I mean, like within hours and days, rather than weeks and months. But the SPAC sponsors want to make some money.

By Wolf Richter for WOLF STREET.

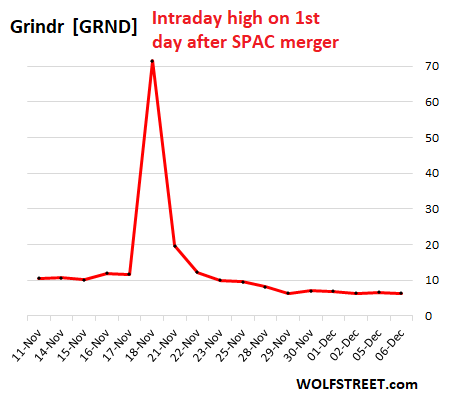

Grindr, which describes itself as “the world’s largest social network for the LGBTQ community,” went public via merger with a SPAC on November 18, 2022. On that first day as a public company, the shares shot from the price of the pre-merger-SPAC of $11.63 to an intraday high of $71.51, at which point the collapse started, and 7 trading days into it, the shares had kathoomphed by 91% from that high, and today, 12 trading days into, they’re still down 91%, at $6.37. This chart is just nuts:

SPAC sponsors – often private-equity firms, venture-capital firms, or wealthy people – want to make some money. But they will only make money if the SPAC merges with a target company because when the merger closes, they typically get 20% or so of the funds raised in the IPO of the SPAC. After the SPAC’s shares trade under the ticker of the acquired company, and crash, well, the sponsors already got their 20% out.

But if that SPAC cannot merge with a target company by the time the two-year deadline comes around, it has to shut down and return the money raised in the IPO to the SPAC’s shareholders. At that point, the sponsors won’t get their 20% of the funds raised. Plus, they will lose the startup capital that they put into the blank-check company and that was used to pay underwriters, lawyers, registration fees, etc. on the way to the IPO to become a publicly traded SPAC.

That’s the tradeoff: If the SPAC completes a merger with a zombie, and starts trading under the zombie’s ticker, the sponsors make a ton of money even if the shares collapse. But if a merger cannot take place by the two-year deadline, the sponsors are out their startup capital. So you can figure how that motivates the sponsors.

In the three years of 2020 through 2022, a total of 944 SPACs were formed and went public via IPO in the US, according to the count by SPAC Research, raising money that way to be used to acquire a real company which would then become the publicly traded company.

It might seem that 944 merger targets would be a lot of companies to acquire and turn into publicly traded stocks. But hey, it was the era of consensual hallucination, and everything flew, everyone went along, money was falling from the sky, and a mad scramble ensued to line up celebrities of all kinds to promote this stuff, and when this stuff then collapsed, some of them got sued.

But the time-frame of that collapse is getting much shorter.

Grindr’s implosion started within hours of it as a public company, and took it down by 91% in seven days. Grindr has revenues, but not a lot, just $50 million last quarter. And it had a net loss of $4.8 million in the quarter, according to its first preliminary financial results released yesterday. This is a smallish company that has been around since 2009, and it’s losing money.

When the SPAC deal was announced in May 2022, it was done at a ridiculous $2.1 billion valuation that would require a huge amount of consensual hallucination to pull off.

But consensual hallucination has been fading, though it hasn’t faded nearly enough yet, and the shares plunged, but at $6.37, they’re still giving the company a ridiculous market capitalization of $1.1 billion.

On November 16, the SPAC’s shareholders approved the merger, and it was off to the races. But about 27.1 million shareholders of the original SPAC, or about 98.2% of the shareholders, voted to redeem their shares, and they’ll get a little over $10 a share (original IPO price of the SPAC plus some interest). They didn’t want to hold those shares when they started trading as Grindr.

This left Grindr, when it actually started trading, with a very small float of about 500,000 shares, and it left it with nearly none of the cash that it would have received if 98.2% of the shareholders of the SPAC hadn’t asked for their money back.

Essential financial details remain fuzzy; they weren’t reported in the preliminary results document released yesterday, such as how much cash the company actually has post-merger, and how it would pay down its $137 million in existing debts, etc., etc. Because this wasn’t an IPO, this was a SPAC merger, and the disclosure requirements are minimal, and the promises made are huge, and you end up with whatever.

But what else can SPAC sponsors do?

Sponsors can shut down the SPAC and return the money raised in the IPO to the shareholders, if they cannot find an acquisition target within the deadline – rather than scrambling to buy whatever at whatever price. But then the sponsors are out the startup capital they plowed into the SPAC. And this is now happening a lot.

For example, Altimeter Capital, a venture capital fund, announced on December 1 that it would dissolve its SPAC #2, the Altimeter Growth 2 Corp [AGCB]. The SPAC had a deadline of January 11, 2023, to find a merger target. But it’s tough amid this shortage of consensual hallucination, with stuff imploding left and right. So it pulled the ripcord.

The SPAC’s shares [AGCB] are trading at $10.07, which is near the IPO price of $10. The company will redeem all of the outstanding shares at the per-share redemption price of $10.11 paid for with funds in the trust account.

Altimeter Capital has already become infamous. Its SPAC #1, Altimeter Growth Corp, had acquired SoftBank-backed Grab, the largest ride-hailing and food-delivery app in Southeast Asia. The merger, announced in April 2021 and approved by SPAC shareholders on November 30, 2021, valued the company at $40 billion, making it the biggest SPAC deal ever. The shares started trading under the new ticker [GRAB] on December 2, 2021. And promptly collapsed.

This was further aided on March 3, when Grab reported earnings for the first time as a publicly traded company: a monstrous loss of $1.06 billion for Q4, and of $3.45 billion for the year, on top of a loss of $2.61 billion in the prior year – for a total loss of $6.1 billion in two years. I suspect that no SPAC had ever produced so much red ink in such a short time. Shares kathoomphed 37% on the spot, and by 81% from the intraday high four months earlier, and I honored Grab with an official spot in my pantheon of Imploded Stocks.

SPAC dissolutions abound.

So far this year, about 100 SPACs have thrown in the towel on a possible merger. Of them, 60 SPACs redeemed the shares and dissolved, and about 40 have started the dissolution process, according to a report by SPAC Research. Another 40 have year-end deadlines, and they may seek deal extensions from their shareholders or shut down.

Two of the SPACs being dissolved are creatures of busted “SPAC King” Chamath Palihapitiya, whose venture firm, Social Capital, had put together six SPACs. The other four merged with companies and their shares collapsed:

- Opendoor Technologies [OPEN], house flipper: $1.41 (-96% from high).

- Clover Health Investments [CLOV]: $1.19 (-96% from high).

- SoFi Technologies [SOFI] online student-loan lender that pivoted to stock & crypto platform: $4.32 (-85% from high)

- Virgin Galactic [SPCE], dreaming of space-tourism: $4.62 (-93% from high).

Palihapitiya’s firm, as sponsor, made a ton of money on those four SPACs that merged with Opendoor, Clover Health, SoFi, and Virgin Galactic, though shareholders got ransacked. The two SPACs where Palihapitiya’s firm lost money were those that are being dissolved — and where shareholders didn’t lose money.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The day GRND went public, I wanted to sell them to short but looks like it was not available to short.

I wish that there was a dedicated index that tracked the money lost by all the stocks, cryptos and SPACs that went viral on TikTok.

I still make money ole fashion way – working

wally street is PONZI scheme like crypto, SPACS, etc.

now I need to get some sleep so I can continue making money

and not have to worry about some ‘financial’ advisor who’s only out to get my money to put in his bank account

same / and no option yet

Let me help everyone on Wolf Richter’s excellent site. Shorting individual stocks as an investment strategy in a bear market, such as we are in, is very unlikely to result in a profit. I can promise you that your broker is working against you.

Since November 2021 I have advocated using SRTY and SQQQ as trading vehicles, buying when they are getting pounded and selling when your account is hitting new highs. Notice that I am advocating locking in profits when your account hits new highs. If you allow your greed to dominate and not sell at account new highs, you will eventually lose all you investment money.

This is so right. I don’t want folks here to go after obvious shorts because:

1. Shorting provides price support to crappy worthless stocks as Short sellers buy shares to close their positions.

2. The premiums on options are too high, so you can be right but miss the small time interval where shorts are profitable.

3. I don’t want wolfstreet readers to lose money. And there is still so much liquidity out there (see reverse repos) that wallstreet can spin a Pivot rally anytime to squeeze shorts.

I have shorted many stocks and made money.

I close frequently and my sizes are small.

I try to make sure the broker is not charging outrageous hard to borrow fees.

If it is hard to borrow either I don’t short or close shortly

Jon, can you tell us which brokers will show explicit borrow fees?

My experience with shorting has always been with one of the bigger brokers such as Etrade. If I remember correctly, Etrade does not charge explicit borrow fees. But instead you have to post 50% (or whatever) extra *cash* as margin. Or you can post other stock as collateral to borrow the 50% cash, in which case your “borrow fee” can be thought of as the margin loan interest on the “cash” you need to post. At least I think that is the right way to think about it.

If you post margin cash, the broker will gladly lend that same cash out to somebody else who has a (long or short) margin loan, and make a huge profit. It is also low risk for the broker because they can “net” the customers long and short positions against each other as far as margin loans go, and of course they will iquidate your long or short margin position well before they are about to lose any money on their lending to you.

But again, which brokers operate with pure “borrowing fees” model, rather than the collateral+borrow structure?

@ Harry Houndstooth Always appreciate help, but if one were going to short individual stocks, wouldn’t a bear market typically be the best time to do it?

” Shorting individual stocks as an investment strategy in a bear market, such as we are in, is very unlikely to result in a profit.”

Try shorting my list from Late June 2022 when the ‘Pig went to the trough, yet again”

W – Wayfair

RDFN – Redfin

ZG – Zillow

OPEN – Opendoor

CVNA – Carvana

MSTR – Microstrategy

SI – Silvergate

RIOT – Riot Tech

MARA – Marathon Holdings

This market is ripe for the picking for ‘Roasted Pigs”

Harry Houndstooth

Front running on the wisp of any thing like (real or NOT) peak inflation, pause, slowness in rate increase, pivot dreaming by the financial media and the wall st, can put sudden and serious dent after buying inverse ETFs. So watch out.

These are short trading (position trading within days) tools. But they have to tempered with some long positions(long ETFs) against them, against the whiplash(s) down the road. Not that easy but one should be acutely aware of these negatives. B/c of crazy ‘front running’ I hardly buy any puts. if I buy there will be hedged with a few calls.

This is going to be secular bear with lower of the highs and lower of the lows, in the long run. But intermittent with feverish bear rallies. one has to be flexible with high cash levels

Since ’82, I have gone through both bull bear cycles, more than once. But nothing like this ‘surreal’ Bull ( everything bubble) being slowly slaughtered, against the wishful thinking retail investors, who are in denial.

No Fed’s put, No QE, No ZRP= NO mkt!

Surely they will have a back door.

As almost all SPAC mergers are total garbage, you can sit back and wait till lock up is over and more shares are available. Shorting early is risky and expensive. It does not matter if you short at $12 or at $5 if the stock is heading lower.

Look at QS as an example. It is trading around 7 now, has a borrow rate of 12% and is optionable. I am holding a few longer dated ITM puts and just wait.

On average, SPAC mergers made a new low yesterday.

Doubtful grnd debut would have marked any kind of bottom.

Surprised they didn’t try to sell fewer shares at 420.69

Makes me wonder if any of the cannabis-related stocks IPO’d at $4.20

$0.420?

When a top grinds on a bottom, the result is usually a spac that someone has to clean up.

So is the trading, my last trade was pipelines early November. Everything falling like a knife now. Holding cash, maybe trade around one position, just taking what they give me. Your writings have help immensely.

Sam : The real question is: who are we selling this to?

John : The same people we’ve been selling it to for the last two years, and whoever else would buy it.

Sam : But John, if you do this, you will kill the market for years. It’s over.

Sam : And you’re selling something that you “know” has no value.

John : We are selling to willing buyers at the current fair market price. So that we may survive.

Sam : You would never sell anything to any of those people ever again.

John : I understand.

Now replace layered MBS with SPAC Zombie, or Sombie (or SPombie), and we have Margin Call 2.

They’re too pessimistic. Of course they can sell to those people again. Just give it a new name. Just like LBO firms got renamed to private equity. And CDS have been renamed to a whole plethora of private label swaps.

Heck, even SPACs is just a name for a company too sh*tty to meet the basic disclosure and financial requirements necessary to IPO (so you IPO on a cleansheet company with good financial terms that you can disclose, then merge with a sh*tty company that would never pass muster if they had to open their books prior to selling their shares to suckers. Easy peasy!).

Just an old whore in a new dress.

Whores: at least they provide a real service.

How on earth were the “rules” for SPACs created? Why did the SEC allow something as insidious as this to see the light of day?

The SEC should have nothing to do with it. Anybody who invested in a SPAC needed a lesson in loss-making.

In a free market, you need freedom to succeed and fail.

Bottom line is they were greedy fools who knew what they were getting into.

If somebody wants to pay $1000 for an advertised bag of butt hairs, they should have that right, and taxpayers shouldn’t be required to bail them out.

Bobber

“In a free market, you need freedom to succeed and fail”

Since March of ’09. with continuous Fed’s PUT, QEs, ZRP, there is/was NO longer any kind of FREE mkt but Crony capitalism managed by the Fed.

NOW, no more Fed’ PUT, no ZRP and no QEs, the reality of fundamentals is slowly descending. Fed is trapped and are clueless. Their karma is biting us all.

This is the era of ever-more-compressed attention spans, and matching smooth and efficient fads, manias and collapses. I am enjoying the dispatch and symmetry of crazes, instantly reversed, and wealth (and lessons), instantly dispersed.

It took some thinking to put together these clever little houses of cards. And the “investors” thought they were being mighty clever, and putting one over, for instant wealth, too.

We’d be mistaken to think anyone actually viewed SPACs as investments. They were highly speculative bets on something that moved a lot in price. People love to gamble, and they wanted instant feedback. They got it.

It’s an extension of Las Vegas, simple as that. People like to gamble.

Fix income trader bonuses might rise by 20% y/y.

Wall street bankers payout might plunge by 45% y/y as financiers face headwinds or a looming recession. 2021 was a banner year, but in 2022

the bankers of the world might face some difficulties.

Job cut might be next. The bankers of the world will do what it takes to survive the next downturn without gov support and avoid the fate of SPACs

Easy money caused a lot of trouble. Reviewed several measures of stock market valuations as of the end of Nov. All tell the same story. Stock market was still more than 2X the long term mean and more than 5X the valuations when Volker was slaying inflation.

Still in the first half of the tightening game and the false wealth is being evaporated. Much more to come.

Perhaps if one were to evaluate the current situation through the lens of history. Since the previous scenario has no precedence in history, zero and negative interests rate, it is difficult to judge and compare the value of assets in real time.

While I agree with your assessment, I’m not ready to embrace the predicted outcome.

The outcome is inevitable. Stocks will revert to the mean and may even overcorrect. This isn’t an if it’s a when. That might be a crash or it could be a lost decade or two. No one knows what it would look like but anyone who understands markets understands that it is inevitable.

This is not correct. Clearly QE produces abnormally high valuations. These valuations may persist indefinitely, until the USD loses the last 3% left in value and gets retired/replaced. Essentially QE put a higher floor under the market, therefore old means do not apply.

I’m about to put a picture of Palihapitiya on my dart board but I’ve still got pictures of all thes3 energy companies Ceo’s to get through (I’m just jealous my conscious won’t let me scam – business is no place for me),

Having thrown darts at phantoms at various times through the years, I sorta understand, while disagreeing with, your rant.

First off, CEO’s, are an untrusty lot, no doubt. However, they are protected from the chaos they are prediculated to cause.

Second off, they will die, guilty, for their sins, like the rest of us.

Chestnuts roasting in the open fire.

I think we’re having another late 90s moment where the markets have to realize that a company is supposed to have some substance and make some money. Just because someone can use apps like Grindr doesn’t mean it’s something worthy of being taken public.

The days of easy money from selling wvery shred of consumer data are also increasingly at risk as governments tame that particular wild west, and I don’t have it in me to be mad about that. So where’s the money in a hookup app? Where’s the money in half of these idiotic SPACs? It’s only there for the conmen taking them public, now that the earliest bagholders are taking haircuts too.

They can’t go away soon enough as far as I’m concerned. The casino is closed.

Relatively small companies like Grindr can make money just fine. But going public is expensive, and then there are the stock-based compensation packages and the expenses associated with having to grow exponentially, which is expected of a company that just went public, but growing exponentially never works for long anyway. This company should have never gone public, especially not at a $2.1 billion valuation … that’s just nuts. Maybe at a $200 million valuation might have kind of worked, along with proper disclosures of financials for the past three years, and the kind of stuff you do for an IPO. But people just got too crazy.

What seems to be missing is a collection of vitally necessary adult fairy tales. Crypto, SPACs, NFTs, the Deep State, QAnon… these exist because there’s been a serious shortage of fairy tales with talking animals, magic wands and similar. Things like the Tooth Fairy, Santa Claus, Superman, Goldilocks and the bear family have lost their cred. The collective IQ has dropped to the extent that we are bewildered about what to do, what to believe, what’s fair and decent, which way is up.

We just need a new, fresh set of adult fairy tales. They don’t need to be clever or sophisticated. They can stink to high heaven. Just make ones with a lot of tattoos, idiots with big biceps and blue hair and ninnies that can find conspiracies in every nook and cranny.

Surely, Wolf, you can write up a pantheon of fresh imaginary heroes and demons.

We already have Elon Musk.

“…calling Joseph Campbell, Joseph Campbell to the white courtesy phone, please…”.

may we all find a better day.

Noticed in the couple of crashing and crashed Spacs you highlighted none of the financials in their SEC filings are audited. Is that now common?

Sorry if this is a dumb question.

Not a dumb question at all. A real issue — but not with our heroes here yet.

1. Quarterly financial reports are generally not audited.

2. But public companies have to file audited annual reports (10-k) x months after the end of their fiscal year. If they fail to do that — lots of SPACs fail to do that — they have to say in a filing, I’m sorry I failed to do that, because my audit firm quit in disgust, and I haven’t found a new one yet, or whatever. And if they fail to do it by the time the deadline passes, the shares will get delisted.

WOLF

Yes, I did RTGDFA. ;-)

You state….

“….But they will only make money if the SPAC merges with a target company because when the merger closes, they typically get 20% or so of the funds raised in the IPO of the SPAC. After the SPAC’s shares trade under the ticker of the acquired company, and crash, well, the sponsors already got their 20% out…”

As for “…crash….they (sponsors) already got their 20% out…”

How did they “already get it (20%) out?”

I reading from you that the sponsors provide only fees / expenses related to the merger which “entitles” them to 20% of the IPO raise ? If so, and the IPO raises diddly squat, the sponsors are also at risk, for their “fees / expenses” $$$ being lost, are they not ?

If I missed a step in the process, my apologies.

If 100% of the SPAC shareholders redeem their shares, the company gets “diddly squat,” as you said. But then I think the merger is dead.

Not sure exactly how these borderline cases are being dealt with.

I doubt all the shareholders can sell. Some might not be 100% vested. And also like subscriptions. A hassle to cancel. There’s probably a fair amount of smucks just like me who are are too busy with other things or too burnt out to get anything out of their shares.

Love the advise to sell stock when it goes higher than it should. I’m gonna start paying attention to that strategy rather than letting retail investors put my money into Twitter . That is quite simple and yet the only way to put capital to work without playing into this madness. If it were up to me, I’d invest only in R&D, vocational schools, immigration, utilities, infrustructure, computer chips, defense contractors, and hardware stores.

“SPAC sponsors – often private-equity firms, venture-capital firms, or wealthy people – want to make some money. ” from your post.

I think captures the greed, enabled by reckless monetary policy. Gamblers with nothing to lose will gamble.

Since I have seen the sausage being made, I feel that somehow I may be culpable for the carnage that is likely to ensue.

A country adrift, trying to decide whether the foundation is solid or flexible. Making lawful, the unlawful practices that the concentrated wealth impose, thinking that is what they desire.

Several things have been instrumental in the formation of this young, great country America.

Number one is the belief that every single one of us are eligible for a life that exceeds what are immigrant parents experienced.

Number two

The implosion of the wall street schemes are normalized by the implication that the investors were clamoring for risk free assets. Which meant that even the speculative bonds paying 2% at zero FFR pct interest were a viable investment.

Hey Wolf, ChatGPT just discovered your blog.

Dang: “Number one is the belief that every single one of us are eligible for a life that exceeds what are immigrant parents experienced.

Number two”

You really nailed it with “Number two”. We’re swimming in it.

@Dang I threw together this grid to better understand where we’re at in history. Greene offers a hopeful phrase, “This revolution can be extreme and violent, or it can be less intense, with simply the

emergence of new and different values.”

Civilization Cycles Compared

https://drive.google.com/file/d/15qRymG5V2hq9wUzt226XiTjrtd_iPOCC/view?usp=share_link

“Scamath” as I’ve read it on the reddit

Earnings have actually mattered with year unlike in the past.

I can’t help but to think about the outlook for corporate earnings which are likely to be dismal.

Thanks for putting all of this in laypersons terms! This is a topic that is not well understood.

It might be interesting to do a metachart. Not just the invidivual entities that have collapsed since the counterfeit fountain shut off, but the TYPES of entities that no longer exist. Bitcoin exchanges, altcoins, SPACS, DAOs, NFTs, Web3, and soon all IPOs.

Visual Capitalist is started to get into these subfields, with interesting graphics. But Wolf’s are so pure and clear, kudos for that!

I won’t blame the SEC for not being on top of the crypto situation… cryptocurriencies are new, exotic, and nobody quite knows what to make of them.

But come on! These SPACS are just garden variety pump-and-dump schemes. How is the SEC letting 944 of these things come into being in just three years? That is basically one per day. Explain the logic to me of shutting them down if they are run by the Gambino Family or the Colombo Family but turning a blind eye if they are run by Altimeter Capital or Social Capital…

Why do we need any regulatory action? SPACS are plainly fraudulent anyone with an ounce of financial intelligence. They are about to self terminate, and any moron who invested in them gets zero sympathy from me.

Market discipline is a beautiful thing, unless its bells toll for me.

phleep

What market discipline under Fed supported mkts since ’09?

No ZRP, NO more QEs but QT and no more Fed’s put.

Now the reality is bringing back the discipline

Darwin Financial Award winner for 2022? I nominate the American public.

@ Happy 1-

@ Wolf-

have there been any successful SPACs?

I’m not a finance blogger and I’m no expert in these matters, but I’ve lived long enough that when I see an investment vehicle that says “give me your money and I’ll decide what to invest it in later”, that’s about all I need to know. What moron would put money in that? Would you lend money to anyone with that pitch?

It’s a big club, and you ain’t in it… I work in the industry, I could write at least 50 pages worth of scams being perpetuated. It is not my place publicly to say anything, and some of us go along for the fat pay, but it’s very clear that the financial “system” as we know it is imploding and never coming back to it’s glory days. The drastic lack of innovation and investments going towards innovation is what is killing the global economy really. Capital investment in companies has more or less nothing to do with innovation or even basic economics anymore, it is strictly based on one criteria, if you’re part of the system, as they call it.

SEC and CSA are just there to create the illusion to the public that there is oversight, but there isn’t, at least not when it comes to the “brotherhood”. Money managers, investment firms, VC’s and bank executives are all in the same “organization” in one way or another. If an outsider cheats the system, they get punished, but when insiders pig out, they call it “stupidity” and move it along. If Chamath wasn’t part of rituals and “ceremonies”, do you think he would of got away with any of this?

You try setting up a money losing SPAC, and doing the same things these guys do, and see how it evolves… You won’t even get a penny from “investors”. You have a legitimate innovative concept or product already in the works? No funding, I have seen it with my own eyes. But, if you’re willing to “join” the big club, you get massive funding, regardless of how stupid or absurd the company you’re pitching is.

You see, money isn’t real, it’s created out of SQL databases nowadays, it’s just digital numbers. “Losses” or “profits”, it doesn’t matter to the pigs, you invest in those in the club, and you shun outsiders, period. Many colleagues like to say they are non-conformists, but in reality, there’s even more conformity on this side then the cattle’s side.

Wolf, should there be an “to” in “But the SPAC sponsors want make some money.”?

What, me worry?

Mo’ money, mo’ problems.

I got 99 problems, but a SPAC ain’t one.

10-years-ago me: “How could an app used exclusively by gay men possibly have $50 million in revenues?”

Today me: “How could an app used exclusively by gay men possibly have only $50 million in revenues?”

All this BS came from an indifferent government. De-regulate me and I will make everyone rich! Sucker.

Are pension funds and endowment funds the ultimate losers in these scams, or whatever they are?

SPAC and cryptocurrency are just other ways of saying “SCAM”!

Not totally on topic, but CNBC’s headline is now something like “Stocks little changed as TRADERS weigh…”

They used to use the term “investors.”

It’s almost a tacit admission that the modern market isn’t about investing, but trading.

At least once every decade or two sp500 will get marked to where you can justify their value on discounted cash flows of the dividend only. Last time that happened was 2009. At 1.7% yield and a 4% t bill we are a long way from there in price, maybe not in time.

I think Wolf starts from the premise that the people who put money into spacs, cryptos, meme stocks and the sketchier IPOs are investors behaving irrationally, when in fact they are not investors at all, they are gamblers placing bets in the casino economy based on the “greater fool” theory. A gambler playing this game well can make money, getting in and out at the right time, and would not fairly be called irrational.

Exactly. In reality if you aren’t doing some kind of long term assessment of the companies earnings and looking at the balance sheet for risk you are not a value investor.

You can do something else and make money, but getting value for your money outlay is the most logical approach like buying anything else.

“You gotta know when to hold ’em, know when to fold ’em” – Kenny Rogers. Kenny was a rational being.

No- while acknowledging the late Mr. Rogers,’ excellent cover, in the interests of doing our best to give credit where it’s due (I ref the shameless purloining of our most-excellent host’s fine work), ‘The Gambler’ was composed and first performed by songwriter Don Schlitz…

may we all find a better day.

In financial markets, there is no actual difference between “investing” and speculation. It’s a matter of the risk being taken, that’s all.

Still few investors are pure gamblers meaning the bias is there to make money into the absolute riskiest gambles. Most people miss this fact.

Obviously our secondary and higher education programs represent a serious flaw in our national defense strategy. Is there an unlimited number or “greater fools” out there? Probably not- they’ll try to get back to work during the “soft landing” recession. I have to get back to my “stimmy” fix boost on Chinese Tik Tok now. Have your kids been reprogramed while you read this post? You won’t know until its too late.

Good comment MM!

Teaching a class in construction in two high schools in the mid 1980s era, I was appalled by the lack of elementary school skills of the majority of the students.

Many, probably most, did not know fractions, at all,,, and some were at least hesitant in any multiplication and division, with some totally unable to do those basic maths…

Seemed to me to be deliberate, and when I was summoned to ”faculty meeting(s)” and said so, I was rapidly and repeatedly scorned because it was, ”all the parents fault.”

Still seems to me, many years later, it is a DELIBERATE action to dumb down anyone but the very very top kids:

1. To bee suckers for the various and sundry financial stuff such as payday loans, SPACs if they ever did get enough to rise above the paycheck to paycheck.

2. To bee cannon fodder to protect the assets of the now very clearly ”owners” AKA oligarchy.

3. To bee wage slaves for peanuts, as has clearly been the case since then.

4. Etc., commenters on here can likely add at least a few more examples of the WHY and WHAT the teachers unions, now clearly taken over per the instructions of the USA leftists of the 1960s era have done to DUMB Down our children since then…

Your list seems to be accurate but incomplete. You left out woke virtue signaling political correctness.

The country will go down in flames (literally) before its proponents will abandon it.

“Still seems to me, many years later, it is a DELIBERATE action to dumb down anyone but the very very top kids:”

I don’t know about that, but I do agree that many students do get left way behind in math. I’ve toyed with the idea of volunteering to be a math tutor when I retire… if I still have the energy.

“Still seems to me, many years later, it is a DELIBERATE action to dumb down anyone but the very very top kids:” Your comments have been quite reasonable over the years. This one is a stinker. You don’t impress me as a reader here who’s prone to conspiratorial crap. No need to start now.

Harvey, I think the problem is pretty inevitable: kids know early on that some of their classmates pick things up quickly, others are slower. They self-reinforce this, and it’s also coming from the social environment, that is, they know if they’re falling behind. It’s pretty much established by the 3rd or 4th grade.

Teachers (almost all) try hard to get the slower kids up to speed on every skill. It’s a bit heart-breaking to be face to face with kids who can’t grasp very simple concepts, adding 3 sets of whole numbers, for example, that is so “explainable” but just doesn’t connect, or it isn’t retained.

There are physical resources to help kids who learn better by handling items, or other “modes”, but this can stigmatize if certain kids need little blocks to add thing up while others don’t, etc.

Kids develop an internal monologue that they’re getting along well or they’re falling behind. But, almost always, teachers are pulling for the slowest. It’s sort of unfair to the ones who are really quick. You readily see this in athletics but don’t think of it in the same way.

I’ve never met a teacher so cynical or malicious as to want to keep some kids down while favoring fast learners. Charlie Munger comes to mind as an exception, only wanting to donate help to the best and the brightest, not kids in “the gutter”, but he was never a paid teacher.

Long ago pedagogists felt that education had to be dumbed down in order to appeal to the masses. Richard Hofstadter wrote about that topic in his book Anti-intellectualism in American Life. From what I remember, public intellectual John Dewey figured prominently in that fiasco.

Hofstadter’s book was about the frequent rise of populism and the fear/distrust of intellectuals. I don’t remember reading anything about his opinions re: education. Are you saying he was in favor of dumbing down, or against? I’ve read a good share on American education and do not remember any writer encouraging “dumbing down”.

Keeping the average and below-average student interested in any subject does require pitching things at a level that they can understand. Read Piaget on that, and Erickson.

If you have 30 kids in a classroom and aim the discourse to the brightest one or two of them, you’d have a lot of kids pissed and completely disengaged.

Is this a real fiasco or one you’re imagining?

TSLA is imploding as well. That one had a more elaborate sales pitch and prized celebrity, so it is going on longer.

Waiting for Telsa’s quarterly ”emissions tax credit subsidy” to wind down, then face their quarterly ”credit facility financing” costs to double.

This morning CARVANA stock fell ANOTHER 45% after having already FALLEN 98% this year, and it appears that their last minute desperation talks with creditors to keep their doors open are not going quite as well as expected!

I do not like green eggs & SPAC, Uncle Sam I am.

Xavier C. – getting closer to perfecting your standup routine (iow, I now expect at least one well-crafted laugh when you post. thanks for lightening the load of the day…)!

may we all find a better day.

On reading this article, all I can is ‘Wow, just wow.’

As Wolf points out:

This was further aided on March 3, when Grab reported earnings for the first time as a publicly traded company: a monstrous loss of $1.06 billion for Q4, and of $3.45 billion for the year, on top of a loss of $2.61 billion in the prior year – for a total loss of $6.1 billion in two years. ‘

Now, colour me stupid, but how did they get anyone to buy shares at initial offering of a firm that had prior year losses of $2.61 billion dollars?

“Step right up, folks

And see Little Egypt do her

Famous dance of the Pyramids

She walks, she talks

She crawls on her belly

Like a reptile

Just one thin dime

One tenth of a dollar

Step right up, folks”

Wolf,

In the end, is the appeal of SPACs for sponsors and underwriters the fact that, unlike an IPO, there really aren’t no-selling lockup periods (ie, the insiders can dump to public buyers more or less instantaneously vs an IPO six month lockup)?

And, I imagine the merger approval vote removes any fiduciary liability for the sponsors/underwriters.

(The gaming dynamics of those merger approval votes might be interesting to discover…not only does the underwriter have to bamboozle hundreds of millions of dollars into a blind fund…the sponsors then have to later convince those same suckers (who you think might have sobered up) that the proposed merger candidate is valuable enough. Most con men take it on the lam after the *first* scam is completed. Makes you wonder how the “approval” phase gets pulled off – can voting authority be contractually defaulted to the sponsors as part of the SPAC IPO? If so, perhaps fiduciary/securities law liability might raise its weary head again…)

There can be lockup periods — this is a negotiated item. Those stocks tend to plunge when the lockup expires. BuzzFeed plunged 40% in one day when the lockup expired.

I think it is pretty fair to say that a SPAC is a lot like classical Private Equity deal, except taking a company public instead of going private.

The original “investors” has a special deal to get their money out first, and anything more is pure profit for them, whereas the company may or may not survive and may be loaded up with debt.

Maybe the above is a bit simplified but I think it is largely true.