And there were big upward revisions of the already hot readings for January.

By Wolf Richter for WOLF STREET.

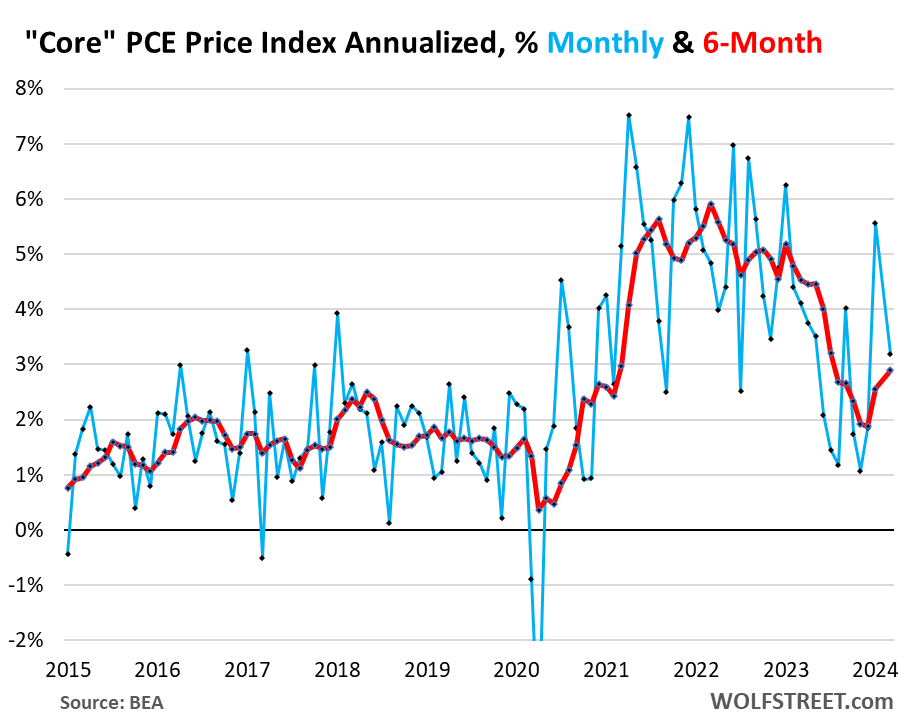

The core PCE price index, the inflation index that the Fed is focused on and refers to all the time, was revised up today for January to an annualized month-to-month growth rate of 5.6% (up from the original 5.1%) on a big up-revision of the index for core services to an annualized rate of 7.9% (up from the original 7.1%). In core services is where inflation is now solidly entrenched.

So in February, on top of those upwardly revised figures for January, the core PCE price index rose by 3.2% annualized from January (+0.28% not annualized), according to the Bureau of Economic Analysis today. This pushed the six-month annualized core PCE price index to 2.9%, the highest since July.

Powell cites this 6-month measure (red in the chart below) all the time because it shows the recent trend better than the month-to-month readings (blue), which are super volatile, and the year-over-year readings, which are too slow in reacting to changing trends. The Fed’s target is 2%.

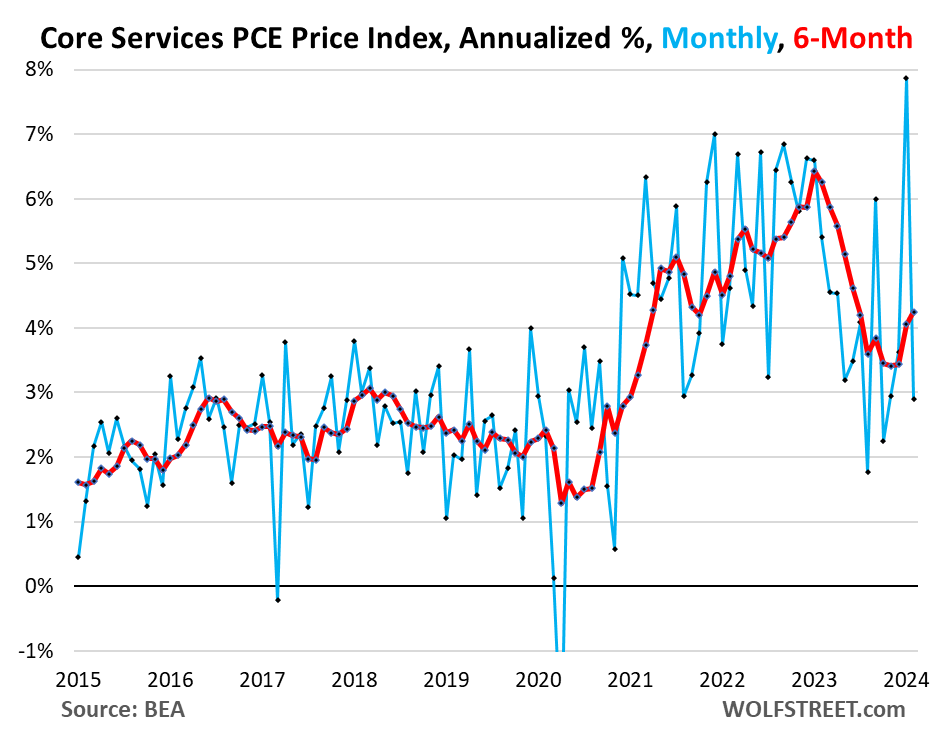

Core Services PCE price index is where the action is. Energy prices plunged since mid-2022, though they’ve come up again recently, and durable goods prices dropped, and those have produced the cooling inflation rates we saw last year.

But core services inflation – services without energy services – has remained at high levels and has started to re-accelerate. Core services is where the majority of consumers spending goes. And Fed speakers have discussed this issue endlessly.

The horror show came with the January reading of “core services.” In the reading released a month ago, the PCE price index for core services spiked to 7.1% annualized in January from December, the worst month-to-month jump in 22 years. Today this was upwardly revised to 7.9%.

In February, the reading of core services rose by 2.9% annualized (blue line in the chart below). And the 6-month reading rose by 4.25% annualized, the highest since June 2023.

For five months in the second half last year, the core services index had gotten stuck around 3.5%, which had triggered the discussion about sticky services inflation. But core services inflation then got unstuck and has ratcheted higher.

In the month-to-month readings (blue) since August 2023, we see higher highs and the higher lows. This is when the trend changed, but it was hard to see initially due to the huge volatility. Now it becomes clearer:

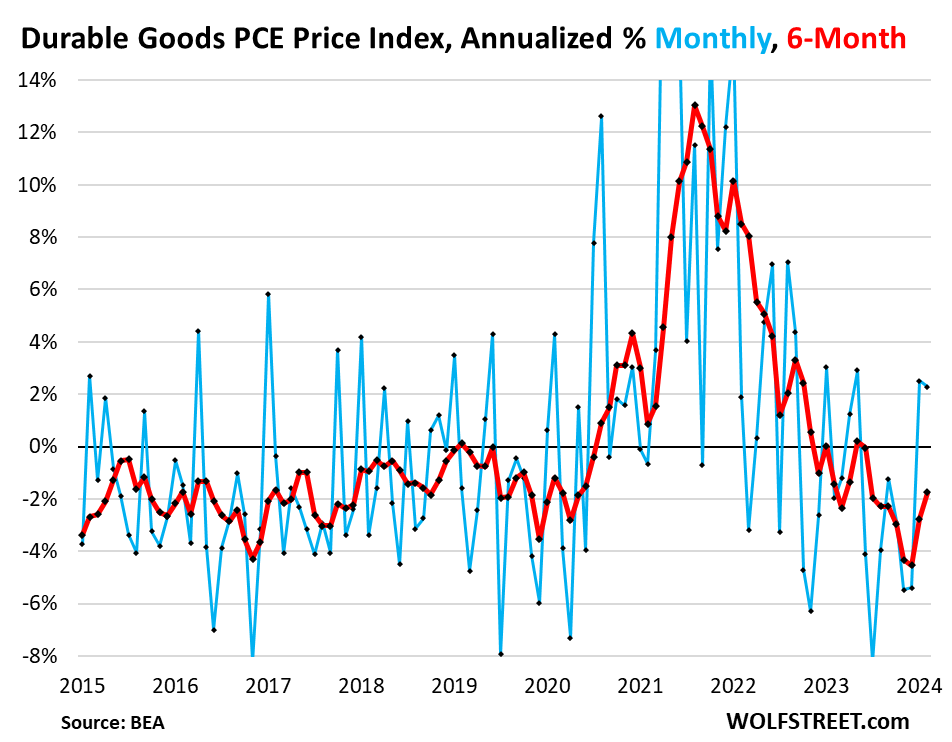

Durable goods PCE price index rose in February by 2.8% annualized from January, the second month in a row of positive readings, after a big dive into the negative (blue in the chart below). This raised the 6-month index to -1.7% (red).

What we’re starting to see is that the big deflation in durable goods has likely ended, and durable goods price developments are now normalizing, which removes some of the counterbalance to hot inflation in services.

Durable goods pricing is what we’re going to watch very carefully. It’s durable goods and energy that caused the big and very welcome cooling of inflation last year. But energy costs have been rising for months, and now durable goods are starting to become a concern again.

The 7 Core Services Categories.

Core services are grouped into seven PCE price indices. The month-to-month data in these categories of core services can be super-volatile (blue in the charts below), so we’ll focus on the six-month annualized readings, which iron out this volatility and show the recent trends (red in the charts below).

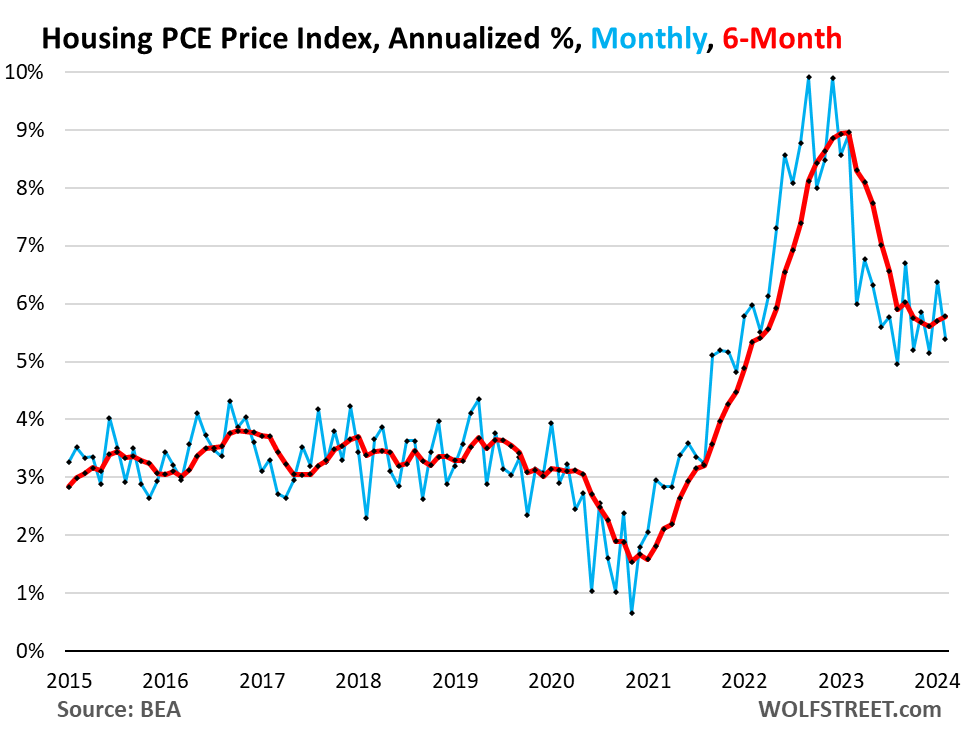

Housing, 6-month annualized: +5.8% in February, having hovered just under 6% since August 2023. The stickiness of housing inflation has surprised lots of people.

The housing index is broad-based and includes factors for rent in tenant-occupied dwellings; imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings.

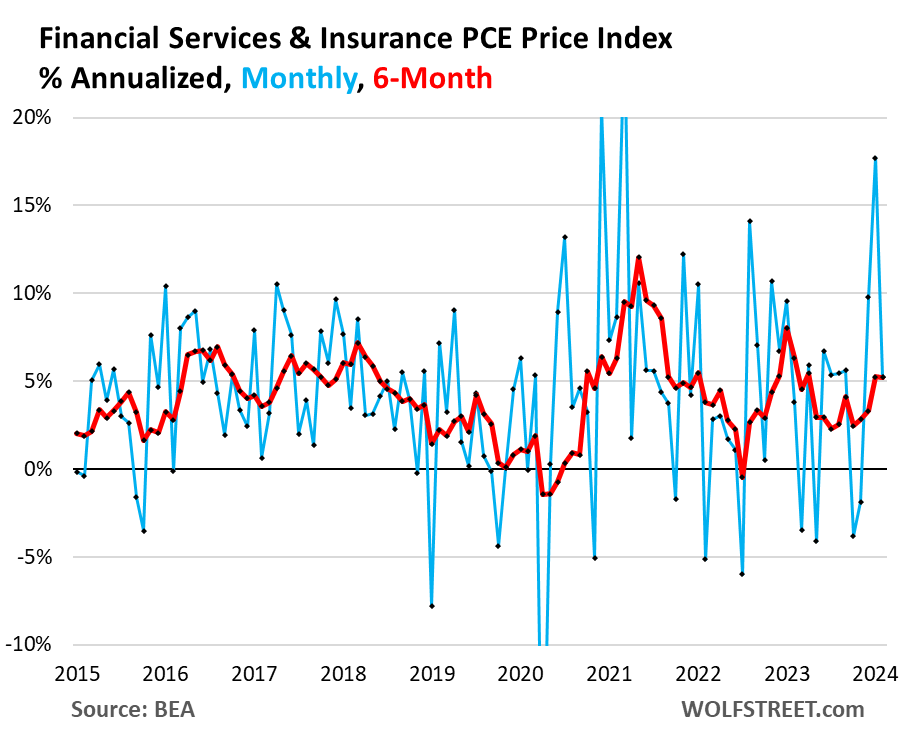

Financial Services and Insurance, 6-month annualized: +5.2%.

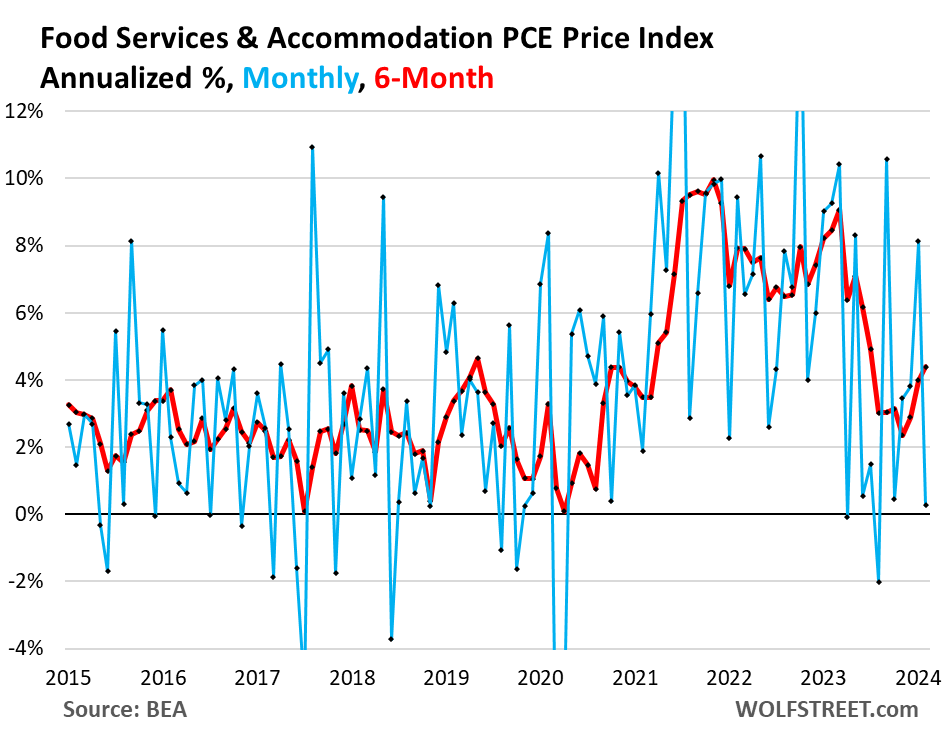

Food services and accommodation, 6-month annualized: +4.4%

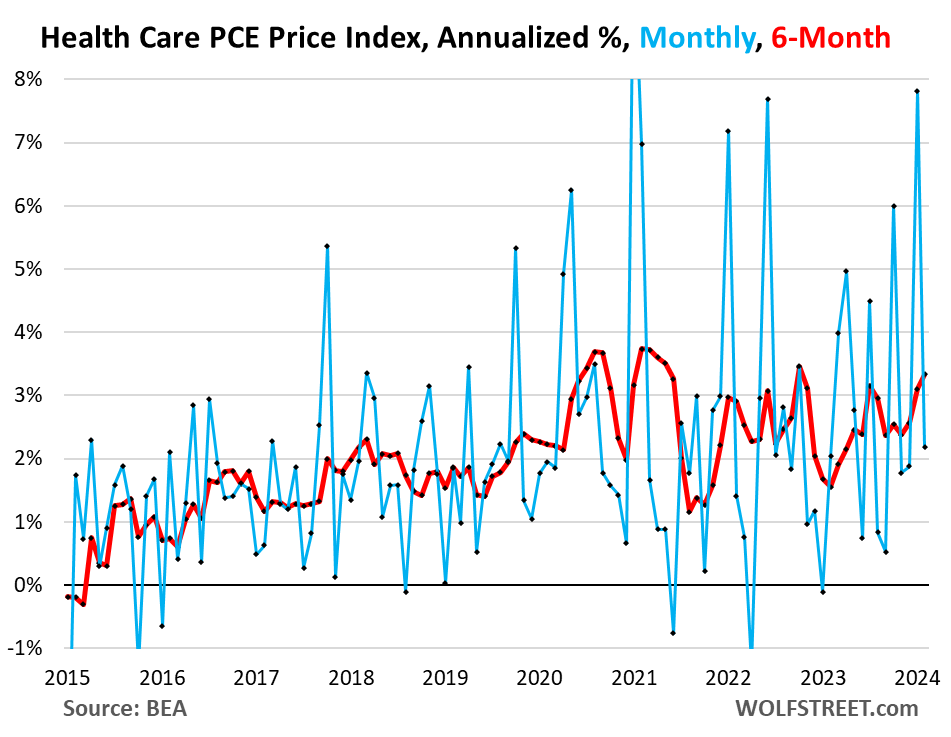

Health Care, 6-month annualized: +3.3%.

Transportation services, 6-month annualized: +4.9%.

Includes motor vehicle services, such as maintenance and repair, car and truck rental and leasing, parking fees, tolls, and public transportation from airline fares to bus fares.

![]()

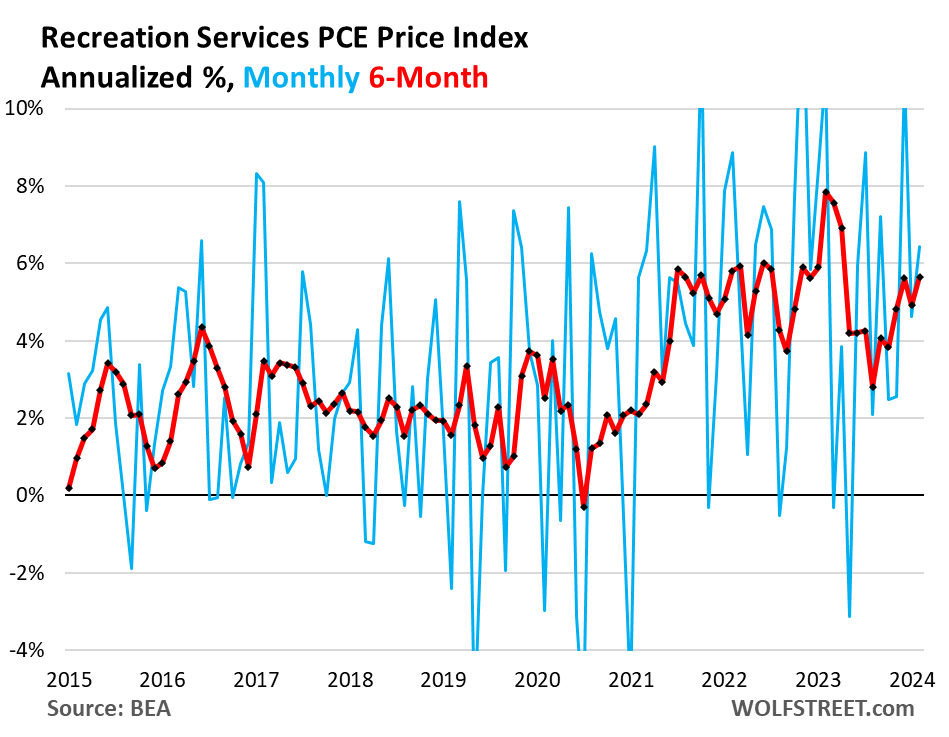

Recreation services 6-month annualized: +5.7%.

Includes cable, satellite TV and radio, streaming, concerts, sports, movies, gambling, vet services, package tours, repair and rental of audiovisual and other equipment, maintenance and repair of recreational vehicles, etc.

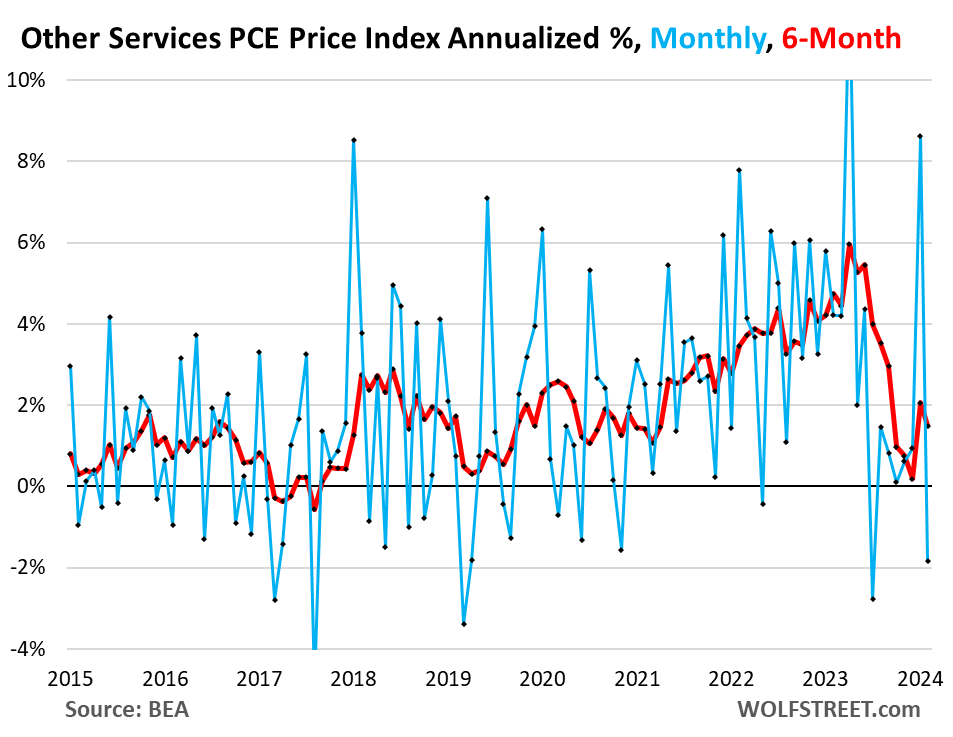

Other services, 6-month annualized: +1.5%.

A vast collection of other services, including broadband, cellphone, and other communications; delivery; household maintenance and repair; moving and storage; education and training across the board; professional services, such as legal, accounting, and tax services; union dues, professional associations dues; funeral and burial services; personal care and clothing services; social services such as homes for the elderly and rehab services, etc.

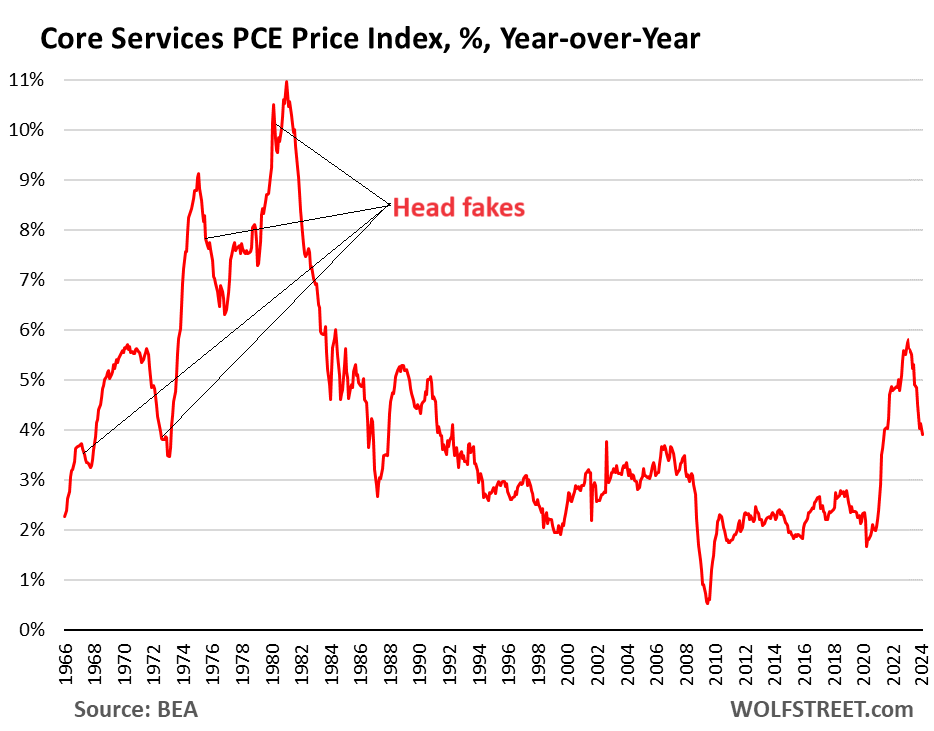

The core services inflation head-fakes last time.

Last time core services inflation of this magnitude and higher occurred – in the 1970s and 1980s – there were clear signs that inflation was cooling sharply, that the high interest rates had pushed inflation back down, which caused the Fed to ease, then the core services inflation resurged, and the Fed jacked up rates even further.

So this is the year-over-year “core services” PCE price index which excludes energy and the direct effects of the two oil-price shocks at the time. Powell has mentioned the risk of being misled by head-fakes a few times to support the Fed’s wait-and-see mode.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Fed is still scared of deflation more than inflation. Powell is incompetent.

The Fed let asset prices and debts run so far so long, it’s now impossible to predict what a recession would trigger. Markets are betting the Fed would never allow it to happen. The thought is that any significant asset price drop (say over 25%) would be met with immediate large scale monetary stimulus, so there is no reason for asset prices to ever drop. Instead, they keep rising.

I have to wonder whether it is possible to ever control inflation while QE remains in the toolbox for the next emergency. I think we’ll get 2-4% steady inflation as the Fed attempts to avoid recessions on a regular basis, then we’ll get sharp bouts of additional inflation in response to the inevitable emergencies.

Inflation can continue to run hot and long term interest rates can theoretically be kept in check as long as the threat of QE and ZIRP exists. It’s similar to the current nuclear deterrent that keeps countries in line.

Unsuspecting, trusting savers are the oil that lubricates the system and keeps it functioning.

“I think we’ll get 2-4% steady inflation as the Fed attempts to avoid recessions on a regular basis”

I think the FED would be happy to get 2-4%

This “deflation is automatically bad” mind-set is a big part of the problem, not all deflation is like what we saw in the 1930’s. Sometimes deflation is used to cool off speculation or gouging with prices, and it’s absolutely necessary then, otherwise Dutch tulips would still cost like 20K each.

In this case with the Everything Bubble and housing bubble particular, costs of even essentials have soared way beyond incomes and are damaging the purchasing power of Americans severely. And even if we have some deflation in the next few years, it would just be a corrective to the severe inflation since 2020, on net there’d still be some inflation since then. Some modest, sustained deflation right now would be not only fine, but necessary. Especially in things like rent, mortgage payments, cars, stocks and groceries. Paul Krugman has been especially bad with the blinders on but he’s not the only one. When inflation has been this severe and persistent and wages haven’t caught up–and most Americans can’t just up and leave their job to “get a raise”–then some deflation is fine. And needed. Another reason the Fed should take a tougher line with interest rates and especially QT, and read up on Paul Volcker for once.

Sustained deflation is terrible for an economy. Spending comes to a screeching halt (why buy something today when it will be cheaper tomorrow?), workers and businesses suffer (who wants to regularly get pay DECREASES ?), plus when deflation is more than temporary, it can be really hard to turn around. Furthermore it would probably lead to some severe issues for the dollar as the world’s reserve currency.

I have never met anyone who has a serious understanding of economics who wants sustained deflation. It is brutal.

It seems many posters here are committing the logical fallacy of Anchoring regarding prices. They want deflation to make up for past inflation. They are anchored on what prices “should be” in their mind and cannot get past that. A gallon of gas shouldn’t be $3.00 a gallon anymore than it “should be” $.25 a gallon.

Life will be better for them if they just accept prices as they are and adapt.

Play the game with what the circumstances are, not what you want them to be.

I understand and agree long term deflation is a bad this. One only need look to Japan to see how that has played out.

However, Miller has a point temporary and sector based deflation isn’t a bad thing. It flushes weak hands and forces reallocation of capital. That’s a good thing and makes our economy stronger and more diverse.

There is an irrational fear of the deflation death spiral. And it’s led to a lot of bad monetary policy especially over the last 20 years. It’s long last time to allow true price discovery in the marketplace.

There is deflation in durable goods — and that’s normal. Before the pandemic, the normal status of durable goods we a little deflation followed by a little There is deflation in durable goods — and that’s normal. Before the pandemic, the normal status of durable goods was a little deflation followed by a little inflation as manufacturing got more efficient and as technology advances. Just compare the prices of computers: in 1985, I bought my first PC and printer (daisywheel, LOL). It cost $4,000 then, and it had no hard drive, two floppies, almost zero RAM (640k), and was essentially a boat anchor. I just bought a new $800 laptop with 500 gigabytes of SSHD, a graphics processor, 16 gigabytes of RAM… it can handle more than a super-computer, costing many millions of dollars, could have handled in 1985. That’s deflation in durable goods, and it’s normal.

But deflation in services is not normal.

^^^ HEAR HERE ^^^

Even Econ101 teaches that.

Yea, I’ve been waiting to buy my first computer since 1975 because they keep getting cheaper and faster!

“Furthermore it would probably lead to some severe issues for the dollar as the world’s reserve currency.”

How?

Depreciation means the dollar’s value is increasing.

Sdarules,

I fully agree that temporary, sector inflation can be beneficial. Absolutely no doubt.

However, that is not what Miller was talking about. He mentioned sustained deflation, he mentioned deflation making up for past inflation.

Those are not the words of someone talking about temporary sector based deflation or the reallocation of capital. Those are all good things, but that isn’t what he was talking about.

I agree that there have been a lot of mistakes made over the last 20 years (I would even say the last 30 years), but thise mistakes were not made because of some irrational fear of a deflationary death spiral.

The mistakes were made because of catastrophic shocks to markets and an arrogant FED that thought they had new tools that were more powerful than they really were.

Powells 5.5 doesn’t impress the *fat lady.

Interest rate rises are welcome to me, being the greasy American that I am, treasuries= $

Seems a dog fight ahead for the have nots to get some breathing room, no fun living like a dog.

*fat lady is the US economy, lovingly.

Wolf, what do you make of the latest noise from Larry Summers, arguing the use of the pre-1983 methodology to include interest costs when calculating CPI?

This Summers stuff is BS. Economists say a lot of stupid stuff all the time, but now it fits into people’s narrative, and so suddenly he’s some kind of Jesus??

What the paper he co-authored proposed was to add mortgage interest rates back into the CPI basket.

Here is the paper:

https://www.nber.org/system/files/working_papers/w30116/w30116.pdf

If you add mortgage rates into CPI, then you would have had mega DEFLATION from 2008-2018 and then again from 2020-2022.

Yes, mortgage rates were part of housing CPI before 1983. But thank god they removed them because we would have had DEFLATION, which would have caused the Fed to go to negative interest rates and even bigger QE, which would have inflated home prices even more.

These economists are idiots sometimes.

Also life has changed. Lots of products and services that we have today that are in the CPI basket didn’t even exist back then. So CPI has to be adjusted to modern times. People who claim that the old method was better don’t have a brain. They need to look at how people today spend their money and how that differs from what they bought 40 years ago.

Summers is responsible for a lot of stupid shit, including helping repeal Glass-Stegall, thereby preparing the way for the Financial Crisis.

Here is a fun-to-read piece on Summers from 2013 when he was trying out for the Fed chairman job.

https://www.thenation.com/article/archive/return-lawrence-summers-mr-spectacular-failure/

This is how the article starts, to give you a flair:

“Tell me it’s a sick joke: Former US Treasury Secretary Lawrence Summers, the guy who tops the list of those responsible for sabotaging the world’s economy, is lobbying to be the next chairman of the Federal Reserve. But no, it makes perfect sense, since Summers has long succeeded spectacularly by failing.

“Why should his miserable record in the Clinton and Obama administrations hold him back from future disastrous adventures at our expense? With Ben Bernanke set to step down in January, and Obama still in deep denial over the pain and damage his former top economic adviser Summers brought to tens of millions of Americans, this darling of Wall Street has yet another shot to savage the economy.”

Extremely insightful. I’m always suspicious of Summers and it drives me nuts that there have been so few thoughtful responses to his paper. Considering the impact that may have had on QE decisions is particularly spooky. Thanks so much for taking the time to engage us readers. You’re greatly appreciated!

Summers, another demon seed birthed from the Creature from Jekyll Island :0

And don’t forget the affairs with Jeffery Epstein. May 5, 2023 – Former Harvard president Lawrence H. Summers met repeatedly with and solicited donations from sex trafficker and financier Jeffrey E. Epstein, the Wall Street Journal reported…

Totally agree. Larry Summers is an idiot who has succeed brilliantly despite his brilliant failures. He is part of the cabal responsible for dismantling the various regulations that served America so well for decades.

Always felt that Larry Summers and Krugman can never be right and can never fail.

They are positioned as economic experts by the political class who in turn can rely on them to recommend the policy the elites prefer.

Agreed. Can’t believe Summers still has much credibility after not only the GFC, but his and Bernanke’s “solution” of basically using ZIRP and QE to inflate the housing bubble. He’s a big reason we’re currently in this mess.

Economists have predicted 8 of the last 2 recessions.

Summers is out for Summers.

Listen to a real economist:

“The task of economics is to tell the remoter effects, and so to allow us to avoid such acts as attempt to remedy a present ill by sowing the seeds of a much greater ill in the future.” Ludwig von Mises, Theory of Money and Credit, Preface to English Edition

So would these “remoters” be known unknowns or unknown unknowns?

I don’t know Econ very well at all, just here to learn, so I thought it best to ask about a real economist’s view first rather than a fake one.

Larry Summers reminds me of how Buffett used to talk about intelligence.

Stupid people are obviously dangerous, but their danger is usually limited to themselves and those around them because they are stupid enough that no one willingly pits them in positions of power.

Intelligent people can be far more dangerous. They are smart so people trust/follow them. Therefore people will put them into positions of great power where they can do a lot of damage.

Larry Summers is extremely intelligent. Very intelligent.

One of the potential problems with extremely intelligent people is that they are often right. Far often. Growing up they knew all the answers in class far quicker than their classmates. Even early in their career they know the answers better than the co-workers. They are simply smarter than most they work with.

The issue is that they potentially never learn to figure out how to adapt when they are wrong. Since they are right most of the time they never had practice on what to do when they are wrong.

Don’t get me wrong, most stupid people don’t know what to do when they are wrong either. They are too stupid to even know they are wrong.

What is best is people who understand the limitations of their knowledge and know when they are certain about something and when they are fairly sure, but might be wrong. Knowing one’s limits is probably the greatest thing a person could ever know. They will lead a happier, more productive life.

Unfortunately Larry Summers never learned the limits of his knowledge. He never learned when he should be certain and when he should be more cautious with his opinions. He always thought he was right and he bullied others who were less smart than him (but more cautious), and led the country off of a cliff with the repeal of Glass-Stegall.

I’m an engineer and having worked with a LOT of really smart people, this is the most cogent piece of wisdom anyone could have ever written! I wish the world could begin to even understand this!

Thanks for your work Wolf!

I wonder about a different family of charts that reflect real effects of inflation in actual dollars. Maybe the Wolf Reality Index, WRI…

I find charting before 1975 unhelpful since the concept of value became only an opinion after going off the gold standard. I also think how CPE is reported hides Reality. It is a rate of change statistic, and many of us have forgotten our calculas classes and the first differential.

I propose 3 base curves for the WRI, each starting with $100 and beginning in1980, after the 1975 volatility, 2008 or thereabouts after the crash, and 2020 after the Rona Birus, as my grandson called it.

The first panel would have all 3 curves, standing in for the value of a Buck in the long, intermediate, and short-term intervals. Other panels would isolate one of the curves and graph it against values like the 2-year and 10-year treasuries, M2, the Fed balance sheet, or GDP.

I think the look and feel would bring the same sense of Reality as your housing bubble charts do….

“The Fed is still scared of deflation more than inflation”

This will never change for the Fed or any central bank, sadly!

Why is that sad?

Entrenched deflation is is far worse and far harder to break than entrenched inflation.

JimL-

“Entrenched deflation is is far worse and far harder to break than entrenched inflation”

I would be interested to hear how you would explain that to consumers and savers in Argentina, Lebanon or Turkey.

Easy.

I wasn’t referring to runaway, out of control inflation. I thought that was obvious.

There is no doubt that out of control inflation is bad. That wasn’t what was being referred to though.

I was talking about the more subtle choice of slightly mild inflation versus slightly mild deflation. It has been shown repeatedly that an economy can not only survive, but even thrive under a mild inflationary environment. I don’t know of too many economies that has been able to escape, let alone thrive in a continuing mild deflationary environment. Mild deflation sucks people into a death spiral more harshlyvthan mild inflation does simply because it goes against human nature. It isn’t human nature for people to expect pay cuts. It isn’t human nature for people to expect overall prices to drop (yes, it happens in certain sectors, but not overall).

Runaway inflation is terrible and definitely worse than mild deflation, but mild inflation is way better than mild deflation.

That was my point.

I’ve been wondering if total spending for durable goods has been increasing or decreasing. Energy prices as Wolf noted make up a part of durable goods production, but so does labor cost and commercial/industrial rent. Are durable good producers becoming more efficient and in return keeping inflation is that area somewhat cooler?

The opposite could be said for services, where labor cost for businesses can drive up prices pretty easily.

Update on inflation-adjusted spending — including on durable goods — coming shortly. Stay tuned.

I’m parked in a lot of T-bills, and if the Fed were practicing straight economics I would be confident I could roll those over into the same >5.1% rates for a while and even start lengthening duration while keeping above 5%. But it’s an election year, so all bets are off what rates will do, so I have a bit of risk in my “safe” Treasury strategy.

When will the enraged rabbit strike? I think we all know the answer to that question.

One thing the rabbit is probably working hard on……arranging all those director seats for the after federal retirement period. I hear the buffet served up at the Apple Board is much better than the one at Home Depot…..so…..well….why choose……sit on both and pass the wine and cheese.

It’s obvious to just about everybody that this FOMC has no intention of halting inflation……got to pay off that debt……good luck catching up to that whirling toilet.

What you’re describing is the scenario for higher interest rates forever. In your scenario, those low rates from a few years ago are history because inflation is here to stay.

Yep……..the boomers are not downsizing like most of us thought they might…..they are spending like maniacs in retirement with lots of ammo and the millennials want what daddy has at age 65 at age 33. Demand is exploding while the dollar is shaking over the long term for a variety of reasons. Meanwhile DC, no matter the party spends, spends and spends.

While the fed fights deflation.

The fed might drop rates a smidge, but to think we’ll see rates similar to the last decade…..nonsense.

Which is why IMO central banks that are unfriendly to the US vacuum up gold. It was just a decade and half ago that we ran 4.0% inflation every year and everybody thought it was just fine.

Of course, having done this for 60 years, I’am fully prepared to completely pivot in a NY second should AI or another black swan arrive.

Millennials and gen Z are getting daddy’s money at 33. A recent study showed that twice as many members of these younger groups are getting help from their parents to buy homes. It’s gone from The High Teens to the mid 30% range

I posted this about a year ago, so given the environment, thought it a touch of irony and am reposting….

”

Volcker proved in the 80s the way to quell inflation is to raise the target rate above the inflation rate. Powell is not doing that (target rate currently 4.75%, and probably going to 5.25%, while inflation is 7-8%). Powell is testing a theory (the “soft landing”) by raising rates somewhat below the inflation level and then speculating those rate increases will bring down inflation over time. It remains to be proven this approach will work. Instinct says this may work over time, but the time frame is uncertain and unlikely to be short (I’m guessing 24 – 36 months?). When Covid hit, the Fed dropped rates to zero for two years – I suspect it will have to keep the 5.5% target for at least two years to balance the effect of their (panic) move in 2020.”

Inflation is still not where the FED or anyone else wants it to be, but it definitely isn’t at 7 or 8%. That is just crazy.

It was a year ago.

Yes. It was also more than 7% or 8% on the 1970s, but what does that have to do with right now?

I have legally driven 140+ miles per hour on the autobahn many years ago in Germany, but that doesn’t mean anything when I am currently stuck in traffic on the 101.

The poster I was referring to was talking about current rates versus current inflation.

I am more than open to the idea that the FED will have to raise rates. In fact, being a betting man, I would bet on a rate hike before a rate cut, but I also think it is close.

I think dealing with current facts as opposed to what the facts were in the past is better.

I read 2 articles on the numbers before Wolf’s and wolf was the only one to call out the January revisions. That’s why this website is indispensable in a world of race-to-the-bottom quality mainstream journalism.

Howdy Alpha. YEP Always knew everyone was a comic show. Nice to find truthful information…..

The charts are still VERY clear. The FED is going to cut rates by some 0.75%, in spite of “high inflation”.

🤣❤️

People don’t give up, do they?

LOL!

– I can say the same for one Wolf Richter because he doesn’t know what he should be looking at, what metrics to look at.

– The charts (from e.g. Stockcharts.com) are even saying that there could be a rate cut as soon as next month (april 2024). And that doesn’t bode well for the stockmarket(s). Mr. Market will tell us in advance.

– Mr. Market is very clear: up to say october/november 2023 there was a chance of the FED hiking rates. But after october 2023 Mr. Market has continued to say that the chances of rate cuts are (much) larger than rate hikes.

– Mr. Market also told me in the last 4 months of 2021 that rate hikes were coming and that was well in advance of the actual rate hikes.

“A rate cut as soon as next month (April 2024)”

You people are a joke. Your “Mr. Market” is not only a joke but a hilarious joke. Last December/January, your Mr. Market predicted 6-7 rate cuts in 2024, starting in January 2024, to the amusement of us all, LOL.

You think rate cuts would be bad for stocks?

Yep, half the world is wishing for lower rates to buy homes or has a child or grandchild or other family member waiting for the same thing

That is the problem for many people. They act on what they “wish” the facts were rather than acting on what they actually are.

Howdy Folks. Follow the dots I say. Seems to be a better indicator than anything else. Never would have found the dots without Wolf Street.

The rise of the $20/hr minimum wage is only going to increase the devaluation of the dollar and push inflation higher. There’s way too much money still floating around and I can’t see anybody seriously tackling either of those issues until after the next prez is sworn in, if at all.

It’s always funny how it riles people up that the lowest-paid workers get a raise. You just want the cheap lunch? It’s not those poor schmucks that are going to drive inflation, it’s the people with their $200k paychecks and stock compensation packages that pay whatever for anything.

Thank you Wolf the low wage gains I had for 3 decades of the 1980s 1990s and 2000s made life difficult. The lower middle class are still very squeezed and any welcomed higher wage yes may be inflationary. You are so right about the to 20 percent driving the behavior they do just buy whatever . Both my kids mid 30s are in the 200k range. One is getting new windows and a patio total cost of 50k and neither is needed the other is in Mexico for spring break family spending 20k for a week vacation . Top paychecks lead the way for spending

I spent the afternoon cleaning up dog shit for my blind neighbor, he’s got a beautiful shepherd named Marco and he needs help in many ways. He’s a tough old bird, good to have a friend.

Now back to kung fu, the series. Qui chang kain ( David carradine) he didn’t need much of anything, walk around shoeless, no money. Kick somebody now and again. Recession, depression he didn’t care, just pull some bulb from the ground for a bite to eat…

“It’s not those poor schmucks that are going to drive inflation, it’s the people with their $200k paychecks and stock compensation packages that pay whatever for anything.”

An excellent point, Wolf, thank you.

The working poor can barely survive buying only bare essentials, which sucks doubly for them when inflation rages. Even worse, at some price-point employers will just offload those workers for cheaper options, like Pizza Hut cutting over 1,100 drivers and using 3rd party contractors ahead of mandated wage hikes.

Tale of two worlds. In Seattle, I estimate 100,000 families tied to the tech industry are making $400k to $1M per year, plus additional huge amounts for stock appreciation on past stock grants. They are spending on everything like drunken sailors. These are employees of Microsoft, Amazon, Facebook, and Google. Dropping $2-3M on a house might just be a couple years’ worth of income and gains.

If these companies can afford to hand out so much wealth to so many employees, it makes me wonder if there is a competition issue.

Not to mention, where I live a $20/hr job offer would bring the town to a stand still. Everyone would be laughing so hard they wouldn’t get anything done!

I think people should be paid higher, based on their abilities. Those $200k jobs are the direct result of the loss of purchasing power, and that’s driven by (among other things) the minimum wage.

The minimum wage is what you pay people who have no skill set. And anyone over the age of 25 lacking the skills to make more than that has wasted a huge portion of their life. It used to be that schools trained individuals to be able to make a living wage upon graduation from High School. If you wanted more, you figured out how to make it; learn a skill, get more education, whatever it takes.

There are a lot of jobs that pay very well, even if you never graduated HS, but they do require you get up, and go to work, and learn how to do that job. The problem is they are usually physically demanding, not attractive, and require the individual to actually show up, every day, on time, and WORK.

I can name a dozen career fields looking for employees where an individual can make six figures after a few years training. But they’re not for people content to make minimum wage.

Jobs are what you do to be able to live in the lifestyle you want. The idea that society should support your lifestyle no matter how productive you actually are has never worked.

I’ve worked for minimum wage. It sucked. I spent a huge portion of my time and earnings getting skills that made me more employable. I worked 2-3 jobs at a time most of my life. I traveled the world taking jobs that made me more money. My incentive was not to have to depend on society to live, because I never wanted to live in places where you could get by on welfare or minimum wage.

You think it’s great they hand $20/hr to the guy flipping burgers or pouring coffee? I think it totally sucks for the guy who spent his whole life working for a retirement that gets devalued every year.

Yes, you do want that cheap lunch, that’s all you care about. I was afraid of that.

I am someone who earns more than half a million a year.

I can tell you with all honesty that I don’t deserve to be paid this much.

My ceo makes much more than me and he does not deserve that

I am very happy that minimum wage is going to be 20 per hour.

I have friends who make as much as me and they think they deserve more .

Wolf they aren’t the lowest paid anymore. And they weren’t before the law passed either.

I see many postings in establishments with wages lower than 20 an hour(just saw one for 16.50 an hour the other day). What the CA government is essentially doing is A) squeezing out franchisees and ensuring corporate owned only stores are feasible due to their ability to spread cost spikes. And B) CA is using the fast food industry to influence all other low skilled jobs with an arbitrary panel of unelected bureaucracy that can hide behind people like you saying “you hate the poor people”. Wage law should be just that, law. not subject to whims of an arbitrary bureaucracy.

Are you in favor of large faceless corporations over.mom and pop franchisees?

I’m in favor of paying the lowest wage-earners more.

The estimated impact, assuming prices are passed to consumers which is reasonable, is 2.5% to 3.75%.

It surprised me that there were FRB members willing to continue forecasting 0.75% rate cut by end of year, when reinflation had resumed compared to when that forecast was first made. Yes there were changes to the tails of the dotplot, but those were completely overlooked or ignored.

In addition, if the goal is to bring down inflation, then surely it’s more effective to telegraph a delay to rate cuts, so you’d think there would be an incentive to err on that side.

How does one get these FRB jobs anyway? Wolf can we nominate you?

Heck, at my advanced age (retired, pretty old), and a career engineer, I should be qualified for one of those FRB jobs since I can easily place a dot on a graph!

Sorry Anthony A.

You are over qualified for the job!

I will admit that I was mildly surprised when many of the FED members were still predicting three rate cuts. That said, it wasn’t too terribly surprising. It is simple human nature. It is the FED’s job to fight inflation. Ask anyone holding any job in the world to predict their future performance. Almost everyone will predict they are going to do their job well. If the FED does it’s job well they will be easing rates as inaction moderates.

Baseball is just starting. If you went around and queried every major league baseball player as to what their teams winning percentage will be at the end of the year, you will find that in the aggregate, they predict their team will finish above .500 which is mathematically impossible.

Human nature.

It should also be noted that the FED isn’t supposed to be predicting future inflation and rate cuts. Their job is to look at CURRENT existing data and decide what to do. Having people making predictions when predictions are not part of their job is silly.

I have never liked the FED dot plots. I understand why they started it (they wanted to provide more transparency into how FED members were thinking), but it is a poorly constructed way of doing it. For one, they are asking people who are not trained to predict the future to make predictions. For two, as described above, it will incorporate too much human bias to make it worthwhile. For three, it reduces a very complex topic that no one completely understands down to a simple dot plot. The economy is very complex and there are always unknown factors that greatly affect it. No one knows when war is coming, no one knows when there will be weather related affects to the economy, no one knows when there will be a pandemic, etc. There are numerous factors that affect the economy and are completely unpredictable. Reducing all of that to a simple dot plot is silly and is more unhelpful that anything.

The blue lines for most of the services look like scribbles!

The 6-month average red lines don’t provide much of a smoothing function, except for housing.

How can anyone make meaningful decisions based on interpreting it?

The volatility of the data and the upward moves of the 6-month trend are the two reasons why wait-and-see is important.

I guess Powell imagines he has always had to allow inflation. People imagine that because deflation and inflation are kind of opposites that there must be some sweet spot between the two, actually there isn’t. Either you raise interest rates to levels where there are substantial defaults or you continue to debase the currency as fast as you can. There is no middle.

Even on the Feds own highly dubious figures of 4.7%, 8%, 4.1% over the last three years thats almost 18% inflation over just three years compounded.

The problem is that the rate is simply too fast and I would also say that that policy makers imagine they will always have levers to pull and control of the situation, but history says exactly the opposite. The problem is when the brakes really need to go on the debt level will be too high. I read recently that every 100 days now the US adds 1 trillion in public sector debt.

On bright side, it’s fun to watch, as long as you own enough stocks and commodities to keep pace with inflation. Also need lots of dry powder in case of deflation.

The Fed may like walking the tightrope over a 2,000 foot canyon, but investors don’t have to.

But we don’t own enough and our earning power as a retiree is limited . My biggest challenge as a retiree is fixed costs going higher

Why do you consider the federally calculated inflation rates to be dubious? What are you basing that description on?

Also, just to be clear, the FED doesn’t calculate inflation rates. They use data provided by departments of the federal government.

He prefers the private-sector lies that are being proffered to shock people who cannot do compounding math into spending money on newsletters or gold-bug stuff?

I agree with that guess, but i wanted to hear him verbalize it. Sometimes forcing people to verbalize their beliefs makes them realize just how crazy they are. I hoped to help him even though it was unlikely.

How can inflation slow down or even stop while the national deficit is going up exponentially the FED has to print more money in order to sustain that so inflation will not end here. This nonsense of 2% inflation is just that nonsense just do the math. You are looking at 15 to 20% real inflation until something is done about the deficits. It’s sort of like leapfrog.

Wolf,

Wow! Just WOW!

Now that I’m retired I am trying to relearn (unlearn?) the economics I took 5 decades ago in college. Your blog is one of the clearest, most insightful, and unbiased sources of information I’ve found.

You don’t seem to have ‘an axe to grind’.

You let the numbers speak for themselves.

And then explain what they mean in a very clear and understandable manner.

Please … keep on keeping on.

Clearly the most vulnerable in society will continue to suffer. California is facing significant budget issues for the foreseeable future and other states such as New York and Pennsylvania are very serious. Many other states have issues although more easily manageable. There must be more creative solutions than what we seem to be sticking to. Those seem to be untenable for a lot of reasons.

Was looking forward to your writing on this as soon as the PCE came out this morning. I’m beginning to understand a lot more Wolf. Looking forward to the durables. Thanks so much.

This adds to the lag quagmire — accelerating inflation and higher for longer stressful yields and the dynamics of post pandemic zombie survival. The brake pads on the runaway train are becoming more of a concern as the train picks up speed. lol — a really soft landing for a resilient black swan that refuses to die.

The resilience of zombies is a balancing act — on one hand, cash burn is a slow progressive cancer, but on the other hand, they’re learning to survive with less and less hope.

The talk should not be about rate cuts, but rate HIKES. The FED is always leaning towards juicing and pimping the markets. Instead of saying “we will need to see xyz before cutting rates,” they should be saying “if xyz doesn’t happen, we will be raising rates.” The bias is ALWAYS towards inflation. It’s a scam. The FED is crooked.

The Fed:

Crooked? Probably not.

Stupid? Probably not.

Inept? Probably not.

Trying to solve for polar opposites at once? Probably…

Your inability to comprehend does not make it a scam or the FED criminals.

You continue to blame others for your own failures. The first step to doing better is to look at yourself. Your constant victim mentality will ensure you are always a victim.

Respectfully, labelling “them” as idiots or incompetent is missing their intent. If one looks at an income inequality graph, it is clear “them” is working successfully for the ~1%’ers and the 0.01%’ers.

With cumulative inflation of 25% to 35%, those that can increase their wages/salaries/prices will do so. Those that can’t are screwed.

And governments (which have these cost increases too), will shift to larger deficits, higher taxes, and down load services/taxes to the municipalities.

Hence, the for now higher inflation continues; especially in services.

Loss of western productivity and manufacturing has a serious consequence. Not all services are a necessity. Substitutes to cheaper goods creates fissures.

The outlook is not good; for most of us.

The fact that you refer to “cumulative inflation of 25% to 35%” demonstrates that you are committing the logical fallacy of anchoring. Depending upon your starting point, inflation has accumulated many orders of magnitude more than 25 – 35%.

Seems like most of the core services inflation is caused by higher interest rates, or interest rates have no effect. Housing is expensive because their isn’t enough. Higher interest rates aren’t helping that, although lower interest rates would probably push single family homes up. Healthcare is a function of an aging population and the terrible lifestyles of way too many people. The cost of automotive services is catching up to goods inflation. It became more expensive to fix cars and now insurance is rising to account for that. Mechanics need to make more money to keep pace with inflation and it’s finally starting to show. The only place higher interest rates should have an effect are things like cable tv, streaming services, etc which one could argue whether or not that should be included as these aren’t things a person actually needs and as subscribers fall, prices tend to rise instead to make up for it.

The tv cable internet has fixed expense and i would expect them to increase maybe more than inflation since technology and infrastructure has to be replaced frequently

The commodity that has experienced the largest drop that has kept inflation at bay for decades is energy. Oil prices in 1980 were 40 usd a bbl and Natural gas was north of 3 usd . NG use has grown since 1980 and generates a great deal of USA energy plus exports and currently has large supply at current prices plus price is under 1980 price siting at around 1.76/mmbtu!! Go energy and fossil fuels

While an aging population that regularly engages in terribly unhealthy habits are certainly factors in the price of healthcare in this country, they don’t come close to being the biggest cost driver of healthcare.

The way our healthcare is set up in this country is one of the biggest drivers of cost.

“Mechanics need to make more money to keep pace with inflation”

Sure but like all things, raising the price too much will drive away business. And we live in an era where you can find free Youtube tutorials on how to do most repairs & maintenance,

Great article Wolf. The elephant in the room is the US debt and increasing deficit spending. At current interest rates the annual US debt servicing expenditure has become one of the biggest if not the biggest govt spend. Unless the govt commits to drastically cutting spending ,this debt can only increase. Inflating away the debt appears to be the only way this can happen and Powell knows it.

Apparently the Gov’t can only cut taxes on the wealthy and corporations and never increase their taxes to reduce the debt.

They’ve been doing it since the ’80s at the expense of Middle Class Americans.

Powell PR interview today seemed a bit too cavalier and overconfident, as well as too pre-scripted. It’s like an echo chamber with virtually everyone confidently exuberant about inflation being vanquished as the economy explodes with powerful growth.

It’s getting harder to be pessimistic. What’s equally bizarre is that universal attitude, universally agreeing that Biden screwed up the economy, thus bringing up the the concern about what follows this recovery period.

I’m burning out on this game!

Yes, historically, the Federal Reserve has often been considered a lagging indicator, reacting to economic data rather than proactively influencing it. The challenge lies in them being data-dependent, which can lead to delays in policy adjustments. The current economic growth may persist for another quarter (or two), bolstered by upcoming events like the Euro Cup and Copa America. However, shifts in the narrative come fall could alter market sentiment, potentially impacting forward indicators like CPI, PCE, and PPI. But then cuts might get a whole different meaning for the “market” (such as, recessionary??). Market psychology is easily predictable nowadays.

The FED should be reacting to economic data rather than pro-activly influencing it. To be pro-active requires a person to be knowledgeable about the future. This is absolutely impossible given the complexities of a market economy.

I would say keep an eye for those initial jobless claims.

We’ve been doing that for two years, and what we keep seeing is that they’re near historic lows. “Continued claims” are may favorite inflation indicator, and they’re still very low.

From today’s Wall Street Journal afternoon briefing: “2.5%… The increase in the overall personal-consumption expenditures price index over the 12 months through February, the Commerce Department said. The bump in the Fed’s favored inflation gauge and the 2.8% rise in core prices excluding volatile food and energy prices were in line with forecasts. Central-bank officials last week reaffirmed their projections for three interest-rate cuts this year, though the timing remains uncertain.”

In other words, nothing to see here people, move along. Cut those rates, Fed.

Thank you, Wolf, for helping us to see through the nonsense and understand what’s really going on.

I saw that. The propaganda is disgusting.

The good thing is that the Fed people aren’t getting their info from the WSJ. They’re looking at exactly the stuff I’m looking at, and they’re talking about the three-month and six-month inflation rates all the time and cite them as reasons to wait and see.

The WSJ contains a lot of propaganda. Every day I tell myself I should cancel my subscription. But then I don’t. They do have some good stuff, but economic and Fed coverage is not one of them. They do have a great cartoon about office life at an ad agency tho

That is what you get for reading the Wall Street Journal.

Use better sources of information and you won’t have to deal with nonsense.

My bank (Wells Fargo) must have anticipated this and be thinking higher for longer. Suddenly they are offering 5.05% short term CDs, formerly 4.4% …… and 4.6% passive savings account no minimums – as long as there is 10K all accounts combined. Or they just need deposits badly.

I actually got a call from Morgan Stanley with a special deal for 900k minimum for new money. I didn’t have that much available so I did not get the details. But very interesting that they are getting that aggressive.

Wolf,

Thanks for giving real and complete picture on Inflation. I like many here appreciate it.

On another note, today I watched Powell’s talk in SF FED on 29-Mar-2024. Personally I felt, interviewer did good job. It was lot more informal style than prior ones. Powell answered most questions very openly and clearly and explained thought process. Many times he said we don’t know and we will let data tell us. He clearly said if we dont get the data what we expecting, they wont cut the rates. He even talked about QT, separate from Rate policy and may even reduce the balance sheet more than previously thought. As usual mainstream media twisted the words. It was a mainstream article which told me Powell spoke in SF today. So I went to YouTube to watch it to view the original.

I think next 3 months CPI and 2 months of PCE reports will clear the picture. Many people think FED maintained the 3 rates in March SEP. They still dont see how dot plot changed. Only one said more than 3. It was very close call. I am guessing many will move to 1-2 cuts by June SEP.

I agree… it was a VERY interesting interview in San Francisco this morning, if only because of the laid-back style of the interviewer. In fact, his voice and interjections reminded me of Jon Stewart (WITHOUT the politics). He showed some humor but examined in more depth a few topics that usually just get glossed over. He repeatedly, repeated a question, saying Powell didn’t really answer it originally… no real news, but it was more in-depth than other conference discussions and the post-FOMC press conferences.

They need deposits badly. No rate cuts look at how the fed gets paid.

when you make a lot of money for not doing anything- Congress- politicians- Powel-Yellon. These people do not have inflation. When you work hard and try to feed the kids and pay rent, a car maybe a mortgage, and make 100,000$ then there is inflation. So when the cost of things rises it affects the rich not at all.

Good to see lagging indicators doing their job. Since March 2020 self induced crisis we seen everything bubbles from Bath, Bed, and Beyond. PPP loans, and Crypto. Mortgages and student loans deferred for 2 years and a run on physical assets right down to treadmills. 4 years later there are indeed winners and losers, market participants are the true winners. I see and hear the 18-35 y/o who are not giving up but choosing video games over marriage and the white picket fence. They don’t need a dot plot to tell them that things are out of reach.

Granted, playing video games is not very productive, but it can at least be entertaining and occasionally educational.

What is the value of white picket fences?

I know you are going to be dismissive of my question by saying your use of a white picket fence was symbolic, but my question referred to your the greater point you were trying to make.

The FOMC jumped the gun talking up rate cut prospects. It sent asset prices up and the dollar down, just what Powell said they wanted to avoid back in 2022, and which has already started to filter into lagging government inflation series.

Ironic. By stoking early rate cut speculation, they might have to put off actual rate cuts longer.

The FED didn’t talk up rate cuts anymore than they talked up rate hikes. They have made it fairly consistently clear that they were going to react to what the data told them.

Now, to be fair, many news outlets have spun that into rate cuts in the near future, but that is more a problem with the news sources you use than it does the FED. Use better sources and you will be better informed about FED thinking.

I am pretty sure the FED (as a whole) has been waiting for a clearer picture of inflation before they reacted and moved rates in either direction. The last thing they wanted to do was react too early (either way) and then have to yo-yo markets by undoing recent previous hikes/cuts. They want to make sure of the future direction of rates before committing.

I think they are/were smart to do that. The last thing the economy needs is the FED whipsawing the economy back and forth by cutting and raising rates willy nilly every few months.

That said, I think it is becoming more and more clear that rate hikes will likely happen before rates are cut. I think gradually rising inflation is more than just a head fake. It is still a close call, but the signs are pointing to higher inflation unless something is done.

If I was going to bet, I would bet on rates being higher before they go lower.

That said, recessions are always around the corner and always unpredictable. Much of the rest of the first world is fearing recession more than runaway inflation. The US is rather unique in this regard. So I also wouldn’t be surprised to see foreign recession to seep onto the US economy.

The Federal Reserve needs to talk about increasing the interest rate. The FOMC has cleverly framed the debate around rate cuts and we are all waiting on pins and needles for inflation to explode when they do. Your charts make clear that staying the course isn’t working. It’s high time for the FOMC debate to return to how much rate increase is required; especially since Jerome Powell says he is data driven.

Interest rates at 5.5% are above all year-over-year inflation measures, so those rates are fairly high. They may not be high enough to do the job, but that’s not certain yet, and it will take more time to determine.

Shorter-term inflation measures are heading up. So that’s a new trend. But we don’t know if that trend will continue.

But here is the thing: forget about the Fed wanting to eliminate inflation. They want to keep a lid on inflation, they don’t want it to blow out, but they want moderately higher inflation and a growing economy because the huge and ballooning federal debt cannot be deal with in any other way. Just imagine what happens when we have five years of near 0% growth rates interrupted by recessions which totally blow out deficit spending and the debt. This would be a fiscal catastrophe. So they’re keeping rates high enough to keep a lid on inflation, but not so high as to throw the economy into a recession. This is where they higher for longer — or really higher forever — comes in. Both: higher interest rates and higher inflation, essentially for as far as the eye can see, but not too high.

If we must have elevated inflation for many years or decades to survive financially, is it possible to defend monetary policy decisions and communications at this point?

The Fed still insists there is a 2% target, so if 3-4% inflation becomes the norm, a deception is in the cards. On the other hand, if the Fed really thinks it can achieve 2% inflation in a year or two, but it clearly cannot (based on current policy of avoiding recessions), perhaps there is ineptitude, as opposed to deception, but either way the public interests are not served.

Over time it will become evident 3-5% inflation is the realistic goal to which monetary policy will migrate, assuming recessions are continually avoided via monetary interventions. Long-term rates will blow unless interventions increase, not decrease, with QE, yield curve control, etc.

Assuming nobody would explicitly agree to a government takeover of the yield curve, monetary authorities around the world can be criticized for lack of transparency AND not having a legitimate exit plan. The public wants capitalism with a safety net. The public deserves to know whether market forces or government will be dictating interest rates over time.

It is practically impossible to have a fiscally responsible government in the US. Even so-called fiscal hawks want to bring home the bacon (=pork barrel spending). And no one wants to increase taxes to pay for it. So here we go: inflation is the only solution. They all know it, and that’s what we get. I’m not saying it is good, but that’s the system we have, and I’m trying to explain it.

Thanks, Wolf. These are some of the most insightful comments.

From a lay perspective, what I don’t understand is, wouldn’t the higher for longer interest rates negate the effects of “deflating” the debt, since the Federal government will have to pay higher interest payments on the existing debt?

Hot off the press to address your question — the interplay of the ballooning debt, rising interest rates, and inflation which also inflates tax receipts:

https://wolfstreet.com/2024/03/31/curse-of-easy-money-us-government-interest-payments-on-the-ballooning-debt-v-tax-receipts-amid-higher-interest-rates-inflation/

I think it is pretty clear that the FED will dictate short term rates over time and the markets will dictate long term rates over time.

Housing prices went straight up with QE, the houses are not more expensive, your money is worth less. 😡

Yes, but your money is worth more now when you buy a new house, whose prices have come down, and your money is worth a lot more than it was a few years ago in cities like San Francisco and Austin, where home prices have come down a bunch, and your money is worth a whole lot more if you buy office towers, malls, apartment buildings etc. The purchasing power of your money has soared with regards to CRE.

In My hood.. new homes have increased in price by 60 percent or so in last 4 years.

How come usd is worth more ?

In your downtown San Diego, the value of office towers has plunged by 60%, and so the same amount of USD can buy 2.5 office towers compared to just 1 office tower five years ago, and so the dollar has gained lots of purchasing power in that area and has become “worth more.”

After CRE, we wait and hope that money will become more expensive in terms of private housing, lol

Anecdotal evidence suggesting a soaring demand for travel, reaching unprecedented heights with an accelerating momentum reminiscent of the post-Covid reopening phase. Consumption is on the rise, both in terms of price and volume. Additionally, there’s a concerning trend of individuals investing significant sums in jewellery and bullion. Rather than shopping for specific items, they seem to be seeking anything valuable enough to exchange large quantities of USD/EUR/GBP.

I call it a deliberate currency debasement and debt monetization, with the Fed paying lip service to concerned USD bagholders, I mean, bondholders.

Yes, tightening did have historically a 12-18 month lag but we are past that due date with conditions just getting the opposite of the price stability.

Gold price at ATH is a “no confidence” vote to the United States financial assets.

In a scenario of high inflation well into the future there will be a strong demand for gold; and while apparently near useless, gold has persisted for thousands of years. The TV shows of the early sixties, including one 1963 episode of “my favorite Martian” where he had a “Midas touch” had the police going crazy over the major felony of owning gold. The old relatives born in the 1890s talked about the confiscating of their gold forever. The Blackrock CEO is bad mouthing India for the people’s gold owning tradition. This type of inflation to erode the national debt and deficit spending can arguably only take place in a society where gold is illegal again.

Surf’s up, the second wave of inflation is incoming. hedge accordingly!

Is it just me or does anyone else notice that Financial Services and Insurance inflation is consistantly averaging about 4-5%… even during the good times!