Delinquencies mostly edged down. Foreclosures have formed a frying-pan pattern.

By Wolf Richter for WOLF STREET.

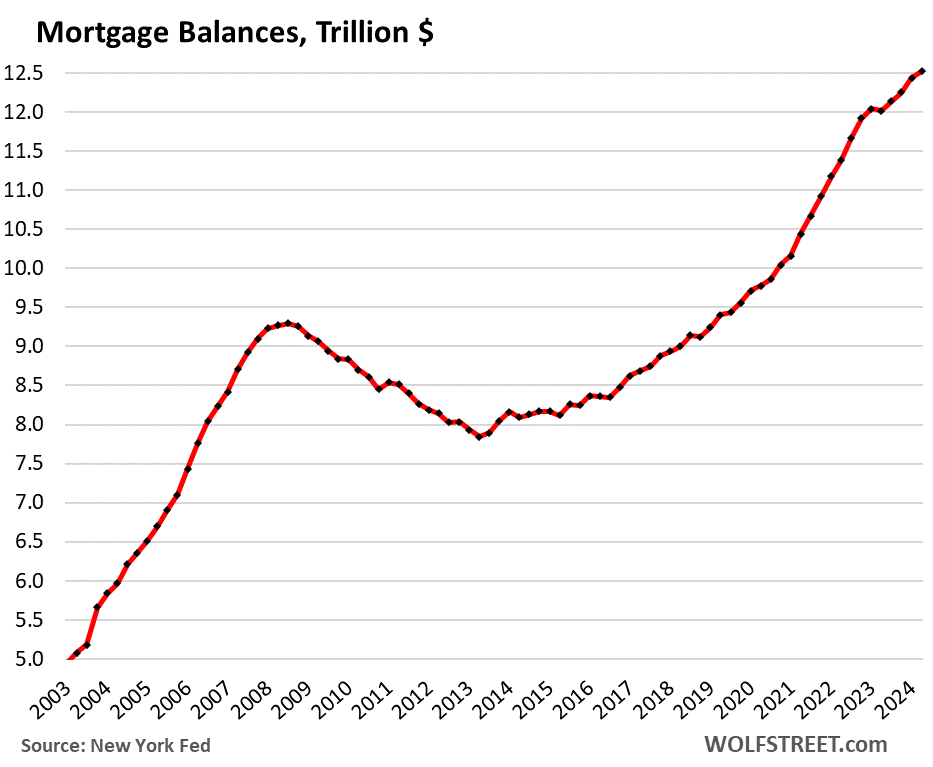

Mortgage balances rose by just $77 billion, or by 0.6% in Q2 from Q1, the smallest percentage increase since the dip in Q2 2023, and the second smallest since 2018, to $12.5 trillion. Year-over-year, balances are up 4.2%, according to the Household Debt and Credit Report from the New York Fed today, as sales of existing homes have been creeping along rock-bottom, new-home sales are also down but not as much, and mortgage applications to purchase a home have collapsed by nearly half compared to 2019, while people with cash are foregoing mortgages altogether.

The slowly rising balance in recent quarters is driven by higher prices and larger amounts financed amid a shift in the mix of homes that sold to the higher end, where sales remain fairly strong.

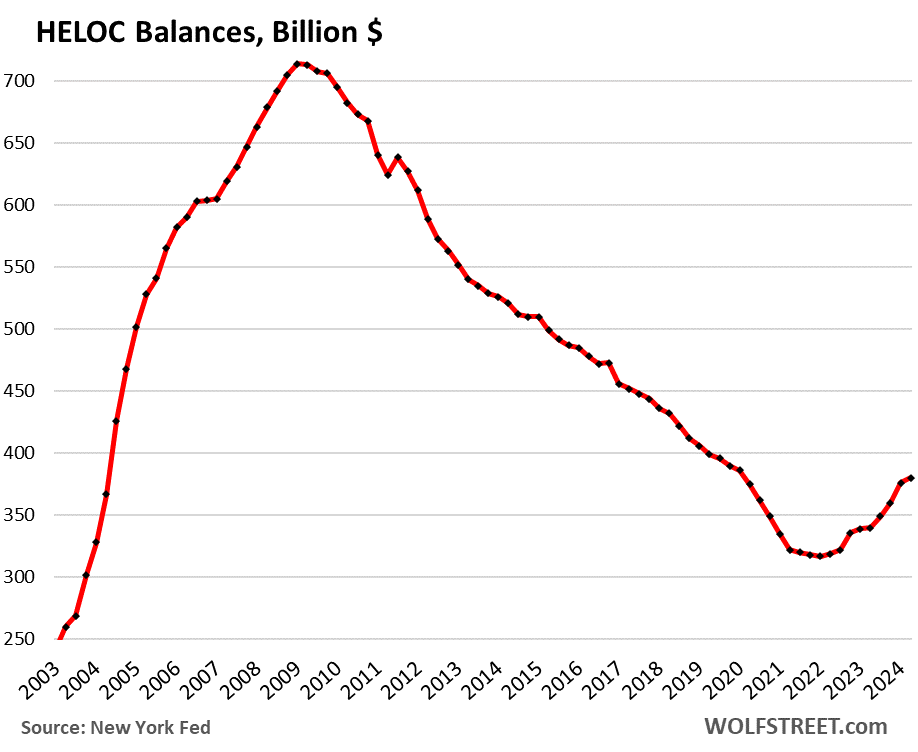

HELOC balances rise from the ashes.

Balances of HELOCs (home equity lines of credit) rose by 1.1% for the quarter, and by 11.8% year-over-year, to $380 billion. But the Q2 increase was much smaller than the jumps in prior quarters. Since the low point in Q1 2022, HELOC balances have surged by 20%.

Despite the surge, HELOC balances remain historically low after 13 years of incessant declines. And they’re still only a tiny 3% of regular mortgage balances. Back in 2005 through 2012, HELOCs amounted to 7-8% of mortgage balances.

HELOCs are a credit line that homeowners can draw on to turn their home equity into useable cash. If a homeowner owns the home free and clear and wants a substantial standby line of credit, such as for home improvements or other projects, a HELOC can be a good solution. HELOCs can get riskier for the borrower in a downturn if they pushed the limits.

Borrowers have to pay Wall Street fees and interest, but that’s a lot cheaper than the primary home-ATM, cash-out refinancing, which these days would replace a 3% mortgage with something like a 6% or 7% mortgage. People still do that, but the payment is going to be a shocker.

Second-lien mortgages are another option to extract cash from the equity in the home, but unlike HELOCs, they come with fixed payments over a fixed term, and both are far less expensive than doing a cash-out refi, where the entire debt gets the much higher mortgage rate.

About 1.8 million HELOCs were originated in 2023 and the first half of 2024, with these credit limits, according to a blog post by the New York Fed:

- Below $50,000: 28%

- Between $50,000 and $100,000: 29%

- Between $100,000 and $150,000: 18%

- Over $150,000: 25%

- Over $650,000: 1%

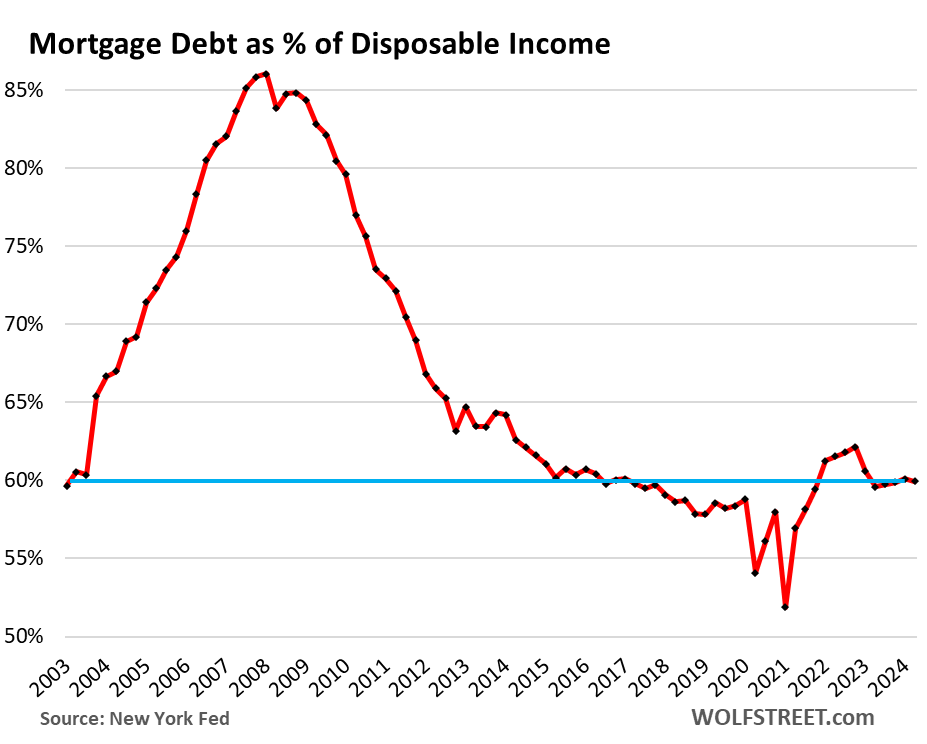

The burden of mortgage debt compared to income.

One of the ways to measure the burden of mortgage debt on households is the comparison to disposable income, which is what households have left over from their total income from all sources after payroll taxes and social insurance payments. This includes income from wages, interest, dividends, rental income, farm income, small business income, transfer payments, etc. It’s what they can use to deal with their costs of living and servicing their debts.

Quarter-to-quarter, disposable income rose faster (+0.9%, per Bureau of Economic Analysis) than mortgage balances (+0.6%), and so the ratio of mortgage balances to disposable income edged down a hair and has been roughly flat for the past five quarters at around 60%, a historically very low level.

Note the scary levels of mortgage debt to disposable income in the years before and during the housing bust. In Q1 of 2003, they were still at 60%. But by 2006, they were over 80%, and in 2008, they reached 86% as the housing market was already toppling and homeowners began walking away in large numbers from their mortgages, leading to the mortgage crisis.

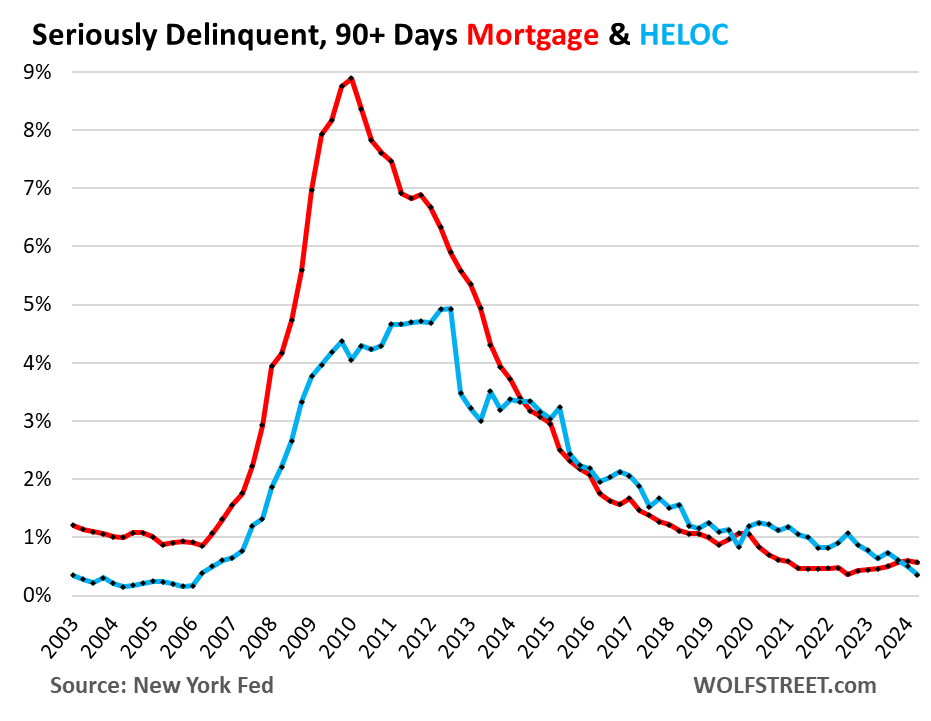

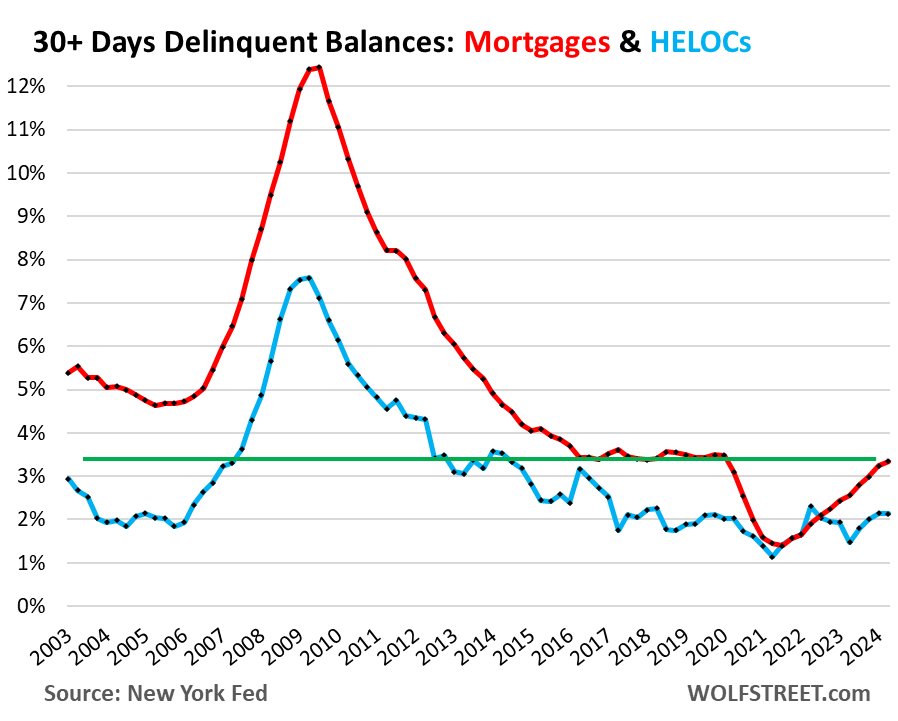

Delinquencies mostly edged down.

Serious delinquency: Mortgage balances that were 90 days or more delinquent edged down to 0.57%, compared to 1.0% and higher before the pandemic (red line in the chart below).

HELOC balances that were 90 days or more delinquent dipped to 0.36%, the lowest since 2006 (blue line).

In other words, more borrowers that had fallen behind are catching up again.

Transitioning into delinquency: Mortgage balances that were delinquent by 30 days or more ticked up by just 11 basis points – the smallest increase since the free-money era in Q1 2022 – to 3.3% of total balances, which is at the low end of the spectrum of where it had been before the pandemic. And it seems to be stabilizing (red line in the chart below).

HELOC balances that were delinquent by 30 days or more edged down to 2.1% (blue line).

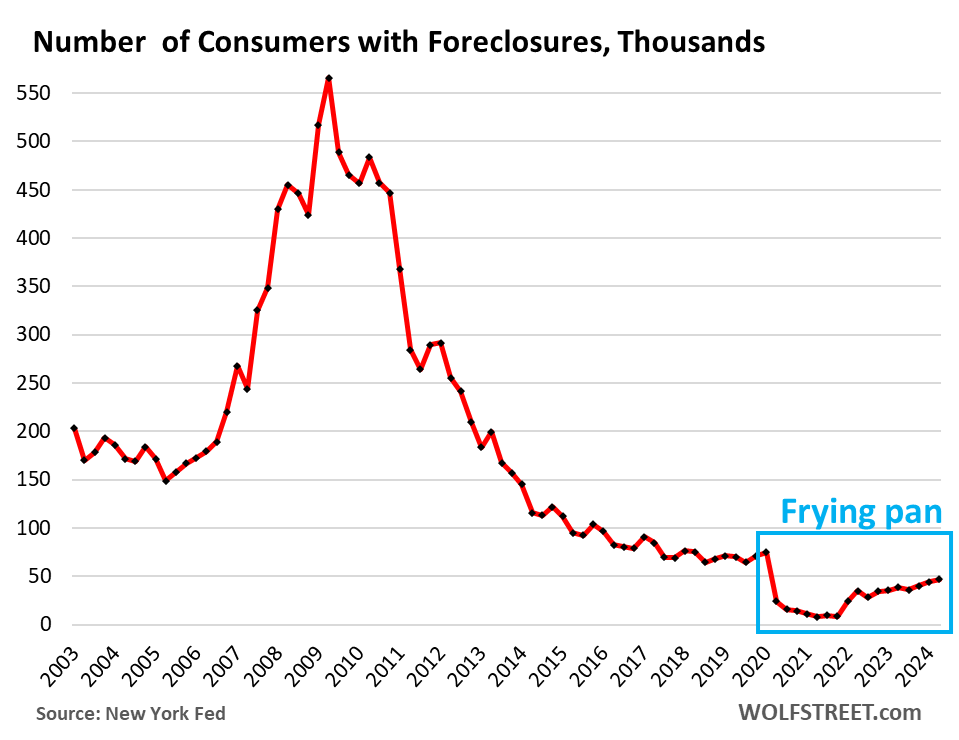

The frying-pan pattern of foreclosures.

The mortgage forbearance programs and foreclosure bans during the pandemic reduced the number of consumers with foreclosures to near zero. They have risen since then but remain well below the prior all-time lows.

In Q2, there were 47,180 consumers with foreclosures, compared to 65,000 to 90,000 in the years 2017 through 2019. They haven’t even normalized to Good Times levels yet. The post-pandemic frying-pan pattern has cropped up in other data as well:

Foreclosures won’t be a problem until home prices sag by a whole bunch, and simultaneously lots of people lose their jobs. That’s what happened during the mortgage crisis, when the unemployment rate reached 10% and stayed above 7% for five years, as home prices plunged.

In July, the unemployment rate was only 4.3% — still low and now powered by waves of immigrants surging into the labor force, rather than by waves of people losing their jobs. And only some recent homebuyers might be in a position of negative equity.

Homeowners with equity in their homes, when they get in trouble, can sell their home, pay off the mortgage and walk away with some cash, and there won’t be a foreclosure. And homeowners with negative equity can just go about their lives and make their payments, and they won’t even notice it. It’s only when they lose their jobs and cannot make the payments and are trying to sell the home to pay off the mortgage that the problem arises.

And in case you missed it yesterday: Household Debt, Delinquencies, Collections, and Bankruptcies: Our Drunken Sailors and their Debts in Q2

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

2007-2010 was peak gluttony! I bet a lot of people remember these times fondly.

Then we were living Wolf of Wallstreet and today we are living in Disney’s Frozen. 😆

HELOCs are a little TOO convenient a source to draw down debt upon. As with all easy solutions, they can rapidly spin out of control if not managed properly. The lure of easy money (HELOC gold) can make self-restraint damn near impossible, however.

That is sort of the issue with home equity. It is there and you’re proud to have it, but no real way to utilize it.

What if your home equity could be earning 5% a year?

Like Saul Goodman said to Jesse Pinkman “you’re house poor!”.

From what I’ve seen, most HELOC rates are 8%-9%.

I can’t wait until Tbills are paying 11-12% then I’d be happy about pulling out my home equity at 9%.

Bingo!!

What are the odds of a heloc loan fixed at 9 percent?

If rates are 11 percent we have raging inflation !

This is the issue I’m facing as a potential first-time homeowner. The high home prices make it hard for me to see the value of owning a home. I’m exploring different options and investments that offer a high or moderate percentage of return, which seem more appealing to me rather than owning a mortgage.

The proper thinking is to give all your money away for a pretty house. Sign the 30 year mortgage then discovering you don’t like your job, your house, your neighbors, you might not even like yourself anymore and the dog starts whining and howling.

But it sounds like you have a good outlook…no worries.

i’m seeing specials and some actual rent reductions around here… [ You CAN RENT] …. also see home sellers that NEED to sell dropping by up to 25k off asking. depends on situation but search around what is going on. the correct home or abode will add pleasure ..we waited and now have 3 properties / not as investments altho they ARE ..but for enhancement of life. if you need wealth accumulation i wouldnt pick a home for that in this era……too many variables. home builders will come back and the costs of living will lead to builders finally getting smart with efficient homes/ smaller / good localities/ amenities [already seeing it] …..its hard to compete with that as a retail / personal home owner thinking youll win as an investment strategy.

Doc,

Historically, if you buy and hold and enjoy a house for 12-15 years, you will come out ahead financially.

Every Wolf chart confirms this.

The in-between will cause hard work and unknown expenses that will cause you to lose sleep while you happily notice surrounding rents are larger than your mortgage.

It is not an easy long-term investment

You just made my point that many do not want to accept. New homeowners or buyers are much worse off because of low interest rates pushed down for decades. The huge price increases reallyWe could of bought our first house when it was $189,000 but we didn’t. Now, it would cost $620,000. This is 25 years ago. We moved to a much 30% lower rent area of the country and our wages are only 10% lower.

We just saved alot and kept getting dinged with low interest rates, CD rates. We made sure we put the maximum in IRAs, joint CDs. We will not buy stocks, mutual funds, anything we can’t get a fixed rate, principal back. The bottomline is, we rent, we have plenty of space, 2 kids grown up now moving out. In our eyes just because we don’t own a home does not mean we are not successful as we have $1.3 million in net worth, no debts.

The Happy Renting poster you brought up joint CDs, IRAs. I don’t know if you ever seen these but we locked in a bunch of 10 year jumbo CDs, IRA CDs last year at 4.45% to 4.65% fully CDIC insured and some through credit unions that are fully insured NCUA. Interest rates have somewhat since 2023 but a few are still giving 4% to 4.10% others 3.71% to 3.85%.

We were able to retire much earlier than we planned. We were depending on 2.25% to 2.50% CD rates for retirement and so we were looking to retire at the end of 2028 to early 2029 based on our CD, IRA CD balances by then.

We were truly surprised how much CD rates increased over the last 18 to 24 months. Many borrowers with mortgages, refis, helocs, car loans, other debts had interest rates low for a long time what 10 years at least. We needed some relief and reality to get back to more historical normal interest rates for CDs.

Wolf, I hope this guy’s aunt is not using her house’s equity as an ATM machine like back in 2007 to 2008. If she happens to be lucky and see HELOCs or other borrowing going back to 2018 to 2019 levels 4% to 4.5%, she still has to pay $12,000 to $13,500 a year in interest. Also, I hope she is not just paying interest or worse, the interest accumulating and in 3 years say has a $320,000 line, loan or borrowing balance.

@sufferinsucatash most people are “earning” way more than 5% on their home equity when you add what they are “earning” on their debt (if guy puts $100K down on a $400K home and it goes up in value by 5% he gets a 20% return on his equity).

Real estate can crash. See commercial atm and 2008-2014. But in some ways you are correct. If you can time it correctly and not get screwed over.

As BobE mentions above, heloc rates are 8-9%. That’s not cheap money, and exactly how higher rates are supposed to restrain spending.

I think some people don’t understand that accessing home equity is not free. I’ve heard comments like: “But it’s MY Equity, why isn’t it free?” That conversion from equity to cash is not cheap.

I hope people are not just seeing a pile of cash to spend.

I agree that it is a good emergency fund and better than having a 30% credit card debt.

And that’s why a cash out refinance is still better..you get a 6-7% rate. Better than 10-11% heloc. And heloc is interest only until draw period ends. That money can be spent better in a regular mortgage. And after draw period it’s principal + interest.

People are really financial morons or just lying to themselves. My aunt borrowed $300,000 on a $550,000 home. She got a cheap interest rate back in late 2019, 3.75%. What she did not know is it as adjustable after 6 months. It was a promo. The rates did not climb that much until 2022. Now, it is at 9.25% and she got a small break going down to 9.10% but she is in real deep trouble.

She’s not really in trouble, I would venture. Depending on when she bought the home, she can sell the home now, pay off the debt with the proceeds, and walk away with some cash, on top of the $300,000 in cash she already pulled out. And then she can use the funds for a big down-payment on a smaller home and finance the remainder with a purchase mortgage at around 6.5%.

How many used HELOCS to buy crypto? That’s too risky for my blood.

How many used credit cards?

Most exchanges require you to link a bank for ACH transfers and don’t accept credit or debit cards.

Do you mean “monthly” mortgage debt as a % of monthly Disposable Income?

Or is it total mortgage debt as a % of Annual Disposable Income?

Total mortgage debt at the end of Q2 divided by the seasonally adjusted annual rate of disposable income in Q2.

Of course we should be careful to remember that income is not distributed evenly so working in gross numbers does not give a full picture.

Right now everything seems dandy. Fiscal deficits running at 6% of GDP seems to be no problem.

Finding people to work still seems to be a bigger problem than people not being able to find work.

Our great service economy chugs along but it seems like service in almost every category gets worse and worse unless you sign up for the Platinum plan.

And none of it really explains why the economy can’t build ships for the Navy or missiles for the Airforce or artillery rounds for the Army or why Boeing cannot design a new airplane or build the designs it has to spec or why Starliner is still stuck at the ISS or why Intel seems to be having more and more trouble building high end semi-conductors.

But there is no denying that people seem to be spending, unconcerned about money and traveling.

danf51 – …the issues that arise when one starts to place all faith and belief in their press releases, old and new…(…so rolls history’s wheel…).

may we all find a better day.

In 2021 and 2022 there were lots of credit unions doing HELOCS for up to 95% of the home’s value. Wonder what loan to value ratios they are doing these days?

Even back then a HELOC would have had to be up to whatever percentage of home EQUITY, not “value,” (equity = value minus debt). Or both mortgage and HELOC combined to value.

As a mortgage loan officer, I can tell you that they are still mostly capped at 95% CLTV (combined loan to value). Usually, to go to 95% you need a 720 representative credit score and a strong debt to income ratio. The rate is indexed to the prime rate, so right now I am seeing them in the 9% range.

People doing them now seem to be doing them mostly to either pay off high interest credit cards or to do home renovations or repairs. Usually, for lines of credit under $150K, you don’t need an appraisal.

Thanks for the info. What Lenders right now, usually don’t require an appraisal if less than $150,000?

Most credit unions will not hit you with the appraisal requirement–Tower, NASA FCU, Navy Fed, etc. A lot of these credit unions are doing open enrollment in the sense that you don’t have to have a natural “in” for the credit union to be eligible. NASA FCU for example I believe will make you a member of the national space society to make you eligible.

If you invest in a high yield bond @ 5% and write off the 9% interest then your in the positive until you make another investment.

F&L,

As a loan offer, doesn’t 95% LTV seem irresponsible to you?

HELOCs frighten me.

At 8-9% adjustable interest+fees, whatever I needed it for had better be worth it. I’d rather save up and pay cash or have a sure “bet” paying a higher return.

I suppose it would be worth it to pay off a 30% credit card debt.

I don’t live that way.

With a significant stash of T-bills, you can “borrow from yourself” at 5% which is a much better deal than a 9% heloc.

They’re interest only and an excellent way to finance investment projects short term. I use mine all the time, even at 9%. COB: cost of business. A few thousand over 6 months is negligible when the deal is 100k+. Discipline is to have the cash or cash flow to pay it off, but elect not to as $ should always be making you more $.

3 general rules for young:

1) don’t buy first home for self, buy a rental or duplex and let someone else pay half your bills. Repeat and you live for free and are building wealth. As trading hours for salary will be primary source of wealth building for a very long time, this maximizes investment income.

2) no car payments. Do whatever you have to, but expensive, depreciating assets are wealth killers.

3) absolutely no financing recreational or discretionary purchases including student debt. Later in life when you want and can afford a z06 vette, buy a house instead and rent it. That way the rent makes the payment and you get a house and vette for free.

Note: I don’t care about expensive cars and don’t own one and wealth equates to freedom of opportunity.

A possible 4th: don’t make poor relationship decisions. Unplanned children and/or divorce destroy ability to create wealth.

Those rules are 30 years outdated. You’ll be lucky to break even on anything less than 6 flat. And I’m talking doing most of the work around it yourself.

Not to mention, last thing you want to do is live next to your tenants. It looks good on paper, but all it takes is one bad renter. And that’s not matter of if that will happen, but when.

@Pilotdoc, all great advice, any tips on grtting kids to actually “follow” the advice?

I have just one (1) young relative that is interested in my advice (that is now worth over $1mm at 29) but the rest of the kids I know are paying crazy high rent for fancy apartments, borrowing over $100K for degrees from B list private colleges that are not “worth” a penny more than a degree from a state school (that is almost free) and buying (and even worse “leasing”) fancy cars with huge payments. Your 4th should be 1st, I try and tell all young men that unless they are married and “planning” to have a kid in the next 9 months they should wear a condom.

I like the way you think in general, but…

“Discipline is to have the cash or cash flow to pay it off, but elect not to as $ should always be making you more $.”

Let’s say I pull $100k out of my house at 8%. What can I do with that cash that will /reliably/ earn me a greater yield?

I’m aiming for a 10% yoy return on my investment portfolio, which is made up of mostly high-yielding credit funds and T-bills. But the former involves risk, and the latter yields less than the loan’s interest rate.

I’ve seen another commentor frequently mention the “heloc and invest” strategy, but I’m just scratching my head at what kind of investment is worth going into debt @ 8% in order to fund.

We set up a HELOC in case our small farm business needed it, and never tapped it. It was comforting to know we could grab some cash, and more comforting to not have to do it. I don’t think it cost much to establish the capability, but that was some time back. Probably different now.

Yes, the real and possibly only value to a HELOC is to have an easily ready source of emergency funds. I’ve had one in place for years. I used it just once to demonstrate to my grandkids how it worked. I activated the “loan”, which transferred money into my bank account, I then bought a pizza for them, and then paid off the”loan” the next day with another bank transfer.

It is so easy and slick and would work great in an emergency but is dangerous to un-disciplined participants.

I can’t imagine the situation that would persuade me to put the security of my paid-off home at risk by using a HELOC. Certainly not to pay off other debt or finance a business deal. Maybe to pay ransom for a loved one kidnapped by drug lords.

A loan originator once said to me “A banker is the only person who will hand you an umbrella when the sun is shining, and take it away at the first sign of rain.” Most HELOCs contain a call provision that allow the lender to accelerate the loan at their discretion. Lots of HELOCs were called or frozen during the GFC. I’m keenly aware that sometimes, it’s the only way to get cash for start up/small bus ventures. But co-mingling title to one’s primary residence with business liabilities is playing with fire. To be avoided if possible.

We did pretty much the same. Set up a HELOC that was there ‘just in case’.

We didn’t tap it until we moved. Then we took most of it out to help with an all cash purchase of our downsized condo. We thought that would be easier than scrambling for a “bridge” loan during our move.

When sold our house the proceeds were more than sufficient to pay off the balance on the HELOC. It was very convenient for us.

We don’t have a HELOC now as we don’t anticipate any need to tap the equity of our new “crib”. :-}

Please take note of all this, JPowell.

Real stress in the economy remains elusive. Banks are not going broke. CRE remains simmering and not a big issue with lenders striking deals to kick the can down the road. CPI has plateaued above your target. Manufacturing is picking up steam. Unemployment is NOT shooting through the roof, only slowly building. And even at 4.5% maybe by Sept, that’s still historically low.

There are many reasons not to cut, but we all know you’re going to ignore the real data hand the Dems a gift, possibly even by 50 BP.

Looks like the housing market is healthier than its been in a long time, which is surprising given these interest rates.

I took out a HELOC before the 2008 crash and everyone said I was crazy – rates and payments were going to go up and up and up. The initial rate was in the 7-8% range and guess what? After 2008 and until the last couple of years my rate was down to 3% – best loan ever. Same with my variable rate mortgages on investment prooerties. They dropped from 6% to 3.0 for over a decade!!!

The time to take out variable rate loans, like HELOCS is when rates are HIGH, like now, not when they’re low. When mortgage rates drop, so will the HELOC rate.

Only if you think rates can only go down from here. That’s the problem with gambling on things you don’t have control of. Or assuming (like all of Wall Street) that rates are going down.

“The time to take out variable rate loans, like HELOCS is when rates are HIGH, like now, not when they’re low.”

The problem with this thinking is that 10 years from now, today’s rates might be considered low.

The last bond bear market lasted ~25 years. Interest rates only bottomed about 3 years ago.

To be sure, you made a good play because you took out your variable heloc during a regime of falling rates. But now we are in a regime of rising rates, which means you won if you took out low, fixed-rate debt.

The king is dead, long live the king.

‘…bet the ranch…’. ‘…don’t bet the ranch…’. ‘Nomadland’ or ‘a Homestead’? Ah, ‘Murica, with it’s endless possibilities and varying mileages…

may we all find a better day.

Disposable personal income is : $21T. Renters have personal disposable income who pay no mortgages. Many homeowners have disposable income but are mortgage free, or almost free. The burden new owners personal disposable income is high, but several wage earners in one household, like a husband and wife, or a family with grown up kids, can cover mortgage debt. Household debt payment/Disposable income is 10%. One household might include several wage earners who cluster together.

Between 2008 and 2013 lenders took a $1.5T hit. 30 days delinquencies

are much larger than 90 days delinquencies. Lenders kicked the can down and settle with borrowers to avoid another hit and keep total assets intact for window dressing.

The rentals suck though.

I know of a couple who sold their house for 2.1 Million, moved into a rental and it had all kinds of mold.

Like awesome you have a good bit in the bank but now you are living not in a 2 million dollar really nice house but a run down rental that poses as a luxury home.

My fried sold his home for 1.8 million dollar and is renting a similar house for $6K/month.

No issue for him.

I guess the nice thing about renting is the mold problem is not yours to spend $$$ to fix. If you have mold in the house you are renting, just walk away at no loss to you (except moving expenses)

My son is still renting at almost half the cost of a mortgage on the same house. The landlords purchased long ago and can only charge the current going rent.

I’m still watching Wolf’s awesome chart showing OER vs Case Shiller home prices. When they intersect, he will buy. So far, rents and mortgages keep going up together.

“I guess the nice thing about renting is the mold problem is not yours to spend $$$ to fix. If you have mold in the house you are renting, just walk away at no loss to you (except moving expenses)”

The problem is when you have a crappy landlord who procrastinates on the issue, and meanwhile you and your family are breathing in mold spores.

I’ve never dealt with this personally, but have heard stores.

Additionally, you can’t just walk away from a lease. I suppose you could argue that the landlord violated the lease by not removing the mold in a timely manner, but the landlord will surely report it as nonpayment.

Not quite related to HELOCs and Mortgages, but…

I just got a notice from Schwab this morning that my 10 year, 5.98% Federal Farm bonds are being called. I bought them earlier in the year and only got one coupon out of them – bummer.

I wonder if this was done because they’d now sell at a significant premium to par, or because someone in the Fed Farm Dept thinks rates will be lower and doesn’t want to pay almost 6% for 10 years?

Yes, Many CDs are now callable. I haven’t had that happen yet.

The initial rate is tempting, but buyer beware that you may be forced into lower return if your CD is called.

Banks play to win.

Don’t buy callable CD’s. It was posted on this website couple years ago, what to look in brokered CDs.

These are agency bonds, not CDs, although the principle is arguably the same.

I normally avoid callable products, but couldn’t resist the allure of almost 6% for the next decade. Fortunately I only paid a few cents over par.

Seems like rate cut mania has infected the Fed Farm Bank.

We bought our house down in Florida here for $500,000. We put $50,000 down, money saved while my wife where working 60 hour weeks for $14.50 an hour for 60 hour weeks saving like mad. We did that for 2 years while living at home before we got married, fully paid not debts at 24.

We are now both 30 and through the Pandemic, economic downturns, temporary layoffs, still worked 40 hour weeks for a while until 50 hour weeks at now $18 an hour. Basically we paid off $100,000 in 6 years off our mortgage, raising 2 kids and no debts, 1 car, no loans, debts bedsides our $340,000 balance.

This is why you stick with family, our parents help alot with watching their grand kids.There is nothing more important than family. We were smart enough and took the advice of the credit union manger at our local credit union and locked in 2018 a 3.95%+ only 1 point 30 year mortgage. I keep hearing mortgage rates are 6.5% or so. Debt is like paying with fire, if you don’t watch out you will get burned.

I see this as gaining by abusing.

I know you love your family and everything. But you do not pay for the childcare that your parents are giving. If you did, you would be in worse financial shape. And they would be enjoying their retirement more freely.

I have relatives just like you. And oh man do they abuse the $h*t out of the situation. Honestly if they can sleep at night, they will be financially better than a lawyer once all the granparents croak. They will get all the properties.

NYT did an article on this “eldar abuse” because genx and millieniels are stealing their parents time and money, versus actually just being on their own and getting life done.

So yeah what I say is harsh, but it’s the truth.

Mortgages as a percentage of disposable income sounds dumb to me. Are we looking at disposable income as just the percentage of take home pay, or money after all the necessities are paid for. The latter is the one that I think of, and if that’s the case, shelter is necessary, so why are we looking at disposable income? Just tell me what percentage of take home pay.

Disposable income is take home pay after all your payroll deductions – income tax, SS/401k/healthcare contributions etc.

My gripe with disposable income is there are plenty of taxes and other legally-mandated expenditures beyond what’s deducted from my paycheck.

Is that income really disposable if the city takes its pound of flesh before I get to spend it?

Cole,

“Mortgages as a percentage of disposable income sounds dumb to me.”

You sound dumb to me, as per the rest of your comment.

Take home pay as ShortTLT describes it is standard. Everyone pays Federal tax on income (10-37%). Many pay state tax (0-13%). All have healthcare deductions. The rest is disposable income.

If you pay $6K or $200 per month in rent or a mortgage, it comes out of disposable income.

If you eat out or in every night, that is disposable income. We had some minor stock option decisions once which amounted to $300. My coworker was excited because that amounted to his nightly bar tab. It was 1 month of in-home food for us.

If you drink fine wine/brandy/tequila or Bud light, that is disposable income.

It is hard to characterize people’s priorities but the rules for disposable income are set.

Howdy. Foreclosures should finally be rising since all the Covid laws / rules taking away property owners rights are finally over…. HELOC s are a great tool to build wealth. Of course, YOU must know how to manage $$$ and how to build profitable ideas. Thats right prisoners, HELOC your way out of prison. MA and PA own the most 2nd homes. Get some courage and work hard for additional wealth. Sorry, never mind, too much work for the Youngins.

DFB,

What can invest with my HELOC money that will reliably yield more than the 8-9% that it will cost me?

If the Fed cut rates and demand for highly skilled workers and semi highly skilled will be high disposable personal income will rise to a new all time high. A husband, or a wife — not a husband and his wife, or the whole family clustered together — will be able to buy a house and feed a family.

When disposable personal income rises ==> tax collection will rise. It will fill gov coffer. The budget deficit will flip to green. The surplus will enable the gov to cut debt, if they are fully committed to cutting debt, even with a few pet projects to please congress.

Thank you everyone on the information on how to leverage my primary home into incredible wealth!

I’m not wired that way or I’ve seen too many co-workers still working at 70 who leverage themselves into incredible debt in 2001 and 2008.

There are always winners and losers.

@BobE,

To be fair, not all people who are still working at 70 have to. Some just enjoy it.

Sorry! No offense to the 70, 80, and 90 year olds who still love working.

I now can never run for public office.

And not to cast the first stone, I am in OK shape because I took more risk investing in stocks and a primary home instead of 0.01% savings accounts. I did leverage on the primary home since even back then, nobody could save enough to pay cash.

It still remains to be seen on how that will work out when I can retire.

I wonder what the length of time a mortgage has been retained and proximity to beginning retirement effects HELOC starts. For instance, if you are a homeowner and you’ve had your mortgage for 15 years and are considering retirement within 5 to 10 years, would you want to take out a high interest loan against your mortgage as you enter retirement? Does that sentiment have an effect on the lower levels of HELOC starts in addition to the rates, of course?

mortgage lending is simply more responsible today. While you can still find a few select lenders offering no doc; no job and no income disclosure loans, that non-qm lender requires 20% down and the buyer to have 12 months of reserves. They are de-risked because most people don’t away from today’s avg. down payments on a non-qm loan. One of the nation’s largest home equity lenders reduced their CLTV maximums from 95 to 90. Possibly due to a shift with more declining markets like Seattle, Austin, Denver, Phoenix..etc.