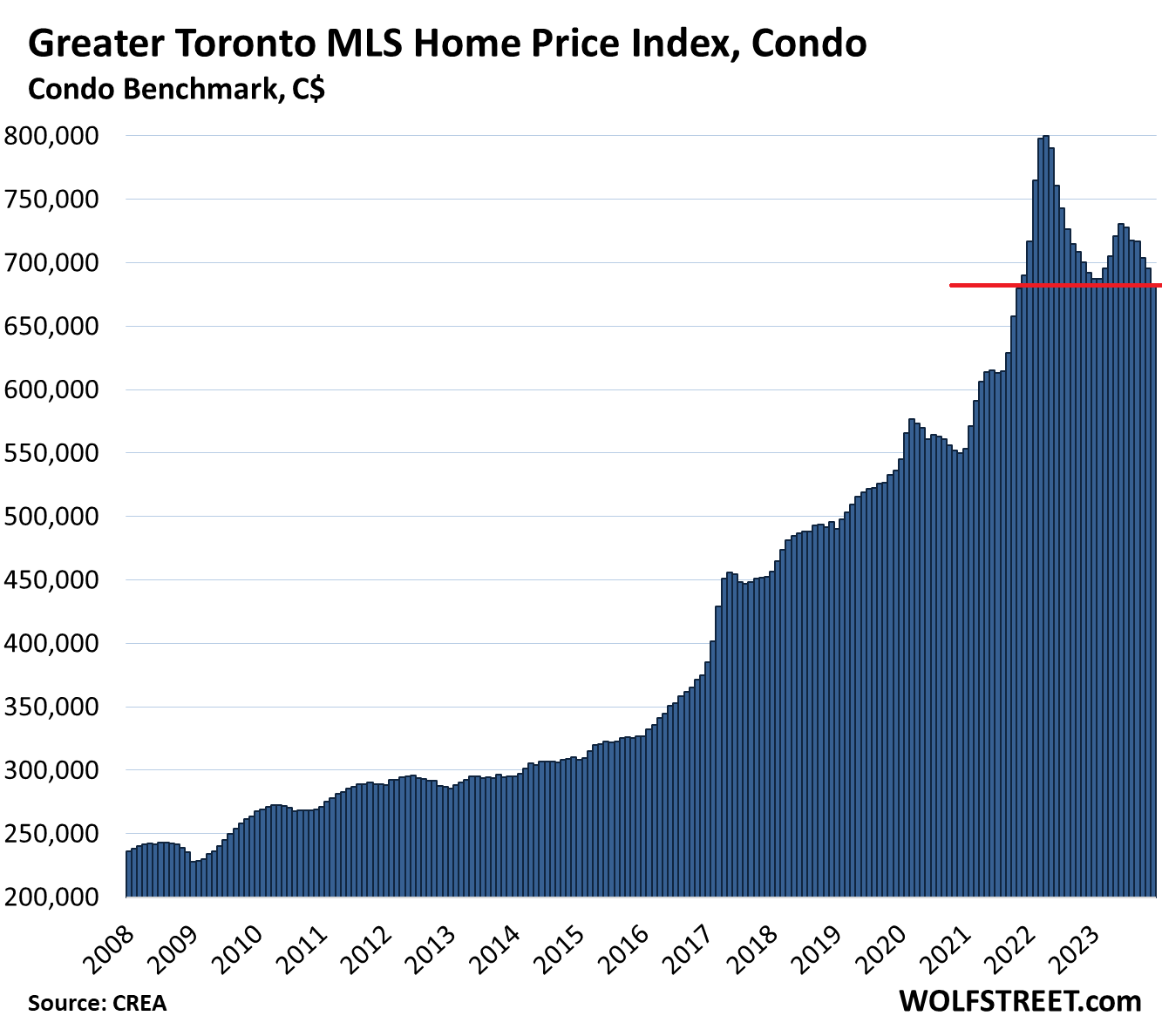

Condo prices in Toronto carve out two-year low, house prices just a hair behind.

By Wolf Richter for WOLF STREET.

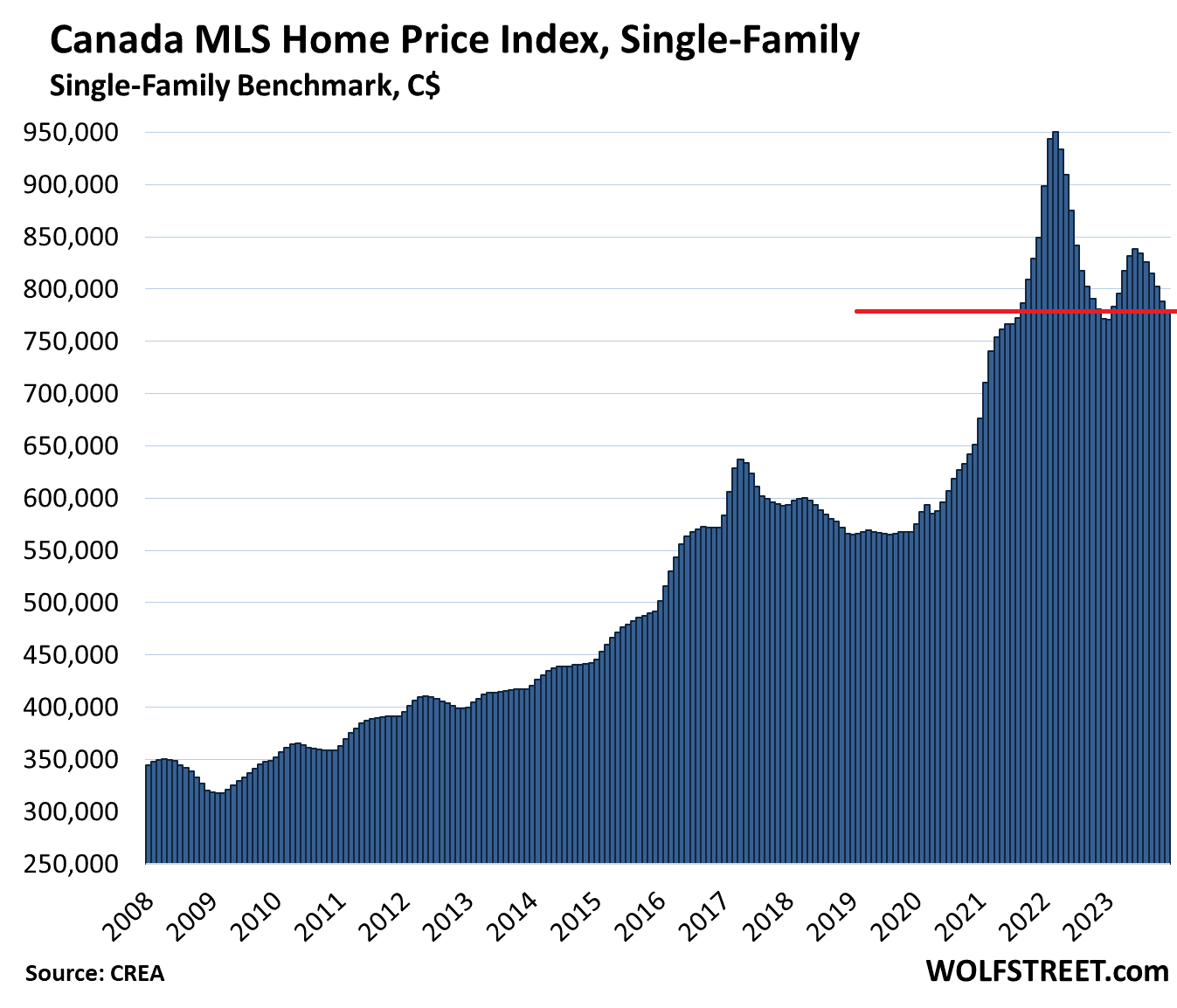

House prices in Canada have now fallen by 18% from the peak in March 2022 – or by $171,500 (all in Canadian dollars) – after the 1.2% drop in December from November, the sixth month-to-month drop in a row, according to the Home Price Benchmark Index for single family houses by the Canadian Real Estate Association (CREA) today.

This brought the national price down to $779,100, the level first reached on the way up in September 2021. Compared to December a year ago, after the massive drops in 2022, the price was up by 1%.

Big losses spread across most of the major markets. And even in Calgary, prices dropped from the record. We’ll get to the individual markets in a moment.

Home sales in December rose by 3.7% from a year ago; and on a seasonally adjusted basis by 8.7% from November. But for all of 2023, home sales fell by 11% from 2022, making it “the lowest annual level for national sales activity since 2008,” CREA said.

“Was the December bounce in home sales the start of the expected recovery in Canadian housing markets? Probably not just yet,” said Shaun Cathcart, CREA’s Senior Economist. “It was more likely just some of the sellers and buyers that were holding onto unrealistic pricing expectations last fall finally coming together to get deals done before the end of the year.”

The problem is that prices are too damn high, inflated by years of the Bank of Canada’s near-0% interest rate policy and by its massive QE during the pandemic.

The end of easy money.

The Bank of Canada has tightened policy, the easy money is over, it hiked its overnight rate to 5.0% in July and has kept it there. Inflation in goods and energy has vanished, prices have come down, but in services, inflation is hot and isn’t backing off, and inflation in rents has exploded. The Bank of Canada doesn’t appear to be eager to fuel this inflation with rate cuts, and it has taken a careful wait-and-see approach.

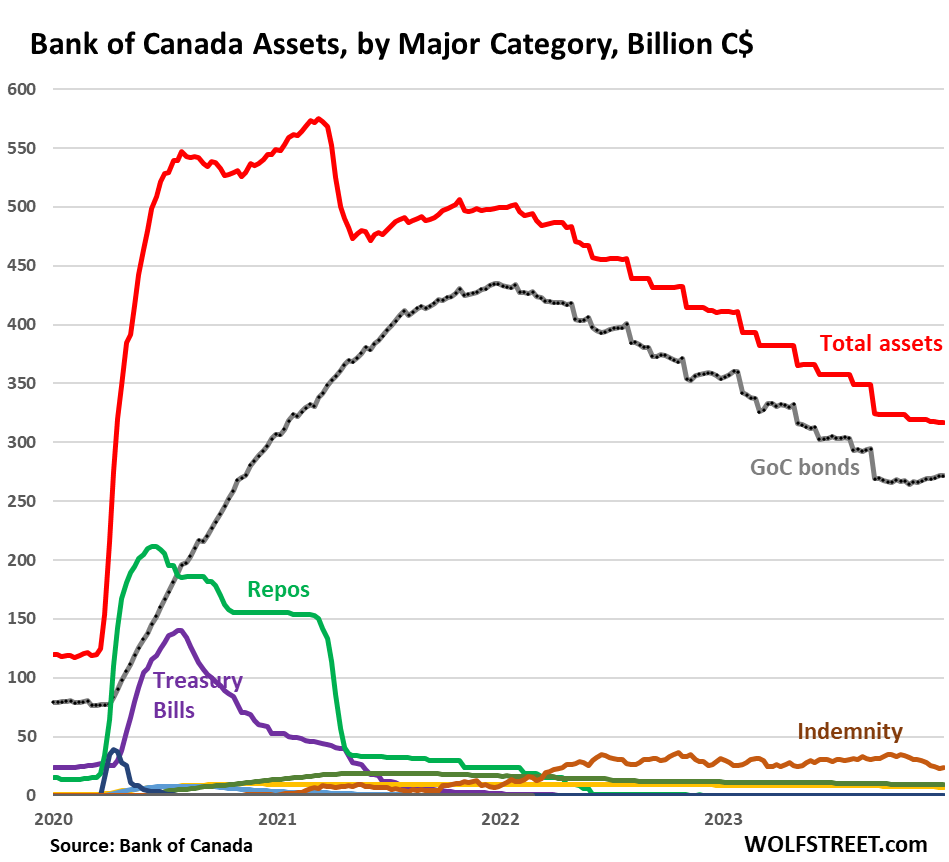

At the same time, the Bank of Canada is unwinding the results of its massive money-printing during the pandemic and has already shed 57% of the $455 billion in QE assets that it had added during the pandemic.

There is still aways to go to drain the crazy liquidity thrown at the markets during the pandemic, and more will drain this year, including on February 1, March 1, and April 1, when some big chunks of the Bank of Canada’s holdings of Government of Canada (GoC) bonds mature: $33 billion combined is scheduled to come off by April 1. In other words, over the next three months, the BoC’s total assets will drop by another 10%:

Single-family House Prices by Market.

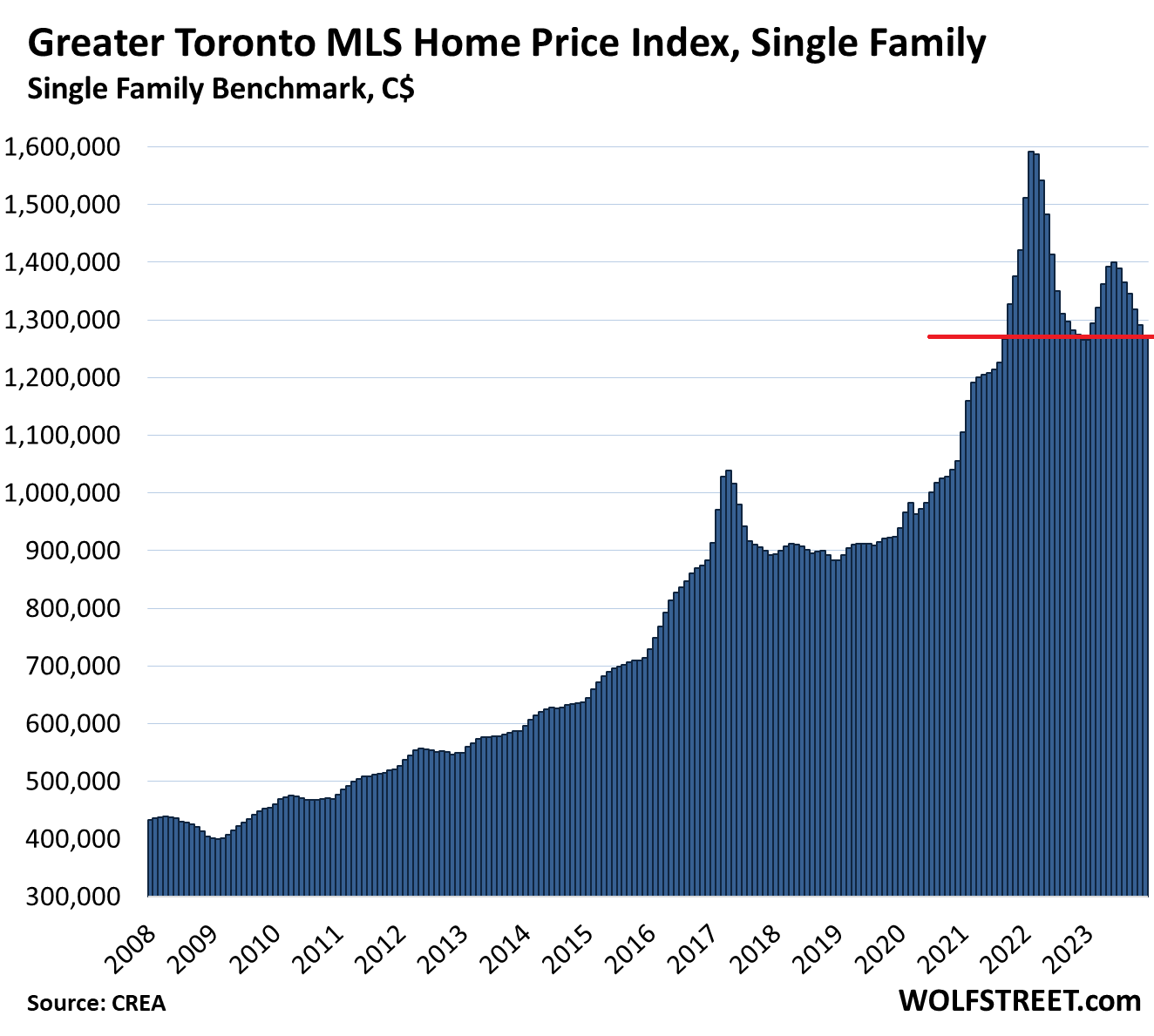

Greater Toronto Area (GTA): The MLS Home Price Benchmark Index for single-family houses fell by 1.4% in December from November, to $1,273,300, the sixth month in a row of declines. The drop whittled down the year-over-year gain to 0.6%.

The benchmark price has plunged by 20.0%, or by $317,700, since the peak in February 2022 and is now below where it had first been in September 2021 on the way up, and is just a hair from carving out a two-year low:

For condos in the GTA, the benchmark price dropped by 1.7% in December from November, by 1.3% year-over-year, and by 14.6% from the peak in April 2022, to $683,200. And it has successfully carved out a two-year low:

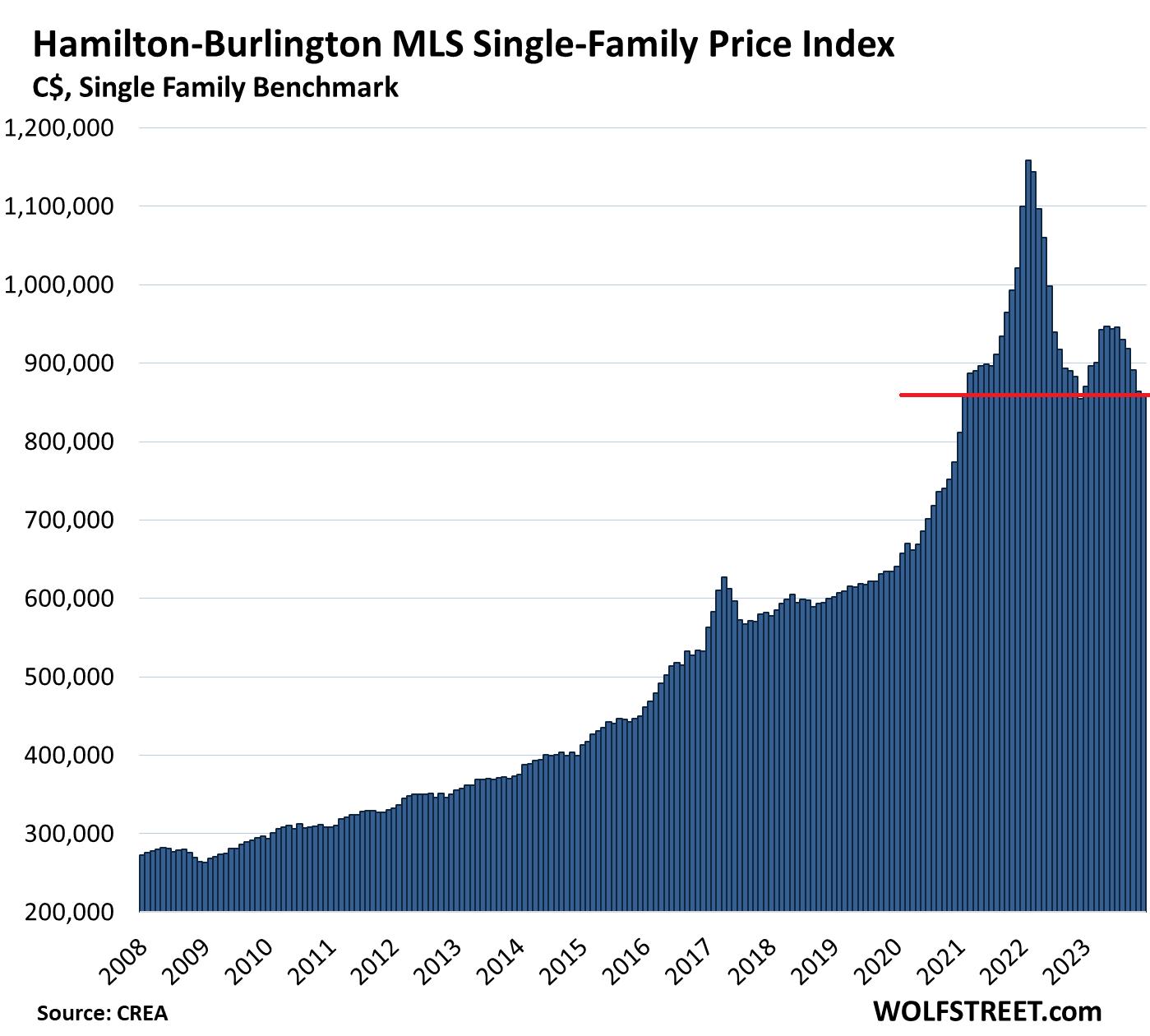

In the Hamilton-Burlington metro (part of the “Greater Toronto and Hamilton Area”), the single-family benchmark price declined by 0.4% in December from November, to $861,100, a hair from carving out a two-year low.

- From peak in February 2022: -25.7%, or -$297,800

- Year-over-year: +0.8%.

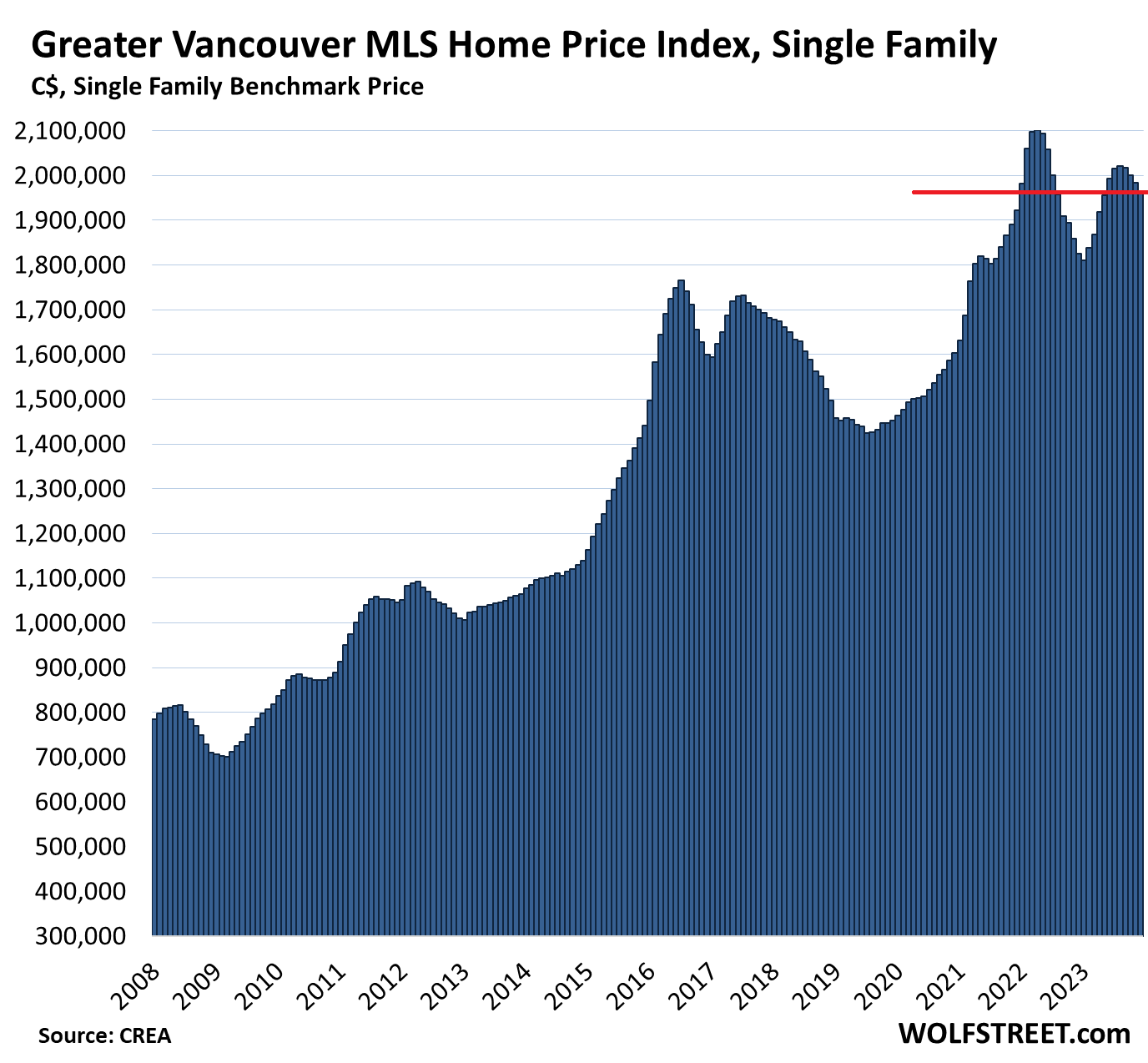

Greater Vancouver: The benchmark price for single-family houses fell 1.0% for the month, to $1,964,400:

- From peak in April 2022: -6.6% or -$137,700

- Year-over-year: +7.6%

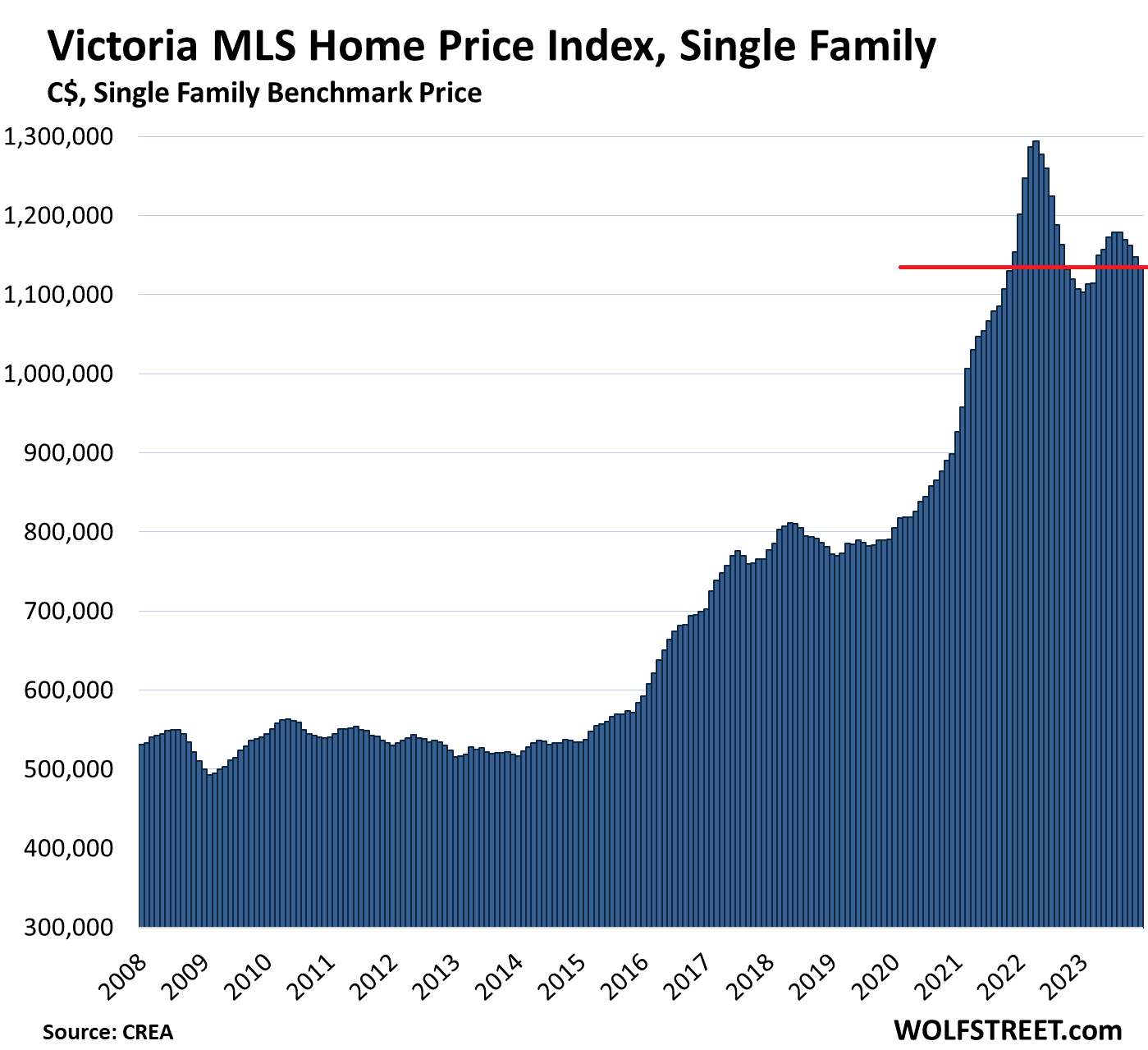

Victoria: The single-family benchmark price fell by 1.2% for the month to $1,134,600 million:

- From peak in April 2022: -12.3% or -$159,800

- Year-over-year: +2.5%

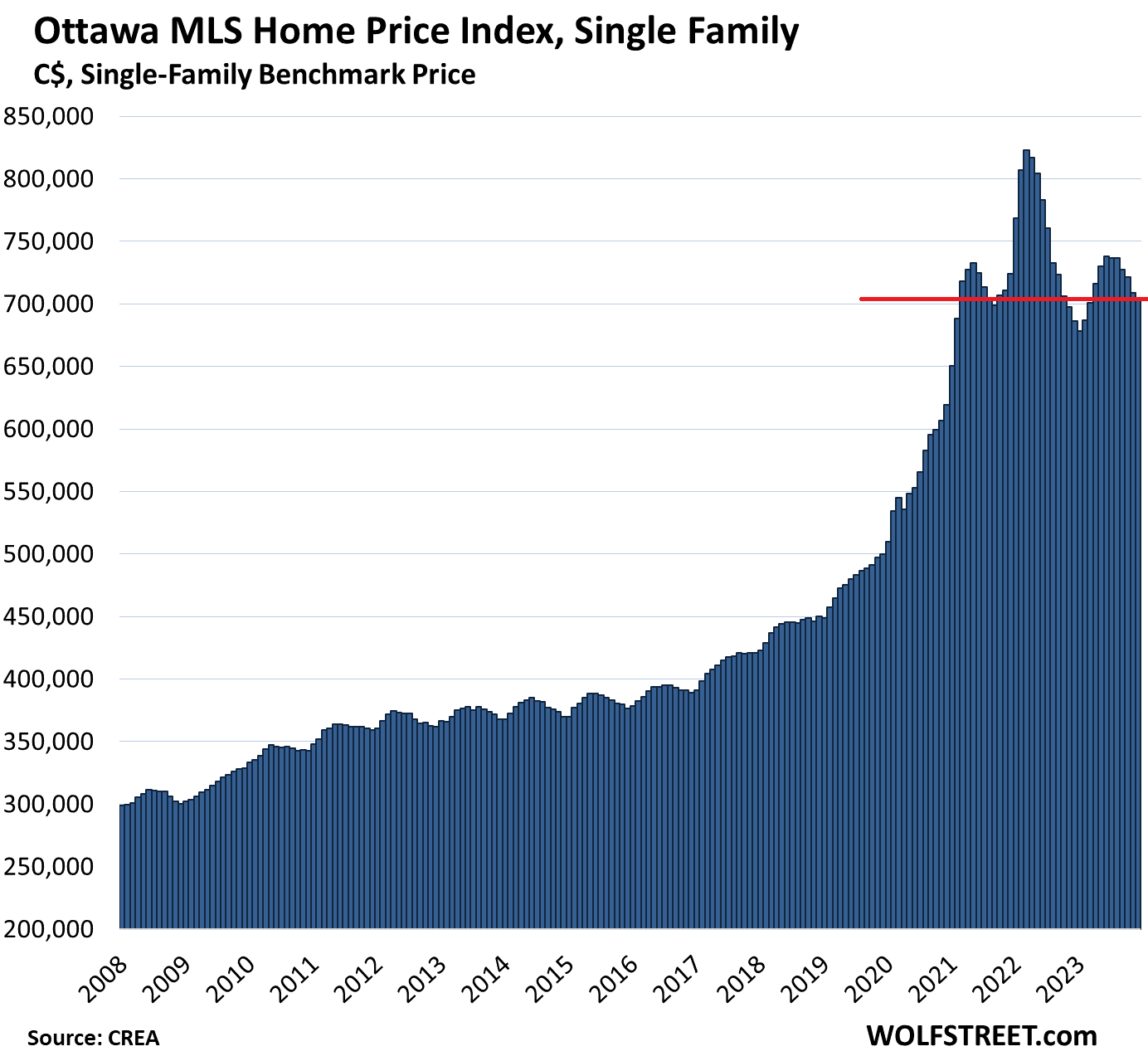

Ottawa: The benchmark price of single-family houses fell by 0.6% for the month, to $704,900, below where they’d first been in March 2021:

- From peak in March 2022: -14.4% or -$118,300

- Year-over-year: +2.7%.

A head-and-shoulders chart for the housing market.

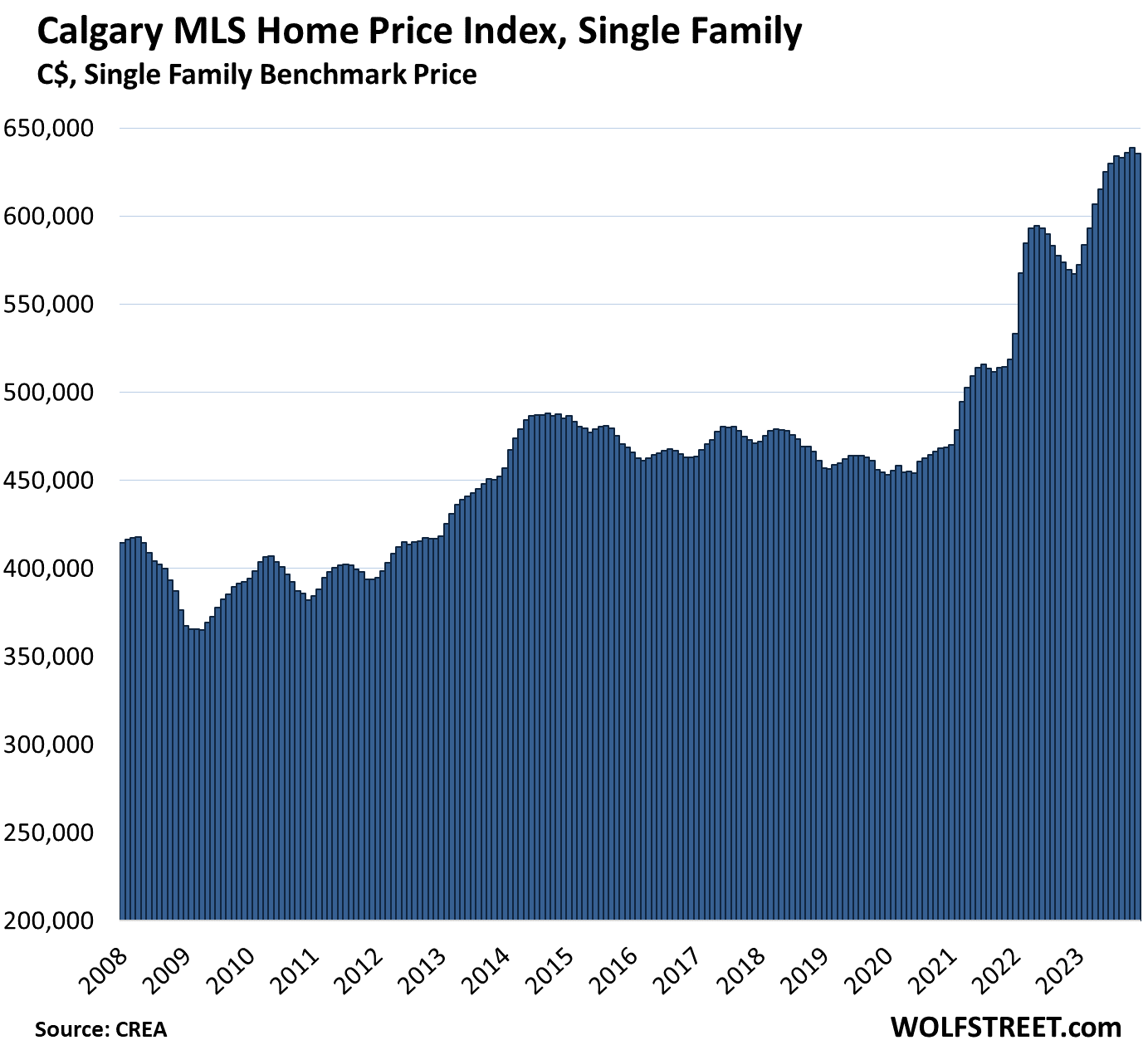

Calgary: The single-family benchmark price fell by 0.5% for the month to $635,600, having now roughly flatlined for the past four months, after the big surge earlier in 2023. Year-over-year, the benchmark price was up 12.1%. Note how prices essentially went nowhere between 2008 and mid-2020, when the effects of money printing and the renewed oil boom kicked in.

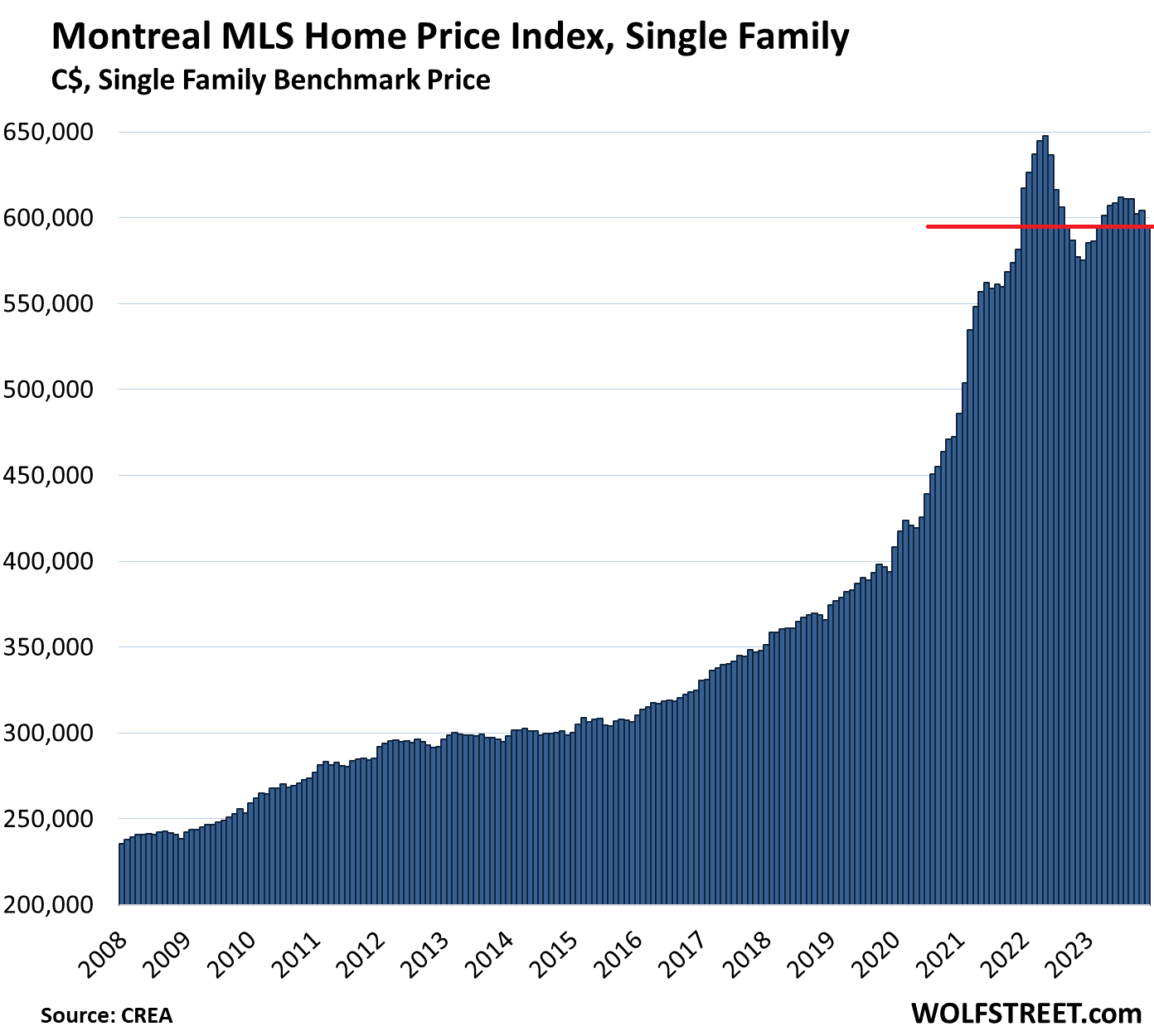

Montreal: The single-family benchmark price fell by 1.4% for the month, to $595,600:

- From peak in May 2022: -8.0% or -$52,000

- Year-over-year: +3.5%

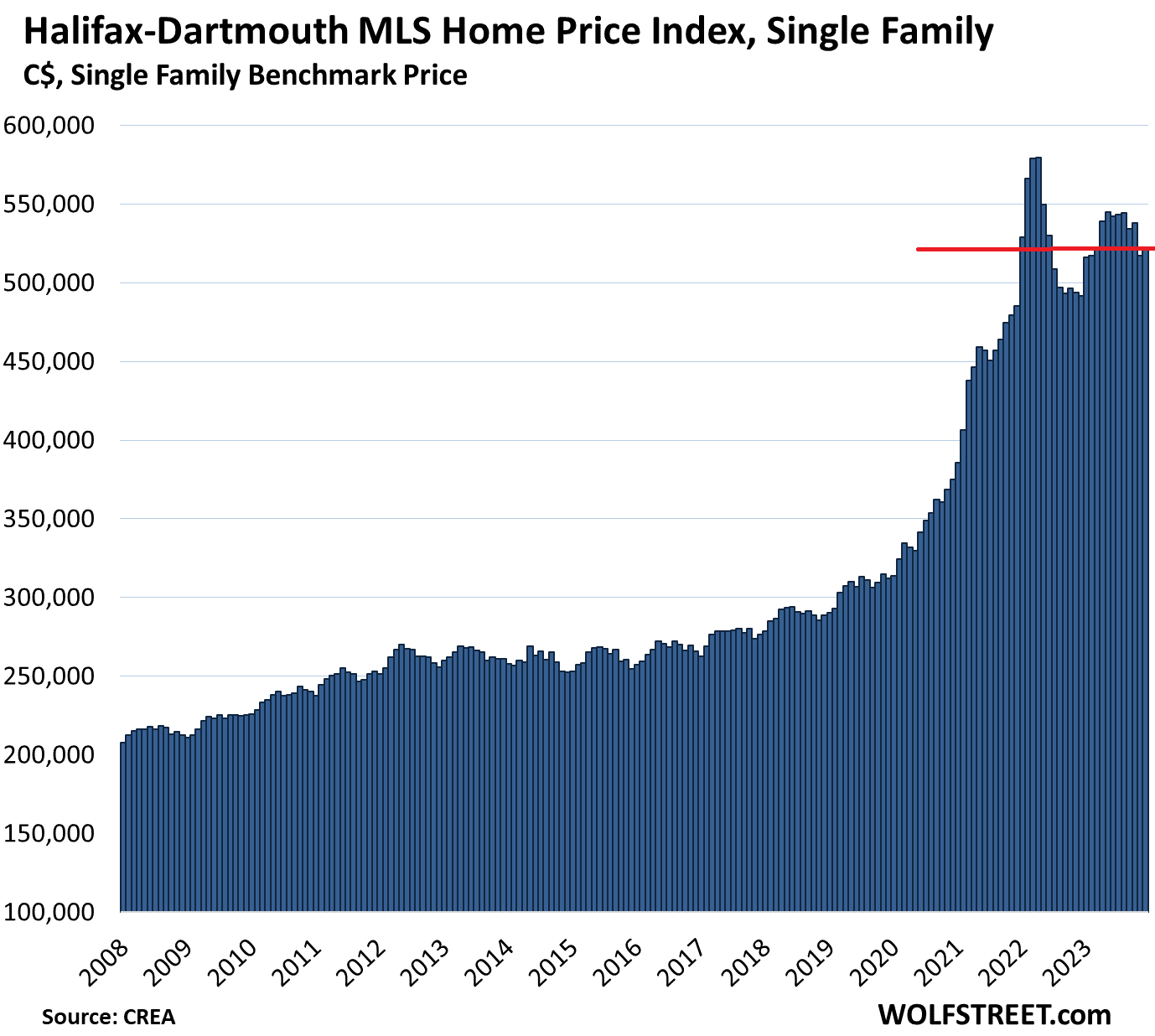

Halifax-Dartmouth: The single-family benchmark price ticked up by 0.7%, after the 3.9% plunge in the prior month, to $520,800:

- From peak in April 2022: -10.1% or -$58,700

- Year-over-year: +5.9%.

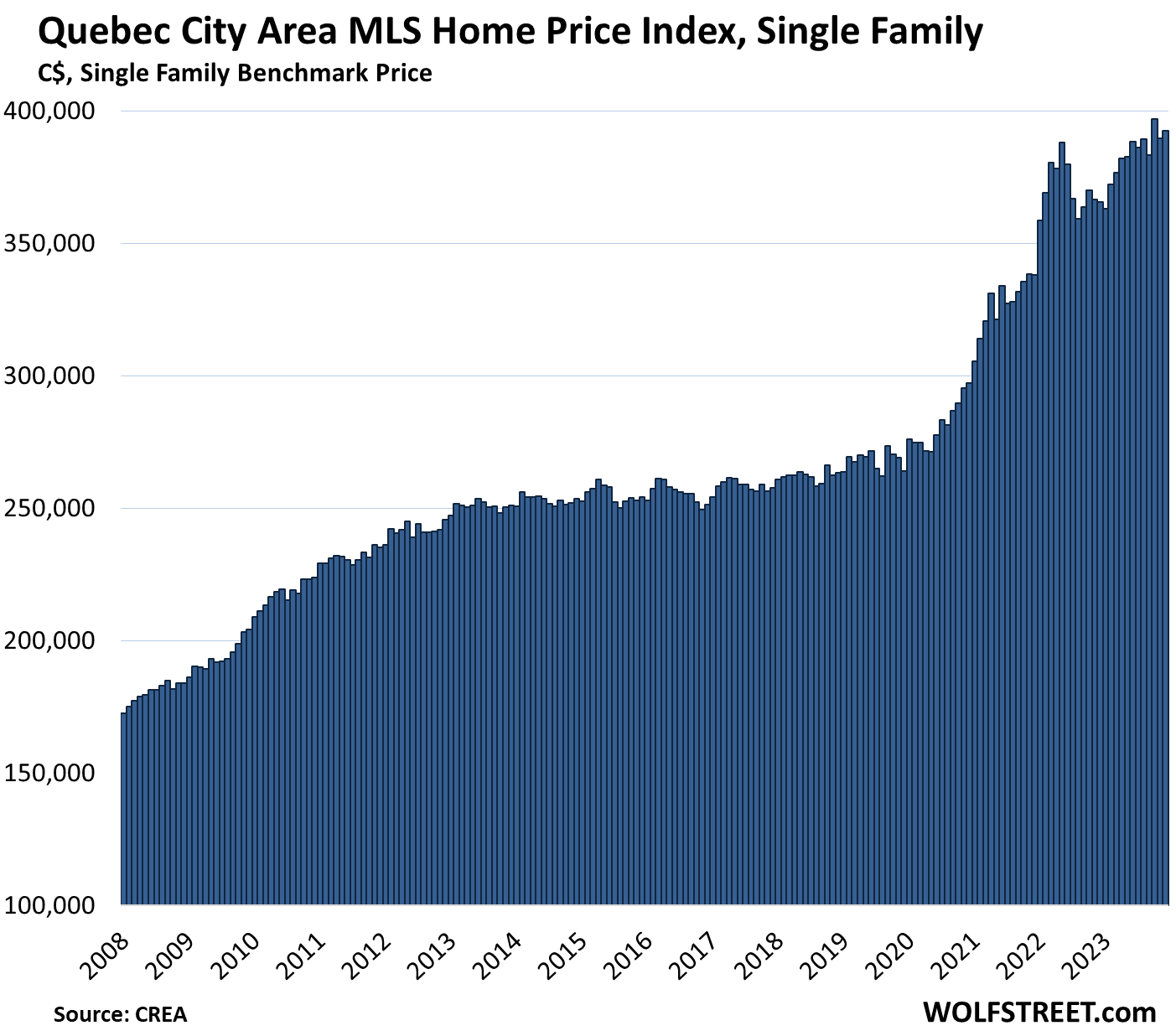

Quebec City Area: The single-family benchmark price rose by 0.7%, to $392,500 and was up by 7.4% year-over-year. October had set a new high:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The park’s are spectacular as the helium balloon bubble took home prices to the sky. Gravity and WT doing the deflating . Takes time and happens faster in Canada I Finn because the mtg rates are not fixed rate or many are not .

All the whiners here who’ve been wishing for a crash in US real estate prices can soon take advantage of the crash up north and move their complaining bitts to Canada.

Oh wait, most of them missed a 12 year bull market in housing right here. They’ll probably just do nothing again and miss another once in a lifetime investment opportunity. They’ll whine some more instead of putting their money where their whiney mouths always are!

Stocks have done much better with less hassle, but thanks for the reminder that RE can do OK. It was a definite option for slower parts of the portfolio, at least before things started tipping.

Oh hey, another housing monger reeling out hype by-the-yard.

Could it be that not everyone wanted to treat their domicile as a poker chip? Maybe some poor slobs simply weren’t fortunate enough to develop a gambling addiction or weren’t born pathologically greedy.

The world would be miles happier & nicer if jockeys like you would just stick to flipping bitcoin & Tesla stocks back & forth to one another and just leave all other items essential to life, love & the pursuit of happiness alone.

100% agree, the greed in this world is getting worse every year, even being glamorized.

bulfinch – absolutely agree –

CCCB sounds like he’s scared He waited too long?

Now he’s trapped ?

I don’t take CCCB’s comment the same way. I interpret it as he was referring to the risk averse that have sat on the sidelines because houses were “too expensive” for the past decade (or 3 years or 4 years or however long – pick a number). Now they are more so – despite the declines.

Will there be a collapse? Maybe. Maybe not. Prices have adjusted somewhat and once they hit a point where the emotional value of having a home for your family overcomes the rational side of the fear of paying too much, it’s advisable to pull the trigger if you’re planning on staying in that area for the foreseeable future. You’ll never time it right. If you do, it’s more raw luck than financial prowess.

El Katz,

I think he is looking at the quality of decisions in hindsight, which is unsophisticated. The demeanor confirms it.

He’s now got a hole to dig out of.

Bulfinch.. you hit the nail on the Head!!! The world needs more people like you. Love and regards to my unknown friend!!

Great sets of wisdom and advises from bulfinch, El Katz, and Bobber, helping to guide the kind of thoughtfulness that’s much needed in the world.

I guess also thanks to the first two comments that invited this thought. It’s only normal…

Dude,

Chill out. If you had the money to invest, good for you. A lot of people on this site do whine, and it can be both annoying and informative. Many people don’t have the means to purchase real estate so they feel left behind. In all honesty, Wolf began this site to share his ideas on the economy and many traditional investors thought he was whining, but he was also educating people by providing information. Think about it this way: You were whining and it wasn’t in an informative way so… Empathy goes a long way.

Prices are coming down in the USA too. Too bad you didn’t sell at the top. I guess timing the market wasn’t your forte.

In US, those who don’t own a house can no longer buy it. Those who do own one will have to pass the same old house to their kids as I will ensure that their kids cannot buy it in future.

Our future is a country of debt slaves who slog all their lives only for shelter, even when the country isn’t short of either land or natural resources. Looks like the 1% are becoming too greedy and the system needs a reset.

We are not very far from that point.

Repo market is close to blowing up in Fed’s face like 2019. QT is going to be shot down and QE is coming soon after. Mark my words.

I can’t think of a quicker way to get long term interest rates up to 7%.

Bobber,

Meant “more quick”. Can’t blame the spell checker.

“Quicker” was just fine. “More quick” hurts my ears.

You conveniently neglected Vancouver, North Vancouver and Burnaby. These cities have been resistant to deflation for over 40 years, or more than 1/3 of their time in confederation. It is not a bubble.

Vancouver house prices went south quite a bit from 2016 until the BOC started the money printing in March 2020. See the chart above. The BOC saved it from further declines with 0% interest rates and money printing. Now there is inflation, and no appetite at all for 0% and QE — au contraire. So good luck.

By the way, a “bubble” is on the way up. A “bust” is on the way down.

Guess u weren’t here in 1980.

50% haircut. 20% interest rates. Crushed the RE market. Didn’t recover till after EXPO 86. When the politicians gave away that land to Li ki Shing for 125 million. We are a country of idiots.

House bubble 6x yet to come down. It’s been too long inflating.

Every year people in the millions by homes in the US. Every year. Expect around 4M sales annually. We can debate bubbles and stuff all year but that won’t change the fact that millions will buy in 2024. Millions.

4 million, down from 6 million.

But, but, in the Great Ole America, according to pump pushers,

“Housing: Bidding wars erupt as 2024 kicks off, with some listings seeing over 30 offers

Improved mortgage rates means buyers are coming back — and that means competition.”

Yes, this clickbait BS in the media, designed to hype the housing market, never ends. No matter what. The industry pays the media to post this BS — “sponsored posts” they’re called. And the trolls swarm out to promote it. RE trolls are among the most insidious trolls out there.

30 offers lol. It’s disgusting. Unfortunately, there are morons buying into the hype, but there are also many others who see through it.

No morons, “investors”. The 1% getting all the properties unlimited competition to feed realtors greedy approaches

Would anyone agree? The most conservative definition of real estate “AIR” is the difference between the highest offer and the second highest offer.

The “economists” are already saying the “high” rates will come down. The rates have yet to be high and still need to go up to normalize society as housing costs are still unsustainable.

I would love to see a break down for inflation in services for Canada and see if they actually adjusted in the cpi. I sense shenanigans’.

Services inflation is included in CPI. Your desired breakdown is in the article I linked for you right here. At least look at the pictures, including services CPI and rent CPI:

https://wolfstreet.com/2023/11/21/rents-in-canada-explode-services-inflation-heats-up/

Funny how when people don’t know something, they instantly “sense shenanigans” because they don’t know, and because “sensing shenanigans” is easier than trying to learn?

The Economist’s old international comparative value standard was McDonald’s Big Mac.

In Canada in 1970 I got change back from C$1.00 precisely as McDonald’s advertised.

Today, with no change in Quality nor Quantity, the same meal deal is C$11.59.

Eleven and 1/2 times more money for the same meal doesn’t appear to be the 2.86 times my calculator says, compounded for 53 years.

Governments jig the numbers and do not take into account shrinkflation.

kam,

1. Using the price of a McDonald’s hamburger as a measure of overall inflation in a country is braindead stupid ridiculous BS.

2. Your line, “Governments jig the numbers and do not take into account shrinkflation” is ignorant BS. Government CPI measures track quantity by weight, volume, etc. So they measure gasoline by the gallon, not by the tank. They measure cereal by the ounce, not by the box. They measure OJ by the ounce, not by the carton or bottle. Every product you buy that comes in a package or bag discloses the weight or volume.

3. Quit posting this stupid BS here.

Burger King was charging $8.99 for a postage stamp size hamburger in downtown DC. I told them to cram it. There was hardly anyone in the place. I would rather buy a hot dog from one of the street vendors for $5. I’m going on a buyer’s strike. Price gouging is alive and well here.

Swamp Creature,

I’ve found fast food has gone up way faster than everything else. Most prices are up 20% since pre-2020 (not a surprise given the Fed’s balance sheet and the money supply), but fast food is up 50-80%.

It’s at the point where a Big Mac value meal is $11, while you can get a burger, fries and drink from a casual chain (Chili’s, Buffalo Wild Wings, etc.) for only $2 or $3 more.

The value for fast food just isn’t there anymore.

SwampCreature, many will surely say its due to the increases in minimum wage. I defer to Wolf’s data pulling abilities for that sort of thing. What I am noticing, (anecdotally of course, as everyone loves that here. /s) is even my low income patients, especially their young adult children, started reporting cutting way back on fast food as it became expensive but before it became outrageously so, because the knowlege is out there know even among the more poorly educated that the stuff is just terrible for us. It’s not the 1980s-90s anymore, the long term effects of ultra high processed food diets are noticible by the lower and middle income younger gens who don’t have the $ to waste on pure junk.

fair enough, I’ll go learn. I didn’t think you covered Canada’s services inflation. Only the US, my bad.

Update coming in a few hours, the new CPI just came out.

“The rates have yet to be high and still need to go up to normalize society as housing costs are still unsustainable.”

Rates, up or down, aren’t going to make housing more affordable. It takes a shift in buyers’ willingness to pay to make housing more or less affordable. The huge drop in affordability has come from people simply being willing to up the ante and pay a greater portion of their income or wealth.

NOTE: do not confuse PRICE with AFFORDABILITY.

Well it will make it more affordable by driving down the price and allow people to pay cash. Raise mortgage rates to 15% and watch the bubble implode. Then the housing ponzi scheme will end and the people who purchased in the last 15 years will be forced to drop the hot potato driving prices down even more.

Or it will just freeze up tighter than a frog’s tush.

Unless someone is forced to sell, any replacement house – if they repurchase – is inflated as well. Old geezers likely realize that “downsizing” might actually cost them money (rather than save it) and won’t sell. Youngsters will keep their low mortgage and simply put up with the floorplan they hate or bunk up two of their kids in one room – HGTV “dream home” be d@mned. The remaining stock will still be in short supply and prices will remain out of reach for the “get me dones” simply due to supply and demand. Builders will still build, but the lots will shrink, the houses will shrink, the material and finish quality will deteriorate, and the development may not be in the most desirable location.

I sold my sister’s house for a few hundred thousand less than it was allegedly *worth*. Why? The “loss” could be recouped via not having the carrying costs, paying a house watcher to guard it, risk of storm damage, the soon-to-be-absurdly-inflated insurance premiums, rising property taxes, amenity fees, lawn care, pest control, landscaping crews, my travel back and forth so the house was not considered “abandoned or vacant” by the insurance company, and so on. Then there was the lost opportunity of investing the proceeds.

All total, the break even is likely somewhere in the vicinity of 12 months. I evaluated the offer on its merits…. two week close… cash….. no contingencies (other than inspection). The key was cash… I took a lower offer for cash than a higher offer from a buyer in short pants.

An extra added bonus is that I will never have to go to Florida again.

That’s how we got my daughter’s ex-house during the 2010 pullback. Cash. 30 day close. No contingencies. The seller jumped on it because most others were FHA, VA, 5% down, blah blah blah. Too much brain damage and risk of the deal unwinding with stringent inspections (VA, FHA), short pants financing and risk of the house not appraising and the buyer not being able to fill the gap, buyer’s remorse.. and the like.

There will always be forced sellers. Death, taxes, unemployment, divorce, and medical debt. People’s fortunes change all of the time. They won’t sit on the house, as you say, because carrying costs are enormous compared to almost any other investment. Even renting it out is looking worse and worse.

Anecdotal but here in Sacramento it’s inventory galore on Zillow and a lot of them right around me seem to be rental units. They’re selling both sides of a duplex or a whole 4-plex etc, most with no recent sales history and many with price reductions. Unusual because usually all that’s available is a handful of “renovated” flip houses.

Well said El Katz. I am totally in your camp on the 1st paragraph if we do not have a big recession. I think we start to see house shrinkflation. Smaller lots and smaller houses.

One thing I remember during HB1 that sort of stuck out to me. This also ties into what Wolf said is a subprime borrower. It is a borrower with a poor credit score for whatever reason. Usually they are financially challenged which could mean a person with a $50k salary or a $300k salary. Essentially, they do not know how to stay within a budget. (They took out HELOCs for vacations or fun toys. They did interest only or adjustable rates to buy a bigger house then they could afford. , They were laid off for 4 to 6 months and could not meet their mortgage payments)

Anyway, a landlord friend of mine who had a good job as a director for the government agency at the time (he was in the 80% income level) told me during HB1, about a 1/3 of his new renters in 2008 through 2012 made more money than he did but they had lost their homes for whatever reason during HB1.

They aren’t making any more muskeg.

Should do a graph for each with the median salary in each region over the same time frames

It looks to me like home prices that triple in prices in 12 years favors only the ones that can afford the assets. What happens to everyone else? What happens to people where wages don’t triple in the same time frame? Surely the framers of such policies that promote this must see this. I mean 2 million for a single family? Now I’m no nastradamus but a reset cometh. So sayeth Jimbobjoe.

The answer to that question is “tent cities”. They are all across Canada, because rental prices make no difference whether it be in Victoria, BC or St.Johns, Newfoundland.

Rent prices are the same C$2,000-$2,500 a month for a one-bedroom apartment.

Meanwhile, wages net of taxes is about C$2,000-$2,500 depending on province. This doesn’t take into account the cost of a bus pass or car ownership, or additional rental costs like electricity, and sometimes heat and water.

I assume you are talking about rents in Toronto and Vancouver

In Quebec and Calgary, rents are around 1000-1500 sad

In Quebec and Calgary, rents are around 1000-1500 CAD

Immigration polices keep wages down. What Canada wants is indentured slaves.

Hey, Jimjoebob.

Is Jimbobjoe your cousin?

What is not factored in and this is no reflection on MR Richter it the happy data culling from sources who need to do

Better in Canada but the cost of housing maintenance specialist ally for the so called lowest rung eg condos strata’s

There is more to this than the mortgage as special assessments now no longer rare are not discretionary and the. Canadian Institute of Actuaries has flagged shallow reserve pool funding it its detailed report on the costs of aging condo infrastructure warning back in 202- that prices were way over valued in context to. This issue of structural maintenance

A condo building in Miami collapsed because the HOA couldn’t agree to do the large-scale work needed and stick the condo owners with huge assessments. Most of them wouldn’t have had the money anyway. Condo buildings can be a very expensive place to live.

Interestingly, the exact same building across the way – Champlain Towers North – is in good condition because the board insisted on regular preventative maintenance. They made the residents pay somewhat more on an ongoing basis, so no assessments were ever needed.

Keep a close eye on Markham and Richmond Hill, Ontario prices in the entire Golden Horseshoe follows whatever the prices do in these two cities. To a lesser extent the entire country of Canada follows whatever happens to these two cities. Interest rates and recessions do not affect Markham and Richmond Hill. I expect double digit gains in home prices this year and next year.

LOL. It never lets up with these real estate trolls.

The Real Tony is trying to say that real estate investors from China will continue to buy real estate in Markham.

It reminds me of a guy back in 2021 who told me that a dude with a thick Chinese accent offered to buy his townhome in cash, no questions asked.

But I wonder if those same investors lost money in Evergrande?

No one wants to buy assets when prices are dropping. It takes all the fun out of it. There are plenty of Chinese investors in Toronto too, and look at it. This stuff is just troll BS.

True.

It should be noted that the industry justification for Canadian real estate prices to the moon is because of a rent-seeking economy where wealth is gained from extracting the wages of the renters.

In other words, people are buying houses in Canada to extract rent money from renters.

The problem is that Canadian birth rates are lower and lower every year, and many people across the world are in countries where their economies are growing, and see no basis to pack up and leave their affluent lives in emerging economies to live in a basement and pay rent from their factory wages.

No one who could & would buy real estate in Canada is also buying either Evergrande properties nor Evergrande debt, for a bunch of reasons.

Foreign buyers was the bogeyman under the bed for people to blame real estate prices, but that scapegoat was slaughtered by outlawing foreign purchases. Plenty of “thick chinese accents” may buy real estate, but they are either immigrants or permanent residents. And isn’t the whole point of Canada’s immigration policy to encourage educated & successful foreigners to bring their suitcases full of cash & invest it in Canada??

Gen Z:

I really dislike your viewpoint on this. You’ve adopted the anti-landlord language of the crowd seeking to outlaw the entire residential rental industry.

Firstly, you should be aware that rent-seeking is an economic concept that is basically totally unrelated to buying something with the intent to rent it out for use by someone else. I’ll let you go research the term for yourself in the hopes you’ll stop using it incorrectly.

Second, you speak of the investment homebuyer like they are an evil, all-powerful scourge. When in reality, these people were largely just responding to the incredible influx of liquidity seeking a place to land. This is an inevitable outcome of too much cash in a system. Look to the govt and the Fed. But perhaps more relevant is the fact that purchasing a property with the intent to rent it out is not a risk-free or a responsibility-free venture. This seems especially true for properties bought in the past 4 years, during this incredible run-up. There is real risk that prices fall in coming years. Rental prices, which have also risen quickly, could likewise fall, in some places they have already fallen from their panicky highs in 2022-2023. The entire financial strategy underlying a residential investment could come apart rather quickly, and in a way that results in lost money to the investor. And in the meantime, they are on the hook for taxes, insurance, maintenance, and managing the relationships with renters, finding new renters, etc.

Third, landlords aren’t “extracting the wages of the renter.” The landlord and the renter mutually enter a contract together. The landlord provides housing at a price the renter is WILLING to pay. No one has a gun to their head. A renter unwilling to pay a requested amount for a property, will walk away. If enough people walk away, then the landlord will lower the price or face carrying the costs of an empty property. I know a few small landlords who own a property that is being rented for LESS than the property costs to maintain. They keep renting it out for reasons other than a monthly profit. In these cases, is the renter “extracting wages” from the landlord, who is subsidizing the renter with his own personal funds? No! Of course not. This is a business arrangement that both parties agreed to.

Lastly, you must keep in mind that landlords also play a critical role in the housing industry. Many people can’t own their homes, or don’t want to. If you erase all current landlords, then you’re creating a system where people can only live in a house they can afford to buy themselves. This will leave many people homeless. We need landlords to put their finances into risk and assume responsibility for the property to the benefit of people who can pay a certain amount each month, but can’t or don’t want to take on a long-term financial obligation. In exchange for that risk, they get a profit. In most cases the profit exceeds the risk. But not always.

Zest:

I haven’t said anything about banning the rent industry, except that Canada uses a literal rent-seeking model with an intention to extract as much rent from newcomers in a Ponzi scheme housing bubble.

The rent industry is a service, but the issue is when greedy people try to profit from a housing crisis which emulates British feudalism.

@Zest — run along now and read Henry George’s “Progress and Poverty.” You’re not fooling anyone.

You are a bot.

It is easy to tell, look at your grammar.

You should do us all a favor and buy buy buy in Markham & Richmond Hill.

Buy as much as you can there, and come back here and let us know what you bought, and we will check it out and assess your decision.

Canadian QT is progressing at an enviable pace as well.

Meanwhile here at home I’m reading (ZH) the QT limit of monthly T”s rolloff will be halved to $30B per month.

Disgraceful.

Quit reading ZH unless it’s for entertainment. And if you read it, pleasure yourself with it in the privacy of your own home, but don’t drag that BS into here.

ZH has been on the forefront of the QT deniers and rate-hike deniers. In June 2022, they called for rate cuts in September 2022, LOL. Ever since QT started, they said that the Fed will flip to QE in two months. The place is a running joke.

And I crushed those comments at the time when people dragged that ZH BS into here.

Take ZH seriously at your own risk. What’s “disgraceful” is you dragging this BS into here.

Hmmm.

What was it about my response to you that warranted its deletion Wolf?

So this is a general rule: If you see something on ZH, do NOT drag it into here. ZH is full of toxic BS — a lot of it is funny, so it’s good for entertainment — and it’s not my job to debunk it all. I won’t allow my site to be abused as a platform to spread this stuff.

If the ZH piece is some ripoff of a WSJ article, you go to the WSJ and read the entire article, understand timing and nuances, and who said what — was it someone from the Fed or some Wall Street goon with a book, and you ignore what the Wall Street goon with a book said and try to understand what the Fed person said — and then if you have a question about what the Fed person said, you can ask and see what happens.

If you can’t get to the WSJ article because you don’t subscribe to the WSJ, that’s your problem, don’t make it my problem, stick to ZH in the privacy of your own home and get a good laugh out of it.

A big part of the WSJ article was about Logan’s speech last week on eventually slowing QT as RRPs approach zero. I posted her QT speech here FOUR times. The WSJ article also quoted several Wall Street goons with a book, and they were just bullshitting. You didn’t read that WSJ article, you read a ZH headline and maybe a paragraph or two that twisted that WSJ article in pure BS. And you twisted that pure BS into even purer BS in order to rile people up.

This crap is not worth my time. I’m so done with it.

ZH – They cut and paste to spin almost any article into their narrative.

You need to always go read the original article that ZH used as a reference as most everything on ZH is not original.

In the past I have read a ZH article that is all doom and gloom and I read the original article and it was actually very bullish

So this article lies I wad told at the peek my house was wroth 1.3 million now its value is 650 000 if I want it sold fast. Thats over a 50% drop. So I feel trapped as our market is falling hard and fast.. and the rural areas which I want to escape to have not fallen so far yet. Do I wish I moved at the peek yup. Will I feel housing is a safe investment never. Housing is a money sucking pit. Home renovations fail. Matience is a sucker punch. And renting means that someone else figures out how to solve your problems. Probably cheaper in the long run. And I purchased at the low… we lie constantly. Please be honest we’re in a free fall, and 7 % interest is being charged to people looking at variable rates… because we lie.. 5% is a a normal rate of return on an investment.. sell now take your cash and buy what you can afford.

Howdy Lone Wolf. HEE HEE. I read ZH articles daily. You are so correct about what they are.

DFB,

Wolf ain’t lone. Plenty of company and followers here.

Zerohedge is a vehicle for Russian propaganda. There is no there, there. It once had a contrarian focus, but the doomsters, antisemites, and Russian trolls took it over. Wolf is correct. Read it for entertainment only.

Exactly right. I used to read it many years ago for a different POV but it got crazier and crazier. I finally said to hell with it and I have never missed it.

ZH is not a vehicle for Russian propaganda.

ZH is a useful aggregator that is a bit less curated than most official MSM outlets. There is a lot of crazyness on ZH but I can go there and find articles about the same event that covers the entire spectrum of opinion.

Everything, including the content of this blog must be read with at least a bit of skepticism.

The only sources of information I avoid all together are the official media. NYT, WP,Network News, MSNBC, CNN and much of the British press. Unfortunately, WSJ has increasingly fallen into that camp so I dropped my expensive subscription to them.

I keep wondering how we can fix (ie destroy) the current information infrastructure in the US. There is no silver bullet, but I wonder if simply banning advertising on the internet except at designated market place sites might work.

Every newspaper we read is simply a business that exists to be a platform for advertisers. If we simply said that all content must be paid for by the consumer through subscription or some sort of token scheme the entire climate would change.

Let’s give Wolf a heart attack ( ha , just kidding)…..

from Zero-Hedge …..

“It’s All Over”: Powell’s WSJ Mouthpiece And JPMorgan Confirm Imminent End Of QT

This is the kind of silly humor that makes ZH pure entertainment.

ZH “pivoteers” are a view to behold.

It looks like Canadian real estate was the Tulip Mania mixed together with a Ponzi scheme.

It appears that nobody can afford higher than C$2M for a home in metro Vancouver or Toronto, despite what realtors advertise.

By the way, the collateral damage of this real estate bubble and rent-seeking are the countless videos on TikTok illustrating how the police are very fast to evict tent cities which park themselves near upscale residential areas in Vancouver, Edmonton, Calgary, the Greater Toronto Area, and even as far as Nova Scotia.

Many Canadians are one rental lease away from becoming homeless. Nobody can afford to pay C$2,500 a month to rent a one-bedroom apartment on a C$2,000 a month net of taxes salary.

Canada didnt have a real estate crash back in 2008 like we did in the US.

This will be their Real estate bubble 1.0 and a great learning and investment opportunity if it turns out anywhere similar to US Real estate bubble 1.0.

The charts above show a slight dip in every one from 2008-2010. And what buying opportunity when Canadian real estate does the crash of all crashes?

This isn’t the 1970s when the rest of the world was dirt poor, and everyone wanted to start a life in Canada.

Emerging economies have growing middle classes, and even Canadians are leaving Canada to live abroad in those emerging economies.

Nobody wants to leave their comfortable jobs and pay rent as a general labourer in Canada. This is the reason why Canada is resorting to unlimited student visas which brought in the topic of cash cows and exploited labour.

Nobody wants to become a rent serf in Canada anymore, when they can live a middle class life in their home countries.

Whoever told you that more people are leaving Canada to live abroad than are immigrating into Canada is delusional.

Probably they are mixing some “pandemic remote-work from cheap paradise” anecdotes with wishful thinking to come up with that silliness.

I didn’t say anything about the number of people leaving Canada, compared to the open door immigration policy which benefits the land owners and corporations in a literal rent-seeking economy.

A simple YouTube search “leaving Canada”/”leave Canada” generates at least 500 results within a year. There are dozens of news articles and episodes regarding that issue.

This rhetoric is sounding like the land owners crying over a $20 monthly property tax increase to fund more police whose (informal) duty is to protect the capital and properties of the land owner class.

And asking rents in Quebec (in small towns which speak Quebecois French good luck finding a job there as an English speaker) are about $1800 and in Alberta about $2000 according to a latest data release.

grant,

Better dweling

December 20, 2023

Canada’s Immigration Plan Is Not Viable In Any Version of Reality: BMO

I deleted the link to the blog. Here is the real discussion of the economic issue, and they’re all now discussing it:

“Canada is caught in a population trap” by National Bank of Canada

Currently the federal government and ontario’s government have a “benefit” deal in place that basically subsidizes the rental market for “lower” income earners. The benefit rate varies from municipality to municipality and also depends on income levels and number of dependents. I’m sure other provinces have similar deals in place with the federal government. What absurd levels this country is at to try and buy enough time and civil rest as the the bubble deflates and interest rates come down enough for a chunk of the population to gorge on debt.

Wolf,

“I deleted the link to the blog. Here is the real discussion of the economic issue, and they’re all now discussing it”

I read this site often.

Do you think the information on this site is not reliable or are you just giving the original article?

I generally don’t allow links. I occasionally allow links to sites that are solid information providers, that don’t just rewrite someone else’s stuff.

Canada didn’t crash because Harper gave the CMHC 25 billion dollars to insulate the problem as he was more worried about reelection than doing the right thing by letting the bubble pop. In 2003 ish CMHC was very vocal saying housing inflation was unsustainable then. Now it’s looney tunes land.

Well, we also didn’t have the infestation of fraudulent mortgage originators that plagued the US in the run-up to the Great Financial Crisis. See Bill Black at University of Missouri Kansas City for all the gory details.

@eg

Are you sure about that?

Auto loans and housing numbers are used for Canada’s gdp growth. In the auto industry as long as underwriters check the “boxes” and call dishwashers “managers” the deal auto snaps with no oversight for 100k deals…. Was the housing sector similar?

Obviously a lot of somebodies can afford and are paying those prices and will be doing so for quite some time ahead.

I think what you’re missing here is that if large numbers of people can’t afford their rentals, then they’ll stop renting. And if enough stop renting, then rentals will sit empty, forcing landlords to drop prices down to a level that people can afford.

Furthermore, I don’t envision many people would actually end up homeless. More likely, they would end up sharing housing with more people. But that would have the same effect of reducing the number of available renters, forcing down rental prices, as demand drops. Unless, of course, the volume of renters keeps growing faster than the volume of rentals. Then, yes, it may be inevitable that some people have to live in more crowded settings to share rent. What I think is most likely is that anyone only taking home 2k a month is simply too poor to expect to live in their own apartment in Toronto. That person either needs to find roommates, or take steps to increase their salary. Or, they may need to move to the outskirts, or find a new city altogether where the economics make more sense for their situation. You say people can’t afford these rental prices, and yet here they are, hundreds of thousands in Toronto alone, affording them. The people who can’t compete get priced out and they find somewhere else to go.

In reality, people ARE making these choices all the time. We’re all finding roommates, living on our own, getting more income or less, adjusting our lifestyle and location based on what we can afford. This is just the reality of life.

Wolf, I think you might have left out ‘fallen’ from the first sentence.

Thanks!

>over the next three months, the BoC’s

>total assets will drop by another 10%

It didn’t drop during the last 4 months, and Tiff Macklem kept telling us that BoC continued QT?

Nick,

You got this ignorant BS from a braindead blogger who doesn’t know crap. Don’t go back to that site. You’re being lied to.

GoC bonds mature on the first of the month. None mature over the holiday period between Nov 2 though Jan 31. And none mature over the summer from June 2 through August 31. It’s the same every year, no matter who holds those bonds.

Maturities of the BoC’s Government of Canada bonds. When they mature, the BOC gets paid face value for them, and they come off the balance sheet:

Thank you for spending so much energy to dispel BS by your readers…

Hats off to you 👏

Will Canada follow our lead if QT comes to a grinding halt here? I’m really curious how that would play out. And before I get shot down, I’m not saying QT is ending, just wondering how much they would follow or us, or if they would have the backbone to do the right thing and continue to tighten things up. Their housing mess up there is quite possibly worse than ours down here.

QT won’t come grinding to a halt for a while in either country. Lots of BS has been circulated for two years about QT either never happening or ending next month. The Fed will tell you well in advance how and when it will slow QT. And slowing QT just means it will go on for even longer, as the Fed’s Logan said last week, the purpose of slowing it would be to allow liquidity to move where it’s needed and avoid a disruption that would “prematurely” end QT, she said. Slowing QT would assure that it could go on for a long time. People need to read what these Fed people say and not just regurgitate ZH headlines. I posted her actual speech here four times.

This inflation we’ve been seeing for the last few years is bad for everyone but particularly bad for the rank and file employee who lives paycheck to paycheck. It needs to be reigned in. I’m not relying on what various website folks are saying, but what my gut tells me happens each election cycle, no matter who the current powers that be happen to be. It almost seems like clockwork that every 4 years we hear that everything is great and only getting better (let me emphasize that I’m not taking a side here, just observing so many of these cycles and seeing a pattern). All I’m wondering is if Canada will ignore the usual spin and do what’s right and get this under control.

Some people mistake the fact that Canada/USA have highly coupled economies as meaning the BOC is a bunch of blubbering idiots who are only capable of copying the fed.

In reality, the BOC has a lot of smart people who are capable of actually analyzing domestic economic data to plan its actions.

BOC will alter its QT plans if & when Canada inflation looks at risk of falling below 2%

Yeah, real smart people. They helicoptered a half a trillion dollars to the commonfolk, drove asset/goods/service prices to the moon, and are now baby-stepping their way back to normalcy because to do otherwise “might hurt homeowners”. As if that should even matter. Meanwhile, nobody can afford sh!t anymore because the people who control price stability, lost control of price stability.

Geniuses.

Get off your pedestal, grant. The BOC are idiots with no accountability.

And all the BOC does is deal with Loonies

We will have to watch and see what happens in spring and summer if the Bank of Canada does cut interest rates. The Canadian housing market is incredibly expensive, yet the country has admitted 1.2 million newcomers over the past year. The Bank of Canada has acknowledged that population growth is adding pressure to shelter price inflation, yet the government plans to continue its current immigration policies. These are difficult times for Canadians and I hope things improve.

Way back in 2005 W5 did a documentary pejoratively referred to as “NotCanada” based on the website’s name, about educated newcomers, mainly teachers, surgeons and accountants who were promised a career in their fields, only to end up being excluded due to licensing bodies and the system.

The internet was at its infancy and the website mysteriously got deleted, and all traces on the Wayback Machine were vanished.

Now type in “Leave Canada” on YouTube, and the amount of people who are dissatisfied with Canada are through the charts.

Many educated people in emerging economies don’t want to be packing boxes in Canada, and handing over a large portion of their meagre wages for exorbitant rent, when they owned property in their home countries and were middle class.

One aspect of democracies is that majority rules, which has drawbacks for minorities. When a majority of families owns houses, it’s tough for renters to get adequate representation. Its why we see so many home subsidies in the US such as $500k gain exclusion, mortgage interest deduction, tax free like kind exchanges, etc.

Problem is, once home prices skyrocket to price in these incentives, home buyers need more incentives, like years of zero interest rate policy. Once that gets priced in, the question is not whether they can buy RE, it’s whether they can afford lube.

Canada allows a principal residence exemption for capital gains. The major issue with Canada is that it’s no longer attainable to save money for a downpayment, much less enter property ownership due to high rent costs.

The rent costs are like the modern day feudal system where newcomers just exist to work dead-end jobs, pay usurious rent prices, and save nothing at all.

This wasn’t the case 20-30 years ago. It’s like those who already own property decided to pull the ladder and use real estate like a Ponzi scheme.

GenZ,

Capitalism has many of its roots in the fuedal system. When people grew stuff and gave most of it up they didn’t try to be super productive. So they rented the land and as people became more productive they simply raised rent. Capitalism is often referred to as modern day fuedalism. Capitalism is better but the land owners/capitalists still and always will have the upper hand.

Glen, Canada’s case is a bit weird, in that the land owners collude with the state to make it profitable to invest in real estate.

This is why despite complaints about a housing shortage, housing crisis, jobs hard to find, the policies are there to encourage a constant supply of greater fools coming here under the impression that they will live a middle class life with a home, 2 cars, and a yearly vacation.

However, when they arrive in Canada and spend away their life savings, they can’t go back to their homelands due to having no money and estranging their social and employment connections.

So they are stuck in Canada breaking their backs in warehouses, factories and driving taxis late at night with little chance to go up the social ladder.

The smart ones eventually realize in a few weeks, that Canadian consultants lied to them, and they jump ship before ending up in a trap of no return.

Someone who has emigrated to USA as a high skilled worker 24 years back .. based on my experiences and current conditions in UsA I tell my folks back home to stay put if they are in the upper middle or higher economic strata. It simply does not make sense for them to come here as the other countries made so much progress and usa went down during 2 decades or so relatively.

Although usa still the best out there but the hassle and other inconveniences are not worth it.

Actually the federal government is talking about reducing “temporary forgien workers / migrant workers” and international students. Immigrants and refugees are not being considered for reductions at this point.

The catch (and possible pit fall) to this is that migrant workers are seen as the most productive workers (mostly lower wage jobs) and greatly reducing their numbers would likely guarantee higher wage inflation.

And international students…. many educational institutions have become hooked on the greater revenue that is generated from having a higher percentage of international students. Laurentian University during covid and currently a number of other universities (notably Queens university) are now not only reducing profit – some are immediately running a deficit having to make moderate cuts to the volume of international students (and cutting courses). If the university’s increase costs to domestic students that would guarantee higher student debt.

No answers or solutions that don’t cost.

The federal government has released several statements over the past year regarding “considering reducing non-permanent residents”, yet nothing actually has been done. The Liberal Party has plummeted in the polls and the anger regarding housing costs, cost of living, and the link to immigration is palpable in Canada.

The December inflation report today showed rent rising 7.7% on an annual basis. Housing costs are by far most people’s largest expense and cutting newcomers will provide relief. Perhaps there will be wage inflation and higher university costs, yet history has shown that Canada did just fine with lower numbers. Besides, for those struggling to keep a roof over their heads, these concerns are not at the top of their mind.

Many of the jobs that international “students” are doing used to be done by high schoolers doing a summer job, or people who got laid off, and wanted to fall back on something until they get re-employed in their fields.

These days, getting a part-time job, or a minimum wage job in a factory or warehouse is like finding oxygen on planet Mars, because those vacancies are already staffed with international “students”.

And what’s a stick in the eye to someone’s dignity is when someone gets laid off, can’t find a quick job to fall back on, exhaust EI and end up on welfare, told to find a job as if the person wasn’t trying to find a job in the first place.

No wonder more and more Canadians are unhappy.

I guess it’s encouraging to see that there are some countries where the housing gigabubble is being allowed to deflate.

All bubbles can very easily and very rapidly deflate everywhere.

Edmonton had -36 deg F temperature and -75 deg F windchill over the weekend.

No housing crisis there, I bet.

Edmonton just took down 8 tent cities in the last 2 weeks.

The Provincial governments have a large affect on rental prices by very landlord unfriendly legislation. A favorite strategy is to pay first and last month’s rent, move in and then simply stop paying rent. The system is so backed up it can take 18 months to repossess your property. Appeals, or a simple mistake in the complex legal procedure can drag this out further.

Some tenants even sublet rooms during this time and make huge profits. Many also trash the property with no repercussions. It has happened to my family 3 times. I would never rent out my property in Canada again.

This is what happens when the wealth inequality increases a lot and few people are renting to larger population.

People who can’t even afford rent forget buying would have nothing to lose and then try these shenanigans.

It is bad for the society over all with this much wealth concentration and rentier economy.

In the end even the land lords would suffer big time .

Those renters must have learned those tactics from renters in the U.S.!

Thanks Wolf!

Thoughts on housing and the economy from the perspective of someone that came of age in the seventies, another tough time.

Real estate won’t fall heavily anytime soon because the Fed has too good of a grip on the economy nowadays what with QE, QT, and interest rates, and the U.S. current U.S. technology ‘bloom’ is enormous.

The boomers will pass on their wealth gradually and those younger people that have kept their nose to the grindstone will eventually benefit.

There are still ugly desolate places where land is cheap.

Barndominium shells are affordable for those willing and able to put in sweat equity.

Likewise in sweat-equity in the rural West and in some other places rain harvesting, compost toilets, solar tax credits, and IRA rebates are making off grid living more affordable.

Global war or a pandemic are about all that I think could derail the U.S. economy and radically lower housing prices quickly and that would be worse for most.

Canada 5-year bond increased by almost 5% today (currently at 3.42%).

This means that the concept of interest rate cuts to 0% interest rates is not plausible in the near future.

Which means that real estate prices will struggle.

MW: US Treasury yields rise by most in a month or more as US, European central bankers try to cool rate-cut optimism

MW: No rate cuts in 2024? Why investors should think about the ‘unthinkable.’

One thing I noticed people not mentioning is the why. Why was Canada actively increasing its housing bubble. I saw a stat today that Canadas GDP growth rose 166% since 2000. I also read that in Q1 2022 Canadas residential investment grew 5x the rate of GDP. Isn’t this what drove the US housing bubble? So was / is Canadas only way to build GDP growth through its housing bubble? If so, this explains why they now need large numbers of international students and new Canadians?

Builders cutting prices by throwing in MANY concessions. $20-40K….

While not major “decline”…it’s just compressing their margins. If this continues, at some point, it will HURT profits. They aren’t building smaller homes. They have the same basic plans……just selling them for less than they were a year ago. Many large builders have their own lenders and offer buy downs……2%.

Amortized over 30 yrs…..2 point buy downs are HUGE.

I am an appraiser……just reporting what I see.

So called price declines are deceptive…. no one buys real estate in Canada during the winter months. Come back and check those numbers in the spring. — and what happens when interest rates start decreasing?…..prices will go up again.