free.

sounds like you’re making the perfect argument for dollar cost averaging: i.e., there’s a high-but-unknown chance that indexes will have a low-or-negative return for an unknown number of years.

Absent a crystal ball, DCA investments during this period will increase the rewards when the (supposedly inevitable) upturn happens.

What is the alternative… hold all cash and try to time the market? great idea for some people but not ordinary people.

I think he’s using mainly the discount cash flow analyses by Graham and Dodd and how many stocks or indexes have performed over a long period relative to their fundamentals, so based on real data. The valuations could become favorable fast if prices fall a lot or maybe if earnings rise a lot. You start to dca or more when the valuations are a lot better, not now. Better prospects investing in t bills until then. Agree most ordinary folks are probably unaware so someone should tell them not to listen to the always bullish wall street hype that they generously give us.

Don’t put all eggs in one basked. Young people need money for housing downpayment too – maybe even more than saving for retirement.

As a young person about to start a family, I tried both Index dollar-cost-averaging and “House Downpayment T-Bills” in 2001-2007.

Did fine on both, but the House Downpayment T-Bills led to a house, which then did as well or better than the stock market AND gave me a nice place to live for over a decade.

Hard to call Nvidia an imploding stock (yet?). There may be more waves up. Earnings in a couple of weeks. That’s when the real fireworks start again. Hard to predict.

To qualify for a place in the Imploded Stocks pantheon, the stock needs to drop at least 70%. Tesla made it in late 2022, but then in 2023 went on temporary leave of absence.

It would be interesting to see how many of the Russell 2000 are profitable – historically (well before SPAC-a-rama) a shockingly high number – like 500+ – were losing money. And that was a pretty consistent number – year after year after year (although maybe not always the same 500+) – it was such a high percentage that the cooked PE ratio for the Russell 2000 (defined to exclude money losing companies!) was a dangerous joke.

Post SPAC-a-Rama, I wonder how much worse it is…and how many SPACs/SPAC spawn make up the Russell 2000 today.

At their peak, there were hundreds and hundreds and hundreds of SPACs.

Many shut down and returned the money to shareholders…but plenty have SPAC spawn and those are likely to be money losers too. I wouldn’t be shocked if 30%-40% of all Russell 2000 companies have negative earnings for 2022 and/or 2023…and things are looking darker for 2024.

Russell 2000 are small companies no one has ever heard of. Heck their Bank’s prob don’t even like them. And you want to put your $ there?

😆

Are Russell 2000 entrants and SMEs the next zombie foot to fall after commercial (chimerical) real estate? If they are this precarious, a rate cut could be too little, too late for them. (Wolf’s facility with data is so terrific!)

Not all companies can be or want to be huge. That doesn’t mean they’re not profitable in their own arenas. Why this big obsession when it isn’t either reality or suitable for most companies?

On the contrary, the Russell 2000 has a lot of household names in it. More importantly, it has the early phases of all the growth stocks you want to get to know BEFORE they rise into the S&P500… as well as Wolf’s Imploded Stocks. The challenge, of course, is figuring out which is which!

Carvana

Super Micro

Sprouts

E.L.F. Beauty

Abercrombie & Fitch

AAON Hewitt

Meritage Homes

KB Homes

Dillard’s

Beacon Roofing

Madrigal Pharmaceuticals

Boise Cascade

Shake Shack

American Eagle Outfitters

Hilton Grand Vacations (didn’t realize this was a separate stock!)

Atlanta Braves (didn’t know they were a stock either!)

Energizer

Yelp

Foot Locker

SkyWest Airlines

WD-40

… which reminds me of an old investors’ adage: “never invest in a tech company you’ve already heard of”.

I hear energizer has a bit left to give!

😆 🥁

On a trailing 12 month basis, 42% of the Russell 2000 generated a net loss.

Thanks, Kile.

(Very useful info that probably took some work).

My guess is that that metric would shock the hell out a lot of retail investors.

And a decent guess is that R2K money losers *stay* money losers – ending up bought out or going to bankruptcy.

And yet the R2K index numbers don’t seem to reflect this over a period of years.

I wonder if the R2K’s cap weighting really obscures/ignores index members that implode one way or the other.

(That might be a defect in *all* cap weighted indexes – leaving raw returns out of it, it would still be useful to know if x% of index members implode within x years. It is possible that Mag 7 madness obscures a lot of ugly business on the ugly end of the SP 500 cap weighting table)

As the Swamp predicted a few weeks back, Tesla will be making it into Wolf’s list of imploded stocks along with the rest of the garbage that resides there. The Tesla chart looks god awful.

But Teslas are everywhere on streets, everywhere…I’m confused…

It’ll go back up. They just love to revel in bouts of “told you so”. I mean I can’t say that I don’t as well. It’s just these are the best companies on earth. Their stocks will rise.

Doesn’t TSLA need protectionism, to survive in the USA? Ironic, given some Musk’s pronouncements about government, and involvements with China. Because my impression is, there is a $12,000 (non-Tesla) EV out there from China waiting at a port to ship, that I can’t buy.

@phleep,

That’s the same protectionism that covers GM, Ford, & Stellantis and American pickup trucks have been protected for decades. Not saying its good. I’d like one of those $15k Chincom EVs too.

Such assurity on the “to big to fail”

Mr sufferin.

My girlfriend and I were golfing and were teamed up with a 12 yr old girl and her father, me being a good golfer and thinking these two would slow us down on the course…Well the girl was phenomenal, she was a superior golfer competing in a junior regional tournament, I thought I was to big to fail, when in fact in my thinking I was to small to succeed.

Tesla cars are pretty good and I have one.

I am a fan of tesla cars and evs ate made cool just because of tesla.

But their stock valuation is too rich and would cone down to earth over time

It does not make tesla a bad company.

Where I live the Chinese still drive brand new white Mercedes not Tesla’s. With the Chinese its always either or but never in-between.

Just because those cars are visible in some areas doesn’t mean the company is either profitable or sustainable, does it?

SoCalBeachDude,

In terms of Tesla, it’s very profitable. It’s Ford and GM that lose tons of money on their EVs. Rivian too.

The Tesla PE Ratio: 56.18 for Aug. 9, 2024 and a normal car company should be around 6 making Tesla vastly overpriced and if it didn’t get government subsidies their profit would fall very dramatically from where it is now.

Tesla being worth more than Toyota doesn’t and will not ever many sense. I like EVs. I own one. But it’s still a car, not space magic. Tesla being valued like a car company makes it an imploded stock.

Once the tax credit subsidy is eliminated on Tesla’s and the Mexican plant that is building EVs starts shipping $11,000 EVs across the border it will be game over for Tesla. It will also be game over for most of the jobs of workers in the UAW who are employed building ICE vehicles and higher priced EVs domestically. The UAW endorsed this disaster by supporting the party that allowed this to happen. They will see their jobs eliminated and outsourced to Mexico. I won’t shed a tear for them when this happens.

“Once the tax credit subsidy is eliminated on Tesla’s … it will be game over for Tesla.”

The original $7,500 tax credit expired for Tesla at the end of 2018. Smaller amounts applied in 2019 during the phaseout. Tesla buyers got no federal tax credits in 2020, 2021, and 2022. And during those years of no tax credits, Tesla had its biggest sales success ever and became very profitable.

2020 was its first profitable year. Net income (GAAP):

2020: $690 million

2021: $5.5 billion

2022: $12.6 billion

2023: $15.0 billion

Tesla sits on $30 billion in cash and has only $2.7 billion in long-term debt (owed the government of Shanghai for the Tesla plant) plus a long-term lease obligation on the Shanghai plant of close to $4 billion). So it’s not going out of business anytime soon.

In 2023, the new tax credits came along to boost Ford and GM (union shops). The Biden administration hates Tesla (non-union), and everything was done to promote EVs from Ford and GM, including Biden’s personal involvement and test drives (Ford EV pickup). He never even mentioned Tesla though Tesla was the only US company that actually mass-produced EVs. It was all about Biden trying to buy the union vote. This was part of the reason why Musk is so pissed off about the Biden White House. Most of Tesla’s Model 3 don’t even quality for the new tax credit.

In terms of competing with other EVs, Tesla would be far better off if the tax credits were scrapped altogether. It’s still the only profitable US EV maker.

That said, the stock should trade like the stocks of automakers, with a PE ratio of 10 (slow growth) to 20 (rapid growth). PE ratio is now 56, based on the past four quarter. But income has dropped in Q1 and Q2 due to the price cuts, sales declines, and Cybertruck ramp-up.

To get to a PE ratio of 20, if Q1 and Q2 income continues, would mean a share price of about $34 a share (compared to $200 now). Then it would be valued like an automaker.

Obviously, the Tesla stock promoters will say that Tesla is NOT an automaker, it’s AI plus humanoid-robots maker plus robotaxi maker plus semitruck maker, plus whatever. But Tesla doesn’t have any of these things yet (while Waymo already has robotaxis). So to me, Tesla is an automaker, and it should be priced like one. And someday, it’s going to be priced like one. It’s already halfway there.

Wolf, Good comeback. Thanks for the clarity on these matters.

“supporting the party that allowed this to happen”. NAFTA was negotiated by Bush and signed by Clinton. The agreement ratified in senate + congress with bipartisan support from both chambers.

I think you’ve been brainwashed by someone into believing “the other side is the bad guy” on NAFTA.

It’s a liquidity darling and the multiple it and many high flyers trade at is absurd, there is no way they can provide enuf guidance to not drop by 40% at some.point, there’s already skepticism on continued AI spending.

I run a law firm and everyone is trying blow AI up our orifices but I don’t see any concrete uses for my business. People will grow skeptical.

AI could help you find accident victims.

Ha Ha. You must be kidding. Or indulging in wishful thinking……

I can’t think of anything AI (massive memory and information retrieval speed….like simple recurring verbal notions with Latin or Greek names. And “case law” or “case at hand details”….Even going back to Greek thought (or even Sumeria if relevant to “creating arguments”) is better suited for. And unlike most attempts at understanding the physical world, Law is ALL manmade.

How many pounds of law books ya got at your “Firm”? How much paperwork? How many secretaries and para-legals? What does an expert witnesses’s collection of “knowledge” cost? How fast can juror info be collected and “Monte Carlo’ed”

Better have a lot of TRUSTWORTHY connections. When is the last time you took a local judge on a fishing trip to the Caribbean? I KNOW you can’t afford a SCOTUS judge friendship like C Thomas’.

Intel corp has had a greater fall than Cisco, going from 508 billion $$ to now $84 billion! Their failure in the foundry business, even with the 10s of billions of gvt cheese, is the root of their problem!

Intel is a another perfect example of a company that has its head so far up its A$$ they forgot what daylight is like. Constantly antagonize their loyal customer base in the PC world with shady greedy tactics that eventually piss off most of their customers. Them and Boeing have a lot to learn from each other and I have a feeling the big 3 automakers will be joining them soon enough. The big 3 also do a good job at gaslighting and antagonizing their own customer base

Intel 1980-2024 is like General Motors 1960-2009. They’re still around making a bit of money..with 1/4 the market share they used to have.

Intel had a $0.38/share loss in their last quarter. So at the moment, not quite “making a bit of money”.

Mediocre car manufacturers can always find a place in a crowded market with some combination of styling, features, price, and brand loyalty.

Semiconductors on the other hand mostly boil down to cost vs. performance- the “superior” choices very quickly become apparent and dominate the market.

Intel having “25% of the market” is not a stable place for it to be: they will either find a way to regain technical leadership, or they will exit the cutting-edge market, and be relegated to making inexpensive, lower-tech commodity microchips like global foundries did.

If you bought in 2016, you’d still have your original investment!

So really not too terrible. They still power a lot of PCs and Laptops. And in the IT world their product was always the best. Fanboys and Cheap gamers preferred AMD. Blehhh , Intel owned AMD in processors.

I say the stock sorta recovers

They haven’t been the best since AMD launched Zen 2. That’s the problem with being the best, if you stop innovating and get distracted by financial engineering like Intel did, you eventually look up and realize you aren’t the best anymore.

AMD makes far superior CPUs compared to Intel in both the PC and the Service space and has for many years.

Nope.

I still will not buy Amd anything.

Nvidia and Intel are the best in the PC realm. Hands down. Amd couldn’t innovate their way out of a paper bag.

If someone really knows IT and quality PC products they would know this. There are a lot of posers tho. 😆

Intel CPUs are far behind those from AMD which has set the standard in design and quality for many years, and Nvidia is just a CPU graphics chip designer and nothing more and nobody needs anything from Nvidia for a PC.

You might want to avoid those Intel 13th and 14th-gen processors that have the crashing issue due to the faulty power. They can permanently destroy themselves.

So cal , you don’t know what you are talking about.

Of course you need Nvidia for a graphics processing unit. A GPU, you see your games with this “video card” as they used to be referred to.

I’ve been building computers for 30 years. Intel is gold. Amds processors caught fire, literally. And always trails NVidia in the GPU world, like they cannot even keep up. Nvidia invented this beautiful tech called Raytracing. It made games gorgeous to look at. But all the fanboys disliked it because their cheaper amd GPUs couldn’t even use raytracing.

Amd sucks, and people will rue buying that stock if they do.

The only traction AMD gets is from poor kids who fuss a lot on social media. Anyone with deep pockets goes Intel and Nvidia because they are the adults and smartest people in the room.

Suffering, if you spend limitlessly without considering value, maybe the kids in the room are smarter. The last few custom builds I’ve done, benchmark comparisons have shown AMD processors to be a much better bang for your buck. If you want to spend double the money for that last 5% of performance improvement, you do you, but I wouldn’t call that intelligent. AMD chips have been a better value as far back as I can remember. Different products for different markets in some cases. But in general consumers tend to spend more on inferior performing Intel chips that are less energy efficient to boot, which benchmarks clearly quantify.

Buying an SPAC is anolgous to buying a home in a flood zone or in a California wild fire zone or even in earthquake zone San Francisco! One day you will be wiped-out!

One day we will all be wiped out. — The ghost of John Maynard Keynes

So when is AI going to genuinely transform some businesses and see them laying off workers, to finally provide the profit margin required to pay for the AI itself, and justify all the up-stream spending/valuations?

How long can all this be seemingly deferred value?

I know this is like the heady days of having a website and no one really knew how to make it work for them, they just knew they had to have some “internets” otherwise they’d be left behind forever!!11!!!

I still think the base level web paradigm is broken before you even add AI on top.

Ie, Google, Meta, increasingly MS, apple etc, all make money by scooping data or fees on transactions, which are increasingly unethical or valueless in society.

Ie, kids getting rinsed on micro transactions, whale abuse, MS getting you to pay subs forever to buy software that’s changed little since 97 etc etc.

Adding AI on top surely can’t rinse more money from people for the same old rope?

It’s only true value is replacing workers. But I’m not seeing millions being laid off yet.

I know companies that have never laid off people even after they began implementing computers 45 years ago. To some extent it goes against human nature. Department managers get ahead by growing their empires, not cutting them. The goal will always be to grow revenues to pay for the AI, not cut staff.

HT – …state not who the slaughterbots are coming for, for you, too, will likely be in the way (the revolution will be partially-televised and ai-edited…)…

may we all find a better day.

(…with apologies to Gil Scott-Heron…).

may we all find a better day.

That’s how they are selling AI tho, “do more with less employees”.

Cmon, it’s all about cutting and bonuses now.

Healthcare executives make millions and do not add any value to organizations. They make millions cuz they cut. They are drooling with helicopter monthly magazine in hands looking at AI to cut their workforces by a third.

I am a surgeon. No AI is going to replace any meaningful % of the healthcare workforce.

So far the most promising thing they have to offer is high quality automated EKG reads and they can write an OK telehealth visit note if they are allowed to capture the audio/text.

They are lightyears away replacing radiologists. and definitely not surgeons. Or even the medical assistants, for that matter…

I don’t know what industry AI could plausibly be poised to replace workers in, but its not healthcare.

The number of actual healthcare providers such as nurses and doctors per capita haven’t really changed in ages. It’s the billing coders, insurance adjusters, pharmacy managers, administrators and every other overhead function that has exploded in costs. Those are the ones that should be replaced with AI.

Dr L,

They are making docs near me use it for their notes here in Raleigh.

Ethical? Nope. Is it younger people’s in administration pet project to look good and cut costs? Yep

I’m not even sure my state’s general assembly has allowed its use. I was reading a law professor say that once a physician starts using it, it opens up a whole Pandora’s box of legal headaches because supposedly it is superior in some ways. And you could make a mistake by not referring to it and a poor outcomes happens. Then all opposing counsel has to do is say “well you should have referred to AI, like you did in the past. Now Jenny sue has no legs…”. Or some bullshit.

But anywho, I’ll leave it up to the healthcare pros :)

REAL Docs/Nurses care about people….you guys just care about prestige, money, big homes, and trophy wives.

I completed pre-med by ’78….took over10 years..saw a LOT of good people turned down. If folks were rich they went to Italy or Grenada. Like the fast moving, shoving, crowding, selfish bitch that spilled 10 ml 20% H2SO4 down my back in Organic Lab. (luckily I had worked in anodizing and didn’t panic like most would, and flatten her…and gotten away with it)

You know as well as I do why they were turned down.

And ALL successful Health Maint Managers DO HATE that high priced labor….and are ruthlessly creative…more ruthless than you guys….far more.

Actually I didn’t take the year of Infection and Disease because was going to Pharm School and as good Biologist knew that was BS, anyway. And it was only about 1/2 if 10ml graduated cylinder…first thing I checked when she bumped me and I felt liquid on back.

Just being completely honest and truthful, unlike you were trained.

PS…don’t you even know about the battle over the Pulse Oximeter for paO2? Cost cutting won over accuracy.

Medicine is mostly BS, anyway….except trauma.

SufferS has this one right….must be one.

That’s the funniest thing ever “grow your staff” wouldn’t that be a bonus.

Kenny, Im using MS Office 360 on chromebook and never paid any fees or subs. It may be lacking some features, but none that I ever need.

Are they calling it Office 360 now because their cloud services aren’t reliable enough to advertise 365?

No that’s the number of degrees your head spins when you find out just before a big presentation that the cloud is down due to another hack like the crowdstrike debacle :)

No fees ? That’s confusing a stand alone MSFT suite on a personal PC is 7-8 usd monthly license cost. Can be shared on 5 machines i believe .

Buy n Hold unless u r Buffet I guess…

Do the growth numbers overall justify 5400/4000 since 2021? ~12% a year sort of averaging out the rollercoaster… I can’t see it but maybe my scales are off. Got a pretty big popularity contest going out there that might be scrambling for the last chair atm. I am murdering the metaphors these days at least! :)

1) TSLA has the highest weight in Mag 7. Kamala Harris will raise a lot of money from the SF gang, bc Googl need some help in front of the US supreme court.

2) [1W] SPX BB : Mar 25/Apr 15 2024, 5,264.85/ 4,953.56. SPX dropped to the its middle, closed above, under DM #13.

3) The US gov vs MSFT Antitrust case : Microsoft monopolized the web. In Sept 2000, after MSFT CEO rejected the US gov, NDX plunge 80%. Last week, under Sherman Law, the US gov sued Googl for an unlawful dominations of the search engine, gouging competition and the internet ads, that enable them to raise ads prices above market rates . Googl has exclusive deals with AAPL and Samsung, paying them $18B out of $300B they collected in 2021.

I didn’t understand the point of the case. It seems like the issue that the government had was them paying Apple and Samsung. Okay well great, what happens next? Alphabet saves 20bil and Apple loses 1/5th of it’s revenue? People are already free to use another search engine if they want if they believe there are superior products out there (my personal opinion). I guess time will tell what the resolution is. Sounds like Alphabet is going to appeal the case and it could take some time to play out. Although Alphabet hold’s the dominant search position, competition is heating up. I don’t even think Alphabet is that expensive of a stock at the moment. This of course is my personal opinion and I’m sure all the stock market T-Bill and Chill folks will vehemently disagree.

A furiously bought dip!

Isn’t that just how institutions unload to the retail bag holders?

I saw a headline saying that institutions bought the BTC dip. I haven’t looked at the money flows, but I remain skeptical.

Call it spoofing, market making or whatever: the house wins.

No signs of an imminent collapse.

No signs of a healthy market either.

Economy seems… fine.

Yeah, the market came roaring back – on very little volume. If white collar crime was prosecuted in this country we wouldn’t have a stock market, everyone who works in it would be in jail.

July was an inflection point for both R-gDp and N-gDp. Inflation will never get to 2% unless velocity falls.

If Nvidia fell to $40 it would still be an 8-bagger from early 2020. The financial media would very quickly pretend that nobody actually bought and lost their shirts in the ~1-year round trip from that level and back. I’ve seen this before.

Drama indeed. Monday morning the VIX spiked to levels not seen since the Covid bear market and out of all proportion to the size of the decline in the S&P 500.

The “size” of the decline in the indices is not the problem, rather the underlying bad health.

The VIX spike represents both deleveraging and protective repositioning.

Looking at S&P volume, the Friday and Monday sessions were somewhat high and less than the high volume seen at the end of June (and March, and December).

Yes: quarterly rebalancing (buying in December and selling in the previous two quarters).

Yes: a bit of insight into institutional activity.

Yes: Breadth has been low and many indicators have been showing a “bearish posture”

Yes: bad market performance happens in election years (and whenever the sellers take control).

T-Bill and Chill. I think there’s some life in that yet!

Vix only tracks 23 to 37 days options, so it’s a small sliver. Japan’s one-day 12% drop spiked sp500 puts, so they locked the hoi polloi from their brokers accounts. By the time you had access those short term puts would be down 90% from the panic level and will likely expire worthless now. The house wins again.

This was reply to Andrew Stanton above.

Stock market entering prolonged period of chaos?

wild oscillation is designed to suck in naïve retail investors thinking that they are getting a bargain while in realty the hedge funds are just trading inflated tech stocks all the way down.

You could add expensify to the list of imploded stocks. And it’s out of Portland no less.

According to Larry Summers on Wall Street Week, the Japan Fed’s temporary flub of a pivot in interest rates was combined with inadequate liquidity in the US options market which drove the US stock market to extreme lows on Monday, a case of the tail wagging the dog. It looks like its all over for now unless more unexpected bad news materializes on the economy or geopolitical front. Turned out to be a Buying Opportunity.

When all’s said and done, the “magnificent 7” are up somewhere in the ballpark of 20% this calendar year. For *trillion* dollar companies, that’s astonishing.

Thank you so much Wolf! I am now very leery about rotating into small cap stocks which are imploding regularly due to SPACs and PE firms milking them dry.

I am also leery about Tech stocks riding the AI bubble. This includes a large part of S&P 500 index funds.

What’s safe? The Dow?

I guess I’ll just TBill and chill.