“Expect more distress from some owners as loan defaults and relinquishing of assets could increase going forward.”

By Wolf Richter for WOLF STREET.

The biggest office REITs — publicly traded landlords that specialize in office properties — have gotten massacred in the stock market since March 2020, after having already had a hard time before. Some of them had hit their all-time highs in 1998 or 2000 or 2007, and they’re down 65% and 75% from those highs. And some of them are now back where they’d first been in the 1990s and even the 1980s.

But it’s the problems in the office market since 2020, since the large-scale arrival of working-from-home, and with it the largest office glut ever, with record amounts of office space vacant and on the market for lease, that these REITS have taken the most recent hits.

Interestingly, they plunged during the March 2020 crash, but then they recovered partway up toward their February 2020 level, only to let go again in a very systematic manner this year to either reach new decade lows or get close to them. We’ll get to those big office landlords in a moment.

These landlords face office gluts.

Commercial real estate advisory Savills today released the first batch of its Q3 quarterly office market reports on the major markets in the US, 12 markets in total. Houston tops the list in terms of the largest share of vacant office space on the market, with an availability rate of 30.7%. San Francisco is second with 28.9%, and shooting higher.

A big issue is sublease space. This is space for which companies are still paying rent to the landlord, but they’re not occupying it, and instead they’re trying to find sublease tenants for it to help defray the expenses of that space. These companies will price their sublease space aggressively since they don’t have to make a profit on this office space, but just want to lower their costs of holding it until the lease expires. Sublease space puts downward pressure on effective rents – even as landlords are tying to hold the line.

Houston has long been the hardest-hit of the big office markets due to the oil bust that started wreaking havoc in 2015, followed by the pandemic and the shift to working from home. But things are getting slightly less bad. The construction boom that took off during the oil boom kept throwing the latest and greatest office towers on the market at the worst possible time, with projects that had been planned years earlier. These fancy office towers triggered a flight to quality, with companies leaving their old digs when the lease expired.

Here is the fate of some of those older Class A office towers built in the 1980s, after the tenants moved to one of those new fancy towers: The landlords defaulted on the loans and let the old towers go back to the lenders – the CMBS investors – which then sold those towers in foreclosure sales at gigantic losses of 82% and 88% (which I analyzed here earlier this year).

It’s the old towers that get into existential trouble – not the latest and greatest. But even the owners of the latest and greatest have to deal with the glut, and they can’t get the rents that make those towers work. And in the tech sector, such as San Francisco, it’s even the latest and greatest towers, such as the Salesforce Tower, owned by office REIT Boston Properties – which we’ll look at in a moment – that have huge availability rates. Tech is moving out of the latest and greatest, and no one is moving in behind it.

But in Houston, the worst may be finally over. The availability rate dipped to the still worst in the US of 30.7%, but that’s down from 31.1% a year ago. But available sublease space rose again, after falling, to 7.7 million square feet (MSF)

Leasing activity jumped to 3.8 MSF, roughly in line with pre-pandemic activity. But a number of those deals were downsizing moves by energy companies that moved from larger spaces in older buildings to smaller spaces in new buildings, some of them consolidating offices spread over several buildings into one. And their current (larger) digs in these older buildings will come on the market, adding to the pain — and to availability. This is going on all over the place.

San Francisco, until 2019 the hottest office market in the US, is closing in on Houston. Availability rate rose to yet another all-time record 28.9%, up from 26.2% a year ago. Back in the Good Times, Q3 2019, availability was 7.1%. From red-hot office shortage to the worst office glut ever in three years, as tech companies realized that the vacant office space they were hogging for the future wouldn’t be needed because that future wouldn’t come. It has been cancelled by the shift to working from home.

Sublease space dipped to a still huge 7.7 MSF. Leasing activity fell to 1.0 MSF, the lowest since the lockdowns, and less than half the activity during the last three pre-pandemic Q3s.

Asking rents had peaked in 2019 and have been sliding since then. In Q3, the average overall asking rent dipped to $71.25 per square foot (psf) per year.

“Expect continued downward pressure on average asking rents and effective rental rates as landlords aggressively fight for occupancy amidst sluggish demand,” Savills said in its San Francisco report.

“The pullback in leasing in the technology sector this year has added another headwind to any office market recovery which has struggled as many office workers have continued to work remotely,” Savills said. “As a result, expect record high office availability to continue to increase through the end of the year and into 2023.”

New Office Towers continue to be added.

The table below shows the 12 office markets for which Savills released its Q3 office reports today, in order of the availability rate.

The right two columns show the total office market size in Q3 2021 and in Q3 2022, in million square feet.

The bold column shows the net amount of office space added since Q3 2021, in million square feet – a total of 19.3 million square feet of net new office space was added in these 12 markets in one year.

The most office space was added in Seattle/Puget Sound (5.2 MSF), Boston (3.3 MSF), and San Francisco (2.2 MSF) over the past year. This will continue for years as office projects are being completed. But Houston, a market over twice the size of San Francisco, added only 500,000 sf, as the building boom has run its course.

| Office space, MSF | ||||

| Availability rate | Increase YOY | Total Q3 2021 | Total Q3 2022 | |

| Houston | 30.7% | 0.5 | 192.6 | 193.1 |

| San Francisco | 28.9% | 2.2 | 83.3 | 85.5 |

| Atlanta | 25.8% | 0.6 | 174.1 | 174.7 |

| Los Angeles | 25.4% | 1.7 | 219.4 | 221.1 |

| Chicago Downtown | 24.5% | 1.3 | 148.1 | 149.4 |

| Philadelphia | 21.9% | 1.0 | 132.7 | 133.7 |

| Orange County | 21.9% | 0.1 | 85.7 | 85.8 |

| Washington D.C. | 21.5% | 0.0 | 122.6 | 122.6 |

| Silicon Valley | 20.8% | 1.4 | 85.6 | 87.0 |

| Seattle/Puget Sound | 20.5% | 5.2 | 114.5 | 119.7 |

| Manhattan | 18.0% | 2.0 | 467.6 | 469.6 |

| Boston | 16.4% | 3.3 | 258.3 | 261.6 |

| Total office space added in 12 months | 19.3 | |||

In Chicago Downtown, the availability rate jumped to 24.5%, from 22.4% a year ago,

In Los Angeles, the availability rose to a record 25.4%. And sublease space jumped to 9.6 MSF, from 8.2 MSF a year ago as Netflix and PayPal put some of their vacant office space on the sublease market.

In Seattle/Puget Sound, the availability rate rose to 20.3%, the highest in the data. Class A availability jumped to a record 20.5%. Sublease space rose to 5.7 MSF.

In Silicon Valley, the availability rate dipped 10 basis points to 20.8%, based on one large deal: TikTok’s parent Bytedance subleased 658,000 sf from Yahoo. And so available sublease space dipped to 4.5 MSF, as that Bytedance deal removed 658,000 sf. Leasing activity in Q3, driven by the 658,000 sft Bytedance deal rose to 1.7 MSF, from 0.9 MSF a year ago.

In Washington D.C., the availability rate rose to 21.5%, and sublease space jumped to 3.4 MSF. Leasing activity in Q3 fell to just 1.1 MSF, the lowest in many years, lower even than during the lockdowns, and about half the five-year average activity.

“Hefty concession packages are indicative of landlords being forced to do more to chase potential tenants and keep existing ones,” Savills said in its office report for Washington D.C. “Class A new leases average now $150 psf in tenant improvement allowances and 24 months in rent abatement, totaling $282 psf in concessions.

“With office market fundamentals remaining soft, expect more distress from some owners as loan defaults and relinquishing of assets could increase going forward,” Savills said.

Shares of office landlords plunge.

The shares of the five largest office REITS by market cap have all plunged from their recent highs – and some of them much more from their distant all-time highs. Many investors buy REITs for their yields, but taking a 50% or 70% capital loss to get a 5% yield is not a good deal.

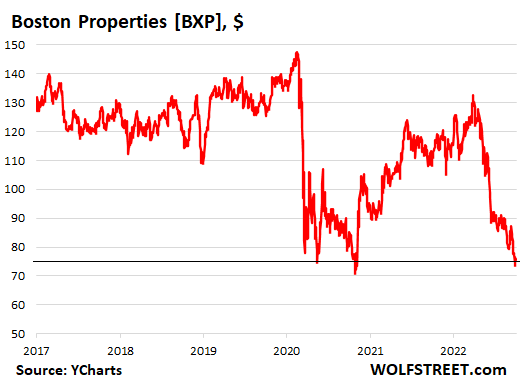

Boston Properties [BXP], the biggest of them, reached an all-time high in February 2020, and then plunged in March 2020. During the subsequent mega-QE era, it regained much of what it had lost in March 2020. But in April this year, as the Fed’s rate hikes were beginning to do their magic, the shares began to plunge again.

Today, despite a mild gain over the last few days, shares are down 48.7% from their February 2020 high, barely above their March 2020 low, and just a tad away from carving out a 12-year low. And they’re back where they’d first been in 2005 (data via YCharts):

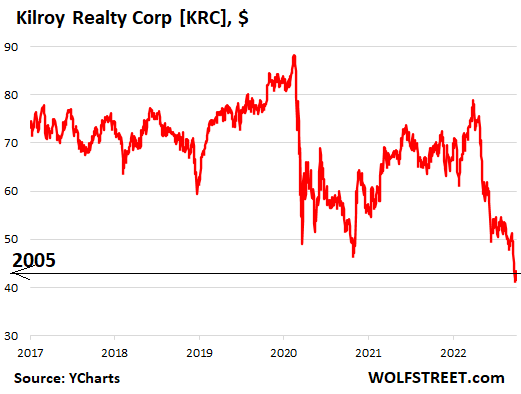

Kilroy Realty Corp [KRC] today closed at $43.37, down 50.9% from its high in February 2020 (which was about level with its prior high in February 2007). Most of that plunge came since April 2022. Shares are now back where they’d first been in 2005 (data via YCharts):

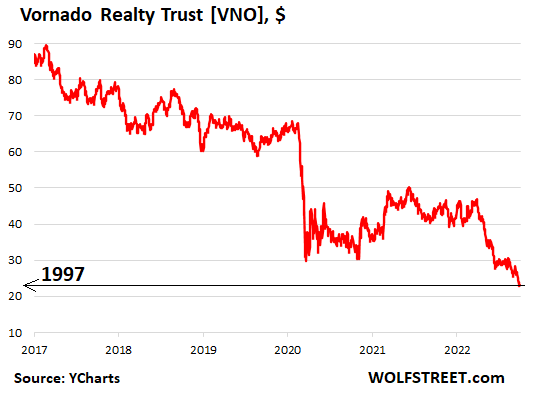

Vornado Realty Trust [VNO] shot to an all-time high in February 2007, before plunging during the Financial Crisis, and then reached a lower high in February 2015, where this chart starts. Since then, the shares have plunged 74%. And since their most recent lower high in January 2020, shares have plunged 66%.

These misbegotten shares are now back where they’d first been in 1997 (data via YCharts):

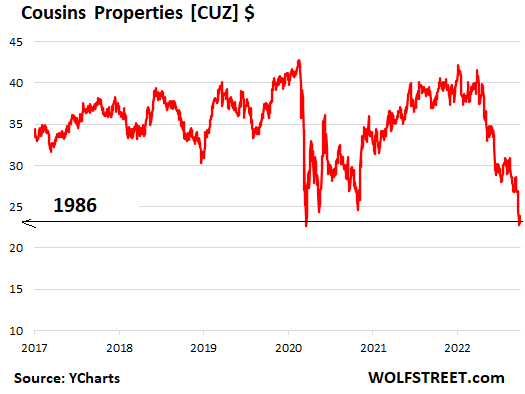

Cousins Properties [CUZ] had spiked to their all-time high during the dotcom bubble, then plunged, then reached a lower high in 2004 and then again in 2007, and then collapsed. As of the close today, shares have plunged 81% from their all-time high in August 2000. From their lower high in February 2020, shares have plunged 45.5%.

Shares are now back where they’d first been in 1986, good lordy. But if you bought back then, and collected the yield since then, you’re in pretty good shape because at least you got the dividend yield. If you bought during most of the time since then, your dividend yield was a lot lower, and your capital loss was high, and that’s just a bad deal (data via YCharts):

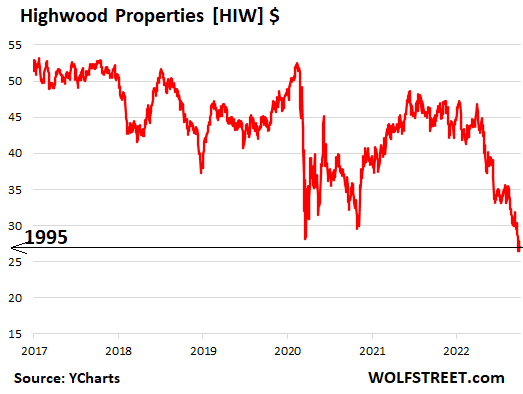

Highwoods Properties in February 2020 got close to matching their all-time high of 2016. Since February 2020, shares have plunged 48.6%, most of it since April 2022, with a big trough in between, and last week they hit $26.41, the lowest price since 2011. Today they closed at $26.98. These shares are now back where they’d first been in 1995 (data via YCharts):

The somewhat smaller office REIT Equity Commonwealth [EQC] is down 31% from February 2020 and down 65% from its all-time high in February 1998. SL Green Realty Corp [OFC] is down 60% from February 2020 and down 75% from its all-time high in 2007. Turns out, these office REITs, once among the hottest stock trends, weren’t such great deals after all – and they really don’t like working from home and higher interest rates.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When the real estate market collapsed in CT in 1988, it started with increasing vacancies in the commercial division. This was followed by a lengthening of DOM (days on market) in residential and a long downhill slide in prices. I have always watched the commercial market as a bellwether of residential.

roddy6667

Any chance this was localized, like Houston seems to be 2015-present ? Did you see the trend repeat after 1988 in CT ? I bought residential in So Cal in 1988 and it went up 7% / year for the next 3 years until I sold in 1991.

For commercial, a major change is in software companies where WFH is very much possible.

Management isn’t able to convince employees to come to office and the rewards for coming to office is lower than the rewards from switching jobs!

The attendance in these companies remain around 25%.

Homes in Seattle area, that are close to offices, are still marked 70% over Prepandemic price. Forcing someone to come to office is forcing him to become poorer from buying and unaffordable house.

So office REITs are not recovering soon.

Houston isn’t localized now. Read the article.

Commercial is not localized to Houston now – that is obvious. I was wondering about a tie to residential. That may have been a one off thing in CT in the 1980s?

Probably a stupid question, but does a REIT ONLY INVEST as opposed to Simon Properties (they own or run two local covered malls) making them a developer or management outfit that a big REIT would only invest in, providing them funds to do their thing?

These many levels of corporation structure drive me nuts….who OWNS who? Who REALLY calls the shots in the end?

Corporation;

An ingenious device for obtaining profit without any individual responsibility.

Nice comment.

Personally, I think that current real estate bubble is several multiples worse. It is only my feeling, having no affidavit that attests that I have any specific intelligence about the housing market other than hearsay.

The situation does force me too think about the future and how badly the future turned out for so many societies,

As far as the course of the expected collapse of the housing bubble, let me say one thing about it,

That the collapse of bubble in housing has begun and will collapse at it’s own rate.

In terms of current and future trends, I’ve lost track of the co-working office market and the extent to which it may be exploiting the opportunities that exist somewhere between WFH and WFO. Is there any insight worth mentioning here?

I recently came across an independent, new and quite upmarket co-working office space in a small but well heeled and geographically well connected University town. It was oversubscribed and an inviting place to work.

Flexible membership terms upstairs and free access on the expansive ground floor, covered by lunch, snacks and coffee purchases. Arguably better than working from home and the traditional office and not overtly competing to eliminate either.

I think co-working offices have become the golf clubs of the 1950’s. A place to network.

I always thought that was the ENTIRE purpose of golf, and still is. Nobody can network in basket ball or any other kind sport where age is a much larger advantage, not to mention height, body condition, stamina, speed, coordination, etc, etc, etc, that I know of. Not to mention it can be exclusive and expensive to keep out the “riff-raff”.

It’s where my lobbyist uncle made/maintained contacts and also did business.

I tried playing just once with him, saw it was difficult, but with no conditioning value at all unless one carried their bag, and then just drove the cart and went for drinks, or avoided it entirely.

Given enough “attractive” incentives, I would be compelled to co-work as well.

I find working from my HOME OFFICE still is cheapest

been doing it for 25 years now

well – break time is over and it’s time to go back to work

—

and during the pandemic I didn’t have empty office space

—

and the commute = down hall and to right

Another set of numbers retrace to levels further and further back in time. Things may level out for a buy and hold investor, but the question increasingly looms, how long might that take? And how long will it take for each tranche of investors to bail out? Which of course has the obverse, bargains, but one had better be darn picky. There was a time when everything hit a bid, and that was so recent, but time does strange things when markets undergo a regime change.

Level out for long-term buy and hold “investors”?

I think a more accurate analogy is Rockefeller Center Properties in the early 90’s. It too had a high yield until it went bust and the dividend was eliminated.

That’s where I think practically every one of these REITS is headed, eventually. The economy isn’t even officially in recession now and the stocks have already crashed.

Once the pink slips start flying and credit conditions tighten a lot more, over leveraged companies (which is most) will have (far) fewer employees and cutting expenses to stay out of bankruptcy court.

The problem for REITS is that they frequently bought at bubble prices, are overleveraged, and can only stay solvent at inflated rents with a fake economy.

It’s a problem for current lenders and “investors” but nothing that can’t be resolved by foreclosures which will allow a new owner to charge lower rents and still make money.

Augustus, your program for the collapse of western civilization seems plausible if not probable, but is not likely.

Because the powers that be will not allow it. I remember back in 2008 and my father in law was encouraging me to buy the market. I expressed my bear market scenario to him and still remember his response:

They’re never going to let that happen.

Shades of Ozymandias.

Hey Wolf, it’s interesting that all of these firms share price seemed to go up during the pandemic… was it the Fed buying into the Corporate Bond Market (bail out for REITs) or just the sloshing of cash?

Interest rates explain all of this. REITS go up in declining rate environments. All these were sells when the Fed started raising rates, and they won’t be buys until the Fed stops raising rates.

Considering the interest rate cycle almost certainly turned in 2020 after a 39-YR bull market, that’s several decades.

I made quite a bit in REIT’s debacles of past

mostly by finding best quality, waiting for right time

and buying PREFERREDS with great yields

Wolf is right,WAH has changed the market in dramatic fashion and was never figured in when they built these office buildings. There is another factor that will affect this market and that is automation and technology itself. A lot of jobs have been shrunk,duplicated, and eliminated by leaps in software and the cloud. The precious job I had at a big Semi truck parts warehouse gutted most of the front end office jobs with auto billing the automation of the process with the dealerships.

The job I work now is a ISP that is in growing markets, providing 1-2 gig fiber. Areas like Bend.OR, St George,UT, Boise,ID, Mt Juliet,TN, and others are booming. Now, a lot of this is rentals, so we will see how the interest rates affect this. But we have a virtual company for the most part and we have cut in half the number of people who are in mgmt and admin. So if we all went back to the office, my company only requires 2 floors if a small office building, so no big office space req. at all.

They might fill some up with government divisions or if they can increase new startups , but otherwise Commercial is in trouble.

The Pressure/Benefit of Automation Processes is now

Ramping up.

One Firm I work with went from 150 Front End office workers…

(Many Legal Bookeeping/Accounting and Tax Specialists…

Who thought they were “untouchable” ).

Down to 15 and they Tripled the Volume…

A major Legal Firm I work with

Total re work of the Business Process…

50+ Staff

Down to 3 now, again Double the Volume and climbing…

Dumped the expensive office downtown too..

Everyone works from home…

Layoffs

Not Just for Blue Collars anymore…

White Collar workers are now a very tasty automation target…

Futures up nearly 2%, looks like happy days on Wall Street are here again!

Inflation is conquered and tightening is done! /s

Sadly yes. The pivot has been broadcast.

There is no pivot. In fact, the entire economy is so awash in cash that more of it came roaring into stocks today, to BTFD, that the FED is going to uncork another massive rate hike to try to cut the legs off of this out of control monster they have created.

First, BOE (sorta)

Second, RBA (smaller than expected hike, HUGE rally on their market)

Third FED?

I’m waiting for your hawkish speech Mr. Powell. The market is calling you out once again.

Hahahaha, everyone of these bounces makes it that much easier for the Fed to hike rates — we’ve seen that time after time this year. Now that the wailing and gnashing of teeth on Wall Street ended with this bear-market rally, the Fed can go on about its business of hiking rates. Been there, done that.

For nine months now I have been reading this “Fed Pivot” fiction here with amazement, while in reality we got the most aggressive Fed rate hikes in 40 years. People are just loving this Fed Pivot fiction — it’s similar to romance novels, I think.

BTW, the BoE’s “QE” has already fizzled to nothing.

Additionally, it looks like every one of these recent bounces happens exactly in line with major support levels. You can almost set your watch to it.

Let’s see if the market continues higher and $SPY touches $390 around 10/14 when the Fed minutes are released OR if more drastic measures are taken as a result of the Fed closed door meeting to kill this rally / squeeze.

Also, since I was caught in Hurricane Ian (about 30 miles N of Ft. Meyers) I am just now getting access to power and internet so go ahead and recall the Search and Rescue team as I’m back in the comments, baby!

Wolf

Since I was unable to comment, on time (due to the FL weather), in the “UK Chaos Econ” thread, I hope I can use this thread to post a question:

With the BofE stepping in to bail out the leveraged pension funds, won’t this create a possible circle of QT and money printing? Especially if similar retirement funds, that were designed to be low risk but forced into a riskier approach due to ZIRP, begin to send out their SOS signals?

If so, then couldn’t this keep pushing the GBP lower, while foreign investors sell UK debt as yield goes down, applying even more pressure to the GBP?

If this is all possible, then BoE might have opened themselves up to another 1990’s style attack as it might cause some high-level investors to test its ability to keep up with this high wire balancing act.

The BoE has bought only small amounts of bonds on the first two days and nearly none on day three (yesterday). It may be done buying bonds. This was a backstop operation to halt a panic, the panic has been halted. The possibility that this BoE “pivot” is already re-pivoting back to the tightening phase is going to be very inconvenient, and no one here is going to talk about. But I surely will when I see how it develops.

As long as the shills and mountebanks keep braying about a “pivot” it’s not going to happen. They need to be crushed utterly so that capitulation can do its work.

One weird observation: I’ve just received a couple offers from my credit card companies. 1 year interest free for as low as 2%. This makes no sense – I could go buy T-bills yielding almost twice that for near zero risk. I could go buy a brokered CD from the same bank yielding about twice that. iBonds are yielding a lot more.

Yeah, I know these are teaser rates and I’m not suggesting this as an investment strategy, but my point is this: I’m just a guy opening my mail. What if I was actually looking to borrow money and had relationships with bankers? It looks like there’s still a ton of money out there looking for a home, so much that lenders are willing to lend out below market rate to make… something?

So with the credit card companies, it’s not that they really want to park money at 2%. It’s that they hope you screw up (check the fine print, often if you are accidentally late on a payment on that card, or even on another unrelated bill, you get hit with the full 20% or whatever) and they can raise the rates, or that you don’t have the $ to pay it off at the end of the year.

I agree there’s a lot of money looking for a home, but this isn’t a good example of that, in my opinion.

Is this a balance transfer offer? Is there a cash advance fee associated with this offer?

Yeah I was going to say Wolf really made a GREAT market call this past weekend where he expected stocks to go up Monday/Tuesday.

Things can’t go to heck in a straight line and this looks like yet another bear market trap. Are buying programs deliberately hiking the prices to sucker in new retail money so the rug can be pulled out a week or two from now when things deflate once more?

Anyway, great call by Wolf on this.

Bad economic news will be good news for the stock market. Job openings dropped.

The more bad news that can pop up, the closer we get to a FED pivot. The stock market players want to always be optimistic and want stocks to go up.

The FED will eventually Pivot but nobody knows when. Market were oversold and this is not enough bad news yet. We need unemployment rate to start going up to really get close to a pivot.

Stocks were oversold and we were do for a bounce. Stocks have dropped a lot this year but forward earnings forecast have not. Thus PE rations have dropped a lot and actually, from a fundamental perspective, stocks are starting to look like a good buy at a PE of 18 when compared to the end of last year it was in the mid 20s. If you take away the big FAANG stocks, I think PEs are around 15.

I think we’ll see a lot of earnings misses this quarter. The “forecasts” are largely BS.

Stocks have also been “over bought”, “over owned” and mostly “overvalued” for more than 20 years. That’s how long the US stock mania has lasted.

P/E ratio is a lagging indicator and one of the worst measures of relative valuation. The only reason it has any value as an indicator at all is because the “P” IS the market. It’s also often high at market bottoms when it’s actually a good time to buy because earnings crash into the low. That’s what happened in 2009.

Earnings aren’t even real money, yet practically everyone uses an accounting number for market valuation.

“Bad economic news will be good news for the stock market. Job openings dropped.”

That wasn’t “bad” economic news: it showed a slight softening of the most contorted labor market ever, and that’s “good economic news”:

https://wolfstreet.com/2022/10/04/layoffs-quits-job-openings-hires-slight-softening-of-contorted-labor-market-amid-still-massive-churn-and-job-hopping/

I would qualify your comment as a raucous endorsement of, I’m not sure. Is it that stocks are undervalued or the end of the world is a buying opportunity.

1) FL massacre destroyed cars and homes. What will happen to bank’s loans.

2) The weekly Dow Nov 2/9 2020 gap is still open. If the Dow will close

it the weekly ma200 will turn down for the first time since Sept 2008.

3) In Sept 2008 LIBOR3 went crazy. It jumped above the 3M and Fedrate.

4) In Sept 2022 Ian and the British Pound sent LIBOR3 – SOFR to Mar 2020

level, but instead of rising vertically, it cluster together, increasing volatility for 7 months slightly under Mar 2020 high, but well below Sept 2008 high.

5) JP maginot line is rock solid, but the new financial system seismic tremors might destroy it.

1. Car destroyed. Bank / finance company is on title as lienholder and insurance company pays them first – the defaulted borrower second. If defaulted borrower has any intention of buying another vehicle on credit, it would be foolish to default. Many people are cheap and don’t carry comprehensive insurance – which is what covers destruction from natural causes. They get bupkus. Finance companies reserve for that event.

2. House destroyed? Must still make payments unless bank allows forbearance (but interest will still accrue). If borrower defaults, insurance company pays the lender as they, too, have a lien. After fees, etc., they may send the defaulting customer a bill. The property tax liability remains. The county requires the property owner to secure the area if it’s a hazard and the debris must be removed (and paid for by someone). The bank won’t want title as that liability falls on them. Many of those homes will not be allowed to rebuild as zoning has changed. The destroyed ones at ground level will either have to raise the home if they rebuild it or make it a vacant lot. (Friends of ours went through this several years ago in St. Pete Beach)

It’s a tough slog to get your personal property replaced. The insured may get an emergency “advance” of $10k or so, but will need to reconstruct their possessions on a claim form and, if the hurricane blew them out into the ocean, it’s tough to prove to an adjuster that you had an 18K Rolex Daytona that you got as a gift from your ex-girlfriend who returned to Russia.

If you read your homeowners policy, the expensive toys must be insured separately. No proof – no pay.

Cool that you posted a bread crumb trail for our brothers and sisters in FL whose property has been destroyed by nature.

I keep telling my wife, it may be boring but there aren’t any regular, natural disasters that are liable to change our base understanding of what the hell is ones place on earth.

Sitting on the couch one day drinking beer, the next day fighting the insurance company for compensation for the loss of one’s home and ride.

I can’t imagine why a significant portion of the population chooses to commune on the coasts of these here United States of America.

I grew up in the mountains, seeing the ocean for the first time when I was too old to get the vibe.

I got a different vibe which included a dark secret in my teenage years about yearning to go to the summer of love. Leave the solitude of the mountains for the calamity of the city on the coast.

The day before the bad weather rolled in, I glanced at the front page : “6 Property Insurance Companies Declared Insolvent.”

Insane – no sanity

Insolvent – no solvency

Inhumane – no humanity

Insurance – no assurance

This is where the new ESG credit scores are making a big impact in business dealings. The current framework embraces WFH and asks orgs to lower their REIT carbon footprint. This is for good climate best practices established by lending orgs. Implementing these practices ensure discounted interest rate business loans and tax deductions. Sometimes cost savings in the millions. The only way corporate REIT can fight this is if communities charge extra taxes for headcount that would be in the office. Some small towns are getting desperate for income from foot traffic WFO brought. As WFH, my salary is not the best because of the flexible schedule related to WFH. When I asked about our small raise, and the fact that housing (near the office) is 7 x our average salary, they said we are WFH. They do not care where we live as long as it is in the USA. I am not beholden to the location. As you can imagine, the city that paid for all of the expensive infrastructure for this headquarters, is not very happy. Not to mention affordable housing is over an hour away. Those town are getting hit with a housing boom. Unfortunately, that is pricing others out. The question is what happens if or when WFH ends?

I just finished up a WFH stint with a large global enterprise (approx 120,000 headcount). A very large percent of workers in the IT/developer departments of this firm are 100% WFH, and out of state or country from any physical office. Unless this company has a dramatic downsizing/layoffs in their future (such a scenario would surely be part and parcel of a global economic crisis/great depression), these workers are staying and aren’t going to be replaced.

WFH is here stay for industries where it is possible. There is no going back and it is a good thing. There will lots of one and two day a week in office or in office for monthly meeting type things. You can bank on it.

>The question is what happens if or when WFH ends?

I don’t believe it will, nor can, at this point. When you have whole industries (such as software) forced into WFH, and discovering that it has benefits for both the employer and employee, any company trying to revert back to the WFO model will quickly discover that its employees understand that they can now work for anyone in the industry across the country without having the “move” hassle of even moving their computer across the room. I can’t imagine how the entire industry would be able to, or would want to, shift back to WFO simultaneously to stop this brain-drain effect, especially as VR is poised to make WFH even more like being in a physical office.

As you pointed out, though, this change in work model has caused significant changes to many communities whether urban, suburban, or rural. We’ve had probably several decades worth of normal work model evolution happen as a big bang in the first three months of the pandemic. This leaves a lot of known and unknown problems on the table.

I wonder if Houston’s Wild West zoning will actually help them when it comes time to convert the vacant office space to housing or other uses (not sure what that use would be, though). Because all of their office space is so spread out in residential, industrial, commercial, etc it doesn’t mean a bunch of towers all centrally located. Who knows, maybe a bunch of towers together all converted to condos and multi family rentals would be good, too.

I wouldn’t be surprised if our crazy politicians in California decide it makes sense to rent them and house all of the country’s drug addicts in them as a solution to the “housing crisis”.

Regardless, it’ll be interesting to watch what happens.

I’m sure it would cheaper to knock those towers down than to convert to residential.

Just the asbestos and lead paint remediation would be costly.

A trend we will see this winter in Europe, and perhaps here in a few years is work from home fading as people head in to the office to get warm for a few hours a day. Large, multi-floor commercial spaces stay warm without much heating. The opposite might be true in places like Florida and Arizona where people might want to spend the day in a place where the company pays for increasingly expensive air conditioning.

Looks like we are back to Pivot Hoping.

Yes. And notice how the wailing and gnashing of teeth about the Fed “breaking” something has suddenly died down?

Every one of these bear-market rallies makes it that much easier for the Fed to do this business of hiking rates. The market is now giving the Fed another all-clear-for-a-rate-hike signal.

This is how the market digests those rate hikes — I’m going to do some more thinking about this because it may be worth an article. This is why the Fed cannot hike too fast because the market won’t be able to digest the rate hikes. And these rallies are part of the digestion process. It’s messy — like all digestion processes — but it seems to work.

That’s an interesting hypothesis and if you can identify the pattern you can make a ton of money playing it.

The counter-trend is set, right now, by the other central banks actually turning more dovish, not the Fed yet.

Front-run every big economic number and Powell speech? Next big one is the unemployment report on Friday morning.

But by not hiking fast enough, the patient lingers in hospice care.

Powell needed to be doing 1% hikes at every meeting since last Winter.

I see the UN is pressuring the central banks to implement price controls over hiking interest rates. First, isn’t that stepping on the toes of independent FEDs in most countries. Second, in America isn’t it the FTC that should be over the price controls in the forms of monopoly controls and anti-trust laws? Such as Amazon not getting into health care? Or fleecing Americans with price gouging? Finally, can the UN have an impact on our Feds pivot plans? I am curious to see if they can control the “fleecing” of house prices by taking the National Realtors and Mortgage orgs to task. However, because the Fed owns MBS isn’t that conflict of interest?

Since when is ANYONE listening to the UN?

Aside from the obvious, ” Who cares what the UN thinks”, the issue:

“I see the UN is pressuring the central banks to implement price controls over hiking interest rates.”

The strong dollar and rapid interest rate hikes with looming QT in the face of an abundance of currencies losing value as a result of QE, seems like a recipe to precipitate a dislocation in the financial system.

Foreign firms that borrowed in dollars are finding their dollar cash flow debt burden is not sustainable. They have to raise prices to stay in business.

Perhaps, that is why the UN is warning about the effects of interest rate hikes and suggesting price controls may be less painful.

It is a real problem.

These other countries need to raise their interest rates ahead of the Fed, and if they did QE (Japan and European countries/Eurozone), they need to do QT. The Fed gave them a year’s worth of warning.

The countries that have raised their interest rates starting in early 2021 and well ahead of the Fed — such as Brazil and Mexico — and I covered those, they are doing just fine, and their currencies are holding up just fine against the dollar. It’s the laggards whose currencies are getting crushed. And they should get crushed. It’s self-inflicted wound, and they should stop blaming the Fed.

Regarding Boston’s real estate market, there’s a lot of conversion of existing office space to life sciences. While it doesn’t seem to effect the new Class A, many of the other real estate including older and suburban Class A, retail, and Class B space is being converted by both major players such as Alexandria and smaller regional and new entrants.

Reminds me of the WeWork types Wonder how they are fairing in this environment.

Initially, I’d guess they would be suffering a lot more than the various firms whose charts are shown.

But, then again, wonder if a side effect might be office centric type firms looking for less “permanent space” as a sort of hedge against where work from home may be headed.

Weird world eh?

Adam Neumann is a billionaire. He’s doing just fine.

I advanced a similar line of enquiry.

WeWork and similar may not be precisely REITs related but they are part of the broader picture.

Wolf,

Very interesting and I read the reports from Savills and closely read your analysis and it’s right on target!

I’m a member of Seeking Alpha and I checked their ratings on Boston Properties (BXP) and was shocked, and here is a brief rundown of their ratings, – from 1 to 5:

Quant Rating – 3.0 – (Hold) – (it’s a AI like formula of 100+ variables, or so)

SA Author Rating – 4.5 (Strong Buy)

Wall St. Ratings – 3.9 (Buy)

Ironically the author who called it a (Strong Buy) published his article Oct 2, 2022, and their is about 50/50 agreement, and disagreement in comments – I think he’s crazy!

I will send the whole report if you want it.

Also good call about the market rally for Monday, and this market reminds me too much like you said of the 2000 dot com crash, and a whole host of big names like Ray Dalio, Jamie Dimon, Nouriel Roubini, Jeremy Grantham, etc have warned of the coming disaster too – I won’t argue with these folks.

The UN has now joined the chorus of “moar free money!” LOL

Birx: Jirx wirx.

*** Typo Alert *** “but” should be “put”

“In Los Angeles, the availability rose to a record 25.4%. And sublease space jumped to 9.6 MSF, from 8.2 MSF a year ago as Netflix and PayPal but some of their vacant office space on the sublease market.”

You report mind bending data so dispassionately, that it would be easy to miss a seismic shift in the economic reality that the data represent.

Office vacancies of 30 pct in the glow of excess, anchored, speculation.

One never really knows which way the wind is blowing, on average.

I felt disgust, watching the feeding frenzy that occurred on Wall Street this past two days. The averages up 5% in two days. I can’t shake the image of the wall street wise guy selling a bloke a share and, immediately, borrowing it back and shorting it.

I have been toying with the idea to approach the Las Vegas casinos and proposing that they should offer their poker chips as a competitor to bitcoin. Just a thought, destined to be shot down by reality.

The backdrop is so human. With dower predictions that the credit crisis is already underway from several, credible sources that have the intestinal fortitude to publish their misgivings.

Such as Roubini and Yves Smith, not one to swap lies.

Meanwhile, the keggar dominates another day.

I assert the following statement, well aware that there are opposing imaginations, that shall rightly have their opportunity to autopsy my comments.

The model of a privately owned Federal Reserve has clearly failed and should be replaced with a National Bank agency that is more attuned to the interests of the vast majority of citizens.

Don’t get me wrong, I’m grateful that none of the wall street wise guys suffered the last time they set off a significant financial shock as a result of their malfeasance in the housing bubble . (snark)

Funded by a captured Fed without the sense of a spavin jackass.

I’m coming round to the idea that, perhaps, the FFR at 4.25 by December is a bit aggressive, given that state of speculative, financiaily vulnerable firms that were spawned by the Fed’s manipulation of the value of the currency, these past 15 years.

Europe is in entering rehab from the addiction to QE, enough cash in circulation to force the interest to zero, or below.

I remember asking a passing family member, watching their response to see if they had a similar historically based precarity. The question was:

Would you lend Italy $1 MM for 50 years at -.25 pct interest. I said no, I wouldn’t because it seemed irrational.

Good. I shed zero tears when rentiers get it in the neck.