To get rid of ballooning inventories amid spiking cancellations & plunging sales, builders try to sell to rental operations, but they pulled back too.

By Wolf Richter for WOLF STREET.

If a homebuilder cannot sell their ballooning inventory of unsold new houses to households, at current prices and mortgage rates, amid plunging sales and soaring cancellation rates of signed contracts – topping out at 45% in the Southwest and at 38% in Texas – despite aggressive incentives such as mortgage-rate buydowns to stimulate sales and prevent cancellations, well, whom are homebuilders supposed to sell those houses to?

Rental operations? That may be hard too because many have pulled back for all the same reasons as households: Prices are too high, and financing is too costly. Sales to single-family rental investors have plunged by 32% in Q3 from a year ago. So here we go with a good-luck nod…

Lennar, the second-biggest homebuilder by market capitalization, has been approaching big rental landlords with an inventory list of about 5,000 houses, that it wants to offload, according to sources cited by Bloomberg. Many of the houses are in the Southwest and Southeast. They include entire subdivisions.

Lennar has sold about 1,000 single-family houses to rental operators in its third quarter – and some of those houses it sold to its own rental operation. Last year, Lennar obtained $1.25 billion in equity commitments from Allianz Real Estate and Centerbridge Partners for its rental division to buy rental houses.

“Our program has taken a very disciplined approach to stepping back and waiting for the market to kind of reconcile itself,” Lennar Executive Chairman Stuart Miller told analysts in September. “Contrary to what you might have thought, we’re probably selling less to our own program and more to other SFR programs outside of Lennar.”

It’s across the industry: Homebuilders have pitched at least 40,000 new houses to rental operators in recent months, Jeff Cline, an executive director at commercial real-estate advisory SVN, told Bloomberg. He said that many of these houses had originally been sold to individual buyers who then canceled the purchase contract.

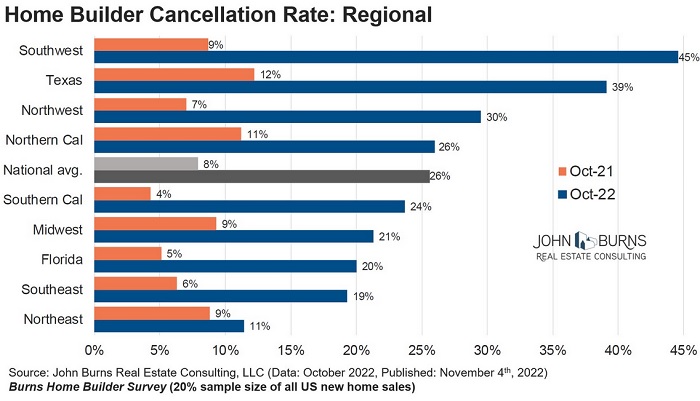

Cancellations of signed contracts with individual buyers have spiked. According to a survey by John Burns Real Estate Consulting of homebuilders that account for roughly 20% of all new home sales, the cancellation rate spiked to 26% in October, up from a rate of 8% a year ago, and up from 11% in October 2019.

The cancellation rates topped out in the Southwest at 45%, up from a cancellation rate of 9% a year ago. In Texas, the cancellation rate spiked to 39%, up from 12% a year ago (chart via Rick Palacios Jr., Director of Research at John Burns, click to enlarge):

With the median sold price of a new house currently at around $450,000, those 40,000 houses that builders are trying to offload to single-family rental operators would run around $18 billion.

But rental operators are in no mood to pay peak prices. They might bite after massive discounts – discounts that homebuilders are not nearly desperate enough yet to offer.

But they will eventually be desperate enough to offer those discounts – that’s the bet by some big investors in the process of raising funds in preparation for that moment.

Increasingly, homebuilders are trying to sell one or more subdivisions at a time, SVN’s Cline told Bloomberg.

Incentives, especially mortgage-rate buydowns, for individual buyers. Trying to sell houses one at a time to individual buyers is tough at those sky-high prices and current mortgage rates. The obvious solution would be to cut prices, but that’s like the last option for homebuilders for a variety of reasons, including financial metrics that Wall Street looks at. Incentives come first.

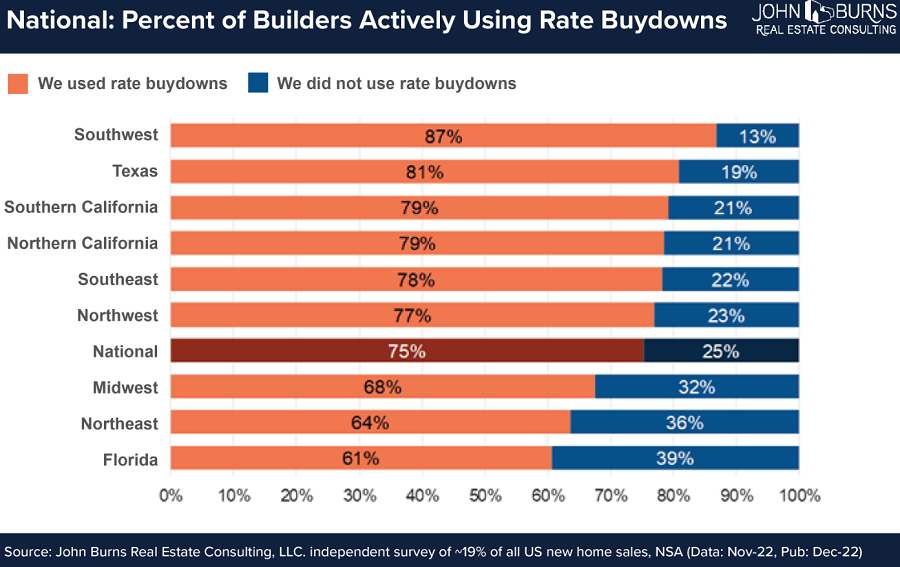

The big incentive: mortgage rate buydowns: In December, 75% of the home builders in a national survey by John Burns Real Estate Consulting said that they’re buying down mortgage rates to lower the payments for buyers. They fall into three categories of rate buydowns:

- 32% are buying down the full 30-year term. To lower the mortgage rate by 1-2 percentage points, the up-front costs for the builder amount to about 5%-6% of the sales price of the home.

- 30% are buying down the rate for only the first two years of the mortgage. To lower the rate for the first year by 2 percentage points, and for the second year by 1 percentage point, the up-front costs for the builder amount to about 2% of the sales price of the home.

- 13% are using less common buydowns.

Builders are using these incentives not only to make sales, but also to prevent or stop cancellations of sales that had already been made.

In the Southwest, 87% of the builders in the survey are buying down mortgage rates; in Texas, 81%; in Southern California, 79%; in Florida, 61% (chart via John Burns Real Estate Consulting):

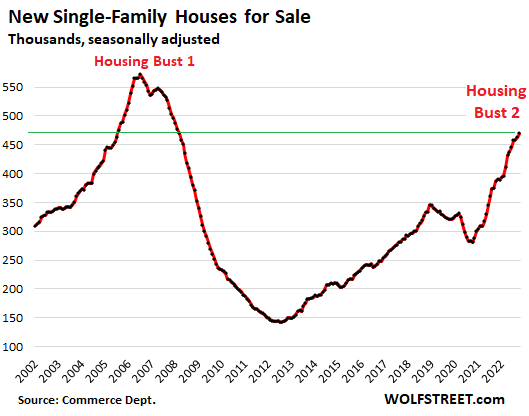

What builders are up against: Inventory of new houses for sale in all states of construction in the US has ballooned to 470,000 houses, up by 21% from the already high levels a year ago, and the highest since March 2008, and about where inventory had been during the ramp-up of Housing Bust 1 in September 2005 before it all came apart. Which destroys the theory that home prices are high because the industry isn’t building enough houses:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Lumber prices are down 72% in nine months.

Could I ask where or what market you are referring to? Source of the information? Not saying you’re wrong . . . just wondering. Any info on building materials other than lumber?

“Finviz lumber futures” is your friend.

I’ll take 1,000 of those houses – provided FED gives me 100% loan

I have been doing renovations in my places in Oregon for the last 3 or 4 years or so, and I also work as a cabinet maker and make some furniture part time. I haven’t seen a drop in lumber anywhere, just a little relief. I do wish we got some discounts… But at least it did come down from the crazy spike… For example 2x4s were about 2.50$ or so in 2019, then went up to 9$, 12$ or even 15$ each, and now they been sitting at 3.90$ or just over 4$ for the last six months… that’s probably more than a 70% crash from the peak, but the price is still way above what it used to be. And that’s just one part of an house, paint for example is about 30% more and so on

I just read this quote:

“Once inflation goes above 5%, it has never come back down without the Fed Funds Rate exceeding the CPI”

~Stanley Druckenmiller

November CPI will be coming out tomorrow. Let’s imagine a fed funds rate ABOVE that and what that means for mortgage rates and this housing bubble. She gonna blow…..

This was not meant as a nested reply, it was supposed to stand on its own at the bottom.

Truth is, at almost *any* level of CPI, the Fed Funds Rate pretty much always exceeded it, except for the past 15 years. That should be the normal state of things. Before the financial crisis, even the mighty US Govt. couldn’t borrow at a negative real rate. Now, a subprime borrower building a house on swampland in Florida can get it. That’s abnormal.

Lune,

That’s a very good point. I do wonder if there is so much debt in the system that the interest rates don’t need to get above CPI to bring down inflation like in past cycles. We’ll see. Negative real rate are definitely abnormal.

I don’t mean to dispute Druckenmiller statement, but let me point out that never in the past US consumers were do badly indebted as they are now. When levels of consumer debt are low, Federal Reserve has to raise interest rates to a very high level in order to make this debt levels painful. When levels of consumer debt are very high, Federal Reserve may only need to raise interest rates somewhat, to levels below current inflation, in order to induce great pain to debt addicted consumers. In my [admittedly economically ignorant] understanding is is Federal Reserve’s current plan of inflation fighting.

2×4 PET stud $280/Mbf $1.49/each

2×4 framing lumber. $390

3/8 plywood $16/sheet

7/16 OSB $9.60/sheet

Cedar shingles (U.S.) $400/square

Everyone on everything, looking for offers.

The Recession started in late Spring.

$16 a sheet for 3/8 plywood?

Where are you located?

Those are mill prices, not distribution centers, nor retail.

https://tradingeconomics.com/commodity/lumber

I don’t have transparent data, but as a home builder: osb was $50-55 a sheet. Now its $14. Dimensional lumber has fallen a lot too. I’d say 2x4s are half or less than what they were when we were paying $50/sheet.

50% cheaper than peak

but still $3.90 v. $2.90 in 2019 = 30% higher price

Wow!

This is the first inning of this massive down-cycle in real estate. The cycle goes…

– prices finally see year over year declines (next couple months)

– during spring and summer the number of homes for sale increases and days on market gets firmly into buyer territory

– sellers either cut prices or dont sell

– as home continue to fall 3% every month on average, buyers pull back even more and just wait it out

– home flipping businesses pull back or go bust

– equity balances start to disappear and smart owners decide to sell before their equity is wiped out

– a portion of homes finally go underwater

– recession and job losses hit

– more homes go underwater

– with prices down 35-50% foreclosures, short sales are again prevalent in the market and the final flush of the bubble is upon us.

it finally makes sense to own real estate again in 2 years, but prices are 50% lower.

Two years? Last time around it was 6 years from peak to trough (2006-2012)

Won’t happen. Your typical homeowner in the current market maybe loaded with debt from the high home price, but they are not leveraged like 2008. People were putting 20+% down in competitive markets. Not everyone bought their homes in last 2 years. People who may have overpayed have locked in low interest rates. There’s a lot more that has to go wrong this time around for someone to walk away with 30% equity in their home. Yes prices will correct and should correct. But they won’t correct 35%. There are a lot of money still sitting on the sidelines.

Fed is not going to cause 8% unemployment intentionally.

And yet I check LVL & I-Joist prices on Menards a couple times a month, and these prices haven’t dropped one red cent.

OSB subfloor & 7/16″ have dropped dramatically though.

Like everything else, nothing makes sense anymore.

Menards not very smart in their commodity buying. And very, very slow pay to the mills. Therefore retail prices usually overpriced at their stores. Like Walmart, if you like 90 day payment terms then go ahead and sell them. At a high price.

LVL and I-joists have a lot more labor involved, and LVL probably has significant non-wood materials costs.

Wolf,

Thanks much.

We’ll know homebuilders are getting desperate when they begin offering both mortgage-rate buydowns and home price cuts concurrently.

Desperate is when home builders go bankrupt.

That no longer happens. Nearly all mortgages are backed by tax payers. So all they need to do is move it off their balance sheets.

Meanwhile just searched zillow in Seattle area and could not find a single house for rent that was above 2000sft and made after 2020. Clearly the rental shit doesn’t work in Seattle as the houses are losing $25,000 per month and rent won’t be higher than $5000.

Only conforming loans correct?

And all the workers get laid off. They won’t be able to buy any of the homes they’re building.

The big home builders will not. The Government bailed them out the during HB1. The small builders are the ones who go bankrupt.

Wolf, the article said “,,,,With the median sold price of a new house currently at around $450,000, those 40,000 houses that builders are trying to offload to single-family rental operators would run around $18 billion.

But rental operators are in no mood to pay peak prices…> and “…. Lennar trying to sell…Many of the houses are in the Southwest and Southeast. They include entire subdivisions…”

Are there any reports or anecdotal stories about how big a discount is currently being offered OR expected to be offered, per…”…But they will eventually be desperate enough to offer those discounts – that’s the bet by some big investors in the process of raising funds in preparation for that moment.

Just curious at current expectations vs reality… Thanks again for this, the comparison of inventory w/ Mar 2008 is quite interesting

“Are there any reports or anecdotal stories about how big a discount is currently being offered OR expected to be offered, per”

I don’t know of any. What we have heard in earnings calls from SFR REITs is that they have pulled back because builders are still thinking they can get “March 2022” prices, and so these REITs are not buying. They didn’t say at what price they will buy again, but they’re going to wait until this shakes out.

Wolf, Can you add color to Blackstone hitting the limit on redemptions in its commercial real estate fund. I read that Asian clients comprise 70% of redemptions, although they make up only 20% of clients. Does it have anything to do with Saudi Arabia and other Gulf states agreeing to sell oil and gas to China in yuan?

I’ll add color: the idiots didn’t read the documents that specified that this non-traded REIT had redemption limits of 2% a month and 5% a quarter. Real estate is illiquid. You cannot sell a warehouse or an apartment tower from one day to the next, just because some people want to cash out. Deals take months to pull off, or longer. So the redemption limits protect the fund — and the rest of the investors — from becoming forced sellers at fire-sale prices. If you invest in a fund like this, read the friggin documents.

In addition, it looks like that these idiot investors were also greedy investors. They liked staying in the fund just fine because its value kept growing, even while publicly traded REITs were falling. They wanted to ride that baby to the top and then get out. So now they find out that they can’t get out, LOL.

That the value of these non-traded funds kept rising even while traded REITs were falling is a flashing red warning light, and it has been flashing just about all year.

I have long said that I HATE mutual funds that invest in illiquid assets, such as RE, leveraged loans, and bonds. These non-traded REITs are like mutual funds and have all the same risks. The gating provisions are there to mitigate those risks.

That’s what’s going on here. Greed is getting punished.

We have covered numerous non-traded RE funds here that were gated — and warned about these types of funds years ago!!

Idiots that don’t read the prospectus can take their fire sale to other assets- like stocks. Still waaay too much money around for any deals.

An educated guess to the discount builders will accept is the 1 minus the construction loan amount as a percent of asking price. Builders wanting to get rid of debt will price the homes to payoff the loans. The problem happens when loan outstanding exceeds price.

I have a realtor friend, and he says almost everyone getting a mortgage right now is doing this 3 / 5 / 1 loan. I believe they’re buying the load down to a lower rate for 3 years and then it resets to something like 4.5% then it goes to market after 5.

The whole selling of new homes to rental investors just smacks of how desperate some builders are not to get caught with large inventories going into next year that could be brutal.

Time will tell.

There is no accountability. It’s like when Intel reported horrible results, they talked about laying off thousands to prevent share prices from tanking. Then months later they laid of 300 employees, hoping that its all forgotten with time.

Most probably Lennar is gonna report pathetic results and is trying to rub the investors to protect shares from tanking further.

This is going to be hard to predict, because what landlords are willing to pay will also be based on they can charge for rents. If rents continue to increase fast, then they’ll be willing to pay high prices (maybe even as high as the builders currently want, if rents rise fast enough).

OTOH, if rent increases slow down or even reverse, then their willingness to pay might decrease faster than builders’ price cuts.

And a recession doesn’t always lead to lower rents. If the housing bust leads to a banking crisis leading to constriction of credit, then lots of people who could afford a house might not be able to get a mortgage and might be forced to rent. So ironically, a recession can be marked by rent increases and home price decreases at the same time, because of the constriction of credit. This happened to some extent during the last financial crisis, when you could make a ton of money buying houses on the cheap and renting them at still good rental rates, *if only* you could get the bank to lend to you, which they weren’t.

Isn’t there a huge amount of rental inventory in the form of large complexes coming to market? Here in Northern Virginia there are some pretty large ones just finishing up. What timing. On top of that, with inflation people are starting to compress together again. There was an article the other day about millennials moving back in with parents. Weak demand and new construction leads to more product on market. Sure the big corps can hold out but mom and pops will undercut them.

Get ready for the fun part of the rollercoaster!

Weeeeeeeeeeeeee!!!!!!!!!!

J Pow: I’m gonna hike rates by only 50 basis points.

Wallstreet: Start new year Pivot celebrations, push 10 year down by 50 basis points to 3%.

J Pow: See how I say QT but mean higher inflation. Even the best politicians can’t pull off such doublespeak.

For your lips to BofA’s ears: ” Global oil benchmark Brent could rebound and quickly rise past $90 per barrel on the back of a dovish pivot in the U.S. Federal Reserve’s monetary policy and a “successful” economic reopening by China, Bank of America (BofA) Global Research said.”

https://www.reuters.com/markets/commodities/brent-could-quickly-top-90bbl-fed-pivot-china-demand-recovery-bofa-2022-12-12/

Your comment is BS. “Dovish pivot”???? If that’s what the Reuters reporter said, surely they’re braindead. Maybe they’re into cryptos too, which would prove they’re braindead LOL

“Which destroys the theory that home prices are high because the industry isn’t building enough houses”

FOOD FOR THOUGHT, Maybe:

1) SINGLE FAMILY PRICES ARE GOING TO GET IN LINE WITH THE ACTUAL COSTS TO HIRE A GENERAL CONTRACTOR, BUY DIRT AND BUILD A HOME;

2) IF PRIVATE EQUITY HAS ITS WAY, MANY AMERICANS WILL BECOME INVOLUNTARY RENTERS AND OWNERS WILL RAISE RENTS TO PROFIT FROM THEIR OVERPRICED INVESTMENTS–BUILDERS CAN BREAK EVEN RATHER THAN TAKE A LOSS, BUT THAT RESETS THE LOWER PRICE FOR A HOME;

3) CITIES AND STATES MAY IMPOSE RENT CONTROLS TO COMBAT GREEDY PRIVATE EQUITY AND THEN THE BIG GUYS WILL STOP BUILDING IN RENT CONTROL AREAS;

4) RENTERS WILL WANT TO HIRE A GENERAL CONTRACTOR, BUY DIRT, AND BUILD A HOME…

5) WILL LENDERS OFFER AFFORDABLE LOANS THAT ALLOW RENTERS TO BUY DIRT, HIRE A GENERAL CONTRACTOR AND BUILD A HOME?

6) WHAT HAPPENS WHEN MANY OF THE HOMES PURCHASED FROM 2020, (MANY BY PRIVATE EQUITY) ARE UNDERWATER IN 1 YEAR?

7) DO THE BIG BUILDERS ESSENTIALLY BREAK EVEN OR TAKE A LOSS WHEN THE PRICES BECOME CLOSER TO THE ACTUAL COST OF DIRT AND CONSTRUCTION?

HOUSING BUBBLE 2 MAY BE MORE INTERESTING THAN HOUSING BUBBLE 1 BECAUSE INSTEAD OF GARBAGE MBS FLOATING AROUND, PRIVATE EQUITY AND BUILDERS HAVE OWNERSHIP OF THE ACTUAL DEFLATED GOODS AMERICANS NEED TO LIVE IN AND CANNOT AFFORD TO RENT AT DESIRED RATES.

Shhhhhhh. Try whispering.

My apologies…

U should and did,,, and i for one accept your apology.

Did not read your post because of the all caps…

But, in spite of that, please continue to add to my knowledge of your insights, but ”within” Wolf’s commenting guidelines…

And to be clear, Wolf has absolutely ”punted” some of my comments to be gone,,, and will ”likely” do so again…

Wolf’s Wonder IS ABSOLUTELY ”his” to discern, and IMHO he does such a good job that I am willing and still able and absolutely WILL continue my contributions,,, may even increase those because reading on here, Wolf’s and commenters from all over the world,,,

Have absolutely saved WE, in this case the family WE a TON, so far….

Noting that “Unamused” is not with us,,, all I can say is,

” Thanks to Wolf and ALL the ”serious” commenters…

And Merry Christmas to all y’all…

It’s funny how that became a thing; I see all-caps and I just think track lists handwritten on legal pads or Western Union telegrams — not vociferation. NOT UNLESS ITS PUNCTUATED BY SEVERAL !!!!!

“IF PRIVATE EQUITY HAS ITS WAY, MANY AMERICANS WILL BECOME INVOLUNTARY RENTERS”

It’s not private equity, it’s your government. Private equity, which includes mom & pops are trying to protect their savings from inflation.

“CITIES AND STATES MAY IMPOSE RENT CONTROLS TO COMBAT GREEDY PRIVATE EQUITY AND THEN THE BIG GUYS WILL STOP BUILDING IN RENT CONTROL AREAS”

Rent control is the single biggest reason why rents have gone sky-high in California. If you’re a landlord in California you know why this is. Why is it considered greedy to keep what you’ve earned? Do you believe in double taxation, is that what you’re saying?

Rent control has been around in California for decades. Rents only went sky high during the last few years.

LIMITED rent control has been around in A FEW CITIES in California for decades. It went state wide about three / four years ago.

David G LA,

I personally don’t believe rent control is an effective affordable housing policy, and it really only benefits a lucky few who are effectively given a type of ownership interest in the property they “rent.” After all, if you can’t or it’s difficult to evict a tenant, who owns the property?

That said, California’s statewide rent control law was largely political grandstanding. It was passed in 2019 and allows rent to be raised the lower of CPI+5% or 10% annually. In normal economic circumstances, like the ones prevailing in 2019, those thresholds should hardly ever be breached and something is very wrong if they are. Unfortunately, something is very wrong right now.

Statewide rent control in California only started a few years ago. It provides and incentive to landlords to keep rents near market. 5% base plus 5% cap on CPI compounds quickly over the years. In the past when you could adjust to market, buyers would utilize projected income while considering the in-place income.

Not true PS:

Rents in the parts of CA that I lived in from first out of Navy in ’66 in LA to last rental in Berkeley in ’70 went absolutely ballistic many years ago.

My best ever single/studio apt was $50 per month from ’68 to late ’69, now $2500,,, and most of that incredible rise was much more than ”a few years ago”…

SO sorry for young folks who are focused, as I was, to be able to ”work” repeat, work my way through college.

Seems almost impossible for anyone willing and able to do so these days, which IMHO is a shame on our current system of ”higher” education.

VintageVVet,

It’s interesting to use your rent from 1968 to demonstrate how the California statewide rent control law is largely political grandstanding. If the CPI was 3% every year since 1968, landlords could raise the rent by 8% each year. Rent increases of 8% means rent doubles roughly every 9 years and 2022 is 54 years since 1968. That means the rent could double six times over during the period. If that had happened, rent in 2022 would be $3,200. It’s a bargain at only $2,500! ;-)

Landlords (like banks) are parasites. Doesn’t matter if you are a “mom and pop” landlord or a giant property owner.

Matthew Scott

Landlords and banks are not the same, ESPECIALLY Mom n Pop landlords. They cannot simply will money into existence to purchase / maintain housing. They have to come up with their own $$$ to purchase thecasset, just like anyone else.

Rental real estate is a legitimate and viable way to take on risk and hopefully get rewarded. That does not always happen, but nothing ventured, nothing gained.

If your disdain is for any person or business which is built on a model of profit from markets, that is a different ideological discussion. I would agree with you that banks are parasites since they earn interest (profit) on assets they did not have to earn / build.

YOU might be a disgruntled tenant. People like you increase the rents, because your mentality is to screw the owner instead of living in a home and take care of it as your own. Shame on you.

Doomz,

Would you give up prop 13 for rent control to go away?

the biggest reason for high California real estate prices is Prop 13, which limits property tax increases, otherwise, the owners would be forced to sell to pay for the property taxes.

Prop 13 is actually a bad law when you look at the long term effects. Government should be collecting the same property for the same home value from all residents, rather than just from the new residents to an area.

The government needs to stop picking winners and losers.

Rent control is very bad and has pushed rent up, but restrictions on housing construction are very bad and themselves probably beget rent control

We are mom and pop investors. We were sitting on the sidelines with some money we would prefer to invest but not at today’s housing prices. However, just this week, we decided to take the plunge on LOW offer prices, as in 2019 prices or better. We will be making an offer tomorrow and plan to make another offer, both 60K under houses that have already dropped their price 40-60K, in popular resort town locations. We’ll see how that goes. The house on which we will place an offer tomorrow has 6 other offers (because the listing agent urged the seller to list a house at 100K in an area where you haven’t been able to find a house for the 300K in a LONG time). It’s in rough shape but has good bones and a very nice lot in a decent neighborhood. Despite the other offers, we will not go much higher. The other one is sitting without any bc the seller, despite being “MOTIVATED,” still hasn’t accepted the new reality. He or she has already dropped the price from 240K to 200K and still can’t get any offers. So we will be offering (and holding) probably at 140K.

So we think it’s worth giving that low ball offer here and there (or searching for that rare estate sale deal, which is what both of these are). Some people will bite. Sellers need to learn the new numbers. And transactions, if they happen, will adjust the values.

When we look at houses, we are looking at 2019 values. And that’s about what we plan to offer.

We still might be making mistakes buying right now, even at what seem like fantastic prices. But that’s impossible to know.

Oh I should say these are in different states. The 100K house still has no other houses below 300K in the area. And most are above 600K although larger.

Bottom line: we think it’s okay to buy as long as you hold strong on very low prices even in multiple offer situations. Our only question is whether we are still paying too much, which we might be.

Why the need to buy houses now, when prices are falling fast, and Spring selling season is shaping up to be a disaster?

Granted, it may be difficult to lose much money on the homes you are trying to purchase given the low prices and opportunities to increase price via improvements and sweat equity.

@Tina W.

I am using the logic in our target market. Prices are still 30% to 40% above the 2019 levels. The target market is very good value in my opinion and is attracting cash buyers from blue cities and states. Just sitting on our hands for now and planning another research trip early next year to checkout a couple of other communities.

ONE word FOMO 🤣🤣🤣

Impossible to know what is going to happen, but you seem to be buying at a price that is a major decline. What is interesting to me is that your new really low home price will become the new comp in the area. And that is happening everywhere. The seller willing to take the lowest price and close a deal becomes the comp that is the comparison for the future. Then the future sellers have to deal with the new set of low comps and buyers who want a price better than your deal.

I’m not sure 2019 prices will be good enough. I think 2014 prices are the target in 2 years from now.

MORE like 2010

I wouldn’t give a flying phuk if you are writing in all caps, cursive, or lowercase letters. You are not in my face yelling 1ft away from me so it doesn’t matter. Tooo many sensitive people acting like ALL CAPS bothers them lol. Get a life! As long as I can read it and can follow your logic- that’s all that matters. Stop making mountains out of mole hills

Plenty of garbage MBS on Fed’s balance sheet. These morons were buying in the billions a month well into the bubble, then wonder why housing to the moon?

“Garbage MBS?” All MBS that the Fed bought are guaranteed by the taxpayer via Fannie Mae, Freddie Mac, Ginnie Mae, etc.

In practice, that reads like another “Deferred Asset” in the making.

“3) CITIES AND STATES MAY IMPOSE RENT CONTROLS TO COMBAT GREEDY PRIVATE EQUITY AND THEN THE BIG GUYS WILL STOP BUILDING IN RENT CONTROL AREAS;”

The most populous city in NC recently changed zoning rules to allow for new duplex and triplex structures, and even quadraplexes in some instances, on previously SFH postage stamp lots. Rent controls city wide would be wildly opposed by landlords and perhaps even unconstitutional so the goal instead is to cram as many people into as small a space as possible and then label it “affordable housing”.

…and that’s what works. Lots of people are fine with that, and rightly so. Minneapolis did this and it was wildly successful and only scratches the surface of what’s possible.

Dense cities are more interesting. I think this is a good move.

My eyes thank u

Builders will want to unload at a 25%.discount and avoid the uncertainty of next year. I would think private equity buyer would bite given rental rates, where else can they make those returns.

What if there’s just so much money stuffed in so many peoples pockets who got big-time lucky before the music stopped that petit details like price corrections or being trapped underwater just won’t matter that much? America is suffused in cash. $3500 a month mortgage? Easy Street. $150K Fords? Why, sure!

And even if you didn’t somehow manage to dip your cup in any of the myriad magical punch bowls this past decade, then you’re still job hopping & getting 20-50% pay raises each time.

Everything’s gonna be fine.

Cool. Get ready for 20% mortgage rates then.

I think bulfinch has a point.

But as to asset prices, fear and greed are both strong motivations.

As a person myself on the sidelines – did not grift through PPP, etc., and avoided speculative assets – it does cause angst.

He has an excellent point. This quote alone-

“But they will eventually be desperate enough to offer those discounts – that’s the bet by some big investors in the process of raising funds in preparation for that moment.”

supports it well. I keep hearing from so many people that they are waiting. Well if so many people including investors are flush with cash just waiting to pounce on a decline, you can bet that decline won’t last. Same thing for pent up demand for cars.

Add to that if the fed slows down rate hikes then I think you will see a very small decline and with a quick reversal to the upside.

Yes and no. I get what you’re saying, but people are irrational. All those people “waiting on the sidelines flush with cash” are all assuming a recession won’t affect them. Say you have $100k in stocks “waiting to invest” in real estate. What happens when stocks tank and you only have $50k?

Or let’s say you’re “conservative” and your 100k is in the bank. What happens when the recession comes and you lose your job? All of a sudden, all that cash you were flush with is no longer available for investments.

People underestimate the carnage that a real recession — nevermind a depression — can inflict, and they always assume it won’t affect them. Just like people who think real estate declines only happen in other locations and somehow their town is special.

On a macroeconomic scale, the Fed is withdrawing $100bil in excess cash from the market every month. That money is coming from somewhere. By definition, that means that every month there is $100bil less cash sitting in investors’ pockets waiting to pounce on a decline.

Until we get to a point where there are plenty of bargains that are going begging because people simply don’t have the money to buy even at firesale prices (like we got to in 2007/08), we’re unlikely to be at the bottom of this particular cycle.

As long as there are investors “flush with cash” waiting to pounce on falling knives, the Fed will continue squeezing excess money out of the system.

His post has to be intentional exaggeration.

$3500 a month mortgage means total occupancy costs of about $4500. That’s mostly with after-tax money, due to the SALT limit and high standard deduction.

Many prospective buyers (but nowhere near most) have substantial equity, but if they don’t, less than 10% of the population can afford it and there aren’t anywhere near enough people getting sufficient raises to change the math.

No different on car payments.

Hey – exaggeration is the order of the day.

The goalposts have been moving since ~ 2000 at a rate which suggests the playing field is composed of greased banana peels. This has had the effect of shifting popular mindsets as to what healthy or “normal’ baselines are when it comes to the prices of goods and services. Perceptions have become skewed. If you only ever ate lunch in airports, you might become inured to paying 15 dollars for a bottle of water. In fact, you might be perturbed or become wary at the idea of paying anything much under that. It’s the same thing coming of age in the everything bubble.

In addition, enough young Americans seem to have been either shrewd, savvy or just plain lucky enough to keep pace with the madness this time around vs 2008. Look at the numbers. Now, maybe the house always wins in the end, but for now at least, it’s the roaring 20’s and the nouveau riche are palliating their pandemic doldrums with pent-up consumption, seizing the late afternoon after having their morning stolen from them.

I’ve looked at the numbers, the numbers for median net worth and median household income for the 21st century reported by FRED.

Neither this data nor any other paints a “Miss Rosy Scenario”, the famous dame from the 80’s.

The Fed is determined to make “excessive savings” evaporate, and kill the job market. They will make it go down no matter how much despair they cause in the process.

Meet the new boss, same as the old boss.

I think they are determined to make excessive spending disappear.

6.8% Ibond and 4.8% short term TBill yields are tempting savers to save.

10-90% losses in other investments are discouraging savers to speculate.

Cushy jobs with high pay may have to disappear to make this happen.

Bitcoin Dogcoin and any stupid e_coin or Robin hood ground comes to mind. 🤣😂😂

It’s only been maybe 8 months since the real estate peak, not even a year from the stock peak (if it has). Everyone, investors and the general public, is expecting things to work just like they did the last time things dipped. It’s Pavlov’s dogs doing what they’re conditioned to do.

But this downturn is most likely NOT like what the’ve been conditioned on. The “bottom” of this downturn will only be the first bottom of several larger swings. It’s going to take time to break habits, and it will take PAIN to break the conditioning that things will just rebound.

We’ve had nowhere near enough time, and basically no pain at all thus far. That will change.

Bulfinch–

I do it so: 1) I can recognize MY messages quickly and; 2) when I hit “all caps” I dont run the risk of accidentally hitting “all caps” with my pinky mid-stream and putting words “out of proper case”, before I see what I have written. It’s more efficient for me than punctuating–especially, where there are many proper nouns and places involved. The ALL CAPS Is not done out of disrespect or for emphasis, in any manner. As I always say, its better to “satisfy the least sophisticated consumer” than assume they know or should know what you mean…. so, I will simply comply and ditch the “all caps”, lest I offend those who respect and cherish social media protocols or are simply letting me know some may find “all caps” offensive. I prefer not to offend, which is a very slight inconvenience to my habits and customs.

It’s just a bad reader experience. Look it up. Here’s a start: https://uxdworld.com/2017/12/30/all-caps-on-ui-good-or-bad/

You are not offending ME… I could care less. I don’t know you at all and there is no reason that you would be yelling at ME. So it cannot be personal.

But I will say that I simply skipped over your post rather than read it. The ALL CAPS formula eliminates so much White Space that it is simply much more difficult for my older eyes to read.

I skim over or just plain skip all caps posts in any forum. I only went back to read it after seeing the reply responses.

It’s nothing personal, but it just screams spam, lack of education or obliviousness to written social norms where actual discourse is expected.

Now your explanation and the content of your post proves that you’re an outlier, because you’ve demonstrated none of these negative qualities.

I can’t speak for others, but I’ll still be in the habit of glossing over these posts. It’s not you, it’s me. Most of the all caps content out there is worthless and my brain is conditioned to filter it out in the interest of efficiency.

Nathan, the reasons you give for doing all caps are for your own convenience. However, you are writing to communicate with OTHERS. All caps are disliked by OTHERS for various reasons, therefore using them makes your message less effective at best, completely ignored at worst.

Thank you Ted. This is the same when I explain to people to minimize the use of acronyms. Acronyms are for you. They are easier to write. But they make it harder to read. Your comment reflects well why Nathan should avoid using all caps for his own convenience, because it makes his post(s) unintelligible to his readership. I flat out skipped it. I don’t think I’ve ever read a post in all caps. Easy litmus test.

I can handle the caps lock, but I always skip over posts that contain ‘its not you, it’s me’ because I just assume I’m being broken up with again ;)

Just rolls off my shoulders like transitory these days

Whether or intentional or not, all caps is in fact a lack of respect for your readers. All the reasons you have given are focused on yourself on not for your readers.

Like the others I just skip over those postings. If you can’t put the effort into writing in a normal fashion that is easy to read, then I am certainly not going to put any effort into reading.

@Nathan,

Don’t worry about it, you’re not breaking any of Wolf’s posting rules. I didn’t even notice the CAPS until it was pointed out. My wife says I’m not very observant, yes she is right… again!

It doesn’t fuss me, Nathan. We’re suggested that it should, but unless it’s italicized or accompanied by !!!!

CHINASKI!!!

I don’t feel one way or the other. Again, it just reads as more of a mechanized dispatch to me, a la, a headline ticker or a telegram.

Canaries in the coal mine?

“– 32% are buying down the full 30-year term. To lower the mortgage rate by 1-2 percentage points, the up-front costs for the builder amount to about 5%-6% of the sales price of the home.

“– 30% are buying down the rate for only the first two years of the mortgage. To lower the rate for the first year by 2 percentage points, and for the second year by 1 percentage point, the up-front costs for the builder amount to about 2% of the sales price of the home.”

Something doesn’t seem right here — how can 2 per cent off in year one and 1 per cent off in year two cost the builder more than a third of what it would cost him to give 1-2 per cent off for the whole 30 years of a mortgage?

A bit of playing around on Zillow makes me think that 1-2 per cent off a 30-year mortgage equates to 8-16 per cent off the price, assuming current interest rates of about 6 per cent and a deposit of 20% of the original asking price. But I could be wrong…

I noted this too, but didn’t really care to do the math. My BS/screwjob filter always assumes that these games, in any industry, have two goals:

1. To appeal to your lizard brain, which these days means the monthly payment.

2. To back door as much profit as possible at your expense, without you realizing it, because you won’t do the math either despite your money being on the line.

Cynical? Yes. Been in business far too long in this country to trust anybody whose job is selling you something that relies on financing.

I agree. I just can’t believe how many people blindly accept that most are signing away any chance of actually owning that house outright before 30 years have passed, especially well before. No way man! You can’t have my freedom!!

Or fine print.

Math is hard – mmkay…

It’s worse than that. For the same monthly payment, I’d rather do the opposite: record a lower purchase price, and pay a higher mortgage rate. For 2 reasons. First, your property taxes are based on your official sale price. Inflating your purchase price by 10% above what you actually paid for it just means you’ll be paying 10% more in property taxes for many years. Secondly, if you plan to make some early payments on your mortgage, you’re saving a higher proportion of interest (i.e. making early payments saves you more money when your mortgage rate is higher).

On balance, the only benefit of paying a higher purchase price is that that lowers your capital gain when you ultimately sell. But if this is your primary residence, federal tax law allows you to defer most of your capital gains anyway, so this doesn’t really help much.

Property tax is based on the value the appraisal company assigns when they do the appraisal for the assessor. This from Wikipedia explains it:

“The appraised value of your home represents the home’s fair market value (what a buyer might expect to pay if you listed your house for sale on the market), while its assessed value is used to determine property taxes (which increase the larger that your assessed value becomes).”

I can only speak for New England, but wiki is wrong here.

In this region your assessed value is set by a town employee, the assessor, who should do his or her own work, but usually uses an outside company to provide valuations periodically based on market data.

The appraiser in a sale works for the bank.

Now in theory, home valuations are set based on Fair Market Value. But everyone who pays attention knows that when a sale happens that property, more often than not, triggers a review in the assessor’s office which somehow adjusts the sale price of that home, and that home only, to the new appropriate valuation. Longstanding residents with similar homes have valuations that lag far behind.

So in New England, when you buy a new equivalent home, you can expect a big property tax increase.

I’ve long argued that this is a sh%tty system because it frequently results in a buyers surprise. A realtor gets to list the house with $4,000 in property taxes because that is what the old owner paid for a decade, a new buyer purchases it and ends up with an $8,000 bill that they don’t understand the next year. It inflates sales prices in favor of the seller and realtors, of course since the PITI calculations only figure in the old taxes.

The other downside of this system is that there are a lot of way undervalued homes and their services are essentially subsidized by modestly priced homes. The nonprofit URBAN3 has done a lot of analysis proving this point.

Property taxes increased 10-30% in Omaha ne don’t move here ,I want to move but family,grandkids keep us here . Told my kids we will all end up living in one house,they laughed at me now there property tax increases are biting them in the ass .My daughter built new house 400k = taxes of 12 k unsustainable

Technically, you’re right. But how do you think an appraiser figures out your value? A private market sale (i.e. not a foreclosure or something) is the absolute biggest and most solid evidence to base an appraisal / comps on.

So if you bought your house for $500k, your town will almost assuredly set your appraised value at $500k. You can of course file an appeal on that appraisal, arguing that the house is actually only worth $450k, but good luck winning that appeal if you willingly paid $500k for it just a month ago.

OTOH, if you bought it for $450k, the town’s assessor will be hard-pressed to set the value at $500k, and it would be much easier for you to appeal, since the seller willingly sold it to you for $450k.

So in theory, you’re right. But in practice, I agree with Digger Dave: your purchase price has the biggest influence, by far, of any factor on your appraisal (and sometimes resets your neighbors’ appraisals too, much to their chagrin :-). Which is why it makes financial sense to keep it as low as possible.

Ideally you want interest rates as high as possible to push down the price of homes. Then you pay cash and it lowers your income tax. Usually the best time to buy a home is when interest rates peak or shortly after.

In Cook County IL, when assessed value drop, they adjust modifier to make up for drop.in assessed value and drop in biz taxes, tourism and licensing. A version of this must be common; its not like a municipality can pay services, debt and other steady costs and not make up for drop in assessed value.

It’s sad but there’s not really a middle, you have to crush it and be smart in how you deploy income or you’re relegated to some degree.of financial distress or have rich boomers parents to save your situation, if you live in some.proximity to a metro area.

The average mortgage only lasts, on average, around 6 years due to sale or refi. So buying down only 2 years basically is buying down 1/3rd of the expected life of the loan.

Part of the reason that the cost to subsidize 30 years, is proportionally less than the cost to subsidize a few years, is because the average real maturity of a 30 year mortgage, is well under 30 years.

In other words, people sell, refinance, etc., before 30 years.

Thanks to you and Brian for the explanation. If the average 30 year mortgage only lasts 6 years, that would certainly cut the builder’s costs of subsidising it by a large amount.

However, one wonders if such mortgages will be terminating so quickly in future. If I buy a house now and the builder effectively gives me a mortgage at 4 per cent instead of the current market rate of 6 per cent, then I have a big incentive to stay in that house until (a) I have made a profit and (b) mortgage rates are back under 4 per cent. The way house prices and interest rates are going these days, that could be a long time coming.

The interest rate buy down impacts the amount of the interest payment, not the principal of the loan. As the loan amortizes, the amount that goes towards principal increases and the amount going toward the interest is reduced. A buy down is nothing more than prepaid interest. Hence, buying down for 30 years is less costly on a per year basis than the 2 year when you consider the amount of the payment going towards the interest is declining over time.

Hopefully, that makes sense.

“In other words, people sell, refinance, etc., before 30 years.”

Not sure that is still true with so many homeowners with 3% 30year fixed loans.

I predict sales of existing will be down for many years.

Definitely motive to talk, “Fed will pivot and Fed is trapped.”

Hi Wolf! Ryan Homes has started the first spec home development in my town of about 20,000 to be built in many many years. They started out pricing homes in the $240’s and are now in the $190’s. The homes do not seem to be selling. They have about 16 up at this point and maybe 2 – 3 have sold. There is a new EV battery-related manufacturing company supposed to open in our community next year that will require a lot of workers but they haven’t really even broken ground yet so I am not sure what is going on there.

Without knowing where those homes are and what the market prices are on comparable properties, it’s difficult to say.

The advertised price variance could be the result of removing content from the original spec and now everything is an additional cost “upgrade”. With the HGTV image of home ownership, most people don’t want builder’s grade anything and, by the time they make it what they want, the cost exceeds the original $240K price for the same final product.

Homes in the low 200s?

Maybe the Midwest somewhere far from a major city.

190k has to be close to building and land acquisition cost for even a modest house.

Sounds like location could be Clarksville TN to me.

EV manufacturer, Like Jeeps in Illinois, may be going south for cheaper

costs & energy.

Todd, check the quality or rating of the school district these homes are being built in. Schools = good indicator of the desirability of the house going forward.

Thanks for the local color, Todd!

Home prices are driven by building costs.

They are also driven by salaries of buyers in areas who have more money to spend. This typically means a high demand for workers and a higher demand for houses in that area.

They are also driven by the desirability of the area. (ie is it a resort town desired by tourists?)

If an area does not have a high salary demand or isn’t a tourist destination, I believe the price of homes reverts to the building cost.

The WFH during the pandemic distorted this. Everyone can move back home to their quaint hometown anywhere in the US while being able to bid up housing prices with high remote salaries.

Retirees can also do this if they move to Phoenix, Florida, or anywhere.

Retirees may be a little different since they generally want to be close to doctors and medical centers instead of paying an extremely low price in the middle of nowhere.

If prices were based upon costs, builders would never lose money. Most of the time they don’t, but prices are still not determined by cost.

True, there are fire sales. I don’t think we are there yet.

A builder wouldn’t build unless they can show a profit over building costs. That is capitalism.

Building costs can be extremely low in some areas that have low cost housing.

Construction labor does not demand a premium when the demand is low and the cost of living is also low.

An example is a retired contractor living in a low cost area with a paid-off house and labor willing to work to make a few extra bucks. I have lived in one of these areas. You can find some relatively low priced competent handymen who do not charge you an extreme rate. If the demand for building rises, these people will raise their rates and buy steak instead of hamburger. Nothing wrong with that. They are in demand.

It’s not just fire sales. It’s math.

If buyers don’t have the money and/or can’t qualify, they don’t buy. Nothing complicated about it.

Housing being a necessity doesn’t negate math, something I read in comments here regularly.

The belief behind this premise is based upon the concurrent belief that every American adult or household gets to live in their own housing unit, more or less.

No, they don’t, because US society isn’t exempt from math, even though most Americans seem to think so.

Just some thoughts on developers selling single family homes to the big rental companies. The entire subdivision being sold as a rental community is different than selling a percentage of the homes in a community to the big landlords.

As a buyer, I would never buy from a developer selling to big landlords and families. The big landlords will never invest heavily in their properties or improve them beyond the lowest requirement. The overall investment value of all the homes in the community is diminished by the presence of the big landlords. I’m taking into consideration the transience of renters who typically are only offered one year leases. I would run like hell from these communities and steer clear of these builders.

I lived in Florida during the GFC and got to see the rise of the big landlords up close. It was not pretty. The political ramifications in these areas are real as well. The big landlords will exercise influence over local politicians, HOAs, school boards, and services. In my opinion, the big landlords lower the overall value of any community.

Good advice, Petunia. Also the upkeep of the community is doubtful if there are too many renters.

Housing prices peaked in June. Wages are rising. Mortgage rates have risen 100% or more in the past 52 weeks (Mortgage News Daily).

Wages are rising? I beg to differ. Maybe *some demographic wages are rising, but not for 30-60 year olds. Not in California.

As reported in the Twin Cities 3 December:

“This spring, there was more work than many companies could handle, but a shortage of labor and materials. Within months, interest rates doubled and home building plunged.

Jon Ryan is president and owner of Genz-Ryan, a market-leading HVAC company founded more than 70 years ago by his father. For years, the company’s bread and butter was installing furnaces and air conditioners in new houses.

Not anymore. He recently shuttered the new-construction division of Genz-Ryan, wiping out the work of 40 people. The company will focus on service and installations.

“It’s been like trying to turn the Titanic,” he said. “Only about one-third of what you can see is above water. It’s what you can’t see that worries me.”

After a pandemic-fueled building boom that left builders and their subcontractors overwhelmed and exhausted, a sudden contraction is shaping the industry.”

The decision to close the new-construction division was not something Ryan wanted to do. He called it a “gut punch.’ But he added that it’s the right decision given the ongoing challenges facing the industry.

“It was really about rising interest rates;that changed everything. The study of economics is the science of trying to satisfy unlimited wants with limited resources,” Ryan said. “This really came down to a handful of decisions.”

A nice note on the 40 employees: some were reassigned within the company, and many others quickly found new jobs.

In other news, Mr. Ryan now is wanted on a charge of torturing two different metaphors almost to death

🤣

speck of sand on the real estate story- selling lake home in northern wisconsin- bought in 1987 for $89,000 – was a second home – over the years we kept moving south – time to sell ?- well we spoke to a realtor we know and she suggested listing it for $399,000 – never got to MLS- sold for $414,500 bidding war between 3 people 1 from mpls and 2 from chicago –

Thanks for the self boosting, very helpful to the conversation. Let me give you a pat on the back. Good job :-)

Now tell us about that vein of gold you hit while backpacking.

Huh? I thought he was complaining….that’s only a 4.02% annual return. worse than CDs over that period, and, what, less than half the SP500 return? And that’s before factoring in cost of ownership.

You guys are so insensitive. I’d say a more appropriate response to him is “Sorry for you loss”….

I grew up in a family of small homebuilders. Our busiest year was something like 30 homes built and sold, because my grandfather refused to borrow a lot of money to lever bigger projects. That kept us from getting really rich like some of the others we knew, and in 1982-4, that kept us from going bankrupt like some of the others we knew.

For a handful of homes that simply wouldn’t sell after over 2 years of trying, we leased them. It worked out very well, in the end, as they were able to work down the small loans against them, and quickly build equity when the market inched back, then roared back.

There are also big tax benefits to landlording. You can be cash-flow positive almost immediately (if you haven’t borrowed heavily) and the federal taxes are low because of amortization of the building. (Property taxes shoot way up, though, because there’s no homestead exemption.)

But you can’t put the genie back in–if you sell the home, all that accumulated depreciation comes crashing back as taxable income. So hope you plan on being a landlord for a long, long time. And dad and his brothers found out that landlording is another full-time job, in addition to building.

Still very, very glad they did it. It build a good foundation for the family that we still enjoy today. But it was never easy money. Mind you too, this was in a family of people who know how to build and repair things.

And if a landlord dies and his children inherit the property–all the amortization tables start at 0 again–good news for my brother and me. Don’t know though how it works for a public company like Lennar? I guess if the corporation lasts forever, the depreciation benefits go away at 22.5 years, and are gone forever?

The cost basis on which a residential home is depreciated is stepped-up under the estate tax following the death of the owner. The logic being that the property was subject to estate taxes as part of the deceased owner’s estate. You’re correct, since a corporation can’t die, the cost basis of property owned by a corporation will never get a step-up under the estate tax. Correspondingly, the property will never be subject to the estate tax. The depreciation term for residential homes is 27.5 years.

2 points here.

Yes, a primary home is a long term investment. If you die in your home, your heirs inherit tremendous tax benefits with a stepped up basis.

Since the Supreme Court ruled that Corporations are people, why can’t they die like the rest of us?

Ah, but the SC has ruled corporations are “people” for limited purposes, such as making political donations. The SC has not altered the definition of a corporation under the Internal Revenue Code. Being immortal, corporations are a very special type of “person” that is not subject to the estate tax or its step-up in basis.

They die all the time, like FTX, it’s called bankruptcy

Mr. Wolf,

Any idea how bad this could be? Just going back to 2019 pricing is what a 30% price cut nationally? Are we looking at pre-2019 pricing? Maybe 2012 pricing, and a ~50% cut? Worse?

Is there any way to qualify how low this might go? I can’t even find a way to draw a historical analogy or metric that might describe where this might end up.

The big change between the current SFR market and prior markets is the influence of corporate buyers and RIETs. Based upon affordability of average income Americans, prices should come down 30%, or more, the question becomes if the corporate buyers will peg the market in an attempt to prevent a significant price decline.

The last two years house prices have gone up 45%, 20-22. Never, ever, ever happened before!

History tells me how this will unfold over time having experienced several housing downturns. Especially oil boom towns in Houston Tulsa Denver OKC and Midland. I have moved 13 times in 40 years of oilfield work and bought and sold both new and used homes during that period with interest rates starting at 18 percent culminating with rates at less than 3 percent. Home prices are very much dependent on income levels of renters and Mtg rates and population growth of wage earners . Because during these periods of price declines other areas of the country experienced rising prices . The nation thrived on cheap energy for decades and the economic growth driven by the global economy that was concentrated in the USA and the two coasts. Demographics high energy costs and a lack of demand will drive the prices down for new homes that compete with empty existing homes that Wolf mentions is not accounted

for in inventory. Bubble i think is is bigger than the previous bubble and we did not have the inflation issue to deal with or demographics. The drop I think will be larger but will be slow and painful.

At least in Florida, mortgage rates are now only PART of the ordeal. Insurance rates are out of control. For many people, that cost has doubled. So add that to the much higher costs that Lennar’s buyers are suddenly facing….

In FL, the problem is roofing fraud. There are lots of fly-by-night roofers knocking on doors and doing unnecessary roof jobs. They’ll find one shingle that has a pea spot on it, then use that as justification to redo the entire roof. That happens all over the country, to a lesser extent.

Anytime there is hurricane or hail, you can count on roofers to be out in full force, scamming the insurance system.

It gets to the point where home owners want a new roof just to avoid being the mark.

Florida is the poster child for global warming. Things will only get worse from now on.

When the northern states heat up, all those who moved to Florida will return to their roots and buy a cheap house and insurance. Florida will go back to being a swamp again!

People are still paying tens and even hundreds of millions for waterfront property in southeast Florida, Fisher Island is the wealthiest zip code in the US, climate change isn’t meaningful in any way as long as the smart money is pouring into those places. And it still is.

In think in some ways, roofing fraud is endemic.

So many roofers look for hail damage which covers most of the US.

I expect insurers will stop insuring hail damage in policies for houses and cars.

This honestly sounds like an issue that requires a technological solution. We just need vastly more durable roofs. Perhaps easier to fix too.

Interesting roofing story but yes everyone on my street has new roof and my insurance company does not cover any roof older than 15 years . My roof is 15 years old .

Yes, as Wolf Richter has documented, we can expect property values to drop in the next two years in all areas in the United States. In many areas of coastal Florida, the hurricane insurance will be as bad as increased mortgage rates to hasten the decline for those not paying cash. NOAA is expecting 4 to 8 inches of Gulf Coast sea level rise in the next 30 years; they expect a foot of rise on the Atlantic Ocean. (Of course, I would have gotten this wrong a a multiple choice exam, thinking that all large bodies of water tied to the oceans would rise at the same).

I live in the Coachella Valley and the price of SFR and condos has gone crazy over the past 3 years. Nice middle-class SFRs that sold for around $350,000 in 2019 (pre pandemic) were selling for $700,000+ this past spring. Back in the spring most new listings sold within a week or so. Things have changed remarkably over the past couple of months, now there are lots of listings on market for 50 days, 70 days, etc. Not only are the DOMs increasing but around 25% of the listings have price reductions, some of up to $100,000 – and they are still overpriced compared just 3 years ago.

If it is this bad for the big builders with new houses, I bet the flippers are being taken to the woodshed.

Why are builders not going hat in hand to the Chinese or Japanese or George Bush’s second family; the Arabs? Prostituting the country for a few bucks never bothered any of these low lifes like the politicians, realtors, NBA etc. Heck lets sell the “freedom towers” to a Chinese company and put 笨蛋 on them in bright red neon sign.

Unironically a good idea. Foreign investment is always good.

Wolf, what are your thoughts on the new legislation being proposed to block hedge funds from buying single family homes? In many metro areas they bought up to 40% of available homes driving up prices for homebuyers.

” new legislation being proposed to block hedge funds from buying single family homes”

What ? And end the Fed-funded vulture capitalism that predates almost every aspect of our society?

You must be a terrorist , ha

I know from where I live the problem is when the Chinese start buying up homes because the price is completely irrelevant to them. So far the hedge funds haven’t tried to turn housing prices into a ponzi like the Chinese do by paying more and more with each passing day.

LOL. Not driving up prices now, gonna taka a loss on this stuff. Fine with me. Let them blow up.

Disgraceful. A complete violation of individual rights.

In Utah the way the calculate inventory deficit is so flawed, few ever read the actual report, especially the realtors who are always screaming about no inventory. In Utah, anyone that is over the age of 18, under the age of 65, and is not incarcerated, is counted as demand for inventory. What?? Meanwhile everyone ignores the institutional buyers and iBuyers, realtors be like, “who?”

Nobody here is even remotely considering the idea that this may be a great time to buy and that we might be close to a temporary bottom. And that we might have another wave up in real estate in the next year or two.

If we don’t get that hard landing and massive job loss, nobody is forced to sell, especially with low mortgage rates locked in.

So everyone sitting on the sidelines waiting for “the crash” to buy on the cheap may be caught chasing the market up again if that crash does not occur. Especially if interest rates moderate next year.

Neil,

Read the article, for crying out loud, before posting this ridiculous BS. Are you like a badly-coded RE promo bot???

Prices are NOT cheap — that’s the WHOLE PROBLEM pointed out in the article. Homebuilders are buying down mortgage rates instead of lowering prices. Investors stopped buying because homebuilders are clinging to their March 2022 prices. Buyers are cancelling the purchase contracts they already signed because now they realize the overpaid, given the higher mortgage rates.

Your kind of BS is just exasperating.

Maybe Neil is a realtor.

Pure wisdom dispensed daily. Tolerance for dissent, but intolerance for misinformation. Neil may be fantasizing about his holdings, not uncommon before a major crash, in my humble experience, as the majority get wiped out. We are staring over the edge of a cliff of a monster drop and the only way out is to sell now.

Truly a contrarian bet on housing. Contrary to reason, unfortunately.

Your comment is not so good …

I’m sorry.

Think about what you wrote and try to give us something better:)

Neil, I have some friends with your perspective. They are not dumb people and I’m sure you are not as well. I don’t think you are thinking this through, though. My ask of them will be the same as my ask to you: take a look at the mortgage payments for a typical home that sold about a year ago. Now take that same price and just use today’s rate.

Now, multiply that last number by about 3. This is the monthly income required by anyone with decent credit to purchase that home. Is this realistic in your area?

Here is an example:

Home sold in October 2021 for 1.1m. Assuming 20% down, the payment with the interest rate at the time was $5,500 per month (requires a monthly income of about $16,500/month, about $200k/year).

If the same home were to be purchased today at the same price, the payment would be $7,300 (requires a monthly income of $21,900, about 260k/year).

In my area, $200k it roughly 80% higher than the median family income. But with 2 working incomes its not all that uncommon (2 jobs at $100k each). $260k, on the other hand, is rare – and that would be the MINIMUM required to purchase a home.

The point is, housing markets are not financial markets (though lately sometimes they act that way). FOMO has a limit in housing markets. People actually have to qualify to buy something – it’s not just a click of a button like buying a stock or crypto. It’s tethered to reality.

So for your thesis to be true and prices to begin going to the moon again, there needs to be enough energy to create that FOMO again in the housing market AND there needs to be enough cushion in incomes for the qualifications to happen.

While rates may go down over the next year, we are not returning to the world in which these prices were driven so high. The global dynamics are different. And in my opinion, the dip in rates we may encounter next year will be the bear market bounce as they ultimately head into double digits.

@Here

Well-presented and written!!

You’re confusing him with logic.

I’ve run these “X sold for this much and payment is _ _ _” examples on here before. It seems most people just refuse to admit reality or do not have the attention span necessary to understand basic math. Either way, well done.

Being locked into a 30 year mortgage at 3% seems like a great deal at first blush, but I think it could be a Trojan horse. It never makes sense to buy an asset that has high likelihood of price decline, no matter what your finance rate is. The low interest rate could influence some homeowners to hold tight, rather than sell, as big gains evaporate.

Home prices are going down at a rate of 1% per month right now in cities where prices rose earlier. That’s a huge trend that many homeowners refuse to respect at this time.

Amazing fixed rate of 4.50% (4.547% APR)¹ OR 7/6 ARM rate of 3.875% (5.376% APR)²

² This 7/6 adjustable rate remains fixed at 3.875% (5.376% APR) for the first SEVEN years of your loan. Starting in year EIGHT, the rate can adjust every six months based on index changes. ¹,² Offer available when you sign a purchase agreement on a select move-in ready home in the greater Southeast Colorado area between 12/06/22 – 12/31/22 and close by 01/31/23. Offer requires qualification for rate and financing through Lennar Mortgage, LLC

In my opinion “Mortgage-rate buydowns” are fraud and should be illegal.

MRB exists for builders to pretend that they did not give a discount on the price, to maintain the fiction of a higher price.

Both homebuyers and builder investors are mislead.

Not to mention. . .a bit of an elephant in the room as of the last 20+ years. Intermediation. It seems shenanigans such as rate buy downs are another way for the lending (in this case building) industry to shirk the responsibility of lending intermediation, which is just to say: “We cannot lend you the funds for this home, as YOU cannot afford it.”

“Intermediation involves the “matching” of lenders with savings to borrowers who need money by an agent or third party, such as a bank.[1]”

Does intermediation (your meaning) mean new house sellers are steering people to certain mortgage brokers/lenders?

MRBs go by different names in different types of businesses, but they’re not illegal and should only be outlawed for people who cannot figure out which way is up.

There are a growing number of gullible people in our current population. Notice how easily “misinformation” is gobbled up by the gullibles. Got any crypto?

Great article.

These price gyrations seem like attributes of a deficient economic control model.

If those houses are empty for any significant period of time, they’re going to be in rough shape. An entire empty subdivision would start to look like bad parts of Detroit.

I may have happened to stumble upon one of the early impact craters – Bolivar Peninsula, east of Galveston, Texas. OMG – there are HUNDREDS of “for sale” signs in just a couple of miles. This is a resort area on a sand bar along the gulf coast. Aside from the obvious issues of hurricanes and coastal erosion, this apparently became a target for AirB&B investors during the pandemic, and well, it’s not penciling out for them. In addition, checked Zillow and lots of very expensive properties and “new construction” units – SHEESH. Texas rental property taxes – I think it’s 3% – and breathtakingly high insurance rates – if you can get it – and what a mess this may be. A lot of these places are going to be underwater both literally and figuratively. Thank you Federal Reserve!

almost 57% of the short term rental properties were bought in last 30 months or so.

You can imagine the extent of impact of cheap/free money.

Now, most of these investors would like to unload these STR properties and numbers won’t make any sense to them.

Also, if the economy weakens, people would cut back on discretionary expenses.

KF, alot of those places on Boliver will be “underwater” when the next hurricane hits. It’s been done before. The lots are really heap then because the house is gone.

“The lots are really heap” Woops…..mean really cheap

“…when the next hurricane hits.” — I’m sure the “Ike dike” will fix everything! /s

Anecdotal In Seattle.

One year ago almost to the day we were approached by a national top 5 home builder / developer to buy our home and lot along with my 3 other neighbors. Their plan was to knock down the houses and build 28 high end townhomes. We were paid 50k earnest money with the agreement to close in one year. The contract included 5k a month for a maximum of 6 months if they needed to extend the closing date. We received an email from their lawyer 2 days ago at the 11th hour stating they would like to restructure the contract to lower the agreed upon price by 20% and push the date back nearly a year with no 5k extension payments. Sounds like a great deal! We were caught holding their bag and their risk. We will be telling them to kiss our ass on an upcoming zoom call. Our lots were recently rezoned for density near the construction of a light rail station. Someone else will come along to buy, but we’re prepared to have to sit on it for 5-10 years until we can fetch the original agreed sale price. Fck these developers

You got $50,000 for doing nothing. What’s to complain about?

We feel that we were held captive for a year under contract while fielding million dollar offers by other developers. We should not have agreed to give them a year to see how the market was going to shake out before paying us. We got out foxed is all I’m saying. But what I’m also saying is developers are bailing on projects and I have a first person POV

We just did a new 500 sq foot condo in downtown DC and it sold for $320,000, well below the original listed price of $375K. The investor who renovated the building even offered to buy down the interest rate to make the deal. Looks like the rolling recession in RE is well under way here and probably in most metro areas. If the Fed continues to jack up interest rates this will turn into a depression in RE. J Powell will be forced to hold off on tightening any further until the fallout from previous Fed actions have had a chance to work their way through the system.

Swamp Creature,

What exactly would force J Powell to “hold off on tightening any further”? Exactly what mechanism(s) are you referring to?

The lag time from rate increase to

Impact on economy.

Laughing Lion :

The Congress but I would not wait or expect them to act anytime soon or they would have already done such

Laughing Lion

The Fed would be better off to stop tinkering now with the Fed Funds rate to stop inflation. That is not working. They have wrecked the RE industry. This RE recession will roll over into other sectors. Let interest rates seek their free market level.

“Let interest rates seek their free market level.”

Well uh that can’t really happen so long as the fed exists as it does. The only approximation of a free market fed is the one that targets the Taylor rate and lets QT rip. Which is pretty much the opposite of what you suggest.

There is nothing wrong with cratering RE or any part of the economy. It’s a necessary cleansing restructure.

Cytotoxic

I have no dog in this fight, but if you crater the RE industry you kill hundreds of industries that feed off that industry. It’s already heading south big time here. Be careful what you wish for.

If the Fed keeps up what they are doing, we will have a repeat of 2005/2006/2007.

1) It’s cold in Maine. WTI plunged < $70. That wouldn't last.

2) The German yield curve is a bunny slope. It will get steeper, dragging

US long duration with it.

3) TY twice tested Oct 4 close. It will move higher.

The Fed want to kill US gov debt. The Fed need CPI above EFFR, perhaps for a decade. In the 60's EFFR was 2%-3% above the CPI, hugging it in the late 70's until Paul Volcker electric shocks to save the patient.

4) If in the next decade the average inflation will be 4%, $31T x 0.96^10 =

0.66 x $31T = $20.50T.

5) If 6%, $31T x 0.54 = $16.75T.

6) The same rough calculations for real estate.

Michael,

4) & 5) That is similar to what Russell Napier stated in mid-October, and I concur.

“Engineering a higher nominal GDP growth through a higher structural level of inflation is a proven way to get rid of high debt levels,” said Napier. “Of course, nobody will ever say this officially, and most politicians are probably not even aware of this, but pushing nominal growth through a higher dose of inflation is the desired outcome here. Don’t forget that in many Western economies, total debt to GDP is considerably higher than it was even after World war II.”