Those who can, pay cash to avoid the interest rates. Subprime credit tightens substantially.

By Wolf Richter for WOLF STREET.

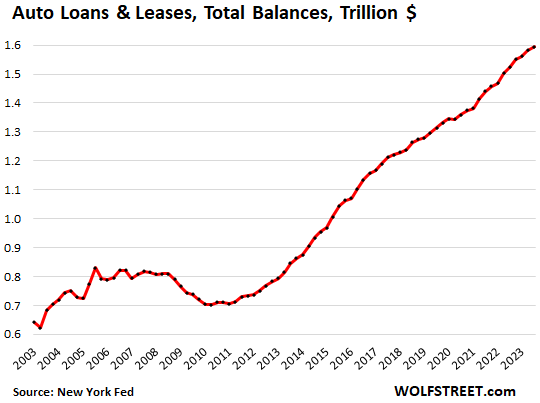

The balance of auto loans and leases rose by 0.8% in Q3 from Q2, and by 4.7% year-over-year, to 1.60 trillion, driven by financing of new vehicles, according to data from the New York Fed’s Household Debt and Credit Report.

New vehicles account for the bulk of the auto loans and leases. New-vehicle prices still rose in Q3, and new-vehicle unit sales jumped 20% year-over-year. So that’s where the increase in loans and leases came from.

By contrast, used vehicle prices have been falling since the ridiculous spike through 2021, and retail sales of used vehicles in Q3 were roughly flat year-over-year. Used vehicles are not contributing to the increase in auto loan balances.

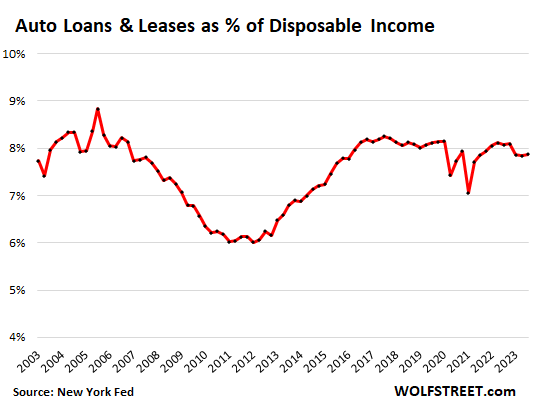

More buyers pay cash. The much higher interest rates make borrowing unattractive. With new vehicles, automakers’ captive finance units are buying down interest rates to 1.9% or whatever. But this is an incentive in lieu of cash incentives, such as a big rebate, that cash buyers get. And so the percentage of cash buyers has risen this year for both new and used vehicles.

About 20% of new-vehicle buyers and about 61% of used-vehicle buyers paid cash for their auto purchases, according to Experian’s Q2 report on auto finance, up from 16.5% and 58.5% respectively a year earlier. And these buyers have no debt burden associated with their vehicle.

The debt burden fell this year. In terms of the aggregate debt burden, total auto loans and leases outstanding amounted to 7.9% of total disposable income, a tad below where they’d been during the Good Times before the pandemic.

Disposable income is income from all sources except capital gains, minus taxes and social insurance payments. This is the cash that consumers have left to spend on, for example, cars.

The fairly sharp drop in the debt burden ratio this year was due to the increased portion of cash buyers along with the biggest pay increases in 40 years:

Credit has tightened substantially for subprime. The part of auto lending that is seeing tighter financial conditions is subprime lending. Loans are harder to get, some of the most aggressive lenders/dealers have filed for bankruptcy, and other lenders have tightened their subprime underwriting. Losses lead to more prudent underwriting, which eventually leads to fewer losses. This is part of the subprime cycle.

So the share of subprime as a percent of total financing has dropped. According to Experian’s Q2 report, subprime’s share of total originations of loans and leases dropped to 15.0%, down from 16.8% a year ago, and down from 17.8% two years ago.

Prime borrowers have no problems financing or leasing a vehicle, but the cheap money is gone.

Borrowers pay out of their nose: According to data from commercial banks collected by the Federal Reserve, the average interest rate for 72-month new vehicle loans has spiked from 4.84% in February 2022, before the rate hikes started, to 8.12% in August 2023.

But it’s less shocking than it seems. For example, for a $40,000 loan at 4.84% for 72 months, the payment was $642 per month; at 8.12%, the payment is $704. I can already hear it: “Just $62 a month more, and you get your dream.” And people want their dream.

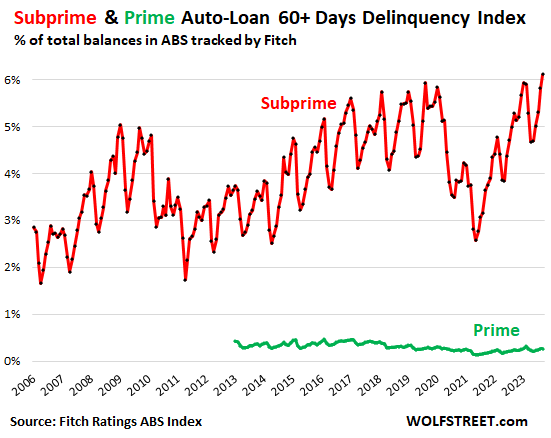

Delinquencies are driven by subprime. Subprime is always more or less in trouble. That’s why it’s subprime. In the auto-loan market, selling and lending to customers with subprime credit ratings is a high-risk high-profit specialized activity, largely limited to older used vehicles. It has attracted a bevvy of specialized lenders and dealers, often backed by PE firms. The system hinges on being able to securitize the subprime auto loans into Asset Backed Securities (ABS) and sell the investment-grade tranches of those ABS to pension funds and other yield-hungry institutional investors at relatively low yields, and that works until it doesn’t, and now it doesn’t.

A number of those ABS deals got scuttled recently, and some got pulled off only after they’d been renegotiated, and several of those specialized operations have filed for bankruptcy, and we covered a couple of them here.

There’s a peculiar subprime cycle, where low yields enticed specialized companies to get very aggressive and take huge risks, backed by yield-starved investors that buy the ABS. But after a while, because those deals were too aggressive, the risks come home to roost, and investors are taking losses, and they’re getting skittish, and the whole math sort of begins to unravel. That happened in 2018, and it’s happening again.

But subprime is only a small part of the auto-lending business, and an even smaller part of the auto-sales business because lots of people pay cash. Of those buyers that finance new vehicles, only about 5% are subprime; and of those that finance used vehicles, 22% are subprime, according to Experian.

And subprime loans that are at least 60 days delinquent spiked through September (red line). But prime loans are rock-solid with minuscule and stable delinquency rates that are below where they’d been before the pandemic, according to the auto loans backing the ABS that are tracked by Fitch Ratings:

The overall delinquency rates of auto loans and leases are always fairly high, compared to mortgages, but are below the delinquency rates for credit cards.

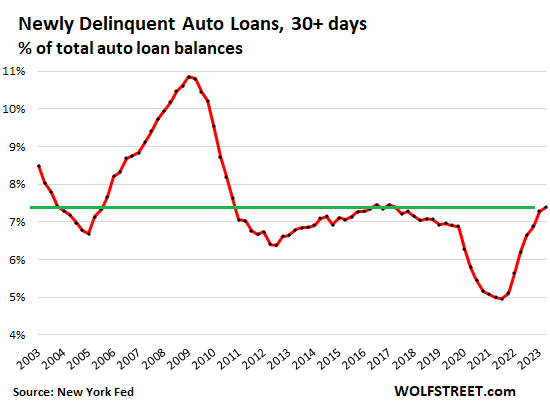

Auto loans and leases that just transitioned into delinquency by the end of Q3 inched up by 11 basis points – the slowest increase since they started increasing in Q1 2022 – to 7.39% from 7.28% in the prior quarter. So they’re roughly back in the normal range:

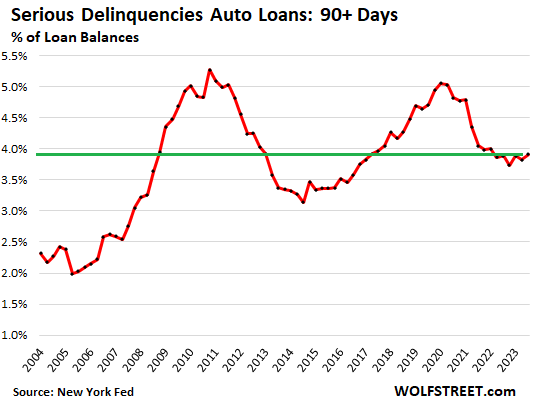

Auto loans that were seriously delinquent – 90 days or more past due by the end of Q3 – barely ticked up in Q3, after dropping in Q2, and are relatively low, compared to the past 15 years:

Earlier today, we were wondering, “where’s the hangover from the party?” Read… Mortgage & HELOC Balances, Delinquencies, Foreclosures: How Are our Drunken Sailors Holding Up?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s kind of comical to witness how people were tripping over each other paying well over stickers in 2021 and 2022 to now see their beloved vehicle value depreciate quite a lot especially when you consider the over the sticker premium.

This is especially hilarious for all the FOMO buyers on hot electric cars back in the craze and fast forward to now electric cars have some of the worst depreciation. Doesn’t help also when Tesla undercut brand new owners with price cut as a sign of appreciation to their loyal customers :) All in all, great to see some of these FOMO buyers get their A$$ handed to them now, for most if they actually can exercise some self restraint and do a buyer strike perhaps we wouldn’t be in as nutty of a market as it is now..

New-vehicle price cuts, huge price cuts after years of crazy price increases, are exactly what consumers and this economy needs. US legacy automakers are 10 years behind and are falling further behind by the day, they’ve gotten fat and lazy riding up their pickup-truck cartel to huge price levels, and their entire top five layers of management should get fired and bonuses clawed back for idiotic decision making. And people that bought a Tesla before the price cut, well they’re going to have to hold it till maturity, LOL.

And people that bought a Tesla before the price cut, well they’re going to have to hold it till maturity, LOL.

LOL… in this case that means as long as the battery lasts.

Surprisingly, these EV batteries have been lasting quite a long time in use, very much longer than the owner’s desires for the next new car. And the loan balance at trade in can always be rolled into the new big note!

Cars aren’t sold on price, but the customer’s monthly payment. Are there now 84 month auto loans?

The ability to roll over negative equity into a new loan hits a tipping point, especially at 8-9% interest. Most credit buyers won’t exceed certain parameters (% over MSRP) when evaluating a loan app.

Tesla’s price cuts are more transparent than the funny-money dealer cash discount programs most manufacturers rely upon. Customers know up front what the “incentive” amount is when the price is reduced…. vs. hidden cash that the dealer can use (or not use if they find a chump). Both have the same effect of reducing the trade in value of existing rolling stock. Companies spend an inordinate amount of time evaluating future values. IF the vehicle is leased, the customer is insulated from the impact of discounting as the residual on his contract doesn’t change. The retail buyer ain’t so lucky.

Just make sure you have GAP insurance in the event you wreck it before the lease matures (or your retail loan for that matter).

Anthony A – loan terms > 72 are becoming more and more common. Think 30%-40% of new unit volume depending on the brand. Most common for banks, still rare for OEM captives. Notes > 84 remain exceedingly rare regardless of finance source.

El Katz – a GAP debt waiver is generally included in lease, but Toyota Finance is a large and glaring exception. However, loan GAP is a must have in this environment. If you can avoid it don’t buy from the dealer, they’ll mark it up by $300-$500. Buy separately after you leave the dealer.

Also on GAP, it’s smart to cancel after the first 24-30 months of your contract. 80%+ of GAP loss happens before month 30 when negative equity is highest but refunds are pro-rata so you’ll get back 60%-70% of your premium (ex a common cancellation fee)

You don’t need gap insurance if you are putting down 20%.

Anthony A: “Cars aren’t sold on price, but the customer’s monthly payment.” Yeah, that’s the standard salesman’s approach. We shoot that the eff down immediately. Anyone who doesn’t negotiate on price is a sucker.

The idiocy of management in the auto manufacturing business is comical.

It will be long time, if ever, that US auto industry implements effective, efficient management practices.

Teh current crop of white hair executives were the yes men and women of the 1980’s era that destroyed GM by following the misguided management principles and practices of Roger Smith.

Peter Drucker, renown author on management wrote extensively about the US auto industry’s practices and problems 50 years ago. Sadly, time stood still for these revolutionary leaders and managers for many of the same problems are still besetting the auto industry today.

The auto industry changed for the worst when the MBA’s took over, replacing the engineers and / or automotive industry experts personified by people such as Bob Lutz. I lived it. The new breed tripped over 10 dollar bills to pick up nickels. There was no rheostat on decisions… just an “on” and “off” switch.

Once everything became about price/profits/cut-cut-cut, that was the death knell. Financial engineering became more prevalent than actual product engineering.

“Ya want it fast, good, or cheap? Pick 2.”

Comical for sure! These guys decided one afternoon all they had to to do was yank out a gas engine, toss in an electric motor and they were in the game. No thought to charging, no thought to the modern way to sell cars. No thought to anything. Now they have a mess on their hands. Tesla figured it out and figured it out well. And no, I don’t mean Musk. Tesla has high quality people no one has ever heard of and they figured it

US Big Three automakers do not want to sell electric vehicles. They make a lot of money selling trucks and SUVs. Each EV they sell is one less truck they will sell. The more EV’s they sell, the less money they will make.

Eventually they could make lots of money selling EVs, but Wall Street looks to the next quarter and their bonuses are not based on future profitability.

That is why new entrants to the game have the ability to surpass the Big Three. They have no legacy products that they need to protect.

Mea Culpa, I was one of those automotive managers that thought Elon never had a chance to create a car company from scratch, an electric one, no less. That was a decade ago, and jeez, look now. I thought he had a chance to be a niche player, at best. When you consider what he accomplished since then, it is astounding, and a worldwide company – no less, and in barely over a decade. He and his team totally upended the thinking of all automotive planners, almost overnight. Around mid-decade, we went from “ignore him, electric will not catch on for decades, IC engines and oil interests wouldn’t go down without a fight.”, to 200 slide McKinsey PowerPoint decks on the “Tesla defense strategy”.

The hazard in the auto manufacturing business is how to respond to the sometimes limited attention span of the herd. In the ’70s there was the huge demand for smaller cars based on the pump price for gas and the media-generated ‘crisis’ mentality; then the market evaporated when gas prices declined and the herd wanted big cars again.

In recent years the established automakers, and new automakers, have put hundreds of billions into electric cars, a lot of which will now need to be written off. There is a market for these products, but surely not as huge as was believed not long ago, and the evolution of the business will proceed as economic viability allows.

Attempting to run huge companies when the market is motivated by fads or temporary events is difficult. And companies that are excessively motivated by their marketing departments are especially vulnerable if they are focused exclusively on short term sales numbers rather than taking a measured approach.

Arbitrary product composition goals based on a current mania, issued by politicians and bureaucrats responding to the latest poll numbers or media headlines don’t help either.

ElK – very true, when upper management never works a single day on the factory floor, their favored skillset being a highly-portable one of monetary manipulation with no actual need for love of, or even familiarity with a firm’s base product. That said (at the risk of examining deeper history), the ossified Detroit engineering/mg’t establishment patted Deming on the head post-WWII and continued much as before (…even MacNamara’s ‘Whiz Kids’), leaving him to converse with Japan. The results of the long, slow roll from there still institutionally denied by the (formerly) ‘Big 3’…

may we all find a better day.

91B20 1stCav (AUS), year after year, I read the annual ratings of cars by Consumer Reports. I felt loyalty towards the “Big 3” and didn’t want Japanese car manufacturers to beat them at their own game. What followed was that I heard about Deming and the fact that Ford completely disregarded his advice. I eventually lost all hope. I have only bought Japanese cars (and now South Korean), in the last 35 years.

Are all the cash buyers really cash buyers, or are they financing elsewhere and just not at the dealer?

Max,

No, unless they borrow from grandma.

ALL lenders put a lien on the title, and this data is based on registration data and liens, obtained by the credit bureau Experian. Credit bureaus know everything about your credit, LOL.

BTW, dealers just arrange the loans, and get paid to do so, they’re not the lenders.

@Max just like a huge percentage of real estate “cash buyers” are buying with a loan secured by another piece of real estate to speed up the transaction a huge number of “all cash” car buyers are buying with HELOC money (less today than three years ago and there are many comments on the Bring a Trailer used car site about how the classic car market has slowed now that HELOC money has gone from under 5% to over 8%).

ApartmentInvestor,

OK, you can put up your house as collateral to finance a car with a HELOC instead of with a car loan. But you’re dragging oddball examples into here by their hairs…

1. You can lose your house if you default on the HELOC that you bought your car with, instead of just losing the car if you default on a car loan. Borrowing on your house to finance a car is dumb from a risk perspective. I cannot believe an RE guy, of all people, is even suggesting this.

2. Look at the HELOC numbers: they’re minuscule. Not many people are this dumb to finance a car with a loan secured by a house, when they could use the car as collateral. HELOCS are used for home remodeling projects, medical emergencies, and the like.

3. The people that buy classic cars are a minuscule number. So that’s a stilly example. This is NOT a mass-market activity. They’re so small it wouldn’t even make a ripple in this data. New and used vehicle sales retail in the US are close to 30 million units a year — and over that in a good year. Classic cars aren’t even a flyspeck in comparison to 30 million units. And they have a special problem: finding lenders that lend on a classic car. So they may have to find other sources to fund their classic cars.

4. You can obviously borrow against your stocks (margin) to buy a car, at a rate that may be higher than a car loan, and then you get a margin call, and then you have to sell your stocks into a crash and lose part or all of your portfolio and equity, but at least you get to keep the car?

well yes and no Max

my daughter decided she needed more fuel efficient vehicle

graduating college next month(BS)

she had 2016 ford expedition – used to haul teens for church as she was teen leader

dealer didn’t want to give her value – $13k

she sold it in 2 days for $16k to another member of church

she bought 2020 as they didn’t want to deal with new 2023

she saved $7k and has vehicle with 20k miles and 2 years left on warranty

She worked and saved during college and had over $10k, balance as LOAN from me given her 700+ fico

If you consider the amount of money saved monthly through new and refinanced mortgages at sub 5% rates during the past decade, this all not only makes sense, it means consumers will stay drunk for years to come, so they’ll be buying la lot of more expensive cars and a lot more Chinese (and now American & Mexican) made junk.

Here’s the Math:

*Mortgage rates for the past 50 years averaged 7.75%

*62% of the 85+ million homeowning US households have mortgages under 4%

*At an average home price of $350k with 10% down, that’s a savings of $12,000 per year

*Multiply that times 52 million homeowners and there’s now $625 BILLION DOLLARS more EVERY YEAR being pumped into the economy.

These drunken sailors have legs. Time for another round of shots!!!

***(Note – I googled all the statistics, so hopefully they are close to accurate)

Nice step through and worth reviewing.

One immediate thought…there are likely about 25+ million households without any mortgage debt (paid off…skew older). When those homes hit the market as Baby Boomers retire to sunnier climes/die, those sales-price-less-sensitive homes will drop average home prices…which might undercut the spend-stimulus you lay out.

Right now the transaction-starved mkt is seeing high prices propped up by…transaction starvation (lack of listings). That is unlikely to last (see sunnier climes retirement/pushing up daisies above).

Still like your step-through though…keep em coming.

Your stats look pretty good. The 10% down figure you state is going to vary a bit but otherwise it looks alright.

The good news is there are bargains on used Teslas. I just bought a Model S P85 with rear facing third row seats (to separate the kids) and Unlimited Lifetime Supercharging and a new battery for $17,500.

You have to take it real easy on the accelerator pedal, these things are fast. Oh, just to let other rednecks know, there is no AM/FM radio.

A new battery? Did the prior owner replace the battery, like under warranty?

“ And people that bought a Tesla before the price cut, well they’re going to have to hold it till maturity”

I’m sitting in my town’s barber shop right now reading this article while listening to an old guy tell us he sold his Tesla after two years because the insurance was sky high. Repair costs are the assumed reason for that. It’s always a shock how much insurance jumps on a new car purchase, but might be wise to check in advance before you buy your dream.

Auto insurance spiked in general.

This Drunken Sailors thing, I mean.

Like the well curated general actitud of this forum, perfectly summarized here: “if they actually can exercise some self restraint and do a buyer strike perhaps we wouldn’t be in as nutty of a market as it is now”.

Yeah, it is the people! It is the fault of the people. Those drunken sailors!

If they just were willing to hold on to those depreciating dollars while the Government inflates their value away, we wouldn’t be having these problems. Show some self-restrain people!!!

Let’s blame the people, not the Government for running those massive, *M*A*S*S*I*V*E*, debts which I am absolutely sure are not being/won’t be monetized by the Fed. No, no, they will be paid with the taxes of our increased productivity, AI and the rest. How come people don’t see it, darn it!

Let’s not blame the Fed for injecting unprecedented amounts of liquidity into the system, i.e. money supply. Hey, don’t you see we are tightening now? Forget about the previous years. Rest asure if something goes wrong the Fed won’t open the floodgates again alas 2008 or SVB, promise! pinky?

Argh, drunken sailors. Hold onto those depreciating dollars people!!!! We are trying to accomplish something here!!!

Its not like the only places to store wealth are the USD and housing.

T-bills yielding 5.5% currently accrue interest faster than inflation eats away at the dollar. I am personally keeping my savings in T-bills.

No one is *forcing* you to spend your money – that’s on you.

NB: I do agree the Fed’s policies are also to blame.

BUT, no one is forcing you to spend $5 on coffee every morning, or buy all that stupid crap from Amazon that you don’t need.

Learn to live within your means, and save/invest your money instead of blowing it “because inflation” or some other excuse.

You have a point, but in keeping with the drunk sailor analogy, lets not blame the bar and the barrender for thepatrons getting and staying drunk all the time.

They could save their extra money and avoid the bar. Blame falls squarely on the drunks, who will eventually stumble, drive or uber home, out of money, wasted and facing a nasty hangover the next day

It seems someone here enjoys a little bit of Shadenfreude 😆. Never thought I’d get to use the word and mean it lol. Personally I feel a bit bad for FOMO buyers of anything, most aren’t going to be tracking markets or whatever and majority buy a car because they need to get to work. Though it’s a fair point that if consumers were more educated and had more restraint the balance would be less in favour of dealers and the rest of us would have better deals when we need to replace our cars and stuff.

Seba – putting the ‘mal’ back in ‘malinvestment’?

may we all find a better day.

I don’t feel bad for the fomo crowd, they helped create the problem that is the bear trap that has them by the leg. Idiot bought house next door sight unseen for 850k, at least 100k over market during the Plandemic and about 6 months later got transferred. Can’t convert it to an STR and can’t get a long term renter that will cover the nut and not trash the place so it sits empty for many months. Too bad so sad!

LOL let me enjoy my schadenfreude please..there are so far and few nowadays so when one comes along… The last couple of years it’s tough to see every lemmings act like they are genius, paying over MSRP on crap cars and do most of these people really need a new car? Probably not but the FOMO want is there, without their stupid participation, I am sure we would be in a different place now so it’s always fun for someone with self restraint starting to see the trend starting to turn..

Hopefully housing is nice but not holding my breath on that one, couple of buddies of mine that bought over asking still thumbing their nose at me and pity me for missing out..since they live in desirable part of SoCal, I guess they can still say that now but not so if you look at it from a nation wide perspective. Oh I got most of schadenfreude reserve there if the time comes..

Could we actually be seeing the beginning of true price discovery? At least in the auto market…

On another note, how is it possible that the dollar is strengthening while yields are going down? Makes no sense at all.

Yields (10 year) are up 30+ percent in the last 6 months

Was looking at the last 4 days.

1) Serious delinquency auto loans 90+ days are in a zigzag up to a

min of 6.5%/7%.

2) The trend is up, the left hand side of bubble tops are fake positively

biased. Fake, on the cusp of a major recession.

3) When the layoffs start the ratio : Real DPI divided by mortgage debt,

auto loan debt, c/c loan debt, student loans debt, Hell debt… might rise

to a new all time high.

4) Why layoffs : plenty of reasons.

I don’t know why you don’t start your own blog, this is gold. Hell debt? I need to go talk to my accountant

Howdy Folks. Well this old fool is spending even more currently and planning to increase the spending even more in 2024. Still saved more this year than last year too. Debt Free is Real Freedom for some folks…

To summarize.

The drunken sailors are still going “party on” strong and drinking everything in sight. Even as the price of drinks keeps going up.

And do have an eye on a cute potential new friend if the party keeps going.

And the military police (Shore Patrol) are not even warming up their batons.

I can’t be the only one observing all of this and just wondering when the first domino will fall.

In this hyperfinancialized clownworld it feels like nothing makes sense anymore.

I’ve never felt a greater disconnect between what I see around me and everything from the financial economy that hits the news.

I don’t believe in incompetence or policy-errors anymore.

This is intentional and somewhere behind the curtains there’s a masterplan waiting to be activated.

Especially in the EU where the delusions of grandeur have reached epochal proportions. While the Union is noticably falling apart, they talk about even more centralized power….where o where have I’ve seen that before?

Perhaps it will become more apparent at the start of next decade. That is roughly when Social Security will be in serious jeopardy. From Center on Budget and Policy Priorities-

For example, while 2035 is the trustees’ best estimate of when the combined trust fund reserves will be depleted, they judge there is an 80 percent probability that the reserves will be depleted sometime between 2032 and 2039. The Congressional Budget Office projects that the trust funds’ reserves would be depleted in 2033.

If the cap is removed from Social Security contributions, the crisis is over.

The Social Security tax limit increases to $168,600 in 2024, up from $160,200 in 2023.

Why is there a cap??? Social Security is a shared insurance for all income earners. If you earn more than the cap, all the more reason for you to be contributing. Otherwise who is going to foot the bill for your product or service? I’m paying increasing auto insurance premia for what? I’ve never had an accident. I’m paying for Medicare but have good health. It’s just a shared expense – communal if you insist.

I’ve been saying this for years. Additionally, based on longer longevity, if they raise the full retirement age by 1or 2 months for current 50 year olds, 2 or 3 months for 45 year olds, 3 or 4 months for 40 year olds, etc….or something similar, there would be barely a whiff of complaint, and the two changes would insure SS solvency. Also put a net worth cap on collecting SS of say 10 million and that might help, because they are all probably in the max payout level group and don’t really need it. Doubt that would ever pass (income re-distribution!!!), but I sometimes wonder if most of them even collect it. I wouldn’t if it was a mere decimal point on my income, but some just want it all.

I hear you. The disconnect is “suppressed news “, “filtered news “, and “secret behind the scenes bailouts, market manipulation and effective use of AI to ‘ pull off ‘ the greatest ‘ snow job in American history “. And we’re living it right now. We probably will have the “longest “ recession/ depression we have ever had. A whole new lower standard of living and poorer way of life is the probable outcome. Welcome to the new world order.

Augustus Frost, is that you?

Had my 2016 CRV serviced the other day at the Honda dealer. Checked out the new CRVs. I don’t like the new body styles. Wish Honda would quit fixing things that aren’t broke. Anyhow, salesman had a look of desperation on his face, whining how he was commission based. Tried to tell me I should consider leasing my next vehicle. Lol It was all so funny since I have no intention of buying a new car right now, maybe never. If I did, I’d pay cash.

A wise and healthy attitude.

I’ve always acted in that way, not living beyond my means.

I feel it’s something deeper than just plain old greed and instant gratification though…like consumption is filling the void of a lack of meaning.

The older I get, the more I just come to learn that ‘stuff’ isn’t important.

But when 70% of a country’s GDP consists of ‘buying and selling stuff’ and chasing instant gratification, perhaps I’m right about that.

I think you are confusing what “personal consumption” means with regards to GDP.

The other GDP categories are business investment, government spending, and exports.

Not sure 70% of GDP being consumer spending is bad. Maybe in relation to net exports, but that is beyond my limited research/understanding

“The older I get, the more I just come to learn that ‘stuff’ isn’t important.”

Bingo! I have always felt that way, even when I was young. Yes, I like to have a few nice things, but this country is excessive, and I hate that about us. I am a saver, always have been. I get more pleasure out of saving as it is security for me. I struggled when I was young and never want to be in that position ever again. I am finally in a good spot but feel it is never enough, if you know what I mean.

You may think you own things, but the things own you.

I agree – can’t stand the look of the new CRVs (and HRVs too). And those giant screens they all come with are so distracting.

Its my goal to drive my 2013 for at least another decade (and 100k miles). If it lasts longer, all the better.

They look like every other manufacturer of SUV all thrown together. Honda used to have a distinctive look. 2017 they changed the body style big time and have progressively gotten worse. I love my sporty 2016 SE with the sporty wheels. It is a pretty car, IMHO. I keep it looking good.

aerodynamics and CAFE…

may we all find a better day.

The thread here seems to be a mixture of housing as well as automobile comments. i’ll limit my comment to just automobiles.

The legacy manufacturers don’t realize it yet but they are each on the verge of having a “Kodak” Moment. Kodak as you recall, did not see the revolution coming in imaging; fearful any embrace of the digital world negatively affecting their bread and butter business of film, paper, and chemicals. One can see how that ended.

The same is going to happen to many if not all the legacy auto manufacturers.

They need vehicles that are truly innovative as well as fully developed charging networks. Abandon the dealership notion totally. Just a couple of examples. Actually pretty much do what the Tesla Corporation is doing now.

…when the sweet wine of hubris blots out the necessity of constant, complete and honest SWOT analysis…

may we all find a better day.

“Of those buyers that finance new vehicles, only about 5% are subprime…”

The fact that there are *any* subprime borrowers financing a new vehicle is nuts…

Wolf,

Quick question re your 60+ day delinquency chart. There is a clear seasonal aspect to the subprime delinquencies, but I can’t tell from the chart what is the typical bottom month and what is the top. Could you let us know please? Thanks!

The typical bottoms are in April (effects of tax refunds?), and the typical tops are January/February. So if this year follows seasonality, the peak in Jan/Feb should be higher still.

The interest rate and the expense of vehicles has me, despite my desire to live, considering paying cash for a new motorcycle as my next vehicle purchase.

hollow – if you’re serious, strongly urge, no, BEG you to take a new rider’s course, FIRST (that MiniTrail you may have ridden at your grandparents country property doesn’t count)-it will save you from major $ outlay before actually committing to two wheels. Next, when you’ve decided on a moto, check out tire pricing-their performance is nothing short of magic these days, but that performance costs, and it’s likely you’ll be replacing them every 10k miles +/-. Ditto chains/sprockets (unless you’ve opted for shaft or belt final drive). Find out what periodic service $ will be if not prepared to learn/DIY. Don’t skimp on good riding gear, either, remembering that riding a moto is more akin to piloting an aircraft than driving an auto, and just as unforgiving of pilot error. (That said, though still MY favorite way to travel, the $ savings probably won’t honestly pencil against a good used econobox…). Best.

may we all find a better day.

If you don’t have good peripheral vision, skip it. You will not believe how many times someone from the lane left of you will make an unexpected right turn.

How – one can count on that…

-Best.

may we all find a better day.

91B20 1stCav (AUS)

A bit late with comment but have been traveling for a few days.

Your entire comment is the best advice I’ve seen as to two wheel riding. It’s been over 65 years since I first swung a leg over a seat for a ride. Almost always rode a Harley and still have an 82 FLT with over 250M miles and one drop. Slick road and cold patch asphalt at an intersection is the only mishap.

Own a 97 FLSTS with over 100M miles. Could attach an odorometer photo but Wolf would delete. Both good dependable bikes. Enjoyed riding over much of the country and still ride local having passed Illinois tests at 79.

So Hollow I would listen to the man’s advice. It might save a life.

Costs of operation is at least the same and probably more than a car or cowboy Cadillac.

Softtail – thanks for kind concurrence. Never been a Motor Company afficianado, but to echo our fellow rider VGV (DanRo), ‘tout sommes est belle’. Hope I’m still able (71, now) to saddle up at 79!

Best.

may we all find a better day.