Turned upside-down since late 2008 with QE and interest rate repression, it still hasn’t been turned right-side up.

By Wolf Richter for WOLF STREET.

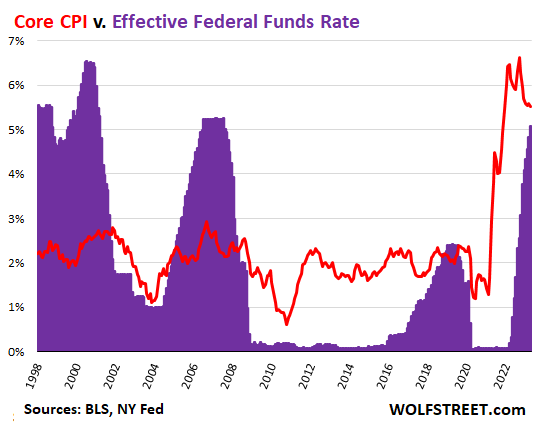

The Fed has now raised its policy rates by 500 basis points in a little over a year, with the top of the range now at 5.25%, and with the Effective Federal Funds Rate at 5.08%. But “core” CPI, which excludes the volatile food and energy components, has gotten stuck at around 5.5% to 5.7% for the fifth month in a row. There wasn’t any progress at all with core CPI in five months. Inflation intensity is simply shifting from one category to another. As inflation temporarily subsides in one category, it resurges in another.

The Fed’s short-term policy rate, as measured by the Effective Federal Funds Rate (purple), is still below inflation, as measured by core CPI (red):

With core CPI at 5.52% in April, the “real” Effective Federal Funds Rate (EFFR minus core CPI) is still a negative 0.44%. And negative real policy rates are still a form of interest rate repression, and are still stimulative of the economy and of inflation.

And so core CPI got stuck at 5.5% to 5.7%, and isn’t making any efforts to be heading toward 2% or whatever, and instead, everyone has gotten used to this inflation and accepts it, and deals with it, and builds it into economic decisions, which is nurturing this inflation right along.

In other words, with its current policy rates, the Fed is still just removing accommodation, rather than turning the screws on inflation.

But the crybabies on Wall Street are out there in force screaming about those unfair interest rates and clamoring for immediate rate cuts, like in June, to remove this incredible injustice of 5% short-term rates and even lower long-term Treasury yields (the 10-year Treasury yield is at 3.43%, LOL), when core CPI is 5.5%.

For those crybabies on Wall Street, the best money is free money. They want their 0% back, and they want their QE back. But now we have this inflation that’s not going away.

When we look back 60 years, we see what an extraordinary period this QE and interest rate repression since 2008 has been. During almost the entire 14 years — except for a few months in 2019 — the Fed’s policy rate was far below the rate of core CPI. And to this day, it remains below core CPI. But that’s an upside-down version of what was the rule before 2008.

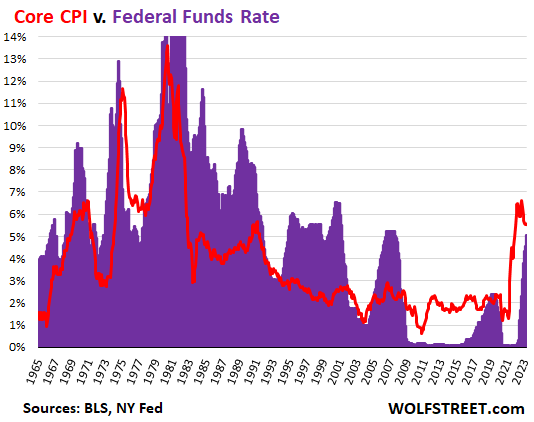

The chart below goes back to 1965. Before 2008, the rule was that the Fed’s policy rates were nearly always higher or substantially higher than the rate of inflation. For example, in the 1990s, the EFFR was around 5% to 6%, while core CPI was around 2% to 3%. In other words, the EFFR was double the rate of inflation, which is what pushed down inflation. And those were booming times. I mean, we even had the magnificent Dotcom bubble.

Over those decades from 2008 back to 1965, there were only a few relatively brief periods when the Fed’s interest rates were below the rate of inflation as measured by core CPI.

But since late 2008, we’ve had the opposite. Policy was turned upside down. And it still hasn’t been turned right-side up. There is still a ways to go. And just looking at this chart, I get the distinct feeling that inflation is just being fueled further, rather than being doused, by the Fed’s current interest rates:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

M2 is decreasing for the first time in our lifetimes.

Bullwhip?

We’ve had lots of inflation in our lifetimes, including in the 1980s. Why wasn’t M2 decreasing then? Looks like M2 is a measure that is irrelevant to inflation.

Also M2 experienced a gigantic spike in 2020-2022 because of mega-QE, and now it’s just unwinding the first little corner of that spike due to QT. Look at the chart — the one in billions of dollars, not the year-over-year percent change chart. It’s an eye-opener. That little drop is barely a dimple compared to the spike in the prior two years. So in terms of inflation, M2 is irrelevant.

Guess I go by the old definition of inflation, monetary not price. Even if you go by inflation as a change in price, money supply would be the numerator with goods being the denominator. I guess an arguement can be made that M2 isn’t a reliable indicator of the money supply.

Yeah, I saw the giant spike in M2. It’s crazy, scary even. That’s why I’m worried about a bullwhip on the way down. I think Powell is going to try and catch a falling knife, similar to that reactor analogy from a previous poster.

It’s not M2 in the denominator, it’s (very, very roughly) M2 x velocity. What’s velocity doing? Also, you know what can really boost velocity? If people think their money is going to be worth less tomorrow, so they want to turn it into something else TODAY.

This is why it’s so important that they get ‘on top’ of inflation. If you look at a graph of M2V it is at an extremely low level historically – pretty much the inverse of M2 volume (fed would say this is why they had to do QE, some would say this was caused by QE…). If this really takes off just imagine how much liquidity they will have to suck out of the markets to try to pull the thing back. That is the tinder box they have created with QE.

Also M2 is not even a good measure of money supply, but they gave up trying to measure M3 as it became too complicated.

As there is more money than counted as M2 money, M2 do not necessarilly indicate either inflation or deflation of the monetary base.

Today the technology to switch to serial number accounting exist. That is, every dollar get it’s own serial number. Controll on the amount of money could be implemented, and if they deflated the amount of money prices would maybe come down to.

Most of M2 is actually someone else’s debt. It’s just another measure of readily accessible credit.

There is always the psychological component of inflation, but the secondary enabler (after still loose credit) is massive government deficits. That’s where most or all current “growth” comes from.

Cut government spending noticeably and I can assure you most (if not all) of this inflation problem will disappear.

Much of government spending = consumer income which is where the purchasing power driving current inflation originates.

Ltlftc,

There was an enormous increase in M2 in 2021/2022 as Wolf noted. That has to be taken out before it becomes embedded. The sooner it is taken out, the less chance for the bullwhip you mention.

The Fed needs to remove the MBS from the balance sheet at a much quicker pace. People are getting huge mortgages and drastically overvalued RE as we speak. The longer the Fed delays, the more people go out on a financial limb and destabilize the financial system.

The MBS purchases were meant to be temporary. COVID ended a long time ago. Get the darn MBS off the balance sheet!! Replace them with ST treasuries in a twist, if necessary. The Fed’s distortion of LT interest rates leads to long-term distortions. The public expects the Fed to stick to its mandate.

Read the latest Hussman market commentary for a great description of how the Fed is disregarding its mandates.

# Agustus Frost.

Most of all money is debt, and it do not matter if it is the government or someone else that spend the money. Inflation as we now see it is a feature of the monetary system.

Switch to a fixed amount monetary system and we would not see inflation as today. Instead we would see a different set of features of the system.

Both type of monetary systems can to an extent be managed, but making the systems stable restraints the possibility of geting rich fast and necessare less wealth disparity.

Jon W:

M2V is just GDP over M2. It’s pretty much the inverse because it’s calculated as the inverse. With an increase in M2, M2V would thus be lower, as GDP is much more linear recently. Are you saying price is roughly a function of GDP per goods?

It’s a race to the bottom to remove money supply in any inflation arguement, and instead look at it’s results. (Not directed at you) Yet mention “money printer” and “devalue the currency”, and even average joe understands.

Though M3 is discontinued, OECD is showing a decrease in M3 US as well. Again, large spike during covid.

Bobber:

A twist out of MBS into TST would be interesting, though existing home sales have slowed quite a bit, and reducing demand further is just pushing on a string. Really need unemployment and a reduction of excess savings.

Wolf in most of your articles you are optimistic when talking about the interest rate hike and QT. I think I detect pessimism from you in this article?

What I gather from your posts is that you have been a supporter of the idea of higher interest rates and inflation for quite some time. Is there a change in this thesis and if so, what is new?

I am also confused that you wrote an article about the possibility of a recession being avoided and then I read your comment that a recession is inevitable because every expansion follows a recession, but no one knows when. However, do you think there will be a recession in the near future?

Wolf is just stating the fact that Fed has failed to meet its inflation target despite all hikes and QT.

Wold doesn’t apply mainstream media spins to say that all news os positive for wallstreet. Like:

Job numbers good => economy strong => markets rally.

Job numbers bad => Fed will Pivot => markets rally

I thought the exact same thing. It wasn’t quite the article that Depth Charge would have written but it was definitely pessimistic.

I’m starting to see a few elements of the worst-case inflation scenario crop up here and there. Not a lot of elements, but some. The recent data is worrisome to me. It shows that people and businesses are getting used to this inflation and are incorporating it into their decisions, instead of fighting it.

Businesses like the ability to raise prices (which is what inflation is). And they’re willing to pay more. Consumers like making more money, and so they’re willing to pay more. This helps propagate inflation.

If a company borrows money at 4.5%, as many companies can, and it can raise its prices by 6% or 12% or whatever, they’re still getting free money in their view (below the rate of their price increases).

We now see that bond issuance and leveraged loan issuance has taken off again. Yes, banks have become a little more careful in lending, but that’s compared to the crazy days in 2020-2022.

So I still think that the 5.5% Fed rate scenario could at least halt inflation from getting worse. But I now see more evidence that those rates will not bring down inflation to 2% or whatever. I now think that there is a risk in this scenario that inflation will do what it did back in the 70s and 80s: take off again for a second and much bigger wave.

I’m not opposed to the wait-and-see approach at 5.5% because it might still work. But I’m less confident that it will work.

In terms of a recession (yes, every expansion is followed by a recession), I don’t see this economy heading into a recession at these rates. Growth is slowing. There was a slow spot late last year. It seems to have picked up again so far this year. And so the economy will just muddle through at these higher rates, that’s what it looks like to me.

Let me just add this to my above comment: The Fed also needs to be careful to not blow up the banking system with its rate hikes and QT. Years of QE and 0% have bloated the banks, and that bloat needs to be let out slowly, not all at once. The Fed is keenly aware of it.

I’m glad I’m not a Fed governor now. It must have been a lot more fun during QE, just giving money away. Now, it’s like all the choices are more or less bad.

This only proves your point

1 relatively high inflation and interest rates for long time

2 option similar to the 80s where the Fed is forced to act on fire leading to a recession.

I now think that there is a risk in this scenario that inflation will do what it did back in the 70s and 80s: take off again for a second and much bigger wave.

Wolf, if this is the case, then there is NO way the Fed will pause rate hiking in the next few FOMC meetings. Don’t you think so?

The stock market currently prices in a rate CUT by September 2023! That’s insane.

The FED makes a mistake, by not hiking the rate above the core PCE index (as shown in your graph).

I do see that it is concerns about blowing up the banking system. On the other hand, can it not be looked at as any other demolition job, or rather explosive ordonance disposal?

With exposive ordonance disposal the job is planed and site prepared to minimise damage on the suroundings. The same could be done with the banks and QT. Plan, prepare, light the fuse and take cover.

Ok, to some it would be the end of the world as they know it, but it would definitively not be the end of the world if precautions where taken. It would mostly be shifting wealth and power around. Most people would maybe see little change in their day to day life, a few very wealthy and powerful would find they after all was just ordinary.

I do not see a slow down during this spring RE market.

Last year in the Bay Area houses were flying off the shelves > expected market time was 31 days.

This year (May) it’s 41 days.

So it takes about 41 days from the day it’s listed until it’s under contract.

I was hoping for a slooow spring market and price reductions.

Looks like QT will have to rise $50 billion more each month.

First, Fed has to actually meet its QT targets.

Second, it cannot be QT for 99% and QE for “too big to fail (not really)”.

In last 2 months Fed balance sheet is higher by $160 billion, when QT should have lowered it by $160 billion.

The latter would have corrected markets by atleast 10% and reduced core CPI inflation by atleast 0.5%.

Wolf, money has piled into private credit and the demand is nutty. The underwriters that I have talked to at Ares and Monroe say demand is incredible despite 12-14% rates.

Bank deregulation caused backlash into over-regulation and you are 100% correct that now the Fed itself is fueling inflation by providing government money markets with a 5% overnight rate on money held there.

Other way around. The Fed providing 5% overnight interest prevents the holders of those dollars from instead deploying it to buy risk assets, contributing to asset (and ultimately, CPI) inflatoni.

Are you saying the Fed paying a 5% overnight rate, which is necessary to maintain its policy rate, is fueling inflation?

If so, I think you’ve misunderstood the article. The point of this article is that the current FFR, which is negative .44% in real terms, is “still stimulative of the economy and of inflation.”

Great write up. One of the best in a while that shows just how out of which things are historically. IMHO, these things will keep inflation high, ranked in order of importance:

1) Massive federal deficit spending to the tune of $2T in FY 2023 and most likely at least 1.5T annually as a structural deficit. That’s a ton of extra juice for the economy, and it isn’t going away anytime soon.

2) A housing market that is defying gravity, meaning most local governments are flush with cash because property taxes are still creeping up.

3) A labor market that is defying gravity which is being supported by strong corporate profits, for now.

4) A stock market that is defying gravity adding fuel to the wealth effect of the top 20% who are really keeping the economy moving along.

5) A services market that is defying gravity which is supported by 1-4.

And, I find it hilarious that really cool websites like visual capitalist do this rate hike analysis pointing out how steep the slope is of the current rate hiking but fail to go back to the early 80’s when Volcker pushed up the FFR 900 basis points in 7 months.

I like you points in a previous post about how the YoY floor will affect CPI in the back half of the year.

You’re right. It really seems like the public has come to terms with this high inflation. I really want to see some serious cracks develop in consumer credit, new autos, used auto and finally homes sometime this year. Those and a turn in the labor market will signal a recession is coming. At this point, guessing when a recession might arrive is nothing more than an uninformed WAG!

I do not post often but I had to address this:

“2) A housing market that is defying gravity meaning most local governments are flush with cash…”

I am on our local school board in a middle-class, middle-sized (3200 enrollment) bedroom community. ESSER funds (fed covid money) that allowed the state to fund schools using their enrollments from 3 years ago run out this year. Enrollments in public schools across Jefferson County dropped significantly in all but 1 large and 2 small districts, on average about 5%.

Our CFO projects a structural revenue loss of $1.5 million starting next year and getting worse due to slowly dropping enrollment. Overall revenue is about $46 million right now, all spent, 80% on salaries.

Voters rejected a levy increase once and a bond issue twice, which has not happened in over two decades. The local fire dept. also failed to get a levy twice. All this in the last 18 months.

Some local boards are still getting the votes for borrowing and taxes, but it is clearly no longer a free pass with inflation putting the voters in an ugly mood (me included).

Property values do not play a role at all until the local Assessor’s office does an update, which is not annual here – it can be many years, depending on who is in charge.

As for my school district’s reserves, yes with all the strange distortions they ended up at a 30-year high in terms of ratio to budget, over 20%. So currently “flush with cash”. But the teacher’s unions want to gobble it all up as if the covid revenue stream was permanent. So, the long-term outlook is gloomy. CFO just did a 5-year projection and reserves may well be at 11% in 5 years. After that…

And of course, this all assumes no negative events like a state budget crunch, continued wage and supply inflation, etc.

Just needed to point out that here in middle America, much local gvt. is cash-rich but revenue-poor due to covid funds plus inflation. Good short-term outlook, but unsustainable in a few years. We told the teachers that and we almost got through. They asked for a smaller raise on top of their automatic annual raise.

Sigh. Baby steps.

I see you talk alot about interest rates and inflation, but you dont spend as much time talking about the massive balance sheet as the driver of inflation.

It is my theory that the real root cause of inflation is a “wealth effect” that is a result of 1) the cumulative effect of the balance sheets of the Fed, ECB, BOJ and other central bankers 2) real estate prices which give the middle class the illusion of wealth (some people would feel rich with just $300K of equity) and 3) the remaining higher bank balances and lower credit card debt that still lingers from all the stimulus money (although this is being burnt off).

The financial media also goes on and on about the interest rate, but there is a real paucity of discussion about the massive monetary and fiscal stimulus.

Any reason this is not more of the focus? Is there an economic reason that the massive stimulus, both monetary and fiscal, is NOT the primary driver of inflation and thus needs to get alot more scrutiny by the financial media? (it would be nice for Powell to get a single question in his press conferences about the pace of the QT and for example the lack of any significant unwind of the MBS positions).

I personally think that the central bankers have chosen the method of transmitting monetary policy to hurt the middle class and slow down the real economy, while leaving asset bubbles intact as much as possible, because they really only serve the interests of the rich. Do you believe there is a different impact on asset markets if the Fed uses more or less QT versus rate hikes to accomplish its inflation reduction goal?

there is more scamming going on than ever. Covid brought it to fever pitch. And everbody is in on it. Especially the Fed, Wall St and Washington.

You cannot contain inflation with tightening Monetary Policy and OUT-OF-CONTROL Fiscal Policy with deficits forever on the horizon.

Period. Full stop.

And sanctioning countries that produce key commodities, including energy, rates as the dumbest of dumb.

Yet M2 seems to have a definitive correlation with the “paper wealth effect” the recent Fed chairs have blessed/cursed us with over the last few decades, as shown in historic charting detail per Jesse Felder’s May 10th article titled “The Great Wealth Illusion”.

In particular, GDP/M2 and Household Net Worth/GDP charts hint strongly that we are all living inside a gigantic illusion of wealth bubble.

Thus a higher probability of future financial volatility as stagflation confronts “The Great Wealth Illusion” over the next few years as stagflation “douses” the illusion of wealth.

Fed is not tightening because it is suddenly in love with the working class. It is tightening only because otherwise high inflation would become hyperinflation, the system where Fed is God will breakdown.

At the same time the Fed doesn’t want any highly indebted institutions to fail. So, because there will be no bankruptcies where debt will be written off, the bailouts will simply transfer all this debt to taxpayers.

It means that in this “land of the free”, our kids are now born as “debt slaves”, doomed to live poor all their lives, to serve their 1% masters that now own most of the land and other assets.

Fed keeps playing the zero sum game to make the 99% poorer for making the 1% richer, as productive decreases. Hence QT will be slower than creation of government debt and inflation will be made to run high to inflate away this debt.

Yet, in this scenario, interest rates would be high so that there would be no hyperinflation, as you say, and QT would continue. This will hamper asset and property prices and eventually they will continue to fall. And if the labor market slows down, this will only increase the effect. There will always be a recession.

Without a lot of bancruptcies, high interest rates are monetary inflationary as long as debt is rolled over.

If high interest rates stop consumer price index rising, that is because they halts or crashes the economy.

Long before there was any inflation in the real economy, there has been inflation in asset prices. Apple computer for example is trading at a P/E ratio in the high 20’s, much higher than its average over the past decade, yet revenue growth is negative this year and it appears that the many decades of revenue growth might just be gone for the entire smartphone device industry. The list of consumer staples companies with p/e ratios in the high 20’s, 30’s or even reaching up to 40, with limited revenue growth in the current periods is substantial.

The Fed started to bleed off the balance sheet and it reversed course simply because the stock market fell off. That tells you the whole story. The Fed wants to blow asset bubbles, but keep inflation in the real economy down. It doesnt have any intention of popping any asset bubbles that would hurt the rich. Despite the fact that there is a greater wealth inequality in the country that at any point in the past.

This is a con game at the highest levels.

The Federal Reserve wants to inflate the asset bubble but keep inflation in the real economy low. He has no intention of bursting asset bubbles,

Agreed, BUT as we all see that is impossible. Inflation is here to stay and interest rates are bringing down the property and stock markets.

Leo ,history will take care of these problems

Agree and a point should be made – debt slaves are we (almost)all by the Fed. Now we just had the black slaves reparations board submit that everyone who had a slavery lineage or whatever should be paid $200 million each person for justice. But what about all us debt slaves working day and night for nothing by inflation under financial repression? Should we also not be recompensed for our injustice? Maybe $1 mil each? The Fed is abusing us right?

All I know is that my coffee and bread went way up

“Examining the relationship between 3-month and 10-year benchmark rates and nominal GDP growth over half a century in four of the five largest economies we find that interest rates follow GDP growth and are consistently positively correlated with growth. If policy-makers really aimed at setting rates consistent with a recovery, they would need to raise them. We conclude that conventional monetary policy as operated by central banks for the past half-century is fundamentally flawed. Policy-makers had better focus on the quantity variables that cause growth.” ?

I didn’t read the entire article, but correlation isn’t causation. Of course, central banks raise rates as a recovery gets steam, unemployment abates, and the GDP gap closes. And when they got hit in the face by a recession, they lower rates if inflation allows it.

As a brazilian, all this MMT talk north of the equator just makes me laught. But then, all the Krugman and Stiglitz types atop their ivory towers envy our “just a little more inflation”…

Just saw that the “voice of the fed”, Nick T at the wall street crybaby journal said today’s inflation report shows the fed can take the summer off from fighting inflation. WTF?

This guy is just a professional liar.

He gets in a room with Powell and asks what they want. In exchange he gets to be the mouthpiece.

All the headlines popping up in my news feed are touting a 4.9% inflation, “lower than predicted! Proof the rate raises are having their intended effect!”

He has said a huge amount of BS before, including that the Fed would pause at the “next” meeting, which at the time was the March meeting, at which the Fed raised, followed by another hike in April. This was based on a Goldman Sachs promo that he’d swallowed hook, line, and sinker, and cited in this piece.

He’s just a young reporter whose job it is to write about the Fed. That’s his beat. He doesn’t have any kind of special insights or access to the Fed.

This reminds me of another reporter, named Lance Lambert, who writes about the housing market for Fortune. He’s the same way. One week he’ll write the housing market has bottomed out and the next week it will be the opposite story.

If they “predict” all possibilities, they can always go back and reference a piece that was accurate to gain credibility. In other words, why adjust your scope when you can make the target bigger? All part of their scheme in mainstream/clickbait news land.

All these people along with Fed think they are winning this war against inflation as inflation is going down.

With interest rates 2-3% above actual inflation, who needs the stock market casinos? Let alone “futures”?

Only the billionaire gamblers, but with FED safety net on demand for these privileged few.

“With interest rates 2-3% above actual inflation, who needs the stock market casinos?”

?????

Only rates shorter than one year even got close to the inflation rate….longer maturities have stayed well below.

What metrics are you looking at?

The real inflation is almost 15 percent or so on the ground

I know people put too much faith on manipulated government metrics.

Obviously not at all.

You are right if you believe the government propaganda.

I’m not sure if the Fed funds rate needs to be strictly above core inflation to be “sufficient” (economic theories and theorems are not immutable laws of nature, and inflation statistics have lots of adjustments anyway)

Though… so many people now have 30 year fixed rate mortgages that are a) a lot lower than the FFR and b) lower than the rate of inflation, even inflation expectations. That sounds like something that could have impacts for years – the people with nice mortgages can do what banks do, except sort of in reverse (borrow long, lend short, profit)

ARMs would be better, so that rate hikes and drops would affect consumption quicker? Heh.

Unqualified armchair economist here, joining the brigade.

It’s going to require real job losses to break the property bubble the Fed produced from 2020 to 2022 with unnecessary low rates and QE buying MBS.

From 2020 to 2022…

Try from 2007ish until now.

Prices didn’t start rising until 2012

Agree with U,,, AND all good:

Crazy times did NOT start in second decade of 21st century, but, rather, much earlier.

And IMHO, the longer the crazy, the longer it takes to make some sense and appropriate ”corrections” to the crazy.

U can ”spin it” any way and every way,,, but sooner and later, the chickens come home to roost…

AND, also IMO as having been watching RE mkts in many locations since the middle 1950s…

WE, in this case the WE wanting a ”reasonably priced ‘home’ will suffer until the PTB decide to let us have at least one more chance before they make SFR and even MFR go TO THE MOON, Alice,,, as Jackie Gleason was known to say almost every episode,,, a clear msg IMO from our ”owners/rulers.” back in those days, eh?

That’s exactly what I’m doing – making the minimum payment on my 2.7% mortgage and laddering short-term CDs and T-bills >5%.

There are plenty of places in the World that make all the products we use much cheaper; our problem is to get used to foreign brands and for enterpreneurs to increase our foreign imports. Not that many people are involved in consumer manufacturing, there are zillions of people around the world eager to supply our needs at inflation busting prices.

Been there, done that – 30 years of global trade *has been* deflationary, but now the world is bifurcating and we have a future of ‘friend-shoring’ and mercantilism (read: inflation) to enjoy.

U got it wrong we will repurpose manufacturing for jobs ,but fuel will be 10$ a gallon = costs to much to transport goods.easy to figure out

Wolf points out that inflation now is really in services, not goods.

For all of the last 12 months. Yeah, a trend to cite for the long-term lol.

Services prices are already coming down now – even before the recession hits. A recession won’t take services inflation to the target 2% rate btw. It will flip to negative.

It also appears most don’t understand the impact from energy prices and how that has a lagged real effect on many other inflation components. We will see that over the coming months too.

I agree. i think service inflation will start dropping. i know many people who are not getting raises this year.

I think home remodeling spending finally rolled over after increasing for the past 3 years

The Federal uniparty are now the ones fueling inflation. 2 trillion$$$ deficit in supposedly good times and with the Fed debt going over 40 trillion$$ before 2030 and foreign purchases of the US$ for trade means, Mortimer, drum roll, inflation! Nothing like abusing the manna from heaven, the reserve currency printing press, until it breaks!

should be LESS foreign purchases of the US$ for trade

I’ve been critical of Jerome for a couple of years. But he needs the Fed gvt to be onside on the inflation battle which they aren’t! Jerome is going to be left holding the sheet-bag!

This part seems to be always ignored in any Fed criticism. The legislative branch is supposed to be doing most of the work here. The Fed seems to be one of the few institutions still attempting to do it’s job.

I think you’re right Wolf, Inflation has become entrenched and has an inertia of its own. That’s a very important change from the last 40 years.

Regarding implication for Investors :

Stay away from Bonds, especially longer term ones, way over-priced

If yields are likely to grind higher, how can that be good for the very expensive Equity market (based on long term valuations) ?

Cash at 5%+ is no longer “trash” and should be a bigger % of portfolio than seen in many decades ?

The reason long bonds are so low is that people are pricing in the risk of a real recession in the next year or two and predicting that the Fed will pivot, as they have very predictably done since the 80s when markets plunge. I don’t think anyone can predict whether long bonds are a good or bad investment right now. A great many people said the same thing you just did in 2008, and they missed a massive 13 year rally in long bonds.

I like Druckenmiller. He too is not seeing a fat pitch right now because nobody really knows for sure if Jerome Powell will be a Volker or Burns when it comes crunch time.

Choosing 5% cash is an acceptable investment til we see a fat pitch caused by others getting off sides on the inflation bet.

I would argue that monetary policy (FED rate and balance sheet) has been accomadative (loose) for a lot longer than just 2008. I would go back to the early to mid 90’s, basically ever since Greenspan was the Fed chair.

Since that time, monetary has never, ever been considered tight and the Fed has always been looking for an excuse to make it looser.

I think the Fed has just gotten lucky that the tech refresh surrounding Y2K created a nice boost to productivity to help keep inflation down for a few years and then inflation from QE has been mostly restricted to financial instruments and not main Street.

Unfortunately decades of loose rates and QE have come home to roost. The tech boost to productivity is no longer providing cover from inflation due to low rates and inflation from QE has broken loose from financial instruments into the general economy.

“I get the distinct feeling that inflation is just being fueled further, rather than being doused, by the Fed’s current interest rates”

This is a salient point and I think consumers are less ignorant on what to do in higher inflation environments. I know regular folks who are purposely buying extra nonperishable food and also consumer goods because of the continual loss of purchasing power. I fear that the new mentality to keep spending instead of saving will be something like, “inflation is making things more expensive so I might as well buy now” Until saving accounts return a higher rate, then I worry people will keep spending once the paycheque deposits. Personally, I prefer CDs and High Yielding saving accounts over spending my paycheque.

If that were a real estate price chart, the commentary would have been that prices were CRASHUNG and prices were headed at least 50% lower, amidst the end of concensual hallucination.

So I’ll use the same methodology and say that hallucinatory high inflation and interest rates peaked back in 2023 and are headed much much lower because consumers are running out of money and credit. I think Ill even add that lower interest rates are coming soon since no one can afford such high prices and rates.

Interesting how similar charts can be interpreted so differently.

The solution to no one being able to afford the high prices is for prices to come down, not to lower rates so that people can borrow more to pay those high prices.

“hallucinatory high inflation and interest rates peaked back in 2023 and are headed much much lower because consumers are running out of money and credit”

What do you mean by hallucinatory high inflation? That doesn’t make sense.

If people run out of money, then they file for bankruptcy and loose the homes. Or that’s the way it used to work at least.

The problem, of course, is that the Fed & Uncle Sam have turned the system upside down. The pandemic solidified the full on shift to MMT-based monetary policy.

When things get bad, Uncle Sam WILL step in with mortgage & rent relief, meaning the past methods of bankruptcies & foreclosures will not have a pronounced impact on the economy like they did in 2008-2012.

Again, EVERYTHING is upside down now. And there’s no intentions to right the ship.

I really don’t get the message here.

Is it “derned if you do, derned you don’t?”

The was a lot of commentary around here that interest rates needed to be higher because there was too much demand, and it was fueling asset infusion, and speculation, but now the trouble is that the interest rates are too high, that there’s not enough supply and not enough investment?

These 5% rates are not even that high, but would it be better for them to reverse hikes, just to get big business to invest in building out capacity?

There’s already all that CHIPS money and IRA money being dumped on the economy to build out infrastructure.

Personally, I don’t understand why Congress is just sitting back and letting Powell fund these interest rate hikes with more deficit spending. Congress has to sell their debt right now at an even higher premium, and that’s just blowing the budget on these payments that only go to banks and hedge funds and wealthy clients who had the extra money kicking around that they don’t mind having it locked up in a bond for a few years. If anything, why risk building out industrial capacity, when they can just get better returns, by doing nothing?

Personally I’m still stuck buying golden eagles and classic motorcycles. They seem to appreciate regularly enough, but the limited liquidity often gets me scalped.

A clear pattern in that last chart. Every time there is an abrupt drop in CPI – it’s *after* the fed dropped rates.

Higher for longer has never has caused the big drop we’re all looking for – only market crashes.

What most people who want to buy a house want is a market crash in the real estate market.

Markets don’t care what most people want

Sure they do. It’s the very definition of a market. If enough people decide housing costs too much and don’t want a house at the current price, there will be declines. If it’s a large enough group of people there will be a crash.

1. During the Financial Crisis, the Fed cut rates because of financial turmoil (Bear Stearns collapse, etc.), and not because of inflation. Inflation had nothing to do with it. Then during the peak of the Financial Crisis, when consumer demand collapsed, CPI plunged.

2. In 2020, the Fed also cut rates unrelated to inflation, and then CPI dropped as demand collapsed because of the lockdowns.

3. From a long-term chart like chart #2, you cannot tell the timing. Volcker cut rates AFTER inflation was coming down — including a couple of head-fakes. But that’s impossible to see on this 60-year chart. The timing is still hard to see on the 25-year chart. We would need to look at a three-year chart of each episode, and that it gets clearer.

4. What you’re also seeing are the effects of the year-over-year inflation rates. If inflation comes down on a month-to-month basis, for say four months in a row, the year-over-year CPI readings might still be unchanged or even go higher because of the base effect.

They started cutting rates in 2019:

July 30-31, 2019 -25 basis points 2-2.25 percent

Sept. 17-18, 2019 -25 basis points 1.75-2 percent

Oct. 29-30, 2019 -25 basis points 1.5-1.75 percent

Why? No pandemic then, oh and they did secret QE also. Why?

Yeah, it sure feels to me like there’s another massive shoe to drop, or, er go up. Basic supply and demand law. You can’t pump $9 tril into an already inflating market over 14 yrs and then think 14 months of meekly raising rates is going to counter it.

100% agree.

The velocity of money will INCREASE as the money supply decreases, if GDP remains stable.

As for M2, though it may be an imperfect measurement, it did foretell the inflation. For it was the spike in M2 that occurred prior to this last bout of inflation….and Powell dismissed it as a signal.

Higher rates on savings and other fixed income is indeed an economic engine, often putting increased disposable income into the hands of the consumer.

When rates are suppressed artificially, it is the borrower that benefits and gets to spend the “gains”. (ie the government)

When rates are fair, or nearing historical fairness, it is lender who benefits and gets to spend the “gains”.

The powers that be prefer the first arrangement.

100 percent agree on M2.

Would the rate benefits change during the transition or only long after? Banks et al holding MBS and long dated securities aren’t really benefitting right now, quite the opposite.

Wolf, excellent to the point analysis. You should have a job at the Fed. We hope those goons see this sort of information. Do you think they see it as clearly and simply but feel bound by market and political interests to keep rate hikes meek?

Free money? It ain’t free to savers, retirees, pension funds, and others who need low risk and dependable returns on their money and who’ve been getting shafted for years by next to nothing returns. Not everybody wants to go to the casino. Again, boo-hoo and screw you Wall Street. Mommy Fed isn’t going to give you your sugar rush anymore (I hope). Deal with it.

Should QT be considered as some amount of “additional” Fed interest rate? Could we consider the Fed rate to instead be 6% or 7%, when comparing historically, because of this extra pressure that wasn’t used back then?

Yes, they said that, and a year ago, I agreed with it because QT should push up long-term yields. But now, long-term yields are below short-term yields (which track the Fed’s policy rates). So I don’t think QT today has the impact of rate hikes, and may not have any effect on the real economy. It does sap the asset bubble though – but that’s asset price inflation, not consumer price inflation.

QE involved buying securities of various maturities, including at the long end.

QT thusfar has only involved runoff of securities as they mature (with some MBS prepaid due to housing turnover).

Does the fact that long-term bonds are not being sold explain why QT is not driving up long rates the way that QE purchases of long-term bonds pushed down long rates?

Each maturing bond issue (no matter who holds it) is replaced by the US Treasury department with a bond issue of the same maturity. So it issues new 10-year bonds for about the same amount as the maturing 10-year bonds. In other words it refinances them. In addition, it issues new bonds to finance the current deficit. Investors have to buy those bonds. So in terms of the Fed, the critical factor is the speed with which its bond holdings drop. In terms of the market, over a given period, it’s the same whether the Fed lets $50 billion mature without replacement, or whether it sells $50 billion. What would make a huge difference if it doubled the speed by #1, not capping the Treasury roll-off at $60 billion, but letting roll off whatever matures, which in some months is a lot more than $60 billion; and #2 by selling enough bonds to double the speed.

But the banking system would likely not be able to deal with that kind of rapid balance sheet unwind.

Seems to be a typo somewhere.

Charts say PCE but text says CPI.

Thanks. Charts mislabeled.

To the extent interest is a cost to business it is now just another higher cost to be passed through to customers thus contributing to inflationary pressures. But people have money and they are making money so they pay the higher prices. Demand continues despite the price increases, so I think Wolf is right, higher rates are adding to inflation.

But isn’t that probably to be expected in the initial stages of any effort to bring inflation down? The Fed tried to solve the problem quickly, to shock the economy with rapid rate increases, but it damaged financial institutions so has had to slow and will now have to hold rates higher for longer. Eventually higher rates will bite.

“I think Wolf is right, higher rates are adding to inflation.”

I don’t think the article says this. Wolf can certainly correct me if I’m wrong, but I read the article to suggest with the real FFR still negative, it is stimulative to the economy. It continues to be a form of interest rate repression. Maybe I’m missing something because I’ve read this sentiment in at least one other comment.

RTGDFA.

During QE , the Fed bought longer term securities . During the current QT , the Fed is selling zero long term securities ; instead the FED is letting securities run off when they mature. Until the Fed starts reversing QE via selling long term securities , core inflation will continue

I have no reason to second guess my theory. Not yet anyway. If the Fed wants to lower inflation, it will need to deflate stonks/housing/cryptos by more than 30% from where they are today.

If not, say hello to your permafriend, inflation. He will follow you everywhere.

Berna-QE’s wealth effect is the root cause of inflation.

Assets went up so they feel rich….now they are bidding each other for everything and driving up the prices for everyone. I am sure this is not any “theory” taught or written in a text book, but this is what happened imo.

Yes. At the risk of sounding like a broken record, it’s my theory that the top 10% of households in America are driving inflation, feeling rich because of their assets.

Knock those assets down 25-40%, and they’ll stop feeling so rich.

Or just raise their taxes so they have less to spend.

“Or just raise their taxes so they have less to spend.”

The tax collector is the biggest spender of all.

Much much more QT is needed.

$ 4 TRILLION.

Does anyone look at current inflation – and the many cries to let it ride – as a backdoor, unspoken way to transfer measurable amounts of wealth from the baby boomers to succeeding generations? This is speculative on my part but only partly mine: I’ve forgotten when/where I stumbled across this idea in someone else’s writing, years ago.

It’s not the same as, but does run in parallel to the inflating away of pre-existing debt and a (probable) gentler erosion of the worth, hence cost, of pensions (eg, Social Security or corporate) and national health care (eg, Medicare).

Whether or not such a generational wealth transfer is intended, it does seem like one of the outcomes worth noting.

This speculation doesn’t get much press but that alone is not a certain indicator that it lacks validity: some things are just too sensitive for the major media to touch. I’m not pointing a finger at any specific group of elites; one can likely find/imagine plausible motivation in most directions.

Ideas can come from anywhere and, equally, go nowhere. This one may have no legs. Or does it have enough explanatory power to be worth considering as a motive? Or is it no more than a (recognized) side effect that is being tolerated?

It seems the inflation exact opposite of effectively transferring wealth forward? Isn’t that just borrowing from the future?

Also I heard an interesting take on the pandemic problem: the vast majority of the PPP money et al went to the wealthy! Yes, under the guise of business and financial system support.

Who’s best equipped to “best” fill out these applications but the establishment system gamers: tax evaders and fraudsters. Teams of lawyers to help glide through the fabric of bureaucracy.

The system is rigged for the oligarchs. We get beer and circuses. I have been living in the house of the king for a while, the scraps of the top 10% are more than I can possibly consume! Fine food, furniture ($1000s and $10,000s) and so much more is simply discarded.

They are fully looped into the ownership class. Note how Wolf is painting the picture of not just unattainable home ownership but now cars. Next, energy.

Will the masses complain about food rations? Ask the folks in the tent cities.

Trying to keep it simple- when demand finally decreases for a longer time frame than 3 months, prices will come down. It hasn’t yet, overall.

There is still way too much easy money available.

The huge debt levels- government and private, have not caused the flesh wound to become infected, yet.;not until unemployment affects the middle class more, or what is left of it. And then demand will effect/infect inflation

…Expect more bank failures , and dollar destruction until then

Less demand may as well decrease supply as lower prices in the long run.

From less purchasing power follow less purchasing, either in price or volume. If there is no money in providing goods and/or services there will be none.

A luxury car is no cheaper in a poor third world country even if the demand is low.

The hope of Pivot fuels the asset prices. The Fed has to kill this hope. The reality is, the Fed screwed up so big that pivot’s not only likely but guaranteed to keep the engine chugging along. What a mess!

As I posted a day or two back, the pusher is now trying to cure the addicts.

I was wondering this morning, how many people still paying crazy prices for houses might be counting on mortgage rates to drop back to the 3% range so they can refi and comfortably afford the 700k SFHs they’re buying in major metros across the country. They may hope a $4k monthly payment today becomes a $3k monthly payment in a couple years, thereby justifying a purchase of a 700k house that would’ve sold for just 500k a couple years ago.

At the very least, many homebuyers this year must feel convinced that rates will drop enough to spur new homebuying energy to maintain and expand current valuations.

In either case, hope seems to be fueling asset prices, even after so much rate raising. I think the fed needs to stop being so afraid of using darker tone. Stop letting people believe we’re gonna magically go back to 2018 financial conditions. Ain’t gonna happen, no matter what the fed does.

Zest I can tell you that is one of the most common questions I am hearing from people (I’m a mortgage loan officer) when they are getting pre-approved or when they are locking in a rate on a purchase. They ask “when” I think rates will be back in the threes, not “if.” I’m not as smart as the average commenter on this page, but I tell them that they need to wrap their heads around the idea that rates may not be back in the 3’s anytime soon.

I’m actually waiting to see what happens 2 years from fall 2022 when everyone and their sister started getting mortgage rate buydowns. My guess is fall 2024 there’s a lot of people that can’t handle the additional 2% and I doubt a refi will solve their problem at that time.

Hope eventually becomes hoping you can eat today, rather than buying a home.

While not a popular opinion, I believe the Fed engineered this inflationary impulse during the COVID crisis by ensuring all this free money went into spending hands and not asset purchases. Supply chain problems added to the impulse.

I trust we all know that inflation is the only way we’re going to move the needle on this mountain of debt. I don’t like one bit as I’m retired and watching my savings erode, but everyone is getting hurt (unequally of course), save the super rich.

The Fed doesn’t want to crash the economy in attempts to dampen down the inflation. And it doesn’t neet to raise rates much more to do that. We have a very weak (pitiful) economy compared to the 70’s. Much of our economy is “nice-to-have” crap/stuff. So inflation will exact its toll on that part of the economy, businesses will close and jobs will be lost.

It will take some time but not as long as one might think. There is nothing like the worker wage power of the 70’s in our economy (no unions primarily).

Finally, the Russia/Ukraine war has thrown a huge curveball to the Fed and US. This event and how the US responded has weakened the dollar abroad in a significant and perhaps permanent way. The Fed is very mindful of this change as well as more members of Congress. Interest rates will remain in this range. US deficits are going to have to shrink significantly.

Plan accordingly.

But I also believe that the Russia/Ukraine (and larger dollar hegemony challenge) came as a surprise to this plan. So

Agree with Wolf, NFCI is still too loose. But will they have the balls to buck the markets and raise another 25 basis points?

Index Suggests Financial Conditions Loosened Again in Week Ending May 5

The NFCI ticked down to –0.28 in the week ending May 5. Risk indicators contributed –0.13, credit indicators contributed –0.10, and leverage indicators contributed –0.05 to the index in the latest week.

The ANFCI also ticked down in the latest week, to –0.26. Risk indicators contributed –0.19, credit indicators contributed –0.06, leverage indicators contributed –0.05, and the adjustments for prevailing macroeconomic conditions contributed 0.04 to the index in the latest week.

Focusing mostly on the 2000, 2007, and 2019 periods, it appears the Core PCE lags the FFR. Do you think it’s possible that holding rates where they are will allow inflation to come down to the 2-3% range?

Employee dependant businesses at any level now must continually watch for the opportunity to push upward their prices to meet profit goals. It’s part of staying in business. The dog is chasing its tail.

Gone are the days of 0% loans with flatline labor costs, a heck of a change in doing business.

Mr Frost has a good point. While we hear myriads of commentary about how “monetary policy only works with a 12-15 month lag”, it’s a little unclear how that all works on parts of the economy that are not interest rate sensitive. But no one seems to talk about the countervailing and super stimulative fiscal policy. Without both policy levers, working in tandem, I am not sure the inflation beast can be slain.

What evidence do we have that the Fed wont instantly return to ZIRP the moment theyve decided inflation is contained? They got 14 years of asset inflation pushing wealth to the top for the first run of things before having to act, we have to assume Powell thinks he can do it again.

Don’t think anyone believes what Powell thinks. Don’t think anyone believes the Fed either. Since this is a casino, and we are all hoping to get some trades right and hit the “big dirty.” I know most of us will lose, but sure we can try/hope.

In a way it feels like playing a lottery is more honest thing to do than to play the Fed induced casino.

The economy is out on a ledge, well past the point of considering defenestration as it already went past the lending window, and Jay Powell is trying to talk it down.

Things have to break, or inflation won’t be tamed.

Not only brake, they have to leave them broke. There’s no point in printing another 10 trillions soon after something is broke.

I am afraid, this is the most likely scenario.

…dammit, auto – c, now I can’t tell who’s saying things have to stop (brake), or be wrecked (break)…

may we all find a better day.

“Before 2008, the rule was that the Fed’s policy rates were nearly always higher or substantially higher than the rate of inflation. For example, in the 1990s, the EFFR was around 5% to 6%, while core CPI was around 2% to 3%. In other words, the EFFR was double the rate of inflation, which is what pushed down inflation…

And just looking at this chart, I get the distinct feeling that inflation is just being fueled further, rather than being doused, by the Fed’s current interest rates.”

Yet you are on the record saying a pause is the appropriate course of action, Wolf. And when I said that they should have never stopped the 75 basis point hikes, you accused me of wanting to crash and burn everything to the ground. But if they had continued with the 75 basis point hikes, we’d now have a fed funds rate that was well above CPI, and more in line with the prior policies.

Let’s be honest, the FED is engaging in what can only be described as a fake inflation fight. Jerome Yellow Powell had the audacity to name drop Volcker when in fact he makes Arthur Burns look good. The FED is dying to pause. They are looking for every little tidbit they can to justify it. Everybody knows it. They begrudgingly raised rates, only after rip-roaring inflation for more than a year while they stood by and made up lies, calling it “transitory.”

This doesn’t even get into all of the fake tough talk on their balance sheet and how they were even considering selling MBS outright. Whatever happened to that? We know – it turned into not even hitting their MBS sales target. And now housing has started to catch bids as mortgage rates are falling.

The FED is a serial lying entity which needs to be abolished. There’s a headline on one of the fake news financial sites this morning talking about how Social Security checks have lost 36% of their purchasing power since 2000. The FED is robbing society blind and handing the money off to billionaires and hundred millionaires so they can upgrade their yachts.

“fake inflation fight”

Exactly! Perfectly fitting with the everything fake society of today’s.

I agree.

Totally agree with you.

Powell is saying he is serious about fighting inflation but he is lying.

Why isn’t Biden questioning any of this? He needs to be paying more attention to what the Fed is doing.

FED is supposed to be independent. Biden needs low rates to fund his govt deficit spending so he is also complicit.

Also, mid term was supposed to be bad for Dems because of inflation but it was pretty good relatively. So Dems don’t really care if common joe is getting scrwed as long as they keep getting voted in.

There is a huge inflation lobby out there that no one is talking about. A lot of entities benefit from inflation. The government itself gets to pay off it’s debt with a devalued currency. Asset rich entities get the same, while their assets increase in value. Meanwhile all the cost of the inflation is passed on to those at the bottom of the economic latter. So we have social unrest as the gap between the rich and the poor widens. The middle class is caught in the middle having to pay for social safety net for the poor and subsidize the rich while having to pay higher taxes and higher cost for necessities. Everyone loses except the rich.

So aptly said SC!

I firmly believe that FED is sold out to rich and elite and they are having a facade of fighting inflation but their intentions are not.

Actions speak louder than words/charter.

Either WR’s article is wrong and inflation is going down or FED is simply playing with words.

If FED were really serious about inflation, they’d have raised by 50bps at at least.

I’d say the Fed is simply playing with words.

I think Wolf is right, raising rates more so soon will send the markets, banks, etc into greater risk. At least a worse problem may be prevented because Wall St lives and breathes by every word the FED says, so the Fed can keep them hanging for a while.

I think the Fed was actually trying to get rates up 2018-19 but it got knocked down by then POTUS. How much better would it have been to enter the pandemic with 2+% interest rates?

Then you have Congress whose only answer to anything is to spend like drunken sailors. No help there.

The Fed is in a juggling act. Dang if you do, dang if you don’t. Their real only solution is to prolong the boat ride and not hit the iceberg head-on.

> fake inflation fight

Exactly this. A filibuster and soft default.

They had no remit to purchase MBS, yet they did it.

As if an entity which breaks the rules to buy MBS wants to see housing fall.

High house prices are used to force us to work in our “free” West.

Have to keep housing high ,or black stone goes BROKE

As a retired lifelong saver, toaster give away receiver, and now, the Wolfman explains more of my frustration with Government, AGAIN.

THANKS,,,, love reading your articles

Wanted to add.

Welcome back Carter/Reagan?

“With core CPI at 5.52% in April, the “real” Effective Federal Funds Rate (EFFR minus core CPI) is still a negative 0.44%. And negative real policy rates are still a form of interest rate repression, and are still stimulative of the economy and of inflation.”

I have to partially disagree with your statement above. You are comparing the present fed funds rate to the past inflation rate. If we shorten the calculation period of the inflation rate to a six month annualized rate from your 12 month rate we get an April annualized six month inflation rate of 2.8% (March also had a 2.8% annualized six month rate) considerably below the 5.08% Effective Federal Funds rate. Using this measure (the six month annualized inflation rate) conditions are tight, hence the financial troubles in the banking and commercial real estate sectors.

That said, as you say, inflation is entrenched and it will probably take many months, if not years, to squeeze it out of the system. For now, the Fed should hold rates steady. I was against the last rate increase of .25% (but its probably not significant) and let the economic fallout continue (Schumpeter’s creative destruction).

The FOMC doesn’t give the slightest bit of a hoot what stock markets do and will continue to tighten even if many stocks go to zero.

I disagree. The Fed works behind the scenes to keep stocks up. A crashed stock market would be devastating.

At this point, I believe it is not the interest rate but the increase in money supply that is levitating asset prices and inflation.

If the Fed pauses rate hikes, it needs to significantly quicken the pace of QT. When people are unable to create huge wealth by pushing buy/sell buttons on a computer, they must create real value in order to survive and spend.

The Fed knows the wealth effect creates inflation, and that’s why they created phantom wealth in the first place. Bernanke explicitly targeted it via his QE program. Why is the Fed so reluctant to reverse that QE now that they see inflation levels at 300% of target, for years?

Perhaps there is a different purpose for creating the wealth effect.

A 6-month inflation rate of 2.8% is 5.6% annualized; still above the EFFR of 5.08%.

Sorry, I tried to make that clear. The six month rate is Nov 0.1, Dec -0.1, Jan 0.5, Feb 0.4, March 0.1, and April 0.4 which totals to 1.4% for 6 months. Times 2 gives an annualized rate of 2.8%.

Progress on final inflation stopped after stock prices stopped going down. Stock prices are the canary in the inflation mine. The Fed is probably waiting for them take another leg down before giving Wall Street the rate cuts it craves.

But the balance sheet, despite coming down recently, is still much bigger than pre-Covid. And bank reserve requirements, cut to zero on March 26, 2020, are still zero. (hmmm) Monetary policy hasn’t been as tight as Fed funds alone would suggest.

Why is that?

The Fed has all the data and can reduce inflation, if it wants. Why is the Fed protecting asset prices? Why is the Fed endeavoring to preserve wealth created out of thin air?

Is the Fed pursuing some sort of trickle down theory?

The Fed’s been in the trickle down business ever since Bernanke decided to promote a “wealth effect”. The idea was that by kiting asset prices, people would feel wealthier and spend more. Of course since the wealthy are by definition the owners of most of the assets, it made the rich richer. The rest got what trickled down.

You could make a case that the policy dated as far back as the Greenspan era. Greenspan supplied the monetary helium for the 1990s stock bubble, and again for the 2000s housing bubble.

Powell now seems intent to stop playing reverse Robin Hood. Guess we’ll have to see to what extent he succeeds.

Powell hasn’t been tested yet. So far, he seems eager to please the crybabies on Wall Street with tiny rate hikes and prospect of a pause.

On Powell’s X-Rays, you can see something that might be a spine, but odds are it’s a puppet stick.

You do realize that banks have more than $3 trillion on hand in the EXCESS RESERVES ACCOUNTS inside the Federal Reserve, don’t you?

$3.258T as of latest(March) report. Of course, this is the total, and does not identify how much is of each individual bank.

haha that’s one hell of a transitory inflation….

I think a recession is unavoidable, that the Fed is trying to induce one and that is a good thing. Their only hope is that it be short and shallow.

You don’t get a binge without a hangover, or get off H without ‘cold turkey’.

Here on Van Isle, housing inflation has been well into double digits for several years. Rents have doubled in 5-7 years. This is not normal and a return to the mean will require several years of housing deflation, i.e. a recession.

As the Fed piddles, asset prices continue to inflate. Elevated inflation becomes an expectation.

The Fed needs to do its work. Sell the MBS. Wall Street crybabies are just a sliver of the country.

The Fed owns this problem that it created.

It’s interesting how Wall Street is crying for lower rates to reduce debt burdens, but few companies in trouble are out there trying to raise equity capital, because it will decrease stock prices down to rightful levels.

Wall Street is begging for a continuous handout, as a consequence of the Fed’s free money policy.

Looking at my credit card statements post-Covid and realizing how much more I’m paying to eat out, I’m starting to get much more serious about cooking at home. The first dozen or so times being hit by checks twice what they used to be I sloughed off, so nice it was to get out. But it’s gotten old. I’m pushing back.

How many others starting to do the same?

Judging by parking lots around restaurants during the evening, i am going to say that not nearly enough people are doing that so far.

We used to eat out 1-2 times a week. Now we order takeout pizza once a week and go to a nice place on birthdays. Cooking at home gets old but eating out is so expensive.

And you can make a good pizza for a small fraction of the takeout price….

We live on a budget. If our dining out budget is spent, once it’s gone, it’s gone. If it buys 4 night out, fine. If it’s 3, fine. If we blow the bank all at once, fine. But that’s it until next month.

We’ve always lived on a budget. It’s an easy way to rein yourself in from spending like an idiot. Helps you avoid a lot of potholes on the road of life.

1) From 75% suckers money and 25% printing to 75% printing and 25%

sucking.

2) Hundreds of wheelbarrows crossed GW bridge and park in front of NY

Fed Williams to count the new fresh cash.

3) Not as fast as clicking, but good enough to prevent default. After the initial shock banks will feast on higher rates loans.

4) Just for u teaser at 0% til 4/2024, or 1.99% til 7/2024 with 5% fee. Thereafter c/c rates.

The fact that people don’t expect FED to fix the problem, which was created by the same institution to begin with. The same people in charge that saw nothing wrong with insane amount of QE. That’s why people believe this inflation is here to stay and it very well might. Any inflation short of 0% is already bad in logical way. Therefore if we were able to live with 2% without issues, therefore we will now live with 5% instead. As long as Inflation will stabilize, i think consumers and FED will be content.

Sorry, I missed Dazed and Confused’s comment. Please delete.

It’s not just crybabies for free money. There’s a “regime change” on wall street and it hurts (them)! The zombie companies with leveraged loans cannot roll over there coming maturities at full value anymore! Bloomberg ran an article: the “leveraged loan” market is ~$1 Trillion in size. $500bn is coming due in the next 2 years! (the article quoted King Street capital mgmt, dear readers, if you wanna google it, put that term in).

We need “Shock and Awe” w/r to interest rates. These gradual interest rate increases aren’t gonna cut it. They are still well below the rate of inflation which I put at close to 15% not the 5% being reported. Businesses just pass these costs on to the consumer who winds up paying higher prices. So, we get more inflation as a result. The rich deduct the increased financing costs off their taxable income and are not affected. The only solution now is to do what the commander did in NAM.

“Destroy the village in order to save it.”

Volcker came the closest to doing just that in 1981. It worked then and would work now.

There are several ideas that I think need fleshing out such as we ” need shock and awe”, which I counter that the citizens have had enough of that.

Instead, I suggest, the Fed should unrelentingly increase interest rates at every sixth week meeting by at least 25 bpt as long as the prices that are charged to the people increase.

I’ve definitely contributed to inflation – just spent $$$$$ on shiny new solar panels for my roof.

I did it primarily for economic reasons (although I also believe renewable energy is good) – I’d rather spend my capital now to protect my future self from rising energy prices.

Isn’t government shelling out $ as an incentive to install those, or is that program over? Also let me know, when they come up with an esthetical way to incorporate those into a house…

I agree. Solar panels sure are ugly.

I’ll get a tax credit when I do my taxes next year:

I bought the panels outright rather than leasing, and put half down and borrowed the rest. I’ll either use the credit to pay down the loan or I’ll stuff it into a CD – depends where rates are and whether or not I can get a higher APY than the loan.

Of course they’re ugly, but now I’m a net exporter and actually sell power to the electric company rather than buying it. My “trade” here is betting on higher inflation (and therefore utility prices) for years to come.

It would be great if you were to be so kind as too enlighten the rest of us (me) as to the cost as well as the construction requirements of a solar installation since I am considering the same. Thanks in advance.

Question for Wolf and a recent inflation tracker that looks very suspect to me based on Wolf comments of data tracking error and websites.

truinflation.com with current inflation real time under 4 percent.

I see the biggest errors is the allocation of rent in their equation (under 30%) and sources including folks like carguru and zillow. Keep up the great work and I agree with Wolf we are still in an accommodative environment. But a comment from Wolf on their methodology would be helpful for a novice like me.

Recently mentioned by an ex Fed economist.

To be fair, the MMT crowd have been saying this for a long time. No recession this year and these rate increases could actually support inflation (cost of credit is reflected in the price for goods and services) until something break down (for example, construction activity is particularly sensitive to rate increases).

Higher interest rate + high budget deficits = lots of money sloshing around via the interest rate income channel.

Someone posted a chart on Twitter, federal government interest spending is now equal to defense spending and 30% of the debt has to be refinanced in the next 12 months….lots of private sector spending support.

The MMT crowd is a mouthful without skepticism. I’ve always thought that QE is the real world corruption of the MMT principles in action.

Inflation plateaued at 5.5% per year translates to average inflation of roughly .5% per month. Assets are considered protection against inflation, and asset prices can be expected to increase by the same .5% per month, on average over time.

Total hard assets in the economy are something like $100T, and a .5% increase in the value of those assets equates to about $500B of artificial wealth transferred, every month, from the asset poor to the asset rich.

So, what explains the lack of urgency at the Fed? If the Fed pauses, the markets will not. Markets will bank on loose monetary policy, and run.

How do you explain the fall in home prices from peak ( rought 13% ) when the inflation is running high..

It’s a short-term blip. Housing prices are up 30-100% the past few years. If the Fed continues its loose monetary policy, housing prices will re-ignite.

Nationwide housing prices have gone up around $10T a year the past several years. That’s been a transfer of wealth from current home owners to future homeowners of about $500B to $1T a month. The slight decrease in prices of late pales in comparison.

This Fed has lost its mind, or perhaps it seeks to create an aristocracy.

Inflation will be high for a few more years my take. What do you put the odds at that real estate will continue it’s climb.

I agree but the trend is downwards only and housing is solely decided by affordability which is dictated by rates and wage inflation.

I don’t know how would this end but I know that housing un affordability is all time high and my supposedly hottest market has seen many boom and bust cycles.

Home prices are yet to catch up with rates and it’d happen sooner or later.

Its all a game of monthly outlay for housing,

I call a bluff on this whole housing bubble. When there is a will, there is always a way to build more cost effective, especially if the demand was truly there.

Inflation + shutdown of economy created shortages and prices of construction materials increases. Those are now back to reasonable levels, some even below pandemic, yet builders aren’t too keen on fulfilling the market.

During Housing Bubble 1, there were subdivisions of new houses built left and right, I don’t see that now at all. There is a reason.

“This Fed has lost its mind, or perhaps it seeks to create an aristocracy.”

We are headed for, steered towards a nationalized banking system and a digital currency.

With every “emergency” there is the opportunity for powers to accrue even more power, though the “emergency” is usually from their own policies and actions.

Or the Fed is the face of an established aristocracy that is comparable to the economic tyranny that instigated the revolutionary war waged by the 13 original colonies.

Well my disagreement with your hypothesis is that asset price increases are not linear across time but are more parabolic, with a peak, like now.

The current level of asset prices require zero pct money, as Wolf described.

What, I think, is an under appreciated perspective is the degree of over valuation of the four asset bubbles that the Fed is feverishly trying to undue since it was them that created this monster.

Housing, stocks, bonds, and the military.

The Fed is more a repent felon than a hero, I would assert.

Housing in the Swamp is still 30% over the level prior to the pandemic according to the MLS. No housing crash yet.

Name a single item with a 30% increase in price.

China export and import are falling after China opening. US and Europe

are China biggest customers. Let them sell to Iran until US econ recover

from the slump.

CNBC: Jamie Dimon warns panic will overtake markets as U.S. approaches debt default

JPMorgan Chase CEO Jamie Dimon said Thursday that markets will be gripped by panic as the U.S. approaches a possible default on its sovereign debt.

“The closer you get to it, you will have panic” in the form of stock market volatility and upheaval in Treasurys, he said.

Such an event would ripple through the financial world, impacting “contracts, collateral, clearing houses,” Dimon said.

JPMorgan, the biggest U.S. bank with about $3.7 trillion in assets, has been preparing for the risk of an American default, Dimon said.

Such an event would ripple through the financial world, impacting “contracts, collateral, clearing houses, and affect clients definitely around the world,” he said.

The bank’s so-called war room has been gathering once weekly, a rate that will shift to daily meetings around May 21 and then three meetings daily after that, he said.

Not sure that this debt crisis nothing burger even compares to the hysteria of Y2K. I was there in the plant when the clock kicked over onto the new century and then nothing happened except the tech stocks reached their peak and began too fall in price.

How does one get a 1.7 trillion shortfall and also a 3.4% unemployment rate at the same time? One of those numbers isn’t true. In this day and age it may be both ;)

And if current trends continue you’ll probably end up in jail as a domestic terrorist for pointing it out! ;)

Now that I get 5% dividends in my bank. Why not spend that on core CPI to enjoy life while I wait for a drop in stocks or house prices. Nothing better to do…

Jamie warns us ==> next week the regional banks might popup.

Hey wolf – Richard Werner wrote an article on “the conversation” concerning the invention and uses of QE. It was posted March 14th of this year – in case you haven’t seen it, you should check it out. Let us know what you think.

I’m retired and because of the higher interest rates on my savings, my income has increased 16%.

I’m locking in the 4% for 3 years, on some, thinking inflation is slowly starting to come down.

Buffett raised 2 billion in cash in the 1st quarter. He seems to be preparing for a stock market crash. He’s waiting to by a jumbo business when prices drop.

Higher rates will depress the stock market sooner or later.

Agreed on crash coming. The market is WAY overvalued with people expecting interest rate drops in early fall. I don’t see it happening with inflation where it’s at. FED has to keep rate high for much longer than ppl are anticipating

Until Powell unloads mbs, we will have inflation. So, inflation will not drop measurably for the forseeable.

7% mortgage rate would gradually kill the housing market over time.

Is Core CPI, or straight CPI the metric that should be used?

Core CPI doesn’t work the way anyone I know runs their household spending. If gasoline goes up, that doesn’t make the household budget bigger, something else gets cut. If gasoline goes down, the household budget doesn’t get smaller, spending happens somewhere else.