What homebuilder PulteGroup said about mortgage-rate buydowns. Homebuilders have figured out this market, homeowners have not.

By Wolf Richter for WOLF STREET.

To sell new houses in this 8%-mortgage environment, homebuilders – whose stocks have gotten battered since August – have resorted to mortgage-rate buydowns through their own mortgage companies. Earnings calls are now all about those buydowns and their costs, including PulteGroup’s earnings call yesterday which is currently buying down 30-year 8% fixed-rate mortgages permanently to 5.75%.

That incentive works in selling houses; but costs are steep. We’ll get to the earnings call in a moment, but keep that in mind as we walk through the figures on new house sales, prices, and inventories.

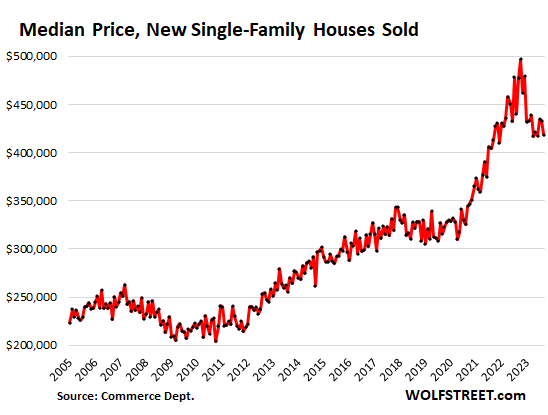

The median price of new single-family houses sold in September fell by 3.3% from the prior month, and was down by 12.3% from a year ago, and down by 15.7% from the peak in October 2022, according to data from the Census Bureau today. As you can see in the chart, following a big drop, it has essentially moved sideways since April.

But these are contract prices and do not include the costs of mortgage-rate buydowns and other incentives such as upgrades of countertops.

In this regard, Pulte said that its “incentive load” – now mostly mortgage rate buydowns – was 6.3% of the average selling price of $549,000 in Q3, or $35,000 per house. These buydowns effectively lower the buyer’s costs, but they’re not included in the data here by the Census Bureau, which tracks contract prices.

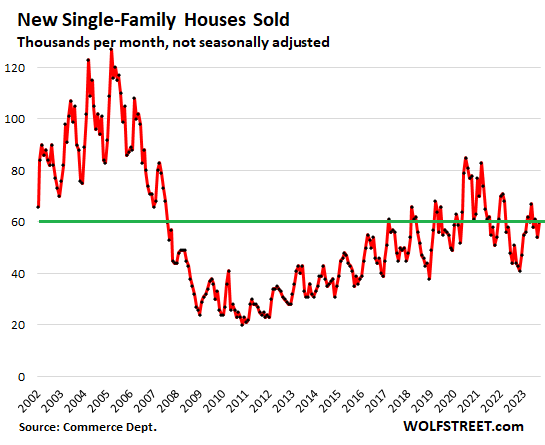

Sales of new houses – not seasonally adjusted, and not the annual rate of sales – rose to 60,000 houses in September, up by 36% from the beaten-down levels a year ago. These sales levels would normally be nothing to write home about, but in the 8% environment, they’re pretty good, testimony to the effectiveness of price cuts, houses built at lower price points, and mortgage-rate buydowns.

Homebuilders, unlike current homeowners, have figured out this market. Their business is to build and sell homes no matter what the market does. But homeowners who want to sell are still muttering, “this too shall pass,” and are not putting their homes on the market, and those that are putting them on the market are now cutting prices at a substantial rate but not nearly enough to bring in buyers, so sales of previously owned homes have plunged.

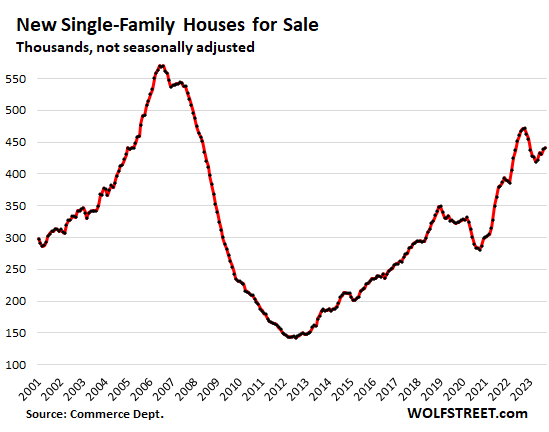

Inventory for sale of new houses in all stages of construction rose to 441,000 houses. And supply, given the increase in sales, dipped to a still fairly high 6.9 months. This would have been the highest supply in the years between 2011 and March 2020, so more than ample inventory and supply, and homebuilders will have to move it, and they’ll be motivated to play with prices and incentives:

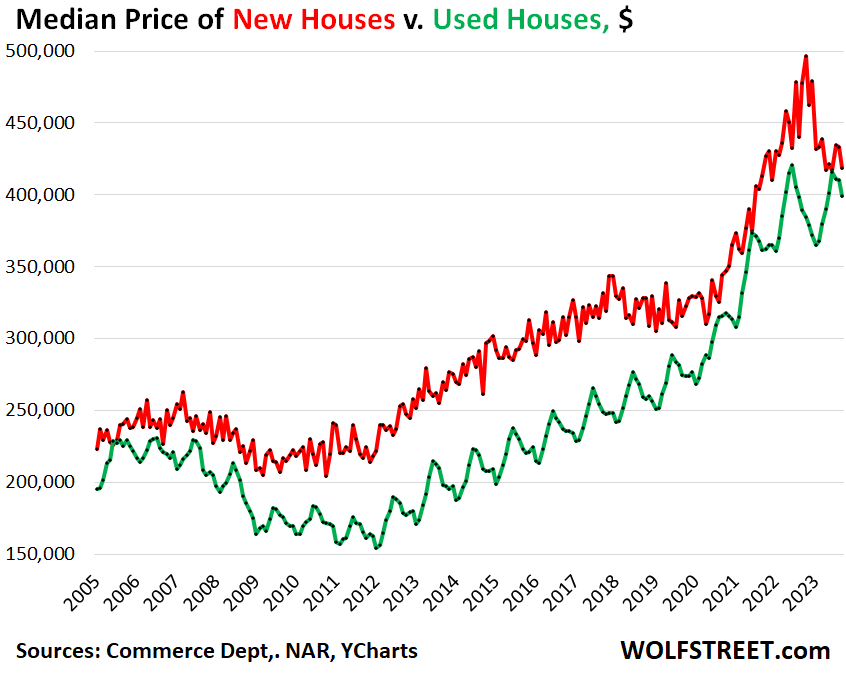

New houses take share from “used” houses. You snooze, you lose. “New” houses compete with “used” (previously owned) houses on price. And they’re now just a spitting distance apart, with prices of new houses down sharply, and prices of “used” houses down just a tad from the peak in June last year:

What PulteGroup said about mortgage-rate buydowns.

The earnings call yesterday was dominated by questions about mortgage-rate buydowns (transcript via Seeking Alpha). Here are some of the salient points:

“We continue to use the permanent 30-year buydown as probably our most powerful incentive. Right now, we’ve got national incentives that offer 5.75% on a 30-year fixed,” when “rates today on the open market would be over 8%,” CEO Ryan Marshall said.

“I’ll remind everybody, what we’ve done is we’ve simply redistributed incentives that we’ve historically offered toward cabinets and countertops and things of that nature, we’ve redirected those to interest rate incentives, and I think that has been the most powerful thing for that buyer group,” Marshall said.

“There are other buyers that decide that they don’t need to go all the way to 5.75%, and they’d like to have a little bit higher rate and use some of the other incentive money that we’re offering for other things that they see value in. We’re seeing about 80% to 85% of our buyers are getting some form of incentive towards interest rates. That doesn’t mean everybody will go to 5.75%. Just some fraction of our total sales [25% CFO Robert O’Shaughnessy specified a minute later] end up in that very lowest category,” Marshall said.

“The big headline is that we’ve got the tools out there, and our sales team has got the tools out there to help individually solve what each and every buyer needs in order to make the transaction work for them,” Marshall said.

About the costs of the buydowns and incentives, Shaughnessy said that their “incentive load” is about 6.3% of the average purchase price of $549,000, “about $35,000” per house, and “the majority of that incentive is rate buydown for financing support.”

Pulte’s shares [PHM] have dropped 17.5% from their all-time high on August 8, to close at $71.01 today.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just checked, even my trusty credit union is only offering 8.15% 30 years fixed mortgage and this is on 750+ score and non-jumbo. This show is getting good and need to buy some more popcorn to enjoy until the next Spring pop in 2024, wonder what rates will be like by then..

Wolf, any prediction where we will be at for mortgage rate by end of this year and majority of next year? If rate continues to be high, wonder how long these new home builders can keep up with more aggressive rates buydown?

I visited new $2.3 Million houses at a renowned builder in Sammamish suburb close to Seattle to learn the really crazy Math of mortgage rate buydown. There was offer of 30 year FRM (fixed) of 5.5% on these houses when the rates are around $7.5% FRM for buyers with good credit. However, when I saw King County assessment of these houses for 2023 property taxes, they came to a meager $1.2 Million. Normally these are accurate assessment with around 90% of market value and so these houses should sell for about 10% more i.e. $1.32 Million.

So, why are these $1.32 Million houses listed at $2.3 million? The EMI for 80% mortgage amount @7.5% FRM is $12,866. With builder buydown to 5.5% FRM, EMI is $10,447. The $2,419 difference in EMI is proudly stated by builder as $870,841 discount by builder. So on paper this looks like a good deal because now the $2.3 million house seems discounted to $1.43 million. Throw in a couple of upgrades and some closing cost and it looks like we have a good deal.

Why does the builder buydown rates instead of marking the house lower?

1. Marking one house low will decrease sales price of all unsold inventory.

2. This 80% higher inventory markup based on crazy pandemic prices is what is causing builder balance sheets to remain balanced. If the lenders find out true worth of this unsold inventory, they will ask for money back bankrupting the builder.

3. While the builder can claim $870,841 discount, in reality he foots only $346,000 to reduce 7.5% EMI by $2,419 and pockets a wopping $524,841 in cash from house sale.

4. Most cash buyers at $2.5 million ranger aren’t idiots, and have already been home owners. So builder knows that he is not losing customers, as cash buyers were never the target customers.

Can it really be bad for buyer given that builder is helping buyer with mortgage rate buydown?

1. The buyer committed to very high house price of $2.3 million, relevant debt and a specific lender with very harsh terms (may even be no-recourse) and these cannot be easily negotiated in future, even if mortgage rates fall.

2. The overvalued house will have overvalued property taxes for some time.

3. The house can only sell for market value at a future date. So while buyer buys it at $2.3 million, chances are high, that after 2 years, it will sell closer to its real market value of $1.3 million. The mortgage lender may ever refuse this short sale forcing buyer to hold.

So its important do the Math before going blindly for a mortgage rate buydown.

Clueless Idiotic Bullshit. Idiotic fiction. Pulte’s average selling price in Q3 was about the same year-over-year, they did not inflate prices for those buydowns. Other homebuilders are in the same ballpark with average prices flat or down.

Leo, how stupid do you think we are?

My comment is not about Pulte. It’s also not about an Area where median price is $500,000. It’s about an Area where median price is above $1.5 million.

Just checking zillow and King County property tax website. The data is public.

Leo,

What’s BS are your fantasy allegations. It’s one thing to look up a price, it’s another to make up all kinds of allegations about the builder’s balance sheet, buydowns, and reasonings, and how prices work.

That said, I should have specified the offending portion. It was a little harsh to put that comment out there in generic form.

I don’t think he was claiming that Pulte inflated its prices to do the buydowns. I think what he’s saying is that they’ve maintained the 2019-2023 run up in nominal price, by reducing the effective price by way of mortgage rate buydown.

I read his comment as saying that Pulte could have just reduced their selling prices to the 2018-2019 price (or the $1.3 million number he quoted) and had people get traditional mortgages.

Wolf,

I agree with Einhal…I think that it is worth taking a breath and slowly stepping through all the potential implications and consequences of the buydown “innovation”.

If nothing else, you yourself indicate that buydowns are resulting in misleading info being fed into the widely publicized Census survey data.

This has more than a whiff of earlier “innovations” that gamed/distorted/deranged various Government tracking/regulatory measures that kept foolish booms lasting longer and making their collapse more profound.

At first glance, buydowns seem to be an almost model example of “financing-led” price inflation (or “financing-perpetuated” price inflation).

Those sort of things have had bad outcomes in the past (frequently in unpredictable ways).

Cas127,

You people get the basics confused.

The selling price is for the BUYER to decide. Builders build homes and will do what they can to sell them, to maximize their profits, always have, always will.

Buyers don’t have to go for it. They can just stay away, and then builders have to use more radical price cuts, etc., to find buyers willing and able to pay those prices. Prices are set by buyers who are willing and able to buy, and decide to buy at that price. Prices are NOT set by builders.

It’s just silly to blame builders for high prices. The onus is on the buyers. If they don’t buy, those high prices are just items on a builder’s wish list, not reality.

Einhal,

You’re presupposing the market value of the homes is actually $1.3M as suggested by Leo. That seems odd to me for a couple of reasons:

1. Someone in the market for a home with a price of $2.3M, whether they’ve owned before or not, should be able to figure out the “discount” of $870K is just the reduction in the monthly payment times 360. Therefore, they know immediately it’s not really an $870K present value discount from the builder.

2. It seems odd that a newly constructed home in 2023 would be assessed for tax purposes in 2023 based on its market value AFTER construction. In other words, does the $1.2M taxable value figure represent the lot value, or was the home completed before the 2023 tax year and it has been been sitting empty all this time? If the home was built in 2023, its 2023 tax assessment should reflect its pre-construction value. At least in California, there is always a lag in increasing the assessed value of new homes between the tax on the empty lot and the ultimate assessed value based on the sales price of the new home. I admit I do not know how Washington reassesses properties after a home has been built.

I just have a hard time believing that the “market value” of a home is $1.32M but the builder is able to sell them for $2.3M because of a 2% mortgage rate buy down. That doesn’t make any sense unless buyers in Washington are exceptionally dumb. I’m guessing the problem is in the actual numbers though.

I was curious and looked up how Washington taxes real property at the Washington Department of Revenue website. Real property taxes are paid in arrears using a January 1 valuation date with taxes paid the following April and October. Therefore, the 2023 taxes are based on the value of the property as of January 1. In this case, was the new home constructed by January 1, 2023? If it wasn’t, the 2023 tax bill isn’t going to reflect subsequent improvements to the property.

Wolf,

“Buyers don’t have to go for it”

Of course.

(And I don’t know that I “blame” builders for high prices anymore than anybody else…they are simply trying to maximize their return. But…)

The crux here seems to be the increasing techniques (financial and otherwise) to avoid simply competing on straight price.

Of course builders are free to structure their offered transactions however they want…but the wise consumer is well instructed to be very (very) wary of increasingly convoluted (and/or stretch) proposed deal structures they may not fully understand/appreciate. (See mortgage resets circa Implosion 1.0…)

If builders pitch some “innovative” financing structure to walk away with more money and some buyers climb on board to get homes they really can’t afford (and shortly blow themselves up) they are not absolutely the only parties affected.

The preceding dynamic (pre Implosion 1.0) drove the apparent market price way-the-hell up…for *everybody*, not just the parties most immediately involved.

Smart buyers looked at the inflated prices, convoluted terms to “offset” the inflated prices, and said hell no.

But the “creative financing structures” kept inflating the “market price” until there was a shattering collapse of the whole rotted-through structure.

And then taxpayers and dollar savers (see ZIRP) had to pay the price for *others’* housing delusions. And the wary had been priced out of homeownership for years. And the unwary had been gutted.

To some extent, this ugly process is self-correcting…incrementally more buyers learn to be wary (there were fewer buyers during Doomed Boom 2.0 than 1.0).

But it is a bit nauseating to see the whole sick show repeat itself over and over, so shortly after the prior collapses.

There are definitely externalities involved in builders’/buyers’ increasing focus/obsession on convoluted financing techniques rather than straight price.

It wouldn’t be quite so bad if more builders focused on cost-effective production/sales price.

But out of the Top 100 builders perhaps 5% do so…the other 95% have long since become *very* comfortable using financial “creativity” to create an inherently unstable housing/macroeconomic environment.

“The selling price is for the BUYER to decide.”

Yes, at the end of the day the buyer can make the purchase or walk. But their decision is based on what they’re trying to buy. Are they shopping for a price like a cash buyer would do, or are they shopping for a monthly payment? Wolf, you’re overestimating the financial brains of the average American here… People make terrible purchasing decisions all the time based on what monthly payments they can fit into. The average person barely understands how interest works… They buy cars and houses based on the monthly payments. You were in the car business, so you know that pushing a monthly payment is a car dealership’s key sales tactic. They always ask what kind of monthly payment a buyer can swing to “match” the buyer with a car. Can’t afford it at 48 months? No problem, here’s your payment at 60 months. Awww, you can’t afford that? Well don’t worry, I’m sure you can make this even smaller payment work at 72 months!

If a buyer is shopping for a monthly payment, then a rate buy-down makes excellent sense for the builder. The buyer will go brag about the great deal they got on the financing and the builder doesn’t have to poison the comp price of the whole development to make a sale. Plus the government gets a bigger tax assessment. Financing can grotesquely skew market values. It’s the American way!

Buyers shouldn’t be shopping AT ALL. To get prices down, buyers should go on strike. As long as these buyers are out there buying this overpriced stuff, builders should just rip them off to teach them a lesson.

Leo -I do appreciate your detailed post.

Now I do understand all this buydown interest rate from builder.

PS.I do live in Seattle area-the home of the four economic gorillas ( Microsoft, Amazon, Meta and Boeing).

As long as east side household income is almost $200 K/year-home prices will stay elevated.

The taxes probably just haven’t been reassessed yet. You’re overthinking this.

I second this question, which you didn’t answer — where will mortgage rates be this year and next?

Inventory data shows lowest new listings in the history of the United States. Wow

1. the data goes back only to 2016. So not “history of the United States.” But since 2016

2. Low, but not “lowest”

3. But lowest DEMAND since the bottom of the housing bust in 2010

Howdy Folks. If you are purchasing a 1/2 million dollar new house, you should have a good amount as a downpayment. If not, you should not purchase such a home.

What’s consider a good down payment? Do you think $300K or $400K is a good down payment or still not good enough? That’s the sad twisted reality of this F up market, especially in South and NorCal. $300K down on an average price home in a decent neighborhood, nothing to write home about, you’re still staring at a $6k to $8k if not more monthly expense all said and done…somehow this market should make sense if you listen to NAR or your friendly RE agents…

and this is assuming most even have that much of a down payment to begin with…

Howdy Phoenix Depends on the amount of debt one already has.

I put down 100k when buying house… instant 30% equity,

Not sure why folks need to live in the most expensive part of the country… with that 300k you could buy outright an entire house and 1/4 acre of land in northern New England suburbia.

buying my* house

In 2003 in FL, I put down $100K on a $275K house. The house went to a high of $550K in less than 2 years and after the 2008 crash, when I lost it, it eventually sold for $180K in foreclosure.

You guys are delusional about how low or high a market can go. Your 100% equity can disappear for a variety of reasons. Right now, I have never seen markets which are so clearly manipulated. The value is just not there, it is all speculation.

No delusions here. If I woke up tomorrow and found my home worth $0 I wouldn’t care.

MM,

300k doesn’t buy a very decent home in northern New England suburbia. It would be a fixer upper in most places.

Lucca – fair point, in that I didn’t consider that others may need more space than myself.

If you’re willing to look in the sub-1000 sqft category, and don’t need to live a stone’s throw from the Mass border, you can definitely find something under $300k.

That said, I agree prices in this are are still far too high, and will correct down in the coming years.

That kind of thinking is exactly why I don’t have my own house, while all my friends who put 5-10k down payments all have homes. So now I have a large down payment but homes are also 2x as expensive.. oh actually more so because of mortgage rates

So yeah, wish I would have just gave the bank 10k instead

Yeah, well, our policy makers have created very poor incentives over the past 15-20 years, and we’re all paying for it now. Hopefully it’s a path never to be trodden again.

Completely the same.

My wife and I were trying to be dilligent and responsible by not levering up on debt, with a low down payment.

Now it just feels like I’m locked out. I keep waiting for some form of real adjustment in the market, and yes I know it takes years. I’ve already been watching this market like a hawk for about 3 years and it’s just insane, still. After the covid run up it just doesn’t seem like these prices will ever fully readjust. Seems like too much extra liquidity still out there,even despite the colossal increase in rates.

I ran some numbers last night, and despite these rate buy downs payments on a house around 400k with a low down payment are still astoundingly higher than 3-5 years ago. Even after rate buy down you’re paying a much higher monthly mortgage/taxes(TX) on a massively increased total price.

Very frustrating. We should have just been irresponsible. Fed policy benefited the financially insane, less prudent among us, is what it seems like.

Don’t feel bad, there are also people like myself, and I could be the rare or not rare breed but can easily afford $300-$500K down but compelled not to buy because the math just simply does not make sense versus what you get for rent. I guess I am going on a buyer strike something that’s not popular among people my age or the consensus…

As my friends like to remind me over and over I am missing out on a gold mine that will only go up and I like to remind them how much is their house paying them per month? Because at the current rate, it covers my rent and then some :) Not to mention, I am not sitting there pretending my $1M+ 1300sq ft house is a good value.

@Phoenix

We could currently afford a relatively substantial down payment, and if I pulled from our IRA I could double that pretty easily, still wouldn’t be near 300k, but this has multiple drawbacks. I’m more comfortable with that $ in 5% MMFund and short term CDs.

I also don’t see the point of buying now with everything going the way it is. Part of why I read Wolf so diligently, to see which way the wind is truly blowing. Seems to be the only place to get real data. I am still hopeful it will come down, yet frustrated waiting, and I generally lean towards pessimism so it is hard for me to just hope it’s going to come down.

I have most of the cash that’s outside IRA making decent interest finally, and we are saving the cost difference between renting our current 3 bedroom house and buying the same. Comes to almost 1k a month. I will keep doing this for another 2 years if needed. But I must admit to being tired of burning money on rent, rather than building equity. If I calculate how much we have spent on rent the last 15ish years, it hurts my soul.

Thank you for the perspective, I do appreciate that there are others who think similarly to myself.

to quote CAV:

May we all find a better day!

@Biorganic,

“I have most of the cash that’s outside IRA making decent interest finally”

After reading your post, I just wanted to make sure you are aware that the money that is in your IRA can be used to buy treasury bills.

@HarveyM

Yes, I do realize that. The IRA funds are mostly in 3 and 6 month CDs, very similar return to treasuries, with FDIC insurance, if that even matters.

Thank you!

Hang in there man, I think the writing is on the wall. I found some incredible people in the last 2 years that share data on X and YouTube, many of which also survived the GFC like me. I sold my house 18 months ago at the first top and leased it back. I’ve put that money into a money market fund and the interest pays my rent. There are so many macro factors brewing that IMO have us closed to a global recession with every week. The M2 is being sucked out rapidly and asset inflation is starting to turn in stocks and housing. We are literally seeing the same headlines we saw in 2007, it’s just unreal. Like a bad dream, but this time I’m on the right side and so are you. GDP numbers today are almost exactly what they were Q3 2007. The housing price appreciation we just saw is not real or sustainable. Its not. Now, we go down, but as you noted it’s a slow process. Watch inventory starting to build, shipping and trucking starting to collapse, CRE folding in office, retail and multifamily, Germany already in recession,years breaking out, stocks starting to turn and unemployment is the last to fall, then it all comes down. It won’t be pretty or fun, but you’ll be able to buy your friends house from the bank.

Bubbles don’t last. There will being good buying opportunities in the future. Likely within the next two years.

The debt-to-income ratios are very high right now. The housing market will continue to struggle if they don’t come down.

You can probably still buy a house, that is one with rental income— duplex or granny suite. That way someone else helps make your payment. Since your home is a partial rental, you can tax deduct improvements made on the property. A decade from now, take out a heloc for a down payment on your next (nicer) home…..keep going from there and soon you’re the senior owning all the property that everyone complains of online. ….. but if you don’t have good credit, well … nobody can help you

This is precisely my situation. I’m super pissed that playing it responsibily hasn’t done me any good.

In the same boat. We paid off the student loans first to get rid of outstanding debt and then the housing/inflation went to the moon before we could save up enough to get that 20%. We have the old 20% saved up now and it’s nowhere near enough for a home these days.

Indeed good advice.

Much along the lines of “have you tried not being poor?”

>> PulteGroup’s earnings call yesterday which is currently buying down 30-year 8% fixed-rate mortgages permanently to 5.75%.

>> In this regard, Pulte said that its “incentive load” – now mostly mortgage rate buydowns – was 6.3% of the average selling price of $549,000 in Q3, or $35,000 per house.

Is this correct math by Pulte? A 2.25% reduction in mortgage rate for ***30 years*** seems like it would correspond to more than a 6.3% effective price discount. Any mortgage wizards care to weigh in?

That’s not how it’s figured. This is much more complex. Pulte discussed a few aspects of it, including the forward contracts it uses, etc., in the conference call. I linked that transcript of the conference call so you can read it.

Also, few 30-year mortgages live 30 years. The average 30-year mortgages lives about 7 years before it’s paid off, either when the house is sold or when the mortgage is refi’ed. If mortgage rates drop to 5% or below, those bought-down to 5.75% mortgages will be refi’ed. That’s what makes the buydown calculation very complex. It’s not just simple mortgage math.

The “forward contracts” sound a lot like the infamous “interest rate swaps” that Wall St banks have been doing.

I think it means that someone on Wall St is betting hard that mortage rates will be down by a lot within X years. The big question is, what is the balance-weighted average X, and what will blow up if the bet goes bad? And will Fed then rescue the swap-sellers (again?), thereby shooting the nation in the foot WRT. the fight against inflation?

My understanding is that these are short-term contracts, from the moment they advertise their buy-down rate until they end the deal and close all sales with these buydowns. This locks in their costs — that’s how I understand it.

Wolf a few comments on Pulte,

Their margins remain at 29%+

They have net zero debt

They use options to purchase lots.

I will buy their stock if it approaches 1x book.

Stop this BS already.

1. “Their margins remain at 29%+” That’s a lie. Their margin FELL 100 basis points, to 29.5% from 30.5% a year ago

2. “They have net zero debt” That’s either a lie or nonsense, depending on how you figure it. They have $2 billion in bonds outstanding; they owe customers $770 million (deposits); and they have $425 million in financial services debt. That’s $3.2 billion in debt. In addition, they owe their suppliers $570 million (trade debt).

They have $1.8 billion in cash, $570 million of which they need to pay their suppliers, leaves them $1.27 billion to cover $3.2 billion in debt.

3. “They use options to purchase lots.” So what? They use forward contracts to buy down the mortgages. So what. They’re sophisticated players.

4. “I will buy their stock if it approaches 1x book.” Yes, by all means. Someone needs to buy the stock.

But do look this stuff up before posting:

https://www.sec.gov/Archives/edgar/data/822416/000082241623000042/phm-20230930.htm

THE PULTE PRESS RELEASE YOU QUOTE CLEARLY STATES THAT THEIR GROSS MARGIN FOR THE QTR WAS 29.5%.

HOW IS THAT BS, WOLF?

Like I posted below, is their GM calculated before or after the 6.3% is deducted. If it’s after like I would think it is, then that means they’re even more profitable than we would otherwise know.

It FELL 100 basis points to 29.5% from 30.5% a year ago. Read my comment, and then read the 10-Q they filed with the SEC. I gave you the link.

You said “remain at 29%” It’s the “remain” that’s wrong. Their margin fell.

That’s gross margin….lol…. I don’t even think the op understand the difference

More importantly stock price is how much off the highs?

Falsus in uno, falsus in omnibus. Learn the difference between gross margins versus net margins.

3. “They use options to purchase lots.” So what? They use forward contracts to buy down the mortgages. So what. They’re sophisticated players

That means, since they are such “sophisticated players” they are “hedged” with some fancy interest rate swap.

Like the british pension funds.

It’s only short term because when the house is sold and the mortgage is signed and the is deal closed, they eventually sell the mortgage to government agencies (such as Ginnie Mae) or the GSEs such as Fannie Mae and Freddie Mac, or they pool them into private label MBS and sell them to investors, and wash their hands off it. All they then have to deal with is the upfront cost of the buydown.

Pension funds make long-term bets, and those long-term bets unraveled for the UK pension funds.

Responding to Wolf & my reply below, Tim is the one who said “remains” not me.

Be that as it may, all, I think, he’s trying to say is that their GM “remains” at high level. There’s not BS in that. And, who really cares that their GM dropped a measly 1% / 100 BP? That’s like nothing!

Again, the most important question here is 29.5% after the 6.3% is subtracted off?

If this is the case, then they have a GM that “REMAINS” quite high after removing the buydown. Two years ago, when there were ZERO buydowns, I know that one of the big builders like Pulte stated their GM was at least 41%, possibly has high as 43%, if my memory serves me correctly.

In either case, these are breath-taking gross margins, given the rate environment and the fact that new home prices have dropped 15%.

My takeaway is that housing remains completely out of whack. Now granted, we may have 2-3 or more years to go before housing finds its bottom. It’s obvious that the Fed wants this to take AS LONG as possible, which means we will be dealing with higher for longer inflation and rates.

GDP just came in @ 4.9% which is HOT, yet the Fed is content with letting rates remain in a pause. The FFR should be at 6%, given all the data we have available to us.

This has been exactly my gut feeling about the big builders in my area. I see these 1900sqft townhomes going up on tiny lots in huge developments, being built with questionable quality. (But hey, they have “hardwood” floors and quartz counters.) They are so keen on preserving their margins that they’d rather eat the carrying costs of taking 10 years to build out these massive developments than to build and sell at a consistent rate.

I’m sure it’s great for their margins and stock price. But it indicates to me a lack of competition in the marketplace. As with seemingly every other industry in our economy these days, most regional markets are down to 2-3 major players who don’t end up competing all that much with each other.

A truly competitive market will push profits towards zero. Refusing to sell a townhouse that costs 350k to build for anything less than 550k, even in increasingly horrific market conditions, reeks of anti-competitiveness to me.

Just my gut.

Home owners are emotionally attached to their homes. Home builders act and work on pure $$ numbers.

Home owners, un sophisticated investors would be caught holding the bag like always.

Home owners generally use their homes for things other than investing.

For example, having a place to live.

Sorry for confusion.

When I say home owners I meant small investors or people with multiple homes.

I have friends owning 4 or more homes and they think home prices can only go up over the time.

They are not using these 4 homes to live as they can only live in 1 home at a time.

For them these homes are investments.

What does it say about consumer mentality when a builder can be successful at inflating prices and offering sizeable incentives at the same time?

Do people actually get excited about getting “money back” towards appliances and fancy countertops? Don’t they realize they’re paying for these items three times over through the course of the loan?

And the local property tax entities benefit – forever- by higher sales price.

Yep…and ain’t that an interesting dynamic.

Especially since the local G is also determining the entitlement/zoning rules that have a deeply profound impact upon the supply (and therefore price) of housing.

It’s a small club…and very, very (very) few are in it.

I think it says they’re just not thinking. The median home price high in the GR was Q1 2007 @ $257,400. The low was Q1 2009 @ 208,400. That’s only a 20% drop.

New homes which are only part of the overall median home price have already dropped 15%, and we’re nowhere near the end of all this. The GR took 2 years for the median home price to bottom and that was during a recession. At this point, there’s NO recession on the horizon, so IMHO this has the potential to play out much longer than 2 years from top to bottom. We’re already at about 14 months or so of declines.

Yet, new home prices have dropped 15% and builders like Pulte still have a near 30% margin, and it makes sense that this is after the 6.3% buydown that Wolf speaks of. I’d love for someone to definitively answer that very important question.

Housing is absolutely messed up, and the Fed created this mess along with the help of Congress with egregious deficits over the last 5 years.

It’s stunningly laughable that the Fed is going to take a pass on raising interest rates by .25% when GDP for the most recent quarter was 4.9%. Economist need to start calling them out for this quagmire they’ve created.

TomS,

That gross margin is after the incentives. The financial statements inform that Pulte reclassified the incentives from an expense to a deduction of home sale revenues:

“Effective with our first quarter 2023 reporting, we reclassified our closing cost incentives provided to customers, including seller-paid financing costs, from home sale cost of revenues to home sale revenues. All prior period amounts have been reclassified to conform to the current presentation. As a result, all sales incentives

provided to customers are classified as a reduction of home sale revenues. This reclassification had the effect of reducing both home sale revenues and home sale cost of revenues by the amount of such closing cost incentives, which totaled $48.8 million and $133.3 million for the three and nine months ended September 30,

2022, respectively.”

Howdy Folks. Was wondering if you can still get a no money down home loan?

Only if you’re a veteran that I know of…

If you think that is foolish, just wait to see what happens to Malibu or other, coastal real estate in about a decade during a full moon and a high tide. LOL Read new prediction that, for whatever reasons people may debate, the West Antartic Ice sheet will melt, inevitably. Do not believe my and many others’ warnings: buy coastal property like many “invested” in CCP, Ponzi companies despite warnings. LOL

So as every RE agent will tell you, good to buy in Malibu now since this dire situation hasn’t happened yet or good time to buy then since you will get a free pool in your backyard? Well if you like salt water pool…

RH-

“Read new prediction that, for whatever reasons people may debate, the West Antartic Ice sheet will melt…”

I read of a respected politician in this nation’s lower house predicting that Guam could ”capsize” due to the weight of US military base there. I guess anything is possible?!

respected politician. Is that an oxymoron?

Aren’t most Malibu houses a good number of feet above sea level? Miami is different.

You can get a separate down-payment assistance loan. This would be a loan on top of the mortgage, secured by the property.

Good lord. I’m not financially educated to know what a lot of this stuff means but I know getting a loan to get a loan is insane if you’re just a working class home buyer.

Howdy Trucker Guy. Heres some real insanity for you. They use to have no income verification loans too. Also, a person could purchase a home, no money down, sign your name, and walk out with a check made out to the purchaser.

Yes. Credit unions offer them, such as Navy Federal and NASA Federal. Different criteria on these products, but they typically require enough funds to cover some of the closing costs plus payment reserves.

I’m not here to shill for myself, but as a credit union loan officer I have helped numerous homebuyers get into a home using 100% financing. It can be a great product for the right buyer.

In the long run two trends are certain. With the U.S. living on more and more borrowed money interest rates will continue to go up.

Declining fossil fuels will lead to a reversal in the agricultural revolution with more and more labor needed to cultivate land and provide the fertilizer we now get from converting natural gas ( Haber-Bosch Process). So the percentage of the workforce that needs to be involved in growing food will increase over time.

So many of those involved in the real estate industrial complex will need to start preparing for their new careers as field-hands.

I remember toward the end of housing bust one, there were a lot of games/shenanigans played just to pull folks off the fence and get the people to sign on the dotted line. I imagine the “buy down” is ‘permanent’ between only those two parties, buyer and seller. I doubt its transferable. So if the buyer gets in trouble or needs to sell, I doubt they’re gonna be able to pass on the subsidy. They’re gonna have to off load at prevailing rates. Whatever they might be. I wonder how much of this ‘subsidy’ stuff also serves to freeze up more and more of the market. Folks just wont hop from one house to the next unless the *next* buydown make sense for them. But if it is to be higher for longer, I think there is a limit to this game. November should be interesting.

You’ve raised a good point. That mortgage buy-down can without doubt not be assumable by the next owner. That’s got to affect the selling price.

When the next owner buys it, it will be a used house and no longer new, ergo no one to provide the rate buy-down.

The new owner will just have to find a buyer the old fashioned way (reducing the price to where buyers are).

I’d be interested if Pulte were to offer an 8 percent negative interest rate for the term of the loan.

No problem. The house would simply cost about $2 mil.

I was in a bad mood when I posted that comment. Unfortunately, I couldn’t delete it. What really annoys me is that fact that these rate buy downs by builders aren’t reflected in the MLS and, hence, the comps, which leaves the comps artificially high. Markets can’t work efficiently when data are missing.

Not only that, but taxes and insurance are based on the higher selling price as well.

“buydowns – was 6.3% of the average selling price of $549,000 in Q3, or $35,000 per house.”

Also from Pulte’s press release today, and I’m very surprised Wolf doesn’t mention this:

Home Sale Gross Margin of 29.5%

So does Gross Margin include the 6.3% buydown, or is GM after the fact?

Either way, they’ve still got a lot of room to remain profitable. But don’t worry, if the NAR gets their way, we’ll just worry about rates & not prices. It’s is good to see prices coming down. DM me when the median sales price returns to something below $300K and then we can have a conversation about housing affordability.

Gross margin is, by definition, before other expenses that take away from the overall profit.

So they usually discount cabinets and granite but they have stopped doing that.

So the guy on is saying he redistributed the discounts they used to use to incentivize buyers and now are pointing at Powell and his 8% interest rates, to say “not our fault!”.

How would that redistribution work anyhow? Are they doing illegal things in the mortgage paperwork to claw back what they used to give as discounts.

He just makes it seem like they aren’t losing any money. Like “nudge nudge, these suckers do not even know.”

That is what I got from the quote.

Selling a $419k used home and buyer asked for $21k closing costs. We said yes but raised the house price to cover and they accepted. Probably a lot of that going on.

That’s stupid. They’ll be paying for those price increases both in interest expense and property taxes, indefinitely. But they may have more interest rate deductibility on their taxes. I doubt it makes up for the additional costs.

Last time the realtors wanted to add costs to my house sale price they also wanted commission on that so I told em just commission on the original price before the add-ons. They were pissed off, but took the deal.

make them work for their lazy profits. just like bank fees, mutual fund fees etc. etc. human parasites. They want their cut of the moving money with a ridiculously miniscule amount of work.

Pulte the giant coach roach is hitting the cryogenic freeze of 08 again… along with the usual band of parasites Lennar, Clayton, etc. welcome home america we corporatized and financialized a roof over ones head to the point of no return. Casinos within casinos, where the slaves ‘grease’ all the wheels so the sticks get thrown up in a half hazard manner and ‘they’ still can’t get the adderol and Diet Coke addicted farm animals to buy

I am assuming that the worst time for homebuilders is still coming. That should be when prices on previously owned homes have fallen for a couple years straight and inventories of homes is much higher, so more competition for new homes.

Wolf:

From the charts, it looks like during the period — Mid 2017 to Mid 2018 (when Powell tried to increase the FFR, we had Trump temper tantrum, the rate was held steady (?) for another 6 months) — prices etc. sort of flattened giving us a warning what would happen if the interest rates were to rise. We had the pandemic to postpone things a little bit and lead to pouring more gas on the fire. As folks kept saying, Kicking the can further worked for a while and seems to have caught up with us. What if the rates were to go much higher like in the 1980’s? It looks like it is possible given many things happening — Green revolution to avoid further global climate damage, on shoring and everyone needs subsidies to produce things at home. Would be interesting to watch.

Homebuilders can deal with higher rates by building at lower price points, and they can sacrifice a little margin, and they might lose money and some might not make it, but others will.

Homeowners who want to sell cannot deal with higher rates, because at the prices they want, there won’t be any buyers. So they have to bring prices in line with rates, or they don’t sell. That’s kind of where we are now; and if rates go higher, it gets even worse. At some point, enough homeowners HAVE to sell (moved to a different city, lost job, moved into a nursing home or died, etc.). And that’s when prices have to come down to where the buyers are. People will cuss themselves for not having put the home on the market in 2022 and 2023.

It’s funny about these existing hold out sellers, I have read on certain forums these frustrated sellers are taunting buyers about being p$$$$ on the high interest rate, especially since in their view the house will continue to go up on value so why be afraid of the high rates? They also like mention about interest rates in the 80s and we are only about half way there so no biggie…

So no layoffs and no increase in unemployment in the near future and no recession. At a broad level would that be a correct assessment? Thanks.

That’s only in deflationary scenario. We live in the world where money are printed at a higher and higher rate. No way any material asset would go down in price.

LOL, commercial real estate prices have collapsed in the office, retail, and lodging sectors, for example. Collapsed by 60%, 70%!! Investors that believed your BS got completely wiped out. Lenders that believed your BS are taking huge losses. This BS about real assets not being able to decline in price is just idiotic. I have no idea why that’s still being regurgitated. Well, actually I know why. So that’s for the US and USD-denominated real assets.

But in Russia, whose ruble has collapsed by about 70% against the USD in 10 years, or in Argentina, whose peso collapsed against the USD even faster, your statement may be true. That’s what happens when countries destroy their currencies.

Over the long term I agree with Sergy. Government debt is inflationary because it devalues the currency. Even as the currency is devalued, the true value of the asset remains the same. A house is a shelter. Farm land produces grains or livestock, etc

My house I live in for the past 22 years has increased 100% in price but it looks the same as it did when I bought it. The only change is I added granite counter tops in the kitchen. It provides the same value to me at $186k and as it does now at $410k. It just costs a lot more in devalued dollars to buy the same assets intrinsic value.

Of course there will be peaks and valleys along the way as things are become overvalued or undervalued depending when we get hit with easy money bubbles and liquidity recessions. Asset price can drop an lot during during a recession. Just look at oil. I think it actually dropped briefly to zero during covid but now it is much higher.

Now if you live in a country that has a declining population, then assets like real estate and land could go down in price as you have fewer people buying the fewer things (Japan). Supply is greater than demand.

I wouldn’t be surprised if you are Russian or Eastern European.

Your opinion is widespread in these latitudes.

However, it is surprising how people’s memories are so short.

You forgot the period from 2008 to 2016 very quickly

Wolf-

”Homebuilders can deal with higher rates by building at lower price points, and they can sacrifice a little margin, and they might lose money and some might not make it, but others will.”

One other lever the SFH builders have at their disposal to protect their margins in a challenging market is to reduce their building cost: by using lower quality materials, building methods and subcontractors.

At least that is my experience on my 2018 built tract home…

Yes. And building costs can go down naturally when demand for new houses slows and material costs go down, lead times go down, and labor is more readily available. We’re already seeing some of that, off the cost spike in 2021.

I wonder if there is any comprehensive research on how much it costs to build a house by region and, maybe even more important, how big this fraction of “real” costs is in the total selling price of the house and how it changes over time?

The reason why I’m curious is that I got a new build deliberately with lots of default/basic options, hoping that as long as I am handy enough I can add stuff over time for much less than the builder wanted for those additions. The reality hit me on my head REAL hard – a part of it, of course, was timing (I moved in in Jan 2022, right before the market reached its peak), but nonetheless I never realized how expensive certain things are even if you are paying just for materials and do most of the stuff yourself. Heck even replacing electric switches with “smart” ZWave ones in the whole house can easily cost $1k+ just in materials alone.

Pulte and likes of it, of course, use the cheapest stuff available at wholesale prices, as well as the cheapest labor they can find, but I still wonder how big their actual margin is and how it changed over the last 5 years…

Wolf

“ People will cuss themselves for not having put the home on the market in 2022 and 2023.”

Are you selling your home in SF?

I’m talking about people who wanted to sell, such as people that moved, but wanted to sell all the way at the tippy top, and then didn’t want to sell because suddenly it was getting tough to sell with 5% mortgages. That’s when buyers began to vanish, at 5%. Now volume has collapsed, buyers are gone, and these sellers have the carrying costs to deal with.

Obviously, if someone is happy in their home, and doesn’t want to move, they should just stay there and not sell. That’s the vast majority of the homeowners in the US. Potential sellers are just a small fraction of total homeowners — that’s always the case. But that’s who we’re talking about.

Wolf – have always admired your great patience in reminding us to occasionally flip our telescopes…

may we all find a better day.

I wonder what happens if and when the real mortgage rate falls below the rate set. It would make sense as rates go lower then the builder pays less and if they drop below the rate they set then they are off the hook. Seems like they have to pay extra for a fraction of 30 years depending of course on interest rates.

That’s what most of the housing market is still riding on, a reduction in rates. It’s a terrible bet with federal deficits running 5.7% of GDP and increasing, but it’s the only think that saves most of these guys. Federal deficit is straight credit inflation. They continue to extend and pretend.

“It would make sense as rates go lower ”

What makes you think rates are going lower?

I disagree with this premise – they will remain higher for longer, imo.

A 30 year mortgage is a long time and so I agree rates are longer but seems hard to make predictions anymore than a few years out.

Developers in China did the same thing. Worked like a Charm, just ask Evergrande and Country Garden. And basically all the Rest. “But we are different!’. Yeah, right.

By now it makes Sense financially to wait for the fire sales to start when the first builder goes down. On the other hand, when all the inventory gets re-priced at once (markets are cruel) buying a House might not be your first priority. Buying some gold or silver might be. But that will be un-obtainium then.

But you can’t live inside your gold bars. They won’t protect you from the rain or wind, or keep you warm in the winter.

Fundamentally different assets here. Own gold if you want to be short the dollar and/or US Gov’t.

Only a complete idiot owns rocks like gold and silver. They have done nothing in the last decade.

“But homeowners who want to sell are still muttering, “this too shall pass,” and are not putting their homes on the market, and those that are putting them on the market are now cutting prices at a substantial rate but not nearly enough to bring in buyers.”

Truth. I also wonder how much of this ongoing aggressive pricing is due to the desperation of the agents as the supply of used homes on the market continues to decrease. Just as the homebuilders find ways to navigate a more challenging sales environment, so do the experienced RE agents of used homes.

One tactic I’d bet they use is the “initial highball” price when they first meet with a prospective client. The agent confidently tells them they should ask this high price regardless of the recent interest rate hikes. And the agent is “certain” they can get it. Some of those homeowners buy into this BS and choose the agent who claims they can get the highest sales price.

Then they do not get that price. And the agent is back in say, 60 days telling the homeowner they may want to consider an asking price decrease because “things have changed since our initial meeting” or some other such nonsense. When the truth is the agent knew all along that initial price was too high for current market conditions. But it worked for the agent to get the listing.

Here in flyover land, many listings are showing decreases from the initial asking price. But the decrease is only to a “less ridiculous price.” As Wolf said, that is not nearly enough to bring in buyers. The seller attitude of “high price entitlement” is still very much in play.

A 250bps buydown on a 30y at the median new home price (80% LTV) is approximately 18%. He said only 25% of customers are doing that–4.25%. Homebuyers may be unsophisticated and choose other upgrades. I doubt pultw could afford to buy down 100% of buyers 250bps.

Excess spread on 30y mortgage over 10y is appx 200bps. That’s a risk premium representing 15%. Lenders/investors do not trust LTVs, pricing in 15% risk.

There is more risk in the housing market than advertised, it’s priced appropriately in actual lending, but the broader financial world is focused on lagging indicators of overall equity which ignores the fact 8T+ of the total mortgage debt was originated 2021+ at the inflated <3% mortgage period. A 15% broad value decline in housing would push close to 25% of mortgages to rates of 80%+ LTV making them impossible to refinance and the vicious downward cycle could begin again.

8% mortgages have pulled $12T of credit out of the system. Consumer spending is completely unsustainable and this is a tinderbox waiting for a spark.

Just one guys napkin math take.

When you look at houses being listed now, a large percentage of them were recently purchased in the 2020 to 2023 time frame. That tells me recent buyers know they are out on a limb and expect prices to fall, eliminating the substantial and quick equity they’ve realized in 2-3% years. These sellers are trying to sell the homes at 10-30% price gains, so a 15% price decline would not eliminate their initial equity. It would merely wipe out some or all of their unrealized gain.

I’d think we’d need a 30% price decline to see passive sellers become active sellers.

As LT interest rates remain high, and huge numbers of new apartments are released, more and more potential buyers will wait this out. At the same time, potential sellers will come out of the woodwork as they salivate over the prospect of locking in a 5% to 7% safe retirement stream on their substantial home equity.

It’s just a matter of time.

C,

Your “napkin math” is NOT how buydowns work and how they are figured. Your napkin math is fundamentally wrong. Reality is much more complex.

Pulte discussed a few aspects of it, including the forward contracts it uses, etc., in the conference call. I linked that transcript of the conference call so you can read it.

Few 30-year mortgages live 30 years. The average 30-year mortgages lives about 7 years before it’s paid off, either when the house is sold or when the mortgage is refi’ed. If mortgage rates drop to 5% or below, those bought-down to 5.75% mortgages will be refi’ed. That’s what makes the buydown calculation very complex. It’s not just simple mortgage math.

Wouldn’t you expect the average life of a mortgage to lengthen as more people feel locked into their low rates? Refinancing is certainly way below average.

It will lengthen if rates stay at 8%. But it won’t lengthen all that much because Americans are very mobile and move a lot for jobs or change of scenery or to live closer to relatives, etc. And each time they move, the mortgage gets paid off.

If rates keep going up won’t this blow up like what just happened to the banks with there bonds?

No, because the taxpayer guarantees the these mortgages, and they’re rolled into MBS. Those MBS with 8% mortgages offer juicy yields and make for good investments, even if rates go higher. Hold the MBS, collect the high yield, collect the pass-through principal payments, and some years later collect the remaining face value when the MBS is called.

You have to remember, the builders pays to have the mortgage bought down to 5.75%. So the mortgage pool has the 8% mortgage.

I wouldn’t say it’s fundamentally flawed. We’re both making assumptions about duration and collateral values. The ability to refinance requires equity. A modest fall in home prices could extend the duration and credit risk materially and I think that’s why the spread over the 10y continues to expand. Investors are concerned and the market is speaking.

Hey Wolf, thanks for another exceptional analysis. I’m curious why homebuilders choose mortgage rate buydowns (or a combination of that and other upgrade incentives) rather than straight up bottom line discounts. If they cut that $35,000 average right off the top it would similarly help customers who were priced out. Would it also result in less taxes from the sale, or influence property taxes positively? Plus, if rates are lower 10 years from now or whenever, customers can refinance. It seems like that would be a bigger draw for customers, and there must be a break-even point where the homebuilder is indifferent between those approaches. It sort of feels like lower prices would be more of a win-win compared to buydowns. Am I missing something?

The point is to lock in the buyers so they cannot flip the houses. A buyer with a high balance and low interest rate won’t turn around and sell and thereby compete with other new homes for sale by the builder.

Most people buy the monthly payment.

They live paycheck to paycheck so what

will that paycheck buy ? Lowering the price does no good if the monthly nut

can’t be met.

Builders choose what causes buyers to buy in a way that allows builders to maximize their income.

Buyers don’t have to go for it. The onus is on buyers. If buyers fall for mortgage rate buydowns rather than a 30% price cut, it’s their problem. Buyers could just refuse to buy, and then builders would have to come up with more radical price cuts to sell their houses. But buyers are buying those buydowns hook line and sinker, and that’s why builders are using them. Quit blaming builders, and start blaming buyers for the high prices.

BTW, a $35,000 discount has far less impact on the monthly payment of a 30-year $500k mortgage than a 225 basis-point rate buydown. That’s why buyers go for them.

In the years after 2007 I was a RE agent and auctioneer. What I learned is that non-forced sellers will hold on to a property for years rather than cutting their price to meet the market, in fact they will ride it all the way to the bottom before finally capitulating. Meanwhile the property rotates through all the realtors in town and the seller is disgusted with the worthless realtors while in fact the ONLY reason a property doesn’t sell is because it’s priced too high.

Many homeowners fail to understand the total costs of holding a property such as missed opportunity costs where if they would sell their property they could deploy the proceeds into more profitable ventures instead of of keeping it tied up in a depreciating asset. In this situation the seller that panics first panics best.

Another thing that happens to stubborn sellers is that the 3 D’s can cause a non-forced seller to become a forced seller at any time and then the property sells for current market value or goes into forclosure depending on the situation.

Wolf,

Who holds the mortgage after the buy down? How does that work?

Does Pulte pay the mortgage holder enough to reduce the 30 year mortgage rate to 5.75%?

Yell at me if this was detailed in your article but I did scan for it.

Most of these mortgages, like most mortgages in general, are sold to government agencies such as Ginnie Mae, or the GSEs, such as Fannie Mae and Freddie Mac. The mortgages that cannot be sold to those entities are pooled into private label MBS that are then sold to investors.

There were questions in the conference call about the mechanics of the buydowns. The answer from the CEO was two-fold: we’re using forward contracts; and we can’t talk about it more because we “don’t want to give away all of our trade secrets on that.”

Thanks Wolf!

“CEO was two-fold: we’re using forward contracts; and we can’t talk about it more because we “don’t want to give away all of our trade secrets on that.”

Can’t believe he said that…What arrogance!

I mean, it’s not arrogance, it’s black letter law. If you have an idea that is not patentable, the only way to protect it is to keep it secret. If he discloses it, any other builder can use it.

My guess is that they’re using some form of derivative where they make payments as long as interest rates are above the “bought down” rate. If they drop below it, they don’t pay anything.

Will be interesting to see how lawsuits play out against NAR. Case is only starting but would be interesting to see how it shifts commissions and market. My house is paid off and now worth probably 600K down from 700K from last year or so. I was considering a move and selling myself as when home prices go up the commission goes up significantly faster than inflation.

Einhal,

You said, “I mean, it’s not arrogance, it’s black letter law. If you have an idea that is not patentable, the only way to protect it is to keep it secret. If he discloses it, any other builder can use it.”. —-

You missed my point. When companies refuse to disclose financial information to investors during conference calls, investors get antsy and tend to go elsewhere.

The Pulte CEO, not understanding this and having a financially verifiable answer ready behaved stupidly, and his stupidity was probably born of arrogance or maybe even something worse. You do not refuse to answer questions during conference calls.

Further, 30 years is a long time. All sorts of things can happen in 30 years. There may not even be a Pulte in10 years. Will homeowners be left holding a bag?

Buying a house from Pulte with one of these tied into the mortgage and not understanding it’s implications would be stupid of a home buyer.

Anecdotal RE Vancouver Island:

In my area, nothing selling at all. However, no one yet dropping prices. I hear people say, “I need to get this much”, or talk about how their property is really worth +++. We’ll see.

My buddy manages a very large lumber yard, the one contractors use as opposed to Home Depot type stores. Slowing down big time. Trucks in the yard, guys rushing out to help me load up, talk of layoffs for the first time in years. A cabinet installer I know has had 3 contracts cancelled this month alone. He let his apprentice go and his wife now helps out. I assume his general contractors are doing their own installations to keep their people working. My brother in law still in the trade and while they are busy in their niche market of high end renos, regular house building is dropping. Tradesmen phoning about work.

8% is nothing. If folks think this is a shock think about the 18% we experienced in the early 80s.

There is a breaking/tipping point. I remember many people absolutely unscathed and never missed a pay cheque in the 80s. However, I was one of the million laid off in Canada in 81 and had to work away from home and finally just moved. Broke even on the house sale, didn’t make a dime on all the improvements made. Not one dime. The good thing is never went into debt ever…even when times started booming. No debt = safety.

Comments like yours are why reading this blog is worth more than all the rest of the financial press. The voice of experience.

Prices of new homes are consistent with the reality. However, the prices of the previously owned homes have detached from the reality long ago. I think many existing home owners feel like there is a divine rule stating that the home prices must rise at least 5 to 10 percent each year, regardless of the rates and macroeconomic conditions. However, many (to be) buyers are not qualified to borrow enough to pay those prices, even they want to.

So, there is a deadlock pushing the previously owned home sales to the bottom. I feel like most existing home owners are ready to wait a few years for the FED’s next money printing spree to sell.

The only thing that can break this deadlock is a panic in the market. But there is a paradox in here: At the slightest sign of panic, the FED immediately starts printing money, reinflating the prices even more. So, the previously owned home prices seem like settled at this exorbitant levels, despite the high rates.

Survey from Zillow said that 23% of homeowners are thinking of selling in the next three years. That is up from 15% a year ago. Out of those people 4 in 10 were thinking of selling in the next year.

If that actually happened, there would be 23% times 40% or 9.2% of homes being sold over the next year. I saw another statistic that 1% of homes were sold in first half of this year, so moving to 9% of homes being sold would be a 400% increase in homes being sold. Although I am sure that intentions and actions are not the same thing.

I think what pushes people to sell is declining prices. Homeowners have not sold because they see the low demand, but if prices are falling, then they want to sell sooner.

Once mortgage rates hit 10% and demand is even lower, then homeowners begin to try to sell, prices will start to really plunge. Throw in a recession and some job losses and you have a formula for the bubble to burst in a significant way.

Looking at their financial statements because of the margin discussion, I find more relevant the information about cancellations. Although small (15%) right now, this is one of the things that can bring the sector in dire straits.

In Brazil, cancellation rates reached very high levels (50%+) and almost brough down the entire sector untill the government allowed builders a retention fee of 25% in case of cancellations.

Anybody else notice the traffic is back to very bad levels again? The WFH trend dropped traffic levels for a while, but now I think it is worse than ever. I imagine this is causing must frustration for people who bought in outlying suburbs during the 2020 to 2023 period. Perhaps that is a key reason why lots of these homes are for sale now.

I work with a lot of state employees who are transitioning from full remote to hybrid models. More and more of my neighbors are heading to work in the morning just like pre-pandemic times and as an avid cyclist, it’s getting dangerous again to be on the roads.

OutW-gets me to wondering (anecdotally, of course)…

I live in a rural part of my county, and despite the reported drop in its population (California, natch), traffic is worse now, out here AND in the suburban/urban areas than I ever recall. Could some of it be WFH’s popping out to run errands, shop, have a meal? (Tempted to use Wolf’s ‘drunken sailors’ term, here…).

may we all find a better day.

Boston traffic is nearly back to pre-2020 levels.

Anecdotally, of course.

In two thirds of Canada by population doctors and lawyers are shutout of the new detached home market. The Chinese really overdid it to new home prices.

Can you please come up with a new whipping boy? Maybe the Kiribatians or the Dubaians? Or God forbid, the Canadians!

Homebuilders, like Pulte Homes, are in the business of building and selling new homes. I believe they are the biggest in the nation and one of the few that have their own mortgage companies. However, new home sales are less than 10% of the real estate market. It is previously owned homes that make up the bulk of home sales. Several things I noted in this article, which weren’t further analyzed. A 35K hit on the sale of a home where the buy-down is substantial and no wonder Pulte stocks took a huge tumble. This affects their bottom line and erodes their margins. They probably cannot make that up with volume since that would be impossible on that kind of scale. Secondly, current homeowners are still in the catbird seat. Many of these, if not most, bought their homes when interest rates were near rock bottom – between 2.5% and 4%. Why in the world would these homeowners want to sell their homes with these fantastically, low home interest rates to buy a home at 8% or even a Pulte home at 5.75% buydown rates? This affects inventory, which is not to be had, because these homeowners are sitting tight and holding on to their homes. Tight inventory is why the median price of a house is still in the low-to-mid 400K range – median, not average.

I paid my house off back in June 2023 and I had a 3.99% rate on 15 year loan. All I have to worry about now is taxes and insurance, both of which are going up in Florida, thanks to Hurricane Ian and climate change. This is the price we Floridians pay to live in Paradise, especially those of us in the subtropical climes of South Florida. However, following and analyzing real estate will continue to be my hobby as it has been for the past 30 years. Cheers and thanks for all the fish.

“new home sales are less than 10% of the real estate market.”

That was before existing home sales collapsed. In September, only 347,000 existing homes (houses, condos, co-ops) were sold, but 60,000 new single-family houses were sold; so now new single-family house sales are 17%. If you include new condos for an apples to apples comparison, it’s over 20%.

How does the rate buydown work if the builder goes out of business before the mortgage is paid off? Is the owner simply stuck with the original rate if they can’t refi?

That is what I asked Wolf and he said among other things that the Pulte CEO refused to disclose the mechanics of the buydown in the conference call. stupid……..

Well I certainly hope you don’t own any shares of Pulte…

I’d say great time to short the homebuilders and housing market in general.

(Disclaimer: I am short housing, and this is not financial advice).

Slightly off topic, but something I’ve noticed recently on Redfin is SFHs and large townhomes being advertised as individual rooms for rent. Maybe landlords aren’t finding folks that want to rent out a massive expensive luxury townhouse?

It seems we could be moving back to the era of boarding houses.

While prices have been declining in a number of regions over the 1.5 years (almost 2 years) and the bubble is deflating…. we’ve never dealt with this type of inflation before at the same time.

I think we’ll continue to see lower prices, but the bottom won’t look like the GFC in most cases… Just because the higher labor costs, cost of inputs, etc will most likely not be going away across the board. As a result, this slo-mo housing crash may not “seem” as bad because inflation will “prop” up housing prices in a deceiving way.

Why can’t I pay 6.3% more for a house to get my mortgage rate discounted by 2.25%? Only new homebuilders can do this?

Isn’t the national house price just back to all time high recently?

No.

Existing homes, national median price, peak was June 2022:

New houses, national median price, peak was Oct 2022: