Inflation in many services is red-hot. Health insurance CPI pushed down again by record mega-adjustment.

By Wolf Richter for WOLF STREET.

Are these finally signs that inflation is starting to react to the Fed’s rate hikes and QT, or are we seeing just another head fake? Inflation has a long history of dishing out head fakes, and just when you thought that it would abate, it jumps all over again. This is visible in the long-term charts below.

Prices of some durable goods have been falling for months and they did so again in November. Energy prices plunged. But food prices jumped up and down from item to item; for example, they backed off for meats but spiked for eggs, fresh fruits, vegetables, coffee, and booze.

And then there are services. That’s where nearly two-thirds of consumer spending goes, and many services prices are surging, but under ongoing record-massive mega-downward adjustment to the way the CPI for health insurance is estimated, the whole medical care services CPI dropped.

But this adjustment doesn’t take place in the Fed’s preferred inflation measure, the core PCE. And “core services” – an item Powell specifically pointed out – picked up inflation momentum, and we’re seeing some of that in the CPI as well.

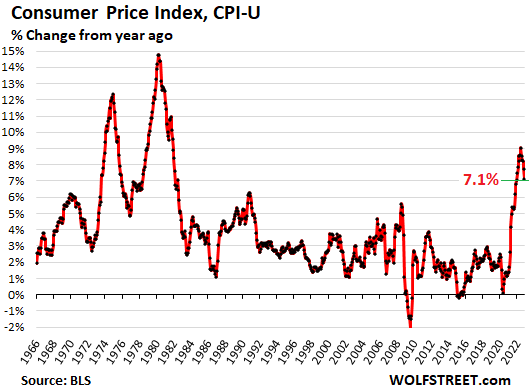

Overall CPI.

Pushed down by plunging energy costs, the all-items CPI rose only 0.1% in November from October, and was up 7.1% year-over-year, a further deceleration, according to the Bureau of Labor Statistics today.

Spot the head fakes that CPI dished up throughout history. The Fed has been warning about these kinds of head fakes for months because that’s what caused a lot of problems back in the 1970s and early 1980s when the Fed undid some of its tightening, fooled by inflation head fakes, only to see inflation spike again, and then having to tighten a lot further:

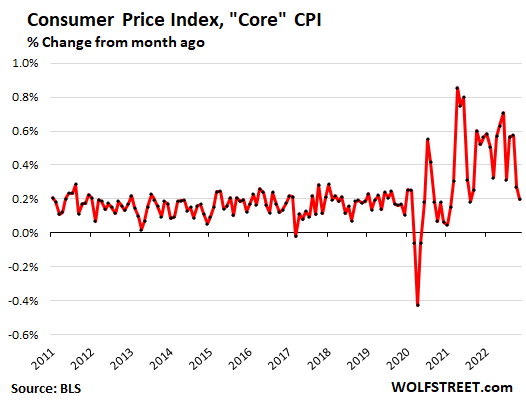

“Core CPI.”

The core CPI, which excludes the volatile food and energy products, rose 0.2% for the month, thanks in part to the massive health insurance adjustment. Here too, there have been lots of head fakes over the past two years:

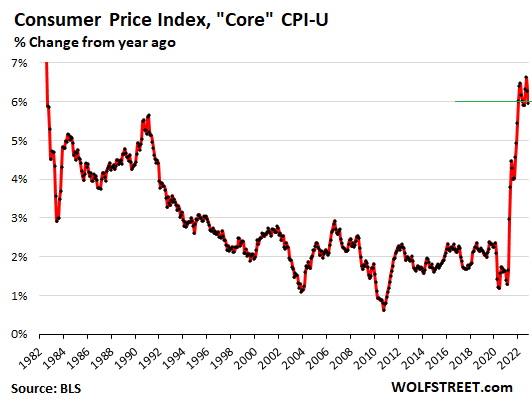

Year-over-year, core CPI jumped 6.0%, and has been just above or just below 6% for the 11th month in a row:

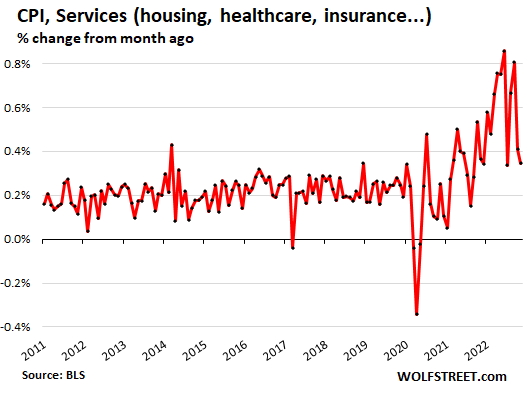

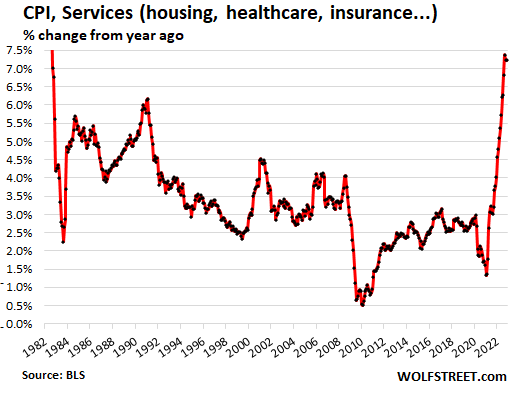

Services Inflation.

The CPI for services –where the massive mega-downward adjustment of health insurance is distorting the numbers – rose by 0.35% for the month, the smallest increase since July. And we learned in August and September that July had been just another head fake:

On a year-over-year basis, the services CPI jumped by 7.2%, same as in October. The last three months, all above 7%, were the worst since August 1982. Without the health insurance adjustment – which we’ll get to in a moment – the year-over-year spike may have set a new four-decade record.

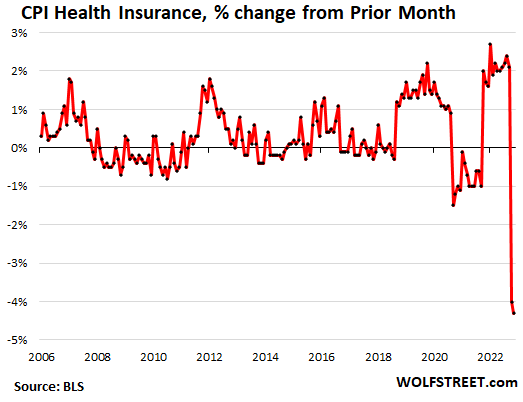

The health insurance adjustment.

The BLS undertakes a periodic adjustment in how it estimates the costs of health insurance. November was the second month of 12 months of adjustments (I’ve discussed this in greater detail here).

Due to this massive mega-adjustment, the CPI for health insurance plunged 4.3% in November from October, after having plunged by 4.0% in October from September. This was by far the biggest month-to-month plunge in the BLS data going back to 2005.

These two months in a row of mega-adjustments reduced the year-over-year rate of the CPI for health insurance from 28% in September to 13.5% in November. These adjustments have occurred before, but never at this magnitude.

What this adjustment means is that health insurance CPI was overstated for the 12 months through September, and is now being understated, and will be understated for 10 more months, to rectify the overstatement:

But no adjustment for the Fed’s favored “core PCE” index, released by the Bureau of Economic Analysis, which uses a different and broader methodology than the BLS, and figures health insurance inflation differently.

Services CPI by category.

The table shows the major services CPI categories in order of the month-to-month change. Many of the very common services had big month-to-month increases.

Note the Medical Services CPI at the bottom, part of which is the massively mega-adjusted health insurance CPI (both in bold).

| Services | MoM | YoY |

| Overall services | 0.3% | 7.2% |

| Telephone services | 2.1% | 1.5% |

| Motor vehicle maintenance & repair | 1.3% | 11.7% |

| Recreational services, admission to movies, concerts, sports events | 1.1% | 4.4% |

| Motor vehicle insurance | 0.9% | 13.4% |

| Video and audio services, cable | 0.9% | 4.2% |

| Rent of primary residence | 0.8% | 7.9% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 0.8% | 6.5% |

| Owner’s equivalent of rent | 0.7% | 7.1% |

| Pet services, including veterinary | 0.7% | 10.9% |

| Water, sewer, trash collection services | 0.3% | 5.0% |

| Postage & delivery services | 0.2% | 4.2% |

| Hotels & motels | -0.9% | 3.3% |

| Car and truck rental | -2.4% | -6.0% |

| Airline fares | -3.0% | 36.0% |

| Medical care services | -0.7% | 4.4% |

| Includes: Health insurance | -4.3% | 13.5% |

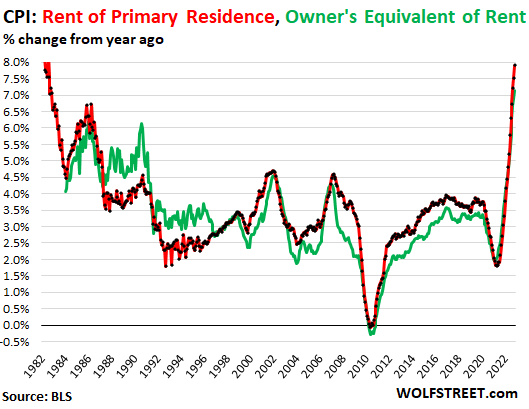

The CPIs for housing costs spike.

The CPI for “rent of shelter” accounts for 32.3% of total CPI. It tracks housing costs as a service, not as an investment asset, and is based on rents:

“Rent of primary residence” (accounts for 7.4% of total CPI) spiked by 0.8% for the month and by 7.9% year-over-year, the highest since 1982 (red in the chart below). It tracks actual rents paid by a large panel of tenants, including in rent-controlled apartments.

Other rent indices, including Zillow’s rent index, are based on “asking rents,” which are the advertised rents that landlords want to charge future tenants. A landlord may lower the asking rent if potential tenants are not biting.

“Owner’s equivalent rent of residences” (accounts for 24.0% of total CPI) jumped by 0.7% for the month and by 7.1% year-over-year (green line). It tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

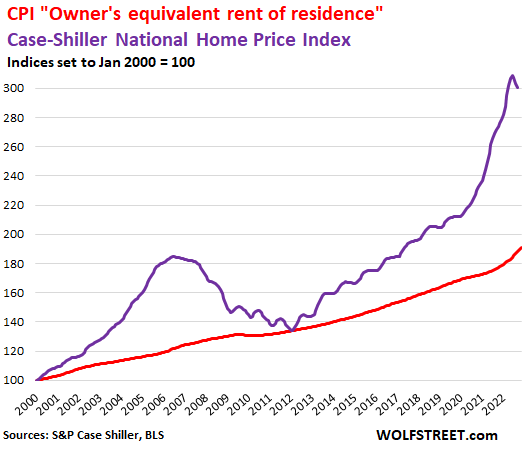

Home prices have started heading south on a month-to-month basis, according to the most recent Case-Shiller Home Price Index (purple line in the chart below), which I track market by market with my series, The Most Splendid Housing Bubbles in America.

The red line represents “owner’s equivalent rent of residence.” Both lines are index values, not percent-changes of index values:

Food inflation.

The CPI for “food at home” – food bought at stores and markets – jumped by 0.5% for the month and 10.6% year-over-year. Some prices that had spiked earlier this year fell, but other prices spiked, continuing the game of inflation Whac-A-Mole:

| Food inflation | MoM | YoY |

| Overall Food at home | 0.5% | 12.0% |

| Cereals and cereal products | 0.6% | 16.6% |

| Beef and veal | -0.8% | -5.2% |

| Pork | -0.3% | 1.2% |

| Poultry | -0.8% | 13.1% |

| Fish and seafood | -0.1% | 6.5% |

| Eggs | 2.3% | 49.1% |

| Dairy and related products | 1.0% | 16.4% |

| Fresh fruits | 2.3% | 6.6% |

| Fresh vegetables | 1.2% | 9.6% |

| Juices and nonalcoholic drinks | 0.5% | 12.9% |

| Coffee | 0.5% | 14.6% |

| Fats and oils | 0.0% | 21.8% |

| Baby food | 0.3% | 10.9% |

| Alcoholic beverages at home | 0.8% | 4.5% |

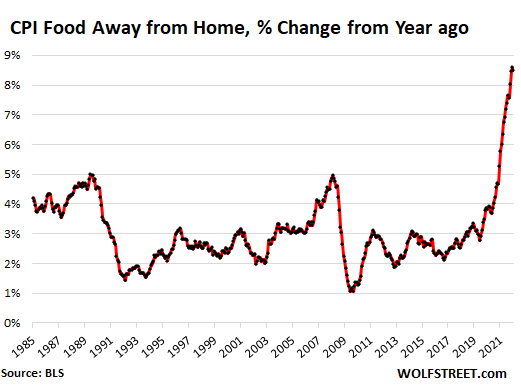

The CPI for “Food away from home”– restaurants, vending machines, cafeterias, sandwich shops, etc. – jumped by 0.5% for the month and by 8.5% year-over-year. Over the past three months, the year-over-year measure has been at around 8.5%, the worst since 1981.

Energy prices plunged for the month, still up big from year ago:

| Energy | MoM | YoY |

| Overall Energy CPI | -1.6% | 13.1% |

| Gasoline | -2.0% | 10.1% |

| Utility natural gas to home | -3.5% | 15.5% |

| Electricity service | -0.2% | 13.7% |

| Heating oil, propane, kerosene, firewood | -0.4% | 41.7% |

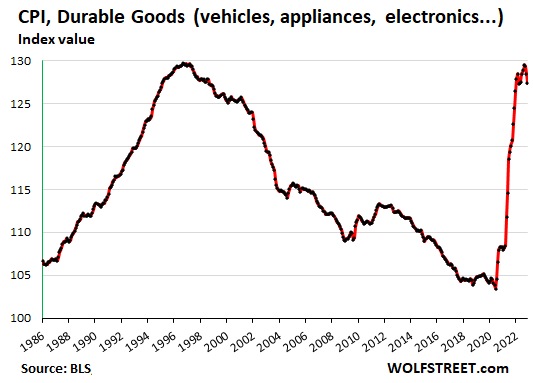

Durable goods CPI.

The CPI for durable goods fell for the third month in a row, after the ridiculous spikes last year and earlier this year. This whittled down the year-over-year gain to just 2.4%, down from the 18% range earlier this year. Here are some key categories. New vehicle prices are still increasing month to month, though a less red-hot pace:

| Durable goods | MoM | YoY |

| Used vehicles | -2.4% | 2.0% |

| Information technology (computers, smartphones, etc.) | -1.0% | -10.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.8% | 7.6% |

| New vehicles | 0.4% | 8.4% |

| Sporting goods (bicycles, equipment, etc.) | 1.6% | 3.0% |

The CPI for durable goods, expressed as index value, not as percent-change of the index value, shows just how crazy the situation had gotten and that prices are just dipping a little from the ridiculous spike. The largest categories in this index are new vehicles and used vehicles:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Prices… spiked for eggs, fresh fruits, vegetables, coffee, and booze”

Well crumbs, that’s about all I buy nowadays.

I have stopped drinking…

Where’s your priorities?

doing large job and bought lunch(subway) for 3 workers

$35 for LUNCH I picked up

I’m working for less on this job since we now do profit sharing

1 hour to pay for lunch

3 days work and $1,000 bonus EACH

You forgot to say you live in a small tool shed on the job site and eat what your worker’s dogs eat.

“I have stopped drinking…”

But that’s one of the few areas of inflation the Fed is keeping up with:

Alcoholic beverages at home 0.8% 4.5%

I have ramped up my drinking. I stockpiled booze in anticipation of inflation, thus contributing to inflation, but of course since it is all sitting around the house, I drank it. And now I need to buy more while having exacerbated my desire for it. This is the kind of complexity that Wolf is getting at. But the Fed’s models surely account for such nuance.

John C, best laugh I’ve had in a minute, I’m working on the ice cream, funds rate aint even close….

I was in Total wine and more in Arizona last week

guy had cart full of booze of all types

asked if he was hosting holiday party

NOPE – stocking up – live in Washington and booze is double/triple prices here

I also stopped drinking.

At some point after all, I do have to sleep…….only to awake, read Wolfstreet and have even more reason to continue.

I have started drinking.

Cheers!

I stopped 10 years ago, but I am thinking of starting again. Reality sucks.

Me too, I have lost 3 stone and I must say I feel so much better so there has been a positive side to this depression

Wolf: “Are these finally signs that inflation is starting to react to the Fed’s rate hikes and QT, or are we seeing just another head fake?”

Laughing Lion: “Well crumbs, that’s about all I buy nowadays.”

I truly hope it gets better and basic necessities become affordable, sooner than later.

It is possible the drop is a “head fake” and not part of a downward trendline. Perhaps its a “marker” simply attributed to greed based pricing, as suppliers push prices up as far as they think they can until people just can’t pay anymore and start to go away….then they slightly drop to the absolutely highest prices one can charge and still sell enough of the items at cost and enough to cover C suite salaries. It is also possible that when the customers go away or greed dissipates or there are alternative suppliers at better prices, then we may get a break from inflation. One hopes its not a “head fake”, yet rather a downward trend.

Maybe the free market is breaking and we are in the last stages of the “engulf and devour” of concentrated wealth. There is some evidence in the increasing number of companies doing very well, focusing exclusively (or almost or exclusively) on high margin luxury items (like $150K trucks), the rise of Whole Foods and the reality of Dollar Stores and food deserts in poorer areas.

Food for thought: We may soon see a lot of billionaires or their puppets running for political offices, as they try and topple democracy, which gets in the way of this “engulf and devour” strategy of concentrating wealth.

” There is some evidence in the increasing number of companies doing very well, focusing exclusively (or almost or exclusively) on high margin luxury items (like $150K trucks),”

This morning I read a hilarious article on the “Daily Upside” attributing the luxury brand windfall in these times to Gen Z living with mom and dad splurging on Gucci clothes and Rolex watches with their extra cash🤣

I dunno, maybe I guess, but it sounds really strange to me. Maybe Wolf cashed some light on the situation at some point here 😆

*can shed not cashed.. autocorrect 🙄

Ha! The crazy new internet world of TikTok and You Tube influencers. The world will never be the same after the Kardashians! Probably partially true,…except for the live at home part! Granted there are some “tweens” buying Balenciaga and waiting to turn 16 for their first Lambo! Rolexes (on the secondary market are finally dropping in price….). I will check it out for a good laugh.

“This morning I read a hilarious article on the “Daily Upside” attributing the luxury brand windfall in these times to Gen Z living with mom and dad splurging on Gucci clothes and Rolex watches with their extra cash.”

Wouldn’t surprise me in the least. I remember reading a comment somewhere, perhaps here, from a parent stating their 20 year old, still living at home, son had purchased one of those brand new almost $100k diesel trucks because he “didn’t have to pay rent so he could afford it.” Welcome to Jerome Powell’s Clown World.

Most of the sheeple don’t care about democracy or the Constitution or any of it. As long as white supremacy is the order of the day, nothing else matters. Billionaires may as well run the country keeping the riff raff foaming at the mouth over nonsensical cultural issues – that’s the plan anyway!

Weird comment. The dividing line separating riff raff from whatever the next trophic level is has no decimal point; money does not decide whether you’re a garbage person.

And there’s no grand plan. That thinking lets people off the hook for being perfectly stupid, selfish & vulgar of their own volition. We are autonomous individuals with mostly full agency and outside of cancer & billboards, we suffer what we choose.

“Maybe the free market is breaking and we are in the last stages of the “engulf and devour” of concentrated wealth.”

It’s oligopolistic corporatism in collusion with bought and paid for big government.

The “free market” (the private economy) doesn’t provide anything to those who can’t pay for it, but what exists today isn’t a real private economy.

Well, as voters we better do something quickly to save our country. There is huge power in sheer numbers who are united, as American consumers, with a common goal. Time to act, post haste!

Nathan, that doesn’t work when a huge portion of the country is voting for free stuff.

Also does not work when ”voters” are fed constant propaganda, basically these days ALL created and paid for by our owners.

Used to be the king and loyal royalty at every level.

Now the oligarchy ”behind the scenes”, mostly, so far, with newbie oligarchs having to do their thing for public consumption to be invited to join the party.

Ya don’t hear much about the ‘old money’ folks for very good reasons, eh?

Voting doesn’t fix this. The government is comprised of a corporatist uniparty where each side only differs on social issues meant to distract. The biggest morons are the ones who think that voting really matters.

I think “plutocracy” is a better term than “oligarchy”, at least by the way I just read the two latest definitions, but that’s a stupid comment on my part.

But in any case, there are a lot of people to get rid of, and because using nukes ends the whole game (including for the rulers), something very clever is going to have to be thought up…they can’t even keep on having limited wars, unless they can keep control on much bigger ones somehow. So a lot of my time is spent wondering just how they will pull this off, or if I will even see it….although I think I have watched the start (or continuation) of it all my life.

There is no doubt the peasants have been suitably dumbed down, and kept watching or arguing over meaningless things, and that effort continues, and seems to be working as intended, thanks to our two Political Corporations and “tuned” media.

Fortunately, they all have the same disease, so they can’t help but go after each other unrestricted, except for maybe within the confines of the “constitutions” of their own form of government known as a “corporation”, which is just your run-of-the-mill fascist state.

BTW, I followed the methodology of the new health care cost calculations back all the way, and was gradually led into a big bowl of “word soup” and naturally became completely lost.

Anyway, that’s my version of the “I should start drinking again” conversation, but being a Biologist, I want to see this next phase of hominid evolution with a clear head, otherwise getting wasted sounds REALLY good.

Oh, and in keeping with the general theme of this site, Central Banking seems a good tool for the plutocrats to use, and certainly much safer for them than the wars for territory of old….as long as enough people are willing to play “buy” rather than “take”.

But that’s always what the Military has been for…sometimes simple “cops, laws, lawyers, and jails” just won’t cut it.

Just another note on CPI health care “cost determination”;

“But for many Americans, the law failed to live up to its promise of more affordable care. Instead, they’ve faced thousands of dollars in bills as health insurers shifted costs onto patients through higher deductibles.

Now, a highly lucrative industry is capitalizing on patients’ inability to pay. Hospitals and other medical providers are pushing millions into credit cards and other loans. These stick patients with high interest rates while generating profits for the lenders that top 29%, according to research firm IBISWorld.

Patient debt is also sustaining a shadowy collections business fed by hospitals ― including public university systems and nonprofits granted tax breaks to serve their communities ― that sell debt in private deals to collections companies that, in turn, pursue patients.”

-From a Kaiser Health News study, and there is much more info there. 4x the debt from telecoms, the next highest category in the study.

Much of this “disappears” what little savings most people do have, while the rest goes on credit cards or friends/relatives.

Plot twist: where it turns out that the 80s disinflation was caused by China (globalization), not interest rates! In fact, interest rates will have long killed labor and the lower classes before killing inflation, if it wasn’t for China to absorb all the printing. That free lunch is over, inflation will persist and skyrocket.

I don’t drink any more,,, but I don’t drink any less either!!

Seriously, knew an old guy who took dad and me hunting on 100 sections back in the early fifties who said, ” A young man shouldn’t drink, but a man over 40 should drink a few sips of good whisky every day.”

He lived to 104, and according to his grandson, worked every day up until the last two weeks…

OTOH, my neighbor said he quit drinking, smoking, and having sex; said it was the worst 15 minutes in his long life.

And so it goes, eh?

The way Wallstreet sees this : Lower inflation => Lower Prices! => Lower 0.5% rate hike => Instant Fed Pivot => Free Money => 10 year yield plunge 0.5% to 3% => Massive stock rally => screw shortsellers

Hahaha, yes, Wall Street thought yields would go negative in 2020, and the 10-year yield dropped below 0.5%, these IDIOTS! They were utterly clueless. Consensual hallucination. They got their faces ripped off. That’s why bond funds had the worst performance in many many decades. Horrible losses. These IDIOTS are back at it. Fine with me.

Wall Street is definitely hallucinating.

China just agreed to buy oil and gas from Saudi Arabia and Gulf states in yuan instead of dollars.

One half of the Russia FX market is now in yuan instead of dollars.

Even Australia is now selling iron ore to China in yuan instead of dollars.

China, Japan and KSA dumped billions of dollars worth of US treasuries and bought gold.

No wonder the dollar has been dropping like a stone this month.

Inflation is here to stay. QE is dead!

There really are a number of posts that could be written about various migrations to the Yuan.

And I think solely relying upon reported FX reserve compositions and supposed intl trade value composition are worthy of close re-examination too.

Mainly because once a long sick, continuously abused USD goes, the political illusion of the “American Way of Life” vanishes immediately.

That’s probably worth monitoring closely and frequently.

According to Credit Suisse Ultra High Net Wealth Report over half the people with more than $50 M LIVE HERE. Around 80K people last I saw.

All those palm tree islands and the world map islands in Dubai are unfinished and empty……

Location, Location, Location.

As you well know, without a recession a head fake lies ahead. That’s a given. What’s not a given, again as you well know, is how far housing falls before it stabilizes & whether or not a true recession comes to pass in the next 18 months.

And of course, there’s always the Fed pivot that lies ahead. To use your head fake analogy, markets seem to think JPowell is pulling a head fake. And these nimrods will be sorely disappointed when the moment comes that JPowell pulls out his Volcker Big Boy pants and stares them down & explains why the Fed can’t pivot with when Core PCE approaches 4%.

Ditto, Wolfster, I may be putting a pinkie back in the short bond market waters pretty soon via TBT which is for trading, not a long term investment. Keeps me out of the bars! Covid keeps me out also.

COMPLETE IDIOTS, Rising interest rates are still rising interest rates albeit slower rising interest rates. Rising interest rates = decline in bond market prices. I learned this is 1994.

The Fed will pause on interest rate hikes in the future; but, the economy will be in recession/depression and risk not meeting earnings will be higher. Stocks will be and are still are expensive.

Zombie companies will go under which means stock/bond risk is higher.

What am I missing?

Looks like market is taking this cpi report as positive.

Haven’t you heard? Inflation has now been conquered, so Powell can stop raising, and drop to 0%, as soon as tomorrow. He can also resume QE. Raising stonks to all time highs is the new Fed mandate.

/s

I detected sarcasm long before the tag.

Yes, the market and media coverage seems to be all about “turning a corner” on inflation … do you think the Fed will pull their punches? Eg 50bp raise and dovish comments?

The market looks to be setting up for a big drop tomorrow. I’ve learned over time that these moves are irrelevant to the content of what the Fed releases, but I’d say “logic” at the moment leans to the side that the Fed is going to be more hawkish than expected.

But seriously, the move the market makes after these announcements are usually unrelated to the actual content of the the decision or statements.

Here it comes

I’ve been pointing out in a couple of recent posts that the market response to recent FOMC meetings has been driven by the conclusion of the events rather their content – but only communicated by me with the benefit of hindsight.

I feel compelled on the eve of the latest FOMC to predict the market’s reaction tomorrow before it takes place.

Stock market sharply up by close of play. (Predicting market moves in a single day is not my thing, but just for fun, I’ll give it a go).

I sold my beloved TSLQ today and bought TSLL. I almost never time the market properly, but anyway…

“I sold my beloved TSLQ today and bought TSLL. I almost never time the market properly, but anyway…”

When we hear your trading account was shut down, we’ll know we’re getting somewhere on inflation.

AB, I strongly believe that the moves the market makes are not driven at all by what the Fed actually says. The market is now about 15% up from the October low, and in that time the Fed hasn’t changed a thing, has raised rates by 0.75%, and arguably has spoken more hawkish than expected. The TLT fund is up 17% since the end of October. It’s very hard to argue that this is because of something the Fed did, or that the Fed is in charge of this.

I’m still writing this before the Fed announcement and I’m telling you the positioning of the market is such that there is likely a big drop coming. It may not be sparked by the Fed at all. But the setup is there, regardless of the Fed’s decisions.

That same setup to rip higher is just a stretch right now. Anything is possible but probabilities point to a sustained move lower (ignoring and volatile spikes we may get).

Milk, Butter bread and eggs are even higher than 2 months ago. It seems that what I’m seeing isn’t what the government is seeing.

Stoke up the stove, there’s wood in the grove,

And prices are always dropping;

Your Uncle Sam is stewing lamb,

While Aunt Martha does the chopping.

Don’t lose your head, over the cost of bread,

As all other things are equal;

This may be the week, when prices don’t reek,

But we’ll bite you in the sequel.

Your poor milk, butter, bread and eggs didn’t get that special healthcare “adjustment” that made all inflation magically wane. “What I’m seeing isn’t what the government is seeing” either. I rarely pay labor, but I had to have a leaf spring taken apart on a piece of equipment. Their labor rate is up to $150 per hour, and parts and supplies have shot the moon. This isn’t over by a long shot.

Just dropped $4000 on a transmission for the truck.

Son of a bitch.

Good news is EV trucks don’t have transmissions!

Bad news is they cost 25 times $4K.

And can only pull a bass boat 20 miles on a full charge. And they won’t easily fit at a charging stall with a trailer hitched to them.

I own an EV and love it, frankly don’t ever want to go back to gas.

That said, the design of charging stations make it impossible to charge an EV truck with a trailer attached. Even if those trucks can make 200 miles pulling a heavy trailer, you will currently have to unhook the trailer to charge the truck on a road trip.

That is a deal breaker for most truck buyers, for now.

And you may have to wait a year to get one LOL

That’s why I spent $4000 on a transmission.

I feel you. We just put new rubber on a Journey that will be 13 years old in a month — rolling the dice that it will last as long as the new tires …

10-4, ditto 10-4 eg, ditto:

Just did an over all ”refurb” on the 14 yo Cobalt to make it run as well as new, including tires…

Great economy car, and spouse finds it much easier to park than the 3/4 ton pick up she drove for years,,,LOL

My step-daughter was by the house yesterday for a while and parked her 2002 Toyota RAV4 in the street. A while later, a guy rang the doorbell and asked her if she wanted to sell it. She said no, as it only has 150+ K on it, and she wants to keep it a few more years.

This old stuff is like gold anymore if it’s in good condition.

I’ve never understood the addiction that most of my American peers have for pick-up trucks and other large vehicles. The most common answer when I inquire about vehicle preference is “utility.” I typically follow up with a question as to how much utility there was in paying twice the price of a comparably optioned sedan that gets almost double the mileage. They say they can just throw things in the back of the truck whenever they need to. I ask them how often they do this. They (at this point getting tired of me and knowing where this is headed) say at least 3 or 4 times a year (Christmas tree, fertilizer or mulch from the hardware store in spring, a new piece of furniture, etc.). I joyfully inform them that U-Haul will rent them a pickup from their fleet for $20 and gas costs. The $20 could easily be found in gas savings reaped in 1-2 weeks of driving a practical vehicle. Also, U-Haul performs all of the maintenance so you don’t have to. The price difference for new tires for my wife’s 20″ wheels was almost double my 16″ ones.

To me, a truck is always and has always been a tool. It’s absolutely stupid to purchase a tool that you don’t or rarely use for its intended purpose if you have the option to borrow or rent it. For many, I’ve realized trucks are fashion accessories. Hence why they’re often covered in lifestyle stickers. To each his own, but I don’t think I’d like to pay $30,000+ over an alternative to inconvenience myself (economically or otherwise) on the off chance my status symbol might be useful a handful of times in a year. My wife’s SUV makes the purchase even more redundant, and it’s still a small 3rd-row seater with a 2.5L turbo 4 that gets tolerable mileage at 22 urban/suburban.

My current sedan gets 30 MPG easily in urban/suburban settings and has occasionally gotten 45+ highway. It runs on regular gasoline. Parts are moderately cheap (as was the vehicle itself), and it’s still got enough power thanks to its twin-scroll turbo to be “fun” to drive once in a while. Am I able to fit a refrigerator/freezer combo in it? Of course not. I use my wife’s SUV, enlist the help of a friend who owns a truck, or swallow my pride and go to U-Haul.

Has anyone health insurance dropped when they re-enroll in Nov?

No, my health insurance didn’t drop. Every year my employer brags about rates not going up, or barely going up. Then, every February, a month before my birthday I get a letter from my health insurance company saying they’re increasing my monthly rates due to my approaching “milestone” birthday.

I’m in the marketplace as I pay my own. It’s WAY up over last year. My rent is going up in January, but fortunately that’s a small increase and still reasonable.

Gas where I am is still around 5.60/gallon and lettuce is more expensive than some cuts of beef.

Dang, where do you live? Gas is 2.43 here in the Ozarks today and got lettuce growing in the garden.

Mine dropped 30 bucks/month, at least that was the promise of the notice I received in early November, but the truth is I won’t know for sure until I finish the process tomorrow.

Nope. I work for .gov and before open season even started they were warning and explaining rate increases. Coverage is great, but pay increases are few and far between and I keep falling further behind.

Nope. Used to having to shop our insurance every year.

That said, we settled on a policy that kept our deductible the same,

and our premiums went up 11% ( 1450/month ).

Nope. My health insurance has not dropped. Never has. It goes up in increments every few years of life. My insurance for my house, my rentals, my cars goes up too. Food is still up. Gas came down, but if the economy picks up will that go up again?

All I can do is believe what I see with my own two eyes. Inflation is here to stay even if they claim it’s retracting.

Nope, went up about 60 bucks / week. So a hidden pay cut. Another reason to work just enough to not get fired and not a minute more.

On home insurance, I saw a recent case where an insurance company proposed a doubling of the premium this year due to Hurricane Ian and roofer fraud. The home is in FL. The policy holders were able to keep the rate level by waiving rights to court hearing and committing to mandatory arbitration in case of a conflict. Also, the existing insurance limit was based on replacement cost, which was much higher than market value, so the insurance limit could be reduced quite a bit.

These were two policy changes that halved the proposed premium, while not materially impacting the coverage.

Based on this experience, I imagine a lot of homeowners could save a lot money by adjusting a few terms.

Yesterday WTI was 70, today 75 on the way up til next year.

LNG will do even better.

My natural gas heating bills doubled last winter compared to 2020-21. I checked the latest fixed rate per ccf gas unit, and it seems my heating bills will rise ANOTHER 66% this winter (3x as much as two years ago).

I certainly don’t see any signs of inflation easing except for recent gasoline declines.

Yes, you are right. I live in a 3500 sq ft house. An downstairs and upstairs. I run the heat come darkness when I get home and set at 72. My bill went from low 400’s a couple years ago to low 700’s for this last month.

No, I don’t see the drop either. Today, my trading buddy was laughing about these garbage numbers. He sees no drop in inflation either. This is government propaganda.

We set our heat at 69 and wear sweaters, winter pj’s and bathrobes. Also wool socks help.

Food is costly. We have only one car. Retirement on a fixed income.

There are other things we do want to spend money on, so we save.

IMHO….and I mentioned it before, look at oil as a forward indicator. I am on the macrotrends web site looking at the historical price of oil that is inflation adjusted. Basically every CPI peak at 6% or higher in Wolf’s chart corresponded to an oil peak

Here is the oil peaks info I pulled from looking at the chart. The following is in todays inflation adjusted dollars.

1980 – 0il peaked in 1980 at $140 then dropped an bottom 1985

1985 – spike bottomed at $28

1990 – Oil Spiked to $89 because of the gulf war

1998 – A spike bottom $23

2008 – Oil peaked at $157

2022 – May 16 oil peaked and has been dropping since

Oil is dropping and CPI historically follows based on charts from 1970. But as Michael mentioned, oil is now in the 70s. We should see the inflation rate drop some. I am not saying it will drop a lot but it should drop some. Maybe in the 6% range over the next few months. But if oil goes back up to 90 or 100, CPI will probably rise too.

If you look at every oil peak, there seems to be a peak in interest rates shortly after and then a recession. So was it the fed rate hikes that slowed the economy and killed energy prices? Was it rate hikes that caused oil to drop or is every oil peak and rate hike a coincidence. Just thinking out loud. Heck if I know.

Great report Wolf!

Can’t believe the market looks at the MOM and not the YOY. Anyone heard of random walk?

12 months make a year.

Thank you for the detailed summary.

I’m guessing the slowdown in inflation is transitory.

Based on Wolf’s charts, I’d say it’s almost certain it’s all just another inflation head fake. The charts show it takes years to bring down inflation. A few months of QT is not going to be enough to bring inflation down as history and Wolf’s charts show.

!) According to econ 101 experts the probability of recession in 2023

are high.

2) The Fed want to kill gov debt. Today CPI results are good enough for them.

3) In order to stay the course and avoid cutting rates the Fed shouldn’t raise rates too aggressively.

4) Suppose inflation waves will osc between 1% and 10%. At 1% EFFR

will be above the CPI. At 10%, below.

5) The Fed should target a spot slightly below the middle.

6) When the CPI will below EFFR, the experts will blame the Fed for being

too aggressive. At 10%, the Fed is behind the curve.

Soon there will be a Showdown between government who wants to increase spending at the cost of inflation, and what’s left of the banking cartel (the FRB) who still have a notion of sane monetary policy. Our money will finally be defeated in that clash, when the government finally takes control over printing.

Interesting, thank you. It looks like higher rates are needed. Noise in the CPI statistics and markets go crazy.

My hunch is that people are beginning to tighten their belts and go on a buyers strike. I have been for 2 years now. Prices are only going to drop when everyone stops buying at inflated prices. I clip grocery coupons and shop at the thrift store for household items. Today I got what looks like a brand new pair of Nike running shoes for $8. It’s really fun finding good deals. I don’t buy anything that I don’t truly need for my family. I don’t buy eggs anymore but 2 years ago it was a cheap source of protein (10 cents per egg). Not anymore. I buy NY steaks on sale for $5/lb and even though it costs more per pound than eggs, it’s a better deal. Albertsons hates me because when I go there, I only buy stuff on sale and typically save 40-54%. They even call the manager over to check because I saved too much. It’s all a game to me but it’s fun when you win. Play well folks. For the guy that just dropped $4K on a new transmission for his truck…buy a Toyota next time.

I agree the American consumer should go on a “buyers strike”. The problem is Food, Clothing and Shelter are hard to go without. We have a much bigger problem than what the Fed does with QT. It’s “Main Street versus Wall Street”. I don’t think the Fed can do much for Main Street until Greed based pricing is under control and Wall Street “closes the casino” and gets back to fundamentals for stock prices. The insanity of the financial markets should not affect the price of a loaf of bread.

I am in the same boat. But I am also trying to produce more of my own food. I raise chickens and ducks, although had a set back due to the neighbors dogs. Next year I am hoping on raising some sheep. Depending how well I do, perhaps sell some extras. I also try to garden, but I am pretty horrible at it. But that is my goal, increase my wealth, so to speak without income. Also, with proper fencing, livestock is pretty easy and not much work, once they are no longer babies.

If you really want to stretch those dollars in the name of cheap protein, there’s always dried lentils, quinoa, and chickpeas in the supermarket bulk section.

Take a half of a $1.30 pound of dried chickpeas from Wal-Mart and stir them in a slow cook Crockpot for 6-7 hours with 6 cups of water & 1/2 tsp salt. Drain, then put beans in saucepan with condensed store brand tomato soup with 1 extra can of water, throw in a bunch of raw spinach. Stir occasionally over low heat for an hour for a very cheap, protein-filled, vegan, healthy, hearty winter soup.

Iam a vegeterian all my life.(not even egg but use milk/yoghurt/butter /Ghee (clarified butter) in my diet in all my 60+ years of existsence.

Lentils /Legume (say 5-6 types I eat regularly) are a major portion of my diet other than veggies with flatbread /rice. In my country average priceis $1-1.3 /KG lentil producers all over the world export to here as world;s top lentil consuming country of 140 billion !

The trick to cook lentils is to” soak in hot water” 2 hours earlier /over night and always cook lentils in “pressure cooker” .

never more than 30 minutes cooking this way.

If anyone is curious type in Ytube “DAL MAKHANI “/ “DAL TADKA” for a delicious comfort food that you can eat with store bought flat bread /plain rice or “JEERA RICE”

I buy things from Amazon and only buy on sale. I’ll put what I want in my basket or save for later. After a while they will lower the price 20%/give me a 20% coupon or show me something cheaper but with the same quality. Then I will buy it.

We used to eat eggs all the time. Now the Mr. will eat eggs twice a week and me not at all (better for low cholesterol diet).

All we need to do to kill the rest of the inflation is to find another Strategic Petroleum Reserve to empty.

I’d suggesting the global economy find another “Strategic Labor Reserve”, as due to the pandemic, it would seem that early retirement, long covid, and a mega working to live versus living to work paradigm shift could easily make inflation hover around the 3-4% range for 3-10 years.

Thus one of many reasons why I think the Fed will have to raise the inflation goal to 3-4% (3.25/3.5% best guess), which is the exact range El-Erian suggested Sunday via FT article.

Per Fortune:

Meanwhile, accelerating wage growth and strong monthly job gains suggest inflation could continue to “overshoot” the Fed’s forecast, El-Erian said.

“Rather than fall to 2-3% by the end of next year, U.S. core PCE inflation will probably prove rather sticky at around 4% or above,” El-Erian said. “This is what happens when an inflationary moment is allowed to get embedded into the economic system.”

A 3% to 4% inflation target would be more reasonable, El-Erian said, given the instability of supply, the transition away from fossil fuels (likely because the transition itself can be costly), and an extended period of nearly zero interest rates.

What could be happening is that the Fed is publicly signaling a 2% target, but could instead pursue a higher number and hope the public accepts it, he said. However, if that were to happen, he said, the Fed would risk raising more concern over its “accountability, credibility, and autonomy.”

“Yet, given the extent of economic uncertainty and financial fragilities, the Fed could end up thinking that this far from perfect policy approach may be the better course of action,” El-Erian wrote.

That much above 0% (4%) will prove incredibly difficult to maintain long term. People start to notice it around 4-5% (and remember, that number is certainly an underestimate of the real rate people deal with every day), and begin to plan for it which only increases the upward pressure.

Inflation is dropping, but prices are still going up at a fast pace. Is that a cause for celebration?

Do we celebrate when a dentist is mid-way through his drilling? Do we celebrate when he turns down the drill speed a little bit and pulls out the pliers?

Yoy PCE will explode higher for the next two months, simply because large negative prints are rolling off from last year. We will see 4.5%+ CPI inflation through at least 2025. A large number of people got fabulously wealthy over athe last few years, all of whom have a “pay whatever” mindset due to their huge instant lotto winnings. Unfortunately that 10% of the population acts as an achor for price setting, pushing up prices for everyone else. Unfortunately, it’s not going away anytime soon because that pandemic money is still circulating in the economy, changing hands everyday. There is insufficient QT, and rate hikes don’t cool the lotto spending of the lotto winners.

Not entirely. A drop in asset prices can happen without that amount being removed. That said, I do agree that the “rich” are driving inflation these days.

That was the ultimate flaw in QE. You can never guarantee that printed money won’t reach consumer goods and services. In fact, I’d argue that it was destined to happen at some point.

The fact that it was dumped in effectively instantly is what messed things up. If a million dollars lands in your lap effectively overnight, why not bid an extra $200,000 over asking to get just the house you want? Heck, there is $800K left over to blow! That’s exactly the mndset we have been seeing for the last two years, and will continue to see for at least two more.

Look at it this way: $10 trillion was dumped into the US economy, effectively overnight. If that were to be spent down evenly over *5 years*, that would come out to an additional $5.5 billion per day of e onomic activity, meaning $165 billion a month of *additional* economic activity over pre-pandemic spending, assuming *5 years*! In other words, the goverment really did a number on us.

Right. And they think that a few paltry rate hikes to a fed funds rate of 5.25%, FAR below CPI, has tamed inflation – the easiest inflation fight in history after the largest money print in history. These people are insane.

Of course, what’s really going on, is Powell and Co. aren’t stupid. They want to keep those financial gains they and their rich buddies just stole from the futures of the young. Jerome Foul is try to put a floor under asset prices.

Vehicle insurance is going crazy in Fl, but ohio is low. So the two offset each other, one has massive growth the other has zero. The problem is its Avg across the whole U.S. and it looks low. I think that soon Fl will slow alot and then other states without consumer protection are going to go up fast, it looks calm on the surface, but both combined will be massive inflation for everyone. I think inflation is entrenched, as long as demand is there, companies are loving the high rates. I just wonder when PPI and factorygate will hit wholesale and retail inflation numbers.

Since these reports have lag, no one sees the real numbers and Wallstreet is loving the bull runs, and soft landing the Fed is giving them.

No way Will. This is Fla. We lead the nation in auto fraud and roofing fraud scams. We earned our Fla-man memes and aren’t giving up the title so easily!

Hurricane damage 500 miles away?… call FEMA, I gots damage.

The fraud in Florida over roofing claims is unreal. My next door neighbor has a 28 year old roof. The underlayment was totally rotten. An adjuster knocked on his door, he signed over his rights. He won even though we have not had winds greater than tropical force pass anywhere near us. Florida insurance companies have to pay their own legal fees plus plaintiffs. We have 654 homes in our community, a roofing company owner lives here. Now I am paying for everyone else fraudulent claims even though I paid for a new roof 6 years ago. A concrete plantation style tile roof averages $50K. Add this to the claims from hurricane Ian and Nicole and Florida Insurance market is beyond broken. The governor and the Republican legislator could have fixed this years ago but too many donors were making too much money so they looked the other way. My house has new Hurricane code , windows, doors, roof, 4 point inspection snd it still is 5 grand a year. Florida’s whole economy is real estate based. Insurance is a deal breaker for lots of people moving here.

move away from the coast, our homeowners insurance is the same or less then 6 months of car insurance and has been that way with multiple different houses in center of the state away from the coasts.

The problem with Florida is that the insurance companies never charged enough for insurance and it let people build too much where hurricanes hit. In the past only the rich and those who built smartly could afford to build near the coast. Now insurance has gone up for everyone, to make up for them not pricing insurance correctly in the first place.

Still well within zone of uncertainty. But Fed has clear cover to go with .50 and harsh language.

Wolf:

I am trying to understand why JOLTS looks lagged.

They released it for October, but the website is saying November will be in Jan and October will be Dec 15th.

https://www.bls.gov/jlt/

I think its to frame the market and scenario.

What do you think?

Hahahaha, no. JOLTS comes out at the end of the month. October was released on Nov 30. November would be released at the end of December, but Dec 30 is a Friday, and the 31st is Saturday, and it’s during the holidays, so they will release it on Jan 4.

What will be released on Dec 15 are “State Job Openings and Labor Turnover data for October 2022,” as it says. “State” as opposed to “national.”

The conspiracy theories people concoct about even normal calendar functions are just stunning. Don’t people have anything else to do with their time LOL?

The Fed has little or nothing to do with the current drop in inflation. The real reason is people are mostly completely broke just paying for necessities and have little left for discretionary spending. I’m on a buyer’s strike. Spending most on services that I have to have and a little on entertainment at my local Irish Pub, and Sports bar.

We have stopped going to our favorite restaurant except for every now and then we get takeout of something less expensive. Now when we go out to dinner, maybe every few months, we go someplace upscale. If meals out are going to cost a fortune, we want the best at the finest places.

We do probably spend the same amount of money for one exceptional meal vs 4 ordinary meals.

High enough inflation to be a severe concern.

Low enough to slow down hikes, which is probably good for avoiding a collapse and another ZIRP bailout.

Even with the most dovish lens the problem is housing and jobs which have yet to move much so higher for longer still rings true and keep rolling with the QT until assets get back under control.

Nice to see we didn’t go 🚀 today with stocks rejecting the 200 and 100 day MA and the ten year held at 3.5%

Let’s see if Santa JPow from two weeks ago turns into the Grinch tomorrow.

I feel like if everyone expects the Santa Rally we won’t get one. Kinda like today many thought a beat on CPI expectations would result in a massive rally, but it ended up less than yesterday. Christmas is right around the corner…

Yes govts fighting inflation will go straight to the source, the statistics themselves, and look for ways to improve the figures. Wolf has pointed out the fake negative value for health-insurance. Now let’s see what happens to the fake “Owners equivalent rent”, originally put into the CPI to understate house-prices but now working to overstate the index as house prices are falling faster than rents.

And watch for the shonky dodge of “chain-weighting”. When something goes up, say beef doubles in price it’s assumed people can’t afford it any more and the magic wand waves that item away, removed or reduced in the index and something cheaper substituted. Ugh.

Exactly framing the scenario, it doesn’t account for the avg consumer budget.

It’s not a conspiracy, when they manipulate the numbers. It has to look like its always in control. I do alot of data analytics, for a supply chain, it’s my job. I see the real functionality of a system, but the numbers are framed to cover for failure. I’ve seen it everywhere, I show the flaws, but the reality is scary and don’t want the truth. With this in mind is it so hard to believe the scenario is framed to keep the destruction of asset prices from happening? Is it for the betterment of the people or the massive dumping of money into the system to inflate assets and keep it there for wealthy to make money?

This a Great Blog post with these Once again Results Charts showing our economy’s current Condition . These are my words of course as I try to understand just how current conditions have affected our lives and future.

Perhaps one day I shall see here some Charts showing the Cause a list of all the Monies made by Various People Like the leaders of the Fed and Political leaders , Congress the list is long . Something like a List of personal Investments and Gains from those Investments like as exampleall the various Millions perhaps Billions of Dollars made by named Persons and agencies . Cause & Results Charts YOY .

I am in the Philippines Now in Manila a Huge City with unbelievable Trafficfor a Month then to Baguio for another Month not sure how long I will stay this trip but all in all the cost of living so far is so Low you almost think in terms the spread is so Vast you can’t compare An hours drive in a UV Cab( that’s the lowest cost Van type Cab ) Cost is by distance at 50 Pesos Per head that’s only $1 US for about 1 hour of travel > Shorter Travel by Trike( a 3 wheel Motorcycle that can haul 4 people costs 10 Pesos ($0,18 ) cents per head for about a few miles . Food is incredibly Cheap compared to the USA a Complete simple meal at a restaurant for 4 People Rice Dumplings Shrimp & drinks came to P500 that’s less than $10 USA !

Bask Bank ( Texas) Just went to $ 4.03 APY Saving rate this morning. That’s a Liquid daily in and out no fees and I am seeing some questionable other Banks in the USA offering 5% CD Rates Now 7 Mo and up. I guess I should consider their rates ” Results ” I am not sure ? perhaps they will Cause something scratching my head LOL

5 percent cd rate yesterday Dec 11 and today 5 yr 4.75 because of the cpi number

Fidelity CD website

How’s the cost of living in Mendocino ?

I suspect that it’s increasing in a manner that harshes one’s mellow.

I have had the opportunity to visit and build mines in several of our sister and brother countries south of the American border wall. The dollar is preferred to the peso or soles.

I would move there, maybe, no, except for the political instability.

As a Colombian engineer chided me one time, whether it is North or South, it is called America.

It’s all fun and games until a narco decides to pull a kidnapping for ransom scheme on your lily white a**. When that rich family they thought you had doesn’t exist, your lifeless body will be tossed into some shallow grave to petrify in the Mexican heat.

Cost of living in Mendocino > www. mendocino. com its one of the 10 most Beautiful places in the world I can say as a world traveler . (2) the other saving grace is the fact there is no Freeway from inland 101 over to the Coast but rather a 1 hour and 15 beautiful drive on 128 to coast some 3.5 hrs from the SF Bay area. Freeways Bring Lots of traffic & People You can get a decent Home on 1 Acre for about $750,000 but the listing are few , many just buy land and Build > as a retired Rev Hab developer I bought a fixer in 2002 for $190,000 with 2 houses on 1 Acre Lot walk to the ocean side 5 min weather always 55 to 70 degrees. Dream weather for me. Heck if you got the bucks this is a fantastic place to live with no Pollution

Mendo – living in a “…you can’t get there from here…” area has it’s advantages, especially when it possesses natural beauty ‘not available in stores’.

(fortunate enough to live in north coastal Sonoma, meself – the drive to Gualala/Pt. Arena is always a sensory (if not expeditious) pleasure, even better astride a motorbike…).

may we all find a better day.

Yea the market was up alright. What I saw in the tape was selling the rip.still negative rates, Fed wants real which is positive not negative. We are at 3.50-4. now. A ways to go still.

Personally, I believe that Fed Funds Rate (FFR) will eventually have to exceed the measured inflation rate which is presently greater than 7.1 pct.

The world, as usual, is experiencing a chaos that is related to the failure, and reversal of the central banking policy. When protocol fails.

Adding further to Wolf’s point that Healthcare PCE differs from Healthcare CPI (which is one of many reasons JPow favors PCE versus CPI)…

Per Investors.com:

Health care spending in the CPI excludes the bulk of outlays: spending covered by employers and government programs. Further, the outright declines in medical services prices in the CPI reflects stale data on insurer profits. By contrast, PCE health care services inflation is on the rise amid higher labor costs.

Thanks for the bald face presentation of the data, both graphically and in your commentary.

The problem that I have, is that, statistically, the rate of inflation is the same as it was a year ago, nevermind, the thumb suck, month over month reported change in the data point of negative 0.1 pct.

The necessary plots of multi-year data, obscures the insignificance of the random oscillation of the data around the mean value.

I am a curmudgeon as nurtured by my Mother cautioning me about the other shoe that is likely to drop. The Federal Reserve Board is likely to make a historic mistake in the morning by raising the FFR rate by 50 basis points, rather than a more appropriate 75 bpts, which will partially reinflate the enormous bubbles they are attempting to gently deflate.

It will also demonstrate that the FRB is a supplicant to the Powell controllers.

There’s no reason for .75, it looks like the fed raises are working, 6 month annualized ppi says .50 is sufficient

Nope. Need to get back to precovid prices. Hope for recession.

Nope, recession is needed to get out of this mess. Hope the Fed crashes the system.

Which means that you disagree with my assertion that 0.75 is the correct tonic based on a lame ass brain fart that you exuded ” it looks like the raises are working”.

Well, may the best man win.

Dang, stick to facts not hyperbole city, 6 month annualized shows the moves are working, it’s undeniable

Rookies!

What are you talking about? Jpow makes money off the stock market, he knows what words to say to cause a direction of the market. Each word can move billions of dollars in a different direction, trillions even. His buddies just know before what will say

So do we still believe that 5/10 year treasury rates have yet to peak? Seems like data and the FFR is irrelevant at this point. Powell will come out tomorrow with a weak dot plot putting the nail in the coffin. The party is over.

Make sure you check back in tomorrow after we get the dot plot.

Nasty 😂

It’s hard to imagine we have central bankers who think it’s OK for money to lose 10% to 15% of its purchasing power in two years. If they thought it was a problem, they would reverse the inflation, not just reduce its rate of increase.

The fantasy is that high inflation will solve the debt ponzi scheme that the entire globe has embraced over the previous forty years.

Yet even the St. Louis Fed knows this is not a long term solution and will inevitably raise future borrowing costs…

Per StLouisFed dot org – Aug 1 2022 article titled “Inflation and the Real Value of Debt: A Double-edged Sword”:

While a surprising burst of inflation immediately reduces the real value of a borrower’s debt burden—transferring wealth from lenders to borrowers—it is also likely to raise future borrowing costs because investors will then expect higher inflation and demand higher nominal yields on debt to compensate them for the expected loss of purchasing power and the associated uncertainty.

In summary, the recent burst of inflation in the U.S. and the rest of the developed world will have two effects: It will immediately reduce the real value of existing debts, but it will also tend to raise expected inflation—and therefore yields—perhaps for years to come, which will increase the cost of borrowing in the future.

Wolf, I’ve stumbled across TRACE monthly files on bond market volume. Is this data that you’ve ever covered? Interest rate changes are easy to follow but it seems overall volumes trading in Treasury and Corporate bonds would also be interesting to track.

Any thoughts?

I generally don’t cover volume of trading of anything, not stocks, not cryptos (volume collapsed), not bonds.

Booze was already expensive. I feel happy that my side hobby is turning moonshine into decent booze. Hurray for old traditions. But seriously, today’s inflation print vs, and estimate. I be GS made the estimate and made money today. 7% is still high whether we call it 7.1 or 7.3

Having been in the military for the past few years, I moved too often to get my homebrewing station set up well. Also, nowhere we were stationed had basements. My current house that we bought when I ended service also has no basement. Regrettably, fermentation does not go nearly as well when there’s fluctuations in heat. The garage is a bad place due to the lack of insulation and high-variable weather (32 F yesterday, 50 F today, 32 F Friday). Ze kinder will get into it anywhere else I store it in the house. Well, at least the state I’m in only has a prohibition against owning a still, as opposed to, say, a water distiller. Some cheap swill might be getting transmuted into decent brandy.

Clear off a shelf at the top of a closet.

Shelter inflation alive and well in Phoenix metro. I suspect this will end badly in a few months, badly as in sellers will be crying a river. Good! Might help the water situation. Lol

The improvement is real, but still tentative … the recent dollar weakness and resurgence of asset price inflation puts continued progress in question.

When the dollar depreciates in capital markets, asset prices respond in real time, tick-by-tick. Consumer goods and services and wages though are several layers behind in the price response chain. Exhibit A is the surge in bonds, stocks and commodities as the Fed unleashed trillions in QE and promised ZIRP forever starting in March 2020, and consumer prices taking flight over a year later. This was on top of the prior twelve years of inflation still working its way through the system.

The Fed has correctly noted that tightening “financial conditions” are needed to quell consumer price inflation. If it allows inflation to reignite in asset markets, progress on consumer price inflation will stall and ultimately reverse.

Inflation is an economic opiate that feels good in the short run, while destroying the long run.

Self interest is the correct point of view which my Father in Law, a WW2 veteran that made a fortune investing in the US stock market told me 20 years ago.

I was talking about why it was a bad time to invest in stocks because the fundamentals weren’t correct. And he uttered one of the most accurate utterances I have to live with:

“They’re not going to let that happen.”

He was with an engineering battalion during the European winter, tasked with collecting the frozen bodies of the dead soldiers left after the battle of the bulge. Now, as his 99th birthday approaches, he feigns the same callousness that carried him through the atrocities that he witnessed.

After 3-4+ inches of rain in Cal this past week went out wild mushroom hunting. Cooked up a pan of Honey, Bluett, King Bolete and Slippery Jack mushrooms in olive oil and butter. Mixed into a stir fry of fresh Italian, Summer, Yellow squash with green beans, broccoli, Brussel sprouts, carrots and bean sprouts. A gourmet feast for about $15. No inflation problem here. Lots of leftovers. Although probably cost $7 – $8 last year.

That description of the ideal food preparation, reminds me of the misery of the college freshman dorm where the posers were in charge.

Inflation is coming down; this has to be the biggest gaslighting of the plebs.

No, inflation is not coming down, its increasing less rapidly than before, but still more than 7% compared to last year that also had an increase of more than 7%.

Plebs lost close to 20% of the purchasing power in the last 2 years and this according to official stats because most prices have doubled I would say post covid.

The money that was printed is not being withdrawn so we are just going to set at a higher price level for everything till next crises when the Fed injects more trillions and we settle at a new higher price level again.

What a way to confiscate people’s property, tyrants and kings of all time could have only dreamed of such powers.

I anticipate new all time highs on the DOW forthcoming. The Treasury Troll Secretary just emerged from under the bridge and belched forth something to the effect of “we don’t even need a recession to cure inflation.” Arthur Burnes Redux is set to start cutting back on the rate increases, and everybody is now singing Kumbaya.

A massive Ponzi in crypto called FTX was uncovered and vaporized with barely a hint of blowback on the market as a whole. The “true believers” are still “all in” even though everybody deep down knows Binance is its financial twin.

They printed so much f***ing money it’s sickening, and they think they’ve already conquered inflation, and all the speculators are largely still cashed up and ready to run things into the ether. No, inflation is not over with. It’s probably just getting started.

We saw the smart money come in to short the major market indexes yesterday afternoon. Looking for a brutal January as inflation comes screaming back in the first three months of next year. I’ve got a crash alert for January 5th 2023.

core PCE next update 12/23.

tho, any news is good news to this market.

“Pushed down by plunging energy costs, the all-items CPI rose only 0.1% in November from October, and was up 7.1% year-over-year, a further deceleration, according to the Bureau of Labor Statistics today.”

Bah Humbug, a decrease in the rate of inflation, is the last thing the data indicate. The data indicate that inflation has settled at a rate of increase that is far above the acceptable level.

Only fools are able to celebrate such nonsence.

The price of oil was artificially suppressed which is not the same thing as falling from true or real market forces.

The price of oil is always artificially manipulated. OPEC exists for a reason. People who whine about the SOR releases need to remember that.

I do want the Fed to accelerate QT to 120B each month. Or is there a reason why even that is too high?

Pushing the FFR greater than the 3 month T-bill increases the chances of a cave-in. Things may happen more quickly.

Bringing down inflation from 9% to 5% was always going to be a fairly simple undertaking thanks to fading year-over-year effects.

Bringing down inflation from 5% to 2% may be prove to be a much more difficult undertaking as long as there are two job openings per unemployed person.

The U.S. dollar is falling, China has reopened and Biden will be forced to pay top dollar to replenish the oil reserves. The artificial suppression in the price of oil is over (Boxing Day it ends). I hope all the government manipulation in the oil and gas sector helps the 4th quarter GDP which will just make things more inflationary. Fourth quarter window dressing in technical terms.

After reading and listening too all the reasons the Fed will only 50 basis points,readers were reminded of the head fakes,by Wolf…

Come to think about it,Tom Brady has been the master of head fakes for years…

The problem with looking at statistics is that it is like trying to determine where you are going, by looking in your rear view mirror.

What drives inflation is out of control government spending, which in turn devalues the money by putting more and more of it in the system outpacing the production of goods and services. That dynamic has not changed, and will not change until it succeeds in causing an economic crisis. For government, spending is power, and it will not stop out of control spending until it is forced to do so.

Anyone who believes this problem can be solved by lowering interest rates does not really understand the mechanics of what is happening.

What proportion of the total inflation measurement does health insurance carry? If it’s small (1%?) then the mega adjustment it’s not going to make much difference between the two inflation indexes, right?

Without this adjustment, the year-over-year services CPI would have been +7.4%, matching the 4-decade high in September, compared to the reported +7.2%.

Here’s the math:

Health insurance accounts for 0.9% of total CPI and for about 1.5% of the services CPI. It plunged month-to-month by 4.0% in Oct and by 4.3% in Nov. And there will be 10 months of plunges. And their impact is cumulative.

1. Month to month, the 4.3% plunge translates into roughly a 6.5 basis point (4.3% x 1.5%) pushdown of the services CPI.

2. The services CPI rose by 0.346% (rounded to 0.3%), or by 34.6 basis points. Add the 6.5 basis points back to get an increase of 41.1 basis points.

3. But that would assume that health insurance costs didn’t rise at all. But if health insurance costs actually rose by something like 0.5% (50 basis points), then the swing effect is an additional 0.75 basis points.

5. Add the 6.5 basis points + 0.75 basis points = 7.25 basis points swing.

6. for a total services CPI increase of 34.6 basis points plus 7.25 basis points = 41.85 basis points.

7. So now there are two months in a row so far, so 2 x 7.5 basis points for an increase of +15 basis points. This would take the year-over-year CPI from +7.22% to 7.37%, matching the 40-year high in September. Rounded it would go from 7.2% to 7.4%.

And this will keep going for another 10 months.

That’s why it matters.

It is truly the Whack A Mole inflation data, and if Powell wants to even come close to the fortitude of a Paul Volcker he should just bite the bullet and raise 75 basis points today to front-load the cost of money pain. Fed is still way behind the curve in fighting inflation, because a 7.1% print year over year for the CPI (with suspect Health Insurance machinations!!) is just the tip of the cost iceberg that is killing the spending power of the average American consumer.

I have Medicare with a USAA supplemental policy that covers everything except hangnails, and I know that my monthly premiums have gone up about 23% since this time last year. So I ain’t buying the BLS (Badly Listing Ship) magical adjustments because due to virus invasion, loss of healthcare workers, and clinic/hospital operating costs with spikes in patient loads, the near-term trend for healthcare is only up, up, up.

Technically, and I think the Fed will move the Inflation Target Goalposts before the doo-doo really hits the fan, the Fed is still 500 basis points away from target. Like shooting a rifle with bent sights or with both eyes closed. There are plenty of hot-cost pigs in the python supply chain that are going to pop out the other end in a not-consumer-friendly manner in the next 6 to 9 months.

You would think investors in stocks and bonds and anything with half a pulse would have learned something from the crypto crash that has begun in a very big way, but speculation, fed to a feverish pitch, is extremely difficult to wring out of the psychology of an investing public after a sugar high that lasted over a dozen free-money years. The good times do not run forever, especially since the Central Bank is putting the punch bowl into cold storage.

We just had a spectacular Intra-Day Reversal yesterday the 13th, and the Fed will be raising rates longer than Wall Street is expecting via these price burps that vanish into thin air, and the terminal Fed Funds will be higher and last longer than the unwashed on Wall & Broad are currently employing into their bullish assumptions. Corporate earnings in the 3rd Quarter were 8% below 3rd Qtr. 2021. Duh, when the E in P/E’s is shrinking, the ratio is growing without the benefit of bull moves upward in stock prices. Got cash? Got gold? Silver now positive for 2022. Got booze??? Got patience and a mute button for the TV??

Got silver, but I should probably get more booze. Definitely for trading and no other purposes :^)

1) One day Gen-z will have to live without Chinese gadgets. What will

they do.

2) Male prime age (25-54) activity in the econ is down from 98% in 1960

to 88%. Prime age Female stalled at 77% since 1997, after rising from

40% in 1960, when a working man could feed a family of four.

3) China love whisky, Keynes and Adam Smith : consumption is the sole

and purpose of all production and the interest of the producers ought

to be, as far as necessary, for promoting consumption and mass

happiness.

4) China loved the Fed, but EFFR half of the CPI might screw up the year of

the Rabbit and their five years plan.

“1) One day Gen-z will have to live without Chinese gadgets. What will they do”

I guess they’ll have to start using the robust, manly and 100% Western-made gadgets that you are using to post in Wolf’s comments every single day.

There was once something known as a “family wage” that was meant for one wage earner to support their family. Post WWII we happily gave that up in the name of equality. Corporate America and the Government were in full support of slowly splitting the family wage in two. How much of an upward impact did that have on worker productivity for decades? And more importantly what were the hidden social costs that it kicked down the road a generation or two?

Cattle herds in the west are being culled at a historically high rate due to drought. “Relatively” cheap beef has the domino effect of lowering the price of pork and chicken. That’s one mole that will definitely be popping back up in the near future.

Head Fake. No sane person believes the 7% inflation nonsense.

Some one obviously is not following the advice to “Do not fight the FED”. I am sure JP will rip their faces off shortly.

Zero Hedge just put out an article saying today is the last rate hike. I find it amazing that I found Wolf on that site. Couldn’t be more opposite in writing style/content.

ZH put out article after article saying that the Fed was trapped, that it could never hike interest rates, and then in March it said that this was the last and only rate hike, and when more rate hikes came, it said that the Fed would cut rates and restart QE by August (last August), LOL.

Those articles got lots of clicks. The other stuff that ZH publishes that is often very good and arcane, hardly anyone clicks on. That’s the sad part about this industry: nonsense gets the most clicks because people love nonsense.

Wolf, I agree with you about ZH. Lots of garbage, but about 20-30% of the articles are deeply cogent masterworks on their topics. Too much hassle for me to properly sort through it all only to prepare my brain for a brilliantly brutal grandmaster level economics workout.

I can’t take a publication seriously that is too cowardly to even identify its writers.

Speaking of…

Is there a way I can totally extract Elon Musk’s thoughts about the Fed, inflation, the economy, etc. from my news feed? Thanks. – Signed, Every Person I Know.

Please let me know if you get an answer. You may be onto something – a bull-sh*t blocker, revolting personality blocker, for example, an orange person blocker.

Some of my take aways from Mohamed El Erian’s recent interview on the Ezra Klein Podcast.

El Erain’s answer when asked why bond markets are so calm in this new inflationary environment:

1. Conditioning: decades of supportive bailout. World economy conditioned to follow the trend of the last 15 years.

2. Policy narrative from FED: continually wrong. “Inflation is transitory.” JP “We’ll be cutting by the middle of 2023.” Mary Daley, SF FED. FED lack of humility and not considering the conditioning of the markets it has created.

3. Mindset: Most people in the financial sector today did not grow up with inflation in the 70’s. No idea really of what it is, what it can do.

4. Constant reframing by business media: There will be a recession in 2023. But it will be short and shallow!

5. Active inertia: Human condition to repeat the same behavior based on previous outcomes. No change going forward. FED pivot coming just around the corner.

6. Market only hears what it wants to hear and channels that message through the business media and internet: “Inflation is only 7.1%? That’s fantastic! It can only go down from here.”

7. Urgency in the whiplash narrative: Inflations coming! Inflation?? What inflation?? Constant and continual redirection.

All of these factors were discussed in detail by El Erian, as well as many other global developments including new geo economic structuring, geopolitical maneuvering, new and lasting changes in the labor markets as well as on shoring or re-establishing domestic industry if not only for economic resilience, but also national security.

Of course, the FED’s role in how we’ve arrived where we are was discussed in great detail.

Long story short, all of these changes that are occurring coupled with the FED’s disastrous policies over the last 15 years, in his opinion, are inflationary.

He goes on to say his biggest worries going forward are:

1. Over leverage

2. Liquidity give up

3. Structurally weak assets classes

He ends with, I am paraphrasing:

” because of the extremely fragile conditions of the present financial markets, my fear is we will undershoot for the future and the most vulnerable will be hurt the most.”

I think that speaks volumes for an opinion that is as intelligent, well explained and as honest as I can discern in all the noise out there.

Definitely worth a listen.

If he starts saying inflation needs to retraced (i.e., a period of deflation), then I’ll listen to him.

The most vulnerable are always, always hurt the worst. Inflation or recession – always the least get hammered the hardest.

Aren’t most head fakes made out of styrofoam?

Here is an example of the service sector jumping into the price increase mentality.

Dear clients,

Effective 12/15/2022, you may notice that our prices for medications, diagnostics, and our services have increased. This is an unavoidable part of being able to remain open with qualified staff to provide the care you have come to know and expect for your beloved pets. We believe in treating your pets as if they are our own and we understand this may be an inconvenience for you. We are able to provide estimates for care prior to service. Simply speak with anyone helping you to discuss your pet’s treatment and associated costs.

Thank you for trusting us to be a part of your pet’s family.

Sincerely,

Nazareth Veterinary Center

Veterinary costs have exploded the past 10 years, with the past 5 years of increases going almost parabolic. The industry itself seems to have a greed problem. The unfortunate side effect is that pets will go without care, and the shelters are bursting. It’s sickening.

In my experience, the only professionals that rival Wall Street for greedy crooks are vets and dentists.

So can someone please explain why 5/10 year treasury yields dropped again today despite the 5%+ dot plot and no pivot anytime soon? What am i missing?