Interest income is a big number that got a lot bigger, and people are spending some of it.

By Wolf Richter for WOLF STREET.

Interest income to households is surging, fueled by 5% money-market funds, 5.2% CDs and Treasury bills, 4.5% savings accounts, and other fixed-income products that people have invested many trillions of dollars in. Those rates are now producing a significant increase in cash flow to those households – and many are spending this extra cash, especially retirees that have gotten bludgeoned by the Fed’s interest-rate repression over the prior 15 years.

But interest payments that consumers are making on their mortgages and consumer loans are going up. And they also make a difference. We want to see to what extent higher interest rates on net (interest income minus interest payments) have cut into overall consumer income. Turns out, they barely have – which could be one of the reasons consumer spending has remained surprisingly strong, and why core inflation is so sticky.

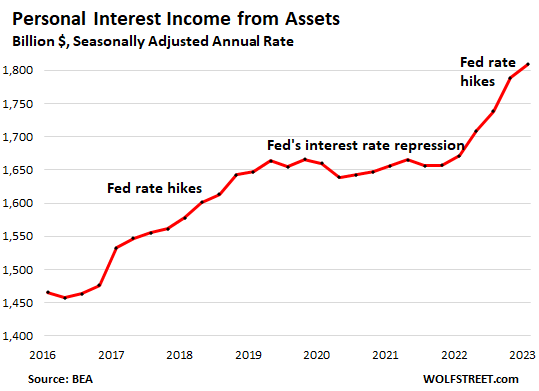

Interest income earned by consumers from their assets jumped by a seasonally adjusted annual rate of $152 billion since the Fed started hiking interest rates, and by Q1 reached a seasonally adjusted annual rate of $1.81 trillion, according to data from the Bureau of Economic Analysis:

You can see the stagnating interest income from Q3 2019 through Q4 2021, when the Fed repressed short-term rates to eventually 0%. And you can see the increase in interest income from Q1 2017 to Q2 2019, during the Fed’s prior rate-hike cycle.

Two different groups of people, with some overlap. People who earn interest income overlap partially with the people who make interest payments.

For example, many people financed or refinanced their home back when mortgage rates were around 3% even if they could pay cash for it. Those 3% mortgages are still out there in massive numbers. Many of these people also have assets that now produce interest income.

There are other people who now borrow to finance a home and/or a car, and some also owe some interest-bearing amount on their credit cards, HELOCs, personal loans, etc. And many of these people don’t have significant interest-bearing assets or else they would have paid off their most expensive debts first, such as their credit cards.

So we’re talking about two different groups of people here, and those two groups overlap to some extent. But in terms of the overall economy, it doesn’t matter how it splits up since we’re looking at overall income, overall interest payments, overall demand, and overall inflation.

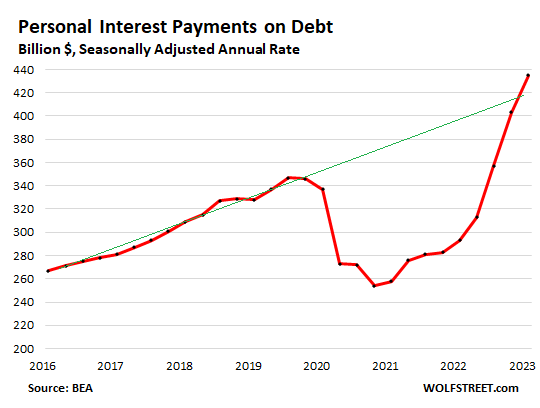

Personal interest payments also jumped by $152 billion seasonally adjusted annual rate since the Fed started hiking interest rates, and by Q1 reached a seasonally adjusted annual rate of $435 billion.

We note once again with our pandemic-special forever-bedazzled grin how the pandemic-era’s mortgage forbearance, still ongoing student-loan forbearance, and the free money that people used to pay down their credit cards have created a historic plunge in interest payments. That plunge started reversing in 2022 and has how shot above the multi-year trend line:

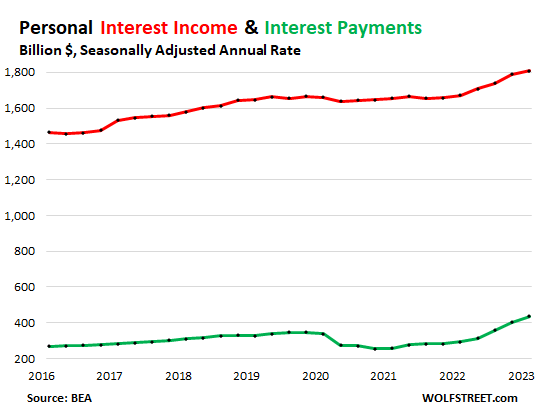

But interest income is always much higher than interest payments. Roughly one-third of households own their home free and clear and have no interest payments associated with their home. Over one-third of households are renters. Many of them are renters of choice,” as they’re called, that live in higher-end houses, rented condos, and higher-end apartment buildings, and many of them have plenty of assets and no debt. Then there is a smaller portion of the population that is up to their ears in debt.

So here on the same chart are interest income (red) and interest payments (green), for a sense of relative proportion. Both of them went up by the same dollar amount ($152 billion annual rate) since the start of the rate hikes.

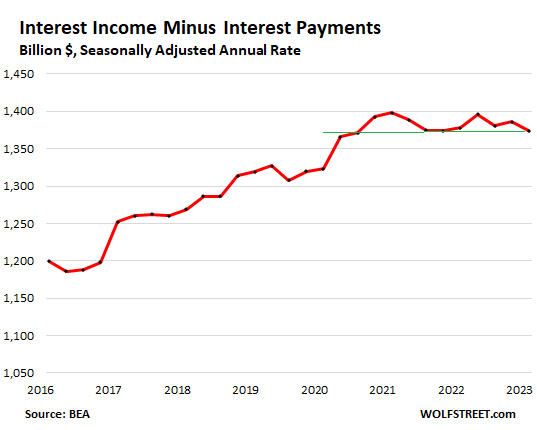

So, the net of interest income minus interest expense is roughly unchanged since the Fed began hiking rates, at $1.37 trillion annual rate – meaning that consumers earned $1.37 trillion annual rate more in Q1 in interest income than they made in interest payments. And this net difference hasn’t changed much since the end of 2021:

For people who have no debt but have interest-earning assets, the rate hikes just produce higher income, and they’re loving it, and many of them are spending some of it.

For people who have a 3% fixed-rate mortgage and no other debt, and are not in the market for a car, they won’t feel the higher rates either; and if they have fixed income assets, they’re getting higher incomes from them – interest income whose rates now exceed their mortgage rate!

But people who now want to buy a home or a car will face much higher interest payments, and that’s where the brunt of the rate hikes hits, and that’s the angle where rate hikes push down demand because fewer people will buy houses and cars and other stuff that they fund with borrowed money.

Chipping away at this reduction in demand is the portion of increased interest income that people are now spending that they wouldn’t have spent otherwise. Retirees are a big player in this category.

A retiree with $200,000 in T-bills or CDs or money market funds now earns $10,000 more per year than two years ago, and many retirees, after getting bludgeoned for years by the Fed’s interest rate repression, are loving it and are spending a big part of that income. That’s quite a bit of extra demand now washing over the economy.

But as more people buy homes and cars with 7% debt, interest payments will spiral higher, and they will have less money to spend on other stuff. At the same time, interest income growth will begin to slow as rates stabilize. So eventually, the downward pressure on demand from higher rates will become more noticeable. But not yet.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

One can make money in risk-free 5% CD. And one can make make money in Nvidia stock going from $250M to $1 Trillion in under 10 months. It’s the best of both worlds.

One can make money when Nvidia goes back to $400 billion, you forgot to say? It already gave up the first $50 billion.

Right you are. Still some momentum left in the big 5. Can’t possibly last too long. Small caps spiked the last time right before the top was in (already started). Vix collapsed. Feels like good time to start with the puts again.

If you look at a long term VIX Chart, when the VIX has bottomed under 10………It take a few years before the stock market enters another huge Bear Market.

This time could be different ? Rates are moving higher, faster than any other time in history.

A Black Swan could arise from China/Taiwan, Climate Change, Ukraine, or something ?

This time we are in one of the “great bubbles”. And it already cracked. Also, the way Vix is structured, it is the amplitude that is important. Try reading a sine wave on a long chart.

sorry wolf

not 5% risk free

forgot to pay tax man

You always have to pay the taxman, even when you make money in stocks, LOL

With Treasuries, you don’t need to pay to state taxman, though.

some people don’t realize that the interest they’re getting currently doesn’t even maintain their money’s purchasing power after taxes.

You always hear that line everywhere from people without a lot of cash. My income more than doubled in one year thanks to rising interest rates. The workers pay didn’t double in one year.

It’s incredible to me that people don’t understand if you’re earning 5 percent that gets taxed as ordinary income when inflation is 6 percent, you’re actually losing money in real terms. You need to find assets (stocks, real estate) that actually protect you from inflation.

What is all this exasperating nonsense?

The purchasing power of stocks and real estate and bonds and cryptos also declines with inflation.

Why is it that people always single out 5% CDs but never stocks or real estate when it comes to losses due to inflation. What kind of Wall Street propaganda BS are you all posting here?

With stocks and real estate you have the risk of capital losses IN ADDITION to inflation.

S&P 500 is down 11% from peak, Nasdaq is down 18% from peak, IN ADDITION to having lost value to inflation. Why don’t you point out that DOUBLE LOSS?

Yup, they’re losing more today at ~ 4-5% ROI than they were when inflation was at ~ 1-2% making nothing in interest/ROI.

Spending it isn’t a great idea right now. Then again if they’re drawing down to live off it any way… may as well front-load the spending given inflation.

More forcings causing a spike into a subsequent tightening.

It does for me. But I’m out of the market for highly inflationary products: rent, autos, eating out at fancy restaurants, and in the market for deflationary products: gas, golf & cooking at home. But everyone gets to choose their own lifestyle.

I think many people *do* get that the 5% interest is taxed and the inflation rate is higher. However, it is relatively RISK FREE and the return is juicy vs. .01% and 2% inflation. Keep in mind that during the times of 2% inflation, big ticket items were climbing rapidly… as was medical cost and pharma… but there was near zero return for those who are savers and don’t have the stomach for the Wall Street Casino.

We have a bit that is earning 5%+. It’s adding significantly to our monthly income. We only spend from our income stream, never from savings. So… while not out buying Lamborghini’s and Gulfstream V’s, we are upgrading things that make our life more enjoyable/comfortable. We’re not sloppy with it, but we also aren’t agonizing over things like upgrading well worn linens.

You can both spend and be frugal. Lost purchasing power is not absolute as you don’t replace or purchase everything in the basket of goods simultaneously nor monthly. Some of it is discretionary. And prices of certain items rise and fall (witness autos and RE in certain markets). As Wolf has pointed out, it’s services that are now going berserk. Also, a lot of it is age dependent.

As has been driven into my noggin by recent family events, there is not much purpose to continual savings and wealth growth if you’re in a pine box or have lost physical or mental acuity with a life that has been reduced to watching Gunsmoke reruns between naps.

If I were younger and had a young family, my perspective would likely be different. But I’m not and I don’t.

Wolf is spot on….

Yes. Real (inflation adjusted) interest rates are about zero. People spending there nominal (but not real) interest are actually spending their principal.

I never take financial advice from people who don’t know the difference between “there” and “their”.

Richard y

I’m one of those people who don’t spend a penny of the interest on our deposits. My wife and I get by on the salaries we get. We only buy promotions so our food costs are the same as they were 2, 3 years ago. The only thing we can’t avoid as an increase is utility and fuel prices. We go on excursions by choosing such prices that we have been paying for the previous 4 years. What is increasing is our savings thanks to higher interest rates. For now, that’s fine with us. And when property prices drop to normal levels, we can buy another property

We hope high interest rates stay high for a long time.

Richard W:

So what’s the “real” return on real estate after expenses and taxes? Or stocks? Or commodities? Gold? Silver?

The values are all eroded by inflation. It’s not that one is insulated from it and the others are not.

I’m w/ the calling BS crowd.

Example:

Real estate isn’t going up.

RE: $500k and will remain and/or decline.

That same $500k will INCREASE by 5% per year compounding.

I can buy a house cheaper by waiting 3 years.

As for STONKS go up crowd… Dividend stonks paying like 3.5% in my ETFs.

5% risk free beats that 3.5% and if I re-invest my bond it “grows.” Dividends also get taxed btw (at a lower rate).

If you’re high tax VTEB (Muni bonds) pays 3.45% tax free. VTES pays 3% on short term Munis.

Ignore AI hype. Buy bonds.

T-Bills pay the bills.

Wallstreet propaganda!

I told everyone on every blog, the newsgroups, everything to buy Nvidia back in 2015 when it was 20 dollars. This was just before the launch of 4K TV sets.

Tony, that was excellent adivise to buy Nvida in 2015.

Please share your advise for 2023.

Buy Tech or Run for the Hills ?

My Crystal Ball never worked.

This exercise by Wolf might be another argument for why raising interest rates to cool demand/inflation was not the right prescription. The better mechanism would have been to liquidate the balance sheet and deflate the bubbles.

But that would have hit the rich harder than the poor and we know the Fed and the permanent government overlords only care about the rich.

Rate hikes were necessary but aren’t enough just yet (this impacts the short-term rates).

But yes, the trillions of dollars that the Fed printed are circulating and will continue to fuel inflation, as will the huge government deficits. The Fed should definitely speed up QT, and the government needs to reduce the deficits. Both of those would help a lot in getting inflation down.

Too late for QT as a tool. Inflation is already entrenched. The Fed totally missed the boat on that one. How long can the Fed continue QT at its current pace before they have to start QE again? You did the analysis for minimum Fed balance sheet about a year ago. It would be nice to see that analysis again with all the new doodads the Fed has tacked on, like the BTFP.

PS It would be a bonus to see that information with and without the MBS component, since MBS is such a difficult monster for the Fed to deal with.

Shelter that 5% CD in a Roth IRA. Screw the tax man.

Robert (QSLV)

Spending interest earned is spending your savings, since interest is still below the rate of inflation (for most) and especially so after tax.

:-(

You don’t understand retirement. What else are you going to do with it. Take it with you?

It beats making 0% when inflation was 3%, which was the case before 2017.

In terms of inflation: it screws everything. Your stocks that are down 11% from the peak (S&P 500) or 18% from the peak (Nasdaq) also got hit by inflation, and in reality after inflation, they’re down a lot more.

And they’re subject income taxes if you make money on them and sell them. No escaping that 🤣🥂

just trying to stay above float

TI is expensive and needs to be saved for

gotta pay annual grift to local govt

Right O Mr. Wolf. The country song about ever seeing a Hearst with a trailer hitch. Unsure how many people are in my category, but, this retired couple is spending.

One needs to consider their life expectancy and the size of their earning assets to know how much they might spend without risking running out of money before they pass onwards.

I can only live frugally (for my current level of assets owned) and hope my stocks recover. Long term holdings will likely follow the historical performance record.

Right now we are losing money due to the effects of inflation in many asset classes.

Sure, Wolf, it might make sense for retirees to draw down their principal. That doesn’t alter the fact that’s that what they are doing, and it’s wise for them to be aware of what they are doing, so they understand the risks.

Personally, I’m investing in stocks with healthy dividends,

and hoping to live off just the dividends, so however long I live I’ll have a nest egg left for end of life care if I need it. It remains to be seen whether I’ll succeed.

The purchasing power of stocks and real estate and bonds and cryptos also declines with inflation.

Why is that people always single out 5% CDs and T-bills but never stocks or real estate when it comes to losses due to inflation. What kind of Wall Street propaganda is this?

With stocks and real estate you have the risk of capital losses IN ADDITION to inflation.

S&P 500 is down 11% from peak, Nasdaq is down 18% from peak, IN ADDITION to having lost value to inflation. Why don’t you point out that DOUBLE LOSS?

Agree. Retirement requires switch from saving to spending. Example, We retired late 2015 traveled 6 to 9 months each year and returned March 2020. Our 2 million savings increased one million dollars in 5 years with 30S/60B/10C. Off to Hawaii again for 2 or 3 months of scuba this fall and early winter. Alternative cancer treatments 160k out of pocket in 2021. Enjoy every day !

Yes this is the point. For those of us in the accumulation phase who are young and working and don’t have piles of cash accumulated over a life of working and the last 12 year bull run (or longer), it’s not enough to get a true -3 percent return so HYSA’s and CD’s and money market funds aren’t exciting. If you want to get ahead you have to be in the markets or in real estate and be crushing it in your career.

This is an unlikely scenario and possibly represents choosing a time frame starting at the depths of the pandemic-associated stock crash.

My 80% equity portfolio has possibly increased 40-50 % since the lows, but I prefer a longer time horizon or one where we do not start at the lows of a recession

Sam:

Go read the fable of the tortoise and the hare.

However, we started saving for retirement when we were 23. Lived on one income when we had two. We never spent a bonus, but invested it. And, when career advancement happened, we never adjusted our lifestyle to that of the rich and famous. My wife retired when our first kid was born. The tax hit, childcare expense, and cost of commuting didn’t pencil.

Our financial progress didn’t make good cocktail party chatter, but we’re in a really good position by going slow and steady. I have friends that chose their spouse poorly, gave up half in a divorce, paid child support, then got their brains blown out in 2008 and never recovered.

@El Katz

Agreed about the “cocktail party chatter” point on saving consistently and starting early. The tortoise approach to the race was not exciting but it did win – in the long run.

This was documented extensively by Thomas Stanley in the “Millionaire Next Door” books. One common theme Stanley found as he studied and interviewed people in those households: they spent less than they earned.

The problem, as you well know, is such behavior does not make for good clickbait headlines. It is not fast, it is not sexy and it involves long term hard work and commitment.

I suppose that is part of the reason why “get rich quick” scams continue to proliferate. It seems there will always be a population of people who believe becoming wealthy involves a “secret” of some sort.

Another thing to consider. For us retirees drawing SS, we have gotten large raises in the last two years. Between my wife’s account and mine we receive about $500 a month more than we did 3 years ago. So seniors have a little more spend or save every month.

But then my property taxes went up $1200 ,so we lost money again

“You don’t understand retirement. What else are you going to do with it. Take it with you?

It beats making 0% when inflation was 3%, which was the case before 2017.

In terms of inflation: it screws everything. Your stocks that are down 11% from the peak (S&P 500) or 18% from the peak (Nasdaq) also got hit by inflation, and in reality after inflation, they’re down a lot more.

And they’re subject income taxes if you make money on them and sell them. No escaping that 🤣🥂”

HA! I do understand retirement, I’m sort of technically in it.

It gets worse than having to pay taxes on those stocks. As you know, you have to pay taxes on “gains” even if they are only nominal, and negative on a real basis. Same as any other sale of an asset. Brutal!!

“Long term” capital gains tax is 0% for less than $83,350 when married so that is completely free money each year. Definitely nothing to sneeze at when you own home and auto free and clear.

Gatto,

A lot of us peons can reduce our taxes in retirement if you start planning for retirement early. I have done ok on it, but made some mistakes.

Multiple accounts like 401ks, IRAs, Roths and regular after tax accounts allow you to have flexibility as the politicians change the tax game.

There are some nuggets in the tax code too that rich people have gotten put in place that can help the average guy as well. I know a few, but I am sure there are many more.

I think the bottom line is if you are facing a huge tax bill, it probably pays to see a tax attorney who might be able to rescue you for a big fee.

Speaking of taxes drunkenmiller interview stated ,either entitlements Godwin 40% or taxes go up 40% . Me thinks uncle will do both .Except for tax exemptions for top 1%

Since the net of interest income over interest payments hasn’t changed since this rate increase cycle began, it is no wonder that rate increases so far haven’t slowed the real economy and that Wall Street is in party mode again. However, trend lines indicate that the net may begin to decline, which may be one reason the Fed wants to skip or pause. The problem is that inflation becomes a little more entrenched with each passing month as the Fed tiptoes to a neutral rate.

One thing that is different from rate hiking cycles prior to 2008 is that the Fed is now paying interest in order to support the lower bound of its target range. These payments rise as its rate targets rise, potentially helping to explain why rate hikes have thus far been less potent than one might have expected based on historical precedent.

The insanity of tightening by paying more interest instead of unloading the illegally acquired assets- MBS & QE. Just dump those on the market, no more wealth effect which is artificial by Fed put anyway, deflation incoming, mission accomplished!

Interest income, excluding munis, is generally taxed. Interest expense, except for mortgage interest below the cap, is not deductible.

Therefor equal growth will be a negative after taxes.

Yeah, but the same applies to any taxable investment….. including real estate profit over the $250K individual exclusion, stocks, dividends, commodities… they even came after your ability to sell grandma’s silverware by taxing 1099 income. There is nowhere to hide from taxes.

It’s all the same…. the difference is the risk associated with it. The 5% (for me) is significant in terms of real dollars, even if they are taxed and I am pushed into a higher monthly Medicare cost bracket. I ran a tax estimate for 2023 – considering all additional costs – and I’m still well into 5 figures to the good and have zero panic attacks with market fluctuations.

As an aside, I saw an article about people getting calls to fund their escrow accounts or increase their monthlies because the amount being sent to the bank from their regular mortgage payment (PITI) is insufficient due to the combination of rising insurance premiums and increased tax assessments. Ya gotta wonder how this might manifest itself in the economy as more money is removed from household budgets…..

El Katz said:

“There is nowhere to hide from taxes.”

Hilarious quote.

In 2011 Jeff Bezo’s received a $4,000 tax credit. He was with 18 Billion.

“Bezos paid no taxes because most of his wealth came from company stock, which isn’t taxed until it’s sold.”

Many uber rich pay no taxes or approaching 0%.

Even poor’s like us can: Max 401k, Roth, HSA, 529, bunch charitable contributions, tax loss harvest, depreciate rental RE, Muni Bonds, ECT.

On phone. With should read “worth.”

The other impact is on entities other than households. This includes government (at all levels) and corporate. The US is also a net external debtor meaning some of these increased payments are paid to non-US entities.

As usual, the talented Mr. Frost for the win.

1) It would be *very* interesting to see similar “two sided” analyses of rising rates for the corporate and gvt sectors. As usual, I am volunteering Wolf for a ton of uncompensated additional work. But it would be valuable!!

The close-to-net-zero result for individuals sorta-makes sense in a very broad, very very rough way…for everybody paying more in interest, somebody (or some entity) is getting more interest. This of course ignores cross-sector (indiv, gvt, corp) and cross-border flows.

Very approx net zero results maybe shouldn’t surprise for macro-measures…when you measure the theoretical totality, numbers tend to have to offset.

2) But…this also smacks a bit of the financial-engineer, MMT’er magic-bunny-out-of-a-…-up-from-his-bootstraps world view. Accounting type concepts are *designed* to balance out…but I don’t know that real-asset-economics is as sanguine.

For one, we’re measuring things here in internationally/real value deteriorating USD…it really doesn’t say anything good about increases in US productive efficiency – which is what matters in the end, not Fed-arbitrary stacks-of-greenbacks (of which I talk smack).

Perhaps that reality might be best captured in the net-interest-payment results for corporations…which have to output *goods/services* in order to increase revenues (my guess is that a pretty small % of non-financial corp revenue is interest income…whereas a *ton* of interest payments leave corps).

Again, I think looking at things from a purely financial-measure perspective (vs. say unit-output) might be dangerously misleading because financial measures tend to look balanced until the cascade collapses start.

Whereas unit output/unit consumed measures (say, autos) might give much, more warning that US quality of life is collapsing.

(I know unit-output measures are much harder to find/aggregate than financial measures. It would be amazing if there were some well-designed unit-output/unit-consumed aggregate measure were out there (analogous-but-superior to financial GDP).

Speaking of unit-output…I don’t know if collapsing birth-rates in the US (among child-bearing age cohorts) speaks well for actual US economic “growth”.

Beaten-down people don’t have kids.

“For people who…are not in the market for a car…”

Not being in the market for a car is a key financial solvency. My “new” vehicle is almost 22 years old. (The old one is 50.) Two weeks ago, I was told that my 2002 Yukon Denali, which has been experiencing random misfires all year that my (former) mechanic could not seem to fix for long, would need a new engine or need to be scrapped. I went to another mechanic who replaced all 8 spark plugs and associated wires, the number 6 coil, and the O2 sensor. She is purring like a kitten for $1,300 vs. over $100k for a new model. Thanks to the new guy for keeping me out of the market for a car for another year…

$1,300 for some spark plugs, wires, 1 coil, and an o2 sensor?

that mechanic is laughing at you, as is anybody else who knows even a bit about fixing vehicles.. you greatly overpaid, and you also exposed yourself as clueless in predication when your old mechanic told you the vehicle needed a new engine. clearly, it didnt. so yeah, if your gauge of ‘savings’ is up against a new vehicle sticker price, then you might have reason to pat yourself on the back. but all you did was spend $1,300 on a sub $500 repair. you actually added to the skyrocketing costs of auto repairs by overpaying when you didnt have to.

Bull….he went to professional mechanic,not a shadetree like you…good repair work costs money…this is not 1972.

bull? did he go to a professional mechanic? did i go to a ‘shadetree’? how would you know either of those things based off the discussion? were you observing from somewhere on high with godlike powers? and because he paid a certain amount of money, that means the mechanic was ‘professional’? you for some reason equate ‘good’ work quality with spending some certain (large) amount of money. that is not automatically the case, as many have found to their chagrin.. flawed logic, spurious assumptions on all counts, o defender of overspending…

You pay a good mechanic as much or more for their diagnostic work as their parts changing. And it is well worth it.

Exactly. I told the new guy of my predicament and told him to spend as much as needed to diagnose every system that could cause a misfire in an engine with 315k miles. He found multiple independent causes and fixed them. Also ruled out fuel system problems-fuel pump and injectors good, ruled out exhaust system problems– catalytic converter good after 22 years, and compression test revealed no internal problems.

Most shops just fire the parts canon – replacing stuff until it works. The key is the diagnosis. Newer technicians aren’t mechanics. 20+ year old vehicles often need a gray haired mechanic to fix them as not everything is evident with a code scanner.

For the budget challenged, you can always try an “Italian tune-up” as some of today’s fuel is garbage.

IsntItObvious,

Cost for changing spark plugs on an inline 6.

Years ago, I had a few Datsun Z cars. Everything was so easy to work on. Hell, I even welded up a motor hoist to get past the long front bumper and have enough reach to pull the engine. Still have the hoist in the garage.

Now, my car is a seven year old M4. Shit, I watched a YouTube video on changing the spark plugs on one of these. Damn, that ain’t an easy job. You have to take so much stuff out of the way to get access the plugs, I will not do that job myself. The carbon-fibre strut tower braces are just one piece of the puzzle that needs to be removed. Thankfully, for the few miles I put on it, that’ll be a long time before needed.

El Katz has commented on subjects similar to this, and he is right. But, even if it costs me some of my “interest income” sometime down the road, it’s worth it to be able to drive such a nice, fast and technically advanced machine.

kramartini,

She isn’t purring like a kitten. Growling like a panther, though.

Cost for changing spark plugs on an inline 6?

i dont follow.. the subject is a 2002 gmc yukon denali. how is that related?

at least you interpreted the possibility of self-repair from my original comment. not all vehicles are equally repairable. european cars are notorious for not even being able to change the oil on your own without some special tool or service protocol, or the procedure being so arduous, you virtually HAVE to pay a shop to do it.

if you keep an older vehicle around, as mr. kramartini apparently does.. for the reasons he stated, you generally learn a thing or two over the years of owning it. his post demonstrated little of that, based off what he wrote.

with a BMW, you are ALWAYS going to pay alot.. thats what you get for driving a luxury/high-status brand. people who own them are generally those that have alot of $$$ to spend on the upkeep. they dont post on WS about how

“Not being in the market for a car is a key financial solvency”

and then talk about spending $1300 on some spark plugs and an o2 sensor.. thats counter-intuitive.

My Datsuns were mid-70’s. Self-repair was easy.

A 2002 GMC Yukon has a port for a scan tool to diagnose ignition coil issues. Self-repair is not so easy.

I was trying to make a comparison between easy to fix and complicated as it relates to how old a vehicle is, and I used my two different inline-6 sports cars as an example. Changing spark plugs between the two inline-6 cars is like night and day.

You’re right, I did not explain the relevance between the two, and I’ll try to be more concise in future comments.

A Yukon’s ignition coils are voltage amplifying devices to feed the spark plugs. Not enough juice, and the plugs don’t fire properly, and that can cause fowling. As an overall refresh, a new fuel filter might also help. And certainly, gasoline that has low ash residue and is preferably non-oxygenated will be better. Gas with ash in it will leave plugs worse-for-wear.

You are right. My BMW does need an oil filter cap tool. So does my Lexus SUV. I recently changed the oil on the M4 for the first time, as when I bought it as a one-owner lease-back in 2020, I also bought a three-years service and warranty package. So it was very well serviced and refreshed two years ago at the dealership as part of the package.

MotivX Tools out of Washington state makes a great 16-flute tool for BMWs (also fits most Volvos), and one is now in my tool box. Plus, I had my local mechanic put it on his lift to help me do the job myself & get my first good look at it from underneath. But no, there’s a lot of service on it that I’ll not try to do myself. Changing spark plugs is one of them.

I plan to keep my M4 for many more years, and I hope ‘kramartini’ keeps his ride for many years as well.

never could spell

vecchio

Thanks, Wolf.

You have no basis for asserting that the diagnosis and repair could have been done for the price you quoted in the Austin area within a realistic time frame, much less same day and within walking distance of my residence. You have even less basis for asserting that I could have driven the vehicle all over town comparison shopping in the condition it was in. You fail to consider the opportunity cost of not having a vehicle–rental cars are not cheap even on peer to peer sites like Turo and I need to get back and forth between my current residence and the new house I am moving into in New Braunfels. All things considered, there was no realistic way for me to capture the notional $800 that I theoretically left on the table. Why are so many “car guys” so mean?

Spot on from an old mechanic here. A shop may have charged you more and replaced ALL the 8 coil packs (@ $100 each). You did good.

And you would have paid for a diagnosis ($130) and SHOP RAGS @ $15!

Nice job!

” You have no basis for asserting that the diagnosis and repair could have been done for the price you quoted in the Austin area within a realistic time frame, much less same day and within walking distance of my residence. ”

irrelevant. my statement was that you overpaid for the work, generally speaking. i state that because you listed what was wrong, so an exact $ figures on the parts can be determined. a diagnostic does not cost multiple hundreds of dollars for a 2002 yukon. diagnostic service at firestone, for example, is 100-150$. the labor is the wild card factor.. but you could have paid 0$ for it by doing the work yourself. changing some spark plugs is a far cry from say.. rebuilding a transmission. your post was highlighting your apparent ‘frugality’ when it comes to your vehicle decisions. i did not say you overpaid for the work with same-day service at a shop down the street in the austin area, necessarily.

“You have even less basis for asserting that I could have driven the vehicle all over town comparison shopping in the condition it was in.”

irrelevant again. you stated yourself that you had a 2nd vehicle, so you (apparently) would not have needed to do what you say here. but you ‘could have’ gotten a friend or relative to drive you around, or made a few extra phone calls also.

“You fail to consider the opportunity cost of not having a vehicle–rental cars are not cheap…”

again.. you made the statement about having 2 vehicles. but id say you failed to consider the opportunity cost of making a few extra phone calls to potentially reduce your $1300 shop bill. you could have paid the diagnostic fee with that mechanic and taken the vehicle elsewhere for the ‘fix’. there are opportunity costs all over the place with something of this nature. you cite one as an example.

“All things considered, there was no realistic way for me to capture the notional $800 that I theoretically left on the table.”

sure there was.. but i didnt know your exact daily life situation. i just stated that you overpaid, based on what you did say.. and based off your posts subject about not being in the market for a car as a ‘key’ to financial solvency. that CAN be a correct statement, under certain circumstances.. but if you’re bleeding out overpriced repair expenses over time on an older vehicle, then it can quickly become the opposite of ‘solvency’.

the point is, as far as taking the facts of what was wrong with the vehicle at face value as you stated, EXCLUDING outside extenuating circumstances, that you overpaid. if that was ‘mean’ of me to say, well.. ok then. i can admit that might be one possible interpretation of it.

And then a few weeks later those new plugs get gummed up and the misfire is back……90% of the time anyway

Definitely a worry. The plugs were far short of their rated life, but they were extremely dirty. However, the fuel injectors were fine. I had run a bottle of Lucas engine cleaner through the system before taking it in. Could that have cleaned the injectors but left the spark plugs fouled? Is there maybe gunk in the bottom of my 22 year old fuel tank?

I have heard it suggested that I not run my tank below 50% full. Any other suggestions would be welcome.

It’s a bit more difficult maintaining a 20 year car in the north east. Regardless of the maintenance and prevention care you sink into it, the rust will come for it. I’m driving a 15 year old Ford Edge, which drives great, no issues there. Unfortunately the rust is making it’s way from the inside out. It might have a few more years. Undercoating every year can only abate the process but not halt it.

Hope your Yukon makes it to 25!

Tin worms are nasty… POR15 anyone?

Guilty as charged Mr Wolf. Great days for savers. What the wife and I cannot spend because of our squirrel mentality, goes to our children to spend while we are alive. Never should rates stayed so low for so long.

I went from 2015 F-150($30k) to a 2003 f-150 with 300k miles

both paid for

1st one used as down payment on house I bought for $200k

got $30k for truck with 85k miles on it

loved it but I utilized stuck value when I can

now considering use for house

RENTAL v. flip-leaning 90% as flip

ie want my CASH BACK for next deal

Exactly, ways of creating wealth you are comfortable with. Had rentals, flipped houses, bought and sold my principle residence 7 times. Was confident as you were about the way we did things. Your own way.

But all this begs the question, who is paying the $1.37G difference between interest income and interest payments? Is this the interest paid on government debt, or the interest paid by industry or something else?

The growing deficit is paying the difference, LOL. Just more bond issuance. More income for the buyers. More inflation for consumers. Higher interest rates for investors and borrowers….

Republicans are now talking about corporate tax cuts. No one ever wants to pay for anything in this joint.

ie hyper debt growth

and then GREAT RESET

When have Republicans ever not been seeking corporate tax cuts? Tax cuts in the nation with the lowest effective corporate taxation already. Not the lowest on paper, the lowest in practice due to workarounds.

Funny how so many Americans tend to vote for the party that supports them the least. They really have people fooled. But sadly that’s not only the US. Blinded by hot button social issues that are meaningless to their standard of living. Hey Bernie Sanders exists so there could be hope if people actually payed any attention to money driving politics.

The guy actually wants to redistribute wealth from the ultra wealthy in meaningful ways back to productivity. Hey it could be applied to the massive national debt instead of the debt having effectively lined their pockets.

Capitalism…(insert quote by Mayer Amschel Rothschild)

The democrats had full control of Congress and the White House and they could have taken steps like passing a bill to at least change the laws on carried interest so private equity didnt get a huge tax break.

If you think Democrats are the party that actually wants to redistribute wealth from the rich to the poor you have your head stuck in the sand. The biggest and most powerful industry lobbies are in healthcare, education and military (along with wall street) and Democrats feed at the trough of those industries in the same way that Republicans do. A small group of Democrats talk about taxing the rich, but they never take any real steps to make it happen.

Ever since Reagan (the worst Republican president) the Republican party has been broken. He taught the Republicans that they can lie to themselves about being fiscally responsible, while they voted for laws that generated massive intergenerational wealth shift.

Yea, as a conservative, I think Reagan was a complete fraud. He was the Republican version of Biden – both of them basically had dementia in office and were controlled by the people around them.

TOTALLY agree with gametv, especially about ray gun… he was a disaster for the republican ”party” and just another lying weasel screwing the public while smiling and talking smooth.

Also right on about BOTH sides of the aisles.

Old theme was repubs represent the rich, dems the poor, and both screw the middle and working folks.

Senators Sinema and Manchin put the kibosh on any changes to Private Equity taxation. They know who contributes to their slush fund.

Yep. It’s why I changed my mind on politicians age not mattering. So many in power today won’t live to see the consequences of their voting.

Lauren:

Two words: Mandatory retirement.

Or another two: Term limits.

McConnell, Pelosi and Co. have presided over almost the total financial destruction of the US.

Pelosi left…it’s McCarthy for another month.

Pass it on to our kids. They arent getting a real education at college, so they are not complaining. Economics taught by an MMT professor should be listed as Non-critical Analysis of Fiction in the course catalog.

A lot of theories work well as long as people are not given a choice in the matter. There certain truths that mess things up.

1. People will not work as hard for society as they will for their own family.

2. People change behavior to get around high taxes.

3. OPM spends easier than if you earn it yourself.

4. People can move themselves and their money/business.

5. Eventually you WILL run out of other people’s money.

This is the part where the banks are insolvent. They are losing money on paying out higher rates than they receive from older Treasuries. They either sell Treasuries at a loss today, or hide the fact and suffer from income losses.

Amazing days for those that locked in 3% mortgages and now receive 5% on savings. I hope they appreciate the transfer of wealth to them with those mortgage rates.

Wasn’t this the entire logic of endowment mortgages in the 1980s in the UK (and possibly elsewhere)

Look how that ended.

There is no free ride that lasts very long. You’ll pay eventually.

Yeah, but the home value is declining in many locations. It doesn’t make sense to pay any amount of interest on a declining asset.

“declining asset”

Depends how YOU value your asset. My house isn’t any crappier, despite the fact that its hypothetical resale value is lower. Still the same roof over my head.

I’m getting extra interest, but I won’t be spending any of it until the Fed starts respecting it’s mandate. There’s too much uncertainty with a rogue Fed and corrupt Congress in play.

What will they do next? Who will they target? How much will they take and when?

Nobody knows for sure, because they don’t follow through on commitments.

Couldn’t agree with you more.

Everybody is getting screwed- the sellers cannot move, the buyers cannot buy. The FRB froze the largest market in the country.

This is why Mosler is claiming that the rise in interest rates is a form of fiscal stimulus (as regressive as it may be with respect to distribution) — especially since US Federal debt as a fraction of GDP is higher than it has ever been and much, much higher than it was during the Volcker era.

Higher rates are a poor tool for fixing inflation. It will eventually work, but through asset price destruction which will reverse the spending from the wealth affect and cause fear. If rates go high enough, the stock market will be worth very little.

You can already see it in utility stocks. Who wants to pay for a 4% dividend when you can get 5% in a m/m? Utility stocks down 20% or so already. The higher the funds rate, the lower the stock price will go.

Keep in mind that the lower the stock price goes, the higher the dividend yield, which at some point will make owning the stock more attractive.

That is until they cut/suspend the dividend to preserve cash. Ain’t no free lunches.

I do, the tax rate on the dividend is 20 vs 37%, and the dividend is growing at close to 4% per year. I. Better off first year and keeps getting better if rates stay same. Are we going to 6% or 7%?

Exactly why it’s the perfect tool. We need asset price and wealth effect destruction. About time. I just hope the Fed doesn’t cave. The casino (AKA stonk market) crashing is music to my ears. Sick of the corruption. Not my fault if people bought into Wallstreet’s propaganda.

Transfer payments to non-productive recipients is not stimulating.

If the recipients spend it, it stimulates “spending,” and spending stimulates production, transportation, employment, taxes, etc., which stimulate further activity, etc. As long as the recipients spend it.

It is great for the ‘consumption’ based economy when the consumers spend from their ‘savings’ and NOT from their credit buying power. Some savings is essential for healthy capital formation for a productive economy. Also saving for a rainy day is also equally important.

WITHOUT deficit spending by our Govt or consumption/spending predominantly, based on credit (CC+) creation, where would be our economy, today?

Our economy is built on DEBT based (Govt) spending or consumption, with DEBT-due CAN being constantly kicked down the road. What a great awaiting future or our(bottom 90%) children and grand children!?

Top 10% who have 90% of Wall St wealth need NOT worry, in our growing Rentiers’ economy. Labor especially the blue collar kind, being constantly devalued and squeezed by capital formation ( upwards trickling) to the top, in our increasingly inequality in income and growth society for the past 3 decades.

Otherwise everything is hunky dory/sarc

Spencer,

Savings=Investment=Higher Standard of Living.

Any drunken sailor can spend their paycheck.

Interest rates ought to be determined by how bad you want to borrow someone’s savings. Amen.

Exactly.

I have some unused money available.

What am I bid?

But you’re saying that salaries paid to productive recipients is? What’s the difference, oh wise one?

As far as higher interest rates being the wrong formula, maybe it’s a way to eventually force the government to slow down spending and reduce the purchase of things that go boom, whoosh, and bang, instead putting the money towards developing products and manufacturing that contribute to the employment and betterment of the citizens governed by customer demand – not executive fiat.

Great info. Much different perspective on interest debt vs. interest income than I hadn’t thought about. Instead of spending the extra, just love the compounding available from Money Market funds, which also doubles as “collateral” for options contracts, rather than leveraging. Currently making 4.75% on the MM and 7%+ on the Options the past couple of months, without the stress of having it all riding on the market ups and downs. I’d be OK if it stays this way forever, after years of pennies on the dollar. I was going to pay off a relatively small HELOC, which soared up to 7%, but as I’m profiting 5% on it, I’ll just keep making payments until reality returns.

ie lend short at 12% and borrow long at 7%

keep it tight

Nice. Which options are you riding your HELOC on?

The important information you are missing is what income bracket is making all that interest income. I would bet it’s the 1% that control the majority of assets in America. Not many but few. Your assertion that the retire making an extra 10k on his 200k in treasury seems a bit underwhelming.

1. I’m not missing anything. But you completely missed the point. From the article: “But in terms of the overall economy, it doesn’t matter how it splits up since we’re looking at overall income, overall interest payments, overall demand, and overall inflation.”

2. The bottom 90% hold $7.9 Trillion in deposits, money-market funds, and bonds, not counting anything else (Federal Reserve data). So if that earns 5%, it’s $400 billion in interest income.

3. Wealth disparity is a real issue in the US, but I’m getting sick and tired of these stupid assertions that 99% of Americans are poor. This stupid nonsense doesn’t belong here. There is a huge layer of people who are between comfortable and wealthy in the lower 90%, and many of the readers here fit into that category, though there are probably a bunch of 10%-ers and 1%-ters as well.

4. People who believe that most-Americans-are-poor BS will never understand the US economy.

It’s really amazing that we now have hundreds of billions being pumped into the economy with normalizing interest rates, while many are still getting the transfer of wealth from their 3% mortgages that they can also pump into the real economy.

Of course the financial economy is screaming.

” transfer of wealth from their 3% mortgages”

Though the Fed doesnt have to take the losses on their MBSs, there is a loss on paper…. currently. The “counter” to that loss sits out there in the economy as a “gain” to those who borrowed so cheaply to buy a home. They spend, and perhaps borrow against that gain.

The Fed has no business in the long end of the market, but that wisdom what violated starting with Nobel Prize winner Bernanke’s QE and MBS antics. Did the Nobel committee take into account the massive unrealized losses the Fed now has on their MBS purchases?

“transfer of wealth from their 3% mortgages”

Except that because of those 3% mortgages, the houses are now “worth” more. For those of us who aren’t selling anytime soon, we have to pay higher taxes on a now “more valuable asset” even though we’re not going to realize those gains.

So really, its a transfer of wealth to municipal gov’ts for some.

wolf – I agree

HOWEVER those 10% who have FEW assets can get screwed real quick

and we haven’t seen any real declines in stock markets have we

caveat emptor

It’s way more than 10% at least 1/3 of people have negative to near 0 net worth

Right. The statistics from a recent article from Wolf implied that about 30% of people spend their entire paycheck when they get it, saving next to nothing. This 30% of decisionmakers are at *all* income levels, not just the poorest 10%. That said, those at the lowest income levels may not have the luxury of choice for how they spend.

I am more interested in the equity numbers for the bottom 90%.

60% of people have either few assets, or negative net worth.

The ‘middle-class’ continues shrinking. One need only look at those surveys asking who can cover $400 on a moments notice.

SocalJimObjects,

This whole discussion is OFF TRACK. The article was about interest income minus interest expense and the impact on demand, and via demand on inflation.

Nicko2,

“60% of people have either few assets, or negative net worth.”

I’m so tired of this most-Americans-are-poor BS. The bottom 50% of households have a net worth of $71,000. The next 40% have a net worth of $758,000 (Fed wealth distribution data).

You’re confusing them with the poor. That’s maybe the bottom 25%, not the bottom 60%.

Agree with you on the poor BS propaganda SO widely disseminated these days Wolf.

Anecdotal I realize, but in our little hood of approximately 9×16 blocks, very diverse in most respects, esp politically, but basically working folks at all levels as indicated by very quiet days M-F during ”work time”, etc., the only even close to poor are elderly women, but typically they have no debt at all, low prop taxes from being in home many decades, etc., and are living well. And good neighbors to help when the ‘canes and storms wreak temporary challenges.

I talk to everyone see while my pup takes me for our daily walk, and most at all ages, working and retired are enjoying life, liberty, and happiness…

Here is an example of that point Wolf just made.

A few miles south of Myrtle Beach SC is a string of a dozen restaurants in an area called The Marsh Walk. Every weekend and most evenings a reservation for dinner is a must. Parking is always an adventure too. A table of four can expect a bill with taxes and tip of upwards of $200. This dining group of people are far from the 1%. Just everyday Americans from all over the east coast on vacation.

It does matter how it splits because the bottom 90% will spend it helping the economy, whereas the 10% will save it, not helping the economy.

Nowhere in my statement did I say most Americans were poor, I said most of the deposits and the interest are controlled by the minority that will not spend it therefore limiting the impact.

That’s my point

Most of the retirees who didn’t drink and gamble their lives away.

When I was younger I spent a lot of money on women, whiskey and music. What was left I wasted.

Brooks:

I think you are confused about how the 1% have their finances arranged. They’re not sitting on CD’s and MM funds. In the last meltdown in 2008, the pawn shops in Beverly Hills were doing a land office business hocking Rolexes so the “rich” could pay household bills. The rich mostly own assets, not passbook savings. That’s so bourgeoisie.

The Federal Reserve’s 5% to 5.25% will do nothing to cool the inflationary economy.

Wikipedia: “Timeline of the Great Depression:”

“Summer: Consumer spending and industrial production begin to stagnate. The Federal Reserve continues with its plan to raise interest rates from 4% in mid-1928 to 6% by mid-1929 in an attempt to combat speculative behavior.”

The 1929 inflation rate was 0% and the USA was on the Gold standard. Compared to the inflation rate of today that is 4% to 6% of real tightening versus 0% to -2% today. Even with that 1929 interest rate everything was still roaring.

Gary Fredrickson A+++

Great comment

Yeah times are good with brokerage accounts now paying between nearly 5% or more for their sweep funds. However, that 2.5 year old used car I just partially financed cost me 5.65% for 48 months and I consider myself lucky getting a rate that low. However, my out of state credit union is offering 5.25% for 30 months, saving $750 in interest costs.

That said, my 5 year old trade in was valued considerably higher than I expected, so things could have been a lot worse. Used car values are likely to continue to head downwards from here as the economy continues to slow.

During the last 12 years we paid 24% for 4 years on one car and 9% for 5 years on another car. The new car loan rates under 7% look like a bargain to me.

Our credit score was wreaked due to foreclosure which also caused us to pay more for car insurance. Notice how wealth trickles up.

No, it’s not “wealth that trickles up”, it’s simply that loans and insurance have risk. How one handles their finances (regardless of the circumstances) is a key determinant in assessing risk. If you’ve defaulted, consistently late paid, or BK’d previously, it’s an indicator that it might just happen again. Our auto finance term for such folks was “credit criminal”. No, not PC, but… just the same.

At one time, in a far away place, we used to run credit reports on potential new hires. Why? Because it’s an indicator of stability and we played with a lot of high dollar assets and corruption was tempting to those who had not much to lose.

As I’ve often said to people who’ve asked to borrow money from me: “Would YOU lend YOU money if you had it?”

Exactly why I tell people no ,when they want to borrow. Best way to lose a friend ,lend him money

I have no idea what my credit score is and don’t care. Our awful financial situation never kept us from buying cars, renting, or jobs. The leeches just charge you more interest or pay you less in wages. It is definitely a trickle up world by design.

P:

As it should be. It’s like the old saying about the golden rule: The one with the gold rules.

If you plight is as bad as you say, you might want to reconsider your approach towards your credit score. A lot more than car loans use that data for evaluation if a company wants to do business with a customer, beyond lending them money. It’s naive to believe that, just because you can buy a car, it means that you are garnering an advantage by “sticking it to the man”.

As an example: A landlord might require a larger damage deposit, not give you rent incentives that a person with better credit would enjoy, start eviction after one or two late rent payments…. it’s a long list.

“Our awful financial situation never kept us from buying cars” is how they get you.

Credit score is a measure of how profitable a customer is to lenders, period. You can have millions in assets, including real estate, without ever having used credit, and have a very low credit score. I’ve never understood people who are proud of having the highest credit score, sin e it is, in some sense, a measure of how big a sucker they are for financial companies to go after.

Fico is now being skewed by the likes of chime and credit building, models will be adjusted for it.

Someday the dealer will get a token from potential lead that has an auto finance scorecard, ustomer sill own their credit data, dealer pays less than pulling credit report. Eliminates all fraud and identity theft

I know al model algos that beat fico auto 9 by 8 basis points. That is a lot more loans for lender

The party will continue until August 29th, then inflation and everybody else must go home.

That’s cryptic. Can you elaborate?

Appletrader is probably referring to the re-start of student loan payments, which will suck a huge amount out of the US economy (and global, since US trade deficits pump so much into other countries exports). Appletrader’s right in that the student loan pause has been, de facto, the largest of the covid pandemic stimuli, even more than the fraud-riddled PPP and even those stimulus checks, and lasted for over 3 years.

However, the drain on consumers will be happening well before August 29 2023, partly because those repaying student loans will need to save up a lot more money beforehand to have the funds at hand (due to the over-spending and credit card and other leverage so far, almost all wasted the opportunity to bring down their loan principal). And, many of the student loans are set up so that repayments are re-starting well before August 29–the official end of the pause will be June 30, and after that, many loan services using automatic payment or garnishment will kick in during July.

Then there’s also the fact that, with the clunky way the debt ceiling was “resolved”, almost $1.5 trillion in Treasury debt instruments is going on-line in a hurry, which is going to suck an even larger amount of money out of the US economy even faster, and put huge pressures on liquidity. And this is when US consumer spending is already falling for other reasons, with savings depleted. The Fed still needs to push up interest rates much more and faster, by 50 bp in the June meeting and especially, be a lot more aggressive with quantitative tightening and especially selling MBS’s as part of the QT, to choke off the speculator asset bubbles still fueling a lot of this inflation. But a lot is happening fast this summer.

“$1.5 trillion in Treasury debt instruments is going on-line in a hurry, which is going to suck an even larger amount of money out of the US economy”

Indeed. The Govt is extracting money from the real economy to appropriate expenditures as they see fit. Wasteful describes how they spend. Inefficient.

We didnt hear much about debt service costs during the debt ceiling fiasco. Now we will, as if it is some sort of surprise.

My DIL used the student loan interest/payment moratorium to pay off her loans. 100% of the payment going towards the principal was the smart play. Only a dope would have chosen to p*ss away that opportunity, only to then to be stuck with the aftermath.

When the Jones’ can no longer keep up with the Jones’, it’s going to get interesting.

@El Katz

“100% of the payment going towards the principal was the smart play.”

Yep and your DIL was smart to take advantage of that opportunity. Unfortunately the data so far are showing that almost no one did this, instead using the student loan pause to juice up wasteful and lavish expenditures. Basically consumer spending and esp retail sales in the US for the past 3 years were heavily juiced by the pandemic stimulus, and above all by the student loan repayment pause partly because there were a lot of morons on the financial shows and social media promising that the pause was indefinite.

It’s the same stupid short-sightedness of the squawkers and Wall Street fools shouting and squawking endlessly about a Fed pivot for the last year (including the WSJ that like the NYT has fallen horribly far from its former perch of respectability), and it’s leading to the same kinds of dumb consequences. Just like the pivot fantasies led to SVB and other bank failures, the delusions about “student loan repayments will never start again” led to a mass squandering of that opportunity, and a huge artificial boost to consumer spending.

Jerome Powell simply cannot pivot or back off monetary tightening now because inflation is destroying the United States, not even an exaggeration anymore. American homelessness is at record highs (research even shows every $100 increase in rent drives up homelessness by about 10 percent), shops are having to shut down or change policies due to the mass theft from shoplifting and even looting by people desperate to just get food, restaurants and hotels can’t get workers because over half the service workforce is being priced out by the outrageous cost of living increases, the US birth rate is at a record low and collapsing further, Asia and the Middle East are de-dollarizing faster (into a variety of other options), quiet quitting and de-motivation at work are crippling American productivity (most workers in the USA are suffering effective pay cuts due to inflation), the writer’s strike is dismantling Hollywood and other entertainment centers as the industry shifts elsewhere, new strikes are brewing and anger, crime and social unrest and instability increase. All of this is thanks to inflation and the Fed’s failure so far to tame it, and now desperate measures are needed.

For similar reasons, the federal government can’t back off student loan repayments with a soon to be $35 trillion national debt. Yet the same kind of bad, stupid advice spread all throughout the financial pages and now, tens of millions of Americans (and indirectly, hundreds of millions due to the businesses affected by their spending) were basically bubbled up on the leverage of a repayment pause that had to stop once the covid emergency halted. And now a painful reckoning is coming.

El Katz

Doesn’t the interest due on student loans accrue during the moratorium? I assume other loans had higher interest rates?

It seems the rise in interest rates will also hurt the Fed. Lyn Alden has written a pretty good article on it. It will have bad implications for the US Treasury.

How the Fed “Went Broke”

“In September 2022, the Federal Reserve began operating at a loss.

This is because they had raised interest rates unusually quickly throughout the year, including on their own liabilities.

From January 2011 until September 2022, the Federal Reserve paid approximately $1 trillion in cumulative remittances to the U.S. Treasury, which was a nice revenue source for the government. Now, those payments aren’t flowing anymore.

In a few months, the Federal Reserve will have lost enough money from this negative net interest income, that it will have negative tangible equity. In other words, its financial liabilities will exceed its financial assets. However, thanks to some accounting gimmicks, their reported equity is basically unchanged.”

People who assert that the Fed can or will go broke are patently stupid and ignorant. Don’t drag these morons into here. These people are just producing clickbait braindead BS.

A central bank that creates money can NEVER go broke or become insolvent or whatever. So losses don’t matter to a central bank that creates its own money. Period.

I have explained this a gazillion times.

Agreed, but they can make their people go broke.

Thinking Turkey and others.

Turkey borrowed in foreign currency. Argentina borrowed in foreign currency. They do that because they ruined their own currency and have trouble borrowing in it. But they cannot print foreign currency — so countries that borrow in foreign currency can and do go broke (the government, not just the central bank).

And yes, inflation is in part a result of central bank policies.

What about interest payments on the debt?? At some point the gov Will be broke. 30tt may be manageable but 60tt would not be

No, a government that borrows in its own currency cannot go broke either. But it can and does create inflation with these deficits, and inflation will destroy the value of the debt. Tax revenues rise roughly with inflation-plus some, and that’s how inflation reduces the burden of the debt.

For example, five years of 10% annual inflation and 2% annual real GDP growth, means that tax revenues also rise about in parallel at around 12%. If the total debt rises by 5% annually over the same period, the burden of that debt actually declines.

Inflation is a special tax on all assets and incomes. Incomes tend to roughly rise somewhere near the rate of inflation. Asset prices may not.

There are people who say that inflation is the fairest tax of all. If a government needs to tax a lot, it should use inflation. Inflation fully hits the wealthiest, though they might not notice because they have so much, while they would raise a huge hue and cry if their income taxes were increased by 1% or some of their loopholes were closed.

That’s how government profligacy always ends up. Higher inflation, higher interest rates, and asset prices that cannot keep up.

Government profligacy.

I had to look up the word “profligacy.”

noun

Synonyms Shamelessness. See abandoned.

“A profligate or very vicious course of life.”

“Shameless dissipation.”

“A state of being abandoned in moral principle and in vice; dissoluteness.”

Yes. That’s a good description of the fiscal policies in Congress and the Executive Office. Thanks, Wolf.

“So losses don’t matter to a central bank that creates its own money. Period.”

Gee, then what happens when other countries refuse to accept the “money” as legitimate? A currency crisis.

So I’d say it does matter.

Your argument is called “whataboutism.” Google it. Soviet propaganda excelled in it.

The statement was “How the Fed “Went Broke”” — and that’s what my reply was about. The Fed cannot go broke. Period.

You raised a new topic, and it’s gold-buggery nonsense. What’s the alternative to the USD? The Euro? The RMB? LOL. The USD is still the cleanest dirty shirt.

A currency crisis is just about impossible for the dollar because it is the world’s premier reserve currency and is used in international transactions. Nasty inflation is the dollar’s Achilles heel.

Good to see you quashing this foolishness, Wolf. These people are brain dead.

Yes. I appreciate Wolf’s insistence on keeping these forum comments rooted in reality. Even though that means he has to repeat himself again and again.

And with a single back-handed slap, the Wolf sends them headphones flying up against the wall.

The two Alden sisters are too young to understand real economics and politics. They never lived through any of it. Recalling something in history books just doesn’t cut it.

Great article wolf. I think this actually reinforces the case for “higher-longer” There are a lot and I mean a lot of boomers now earning interest income in a meaningful sense. What I’m hearing is, again, because you can’t take it with you, then they are spending it. Or perhaps gifting to family in the “give while you live” sense. This interest income/spending, therefore would seem to actually reinforce inflation. Thus the fed-pivot just ain’t gonna happen anytime soon. The interesting thing will be by what measure will the new money continue to put pressure on inflation… it seems those WITH money love this, they are earning again safely. Those WITOUT money, have to borrow, and well, “ouch.” I think that this is an interesting equilibrium to explore —how that “normalization” will play out, and… on what timeframe. Great article wolf — a lot of food for thought.

Dick,

Re boomers gifting to family in the “give while you live” sense.

This seems to be a rising trend: I’ve noticed many UK financial websites now mention the “Bank Of Grandma And Grandad” in addition to the well-established “Bank Of Mum And Dad”..

Most of the Bank of Mom and Dad goes to healthcare and nursing homes in the US.

I am one of those whose annual interest income went from $20,000 to a $100,000 in just over a year. As a classic capitalist pig, I didn’t do much of anything for this, other than stay alive. I did learn how to buy T-bills and learned to watch Powell’s press conferences. I learned the important points are when he grimaces like he is passing a kidney stone. I also studied a little history, and, as I have pointed out too often, current rates (Fed funds and 30 year mortgage) are not much different now from the average over the period 1971-2023. So the economy will keep humming along as usual, perhaps even stronger with the huge increase in interest income as an added stimulus (for a while).

If the Fed pauses, inflation will just keep lurching even higher, which means they will have to raise rates even higher later. If they continue their piddling 25 basis point raises, well, more interest income for me. The Fed is to blame for all this with their prolonged ZIRP, and then moved too slowly with their rate increases. I know there are lags involved, but as Powell says, we don’t know their length, so I will have to settle for my cross-sectional (non time series) estimation. I am staying with faster, higher, longer, if they want to slow inflation. This view has worked fine for me over the past year or so. It will end, but I have plans for that.

While I can’t prove it with data, I suspect that much of that interest income is passively compounding rather than being spent. Some of it is being spent, of course.

But a good chunk of that interest income is inside the truly massive 401k and RRSP universe. Money flows in passively due to employer matching schemes and the like. People pick the “balanced portfolio” checkbox after their HR girl did the “magic of compounding” presentation. After that, they don’t think much about it.

In short:

Interest payments on debt are in your face. Outside of people on a downward spiral to bankruptcy, the interest usually doesn’t compound upon itself. People service their debt because they have to.

Interest income often compounds rather than gets spent. People might not even see the “income” directly because the reinvestment is hidden inside their balanced fund and they haven’t even bothered to open their statements since they can remember.

Intuitively, it’s in the name. Fixed income retirees live on a fixed income. They are the saver (/hoarder) cohort of the population. The spender cohort blew that would-have-been $200,000 t-bill stack on the Audi and the divorce years ago.

Anyone making meaningful money in interest income probably didn’t really need it in the first place so isn’t spending much differently. If you have $1mm in a MMF, are you really getting THAT excited about an extra $50k a year and spending it?

$4000 a month probably doesn’t excite alot of people with $1M in bonds but speaking for my self it covers my rent (by choice) completely leaving everything else duscretionary even if i don’t blow it on Door Dash.

😆

it makes a comfortable life more comfortable. Point is the people that need the money to cover the increased cost of living are the ones that don’t have a pile of cash earning interest income.

I do think retired folk likely have a different view but with 20 working years ahead of me and kids to raise I don’t “spend” my interest.

Yes, spending it. Guilty

I am not rushing out the door to buy a Lamborghini. But I do buy some stuff now I wouldn’t normally buy. All else being equal (ceteris paribus), any increase in demand will raise prices.

As F. Scott Fitzgerald said “Let me tell you about the very rich. They are different from you and me.” Most rich people would kill for a one basis point increase in interest rates, if a lot of their income is from interest. Wealth accumulation in all its many forms is kind of a game to them. Most are merciless.

So if brk has 130 billion that’s a lot of interest.not chump change

Good points about retirees.

In the article it states, “…many of them are spending some of it.” How many Wolf and how much? Those would be interesting data points to ferret out. I posit that many are not changing spending habits much at all, except for the inflation premium. I don’t know how many of these either, but in my circle it is most. So while they are spending a bit more today due to inflation, they are not spending much more than they are receiving in increased interest and Cost of Living increases in Social Security. So, the real inflation pain won”t really be felt by those lucky enough to have IRAs and decent SS, until those IRAs run out, and many won’t really feel inflation pain at all because their IRAs will outlive them. Earlier if inflation continues it’s bite, later if it gets tamed back down below 3 or 4%.

People who had the discipline and means to amass significant funds in a 401K, IRA, or savings and investments are unlikely to become spendthrifts simply because interest rates rise. Most have lived a comfortable life and look at the additional funds as improved financial security or a way to feather the nest of others. At our age, my wife doesn’t need a Louis Vuitton purse nor a 4 karat diamond. Those do nothing more than make you an attractive robbery target anyway.

Assuming rates remain at these levels, I think that interest received will rise as complacent holders of low interest paying bank accounts for example, transition to higher paying assets. Considering services such as checking with interest offered by brokerage accounts, other than perhaps ATM services, why would anyone need a bank account?

Most all folks need banks accounts to do normal financial transactions on a daily basis.

When rates are artificially low due to central bank machinations, it is the govt who spends the “incremental benefits”.

When rates are, shall we say “more normal”, meeting measured inflation….it is the private sector that spends the “incremental benefit” from those interest rates/payments.

Either way, the money gets spent. But who spends it better?

So when the Fed lowers rates to “spur the economy”, IMO, the spending just moves from Private sector to Government.

The private sector getting a fair return on their holdings of dollars is an economic engine, something that seems to get ignored by the Fed. Perhaps they can see it now.

I believe Government and the FED is trapped by their own devise this time around. Hang on for a wild ride.

Wolf, Little off topic but another expense, as far as housing, because of high housing demand. My son owns a house outside of Dallas Texas and in two years it has increase in value by 40%. With that, he just got his new tax bill and mortgage insurance increases. His house payment just went up $460 a month, that is a huge jump for a young family in middle class. That is $460 that will not be spent in the economy each month x how many Americans. I can guarantee workers are not getting big enough salary increases to cover that kind of big increase.

Yes, but Texas doesn’t have a state income tax! Lol. Meanwhile Texas state Republicans have brought the Legislature to a standstill with two alternative proposals to reduce property taxes. One proposal would give most of the benefits to businesses and the other to individuals especially the elderly. I don’t have to tell you which one will prevail! Can you spell D-Y-S-F-U-N-C-T-I-O-N-A-L? I knew you could.

He’s lucky he’s not in Florida where the insurance premiums in some areas are skyrocketing 40-60%. Toss that into the equation.

After the next hurricane you’ll be lucky to be getting any insurance at all. You’ll be on your own and SOL (S$it out of luck).

Our property taxes don’t go up when the assessed value goes up since the tax rate goes down by the same amount. Taxes only go up when the taxing authority raises them which in my State is constitutionally limited or through special levies which are voted on by the rate payers.

That $460 will be spent by the city. So it will still flow into the economy.

The one – two punch of 3% mortgage households with disposable income and 5% TBill households generating disposable income is STIMULATIVE.

Factor in the totally inadequate QT which will not likely achieve $1T in 15 months of existence and its gas on a bar-b-que.

But watch as another regional bank gets singled out for failure this week to force contemplation of a PAUSE.