Driven by manufacturing plants for technologically advanced, high-value products. Automation is the great equalizer.

By Wolf Richter for WOLF STREET.

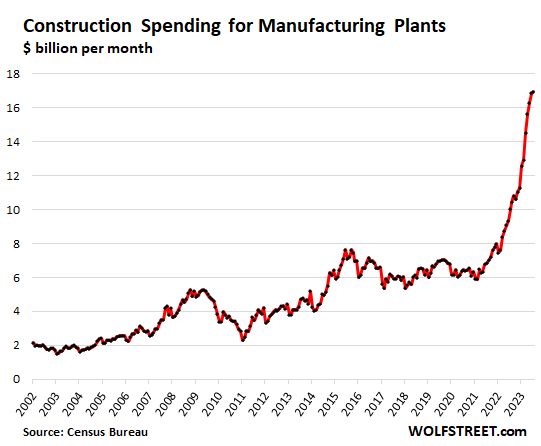

Spending on construction projects for manufacturing plants in the US started breaking out of its long doldrums in January 2021. That month, about $6 billion was invested in building factories, same as in January 2015. But then monthly construction spending for factories began to spike and in July set a new record of nearly $17 billion, a notch up from June, according to the Census Bureau on Friday.

- Up by 186% over the 30 months from January 2021 through July 2023.

- Up by 148% over the 24 months from July 2021 through July 2023.

At the current pace, companies are investing nearly $17 billion per month in building manufacturing plants, or about $203 billion a year!

We’ve been hearing it in the news and in corporate reports: Semiconductor plants, EV plants – Tesla, legacy automakers, and startup companies are plowing many billions of dollars into ramping up manufacturing – component makers, makers of computer, electronic, and electrical equipment, etc. The latter bunch are big drivers behind the surge of factory construction, according to an analysis in June by the Treasury Department.

All of them are technologically advanced industries with high-value outputs. Forget T-shirts and plastic toys.

And all of them use highly automated factories. Industrial robots cost the same in the US as in China. They’re the great equalizer when it comes to costs.

There is still a huge amount of manufacturing in the US. By output, the US is the second largest manufacturing country behind China, and larger than Germany, Japan, and South Korea combined.

The problem is that the US has fallen far behind China, and that many industries are dependent on imports from China and other countries. When covid tangled up the supply chains, suddenly there were massive shortages of the most needed products, including semiconductors. So that was a wakeup call.

In addition, as trade relations between the US and China have soured, companies are seeing new risks in being dependent on China.

The majority of cars and trucks sold in the US are assembled in a factory in the US. All major foreign brands have assembly plants in the US, including BMW and Mercedes. Hondas built in the US have among the highest US content. Tesla makes vehicles in the US including for export. And yet, component shortages, triggered by semiconductor shortages, caused the worst vehicle shortages ever. So time to reevaluate things.

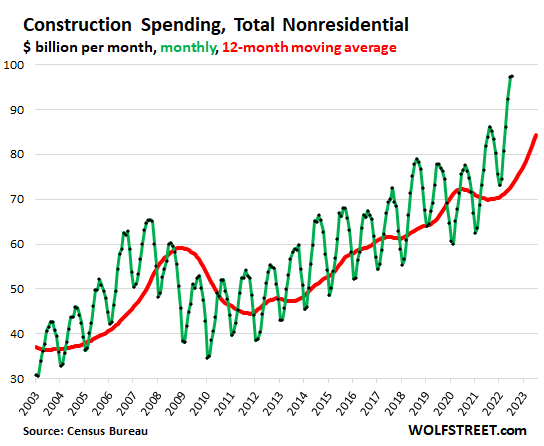

Total non-residential construction spending, which includes spending on manufacturing facilities, has surged as well, but not nearly as much. Since July 2021, it grew by 27%. Nonresidential construction spending is very seasonal (green); the 12-month moving average clarifies the trend (red):

Red-hot increases of construction costs in 2021 and 2022 are responsible for a portion of the increase in spending: A considerable portion or even all of the two-year 27% increase in total nonresidential construction spending may have been due to higher costs.

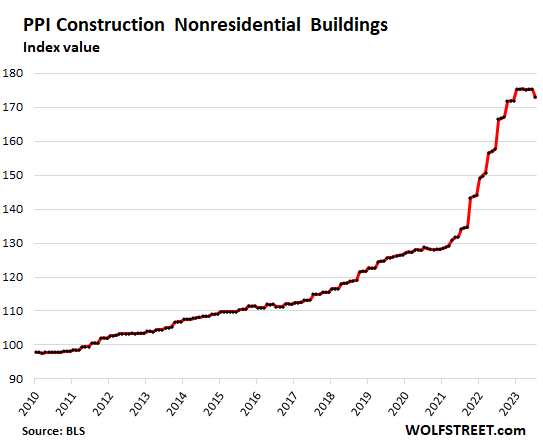

For example, over the same two-year period, the Producer Price Index (PPI) for nonresidential buildings surged by 29%.

But compared to the two-year 148% spike in spending for manufacturing plants over the two-year period, the 29% increase in the PPI would only explain a small portion. The rest is the surge in investment in US manufacturing plants.

Note how the PPI for nonresidential building construction began to flatten out in January 2023, with essentially no month-to-month increases through June, followed by a drop in July, which pulled down the year-over-year increase in July to 3.8%, the lowest since June 2021, from year-over-year increases in the 16% to 24% range in 2022:

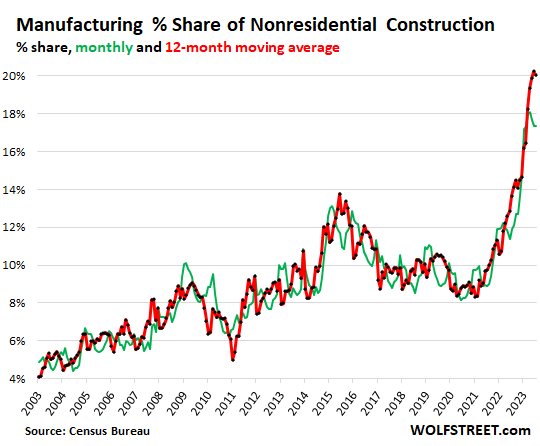

Factory construction spending’s share of total nonresidential construction spending has doubled over the past two years, from a share of 8.9% in July 2021, which was roughly in line with the years before the pandemic, to a share of 17.4% in July 2023. This highlights the surge of factory construction beyond the effects of rising construction costs.

When compared to the 12-month moving average of total nonresidential construction, the share of spending on manufacturing plants soared to 20%:

There are lots of reasons behind the renaissance in factory building. The initial surge started in the spring of 2021. Over a year later, in July 2022, with the surge well underway, Congresses passed a package of subsidies for select manufacturing industries, such as semiconductor makers (they get up to $52 billion). But construction spending doesn’t immediately happen. The government takes its time in doling out money for these kinds of projects. And the factories themselves take time in planning and permitting before construction can even start. So a portion of those subsidies for factory construction are likely to show up here in construction spending in the future.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great analysis. Thank you, Wolf!

what all this free money misses is chance for quid pro quo

make companies take % ‘unskilled’ engineers and train them into the new jobs

companies complain about skilled workers – well then TRAIN SOME on an ongoing basis

I agree with you, but the education industry lags. The community colleges have been on it, but the universities are the weak link. The college just down the road has “advanced manufacturing” degrees and has participated with Lawrence Livermore National Laboratory for preparing technicians for the NIF. The college over the hill has a degree in process engineering – just off the top of my head. They also have paid internships and apprenticeship programs. Where the universities should step in to continue the work they are out selling expensive garbage degrees and blaming every other part of society for their failure.

I wonder if the slack is from technical specialty colleges (IT, auto mechanics, etc.) and not so much community colleges. Anecdotally, I have observed (via my children’s academic path) that standard community colleges are saturated with students that are mired in “entitlement” thinking… few are serious. Don’t get me wrong this is not the case with “every” student.

Just a question really.

Correct re educ industry, especially the public ”highschool fools” that keep pushing most if not all students toward college instead of into trades and self employment.

After teaching at a comprehensive HS w 2800 kids and then a small ”continuation” HS aimed at ”drop outs”, etc., I found the small school MUCH more helpful at actually teaching kids what they NEED to succeed.

Maybe.

So, manufacturing is coming back to the US ?

The land with a reputation for demanding extreme pay that supports a middle class life style. Makes one suspicious of the motive that the demonstrably most rapacious business types are posturing as saviors rather than the representatives of a stateless economic units of production that operates in self interest, always.

Dang….gang it all! I’m not suspicious nor do I label business leaders as rapacious, or your definition of self interest. Any business owner is obviously self interest driven, motivated for their better being. Not all evil. Nor are folks who need assistance all free loaders. Lets keep to topic and facts. That is what makes this site valuable, and Wolf is self motivated. Great job!

I don’t care what Fed, Med, Powell and Mowell says, all I know is Arizona drinks at the gas station ate up from $1 to $1.69, that’s 69% inflation!

I’m quite certain my niece, who just started college, could not calculate that percentage in your example without asking Siri. So, well done!

I wonder if there is a simple, comprehensive list of all the industrial subsidies

passed over the last 3/4 years somewhere on the internet.

Growth is good, but it has to be measured against the subsidies…if it is mostly G money being spent, with little corporate skin in the game, the outcomes are likely to be worse. I’m pretty sure I’ve seen some G language requiring certain levels of corp co-investment.

Hopefully, those won’t be gamed.

And hopefully, the factories will come in on time, with useful products, at affordable prices.

We’ll see. Something needed to be done. It is just this is a country with a history of bridges to nowhere.

We’ll see.

Wolf,

Do you have any thoughts about the UAW strike and how this may play into the liquidity scenario for legacy automakers? If they are strapped on payments for factory expansion, the additional wages could be a real problem.

Interesting interview with the former Ford CEO talking about this– I would love to get your take on it.

Thinking the combo of expansion and union demands might finally get credit spreads moving.

One can hope anyway.

The additional wages – when they’re finally hashed out — are good for workers, and therefore are good for the economy, and they will be another injection of fuel into the inflation scenario. But for automakers (and their shareholders), it sucks. Unions will have to watch out that they don’t push automakers to shift more production to Mexico.

Wolf said: “The additional wages – when they’re finally hashed out — are good for workers, and therefore are good for the economy, and they will be another injection of fuel into the inflation scenario.”

———————————————————

I am not sure what “good for the economy” means in this context.

On this basis, it sounds like wage raises are good. Why not double, triple, or quintruple minimum wages?

I hate it when people do this shit. You cited the first sentence of my comment. READ THE SECOND SENTENCE OF MY COMMENT:

“But for automakers (and their shareholders), it sucks. Unions will have to watch out that they don’t push automakers to shift more production to Mexico.”

Why no increase by 100x!

What an incredibly smooth brained comment. “What does it mean good for the economy?” Means a larger share of the population will receive higher pay and thus spend it.

CB,

I think you would benefit from reading some foundational economics books.

Economics is the study of how to increase production of goods and services, how to best manage what is produced, and the distribution of the production.

This means that sometimes one group is benefited, and another is hurt.

I would start with Richard Cantillon’s study (available for free online) which was written in the 1700s. Arguably this is the first book written which addresses how economies actually work, even before Adam Smith’s Wealth of Nations. Start at the beginning with the absolute basics.

As far as the UAW strike, this is a classic “divide the pie” situation. Likely to be a zero sum game the way things are going.

If UAW is successful, then we should see far more strikes throughout the economy, which is what happened late 1960s and was one of the factors leading to 1970s inflation fiasco.

CB

Carmaker need to get their operations and ev development progressing and the skilled workers of UAW snd their training facilities will be integral to this need.

And not for nothing but the legacies got their bailouts and I don’t believe the workers saw their piece. It’s a smart and right move and UAW assemblers do not make all that much, among the least paid union workers when compared to other tradesmen.

And thank you Wolf.for another excellent article.

@ Bond Vigilante Wannabe –

I havn’t read Cantillon’s book, but I am familiar with the Cantillon effect.

I am always supect of “dividing the pie – zero sum situations”, of not turning out to be zero sum but merely a cog in the inflationary push favored by debtors and an indebted government, and detrimental to savers and non-priveledged workers and the majority of society.

I recommend you read the Economist Henry George, if you can find him.

@ CEM –

Not sure who your comment is aimed at or whether or not it is intended as sarcasm —

but if you are trying to make a serious point, it seems you would be a proponent of Modern Monetary Theory.

and wage or income increases of 1,000x

@ Blam 35-

The legacy bailouts were and are always disgusting. The whole “save the economy” 2008 forward bailouts have been disgusting and ruinous, partially summed up by this quote from Rudy Havenstein:

“Under Bush, Kashkari & Paulson, we gave Hank’s buddies 700 billion fungible dollars (in 2008 that was a big number), and they paid themselves billions in BONUSES.

Then Obama came in & appointed Wall Street lawyer Eric Holder to sweep it all under the rug. THAT is when we broke.”

Of course due to the thereafter money creation and resultant inflation, 700 billion now is almost chump chase.

But a question for you:

How much do UAW assemblers make?

It would interesting to learn more about how contemporary automakers divvy up actual auto production across countries.

Based on my limited knowledge, it looks to be a very international enterprise – engines made in one nation, transmissions made in another, and final assembly made in a third (the US?, to comply with domestic content (?) rules?).

(And why are engines/transmissions seemingly the key parts to be internationally sourced…versus anything else?)

I know these nations vary quite a bit by manufacturer and it must be a pretty complicated process (all that shuffling across borders) and that foreign exchange rate changes can really “throw a spanner in the works”.

Also, it is interesting that China has huge domestic auto production…but no Chinese cars are sold in the US.

“For informing consumers, the American Automobile Labeling Act of 1992 (AALA) considers a vehicle to be domestic if at least 85% of its parts originate in the U.S. or Canada; a part is counted as domestic if at least 70% of its content comes from the U.S. or Canada.”

“but no Chinese cars are sold in the US”

Buick, for one.

The Chinese brands have difficulty getting dealers to sign on because the dealers have been screwed over by their previous attempts to do business with the Chinese distributors.

Building distribution systems, parts networks, dealer networks takes a lot of capital. Plus, Chinese cars (for the most part) are not suitable for U.S. roads and have difficulty passing NHTSA crash tests.

“Chinese cars (for the most part) are not suitable for U.S. roads and have difficulty passing NHTSA crash tests.”

Hmm…pretty sure this has been said about every importer at one time or the other.

At one point, Hyundai was treated as an absolute joke…the 5 yr warranty ended the joking.

Also, I find it kinda hard to believe that tens of millions of Chinese are happily driving around in crap-mobile death-traps.

The other rationales (and political blockade) ring more true.

But it is hard to believe that Chinese cars won’t be coming to the US…absolutely everything else has.

There are already several China-made models running around the US, some for years, seem to be doing fine, including, Buicks, Volvos, Polestars, etc.

I agree with the great analysis,

We ordered last week, a GE washer made in Kentucky. To be delivered September 12th.

GE is now a subsidiary of Haier, a Chinese company. The profits flow to Qingdao, Shandong, China.

I’m curious who makes the automated robot/equipment for these factories too. China making the gear for the USA to build new factories so the USA is less dependent on China?

It’s like two two-headed and tailed snakes eating each others and their own tails.

I’m curious how this can continue to play out with both sides being “happy” participants.

No fears here. The largest robotics manufactures are European( Think ABB and Fanuc) or Japanese. (Think Mitsubishi and Kawasak).

Some years ago, a Chinese company bought KUKA, a top German robotics maker. This raised a huge ruckus at the time. But the Merkel government let it happen.

The word industrial robot can mean many things. The 6 Axis robot arms you see building cars and moving packages are almost all built in Germany and Japan ( Fanuc, Panasonic, OTC, Kuka- German built, Chinese owned). But many people think of the little buggies that move around parts and packages to and from automated warehouses. Those are also dominated by Japan ( Murata), but a few of the simple ones are now being built in the US with Japanese and German components inside.

I’d rather see American workers getting paid and profits flowing out of the country than the other way around.

This is an interesting point, but ultimately, aren’t owners the rulers?

It’s going to be an interesting play between globalism, onshoring, capitalism, corporatism, socialism, citizenship and ownership.

Where are free markets in all of this?

Who will the ultimate owners and rulers be?

Speed Queen

My dad worked for GE in Auburn Ny during the early 80’s making semi-conductors. He came home one night and said GE sold the plant to a Japanese Company. The plant closed a couple of years later after they sent all the equipment overseas. Plant was labeled a toxic waste dump just sits there an old skeleton of its self.

While Jack Welch no doubt made bank out of it, at least in the financial statements.

Sounds like a typical GE employee experience.

It’s jobs for ppl in Kentucky and I couldn’t care all that much where the shareholder lives.

Not really, though. Haier is just a majority owner (since 2016, according to Wikipedia), i.e., it doesn’t outright own GE – not even close, actually. Incidentally, you, or anyone else, can buy GE shares for less than Haier paid. That hasn’t been a great investment for Haier – they overpaid for their stake.

TEMPLE

My understanding is that Haier owns the rights to sell their goods with the GE label on them.

Well, I guess this would in part, explain our low unemployment in the USA.

Demographics work in the backround. Baby boomers like myself are working longer, but eventuall we die, This is from the Bureau of Labor Statistics:

“Because of the decreasing labor force participation rate of youths and the prime age group, the overall labor force participation rate is expected to decline. The participation rates of older workers are projected to increase, but remain significantly lower than those of the prime age group. A combination of a slower growth of the civilian noninstitutional population and falling participation rates will lower labor force growth to a projected 0.5 percent annually.”

Jeesus. Check the DATE when you Google around to search for stuff that fits your narrative. That was from 10 years ago. All the demographics have moved on by 10 years since then. The “youths” you cited have now fully moved into the labor force and have become the largest generation ever (millennials) to drive the prime-age labor participation rate to highest in 20 years:

Or at least read my articles (from Sep 1) before you post this outdated BS:

https://wolfstreet.com/2023/09/01/labor-market-sorts-out-the-distortions-from-the-pandemic-labor-force-spikes-wage-pressures-stuck-at-high-levels/

It was a BLS longterm projection of a .5 decresae going forward from 2022. Therefore it comes form the same sources that you rely upon.

I knew thre date was from 2022, that is not the long ago for a long term projection chart. I was quoting different variables on a different chart that they have in the article than your showing in your chart.

You must have seen the projection chart that the BLS had in the 2022 article? I am unanble to show display the chart like you, but I am just a messenger showing a legitamate chart data from the BLS that is not that old when looking at long term projections. It is good data. Lighten up.

More bullshit from you. The study was published in “December 2013”, and the projections in 2013 was “TO 2022,” and you still didn’t read the BLS article itself, even after I shot down your bullshit, but you only read the one paragraph Google search gave you, or else you would have seen the date of the BLS study, and not posted even more BS here.

Here is the actual study published December 2013, with projections “to 2022.”

https://www.bls.gov/opub/mlr/2013/article/labor-force-projections-to-2022-the-labor-force-participation-rate-continues-to-fall.htm

The dumbing down of America knows no bounds.

“The dumbing down of America knows no bounds.”

Sorry, don’t know if this applies but your response reminded me of the old George Carlin joke:

“Think of how stupid the average American is and then realize that half of them are stupider than that”

Implicit,

Needless to say I don’t anxiously await your comments like I used to.

Markin. Not to put to fine a point on it, which means I will, if half the population of a number is below it, that statistic must be the median, not the average. It could also be the average, but extremely unlikely.

Well, this should keep commodity prices high. Any thoughts on the energy costs moving forward? Manufacturing requires energy.

Right now the re-industrialization boomlet (and I can’t call it anything more than that) isn’t going to move the needle all that much for energy utilization because, while it involves *advanced* manufacturing – it does not involve heavy industry. At least not yet.

Speaking of re-industrialization and energy (electricity) use, I happened to take a look at kilowatt-hour costs by nation…and I’m guessing there is some amount of G subsidizing going on in some industrial foreign countries.

US average (for comparison) – 11 cents per kilowatt-hr (compared to Europe, *we* may be subsidized…)

Mexico .05 (! Why don’t we hear about this more?)

Vietnam .05

Taiwan .06 (small island!)

China .08 (hmm)

India .09 (hmm)

SK .13 (hmm – take a look at South Korea’s location/size)

Germany is at .32 – and yet (until very, very recently) they were an exporting, industrial powerhouse.

That rate for Mexico is deceptively low. Electricity is heavily subsidized for poor customers. Up to a certain tier of monthly usage, the KWh rate is very low, but at higher usage tiers it becomes very expensive. A lower-income household might pay a few dollars a month for electricity, but they are using very little. When I lived in Mexico electricity was our highest utility bill and was higher than in the United States. And we didn’t even have to heat or cool the house as the weather was temperate all year.

Corey – sidebar, same principles often apply to freshwater access here in the U.S. (…and, like electricity, often taken for granted…).

may we all find a better day.

I’d be careful about reading to much into your numbers – they lack context.

Some countries provide discounted electricity rates for heavy industry at the cost of somewhat-increased rates for residences. Are these effects incorporated in your figures?

BigAl et al (so to speak),

The numbers were from a fairly reputable internet source, but I can’t vouch for them incorporating all local complicating factors.

While some places may have some subsidies for the poor, I think most places have most subsidies/”volume discounts” for large industrial users. That’s definitely how it works in Texas (line between volume discount/subsidy can get very blurry) and I’d be surprised if Mexico and Taiwan weren’t operating under similar rules.

In any event, close examination of industrial electricity costs is probably warranted in any discussion of international competitiveness/subsidies. It takes a lot of electrons to bend steel.

The Rule of Thumb: An industrial “shed” used for manufacturing will have an energy demand near 10 times one used for warehousing / simple assembly.

The Opportunity: There’s a lot of roof space for solar PV – even allowing for 10% translucent sheeting for natural light.

[And irrespective of anyone’s views on carbon / green energy], the cost of energy from roof-top solar PV will typically be lower than grid energy.

[And before the “sun-doesn’t-always-shine” shills come out], it is an opportunity for partial substitution, not total replacement.

That 10x rule is interesting. Seems a little low – I would imagine that bending/shaping metal is much more energy intensive than simply fitting parts together (assembly)

It’s good news. And why not bring automation home to USA since manufacturing is headed in that direction?

It’s a crazy situation with China. U.S. retail probably buys 90% of their goods from China not including food items, we get our pharmaceuticals from China and etc etc. Meanwhile, Chinese warships circle Taiwan 24/7 and bully the South China Sea. Now China is making loans to Russia (or many more loans).

Based on your reporting, do you think the CHiPS Act funds are going to projects that likely would have been built any way?

Some of it for sure.

When you build a manufacturing plant, demand for everything else increases too — more office space, housing, lodging, water/sewer, communication, transportation, education, power etc. No wonder the anti-American sentiment is so bad in China right now …

Made in the USA, from 100% American made parts, design, ancillaries, isn’t quite the same as Assembled in the USA from Foreign (Chinese) Parts.

The core of America, the know-how private sector middle class was sold down the river.

Manufacturing swapped out for Financialization and Debt creation. A few winners, many forced losers.

No complex product, such as a modern motor vehicle, is “100%” made in any country. Supply chains are global for everyone, even Chinese companies, and it’s silly to demand that 100% of a modern complex vehicle is made in the US. That’s not happening anywhere, not even in China.

Historically U.S. assembled parts were nearly 100% made in the U.S.A.

The U.S./Canada Auto Pact required building 1 car in Canada for every car sold into Canada.

Managed Trade was and is far superior to “Free Trade” where a few Monopolies control supply in Foreign countries and markets in many countries, including the U.S.A.

“Historically”

LOL. “Historically” doesn’t matter. Historically, cars were simple POS. Historically, people got around just fine on foot, or with horses, oxen, donkeys, mules, camels, and elephants, all of which were made 100% locally.

Yes, it’s welcome news. But I caution people into reading too much into it.

As Wolf does point out – the growth is confined to a few sectors.

To get a fuller picture – I would advise readers to look at this data (which suggests that the factory boom is already playing itself out)

https://tradingeconomics.com/united-states/imports-of-capital-goods#:~:text=Imports%20of%20Capital%20Goods%20in%20the%20United%20States%20averaged%2037902.76,States%20Imports%20of%20Capital%20Goods.

and also read this piece:

Finally, I would remind people that overall PMI has been in contraction for about 10 months and the most recent PMI reading had truly lousy new orders readings.

Wolf, How do you think, will “construction spendings” continue to grow in 2024 and 2025? What is your forecast?

While this is undoubtedly good news and the creation of the factories creates jobs, what happens when the factories are built? Yes some will continue on as maintenance people, but not many.

Where are the jobs to pay the workers to buy the goods? Full automation needs land value tax and possibly a 4 day week.

They will have to pump up the salary to attract workers. Say 200-300K for an engineer, etc… Otherwise, the kids just prefer to be “influencers”.

Anyway, this “stimulus” will come with a cost. It will be interesting in the next 5-10 years. The whole world is gearing toward a greater conflict, pieces are being layout, some moves are already in motion.

Engineers working at at construction engineering firms are making bank. I know a couple that received 40% raises. They are making 140k 5 years out of college.

We are replacing domestic consumption with locally produced goods and services. It’s a transfer of employment, foreign labor replaced with domestic labor.

The construction phase is just the beginning, the better part is yet to materialize when the plants start producing and many new support jobs are created from the off-shoot of manufacturing revenues.

Automation is not an onshoring of manufacturing jobs.

Yes there are maintenance jobs and auxiliary jobs, but it wouldn’t be an efficiency win if as many auxiliary jobs are required as doing the same without automation.

I get your point, Georgist, but there does have to be some occupational adaptation to automation/occupational change.

Otherwise, there would have been subsidies to displaced buggy whip workers until…today.

The problem has been the barriers erected to occupational change (excessive educational/licensing requirements) in those occupations still demonstrating worker shortages.

I don’t know how (with millions and millions employed…) but health care industry wages still suggest worker shortages. Does every nursing job really require a BS in Nursing…or can more jobs be done by CNAs?

What happens when the factory is built? It needs raw materials delivered and properly prepped for the automated machines. It needs maintenance, as you stated above. It needs workers to move the product from one automated station to another, It needs workers to get the finished product out the door.

In short, even the most automated factories employ a lot of people directly, and also indirectly in the neighborhood.

There are about 13 million manufacturing jobs currently in the U.S. Hopefully, we can squeeze out a few more from over 300 million.

Fun fact: There are about 23 million government jobs. And there are about 23 million people who are Millionaires+. And they all work for the government :-) just kidding.

Modern automated factories employ highly skilled people, from skilled workers that do the manual portions of the assembly to engineers that run the systems. The old sweat-shop jobs have wandered off to Bangladesh, and no one wants them back. Manufacturing is hugely important for its secondary and tertiary effects.

The number of workers in a modern auto assembly plant is still huge. For example, at the Tesla plant in Freemont, CA, there are over 20,000 workers. Semiconductor plants have fewer people. But they’re all highly paid.

All these jobs are ADDED to the current workforce. These new jobs at the US plants replace jobs in China and elsewhere. If that plant gets built in China instead of the US, it’s a huge loss for the US, and we have seen that happening over the past decades.

So what’s the investment play in all this activity? Bechtel? Walbridge? Fluor (who also owns 25% of NuScale power, a SMR manufacturer)?

And the highly skilled workers supporting automated factories are paid 3-4 times in the US versus China, so we lose on costs there. However, the losses on labor are less overall given the fewer laborers needed, and maybe that makes up for shipping costs, etc.

But we gain on transportation costs, administrative costs, the costs of delays, and the immense costs of losing your IP when manufacturing in China.

How about the needed skills in the US labourpool ? Are there enough skilled folks out there or has the number of skilled enough folks declined and if this is the case, why ?

The best way to create this skilled labor pool is to create demand for it. That has always been this way. Demand for skilled labor creates skilled labor. This doesn’t happen overnight, but it happens plant by plant over time, and training is going to be a big part of it (always is).

The inverse is also true: a lot of skilled labor was lost when manufacturing walked off to China.

The job structure in the latest high end chip fabs is interesting. They are not your fathers auto factories. There are a goodly number of well paid jobs in constructing the factories and installing the tools.

Once up and running there are few production jobs for non-technical workers ( less than phd). The chips are moved around from process to process by a very sophisticated overhead guided vehicle system. The “tools” are mostly located in level 5 clean areas where humans can not go, even go with bunny suits.

Each “tool” is managed and overseen by at least one engineer or scientist. In most cases these are PHD’s in Chemistry, Physics, or Materials Science. These folks are mostly H1B’s from other countries as the US does not produce many PHD’s in these fields, that are willing to work for mediocre wages.

The largest number of jobs are for people who clean things. Most of these work for outside contractors like Clean Harbors. Once a fab is complete it has to be carefully cleaned 4 separate times from top to bottom, by hand with special rags in a mapped out grid pattern. Each of these cleaning stages can take months. Once it has reached it’s final level of cleanliness everything that enters the fab has to be specially cleaned and bagged from uniforms to spare parts. So in a lot of ways these fabs are like giant janitorial/laundry operations.

The best jobs are in the factories that make the “tools” that go in to the fabs, and the construction jobs building the fabs. But there are thousands of these and well worth having.

great post, very interesting

Don’t underestimate some plastics that are expensive to ship. Schluter recently built a new factory in Ontario to supply it’s NA distribution. Management told me they are saving approx $1M per month on shipping costs compared to the extra cost of importing from their plant in Germany.

Transportation costs play a huge role in re-shoring

I just built a tile shower with Schluter tile underlayment components. You would be correct as all the parts are large dimension, super light , high tech foam. That sort of stuff is super expensive to ship per dollar of value so it makes perfect sense that they set up a factory in North America.

Mark Stoneweapon,

I said “plastic toys” not plastics. The US has the largest petrochemical industry in the world that exports all kinds of materials.

I was differentiating plastic toys from re-shoring production of bulky plastic items, even large plastic garbage containers that hold so many plastic toys for our landfill, etc. You know how people can easily associate plastic toys with other plastics. The main point is the cost per pound, effected by rising transportation costs, tilts the efficiency of the location the product should be made, i.e., plastic playground equipment manufactured for most of our public parks is home based.

*cost per volume in this case.

Love to see value added manufacturing land in USA soil. A very limited positive for the incentives for USA government

I wonder how much of this construction is tied up with and controlled by the MIC, MY guess is that there’s no clear way to sort that out, but one might be able to identify a trend or two.

I’m sure a lot, especially semiconductors and chemicals, but a change in policy has to begin somewhere powerful. As the momentum builds, private capital needs to flow into production much more. I know a lot of people with net-worth over $10 million who are doing just fine with a 5% return because they already own real estate assets, autos, etc. At some point these generous low-risk returns need to be invested into domestic production if the private owners of their capital want to see the purchasing power of their money stabilized! I think the domestic circulation of capital is improving, but better returns should be made in local production. We are just in the beginning phase of re-shoring, but the complexity of doing this is to not break the global economy while reconciling the imbalances.

Mark Stoneweapon said: ” I know a lot of people with net-worth over $10 million who are doing just fine with a 5% return…”

———————————————-

$10 million and you do “just fine” ………………

tells you a lot about the value of the dollars

the purchasing power of the dollar has been obliterated.

Fortress America isn’t going to work. Way, way too late. We are not trying to break the global economy while reconciling the imbalances? Yeah, the world will be sitting still and waiting for us to take back what was ours. Suppression isn’t going to work against China or BRICS+. I would like to think that we are beginning the phase of competing in our best areas.

We are not at war. This is the US hegemonic empire maneuvering and posturing. An actual hot war with China or Russia would be catastrophic for the world. Please be mature enough to understand this difference.

I like your optimism, but I have enough gray hairs to be wary. Good luck.

” able to identify a trend or two”

Sure, easy to identify: there are no shipyards included, and no assembly plants for fighter jets and other aircraft, and no plants for armored vehicles and other military vehicles, no plants for munitions makers, etc. All this is handled via the defense budget, and they don’t need new plants, they already have the plants that they use to ramp up production if they want to.

Sure some chips are going to land in some components that go into military equipment. Chips go into everything, including your toaster.

The DOD led the charge on semiconductors, beginning with massive purchase orders in 2020. Vectors of control from the IC that set the stage and trend on the basis of NS are obscure to most people.

Minuscule in number compared to the semiconductors used in motor vehicles, consumer electronics, etc. (cars, laptops, smartphones, etc.) that get built by the millions and tens of millions and hundreds of millions a year. The consumer economy is a gazillion times larger than military procurement. It’s those products where semiconductor shortage cut production and created these massive historic shortages. Some of the semiconductor plants are being built specifically to address the shortages of semiconductors going into the components for automobiles.

It was plenty enough to disrupt the market, the catalyst and not go into DOD supply-chain funding initiatives and the politics of lock-downs and so on on your blog. We are at war.

Expansion of semi-conductor plants is just getting cranked up here in Oregon sparked by the Chips act. The local pipe fitters union is hiring another 300 apprentices and bringing in travelers to keep up with construction expected over the next few years.

I met a pipe fitter who just transferred up from Phoenix yesterday and he says weird stuff is going on with the TSMC plant in Arizona.

They are building it, but they are way behind because the Taiwanese don’t seem to want to spend the money to translate all the blueprints, specs and work instructions from Chinese in to English. They seem to be trying to construct it based on long emails and elaborate off-the-cuff notes. What TSMC really wants is to get special Visa’s to bring in 500 workers from Taiwan so they don’t have to put the $millions in to redoing all the plans, plus it will save them money on labor.

Wow, it sounds like some tug-a-war is going on to resist translating their trade secrets in English to maintain some dependency on their expertise — less to do with $millions I’m sure.

Gregory Allen wrote a detailed article for CSIS last May worth reading, titled “China’s New Strategy for Waging the Microchip Tech War”

October 7, 2022, export control regulations targeting China’s AI and semiconductor industries was a “Watershed Moment” in US-China relations.

Construction spending in Manufacturing increased from $120B to $201B since then.

Basically, we started a chip war that had not only choke points for China but also for us. We are frantically trying to build more FABs to produce the “lower” end chips so not to rely on China. Most chips don’t have to be high end, that is why we are stuck w/out supply for our cars etc… for the past few years. That is also why we are constraint for a few more years until some FABs are up and running. All this will be added cost to the whole supply chain. China on the other end is trying hard to catch up some key technology such as photolithography from ASML. The recent announcement of Huawei’s newest phone is really a shock to most experts. China might not be at 3-5nm node but they are getting closer and probably at 7nm. Depending on yield, we won’t know how far they progressed.

We are living in a bi-polar world. Our country is in a bi-polar political crisis. What China don’t have is our political garbage.

Try treading the SCMP for a few months Z, and you will see that

“What China don’t have is our political garbage.”

is not only not true, but it’s very likely that their garbage of that sort is much worse though better hidden at times.

Ha that last comment is priceless- they don’t have our political garbage-indeed they don’t. They have a massive top down system that leads to tremendous paralysis and inability to make decisions beyond the rulers. In short, they have a very quietly inefficient system nobody can complain about. Is this better? Only if you like the silence of the grave.

The beginning of a long term trend of increasing manufacturing in America. It’s good to see. Besides for the manufacturing plants themselves it also creates lots of ancillary jobs.

Howdy Folks. Really great article and hope its all true. Love this country, but really love the way it used to be. Got to this quote from the article,,,,

“Congresses passed a package of subsidies for select manufacturing industries “.

Oh well………

Subsidies for corporate America are as old as Congress itself. Nothing new here.

Howdy, YEP and yes sir. Only gotten bigger and bigger picking the winners and losers……

LOL … Government is in thrall to corporations, which are protected and funded by the state. All the externalized costs and consequences of the pillage of the planet and populace are transferred to the state while the profits are of course private or state owned (SOE’s) in China’s case and China’s subsidies aren’t small either.

The days of manufacturing, even high tech manufacturing, being a substantial driver of growth…are nearing an end.

The world economy is living on borrowed time with respect to cheap fossil fuel depletion. The next two decade will be pivotal. High tech will be first to bite the dust.

Weve already hit peak crude, which is cheapest. Prices of fossil fuels likely wont rise much higher since we are already using the expensive ones like tar sands. Theres enough of that in canada to last well past even the slowest conversion to renewables. Solar and wind are already so cheap and likely to continue to plummet in cost. We are likely past the worst energy shocks related to peak fossil fuels. The real issue is avoiding the repercussions of dumping gigatons of carbon into the atmosphere every year, regardless of if people think theres an impact. Facts dont care about feelings and all.

Herpderp,

Tar sands are very expensive to process and require prodigious amounts of water whether you are talking about SAGD, VAPEX or THAI.

That stuff produces *extremely heavy* crude oil.

The irony of your last sentence.

Wolf,

Wondering if you have any thoughts on when the bond market is going to have its “tipping point” and realize no recession is around the corner and zero rates ain’t coming back anytime soon.

Since yields are a function of economic growth, inflation, liquidity and tax rates, if economic growth is going to be this strong, rates have to go up.

The bond market bulls have been clamoring about growth and inflation down because recession, return to ZIRP, blah blah blah.

With labor participation up as fast as it is, the recent spike in unemployment means nothing, meaning no pivot. Even the uptick in unemployment is likely temporary because year end holiday season hiring will probably mop up the unemployed.

I would have expected the bond market to wake up by now, no luck.

Re: “Industrial robots cost the same in the US as in China”

Bingo.

That’s at the core of AI and turning everything upside down, like automating the entire mortgage industry, global banking and the entire spectrum of investments.

The head scratcher here, is what happens to all the people being displaced by the AI Blitzkrieg, who don’t become self employed AI entrepreneurs?

That kinda reminds me of something Peter Lynch said about how, in order for Avon to achieve its EPS forecast, all the Avon ladies would need to sell all their products to the “other” Avon ladies.

In the case of booming factory spending, that’s reminiscent of the current government stimulus spending, encouraging growth in a weak economy. It’s great while it lasts, but it’s definitely not sustainable — somewhat reminiscent of China building ghost cities.

The growth narrative is exciting, but somebody has to pay for it …

Not entirely. Initial capital cost maybe but Industrial robots require energy and maintenance. Cost can still be significantly different not to mention permitting, environmental and safety regulation differences from country to country.

They do help equalize, but the costs aren’t “the same”

Bidenomics. Next year will be a good year for him with those continuing subsidies.

Where can I find the raw data from which first graph is generated? Thanks. Great article!

On the Census Bureau website. Find construction spending and download the specific data set you want.

The five year plan succeeds at factory construction, Stalin would be very proud ……..mission impossible……the fed lowering inflation while oil prices explode.

Why is the US building more factories when orders are falling?

MW: U.S. factory orders down 2.1% in July vs. consensus of 2.3% fall

LOL. Orders fell in July by less than they had SPIKED in June, only partially undoing the gain in June and are still higher than in May or any prior month this year. This is very volatile data, jump up and down a lot from month to month. June was the second highest ever.

You should have disclosed the whole title from MW: “U.S. factory orders plunge in July after four straight gains” — and it undid only part of the last month of the four months of gains.

Folks knew that after the June SPIKE, there’d be a month-to-month decline in July, but the decline was less than expected.

I know you enjoy spreading clickbait headlines, and that you actually never read anything. But it helps to look a chart from time to time, before spreading context-less BS.

MarkinSF wrote:

> Sorry, don’t know if this applies but your response

> reminded me of the old George Carlin joke:

> “Think of how stupid the average American is and then

> realize that half of them are stupider than that”

George Carlin did not tell “jokes” he told the “truth” (things the people running the country still don’t want us to hear):

“Most people work just hard enough not to get fired and get paid just enough money not to quit.”

“Don’t just teach your children to read. Teach them to question what they read. Teach them to question everything.”

“The IQ and the life expectancy of the average American recently passed each other in opposite directions.”

My personal GC fave is: “It’s a big club and you ain’t in it”.

I guess that most future jobs then, will go to the robot repair man/woman….

MW: This hadn’t happened on the U.S. Treasury market in 250 years. Now it has.

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Duh, it’s the end of the 40-year-long bond bull-market. What do they expect? That it suddenly doesn’t end?

Congratulations, Wolf. Yet another megabull article covering the main street economy. Yet the financialization economy MSM considers you a bear!

The lead time for large electrical equipment (gear) is still very long: a year from placing the order. You can shorten this a little bit by prepurchasing the gear (prior to bid/pricing) but not all that much. Add into the mix the long planning/development time on this type of project and you can see why they are often late business cycle type projects.

As an aside, I suspect (much like large government/institutional) that you need to get out of the last downturn long enough to feel confident about your cash flows/bonding before you initiate the project.

The problem with reading too much into the “late cycle” idea is that Covid and the earlier 2008 bust (which didn’t hit large construction until 2010) have probably made a mess of the normal timing.

@russell1200,

Yes. This is a point I keep making.

Really sophisticated capital goods have long lead times in which a very large portion (sometimes 100%) of the overall cost must be paid up front as a deposit.

The USA is not anywhere self-sufficient in these goods.

So when I see charts that look like this..

https://tradingeconomics.com/united-states/imports-of-capital-goods

and somebody pronounces a “factory boom” – I get very skeptical. Notice the tapering off since Q4 of last year? About the time the PMI data started feeling poorly.

And that’s before we factor in that the capital goods for the factories that are being announced are *extremely* expensive. A handful of announced semiconductor fabs – which, as I say, require extremely-high upfront spending – should have sent this chart to the moon. That it hasn’t suggests that manufacturing – outside of the sectors covered by Wolf here – is not doing well.

Well, one-sided… The US is a big EXPORTER of capital goods, and US exports of Capital goods have shot up to a new record, even as imports of capital goods (your link) have plunged:

https://tradingeconomics.com/united-states/exports-of-capital-goods

So now your whole theory is kaput.

@Wolf,

I do like a worthy adversary!

But if you’ll permit me the luxury of a response…

I don’t think it’s kaput at all. Here is why:

a) Remember that US Capital Goods exports include oil and natural gas. Obviously, overseas demand for US exports there is very healthy.

b) The *specific* areas of interest in Capital Goods exports would be items like “Non-electrical machinery” and “Advanced Technology Products”. If you look at the trends for those in the past couple years – they would tend to support my theory.

“Remember that US Capital Goods exports include oil and natural gas.”

No, oil and natural gas are NOT in capital goods, they’re in “Industrial Supplies.” Another argument that went kaput. You’re completely off.

Just look this stuff up. For example here:

https://www.census.gov/foreign-trade/Press-Release/current_press_release/index.html

Seventh link down in the first segment “Seasonally Adjusted (by Commodity/Service)”

Included in “Capital Goods except automotive” (automotive is a separate category:

Drilling & oilfield equipment

Telecommunications equipment

Civilian aircraft engines

Civilian aircraft parts

Nonfarm tractors and parts

Civilian aircraft

Materials handling equipment

Medical equipment

Industrial engines

Generators, accessories

Marine engines, parts

Business machines and equipment

Metalworking machine tools

Railway transportation equipment

Spacecraft, excluding military

Wood, glass, plastic

Food, tobacco machinery

Commercial vessels, other

Textile, sewing machines

Vessels, excluding scrap

Electric apparatus

Specialized mining

Pulp and paper machinery

Laboratory testing instruments

Photo, service industry machinery

Computers

Agricultural machinery, equipment

Excavating machinery

Measuring, testing, control instruments

Computer accessories

Semiconductors

Other industrial machinery