They’re only a small-ish part of the banking industry’s overall loan book. But some banks are more exposed than others.

By Wolf Richter for WOLF STREET.

Banks are still very profitable. The industry reported quarterly net income of $64 billion in Q1, according to the FDIC yesterday. And so overall, as an industry, they can take big credit losses, and they have started to take growing credit losses. But some banks are more exposed to risks and are more fragile than others.

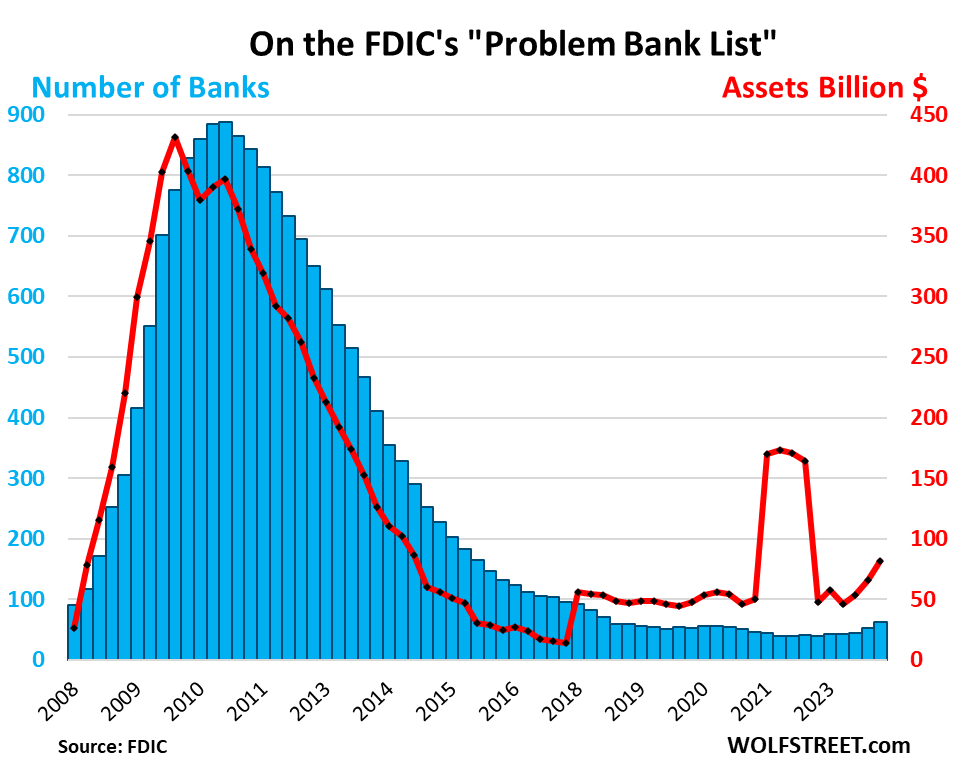

Banks on the FDIC’s “Problem Bank List” rose by 11 banks in Q1 from the prior quarter, to 63 banks (blue columns), of the 4,000-plus banks in the US. The FDIC doesn’t name names, but we can guess some candidates. So there will be some more bank failures – there are nearly always every year.

Total assets on the Problem Bank List rose by $16 billion in Q1, to $82 billion, the third consecutive quarter of deterioration (red line), largely driven by the quagmire that CRE has been sinking into. The chart shows the historic context to the Financial Crisis:

CRE is starting to leave skid marks.

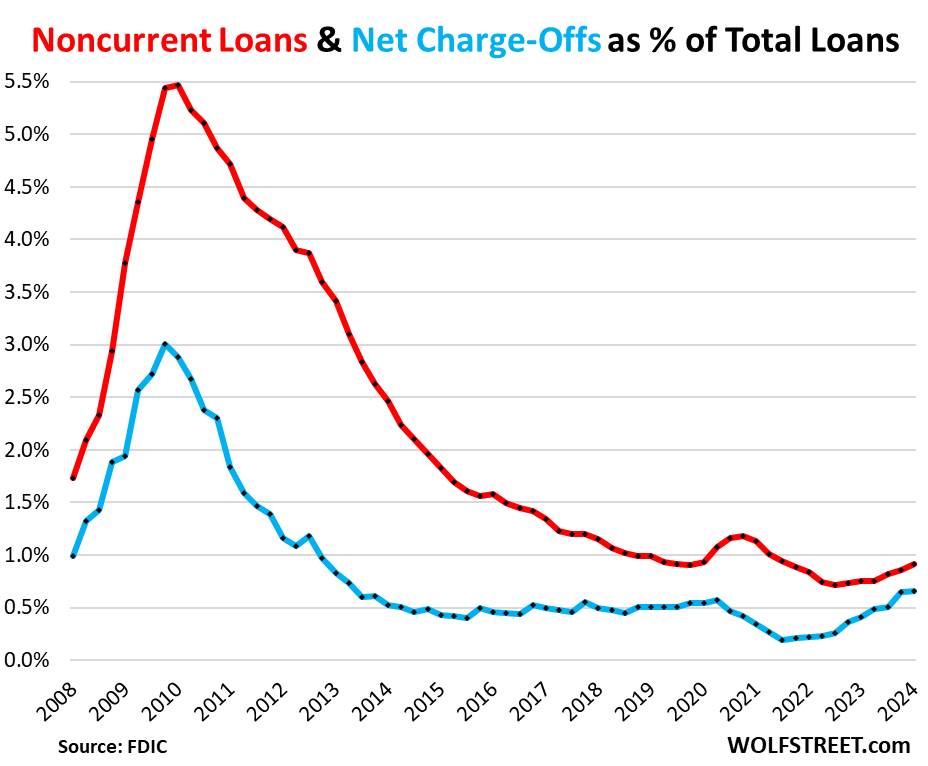

Noncurrent loans (where borrowers fell behind) rose to 0.91% of total loans (from 0.86% in the prior quarter), now roughly at the same rate as during the Good Times just before the pandemic. At the peak during the Financial Crisis, it had hit 5.5% (red).

The deterioration was driven by CRE loans, where the noncurrent rate rose to 1.59%, the highest since Q4 2013, driven by office portfolios at the largest banks.

Net charge-offs (when banks throw in the towel on the loan) were 0.65% of total loans, same as in the prior quarter, but up from the historic free-money-from-heaven pandemic era lows, and a hair higher than during the Good Times before the pandemic. The driver behind the increase from the free-money lows in 2022 were credit cards, where the net charge-off rate rose to 4.70% in Q1, up by 122 basis points from its pre-pandemic average. We went into the weeds of who was falling behind on their credit cards here.

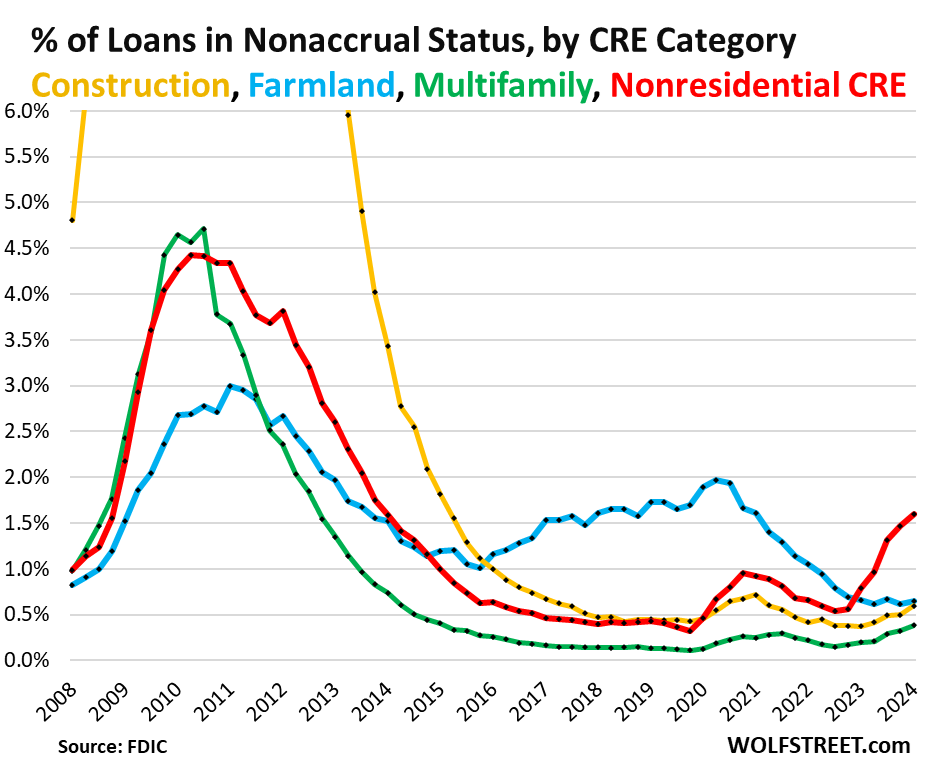

Nonaccrual rates by CRE category.

The chart below shows how nonresidential nonfarm CRE loans (red) have become the outlier in terms of nonaccrual rates, compared to other CRE categories, such as construction loans (yellow), farmland loans (blue), and loans on multifamily buildings (green).

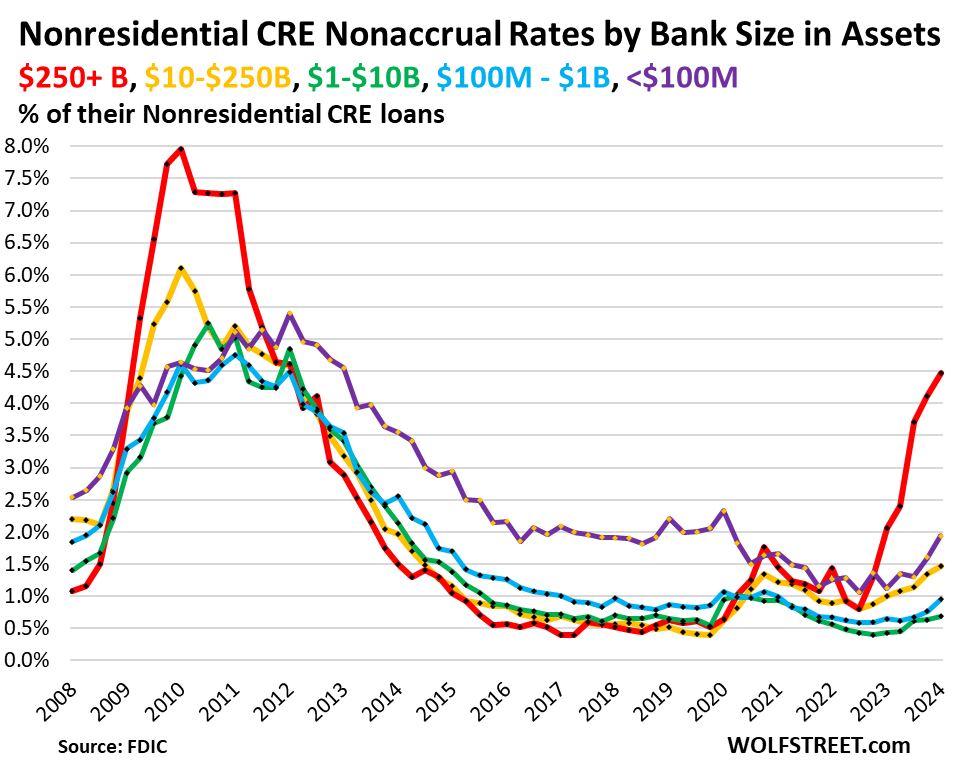

Nonresidential CRE loans at big banks get messy.

FDIC provides delinquency data by bank size on nonresidential nonfarm CRE loans (which include the most troubled sectors of CRE lending, office and retail). The “past-due and nonaccrual rates” of these CRE loans have increased across all bank sizes.

But for large banks with over $250 billion in assets, the rate for nonresidential CRE loans spiked to 4.48% of their nonresidential CRE loans loans (red in the chart below).

During the Financial Crisis, the big culprits were residential mortgages, a much larger category of loans than nonresidential CRE loans. At this point, residential mortgages are still in good shape with historically low delinquency rates and foreclosures.

For tiny banks with less than $100 million in assets, the “past-due and nonaccrual rate” jumped to 1.94% of their nonresidential CRE loans (purple).

Thankfully…

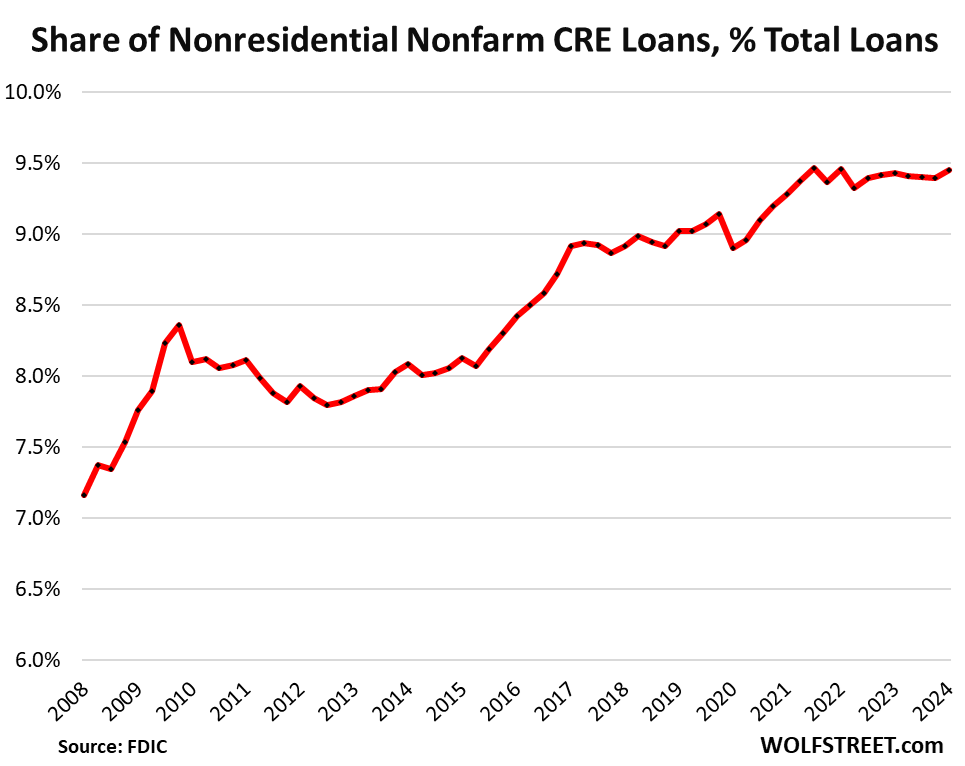

Nonfarm nonresidential CRE loans – where the bulk of the loan problems are now occurring – form only a small part of the banks’ total loan book. In Q1, these loans amounted to 9.4% of total bank loans. Since 2021, the share has been roughly in the same range, just under 9.5%. And the fact that the share of the loan book overall isn’t bigger is a good thing, given how problematic these CRE loans are going to be as the sector cleans house, so to speak, over the next few years:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Total assets on the Problem Bank List” (red one on the 1st graph) would have been parabolic from 2022 except for the $125B or so injected to rescue the three (?) banks. If the higher for longer continues and more importantly the maniac crowd or the investors understand, the growth would be faster. It may become like we rescued B&S, Merryll Lynch went for a shot gun Sunday wedding (?) and Lehman became an orphan.

“But for large banks with over $250 billion in assets, the rate for nonresidential CRE loans spiked to 4.48% of total loans (red in the chart below).”

That is why I suppose the BIG BANKS forced FED to scuttle Basil II or whatever — https://seekingalpha.com/article/4696049-big-banks-are-pressuring-the-fed-to-loosen-protection-for-depositors.

Great going. And now we have a leading presidential C conv_cted of fe_ony. In other parts of the world, there would be strikes, burning the bases and so on.

Your #1: “Total assets on the Problem Bank List” (red one on the 1st graph) would have been parabolic from 2022 except for the $125B or so injected to rescue the three (?) banks.”

1. no banks were “rescued.” Three banks were shredded and sold for scrap. Their securities and loans were sold to other banks and investors.

2. That $125 billion in BTFP “rescue” lending to banks by the Fed — I guess that’s what you’re referring to — was something entirely different; it had nothing to do with credit losses; it was a loan to banks to cover their runs on deposits in early 2023. This was a liquidity measure, nothing to do with credit losses.

Your #2: “But for large banks with over $250 billion in assets, the rate for nonresidential CRE loans spiked to 4.48% of total loans (red in the chart below).”

So I re-read my text here; turns out I goofed by leaving out a key phrase, and the chart was badly labeled too. Now fixed. So thanks for directing my attention to this.

It says now: “But for large banks with over $250 billion in assets, the rate for nonresidential CRE loans spiked to 4.48% of their nonresidential CRE loans loans (red in the chart below).”

So this 4.48% is not of their total loans, but 4.48% of only their nonresidential CRE loans, which themselves are less than 9.5% of total loans (banks overall, last chart). So roughly, those nonaccruals on CRE loans amount to about 0.45% of their total loans.

So this starts to align with Blackstone has been saying all along on the least two earnings calls. The cre sector is bottoming out. Thanks for the analysis.

Funny, my read on Blackstone’s recent comments were more aligned with them “talking their own book”.

1. Over the past 5-6 quarterly redemption periods they were getting hit hard with redemption requests. Comments over the past few months seem to be more reassurance to the remaining investors that were not able to receive their full redemption request.

2. The firm recently purchased some of the “best real estate” from the Signature Bank portfolio for pennies on the dollar. Without new capital flowing to the asset class they don’t need to worry about putting new flows to work. Watch out for when they talk about CRE having more problems than expected in 2025 or 2026 because then you will know that they have new capital to put to work.

3. The PE business has not had much opportunity to monetize underlying companies and time is running out with LP investors. Of course they are motivated to have us all believe things are “hunky dory” the reality though for many operating companies may be very different from what they are saying. Last I looked, they did not own AI winners so the outlook with refinancing needs and slower economic growth is going to be a problem for the operating businesses, for the GP who needs to monetize investments in companies made7-10 years ago, and for LP investors that are waiting for the distributions/performance that they were “sold on” when they made the allocation.

I am interested to hear others thoughts

Did anyone else feel a rush at the phrase: “banks were shredded…” On another subject, Golden Phoenix Jewelry is an omen of things to come worldwide: lots of gold holders/ETFs are not even really required under their contracts with “gold investors” to hold any gold. LOL Some don’t even own gold-foil covered, copper bars! LOL

When the economic storms blow their shields away, the gold holding/ETFs will be revealed to be utterly “nekked” underneath! LOL You “gold intestors” will be revealed to only be holding unsecured IOUs from con men–who even charged you “gold storage” fees on your imaginary gold FOR YEARS! LOL, LOL, LOL!

Sometimes, I even make myself laugh so hard that I laugh myself off my chair, when I reflect on those now poor, gullible, foolish suckers: “gold investors!” LOL

But wait a minute… if I buy gold to stack in the closet long-term, I buy the actual metal. So that’s one thing. But if I want to bet on the direction of the price of gold, I buy a gold ETF. And when I sell, I don’t ever want to get gold in return, I want to get dollar-fiat in return. That’s what I paid with, and that’s what I intend to make a profit with. If I buy a gold ETF, I don’t want gold but a betting instrument denominated in dollar-fiat. How do I get my dollars back, along with my profit or loss? By selling the gold ETF to some other investor in the stock market. It’s just like buying the SPY: I don’t want the underlying 500 stock certificates, or whatever, when I sell; I want fiat dollars, and I will get those from the market participants that want to buy it.

I understand the “want” and in a perfect world, we could trust all of our/foreign corporations (ahem, Luckin Gold, Enron, Evergrande, etc.), but sadly that is not the world we live in now. Thus, read your gold/ETF contract.

Better yet, have a really picky, careful lawyer, who actually takes a long time to read each provision, read it. Ask him, for a writen opinion letter, so he could be liable, as to the following:

1. does the ETF or “gold” deposit holder (LOL) actually have to hold any gold and if any, how much? 10% of “gold deposits?”

2. Is there any security or actual recourse to others if the company with your imaginary “gold” does not really have it and goes belly up?

3. Is there any potential fraud or intentional tort liability arising from the gold fraudsters charging you “storage fees” on imaginary gold deposits? (Good luck collecting from the CCP or other billionaires, who owned the gold-foil-covered-copper-bar company, if Chinese law or certain other countries’ laws are the laws that must be applied! LOL)

Doubt you will like his answers. Best advice: get your money out of the gold-fraud companies– before they fail.

Insist on gold? GET PHYSICAL gold and hike deep into the northern Canadian wilderness to bury it somewhere deep under a tree, so the big, gray wolves, and maybe sasquatches will guard it for you. They probably will ignore it. Worst case: you made a leprechaun very, very happy!

Do not get me started on Executive Order #6102, you gold hoarders! LOL Or read about synthetic diamonds before buying “real” diamonds! Those are just wunderbar too! LOL

I agree with your general comment that if you want gold long-term to never sell, get physical. Stack it in your closet. I said that, literally. We’re on the same page on this.

But that’s not a betting instrument. An ETF is a betting instrument, and I said that.

So in terms of your #1, #2, and #3 questions, with an ETF they don’t matter. Your liquidity doesn’t come from a company, or gold purveyor, or whatever. It’s an ETF, and your liquidity comes from market participants. You bought it from a market participant, and you sell it to a market participant. An ETF is a security that is traded in the market. It’s just a betting instrument, like a gazillion others. Goldbugs have for many years bugged me with stuff about “paper gold” is going to collapse because there isn’t enough gold or any gold backing it. It simply doesn’t matter. You’re trading a security for dollars, not a promise to deliver physical gold. There is a fundamental misunderstanding of what an ETF is.

Can ETFs lose much of their value? Sure. All securities can lose much or all of their value. That’s just part of trading securities. People take risks to make money.

My comments are really about gold “deposit” companies which often allegedly store ‘imaginary” gold. The gold ETFs that I am familiar with are gold contracts or maybe, you maybe include in the term mutual funds invested in gold mining or processing companies.

If those ETFs’ pools of contracts or underlying gold mining companies, etc., are fine, the ETFs are fine. If some are problematic, the ETFs that hold those will lose value when the problems are discovered. Physical gold may face an Executive Order 6102 problem if wars make the government confiscate it for weapons production. Gold is very useful for industry.

I wonder what financial cracks that will need to form before the FED comes in with a bailout.

Honestly, I am guessing everyone here is thinking the same thing or is it just me?

The cracks are already there. Janet Yellen is trying to add everyone she can think of to the “to big to fail” list so they can line up at the trough.

Nothing burger then? At least this will definitely be another nothing burger when it comes to having any effect on bringing down high or rather insane home prices..

Not a Nothingburger. A full-fledged Luxoburger. But it takes a long time to make. The people that make the burger have just laid out the bun and put mayo on it. Next quarter, they’ll add mustard and pickles. Then in Q3, they might add the first patty of meat. But this is a multi-patty burger, with an unknown number of patties yet to come. And then it will be topped off with cheese, maybe double-cheese, bacon, jalapenos, avocado, tomatoes, lettuce, and extra onions. They’re putting one ingredient per quarter on the burger, and this will take years. This is just the beginning of the burger-making. So we’ll watch it right here every quarter as the ingredients get added.

haha, sounds good Wolf, this burger sure do sound delicious, I will just request for that extra home price crash fries on the side please, especially for SoCal.

I’ll put my request in now, so I don’t have to wait in that long line when the reality finally hit MSM :)

Damn. I want those home price crashes too. Too much demand pull forward happend during zirp. There were mofos who were gonna be ready to buy their 2nd or 3rd home only a few years after 2019 or maybe not. Those fvckers got the 2nd & 3rd home sooner during covid due to zirp. People who could get their 1st home had to compete with these mofos or get outbid by them. Yeah, I hope there a mass job losses, especially for the mofos who have no business or financial stability to be owning so many homes. Let the fucking bread lines begin.

I hate that the FED & govt mofos keep doing this to us. I am not gonna vote until the FED has sold off all MBS in their portfolio and zero fvcking QE for the next 10 years. I dont wanna participate in a shithole “democracy” which is considered great only because its better than dictatorship.

Goldman – I understand and empathize with your frustration, but, the constant, always-unpaid-and-PITA, bottom line of a democracy is your informed vote and willingness to find,and work in concert with others of the same mind, and (a) not give up if at first (second, third, etc.) you don’t succeed, and (b) assume that an official ‘fixing’ of an ill of the polity will stay ‘fixed’ if/when you DO succeed. In choosing not to vote, it indicates to me you really are okay with the way things are.

An R.A. Heinlein aphorism, true of ANY governmental system: “…of course the game is rigged. But, if you don’t bet, you CAN’T win…”.

Best to you.

May we all find a better day.

1st Cav,

The keys words in your post are “informed vote”.

Democracy requires a well informed populace. Unfortunately that is severely lacking by a good portion of today’s populace.

This morning I literally had to sit silently while three idiots at my poker table talked about how the 2020 election was obviously stolen because there was more votes tabulated than there are registered voters. Not only is that assertion false, it is easily found to be falsenin about 10 seconds of googling. It doesn’t stop there, they continued to express false assertions about a recent big trial that took place in New York. Assertions that could easily be disproven by simply perusing the official filings in the trial. They are all online and easily accessible.

Unfortunately all three of these gentlemen talked about how they were regular voters.

If voters cannot take the time to understand basic facts, then the democracy is doomed.

I read Wolfstreet for writing like this : “Not a nothingburger, but a full-fledged Luxoburger”

It’s wonderful to read articles from people who write well.

Looking forward to the union of “Luxobuger” and “Druken Sailors” in a single sentence! ;)

Luxoburger not to be confused with Luxemburger, an extremely large sandwich (but small nation) adjacent to Germany, that exists solely as a tax dodge (you can deduct 100k Euro price of Luxemburger from your German taxes, so long as you reside in country long enough to sit through collected cinematic works of Uwe Boll).

Thanks WR

It’s a nothing burger

See my reply to Phoenix_Ikki, where in I explain that this is a luxoburger, but it takes them a long time (years) to make it, as they add one ingredient per quarter. They haven’t even put on the meat yet.

…but are these financial burger-preppers getting a pay raise, too?

may we all find a better day.

I’m sure I’m doing this wrong, I had looked at some of this data earlier this week for the first time and in BankFinder Suite comparisons (on FDIC site) I was seeing $250B+ all institutions non farm nonresidential noncurrent loan % of 3.07% vs the 4.48% in your article. Do you look at a different data set? I’m guessing the 3% might only include 90 days past due or something. Thank you.

I have no idea what you were looking at, but that’s fine. My data is from the FDIC’s official data dump yesterday, all downloadable. That 4.48% even got a special mention in Gruenberg’s presentation yesterday.

Ah, I see 4.48% it in the “quarterly banking report,” thanks for the reply Wolf. As always, great article.

Hi Wolf

Came across this –

“Buyers of the AAA portion of a $308 million note backed by the mortgage on the 1740 Broadway building in Midtown Manhattan got less than three-quarters of their original investment back earlier this month,” reports Bloomberg, “after the loan was sold at a steep discount.”

Would you have any insight on this?

Some analyst are claiming this to be an indication of defaults spreading fast and wide in the near future.

Thanks.

P.S. Sorry, it probably does not belong to this thread.

We covered the story of this office tower (1740 Broadway) a couple of times over the past two years:

Two years ago:

https://wolfstreet.com/2022/03/22/another-office-tower-goes-bust-blackstone-walks-from-manhattan-tower-it-bought-for-605-million-cmbs-holders-to-eat-remaining-losses/

A month ago:

https://wolfstreet.com/2024/04/24/how-itll-take-years-to-clean-up-the-office-cre-mess-with-losses-spread-far-and-wide/

But Bloomberg was wrong in calling this a “first loss on AAA debt since the Financial Crisis.” It said that the loss ratio for the AAA-tranches was 26%. But there were up to 100% losses on CMBS debt that had been originally rated AAA, and we covered some of those here too, including the largest office tower in St. Louis which became a 100% loss for all CMBS tranches. We covered a couple of office towers in Houston with much bigger losses for the formerly AAA-rated tranches than 26% (ca. 85% total loss ratio).

Do you know who’s on the FDIC’s “Problem Bank List”?

The FDIC does not disclose names.

General observation…

In the debt markets, there can be a lot of worry roiling the markets from below, but the wheels don’t fly off (and rapidly spike noncurrent/default rates) until enough panic pools to lock up the rollover/refinancing market.

Interest rates may gradually increase but so long as the latest liquidity-flush sucker exists to take over from the previous now-less-liquid disenchanted sucker, even the worst gut-shot debtors will stumble on.

It is only when enough lenders look around and ask “What the hell have we been doing and how the hell can this end well” that the lending window starts to close and the domino effect of panic takes hold.

There is a reason why the upward slope of default rate increases is so much steeper than default rate decreases.

My company subscribes to a service that tracks NODs and foreclosures. Due to our location, we are primarily interest in SoCal. The number of NODs are slowly increasing and has risen by around 10% Y-O-Y in our selected counties, cities and zip codes. Meanwhile, the regionals that we correspond with are becoming more conservative. Given the massive wall of CRE that is coming due, I fully expect a significant acceleration in NODs and foreclosures over the next few months.

To me the interesting questions are,

1) How were the inevitable implosions delayed so long? Nothing “good” economically was likely to come out of a pandemic…yet we saw a fool’s boom of let’s say 2-3 years and it took 4+ years for the real negative consequences to even really start.

2) Why *now*, finally? What were the proximate triggers? As much as I hate to say it, the Fed’s tracking of pandemic “excess savings” (and their recent extinction) seems pretty spot on.

This suggests that those “excess savings” really played a key role in the 2020-2022 fool’s boom. I think my mistake may have been to focus too much on the government giveaways by themselves (which inevitably were going to have to be funded in one way or another) – but an underappreciated major factor may have been the 2020-2021 reduction in “normal spending” with a concomitant increase in savings/investment.

So long as the various “excess savings” existed, the financial implosions were forestalled.

Now?

The Deluge.

NOD = Notice of Default

I 100% disagree that there was nothing good that came out of the pandemic.

I think one of the biggest positives to come out of the pandemic was a economy wide re-evaluation of the cultural relationship between people and their jobs.

What people did for a living became less part of their identity and more of just a job to pay the bills. As a result, workers are less likely to put up with crap at work. They have less loyalty to their jobs (which is good because their jobs have zero loyalty to them).

It has driven inflation, but I think it is good for workers in the long run.