It’s not just the top 10% or whatever who got the wage increases.

By Wolf Richter for WOLF STREET.

The employment data today poured some cold water on the raging Rate-Cut Mania: The 10-year yield spiked by 17 basis points within a couple of hours.

But surely, they’re going to try to brush the employment data off too, like they’re trying to brush off the FOMC’s push-back statement and Powell’s post-meeting press conference:

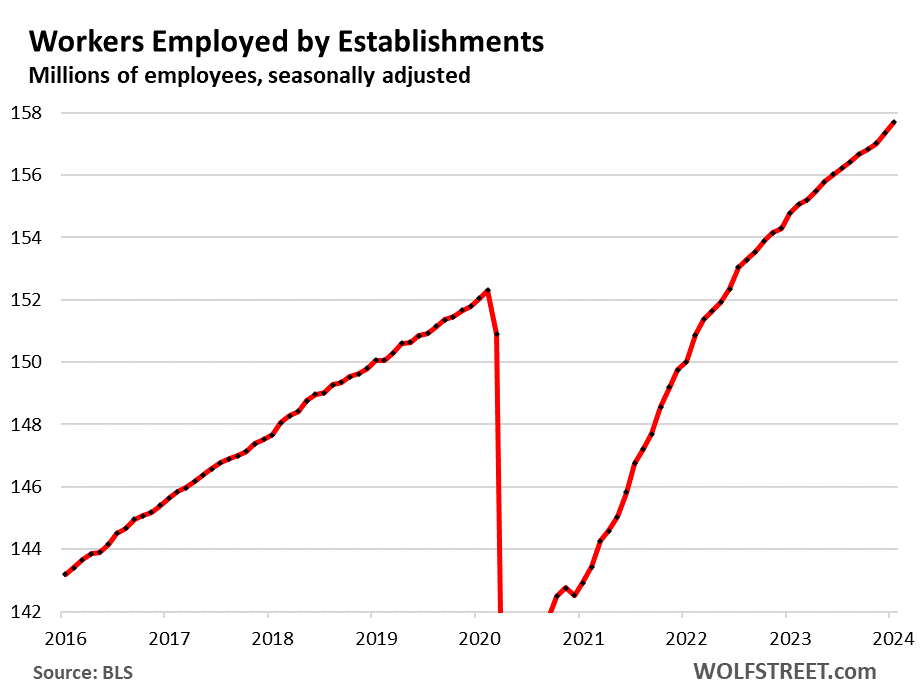

The employment data, released today by the Bureau of Labor Statistics, was fine; it was as you’d expect from an economy that is growing at a good pace. The number of payroll jobs created was revised up for the entire year 2023 by 359,000 jobs.

And in January, an additional 353,000 jobs were created, after the upwardly revised 333,000 jobs in December. So businesses are hiring on net at a very solid pace. That acceleration over the past two months is now visible in the chart:

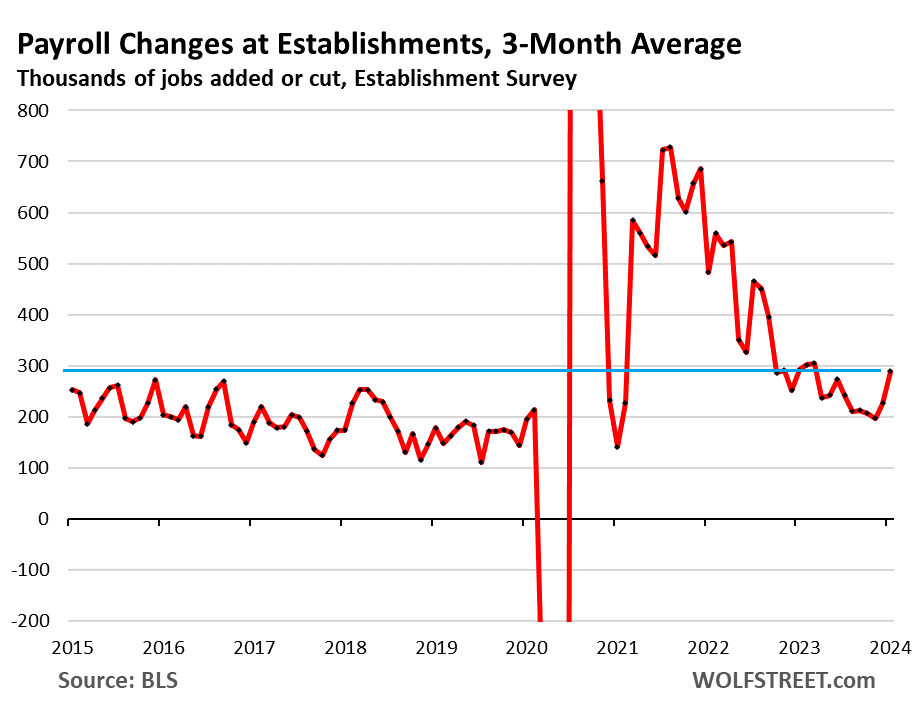

The acceleration can also be seen in the three-month moving average, which irons out some of the month-to-month squiggles. The 3MMA rose by 289,000 in January, the biggest increase since March last year, and bigger than any increase in the years before the pandemic, after it had already increased by 227,000 in December. So this is not just a blip:

On the inflation front: Reheating wage growth.

To be able to hire and retain these workers, employers have re-accelerated their wage increases. We’ve been talking about this for a few months, and it just keeps powering higher, which is great for workers (but not so great for companies, whose costs are rising), and it’s great for consumer spending – these wage increases will power consumer spending nicely, which is great for GDP and overall economic growth. But it’s also one of the potential fuels for consumer price inflation.

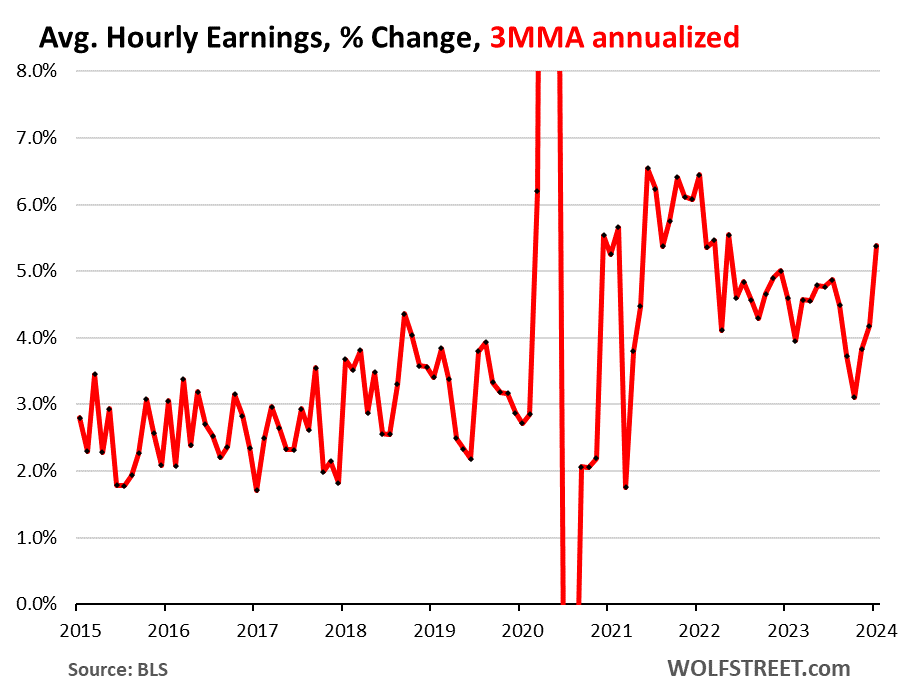

Average hourly earnings of all employees jumped by 0.55% in January from December, the biggest increase since March 2022. That translates into an annualized increase of 6.8%.

The three-month-moving average jumped by 0.44%, which translates into an annualized increase of 5.4%, the hottest since May 2022:

On a year-over-year basis, average hourly earnings rose by 4.5%, up from 4.3% in December, November, and October, thereby marking the re-acceleration even on a year-over-year basis:

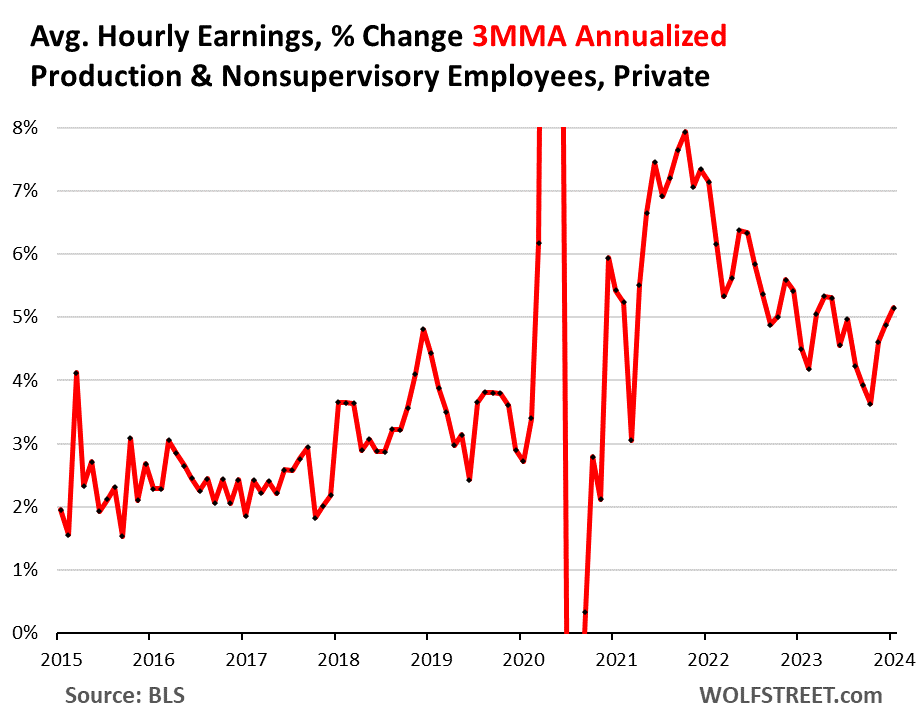

It’s not just the top 10% or whatever who get the wage increases. Average hourly earnings of “production and non-supervisory employees” jumped by 0.44% in January from December, which translates into an annualized rate of 5.4%.

These “production and non-supervisory employees” – the bulk of total employment but not management types – are working supervisors and all employees in nonsupervisory roles, such as construction workers, plumbers, cleaning staff, factory workers, engineers, designers, doctors and nurses, teachers, office workers, sales people, bartenders, technicians, drivers, retail workers, wait staff, etc.

In terms of the three-month moving average, it jumped by 0.42%, an annualized increase of 5.2%, the third month in a row of acceleration:

These types of wage increases are not, as Powell would say, consistent with 2% inflation. In other words, they’re providing fuel for increased demand from consumers, and for increased consumer spending, which is great, but this increased demand also provides further inflationary pressures.

And then there is the element of rising labor costs in products and services that employers will make every effort to pass on to consumers, and consumers, armed with these wage increases, might be willing to pay them, which translates directly into higher consumer price inflation.

And then Powell gets to re-explain to the reporters why these kinds of wage increases “are not consistent with 2% inflation,” and why “we will be very careful… etc. etc.”

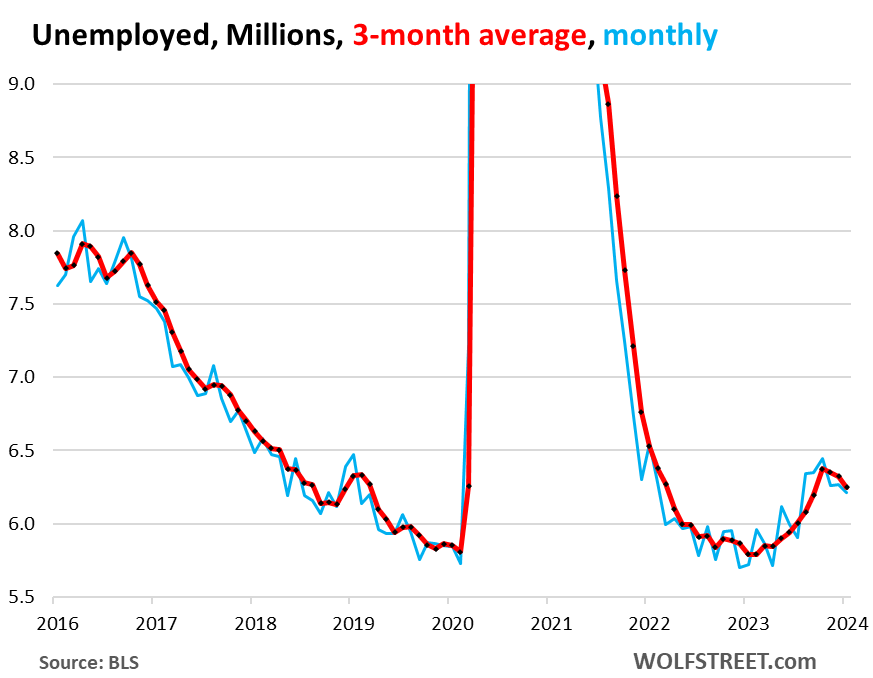

The number of unemployed workers keeps dropping. Unemployment is another key metric for the Fed. The headline unemployment rate remained at 3.7% which is historically low.

And going a little into the weeds, we see that the number of unemployed people who want to work dipped for the third month in a row to 6.25 million. This is a reversal because it had been rising from very low levels of 5.79 million a year ago to a still low 6.38 million in October. But since October, the number has been dropping again – a sign of the reacceleration of the labor market that we have seen elsewhere, including in wages.

The blue line shows the monthly data, the red line shows the 3MMA. The reversal is now getting clearer, indicating that the labor market is beginning to retighten just a tad:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Always insightful, Wolf.

Which is a bigger driver of inflation: Wages or Corporate Profits?

You shared a wonderful article in December on the Inflationary Aspects of Corporate Profits, but it is unclear to me if increases in wages would be deducted from some of that net profit or if the higher corporate profit margins should be considered a new normal.

If wage gains are paid out of existing margins rather than passed on to consumers, wouldn’t that have a moderating effect?

Corporate profits are a RESULT not a driver.

Corporate profits results can be caused by pricing power. Or put another way, lack of competition.

Yes. But where the pricing power comes from is complex. Lack of competition is one reason; but pricing power also exists for example in full-size pickup trucks (four big competitors), and there it is oligopolistic pricing behavior where they’re not competing on price, it’s like an industry understanding, and consumers are willing and eager to get ripped off, providing GIGANTIC profit margins to the automakers. Ford would instantly die without the huge profits on its pickups. But this is enabled by Americans willing to pay whatever for full-size pickups, so there is this mass-psychology behind it that makes it possible.

Mass psychology OR, MASSIVE propaganda AKA advertising???

Been a pick up truck user since first driving an early ’50s chevy with 3 on the column for the plumbing co worked for in early ’60s, and I really and truly feel SORRY for the folks who do not understand that it is a VERY expensive vehicle to own and operate then and now without an appropriate compensation for ”load” or durability when loaded.

Was at a construction company picnic near de twa in the early oughts that included some folks from the BIG 3,,, and after sufficient lubrication, those folks were candid about the PUs margins to the manufacturers….

Never paid anywhere near MSRP after.

VVN

Saw on TV ads tailgates are up to folding SIX WAYS. (I guess they count the original as one?).

How and where do you impress/entertain yourself or someone with THAT?

They already have a good sized TV screen as the centerpiece of the dash….I couldn’t begin to guess what all it does.

Still can’t wait till the low riders take their electronic, hydraulics and servo linkage skills to the tailgates……I bet they can do real “nasty” dances, especially if the whole bed is in on the sequences.

Maybe the dashboard TV screen is for programing/designing the dance routines?

The cowboy boots and hats and big engines, etc of Wolf’s day just don’t piss away enough planetary and human resources to give the “entrepreneur/inventor/advertising/sales” room to properly flex their greed.

Nice to hear it’s all growing well.

I’m sure it must do… if the share of corporate profits decreases as a % of the economy, wages can take up an increased %. The other and maybe larger part of the equation is labor productivity. In theory 5% wage increases are sustainable with 2% inflation, so long as productivity gains remain above 3% (roughly).

“or if the higher corporate profit margins should be considered a new normal. ” is a brilliant question.

And how long is it likely to last, in the face of the historically and obviously a bone of contention that often leads to civil strife in a democratic society, like America, that claims it’s heritage is rooted in poverty.

At some point, the inequality destroys itself and the empire crumbles from old age.

So, I get to keep rolling my 5+% Tbills for a while longer?

It looks like it. That will slow the brutal decimation of the purchasing power of your dollars.

Yup hopefully but that also means housing prices in hot market will continue to be ridiculous…good times..

5.4% 14 month CD Goldman Sachs Marcus

I have one.

My credit union has 12 month CDs at 5.6%. That’s great, but hold the line gentlemen, higher rates are coming, stay nimble and play in the 4- and 8-week T-bills until then. In addition to all the unfunded liabilities, Uncle Sam has 6 trillion in debt maturing in 2024. This isn’t personal, it’s just MATH.

They reckon the Weimar hyperinflationary period took about 14 months to burn itself out, imagine being stuck in a savings account that paid 5.4% interest during that time?

Exactly! Not saying it will be that bad, but real world costs to simply maintain our current lifestyle have been increasing at rates well above 5% already.

So many smart people on here practically lunging for that nickel in front of an out of control steamroller.

I cancelled my six month bill and will invest into 90 day t bills.

Yep, although Vampire Squid claims all the Consumer staples stock are going to increase earnings per share 8% or more justifying their fine looking PE’s of 17-to-45. You wouldn’t want to miss out on this inflation bonanza.

Not sure why, but cd rates dropped back in November. I was getting 5.5 percent then (short term, 3 month) and now the top end is 5.1 percent. I guess the banks were factoring in a rate drop. Hopefully the rates go back up now.

Buy T bills. No state income tax. (Wolf taught us about T Bills)

Of course, that only matters if your state has an income tax. Some states don’t (they get their money by taxing other things more heavily).

Unlike the Federal Government that is able to monetize it’s debt issuing Treasury bills, notes, bonds that are purchase for their ” risk free” return. States have to balance their budget which is a natural contention with the Federal Government over affordability.

Plenty of options for more than 5.1% right now. Bankrate is a good site for finding high rate savings and CDs. Raisin is another good resource for both.

You can also buy treasuries through a brokerage at 3, 6, 9, 12+ months that usually pay more than CD’s, or brokered CD’s

Sofi is planning for rates of 4.5% by end of the year and Ally is planning for a cut in rates by the end of the year by lowering CD rates in anticipation. Sofi has built in an unemployment rate of 5% into their EOY 2024 models and Ally 6% unemployment rate.

Depending on the taxation of your state you are in, short term treasuries are a good bet. I’ve got various auctions of 4 to 17 weeks although I like 8 with auto reinvest. All earning 5.4% and not taxable by California.

I think they are only taxed at federal level (not subject to state or local tax anywhere).

Just be careful with auto reinvest through treasury direct as there will be a “lag” between when the bills mature and the next ones are issued. I know for 4 week t-bills, the delay is 6 days. That means 6 days every 4 weeks, your money isn’t earning any interest. There are some solutions for thi:. If you still want to go TD route, I manually would reinvest my bills as TD doesn’t pull from my bank account until the bill is issued and deposits the funds back into my account when the bill matures, then I earn my bank’s interest for the 6 days in-between. Obviously this issue is less apparent with longer dated treasuries as the problem comes up less frequently. I did call and ask if there were any limits to the dollar amount where this would be true and they told me “no” but I do find that hard to believe. I only did it with smaller amounts as a test as I’m still getting a 5.5% teaser rate from Betterment and I prefer to have all cash right now.

Great explanation why I am in SUTXX instead of Treasury Direct.

Tangojennifer – My experience with 4 week Tbills over the last year has been very different in that auto-rollovers generally execute flawlessly. Now, if I try to get fancy and combine many maturing to one new bill things go awry. It’s worked well enough that I introduced my 23yo daughter to her first TD four week auto reinvesting Tbill. I told her to give it a try unless she wants the bank to give her nothing over the same period.

I grt paid every 4 weeks on my 4 week bills. No lag. The auction happens six days earlier, but the settlement date for that auction is the same day that the funds get distributed from the last purchase.

Tangojennifer- you might want to use a different abacus when doing your t-bill calculations, you might be missing some beads.

CDs seem to be less market-rate-sensitive, i.e. they take longer to catch up to the yields on equivalent-duration treasuries.

Late last year after rates had dropped a little, CD rates were a bit higher. Most of my CDs purchased at that time are around 5.5%, while bills are now around ~5.35%. But new-issue CDs from those same banks are closer to 5.1% now.

What a difference a day makes with bond yields! Holy NFP. Wolf’s call for higher yields looking brilliant. Glad I didn’t go big long bonds yet. I was questioning myself Wed & Thurs after 2 massive bond rally days.

Well sooner or later a recession or higher rates. Higher for longer. Thanks Wolf!

Do your part and be just a little less productive for “the man.” This should keep employment numbers up.

I think everyone that invests for the future is part of “the man” but I understand your notion.

What happened with full-time jobs? Why the difference (continuing) with the Household Survey?

The data of the household survey is very noisy. Just look back at March 2023, when the number of full-time workers spiked out the wazoo, just like that from one month to the next. But the huge and diverse US labor market doesn’t turn on a dime like that, it’s just not how it works, it’s a slow-moving continuous trend that just keeps going unless there is something big, such as a Financial Crisis or a pandemic that can make it turn on a dime. A regular recession will show up in the labor market, but not with a huge sudden change from one month to the next, but with a gradual weakening that will just bend the trend line over months.

Pure wisdom dispensed daily.

What do you make of the info presented on ZH about the latest Biden stats?

Too much to quote or cut-and-paste, hence the URL.

I stopped reading this crap on ZH about 10 years ago. It’s always the same, every month, just with a different flavor. ZH is for your amusement only.

“Biden stats” suggests that ZH has successfully polluted your brain.

There is no “info” on ZH. It’s all crap all the time. I stopped reading it years ago and I have never missed it.

Wolf – anything in the mix of full time v part time v 2nd job that would skew the jobs and/or hourly wages data, in your view? For instance are FT job gains in line with historical norms? Or are these gains skewed by PT or those taking on a 2nd job?

Thanks

I’d like to know this too. How many are taking on a part time job to keep up with rising costs? Is there data on previous retired people returning to the workforce because of said costs?

And wages are up? Everyone I know in CA is preparing for a 0-1% COLA this year in the public and private sectors.

Peeping Tom,

So what? It’s normalizing after having been out of whack during the pandemic:

The ratio of multiple jobholders actually dipped in January:

Wolf – two things, sort of strange that there’s no reply button available under your comment(s), whereas there is one for everyone else, so I’ll reply here to my own.

Is what you’re saying that it doesn’t matter if job gains are FT, PT or 2nd, provided that more people are earning more money and therefore have more to spend in the economy? That’s what I understood from your response showing that the number of PT and 2nd job holders is normalizing. What I simply don’t know is how any of this data is actually collected and where this sort of breakdown (FT v PT) matters. Something to consider adding next time you cover this data print, perhaps. I think you’d done something similar explaining how JOLT data or some other print is actually collected.

Peeping Tom,

1. “…sort of strange that there’s no reply button available under your comment(s),”

Comments go four levels deep (nesting). So: original comment (level 1), reply to original comment (level 2), reply to fist reply (level 3), reply to second reply (level 4). And that is it — for any and all comments. There are no more replies possible because on mobile devices the columns get too narrow to read once you get to the fifth level.

See, there is no reply button under your comment either.

2. “What I simply don’t know is how any of this data is actually collected”

PT and FT jobs data comes from the Census Bureau’s household survey, not from the establishment survey. There is now discussion underway that the Census Bureau might have underestimated immigration-led population growth in 2023. If this is true, then all the household survey jobs data would look a lot stronger than they did. This makes sense to me.

This also happened in 2022. So in March 2023, for the February jobs report, the BLS issued a huge upward revision of 1.5 million additional jobs. This may happen again on the first Friday in March when the February jobs report is released. You might want to bookmark this comment 🤣

Companies are making a killing with post covid pricing so they can afford to hire more workers and pay them higher wages.

I don’t see this train slowing down anytime soon unless the nonexistent recession eventually shows up and that’s no likely either unless we go to 7% on the fed funds rate.

Looks like we’re gonna be at 5.5% for a long time

So it looks like all of the predictions of a recession were really really wrong.

No, not at all,

I would bet on Dow 40,000 instead of a recession. Or have you forgotten the massive budgetary stimulus coming from the federal government?

On a long enough scale (5+ years), the gloom and doomers will finally get their recession.

After they’ve predicted 10 out of the last 1 (actual) recessions.

But some are holding all cash for years always afraid about recession around the corner. If this works for them then ok.

If were one too simply observe the stimulative nature of excessive government debt spending, one may decide, as have I, that recession is the last thing the current government will tolerate before the election.

It is more than unlikely. So let’s spend our new found wealth, wisely. A measurement whose axis has today versus tomorrow, in direct conflict with most of the big spenders who see tomorrow as a function of today..

No, just early

I’ve missed all this and so mad at myself….remember 2018 when just the idea of interest hikes caused 20% market drop…now new highs with record interest rate and QT.

Milo, I wouldn’t be. Back in the 2018 example, the market started going back up throughout 2019 based on the pivot that occurred in January. In a way, it made sense. I remember reading that nearly all of the 30% gain from 2019 was from P/E expansion, meaning that it was entirely due to lower interest rates, and not economic growth.

The same thing is happening here, but this time, traders are trying to front run the Fed before the pivot. This means that if the pivot comes (and rates not only drop, but drop back to 0, and not because of a catastrophic economic collapse, but just because), current valuations are arguably justified. If the pivot doesn’t come, or rates stabilize at 4% or so, then the market remains grossly overvalued.

This isn’t people buying today because they think the stocks are a good value. They’re gambling that rates are going to drop, as there is no way that any of the Mag7 are going to grow into their valuations at current rates.

You only “missed all of this” in the sense that you didn’t throw $100 on a particular number on the roulette table.

I don’t know. I don’t think the market is betting that interest rates are going back to 0 ever, unless a big recession hits I guess. But 3.5 – 4 sounds more like it. You are saying even then market is way overvalued?

The “market” is very concentrated among a few big companies. Equal weight S&P 500 was down today 0.09% whereas the market cap weighted (regular) S&P 500 up over 1%. Over last year, equal weight is up like 3% vs 19% market-cap regular S&P 500.

I tend to agree with your analysis. Is the market way overvalued is a question whose positive and negative responses are emotional projections that are not worth squat.

No matter how we rearrange the set.

You nailed it Einhal.

There valuations are at crazy level but these craziness can go on for quite some time.

Market believes rate cuts are coming sooner than later along with slowness in QT.

The last stage of a bull market is very narrow leadership as we’re seeing now. It was The magnificent seven now it’s the fantastic five, until finally there’s nobody left to hold the ship above water.

The discounted cash flow from the current market valuation will be positive in 25 years under the current assumptions that the Fed’s monetary policy will insure asset price inflation without triggering an increase in CPI inflation. And that the long term interest rate will average 4.3 pct for the next 30 years. A goal that has never been achieved by the US Federal Reserve Bank.

It is the Mag 2 now…

NVDA, a chip maker with no patent protection in a notoriously cyclical business selling at almost 37 times sales, and…

META, where a 50 cent dividend prompted an 87 dollar increase in the stock price. This boosted the S&P 500 yield from 1.45% to 1.46%.

The other Mag5 are headed south.

NVDA P/E ratio today is 83.22. No fluff here. No sir.

This isn’t directed at you, but your post made me think of the comment. There are other options besides certain stocks rising and rising, or crashing spectacularly.

It never gets press because it is boring, but some high flying stocks that outrun sane valuations sometimes then go through many years of going nowhere. They may lose some, but don’t really crash. Eventually their results catch up to their valuation and after that they might make reasonable investments.

Microsoft, Intel, and many other high-flyers from the dot-com bust at the turn of the century went through such periods.

Don’t get me wrong, it sucks holding such a stock through such periods of stagnation, but it is better than a full on crash.

That’s because the market is betting the Fed will blink first. Traders and investors truly don’t believe rates will stay high.

“record interest rate ”

?

It seems 5.25% suppressed nothing.

5.25% will suppress plenty, IF investors believe it’s a new paradigm. If they think it’s a one or two year blip that will drop back down to 0 at the hint of distress, then it doesn’t suppress anything.

Sure, but investors *don’t* think it’s a new paradigm. And why would they? The Fed has given them no reason to. Investors were wildly optimistic about the timing of rate cuts, but they’re not wrong about those rate cuts coming.

The Fed is itching to cut rates, they’ve signaled that loud and clear. They’re just not going to do it until they have an excuse, and they don’t have one yet.

MW: US Treasury yields surge by most in at least six months after unexpectedly strong January payrolls data

Wolf – in your opinion, has the technological development in the job search/placement field (think linkedin, various job search engines) created a new paradigm for “maximum employment/historically low unemployment” much like the advancement in real estate marketing (Zillow, etc) resulted in lower overall real estate inventory?

Job search and talent search has definitely gotten a lot more efficient than during the time of reading paper ads and sending resumes in the mail (though that’s still going on too). I think it made the labor market overall more efficient for big employers. Small employers are having a heck of a time hiring though, and that has always been the case.

Great question. It gives me something to think about. I like Wolf’s answer as well.

5.4% CD Goldman Sachs 14 month

Howdy Folks. Not much to say except the same old stuff. Gonna be fun for the next decade or so………………..

Thanks again for the sanity Lone Wolf…………………..

There is an inverted yield curve in CDs at my local credit union. 1 Year CDs are yielding 5%. Two years drops off to 4%, 3 years to 3%. I went for the 1 year CD.

This happened once at the bank I worked at and it’s funny the banks think they know where rates are going… Not that anyone would take them up on a longer dated CD for less

There’s no money in duration right now. Its crazy.

The highest yields are on the 3 month (!) T-bill.

BMO still has 4.6% for 3-5 years. It was 5% a few months ago though.

Another decade or two of wage increases like this and people will be able to afford housing again.

Yes but unfortunately most of them will be dead by then.

Most people don’t understand the magnitude of how far out of wack housing is right now. Your joke is closer to the truth than most people realize for the youngest cohort of the labor force.

The youngest cohort is keenly aware their wages haven’t been close to being able to afford housing for 15 years, which is why the average age of first time home ownership continues to march upward.

Firmly believe there is no reason to pursue home ownership in this country.

Between the mortgage costs (house and financing), insurance, property taxes, renovations and maintenance.

The only way it works is if equity or home prices continue to grow at a crazy rate but even then it’s flawed because it only works for people who already own and further blocks new entrants

The idea of owning something is a nice notion but around 75 percent of people never pay off there home and that’s a backwards looking statistics when they were starting out with more reasonable prices.

I’d guesstimate a 30-40% decline in prices would make me reassess but might need even more then that

30 years of rent starting at 1500 with 5% inflation will cost you 1.2 million by the time youre 50. Ignoring the fact you’d have to jump to a much more expensive apartment to have room for a family, deal with roommates to reduce the cost in the early years, be beholden to landlords failure to repair anything, loud neighbors in adjacent units, pay an addition $50-$100 a month for the spouses parking spot, etc. Home ownership is not cheap, but neither is renting. Theres a reason no one is having kids and all the replacement workers are being imported.

American Dream,

I knew a guy who used to say that it’s very easy to create clients of the welfare state, but very difficult to defund them, because they vote and will fight like hell to keep their welfare benefits.

He meant it in reference to Medicaid, food stamps, and the like, but it’s also very true with respect to asset gains, including housing.

People who own their homes and bought in years ago feel entitled to policies that will keep the gains. With few exceptions, they don’t care who gets crushed below them.

J Pow told everyone the truth but the economist made up these stories that the public followed. Rates are going higher and I have followed that discipline for years. The NYT only posted me because I was the Contrarian.

Wolf take a look at hours worked. I have a theory that the lower paid workers are being let go and number of hours worked are being cut. So sure we ‘make more per hour’ but it’s still less money. something seems super fishy about all the jobs numbers and that it’s not telling a good story.

No, average weekly hours dipped to 34.1 in January, from 34.3 in December because of very bad weather in January in a big part the country.

Layoffs have been near historic lows. The number of unemployed dropped further. RTGDFA

What’s “fishy” is your imagination.

Paul-

Astute observation. Total compensation has been declining. Credit card delinquencies are starting their hockey stick up at every major issuer. Car dealers are looking for humans the bank will lend to. Car auctions are packed with no sales, much like the real estate market where sellers are not willing to accept reality. Green Street reporting ALL commercial real estate collapsing, not just downtown high rises. Apartments down 30%, self storage down 21%. Check it out.

In terms of Mark Strome telling us, “You have to know when to step on the gas” … this is it.

We didn’t have triple short ETFs when I earned my education in the stock market. How do you profit from a crash?

Almost everything on your parade of horribles is bogus, LOL.

That “astute observation” by Paul was homemade imagination. Just making up stuff.

Here is Lacy Hunt’s take on our current situation

The Buy Now Pay Later debt is being packaged and put into Retirement Funds

Nah, not gonna get my data on YouTube. BNPL balances are relatively small — despite all the doom and gloom crap out there — and they’re included in consumer credit, which I report on with actual data, and the next one is coming up next week.

The BNPL balances are small because people have to make payments every week and pay off the entire purchase in four or five weeks. And it’s interest free to consumers. So it doesn’t pile up like credit cards. BNPL is not a consumer credit problem.

But BNPL is a problem for the companies that provide it, which make big losses, and their shares have collapsed. Shares of Affirm [AFRM], the biggest BNPL provider, have collapsed by 75%, and are in my Imploded Stocks pantheon. It lost $2 billion over the past three years, including $1 billion in 2023. That’s where the problem is with BNPL, not with consumers.

5% Fed funds rate is fine, as long as employment numbers are in good shape, which they are. The average Fed funds rate over the last fifty years 1971-2022 is 4.86%, median 4.97% (FRED). The US economy has done very well over the last 50 years, with occasional stumbles and bubbles of course. If anything, if inflation kicks up, the rate should go higher. I see no point in lowering the rate, except really poor employment data (aka recession).

Well, betting against America, has always been a bad bet.

The doom and gloom has rarely been correct, except in 86, 97, 99, 03, 06, etc.

America has the world currency which allows a number of shenanigans to occur that assists the home team. Did the Great Depression begin in America or Great Britain which was an intact, Royal Empire, in 1929.

John H.

Feb 4, 2024 at 6:56 am

Dang-

Europe (include Germany, France, Italy and many smaller countries) was NOT in good shape in 1929. Specifically, UK set price of gold too high after WWI, causing major labor completion problems, and Germany was attempting to convert WWI reparations debt to corporate and government debt (much of which was purchased by unwary American investors who eventually lost bigly on these speculations).

UK’s currency was permanently unseated as world reserve during the 1920’s and early ‘30’s as the rest of world recognized it’s problems.

That’s the way I understand it… subject to corrections!

Respectfully

“The average Fed funds rate over the last fifty years 1971-2022 is 4.86%, median 4.97% (FRED). ”

So the Fed expects “normal” to suppress an inflation? Seems like hope rather than an earnest policy.

Now, take out the manufactured 12 years from 2009 to 2021…..where rates were touching near zero….

As you know, I’m a big critic of the Fed, but I do think “normal” will suppress inflation when a huge segment of the economy that popped up in the past 15 years is based on cheap credit and not making a profit. If inflation continues AFTER that cleansing happens (and to be clear, it won’t happen if the Fed pivots as soon as it starts), then I agree that “normal” won’t suppress any inflation from that point on.

The annualized inflation rate I’d already at striking distance of Fed’s target rate of 2 percent.

Where and how do you see inflation going up ?

Fed funds rate 1971-2008 average 6.43%, median 5.62% (FRED). See why I think 5% is nothing unusual? We could keep it there forever. . . well, until the next big recession, which does not appear to be happening any time soon when looking at employment numbers. Wall Street’s constant whining for cuts is self-serving and disgusting.

William

You nailed it!

Correct William. Equally disgusting is the ongoing insinuation by some financial commentators that they KNOW that rate cuts are coming “soon.”

They don’t. No one does. But that reality does not stop the “I am sure cuts are coming soon” din.

Bernanke’s wizardry put a lot of people into poverty.

Longstreet and William Leake-

My 2 cents worth is that we’ll see significantly higher rates to wash out the inflationary effects of heightened Fed activity over last 25 years, BUT we will see much lower rates when the sought-after “breakage” of something in the economy occurs.

In the terms of Mr. Jay Powell: higher for longer will eventually be “transitory.”

Channeling Minsky, Schumpeter and Mises.

In the terms of Mr. Jay Powell: higher for longer will eventually be “transitory.”

The underlying assumption there is that the bond market will forever remain stupid.

Aman-

John Wayne had something simple to say on stupid in Sands of Iwo Jima:

“Life is tough. It’s even tougher when you’re stupid.”

I wonder, though, if bond market participants playing the interest rate prediction game are really stupid, or perhaps they are too smart by half. And certainly confident in their own predictive powers.

Came across a great quote the other day but didn’t write down the attribution: “The investment management field is littered with practitioners who have been right once in a row.”

Cheers!

The quote is freaking amazing. And it is indeed true.

And Tommy Lee is next on that list behind Cathy woods

So, what happens when goods deflation bottoms? Does inflation head back up because people are earning and spending? I am reading about a commodity ‘super-squeeze’ in metals and minerals because of NIMBY. Same story in housing?

Will the FEDs next rate move be a hike?

This is one of those times to set on your hands and do nothing.

I listened to several podcast talking about the price of goods dropping but services and leisure are doing great. What these economist see is people are spending money on experiences. They are passing on buying a nice lamp or rug that just sits there all day long, does nothing, and really gives them zero entertainment value.

Instead they are spending money on experiences. Go look at Marriott or Hiltons stocks. Carnival Cruise is predicted a record year and future bookings are great. The MAG 5 are doing well but so are some service companies.

Several reasons are giving. Maybe because being locked up during COIVD could partly be to blame but many young people believe they want to have experiences now because it might not happen later.

“So, what happens when goods deflation bottoms?”

Yes, that’s a real worry, Powell spent some time on it.

Forget the super-squeeze or whatever. More resources are produced when prices spike. Doesn’t matter whether it’s oil or lithium. That’s how commodities work. And they can ramp up production very fast, so fast that they can crash the price in months, see oil and lithium, LOL

I just listened to a David Stockman podcast in which he stated that the real unemployment in the USA is 40%. That would match the work force participation rate which is a little over 60%.

If Stockman said that, he is an idiot trying to sell newsletters. So all the retirees and all the kids under 16 are counted as unemployed, and all the spouses that take care of the kids fulltime are counted as unemployed, and all the students that don’t work are counted as unemployed, and all the people who are sick for a couple of months and cannot look for a job are counted as unemployed, and the two million people a year that get seriously injured in car accidents and cannot work for a while are counted as unemployed, and all the people who don’t want to work because they have enough money and don’t need to work are counted as unemployed????? That number you cite is just idiotic BS.

Stockman did say this. I wasn’t joking. What he said may be BS like you said, but I believe the government’s figures of 3.7% unemployment is BS as well.

We were out of work for 3 months because of a disabling injury in a hit & run accident. We went back to work Feb 1st. We are no longer unemployed. The RE market is booming in DC. Doing refinances. VA has a rate below 6%.

You are being taken advantage of again. Use better sources of information that do not take advantage of your lack of knowledge on certain subjects.

There is a certain segment of the crazy, nutty, far right media that whenever a Democratic president is in office they start talking about reasons the official unemployment rate is a lie. They never do this during Republican administration’s. Just Democratic ones.

They talk about how the employment rate cannot be right. Then they make up “real” employment rates that are ridiculously higher. They do things like include children, retirees, and people full time in school as part of the unemployment rate despite the fact that none of these people are actually looking for jobs.

Basically they take advantage of people who do not understand the economy and what the BLS measures with its various measurements.

Apparently it worked with you.

Why do you think the 3.7% unemployment rate is wrong? What evidence do you have?

Do you realize that in order for an administration to fudge the unemployment rate it would require hundreds (if not thousands) of bureaucratic people (who have worked through many administrations) to be willing to fudge the numbers and keep quiet about it?

These are not political people. They are people who compile the numbers off of what the data says. Why are so many of them staying silent while the numbers are fudged? They could go to an internal Inspector General and report it. They could go on any number of news channels and being evidence, but no one ever does. I know, like most nutty conspiracy theories, the lack of evidence is often evidence of the cover-up.

Here is a question, did you ever question the official employment rate during the Trump or GWB administration’s?

Why not then?

Be a better person. Stop letting people take advantage of you.

A super squeeze in metals and minerals? Really? I guess that’s why the price of silver languishes at $22.69. Some squeeze!

The biggest everything bubble in the history of mankind is still going strong. Inflation is nowhere near contained. The FED is just riding it as long as they can. They’d love to stretch out 4% inflation for another 10 years straight if they could. Looks like they may get their wish.

“They’d love to stretch out 4% inflation for another 10 years straight if they could. ”

No big deal. Average CPI 1971-2022 was 4.01% (FRED). We’re still here.

“Stable Prices” mandate violation.

Whom do we call?

Your ignorance of the stable prices mandate does not make for a violation.

I agree. However, the issue is the debt/GDP numbers and the interest expense. Again, this isn’t personal, it’s just math.

While I agree that asset prices are the highest mankind has ever endured, what you suggest is a general collapse, of a magnitude at least as great as the Great Depression based on a loss of confidence in the currency, which is being systematically devalued.

Well, it’s for our own good.

This ‘great jobs market’ just guarantees much higher interest rates for much longer which is indeed great news.

One can only dream too bad the opposite will happen.

We survived the first wave of inflation, get ready for the second. Lots of options for CDs, but I don’t want to be locked into a 5.5% rate when 6+% rates are coming…

The treasury has 6 trillion in debt maturing in 2024, it is not personal, it’s just MATH. When facing a hard default or an increase in inflation, you know what the banker/politicians always choose. Might be worth looking at adding to some energy and MIC stocks as well…

Interesting times.

Ladder your CDs & Tbills so you have something maturing every couple weeks or month or so. Keep durations short (<1yr).

Then just roll each one over as they mature, and you'll see your ladder's average yield till maturity slowly rise as rates do.

NB: not investment advice.

We all know its an election year so the smart money is moving into long term bonds and long term corporate bonds not staying short less than one year or laddering.

The smart money thought that too in 2020, and the 10-year yield was 0.5% (Aug 2020) and then yields rose and rose and rose, and the smart money got killed.

MM-

Depends on the investor’s circumstances.

If the investor live’s off of portfolio income, keeping ALL investments in Bills (with nothing locked in to notes/bonds in the 2-5 range, for example) seems misguided.

One’s income could halve very quickly.

(I know you weren’t making specific investment advice…)

WB’s concern was about rates rising – ergo he’d want to avoid longer durations. Sounds like he’s looking for cash management.

In the context of an income-producing portfolio, I’d agree with you however.

MM

Good investment advice

I’m not convinced of wage inflation reheating, especially in the Tech/AI field. Big layoffs are happening all over the place and they’re taking out a lot of talent with high compensation packages. I believe there will be more competition for fewer jobs and wage pressure instead.

Many of those companies are in the “Information” sector, and those companies, after shedding a lot of people in late 2022 and earlier in 2023, have been adding people again for the past three months, and in January employment in the sector was the highest since June:

Just out of curiosity, how does green card carrying immigrants as opposed to non green card carrying immigrants factor into all that jobs data. I am not sure if any of that goes into official jobs data as I’m pretty sure neither have a social, are in workman’s comp, or any other governmental official count.

As we know, at least in Florida this workforce is huge. I just left Home Depot and saw 100 in the parking lot looking for work. Are there any underground data sights that focus on this stuff? Just curious.

They’re all included in the data. There is no filter about immigration status in this data.

At the establishment survey: If someone is employed at a company, that person counts as 1 job regardless of immigration status.

At the household survey: anyone working counts as 1 working person, regardless of immigration status; and anyone looking for a job who doesn’t have a job counts as unemployed. Anyone who has two jobs counts as 1 working person with multiple jobs.

I guess the question is whether establishments are less likely to report truthfully when they’re employing illegal immigrants, but there’s no easy way to know that.

If they don’t report them, then actual employment would even be higher, and the jobs report would look even better.

A different issue came up in the household survey, and that does make sense: There are indications that the growth of the working population due to massive immigration over the past two years has been underestimated by the Census. This impacts all the data in the household survey because it relies on population growth estimates. The implication is that if this population growth had been captured correctly, all the household survey jobs data would look a lot better.

I work pretty hard, a few hours a day, managing my investments. I guess I am sort of self-employed. Interest, dividend, and capital gains are not considered earned income which is fine by me. But some people still do work to get them, same with rental income (I think). Nobody asks me if I am employed or not, but I do work. If you threw in people like me, employment numbers would look even better.

Where would you draw the line? Would the 60+ guy who tinkers all day in his garage be considered a full time mechanic? Or a retiree who works in their garden each day be considered a full time gardener?

I think they got who gets counted here right.

Legal immigrants get a social security number as soon as they arrive in the country. I know this for a fact because my mother in law immigrated recently.

Your sources of information are taking advantage of your ignorance to scare you.

Boo. Go hide under the bed.

The illegal portion of the job market is but a drop in the bucket and hasn’t significantly changed in decades.

“illegal part of the job market”

Back in the day we just called that getting paid under the table. But I guess its appropriate if you think every kid running a lemonade stand should be filing a W-4…

not sure what Wolf’s take on this is, but I am particularly curious as to how the dollar strength fits into all this. The DXY is back above 103, and we all know that the BOE, BOJ, BOC, and the ECB are working with the Fed.

DM: America’s savings rate shame – Three biggest US banks raked in $200 BILLION from higher interest rates on loans last year – yet refuse to raise 0.01 percent yields for savers

America’s three biggest banks raked in nearly $200 billion from higher interest rates last year – yet have failed to pass on bigger yields to savers.

People need to take their money out of those banks and put it where it earns some interest. I think JPM is one of them, and I bought a brokered CD from JPM (in my HSA) that pays over 5% a while back. It’s just that they’re screwing their existing customers.

As a condition to access to the FDIC, I think banks should be limited by law as to how much spread they can make. If they’re parking their customers’ money at the Fed for 5.4%, they shouldn’t be allowed to offer a penny less than say, 4.9%.

So you think there should be more government control of the economy?

Yup. Pennies make dollars. I manually rollover Tbills with Schwab (I decide my next move at each maturity).

I have to buy Tbills in $1000 increments which always leaves some “table scraps” that they would like to sweep into the ziltch paying ether.

So, I immediately buy SWVXX (yields over 5%) in $1 increments to maximize the extra.

You are right! I bought several CDs in the past from JPM paying between 5.5 and 5.7% while they offered their customers 4.8% if you deposit or transfer over $100K of “new money” which does not include IRAs/SEPs/401ks etc… They are really bamboozling their customers. But hey, there are still a lot of fools out there.

Plenty of good options out there although I use one of them for direct deposit and low cash balance. I prefer Ally savings as my savings simply because of the simplicity of setting up a trust account online and use that as my in and out to high yield options. 4.3% isn’t great but not a terrible base of operations. Part of my parents estate had to go through probation and want to avoid that.

In Bulgaria the situation is even worse.

Our big banks have made billions paying zero interest on deposits.

The mortgage loans they give are at 2.89 percent or pure profit.

You have a choice with CD.

We don’t have any because the government doesn’t sell government bonds to individuals. Instead, it borrows debt in foreign markets at 4.75 percent.

We have the opportunity to deposit in small banks at 1.5 to 1.9 percent. This is the only opportunity for any profitability.

But many seniors don’t understand that they are losing money when they keep their savings at zero interest in the big banks where they feel safe.

This uncertainty comes from the mass failures of our banks in 1997.

I’ve never believed in the Philips Curve, the tradeoff between inflation and unemployment, the inverse relationship. The demographic shift explains the current disparity.

The seasonal injection of money looks like it was just washed out. If the trend is still intact, then deflation looks possible in the last half of 2024.

If your banks have a history of failing, and your country does not have something like FDIC insurance, then putting your money in low interest earning but safe banks actually makes sense. Maybe Bulgarians should open accounts in US banks, if that is possible. I know Americans can open accounts in foreign banks.

I inflation data comes in hot for January we hit the trifecta. Everyone’s a winner.

I’m seeing climate experts predicting crop failures over the next years, or reduced output.

Would rising food prices be enough to cause inflation? And cause interest rates to rise?

LOL, predicting crop failures? There are crop failures, but they’re not predictable. They happen because of unpredictable events. And they never happen across the world at the same time. This crap has got to stop.

Climate change will generally extend the growing seasons and allow for planting in places that couldn’t tolerate agriculture in the past. Some of this will be offset by natural disasters, but that has always been the case.

LOL on crop failures as well. What the northern hemisphere doesn’t produce, the southern hemisphere makes up and visa versa. The commodity market generally speaking does a good job moving too much supply to where too little demand is world wide. The U.S. has done a good job of teaching the rest of the world how to grow crops over the last 40-50 years. Remember when the old Soviet had to buy U.S. wheat in the 1970-80’s? Then communism fell in 1989, and now Russia alone does around 25% of the worlds wheat exports. Crop failures are a local country problem at this time. They now import the balance of their needs.

Charlie, I agree that predicting crop failures is BS. But it’s a gross oversimplification to wave away crop failures locally and saying the market will fill in the needs of everyone. Tariffs, naval blockades, wars (inter-state or civil), reservoir failures, and natural disasters can all tip a region from *almost famine* into famine.

As for the US teaching the world how to grow croups, it did a great job. But the current system relies on overuse of groundwater and phosphate fertilizers. If wells run dry (which can be predicted in regions with well-studied aquifers), or phosphate production/imports crash, yields drop.

The US is pretty insulated from famines based on its massive agricultural production. The US has untapped phosphate reserves. Although groundwater is running low in portions of the SW and Midwest, there’s still time to change crops and reduce water use.

It’s hairy for much of the rest of the world.

And to tie this back to Wolf’s article regarding inflation, worsening inflation (e.g., 50% per year) in a country plus crop failures domestically can cause food prices to increase to unaffordable levels. I don’t see how crop failures could cause inflation to increase.

MC Bear – I was not saying crop failures over simplified the problem. We have had wars and natural disasters for eons of time. I was saying that markets adjust to those problems to move over supply to demand. However, governments will get in the way all the time to amplify their problem. Case in point is Gaza – who is stealing all the resources from their own population?

I expected a bump in wage costs in January, lots of employees get raises at the start of a year. We all got 15% raises to account for inflation the last three years. We’re doing our part to keep inflation going.