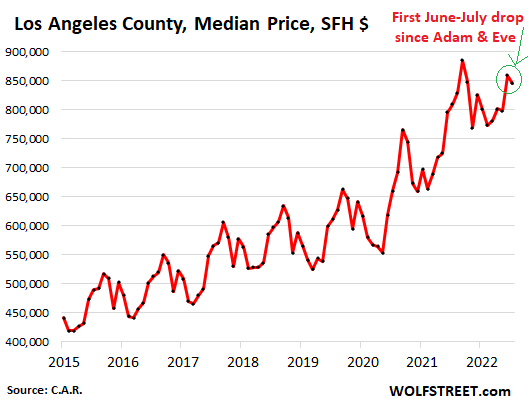

San Francisco & Silicon Valley lead. Southern California is catching up. In Los Angeles County, prices fell in July from June for the first since Adam and Eve.

By Wolf Richter for WOLF STREET.

It’s peak home-buying season in California, but sky-high home prices, holy-moly mortgage rates, the collapse of cryptos, the vanishing DeFi, and the implosion of tech startups, SPACs, and IPOs, all of which are crucial to the wealth, or perceived wealth, of many Californians, pulled the rug out from under California’s splendid housing markets.

Sales volume of single-family houses (SFH) in California plunged by 14% in July from June, seasonally adjusted, and by 31% from a year ago, the 13th month in a row of year-over-year declines, according to the California Association of Realtors.

Sales volume of condos plunged by 18% in July from June, and by 36% from a year ago.

Prices eventually follow volume: The median price of single-family houses dropped 3.5% in July from June, down for the second month in a row, slashing the year-over-year gain to just 2.8%. The median price of condos dropped 2.3%, down for the third month in a row, whittling down the year-over-year gain to 7.5%.

San Francisco and Silicon Valley lead with the declines.

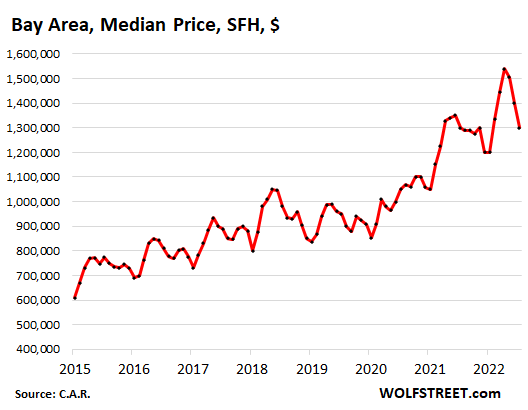

Sales volume of houses and condos in the entire San Francisco Bay Area has collapsed by 37% from a year ago.

Price has started to follow volume. Year-over-year, the median price of houses across the Bay Area was down for the first time since lockdown May 2020.

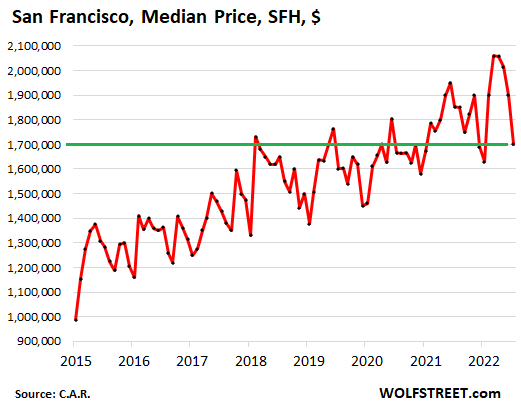

Year-over-year, it was down in three of the five big counties that cover San Francisco, Silicon Valley, and part of the East Bay, led by San Francisco, where the median price was down 8.2% year-over-year. We’ll get to the charts in a moment.

Southern California is behind but catching up.

Sales volume of houses plunged by 20% from June, and by 37% from a year ago. In San Diego, sales volume collapsed by 21% in July from June and by 41% year-over-year. In Orange County, sales volume collapsed by 39% year-over-year, in Los Angeles County by 32%.

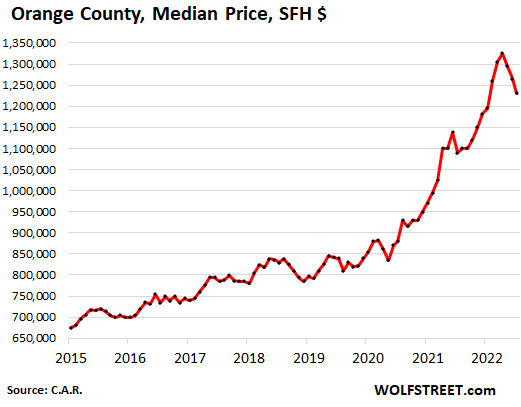

Price eventually follows volume, even in Southern California. In the counties of San Diego and Orange, the median price dropped for the third month in a row.

In Los Angeles County, the median price had peaked in September 2021 and has been on a wild ride since, up and down. But in July it fell, which was a bummer because it always rises from June to July; it even rose in 2009 from June to July, when all heck had broken loose, which puts this drop in a special light.

Supply and median time on the market jump.

In all of California, supply of houses and condos for sale rose to 3.2 months, up from 1.9 months a year ago, and the highest level since May 2020.

The median time on the market jumped to 14 days in July, up from 11 days in June, and up from 8 days a year ago.

In the Bay Area, supply jumped to 2.5 months in July, up from 2.0 months in June, and up from 1.5 months in July last year.

The median time on the market jumped to 15 days in July, up from 12 days in June, and up from 10 days a year ago.

In Southern California, supply jumped to 3.3 months, up from 2.5 months in June, and up from 1.9 months in July last year.

The median time on the market jumped to 13 days in July, up from 10 days in June, and up from 8 days a year ago.

Median Prices of SFH the Biggest Counties.

Median prices are very volatile, and we need to look at them with a good dose of circumspection, and trends need to be confirmed over time. But when the median price is down so far that the huge year-over-year gains in prior periods get whittled down to just small gains or even year-over-year declines, then the data points are starting to acquire heft as trends. And that’s what we’re now starting to see.

The Bay Area leads in price declines.

In the overall San Francisco Bay Area, the median price of single-family houses dropped for the third month in a row in July, is down 15.5% from the peak, and down 0.1% from a year ago, down year-over-year for the first time since lockdown May:

In San Francisco, house prices fell for the third month in a row, are down 17% from the peak and are down 8% year-over-year. These are very large and sudden declines, especially in June and July, and it rolled the median price back to where it first was in February 2018:

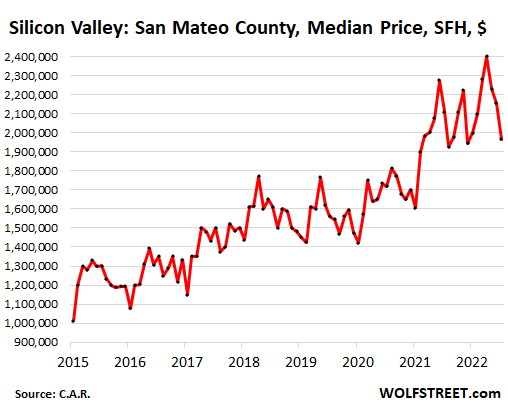

In San Mateo County, the northern part of Silicon Valley, the median price also fell for the third month in a row, -18% from the peak and -7% year-over-year. These are large and sudden drops that took the median price back to where it had first been in March 2021:

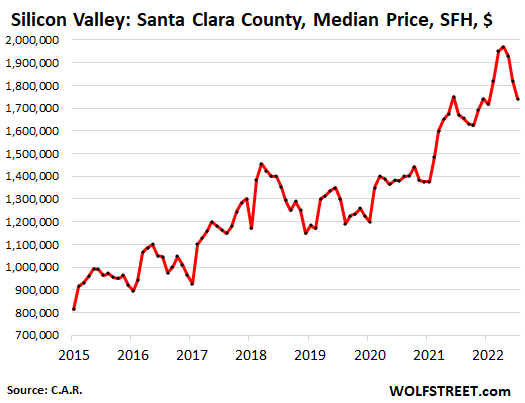

In Santa Clara County, which includes the southern part of Silicon Valley, the median price also fell for the third month in a row, -12% from the peak, but still +4% year-over-year, compared to the 20% gains last year:

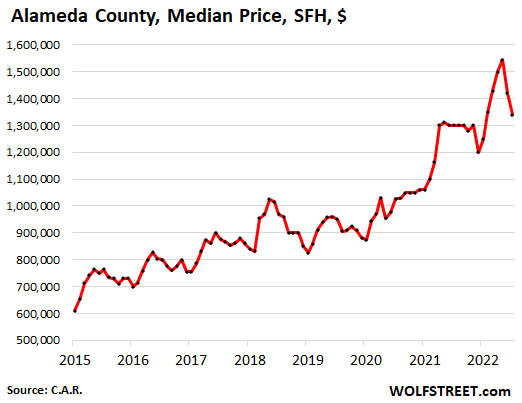

In Alameda County, in the East Bay, house prices fell for the second month in a row, -13% from the peak, but still +3% year-over-year:

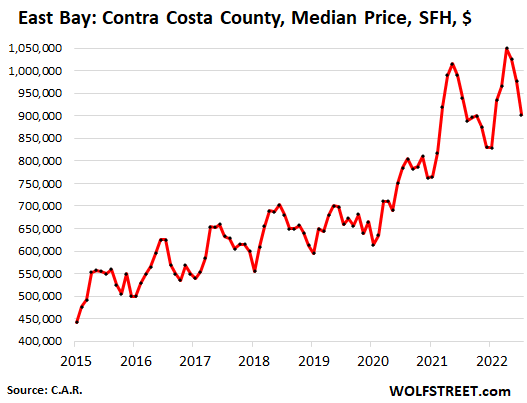

In Contra Costa County, in the East Bay, house prices fell for the third month in a row, -14% from the peak, -4% year-over-year:

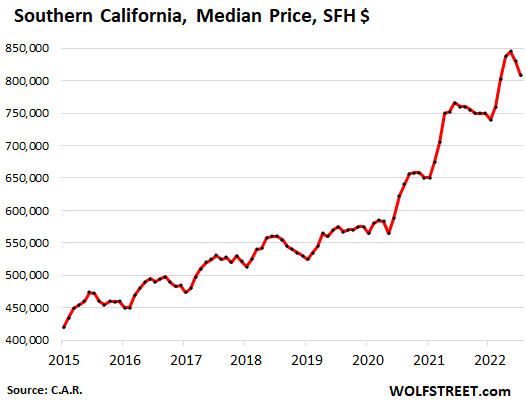

Southern California trying to catch up with the Bay Area.

In Southern California overall, house prices fell for the second month in a row, -4% from the peak, but still +6% year-over-year.

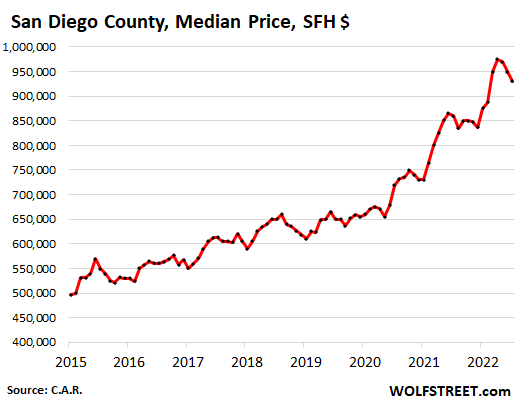

In San Diego County, the median house price fell for the third month in a row, -5% from the peak, which whittled the year-over-year gain from the 30%-range last year to +8% in July:

In Los Angeles County, the median house price has gone wild since the peak in September last year, -4.5% from that peak. Year-over-year, +4.5%.

But wait… special nugget: Seasonally, in LA County, the median price always rises from June to July, and this year’s drop in July from June was the first drop in many, many years. During the Housing Bust in 2008, the median price was essentially flat. And even in July 2009, as all heck had broken loose, the median price rose from June, which puts this year’s 1.6% drop in July from June into a very special light.

In Orange County, the median house price fell for the third month in a row, -7% from the peak, which whittled the year-over-year gain from the 27%-range early this year to 13% in July:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s bad in the Seattle area too, which is comparable to California in terms of tech influence and start-up activity.

For example, look at the median price single family home price declines in Redmond, WA (per Redfin market insights data).

Median SFM sales price:

April 2022 $1.95M

May 2022 $1.74M (6% monthly drop)

June 2022 $1.57M (10% monthly drop)

July 2022 $1.43M (9% monthly drop)

Plus, days on market is ACCELERATING UPWARD.

Want to lose money fast? Buy a home in an area that had 100% price appreciation the past few years.

Smart buyers will wait for signs of a bottom, as the bottoming process will take many months if not years. Don’t catch the falling knife.

Really?

That’s like a 25% drop in 3 months – that can’t be right.

That’s like 70% drop annualized.

Are you sure these figures are correct and meaningful?

Just doesn’t seem plausible ….

It’s median price data, so some of the downward trend is likely attributable to the mix of homes being sold. People can’t afford expensive single family homes anymore, so they are buying lower priced homes, or not buying at all.

If you have doubts about the data, go to Redfin, type in Redmond, WA, then go to the links for “market insights”.

The biggest advantage of living in Redmond is immunity to sticker shock : You can travel to Maui or Switzerland ir even an upscale part of Paris and then realize that your restaurant bill is similar to what you paid at Redmond, WA.

Most people now just drive out of city to eat out!

Thanks, Bobber.

One statistic they don’t seem to provide which might be useful for apples-to-apples comparison is the trend around price per square foot.

Dazed And Confused,

Not much difference. From the California Association or Realtors, Price per square foot, Orange County (because I just pulled the numbers for a reply further down):

July was the third month in a row of declines. Since April, the price per square foot fell 4.5%:

Jul: $630

Jun: $642

May: $656

Apr: $660

Thanks, Wolf.

The Redfin Data Center (thanks, AR) shows a slightly larger dip in sales price per square foot in Orange County than CAR.

From $628 to $593 i.e. 5.6%.

Seeing larger $/soft drops here where the House of Wisdom sits. 20% run-up last July to this spring all unwound now. YoY declines imminent.

Days on Market, inventory, Months’ supply all surging but still historically low.

Sales/month also slowing down.

I’m expecting a slow motion train wreck for next 1-3 years…

There were a number of houses sold for over $3M (!) in Redmond WA in April/May (Redfin will give you the data). It was a crazy times when we would go to an open house only to be told that it was canceled as the owner already accepted an offer only 3 days after putting it on the market. Things are definitely different now, and I hope it continues in that direction

Woodinville WA, another wealthy Seattle suburb, is just as bad.

Median price – single family home:

Mar 2002 $1.80M

Apr 2022 $1.49M

May 2022 $1.65M

Jun 2022 $1.46M

July 2022 $1.18M

Interestingly, these huge drops only bring the market back to where it was last summer. Thus, more drops can easily occur and may be likely. This is just the beginning of a trend that may spread across the nation over the next several months.

These bagholders can blame the federal reserve for continuing its quantitative easing program far too long, so that home prices became distorted.

Bobber,

“More drops can easily occur”.

You bet your sweet bippy they can.

A strong, strong argument can be made that the true clearing price will be in neighborhood of where median prices were the last 2 or 3 times when mortgage rates were above 5% (with semi honest loan applications).

That is going to be years or decades ago for most places, with a *ton* of faux appreciation to be unwound.

ZIRP created decades worth of financial illusions in the housing mkt.

RE your point below, the Redfin Data Center page provides the sales price per square feet data for all the metros they serve. Here is the link in case it helps anyone:

Thanks, AR – that’s very helpful.

For the metros I looked at, sales price per square foot seems to be dropping everywhere over the last few months – anywhere from 5-15% drop.

It’s not a compounding effect.

If the price of goods is $10 and it drops 5% then the new price is $9.50.

Then it drops another 5% (9.50 x 95%) the price is $9.025.

It’s good to keep an eye on how much prices have dropped from your it’s all time highs. This will give you a better I idea of the situation.

The article talks about median prices.

Yes, Redmond, WA is probably the only are falling faster than San Francisco!

Go to Redmond downtown and you see more than half of the shops shutdown. They had started converting malls to offices before pandemic hit and now even those offices are vacant.

The funny part is that many real estate agents still telling people that this is thr right time to buy!

If you really want to lose $500,000 in a year please buy a house at $2 million in Redmond, WA.

I own a number of rentals and have looked at a lot of houses with real estate agents.

I’m sorry, but for the most part, they are equivalent to used car salespersons. I have heard that “It’s a great time to buy” so many times that you just tell them to FO in your mind when they say it. They do not have your interest, generally speaking, in heart. They are commission animals. When I first got into fixer uppers, they provided no guidance whatsoever and don’t count on the inspector to find everything wrong. Moral of the story: the real estate agent is not your friend.

Pull the string on the back of a real estate agent and they will say: “Now is a great time to buy”

If the cost of ownership is 3% for tax, insurance and maintenance plus 5.5% interest cost then the math is going to be horrible for anyone who put minimum down and bought near the top.

Old time land lord folks we worked for in the 1960-1990 era in various states used 10% OS.

That included ”long term” maintenance as those folks never sold a property that I was aware of in those days.

All had positive cash flow from every property, by the simple technique of ”buying right,” and holding for eva.

Believe that is ONE of the major techniques of ”old money” including the family of folks who apparently own most of London, eh?

My uncle, who died recently, owned a lot of real estate in and around Long Beach. He started buying when he received his inheritance of $25K in 1948.

His motto was, “But cheap and keep.”

Pretty nice to get in that early and with the protections California gave to legacy real estate in, I want to say, the 1970s.

That is true, but how can you tell when it’s the bottom without missing out

– As always: Prices follow sales.

– San Jose was down 8% down in the last 3 months and we’re talking prices.

I recall in the bubble that the price declines were huge the first year after the bubble popped. From there, prices dropped consistently but more modestly for several years. I saw it first hand. In late 2007, when the bubble started popping, the builder’s asking price of a house I was watching dropped 25% in three months.

I think this bubble pop will be similar in the speculative areas of the West and South.

Also note, prices are dropping fast in these areas even though transaction volume and supply is relatively low. It only takes one or two transactions in an area to bring everybody’s market price down. Smart sellers are capturing gains while they exist, beating the slow-moving sellers to market. This selling window will not last long because prices are dropping rapidly.

In my greater area the prices dropped more in 2010 – 2012. They were extremely low for about 3 months then they were sold bulk to all “cash” buyers. Banks would not give loans on them to regular buyers. “Cash” buyers being corporations that were given lower interest rates and foreign buyers.

It left a vile taste in many people’s mouths.

Money laundering of foreign corruption via US Real Estate?

What could possibly go wrong?

Just ask the people in Canada. Vancouver has a 30% tax on foreign Real Estate purchases. Too many people found that their kids could not afford to live in the town they grew up in. This has been routine in Marin County for years, but not in Canada.

” Vancouver has a 30% tax on foreign Real Estate purchases. ”

Finally! Good for them! & Yeah, we need laws like that here. I can’t believe the US population isn’t in as much of an uproar over this as they are in Canada, England and Australia. Why it isn’t a top political agenda. People act as if it isn’t happening like that.

Which was the reason so much Chinese money found its way into Seattle. It went from Vancouver to Seattle. The Chinese don’t buy into falling real estate markets so Seattle will keep on falling in price.

Most people here in the USA are too stupid to realize the enormous negative effect by allowing foreign money in local real estate. The realtors get a cut so they couldnt care less… other people that see this seldom say anything cause nothing changes. The radically polarized political climate combined with vested interests of the connected few will ensure nothing changes.

We ran into that exact scenario in 2015 trying to buy a home near elderly parents in the saintly part of tpa bay area Lynn.

Finally found a completely trashed 1950 ”cottage” close enough, then completely ”rehabbed” it for a month, and still there.

Zillow says its up FOUR TIMES what we paid,,, to which I can only say, ”YEAH, RIGHT.”

” “Cash” buyers being corporations that were given lower interest rates and foreign buyers.”

Not so much, I’m a non-corporate “cash buyer.” I pay the standard 0% interest rate available to all “cash buyers”.

I was trying to think of a snarky reply to “Lynn” about the low interest rates being given to cash buyers….

…But you beat me to it.

Nicely done.

Your point Carrie’s over to the LLC buy outs of foreclosures that have since put the rental market into an economic crisis. This is underlying rip tide to sustainable living standards soon to come as climate change calculus regarding home ownership value skews the investable monetized factor; precariously at the apex of an over inflated property investment. I live in Elk Grove CA and see an exodus from the Bay Area buying up new developments here that are simply messing up our scales of economy on a local level. The same happened to Seattle in the 80s when Californians sold their million dollar properties to buy up Seattle’s housing; that created an equity gap of local residents not being able to purchase a home due to the escalated price demand to supply ratio. Moreover, the US GDP macroeconomic formulary is seriously in jeopardy in terms of window dressing an escalating inflationary outcome driven by Wall Street corporate buy backs and inequitable tax brackets. What part of the equation that’s missing here is the loss of agricultural farmland, where in California’s Central Valley is being labeled unproductive to allow for massive solar farm contracts to be implemented as kickbacks to our city’s coffers. It doesn’t bring the cost of utilities down in fact it has increased the kilowatt price. The whole housing market scenario controlled by the banks and mortgage firms couple with lack of accountability oversight of fiduciary duty regulations in total speculative free market is the delusional visions of prosperity as was the Black Tulip Market Crash in the 1600s.

Interesting post, but I can’t agree with your defense of California Central Valley agriculture. There is no way in heck that bone dry land should be pumped full of imported and precious aquifer water to grow almonds and other water hungry crops. It’s a long running joke, and it would be funny if not for the fact that those “farmers” are rapidly depleting a million year old aquifer under the central valley in a matter of decades. It’s so bad that the land in the valley is sinking by several inches annually.

I hope the show has just started.

The home prices has much further to fall.

It may take a year or more I guess.

People say, home prices decline is not good. I don’t see it this way.

I am a home owner and if my home prices goes down by 40% or so or more does not impact me.

If you are an investor, its a different story.

If home prices fall enough, I can see families living in their own home instead many families sharing single home .

Lower house prices mean lower property taxes.

Lower taxes??? I don’t think it works like that.

Maybe it depends on where you live.

During the last housing bust, property taxes fell along with house prices in places I lived at the time at least according to official tax records.

I’m not sure where Dazed and Confused was, but in California property taxes are based on the lower of the Prop 13 value (purchase price plus a 2% annual increase) or FMV. So after the last crash lots of people in California who bought relatively recently had their property taxes go down with the value of their home.

Prices down can lead to rising rates, esp. on multi family … a “soak the landlords” mindset can creep into city governments when revenues run thin…

When your property value drops you can ask the tax collector’s office to re-value the property and thus lower your tax bill. I have done that after 2008, it works well.

Not necessarily in Chicago / Crook County / collar counties. Those pensioners and heath care bennies have to be paid.

“Those pensioners and heath care bennies have to be paid.”

NO, they DON’T. Taxpayers never got to vote on that. As far as I’m concerned, it’s stolen money.

It doesn’t work that way. If prices drop the city will just raise the tax rate. Happens all the time.

Maybe where you live Johnny – but not in many other places.

People can always vote with their feet. You can always refuse to pay those crazy Chicago government pension by leaving Illinois.

As long as the feds don’t bail them out. Then we all pay.

Property tax doesn’t work that way. The town/city has a budget. They have a certain sum they need to collect in taxes to run things. It is collected from property owners. If their house resale value dropped 50% in the last year, it doesn’t matter. They will pay their share. Everybody else’s home value also went down, so everything remains unchanged. The only way to beat this is to sell at or near the top and find a reasonable rent. And sit on all the cash you now have.

Your argument sounds plausible but is simply not consistent with the facts and the data – at least not in places I lived – during the last housing bust e.g. Tampa FL.

Incorrect, here in CA you can have your property reevaluated by your local tax collectors office and they will lower your tax bill. I think you can do this once per year.

In flyover state USA we can appeal to reduce property value and accordingly the tax. I have done it once myself and saved a couple hundred per year.

Your home is not an investment, it is where your family live and enjoy each other.

Phil-sadly, that memo got lost almost two generations, ago…

may we all find a better day.

Exactly. Congress made sure to change all that with laws that made homes into *very* attractive investment assets.

It wasn’t “lost”, it was destroyed by financial marketing doublespeak, plus bought-and-paid for Congressional destruction of the national interest in stable housing markets, and aided by the 30-year rates-always dropping bond market.

Those who want to see 20% rates again may want to be careful what u wish for. What we really need are stable moderate rates and aggregate money&credit growth commensurate with the economy’s growth potential… Sadly language exactly like that used to be the Fed’s mandate, before they dropped the ball…

WS-well stated. When virtually everything is commoditized, little surprise at what results…

may we all find a better day.

A house is a liability and a headache I don’t need. I already have a job, don’t need more chores. The american house ownership dream sounds like a nightmare when you realize what is involved. Also you don’t own it, the bank does, and the government can take it away at any time if you stop paying for ‘protection’. I’m opting out, and quiet quitting. No point working hard when nothing is going to come of it anyway. Don’t want to make my boss rich ;)

Own nothing and have a crappy life.

Unless you want to live rough, you need a place to live though, so they gotcha.

living on a mat is looking increasingly attractive

Concur, zero interest in the chores load of a typical home. Even if you hire labor to do your chores, you still lose time managing the labor.

Right!

Pay rent to me and make me rich instead.

Screw that guy who knows and employs you. All he cares about is money and enslaving humanity.

Van down by the river.

@PilotDoc

Who’s said I’m going to pay rent to anyone?

Maybe you can find someone else to pay you rent.

When my wife and I retire, our paid off home means we will only have to pay property tax and upkeep. A renter will continue having to pay rent… My home will be paid off in 2031, when I will be in my mid 50’s. That will mean an extra @$1500-2000 monthly in the pocket for perpetuity… No mean sum for a middle class couple. I don’t know how we would survive old age as renters.

I have lot of friends having millions in assets and living a crappy life.

At the same time lot of friends having no asset at all living a happy life.

If you can be happy without owning anything you truly are wealthy.

Personally someone who has done very good in life

I believe happiness is state of mind and is really a treasure.

I think you have 4 choices.

1) Rent and make your landlord rich. :-) They are paying property taxes, mortgage, insurance, and maintenance and still making a profit off renters with rent rising with surrounding rentals with inflation.

2) Own and have a fixed mortgage and rising property taxes and insurance. You can either do your own maintenance or hire someone for a greater price than your landlord who probably gets a preferred volume discount.

3) Buy a tent/van and live for free on BLM land down by the river or along any homeless-friendly creek bed.

4) Leave the US for a cheaper country. Watch out for any local revolution where you lose everything and barely escape with the clothes on your back. OK, that is fear tactics.

“Find a way to make money while you sleep; otherwise you will be working until you die.”

— Warren Buffet

It is the land under that house that is the investment!

Exactly. It’s only the dirt that holds true value. The house is constantly falling apart and depreciating like a brick. It’s nothing but a liability.

That’s normally true but not during the pandemic-era inflation.

Even used cars appreciated in value during the pandemic.

It’s the land and the cost to build a comparable house with current construction costs.

Phil, you are spot on. I’m in my late 50’s and I recall houses were where you live as long as you can and maybe die in it. It was not the stonk market.

For some reason, starting in the early 2000’s, housing became a get rich scheme. Most likely Fed with easy money.

My parents and grandparents purchased houses, paid them off, and then eventually died in them (I wanted to say happily died but I don’t think anyone happily dies. Even if they are 100.). Both lived in their houses comfortably, well-fed, with extra money for cruises and other activities for 60 years.

They lived well on Social Security because their houses were paid for.

A house was a place to live and enjoy. They didn’t consider it a prison or a financial investment. Even though by the time they passed, the value of the houses would have carried them another 50 years even if they rented.

I believe the more ‘nomadic’ situation that occurred was due to employment becoming so transitory.

I agree.

Home price decline is not different for an investor unless they are short-sighted and only bought for appreciation instead of the more important and longer-term benefits. Rents are up and going higher so who cares if the home is worth more or less? I don’t, but then I’m a long-term kind of guy.

I’ll even say that the investor is better off than the homeowner because if the homeowner loses a job they might lose the home, but if the tenant loses a job you can rent to the other one that still has one.

How are rents going to keep going up when this expense has risen so much faster than incomes?

It doesn’t matter that it’s a necessity. People will move back into their “parent’s basement” when (not if) they can’t afford it.

It’s going to take a while for the job market to catch up with the interest rate cycle, but if the 1981 bond bull market really ended in 2020 as it certainly appears, it’s going to happen and it’s going to be ugly.

I suspect that smaller homes/condos will retain their value more than larger, more expensive homes over time. Many larger homes were bought to house large families, but most baby boomer’s children have left their homes now. They do not need such large, luxurious homes.

Reportedly, the baby boomer generation is retiring now, albeit a report says that the last ones will retire by 2030. That will mean that many will want to get rid of their larger homes to have money to live, given their limited retirement savings:

See Investopedia quote from “Are we in a baby boomer retirement crisis”:

“Baby Boomers have an average of $152,000 saved for retirement, according to the 19th Annual Retirement Survey of Workers conducted by the TransAmerica Center for Retirement Studies. This is not nearly enough to last through retirement. Based on information from the Bureau of Labor Statistics, adults between ages 65 and 74 spend, on average, $48,885 a year.”

That is what I predict will happen, and I predicted the Chinese economic crash that is now occurring many months ago.

The last of the baby boomers are now turning 60 so virtually all of them will be retired in two years not in 2030. Back in better times a lot of baby boomers retired at 55. Freedom 55.

“so virtually all of them will be retired in two years not in 2030”

Hahaha, my projected retirement date is far beyond 2030, somewhere in the range of “never.”

FYI, the youngest boomers are now about 57. So they’re just hitting their peak :-]

Not in a major bear market they won’t, as their substantually fake wealth evaporates.

I turn 60 next March… but I don’t plan on retiring for another 7 years (God willing). There’s a PHD in my department and he’s pushing 70. I hope he doesn’t retire for a while, because when he does I’ll be “the old guy” in the department.

I totally agree with Wolff re: retirement. I’m 58 and don’t see myself retiring for a long time. I will work part time and have my rentals too, but with inflation and the loss of buying power due to money dilution, we’re all gonna be working until they find us keeled over the keyboard or wherever. Someone’s gonna give us a nudge and say “Hey, I think they’re dead!”

Define “Retired”.

Back in the day with corporate pensions, retirement age was defined on how well the corporation was doing. If it needed to lay older employees off during hard times, early retirement was offered as low as 55.

My brother retired from the military at age 45 after 25 years of service. He still works.

If I retire early, I won’t be sitting in a rocker (OK, I might for a few months with a few good books). I’ll figure out something else to do. It may not be for the same money but I guarantee it will be more enjoyable than my current job.

I suspect Wolf has “retired” from a few jobs and now works at something he likes better.

Given the low unemployment, I am seriously considering retiring now in my late 50’s. I’ll have the pick of any job I want. My current job is actually pretty good. I just wish there wasn’t so much of it. I love chocolate but I’d hate someone telling me that I must eat 1000 pieces per day.

Most of their supposed wealth is tied up in real estate. Expect them to eat the house in various ways from cash out refi to reverse mortgage and helocs. This generation, the “me generation,” are the ones that coined the bumper sticker; “We Are Spending Our Children’s Inheritance.” Used to see that all over the place in Floriduh.

My 80 year old neighbor has a bumper sticker that says; “Money Isn’t Everything But It Sure Keeps The Kids In Touch.” That’s like saying hey everybody my kids hate me. Sad, not funny. The boomer’s kids are the millennials anyway. Everyone knows they hate everything.

Funny how the “me generation” begat the World’s very first “selfie generation.”

Take a look at properties which increased the most since the end of the housing bust from Housing Bubble 1.0. These are the ones which I think will (by far) do the worst, even though these are often smaller and lower priced.

These are located in areas that aren’t good or “suck” to live, often closer to the central core of the city. Some have (temporarily) “gentrified”.

When the bear market is mature and the economy is contracting noticeably with it, I expect these to sell for less than at the end of the last housing bust because economic and social conditions will also be worse. Like some properties in Detroit, some of these might be worth less than zero.

Augustus,

You never know.

As Boomers age, do they want to walk to shopping, restaurants, bars, maybe even Discos :-) ? Do they want to catch a convenient subway, train, or bus to visit museums, opera, theater? As a late boomer, I’d like this. As long as it was safe.

Or do they want to live in an oversized home in safe suburbia relying on their car to get anywhere? In the Pre-Uber days, my grandma lost her drivers license at 88. She enjoyed her home of 60 years, but had to rely on friends for groceries, and getting out since she lived in semi-suburbia.

I like the term “dishonest money” to describe what we have had since GFC. It has been an unsustainable increase in government debt and extreme experimental Fed policy.

We are in a different phase now with inflation. Dr. Doom is saying it’s going to be a hard landing, but he doesn’t know if it’s going to out of control inflation or severe recession. Next 18 months will be interesting.

Anyone care to guess how the current house price declines will impact the “Owner’s Equivalent Rent” component of the CPI in 2023? If I’ve read Wolf’s prior commentary correctly, the latter should continue to rise for many months, but maybe the former will temper it.

We saw that during the housing bust that “OE of Rent” (red line) kept going up (except for a minor hesitation) even as home prices (purple line, Case Shiller) were crashing:

Another compliment for your awesome chart, Wolf!

When CPI “Owners Equivalent Rent of Residence” intersects with the “National Home Price Index” like it did in 2012, I will hopefully have cash to buy RE.

I don’t understand why CPI is not spiking? Rents have spiked ridiculously based on the renters I know. Thanks to Wolf, I do understand the calculation of this CPI has a lag and is based on owners estimate of what they think they could get for rent. When the tax collector calls me for this information, I try to lowball the number since I am not renting out my house and I don’t want my property taxes to increase. I guess I’m paranoid and not a bragger.

It may be interesting to also show the real-time Zillow line for their rents.

Forgot that this is owner equivalent rents, derp. Maybe another chart out there tracking case shiller to overall rents? But I am guessing if that looks like owner equivalent, then it again says rents driven by rental market, which is not materially correlated to housing market.

So idea that institutional investors buying homes to lock would be buyers into rental servitude, which I have read in the comments from time to time, seems unlikely.

“Slight of hand” on gasoline prices before the midterm elections is artificially pushing down the CPI but inflation will take a second leg up at the very beginning of 2023 as oil and gasoline prices spike.

There was a feature on our local news last night about rent spiking up in Raleigh to $1800 for one bedroom. Wasn’t very long ago it was $1100.

I think it would be more honest to define inflation as CPI-rent for renters as it is a much cleaner number than owner equivalent rent. They can have a separate CPI-home owner if they want. A hybrid number based on surveys seems sketchy.

Anecdotally, I do know a few renters who were able to talk their rent increases down a bit from what the land lord wanted. I don’t know how common that is, though.

Lauren, talking rental prices down isn’t only uncommon, but probably illegal, in multi-unit rental bldgs. “Fair Housing” laws dictate that there can be no exceptions to a policy of treating every renter “equally”. Units differ on size, location in the complex, etc., but if there’s an arguable difference, it could violate Fair Housing rules.

Cool chart! Rents to home prices don’t look correlated at all in this chart, so I don’t know why everyone assumes continued rent spikes. Where’s even the correlation in the data, let alone causation?

I guess this makes sense. They’re not really the same markets. While there is some small substitution towards the higher end of the rental market, most folks who rent do so because they cannot buy. Few are renters by choice. Few homeowners are looking to take profits on homeownership and rent if they got kids. There is no waive of foreclosures forcing people out of their homes.

So, the biggest explanation for all the extra volatility over the last 20 years with SFH compared to rents is mortgage rates and income volatility, both heavily impacted by fed policy. Demand is driven more by how much people can borrow rather than fundamentals like intrinsic value, income generated from asset, etc.

How much do major cities like NYC and SF skew this where there has always been a premium on ownership?

Imagine being there at the end of 2018, looking at these charts, noticing a dip, and then start crying chicken little about how the whole markets going to collapse, the bottom’s going to fall out, this time it’s NOT different, 10 year cycle, interest rates are a disaster, there’s massive surplus, the american dream is over.

What?

I think the point is whocoodanode then that prices would run up 3 more years.

I’m in the Naples market. Listings for SFRs bottomed in March 2022 and have increased about 180% by mid-July. I expected those trends to continue through the balance of the summer and into the fall. However, listings started decreasing in late July and have continued lower in August.

While I think prices may decrease by 30% from the peaks in March, those levels are still up 85% since Jan 2021.

I see bottom prices based on a price level which is 5.75% annual appreciation applied to the 2012 price baseline.

I would say 4% and not 5.75% if it was not Florida, and especially if it was not Naples (i.e., white sand beaches, clear water, a lot more upscale and refined than pretentious Boca Raton).

It will crash when all the northerners realize how ungodly hot it is for half the year, particularly when the next big hurricane hits. Also, how terrible the schools are compared to where they came from. Not to mention all the psycho Trumpers everywhere.

Wolf, you have the months reversed in this sentence: “Sales volume of single-family houses (SFH) in California plunged by 14% in June from July”

Thanks 🤢

There’s no better houaing indicator to me than the window of the BRK real estate office on my street in a near Chicago suburb. Once full of million dollar homes, I saw the first rental property in 2.5 years on the glass. Nothing over 500k. And listings sitting for longer. Real rates mean real loans and really paying attention to prices. Potential for losses, holding costs, low liquidity, it’s scaring away those all cash second home or blackstone-esque buyers.

The main force holding the Chicago burb market up are all those young couples with a kid or two fleeing the nice hipster areas of the city ‘for a big back yard’.

You got that right. Although some of those folks probably have no interest in selling for a long time and got a super low rate. But, they better like their house because they’re stuck with it.

We live in an expensive area for housing (Cambridgeshire, England). For years we’ve been getting letters from agents assuring us that armies of refugees from London would like to buy our house and that the agents would be delighted to handle the sale for us.

If we stop getting such letters I’ll know we’re “doing a California”.

Very low inventory here in SD and I dont see any price decline.

If a decent house comes to market, still sells quickly.

Prices might stagnate at those levels but I see no bust, the amount of money printed in the last three years is still out there and isnt being withdrawn, so we got 30% dollar devaluation basically and very high prices.

I get lots of emails from redfins about price reductions in san diego.

I never saw these many in last 3 years or so.

I guess we live in different san diego :-).

BTW, anecdotes aside, numbers don’t lie.

A lot of people in san Diego told me the same in 2007-2009: That San Diego is so nice , come what may, prices would never go down.

The rest is history as they say.

Everybody thinks their area is special and will never correct…until their special area corrects.

“Not in my city.”

“Not in my neighborhood.”

“Not on my street.”

“Not my house.”

Part of the grief process – denial and bargaining, followed by anger and acceptance.

It is true. Real estate prices never go down in the special areas. I will print more money to prevent this from happening.

Durham, NC looks like it’s correcting. Quick look at Zillow shows a lot more inventory than 6-12 months ago and price cuts on almost all listings.

Below are two very nice neighborhoods in San Diego. Price reductions are happening.

La Jolla: 205 active listings, 40 price reductions

https://www.movoto.com/ca/92037/market-trends/

Mission Hills: 97 active listings, 16 price reductions

https://www.movoto.com/ca/92103/market-trends/

Me, I see the drop in SFH here in SD at least equaling the 35-40% drop

we saw over ’06-’12. And, that drop was artificially arrested by QE1, which I do not see coming back for protracted stretches.

I welcome a return to sane home price-to-household income ratios, so younger folks can afford to comfortably buy.

The rapid increases in home prices is still hard for me to stomach, even after watching it the whole way through.

Things have clearly reversed, and the reversal has a long way to go. Who wants to pay 5-6% mortgage interest rate on a home that is declining in price? It’s a recipe for financial disaster. Potential buyers in the South and West should at least wait a year until price trends stabilize. Prices seem to be falling like a rock right now. Also, the job picture seems to be tightening for professional positions, particularly in start ups and tech.

Agree — but remember, historically speaking, 5-6% mortgage rates are LOW.

We’ve had such low interest rates for so long that people have forgotten about “normal” mortgage rates of 8-9%

I kind of feel that way about the auto market. It seems like a complete scam – a ripoff.

Firstly, autos and trucks are made for pleasure which is the big seller,or for work. All of the them are used to sell a finance plan.

I sold a house in 2005 in Northern California. My neighbor uttered almost the exact same words ,” they might level off but never go down”. I bought a house about 5 miles away for $185k in 2012. It had topped out at $500k in 2006. It was a beater, but I added a lot of sweat equity. It actually set me up financially for my retirement. Last year I took a reverse mortgage on it.

You got lucky. You had no way of knowing the FED would be so reckless and push prices like they did. And this “reverse mortgage” thingy….

1) San Mateo, the leader of the pak, is in a trading range since reaching $2.3M in 2021 and plunging to $2M. Breaching the $2M low means weakness, not a collapse. It might happen more than once.

2) San Mateo is either in distribution, or accumulation.

3) The rest, premature.

4) San Mateo RE might be in troubles if AAPL breach June lows and stay below, bitten by the snake river bankers , US consumers, or China.

2000sqft SFR homes here in South Orange Co. were about 1M in November. That went to 1.4M by May. Now they’re around 1.2M. But they’re all still selling. So I have no faith that the prices will ever get much lower.

You gotta be patient. Last one took about 5 years to play out. For instant gratification, you can go see a crypto rug-pull, or a meme-stock BBBY dump (-41% today), but that’s not likely with real estate. Real estate takes time. And these are pretty fast moves already.

This time, because we are in an “everything bubble”, I suspect it may be faster than usual.

We definitely have a setup that could be like in the late 70’s where PE on stock market got to 7 because of inflation. Too soon to know for sure.

People sold stocks wishing they could buy them back at the bottom only to loose again. Scratch off lottery tickets were not enough for a bag of groceries in most cases.

People were writing about the “everything bubble” in 2018. The price of real estate, the S&P 500 and almost everything surged since then. Maybe another Great Depression style deflation some other time.

I know you’re right, it’s just frustrating to watch prices go up 50-100% in 2 years just when we finally save up 20%. Thanks for the advice.

“You gotta be patient. Last one took about 5 years to play out. For instant gratification, you can go see a crypto rug-pull, or a meme-stock BBBY dump (-41% today), but that’s not likely with real estate. Real estate takes time. And these are pretty fast moves already.”

The system is much more unstable now with the amount of debt and speculation in the system. I believe this one will turn into a dumpster fire of unimaginable proportions. There is virtually no room for the Fed to double its balance sheet to save the system again. Our international creditors will make sure of that.

Serious question — where else do your international creditors have to go? Not the Euro, surely, so where? The Yen? I can’t see it.

“…There is virtually no room for the Fed to double its balance sheet to save the system again. Our international creditors will make sure of that…”

I heartily agree. I think the integration of trade in Asia, led by Russia and China, and stretching to the Middle East, South America, parts of Europe, and Africa, will provide solid outlets for sale of goods and payment in sound currencies, or even real money (gold and silver). There will be no need to sell for depreciating dollars.

“For instant gratification, you can go see a crypto rug-pull…”

This made me laugh out loud. Wolf has a way with words at times. For the life of me I have no idea why any crypto is even worth a dollar anymore. WTF is a Dogecoin, anyway? Can anybody name anything this “coin” does?

Yup,

It makes you talk about crap you would have never talked about before…

I think that’s about it …

Haha, if I had extra money to invest I would have bought Dogecoin the first time I saw it advertised and sold it when it doubled. It looked like a really obvious pump and dump. So cute! Hahaha.

This dip in housing prices reminds me of the temporary dip that occurred end of 2018/beginning of 2019 when mortgage rates shot up. The Fed reversed course in 2019 and dropped interest rates and mortgage rates came back down all the way through end of 2021, and housing climbed higher during that time. If inflation calms down and Fed stops the rate increases, that could cause mortgage rates to either stabilize or drop again and housing prices will either stabilize or start climbing again like they did from 2019 to 2021. So not sure if this is the start of a long term drop in housing or a temporary drop depending on inflation and Fed’s push against it. So we will see, but if you have too much patience you might miss the discount depending on how things play out.

beatleme,

In 2018, inflation was BELOW the Fed’s target. Now it’s 3x the Fed’s target. Any comparison to 2018 is inane.

You need to go back to the late 1970s to find comparable inflation. Except back then, we weren’t sitting on the biggest asset bubble ever.

Your post exhibits classic denial and rationalization.

Hello Wolf,

I see your point regarding the difference in scenarios, but my point is not that the scenarios were the same but that it reminded me of that time period in late 2018/early 2019 when interest rates and mortgage rates were increasing. As you pointed out, the big difference in inflation between the two time periods changes things. My interpretation of that difference is that it’s unlikely this time around for interest rates and mortgage rates to stabilize/drop, but things have shot up and down so unprecedently since Covid that I don’t discount it entirely as a possibility, and therefore I am not so sure that this is the beginning of a multi-year drop in housing prices.

Regarding the 1970s and inflation, I don’t know how to post an image but I looked at the “All-Transactions House Price Index for California” (https://fred.stlouisfed.org/series/CASTHPI) and zoomed in from 1975 to 1990. From Q1 1975 until Q4 1981 the index went up from 41.68 to 117.53 (Housing prices almost tripled!) and this during a period of some of the strongest inflation ever. One quarter later, (Q1 1982) the index reached a bottom of 104.32 (11.2% drop) and lingered near the low until it started taking off again from Q3 1982 until Q1 1990, the index going up during this period from a 104.89 to a 227.54 (More than double but at a much slower pace then when inflation was raging). I looked at California because that is where I live and its relevant to me, but if you look at the national data it is similar, just less extreme.

Bottom line is that this may likely be the beginning of a long term housing price decline, but there is an argument for a shorter term dip that will start bottoming as soon as it appears that inflation is under control. Once inflation is under control, the Fed could stop the rate increases and possibly even lower them, starting the next leg up. We shall see.

You disregarded the other part of my comment. This is what I said:

“Except back then, we weren’t sitting on the biggest asset bubble ever.”

That includes HOUSING.

Now we do sit on the biggest asset bubble ever, which includes housing.

Hello Wolf,

I disregarded that comment because my post was getting long and I thought you would consider that housing almost tripling in price from 1975 to 1981 would have felt extremely bubbly back then and arguably more extreme than today due to its speed. Additionally, after a small one year dip in 1982, it more than doubled again in 9 years so you are looking at the housing index climbing from 41.68 to 227.54 (5.4x higher!) from 1975 to 1990! I looked at the 2006 bubble (1995-2006; 199.73 to 646.78 = 3.2x higher) and the current bubble (2012-2022; 381.78 to 868.30 = 2.2x higher) and they are behind and would not feel as extreme to those who lived through the appreciation in housing prices from 1975 to 1990.

Having said that, there will never be a perfect comparison. It’s like trying to compare the Warriors of today to the Bulls of the 1990’s, its just different. For those reading these comments, I simply had to state my take on this situation because I don’t believe it is clear cut due to Covid and the extremes it has caused. Acceleration to the upside and downside has been crazy and this roller coaster is unprecedented in my lifetime. So be careful out there and make sure you really think about the move your going to make, buying a house is one of the biggest financial decisions and you need to know what you are getting into by considering all sides of the story.

As to my approach in this crazy environment, I am being patient as Wolf suggests, and keeping one eye on inflation and the other on housing supply and prices. As soon as I hear that inflation appears to be under control and the Fed stops increasing interest rates, I will dust off my buying cap and get ready to jump into the market, depending on how housing supply and prices are trending at that time. If momentum turns to the upside for housing and inflation remains under control, I will take the gamble and jump in, expecting to ride another leg up in housing.

Kinda sorta agree with the ”Its different this time.” crowd on this current situation Wolf, for two reasons:

1. The incredible bubble in almost all assets.

2. The incredible printing of ”funny money” this time.

We are already set per Phil earlier, with no mortgage, but also with limited raises on property taxes in FL thanks to the same guy who ”got er done” in CA.

Conclusion is too early to tell how the idiots who appear to be running the politics and policies and procedures of the GUV MINT and FRB are going to screw up this one: Two stark choices are, ”burn it down” and deeper depression than the 1930 era; or just keeping printing for eva.

Going to be fun either way, eh?

I’ve been watching price/sqft rise every month in Orange County, CA.

Price/sqft factors out the mix of housing sold and the violent price swings. For example, someone could sell 60 condos one month, pulling down the median price, when in fact the price/sqft has gone up.

JeffD,

OK, look again.

July was the third month in a row of declines. Since April, the price per square foot fell 4.5%

From the California Association or Realtors, Price per square foot, Orange County:

Jul: $630

Jun: $642

May: $656

Apr: $660

Using stats against people how rude. :)

Time to eat crow. I look at movoto market trends, for my data. For the first month, in *August*, $/sqft are down. I’m shocked.

JeffD,

The link you provided was for Costa Mesa, a small town with 16,000 souls. Orange County has a pop. of 3.1 million. The town is too small to have any relevance here in this article.

There are just 139 houses on the market, per your link. And the median days on the market is 6,696 days, six-thousand six-hundred and ninety six days, which is something like 20 years I think, which is kind of long-ish. Not sure about the accuracy of their data LOL

Hi Wolf,

Costa mesa has 120K population. I gave the link for that city because movato has”nearby city” data at the bottom of the page, in case you wanted to compare to the general area. Aliso Viejo is another southeast county that is a good base city in movoto for that “nearby city” comparison. The “days on market” is clearly bogus. :)

Time to eat crow. I posted a link in a moderated comment you can read and discard. The west Orange county and southeast Orange county markets are very different. Here in southeast Orange county, it looks like the monthly $/sqft is finally coming down in this last month, and be almost 5%! Looks like interest rates are actually working.

Hi Wolf. Today I somehow caught your interview by Adam Taggert – Wealthion from 3 months ago. You have a great crystal ball!

el-cheapo plastic version from Walmart

The problem with California is that it is in California.

Wow, how very profound and additive to an otherwise great thread of helpful comments.

One may wonder where you chose to dwell, but then who cares.

“ One may wonder where you chose to dwell, but then who cares.”

As is often can be said about anywhere…

N’est-ce pas…

Several price cuts per day here on the Olympic peninsula. More inventory daily. Homes are selling but most on the cuts.

It did get crazy hot up here for three years. Houses doubled in less than 24 months. San Juan island really went nutters since 2020 and it’s dead in the water now

The WFH laptop class is about to get a housing haircut to go with that paycut. Turns out they’re not essential.

Good to know. We live in San Diego but love our trips to Olympic Peninsula and the San Juan Islands and were interested in buying a second home there (maybe Sequim or Dungeness or Orcas etc). We were shocked by the prices though, esp given the weather 6-8 mos of the year. Maybe things will be more reasonable in a year or two…

In March Zillow predicted that houses will appreciate 18% yearly, in June they reduced it to 7.8% and in July to 2.4% according to an article that I read today on Fortune. That’s hell of a change in just 4 months.

How much zillow’s prices prediction would be next month? My guess: 0.0%

Zillows goal is for people to type zillow.com not to provide accurate forecasting.

Take a look at inventory in other western cities like Phoenix or Boise. Take a look at Austin.

Pre-covid inventory at post-covid prices at double the interest rate LOL. Wait til the job market cools, that’s when the real fun will begin. San Diego? Scarce transactions = scare RE commissions and loan origination. No refis at these rates. Realtors and mortgage brokers income heading down down down.

I lived in PHX on two occasions from 2010-2011, living in NYC during parts of 2004-2005.

I’d call much of the metro area a dump. Most of it isn’t very nice. I never understood why housing prices were so expensive even then, as it doesn’t even have California weather. The summers are brutal.

Summers in Phoenix are the equivalent of living through winters in NYC and locales with similar frigid weather, except it occurs during opposing months. We simply trade below zero for 100 degrees, with the added bonus of not having to shovel hot air.

Having spent 6 summers here, it’s not all that “brutal”. You learn to adjust your errands to the early AM, stay out of the direct sun during the heat of the day (believe it or not, 100 degrees in the shade with near zero humidity isn’t all that uncomfortable – especially in shorts with a cerveza, under a lazily turning paddle fan). Our electric bill – for a 2,600 square foot ranch house – averages $200 a month to feed two 3-ton heat pumps and electric cooking/hot water, while maintaining 75 degree temperatures during the summer and 70 during the winters. Our hot water heat is primarily solar (best deal out there – one of the few “renewables” that pays for itself before it wears out and reduced our electric bill by about 30%). Our irrigation is connected to our personal weather station that controls when, if, and for how long the irrigation runs (mostly desert plants – a few large trees and the lot is graded with “bowls” near their base to collect water during a rain event in order to “deep water” them). A water study was just run for our area (our subdivision in particular) and was certified by the county to have at least 100 year’s supply. Our local river is running – though the rapids are slower. Most of our potable water comes from 8 deep wells and the aquifer fed by the river. The river is replenished by the runoff from mountain ridges to our north and east (yes, it does rain/snow up there – quite frequently). The local Yavapai Nation reservation consumes all their water allotment (or they lose it) and floods their land – which also serves to replenish the aquifer. Our dishwasher uses 3.5 gallons of water and the washing machine uses about 4 gallons per load. We have a water circulation pump so we don’t run fresh water down the drain while waiting for the hot water to arrive at the faucet. It is on a WiFi switch that runs on demand for about 2 minutes before we shower. We have had 6.7 inches of rain so far this year (8/22) per our weather station. Average annual rainfall is 7.92, so we’ll exceed the average as we still are in monsoon season and we do, traditionally, get heavier rains in December. Our cars get washed every two months whether they need it or not (usually just to get the dust off).

As I write this, it’s 88 degrees at 11:40 AM. Hardly “brutal” and in mid-August. Don’t look at PHX temperatures. The airport is a heat island. Out here (foothills), the forecast high is in the mid-90’s all week.

There are 8 months here where the weather is ideal…. and you don’t have to worry about frozen pipes, black ice, plans disrupted by rain or snow, nor mosquitos with N-numbers on them. Yes, we have creepy bugs (like scorpions), and snakes, bobcats, mountain lions, javelina, coyote, hawks, eagles, and owls (most of which love fluffy puppies for snacks) but those only serve to keep the wusses away. Haven’t worn socks nor closed shoes since March and likely won’t until November. Have yet to have a pair of shoes or sandals wear/rot out since we’ve lived here vs. every 6 months when we lived in Oregon. Don’t own a lawn mower, a weed whip, hedge trimmers, nor a snow blower.

As far as parts of Phoenix being “not nice”, I have lived all over the country – Midwest, Northeast, SE, Mid Atlantic, Pacific Northwest, California and visited all 50 states multiple times on business. I also spend some time in Austin as my son lives there. There’s “not nice” areas in every city – from Seattle to Portland, ME. Even in Honolulu (walk a few blocks off of Ala Moana near the Hawaiian Prince). I also lived in SoCal (OC – Seal Beach) for 15 years and simultaneously owned a house in the Bay Area for 6. We left CA by choice – not as an “economic refugee” – because we no longer felt safe as we got older – even in Belmont Shore or Walnut Creek.

We have free use of a “luxury” ocean view condo in Downtown Long Beach – near Pine and Ocean. Went exactly once. Between the homeless, the drunks, the caterwauling at all hours of the night, not able to walk safely after dark…. no thanks.

I used to ask people who raved about California: If the weather here was like Chicago’s, would you stay here? After the deer in the headlights look faded…. they shook their head “no”. Can’t justify the prices in PHX? Go to Oakland, look at the housing costs and the adjacent “not nice” areas, and then get back to me on what overpriced looks like.

IMNSHO, every place has it’s drawbacks as well as its highlights. I came here to escape living in a “bee hive” with the constant buzzing of traffic “wash”, airborne rubber from freeway tires (yes, it’s a thing), relentless sirens, fart pipes, Harley’s, crotch rockets, constant aircraft noise, mow-blow crews out at 6 AM, and the like. Didn’t care much for the “marine layer” (no sun until @ noon), “May Gray”, “June Gloom”, the salt air (ate anything metal left outside – including the built in stainless steel grill, A/C condensers, the cotton thread in our convertible top – even ate the heads off the roofing nails exposed on tile roofs), and the general madness of people rushing around for no apparent reason. Don’t miss the 909’ers (Fontucky) invading the beaches and the beach cities, nor dodging the used diapers tossed on the sand. We love being able to go to a local bar and immediately get a table, have a beer, and not witness a physical altercation between some crackheads.

If only the snowbirds would get lost, this place would be near perfect. They bring their entitled behavior, consume our resources, tax our supply chains, overwhelm our medical facilities, and then ridicule the place as they watch the golf matches, collector car auctions, spring training hosted here on their TeeVee, all the time acting as if places like Mininoplace are somehow superior.

Sorry to break it to you but the 100 year assured water supply is a joke paper excercise and doesn’t take into account the CAP supply disappearing. Without CAP the Phoenix metro will be out of groundwater in less than 50 years. Maybe long enough for you and me but it ain’t gonna last.

True. Mortgage originations already down 50% per NPR (Marketplace).

Read an article in WSJ a couple of weeks ago about Boise (poster child for runaway price appreciation). Their market is apparently starting to crash.

We spent time in Boise about 5 years ago and LOVED IT. It was just the right size, big bang for your buck in housing, dining, etc. Great cycling and hiking. I guess we should have invested there, but I wouldn’t go near there now as it is swamped with California refugees and prices spiked.

I heard Adam & Eve were doing a real estate flipping show on tv, but got banished after a staging expert got bit by a serpent.

Liability insurance in Hollywood has limitations on what pets are allowed on set. They needed a special addendum but the couple don’t have deep pockets so they couldn’t afford the coverage. I think the humane society even got involved in this debacle.

One site shows 7 of the 10 most expensive U.S. cities are in California. They base this on the home price to household income ratio. L.A. and San Francisco are the most expensive in the nation. This may be why people are leaving California.

The Midwest has the most affordable housing.

Basically where people want to live is where it’s most expensive.

Truer words were never spoken (or written).

I’m wondering about the name: Nanna Potato. Grandmother living in Idaho?

Most expensive? Not necessarily. Expensive? Yes

Much or most of Switzerland is nicer or much nicer than most of California. It just doesn’t have the weather. It also isn’t turning into a third world country, at least not yet.

And they don’t want anyone else there.

Atherton California is often at the top of the list and residents there become extremely vocal when the city floated the idea of allowing apartments to be built within the city.

What is wrong with that? If you own a single family home you would not want an apartment built next to it? Who would except the apartment builder.

As wolf mentioned. some people want to live in dense urban areas and some people choose not to and do not want dense. Cities should zone accordingly. But for some reason apartment builders like to put apartments next to nice subdivision and use that as a selling/renting point. When selling a home, you do not see a realtor advertising that a home us next to a big apartment complex and saying this is will make your home more sellable.

City planners should zone dense areas and non- dense and nit mix. I learned that from playing SIM city even. lol

Adam & Eve didn’t have very deep pockets. They wouldn’t be able to afford much that’s why they hang out in people’s gardens. I’m sure they’d give their collective shirts off their backs to attain a nice home where they don’t have to be worried about sunburn.

Huntsville Al is booming : Boeing, Raytheon, Airbus, Toyota… real stuff

I wouldn’t drink the water anywhere near the first two.

Yay!

Thank god. I own two properties in San Diego but have been waiting to buy a new primary residence in a nice central area with good schools. Unfortunately for San Diego that means 2.4M price tag right now. Waiting for this market to correct so I can have something to get into.

I have 4 properties in San Diego.

I sold 3 last year.

Only my primary is remaining.

Lets see how things fold out.

I want to exit California but for my kids for few years.

So school teachers in the good school districts can afford a million dollar home or do they have to drive an hour to work

Often times they live multi-generational, have spouses with good income, help from the bank of mom and dad or rent small/ far away.

Even a lot of the engineers I know are in tiny apartments paying near half their after tax incomes on rent.

Many of those fleeing CA are heading to central Ohio. I believe we may become the little bubble that could. Houses are getting multiple offers, prices over asking, and contingency is waved. It’s a weird world right now!

Presumably a consequence of the Intel boondoggle, right? Very sorry to hear this. Sounds like morons from Cali are coming in and tearing a big ahole into the buckeye state. I bet natives will ultimately be sorry about this when they’re all priced out by the calidiots.

“Drive ’til you qualify” on steroids. I’ll never forget passing through the Ohio River Valley and seeing the shanties to the side of the highway.

The real question: At what point do climbing rents clash with falling house prices. The rent/buy tradeoff will keep somewhat of a floor under housing – as long as rents keep rising – which in general they seem to be doing (in our area at least) – and if wages also rise this puts a floor under rentals.

Of course if and when economic reality finally kicks in and unemployment actually starts to increase then we see real moves.

There are so many empty housing units right now that I expect rents to absolutely crash through the floor in the next few years.

What is the source of your info on empty housing units? Most property managers I’ve spoken with in recent past have indicated very low vacancy rates, so I’m not sure how that reconciles with what you’re saying. Glad to learn what I might be missing though

Rob,

Over 40,000 empty housing units just in San Francisco. Google it.

You’re in California: the state overall, and the coastal areas in particular, have lost population over the fast few years, while adding new housing units.

Is there any way to cut the data based on where in a county you are? I don’t know if Redfin or the data gets that granular.

Wondering if (let’s take North County SD or OC) are these cuts are more pronounced for those still listing properties 5-10 miles from the ocean like the market hadn’t turned. Is it more acute the further inland you go? Or are properties west of 5 seeing the same level of haircuts?

Would be fun to put the “coastal SoCal RE is more bulletproof” theory to the test as these trends play out. Some of these counties are so big.

The locust landed on our statues, on our fathers graves, on the

the retail stores, on our cities, on the media…the 2008/2022 locust era might be over.

No. The locusts came in 2012.

Time on market is still surprisingly low in most of those markets despite the median sales price declines, indicating properties are still selling at a decent clip despite surging inventory. The fact that median sales prices are declining as fast as they are is notable. It’s also comical how expensive the cost of living is out there. 99% of Americans are basically priced out of those markets. Make 300k a year? Bummer, you’re still broke in SFO!

When the executives and management start to get laid off, that’s when the coastal Southern CA gets busted. So no, that area is not immune, as long as you’re employed, you can get laid off.

OK Wolf so prices in some areas have come down a tiny bit from their recent highs. For those of us who don’t have very high incomes, housing is still extremely unaffordable everwhere. The metric I watch is [median home price] / [median income]. I am not interested in buying any house until this ratio is below 1.

My guess is that the following fundamentals will continue to drive housing up long term in USD: 1) Govt supported interstate oligopolies buying houses with cheap leverage to rent out 2) Billions of people on earth would love to move to the USA right now 3) Hundreds of thousands of people from all over the planet travel to Mexico and cross the southern border without visas 4) Both dominant parties love money printing and have shown their excitement to massively print USD at every opportunity 5) Literally everyone in my personal network is obsessed with buying houses, talks about it all the time, how wonderful it is, how smart it is, and how I should buy houses too. 6) Both parties and the people enthusiastically agree that the federal government should continue owning and buying as many mortgages as possible.

‘ I am not interested in buying any house until this ratio is below 1.’

Has this ever happened?

This east coaster thanks the west for just about always showing us what is headed our way relative to housing. Easy to know what is coming.

Sure, Pa Ingalls could put up a house in a few weeks that was good enough to get the family through a midwest winter. Let’s say 6 weeks. That was a ratio of 6/52 = 0.12

Another way to look at this – if the custom today is to spend 4x my salary on home, I might as well take a year off and build my own stupid house, saving 3 years of my life for better activities than working.

If you plan to build it in California, better set aside a couple of years to get past the county permit system and bring a bag full of money to give to them.

nah I’ll just build a shanty in a public park in San Diego. Since I’m homeless I don’t need to follow the stupid permit system.

AA is right arm the money in this discussion:

Last house we built in NorCal, after our house was destroyed in Loma Prieta earthquake,( it split at the ridge and fell to pieces, ) took six months and $22,000.00 in ”fees” just to get the permit.

Friends who wanted to build ONE HOUSE of their acreage just spent 3, THREE years and over $300,000.00 to get their permit, same area near Santa Cruz…

Crazy crazy game in CA these days, far damn shore…

Last house we built in flyoverstan,,, two permits cost total of $125.00,,, both over the counter including ALL inspections for septic system with county inspector standing and watching the whole time, and state electrical inspector who was apparently on duty for 5 counties and sometimes arrived near midnight to sign off our efforts…

”LOCATION, LOCATION, LOCATION.”

It was probably assumed that I’d chime in and here I am. Definitely true that sales are dropping. Price is already dropping countywide, no arguing that at all. The City of San Diego presents interesting considerations, though. My observations (and they’re only observations) is that junk is sitting still and experiencing the biggest drops to attract attention. When I say junk I’m referring to the obvious junk no matter what the market. Add to that houses on or near busy corridors, next to drug rehab, etc.

However, several houses in some neighborhoods are still going for insane prices and I attribute it to city policies allowing for the building of multiple units on single family lots. Also, proposed zoning changes have people snatching up as many SFR parcels as possible. This is dramatically reducing the SFR’s out there for public consumption.

Please don’t take any of this as me saying this time is different. All I’m saying is that there are some micro forces at play here keeping some zip codes cooking. No doubt on the macro level we’re seeing the beginning of a nationwide collapse. Interesting that a collapse is happening with 5% loans. This should scare everyone given that most of the older posters here would’ve loved to have bought our first house with a 5% loan. Should this go to 7 or even 10 then all bets are off.

Prices going back to levels of three years ago cannot be considered a crash. We haven’t even rubbed off 2021 gains in stocks or RE.

Your statement on older posters being happy with 5% may be incomprehensible to younger readers. In 1977, I bought 50% ownership in a house in Silicon Valley with a mortgage rate just north of 7%. In 1980, I got a $30K loan from my parents to purchase the other 50% of the house. I wanted to pay the market rate but we settled on slightly lower rate at 8% per my parents. In the coming years that rate turned out to be ridiculously low as inflation ballooned. In those few years, 1977-1980, the house appreciated from $62k to $110k. From there my mantra has been house prices can’t go any higher, how can the ordinary person afford them? Good thing I kept my day job(and my house) and left real estate speculation to others.

The mortgages I obtained for most of my life were over 5%.

I must be old.

Was I unfortunate to have paid over 5% most of my life or was I fortunate to be born when locking in a house price when houses were only “expensive” and being able to bring down the payments with refi’s?

If you purchase a house now at 5%, and can afford it, will the economy crash and rates drop to below 4% again so you can refi? Or will rates rise with a soft landing with long term savings accounts paying over 6% again?

My parents lived in similar times to now.

They had a mortgage from the early 70’s at 6.5% and watched rates climb to above 18%. They just paid the 6.5% mortgage on time and stashed cash in their 15% long term savings accounts.

When savings rates dropped in the mid 90’s, they finally paid off their mortgage. They were not affected that much by high inflation since they had a fixed rate below inflation. They also did not refi at all.

Having a 5% mortgage during 10% inflation is likely a good financial move if you can make the payments. If rates drop below 4% again, you can refi. If rates go over 10%, put money in long term savings accounts and don’t pay down the mortgage.

30 year fixed mortgages and staying in your home gives you a lot of security. It is much better than most countries that only have adjustable mortgages.

I am in San Diego.

I think this time is different and we are special.

Buy now lest you are priced out forever because real estate in San Diego can never go down.

Finally someone who gets it.

I think you are being facetious.

Nonetheless: I hold multiple rental properties in San Diego. Earlier this month I had a tenant move out of an condo in a c 1975 building in Normal Heights. Put it on the market and it sold in 5 days and closed in 14 days. Above asking price (asking price was not below market). Go figure.

In SD where I live in east county, investors have exited the market and solely trying to sell whatever they bought at the peak (Feb – May). They’re struggling with selling these insanely priced properties even with multiple price reductions. A slow buying activity around here but the nicely done homes with a good floor plan and views don’t stay on the market more than a week. These still get multiple offers above the asking price but things are a lot calmer than earlier this year. I go to open houses and I don’t see many people (1 or 2 families at most). I agree with you, a lot of junk out there next to main roads and freeways that nobody wants to buy. Probably these were rentals and finally able to sell after evicting the tenants. It seems that the psychology has shifted that there will be a downturn around the corner and buyers are sitting on the sidelines waiting for good deals. But, a lot of relatives and friends keep saying SD is different and there will be no deals. I am waiting though and have been waiting since Selling my house last May. Not paying rent, but living in another house that we own where other family members reside.

What might be as interesting is to track migration within the US. Then compare apples to apples of values, for sale, sold, all of that, on states losing people as compared to states gaining people. A ‘from, to” analysis.

If you want to ignite a lost of commentary, ad the politics of the losing vs gaining states into it, then stand back with a fire extinguisher handy.