Either mid-June or possibly in July.

By Wolf Richter for WOLF STREET.

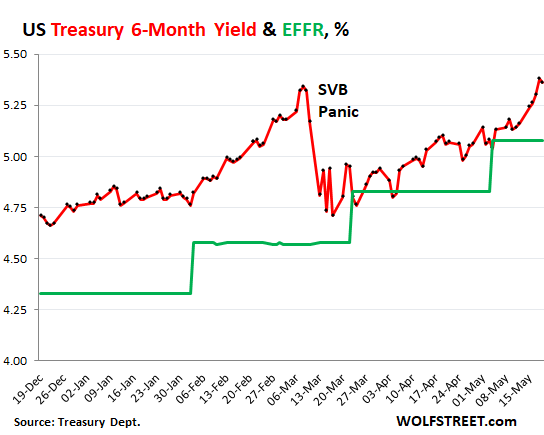

Treasury yields and mortgage rates rose essentially all week and passed some milestones for the first time since the collapse of Silicon Valley Bank:

- The six-month yield hit a 22-year high (5.38%)

- The one-year Treasury yield edged above 5%

- The 10-year Treasury yield rose to 3.7%

- The 20-year Treasury yield edged past 4%

- The 30-year Treasury yield rose to nearly 4%

- The average 30-year fixed mortgage rate rose to 6.90% (Mortgage News Daily).

But what is really interesting is the action in the six-month yield (securities that mature in November): Buyers and sellers in this section of the bond market got over their bank-panic and now are starting to price in another rate hike.

The six-month yield now prices in one more rate hike.

The six-month yield closed at 5.36% on Friday, after the 5.38% close on Thursday, both the highest closing yields in 22 years (January 2001), having now entirely shaken off the spooky collapse of Silicon Valley Bank.

The effective federal funds rate (EFFR), which the Fed brackets within its target range between 5.0% and 5.25%, has been at 5.08% since the last rate hike. Another 25-basis point rate hike would bring it to 5.33%. That additional rake hike would put the EFFR just below where the six-month yield is already today.

The part of the bond market that is trading the six-month maturities, after calming down from the bank panic and then re-reading the tea leaves that the Fed put out there, is now starting to see another rate hike over the next few months – if not in June, then at one of the following meetings. And it is getting ready for that rate hike and is starting to price it in. That’s what the six-month yield shows.

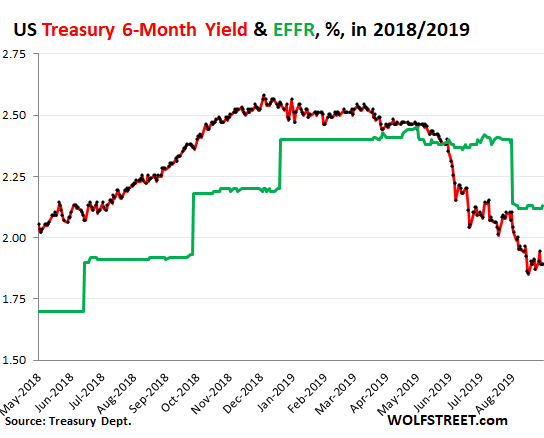

To compare: End of last rate-hike cycle in 2018-2019.

The last rate-hike cycle was a timid affair. But inflation was mostly below the Fed’s 2% target (core PCE price index), and occasionally hit the Fed’s target, but never seriously swerved above the 2% line. The Fed was hiking rates to “normalize” monetary policy, not to fight inflation.

It started with one hike in December 2015, another hike in December 2016, three in 2017, and four in 2018, each hike a basic 25 basis points.

By 2018, stocks were tanking, real estate started to lose ground, and President Trump keelhauled Chair Powell (whom he’d appointed) on a daily basis because of the rate hikes and QT. By late November and early December, Fed governors were alluding to eventually ending the rate hikes. At the December FOMC meeting, the Fed hiked one more time and signaled that the rate hikes would be over.

Even before the December 2018 meeting, the six-month yield started edging lower. It peaked at 2.58% on December 4, and by the time of the FOMC meeting on December 19, it was at 2.54%, and then began heading lower gradually over the following months, while the Fed kept policy rates unchanged.

By early June 2019, when the Fed was signaling rate cuts, the six-month yield fell below the EFFR and started pricing in the first rate cut, which it had fully priced in by mid-June. The rate cut came on August 1:

The six-month yield reflects securities that mature in November, and the debt-ceiling turmoil doesn’t impact it. That turmoil and the risk the US might default in June has thrown the one-month yield into utter chaos though.

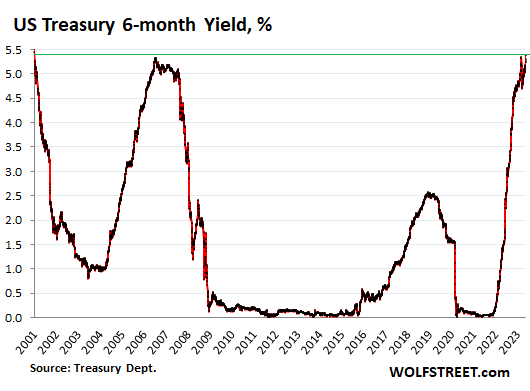

The part of the bond market that is trading in long-dated securities is often hilariously wrong. Remember when it took the 10-year yield down to 0.5% in August 2020, betting on the 10-year yield going negative as it had already done in Europe.

Banks, which are a big part of the bond market, believed this nonsense too, and they loaded up on long-dated bonds and MBS, and then when yields began to rise in reaction to the first signs of big inflation, banks doubled down, believing the Fed’s nonsense about inflation being “transitory,” and when the Fed ate its words and started hiking rates, they continued to buy long-dated bonds instead of dumping them, and then several of these banks collapsed because of their stupid decision to pile into long-dated securities as inflation was rising. So that’s part of the long-dated bond market.

But the other end of the bond market is trading short-term, with securities that mature over the next few months to a year. And they watch what the Fed is actually doing, and they listen to the short-term guidance the Fed gives through its policy decisions, the press conferences, the meeting minutes, and the countless speeches Fed governors give. And by the time the rate hikes or rate cuts take place – unless they’re a surprise – the short-term yields have already mostly or totally priced them in.

The six-month yield now highest in 22 years:

The six-month yield on Thursday at 5.38% and on Friday at 5.36% is now at the highest level since January 2001, having edged past the 5.34% of March 8. A 22-year record is something to celebrate, no?

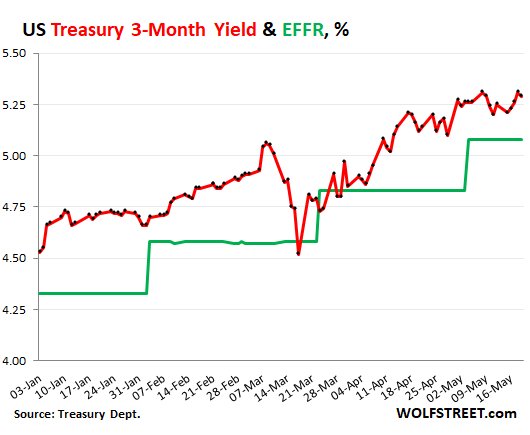

The three-month yield, after the bank panic, also reads the tea leaves and gets on board:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good. I’ve got some Tbills maturing June 1 and I’m backing up the truck.

David Hunter says S&P is going to 8000 forthwith. I guess I’ll miss out.

In the casino, the house always wins. That doesn’t mean that S&P has to reach 8000. It only means that David Hunter has to find a stupid bag holder for his crap.

mortgages at 7%

refi’s dead

cash speaks

Except those “willing buyers at current fair market price” are scumbags using other people’s money for a commission and probably a kickback.

LOL David Hunter…guy has been saying meltup for years now…

Anyway…Wolf I’ve seen in comments here by others a few times regarding the Tbill/bond yields and debt ceiling raises. They’ve said yields will shoot up when the debt ceiling is raised. Is this due to a simple supply and demand issue if/when the Treasury can issue up to whatever more Tbills/bonds than the market wants at that moment to get bids? And if so, approximately how much more could one expect yields go to up?

Regarding S&P to 8000…I found an interesting chart I think Fidelity or Bloomberg put together that estimated liquidity and therefore US equity valuation (S&P500 was overlaid on the chart). They had it as Fed balance sheet minus TGA balance minus o/n RRP market balance as the number for liquidity the market can have. So when TGA is drained and going down (like now) that increases liquidity for that end of the equation, but then a debt ceiling raised the TGA shoots up and liquidity goes down…so S&P 8000 based on that I doubt. Because Fed is doing QT, TGA is about to go up a lot, and o/n RRP still sitting pretty with over $2T parked and not coming down (meaning not entering markets).

Most of my money is in 3 or 6 month T bills. I’ll roll them over forever, or until the stock or housing market becomes better priced.

The wall street game has always been to entice retail investors in with grandiose predictions. We should always assume they’re doing that because they want volume to sell into. I love reading Reminiscencesof a Stock Operator, because it shows how nothing has changed in 100 years. Except of course telegraphs have been replaced by server farms.

Funny, most of “Wall Street” has been doom and gloom for the past twelve months. Including sell calls when market hit its lows last year…

Most of the big investment banks have had hold or sell on equities. Most of the big name hedge fund managers / asset managers too.

The smart money, maybe. The dominant mainstream media narrative has been that once we get these temporary obstacles (debt ceiling, banking woes) out of the way, a forthcoming Fed “pivot” will kite stock prices. Get in ahead of the crowd.

Never mind that the Fed eased all the way down the last two major bear markets in 2000-2002 and 2007-2009.

Once you retire you have to be more concerned with tail risk of stock losses. I think a lot of people are over exposed to equities. With dividend yield of 1.6% you could get caught in a Japanese style bubble collapse where you need 30 years to claw back to even, but you can’t do it if you need income of more than 1.6% plus to keep up with inflation.

In some ways the old rule of thumb of limiting stocks to 100 minus your age can help keep you out of trouble. Then you can build a ladder or duration match treasuries for the rest. Inverted yield curve temps you to put it all in short duration (which I have done), but might not be the right thing to do longer term with reinvestment risk.

Harrold – I am in exactly the same situation. Started buying T bills for the first time in my life when rates spiked.

I have no exit strategy since I’ve never been in this position before. Not worried about it in the slightest….currently enjoying a risk free return.

David Hunter is a toolbox.

The Fed is fueling inflation at this point. MMF’s are 4.5-5% held at the NY Fed primarily.

People are leveraging that for margin and rolling options endlessly.

The Fed has zero control over consumers. Private lending is offering short term rolling loans for less than banks considering origination fees.

The entire system is a mess. The only fix is deflation. It’s unavoidable and unemployment is far, far too low. Even housing could get clobbered. The equity was pulled out two years ago. Nobody gets margin called on that. The stupid failed banking system eats that loss.

Roger

“The only fix is deflation.”

Nit pick. We need “disinflation”….. a retracement of these inflation spiked.

Even 2% up is not good. It will be stacked upon the 20% of the past 3 years. That is hardly in the success band of 2% per year as targeted by the Fed. (even that is theft) YOY should not be the window of measure….the initial spike should be the starting point.

Funny to “nit pick” and correct something… incorrectly.

You have it backwards. Deflation is a decline in price level. Disinflation is a decline in price increases (a change in a rate).

Par for the course though.

I am very happy to see David Lin’s decision to interview David Hunter just as the Nasdaq 100 cleared the July 2022 peak. One more sign of a top of the first big dead cat bounce in this bear market.

Target, Home Depot and now Foot Locker reported surprise evaporating consumer demand so let’s see what happens.

I couldn’t sleep at night without a short position. Since I am up to my eyeballs short right now, I sleep really well. It also gives me a lot of free time. For me to go more short would require me to ask my wife for more money. I do appreciate David Hunter giving a target for the S&P 500 at 8000 so I know when to ask my wife for more money.

Target, Home Depot, and Foot Locker have plenty of demand. What they’re short of is “customers” who pay for what they removed from their stores.

I wonder how much lumber they pinched.

Plenty of earnings reports this week.

When the sex toy business (Williams Trading) gets hit, Katy bar the door.

Let’s see what happens.

I’ve been a banker for 34 years. The banks used to price every loan off Libor, SOFR or Prime rates. Today, any sponsor with a decent balance sheet, will ask their lender to price off UST’s plus 200 to 350 bps. So, a 5 year loan may be priced at 3.5% plus 3% or 6.5%. Not Prime at 8.25%.

Bottom line, any more Fed Rate hikes have minimal effects on commercial clients.

Here is the issue though, banks are making 30 year Jumbo loans at 5.8% based on 30 year treasuries, primarily to bailout the real estate market, to prevent all their pandemic loans from going underwater.

But the depositors now want > 5% on their CDs.

Something’s gotta give 😀.

“Something’s gotta give”

Earnings.

Really? Banks typically match the index to the expected duration of the underlying loan, and very few mortgages exist to maturity. I suspect the pricing is more likely based on 10 year USTs.

This is the opposite of what I have observed. Lower middle market companies are looking at a half to a full turn less leverage than a year ago, and senior rates are hitting 10%. Check sizes are way down and it’s taking large clubs to get deals done.

Q1 leveraged loan market volume was lowest since Covid. The music has stopped, but it will take several quarters for the drunks to sober up and realize the party is over.

In Q2, the leveraged loan market has come back, as has bond issuance. It’s not over till the Fat Lady sings, and the Fat Lady is still at the bar, staring into her Bloody Mary.

Who is the Fat lady?

The first use in media appeared in the Dallas Morning News on March 10, 1976:[2]

Despite his obvious allegiance to the Red Raiders, Texas Tech sports information director Ralph Carpenter was the picture of professional objectivity when the Aggies rallied for a 72–72 tie late in the SWC tournament finals. “Hey, Ralph,” said Bill Morgan, “this… is going to be a tight one after all.” “Right”, said Ralph, “the opera ain’t over until the fat lady sings.”

…. for those that care…its a reference to the final opera in Wagner’s Ring Cycle….Gotterdamerung…. Brünnhilde: Wotan’s daughter is the Fat Lady

So what happens when it rolls over to sofr

When did “borrower” become “sponsor”?

Nice analysis. It will inform my investing going forward. Some free tax advice. In 2023, the IRS doesn’t tax the first $20K of capital gains for those earning under $44,625 single or $89,250 married. This means that an investor can buy a six month or one year treasury note with a low interest rate (not a treasury bill!) trading at a discount, and pick up capital gains when it matures, up to $20K tax free for federal taxes. With the one year note, one can either let it mature in 2024, or sell early at the end of December to take the gain into 2023.

I need to add to the post above. I was incorrect about short term capital gains (held under one year) they are taxed at ordinary income, but correct about long term capital gains taxed at 0 up to 20K. Sorry for the error. And as always consult your tax preparer before making these investments.

In my experience the uncle doesn’t give anything away free,it’s all about recapture,or your money could just disappear. Next 5 years are going to be very interesting,maybe in very negative way

Interning never knew this thanks for sharing will keep this tip in mind for future plus the gain is long term cap gains regardless

this sounds like a perk for retired folk. Who is making < 90k in a household and has cash to invest in t notes?

Look forward to all your analysis concerning the FED policies as always. Your take on the new dot plot is a forthcoming pleasure for me. Thanks

Economist John Williams at the Fed, just reemphasized that low rates are around the corner ( https://www.newyorkfed.org/newsevents/speeches/2023/wil230519 ),

and r* is 1.1%!

https://www.newyorkfed.org/research/policy/rstar

He and a few other people invented/worked on the formula for r-star 20+ years ago, and it has proven to be nonsense, and they stopped talking about it. But now he is head of the NY Fed, and so the NY Fed is starting to release its estimates for r* again. It’s funny. It’s his baby, and he won’t let it die.

Right. R * is fictitious. Investment hurdle rates are idiosyncratic.

I suspect that all those recurring Wall Street forecasts about the end of rate hikes being near, and rate drops being around the corner, are simply deliberate lies by the financial industry to mislead “the little people” so that they keep investing in stocks and other risky assets…

Personally, I can see a pause in June, or a rate hike. The Fed has been completely and purposefully non-committal, keeping both doors wide open. But the 6-month yield is kind of surprising to me. It’s pricing in a rate hike all the way already.

I personally find the dithering by these clowns over a chintzy 25 basis point rate hike laughable. 25 basis points isn’t going to do jack shit in the grand scheme of things.

Agreed. I listened to the entirety of the FED meeting on Friday, and seeing how social media & new outlets were misleading the statements was absolutely insanity. Makes you question everything you see from non-primary sources.

I have major Long Puts on SPY.

I would worry far more about the MASSIVE INVERSION between short term US Treasury yields and long term US Treasury yields, not to mention the fact that US Treasury yields are SET AT AUCTION and will go soaring once the US government goes into DEFAULT on US Treasuries within about the next 10 days or so!

US Treasury yields are negotiated in the market on a daily basis.

When Treasuries are sold at auction, the yields often track market yields very closely. Sometimes the don’t.

If the government defaults, there will not be an auction. All auctions will be cancelled until Congress lifts the debt ceiling.

Wolf, if it came to ” no auction “, where do you see a majority of funds moving to, as bills come due?

Look, if the government defaults, and the debt ceiling doesn’t get raised, and then auctions get canceled, etc., it will be one gigantic global mess. What positions do I recommend in that case? The fetal position.

What is a Treasury bill?

A Treasury bill—also called a T-bill—is a short-term debt obligation (essentially a short-term loan) issued by the federal government. These bills mature in one year or less from the date of purchase. This means you will see repayment of the amount borrowed plus interest within 12 months. Due to their short terms and lower risk (because they’re backed by the US government), T-bills tend to offer lower returns compared to stocks or even many corporate or municipal bonds.

When you buy a T-bill, you pay less than its face value and then receive the bill’s face value when it matures. This represents the bill’s “interest” payments and is only paid out at the end of the term, not regularly, unlike many other bonds. Therefore, you won’t recoup the full face value if you sell your Treasury bills before maturity.

You can keep a T-bill until it matures or sell it before then on the secondary market. Interest earned on a T-bill is subject to federal taxes but not state or local income taxes.

Their short-term nature and high liquidity make Treasury bills appealing to some investors. Since these investments are considered relatively safe, demand is generally consistent. And though they usually offer lower returns than Treasury bonds or notes, returns can outpace those of a basic savings account.

What is a Treasury bond?

Treasury bonds—also called T-bonds—are long-term debt obligations that mature in terms of 20 or 30 years. They’re essentially the opposite of T-bills as they’re the longest-term and typically the highest-yielding among T-bills, T-bonds, and Treasury notes. “Typically” because this isn’t always the case. When there’s an inverted yield curve, yields on Treasuries with shorter maturities can be higher than on those with longer maturities.

With T-bonds, your interest rate is fixed for the bond’s entire term. However, your actual yield might be higher than its interest rate if you purchase the bond at less than par, or face, value on the secondary market.

T-bonds pay interest every 6 months until you sell the bond or it matures, at which point you’ll receive the bond’s face value. It’s possible to sell a T-bond before maturity, but you could lose money as there’s no guarantee you can sell it for face value.

What is a Treasury note?

Like T-bills and T-bonds, Treasury notes are low-risk, high-liquid, fixed income investments with Uncle Sam standing behind them. However, their maturities and interest rates fall in between T-bills and T-bonds.

https://www.fidelity.com/learning-center/smart-money/treasury-bills-vs-bonds

In some ways you can look at all treasuries as interest bearing money with an active market if you need to sell before maturity date.

How valid a recession harbinger is a severely inverted yield curve when the Fed’s interventions in the Treasury market on the longer end and its bloated balance sheet have helped create the inversion? It seems like Wall Street is beginning to accept that the “higher for longer” and the “no landing” scenarios are not inconsistent as long as fiscal policy and the Fed’s balance sheet remain strongly stimulative and the Fed definitely hits the pause button after one more 25 basis point increase. This scenario is probably going to find CPI inflation persisting at around 4% for the next few years until the government’s massive Covid helicopter drop into the real economy is fully digested. However, if there is another external economic or geopolitical shock during this time, accompanied by the customary Fed reaction, we could easily find ourselves at double digit inflation.

The yield curve has been inverted for something like 10 months now, and still no recession. The yield curve is inverted because the Fed pushed up the front end, and the long end is still weighted down by a huge balance sheet and by other factors. Not sure if this predicts anything.

All the recessions are manufactured by the Fed, since its inception, by restricting ‘money’ (credit) supply. This time it’s taking longer, because they’ve pumped too much, and the bubbles are too big, and Americans may have bought into the ‘wealth effect’. Also this time they also gave some money to the poors (UBI is coming). Without credit, the Fiat Ponzi implodes. It’s taking longer, but it’s just maths.

Recession can show up like 22 months after yield curve inversion tho.

Like: “There will be a recession… eventually.”

Honestly, it’s kind of a terrible tell :P

I always thought unemployment was a better indicator. This dude squished them both together :0

https://www.richmondfed.org/publications/research/economic_brief/2023/eb_23-13

In August he said no recession, now in April he changed his mind btw.

I’m just gonna buy a crystal ball 🔮

WaterDog,

“Recession can show up like 22 months after yield curve inversion tho.”

Yes, eventually, we will always get a recession. So anything will predict a recession because it will certainly come. The periods between recessions — the “expansions” — since 1945 lasted on average 59 months. So about 37 months into the average expansion, the yield curve begins to invert, and then the expansion continues for another 22 months, and then we finally get a recession.

They say that Catch 2.2% inflation is the best catch of all.

The Fed wants to lock in the 20% inflation we’ve seen the past three years and then engineer a soft landing that apparently involves many more years of 3-5% inflation, before we reach a goal of 2% inflation.

So, how much inflation are we looking at for the five year period 2021 to 2026? 30% to 40%?

Obviously, inflation control is not the real goal here. What is the real goal, Fed?

You make the debt worth nothing in dollar terms, oh we owe you for all those treasuries you bought from us, the rest of the world?

I mentioned the Argentine peso was worth 1/200th of its value against the dollar versus the turn of the century value.

Its a double edged sword, your money not being worth anything, mortgage payments become a pittance or any kind of old debt, and your society still kind of functions, but advantage to Argentina as they’ve been going through heavy inflation since the 80’s and are used to the new normal.

Think of all of those 401k’s being worth 1/200th of the present value in dollar buying value terms should it tumble in value, ouch!

There are a lot of fixed pensions and 401k’s with fixed income investments. People that rely on this stuff have been skinned alive by the Fed.

For example, a teacher who retired in 2020 with what they thought was a nice fixed pension just lost 20% of that through inflation in three short years.

She was made to sacrifice so that trillions in PPP and other wasteful spending could be distributed so that rich people could buy real estate and boats.

A lot of these pensions have COLA built in. I knew retired teachers whose pensions grew faster than their cohorts that continued working.

David, what makes you say a lot of pensions have inflation adjustments. Aside from social security, I don’t know of any. I have a private pension that does not adjust. My wife’s private pension does not adjust.

Yea…pensions have COLA adjustments built in. Of course, only around 20% of people have a pension any more.

Bobber, my private pension from the company I worked for 25 years has a COLA. So yes, they do exist

AIG (Corebridge) and other insurance companies have been selling these types of products heavily to dependable middle income employees. Think 403b, which is for “non profits”.

AIG (Corebridge) hands you this brochure with 10 diff funds. But the catch is, they invest for you. And take .75-1.25% of the total sum every year. Yeah your employer is matching 3% to your salary. BUT that is to your salary. Not the total sum in your account, which AIG gets to keep cutting until you pass on.

Schools, universities, Hospitals and all kinds of state agencies have been handing these insurance companies this business the last 10-15 years. It’s a real trash heap product that prob costs most retirees 100k-200k when they retire, just on management fees.

All you fancy old people with pensions…

Keep in mind 5% 401k match is crap compared to pretty much any pension. Your pension is likely worth more than a million. Some pensions are worth several million.

Meanwhile companies shell out $150k TOTAL in 401k matches??? ($100k employee gets $5k per year for 30 years)

Pensions are fat

What do Argentinians favor as inflation hedges? US dollars? Precious metals? Foreign real estate? US equities? In the US even inflation adjusted government debt has been a poor inflation hedge until very recently; the S&P 500 has been the winner since 2008.

Almost anything would be better than pesos, but a smarty Argentine that bought pm’s around the turn of the century looks a genius now.

You just stated the “real goal” of the FED – inflation. That’s exactly what they wanted.

The entity in charge of price stability went totally rogue and destroyed prices on purpose to transfer a massive chunk of wealth – the future of the children – to the bank accounts of the already sickeningly wealthy.

And then they pretended that they could have never seen it coming once it was unleashed, then made up a lie that it was “transitory” while continuing to fuel it for more than a year, then finally admitted it wasn’t transitory and mounted a fake “fight” against it which they are now in the process of suspending because, you know, wouldn’t want to overdo it and actually stop inflation.

What children, may I ask? Please name one. All the children I observe live like kings and queens with more money than they know what to do with!

This will be my last comment to you until you prove that you understand “confirmation bias.” Look it up, learn it, then also look at “median household income in the US” and the actual wealthy disparity charts which Wolf has posted for years which show the gains of the top 1% as compared to the rest. The fact that your son is bilking 3 different companies with some WFH scam is immaterial.

Go over to r/povertfinance on Reddit and you Can speak directly to the disgruntled. They scrape by every month.

honestly I feel solidarity with them, good tricks up their sleeves!

I am well aware of confirmation bias. Maybe you should do some research yourself into the average salaries of Millennials. As a generation they are making more money than any generation in history. It’s not just my seven children – they are all making money hand over fist. BTW working three jobs is not a scam. It requires actual work and obviously you are not acquainted with anyone who actually works!

Depth Charge’s message is very clear. The more money our government prints in the form of debt, the more our children and grandchildren will have to pay back. Not just that, the 8 trillion we printed during the pandemic made the rich obscenely richer, and the poor poorer. Even though some young people are also beneficiaries of this madness of money-printing and are making more money than ever before, we also have a lot more poor people than ever before, whose livelihood is put at risk by high inflation that was caused by our government’s excessive stimulus. It is possible that in our own circles and bubbles, we don’t see the millions of people struggling to get by. But they are real.

Escierto:

“Maybe you should do some research yourself into the average salaries of Millennials. As a generation they are making more money than any generation in history.”

I call BS. This is a feel fact.

Inflation adjust that and show it as real wages.

I dug through some FRED and BLS data and didn’t see this.

There ARE a number of questionable articles from unreputable sources.

They are largely partisan “think tanks” or have loose standards and questionable data.

Among the more reputable Pew Research Center, Harvard Business Review, ECT all call BS on your assertion.

The data series seems to divide by CPI-U to get real wages. Krugman does this and so does BLS:

https://www.bls.gov/news.release/realer.t01.htm#re_table1.f.1

I’m not super familiar w/ FRED and BLS data. Maybe Wolf knows a good source.

TLDR: Show me the data Escierto

If the bond market yields are indicative, they are anticipating 4% inflation for the next 20 years. Probably not per annum but in jumps and pauses. For example, my 64 oz bottle of Heinz ketchup increased from 6 to 9 dollars. Guessing they will see if it holds and shoppers don’t pick up the store brand for 5 dollars. I will change my spending because we are frugal. But many people never understood the home economics class in High School and will buy Heinz anyway. And so Companies will keep raising as long as the price hikes stick. Inflation seems to have a big behavioral dimension, which makes it so difficult to control. So are the 20 year bondholders anticipating higher for longer ?

I just shop all the sales in the ads every week.

Olives go on sale for $2 off, you buy 6 months worth. Shake and Bake goes on sale for $3 off, you buy a years worth. Etc. Etc.

Once you get the hang of how often you consume an item and the pattern of the sales. You can stock up in a smart way.

Been doing that my whole life ,amazing how much money one can save on groceries

Ditto. Menu planning revolves around W.O.S. (what’s on sale) or items on clearance in the store. Only way nowadays to help stretch a limited budget.

I don’t think bond holders are anticipating 4% inflation. I think they are believing Fed will keep inflation close to the 2% target or the curve wouldn’t be inverted.

French’s Ketchup. Same taste as Heinz. Of course, mostly sugar.

I guess the cliff notes version of all that I’ve seen for the last year or three is the short term bond traders are going to front run the FED and now the Congress on debt deal negotiations. The FED/Congress/traders will push rates higher until something breaks. Then most asset prices will collapse, cars will be repo’d, homes foreclosed, etc. Maybe the S&P goes to $1K, I don’t know, but the public and corporations will beg the FED to do something. Powell/Yellen will hold hands symbolizing a merged between the FED/UST. Ride in the on their MMT/UBI white horse with CBDC’s in one hand and negative nominal rates in the other to save the day. At which point all deposits and investment capital is locked down like we were locked into our homes during COVID.

UBI ‘light’ is what we had during covid and it unleashed rampant inflation.

Foreign bond holders can see what it means too.

This wouldn’t save anything, it’d crash everything as confidence would be lost.

There are too many vested interests to see that happen in my view.

UBI/CBDC need to be solutions to problems at the time they’re invoked.

Ie, after years of deflation hits… if it does.

I don’t see much in terms of deflation for a while. Governments printing tons of money in a world with finite (and dwindling) resources seems inflationary to me in the long run anyway. Short-term at best for deflation odds is the ai hypetrain doesn’t end up being vaporware. Ai has been used for years now in radiology where I’ve been at multiple places for CT strokes and it’s still pretty bad where it both undercalls and overcalls abnormalities. It ends up using more resources (time of the techs and radiologists) while costing more and not changing the results. I see this playing out with ai elsewhere as it will not be 100% as some may hope given errors that need finding and correcting and it’s not free nor a timesaver.

Deflation is very easy to create monetarily, and very hard to fix when it’s entrenched. The Fed has fought the spectre of Deflation for a long time, barely winning. Now the problem is the opposite, inflation, and they have a very easy cure for it, in a debt addicted economy. It’s very likely that the Fed will overshoot again and create Deflation for a while.

This deflation mongering is just hilarious to me. In my entire adult live, we’ve had a handful of quarters of mild deflation, and the rest was inflation and raging inflation. And yet, the deflation monster is getting dragged out at all times, even during raging inflation. It’s just funny. It’s like mild deflation is the devil. Not it isn’t. Raging inflation is.

There were winners and losers with mild deflation and there are winners and losers with inflation and raging inflation.

While this is true, I think it’s a little overly simplistic. While people who are given free money don’t really care how it’s spent, and thus how much they’re paying, which leads to the inflationary mindset which is partially responsible for inflation, this analysis leaves out the money supply.

Had the UBI light you referred to been doled out from pre-existing money (meaning money borrowed by the U.S., which would have removed dollars from other assets), inflation wouldn’t have been nearly as bad as it was. The UBI light money was printed and then distributed. So the extent that inflation is a monetary phenomenon, printing the dollars out of thin air was a contributing factor.

Strictly speaking, the money WAS borrowed by the Treasury issuing bonds (or spending money out of the TGA and replenishing the TGA by issuing bonds). The money created by the Fed doing QE is only used to buy bonds (and MBS). QE just drains the extra bonds out of the bond market. You could say that the Treasury was indirectly borrowing newly created money from the Fed.

As the MMT folk point out, in principle the Fed could simply create the money directly in the TGA, ready to be spent. But under existing law they’re not allowed to do that.

Right, but that’s just my point. Let’s say, instead of printing the $5 trillion in stimulus measures, the Fed did not QE and kept the money supply steady.

Investors, worldwide, would have purchased the new bonds that the TGA had to issue. It would have been at a higher rate, since you’re talking a huge amount all at once. Those investors would then be creditors of the U.S., but, since their money would be tied up making 8% (or whatever) in bonds, they wouldn’t have been out buying RVs, luxury cars, expensive houses, and what not.

While inflation would have taken off even without the QE, it was the creation of new money that was responsible in part. How much exactly is attributable to each is anyone’s guess.

I’m curious as to how well the bond markets have historically (say over the last year) at predicting actual Fed rate changes.

My impression is that they have not done very well.

Short-term Treasury market is very good at this because the Fed tells the public in advance what their thinking is. That’s the modern Fed model. Back in the day, the Fed constantly sprang surprises on the markets. Not anymore. That ended with Bernanke.

Long-term Treasury market has a horrible track record of predicting anything.

Well, the interesting part is the Fed has zero credibility in the belief they can control inflation, because price increases by market participants continue in the face of fed tightening. The ability of the Fed to influence real business beyond the input of an interest rate in an ROI calculation seems to be minimal. Now, rational consumers, understanding that inflation will be sticky are bringing forward consumption. When all of that excess consumption from cheap money stockpiles is consumed, then we will get some response. Meanwhile, I, like so many others, has made a rational decision to spend to position for the next five years of meh economy. Buy a ton of capital items so that I don’t have to spend more in five years. But for long term demand this will be problematic. Just like the US auto makers have moved up the market to increase margins (hi basic mba 101 to get bigger bonuses). This pulling forward effect will eventually be resolved, but the shortages from the pandemic also had an effect.

Now, ripping inflation is still moving through the economy, and now it is coming to rest in wages that means that the bottom half of the economy is finally getting a raise.

The hardest part is that eventually inflation will be large enough that the corporate profit party might end, and the easy goose of borrowing cheap to retire equity will be permanently gone….now that is a scenario that most of Wall Street can’t fathom. We have built a system that is too geared, and removing that huge cushion of debt will be crushing to the general economy. Just think of all the debt fueled financial conveniences in business, sell you receivables to the debt factor, everything was just in time, and pay for it net 60, blah blah blah.

Now comes the end of easy money to everything.

Someday this war’s gonna end…

It is amazing that the Fed claims to be tightening. But at a Glacial speed.

Yet Government is spending like a house on Fire.

And somehow the buzz in the wires is inflation is bad and needs to be controlled.

Hmm….ask any old junkie on the Streets of San Fransico what his long term plan is, and you’ll get as succinct an answer as the Monetary and Fiscal geniuses running the West.

The Fed is more powerful than ever before. It can dominate the long term rates.

US10Y might close Mar 7/14 2022 gap, or Dec 27 2020/ Jan 3 2021 gap, a rd trip to Feb 2020 high, for entertainment only and to ease the regional banks pain.

Whoaaaa….. sentences?

The end clearly is nigh.

It was on the verge of being coherent, shit just got real.

Regulation Q ceilings were enacted by the 1933 Banking Act, the Glass–Steagall Act. This was to prevent the excessive competition for existing deposits that prevails today.

Wolf, your graphics are the best I’ve seen.

The divergence in the fed rate and the Treasuries, is more likely to indicate perceived market risks, as well as supply and demand. The short-dated Treasuries seem to indicate more risk buying government debt in the short-term and less risk in the long-term, though I would advocate the two be swapped due to boomer retirement and the social liabilities assumed with that (though those are likely to be curtailed like France).

I’ve closed out all my accounts with Wells Fargo after they showed that they have zero security on their accounts. Anyone can steal your checks forge them with Amazon software apps and then clean out your account in one day. I’m done with them and banks, period. I’m also done with Wall Street as well. My credit union has 10 month CDs at 4%. I’ve moved all my money there. I sleep well at night.

Contrary to your assertions, Wells Fargo has excellent security and alerts on all of their accounts. I’ve been a customer of WFB for many decades and they are one of the best banks in the US.

SoCalBeachDude

I’ve worked in computer security for 20+ years. I know an awful lot about the subject. You can have your opinion, but according to textbook security courses and procedures, which I have taken, they flunk on multiple levels. Where they really fail is in the human element which I give them a grade of “F”.

We had our mail stolen back when banks returned your checks to you each month. They made fake checks and tried to pass them at several places around the State. Lowes took one and an antique shop took one, but the bank didn’t pay either check.

Wow, cheque fraud is still a thing in the USA? That is so wild! I don’t think you’d get very far trying to pull a cheque scam here in Canada, maybe when I was a kid, but now everything is on cards and online. Instead we get flooded with carding, hacking and identity theft type attacks, a real pain in the arse because with that the entire world with an internet connection can set their sights on you.

Seba,

Swamp Creature expressed his fear, not reality.

I was originally a Wychovia customer. Because of the GFC they went under in 2009 because they were loaded with liar loans. Wells Fargo took over all their accounts. I liked Wychovia. Wells Fargo treats you like a number, not like a person. I think they are using AI when you make a complaint about their service. Canned, boiler room answers. Rich Edelman, who runs an economic talk show host here told all of his listeners to close out their accounts. He gave 10 reasons. I think he left out a few reasons.

In my experience, when a person’s bank or credit card is compromised, the money is restored within a few minutes of calling to report it. Maybe for a really large amount they might require a police report or affidavit, but I’ve never had a problem the few times my credit cards were compromised.

I hate Wells Fargo with the best of them.

But what exactly is an Amazon Software App?

I wasn’t even aware Amazon did software.

They send my light bulbs and detergent quickly though.

sufferinsucatash

Wells Fargo is no different than the other big money center banks. Until recently, their customer service was excellent. No more. Employee turnover is out of control. They are using AI to write letters to customers. All boiler plate BS. They are allowing homeless squatters to occupy their lobbies.

Their security is so bad that my 3 year old grandson could penetrate it in 5 seconds. Example: The entire account number is printed in bold print on their monthly statements. Same with Truist bank which Ms Swamp uses. I asked them why not just print the last four digits (like my Credit Union does) , just to prevent some dude from the Post Office from reading the account on your monthly statement without opening the envelope. They had no answer. The crooks opened an AAA membership with just this account number and buy stuff on-line.

To your question: Amazon sells a software apps that blanks out everything on your check except you name, address, and account routing number. So a stolen check can be scanned on an Iphone, “Washed Out” re-written and deposited in any bank in the USA, and cleared through the Federal Reserve system. This happened to me recently in April, and no one from Wells Fargo even called me to notify me that the checks were being cashed at one of their branches. I lost $25K is 30 minutes. The funds were eventually restored but only after a lot of hard work, and I lost months of work because I had to close out all my accounts (even the new one they created, which got compromised with fraudulent ACH transfers from the old account) with Wells Fargo, and close my P.O. Box where the crime originated.

I’m with you on below par bank security, but how do you sleep well at night with all your money in one place? Do you not diversify at all?

Forgive my devil-advocacy, but…

“the debt-ceiling turmoil doesn’t impact it”

How can you be sure? It seems at least intuitive (to me) that rates in the 1-6 month range would be elevated to reflect increased credit risk (debt ceiling drama). The fact that the dramatic 100+ bps spike in the yield curve remained in early June as time progressed supporte this (i.e. bills with a maturity after June 6th were consistently trading at a discount).

Meanwhile, longer-term rates are still saying we’ll cross that bridge when we get there.

Just look at US sovereign credit Default swaps.

That is what anyone has to pay to hedge exposure to US treasuries. Subtract that from the yield and you go Oopsie.

That’s what i call an “Impact”.

You can just look at the chart. There is no visible impact from the debt-ceiling turmoil on the six-month yield. The only hit you see was from the banking panic (panic buying = plunge in yield).

By contrast, look at the one-month yield — that’s the one that got hit by the turmoil:

https://wolfstreet.com/2023/05/06/utter-chaos-at-the-short-end-of-the-treasury-market-and-at-the-28-day-treasury-bill-auction-a-deep-dive/

did you mean 6 month yield for the green line Wolf?

The chart in my comment/reply above compares the 1-month yield (red) to the 2-month yield (green). This chart is to show how the one-money yield went through huge gyrations because of the debt ceiling, and the two-month yield didn’t. The linked article explains it.

This is also due to “Da Fed”.

Why ?

Well, histtorically Money market funds were mostly invested in short-term treasury debt like in the chart above. But with Jolly Jay and his band of merry jugglers paying 5% on RRP, that is where MMF go now. That’s why the reaction of the “Bond vigilantes” to the chaos is zilch.

In short: “Da Fed” has killed the bond market.

That is, by the way, also why “Da Fed” cannot lower rates. The minute they lower the RRP rate, two trillion dollars will go – somewhere.

But maybe it will be just transitory.

“But what is really interesting is the action in the six-month yield”.

Well…..no.

what is really interesting is the action in the four week yield.

That’s – really interesting. And starting Monday it will get reeeeeeally interesting.

See above chart.

https://wolfstreet.com/2023/05/06/utter-chaos-at-the-short-end-of-the-treasury-market-and-at-the-28-day-treasury-bill-auction-a-deep-dive/

“The part of the bond market that is trading in long-dated securities is often hilariously wrong. Remember when it took the 10-year yield down to 0.5% in August 2020, betting on the 10-year yield going negative as it had already done in Europe.”

@wolf Is there any way it can be determined how much of the above happened due to the Fed’s intervention in the bond market vs the bad predictions of the bond investors?

The other way around: the wrong predictions of negative 10-year yields were BASED on the wrong assumption that the Fed would push short-term rates and 10-year yields into the negative, through NIRP and yield-curve control. But the Fed said it would not use NIRP and yield curve control, and listed the reasons for it, but the players in the long-term bond market, such as the failed banks, refused to accept it.

6% inflation suggests the Chairman looks to quit hiking at 8%, am I wrong?

Name calling bs. The Irish gang have the same objectives : cut the debt tsunami, shave entitlements & unfunded obligations and give a bear hug to the radicals on both sides.

On your mark, get set ==> trigger. A trigger to start laying off, to cleanse unproductive workers on the wrong track, on higher wages, the 40+ years the top of their prime age, before it’s too late.

Could it be that the Federal Reserve’s strategy is to let the banks fail and then nationalize them? They keep the large money center banks as retail appendages. Of course there’s no need even for money center banks with CBDC.

The Fed hasn’t “nationalized” ANY failed banks. EVER.

Biden just appointed three losers to vacancies on the Federal Reserve Board. The only thing they have in common is their mediocracy. I have the names.

I think, if I remember your prior comments correctly, every single Fed appointee since Volcker was a loser, in your opinion, some bigger losers than others, I would venture to guess.

Wolf has a good memory. He remembers one of my comments out of 500,000 on his site since I posted my comment about the mediocracy of the Fed Reserve appointees. These SOB’s created the mess we are in now by keeping interest rates at zero for 14 years. This destroyed saver’s nest-eggs and lead to inflation and gigantic malinvestment all of which will have to be unwound before the economy can recover. Everyone will suffer, including those who had nothing to do with these boneheaded decisions by the US/Foreign Central Banks.

I stand by my previous statement. I would add: if you think Fed policies have been bad to date “You ain’t seen nothin yet” .

The T-bill due June 6, 2023 is now quoted :

5.94% bid

5.83% ask

I paid 5.39% for this piglet on May 2, wrongly thinking it was cheap. But catching a falling knife can cost one a finger.

What’s up with this 21 day T-bill at auction on May 23 with an investment rate of 6.33%? I never heard of a 21 day T-bill.

Wow. That yield is awesome. And barring a flight to quality from today’s SPU selloff, that yield will probably remain available (at slightly lower yield) in the secondary market until the bill matures.

It seems recently that Treasury is issuing more cash management bills (CMBs), ad hoc issuance, not part of the regularly preplanned weekly bill issuance.

Because a CMB is a “surprise” it always comes at a discount to the secondary market’s price for the T-bill with which it will share a due date.

I’ve got ideas regarding why Treasury is lately issuing more CMBs but I’d rather hear Wolf’s thoughts.

Its an older bill which is maturing mid-June and being sold by a 3rd party and not the Treasury, I believe.

I too came here to comment on the yields on mid-June maturities – what a roller coaster ride.

No, it’s a new issuance of a “21-Day Bill.” This is a “Cash Management Bill.” Issue date: May 25; maturity date: June 15. Auction results:

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2023/R_20230523_1.pdf

The auction was announced on April 27:

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2023/A_20230427_2.pdf

These 21-day bill auctions are not uncommon. There was another one on May 4, it sold at an investment rate of 4.77%.

Thanks everyone for explaining this. I was using only the colorful Tentative-Auction-Schedule.pdf. I did not know about CMBs. “CMBs are not sold on a regular basis and are only put up for sale when the government’s cash reserves are low.”-Investopedia. 6.33% is pretty nice. Too bad it is only for 21 days.