Powell is going to mention this with some frustration in his voice.

By Wolf Richter for WOLF STREET.

The labor market was supposed to loosen as the Fed hiked rates to tamp down on demand just a little to de-fuel the inflation fire, and the labor market did get a little less tight, but it remains stubbornly tight. Today’s report on job openings, layoffs and discharges, hires, and quits by the Bureau of Labor Statistics hammers this home: while the labor market got a little less tight in some corners, it tightened further in other corners, and job openings “unexpectedly” rose again. Powell is going to mention this at the next post-meeting press conference with some frustration in his voice.

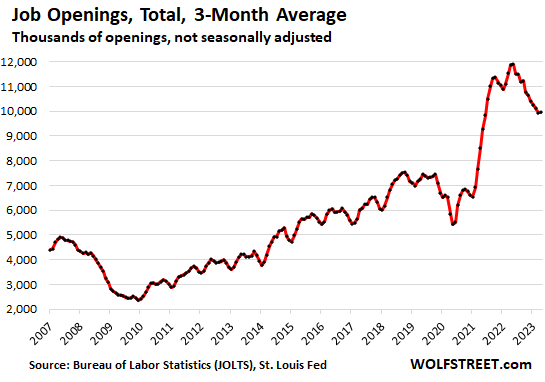

Job openings in April rose by 358,000 to 10.1 million seasonally adjusted; and not seasonally adjusted, they jumped by 1.05 million to 10.6 million. This is not based on job postings, or on fake job postings, or whatever, but on surveys sent to 21,000 businesses, asking them about their actual workforce details.

The three-month average, which eliminates the whiplash-inducing drama of the monthly ups and downs, was roughly unchanged in April from March (not seasonally adjusted) and has remained close to the 10-million range all year. The slowdown occurred last year, with openings dropping sharply from the astronomical zone in April, but then the drop “unexpectedly” fizzled into the end of the year and then stalled. Job openings were still 37% higher than in 2019 at this time.

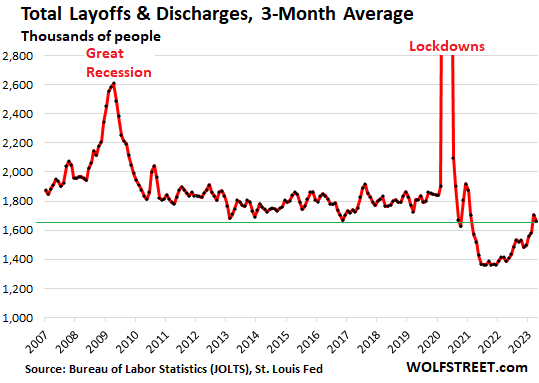

Layoffs and discharges fell again, after having ticked up from the historic low in April last year, and remain below the pre-pandemic Good Times low.

Companies always discharge and lay off people for a variety of reasons. During the Good Times before the pandemic, actual layoffs and discharges averaged around 1.8 million per month. In April, layoffs and discharges dropped to 1.58 million (from 1.84 million in March). The three-month moving average dipped to 1.66 million

These are actual discharges and layoffs by employers in the US, not announcements of global future layoffs or whatever, that may not even take place in the US.

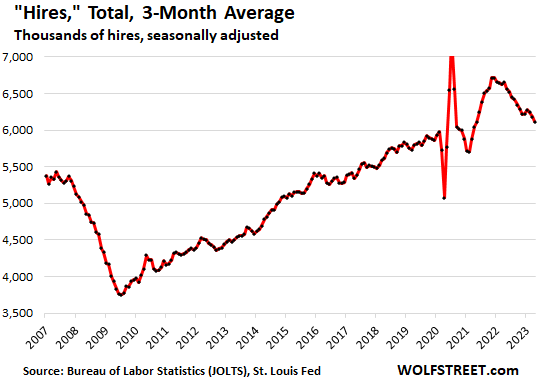

Hiring ticked up again in April, after some dips in the prior months. The three-month moving average dipped to 6.11 million hires in April, continuing a slow decline, but is still up 5.4% from the same period in 2019:

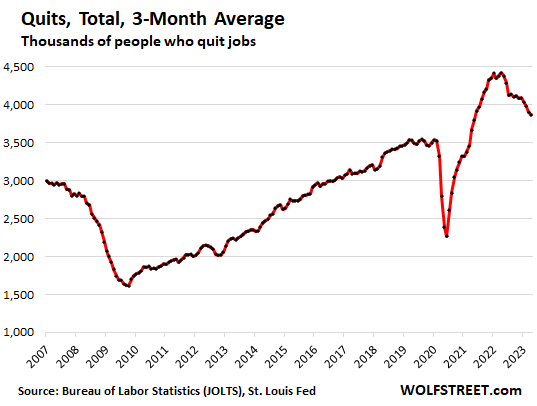

The churn in the workforce is subsiding. The bombastic media coverage of global layoff announcements by big US tech and social media companies, in combination with less-desperate efforts to hire by them, has had the effect that employees are less confident the grass is greener on the other side of the fence, and they quit their current jobs less frequently, and the massive churn in the labor force has subsided.

In April, 3.79 million workers quit their jobs voluntarily, back to April 2021. The three-month average was still 10% higher than in the same period in 2019. There is still a lot of churn in the labor market, as workers are trying to arbitrage the tight labor market to improve their lot. But the churn is way down from a year ago:

Job openings in major sectors.

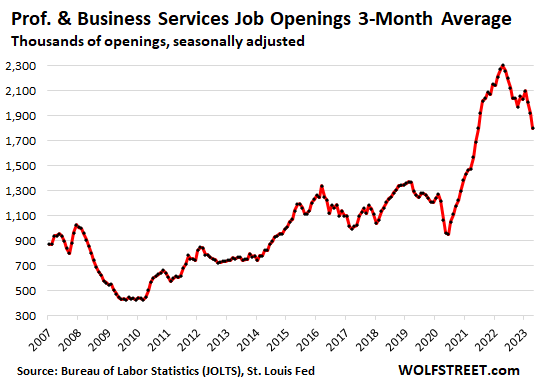

In professional and business services (a big category with 22.4 million employees), the three-month moving average of 1.8 million job openings is still up by 39% from the same period in 2019, though it has deflated from the astronomical levels in 2021 and 2022.

This sector includes Professional, Scientific, and Technical Services; Management of Companies and Enterprises; Administrative and Support, and Waste Management and Remediation Services. Some of the tech and social media companies are included, others are in “information” or in other categories. Included are

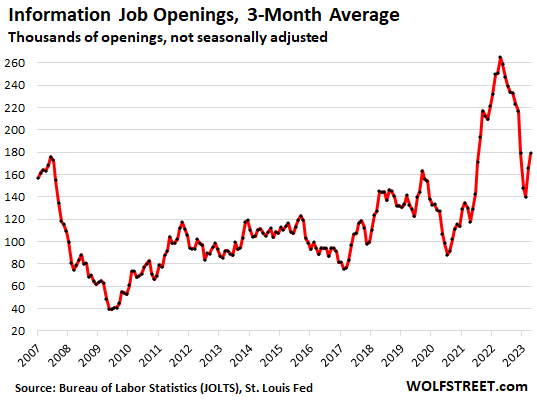

“Information” (a small sector with 3 million workers) contains some of the tech and social media companies with big layoff announcements. After a steep plunge late last year through December to the worst levels since the Dotcom Bust, job openings have bounced back some, and the three-month average, at 180,000 openings, is still up 35% from the same period in 2019.

The sector includes web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications.

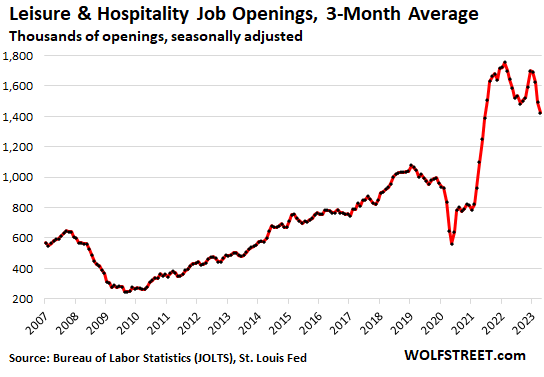

In leisure and hospitality (16 million employees), the three-month average dipped to 1.42 million job openings, still up by 42% from the same period in 2019:

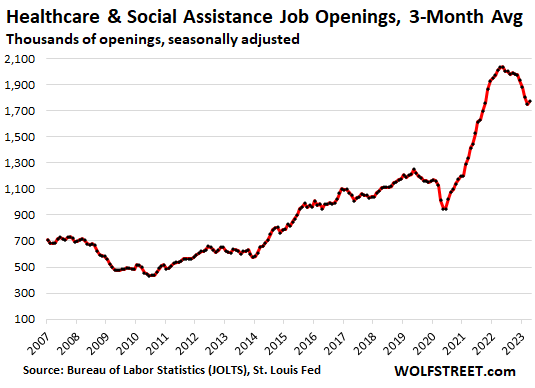

In healthcare and social assistance (21 million employees), the three-month moving average of job openings ticked up to 1.77 million openings, after having fallen for months from the astronomical zone. They’re still 47% higher than in the same period in 2019:

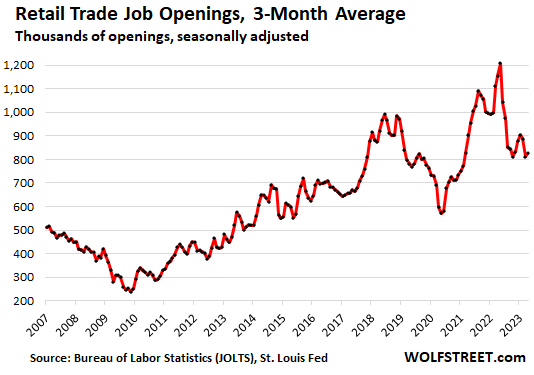

In the retail trade (16 million employees), job openings stabilized at normal levels last year and have stayed in the same range. The three-month moving average of 825,000 job openings was up about 5% from the same period in 2019:

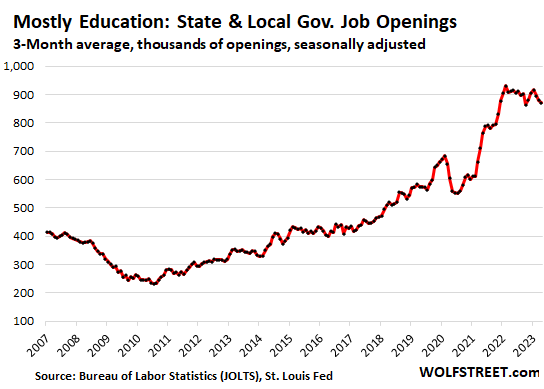

In education/state & local government, job openings have stabilized last year at very high levels, as many school districts still have a hard time recruiting enough teachers. The three month-moving average of 870,000 job openings was 52% higher than in the same period in 2019:

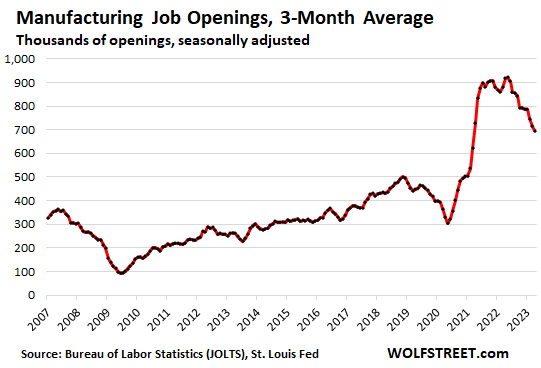

In manufacturing (13 million employees), job openings have steadily decline from the astronomical zone. The three-month moving average of 695,000 openings is still 55% higher than in the same period in 2019:

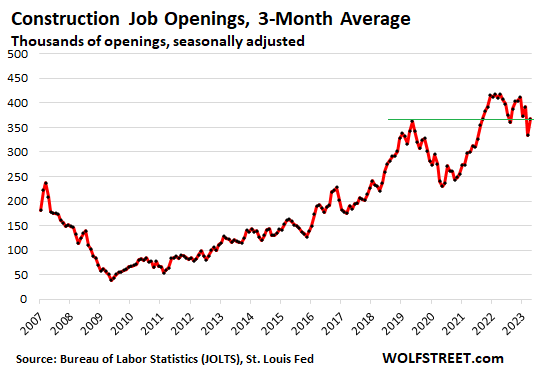

In construction (8 million employees in all types of construction, from powerplants to single-family housing), job openings bounced off the dip earlier this year that had likely been caused by the horrendous rains, snow, and flooding in the West, particularly in California. The three-month moving average rose to 367,000 openings, up by 7% from the same period in 2019:

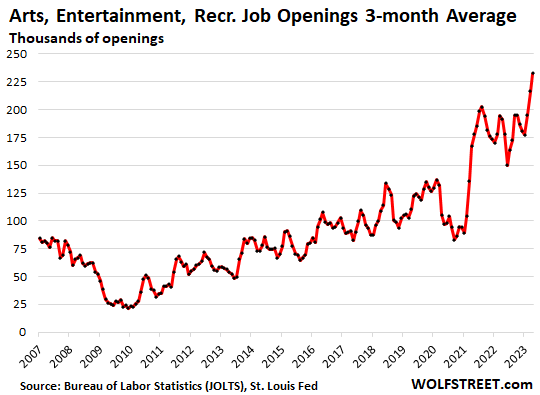

In Arts, Entertainment, and recreation (2.3 million employees in spectator sports, performing arts, amusement, gambling, recreation, museums, historical sites, and similar), job openings have shot to record levels, as Americans are now shelling out large amounts of money for experiences they stayed away from during the pandemic, and the sector is trying to staff up for it.

The three-month average rose to 233,000, up by 111% from the same period in 2019:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Americans are historically solvent and hyper-employable if not gainfully employed already. This seems like good news to me.

Harker said pause in June. No more hikes.

Nah, not what he said.

He said he is “inclined to skip” a rate hike in June but that the jobs report on Friday “may change my mind.”

So now we had the JOLTS report, step one, and on Friday, we’ll get the jobs report, step two. And that’s just Harker.

Bullard wants TWO more rate hikes — he has gotten pretty much everything he has wanted so far. Several others would prefer one hike.

You just will have to be patient and see.

There has been quite a bit of talk about “skipping” a hike in June (“skipping” is the term Harker also used) and then hiking again in July, including right here on Wolf Street 10 days ago: “Six-Month Treasury Yield Begins to Price in One More Rate Hike. Either mid-June or possibly in July.”

Definitely worth the price of admission.

Oh, wait a minute, it’s free.

Pure wisdom dispensed daily.

can’t wait for those student loans to re-start being paid

just $4b per month

of course our exponential debt will keep building

like large sand-pile – keep adding grains of sand til avalanche happens

Seems like a pause or a skip lol is on the menu according to Fed whisperer… NFP could change things but I doubt CPI will change anything if it comes in around 4% yoy that’ll give them the pass they crave

The dumbest shit I’ve seen today is the skip rationale…. Let’s wait and see if we get lucky and inflation goes away…. Like we already tried that in 2021… Idiots… Plus after 500bps of hikes what is one more 25 gonna do??? Cause Armageddon lol

Wolf I’d love to see updated numbers on the housing data yesterday that came in hotter then expected. This seems like a reason to hike again. How could rent inflation come down if housing prices level out or even pick up

Someone from the fed (waller?) just noted (according to bloomberg) that the recent housing data should affect their views on inflation. Sounded hawkish, but I don’t have details and can’t find any online, which seems odd.

They won’t even look at overall CPI. They will look at core, at services, at core services, at housing, and at durable goods.

What has pushed down overall CPI is the collapse in energy prices — everyone knows that. What they’re looking is underlying inflation.

Fed always seems to say something that can be taken either way and people always jump on it. They are not going to “we are going to hike”, which will be taken as “…no matter what”. They have to give some type of conditional out.

I don’t see a pause. But maybe I’m doing the same as those I am criticizing.

I wish they would speed up QT vs more rate hikes. It seems they were unprepared for the increased interest income flowing back into the economy propping up demand.

Inflation is becoming entrenched in the US and our friends in the UK will have a currency crisis on their hands if they’re not careful. The job market will remain red hot as long as fiscal policy remains highly stimulative and monetary policy is skipping and pausing its way to a de facto higher inflation target. If housing becomes a problem the Fed can just start buying agencies again to pin mortgage rates. If auto sales become a problem the Fed can create an SPV and indirectly buy auto loans. The secret is out: nobody in the US who really matters politically has to take losses. SVB et al were proof of concept.

If I’m a politician I’m thinking “Next time there’s an economic hiccup, just print trillions and hand the currency out to everyone’. Problem solved. We’re all rich. Prove me wrong. Jobs a plenty. (This is sarcasm for the sarcasm impaired).

If I were a politician, I’d believe the people willing to throw me a vote for giving out money are dumb enough to believe whatever scapegoat I tell them when the chickens come home to roost.

With 25%+ rent inflation over 2 years, the chickens have already come home to roost.

The difficulty is getting enough people to accurately pin the rap on DC borrowing/printing/spending.

DC is a past master of blaming 3rd parties for the consequences of its own sins.

The rich are no saints…but they don’t run the money printing machinery in DC and that is what overwhelmingly affects the macroeconomy.

A good example? In the midst of pretty historic inflation, the “debt ceiling triumph” clawed back a tiny amount of the Covid trillions.

And, has been well pointed out elsewhere, somehow the Covid “emergency budgets” have become the new baseline budget – htf can DC try to pull that off with a straight face?

It would be insightful to see this type of analysis of job openings compared to a “job quality” metric: number of hours per week worked, average time spent in a position before leaving/fired, % of able-bodied adults that has ‘checked out’ of the workforce, average pay vs. average cost of living (to see the concentration of these jobs in expensive urban areas), etc.

It would be fascinating to see what percentage of the job openings is due to both the domestic and global population aging/declines reducing the number of employable people. Would have to determine based off of labor participation of different age brackets. I think of China and Japan as the example of where we are headed globally and in that situation there is always more work needed to be done then labor able to meet the demand. I know prime age was down after the lockdowns, which would invalidate this and still has me puzzled unless it’s millenials staying home to start having kids or figured out it was just more worth it to have one parent stay home amd one work?

Prime age participation rate:

It would also be interesting to see how many job openings are due to not wanting to hire older workers.

I have some friends like that with impeccable tech resumes, who’ve given up looking because no one is even paying attention to them anymore.

But that has always been the case — only this time around, as we’ve gotten older, my friends and not some older strangers fall into that age group.

The fact that this stuff has been happening forever and is therefore a constant more or less means it has little impact on what the charts show over time. In other words, this constant is not responsible for the big spike in job openings, which was caused by new factors.

This really sucks and needs to be more openly castigated as much as any other forms of discrimination.

Nearly everything I’ve ever learned was invested in me from people my senior who were patient & generous enough to humor my curiosity and/or seasoned enough to spot whatever nascent abilities I displayed and to foster them.

We ignore our own talent and import foreign tech workers due to an alleged shortage?

No way…….

I had a customer on the phone this week who said her boss told her “If I had seen your AOL address on your resume I would have skipped right over you.”

SpencerG,

Yes, they’re ALL looking for little things that will give your age away before they even commit to an interview. Writing a resume to conceal your age past 40 has been an officially taught strategy for as long as resumes have existed.

Those strategies work when you’re 45 or in your 50s and look fairly young. And age discrimination isn’t really that bad into the 50s. But when you’re 60+, those strategies no longer work. You cannot hide your age anymore.

Age discrimination is totally ingrained in the working world, and you cannot stamp it out. Maybe it’s just human nature.

The younger generations that are now committing this age discrimination will also face it in due time. What goes around, comes around.

So my advice to the younger generations is this:

Get ready for age discrimination yourself. Don’t deny its existence. Plan for it. It will hit anyone below the top executives. If you don’t make it to the top by then, there are ways you can dodge it, such as starting your own business or consulting services, etc., where age is often an advantage. Or enter politics, LOL

The answer to age discrimination is to work for yourself. It’s getting harder and harder – guess why that is so as regulatory issues such as Sarbanes Oxley make it harder and harder for Large enterprises to engage with small enterprises

Companies will hire you as a contractor, though they would never consider you as an employee.

Encourage the development of a deep desire for independence in your kids – of course the schools will be working hard to foster the opposite attitude.

Fascism is nothing more than corporatism and communism is simply making the entire nation one large corporate entity.

No article on the US housing market?

This is not a housing-only website — housing is just one of many topics. However, an article is coming on housing in a few hours. I know that’s a long wait, but hang in there.

Yup – just meant that thought you had been recently dropping an article on the Case-Shiller every time it came out.

yeah, “The Most Splendid Housing Bubbles…” is a monthly flagship series that I have done for years and that takes a lot of time to do, and usually it gets a huge amount of traffic, a lot of it from search, Google News, and other Google properties. But then periodically, this slows down, and it gets less traffic from Google, like the energy is gone. And so I learned to take it off for a few months, and then restart it, and WHOOSH, the traffic is back.

The internet is a strange place.

1) Chicago PMI is down to 40. Chicago PMI is Apr high. If so, for funfunfun :

5) SPX might rise to July 7/8 2021 BB : 4,361.88/ 4,289.37, before losing

it’s grip of : Aug 9 2004 to July 17 2006 Lazer.

Trajectory as predicted.

Possibly why labor market is rise in demand not so astonishing.

According to FRED, Non financial business was accumulating l cash after 2010– ten years of low inflation and low interest rates. No great reason to spend it or invest it when inflation is low, and interest rates are low.

Now–inflation is causing that cash to leak out of the bucket– good reason to consider spending it putting some people to work for your business rather than watching the money go down the drain.

Real consumer spending is rising nicely. As long as there are people to buy stuff and services, there will be workers hired to make and sell stuff and services to them. The simple fact is that the current level of interest rates is not much above the average rate since 1970. The overall economy can function well at these levels, as we have seen. Not so sure about 7% or 8% or more, which will likely be needed to knock inflation back to 2%. The dirty little secret (well not so secret on this site) is that high interest rates increase disposable income to many retirees, an ever growing segment of our economy.

The economy will not overheat if people are spending most income from interest earnings. Much preferable to crypto and other insane capital gains or real estate equity.

I like your point about Bullard getting what he wants, & he’s non-voting. In December, he said 7% was a real possibility to push down core inflation to the Fed’s 2% target. The labor market appears far from showing real signs of rolling over. As we tick through major reports (jobs, inflation, unemployment claims, etc) through the summer, it’s going to be very interesting to see how well these metrics old up against the pause / cut rates screaming.

Off topic but interesting none the less :

Washington’s capital gains tax collects $850 million, over three times the estimates.

This is a brand new 7 % tax on the sale of assets over 250k and according to the department of revenue all that revenue came from just 3190 returns with 2500 extension filers yet to be counted. My math may be fuzzy but I think that works out to an average capital gain of 3.8 million. If so, there’s a lot of money sloshing around out there.

I listen to a wide variety of podcasts covering the investing universe – its fascinating the diversion when the podcast hosts are older/more seasoned vs the younger ones (lets say 50 and younger) the young ones see zero 0r very few issues and completely invested personally and financially in the tech area and to be truthful have done and continue to do VERY well- the more older see -doom-gloom- problems everywhere – it is a very confusing world out there

The current mania hasn’t popped. There’s still way too much money sloshing around. It’s not clear to me that the fed has had a significant impact on slowing the rage. Some, but not enough. The result will be continued inflation.

patrick,

Cryptos have collapsed something like 60%. Stocks are down, with the S&P 500 down something like 15%, the Nasdaq down over 20%. Housing is down year-over-year now too, not just from the peak.

Do these “younger ones” you refer to not know that? Or are they telling you that they BELIEVE they will still do well, after having taken all these losses???

The narrative has changed when the Nasdaq 100 is up 32% YTD with many mega cap tech companies at or above all time highs when interest rates were rock bottom.

Many of the younger folks weren’t investing in 2007-2009 or 2000-2002, and certainly not in 1966-1982, the last time chronic consumer price inflation was a big issue.

Ah yes , unbreakable belief in Infinie good times. I was there in 2000 and got rekt and still sit on intc and csco with crippling losses. Won’t do it again and feel sorry for younger folk who will experience the same pain.

I was too young in 2000, but in 2008 I was one of the young fools, fully leveraged up. Lost almost everything. I won’t make that mistake again.

The younger ones have rarely seen above 5% Fed Front rates. These high rates changes everything for all asset classes.

I have seen many homes for 1 million USD, with annual rent of $40K or less.

One can easily park 1 million in bonds/bills and get 5% plus without doing absolutely anything.

what is happening in the market is madness but everything would be reverted back to mean which is quite low unless FED starts QE and cutting rates.

Kissenger, Jamie Dimon and dozens of “captain of industry” are in China right now working to strengthen China trade in the current political atmosphere of “decoupling;” i.e. the captains of industry are working to re-couple and make the relationship stronger than ever.

One aspect that appears not discussed is India’s potential, a nation with some disputes with China. Perhaps some of these job shortages could be outsourced to India in the way that has held down inflation with China. Getting the jobs to India could take care of another few decades and “let the good times roll again.” Ridiculous that basic staples like soap, etc have runaway inflation when every country makes them for low cost.

At least in the short term let’s hope that the China effort can cut down this labor shortage. China even wanted to enter the American housing construction market, certainly a welcome event. In the 1980s the Japanese automobile competition gave us the quality we enjoy today Perhaps China and our other foreign friends can help with our moribund big Wall Street construction pseudo monopolies.

With Jamie Dimon’s well known exceptional banking abilities, this China conference is bound to be a roaring success.

India will never be a “competitor” to China. Having been there over a dozen times, I find the infrastructure almost non existent (okay – a slight exaggeration) and the corruption almost unimaginable.

American labor should realize that corporate America is desperately trying to re-shore a portion of their production portfolio because the cheap labor country has become a muscular teenager, no longer manageable like before.

What they have always been selling is the status of the American family, making family level wages and benefits, and crown thy good with brotherhood from sea to shining sea.

Well, it’s high time for the ones that make it possible, to earn a family level life style in the United States.

The business organizations continue to ram through price increases in order to accomplish their less than family level life style employee compensation packages. The era of the Fed funding the off-shoring of American industry with zero pct interest rate policy is apparently coming to an end.

The Fed has created a financial monster that is neither efficient nor necessary. It exists only because of concentrated power and wealth controlling the levers of government. Like the inept Fed.

Watching the immaculate ascent of the stock market, in the face of a coming hurricane, has convinced me that the fix is in.

A plan to lay the losses off on the index funds, who are forced to buy to match the value of the index. As usual, the totally compromised Fed is the silent banker creating the hysteria that entices human beings to gamble, as a consequence of that’s what human beings do, sometimes, when sufficiently enticed.

My understanding of the facts leads me to an inescapable conclusion about what the Fed should accomplish at the June 14th meeting of the FOMC. In my mind, the decision is a simple one as is the message:

The FFR will be raised by 25 bpt and the rate hikes will continue as long as prices increase.

At this point, the Fed can’t continue to play coy and, at the same time, retain their raison d’etre.

1) The best sector is Art and funfunfun, the smallest one.

2) Next is the Prime Age participation rate, slightly > 2019 high. From 83.0% to 83.2%, an UT.

3) States & local gov are flat at 900K

4) Chicago PMI that cover real stuff in – MI, IN, IL, IA and WI – is down below 50 negative since Sept last year.

I was in Safeway the other day. There was one checkout lady, and she was elderly and handicapped, working like crazy to keep the line moving. All the other checkout lines were unattended. The line was so long I almost walked out. After 15 minutes I finally got up to the nice checkout lady and asked her why there were no more checkout lanes. She said “No one wants to work”. So there it is. This is what happens when you have 7 million abled body people in the prime working age who are paid not to work.

Don’t worry. This debt ceiling deal will cut the deficit from 1.7 trillion to 1.6 trillion and everything will be great.

Well, I have noticed several other swaggering price increases since the forthcoming, favorable legislative concerning the merger of Fry’s and Safeway/Albertsons.

The most obvious exhibition of monopoly power in our western state was that the price of fuel rose from being a historically low cost per gallon to being the highest cost gasoline in the nation.

Who cares.

Keep going…

Nobody wants to work for peanuts, or put another way, stand around doing mostly thankless, mind-numbing, repetitive work for 1/3 of their day or more, just to scrape enough to keep in the game, and not much more.

It’s because Safeway like every other retailer ,wants u to use self checkout.No wages or benefits.

Given that unemployment is historically low and is constantly confounding the FED with its resiliency in the face of rising rates, how can anyone still try and spread the idiotic trope that no one wants to work?

People who get their economy wide employment views from elderly handicapped cashiers at Safeway deserve to look like the fools that are.

I have a two-part question for the knowledgeable community here. If the prime age workers are working at about the same rate as 2019, why do we have worker shortages? And if the worker shortage persists long enough, could it have the effect of eliminating jobs as a result?

Wolf is always talking about home builders that move inventory by finding a price that gets people to buy houses. Could millions of employers have mispriced their wages/salary, and hence can’t find workers?

As an older millennial, I remember sending 100s of resumes in the 2000s and taking any job I could get. By the middle 2010s something changed and I started getting hired more easily. I started my construction company in 2019. I figured I just got older and wiser, but maybe that was the beginning of the worker shortage? Maybe I don’t deserve all these good jobs I’m getting and should be grateful for the worker shortage!

I will say what is appropriate for me which is probably not for you but here goes:

The period you site as your base line 2010 and beyond is the time period of economic stimulation by the QE hypothesis testing.

The labor market will sort itself out like the tortoise rather than the hare.

I can’t speak for everyone or every industry but I can for ours making truck equipment.

Our labor shortage of 2021 to now is due to two things:

#1 a massive glut of orders to fulfill. The speed and magnitude of orders was unmatched in my 20+ years of data…and probably ever in our company history. Just when our backlog appeared to be fading, it shot back to the moon. Hit a record high last week. I attribute this entirely to overstimulus.

#2 everyone else in our area competing for the same workers with the same problem #1. Normally we and the surrounding employers get busy at different times periodically. This time we were all swamped all at once. The folks we might normally tap for outsourcing overflow parts were buried in work too, so outsourcing became unworkable too.

We have so far been able to raise prices, and raise wages to adjust because we are a slightly above average employer in the area who provides great healthcare. Not every business has been able to do the same. Two local restaurants recently closed “temporarily” due to no staff. Another larger business had to close their doors but they were paying minimum wage.

It has been moderately painful trying to respond to this labor shortage but we still call it a “good problem to have” being this busy. Slow sales hurt a lot worse.

Those struggling to attract and retain talent are generally crappy businesses and bad places to work who generally retain staff out of worker desperation, not choice.

I do believe there is a demographic element to these shortages too, but I chalk up 80-90% of the blame to overstimulus. Covid shutdowns slowed our economic engine down briefly. Feds meant to get it back up to cruising speed but accidentally pegged it at red line in an attempt to keep the circus going.

Dang: I suppose I am one of the people who could be grateful for QE which brought house prices down and transferred some power from employers to employees in the 2010s. Kind of ironic now that I’m the employer. Would you care to elaborate how you see the labor market sorting itself out? I assume long-term, you think labor will go down in price.

Random Guy 62: Thanks for the insight, especially the part about the economy being pegged at redline. I’m grateful for the work, but who are these drunken sailors with so much money to spend? The stimulus payments were like $3k that’s barely enough for groceries. The crappy companies you speak of are kind of what I was wondering about. Are they holding out for cheaper labor, like some of the current holdouts in real estate?

Thanks for the replies!

My general understanding is that people come to the US for jobs, and opportunities. Some things never change…

Pure capitalism and the NAFTA nightmare…

Is it China, India or rather Mexico that is emerging as the new manufacturing hub of North America?

Japan and Germany have had their head kicked in many a times for various reasons but at least they came away with the understanding that you never abandon your manufacturing base.

That job you now have, needs to last 30 years or longer to pay off that million dollar mortgage that you are so proud of owning.

The current tight labor market means nothing!

George W,

re ‘abandoning your manufacturing base’

The USA may be guilty of that, but it still has significantly more jobs in Manufacturing (13 million) than in Construction (8 million).

Here in the UK, according to the Office for National Statistics:

UK Manufacturing: 2.6 million jobs

UK Construction: 2.3 million jobs

Given the significant and speedy rise in interest rates, combined with the magnitude (and relatively low duration) of debt in many industries, should one expect corporate earnings to turn south at some point?

Haven’t seen the term “earnings recession” for some time…

And might that be a likely first step toward the end of the current low unemployment era?

Wolf, can you shed light on today’s unemployment rate number that jumped from 3.4 to 3.7%?

I’m finding it difficult to square the fact that the numbers from the past several weeks/months have shown new jobs added being significantly higher than initial jobless claims. If anything I would have expected unemployment to drop lower.

It seems to me that either the unemployment rate is wrong (too high), or some combination of the jobs added (too high) and initial jobless claims (too low) is wrong. Or the unemployment rate calculation has some additional factor I’m not considering.

I guess the unemployment rate could make sense if that the increase will be accounted for in the next data for Quits, given that JOLTS spiked again.

https://wolfstreet.com/2023/06/02/landing-got-cancelled-job-market-still-at-cruising-altitude-with-some-bumps-even-wage-growth-for-nonsupervisory-workers-accelerated/

Nothing short of a black swan event will slow this train. Shock and awe.

Thank you for being a voice of positivity and inspiration in a sometimes negative world.