The vast wealth of the top 1% households declined, the minuscule “wealth” of the bottom 50% increased a tad.

By Wolf Richter for WOLF STREET.

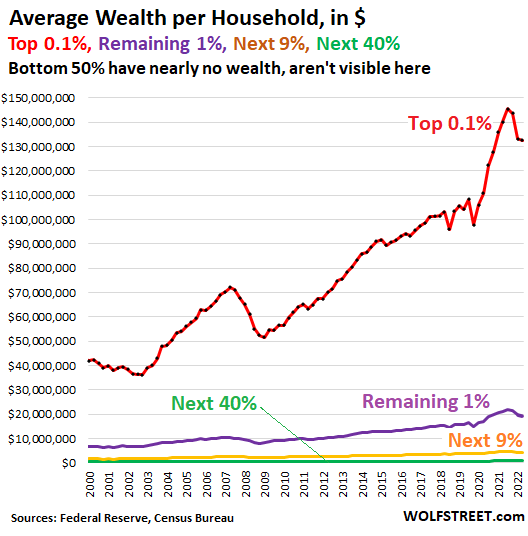

In the third quarter, the drop in asset prices continued to reduce the biggest wealth disparity ever between the “Bottom 50%,” who gained a little wealth, and the very top households – the “Top 0.1%” and the “Remaining 1%” – who gave up some of their vast wealth for the third quarter in a row, according to the Fed’s data on the distribution of wealth by category of wealth.

In other words, the tightening by the Fed – the higher interest rates and the beginning of QT that the crybabies on Wall Street bewail on a daily basis – has undone a small portion of the horrendous wealth inequality that the prior years of QE and interest rate repression had caused.

Alas, the Bottom 50% don’t show in the chart because their “wealth” is so minuscule that it’s just a straight line on top of the horizontal axis. Even the “Next 40%” (everyone below the Top 10% and above the Bottom 50%) have so little compared to the top 0.1%, they barely register at the bottom of the chart (green line). Note the gigantic wealth disparity between the 0.1% and the Remaining 1%. This is the nature of the wealth disparity in America, according to the Fed’s data. But QT and rate hikes are now undoing a little of it:

To put it into the perspective of households, I divided the Fed’s wealth data by the Census Bureau’s number of households to obtain the average wealth per household in the Fed’s categories of wealth.

Average wealth per household, by wealth category in Q3, 2022:

Here is the average wealth per household in Q3, by wealth category, and how it changed from the end of 2021 (in bold). Note the gain by the Bottom 50%:

- “Top 0.1%” (red): $132.4 million (-$13 million, -9.0%)

- “Remaining 1%” (purple): $19.3 million (-$2.4 million, -11.2%)

- “Next 9%” (brown): $4.4 million (-$269,000, -5.8%)

- “Next 40%” (green): $768,000 (-$16,500; -2.1%)

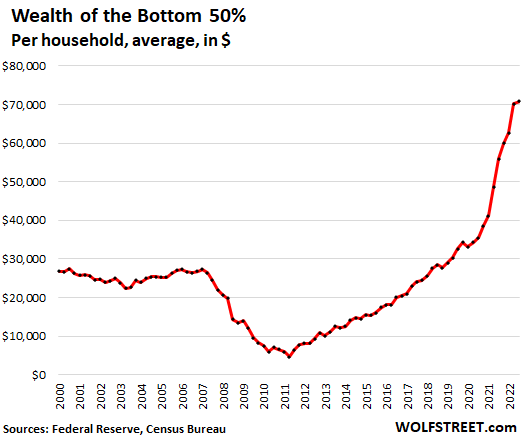

- “Bottom 50%” (not shown in the chart): $70,800 (+$10,800; +18.1%).

The Bottom 50%, 63.9 million households.

The Bottom 50% own almost no stocks and mutual funds, which is why a stock-market swoon doesn’t faze them. Most of their assets are their home and “consumer durables.” Consumer durables are things like cars, appliances, electronics, etc., whose value depreciates.

They have $164,200 in assets per household on average, minus $93,400 in liabilities = wealth of $70,800.

Assets:

- Real estate (home): $96,500 – meaning many households don’t own any real estate.

- Consumer durables (cars, appliances): $30,000

- Stocks, mutual funds: $3,000 – meaning most households don’t own any equities.

- Pension entitlements (defined benefit & defined contribution): $13,600

- Private business: $2,400

- Other assets, including money in the bank: $18,700

Liabilities:

- Home mortgage: $45,400

- Consumer credit (auto, student, credit cards, other loans): $41,300

- Other liabilities: $6,700

Their wealth has increased by $10,800 per household on average in 2022, largely due to an increase of home equity and consumer durables. This is why half of Americans got nearly nothing when the Fed inflated the stock market with QE and interest rate repression; and they don’t care what happens to the stock market. What they care about is the purchasing power of their labor – and inflation, including house-price inflation, ate it up.

Here we’re looking with a magnifying glass at what in the chart above didn’t show because it was a straight line on the horizontal axis:

The Top 0.1%, 127,800 households, primary beneficiaries of QE and interest rate repression.

The Top 0.1% on average own a huge amount in stocks and mutual funds, and they own high-value private businesses. And they have relatively little debt, compared to their assets.

A household in that category has on average $133.5 million in assets, minus $1.1 million in liabilities = a wealth of $132.4 million.

Assets:

- Real estate (residential & other): $11.9 million

- Consumer durables (cars, boats, etc.): $3.3 million

- Stocks, mutual funds: $53.9 million.

- Pension entitlements (defined benefit & defined contribution): $1.2 million

- Private business: $41.9 million

- Other assets: $21.3 million.

Liabilities:

- Home mortgage: $488,500

- Consumer credit (auto, student, credit cards, other): $147,100

- Other liabilities: $461,300

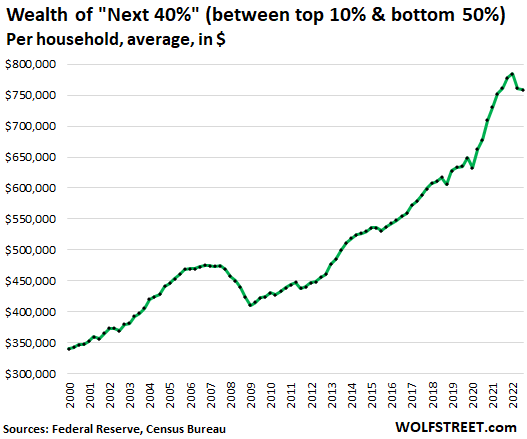

The Next 40%: the 51.1 million households below Top 10% but above Bottom 50%.

Their assets are spread across the board, and they too have relatively modest liabilities.

A household in this group has on average $911,200 in assets minus $152,700 in liabilities = a wealth of $758,500.

Assets:

- Real estate: $336,300

- Consumer durables (cars, etc.): $63,000

- Stocks, mutual funds: $66,900

- Pension entitlements (defined benefit & defined contribution): $235,000

- Private business: $40,600

- Other assets: $150,100.

Liabilities:

- Home mortgage: $112,700

- Consumer credit (auto, student, credit cards, other): $32,600

- Other liabilities: $7,300

Their overall wealth dipped by only 2.5% due to their stock holdings. This is the green line in the first chart above under the magnifying glass:

How did we get here?

During the era of QE and interest-rate repression, the “Top 0.1%” and the “Remaining 1%” got immensely richer, while the “Bottom 50%” had nearly no wealth to begin with, and still have nearly no wealth. QE and interest rate repression created the biggest wealth disparity ever in dollar terms, and in the shortest amount of time – and it turned into the greatest economic injustice of modern times.

It was based on asset price inflation – which the Fed long justified by its official policy, the “Wealth Effect,” which counts on making the already wealthy a lot wealthier by inflating asset prices via interest-rate repression and QE, so that the then immensely wealthier can spend a little of this wealth, so that this can trickle down to the rest of society.

Alas, this era of the wealth effect ended in 2021. In 2022, the Fed began hiking rates and it kicked off QT, and as yields and interest rates rose, asset prices began to fall, and the wealth of the wealthiest households began to fall as well, while the tiny little bitty wealth of the bottom 50% – a large portion of which are consumer durables – has increased.

The Fed’s reversal of QE and interest-rate repression in 2022 is deflating the Everything Bubble and is thereby narrowing the horrendous wealth disparity that the Fed had wrought with its easy-money policies in the prior years.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m in the “Next 40%,” and I feel like I live on a shoestring, to stay there. I watch every dollar. I wonder how the hordes below my wealth live, day to day. They make choices like having kids, that seem to create and carry risks and liabilities (not just for themselves), that are unfathomable to me.

Heaven forbid anyone who isn’t a part of the enlightened rich have children(not that the TFR in the USA supports the idea that many people are having children at all).

This post reminds me of these articles that regularly appear in my wife’s magazines, which feature families with incomes of $250k annually whining about how they live paycheck to paycheck, in some sort of weird humble brag/navelgazing. “Oh no, I only have a 7 figure net worth, poor me!”

I am glad to hear and different view. I makeabouit half the national average income, but I take care of myself and, by carefulness and thrift, my society and neighbors’ financial well being, by not being a bum who is careless about things (like having kids and dumping the risks and costs on others). I will not do that in the name of some “right” or “freedom.”

A flag-waving “conservative” woman I know very well had a child incurring (in the 80s) more than $100,000 medicals that were dumped on the public, and she had zero guilt (sense of responsibility) for this wealth transfer top her. (If the kid makes money, she keeps the gain, but if not, society eats the loss). Now her lifestyle (several children later) means my family will probably have to support her. Freedom isn”t free. It’s easy to be righteous on somebody else’s dime.

Congratulations on thinking you are a genius for experiencing the Micawber Effect, it’s not like Dickens came up with it centuries ago or anything.

I had a feeling this sort of response would be forthcoming. It’s always about some average individual welfare queen, not the ultra rich leftist welfare queens like Bezos and Gates who have dumped billions of dollars of obligations on the taxpayer through loopholes provided by their purchased government.

Maybe the problem in your example is the medical monopolies in the USA and not someone’s kid drawing a terrible hand in life? Just food for thought.

This is your compassionate progressivism right here folks.

No matter how cheaply you live, your very existence costs the rest of us money. Our taxes pay for the fire department and police force that protects you. We help pay for the sewer and water lines you need, for the roads (or public transit) that take you to your job. We pay for the vast military machine that protects you from alien invaders, etc.

This is one of the nuttiest arguments I’ve ever seen in the Wolfstreet comments

Mary – Your argument can’t possibly be true.

How does your economic view work? Where each individual costs, more than the pay?

If you give it any thought, some people subsidize others.

Some people, are subsidized by others.

The expense of all the welfare queens in our country is a tiny fraction of the zero interest rate subsidy gobbled up by the uber wealthy. But the poorest and most vulnerable are easy targets. What happens when the poorest can afford to eat? Civil unrest, crime, desperation? These are social problems that should not be overlooked. And yet as voters we turn a blind eye to the fact that the top .01% hold all the money and the power. We are still peasants. But we have just enough to keep us feeling ok.

There was a billionaire who complained half of Americans aren’t paying taxes. One of his lawyers was convicted of tax evasion. His daughter’s father in law was convicted on multiple counts of assisting in filing false tax returns. The billionaire’s company was convicted on multiple counts of tax evasion. One of his lawyers died of AIDS while under indictment. Another one of his lawyers lost his license to practice law. This billionaire does not want Congress to release his tax returns. Info was leaked to the media this billionaire did not pay any Federal income taxes a number of years.

yes david.

most people know, billionaires, per capita, receive the largest amounts of public assistance. lower tax rates than convenience store workers, and, repeated high-cost bailouts.

Sub,

If you use Microsoft products or Amazon your actions don’t fit your words. If you don’t use them then I hear your opinion.

David Hall,

I think a lot of real estate owners don’t pay much in taxes due to the way the tax code is set up.

You can have a real estate property that cash flows positive, yet there is a tax loss due to depreciation. Maybe I do or don’t like it, but if you are filing your taxes according to the tax code you have done your part.

phleep – the fact that we have allowed our healthcare system to get so very distorted is to me the very central problem with America at the moment. special interests using government policies to become filthy rich.

so the pharma companies and healthcare insurers and device manufacturers, etc all become filthy rich, while they drive people to bankruptcy, but the high costs of healthcare also make many labor-intensive types of American businesses uncompetitive.

and then we bring in millions of illegal aliens, which require government services and who pay nothing when they go to the ER because they have no money to pay, so the bill for someone who is insured is much higher to pay for the care of those who cannot pay (I think I heard that up to 50% of medical bills go unpaid). of course, the billionaires want to bring in illegal aliens as cheap labor, but also as consumers to increase their revenues.

when you think about the attitudes of the people living in/near Washington DC, how they feed off the wealth generated by people in the country, it is just obscene.

I can’t take all this babble….so I’ll address GTV who seems the worst of the lot, although it’s hard to tell.

Healthcare is our “central problem”? (it’s bad, but not the worst).

What about the planet destroying fossil fuel and chemical industries? OR, MUCH BETTER yet the FINANCIAL industries, who do NOTHING but shuffle money around and around and take their cut with each shuffle?

-the 1999 repeal of the Glass-Steagall Act, which had prohibited commercial banks from undertaking investment banking operations (and vice versa);

-repeal of regulations banning off-balance sheet accounting practices, which entail accounting maneuvers that enable financial institutions to cloak their liabilities;

-preventing the Commodity Futures Trading Commission from regulating derivatives;

-the prohibition by the Commodity Futures Modernization Act of 2000 of the regulation of derivatives;

-adoption in 2004 by the Securities and Exchange Commission of “voluntary regulation” for investment banks;

-adoption of rules by global regulators to allow commercial banks to determine their own capital reserve requirements;

-refusal by regulators to prohibit rampant predatory lending and their ceasing of the enforcement of regulations that were already on the books that banned such lending practices;

-preempting, by federal bank regulators, of state consumer laws that restrict predatory lending;

-federal rules preventing victims of predatory lending from suing financial firms that purchased mortgages from the banks that had issued the original loan to the victims;

-expansion by Fannie Mae and Freddie Mac into the subprime mortgage market;

-ignoring of traditional anti-trust legal principles and thus allowing financial institutions to continue to expand and to merge, which led to the emergence of huge banking conglomerates that were deemed “too big to fail;”

-allowing private credit rating companies to score incorrectly the risks associated with mortgage-backed securities despite their conflicts of interest;

-the 2006 enactment of a statute to restrict regulation by the SEC of financial institutions.

To achieve these deregulatory aims, the financial industry, including commercial and investment banks, hedge funds, real estate companies and insurance companies, made $1.725 billion in political campaign contributions and spent $3.4 billion on industry lobbyists during the years 1998-2008. In 2007, close to 3,000 federal lobbyists worked for the industry. Overall, the financial industry spent more than $5 billion over a decade to strengthen its political clout in Washington, DC.

To simplify, it cost lobbyists a hell of a lot to get on the Congressional Baseball team.

NOW! To who’s advantage IS IT to do such meddling in in our attempt at democracy? TO who’s advantage is it to promote the hating of their OWN government and the shrinking/weakening of same?

Look at the insane inequality charts….and you “might get it”.

I won’t even mention the Reagan era crap that began laying the foundation for the above.

Actually, I believe the charts maybe produced some “guilt-trips” (to use my old hippie phrase) among some commenters.

I practice what I preach. I have no kids for reasons of integrity. I don’t front bills to others based on misplaced (biases of) “optimism.”

I, too, practice what I preach.

I had multiple kids and paid for their schooling – no loans – until they earned their BAs.

I now get to spoil all my grandchildren. Lots of fun. And when I get tired I can say:

“Here Son/Daughter your child needs Dad/Mom” and go home for a nap.

We have no debts. House and car paid for.

I do want to give a great big thank you to all you workers out there who are paying for my Social Security and Medicare bills. Thank you very muchly!!

Ya know, dude, it really does take a village. It’s a concept that those in your shoes utterly fail to comprehend time and time again. You go through life counting and keeping track… and figure that everything is a zero-sum game – someone else wins, and you necessarily lose.

News flash, it’s not. Some things are simply not quantifiable. Like the quality of life, community, polite society, friendship, and many other things that do not have a price.

Humans are social animals. We all do better when we all do better, and that means taking care of those less fortunate. As far as kids go, they are one of the most expensive and joyful things in life. And, as it turns out, necessary for the continuation of our species. To relegate parenthood only to those whom you deem to be worthy is blasphemy against the entire human race.

I feel sorry for you, Phleep. Perhaps go and check the “Get Off My Lawn” sign in your front yard… some street urchin may have pinched it. Yikes.

P

Typing with your nose again, eh?

Why?

Because you must have broken both your arms patting yourself on the back.

Anon,

Anyone receiving social security benefits should not fill guilty. You basically had no saying in the matter. Fifteen percent of your compensation went into it. It’s a government pension plan with some warts.

Lost a lot of respect for you based on your posts in this article. Not everything in life is about money, your views on other’s health problems are very disturbing.

“I have been assured by a very knowing American of my acquaintance in London, that a young healthy child well nursed, is, at a year old, a most delicious nourishing and wholesome food, whether stewed, roasted, baked, or boiled; and I make no doubt that it will equally serve in a fricassee, or a ragout.”

-Jonathoa Swift

Perhaps they are more optimistic about their future?

Everyone doesn’t live the same life or assess risks in the same way.

The ‘hordes’ will be fine.

dougzero

An estimated 40% of infants are on WIC welfare.

We all saw how Americans couldn’t survive a few weeks without a paycheck, in 2020.

The hordes have been failing for decades.

I agree with you phleep.

Americans are (largely) divided into the Super Rich and the Generational Poor.

The diminished Middle is forced to subsidize both the Super Rich and the Generational Poor, with constant bailouts, reflected by low interest rates, welfare, speculative bubbles, and inflation.

“The diminished Middle is forced to subsidize both the Super Rich and the Generational Poor”

So True. The diminished middle is now overwhelmed and demotivated. Fed is too slow in correcting valuations as is obvious from above charts.

One more spending bill resulting in one more rally as stock and housing market valuations still remain above pre-pandemic highs.

God bless America.

Agree, wage earners and regular job holders are paying an unfair portion of society’s cost. But we have to acknowledge half the country supports reduced capital gains tax rates for the wealth holders, free basis step-up for wealthy heirs, deferred taxation until appreciated assets are actually sold, and many other tax giveaways to the wealthy class. In addition, half the country supports costly, excessive, ineffective, and often fraud-infested welfare programs for the bottom 50%.

But I’d argue the biggest beneficiaries of our system are the scammers, lobbyists, and special interests that manage to send the government giveaways their way. Wall Street, PPP program fraudsters, unemployment program fraudsters, military contractors, insurance companies, etc., all derive a great deal of wealth from government waste and inefficiency. That’s where the bulk of the problem lies in my opinion. If we would simply move towards a capitalist system with modest progressive tax rates, as opposed to a “who-do-you-know” bailout system, everybody would be a lot better off. If people didn’t succeed economically in that system, at least they’d know they had a fair shot at it.

Fortunately, or unfortunately, we haven’t seen anything yet. Nobody has paid the tab for all the spending put on the $30T government spending spree. Who will have to pay that tab? That is a big question.

yes bobber, the richest certainly get the biggest bailouts.

but hey. those billion dollar sports stadiums. paid for by taxes. they benefit the poor too. it is logical the global poor, spend so much on celebrity and sports.

It depends how you define “wealthy,” but the estate tax basis step-up really benefits the upper-middle class and to a much lesser extent the middle class who own appreciated assets. The logic behind the step-up is the assets of a decedent are subject to the estate tax. Taxing them again under the income tax was deemed unfair, especially when assets often needed to be sold to pay estate taxes.

However, the step-up applies even if the decedent’s assets don’t exceed the unified credit against estate taxes ($12,060,000 in 2022, though much lower in the early 2000s). Many people have substantial wealth below that threshold. Therefore, they avoid paying estate taxes, but their heirs still get the basis step-up.

This issue was highlighted when the estate tax was repealed temporarily in 2010. Due to the repeal, the basis step-up was also repealed. Congress ultimately reinstituted the estate tax and estates for people passing in 2010 got to choose whether to be subject to a new estate tax or take advantage of the repeal. One reason there was widespread public support for bringing back the estate tax is far more people benefit from the basis step-up than will ever actually pay estate taxes due to the amount of the unified credit. This was an area of tax policy where the mass affluent’s interests were protected ahead of those of the ultra-wealthy.

Dear Landed Gentry,

There are tax benefits to having kids, at least in Canada. There is also an incentive, though controversial, that one gets more freebies for having kids.

My decision is not to procreate, because I don’t want my child to become a rent and wage serf to the elites and landed gentry.

Nearly all of that wealth of the bottom 50% is in their home and that is going to evaporate for many people. Of course averages are very different for any individual, but it is likely the average net worth of the bottom 50% will drop by 50% within the next two years. They basically own nothing. Even the next 40% basically have half of their wealth in their home. There are very wide individual differences, but this is basically a completely failed economic system.

So true. If you worked hard and put money in bank savings savings accounts, you would have seriously lost most of your original purchasing power to inflation. If you put it in stocks, you would have lost most of it to scams. Rent houses are the only thing you can make even a little at and they are hard to come by…

What are ordinary wage earners to do?

I believe the saying for those goes like ‘go to hell and die’. Applies to any country now, not just the States.

Thank you for your helpful reports, Wolf. Do you happen to have the “Top 10%” detail section of this one? It leaps from the “Top .01%” to the “Next 40%.” Inclusion of the detail section for the “Bottom 50%” would also be instructive. Thanks again!

The categories are:

Top 0.1%

Remaining 1%

Next 9%

You can combined these top three categories into top 10%.

Next 40%

Bottom 50%.

I gave you the detail on assets and liabilities for the Top 0.1% and for everyone below the top 10%. That’s already too many numbers. What I didn’t give you are the details of the 9.9% below the top 0.1%. But you can guess, and you’ll be pretty close. Model them after the 0.1%. In terms of the asset and liability distribution, they’re similar.

For me, the chart that interests me the most would be “class mobility”. That is, the percent of the population that moved from the bottom 50% to the next 40% and how that has changed from 1945–1980 (before neoliberalism).

Most, if not all, people in the bottom 50% that own stocks is through their works 401K (which usually is very restrictive). So, as this asset bubble crashes, so does their 401K.

Class mobility is dead, IMO. Student loans, asset bubble crashes and consumer inflation has killed class mobility.

Now, where is the motivation for an uneducated American to become a nurse, a chemist or microbiologist, an accountant, or a school teacher? All you do is go deeper into debt and are “vulnerable” to asset bubbles. The benefits no longer outweigh the liabilities.

I suspect that class mobility isn’t dead, only that the direction in most cases is downward mobility.

Agreed, the juice is frequently no longer worth the squeeze for a lot of jobs. The current state of the USA reminds me of those anecdotes from the late days of the USSR, with scientists working as coal stokers because the economic incentives made it desirable.

I think Americans will be surprised at how quickly the service economy goes to hell with service workers quitting in place or just outright quitting once their jobs no longer pay the bills. We are only at the beginning of this.

I started in the bottom 50%. Working class parents with no assets and lots of liabilities who survive on pensions now. Public education with a negative net worth early aughts due to modest college debt. Went into a trade during GFC and have stayed there. We’re in the middle of the next 40% now. Less than 20k in stocks. Wife has a part time day job works for benefits only, puts the minimum in to get the match in the company plan. The trade through the family business accounts for the rest.

Working your way up the ladder is possible. But if your income is not high you need to avoid living like your neighbors. No car loans, no debt, no overpriced fancy toys, skip the extravagant vacations.

I read an article recently that elaborated on how the millennial generation is the unluckiest in US history, having seen the worst economic growth of any generation since the nation’s inception.

A recent BLS report mentioned that the share of wealth held by the top 1% was approximately 1/3 of the total wealth, with the top 10% holding almost 3/4, and the bottom half holding only 2%.

Another report that I’ve seen shows that the top 1% hold a larger share of the national wealth than the entire middle 60%.

The median income has gone up by only about 14% since 2000 and the average ratio of CEO to worker pay has gone from 20:1 in 1968 to 324:1 in 2021, roughly a 1620% increase. It would appear that the neoliberalism experiment was an abject failure from the majority’s perspective.

Correction: CBO report, not BLS. My mistake.

Michael, the top 0.01% might move to the top 10%. The top 10%

might move lower… while the bottom is moving up, starting

small businesses, acquiring new skills in community colleges or tech schools.

Class mobility has been mostly an illusion in US history, just part of the mythology. Of course there are individual examples but statistically I believe it has been negligible. They great advances have been societal ie advances in technology and General well being that we see in the 1940s-19070. Largely this was distributed among the masses to the degree that the Labor Movement and General upheaval of the masses “convinced” a majority of the ruling class on the need to dish out larger crumbs. With the defeat of both the unions and the social upheaval of the 1960s that has ended and less and less of societal wealth is “shared”

Class mobility into the top .1% is pretty much a pipe dream for almost everyone.

But, moving up from the lower rungs is not the same.

If you think you can, you’re right.

If you think you can’t, you’re right.

I’m not sure if that is actually true. Alot of wealth is created by business owners and I think that business creation and destruction is probably fairly high, given the impact of technology.

I would love to see this broken down according to educational attainment.

To Digger Dave, my favorite preach is the line about not taking on expensive vacations/cars/etc. to be economically mobile in the US.

The ol’ Avocado Toast logic.

Solidly middle class (in the 50%?) nurse. Student loans that ballooned nearly 300% from what was actually taken out. No frills compact SUV car loan because after years of thinking buying used was saving me money, I finally realized used cars in the Northeast come with neat extras like frame rot and costly repair bills, and missed/lost work when the damn thing breaks down which it will and you MUST have a reliable horse under warranty to hack it in the mountainous winter-weathered Burbs.

Expensive vacation? What’s a vacation? Surely you gest. Got to use up paltry sick time and still had to keep working through a bad COVID infection. Home haircuts, thrifted clothing, used furniture are the new Middle Class Fancy. And still one catastrophic medical bill away from ruin because ‘Murica.

All this high falutin’ yet still went and had kids. How dare I propigate the species with a stable income, education, and a loving home to offer.

This article is another great Wolf read, but the comments section is particularly haughty and disassociated from reality.

Lili Von Schtupp,

I mentioned nothing avocado toastish. We do thrift clothes, used furniture and home haircuts too but this just has always been the way in my family.

Comments here can be haughty and preachy but many people here do not fit the typical hyper consumptive American way of living.

I basically said you can move up the wealth ladder if you live below your means. This isn’t “skip the latte every day” advice.

I have a family too. We’re lucky to make 80k combined income a good year. We have childcare expenses but we also made a conscious effort to spend below 30k per year, which crept up to 40k when the kid came along. We had a three year period of maxing out our health plans to the tune of 10k per year out of pocket too. The difference is what we invest and build wealth with.

I live in the hills and we get 50 to 150 inches of snow per year. Know all about rust. I’ve run plow trucks for 15 years. Best thing you can do in these parts is buy used – 2-3 years old is the sweet spot. Any modern vehicle is going to get you 10 years with minimal maintenance if you keep it undercoated yearly with something oily or waxy and wash it off. By 2-3 years very little of the factory rubberized paint will have worn off.

But I will preach on vehicles. I often do on this site. Most people make poor vehicle choices. Despite having to negotiate icy and snowy hills all winter, my and the wife drive FWD wagons with always equipped with the best winter tires you can buy. I’ve passed many a CUV or SUV driven down into snowy ditches.

And I will preach about caring for your own stuff – cars and homes. With YouTube today there’s no excuse not to.

We’re so used to living specialist lives where the lucky make 6 figures for doing mundane things only they can do, somehow we’ve forgotten how to take care of things on our own.

My mother’s family comes from 15+ generations of New England Sawyers, millwrights, carpenters and farmers. My father’s family were farmers and fisherman. My grandmother, who watched me and my brother extensively while our parents worked, and came of age in the Great Depression and taught us great lessons about living modestly without wanting for too much. This Old Yankee ethos is still strong in some parts of New England. My brother grows enough food to feed his whole family and barter the rest for other necessities. We take care of our own needs and then, being fortunate, then help our neighbors and friends with their needs.

There’s always constant blame for the system but very little soul searching for how you can live with it and find a way to prosper. And far too much pathetic begging and pandering via GoFundMe, which has become normalized. There’s nowhere near enough intestinal fortitude these days.

Preach over.

Wolf-

This is a fantastic article and piques my curiosity. I see the calculations are based on the Fed’s data. Where does this data come from as I presume most of the .1% have assets in clandestine trusts etc., offshore, which are virtually untraceable back to the individual without some self-reporting or sleuthing I am sure the Fed doesn’t do. Is the data relying on the Census and IRS returns or payroll data. Where do the numbers come from to evaluate how many and whom make-up the .1%, and the other groupings for that matter.

I am simply curious and emphasize my appreciation for the poignancy of the article and its incredibly powerful impact on the readers both at a gut level regarding “equity/inequity” and as an economic study in QE and QT and the real world effects we are seeing.

Maybe unanswerable questions but worth a shot in asking, if you can satisfy my curiosity of where these numbers come from if people are hiding their wealth. I guess it may be true the wealth divide has been indelibly forged into America through wealth preservation strategies and the only hope is to increase wealth of the bottom 90% by figuring out how to spread some of that top 10% around for the good of the country as a whole–United we Stand, Divided we fall. I am a huge proponent of charity and assisting those who cannot (not WILL NOT) make it on their own-i.e. Children, the disabled, the mentally ill, the newly homeless, wounded veterans, crime victims, terminally ill, and many other’s who if given the opportunity and with some support, contribute in their own way making the Nation a better place. Greed will be humanity’s downfall, as most surely know and that is why we must be charitable to counterbalance the most Greedy, likely the top 10%.

Nathan,

The data comes from the Fed’s vast body of data it gets from its surveys of consumer finance and financial accounts of the US, which produces a huge amount of data on all kinds of stuff. I report on some of it.

The US tax code is such that the wealthy, if they earned their money legally, can shelter their wealth just fine without having to hide a few billions. The tax code is a joke, as you know. The wealthy have no need to hide anything.

Surely there is some hidden wealth. There are people that have gold coins and bars or whatever stacked under their bathtub and things like that. And there are drug dealers, crypto scammers, hackers, and the like, that may hide their illegal incomes and assets.

But illegal economic activity is also not included in GDP or in any of the other economic stats. So that’s the same problem everywhere. We just don’t count illegal stuff in our regular economic data.

There are economists who say that we should include illegal activities and assets in our economic data. But everyone is really squeamish about it. So we don’t.

Wolf said:

“The US tax code is such that the wealthy, if they earned their money legally, can shelter their wealth just fine without having to hide a few billions.”

Exactly!

The real wealth effect for the poorest is evidenced right here from QT.

Is it better to go with average or median figures for each broad category? It’s worth noting the very bottom 15% or so has zero or lower net worth.

I once ran into some official document which partitioned exact household net worth in 1% increments on a yearly(?) basis, but forgotten how it was entitled or who drafted the document.

Median is a lot more representative. The median net worth of all households according to FRED was around $130K a year or two ago.

If median is available for the “next 40%”, it’s going to be a lot lower than $780K, probably something like $250K given the overall median.

Augustus, I agree with you here and my question was arguably rhetorical. I noticed Wolf using average figures for each grouping and it seemed like a mistaken approach, especially since net worth increases are exponential as you work your way up the percentages.

If I could edit my previous post, I would replace ‘exponential’ with ‘non-linear upward curve’.

Now that makes much more sense than 780.

I wonder how the RE owning portion of the bottom 50% compare to the non owners, also wonder if they ended up with the majority of the “wealth gain” for that group in this period. If so it could be a little temporary if the RE bubble continues to unwind over next few years.

Only 17% of the bottom 50% own real estate. I believe this number is down form 26% in 2010. The bottom 50% are getting priced out of real estate. But it makes sense. As every industry becomes a monopoly, the top 10% of the workers in these monopolies will become more wealthy and the front line workers will make less. The mom and pop stores and industries are gone. The big companies keep getting bigger. Just look around, the top 3 companies in each industry probably commands 90% of the markets.

Auto Parts: Autozone, O Reily, Advanced Auto

Home improvement: Home Depot, Lowes

Retail: Amazon, Walmart, Target

etc…etc…

A really sobering report, Wolf. Thank you for taking the time to expose what a sickeningly disturbed entity the FED is, and the damage they have done to the USA.

Superb article Wolf. Thank you

Agreed! Thanks, Wolf. I wish TV talking heads reported on this so the public could see the real outcome of the Fed’s work.

The Fed is only a sympton of the disease. The real illness exists in the legislators at every level in this nation, and it’s a very old sickness (or maybe “suckness”). Willy nilly wild west economics just gets you a peashoot between cattlemen and sheepherders, until the bulldozers arrive and throw up crap shacks everywhere. Who wins? Always the moneymen that take control of the lands that came from the public’s resource base. It’s always the land…how you use it, who kontrols it.

Agree with you, like ‘totally’ dude or dudette!!!

Dirt is where it’s at, always has been and always will be…

That’s why the rich folks, newbies or old money, always use what money becomes ”cheep cheep cheap” to buy land as is now clearly confirmed by even the gate guy, eh

In the distant past, before the FRB was started to STOP WE the PEEDONs from buying land when the poop hit the paddle,,, with our gold buried in the jars in the yard when times were good and gold flowed like water, WE PEONs had at least a fairly good chance to turn our work making real stuff into long term family wealth, and many did, especially the many who came to USA to get away from draconian policies and practices in the old world that kept ALL the wealth in the hands of the oligarchy of those times– and continue…

There WAS a very good reason everyone who could wanted to come to USA in the past and NOW,,, that reason was at least hugely mitigated by the establishment of the FRB, and continues to be degraded by current (last few decades) policies of FRB and those politicians buying votes by giving away the SAVINGS of the thrifty, etc…

MANY constitutional amendments are needed to ”RIGHT the SHIP” of USA,,, and ASAP…

Great article. I did not know that the next 40% had so few stocks and mutual funds.

There is a wide range in all of these segments.

The “next 40%” are presumably usually those most would consider the “middle class”/

Measuring financial condition is a lot more complicated than this. It’s a combination of wealth, income, household size, geographic location, and lifestyle.

Considering all five but only using wealth data, I’d classify those in the 81st to 90th percentile as middle class. Many of these people have assets but being retired, are lower in the income scale.

Those in the 51st to 80th percentiles, some unknown proportion I’d classify as middle class, but mostly working class and working poor. A lot of these people live in expensive cities.

People with the top 1% of net worth in the U.S. in 2022 had $10,815,000 in net worth.

The top 2% had a net worth of $2,472,000.

The top 5% had $1,030,000.

The top 10% had $854,900.

The top 50% had $522,210.

Ain’t That America…..You and Me

1) The Fed want to kill gov debt.

2) When inflation was 6% last year and above 8% this year, it’s likely to be above 10%, and last on average a decade, with 60% range between 6Y and 19Y, before falling to 3%. If so :

3) The bond market might suffer.

4) Real estate, in real terms, might deflate.

5) Consumers durable goods might deflate.

6) Pension entitlement might deflate.

7) Real wages might deflate.

8) Consumers debt might rise.

9) The real value of businesses, stocks, and other assets, ex cash, might rise.

10) Cash is king if u know when/ how to apply it.

11) Buybacks and executive perks might deflate. Dividends might rise.

We ‘might’ be getting somewhere!

Come on purple line…

Great piece of research!

A side note: Just received the letter from SS regarding the 8.7% increas in benefits-nice little bump up. Hope to live beyond 77 so it goes beyond the amount that I put in over the years.

Much of the wealth increase for the poor must be due to steadilly increasing social services benefits, not trickle down. The trickle down is analagous to older men with deteriorating prostates,, and its embarrassing effect.

The Canada pension plan sees a 6.5 percent increase this January.

Implicit wrote: “A side note: Just received the letter from SS regarding the 8.7% increas in benefits-nice little bump up. Hope to live beyond 77 so it goes beyond the amount that I put in over the years…”

Congrats on finally getting that letter. Most of the people here at the retirement complex have not gotten theirs. Calls to S..S and they all say printed Nov. 24th.

Checking with USPS, I get chuckles: “Yeah, it may have been printed in November, but it has not gotten to USPS yet, and is probably still sitting in the warehouse at the printer.”

It is weird.

Both my wife and I each get Social Security. She kept her maiden name while working professionally so her SS is HER money.

I did get my increased benefit letter. She has not yet received her letter.

What is really weird is that her maiden last name and my last name begin with the same initial two letters. And we both get our SS ‘benefits’ dumped into our joint checking account the same day of each month.

Stuff from SS goes by your SS #, not your name anon…

Sister and I who got our SS # at similar dates get our REPAYMENTS from our 60+ year contributions on the same 3rd Wednesday.

I am still not anywhere near even with what those payments would have ”earned” in the private mkts according to a friend who knows a lot more about that kind of thing…

I have looked this up BTW,,,

You can get that info on the SS website.

………”The trickle down is analagous to older men with deteriorating prostates,, and its embarrassing effect.”

Implicit, there is a pill for that.

Yup, I know some of the old gang take that pill.

I don’t trust the pharma chemicals too much, and try to take natural remedies.

However, for that problem, I just shake it a couple of more times. I need the exercise.

And the difference between “natural remedy” chemicals and “Pharma” chemicals IS??????

People are trained to love pissing money away on pills and special goo, and then love to argue about this shit that they are TOTALLY IGNORANT of!

Anything is better than a good peasant diet and good peasant exercise?

It will only be included to the extent it is saved.

I’ve never seen the present value of SS benefits included in net worth data. It’s “transcendental capital” which only lasts while you are alive.

Should be the same for defined pension benefits, except to the extent the beneficiary has an ongoing residual interest.

Let them eat cake

A substantial portion of the purported value of assets is a mirage. In the next wave of financial distress – when real asset prices can no longer be hidden from view because QE stopped working – the liabilities are set to grow exponentially as a percentage of the asset base.

In a frenzy to avert their own demise, banks will demand collateral to make them whole. Government claims on a shrinking asset base might also be reflected upon. Let the fire sales commence.

The “Wealth Evisceration Effect” is on its way. By definition, it’s official Fed policy. Along with government, they own it.

(If I read it correctly and for understandable reasons, liabilities associated with Stocks, Mutual Funds, Pension entitlements and Private Business have not been included).

With mortgages packaged into mortgage backed securities, MBS, the banks may no longer have to demand collateral to make them whole.

Wolf could maybe run an article on how this work. Are the money lent by the bank stil a liability to the bank when the debt is sold of as MBS?

Sams

My point was broader than MBS.

Wolf has covered MBS quite a few times. His best work IMO.

Still the question is what liabilities do the banks really have.

How much of the issued debt is on the banks books and not sold of as some sort of securities?

And to what extent is the bank on the hook for those securities?

To me it look like there have been changes to the monetary system where debt is no longer tied to a bank and a fractional reserve as debt is now securitised, sold and filed as a financial instrument.

Banks both securitize their own debt and own the securitized debt of other banks. Maybe their own securitized debt too.

This includes MBS. Bank of America purportedly has a $100B unrealized loss on MBS which they claim to intend to hold to maturity and therefore under current accounting rules, don’t have to record it.

12) The value of family and community will rise.

And isn’t it funny that our current social structure seems to minimize both or outright try to destroy them?

A little off topic…

I was just notified by the CPA that does my taxes this year will cost me about 3 times as much as last year.

So services inflation must be at 200%.

I’m tempted to do them myself.

Tip: prepare it in some software, which charges only for filing to the IRS, but do not proceed with filing. File online yourself on the IRS site.

Alku –

How does that work? How does a person file “directly” with the IRS?

Last time I checked, the IRS does not allow online filing, directly with the IRS. Instead, the IRS refers people to the software companies.

Namaste.

Daisy,

The IRS encourages free filing on its website. The tax filing companies spread a lot of BS about that.

So try this:

https://www.irs.gov/filing/free-file-do-your-federal-taxes-for-free

It says, quoted from the IRS page:

How IRS Free File Offers Work

1. You must begin your filing option at IRS.gov. Going directly to a company’s website will result in not receiving the benefits offered here.

2. Choose an IRS Free File option, guided tax preparation or Free File Fillable Forms.

3. You will be directed to the IRS partner’s website to create a new account or if you are a previous user, log in to an existing account.

4. Prepare and e-file your federal tax return.

5. Receive an email when the IRS has accepted your return.

IRS Free File Program offers the most commonly filed forms and schedules for taxpayers.

thank you once again Wolf,,,

Daisy: been filing my own taxes since a really wonderful woman actually showed me what she did when she figured my very convoluted taxes in 1984.

Been ”audited” by IRS two times since, and after the first audit they sent me a check after many months of threatening to ”garnish” my bank account. Second time they just said ”go away.”

Anyone willing to read thoroughly, i.e. STUDY the IRS regulations will very likely be able to do their own tax returns IMHO…

They are NOT ”rocket science,” in spite of what many folks claim.

Vintage, it all depends on your tax situation. Some are quite complex. If you just receive W2 income, taxes are very simple.

Thanks Wolf.

As my comment, and the IRS website you reference states, this program relies on private companies, to offer their software free, to some users.

It is a “public-private partnership.”

Taxpayers cannot electronically file with the IRS. They need to file through a private company, that in turn, transmits the return.

A big government giveaway to private companies.

====

What Is IRS Free File?

The IRS Free File Program is a public-private partnership between the IRS and many tax preparation and filing software industry companies who provide their online tax preparation and filing for free.

https://www.irs.gov/filing/free-file-do-your-federal-taxes-for-free

a big government giveaway, because for most people with normal jobs, the government should be able to send them a form with the information pre-filled, that the person can either agree to, or not. $0 and Zero hours, for normal people.

that is my understanding in the uk. though i haven’t studied it.

Daisy,

look up “irs e-file” and “Fillable Forms” if your AGI exceeds $73K. There is an even better option if you make less.

I’ve done this last several years and the experience is very positive. The only downside their error reporting is done in not the clearest way possible, but it’s manageable. And refund comes fast.

Vintage,

I’ve also been audited twice. Like you, they had to cut me a check one of the times because I had overpaid, and the second time they agreed I had paid correctly. I got a kick out of the whole experience.

Alku, I am sorry for the confusion. I understand that the IRS finally forced some companies to offer their software for free filing, for some people.

When you write you use the private company software for free to prepare your taxes, and then somehow don’t use the private company to file, but instead file ELECTRONICALLY directly with the IRS, that is what confuses me.

Because the “free software” also allows users to file, for free, if they qualify, for free filing.

I am not aware of any option for Americans to directly, electronically, file their taxes, through IRS software or website. My understanding, is the only way to file federal returns electronically, is through private company software. Some of which is, yes, provided, for free.

====

“Tip: prepare it in some software, which charges only for filing to the IRS, but do not proceed with filing. File online yourself on the IRS site.”

Daisy –

sorry for confusion. What I was trying to say was that you use a commercial software to enter all data and have it prepare everything for filing. Then at the review phase you just screenshot all needed info and fill in the corresponding fields of the 1040 in IRS e-file system.

It is a line item in the Inflation Reduction Act for the IRS to develop the infrastructure to offer in-house free file.

Anyone regardless of income, can use the free fillable forms option and file electronically. Anyone can sign up for an EFTPS account and make electronic payments to the IRS.

I did the free fillable forms for many years but went to a tax precessional a few years ago because of the constant nonsensical tinkering with the tax code made it do I had to invest too much time in learning the changes every year.

They are not for the faint of heart. There are no programs asking you taxes-for-dummies questions while doing all the magic for you.

Your literally filling in blanks on tax forms. You have to be able work through various IRS worksheets, know which credits and deductions apply to your situation and hope you cover all your bases without screwing yourself over too badly. When you’re self employed and own rental estate and depreciable business property, it gets old real fast.

I’ve been doing my own for many years now. Once you learn how to do them it’s a piece of cake thereafter. I have Excell spreadsheets 3 deep on my desktop PC. Every year I just assemble deductions and plug the numbers in, and boom!. Out come the numbers. Never suffered a serious audit. Small mathematical errors are usually caught by the IRS with no penalty.

Wolf, this article made MarketWatch. Might drive a lot of traffic and new folks commenting. Thanks for writing it.

It must be completely factual then. Very impressive!

MarketWatch used to link my article in its article when it cited “says Wolf Richter at Wolf Street.” But now, they just link it at the bottom, where few people click on it (73 so far, LOL). But I’m glad they’re giving this topic front-page exposure to a readership that doesn’t necessarily read Wolf Street.

Showing all traces as percent change would let them reside on the same axis meaningfully, and would also correspond with “sensed comparative income”. All human senses are ratio or log.

That’s the kind of BS that folks have used forever to justify the “Wealth Effect” and thereby purposefully increasing the wealth disparity. So do some math:

A homeless person has $5 in his pocket. I give him $5, and now he has $10. His wealth increased by 100%.

A billionaire has $1 billion in wealth. The wealth effect via inflated asset prices increases his wealth by only 10%.

So who got a better deal? The homeless guy whose wealth increased by 100%, or the billionaire whose wealth increased by only 10%?

And what happened to the wealth disparity between the two? It widened by nearly $100 million.

The problem with percentages is the BASE. If the base is low, even a big percentage increase adds nearly nothing to it.

People who are using the percent-increase logic to cover up the real problem are a big part of the real problem.

This article is good but applicable to the citizens of USA. I have been in China several times and have seen that most of the Chinese live more happily though their income / wealth is not that great but by Purchasing Power Parity, they enjoy a better life than Americans / Europeans.

Suggest you might want to read some of the current literature coming out of China these days…

Not so good relative to other areas, even though clearly majorly better, much much better than before, including especially when China went through various and sundry ”cleansings”

Have done biz with many Chinese folks here in USA, mostly in SF bay area, who were good to work with, and have told me many stories going back to their parents experiences.

They are forced to be happy in China. Complain or protest and you end up in camps with the Uyghurs.

Or worse, the dreaded “involuntary organ donor.”

The reports starting with the fourth quarter will show falling house prices, too, with broad effects on these net worth calculations.

Alex,

Yes, the wealth of the bottom 50% might decline by $10,000 due a 10% house price decline on average, and they don’t care if they just keep making their mortgage payments. The top 0.1% would then see a $1 million decline, decreasing the wealth disparity by another $1 million.

In addition, those in the bottom 50% who don’t yet own a home – and many don’t – can then buy one for less. This means that their labor gained in purchasing power with regards to houses, after losing purchasing power for 12 years. That’s a GREAT thing for them and for the overall economy long-term too.

Very good point on the changing ratio between the purchasing power of labor and the bloated price of houses, which will improve as house prices fall.

1) Normal inflation : up to 10%. Moderate inflation : between 10% and 20%. High inflation : 20% to 80%. Hyper : 80% and above.

2) Since 1013, when the Fed was born, the average inflation was 7%.

3) Since 1913 the dollar lost 97% of it’s value. The inflation accumulation was 2600%. The worse bouts of inflation were in the first 50Y, between 1913 and the 1960’s. In 1967 Egypt closed the Suez canal along with Vietnam and social entitlements.

4) Since the 1982 inflation stayed mute below 7% until this year.

5) Gold was dragged down by the two decades of oil glut. It was up since 2001 when the dollar plunged from 121 until the dollar exited nadir.

6) If u draw the 100y inflation chart there is a downtrend resistance line coming from May 1920 to Mar 1947 to Feb 1980 highs. June 2022 high was an upthrust. Dec 2022 fell below this resistance line, above the 7%.

In the last 100y the inflation boundary was between zero and 7%.

This is all great on paper, the rich are not worth as much as they used to be. In reality though, the top .1 percent still are not going to need to change their lifestyles, while the rest are struggling to survive.

Breaks your leg, but then hands you a crutch and brags about it.

Well said. The way American Governmental policies have treated the downtrodden with over a century of neglect or outright oppression, resulting in what our Government has created and now calls “the needy”, which some complaint about subsidizing. Its past time for all of us to get out there and help ones fellow human being in need and no strings attached. When we need help, it will be there–maybe not from the Government, but they serve an incredible vital safety net for the most needy and we should praise the funding of those programs.

1) The poorest people are rising against their gov risking their lives.

2) Their most important assets are their family. They are home makers, committed to each other, but due to the high inflation they cannot

support their families.

3) They work hard, hoping that their children will do better, living in a

structure, in discipline, among peers.

4) The unemployed are x10 times more depressed than people who are

doing dead end jobs.

5) Their assets are excluded from Wolf charts. The GDP measure

assets growth. Econ101 don’t recognize their real assets : being

productive, family and community.

Get rid of the celebrity and wealth culture worldwide, found in both rich and poor communities. Imagine people no longer fighting over collectible shoes and sports cars.

I wanna be an ‘influencer’!

You mean getting right with Jesus?

Mr House,

whatever works for you.

as an atheist / agnostic, i don’t need to be given a set of values, for my moral framework.

Daisy, I read Mr. House’s comment as sarcasm. I read it now a second time, and that’s my story and I’m sticking to it.

Is that Dr. House? No wonder the deadpan sarcasm. He didnt mean any harm Daisy.

The data points to who does the rich sell their stocks to? Even the 9 to 5ers know the U.S. stock market is all smoke and mirrors and should have fallen over the last decade. Who will be the bag holders this time around?

My net worth went way up in 2022. I’d probably be in the one percentile for net worth. I have relatives in the .001 percentile. I sold the last of my homes last year and had a big short on Facebook/Meta and Shopify. Through pure luck I covered a short on Home Capital before a buyout bid was launched September 21st this year. Rising interest rates pushed my income higher on rising daily interest rates.

Do you know anyone that sends their kids to public school?

Would be comforting to know that some globalists, send their kids to public school. Thank you.

Technically yes. But they moved to specific neighborhoods for the school system. So even though it’s a public school district, it’s still mostly full of rich kids.

Thanks.

Yes, where I grew up, the only private schools are religious.

But people do choose their districts.

I do think it would be wonderful if the people promoting equity, lived their values.

Get ready to open up that check book. Uncle Sam could sure use a little more TAX money. Good call on Facebook and Shopify!

Great article, Wolf. Possible error: under The Next 40%, unlike the other categories, the same figure, $911,200, is listed for both total assets and real estate assets. One of them is probably incorrect.

Thanks. It’s $911K in total assets and $336K in real estate.

Based upon the USA Gini coefficient, since 1990, wealth inequality has increased from .43 to .49 in 2022.

The U.S. easily wins the G-7 with the highest Gini coefficient.

This was not always so.

Other rich countries like Denmark, France, and the Netherlands had populations with a similar distribution to the U.S. 100 years ago. See the chart of “Within-country Inequality” in this link:

https://ourworldindata.org/income-inequality

Whoops, sorry Finster, I now see you already pointed this out.

Wolf, you can delete my comment.

Wolf,

It seems like all “The Big Money” wealth “advisors” are wetting themselves because The Fed is raising the cost of money. Every single one of them is crying that NOW interest rates are too high.

I guess their customers can get a much better rate of return – risk adjusted – with fixed money assets so are no longer dumping their High Net Worth on those poor advisors.

Yes, thanks.

Good article. Thanks WolfR.

We sold our sfr principal home in June 2022.

Net worth has increased by better usage of funds through the acquisition of Gold, Silver and Shorting.

Still planted somewhere in the middle but very happy to be healthy and still kicking 😉🥳

You moved into a rental?

Yes. SFR was sold at the 98% for the zip code. Monthly expense has been reduced $1K+.Expenses going forward were going to be a never ending upward spiral due to Developer / Consultant control of the City. Perfect time to have said Thank You and move on.

The US is headed for a South American solution, such as Rio. The bottom 50% will subsist in favalas, while living cheek-by-jowl with the people that count, who will live in maximum security compounds.

Policeman will be granted open season on the ghetto dwellers, id est, many of we readers of WSR.

You are talking about Brasila under Bolsonaro. Lula is a friend of the Favellas as they put him in office and have vast powers in sheer numbers. Yes, like Rio, America seems like it was destined to becoming a country of Gated Communities and the “have nots”–but our Constitution and legal system will prosecute those who violate Civil Rights laws, especially the cops.

At least some of the favelas have an ocean view, so there’s that.

I disagree that Fed tightening has done anything to lessen wealth disparity.

That is simply a perception based on the fact, like you said, you cannot measure the impact on lower incomes because they had nothing to begin with. That does not mean their living standards are not being drastically impacted, and in their case, when you have no tangible wealth, how well you are living is all you have to measure you “wealth”.

As economic recession continues, the people at the top of the pyramid will benefit from economic recession as much or more than they did from the bubble as they will be able to purchase assets at bargain prices as the lower classes are forced into selling those assets into declining markets to survive. In boom times the rich sheer the sheep, but in bad times the kill them and eat them.

Jdog,

Those is the top .1 of 1% may have been by surprised by the sudden Fed tightening. and suffered a temporary setback. But now that they see the picture going forward they will move their investments to those that will insulate them from the tightening. Look for large inflows into short term Tax exempt Bonds and Bond funds. Those in the bottom 50% will have no such luxury. They are not only getting clobbered by the inflation and fixed expenses but have no capitol to move to shelters. They have nowhere to run and nowhere to hide. Every dime they make from working slave jobs will be taxed to the full extent of the law.

In the multi-decade bear market that is in store, the majority of both the 1% and .01% are going to have their head handed to them.

I get your point, but these people didn’t get rich by stuffing their money under the mattress and will mostly lose big, proportionately.

There were 735 US billionaires in 2020 or 2021 according to Forbes and about 20,000 worth over $100MM in North America (most in the US) according to the Ultra-Wealth Report.

Back in 1982 or 1983, there were 13 Billionaires. Inflation doesn’t account for this change and neither does the actual productive capacity of the country.

It’s the asset mania and the end will mean most everyone, including most of these people, lose big.

There aren’t 735 much less tens of thousands with the political influence to buy their way out of the upcoming asset collapse.

Jdog – Good points. Look at the charts. Top wealth people surpassed their peak 2009 wealth by 2012 as they began buying assets on the cheap. Meanwhile, it was not until 2020 did the the top 10% to 50% surpassed their 2009 wealth.

I meant bottom 50% did not surpass their previous peak wealth. The top 10% to 50% was in 2014, a couple of years after the top 10%.

Those who did not invest in the stock market or housing missed out.

The suppression of interest rates (decline in real rates of interest) boosts relative asset prices (“everything bubble”).

BOE: “QE initially increases the amount of bank deposits (outside money), those bank-holding companies own (in place of the assets they sell). Those companies will then wish to rebalance their portfolios of assets by buying higher-yielding assets, raising the price of those assets and stimulating spending in the economy.”

I learned in simple economic terms that the rich and extremely wealthy get the low interest loans first to buy up assets before they become bubbles and inflation takes hold in the economy.

By the time the media praises billionaires shilling for dog coins, you know that it’s the middle class and poor who will be the bag holders.

When crypto was at its infancy, the banks and credit card companies would close accounts for suspicious activity.

Now anyone can buy crypto at these inflated prices via apps, but to make a profit, the app will freeze your account still and ask you why are you using crypto for day trading.

The rich win in any case.

All these people whining about children. I have seven children and eight grandchildren with many more on the way I hope. All of my children are far wealthier than I am although I want for nothing. My children and grandchildren are the joy of my life.

Esc…

I agree about the joy in life of the blessing of children and grandchildren. A mark of good parenting is that the children are more successful than their parents. Sounds like you qualify.

I am puzzled about the pension component of the “bottom 50%”. I know several people from the 2008 debacle who lost upwards of $40,000 from their 401K pensions invested in the stock market. I see many online weeping about 401K pension losses now. The term “wiped out” is ubiquitous. Is this the ephemeral gains, or have they lost their own contributions? I suspect this is a stupid question, asking it anyway.

“I learned in simple economic terms that the rich and extremely wealthy get the low interest loans first to buy up assets before they become bubbles ”

and this is why many countries put limits on global corporate and foreign ownership of their housing stock. If they did not then 50% or more of their population would go un-housed as speculators bought everything up..

We instead rely on FED cyclical manipulations which can be drastic.

It’s too bad out politicians are heavily invested in RE and cannot for the life of them make uncompromised decisions.

I meant to reply to Gen Z

cyclical manipulations which can be drastic

and don’t work very well..

Easy fix is to start taxing these properties as commercial properties. Will see just how fast they start to offload there portfolios.

The majority of Canadian politicians own real estate or have investments in rental income properties.

It’s terrible for the citizens who pay taxes to make the politicians and speculators richer through rent seeking.

Front running after jumping Consumer confidence to it’s highest level since April. Hence almost 530 points jump in DJIA.

I wonder what else, Mkt ready to spring on the next whisper of any positive news!? Wonder how many are snarled into these furious Bear rallies! Roller coaster ride continues.

Nah. The DOW would have dropped 1,000 points if anyone had paid attention to the consumer confidence number because it means higher rates for longer. These markets don’t pay attention to anything. It was just a low-volume pre-Christmas move, when the sellers had gone skiing.

Wealth Disparity in USA; OK, how about Saudi Arabia, Qatar, Japan, Switzerland, Germany, China, Russia, et al. (good luck finding some of those numbers)…and what % of taxes are paid by each sector…and where do the senior members of Congress sit?

Wealth Disparity is an interesting (perhaps perverse) reality, I think it needs some contextual comparisons.

This was about the impact of the Fed’s monetary policies on Wealth Disparity in the US. I don’t give one iota about Wealth Disparity in Saudi Arabia or Germany or whatever. If that’s what you want to read about, go somewhere else.

It’s humbling to think 1 out of a hundred households, less the top .1%, have an average net worth of $19.3 Million. That’s a lot of households at a high number.

There is a lot of wealth and money out there.

cb

Good observation. 1 out of every 100 is a lot of households !! Makes me even more depressed about how I have apparently missed the gravy train !!

I’m having a hard time with that number. There must be concentrations of populations with that much wealth somewhere else, because the 1% where I live don’t have nearly that much. I can think of one family that might come close. Even though I know it’s the average and not the majority of that segment. Might be true in some neighborhoods of SF and NYC.

Lynn – your ‘neighborhood’ comment is apt. ‘…financially, leaving California is usually a one-way trip…’ has been heard here since the ’80’s…(always exceptions, I’m one…).

may we all find a better day.

Chinese proverb

” No one who rises before Dawn 360 days a year fails to make his family rich”.

And yes. I’ve done it for almost two decades. And no, I wasn’t born into it to begin with, I was raised below the poverty line on what little farm my parents had left after they went bankrupt in the early 80’s.

Yep, how did we get here indeed, perfect:

“Into the blue again…after the money’s gone…”

It’s all an illusion work your life away for dream that never comes true. The dangling carrot.

Real interest rates are far more negative now than they were five years ago, and that could be the reason why wealth inequality goes down.

After all, the rich accumulate their wealth via interest. And wages rise even though they do not keep up with inflation.

Asset prices rose due to discounting insofar as they are related to low interest rates. They were future gains brought to the present.

“After all, the rich accumulate their wealth via interest.”

Misconception here. The wealthy accumulate wealth through asset price increases: real estate, stocks, private companies, sale of private company to the public, etc. You cannot get wealthy by earning interest. But you can protect your wealth that way.