The Fed’s QT is happening for the first time simultaneously with the refilling of the TGA. Both draw liquidity from markets.

By Wolf Richter for WOLF STREET.

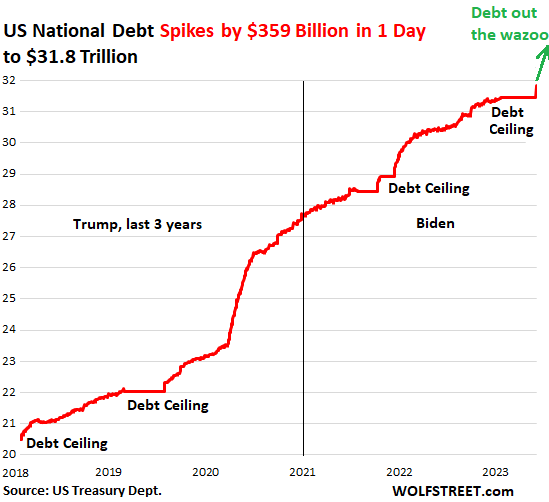

The Debt Ceiling Charade ended over the weekend when President Biden signed the “Fiscal Responsibility Act of 2023,” that suspends the debt ceiling through early 2025. A US default was “averted.” The ending of the charade is always known in advance: Congress will agree on a deal at the last minute, and the President will sign it, as it has been done for the 80th times since 1960. But the process of getting there can make you nervous. Then, after the Debt Ceiling Charade is over, we get a huge spike in the debt.

So the U.S. national debt spiked by $359 billion in one single day, the first working day after the debt ceiling was suspended, to $31.83 trillion, as of yesterday evening, reported this evening by the Treasury Department.

And that was just the beginning, there will be more hair-raising single-day spikes of the debt over the next few days:

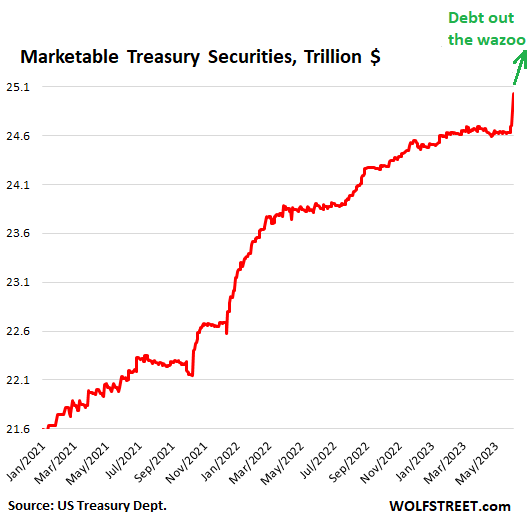

The total national debt comes in two types of Treasury securities, nonmarketable (cannot be traded in the bond market) and marketable (can be traded in the bond market).

Savers’ favorite “I bonds” are nonmarketable Treasury securities. The Treasuries securities held by government pension funds, the Social Security Trust Fund, etc. are nonmarketable. Nonmarketable Treasury securities jumped by $28 billion yesterday, reported today, to $6.79 trillion.

And marketable Treasury securities spiked by $330 billion yesterday, reported today. The chart below shows the shorter view of marketable Treasury securities for more detail. The Treasury Department is now issuing a flood of Treasury bills (with a maturity date in one year or less) and Cash Management bills, on top of the bonds and notes, to replenish its checking account. So this was the first leg of it:

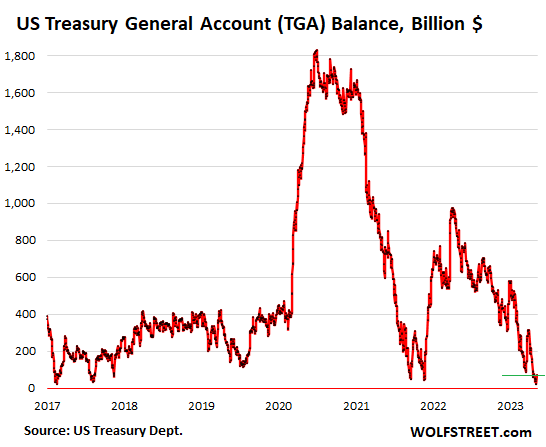

The government’s checking account, the TGA at the New York Fed, had fallen to a closing balance of $23 billion on Thursday and Friday last week. The out-of-money day would have been sometime this week.

During prior debt ceiling charades, the TGA balance had fallen into a similar range before the debt ceiling was lifted or suspended. This $23 billion was a very thin cash cushion, given the huge amounts of money that flow through the TGA on a daily basis: Into it from tax receipts and issuance of new securities, and out of it to pay off maturing securities and meet regular outlays.

The TGA balance jumped by $48 billion on Monday, reported today, to $71 billion. That increase was so small that it is hard to discern in the chart. But it was the first step in bringing it back to a normal-ish level. Massive bond issuance will be required in the near future, along with tax receipts, to:

- Pay off maturing securities

- Fund the ongoing blistering budget deficit.

- Replenish the TGA.

As you can see in the TGA, the gigantic bond issuance in the spring and summer of 2020 to pay for the stimulus packages and other stuff wasn’t all spent in 2020. The year ended with $1.6 trillion in the TGA, after having peaked at $1.8 trillion in July. The TGA was subsequently drawn down to near-nothing during the two debt-ceiling charades in late 2021.

This drawdown of over $1.5 trillion over the 12 months from the end of 2020 through late 2021 moved $1.5 trillion in cash from the bank (the Fed) directly to the markets. This was a huge amount of liquidity to spill into the markets – it was a portion of the QE liquidity that the Fed created and that was absorbed by the Treasury department when it issued trillions of dollars in bonds in 2020, and that was then released in 2021. This mega-shot of liquidity explains in part the hot performance of the markets in 2021.

Then, from late 2021 through May 2022, as the TGA was being replenished, it absorbed nearly $1 trillion, and markets tanked.

Then came the drawdown, throwing this $1 trillion back into the market, from May 2022 through last week, and eventually markets rose sharply. This $1 trillion in temporary liquidity injection counteracted to some extent the Fed’s QT that was phased in last summer.

Now the TGA is being refilled, and this liquidity will be drained from the markets because the primary dealers and investors will buy all those Treasury securities that are being issued, instead of other stuff, and they will sell other stuff to fund their purchases of Treasury securities, and this flow of liquidity alters the buying and selling pressures.

And for the first time, the Fed’s QT is happening simultaneously with the refilling of the TGA, and they’ll both simultaneously for the first time draw liquidity out of the market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well, gotta be honest, I was wrong. I really thought the clown show was gonna drag out longer. Not that I really doubted, bit Wolf nailed it a month or two back when he wrote that it would be handled like they always are because all of congress is basically indebted to the markets / funds / shady deals etc that rely on the debt ceiling not being an issue.

the politicians have far too much insider trading to ever accept not solving the debt ceiling. I just didn’t expect it to be ‘theoretically’ infinity. I know a lot of people aren’t a fan, but it feels like the only thing higher for longer is more spending. Which may or may not be higher inflation for longer.

So, the bank is offering me more than $1 million jumbo loan for 30 years at ~6%. T Bills yield close to 5.25%.

If TBills Rise further or Mortgages fall further, I believe, I could be looking at 5.5% mortgage and 6% TBills.

So, if the bank can give me this Mortgage to buy a rotting house, should it not give me this with TBill as collateral.

Can I create a company that borrows from bank and rollover tbills to pocket the difference. I know it looks like a scam, but believe me I am not manipulating these rates!

“If TBills Rise further or Mortgages fall further…” what scenario would cause that? Generally, they’ll move in tandem in the direction of the fed rate movement… right?

So far, the 10YT has risen since 6/1. 30YFRM haven’t started to fall yet either.

As of yesterday, the avg treasure bill (4-52 wks) have dropped very little, mostly on the up to 13 week term.

The debt ceiling is a dumb idea to start with. If you don’t like how big your credit card bills are, you should stop charging so much on them, not just refuse to pay the bill when it comes.

Oh is housing affordable?

> Checks…

No.

So it hasn’t ended.

I honestly thought the Freedom Caucus would blow up the debt ceiling negotiations as ordered by Trump during the national town hall. I was shocked when it passed just in time.

The Freedom Caucus really only has power over GOP bills where they need all their votes. This bill was bipartisan enough to get support from enough Dems and Republicans to ignore the extremes.

Only way to clear that debt will be a fresh round of inflation! Bring on the printer 🖨️

Nah. There are several other things that can be done.

It is just that almost no congress or senate critter will even consider those since that would mean getting booted from their seat in the next election without a cushy job to retire to.

Corruption at its finest.

We the people ,commenters need to stand up and boot these ,thieves until parties realize we’re not going to take it anymore.

Flea – an always necessary, usually thankless, endless, unpaid, pain-in-the-a** citizen’s job that too-many of our fellows ditch for all manner of ‘good’ reasons until possibly reaching a Captain Renaud moment at Rick’s American Bar…

may we all find a better day.

The funniest part is that now even the “banana republic solution” of trying to inflate a country’s way out of debt doesn’t work anymore, at least certainly not for the US. The inflation just leads to even higher bills for next round of government appropriations, then COLA adjustments for payouts take their toll and debt roll-overs add on so that the country is stuck with the worst of the both worlds, high nation-wrecking inflation and social unrest while the deficit and national debt get even worse. This is even before considering the further costs from inevitable cost over-runs, corruption and embezzlement (often through officially “legal” means) by oligarchs and insiders. The hard truth is we can’t afford an empire anymore, even if we started actually taxing Elon Musk and his pals.

I agree with you. Unfortunately, all too many Americans with influence in high places think that we can keep running up huge deficits with no long term consequences. For neocons in DC, every war is a good war regardless of the costs

Generally more debt is associated with slower economic growth leading to lower inflation. Now if fed is buying the debt outright, that money gets circulated in the economy leading to inflation. But issuance of new debt without fed as a buyer should, in theory, lead to slower growth and inflation.

Debt is inflationary when it’s issued and used for speculation.

If you issue $1mm and it bids up existing assets like housing, that’s inflationary.

If you issue debt and the borrower uses it to add value, by for example building more cars, which increases the supply by more than was borrowed, decreasing cost per unit, that is deflationary.

All this other guff about tga, rrp, etc can’t change these age old facts.

We live in a real world with real things, real people, real energy.

How about land, Georgist?

Just tweeking you…I agree with your post…except that I would claim that from an empirical standpoint 20 yrs of ZIRP produced much more inflation (perhaps hidden, see below) than innovation.

Take housing – by far the largest expenditure for Americans.

20 years of ZIRP created a doubling (or tripling, or…) of home prices/expenditures.

Did cost of construction *really* double or triple or…? Where is cost-saving, ZIRP-powered innovation?

As to inflation, it is very, very possible that the true “China Price” deflation that would have benefitted the US consumer was in fact offset/taxed/stolen by DC’s ZIRP policies.

A retailer keeping costs constant to US consumer when his new Chinese supplier has lowered wholesale prices by 35% isn’t really a benefactor to consumers. Ditto homebuilders keeping monthly pmts constant…while doubling price of the house.

Americans may have been victims of the greatest shell game in human history.

Yep I agree geogist. Government debt is inflationary. I went to the FRED charting tool and I did a overlay of the Government debt versus housing prices. These two data series both have increased the same since we went off the Gold standard. Almost to the “T”. Does it mean anything. Probably not.

You can do the same thing with the price of gold. Same result, They have risen almost the same percentage amount. Interesting.

It makes me think housing and gold are not overvalued because of inflation.

I ran an analysis on gold for the past 25 years. If you bought in 1998 ( you had many opportunities to by gold for $300 – $400 between 1998 and 2003.), you have a compounded rate of return of approximately 7.5 %. $300 to $1940. I suspect the next 25 years might be the same. Regular dollar cost averaging works well in gold just as it does in other investments. You don’t need to be concerned about if it is over or undervalued. Just hanging on to it.

ru82 – check population increase+world resource availability curves over same timeframe?

may we all find a better day.

Maybe not. The money the government get by issuing this debt is to be spent on wages and goods. That translates to demand for goods and workers. If supply is thight, prices will rise.

A trillion drained over how short a period would be some good add’l info. I love Wolfs.commentary but perhaps his emphasis on relatively small and very slowed pace of drawdown as if it’s consequential I suspect is to bait folks into discussion. A generous and warm gesture.

I didn’t want to give over to cynical analysis but it seems an unavoidable conclusion that the fed only seeks to cushion the blow of slight asset price normalization for the uber wealthy at the great expense of the many and the health of the economy. It’s action only seem to benefit the top 1/2 of one percent.

How simple, selfish and short sighted and I get to feel naive about the notion they had any concern for the health of the actual economy.

If the Fed believed in the market and wasn’t filth, they’d own zero dollars of MBS.

“Draining Liquidity from Market”

Very temporarily? Doesn’t this all get spent by the government pretty quickly and/or paid back into the economy with interest? A third of a trillion is the cost of a fairly routine spending bill these days. Congress can fart that much dough out on an average Tuesday before lunchtime.

We’re looking to spend $6.4T in 2023. At that rate, $359B wouldn’t even cover us through the end of the month! Besides that, I would think that prying low-velocity cash from mostly very monied bond holder sources and pumping it into the broader economy in the form of gov spending is inflationary, no?

And let’s face it, a pretty big portion of the $359B is not going to be covered by tax revenue, so we’ll end up printing it one way or another eventually.

“We’re looking to spend $6.4T in 2023.”

That part is inflationary. That’s unrelated to liquidity.

The owner of two of San Francisco’s largest hotels has stopped making mortgage payments on the properties and will let them go into foreclosure as historic crime rates continue to deter tourists.

SF back by August

The landlord (Park Hotels) just f***ed your bond mutual fund or pension fund to enrich themselves. That’s all that happened. You got f***ked by them, if you have a bond mutual fund that holds those CMBS.

The landlord that defaulted on the mortgage is a hotel property REIT that was spun off from Hilton Hotels. That landlord doesn’t operate the hotel, you moron.

Another company operates the hotel, and the hotel will continue to be open for business. This has no impact on San Francisco. But Park Hotels is screwing your bond mutual fund.

So you believe what these people are saying that f***ed your bond mutual to enrich themselves?

These people are effing liars and clickbait producers to cover up the failure of their own REIT. The shares of that REIT [PK] have plunged by over 50% in three years. And the braindead blogosphere fell right for their clickbait Silly Putty.

Hilton was taken private in a huge LBO by PE firm Blackstone in 2017. A few years later, it went public via IPO at a huge profit to Blackstone. A few years later, Hilton Hotels spun off their hotel properties into a REIT, which then cash-out-refinanced the properties with mortgages that were securitized into CMBS and sold to stupid investors (such as your bond mutual fund). Those CMBS were designed from day one to screw those stupid investors (your bond mutual fund), and now those investors (your bond mutual fund) get to hold the bag. These people are something close to gangsters.

And you believe the BS they want you to believe, because the braindead blogosphere is spreading it around to get clicks and to get morons like you to spread that crap further?

I told you in Oct 2020 that these Hilton mortgages would default. This was a slow-moving wreck. There were lots of warning signs:

https://wolfstreet.com/2020/10/12/two-san-francisco-hiltons-add-to-woes-of-hotel-commercial-mortgage-backed-securities-special-servicing-rate-of-hotel-cmbs-spiked-to-26/

Wolf said: “These people are something close to gangsters.”

————————————————

you mean they are not capitalist heroes working within the rules of capital/financial markets to create liquidity and such….?

sounds anti capitalist ,,,,, anti American

what next? are you going to disparage Buffet and/or Goldman Sachs?

This is already hurting the pensioners, I know because I am now hearing about it from them. A 91 yr old woman told me the other day they are watching their pension collapse and then she said to me,’Am I going to work at my age?” The elderly are very nervous and rightly so. I voluteer in my community and am watching, in real-time, how this is touching many lives. Very sad.

WOLF

You state:

“…..primary dealers and investors will buy all those Treasury securities that are being issued, instead of other stuff, and they will sell other stuff to fund their purchases of Treasury securities, and this flow of liquidity alters the buying and selling pressures…”

Can you tease this out a bit? Why will dealers and investors buy Treasury securities yielding less than the yield that equity markets are delivering?

Here’s a thought: those equity market yields aren’t stable. Seems like a great time to take profit on NVDA/SPY gains and put that $$ into 5+% Tbills.

I bought some 4 and 5 month bills today myself.

The move that has been happening the last 3 days has seen the QQQ flat and small caps up. Russel 2000 is up 6% in 4 days while QQQ is flat. R2K could see another 5% to 10% in this move or QQQ drops. IMHO. A hedge play right now would be long IWM and short QQQ.

I guess we will see how it plays out.

Because the bond yield keep rising until they are all bought, and these are the people that switched from bonds to stocks over the past 20 years as rates kept dropping and they’d like to switch back.

Once you get rich you only need to stay rich, not take risks. and 4%/yr on >$250M can be lived on rather nicely

“Once you get rich you only need to stay rich, not take risks. and 4%/yr on >$250M can be lived on rather nicely”

That’s the ideal play, unless your spouse files for divorce and you’re thrown into the predatory arena of the North American divorce court system (or any common law country for that matter, UK and Australia included). Then all those assets will disappear pretty fast, and not just from alimony and child support–the US family courts are a huge profit center for the states, court systems and of course the attorneys, and you are the cash cow that gets milked until dry. See Exhibit: Robin Williams.

Not speaking from experience happily but plenty examples in our circle, and it’s the wealthy and upper-class that gets hit hardest since the judgments scale with income, and courts in the United States can impute a payout demand from any arbitrary earnings year. See also that Bloomberg article on the NY investment banker who got jailed for alimony when the GFC cut his income.

Like an old friend down in Florida who went through this said, aside from maybe a really bad illness (or maybe the cost of elder-care these days), the surest way to go from prince to pauper in the USA is to get dragged into divorce court. It’s why a lot of the consultants nowadays suggest one of the best asset protection strategies, if you have a lot of wealth, savings and skills is to go expat to a civil law country, at least if you actually want to start a family.

The correct advice is actually to not marry a broke person. Any lawyer will tell you they are the most dangerous in a divorce.

…was it Mencken (I paraphrase) who said: “…never marry someone with more problems than you…”?

may we all find a better day.

One reason is that the yield of Treasuries will go up.

Yield in the equity market is something like 1.6%. The rest is gambling on capital gains and losses, including the risk of total loss.

That’s not the same thing as being guaranteed 5.4% plus get 100% of your money back at the end. Lots of people do both. They have their gambling money, and they have the no-risk income money.

Primary dealers buy because they HAVE to bid. That’s part of being primary dealers. They will then sell this stuff to their clients or trade it in the market or hang on to it. Others buy because the yields are juicy.

There are about 20 banks who are ‘primary dealers’ of US Treasuries and they are required to purchase them as that is how all marketable US Treasuries are distributed in the bond marketplace and is the reason those 20 or so banks are designated as ‘primary dealers.’

And gold,silver will suffer no dividend

What´s about a corporate debt

There is no debt ceiling on corporate debt.

Thanks. A question: This corporate debt has also increased I guess. Is it a problem or is it manageable?

Lots of overindebted junk-rated companies will restructure their debts in bankruptcy court at the expense of stockholders, bondholders, and holders of their leveraged loans. That’s how it’s suppose to work. And it’s starting to work that way, finally.

…it’s no longer a casino with an open bar?…

may we all find a better day.

I’ve been waiting for this article for 2 weeks. Thanx Wolf.

S&P headed to 4300. Risk On light is blinking for those who want to take the ride. Fed handcuffs are off with pause, there is money to be made and insiders know it. 5.0% guarantees are better than 0 for all the retirees. Don’t expect everyone to jump to safety.

Who is buying all this debt? And where is the money coming from?

I’m buying some of it. Some other people here are buying it. 3-month and 6-month bills are paying something like 5.4% in interest. One-year bills are paying something like 5.2%. Yield solves all demand problems.

I am buying some of the debt and telling my friends to do the same .

It is that I’m getting a new kitchen over the next two weeks or else that money would go into some form of government bond.

Banks here aren’t moving the dial on money parked in accounts and the difference between 2% for parking money for two years at a bank (3% for 5 years) or getting 5%+ for anything between 3 months to a year is worth taking into account foreign currency exchange rates.

The banks here will do the same. I mean a 3% spread is worth it for them as well.

I’m in.

Wolf – what kind of duration treasuries will flood the market soon? How does that market play out in terms of yields and yield curve impact??

You can look up the current auction announcements here; a lot of everything:

https://www.treasurydirect.gov/auctions/upcoming/

How will it impact yields? They should rise some.

I think Treasury would sell short dated bill aka treasury bills. They may not want to sell a lot of long dated bonds, hence I don’t see any meaningful move in long dated bonds

Nothing is a given to repeat:

Heavy supply of fresh Treasury debt will refill government coffers run low by another protracted fight in Washington over the U.S. borrowing limit. But it won’t necessarily derail stocks, or the broader market, according to a team of analysts at CreditSights.

The Marketwatch team found that the S&P 500 index rose almost 5% over a six-month stretch in 2016 and 2018 (see chart), when a wave of Treasury supply hit the market.

Interest rate payments will become the biggest expense. Similar to using credit cards and not make payments will cause big problems.

Except the government can print and borrow more to pay its debt. You and I can’t do that with credit cards.

your the best on the plumbing but any thoughts on the endgame?

With too much sovereign debt, the endgame is always inflation.

Hi. There is a lot of talk that a significant percent of the drain out because of TGA build up will be taken care by RRP. While the liquidity will drain out along with Fed balance sheet tightening it will not be as significant as expected. Would love to know your thoughts on this?

I think we are in a similar scenario as beginning of 2022 as far as liquidity is concerned and we may see a similar reaction from risk assets.

Thanks.

“There is a lot of talk that a significant percent of the drain out because of TGA build up will be taken care by RRP.”

That’s the hope. But it didn’t happen during the last TGA drawdown. The ON RRP pays 5.05% with easy liquidity the next day for MM funds. After the next rate hike, it’ll pay 5.3%. MM funds aren’t going to give up on it very easily, given the next-day liquidity and the rate. It’s like a savings account with unlimited deposit insurance that pays 5.05%. And at the next rate hike, the rate jumps the next day on all the money you have in it. It’s just a really good deal for big funds.

That’s why it has been fairly steady for a whole entire year. And even before then, it climbed in a steady manner. It’s not correlated at all to the TGA. Look at the two charts. So I doubt the MM funds will buy bills with cash they have in RRPs. There would need to be a bigger spread between the two.

To get the RRPs to come down, the Fed may have to increase the RRP rate less than the other rates at the next hike. For example, it might increase the RRP rate by 10 basis points, and the other four rates by 25 basis points. I think that would drain RRPs at least some. But Powell brushed that off.

Up next are the budget talks. Both parties are salivating over where and how quickly, all this new hard earned money will be allocated.

Wolfman,

As per the website of the Federal Reserve Bank of St Louis, the debt to GDP ratio was about 107% in early 2020 and it has peaked to 135% in mid 2020. It has been slowly decreasing since mid 2020 and is now 119%.

This is encouraging as the USA at least is averting a debt crisis.

It will be interesting to monitor this trend compared to PCE and CPI.

Very Respectfully,

AD

“As per the website of the Federal Reserve Bank of St Louis, the debt to GDP ratio was about 107% in early 2020 and it has peaked to 135% in mid 2020.”

As per the website of Wolf Street, a week ago most recently:

https://wolfstreet.com/2023/05/29/update-on-the-us-governments-holy-moly-debt-interest-expense-and-tax-receipts-and-how-they-stack-up-against-gdp/

Dear Wolf,

What’s your take on MMFs taking cash out of RRP to buy those Treasuries?

In essence, TGA gets filled from money stashed at MMFs and not from bank reserves.

Sorry. You answered this question already. Thank you.

Wolf Richter

Jun 7, 2023 at 1:24 am

“There is a lot of talk that a significant percent of the drain out because of TGA build up will be taken care by RRP.”

That’s the hope. But it didn’t happen during the last TGA drawdown. The ON RRP pays 5.05% with easy liquidity the next day for MM funds. After the next rate hike, it’ll pay 5.3%. MM funds aren’t going to give up on it very easily, given the next-liquidity and the rate. It’s like a savings account with unlimited deposit insurance that pays 5.05%. And at the next rate hike, the rate jumps the next day on all the money you have in it. It’s just a really good deal for big funds.

That’s why it has been fairly steady for a whole entire year. And even before then, it climbed in a steady manner. It’s not correlated at all to the TGA. Look at the two charts. So I doubt the MM funds will buy bills with cash they have in RRPs. There would need to be a bigger spread between the two.

To get the RRPs to come down, the Fed may have to increase the RRP rate less than the other rates at the next hike. For example, it might increase the RRP rate by 10 basis points, and the other four rates by 25 basis points. I think that would drain RRPs at least some. But Powell brushed that off.

🤣😍 Thanks!

1) TGA was almost overdraft. In July & Aug TGA might rise to a lower high, keeping a large dry powder.

2) In 2020 the economy was shut down. The econ was comatose until we know what we don’t. The gov raided in while we have been comatose.

3) There is hope that the econ will stand on it’s own without a new money tsunami and lower inflation.

4) In July/Aug the Dow might turn down to the 30K/31K area, before testing the 2022 highs.

5) If we enter a recession in 2024 the gov will use it’s dry powder poisoning the wells to the R.

The boomers might park their money in the gov vault to preserve what they got.

Gen Z might use AAPL ski Googles to improve the industrial performance.

The Dow, after backing up at the top, might rise to a new all time high on it’s own backbones, with little gov support.

“debt out the wazoo” Scary. There are two storm clouds, no longer small and no longer on the horizon, that have the potential at some indeterminate future date to “wash” the U.S. and the Foreign-dollar “down the drain”. They go by the name of “foreign trade deficit” and “domestic federal deficit”.

These deficits have an insidious, if not an incestuous, relationship. Positive interest rate differentials are significantly responsible for the dollar’s exchange rate support. And an “overvalued” dollar in turn is the principal contributor to our burgeoning trade deficits.

The viability of the U.S. and Foreign-dollar as international units of account is threatened by the huge trade deficits. Given the present and prospective trade deficits, this situation is not likely to continue for long. Foreigners will simply be saturated with excess dollars.

The volume of dollar-denominated liquid assets held by foreigners is extremely large. Any significant repatriation of these funds, by reducing the supply of loan-funds, will force interest rates up – thus increasing the federal deficit and the burden of all new debt.

These events alone could trigger a downswing in the economy resulting in more unemployment, more unemployment compensation, less tax revenues and larger federal deficits. Truly a vicious cycle.

DM: SEC files temporary restraining order to FREEZE Binance assets – after investors pulled out $780M in 24 hours

The SEC is trying to get its hands on the assets of Binance.US – the American branch of the world’s largest crypto exchange.

The US government now has as its first financial mission the need to pay back the nearly $400 billion that it borrowed under ‘extraordinary measures’ from various pension funds from 01/19/2023 up until last Friday when it could no longer plunder any funds by using ‘extraordinary measures’ from various funds. These funds basically go nowhere and have no impact at all on the US economy.

U.S. trade deficit jumps 23% to six-month high as imports rebound

U.S. trade deficit widens to $74.6 billion in April, largest since last October

“Fiscal Responsibility Act of 2023” —

Hahaha. That was funny.

Yes, my kind of bitter humor. That’s why I included it.

I saw an excellent comment somewhere that since the USA has become internally energy self-sufficient (and even an exporter), the agreement with the Saudis, the petro-dollar, that dollars are to be used and inflation is to remain around 2%, no longer applies.

So there is every incentive for the US to default via inflation (as indeed it does) because there is no way for exporting nations to punishingly reprice US imports without boosting the value of US energy exports (in comparison with the UK which attempting the same strategy of shrinking debt/gdp through inflation has immediately caused food to reprice at 20% per year).

Recently I also read an article on inflation in Argentina (which I think is how the USA ends up, the US is very unusual in being a large country with a high per capita gdp they normally are not) with inflation at 100% annual, and people get on with their lives. Its not so bad. They buy freezers and spend all their money on payday. Life goes on etc.

As in now a tirade from all, and plainly obvious, the dollar is being devalued and the devaluation of the dollar is the cornerstone of the US government fiscal plans. There are and will be negative real rates in the US.

The US is in no way at all ‘energy independent’ and shouldn’t be as is just a fungible commodity.

You think they can store enough food in that freezer to last through retirement?

The “Argentina solution” for debt wouldn’t work in the US for all kinds of reasons, partly we have too many appropriations already set out and COLA indexed payouts, any attempt to “inflate away the debt” in the USA would just lead to the worst of the both worlds–high and dangerous inflation and worsening debt in addition. That’s also not something any country that wants to have a reserve currency can do (talking here about multiple countries with currencies in some kind of reserve or 3rd party transaction use, not just one).

The whole point of a reserve anything–commodities, a foreign currency, precious metals, industrial production–is that it holds it’s value through financial storms. If the USA’s own financial managers trash the US dollar through uncontrolled inflation, then the rest of the world ditches it even faster. Bloomberg has already been reporting on oil producers switching over to trades in other currencies (which you’re referring to) and a lot of Asia, even the Philippines, demanding payment in their own or alternative currencies or settlement means. Now that in itself isn’t a bad thing–it’s true that the overvaluation of the US dollar is a big source of a lot of America’s ills right now, esp de-industrialization and the job and health blight leading to the opiate epidemic. So some re-balancing and loss of reserve status can be helpful to us.

But that re-balancing isn’t good when it occurs on the backs of inflation leading to progressive de-dollarization (and not just to other currencies–it’s a death by 1,000 cuts with other sources of value).

Not to mention the domestic effects. Americans are facing record homelessness and crime, looting and shoplifting are sky-rocketing at everything from big box stores to little shops, the US birth rate collapsed to a new record low, the entire US entertainment industry is grinding to a halt with the writer’s strike and more strikes across industries are looming. And all this is connected to the crazy inflation in so many basic areas like rent and housing, healthcare, education and even food. Argentina actually has laws that make sure salaries rise automatically with inflation, that cushions the effect with workers. The USA has no such protections and the huge majority of Americans would have to eat those cost increases when even high paid professionals are struggling, which would demolish what’s left of civil society. Not a good thing in a place with 400 million private firearms. Inflation is a nation-killer in general, but for the United States even more.

With a rather large net trade deficit repricing exports to the USA probably not be offset by higher price on one or a few comodities exportet from the USA. Higher prices on imports may as well translate to higher prices on domestical products, in other words the price rise will be imported.

Rising cost of imports may slow them down bettereing the trade balance, but supply may slow down too. USA may even see what have happened elswhere, goods and coomodities are exported while the home market is starved.

Long time ago i said that the USA is becomming more and more like India, and not mostly because development and improvment in India. The “banana republic USA” is part joke, but also serious. USA have gained more attributes of third world countries this century.

True, esp the last paragraph. The Supreme Court’s “gift” of Citizen’s United basically giving us our own version of corrupt rent extractive oligarchs is pushing the US in this direction too.

The Federal Govt is crowding out the private sector.

Big Time.

I missed any concern, in the debates and machinations over expanding the debt limit, over the costs of servicing this additional debt. Was there any?

The appropriate time for those questions is when debating the budget, not raising the debt limit.

Hmmm. Powell kittenly increases short term rates to reduce economic activity and inflation — and the government increases spending massively to increase inflation.

Who is being herded into the treasury corral? Sounds like another Hotel California. Only the government can monetize fast enough to keep paying the nectar to attract the flies — until it won’t.

Yeah we’re once again reminded of Volcker’s wisdom and why his warning about sound money still holds true, and why Powell and the Fed need a crash-course on him quickly if they want to have any hope of preserving the dollar’s value and the stable society that comes with it. The current mess and Everything Bubble is due above all to the historic mistake of ZIRP with massive QE including the nonsense of the MBS purchases, combined with the $10-12 trillion of pandemic over-stimulus.

The inflation as it already is has been wrecking whole American communities over the past 2 years, so if anything the “2 percent target” (a made-up number as it is) won’t cut it anymore–we need some actual price reductions esp in areas like housing and rents, and healthcare, education and food costs, and to stop being so terrified of a temporary bout of deflation.

Rents and mortgages throughout the US are so high that homelessness is at record levels, tent cities sprouting up even in 3rd-tier cities. Shops and big supermarkets have had to literally change their policies due to the jump in shoplifting and looting, the US birth rate collapsed to a new record low and is headed even more downwards, and to say nothing about the international effects and de-dollarization. Again this is all on the Fed and the short-sightedness of ZIRP and QE, and their interest rate hikes and tepid QT so far (even with the recent data) have been too little too late. Only they can take the more aggressive steps needed.

The 30 trillion question:

At what interest rate was this debt issued ?

Inquiring Minds would like to know.

You’ll just have to follow the Treasury auctions to find out.

I’m salivating for long-term yields to finally go above 6%. There will be demand at those yields. Think of it the other way: the holders of that $30 trillion will finally make some money, and pay income taxes on that interest income, and they’ll spend part of that interest income and stimulate the economy, which is how it’s supposed to be, LOL

Is piling into long-term yields really prudent if the FED keeps chasing out of control gov’t debt/spending and inflation by raising rates? Wouldn’t it be wiser to reduce the interest rate risk and tradeoff some yield with 1 to 3 month T-Bill purchases?

Those who had the balls to buy 30-year bonds in 1981 made one of the best bond deals ever. But this took a lot of balls to do.

So the question is when are long-term yields high enough to turn this into a good deal over the life of the bond. There is huge disagreement over it right now, as you can see, because current buyers think that 3.8% is high enough for a 10-year. It’s not for me. But that’s where buyers are now.

actually a ”hey Wolf”,,,

please tell us what you WOULD consider the right rate to induce you to buy 10 or 20 year US Treasury Bonds.

Thanks,

It depends where I think inflation will be going — but this is a moving target, so today I don’t have a fixed number for the future. If the 10-year is at 6% and core CPI is shooting straight up, and the Fed refuses to act, I’m going to sit it out.

That means in four weeks (when they have to pay it Back) you’ll have another auction at 350 billion * (1+whatever interest they have to pay). Assuming 5%, that would be…. 367,5 billion. Four weeks later…..

Exponential growth always leads to a blowup of the system.

Only a small number of Treasury securities are four-week bills.

Geez Wolf. All excited at paying out ~600 billion in interest and getting back 100 billion in taxes. Some businessman you are. Gonna make it up in volume?

People forget to net them out. That’s why I always bring it up. People always just look at one side.

…not even binary thinking…

may we all find a better day.

The debt ceiling was raised by 4 trillion in the next 2 years with no caps on spending after the 1st year. Add Congressional supplimentals for Ukraine and other boondoggles and we’re into runaway spending. This budget deal was a sick joke. They didn’t cut squat. The Fed can’t do anything to stop the runaway inflation at this point. The only thing left is to

“Destroy the economy in order to save it”.

Powell & company are well on their way to do just that.

“Fiscal responsibilty act” !

Wait for the “Managing economic growth” act !

“Destroy the economy in order to save it”.

lol, truer words never spoken.

Since Mr. Wolf explained how Governments let inflation offset their debt, pretty sure now what the FED will do.

THANKS Mr. Wolf

We got into that above and the “inflate away the debt” delusion won’t work for the US, esp now. That just means cost for government appropriations goes way up much faster than the American national debt can be inflated away, also COLA indexed payouts go up, plus debt roll-overs. And we just wind up right back where we started, but with even worse deficits and national debt, and all the accumulating damage from inflation. So the worst of the both worlds.

And that damage is already bad and getting worse, esp when inflation hits basics like housing, food, healthcare, cars and education so much, esp with rent and mortgages like this. Record homelessness and tent cities all over the USA now, in fact there was some study showing when the avg rent in an American city goes up by just a $100, the homeless levels go up by around 10 percent, and a lot of places have had much worse rental inflation than that.

Theft, shoplifting and looting getting so bad that shops and chains are changing their policies. The US birth rate at a record low and collapsing lower. Things like the writer’s strike crippling the entertainment industry, quiet quitting and the other hits to American productivity–that’s due to inflation and the fact Americans are in real terms seeing pay cuts every month. And that’s even before getting to the international effects and the de-dollarization–it makes less and less sense to hold and use US dollars for transactions or as reserve currency if it’s managers don’t seem serious about preserving the value.

There’s a reason the whole idea of inflating away debt is mocked as a 3rd world or “banana republic solution” by serious economists–it usually backfires and doesn’t work, makes the debt worse and causes even more damage in the process, esp for a country like the US. We’re suffering it now above all because the Fed got caught up in the foolishness of the “wealth effect” and the disastrous ZIRP and especially QE with MBS purchase policies that caused it over the past decade. And the Federal Reserve needs to be a lot more aggressive with the rate hikes and even more, the QT steps to undo this mistake, or else the downward spiral gets worse.

Even on-line shopping getting brutal due to digital thieves. Have been around the bush with Amazon, Walmart, and McAfee.

Don’t leave your credit card with Amazon. I did that and got hacked. If fact don’t leave it with any vendor.

The Fed/Central bank elite will keep raping America and capitalism until the entire country is 3rd world depression chaos and just retire elsewhere. That is the path I observe taking place. We had civility in the great depression where people lined up for work. Today we have civil strife where people just take anothers, violently.

Wolf,

You’ve mentioned Cash Management bills in a previous comment – what are these and how do they differ from other bills?

https://www.treasurydirect.gov/marketable-securities/cash-management-bills/

(A nation) is poor precisely because it has been ruled by a narrow elite that has organized society for their own benefit at the expense of the vast mass of people. Political power has been narrowly concentrated, and has been used to create great wealth for those who possess it.

This site is a must-read, both for Wolfs articles and the comments section.

The take away from it all for now is: the debt Ponzi scheme is still working and looks like it will continue working for most peoples time horizon. That horizon for me is 3-4 years.

Certainly this year is in the bag. Next year (2024) is an election year so it seems like everything possible will be done to keep the train on the rails. 2025 seems to be the first point at which you could imagine that things become uncertain.

The black swan event that could upset everyones known-unknowns is the war(s) our masters talk a lot about and may or may not actually want to see occur.

Our politicians talk war: “dying Russians, the best investment ever”, but really, they are so ignorant they actually believe they are speaking only to their domestic audience. Meanwhile, our competitors hear war talk and perhaps believe it.

The black swan might be grey or pretty close to white. Natural disaster strike ever now and then and they will do again. Natural disasters have brought down society before.

Modern society is technology dependent, we may have reached the point where some fault or malfunction cascades to shut down society in a rather large area for a long time.

Talking about keeping the train on the rails, there is the possibility that someone have pilfered the tracks, sleepers and ballast where the train is to travel a little into the future.

Wolfman, I just read now on Wall Street Journal that $1 trillion of US federal debt to be financed at 6% rate :-/

Very Respectfully, AD

That’s just $60 billion a year. In the $4 Trillion budget.

Hi Wolf, I explored the treasury website a bit. Currently it seems that treasury is paying ~$900 Billion in interest on $31000 billion of debt, so the interest is roughly around 3%. How long it will take before most treasuries will be rolled over above 5%?

Wolf said: “This drawdown of over $1.5 trillion over the 12 months from the end of 2020 through late 2021 moved $1.5 trillion in cash from the bank (the Fed) directly to the markets.”

—————————————–

What do you mean by “directly to the markets”? You dont mean the financial markets do you? I contend it is not to the financial markets but to vendors, consumers, ppp recipients, etc. They money flows into product purchases, savings and various directions with perhaps only a small portion ending up in the financial markets.

Extraordinary GSE (government-sponsored enterprises) growth is worthy of close examination. GSE assets expanded a record $352 billion during Q1 to an all-time high $9.540 TN. This surpassed the previous record increase of $325 billion during pandemic crisis Q1 2020. The pre-pandemic record was tumultuous (subprime crisis) Q3 2007’s $144 billion, which exceeded the previous record $136 billion during Russia/LTCM crisis period Q4 1998 – that had eclipsed the previous $60 billion quarterly high from bond/derivative/Mexico crisis period Q4 1994.

GSE assets inflated a record $1.022 TN, or 12.0%, over the past four quarters. This was double peak one-year growth from 2020 ($523bn). Record pre-Covid peak one-year growth was Q2 2008’s $418 billion, which exceeded Q3 1999’s one-year gain of $353 billion, and trounced Q4 1994’s at the time record $151 billion.

The bottom line is that GSE growth has been nothing short of phenomenal. GSE assets surged $1.248 TN, or 15%, over five quarters, and $2.410 TN, or 33.8%, since the start of the pandemic (13 quarters). FHLB (Federal Home Loan Banks) Loans/Advances surged a record $222 billion during the quarter to a record $1.042 TN. But, as informed by FHLB financial statements, booming Q1 growth was not limited to loans/advances to member banks. Strong expansions in “repo” and “Fed funds” assets – other key avenues for bolstering system liquidity – powered record ($317 billion) FHLB growth to an all-time high $1.564 TN of total assets (having doubled year-over-year).

1. You’re talking about “assets.” That’s the opposite of “debt.” This article discusses government debts.

2. The vast majority of the GSE assets are mortgages they bought (Fannie Mae, Freddie Mac, primarily). The GSEs totally dominate the mortgage market and securitize the mortgages in to MBS (“Agency” MBS), and then sell those MBS to investors. The surge in home prices has led to a surge mortgage

3. A much smaller portion of the assets are held by the FHLB. It issued a record amount of bonds (debt) to have the cash (asset) to support the banks. Some of the proceeds, they lent to banks. The remaining proceeds, they put on deposit at the Fed (reserves) to earn 5.15%, and put in the repo market to earn 5.05%, to earn some interest on cash that they want to keep ready in case banks need more liquidity support.

4. The FHLBs are the lenders of second-to-last resort to the banks; the lender of last resort is the Fed.