Sales volume plunged 38%.

By Wolf Richter for WOLF STREET.

The median price of single-family houses in the San Francisco Bay Area peaked in April and has dropped every month since then. By July, the median price, at $1.33 million, was down by about $220,000 from the peak and by 2% year-over-year, undoing most of the huge gains in 2021 and early 2022.

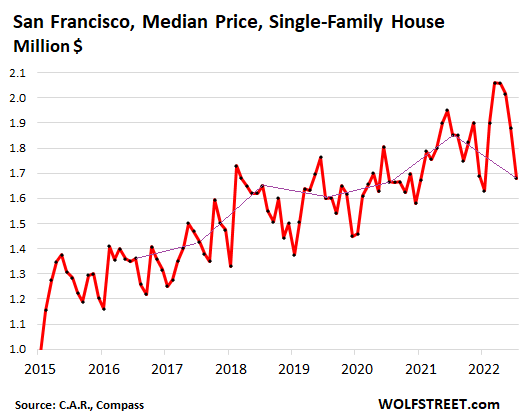

In San Francisco itself, the median price of single-family houses also peaked in April – at $2.06 million, according to the California Association of Realtors. And then it sagged, and then it plunged. In July, it hit $1.68 million. Median prices are volatile from month to month, and they’re easily skewed by a change in the mix of what sold, and by other factors, so we need to be careful here. But this is nevertheless a huge plunge at the wrong time of the year.

Year-over-year, the median price in San Francisco dropped by 9% in July, the second month in a row of year-over-year declines, following the 4% year-over-year decline in June. The first time the median price hit this level was in February 2018. In this chart, the seasonal low points are generally Decembers and Januarys. The summer months tend to be in the upper part of the range – but obviously not this July. The purple line connects the Julys.

Sales volume in July plunged by 38% year-over-year in the Bay Area, according to MLS data cited by Patrick Carlisle, Chief Market Analyst at Compass, San Francisco Bay Area.

“Across the Bay Area, markets have continued to slow and cool, with dramatic changes in buyer demand, inventory, overbidding, price reductions, and year-over-year appreciation rates,” Carlisle said.

“Median home sales price appreciation rates in the Bay Area have generally seen steep declines from those in 2021/early 2022, with some counties experiencing year-over-year median price declines in July,” Carlisle said.

“These changes vary in degree by county and market segment – and monthly data can be volatile, fluctuating according to a wide variety of factors, including market seasonality – but the direction of these shifts is near universal,” Carlisle said.

San Francisco’s extra-special stew of housing market factors.

The spike in mortgage rates to over 5% is tough for homebuyers to digest, and for home sellers to adjust to, and it’s tough for them everywhere.

But San Francisco, with its focus on tech and startups, has become heavily dependent on venture capital funding, and on SoftBank’s funding, and on the hiring by these and other companies, with employees getting huge salaries and fantastical stock options, and all this has become dependent on booming stock and crypto prices. So here we go:

Prices of the most speculative assets have plunged, such as cryptos and stocks that recently had their IPOs or SPAC mergers. Many of these stocks of companies that are headquartered or were headquartered in San Francisco have collapsed by 70% or 80% or 90% and have made it into my Imploded Stocks column. And more broadly, despite the blistering summer rally, the Nasdaq is down 21% from its November high.

The funding of startups has fizzled, particularly the huge amounts that SoftBank used to throw willy-nilly at Bay Area startups, at valuations that turned them into instant pop-up unicorns. But SoftBank got waylaid by the plunge in stocks and disclosed a gazillion dollars in losses on its investments so far this year, and then shut off the money spigot.

Venture Capital firms have pulled back from funding the craziest stuff as the exits via IPO or via merger with a SPAC that they rely on to cash out have been barricaded by the brutal collapse of many of these stocks.

Population declined. From July 2020 to July 2021, the population of San Francisco dropped by nearly 55,000 people, or by 6.3%, to 815,000 people, the lowest since 2010, according to the Census Bureau. But the decline started in 2019. According to estimates by California’s Department of Finance, the population peaked in 2019 at 890,000. So since 2019, the population has dropped by about 75,000 people, or by 8.4%. For people who live here, the City is still immensely crowded and congested, but just a little less so than during peak craziness.

Working remotely and corporate move-outs have left the previously bustling Financial District and the South of Market area a shadow of its former self. According the Savills, 26% of the entire office space in the City is on the market for lease, which is huge. Among the big cities, only Dallas/Fort Worth and Houston are in worse shape.

New housing units have been added at a rate of 2,000 to 4,500 every year. All of them have been multifamily, as no single-family housing has been built in over a decade. Density in the city is growing, and huge areas are being redeveloped. This includes Candlestick Point/Hunters Point Shipyard, Treasure Island, Parkmerced, Potrero Power Station, and others, most of which are industrial wastelands, some of them decorated with nuclear contamination from the US military during the Cold War, the cleanup of which has become its own forever soap opera of scandals. Tens of thousands of housing units are planned for these areas.

But much lower home prices would solve a host of big economic and business issues in the Bay Area – including the entire phenomenon called Housing Crisis.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The purple line is the key. Winter is coming!

Can we get similar data for seattle?

Can we get similar data for seattle?

I would second that.

This is Mr. Richter’s home turf. I think me best go ahead back and read his words me friend.

Not thst i dont see the losses a coming down the line.

-S

Let’s move forward with analyzing real estate prices in the larger metropolitan areas (like SF) not by just talk about the area as one whole market; but, give separate areas their numbers. For example, in SF, Pacific Heights, Knob Hill, North Beach, the Marina, etc. are totally different socioeconomic and financially driven real estate areas than South San Francisco. To lump everything together can give people incorrect impressions. Maybe there’s a better way than what I suggest; but, at least, let’s explore the alternatives.

G,

Analysis by neighborhood is useless on a month-to-month basis because you don’t have enough transactions, and you end up with HUGE and meaningless volatility.

To use your example, Pacific Heights: the median price in July was $5.8 million. But in ALL of San Francisco, there were only 33 total sales of $5 million or more. And they were spread across several expensive neighborhoods, in addition to Pac Heights, such as Russian Hill, Telegraph Hill and others.

I don’t know how many sales there were in Pac Heights, but it was a small number. So one month, you have 10 sales, and another month you have 15 sales, and sales volume jumps by 50%, and the next month you have 8 sales, and sales volume collapses by 47%, and then six super-high-priced homes sell in one month, and the median price jumps by 30%, and the next month it plunges by 50%.

So this stuff is useless my purposes here. If you live in Pac Heights and want to know who of your neighbors sells what, well, then, that’s great, but not here.

The sales #s are too low in Pac Heights because there’s a housing shortage, Wolf. A severe one. Crisis level. There’s just not enough supply!!!!

Bay Area housing prices are so scattered. Foster City just broke records, home bought in 77 for 104,000 sold for 3.68 million last week. Stranger things are coming?

If you want an idea of a smaller area you can go to Zillow and directly compare “sold” houses, apples to apples and by date. You get pics and specifications. You can also go to the “more” tab and choose days on Zillow and directly compare recent weeks and months. Bear in mind the time between when it is taken off the market and closing date. This gives a general time of 1 month, usually, from negotiated price.

This is all Zillow is really good for. Their projected and estimated values are often useless. A property is worth no more than what someone is willing to pay for it and Zillow often has an upward bias.

I agree, Zillow/Trulia have some good data. Looking at comps and prices per square foot would be a way to go. Paragon, acquired by Compass in 2018 had a detailed breakdown of the SF market. Compass’s latest report is for the entire bay area which is useless for this discussion.

Went and looked and Compass’s reports look good. A lot of California Association of Realtors stuff is sales jargon, but their “Weekly Market Minute” is pretty good. It’s audience is realtors rather than buyers or sellers.

Lots and lots of submarine homeowners going to be all over feeling ? Feeling the underwater feeling Mr yellow submarine. We all live in a yellow submarine, a yellow submarine, a yellow submarine…with a nice white picket fence!

Little boxes made of ticky tacky and they all look just the same…..Keep your eyes on the road your hands upon the wheel……Tell the truth. Who’s been fooling who?

Don,

A president once said, “There’s an old saying in Tennessee — I know it’s in Texas, probably in Tennessee — that says, fool me once, shame on — shame on you. Fool me — you can’t get fooled again.”

Hopefully no one was over leveraged and was counting on that sweet equity to fund their lifestyle…

I am sure only sound lending practices were followed.

I don’t think I have ever seen a time that stock and housing market are so unprepared for a tail risk that occurs from time to time. Fed has gotten nearly everyone under 50 impervious to a 1 in 50 or 1 in a 100 year event. Last few times the tail risk has been monetized and the can kicked.

With debt levels so high, inflation running hot and geo political risks simmering the stock and housing markets are not prepared for bad outcomes without a Fed pivot.

I sold out of my last individual stock this morning (except for a gold miner that’s more for protection under certain market outcomes.) The other four stocks I follow are priced as if there is clear sailing ahead.

So…roughly.

Every 1000 drop in Nasdaq equals to a drop of $80,000 in housing.

However, I doubt relationship is linear.

It’s not linear. I did some charts with the prior Nasdaq declines. It’s very nonlinear. It’s all over the place — in part because stocks move so much more quickly, up and down. But you can see the trend.

Its a comin “One flew east, one flew west, one flew over the cuckoo’s nest”

Working its way to the right coast.

Ken Kesey-left coast legend.

San Francisco, Denver, Seattle, Boise, and Austin will likely all experience market declines. I live in a market that’s considerable less “frothy”, an hour drive from Boston where median home prices are ~450k with median household incomes >100k. Even here, prices have soared high enough where there is a stark income disparity between first time home buyers and older homeowners. Young engineers/doctors/wealth managers buying homes from teachers/construction workers/lawn enforcement etc.

*Law enforcement*. Lawn enforcement sounds scary.

JoshWx – That’s what we call our HOA.

LOL. I definitely have mixed feelings about HOAs. Yes, it’s nice that the HOA won’t let your neighbor park three cars on the lawn and paint his house pink, yellow, and purple, but HOAs also seem to always attract the nosy and power-trippin’ types.

Add Miami and Tampa to that list. I’ve heard anecdotes of people buying houses there and also in places like Scottsdale and Austin to “work remote” forever, and now they’re not sure what to do given that their employers want them back in, at least some of the week.

What to do? Do nothing. Or toss the E in ESG back to the C-suite.

Here in Tucson, there’s a program that encourages remote workers to move here. Latest news on this program:

JoshWx,

The way you started off your comment with the string of City names, I thought you were about to start singing Johnny Cash’s song “I’ve been everywhere”. Maybe Wolf can see if there is a link between the cities in that song and the housing bubble cities?

:-)

Happy Friday!

You might be onto something Harvey…

Quicken Loans is offering a 30 yr fixed, 20% down mortgage loan of $300k with a 6.18% interest rate. That rate might discourage some wannabe home buyers.

Not as many $300,000 homes left.

“That rate might discourage some wannabe home buyers.”

No doubt about it!

To stop the inflation, the Fed might need to rearrange those numbers a bit!

I’m thinking 30% down, 20% rates, 6 yr fixed mortgages…

Quicken has to pay for all of that advertising, stadiums, and IT support for their excellent web page. The 300K loan must be some kind of teaser since nobody can find a 300K house.

The Freddie Mac page says average 30 year loans are at 5.22% with 0.7 points.

That’s almost a 1% difference!

Go with a loan broker. You will eventually be sold off to to Freddie or Fannie to someone like Cenlar with a primitive web site but you will still be able to visit the Quicken Stadium to see where other people’s money is going.

that is pretty high, much better buy downs out there

QQQ monthly for entertainment only :

1) Backbone #1 : Jan/ Feb 2018. BB #2 : Sept 2020 hi/lo.

2) June 2022 low, a setup bar. No trigger. June 2022 penetrated BB #2, bounced back up in July and closed above June high, a setup bar. Aug higher high, a trigger.

3) QQQ might turn down, breach BB #2 for a trigger under June 2022

low. That trigger might start a new rally > Aug high.

4) SPX daily gap up on Aug 10 and closed above June 2 high, a setup bar. Yesterday higher high, a trigger. SPX weekly was stopped by the cloud. The monthly might turn red.

SF median price : after x3 dots clustered at the top, the next one

dropped below 2021 high and 2021 lower high.

The last dot dropped below 2018 high testing 2021 low.

2021 low might get a trigger.

Yes, and note the usual seasonality of the lows. Those seasonal factors will be adverse for the rest of the calendar year.

As SS said, Winter is Coming.

in the city worst months are usually June July August….

were under contract at full ask

Some really great data where the housing boom fueled by tech for a few decades maybe going back to the PC or earlier. A master plan for low cost housing and dense population is terrific for economic growth for families where transportation can be mass transit and schools can be planned appropriately. Private companies can accommodate these things governments only want reelection. Pricing starting to reflect reality.

“Private companies can accommodate these things”

You have a severe case of The Cause of the Problem is the Solution.

“…some of them decorated with nuclear contamination from the US military during the Cold War…Tens of thousands of housing units are planned for these areas.”

I suspect that these areas will be sold at a discount as ‘affordable housing.’

“Hell no, we won’t glow” and that sort of thing.

When they built houses on the old El Toro Marine air station, buyers had to agree to never plant any vegetable or fruit trees on their property do to the radioactive waste, PCB, and fuel that was dumped there.

Look up Nuclear Lake in Pawling, NY. Parents let their kids swim in it.

Plutonium 238 and 239: great for the white teeth and glowing skin East Coasters rave about. The latter only has a half life of 24,000 years.

How is the proposal for taxing SF’s 40,000 vacant homes coming along?

That would change everything. Financializationistas would go batshit crazy.

After that all you’d need is an ordinance requiring any and all new development to be single-family homes. Problem solved!

‘Financializationista’. I just made that up.

Copyright © unamused 2022. All rights reserved.

It’s going to be on the ballot. But there are too many exclusions and exemptions for it to be really effective.

I wonder if a vacancy tax would drive many/most of those people to at least occasionally do short-term vacation rentals in them to avoid the tax. I would not think that is an intended consequence.

They won’t tax vacancies. Crushing property values would crush property taxes. It’d be a net loss for the big G.

SF rent looks like it’s going to return to pre-covid levels, although did dip a bit in August.

“They won’t tax vacancies. Crushing property values would crush property taxes.”

Because 40,000 empty homes are so profitable, if only so anarchist wannabes can manipulate supply and rig the market for fun and profit and externalized misery.

Better to put them on the tax rolls to make them affordable and availables, even if the predators have to go cheat somebody else.

Thanks for the purple line. It reminds me that 2019 showed signs of slowdown. But then COVID happened and the easy money. People forgot about those late 2019 and early 2020 price cuts. Looks like the bandaid is about to be ripped off.

I remember thinking in 2019 that houses were getting in the 2006/7 territory and that a pullback may be coming.

HAHAHAHAHA, what an idiot!

Only a bit early,,, as were my thoughts re: RE mkts in the various and sundry states of USA that WE, in this case the ”investors” WE who had been with me since the 1950s thought the same in 2006.

Certainly going to take time,,, maybe more,,, or maybe less than last time…

Remember well that although, eventually, IT IS THE SAME as last time,,, in between it is almost always,,, ”different this time,” but only in some aspects.

FWIW, been paying attention to RE mkts since 1956.

Just to be clear, this is sale price, not asking price?

Yes, prices of “closed” sales.

Welcome to Casino Amerika.

Next up: place your bets on which water source will be most coveted!

Easy, the great lakes. 21% of all fresh water on earth is in the great lakes.

Lower mortgage rates wouldn’t matter, because 1% tax on buyback will kick in.

What does buyback mean in this content?

I think pricing is doing what it does which is causing people to choose alternates to improve their situation. A lot of migration for personal affordability.

Still booming in central NC. Corporations and people still moving in. Real estate development still going gangbusters. Still a shortage of labor.

“Still a shortage of labor.”

I think pricing is doing what it does which is causing people to choose alternates to improve their situation.

Supposedly highest number of people working multiple jobs. Kind of fits what I see with home services. People working a full time job, but moonlighting on the side because people are paying up for it.

Kunal and friends have booked a rafting trip down the river DENIAL.

They won’t go anywhere…

The first two hours will be spent arguing about which end is the front…

The rest of day arguing which way is downstream….

“Year-over-year, the median price in San Francisco dropped by 9% in July”

“Sales volume in July plunged by 38% year-over-year in the Bay Area”

Which one leads the other? Which comes first the chicken or the egg?

What does 38% volume reduction translate into median price reduction?

I’d think a plunge in volumes creates more inventory which in turn drives prices downward.

Inversely, was it high median price levels that drove the volume drop that now drives the median price lower?

Are we missing a component here? What is the buyer pool looking like? Reading about an on going or even accelerating exodus, it is bound to have some kind of influence on this.

“In July, it hit $1.68 million. Median prices are volatile from month to month, and they’re easily skewed by a change in the mix of what sold, and by other factors, so we need to be careful here. But this is nevertheless a huge plunge at the wrong time of the year.”

I think both things are true but the decline is not as drastic due to the overall composition of what has been on the market.

I’ve seen a ton of lower/smaller priced homes on the market in outer sunset and Parkside that appear just from pictures to need a ton of work.

Lots of sales also in all the south of 280 neighborhoods.

I have seen many SF listings get shelved and just taken off the market, instead of giving in to nibbling at multiple price drops. This snapback in markets has been interesting, don’t blink but AAPL isn’t far from its 52-week high. If people still have the paper wealth and a job, it’s hard to see some of the carnage people are predicting here, especially with the amount of wealth already in SF.

Again, if that reverses and/or significant job layoffs come, then you have a different story. But so far, it has been pretty tame and dare I say orderly. Still so much cash floating around out there.

(disclaimer: I have no dog in the RE fight, just trying to sift through the barbell of “ultimate doom and gloom/65% haircuts” and ‘this is just a hiccup on the way to the moon’ mobs; SF has many warts, but also some positives that are hard to match; will be interesting to watch)

It only seems “orderly” because the Fed hasn’t really done much with its balance sheet except for talk. As it is, we’re only 1% down from the peak. Let them increase the speed of the runoff and even outright sell MBS, and the we’ll see.

Completely possible.

Living there for 10 years, SF has some bespoke characteristics though.

1) You have a lot of longtime property owners (many with prop 13 hand me down tax rates from their own parents) who are still so above their cost basis they would need to feel a lot more pain than this and have banked significant sums of money to panic sell a house. They can just wait.

2) You have a lot of offshored cash that found its way into the RE market moreso for parking/safety reasons than for monthly payments. Sure, if the Chinese RE market keeps puking you may have some fall out, but selling their US RE holdings will be one of the last things on the list, as it is their escape hatch in many cases. SF not the only market with this, the whole west coast saw huge influx from 2013-2019 of this type of buyer. A 6% interest rate or a vacancy tax is meaningless to a wealthy Chinese buyer who just wants their cash in the dirt offshore.

3) The trophy house crowd.

All things considered, for all its warts, while sure a correction may be in order, I would bet on SF values holding up before the other ten listed – I think we all knew Boise was unsustainable; you lose your remote job, and how are you recreating that income profile? Some of these bubblicious markets are no brainers.

mid term years in equities, weakness thru 6 months then rush into elections with outsized gains after….

looks familiar, sorry America has followed the path of England, housing will be high for quite a while….15%-20% sure, just enough to suck in more institutions….

been having great time in biostock and mlp rally earning yield and price explosion….heck Buffett was buying big at lows…. scared money makes little

Timberrrrrrr!!!

1. Boise

2. Phoenix

3. Colorado Springs

4. Raleigh

5. Austin

6. Tampa

7. Seattle

8. Sacramento

9. Las Vegas

10. Nashville

Should put Bellevue WA on that list too, even more overpriced than Seattle

Going to be a lot of bag holders for some folks in the coming 2 years if circumstances change for a forced sale.

death, default, divorce :)

Yes, it will be the forced sales that will cause people to stop paying their mortgage and walk. As sales prices keep going down, many recent buyers will not be able to cover the mortgage. People can not care much if the house is stripped and trashed when they hand it back to the bank which causes even lower prices.

Just as the “wealth effect” of QE created the everything bubble, QT will cause the opposite.

Pivot Play is still in effect for stocks.

It does not matter if the FED pivots or not, it is about the perception.

The meme stocks, homebuilders, banks, and tech are hot still

“fighting the Fed’ has been a losers’ game at least so far.

The power of perception(+Hopium++) keep reigning over the reality, unless inflation# in September comes above 8.5%

The most hated rally continues!

Perception is important but Inflation is still at record high. CPI is at 8 plus percent.

FED target inflation rate is 2% plus. Fed has long way to hike rates and do QT. “Richmond Federal Reserve President Thomas Barkin said Friday that more interest rate increases will be needed to tamp down price pressures.”

Market is fooling itself at this point I think.

Bottomline: I don’t see any reason yet for Fed to pivot.

and it will keep on going, printing money in the market has been fun…..mid term election years following same pattern….

so many good buys right now its silly

Funniest site on the web.

The comments here are the best on the internet.

My city is still at the “much fewer sales at higher prices” stage of denial.

I’m just now seeing RE investors as a group- not just individuals, starting to talk seriously about a “possible” downturn (haha), plan “B”s, deleveraging and thinking out loud about liquidating some STRs and “that-was-a-mistake” houses. Also seeing the smarter ones quietly and slowly start to sell off their rental “dogs”, both on online forums and in real life in my area. They’re not selling very fast and are selling for less than asking as they are rank overpriced neglected fixers and tear-downs. Some look to have been vacant for a while. Vacant houses deteriorate fast.

Starting to see a few – just a few more – foreclosures listed as well.

I do see a slowdown in homes listed when the stock market goes up, then a few more when it goes down, but over all there is more and more inventory creeping up as sales are very slow. They are at least halfed, sometimes just frozen.

Lynn

Housing industry is almost 50% of the Economy (includes Consumption segment). The other important component is Energy . Oil may be coming down but it is transient, But natural gas keep zooming up, (electricity) adversely affecting Aluminum and Beer industry! Mkts ignoring the message

“US Industries Are Buckling Under Pressure of Surging Electricity Costs

Industrial power costs are up 24 percent from a year ago according to Energy Information Agency (EIA) data. That was as of May, and the prognosis is getting worse.{..}

On June 22, 600 workers at the second-largest aluminum mill in America, accounting for 20% of US supply, learned they were losing their jobs because the plant can’t afford an electricity tab that’s tripled in a matter of months. Century Aluminum Co. says it’ll idle the Hawesville, Kentucky, mill for as long as a year[..]

Michael Harris, whose firm Unified Energy Services LLC buys fuel for industrial clients, says costs have risen so high that some are having to put millions of dollars of credit on the line to secure power and gas contracts”

(h/t mishtalk)

That ought to get someone’s attention. Our electricity rate has doubled in I think 2 years.

If housing IS 50% of the economy- which sounds rather high to me, that is very sad. And wrong. And accounts for so many homeless people who work and live in their cars as they can’t afford housing. Everything is speculation.

We could use government built housing, although at the prices they tend to pay it is almost not worth it. We just got a small wooden one story new municipal building in our rural area that one of the local contractors could have built for 1/4 of the price, even with materials sky high. The low income apartments they put in a while ago averaged out to $500K per unit in an area where nice SFHs on good sized lots averaged at $250K at the time.

Lynn

You are right Housing appears to be 20% of the economy but count all the secondary and tertiary effects from that (insurance, appliances, furniture++) commuting expenses if away from the job location.

Sunny, I think housing may be 50% of our budget or more but not the economy. But your right, the economy is sinking because a lot of us don’t have extra money after housing and medical.

BTW, it’s interesting that the UN defines shelter for all citizens of a country as a human right but the US ignores that.

& Without major infrastructure changes can you imagine the price of electricity to power electric cars?

It’s interesting that both Idaho and SF are experiencing significant increases in inventory and seem like they will be the immediate leaders in price declines.

That suggests two things: 1) tech industry declines are impacting the housing market (since both areas have more well-compensated tech workers influencing their markets, and at many of those companies, they employees are compensated with stock options) and 2) WFH is somewhat immaterial right now.

If WFH-rollback or continuation was material on housing, you would expect one of these markets doing better at the expense of the other. WFH growth would mean more housing arbitrage because software engineers are good at math. WFH declines would mean folks moving within commute distance of the physical office. Doesn’t seem the case right now.

This makes sense with the tight labor market. We cannot predict what management may do if there ever are a lot of candidates and few openings. But now, seems like management isn’t rocking with boat too much either way on WFH itself.

Wait, wait. Why is it again that so many people live on the street again in the Bay area? Hell just about everyone can afford $1.3 million, you make it sound like That’s a LOT of money. Hell here in Western Pennsylvania it’s chump change. From time to time Wolf post’s some really Funny shit.

San Diego numbers for July are out. I think another 22 percent drop and down about 43% YOY with increasing active listings, but less new listings.

Can you do some commentary about what dynamics you think are at play regarding locked rates, churns, net total of users?

I know you’ve talked quite a bit about shadow vacant homes. Redfin does second home demand metrics, tho I haven’t seen one for June yet. From what I understand, there was also a pretty large extra fee added for second home mortgages several months back. Thanks.

You ain’t seen nothin’ yet!

—Bay Area Realtor(R), 40 years

Yep, sort of. Everybody is putting in solar panels around here (85 miles east of SF) very rapidly because of crazy high pge rates. They could have excess power to directly charge their EVs with.

– Rents seem to have peaked in the US (nation wide). Here 2 articles from the New York Post & Bloomberg that report that rental prices have come down by some 2%.

Perhaps one Wolf Richter has better and more up to date information ??

Rents have not “peaked.” If rents had “peaked,” they would decline after the peak. That’s not the case on a national average — though it happened in some cities during the lockdowns.

What we may be seeing now is that the rate of the rent INCREASES may have peaked on a national average basis, so instead of spiking 17% yoy, they might only spike 12%, but are still going higher.

Yep. And just wait 10 years, when Baby Boomers who bought houses decades ago will start dying off in huge numbers. Because of California’s Prop 13 from 1978, property taxes are based on their historical assessment when ownership last changed, with no more than absolutely minimal increases allowed every year. A house/condo/apartment that Baby Boomers purchased in the 1980s has property taxes more or less based on the purchase price from 30-40 years ago, which in many case is an order of magnitude less than what the current market value is. Unless they had the foresight to put the property into a trust back then, their kids are going to inherit a family house suddenly reassessed at current value, with absolutely staggering property-tax bills. So, the kids will sell the property. To make matters worse, there’s probably not much of a floor to the price they’d be willing to sell at, since there likely won’t be much of a mortgage left, if any, and they haven’t put any money into the house themselves. All in all, starting in the 2030s, California will see the biggest glut of residential property for sale in human history. Much like everything else they’ve touched, Baby Boomers have benefited from low property taxes for decades and will leave an unholy mess for the next generation.