Huge losses, but now revenue growth is slowing. Hilariously, executives refer to the huge losses as “profitability.”

By Wolf Richter for WOLF STREET.

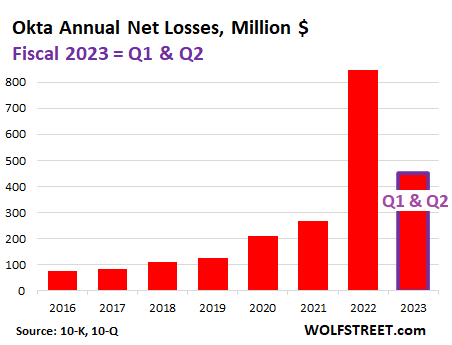

Okta was founded in 2009, went public in April 2017, and isn’t a newbie startup anymore. But last night, it reported another huge net loss for its second quarter ended July 31, of $210 million, on $452 million in revenues. Its losses have increased every year since it started disclosing them seven years ago and now total over $2 billion.

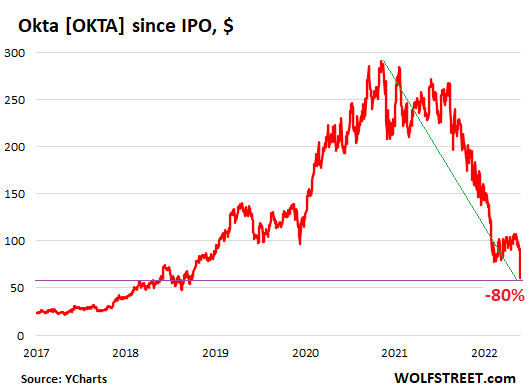

But since the infamous February 2021, when the hype-and-hoopla show came unglued, these types of stocks began to plunge, and I started tracking them in my Imploded Stocks column. Today Okta joined the club that already has hundreds of members. And it did so with flying colors. Its shares [OKTA] kathoomphed 35% so far today, to about $59 at the moment, back where they’d first been in August 2018, and down by 80% from the peak in – you guessed it – February 2021 (data via YCharts):

Okta, which sells services to companies that allow their employees to securely access corporate cloud-based systems, has been following the Silicon Valley dictum of using investor money to buy revenue growth – 42% revenue growth in Q2 – no matter what the costs, because the stock price will keep rising if revenues grow, regardless of the net losses because growth-befuddled investors will ignore net losses and focus on some homemade metrics and revenue growth, according to this dictum.

This formerly sacred and now rotting business model worked for years: Okta’s shares shot higher from its IPO price of $17 to its first-day close of $23.51, for a 38% first-day pop, and then shot higher from there to ultimately $294 intraday on February 12, 2021, before it all came unglued. And it has so far generated over $2 billion in net losses doing just that, with no end in sight.

Today’s plunge of the stock – just the latest in the 16-month implosion – ostensibly occurred because the company lowered its guidance for its billings and revenues for the rest of the year.

During the earnings call (transcript via Seeking Alpha), executives blamed the lowered guidance mostly on “sales challenges,” “integration challenges,” and “sales attrition” related to Auth0, which Okta had agreed to acquire on March 3, 2021, during peak hype-and-hoopla, for $6.5 billion in stock.

The acquisition was just another way in which Okta attempted to buy revenue growth. And now the deal isn’t working out so well.

CEO Todd McKinnon blamed “challenges related to the integration of the Auth0 and Okta sales organizations” in part for the cut in guidance. “I recognize we have more work to do to regain our momentum. We’ve taken some decisive actions that we believe will get us back on track,” he said.

CFO Brett Tighe blamed the cut in guidance on “sales integration challenges” and on “heightened sales attrition, which resulted in a lower-than-expected capacity build as we move through the year,” and added that “a smaller portion” of the blame for the reduced outlook is “related to the macro environment.”

And as you’d expect when an earnings call takes place while the stock is kathoomphing in the background, there was a lot of linguistic hilarity, including about the huge net losses.

No one during the earnings call – particularly not the analysts – made any fuss about the net loss in the quarter, or the prior net losses. On the contrary, CEO Todd McKinnon said, “We produced better than expected profitability” – the term “profitability” having replaced the unpleasant term “net loss” – and the analysts ran with it.

Other executives chimed in about “improving our profitability outlook,” etc. etc., meaning that they want to reduce the net losses from huge and growing to hopefully slightly less huge and declining.

Alas, for Q1 and Q2 of the company’s fiscal year 2023, it lost $453 million, a 17% bigger net loss, I mean bigger profitability or whatever, than in the same period in 2021. Its net losses, I mean profitability or whatever, have increased every year since it started disclosing them with fiscal year 2016 (ended January 31, 2016) now totaling over $2 billion, including the $848 million last year and the $453 million in the first half of this year (fiscal 2023):

Trying to get these losses under control, now in this new environment, means layoffs. Okta has started the process, as many of the other companies on my Imploded Stocks list have done. But as with the other denizens on that list, the scale of the layoffs is still minuscule.

Last week, Okta’s head of global sourcing, Jody Simon, announced on LinkedIn that the “entire US Sourcing Team at Okta has been eliminated.” Later Okta confirmed that 24 people were laid off, around 0.4% of its total global workforce. So that’s not going to cut costs by a whole lot, but it shows that they’re now grappling with the end of an era.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Okta, which sells services to companies that allow their employees to securely access corporate cloud-based systems, has been following the Silicon Valley dictum of using investor money to buy revenue growth – 42% revenue growth in Q2 – no matter what the costs, because the stock price will keep rising if revenues grow, regardless of the net losses because growth-befuddled investors will ignore net losses and focus on some homemade metrics and revenue growth, according to this dictum.”

Another symptom of the FED’s grotesque money-printing scheme.

One reason we have so much inflation is because instead of letting the Okta’s of the world go BK, investors have been borrowing from the Fed on the “fake it till you make it” business model. All that borrowed money sloshes around the economy, pushing up demand in the face of physical limits to supply, creating inflation – but all too often there’s no matching business value.

Consider what happens when the money supply increases faster than the economy can grow. Those who receive the newly-created money & credit feel wealthier, and spend. But at first, no one else feels poorer … until the inflationary price increases hit.

That fits the classic definition of “bezzle” — J. K. Galbraith’s delightful term, derived from the situation when an embezzler starts spending someone else’s money, and both feel richer for a time — until the victims recognize their losses. Galbraith generalized the concept in his book about the 1929 crash — all forms of fake, unsustainable wealth are “bezzle”.

The bezzle today is tens of trillions of dollars. The losses are now showing up. And nearly all of us are losers due to the inflation.

And of course the financiers and their pet politicians will make sure that someone else feels the pain they caused.

US has lost all manufacturing. It’s trying to pretend to be the centre of innovation for higher complexity solutions that can provide greater productivity.

While the cash burning unicorns were supposed to be the side effect, it looks like they have become mainstream now.

I say it’s still not late to un-financialize the whole system and bring core manufacturing back.

That is odd, because US Industrial Production is at all time highs. And 500% higher than the glory industrial days of the 1950s.

https://fred.stlouisfed.org/series/INDPRO

Yep. Almost zero industrial growth in the last 22-years. Thank Goodness we have all these financial services in place to shuffle around ephemeral money to add to our ephemeral GDP😀

That’s the Cantillon Effect you’re describing.

WS,

And the other important thing to never forget is…the enormous/insane interest rate subsidy that kept these lobotomized companies alive and incinerating came from a *Fed forced* transfer of *hundreds of billions*, *every year*, for nearly *20 years*.

By gutting mkt interest rates from 7%+ to 4%+ (or less), every dollar saver on the planet was expropriated. For decades.

(Essentially all fixed income invts are priced at a spread to manipulated Treasuries, so the entire fixed income savings base – tens and tens and tens of *trillions* – saw its returns artificially reduced by 3%+ for many, many years. By Fed fiat (ahem).)

The theme in investor calls this last quarter has been that management teams are reigning in expenses to cut the red ink. But what they dont tell you is that by doing that, they are actually going to stop any growth. The whole reason this is an issue is that the underlying companies have a busted growth model – meaning no organic growth and a negative payback on investment in spending.

I think that the gaming company Skilz fits perfectly into this situation. They have cut marketing expenses, but that has dropped revenues. Sure, they now have a lower loss, but it is my belief that the cut in marketing expense will keep revenues plummeting every quarter. Actually, what they termed marketing was actually free money they gave to new customers to compete in their online competitions. Once they drop the free money to newbies, the whole ecosystem collapses. The stock market also cheered the cut in marketing expenses for Lemonade and I also think this company doesnt have a path to break-even.

On the other hand, one of the few SPACs I think is a winner is HIMS. When the company IPO’d it projected 30% yearly growth, but it is now growing at about 87% year over year. In the most recent quarter they actually increased marketing as a percentage of sales. But the difference is that this is a subscription business with payback on marketing expense of 6 months to 1 year. Management said they were leaning into a less competitive advertising environment with more marketing spend and the stock fell a little the following day. Which was the wrong reaction. When a company can lose a small amount of money and grow at that rate, they should do it. They will reach break-even within a year simply by reducing admin as a percent of revenues.

What the stock market doesnt get is that it is the underlying business metrics that are the difference between a company that should be losing a little money so that it can grow into scale and a company that is just burning money and doesnt have a reasonable ROI on marketing expense.

Not every SPAC is going bust, a very few will be great, but finding the gems is not easy and the trajectory can change rapidly, so it is important to get sense of how long the runway is.

What does HIMS do? Handle bankruptcies? If that’s case they will have a lot of growth.

Their 5 year chart is dreadful, and the net profit shows them hemorraging cash.

Ughhhh, the DotComBomb exploded for the same reasons! Had nothing to do with the Fed printing back then.

It’s a CONfidence game & the more they can make you believe er buy, the higher their stock goes! Who do you think you’re buying from in the 1st place?

I mean, seriously, why is FB (META) in the S&P or called a tech stock? To get it into the stratosphere!

Almost $500 billion in losses in the first 6 month of 2022. And an accelerating trend over time…

You can’t get there from here.

“Trying to get these losses under control, now in this new environment, means layoffs.”

“Almost $500 million” with an M, but still :-]

Saw billions and was thinking that’s Uncle Sam type losses!

Surviving the Dot Com debacle I have been wondering when Tesla and Microsoft will fall into this same rut. I’m not a professional investor but see some similarities in the corporations. I think Mr. Musk might have bit off more than he wanted with his Twitter bet. Time will tell but just a thought.

Microsoft is so deep in so many pies, many of them government contracts. It is not just a software onramp to somebody else’s cloud.

Tesla may well hear the thundering of other EV makers approaching from behind. When I buy an EV, just offhand I figure on Honda or Toyota. I will not put any of my eggs in the basket of some eccentric aging playboy wandering off into twitter beefs, etc.

I always here conflicting stories. Most people say they like their Tesla very much but then JD Powers is not so glowing.

JD Powers ranked Telsa quality at 30 our of 33 brands. Others will offer good competing EVs where the quality may be better but maybe not cutting edge as Tesla.

The problem there is that Musk (and by extension, Tesla) have a cult following. That means that, for those people, their impressions of their cars will always be colored by their faith. It’d be like expecting a religious person to give you his honest assessment of his church’s leadership.

I’d put much more stock in the professional car reviewers for the meme car manufacturers.

“The problem there is that Musk (and by extension, Tesla) have a cult following.”

I can’t stand those kinds of sycophants, I don’t care what or who they follow. It’s like Jonestown without the Flavor-Aid.

I loved them at first or at least the idea, the silence and the speed until I drove in one and was shocked. The iPad dashboard was my 1st clue this thing was just slapped together and it made me want to check my MySpace Acct. For any updates!

Cmon Mush, you could at least have that iPad fold back into the dash when parked or not needed. It just looked stupid sitting there and I felt duped! I don’t even want to drive it!

I am waiting for a M-B electric car. Not in any rush.

I am waiting for a used M-B electric car that’s nicer than the B-class (B250e, with 70 mile range).

Why? I can’t afford a new MB, but my very used 2001 E320 has been solid. I’m hoping that with a simpler electric motor, a lot of the potential maintenance costs will go away. But it’s good to wait and see a bit, because traditionally the Germans have been stronger on quality mechanical systems than electrical (but definitely better than Jaguar’s electrical quality).

Musk is a con artist, not a car guy. He’s lucky Tesla has gotten as far as it has.

He’s a longtermer, an outlandish pseudoscientific religion. ‘Nuff said.

Seriously?

Talk to people like Sandy Munro (who knows cars) and then comment.

He said he has never seen a car CEO who knows anywhere near as much as Musk does about everything from materials to processes.

Microsoft makes products that people will actually pay for. I bought my first Windows computer back in 1992 and have been using Windows ever since. I am not as confident about Tesla. Its cars are expensive and, reportedly, its after the sale service is terrible.

MS makes products people used to pay for. Most people can do without paying for office. LinkedIn is a dud. Bing is kinda poor. Azure is viable right now but google cloud cold put serious damper on it.

Azure is doing quite well over Google Cloud but they both are far behind AWS (Amazon).

Tesla had the benefit of being a first mover in the EV space, but the big automakers are catching up quickly. Rivian is getting hammered right now, but if they changed their business model to serve delivery trucks and vans, they would get a huge boost.

AWS revenue growth was dropping each quarter before the pandemic and then the pandemic gave it another growth spurt, but now each quarter growth rate is dropping. And the gross margin on AWS is dropping. I think Google is willing to buy business growth with pricing and AWS will have a choice to cut profits even more, or lose share.

Tesla owners in Finland are supposedly on hunger strikes over the poor service. Don’t ask, nothing makes sense anymore.

It’s in Norway.

The “Hunger Strikers” said (it doesn’t appear to have been confirmed by anyone outside the group!) that they had been on “Hunger Strike” for 24 hours.

If this is a representative sample of Norwegian Tesla owners, I’ll fly over and sell them a few bridges!

Ms is an awesome company but the current valuation is too rich before of cheap money.

Itd come down for sure and it is coming down little bit everyday

TSLX seems like such an easy play.

TSLQ my bad

I haven’t had a computer other than my phone for several years. Bought a Windows 11/Microsoft laptop. What an absolutely terrible experience. I couldn’t believe how the 2 systems have completely strangled the experience. When I tried to download freeware, I had to get permission and then it went into a freakout tailspin making it impossible to download freeware. The operating system is like a private owned jail where the inmates pay for their time. I took the machine back to Best buy for a refund and they now have another open box discount. Bought a Chromebook, so much nicer.

“The operating system is like a private owned jail where the inmates pay for their time.”

That’s the Software as a Service model. You can’t just go to Best Buy and get the MS Office package any more. A lot of users either stuck with Win7 or went to Linux because SoS is intrusive and abusive. Lot’s of built-in bloatware and spyware. Some people dislike having to pay Big Brother to enforce their totalitarian affections.

In all these years MS never did fix their leaky OS kernel, so it’s an abomination for large-scale mission-critical services. Overall it’s amazing how rich you can get on nasty monopolistic practices.

Is Linux a viable operating system for a personal computer? I have set up a server through command line with Linux but never set up a desktop with it.

Linuz is completely fine, unless you use Adobe products, or other software which is only made for Win/Mac. Unfortunately I use Serato which is only available for Win/Mac.

It has come a long way from a few years ago.

(I’ve installed several distributions over the years, the last being Debian last year – which I surprisingly found to be more usable than Mint or Ubuntu.)

I hate Microsoft, Apple and Google. What are my laptop options now?

I’ve been a happy System76 laptop user for about 4 years now.

System76 is nice as they support the hardware and they have software updates (patches) and upgrades of long term support (LTS) versions of Linux( I started with 16.04 Linux and now running Ubuntu 20.04.5 LTS, and recently got a notification that 24.x.x LTS is now available).

You can also get linux from Dell and others as well.

You can also download and install Linux onto a older machine though you need to do your own research and troubleshooting compatibility of hardware, firmware, software. Complicated sometimes finding reliable advice but doable if you have the patience and interest.

I’m so hoping Musk gets toasted by the whole episode. It will beautifully enable us to witness the end of financial capitalism, as it eats itself to death in a court over who handles the ticking time bomb that is Twitter. So yes, Tesla too – don’t know enough about Microsoft, but I’d love to think that they were vulnerable too. If now isn’t precisely the right time for a new cooperative movement to emerge and boss business, then when the hell is?

Who could know that making an actual profit would be so hard? So weird that the numbers are not 1:1 between revenue at Net loss and profit…

I wonder whether “making an actual profit” was the business model, at all. Finding new-age suckers was certainly prominent, calculated or not. “It might work” is an arguably valid basis for a side bet, in a time of funny money.

“linguistic hilarity”…Priceless…

OK, so maybe it’s because I’m a new guy and have no formal training in investing or how to run a company. But it looks to me like these doinks over at OKTA have never turned a profit in the entire time they’ve been publicly traded. How exactly is that supposed to work?

It works just fine for the yoinks over at OKTA, they’re still getting paid!

Pablo,

As long as they don’t run out of your pension money they will be ok. They don’t need any stinking profits.

In 25 words or less can anyone actually say what the heck OKTA actually produces or provides that is unique and cannot be secured elsewhere if it is really needed. 😉😉

They’ve got pretty good lock-in.

According to my math, Okta has 6,000 employees.

Fortune 100 contracts with friendly buy-ins. It’s all about who you know. SSO are tricky in enterprise environments.

Okta produces Magic!

If you work remotely while traveling or from home, it provides a secure encrypted VPN channel (That can be monitored) to a corporate location.

This will prevent anyone stealing my WolfStreet posts (along with other secret documents that I have lying haphazardly in front of my laptop camera. Just kidding, of course, Mr FBI person)

Never run a Netflix movie on your laptop while traveling with Okta enabled.

IT Security will contact you.

What happens if I download a movie from torrent on OKTA enabled laptop?

Since there is server processor overhead to create a secure encrypted channel, running Netflix or downloading Torrent will have the same result.

IT security is used to secure E-mail traffic. They will contact you.

When I worked for Cisco we had secure VPN tunneling for working from home over 20 years ago. This is not new.

What a mess and yet the stock still traded which means someone at the casino is looking for a greater fool bought today. MDB experienced a similar drop. SPX and Dow ended higher after the 10 year continued the march upward with inflation now under control according to the main stream media financial outlets. Were were they the last 4 trading days and like Wolf predicts will start to ratchet up with the rhetoric on the Fed needing to stop QT and declare work done already!

RSI is at 8 thus we are oversold. I would not be surprised if we see the July bottom visited as long as rates keep going up.

Too bad that stock investors have to actually find good stocks backed by good companies to make a dime now. The good ol days of QE-no interest easy pickens are gone. But it’s never been about solid production material growth for the country since QE began so no one knows what a quality company looks like. Take it to Vegas guys.

Brant Lee

“Too bad that stock investors have to actually find good stocks backed by good companies to make a dime now”

B/c Price discovery was actively suppressed by Fed. Besides at ZRP every asset looked ‘great’ along with Fed’s put. Now no more Fed’s put. Stocks have to be picked on fundamentals. Very few out there since stocks still over valued.

More money will be made by going ‘against’ the mkt (with hedges) than being invested for long, for the next 1-2 yrs.

Many are loathe to go against the mkt. Hence many will end up holding the bag.

“heightened sales attrition”…first time I have ever heard this term.

Is it:

Sales you already have that are leaving the place?

Sales you planned on but went elsewhere?

More sales leaving than you thought would leave?

Sales you had dreamed about but you can’t remember the dream?

Wow, just wow! What a clown show.

I think it means that when they did the merger with AuthO, the sales teams for the two companies got into a pissing contest, and more-than-expected salespeople quit to take better jobs at less-doomed companies.

A polite way of saying that revenues were impacted by management screwup.

Whoever bought at the top, coincidentally when Memestonks were being pushed by the mainstream media, is suffering a huge loss.

The American middle class continue to be robbed blindly and scammed by the whales and uber rich.

Reminds me of those pushing trading cards during 2020 Fed Money printer. The prices peaked in 2021 and are collapsing.

I saw a young stocktwit person last night saying by Okta on this dip. I looked back at their past 6 months of trading and they think they are a dip buyer but they are actually a knife-catcher.

Maybe they had a good run in 2020 and part of 2021. But almost every dip buy they bought the past 6 months is lower now than their buy point.

So right now they are a knife-catcher. If the markets can rebound into the end of the year, they can be rewarded with the dip buyer label. But they need a good rebound.

We use this software at my employer and I have not been impressed. It seems to stumble over itself and require numerous re-logins at times. I can’t blame their product solely as I don’t know how it has been set up. Our IT department is not the most competent and doesn’t seem to have to answer to anyone.

But shouldn’t such a hyped product be somewhat idiot proof?

I do some IAM consulting and implementation for different providers. It’s probably by design and how your IT /Sec admins have the policies configured. Okta is actually the gold standard for IAM so I personally hope they continue to grow and innovate.

…a 17% bigger net loss, I mean bigger profitability or whatever, than in the same period in 2021. Its net losses, I mean profitability or whatever, have increased…

Wolf, your sarcasm is hilarious and spot on.

We used to joke about this in business school. If your company is losing money, you can become profitable by selling off the assets and buying treasuries. No need for expensive employees, offices or equipment. All the hard work you are doing to lose money is wasted effort.

A gorgeous Auth0 exit at probably 10x what the company was/is worth. When the currency used for the acquisition is that inflated, no price is too high.

“the term “profitability” having replaced the unpleasant term “net loss” – and the analysts ran with it.”

The job of a stock analyst isn’t to help firm clients pick good stocks (not retail clients anyway), it’s a form of marketing using “buy recommendations” to generate future underwriting and M&A business from the company they are supposedly impartially evaluating.

Once anyone understands this, the lopsided garbage ratings they publish make total sense.

As for Okta, I use their MFA product at work. I have no idea if it’s better than any others but doubt it. It’s a commodity product which anyone can create a virtual duplicate.

Whatever value this company’s products actually provide, someone down the line can buy the company for pennies on the $ or their intellectual property rights in bankruptcy court.

No big loss (except to their foolish shareholders) either way.

I work with a lot of customers. So I have OKTA, Microsoft Authenticator, Google Authenticator, Pulse Secure, and RSA SercureID apps all on my phone. Plus there are several more out there.

Okta probably hopes an Oracle, IBM, or Cisco buys them out as there are a lot of big players in this space.

I agree with you. That makes sense.

It doesn’t change that the numbers usually don’t add up. A low minority of acquisitions turn out to be smart buys (Disney of Pixar, Marvel, and Lucas Film. Google of YouTube).

Most turn into pumpkins long before midnight. I’d place MSFT buying both LinkedIn and especially Skype in this category. CSCO also bought some company I can’t remember with $10MM revenue for $1B back around 2001.

Augustus Frost: “the term “profitability” having replaced the unpleasant term “net loss”

Why not? Every noun nowadays seems to get a new definition. I won’t go there…

I’m reminded of a saying by Confucius: “The beginning of wisdom is calling things by their right names.”

Wisdom is lacking…

I do IAM consulting and implementations. Okta is actually the gold standard in the identity space. Much more feature rich and has a lot more integrations than competitors. Pretty easy to implement and manage as well. Their biggest threat is Microsoft. Microsoft has an inferior identity solution (though it is catching up) but it’s an easy choice for msft shops and appears cheaper as it’s bundled with certain licenses

The company I work for uses Okta. It is fairly painless and very easy to use. We’ve been using it for 5 years. It hasn’t changed with the UI which is good. I hope it is secure. No rumors on security issues, right?

It is back down to Pre-Pandemic levels. It is maybe where it should be.

The WFH hype Bubble is wearing off.

“It is back down to Pre-Pandemic levels. It is maybe where it should be.”

No, it’s value should either be zero or the net value of its assets.

If there is a reason why any company with cumulative losses of $2B and no viable path to profitability (and dividend payments) should ever be worth more, I have never heard or seen it even once. Only endless rationalizations.

Augustus,

With Open Source S/W, maybe you can get the same capabilities for free now.

That has been the death of many S/W companies.

Otherwise, corporate/government security is a high priority issue. Unless you are using secret documents as napkins at your desk at Mar Lago.

Okta claims to solve this. ( OK, there was one known issue last year that was quickly resolved.) At least there is someone responsible. Unlike Open Source S/W.

My point is that Okta is worth something if your and my company are relying on it for security.

The intellectual property is worth something, for now.

The stock should not be worth more than liquidation value if it can never make any money. Where is the evidence that it can and why would anyone pay even one cent to own a stock that is a perpetual cash burn machine?

That’s not just true of this company, but a huge number of (supposed) tech stocks.

People get caught up in the hype of how great a “widget” some company is selling and forgot that the company is in business is to make a return for their shareholders.

Augustus,

It depends why they are not making money.

They are likely making money from our companies.

What are they doing with this revenue?

Paying CEOs billion dollar salaries?

According to Wolf, they are trying to spend too much to acquire other companies to grow. Will this work? TBD…..

IMHO, the Okta stock growth during the pandemic was all driven by pandemic fear. Okta is now back to pre-pandemic levels so it may be a good time to buy. As long as you trust Okta management to acquire intelligently to grow revenue. I don’t know if the Okta CEO has a billion dollar salary or if the company has competent officers.

I have not invested in Okta ever. I don’t know enough.

A story that should be made into a film that depicts the end of capitalism.

Don’t worry Katie Bell, it’s not QUITE the end of the world.

Another Tech stock bites the dust back to 2019 levels on a bad quarter.

The Pandemic Stocks are returning to reality.

All it takes is ONE bad earnings quarter and Wall Street will punish them severely back to 2019 or before.

I hope nobody had pending RSUs in Okta, Netflix,Dell,………

Let me fix it for you: back to 2019 bubble level, but without QE and ZIRP. There’s blood in the water. The Fed is waiting for the first victims to declare systemic risk and restart the bailouts.

consumers are still awashed with money.

LuLU posted good ER AH.

A $150 Yoga pants from LULU is epitome of discretionary spending and there is no slow down.

People continue to underestimate the amount of money sloshing around out there. Case in point: There is up to a 3 year wait on some brands of bespoke men’s boots and clothing where it used to be a month or two. And it has nothing to do with a labor shortage.

By any rational calculation a firm that has lost $2 billion is worth -$2 billion, but remarkably enough plenty of investors use other types of calculation.

The Imploded Stocks aren’t the only ones facing disaster.

Numerous highly-respected professional investors are predicting an imminent severe stock market crash, most recently Jeremy Grantham in yesterday’s article on BusinessInsider and elsewhere, using words like ‘superbubble’, ‘epic finale’, and ‘tragedy’.

He did not use the words ‘exsanguination’, ‘detonation’, or ‘popcorn’ even though these are perfectly appropriate.

While it’s no doubt true that Nothing Goes to Heck in a Straight Line it is nevertheless also true that just about everything will wend its way there in due course.

“He did not use the words ‘exsanguination’, ‘detonation’, or ‘popcorn’ even though these are perfectly appropriate.”

Or “kathoomphed”, most appropriate of all!

CEO blamed “challenges related to the integration of the Auth0” and CFO blamed ““sales integration challenges”.

Neither one blamed their daddy J POW, and higher interest rates?

They celebrate record profits will suffering huge losses and paying themselves massive bonuses.

And Golden parachute themselves out while they destroy the company.

If everybody did this you wouldn’t have an economy, unless you suppose the hunter-gatherer model technically constitutes an economy.

This is how it actually plays out unfortunately.

Butters,

It is possible to work around Office…but very few do/try.

It is the default option (read safest to choose…nobody ever, ever gets blamed for going with MS) for almost every significant corporation or gvt agency.

I’m not opining on product quality or anything else – but MS is so deeply embedded that long after Apple craters (“you mean I can pay 90% less for an Android phone?”) MS will still be generating $150 billion+ in revenues every yr.

You could probably cobble together a *fully free* suite of products to replace every MS product, but almost no corporate/government functionary would ever take that kind of risk.

MS is what IBM used to be decades ago.

I didn’t dare to short OKTA, lol. Now, looking at the chart, it looks typical.

The market topped, now bounces will be easier to short.

“Growth at all costs” apparently includes the failure of the business as one of those “costs”, which makes the dictum self-defeating by design.

So, of what “value” is “growth” if the business must fail in order to achieve it? It’s not a rhetorical question. The idea is to create the illusion of business “success” by those who can bleed the company to their profit by forcing it to fail.

Grifting as a business model has become fashionable. It works for private equity firms that liquidate major retail chains. It works for a billionaire real estate guy who profits by bankrupting Atlantic City casinos. It worked with Theranos. The “business” isn’t really a business at all: it’s a device whose purpose is to sucker investors by promising them the moon so they can be cheated. The trick is to avoid conviction for fraud and ending up in the prison cell next to Elizabeth Holmes.

That’s the bad news. The really bad news is that this grift has been applied on a global scale. We know how it works, we can tell when it will fail, and we know it will end in tears.

“Yes, the planet got destroyed, but for a beautiful moment in time we created a lot of value for shareholders.”

Darwin: “Shhh. I’ve got this.”

Growth at all costs is a brutal but normal business for growth stocks.

Wall Street will punish any growth stock that doesn’t grow. They could have huge profits and low overhead, but if they haven’t grown, their stock will likely plummet.

Profitability doesn’t prevent a plummet. There are many companies out there with good P/E ratios whose stock prices went into the toilet.

There is a lot of pressure to grow at any means. It is tough to be a CEO when your net worth with stock RSUs could plummet by 70% if you don’t grow. Hence we see some executives bailing out while the RSUs are good.

Being a business dinosaur from the distant and dark past (retired in 2018), it is stunning that none of these folks seem to acknowledge that their costs are what’s killing them.

Back in those prehistoric times, we were constantly hammered to reduce costs of all types. Production, sales, and finance all had serious cost reduction goals every year. Your performance depended upon them being met.

We always made profits and paid dividends. But I guess that is a concept left in the dust bin of business history. Like I said, just a dinosaur from eons past.

Lol yeah ask folks at Boeing how hammering the cost cutting measures worked out.

But only growth is rewarded for these software companies. Cutting costs=less innovation and slower growth. Less resources to achieve your go to market strategy.

All join in on the chorus now;

“And another one gone, and another one gone,

Another one bites the dust”

Queen

I worked for one of these ‘fake it til you make it’ Sili Valley SAAS wannabes for a minute back in 2021, and never heard the C-suite talk much about the path to profitability or even making a great product. Far more attention got paid to finding new investors and positioning the company to get bought by the big boys. Lacking the right temperament for this sort of fantastical thinking I left for greener pastures. Sure enough they’re now in cost-cutting mode as well to stretch out the ‘runway.’

I believe you covered Docusign already. Just to add to the discussion. I signed something via docusign. Easy and quick. Then I guess I have an account. I get weekly emails to look at my docusign account. But why would anyone just look? And how does a signature app get a 10B market cap ? It was 60B at the peak of the hype. This all reminds me of the dot-com bust. But how do we game this out and anticipate the likely outcome? I hope that future posts from everyone include some possibilities as to the future of markets. No wrong suggestions just dialogue. Cheers.