Though spending is slowly shifting back to services, consumers still binged on durable goods.

By Wolf Richter for WOLF STREET.

Despite inflation eating up all income gains plus some in June, and “real” income declining for the second month in a row, and being down from a year ago, and being down from two years ago, and despite massive pessimism for months about inflation and the economy, American Consumers spent their money vigorously in June, and outspent inflation again, and “real” spending rose, even on durable goods, though consumers were supposed to be shifting their spending to services, and real spending on services also rose. You just have to admire this kind of heroic effort to outspend inflation.

Income, adjusted for inflation, fell again.

Personal income from all sources, adjusted for inflation (“real” income), fell 0.3% in June from May, the second month in a row of declines, and was down 1.0% from a year ago, and 1.9% from two years ago, according to data from the the Bureau of Economic Analysis today.

This includes income from wages and salaries, dividends, interest, rentals, farms, businesses, and government transfer payments (stimulus, Social Security, unemployment, welfare, etc.), but does not include capital gains or losses (purple).

Personal income without transfer payments and adjusted for inflation also fell 0.3% in June from May, and was below where it had been in February. It was up 1.4% from a year ago, and has remained below pre-pandemic trend (red).

![]()

Per-capita disposable income, adjusted for inflation, fell again.

The income data above show income for all consumers combined, which doesn’t take taxes and population growth into account. But per-capita disposable income, adjusted for inflation, does.

This “real” per-capita disposable income from all sources fell 0.3% in June from May. It was down 3.5% from a year ago and 6.3% from two years ago, and was up only 1.4% from June 2019. It is expressed in “2012 dollars” to adjust for inflation. It is falling further and further below pre-pandemic trend (green line):

And yet, “real” spending rose again.

Raging inflation bites hard, but no problem, it seems. Consumer spending on goods and services in June, adjusted for this raging inflation, rose 0.1% from May, and was up 1.6% even from the stimulus-miracle last year, and was up by 5.0% from June 2019 (adjusted for inflation!).

It has been very tough for consumers to outspend this raging inflation, given that their incomes aren’t keeping up with inflation, and they’re struggling to do it, but they’re still managing to do it:

“Real” spending on durable goods rose, at high levels.

Inflation-adjusted spending on durable goods – vehicles, appliances, electronics, furniture, etc. – rose by 0.9% in June from May, and was down only 3.1% from the stimulus-miracle spending binge a year ago, but was still up by 22.4% from June 2019, a huge jump (adjusted for inflation!) and still way above pre-pandemic trend (green line).

“Real” spending on nondurable goods fell on cut-backs in gasoline, still at high levels.

Inflation-adjusted spending on nondurable goods – food, fuel, household supplies, etc. – fell by 0.4% in June from May, and was down by 2.9% from the stimulus-miracle binge a year ago, and was still up by 9.6% from June 2019 (adjusted for inflation), and was still above pre-pandemic trend though is reverting to it (green line).

We have seen widespread declines in the demand for gasoline, triggered by sky-high prices that caused people to change their driving habits, such as cutting out some trips and prioritizing the most fuel-efficient vehicle in their garage, etc. We document this “demand destruction” as this phenomenon is called, in barrels per day of gasoline supplied to gas stations, and it was down by nearly 10% in the four weeks through early July, from the same period in 2019. Gasoline is a big item in nondurable goods:

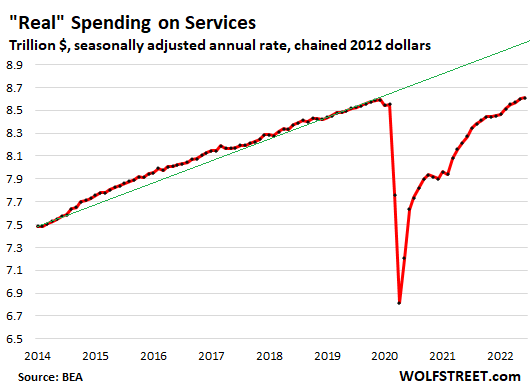

Spending on services, adjusted for inflation, rose.

“Real” spending on services – healthcare, housing, education, travel, entertainment and sports events, haircuts, repairs, subscriptions, streaming, etc. – rose by 0.1% in June from May, and by 4.1% year-over-year. It was up by 1.1% from June 2019 and above the pre-pandemic high for the second month.

Consumer spending patterns have been gradually normalizing in terms of the split between spending on goods, which had been aggressively over-stimulated during the pandemic, and spending on services, which had plunged during the pandemic, when spending on discretionary services – travel, sports & entertainment venues, nonessential healthcare services, etc. – collapsed. But consumers have been gradually shifting their spending back to discretionary services, and away from goods.

The share of spending on services was 61.9% of total spending in May and June, the highest since before the pandemic, and up from the 59% range during the stimulus-miracle goods-buying binge last spring, but remains below the 64% range that prevailed during normal times.

Spending on services still remains well below pre-pandemic trend (green line). Going forward, consumer spending will shift further from goods, particularly from durable goods, to services, though that has been happening more slowly than many had anticipated, and durable goods spending remains very high.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

we spend til we’re on street

coming soon to your neighborhood

I am getting so confused by moves in stocks and treasuries.

Are stocks moving higher because of high inflation given that Fed says it remains committed to QT?

Also, treasuries have deep negative real rates. If Fed is really selling them as part of tightening, then who is really buying them and why?

Traders are buying them, expecting their face value to increase when (they believe) the Fed pivots. They’re not buying them to hold them till maturity.

There is no bear news on the horizon (except Pelosi Taiwan)

*Inflation readings likely to come in with lower gains

*Fed not meeting in August

*Closing in on an election likely to change federal policy direction

*MSM pumping good news for their party

I believe the Federal Reserve’s commitment to QT will prove to have the lifespan of a Mayfly.

QE is “cheating.” It’s cheating everybody but the wealthy out of their purchasing power, their labor, their quality of life. QE is a crime against humanity.

I look at the chart of income adjusted for inflation and income is down. I look at the chart for real total spending and it is below the trend line. Yet, the FED is pursuing a policy that is intended to slow the economy and raise unemployment in order to slow demand? Employment rates have not had much of an impact on inflation recently. I think that many people will suffer from higher unemployment and they may be the same people who are already paying high interest rates on their debt.

I am willing to accept the possibility that I am looking at this all wrong.

American consumerism is so ingrain into people’s mind I think it qualify as a cult like behavior at this point. Inflation is high? No problem we just spend more or take out more debt..what could go wrong?

Where is that money (debt) coming from? The NYFed published in May that Consumer debt increased by $266B, but most of that was in Mortgage based debt. Credit card debt fell by -$15B.

I guess higher rates have maybe limited the use of CC, but is it in Home Equity debt?

It looks like income has increased based on higher wages (not corrected for inflation), so maybe people are feeling flush, but they certainly aren’t saving!

Where is the money coming from — ya gotta be kidding. Very low unemployment, stock/crypto gains, record home equity, savings, pensions. Poor people get welfare, free/subsidized health care, subsidized rent, food stamps.

For some reason most people commenting on blogs like this are very pessimistic. Wolf shows week after week that consumer spending is at record levels. Then come all the claims that the sky is falling. We are due for a correction because of all the debt and bubbles in every asset category, but consumers are just fine.

@Harrold,

I don’t know about others here, but for last one year, I have been spending more and getting less. Spending more is not optional nor pain free.

Any real income gain has been wiped clean. No unrealized gains to offset that pain either.

“Where is the money coming from” is really a good question. Is it BNPL (Buy Now Pay Later) firms like Affirm writing the check, is it just higher salaries, or is it something else? I mean someone’s certainly paying for all of these.

BNPL is minuscule in the overall scheme of things. It was just $43 billion in 2021 (according to Fitch). Near-nothing compared to the $25 trillion US economy. It might amount to $60 billion this year.

Sure Wolf, but then again where’s the money coming from? Remember when there were legit concerns that people wouldn’t be able to pay rent after the whole Covid rent forbearance thing had ended? Not only the whole thing turned out to be a non issue, but now people are spending like crazy.

Something’s not quite adding up here. I think we all know whatever this magic money tree is, that’s going to be the source of the next crisis, just like when people were using their homes as ATM machines.

Read the comment by Rue82. It tells you where the money is coming from.

This is what he said under another article, citing the CEO of Bank of America:

https://wolfstreet.com/2022/07/29/meta-plunged-from-5th-most-valuable-stock-to-11th-behind-visa-in-10-months-647-billion-in-market-cap-vanish/#comment-455577

Rue82

According to BAC CEO, their clients are in very good shape.

Low income clients who had $1k to 2k in their bank accounts pre-COVID now have an average of $7k

Middle class clients who had and average 0f 4 to 5k in their accounts pre-COVID now have $14k.

He said their credit card debt has dropped from 90 billion to 80 billion so their is room for them to increase spending.

He said they also have a lot of Home Equity available.

He said it is odd to see consumer sentiment down so much when financially they are in better shape then pre-COVID.

He also said they their savings are not dipping down.

All of these macro stats are based on samples, with a margin for error and many, many (many) times the collection methodology varies across metrics (different agencies, departments, etc).

So everything is not going to move forward in lockstep.

But, you can get a general feel on direction and speed of change by looking at a large number of metrics.

This should be said more…but it isn’t.

Bite my tongue… thanks Wolf, I guess we are saving! Hurrah!!!

Some purchasing might be fueled by fear: by now or tomorrow it will be even more expensive.

Out here in the Ozark sticks, we be prepin.

Prepin aint cheap…

thanks for the laugh. I was near Warsaw in the stix about 5 years ago, and we bought some eggs from a guy in the neighborhood, who had a .32 in a holster, and he and his mates were ready to blow the local bridges whence the apocalypse.

Fear drives a prepper mindset. I see a lot of friends and family starting to stock up on a years worth of staples. This includes basics for food, hygiene, clothing, and home keeping. Some have pets and are doing the same. Lots of money going in to Prepper Shelters and Off Land Living. I see many old timers paying off all debt and taking to the ground so to speak. I would say much of their behavior is caused from their parents surviving the GD. They say this economy is parallel to the horror stories of the 1930. When people speak like this it usually is from fear.

Preppers be some crazy folk for sure.

With Roubini saying the upcoming turmoil will be worse than the GFC, I don’t blame them…

are they wrong to be afraid?

Better too much food than too much car payment.

Prudence is what drives most preppers, not not fear. Big difference

Yep…it ain’t like toilet paper, baby formula, etc have ever disappeared from the shelves.

All is well.

The philosopher-gods of DC are incapable of error or incompetence.

All is well.

Trust DC.

Love DC.

Obey DC.

Yep, way too much like 1927, 1928, 1929.

“I be planning” to need future farming income since my savings won’t earn anything anymore. I just spent a bunch of it to plant a new cherry orchard in hopes of future inflated income.

Not only that, but, during early Covid time, you couldn’t get anything repaired or replaced and my old equipment started breaking down. I am overspending just to get all the repairs/replacements done cause it will only get more expensive. (New farm equipment, like lots of other things, is wildly expensive and waaay too hard to maintain.)

I’m 71. I am still in pretty decent health, but this has *got* to be my last ride. My husband has crazy dementia, getting worse all the time. He needs “memory care” @ $10,000 per month ++ which *no one* can afford. I am exhausted all the time. I pray daily for him and me.

This monetary and fiscal insanity is killing us all even if daily life doesn’t.

Meanwhile people can’t pay there AT&T bill on time ,there’s a huge disconnect between stock marker and Main Street

Really bizarre times. People can’t pay their phone bills but they can run car and house prices up to record levels? Something’s not adding up.

Depth Charge,

You’re spreading BS.

#1. People are paying their phone bills just fine. What SOME are doing is paying them a little later than before but they’re paying them — as per CEO of a telecom, who was cited on this.

#2 OTHER people are floating in money, and they’re not the ones that are paying their phone bills more slowly. They’re the ones that drove up prices in big-ticket items.

Btw, I am sure Papa Powell loves seeing these numbers, it backs his view the economy is still strong, so absolutely no excuse to back down on rate hike and QT. In fact he should open his eyes or maybe get some new glasses so he can clearly see that consumers and stock market didn’t quite get the memo because trying to scare the market and consumers into restraint to wishfully think that will drive down demand and inflation is absolutely not working.

Yep. Inflation isn’t going anywhere unless rates are substantially higher than they are today and QT becomes faster.

I reiterate my point that I believe inflation is largely being fueled by the top 10-20% at this point, meaning that unless we take some air out of the asset bubble, inflation will continue.

Yeah I saw someone tried to explain it as a pyramid, right now the lower part of the pyramid, lower class, lower middle class is seeing the world through the lens of recession, middle, upper middle, upper class is feeling inflation and for the most part still party on Garth mode and upper upper class is boom time, eventually it will move up the ladder, we are just not there yet. Bottomline is the upper upper class is soooo insulated, if it hits them it will probably take a full on revolution for them to truly panic, The whole moving up the ladder presentation makes sense to me. Just really sucks to me that the bottom are getting the worse of it and feel completely powerless to do anything about it since people in charge have loooong failed them.

Bottom probably won’t feel as worse because they never had it any better. Those who accustomed to pain free life last 2 decades will be hardest hit.

You hit the nail on the head. The upper middle to upper, even the frugalish ones, are basically saying “Ehh, yeah it’s annoying that all of the restaurants cost more now, but what can you do, prices are going up everywhere” and for the most part still pay whatever.

There aren’t enough of the upper upper to really move the market. It’s the upper middle and upper (top 20% or so) that is causing this inflation. As long as stocks and housing is artificially inflated, they’ll continue to do so.

Much of the supposed middle class is actually the “working class” income wise, whether they work in an office or not.

Median household income is about $70K. Median household net worth was about $130K, presumably somewhat more mostly from higher home prices but that’s not directly spendable.

By my estimates, only the top 20% by net worth are solidly and consistently “middle class” economically. By income, somewhat more but only a low proportion who are at or near the median income.

It varies noticeably by household size and location too.

Middle class is the one who would feel the most pain.

People in the bottom has never had it good and govt is/was there to help them out.

People at the top would really feel the pinch if the asset bubble burst big time.

Bottom and middle class really has no stake in these monstrous asset bubble generally speaking.

I guess top 10 percent hold 95% of all assets in USA.

This is great, raise rates higher. Low rates and rentier activity are an absolute cancer on society. I don’t care if he lies about a recession, the best thing he can do is to slay the beast.

I’m thinking this is a poor person’s recession…to wit, Walmart earnings awful but Amazon forecast is great…poor folks don’t buy at Amazon…

Amazon wasn’t any good. But of course the spin is world class.

Poor folks don’t buy at Amazon?

I think that smart shoppers find great deals on both Amazon and Ebay, and no gasoline involved (that is, having to go to the store to get the item) — especially with free delivery. I personally live 15 miles from the closest store, so the wife and I drive a lot less and purchase more online.

We’re not exactly poor, but fixed income (lower middle income).

I saw something a while ago that 166 million U.S. consumers have Amazon prime. I don’t know how that’s calculated, for example, if a family of four has a prime membership that they all use, does that count as one consumer or four? But in any case, it’s clear to me that Amazon is NOT just for the rich.

Once a week driving similar to store was our rule in flyoverstan for many years, so proceeding similarly back in suburbs these days.

Anyone with any idea of how much it costs to run a car or pick up truck can figure out the delta between driving to buy or having ”stuff” delivered.

Doesn’t always work, since some stuff ya just gotta check out in person before buying, especially if you’re the least bit ”picky” about characteristics/quality!

Vehicles are a lot more expensive per mile than most folks consider, but actual average costs can be found at AAA website and many similar.

Most Americans are real bad at math. Almost no one here thinks of the total cost of car ownership. How else do explain people that finance $80,000+ commuter pickup trucks and SUVs with 4-figure monthly payments but expend all their energy complaining about the cost of fuel?

DD-forget ‘math’, start with arithmetic! (fuel costs seem to be at least one thing even the most ‘conservative’ average citizen desires ‘socialization’ of, as extensively discussed in previous editions of Wolf’s most-excellent establishment).

(…and now, previews of the next thrilling episode of our long-running series: ” ‘Honest’ Price Discovery, Perpetual Undercover Agent”…).

may we all find a better day.

There’s a lot of back end inflation, fees and subscriptions, which often are small nominally. My natgas bill doubled to $25 dollars. I thought Powell had it right raising rates in 2018, until the market bent but did not break, and then he caved to political pressure in 2019 and US was heading into recession when Covid arrived. Then I thought Powell had it right on the transitory inflation call, and now it seems to me he has the biggest mistake ever, but maybe these rate hikes just don’t matter. The US consumer through the strong dollar should enjoy an advantage in imports. Raising the interest rate cost of consumer spending is not the right solution. I am getting more than 2% overnight at my bank. The flipside of that is not good for small business while the vultures on Wall St are in the Fed’s pocket. That recent rally off his hawkish boilerplate is an embarrassment to the US central bank.

I wholly disagree. The rate hikes certainly do matter, as they lessen the ability of zombie companies to stay alive, which is fueling overemployment as well as general increased spending.

The dollar is only strong because the FX markets believe Powell’s inflation hawkishness. If he doesn’t walk the walk, watch that go away.

May also lower stock buybacks by companies. But who knows….

QE and ZIRP destroyed the US economy.

There was a book written about greed ,but people tend to ignore it . Also has some rules for society to follow,but people tend to ignore it. History repeats this will end badly .Some really bad players IMF,WORLD BANK,and WEF

yep

Ambrose Bierce,

The Fed relies on the markets to transmit its monetary policies via financial conditions to the economy. If markets refuse to transmit those monetary policies and go the opposite way – which they’re now doing, and financial conditions have become EASER over the past month – then the monetary policies become ineffective.

So the Fed has to tighten and tighten and tighten until it sinks in what it is trying to do, and until the markets fully transmit these monetary policies to the financial conditions and from there to the economy.

In other words, this could get really bad if markets refuse to transmit and continue to be tightening-deniers.

the problem Wolf is that nobody believes that message…I’ll ask again, why did Powell take his foot off the neck of inflation with that press conference? The markets are interpreting what he said exactly as he intended it…he KNEW the markets were looking for a SLIVER of hope…he gave them the full 2×4.

I think we all know answer to this question. Powell is all smoke and mirror, nothing more.

September will finally put this to rest.

Peter

“I’ll ask again, why did Powell take his foot off the neck of inflation with that press conference?”

I’ll answer again: He didn’t. And people/markets who believe that he did are practicing willful self-delusion. The Fed will win this fight with the markets. And eventually, markets are going to transmit those monetary policies to the financial conditions, and the longer they refuse to, the worse it’s going to get when they do. It’s as simple as that.

It’s fine with me because I think much higher rates are what we need, and as long as markets act this way, the Fed will continue to tighten with ease, there won’t be any resistance, and it will be free to tighten because no one is screaming about it.

But then, at some point, it will sink in. By which time rates will be much higher than now, and it will cause a lot more turmoil in the markets. But fine with me.

I do agree with Wolf, fine with me. Plus I like seeing those emails coming through from my bank and credit union that your pathetic saving rate is now at 2%. Still wayyyy behind the curve but I’ll take it, certainly better than pounding sand seeing my money get .5% interest just half a year ago.

Also reminding myself, even not keeping up with inflation with current interest rate is still 1000x times better than losing 50+% if not more had I invested in ARKK

Wolf, today’s Federal Reserve officials are historically talkative and public about their policy views.

They’ve yet to meaningfully push back on the market’s interpretation, which implies they endorse it.

The market believes another 0.75-1% of rate increases will permanently solve the inflation problem, and those increases will be rolled back next year. That’s the full extent of tightening the market has priced in.

Jackson Y,

Bostic just did today! First Fed speaker since the meeting, and sure enough, pushing back. But no one was listening to him because no one wants to hear it. Like a said, the markets are now delusional.

Wolf, your comment reminds me of what Volcker said after his retirement. He was angry that the markets didn’t “listen” to him, when he was trying to talk them down. So he decided to shock the markets with large rate increases.

Same thing happening 4 decades later. Large rate increases and markets rolling on as if nothing is happening. This will give Powell the confidence to be hawkish until something breaks.

“But no one was listening to him because no one wants to hear it. Like a said, the markets are now delusional.”

That’s the moral hazard the FED is responsible for creating. It’s just a bunch of reckless gamblers now, betting that the FED is going to pivot and make them all whole, no matter the risk. Just load up because “the FED’s got my back.”

And this is the part of the story where the FED continues to fail miserably. They have underestimated the damage they have done, and overestimated the effects of their talk and paltry actions. They are not accurately assessing the current situation, and the extent of this mania.

This failure was no more clear than their abysmal performance Wednesday. A 150 basis point hike would have been appropriate given the fact that CPI is so far divorced from the fed funds rate. Yet they soft-pedaled the hike. Yeah, yeah, yeah they are saying they are “front-loading” because they normally do 25 basis points, but this is not a normal situation.

Once the FED stuck to 75 basis points, in conjunction with Yellow Powell’s statement that 75 basis points was not a given for September, the market shot the moon. And we’ll probably see everything go back to all time highs. More failure from Yellow Powell and his buddies. Or is it intentional?

He’s controlled by politicians,isn’t strong enough to do the right thing .TRUMP ran him over should have never been reappointed.Same as giving a career politician the White House as a going away gift

Wolf

“So the Fed has to tighten and tighten and tighten until it sinks in what it is trying to do”

I really want to believe you.

If so why did Mr. Powell said during press conference that Fed is closed to ‘neutral’ rate, NOW. Does this sound hawkish? Mkt decided it is ‘dovish’ with ‘tongue in cheek’ variety and zoomed again and again! Perception kept winning over reality.

If the inflation # in August and or in September below 8%, zoom again Mkts will. It is akin to ‘front running’ when ever QE was announced since ’09, when ever mkt tanked 5-10%!

Call me cynical but don’t have any faith in this Mr. Dovish

Why are you even trying to “fight the Fed?” That’s what you’re doing.

“In other words, this could get really bad if markets refuse to transmit and continue to be tightening-deniers.”

The FED continues to fail day after day, week after week, month after month. They ALWAYS get it wrong. It was clear to anybody with even a modicum of common sense that BTFD, “the FED’s got my back” was so ingrained in the markets that it would take something extraordinary to break these reckless gamblers. They’ve been driving everything to the moon since the last rate hike.

Not only that, after the previous FED meeting, inflation came in “hotter than expected” – another glaring red flag. Then you consider that the fed funds rate is 7% below CPI. Yet Yellow Powell continues to “monitor the situation,” doing too little too late. This guy is NOT THE MAN FOR THE JOB! And now he’s going to sit back for another month or two and let everything rage on.

2 trillion on sidelines = markets got to get that money

Powell is no Paul Volcker, and he’s probably not even in a league with Arthur Burns.

Even after settling for a .75% bump, he could have used more forceful language or at least he easily could have omitted his little accommodative hints if he wanted to get a point across. Statements made by Fed officials, especially the chairman, are very carefully crafted to have a desired effect. He has leaned hard on jawboning this year, but it just isn’t working like it used to. I hope he has grown a pair and proves his doubters wrong, but coupled with his track record, I don’t blame anybody for not taking this guy seriously.

There must be a formula driven “channel” for Fed Funds

If inflation turns out to transitory then the rates raised to meet the threat can be transitory as well.

No more “we think its transitory” and “ we’ll keep a close eye on it”.

Perhaps we need mechanisms that automatically engage and transmit.

yep

ZIRP is just not normal. It has created a whole host of social and cultural problems. Wealth gap being the most obvious, but it also means companies don’t have to work as hard to create better services or products and take on an imperious attitude. It also means ridiculous ideas that during normal credit era that would not have passed common sense filter get funded and become start-ups. Signal to society that common sense is out of fashion. So I totally agree with you that higher interest rates are needed. In some ways I also think it would give incentives for re-shoring manufacturing on the US.

Candid-a lot of ‘the Market’ in the last two decades akin to barflies never quite ripped enough to be cut off and 86’d, but who turn ugly at an increase in the price of served booze? (…and a few now who are getting 86’d…).

may we all find a better day.

wolf you were spot on on this one, kashkari came out today and essentially said that the market “got it wrong”. I wonder how long will it take before the market gets it. perhaps a few more fed speakers will come out the next few weeks to clarify the feds position. personally i think fed will definitely raise rates again in september, either 25 bps or 50 even. that would take the rates right over 2018 when it nearly broke the market.

And on 14 July, in an interview in the Minneapolis newspaper, Kashkari, who is not a voting member this year, stated that he’s ‘open-minded’ about a 1% rate hike. Two weeks before the recent meeting that gave the 0.75% hike. A rare turn for a “super-dove,” as Wolf has described him.

“I continue looking for some good news to suggest things are moving in the right direction, and so far they are not,” Kashkari said.

He added he was disappointed to see in the most recent inflation report that price increases have not started to moderate. “It surprised us. It was higher than we expected and broader across categories.” Again, quotes are from 14 July.

We will see. Asset markets are in $500 trillion range and highly leveraged. If markets get panicked, the Fed will have a hard time not easing.

“That recent rally off his hawkish boilerplate is an embarrassment to the US central bank.”

I think Powell and company realize that they are a laughingstock, but I bet their delusion make them get up each morning.

Dang, my bank’s only giving me 1.4%.

I want to see a 15% CD. Because then I’ll know the Fed is serious.

ibonds are a good investment right now-with a return of over 9%.

Lucca :

but you can’t put any money in ? Its useless

$10,000 Max ?

Series I bonds are 10000 for each account so for my family of 3 that is 30000 a year.

Wolf you should move to a subscription service ,1$ a week I’ll gladly pay

Ambrose Bierce said; ” I am getting more than 2% overnight at my bank.”

————————–

Who is your bank?

Where do you live with a 25$ gas bill I’m moving

CPI probably doesn’t capture actual inflation making it hard to calculate real spending. Also there’s likely a percentage of savers buying goods/preps they anticipate they’ll need in the future but deciding to buy now in case inflation gets worse.

Truflation does list inflation at 9.9% above the consensus 9.1% and yeah, survival mentality could be some of it!

BINGO! I’m surprised we don’t see more of “buy what you’re gonna need and use” as “investment” advice as it’s one of the best ways to save money right now. I’m doing it myself whenever I find I am out of something I just buy a giant batch, e.g. toothpaste, soap, etc. as long as it won’t expire why not buy it now for 5-10% less than later?

We all did the same in the 80s. Get paid, buy extra of nonperishables before they went up again.

We are doing it again now, mostly if something is on sale. A really good sale.

The inflation numbers they use are just made up gobbly gook….they bear no resemblance to reality…this whole inflation fight is a total joke…markets will be at all time highs again very soon…

No, they most certainly will not be. EARNINGS are what matters and EARNINGS ARE PLUNGING. Pay attention to what matters.

Wait there is a denominator in the P/E formula?

Yep I’m busy converting my Clown CAD into goods.

And then there is the bond market inversion… 1’s & 30’s are getting close to inverting! How weird is that!

The drop in 30’s is driving mortgage rates down, which will fuel some home buying perhaps! Let the party continue!

Who cares? What possible difference would that make to anything. The fact is that US Treasury yields (interest rates) are ENORMOUSLY VOLATILE and that is the real issue to watch with them not how they are at any given moment in relation to each other based on duration.

And no reason to dump your rental cuz crypto/stocks are getting higher again.

This is one messed up country or what….

There are alot of very well off baby boomers ( a bulk of the upper class I suspect), still spending like no tomorrow. I’m a tail end boomer, I don’t spend alot, but like many other boomers, we made oodles of money during the pandemic. Even with the down market, most of us are still have a net gain if one goes back more than one year. Phoenix’s assessment is spot on…

Actually, Frank, you would be a member of the

“Jones Generation”…

As am I…

Big, big difference between the groups….

wolf do you think there will be a spending cliff if current income trend continues with fed raising rates again by lets say 50 bps in september?

for a regular joe (like me) it would make sense to hold off on spending on big ticket items until the fall?

If things get bad for regular Joes like you, normally they tend to stop buying big ticket items. On the other hand, your big ticket item could be 20% more by Autumn…..

Prices of big-ticket items like new and used cars could be LESS by autumn. Prices of durable goods are declining at the moment in many categories from their huge spikes. But prices of services are spiking.

That’s not to say that we might get another spike in prices in durable goods. This inflation has dished out lots of surprises.

I recently learned that there are “car flippers” who are buying brand new cars and then re-selling them for a profit. I don’t even understand how this is possible given taxes, licensing, etc.

Went online and priced a new Dodge 2 dr. 4×4 at 37K. Went to the dealer. He figured it at 42K. Special order, so he called Dodge to see if they would take it. Yep,,6 month wait,,46K. Price went up 9K in 9 minutes. I paid zero!

That’s how all automobile dealerships work.

“That’s how all automobile dealerships work.”

Bullshit. They buy wholesale from the manufacturer then sell retail. I’m talking about retail customers buying retail from the dealer, then flipping. Try to keep up.

Is it possible that durable goods spending is on the upswing not because people are flush, but because the durable goods people need are finally in greater supply?

In our little mountain town, for on anecdotal example, people were reluctantly buying secondhand appliances from Habitat and such because Lowe’s was 6-9 months backed up.

Yes, there is some of that. And there will be more of that — particularly new vehicles but other stuff too.

Wolf u we’re in automobile business,what are real margins on cars from dealer to public

Well, it you sell at sticker or above sticker, they’re pretty good :-]

So this is about my experience with Ford (mid 1980s to mid-1990s). Back then, import brands had far bigger profit margins for dealers than Ford had. Everything has likely changed today.

When I was in the business, Ford reduced the spread between “invoice” and MSRP every year or two. For each model year, it would raise MSRP but would raise invoice more, and the spread narrowed. Toward the end of my time, it was about 7%. In addition, we got the “holdback” which was another 3%. And then there were the advertising incentives and the floorplan credit.

So if you turned you inventory quickly and sold at MSRP, you might have made 12% on a vehicle, all combined.

But no one could sell at MSRP. There were 5 Ford dealers in the city, and everyone had the same product at the same cost, and we all competed on price with each other. If you tried to sell at MSRP, your customers would just walk out and go to the next dealer 5 miles away.

Also, expenses involved with selling new vehicles were huge, particularly commissions and advertising. So we never made a lot of money on the new-vehicle side.

But we made lots of money in used vehicles (where buying is the key component).

And we had the largest service department in Ford’s Southwest Region, which was a huge money maker. We had a huge shop, ran two shifts, were open 24 hours a day, except Sunday.

We also had a rental fleet of around 500 vehicles, which was a great deal because we got the rental-fleet discounts from Ford for those vehicles (which was below our normal cost), and we made money renting them (it paid for depreciation, financing costs, maintenance, staffing of the rental department, etc. and generated nice rental profits after all expenses), and then we sold them a year or two later as used vehicles to our retail customers and made good money (recaptured a big part of the depreciation) on those deals.

So you make money where you can.

That’s very possible, and maybe even likely.

Caveats like this, and there are dozens, can give you a sense as to how tricky it can be to do economic modeling and economic projections. It’s a moving target and it morphs in ways that can be unpredictable.

Mix in human psychological anomalies, stir, and maybe have an antacid handy just in case.

Generally, Americans have NEVER HAD MORE MONEY TO SPEND at any other time in the history of America as they do now, and generally, people simply buy whatever they want whenever they want and have little to no concern about marginally higher prices on anything. What possible difference does that even ever make?

No, we can’t buy whatever we want. Most people can’t.

California is a reality distortion zone. People have no fear of debt and no lack of availability of credit here.

“NEVER HAD MORE MONEY TO SPEND”

Wrong they don’t have money however they have access to abundance of credit.

The reason Americans seem to have endless amounts of money to spend is that they refuse to save for the future. If Americans had a decent savings rate to provide for their families in the future they would not have as much money to spend on stuff they dont need.

Instead of saving for things like retirement and future healthcare, Americans expect someone else (the government) to pay for their future.

Can you tell that I am starting to dislike many of my greedy, short-sighted fellow Americans?

Saving isn’t encouraged in a society where the risk-free rate of return is either negative or absurdly negative. One of the many distortions caused by FED policies. The system encourages short-sightedness so cut your fellow Americans some slack.

rojog-well-said. Let us not forget (i admit, in my own anecdotal- geezer observation) this generational aversion to savings had its roots in the stagflation of the ’70’s-’80’s. Savings value was destroyed wholesale as revolving consumer credit became ever-so-easy to obtain. Many, many children grew up and absorbed this ‘workaround’ for living a ‘Murican life in households that maintained an unrealistic standard of living by ‘minimum payment’ on the cards-‘savings’ just didn’t appear to have any day-to-day benefit, or pay for any future family needs as savings value seemingly vanished by the day. (also, card debt was disposed of relatively easily by BK in those earlier years, though BK was somewhat counterbalanced by being less-acceptable societally back then…).

may we all find a better day.

I will admit that far too many Americans don’t save as much as they should for retirement and health care, but considering how for many people it takes two household incomes to maintain what we call a middle class lifestyle and how people who dutifully saved their money in 401K plans saw their investments shrivel up during the 2008 financial crisis, I can understand why they would be wary of trying to save anything.

Where my brother works companojust gave receiving clerk 2$ raise because he had a interview with another company. STAGFLATION RAGING

That’s not stagflation. Stagflation is high unemployment and high inflation.

I believe we have more credit ,not the same as money

Americans tough??? Hhhmmm….that’s being really nice.

Many (not all, but many) Americans are programmed sheep to not save, but the spend, spend, spend and spend some more. Get in debt…..it’s good…..

What a complete joke the inflation figures are.

Who here, who isn’t a rentier, would say they’d score 2014 as a “12” and now as a “14.5” for disposable income?

Would love to see that graph further back. Who is finding they are rolling in it now, as I’m sure a graph back to 2000 would indicate?

Houses keep getting bigger, new vehicles keep getting nicer and more powerful and bigger too with lots more features, and vacations are getting fancier, and people are still paying for this big fancy stuff because they’re getting raises and they’re switching jobs to make more money, and they’re starting companies and are raking it in, and they’re charging more for services they provide, and they’re making more money off their investments, rentals, etc. etc. There are 333 million people in the US, and a lot of them make lots of money. And a lot of them make too little money. And that’s what you’re seeing

What an important chart. When the slope flattens or dips below trend for more than a few years it’s probably a recession. Looks awfully flat with 2019 to me right now.

Money is a debt base system, a minority make a lot of money, the majority owe these people a lot of money. Everybody can’t be rich.

No way has cash held purchasing power anything like as suggested by that graph. The deflator isn’t correct.

I understand that some people think that everything is fake, that the nice houses and the condo and apartment towers are fake, and that the expensive vehicles that drive by are fake, and that the expensive smartphones are fake, and that the expensive farm equipment is fake, and that the factories are fake, and that all this stuff that we see today that we couldn’t even imagine 20-30 years ago is fake, and that all the jobs are fake, and that the only thing that’s real are the homeless people, and that everyone is homeless and jobless and that the whole place has been in a deep depression since Nixon took us off the gold standard, or whatever. I totally get that.

georgist,

This morning I watered my apple trees and my garden. Then I got fresh herbs and a hot banana pepper for my breakfast omelette. Drove my BMW M4 to the beer store for 0.0% NA and a stop at Trader Joe’s. Next was a ride on my $12,400 Bianchi carbon fibre racing bicycle. Before dinner, a quick jump on the V4 Aprilia to go fuel it up for the weekend.

Ain’t nothing fake about living well.

About to listen to my neighbor play the clarinet with the Minnesota Orchestra for a piece by Strauss, Vivaldi and Beethoven’s 5th live from Orchestra Hall in Minneapolis on my HD FM radio via a state-of-the-art made in the USA hi-fi stereo in my living room.

“Life is good in Minneapolis.” -DanBob

Correction: Verdi.

I think you must have inherited it Dan because anecdote != data.

Wolf that was a truly unhinged reply.

georgist,

It was sarcasm in response to your series of unhinged comments.

Georgist, some commenters are braggards and love to rub people’s face in expensive, exclusive sh*t. They blab incessantly about what they own or can do or their education (due to the good fortune of their parents, typically). And for those commenters who blame poor Americans for not saving money, and buying crap from Walmart… it’s because they’re driven pillar to post with anxiety and inferiority over not having the sh*t that some insecure people incessantly brag about.

Wolf I questioned the validity of the deflator on the real GDP figures.

That is absolutely not “fake”, it’s not “unhinged”.

Why have a blog with comments if people can’t make valid comments about the full correctness of the data? We know housing isn’t fully incorporated into the inflation figures under the model of cost-of-carry vs total cost paid. It’s all blows up when rates go up. Exactly the same as auto loans.

It’s your “rentier” nonsense and other stuff that is unhinged. Examples from your prior comments:

“Who here, who isn’t a rentier, would say they’d score 2014 as a “12” and now as a “14.5” for disposable income?”

“Low rates and rentier activity are an absolute cancer on society .”

“Money is a debt base system, a minority make a lot of money, the majority owe these people a lot of money.”

About that last one: Investors are the ones that have a lot of debt, not impoverished individuals. If I invest $100 million to build an apartment tower, I borrow $95 million from the bank (I owe the bank), and put $5 million of my own money at risk, and then I pay back interest on the loan for many years hopefully from sufficient rent collections.

The real source of this ability to consume is government debt. We keep spending and borrowing more to prop up the economy. Along with asset appreciation, that is where much of the wealth has been “created”. The problem is that asset bubbles and debt, and trade deficits, are not sustainable in the long term.

I think what’s going on here is that the American consumer is outpacing CPI; not actual inflation. 4% higher than CPI might be -2% if we used an honest measure.

True, and -2% seems light, really.

Today’s June PCE inflation reports showed inflation increased month to month and year to year. PCE and Core PCE inflation both increased.

Exxon reported earnings this morning. The stock did not grow very fast, but did better if you add in the dividends to the stock price appreciation.

Heroic or stupidity? Heroic or ignorance? Heroic or delusional? Heroic or buy now default later? This as heroic as 2007 with mortgage borrowing, society in the west has changed & totally devoid of sense.

The simple fact is it’s all debt that can never be paid back, unbelievable leverage in all markets, it’s a ponzi, a Madoff of epic proportions, smart phones has spread the indoctrination faster & wider, everyone is totally immersed in debt, they even buy socks with debt.

Soon it’ll collapse, Powell is a fraudster, he is like Bernanke deny reality cuz behind the scenes they’re manipulating markets to try engineer an escape from collapse. It’s always the case, this happened in 2006, when housing started collapsing they desperately loaned to unworthy borrowers, now they’re doing the same 100 x.

Powell saying 2.5% is neutral with 9.1% inflation (reality it’s 20%) also said neutral was 2.5% in 2018 when inflation was 1.8%. A deliberate signal to markets that rates won’t really rise, all the maturing bonds reinvested will ensure that, balance sheet doesn’t have to rise cuz hundreds of billions mature & are reinvested constantly suppressing rates.

It’ll implode & they can’t save it, so be warned.

We are old and have no debt. Many of the olds have no debt, which is why we can still buy groceries.

And because we save, sometimes for several years, we can go on vacation.

That’s cuz lenders don’t give unsecured loans to old people without hard backing assets, but ya the minority, I’m talking about sensible people but but profligate debtors which are the majority.

The point being as unemployment rises so will defaults, another worse financial crises is coming very soon.

“We are old and have no debt. Many of the olds have no debt, which is why we can still buy groceries.

And because we save, sometimes for several years, we can go on vacation.”

Yeah, that’s us too. And there are legions of us watching this Sh*t Show unfold.

It’s almost like going to the movies without actually going.

We are old worked our asses off sometimes 2 jobs most of our lives to get the American dream now beauricrTs,are destroying it on purpose . To what end

Historic or stupidity,my thoughts exactly.If people quit buying this shit would end quickly

100% correct. I normally agree with Wolf but think he’s dead wrong on a hawkish meeting interpretation….and the markets are vociferously supporting a dovish interpretation.

The markets are MERELY BEING DELUSIONAL AND IGNORING THE STATEMENTS AND FACTS about the economy and the Federal Reserve and participants in those markets will end up with huge losses and rude shocks and will be screaming, ‘What Happened?’ The answer, of course, is THEIR STUPIDITY HAPPENED.

Peter,

You and the markets are “fighting the Fed.” Good luck with that. The old rule is: Don’t fight the Fed.

People are being delusional about this, and the Fed will now crack down even harder and longer to get the message through to you.

You’re now my barometer as to how far the Fed will have to go. By the time you back off this claim, I would say the Fed can stop after an additional 150 basis points. So if you still make that claim when the FF rate is 4%, but then at 4.5%, you back off, I’d say the Fed might go to 6% and stop. But if you don’t back off until we’re a FF rate of 8%, then I’d say the Fed will go to 9.5% LOL

You people don’t realize that this kind of market behavior is throwing more fuel on the inflation fire. I thought a while ago that we might see a temporary slowdown in inflation this fall, but at this market action, we may get another inflation spike. And if you really listened to Powell, you’ll know what he’ll do because he said it: the Fed “won’t hesitate” to do 100-basis points at a time.

I’m now going to do a whole podcast on this because this is really crazy.

“You and the markets are “fighting the Fed.” Good luck with that. The old rule is: Don’t fight the Fed.”

What’s funny is these people were making money hand over fist with that mantra, but now that the FED changed course they’ve suddenly switched their belief system to “fight the FED,” believing they’re going to continue making money hand over fist.

I have a question.

If you have a government job, or a government related job that is indexed to inflation, or a government pension indexed to inflation, or government healthcare indexed to inflation, would you be concerned about inflation?

Or would you just keep on spending like there is no tomorrow?

Wolf, you misread me, I have no position in the market, I won’t chase this. Period.

I think it’s insane what’s going on just as you and others do. However, we’ll agree to disagree about the message Powell gave at the meeting which is my only squabble here.

I sincerely hope they raise rates to 10% tomorrow and shut this gambling down…this country needs a good recession and I sure hope we get one this time around.

“And if you really listened to Powell, you’ll know what he’ll do because he said it: the Fed “won’t hesitate” to do 100-basis points at a time.”

Wolf, the point is that while he talks about doing 100bps when it comes to the crunch the Fed loses its nerves. That is why market is calling his bluff.

What stopped him from doing 100 bps on July 27th when Bostic actually put it on the table. Waller and ullard walked it back.

If you only talk and lose your nerves when it is time to act, obviously no one will believe you.

If the Fed really wants markets to believe it (and show them you are the boss) then it needs to do just 2 things

1. Raise more than expected – markets expect 75 bps, raise 100-125 bps.

2. Markets go up, raise rates in between meetings to show you mean business.

This needs nerves of steel, which has gone missing in the Fed for a long time. In fact nerves of jelly is more like it. Pandering to the markets is what it has been doing for the last decade. How does a servant convey to its master that it means business – by socking the master with one of the best. But then you need nerves of steel.

In short, the Fed will appear to be more bark than bit, a toothless tiger till it gathers its nerves and shows the markets it means business. Any of the 2 above will do, both will show the markets its place. Right now it is the Fed which is lying at markets’ feet and barking and the markets is asking it to clam up. This is what happens when you do not have a spine.

Wolf

Mr. Powell talking with forked tongue, giving the impression, that he is really ‘serious’ about containing inflation and the next moment ‘ we are closer to ‘neutral’ rate now’

Which part of his tongue I am supposed to believe in? Is he jawboning again? May be I am paranoid, right?

Powell’s recent press conference was the epitome of duplicity. Out of one side of his mouth Powell talks a big game about stopping inflation. Out of the other side of his mouth, Powell and the Fed are barely even selling the massive pile of MBS and Treasuries they added to the balance sheet.

The yield curve is inverted for a reason. Noone believes that the high interest rates will stay high. They believe the Fed will soon revert to QE. The Fed needs to be converted to a single mandate – price stability. The Fed should have zero responsibility for growing the economy or jobs.

“The yield curvr is inverted for a reason”

Indeed.The Fed owns circa 35% of all Treasuries 10 to 30 yrs

The Fed also owns 2.7 Trillion in mortgages that tend to be long term.

Off the market long term debt owned by the Fed

Imagine that debt “out there”!

The yield curve is “painted” by the Fed to what ever they want, and they want low long rates, admitted by former Fed gov Fisher to Force investors to take more risk

gametv

Exactly!

“A single mandate – price stability”

Yep, Absolutely!

Duh, now how do I, as a concerned citizen, vote for that?

Ccat

The correct way of thinking about this is that when 0% interest rates are “too high” like in Europe, and when the government owns more than half of it’s own debt, like Japan, its pretty clear what has to happen next. “Backed into a corner” would be a vast impovement vs where things are at now.

“We have seen widespread declines in the demand for gasoline, triggered by sky-high prices that caused people to change their driving habits, such as cutting out some trips…”

This is the upside to high fuel prices — peace and quiet because of the lack of tourists. I know, this is being selfish, but the area I live in normally gets crushed by a heavy influx of tourists in the summer. But not this year. It’s been GREAT!

You’ll be pleased to hear that’s just the beginning, as the wheels come off the economy & markets collapse you’ll see less tourists, try not celebrate though cuz they’ll be replaced by evictions, homelessness, abandoned buildings, unemployment, crime & poverty.

Not too mention a sharp drop in tax receipts.

“unemployment, crime & poverty.”

That describes some tourist spots every winter.

Those towns are in trouble if tourism is slowing right now.

I’m in Central FL. I Will gladly post signs to your tourist area if it means one less Mouse-Eared logo Prius around here. Talk about monopolies and corporate welfare babies… But then again, your area is probably real and not make believe fantasies for dorky adults.

The FL theme parks are absolutely crushing it. Record attendance, earnings… for all of them just about. It’s either 1927 or all of us have been played like chumps because there’s a lot of people who have no issues dropping hundreds and thousands to go stand in line in the burning sun for a 15-minute ride this summer. I don’t get it.

Agree

As you point out…

and try and book a warm weather winter vacation…

full

Not recession indicators

I do my part to support this booming economy.

I buy a big bottle of lemon-scented ammonia for $1.59. Then, I pour about 10¢ worth of it into a spray bottle and fill the rest with water. “All Purpose Cleaner”.

And, sure enough, the indices are green again today.

If I ever come to my senses, start economizing

and become known as “Spit Shine Halibut”, the party’s over.

Okay, guess you’re not living large on the fumes of your HELOC.

I guess those Inflation Relief Checks are keeping this boat afloat for one more month.

Here in California, we are still waiting for those!!!

The higher Mr. Powell goes with his interest rates, the dollar zooms and more instability gets spread around the world.

Money runs out of unstable places: China, Russia, Ukraine, Sri Lanka and many others.

Even with all the instability we have here, the rest of the world sees the US the place to send their saved, or ill-gotten money.

So, I suspect legal, as well as laundered, money that is endlessly flowing into the US & Canada is contributing to the real estate bubble as well as to the endless spending on durables.

Good for Mr. Powell. He’ll have an excuse to keep pursuing the Volker paradigm to try bringing his own created gene of inflation back into the bottle.

Higher Fed rates, money keeps flowing in. We could be in another endless cycle.

That also would mean endless dingy boat armadas of desperate folks trying to get into Europe and more waves of refugees at our borders with Mexico.

New world order!

With the rumblings of the BRICS trying to break the petrodollar and the SWIFT system by settling on their own system with their own currencies. Combined with the FEDs ability to extend credit at favorable rates to “allies”, do you think the FED regards the EM crisis as a feature or a bug?

Hey Wolf you are a glutton for punishment this week :) I admire your steadfastness.

What a glorious week to own assets especially crypto. Fraud and bankruptcy isn’t what it used to be. Thank you JP for doing what your paymasters have ordered you to do. To the bottom 80%, let them eat cake. Welcome to the Hunger Games bitches.

Yes I’m being snarky. I believe I have a right to be with all this bullshit.

Hard to be a rational person in a world run a muck with deviousness.

You are my favorite South Park character:)

You have the right to be snarky…Powell and co. aren’t even hiding it anymore…we’ll be at 36K in no time…I have no idea what to think … and I really pity the poor.

Why did Powell give the markets the message he just did if the result is the need to reign in inflation (if that’s truly the goal) even harder? that makes no sense.

The only thing that makes sense is “inflate everything” is the intended consequence…

Look. I detest Powell. I think he’s a limp-wristed bureaucrat who has absolutely no business being in the job he’s in.

That said, he did nothing of the sort. He didn’t give the markets the message you say he did. Actually read a transcript of what he said, not the idiot talking heads’ ridiculous interpretation of it.

FWIW I agree. I watched the entire presser and Q&A. Powell can’t control delusions, he can only stay the course. Eventually market delusions will crash into reality.

Peter,

Powell didn’t give the message. The markets, you included, fantasized about it and ran with a fantasy message. That’s delusional. You’re “fighting the Fed.” And the old rule is: Don’t fight the Fed.

The shorts have little to look forward to.

YOY inflation readings likely to decline

No Fed meeting in August

November election draws closer

Historicus, what’s your basis for saying YOY inflation readings are likely to decline? If anything, inflation has gotten more entrenched. I see no reason to think that’s true.

Einhal,

There is a mathematical reason: we had a huge spike in CPI last fall, and the “base effect” 12 months later will lower year-over-year CPI readings this fall, because the base last year was higher. We know this is coming to year-over-year readings. It won’t be a surprise. To get around it, we’ll look at month-to-month readings.

But this inflation has dished out lots of big surprises already, and I wouldn’t be surprised to be surprised again :-]

Wolf,

Understood, but there are a few things that could counter that. For example, wouldn’t rent, as calculated before it goes into the CPI, have a lag, due to the “owner’s equivalent rent” being based on owner’s subjective ideas about what it would rent for? If they hear that rents are crazy, that might influence their answers. And rent is a huge percentage of CPI.

Also, to the extent that last year’s “base” was when inflation was more based on goods, well now it’s in services.

I’m not saying it’s impossible, but I suspect some of the “inflation readings will decline” is wishful thinking.

Yes, correct, and that will play out. Each month rent factors are pushing straight up. But it still takes a while.

The rent factors are now at ca. 5.5%, and still below CPI and they’re still holding down CPI, but they’re going up by about 0.2 to 0.3 percentage points each month, so it takes them about 3-5 months to rise 1 full percentage point.

At this pace, they may be at 6.5% in October, which will likely still be below CPI, and they’ll be maybe at 7.5% in February and they’ll be at 8.5% next June, which is when they will apply serious upward pressure on CPI.

So this is starting to happen, but slowly, and have more effect late this year, and will come full bloom next year.

That’s one of the reasons why I thought we might have a dip this fall (on the base effect and some other factors) and then see another big increase in CPI next year, assuming that nothing crazy happens in the interim, such as a spike in crude oil to $200, which I doubt.

Tesla is up over 20% and gained 262 Billion in market cap this past month off the lows in July. Crazy. That equals the entire market cap of Toyota, which did go up but only 5% and about $15 billion. Ouch

Risk appears to be on right now. I am sure some short covering is also juicing the markets.

IMHO….in 2018, the FED said they were not even close to near normal. Since then they raised rates only 2.5% and now they say they are close to normal. It looks like wall street thinks 3% to 4% is the most they will raise rates. Does the FED still think we have transitory inflation?

Crazy but the 30 year mortgage rates are down to 5.1% and the 15 year to 4.25%. I am pretty sure JPow wants these rates to be higher.

Well if he wants those rates higher he could always do an emergency raise before September. I’ll bet you 1000 basis points he doesn’t.

Does this mean that people who baught a month or two ago are now refinancing? Can you do that?

I’m one of the ones contributing to this rise in consumer spending. It was not intentional, it was necessary. The cars broke down. I got sick. Our clothing needed to be replaced, as well as household items. Almost everything was more expensive this year than in previous years. Higher priced items tend to be reduced, while the necessary average stuff has increased in price. Sometimes the expensive stuff is the better buy.

Where did the money come from? We haven’t saved a cent this year.

Do you normally save yet had to spend those savings this year?

My college roommate and best friend of 40 years has the largest pool building business on the east coast of Florida, from the top of Miami to Stewart.

He cannot dig the holes fast enough and there is ZERO sign of slowing yet.

His average pool sale is now 6 figures.

He laughs, calls them the cash cow ponds.

I don’t know about the rest of the nation, but there is little sign of a slow down in Florida yet.

I do see price reductions on housing after listing happening now versus the insane increases after listing we were seeing before, but stuff is still selling at a good clip, and at ridiculous prices.

oh, and inventory is still way below anything that would even suggest recessionary collapse. Historically in Florida housing is very volatile. 30% declines in homes, 50% in condos is the norm in recessions.

I have a inground pool .chemicals have increased 150% price gouging to the max .As pool corp owns most of market and bought up a bunch of companies in parts businesses stock they control it.But not a monopoly my ass .Anyway my daughter wants to build a pool told her forget it money pit .Won’t listen can’t fix stupid. In Omaha

I also have an in ground pool. Tell her to call me. She might wanna hold the phone way back from her ear.

Yes I was thinking about letting my pool turn green and stock with fish – you know call it prepping.

Lol

TxRancher

My pool is already GREEN and it has it’s own ecosystem with frogs. And now, NO more mosquitoes. covered with tiny sliver of oil, long time ago

My family has an inground pool in florida. My grandparents blow tons of cash fixing leaks, repainting, etc… Every year more leaks.

Definitely a money pit.

“Literally,” as they say :-]

to your point – my wife and I have been traveling the past 6 weeks – seattle- vancouver- victoria- asheville nc – blue mountain beach fl – all we saw was a tsunami of money being spent – our rental agent in vancouver said the more expensive the rental the faster it books ! -americans stop spending when the casket cover comes down and the dirt is shoveled on

Ultimately, $4 trillion was printed, and most of it ended up in the hands of the top 10%. They’re spending like no tomorrow, and that’s causing most of the inflation, in my opinion

It’s as simple as that.

I moved from near the Hinsdale/Burr Ridge/Oak Brook IL area, including the gated communities where several high-profile tv newsreaders live. That is exactly what’s been going on the past 2 years. Lots o’ helicopter money landed on the right/connected high-end roofs there, especially those who knew how to game and milk the CARES Act handouts. FIRE + big healthcare/pharma.

I’ve noticed this. With inflation, you would think people would pay *more* attention to prices. But they apper to be doing the opposite, actively decoupling the connection between price and quaity, and just paying anything whether or not it makes the least bit of sense. Maybe they are cattoniclly numbed.

That’s why inflation is as much as a psychological phenomenon as a monetary one. And once it starts, it’s very hard to break.

Stuart, not Stewart. I used to live there.

The FED has given up…that’s the clear message…they’ve folded for the mid-terms…

No, but the market “is fighting the Fed.” Good luck with that.

Which Fed?

The Dovish one with Hawkish skin or NOT?

“Don’t fight the Fed” Wink, Wink! He is just ‘jaw boning’ as usual. just carry on I mean ‘RISK on’!

At least until inflation # come out in early August. If it is below 8, Party On -Inflation is responding. If 9 % or above, watch out!

As long as the Perception keep winning over reality, hard to trust this Fed!

Inflation has to work its way into the system as far as durable goods go. So the goods being bought now would have been built some 6 months back, assume. On top of that those who need to replace durables have either been stuck with machines that died suddenly or have been planning for a while. If latter, they have been trained to accept the price. If former, they’ll accept the price given the urgency. So the durable spending should not change because the buyers are willing to accept the price.

IMO, the drop will happen very suddenly with Home Depot types reporting stuff that target and Walmart have been reporting.

As an example, my car mechanic told me there will be no price hikes in parts until he starts seeing them.

There has been a sheer absence of any sane fiscal policy coming from DC in decades. Fed will do what it will do with its monetary policy, which it hs to because of inflation. 4 decades of tax cuts for wealthy & corporations have created massive inequality and a barbell economy. That inequality has come home to roost. The top 10% are living high on the hog and couldn’t care less. Almost everyone else can barely pay their bills and they’re thinking of building guillotines…

Here is what I don’t understand. If 58% of Americans are living paycheck to paycheck, where do all spending come from?

Wolf, I remembered you told me that lots of people still have money to spend. Yes, I complete get that. There were people who earn a lot from crypto and stock market in 2020 and 2021. However, the gain is fake unless people cash out the profit.

I also read your posts about American maxed out the credit card to the roof. They either have to pay back the bill, or bear high interest penalty.

If inflation is soaring to the roof, Americans should have reduced spending in goods or services (destruction in demand). However, based on your charts, it has not happened yet.

Why not?

“If 58% of Americans are living paycheck to paycheck,”

No not 58%.

The problem is that the question has been asked for decades but finance has changed. This question about having “savings” in a savings account to pay for an emergency is silly.

For example, someone has a $1 million home with $400k in equity, and has $500,000 in a 401k and has a bunch of Treasuries at TreasuryDirect.gov, and makes $250k a year, and all the extra cash goes into the 401k or the TreasuryDirect, and he is using a credit card to pay for all expenses but then pays off the credit card automatically every month…

He might not even have a savings account and might answer that he would use his credit card to pay for an emergency repair of $500. And if he does say that, then he’d be defined as living from paycheck-to-paycheck.

The whole question is silly. It needs to be redefined for modern personal finance.

True “paycheck-to-paycheck” means that you will default on your mortgage or rent 30 days after you lose your job. That should be the definition.

And there are quite a few people in this ballpark, but not nearly as many as these “pay-for-an-emergency-repair-from-savings” surveys say.

That’s totally batshit NUTS.

Lies, damned lies and statistics.

So are there reliable statistics to tell us how many people are living from paycheck to paycheck and getting deeper into debt with emergencies (like a fridge breaking down and needing to be replaced or a car repair?). Thanks

If you pay for an emergency repair with your credit card, then that’s not the definition of paycheck-to-paychek because everyone is doing that, even the wealthy. No one is writing checks anymore, and on the internet, you cannot even pay by check. The definition will have to be: If you lose your job, will you default on your rent or mortgage within 30 days?

8_mile_road,

Great questions. All the same ones I have been wondering about myself.

1) AMZN and AAPL gap up because consumers are doing great.

2) NDX monthly for entertainment only :

3) DM flip in Feb. June is DM #6.

4) Apr a setup bat, May a trigger.

5) in order to move up there must be a close > the trigger high, above

May high @13,556.67.

6) In order to cont down to Aug DM #7 there must close < Apr close @12,854.80.

7) In order to move down there must be a close < the trigger low,

under May low @11,492.29.

8) Good luck captain Ingham/Munger.

Amazon just reported 2 quarterly BACK TO BACK LOSSES OF MORE THAN $2 BILLION EACH yesterday.

Hooray! I hate Amazon and have been boycotting it for years.

Yes we need an M E tracker to see which of the M E predictions come true.

Kind of like the one used for Jim Cramer, right?

@Rancher: You’ll have to decipher his posts first.

“The Fed will win this fight with the markets. ”

I hope you are right, but I can’t help thinking that three months from now Powell will be saying the equivalent of “I was doing great until I smashed him in the knee with my balls.”

With bloodshot eyes and alcohol soaked brain, am looking at a FRED chart of the FFR superimposed on the YOY CPI going back to 1965 (spanning 8 recessions). In modern history, it appears that inflation has never been suppressed without the FFR eventually exceeding the YOY CPI. So a 2.5% FFR has quite a hill to climb, even if YOY CPI can be talked down to 5% in a year of so. Logical conclusion: a bloodbath is inevitable, only the timing is in question.

Yes. This is the nightmare you were looking at:

Clearly, the government went off script in 2008, worldwide.

“But then Bernanke saved the world”

If Greenspan should be shot for using interest rates as a tool to pander to the market, Bernanke should be shot for making money printing the defacto monetary policy. And has the gall to tell the world – it is easier to get approval than permission.

Yes, Greenspan’s ‘irrational exuberance’ was around 1996. Then he and his successors proceeded to fill the punch bowl with 200 Proof Everclear.

KPL

Spot on!

Couldn’t have said it better. Same feelings here!

I cringed to hear that Barnake is/was called a HERO,(Atlantic Monthly) at that time.

All with ‘easy-peasy’ money printed out of thin air!

2000 started catch me if you can folly that’s stilled being played today!

but bloodbath has already happened in crypto. where do you think it will happen next? housing? stocks? commodities?

As the Black Knight said, “Ha, It’s just a flesh wound!”

Automotive news is forecasting a 10.8% drop in unit volume in July vs. a year ago.

I had to have some work done on the technomobile and the sales people were hungry. I was upped countless times as I wandered around the building (I can’t sit still…). Looked at one car on the showroom floor and it had a $3,995 “rust and dust” side sticker. Window tint, mud flaps, ceramic coating, and a bunch of other low cost high profit add ons. A sales manager walked over to me and I simply said “It’s disappointing to see that you folks haven’t learned from your past mistakes. This nonsense will come back to bite you.”

There was a line of maybe 30 crossovers sitting outside that were “immediately available”. Maybe the winds of change are coming.

Nice Chinese bicycles have plummeted to $169.99 each with a great selection at Big 5 stores and are a very attractive and green alternative for

paycheck-collecting class Americans now!

“Nice Chinese bicycles?”

A 50 year old Schwinn Varsity or Continental disappears within 5 minutes if they are ever placed by the curb for garbage day. About a month or two later they show up at another handy neighbor’s continuous garage sale as good as new.

In its day, the Schwinn Paramount was a world class racing bike. In 1941, Alfred Letrourner, from France, set the mile record at almost 109 mph on a Paramount. (Huge gearing and drafting behind a wind-block while being timed)

Schwinn sold 1.2 million bikes in 1971 (“A 50 year old Schwinn Varsity …”)

But in 1981, Schwinn opened a new manufacturing plant in Greenville, Mississippi. That was their downfall. They then moved production to Giant in Taiwan. In 1983 they were $60 million in debt.

By 1986, 80% of production was done overseas by Giant. But, at the end of the 1980s, Schwinn cut off Giant and contracted with a company in China. That was a tragic mistake fueled by greed.

In 1992, Schwinn filed for bankruptcy, and was bought by Scott Sports in 1993. Eddie Schwinn torpedoed the company and got rich doing so.

May you Rest in Peace Mr. Ignaz Schwinn.

El Katz,

What brand or automaker was this? Can you disclose?

Take a look at the Big5 web site which is at Big5SportingGoods.com and you will find a wonderful selection. Two lines that are up now for $160 to $180 each are the Kent Shockwave 21 speed mountain bike and the Realm Men’s Transit City Bike. A friend recently bought a rather hideous and really crappy bike made by Cannondale and called a Topstone Alloy with mismatched blue pedals and paid over $1200 for that piece of junk which rode as recently as today to the beach.

Prefer not to as I do, on occasion, let out some things I shouldn’t speak of due to a NDA. Let it suffice to say that it is an Asian brand of high volume.

I don’t mean to pry, but why would you be signing an NDA when going into a car dealership?

Thanks. That helped. I was thinking of a specific brand that I know has quite a bit of inventory now, but it’s not an Asian brand.

We were in Long Beach earlier today and got off the 110 at the Vincent Thomas Bridge in San Pedro and the Port of Los Angeles is now overflowing everywhere including on the ships that docked with contained stacked 10 high as well as the containers all over the roads all the way from San Pedro and the Port of Los Angeles all the way through the Port of Long Beach and all the way down to nearly Ocean Boulevard in Long Beach.

The ports of LA and Long Beach “overflowing” with containers, and ships backed up into the Pacific forever waiting to dock has been one of the biggest supply chain problems for the past two years. Reported here as well. Have you been asleep for two years?

Kent Belmar 7-Speed Cruiser $169.00 (save $30) in store only. Sale ends tomorrow 7/30/22.