BoC already shed 50% of its QE assets. And the shedding continues.

By Wolf Richter for WOLF STREET.

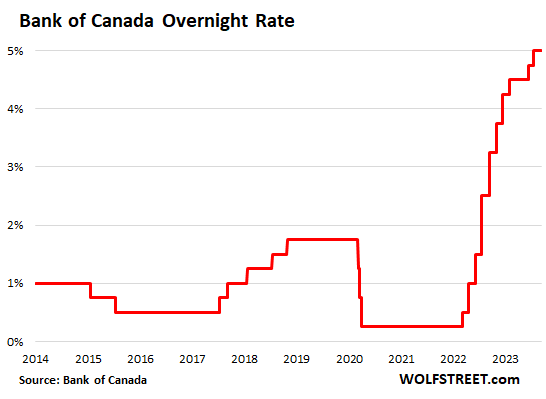

The Bank of Canada left its policy rates unchanged at its meeting today after two consecutive rate hikes following its spring “pause”:

- Overnight rate: 5.0%, the highest in 22 years

- Bank rate: 5.25%

- Deposit rate: 5.0%

And it inserted a clear bias for further tightening: It “remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed,” it said in the statement.

Tightening bias: inflation without economic growth.

The problem the BoC faces is re-accelerating inflation in a slowing economy, with GDP dipping 0.2% annualized rate in Q2, while CPI inflation accelerated from 2.8% in June to 3.3% in July. And the BoC expects CPI to further accelerate going forward.

Economic growth fizzled, “which is needed to relieve price pressures,” the BoC said in the statement:

“Economic growth slowed sharply in the second quarter of 2023, with output contracting by 0.2% at an annualized rate. This reflected a marked weakening in consumption growth and a decline in housing activity, as well as the impact of wildfires in many regions of the country.”

“Household credit growth slowed as the impact of higher rates restrained spending among a wider range of borrowers.”

“Final domestic demand grew by 1% in the second quarter, supported by government spending and a boost to business investment.”

“The tightness in the labour market has continued to ease gradually. However, wage growth has remained around 4% to 5%.”

But inflation accelerated, and inflationary pressures remain “broad-based”:

“After easing to 2.8% in June, CPI inflation moved up to 3.3% in July,” it said.

“With the recent increase in gasoline prices, CPI inflation is expected to be higher in the near term before easing again.”

“Year-over-year and three-month measures of core inflation are now both running at about 3.5%, indicating there has been little recent downward momentum in underlying inflation.”

“The longer high inflation persists, the greater the risk that elevated inflation becomes entrenched, making it more difficult to restore price stability.

So the tightening bias: wait and see, “prepared” to tighten further.

“However, Governing Council remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed.”

“Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation.”

“In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behavior are consistent with achieving the 2% inflation target.”

Quantitative tightening continues.

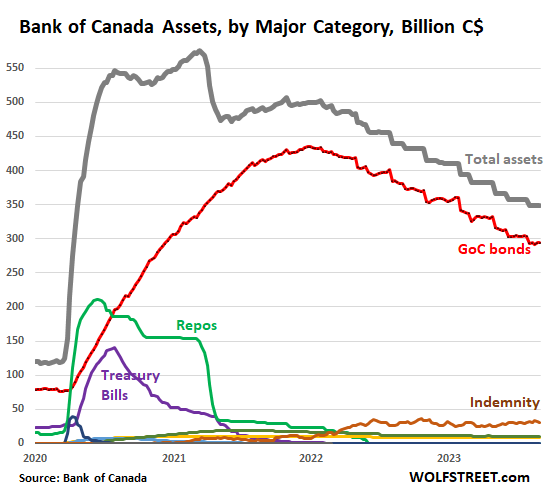

Unlike the Fed, the Bank of Canada has no caps on how much of its portfolio is allowed to roll off every month. Whatever matures is allowed to roll off without replacement.

The main item left on the balance sheet are Government of Canada (GoC) bonds (red in the chart below). During the pandemic QE, the BoC added $356 billion (all amounts in Canadian dollars) to its existing pile of GoC bonds, bringing the peak QE balance to $434 billion. The QE add-on of GoC bonds has now fallen by 39%, or by $139 billion, to $294 billion, as of the balance sheet on Friday.

The second largest asset, behind GoC bonds, is an account the BoC calls “indemnity” (brown), $31 billion, which tracks the unrealized losses on its bonds. Since it holds bonds to maturity, when it will get paid face value, those losses are theoretical, and vary with long-term bond yields. This “indemnity” reflects the losses that the Government of Canada would have to reimburse the BoC under their pandemic-era indemnity agreement if it actually ever sold all its QE bonds, rather than holding them to maturity.

The liquidity measures – mainly repos (green) and short-term Canada Treasury bills (purple) were allowed to roll off in 2021 and early 2022 and have completely vanished. There are only minuscule amounts of other securities left on the balance sheet, including some mortgage bonds and some provincial bonds.

Total assets (gray) have dropped by $226 billion, or by 39% from the peak of QE in March 2021, to $349 billion.

In terms of the BoC’s pandemic QE, it had added $455 billion to its balance sheet from March 2020 through March 2021. Of this pandemic QE, it has now shed $226 billion, or roughly 50%.

And the BoC said today that this QT will continue.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

More rate increases sure to follow coming spurt of inflation.

In more than Canadian locales

Yes, inflation is a monetary phenomena which can only be solved by restricting the supply of money while increasing the cost of borrowing.

Why ? Because, in a world of producers programmed to attempt a price increase everyday, inflation, unfortunately, occurs when the consumers have too much money too spend and agrees to pay the price increase for the product that yesterday sold for 5% less.

It starts small but ultimately becomes a social meme, incorporated into the humdrum economic planning that ordinary people, like me, do.

Canada is a fringe economy, selling it’s excess natural resource based products into the adjacent black hole, the US economy.

The recession starts on the fringe and works it’s way, across the radius of the economy. The fallacy that monetary policy, designed to make the greatest financial swindle in history go away, will go on forever has been the winning hand for the past 15 years since wall street almost blew up the world.

Like Wolf said: There is always a recession.

I really admire QT speed of BoC. 39% is a good deal of reduction. FED has only shed around 10% of its gigantic balance sheet. And it is trembling – feels like they can reverse in any minute – what a shame.

Wolf can correct me, but the Fed cannot shed even 50% of its current balance sheet as a lot of it is other peoples money. From what I am seeing off the H.4.1 release on 8/31/2023, $4.935T is there as other peoples money so they cant go below that level. It’s comprised of currency in circulation (over $2.3T), RRP (nearly $2T and some of that is mine via MMF), TGA (nearly $0.5T), etc. Anyone can look at the balance sheet and see it there if they want. It went up after GFC in part because the TGA moved its funds from commercial banks to the Fed so it had to go up for the TGA back then and now a lot of regular people like me with MMF that do o/n RRP.

Z33, I think you are wrong. Total balance of FED was well below $4T prior to pandemic in 2020. Then, they started printing like crazy and it became ~$9T. They shed around $1T in about a year and it is $8T now. Vast majority of it is treasury bonds (I totally understand the reason) and mortgage BS (totally nonsense action – they were still buying mortgage BS when an ordinary house was getting 20-30 offers – absolutely ridiculous)

The Fed can shed close to 100% of the assets it bought during the Pandemic QE without problems. That would take it to maybe $4.6 trillion. It may be able to shed more. But that’s what it can do, based on its liabilities:

Under this scenario, RRPs = $0, reserves = $1.5 trillion, TGA = $700 billion, currency in circulation = $2.4 trillion

All combined = $4.6 trillion

That $4.6 trillion will rise over time as currency in circulation rises. If the Fed does another 4 years of QT, that $4.6 trillion will be higher.

QT will slow down after a big bunch of bonds have already rolled off… there will be less left over that matures every month. So QT could drag out for many years.

You got that Right Paul Volker all over Again

The US will be exporting inflation to Canada; it is wise of the BoC to be ahead of the curve in that respect, to keep their overall inflation from re-accelerating. Canada will also have currency issues if it does not match rates with the US.

I think that the US is already exporting inflation to the state of Canada.

If you admire the BoC you need to review your entire life.

Housing prices here are *insane* under their watch.

Housing price is a function of supply and demand, mainly.

Local and Provincial zoning laws have tighten supply to insufferable levels, doing a lot of damage to the potential gdp and quality of life of many people, both current and aspiring homeowners.

But yea, BoC has contributed to the demand

It is the central banks and their policies that determine supply and demand.

Low interest rates = high demand and prices and vice versa.

So they are the ones who indirectly determine whether property prices will be high or not.

The supply and demand of credit is hugely important, BoC kept rates too low.

High demand and thus high cost comes (simplistically) from continued low interest rates which is the the fault of the BoC. However, it’s not a mistake but an unfortunate side-effect of choices made to deal with the GFC and subsequent years.

Had the BoC (and the Fed) not done what they did, we might have had a second Great Depression instead of just a short Great Depression. Or something else entirely.

So while there were probably better choices that could have been made, those options were in no way obvious at the time and nobody can say what the TOTAL situation would be (not just housing prices) had they acted differently.

Two or three years isn’t long enough for the effects whoever in Canada and the US that ordered the foolish currency debasement, which stole from the present and future, to show. They likely made the magnitude of the inevitable recession or depression even worse.

Anyone suggesting that one should review their entire life, is generally evaluated as a rebellious individual, ranting against the obvious that no one else can see.

That being said, I agree, housing prices are insane too anyone that is trying to buy, not too the ones that hope too sell.

“The FED has only shed around 10% of its gigantic balance sheet. ”

That is proof that the Fed is not serious about controlling inflation or reversing the damage their irresponsible behavior has cost the US economy and the hard working Americans that have to earn a living and raise their families. At the rate they are going, by the time they get the balance sheet down to anything near pre-pandemic levels we will be in another recession and they will back off and start printing again.

I agree

The welfare of the median population is no longer the objective Fed.

The Fed is mostly concerned about the asset values of the wealthiest Americans.

I do not want a crash. The Fed continues to fund the speculators over the savers, which sustains the massive bubbles in asset values that we all are holding our breath, waiting for them too collapse.

The BOC is in a position too stabilize the Canadian economy but, obviously so far, do not have the intestinal fortitude to prevent the curse of the Volker panic, when he realized that cuddly wasn’t working and that inflation had spun out of control.

The rest is history. This bumbling, government banker realized that inflation is like an insect infestation. Eventually, you have too kill it all.

Wrong… there is nothing “un-serious” about the Fed’s QT. It is just that the Canadian central bank can go faster in downsizing its Balance Sheet because Canada has a pip-squeak economy compared to the Colossus next door… a Colossus economy which Canada has a Free Trade Agreement with no less.

The Fed doesn’t have another large nation to count on if it accidentally blows up its host economy. Nor does the Fed have a GUARANTEE from Congress to make it whole if they sell bonds at a loss. Hence the caution.

But as Wolf points out in this article, the Bank of Canada’s interest rates are the same as the Fed’s… and Canada’s inflation hasn’t been much different from America’s… and is (currently) accelerating faster than America’s as well.

The Fed also has guarantees for some of their programs. Regardless the guarantee is just an accounting thing. The Bank of Canada hasn’t been selling any bonds at a loss. Only letting them roll off. The difference with the US is that the BoC isn’t capping how much can be rolled off.

Yet interest rates are lower in Canada than in America and most assume like Australia the real goal is to prevent any collapse in housing prices.

50% roll-down is impressive, I wish the Fed was on the same path.

Why? What on earth difference would it make at all?

I would likely result in higher yields, which some feel is needed to tame inflation.

Exactly, some feel that higher yields are the solution too an inflation, IMO, that has been caused by Bernanke’s monetary experiment.

In the sense that I think that inflation is only possible when the consumers agree to pay a higher price for the same thing.

There is only one way to stop the current bought of inflation and that is raise the FFR at the September meeting by 25 bpts.

Selling MBS would instantly cripple what’s left of the mortgage market. Prices and valuation would collapse, as well as banks and other entities holding MBS. Instant asset deflation! 🧨💥

No, your scenario would not happen, not even slightly.

What’s wrong with that?

I wish that were true Camille. We need asset deflation as things are currently way way way overvalued.

You wish you were in a country where even someone in the tenth percentile of earners can’t afford the average home price?

That’s the reality of BoC stewardship.

Well, that and the fact that housing starts in Canada peaked in the 70s when Canada had little more than half its current population, eh?

> I was pouring gasoline on the fire but I didn’t start it

No that won’t cut it.

Yes the BoC isn’t the sole cause.

Yes they are totally useless at their job and despicable.

For what it’s worth, I share your angst, hoping that the future will be different than the miserable lot we have created for ourselves.

IMO, housing prices are twice what the median good guy and girl van afford.

Will the lurch toward equilibrium be violent like an earthquake or like popular perception of human history.

Whether by coincidence or on purpose when Stephen Poloz was in power interest rates were lower in Canada than in America and nothing has changed since. Before Poloz was in power interest rates in Canada were always higher than interest rates in America.

The CAD is about 73.5 cents USD as of today. Almost touched 72 cents.

If the Fed keeps hiking, the CAD goes lower, which means more food inflation due to many staple commodities being priced in USD, and imported from California.

Central bankers have created a massive mess and are simply not taking it seriously still. Sure, they have raised short term rates, but Canada is one of the only central banks that have come close to selling off their assets.

If the Fed were serious about stopping inflation, they would at least double the pace of the QT. And they would keep executing QT even after we hit a zero inflation rate. We need to reverse some of the negative impacts of the past 2 years.

I feel terrible for Canada. Its RE market is already a powder keg. If inflation keeps up and rates go higher things will get ugly fast.

We need to build a wall across our northern border.

Can’t blame you. Canada has been giving away student permits like candy, while allowing them to work like Wall Street accountants during tax season.

At least 900,000 student permits were disbursed this year.

They also “miscounted” another million people on “temporary” visas.

As if you can possibly do that! The knew.

@Georgist:

America used to benefit from the Canadian skilled grads. Now they will have to deal with the endless amount of people who are using a student visa as a gateway to the United States. This is not a political blog, so that’s all I can say.

Canada is in a mess right now, and the smart people have already secured jobs in America.

There are a large amount of variable rate mortgages in Canada. The Trudeau government passed a bill to allow longer amortizations keeping the payment the same. However, most mortgages are 5 year and many will not qualify to renew.

We also allow mortgage holders to take out a Home Equity Line of Credit for up to 65% of your equity.

Canadian banks have been increasing loan loss provisions.

It’s a ticking time bomb.

First time buyers also have to pass a stress test which is now 8%.

Except for Calgary Alberta most other markets are declining.

Well don’t feel too bad about the ones that are about too learn about a free market.

The Fed support of the speculators is like support for the British lobster backs against the Continental Army

The current standoff is normal as one approaches the cliff during the night, guiding their self by intuition that the BOC will revert too it’s safe, accommodative position. Whatever the Fed tells them too do. Release money or restrict money, whatever the Fed needs,

@gametv: Slowly but surely lol. The Fed’s Balance Sheet is at April 2021 levels.

@captive: People would rather buy a rental property and charge C$1,000 per person to live inside a room than to invest in companies and stonks in Canada.

This is how entrenched RE is in Canada. Nobody wants to invest in the next big thing, or invest in financial assets. It’s to own a property, and charge rent like the English aristocrats. But the Ponzi scheme is dwindling, because many people want to leave Canada.

Gen Z,

I shop occasionally from websites in Canada. This past year has been especially fruitful. I purchased several nice items at big discounts, availability was very good and shipping super fast. If inflation is high in Canada it is not in high end shopping. I am currently scoring good finds out of Europe.

MW: A rising US dollar is ringing alarm bells overseas. Should stock-market investors worry?

The days of cheap oil supporting the economy when in recession are over. Oil will continue its relentless increase in price. This will cave western economies that have “grown” on cheap oil.

We’ll have rising prices of goods and essential services and most of “nice to have” will eventually fall of the cliff. And there is alot of “nice to have” in the US economy.

Oil was over $114 per barrel many years ago and is now only $87.00 which is much cheaper now than it was.

Oil was $20/barrel many years ago. What’s your point? Look at long term, smoothed out trends.

And geo-politically, we no longer have the Saudi’s in our hip pocket to crank up production and drop prices when a recession hits. Every country with remaining resources is moving in the direction of protecting their remaining assets.

Oil was $9 per barrel in 1999. Its price has always been highly variable ever since Marc Rich pioneered its trading in the commodities markets leading to the mess of 1974-75 and odd/even days to fill up at the pump.

I fall into Mikes camp for the low oil price helping the USA economy as well as exporting manufacturing throughout the 1980s and 1990s etc with wage suppression. Oil price was a function if supply and demand globally and technology breakthroughs for some of that supply. The USA trade deficit and USA job growth is now benefiting from exports of energy due to increased supply of oil and NG. Inflation adjusted I would think 1980 40 usd/bbl is higher than current 90 usd/bbl. Keep drilling!

That’s ridiculous. The earth, as the producers tell it, has been on the verge of running out of refined fossil fuels, unless we submit to their demands. In reality there is an abundance of supply.

Could it not be said that, in order to tame inflation, Fed Chair Powell is raising interest rates to curtail consumer spending. Yet, it is the the U S government that is spending excessively; creating the inflationary forces (this time around) that squeezes the taxpayers with the adverse actions of the Fed. A double, if not a triple whammy to the taxpayers.

Government spending crowds out private spending. This used to be conventional wisdom.

The underlying decay is evident everywhere, apparently offset by the resilience of technology growth — which by it’s nature, seeks to make a select few people less obsolescent.

Technology is definitely helping to provide opportunities for a select few, so that scales of efficiency can benefit the people that can no longer afford to live

Obviously government intervention in adjusting fiscal and monetary policies are caught within this gravitational push and pull, somewhat frozen by the reality of inflation, but playing it’s part to expand the cancer of bureaucracy.

I went to a gas station today for a cold bottle of Starbucks and small bag of M&Ms — $6. I wonder what the equivalent is in Loonies? I doubt anyone cares .

“The underlying decay is evident everywhere, apparently offset by the resilience of technology growth”

Maybe in Canada?

The economy in the US is running hot, accelerating in Q3 from Q2 and Q1. Check out the Atlanta GDPNow for a feel, if you don’t want to read the articles on Wolf Street on this topic — and there are lots of them on this topic. All you have to do is read them.

Saw a goofy Forex article today that said the various Fed officials (in the USA) had all, but promised no rate hike in the September meeting. Which increased the odds of a November rate hike to 40%. What information are these bozos looking at when they write such stuff?

I think they just like to hear themselves talk as it inflates their egos.

oops…looks like a case of stagflation to me but no worries, they can just come out and tell us Stagflation is transitory…much like inflation is transitory here in the states..lol

I think this is the definition of stagflation. There is probably a duration element involved, but I don’t know how long it has to last to be called stagflation.

It is going to take a long time to lower inflation in the us and canada. We are yoked to NAFTA, and the huge trade will mean that we both need to keep fighting inflation. Otherwise, one side of the trade will benefit from a larger devaluation….like 60 cents usd lol. I can only imagine how real asset deflation is going to smack the entire world. Everyone here keeps bleating that JPow is going to be soft and he is not, and the rest of the Fed is going to watch the data and keep tightening the screws. The housing market panic starts at 8% for the 30 year….lol.

Ok first up you cannot just simply state our GDP was basically flat.

Our population went *up* 2% and yet our GDP remained flat.

Our GDP per capita is going down.

Secondly this little matter:

> Three major Canadian banks have disclosed that about 20 per cent of their residential mortgage borrowers – representing nearly $130-billion in loans – are seeing their balances grow as their monthly payments no longer cover all the interest they owe.

Twenty percent of active borrowers cannot even pay the interest on their loan. The money is being added to the end of their mortgage, extending their mortgage term, effectively loading the banks up with an ever increasing negative equity.

Canadians are on fixed rate terms of 5 years. Every single year 20% of mortgage holders have to pay the new rate. 20% of those (at least) will be unable to pay the interest on the new repayments, which will load the banks with even more.

Another stat: the tenth percentile of earners, estimated income $174,000, would not qualify for a mortgage on the average Canadian home of $754,700.

Wolf I welcome your comments on the above.

My take: they are going to have to hold rates or even cut them soon and tank CAD. They are also going to try to roll the immigration dice even more to prop up GDP as the reality of the Canadian “economy” as a rentier soaked mess comes to light. This country is *insane*.

And just to give some context on the rate of increase of negative amortization:

> TD TD-T had mortgages worth $45.7-billion negatively amortizing in the third quarter, the equivalent of 18 per cent of its Canadian residential loan book. That was higher than the $39.6-billion, or 16 per cent of its loan book, in the fourth quarter of last year.

So up 15% dollar wise and up 2% of its loan book in one quarter. BMO similar.

> This marks the first time BMO and TD have provided detail on loans that were increasing in size. Until now, the two banks did not disclose the information to shareholders, which suggested it was immaterial. They repeatedly declined to disclose the numbers when The Globe and Mail asked earlier this year.

What counts here is overall demand in the overall economy to see overall growth and overall inflation, and it doesn’t matter if there are more people — that only matters to the individual as they’re getting a smaller slice of the pie, but this is a discussion about the economy overall, not individuals and not about their happiness as individuals, and their wellbeing as individuals. This is not a social studies project, or whatever, but about the economy overall.

So yes, the Canadian housing market is going down, and I have been saying that for over a year, and I have been saying that the increase in prices this spring was due to the spring selling season, and that prices would go down afterwards, and now prices are going down again. That’s the overall market, and also in various metros. And higher rates put more stress on the housing market and on borrowers, and that’s what higher rates are SUPPOSED to do, as the BoC is desperately trying to cool the housing market. Why are you complaining about it?

So banks have to deal with the risks and the negative amortizations, but banks got paid to take those risks, and they’re going to have to deal with it. So what’s the big deal? They made tons of money on those mortgages, and now they’re going to have some bad breath and a headache. So what? If you still have bank stocks, and you don’t like those risks, sell the stocks and buy T-bills.

My takeaway wolf from georgist is a bit different. In the previous housing boom negative amortization really was a thing. Literally folks were getting these mortgages and making minimum payments and letting the money tack onto principle. Usually at 115% or 120% this would cut off but… this was a game that was played back then to get people into the payment so they could become “homeowners” Me thinks this is akin to the interest rate “buydowns” which are only good for ~five years…. Anything to get a sucker to sign on the dotted line. Is there any way to tell if neg-am shinanagens are back? Sure sign of a ‘top’ in my opinion

I’m not complaining about it Wolf.

I am saying this is not going to be a soft landing, and they might opt to do a soft default via CAD.

Living standards here have fallen considerably and even a tenth percentile job can’t get you an average priced home. I think that is quite extreme.

Healthcare here has basically collapsed and winter is coming. Watch this space.

Canada is a safehaven country. Not only is it a magnet for immigrants, it also has one of the highest per captia populatons of high net worth individuals. So yes, so long as an alt-right, isolationist political party is not voted into office, the flood gates will remain open, there will be no crash, no hard landing.

The idea that Canada is taking in rich immigrants on average is just a myth.

From a GlobeAndMail article dated 2015:

> Immigrants arrive in Canada with an average of $47,000 in savings but end up using more than half that to get settled, according to a new study.

> And almost one-fifth of immigrants come with no savings whatsoever, the report by the Bank of Montreal says.

> After all initial expenses related to making the transition to a new life in Canada, immigrants are left with an average of $20,000, the survey results published Wednesday indicate.

An average of 20k. That’s enough to eat out a few times and get one low-end car, based on 2015 prices.

I don’t know Wolf, the figures bounce around a bit due to volatile fuel prices and base effects and so on, but I don’t really see an accelerating (core) inflation story in Canada.

We will still get supply side effects (such as due to the price of oil, and due to the loonie dropping as interest rates in Canada fall below those in the US), but on the demand side – the only pressure I see is on rents due to the sky high level of immigration (and the impact of the rate increases themselves on the housing component of CPI), otherwise it looks like we are entering a recession, if anything.

Job market tightness is nothing like it was a year or two ago in most industries. Banks are raising provisions, tightening lending standards and laying people off. The housing market is dead and residential construction (which makes up an absurd % of the economy here) is dropping off (despite the pressure on housing from sky high immigration).

Even holding rates steady is tightening, since every day another tranche of borrowers (primarily residential mortgage, but also commercial, auto, etc.) has to renew at the new higher rates and QE continues as well). I’d be surprised if we see another rate hike this cycle from BoC.

Canada mostly dodged the 2008 downturn, but the price we (literally) paid for that was ever-escalating housing prices. Once prices get this high, there is no pain-free way out.

If the Fed hike the BoC have a choice:

Don’t hike and watch Canadians transfer money from CAD to USD, kicking off more inflation or

Hike and watch housing tank.

Who is going to buy Canadian government bonds at a lower yield that UST? Only those forced by regulation.

Financial repression time!

They will let the dollar fall if they need to (based on inflation readings, not on the state of the housing market), the shift in the value of CAD vs USD will offset the difference in rates for investors. It will cause some inflation, but I guess demand side factors will dominate this factor.

In the same way that post 2008 was a good time for Canadians to spend money in the US, the next few years are likely to be the reverse.

I agree they probably will. But if the do let CAD falls then we get inflation and all the fixed income pensioners are back in the hole.

No way out. Canada’s real estate “wealth” was really a millstone.

In Toronto, there are thousands of people applying for entry level jobs which pay minimum wage at the staffing agencies. It’s dire if you weren’t born into wealth with connections like the Upper Canada College elite.

Canada is becoming the way of the developing economy, but with dangerously colder weather, higher rents and housing, and no hope for the future if you’re young, and don’t stand to inherit anything from the Silent or post-war generation.

“tranche of borrowers” this is very eloquent.

A Canadian passport is better than most. It’s peaceful there.

“Inflation is accelerating – yeah, let’s pause rate hikes…”

Brilliant.

They probably figure that they can’t stop inflation with more rate hikes (presuming that the bulk of it stems from energy pricing outside of their control) and are worried about tipping into recession if too many borrowers become insolvent.

“They probably figure that they can’t stop inflation with more rate hikes (presuming that the bulk of it stems from energy pricing outside of their control)”

Wasn’t there a similar setup in the 1970s and Volcker did effectively kill inflation by hiking interest rates enough to tip the economy into a recession territory?

They can’t be afraid of a recession. That is the exact opposite behavior that they need to have right now.

If CAD falls because investors won’t lend to Canada at the same rate as the USA (surprise!) then we will get more inflation.

So BoC pausing is not a good idea.

But the die is cast now, there are going to be problems whatever they do, because the wealth wasn’t real and therefore will inevitably evaporate.

The central banks of the world have shown their hands – they are wholly corrupt inflationists. They will go down in history as the worst of the worst after they have completely destroyed all of the paper currencies. These guys don’t have a plan other than just devaluing money and inflating asset prices while hurting the majority of people in the process of enriching their already disgustingly wealthy buddies.

There are three North American countries struggling with inflation: The USA, Canada, and Mexico. The USA and Canada following similar approaches are struggling with inflation reaccelerating, while Mexico is showing a steady month over month decline, the “disinflation” that J. Powell is working so hard to achieve. Perhaps the financial insights and innovations of the Bank of Mexico may provide a guide and assistance to their Northern neighbors.

1. The Bank of Mexico began raising its policy rates in mid-2021, a year ahead of the Fed, and in big leaps from 4.0% to 11.25% now, and there was no talk about “transitory.” So that’s one lesson to learn: do it soon, do it big.

2. Mexico’s headline inflation number has the same issue as in the US and anywhere: it has been pushed down by the plunge in fuel prices and some durable goods prices, but fuel prices are rising again, so Mexico’s headline year-over-year CPI will rise again as well. We know that already because on a month-to-month basis, Mexico’s CPI jumped by 0.48% in July, up from 0.10% in June. So inflation is accelerating sharply on a month-to-month basis, and this will eventually show up in the year-over-year data.

“1. The Bank of Mexico began raising its policy rates in mid-2021, a year ahead of the Fed, and in big leaps from 4.0% to 11.25% now, and there was no talk about “transitory.” So that’s one lesson to learn: do it soon, do it big.”

Wait, huh? You told me I “just wanted to burn everything down” when I criticized the FED for pausing instead of hiking another 25 basis points, but “do it big” is now a “lesson to learn?”

The Fed raised late, but it raised big. Mexico raised by 7.25 percentage points (starting from 4%), the Fed raised by 5.25 percentage points, but off a much lower base (close to 0%), so proportionately speaking, the Fed raised far bigger. But it was a year late. And that’s unforgivable.

With all of the complaints, the US has strong purchasing power. Their index value is only behind Switzerland and Qatar. Things could definitely be worse.

You cannot make this up.

“Texas paid bitcoin miner Riot $31.7 million to shut down during heat wave in August”]

Riot said on Wednesday that it earned $31.7 million in energy credits last month from Texas power grid operator ERCOT. The company generated the credits by voluntarily curtailing its energy consumption during a record-breaking heatwave.

The total value of the credits dwarfed the 333 bitcoin the company mined in August, worth about $8.9 million dollars as of the end of the month.

ru82 – Sad situation but sign of the times.

With all of the concern with climate change and energy consumption, bitcoin mining should be first to go but is rarely mentioned. There is no societal benefit, only a place to hide assets or speculatively invest.

Bitcoin should have been banned from public trading in the first place. Now that it is being traded in the open market like a stock ETF and the hedge funds have bought into it, it has become politically inconvenient to get rid of bitcoin.

Thanks Wolf. As a Canadian I cannot help but think we are much worse off than the U.S. currently and WE are more likely to dip into recession after the potential stagflation takes a grip. Our housing market is still incredibly frothy and unfortunately a lot of recency bias in the housing market views the Tiff pause as they are about done raising rates + immigration flood many with dry powder are anxiously waiting to buy the housing dip. This will not end well but I’m fairly convinced that Canada will go into recession sooner than later.

You missed the big dump from this week’s update.

The BoC rolled off another $24B in bonds Sep 1st.

Yes, that was a big one. The BoC updates its balance sheet on Friday afternoon (today). So two days ago, when the meeting took place, only last Friday’s balance sheet was available. Here is the updated chart as of today’s balance sheet: