As the condo market is going south on you, you can always try to sell the tower to an investor to convert to rental apartments. But that’s tough too.

By Wolf Richter for WOLF STREET.

“Z&L continues to be interested in being part of the solution to the housing shortage in San Francisco and has been surprised to see such a soft market now,” Darlene Chiu, a business consultant who has worked with Chinese firms investing in San Francisco, told the San Francisco Chronicle.

It’s kind of funny actually, to put “housing shortage” into the same sentence with “such a soft market,” given that there over 40,000 vacant housing units in San Francisco, which has caused such an uproar that folks are now trying to put a vacant-home tax on the ballot. Add to these vacant housing units the completed but vacant and boarded-up 109-unit condo tower, The Oak, that Z&L Properties built.

Z&L Properties is a US entity of Chinese property developer Zhang Li, co-founder of R&F Properties in Guangzhou, China, which is now trying to restructure its debts and is negotiating with bondholders of its foreign-currency bonds. If these negotiations are successful for R&F, Fitch will consider this a “distressed debt exchange” and downgrade R&F to “restricted default.”

The tentacles of China’s collapsing property developers stretch deep into the US commercial and residential real estate market, particularly the trophy markets in San Francisco, Los Angeles, and Manhattan.

Unpaid subcontractors have filed mechanics liens on The Oak; and Z&L owes $2.05 million in unpaid taxes on the Oak, according to the San Francisco Chronicle.

Only 17 potential buyers have put down deposits for a condo at the Oak, and three of them cancelled. The remaining 14 might never get their condos.

The pace of absorption has been much slower than anticipated, Darlene Chiu told the Chronicle. Despite the “housing shortage” you mentioned, right? If I hear “housing shortage” one more time from the real estate industry, I’m going to scream.

The potential buyers got mortgage rate locks back when mortgage rates were in the 3% range. But those rate locks have expired, and now they’d have to get mortgages at current rates, at over 5%. The units are still listed for sale between $625,000 and $1.8 million. So a mortgage payment, when the rate jumps by 2 percentage points, would get very tough, if it ever gets that far.

Rather than continue with condo sales, Z&L has retained the brokerage Kidder Matthews to sell the entire property to a rental housing investor, sources told the Chronicle.

And converting the building to rentals would make sense if you can’t sell the condos because the condo market went south on you.

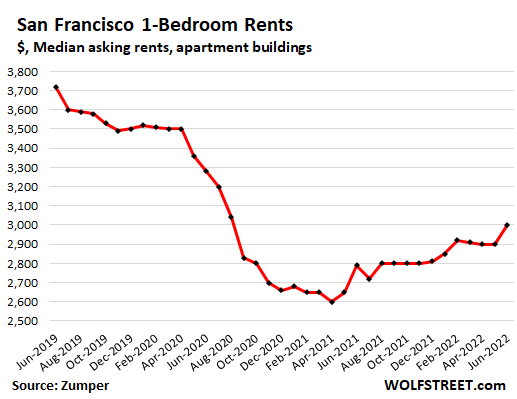

It’s just that rents in San Francisco aren’t so hot at the moment either, with the one-bedroom asking rent still down about 20% from the peak in 2019 due to the “housing shortage,” or whatever, as San Francisco has lost about 6% of its population since then:

The property development industry in China, tripped up by ridiculous speculation and leverage, has been in slow-motion government-controlled collapse. China’s Evergrande was the first big developer to shake up bondholders of foreign-currency bonds last year, and by now foreign bondholders have taken massive losses on their bets on China’s property developers.

And so, we here in the US are stuck with mega-projects that were in various stages of construction where lenders seized the collateral, or where projects ran into other difficulties, amid unpaid bills owed to contractors and subcontractors, mechanics liens filed on the properties, and unpaid property taxes.

Z&L acquired 12 projects in the Bay Area and Los Angeles in 2014 and 2015, during the peak of the China property mania, and was planning to build 3,400 high-end condos. Four of those properties are in San Francisco, including The Oak.

Z&L acquired the two parcels and plans for The Oak from Trumark for $23 million. Trumark had gotten the project approved by the City. In 2019, Z&L obtained $77 million in financing to build the tower.

There have been all kinds of issues with Z&L projects. For example:

The US Department of Labor investigated Z&L’s Silvery Towers project in San Jose for human trafficking and found that, under a contractor, workers were “forced to work without pay” and “lived in captivity in squalid conditions in a warehouse.” The case was settled in 2018. In 2019, a jury convicted the contractor to eight years in prison and to pay the workers back-wages of nearly $1 million. Years behind schedule, the units started selling in 2022.

The City of San Jose removed Z&L from two stalled projects in 2019 because it had broken the terms of its development agreement.

Z&L executive and R&F co-founder Zhang Li was tangled up in the corruption indictment of San Francisco’s former public works director Mohammed Nuru, who’d been investigated by the FBI and was convicted in 2020 on public corruption charges. According to the Chronicle: “The indictment states that Nuru had met Li in China on multiple occasions and that the Chinese developer had showered him with gifts and put him up for free at five-star hotels. In exchange, Nuru ‘used his official influence with other City officials to solve problems’ the developer encountered.”

San Francisco already has the giant Oceanwide eyesore.

The Oceanwide Center, which had an original budget of $1.6 billion, has been seized by creditors after construction was halted when it reached grade, years behind schedule. The mega project by developer China Oceanwide Holdings in Beijing is now a huge eyesore in the middle of San Francisco right by the Salesforce Tower. This is a portion of the project, seen from street level (photo by Wolf Richter, May 24, 2021):

Oceanwide’s huge project in Los Angeles, the Oceanwide Plaza, which is nearly complete, has been financially troubled but still hasn’t been seized by creditors. But Oceanwide’s Manhattan project has been seized by creditors. There are other projects in major US cities by property developers based in China that are now tangled up in the meltdown of property development in China that has been bleeding into the US real estate market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“If I hear “housing shortage” one more time from the real estate industry, I’m going to scream.”

Or from the

Homeless Housing Industrial Complex?

It’s more “shortage of housing that a buyer earning the median income for that area can afford.” The problem with building nothing but high-end luxury housing targeting the upper 10% of earners is that there aren’t that many people who can afford those properties.

But a rich person can buy 2 or more, no?

This is what rich people are doing. Have a friend in san diego, he owns 3 homes and still looking for 4th one. The greed has no end :-). Ofc, he believes real estate in san diego can never go down, come what may. For the last 12 years he has been proven right and smart.

Jon, people said same thing about SD during previous bubble, but it still collapsed, and it was a much nicer place to live back then IMO (I’ve lived in SD for a long time). Your friend’s behavior is a defining characteristic of a bubble.

Not necessarily SocalJohn. Those who held on during the last SD “collapse” have done very well and continue to do so. You know that. My SF property went down 15 percent during that “collapse” but has since gone up 240%. Not that conditions today are the same but I will take that kind of “collapse” any day. And have.

Alternator, I didn’t say that prices haven’t gone crazy as you have observed. I’m not even sure what point you are trying to make, though the price variations you cite are truly indicative of bubble behavior, so thanks for that.

One other thing. The decline here in SD during the previous collapse was much larger than 15%. Your post implies you are in SF… I don’t know how big the decline was up there.

@Alternator – on another note

There are stories about houses selling 30% to 50% from peak prices after the HB1 bubble popped but to get that type of deal, you pretty much had to be connected with a bank or you had to be one of the big Wall Street firms that were allowed to buy $10, 20 or 50 million dollars worth of bundled foreclosed mortgages from the GSEs.

I know of some houses near my rental house, after the fact, sold fold for 40% to 50% less than my rental house value but they never hit the MLS. The best I find on the MSL was about about 15% to 20% off. It was not worth it.

As a matter of fact, a foreclosed house just a few doors down from where I live sold for 25% less than peak value after HB1 popped. More than 1 neighbor approached the bank about buying the house. The bank kept turning everyone down. Next thing we know the house was sold to the son of the relator the banks chose to sell the house. It never hit the MSL or if it did it sold within minutes after it hitting the MSL. He bought it for pretty much what other were offering to the bank prior to giving assigning the house to the relator.

SocalJohn, the point I am trying to make is actually two points. Neither is the person with three houses looking for fourth a defining characteristic of a bubble, not is the downturn you refer to a collapse by any definition other than the most narrowest of minds and windows.

These two downturn situations are VERY different in nature and might have a similar short term outcome but most definitely will have the same long term outcome. Thoughtful real estate investors do very well when they buy on solid fundamentals in well chosen areas and time, and have the long term view. I have 19 properties across CA and they are all (except for two) long term rentals at fair market rental prices. Jon calls it greed but it’s actually a lot of hard work that provides roofs to people of various economic profiles. And a personal choice of how I earn a living.

I’d much rather hear and learn from your own stories – yours and ru82’s – than from what some guy or some other son of realtor in some unknown location did or did not do. That’s not helpful, specially on a macro level. That’s my point or a few. :-)

Alt, I was referring to the belief that prices can never come down as being a defining characteristic of a bubble. At any rate, good luck to you.

Had two rental homes in San Diego i sold both

I am just keeping my primary home.

I don’t know which way the market would go but things look very dicey.

I get multiple emails from Redfin about price reductions now a days.

Liquidated all my bitcoin at 55K

Bough them at 30k.

Still have some stock positions some long some short

Most of my friends are like Abernathy. They think San Diego is special and this time is different. SO no big crash in San Diego 😀.

Quality of life in California is not the same when I first came in 2000.

A lot of sfr is hosting multiple families and generations.

This is not the America I knew.

All good points.

Jon, I’ve been in CA since 1990 and see the same re quality of life across the state, and especially SF and SD. But I think the same can be said for many other places around the US, at least I tell myself that. 😊

Alternator said: ” Jon calls it greed but it’s actually a lot of hard work that provides roofs to people of various economic profiles.”

———————————

How would those people ever find a roof without you providing it for them? Does your “provision” of this roof add anything to their cost of obtaining a roof?

The Apartment Owners Association calls landlords “housing providers.” I have not heard them refer to tenants as money providers.

Why the companies run the numbers and see how many 10%’s there are who want to live in San Francisco and build accordingly?

IF and I mean IF AND ONLY IF Jerry continues end QE and start QT today(as planned) and continues til end 2023

THEN AND ONLY THEN will we see more PROPERLY PRICED debt to equity conversions(say 20-40% of debt value)

we call it destruction of debt and conversion to equity

then I might even consider some IN OUR CITY

Because, when you “develop” a project targeted at the “high end” the costs are almost by definition going to be greater.

The more/higher building costs involved, the more opportunity there is to illegally inflate them and skim the extra.

The core lenders try to police this to a certain degree (it is mostly their money) but lenders don’t run construction pjts day in and day out – they periodically inspect/audit them.

Purpose built “homeless” drug/alcohol/mentally ill demographics is very expensive. There are always $60,000 tents if you want to save money.

Synagogues and churches, which are tax exempt organizations should be the ones to build “homeless” housing, not the public or public/tax subsidies.

“Proposition HHH, a bond program approved by Los Angeles city voters in 2016 to build 10,000 housing units for people experiencing homelessness, cost an average of nearly $600,000 per unit last year, up from $530,000 in 2020, according to a report released Wednesday by Los Angeles City Controller Ron Galperin.”

Opps, hit send too early.

A low-income housing complex being rehabbed at 2206 Great Highway in San Francisco.

(L.A. Times)

June 20, 2022

More than half a dozen affordable housing projects in California are costing more than $1 million per apartment to build, a record-breaking sum that makes it harder to house the growing numbers of low-income Californians who need help paying rent, a Times review of state data found.

Or we could just legalize SROs and motels letting their guests stay as long as both parties consent to. This and generally ending all development restrictions would pretty much end homelessness.

“Low income” rent can be taxed, and is taxed in California.

It’s called the TOT = Transient Occupancy Tax

It applies to Motels – SROs – Extended Stays – RV parks

Municipalities and Counties across California collect TOT. In touristy areas it is a serious source of income. It is up to and in some cases more than 10% of the rent.

State Law **prohibits the collection of this tax on stays exceeding 30 days.** Municipalities hate this state prohibition, hide behind “charter exemptions,” and squeeze lodging owners for payment, because the municipalities and counties “want the money.” Some lodging operations keep municipalities “happy” by essentially illegal workarounds that allow renters to stay longer than 30 days, but renters are “theoretically moved out and then back in every 30 days” so that local governments can continue to collect the TOT.

Onerous credit checks, steep deposits, pet restrictions, background checks, irregular hourly income, occupancy caps, etc. etc. These are the reasons that folks living at “the bottom,” a growing demographic, struggle to put a roof over their heads.

SROs, extended stays, etc. are often the only option available. And because of the TOT, many folks have to pay a 10%+ “premium,” and move every 29 days for the privilege. [Sometimes it just involves moving to another room next door. Sometimes the move is “theoretical.”]

In this small Northern California community, we have literally hundreds of folks — seniors, vets, families with kids — living in the woods, living in cars and RVs, camped on highway rights of way, struggling to make it through the winter. The County pulled it together to renovate a motel, and, naysayers notwithstanding, the project has gotten small numbers of vulnerable folks off the streets.

For one sitting at the kitchen table in one’s own heated (or air conditioned) house, munching on a danish and drinking hot coffee, the “housing shortage” seems abstract, distant, and ethereal. For the mother who, right now, is struggling to get her kids dressed in the back seat of the car so they can get to school, it is very real.

There is a housing shortage. No doubt about it. Whether one wants to “look at it” or “think about it” has nothing to do with whether it is real or not.

Scores of $1.5 million condos in SF or LA or SD are not going to solve the problem. It doesn’t need to cost $1/unit to house folks either; that is corruption at many levels.

Neoliberalism is in total collapse. For those with ears to hear and senses to feel, it is obvious that the rotting piers holding up the entire system are groaning eerily as they bend and then snap under out very feet. Families living in cars is but a symptom.

The failure of Communism is production,

The failure of Capitalism is distribution….

There is no housing shortage in the Bay area. Just alot of people that can’t grasp that property values must collapse!

I wonder how China will deal with an insolvency crisis. Seems like the government (the people) will be absorbing losses of the private sector, based on what I’ve seen so far.

Is there a country on this earth that values fairness and allows debtors to fail?

“I wonder how China will deal with an insolvency crisis.”

The traditional method is to paper it over with debt and kick the can down the road.

“Is there a country on this earth that values fairness and allows debtors to fail?”

Not if they’re politically connected. Those who aren’t just get swept under the rug. Annual US personal bankruptcy filings in calendar year 2021 totaled 413,616, compared with 544,463 cases in 2020.

If you need more, just ask.

It is difficult to know when not being there and understanding mandarin. Still, there are signs that government absorb losses for individual buyers and subcontractors. Larger investors, or at least foreign investors are not bailed out.

Well they called out tanks for that one bank that became insolvent recently.

Not that I can think of. Rent & mortgage relief was the only reason our housing didn’t go belly up in 2020. I guess there are pros & cons.

What would be the con of housing going belly up?

“If I hear “housing shortage” one more time from the real estate industry, I’m going to scream.”

Wolf, man, you better order a case of throat lozenges stat.

Better scream than throw up…otherwise Wolf would be like a regular bulimic from hearing housing shortage from MSM and other housing bulls until end of this year or early next year.

Wonder what other kind of phony narrative they haven’t thought of once the markjet get even worse. Already tried the millennial is the next tour de force in demand to housing is the absolute best at being inflation hedge. I need something more creative from them, at least then when I scream or throw up from listening to it, it will give me that slight amusement. How about Alien is taking over and they are going to be our next corporate landlord..

Inflation may help the developers who overbuilt expensive housing show a paper profit (or at least cover more of their losses…) Inflation could have helped keep more people in their houses during the Great Recession, or at least kept their homes above water.

Millennial niece who is a nurse has no interest in a home,pays parents 400$ a month rent works one day a week ,going to be a traveling nurse. So she can continue to travel ,internationally. Seems like a good time to me

RepubAnaon – Inflation probably would not have helped much. Most of the subprime loans were going to fail. A lot of predatory lending back then. Teaser rates that would last 2 or 3 years and then reset much higher than the actual market rate.

There was no way out for many of those borrowers. Geeze, many did cash out financing to go on a vacation or buy cars etc. That was being pushed by the lenders a lot too.

ru82 said – ” Most of the subprime loans were going to fail. A lot of predatory lending back then.”

————————————

How much lending isn’t predatory?

Inside info

Real estate is worst than you think

A lot of evictions from people who did not pay their rent during COVID is being hidden

Just like Banks are hiding a lot of properties that are being foreclosed due to non payments during the covid mandate

Yes. A friend who lives in Port Saint Lucie, FL (PSL) told me last week that he had met an attorney who specializes in foreclosures. A bank had called him last week and asked if he was fully staffed. He replied that he was and asked why the question? The bank person told him that starting in August, they would be sending him 250 to 300 foreclosure documents each week.

During the subprime heyday, PSL was the fastest growing city in the USA. During the bust it was the foreclosure capital of the USA.

Sometimes I wonder if this housing bubble is worse than the previous one. Some may laugh and say “of course it is”, or “no, there’s no bubble”. Whatever the case may be, there is obviously something out of whack. Somebody just reported a record number of people backing out of purchase agreements. I think it was redfin. If there is a big turn in the herd psychology, we could see some serious fireworks. After the previous bubble popped the Fed provided tons of support, which limited the price decline. What if they can’t do that this time? I can certainly understand why people are canceling purchases.

“Housing shortage” is politician-speak for here comes a politically auctioned subsidy…

Rule #1. Foreigners are at the back of the line.

That rule has been in force for a long time 2banana. In China.

Rising EU and US interest interest rates will deprive China of FDI, little by little. Soon, China will be kaput.

MW: Big Tech earnings are about to determine the direction of the market

Google may be the safest of the digital-advertising giants, but that isn’t saying much right now

Facebook enters a storm of uncertainty, and the wrong kind of ‘firsts’ are showing up

Ad expenses are the first to be cut. If advertisers cut ad expense on snap and twitter, why would they keep it on for FB and Goog ? Just wondering.

How can anyone do an honest audit on Internet companies who tell you what their numbers are.

“I’ve got $100 billion of Widgets in Inventory. Trust me.”

That’s ok, we can make it up on volume

Do a search for “the great salad oil swindle of 1963” – nothing ever changes.

Snap and Twitter are peripheral and the first to be cut when things head south. FB & G are core to most long term enterprise customer acquisition and retention programs.

Good, now we just need all the Chinese money that bought and parked their money in residential single home markets in SoCal and NorCal to take their money out and run home to put out whatever fire they have going on back in mainland. Apparently that urgency is not quite there yet since there are still plenty of parked money in Arcadia, San Marino, Irvine, time will tell if this trend will change in an accelerated pace hopefully.

It’s frustrating to see these people parked their money in RE in certain market for so long, driving up home prices and pricing out locals way before this pandemic parabolic run up.

Nice opportunity for victim’s of Chinese human rights abuses to sue in federal courts and get lien rights on these properties after the local banks get their cut.

Only American citizens should be allowed to own housing. That would solve our homeless crisis, lower rents and home prices nationwide and build more stable communities.

Your legal theory is really strange. Why would a (supposed) victim of human’s rights abuses successfully sue a private Chinese development company.

It’s ridiculous.

What’s at least equally ridiculous is the widespread US belief that US law or “international law” (whatever the US led “international community” makes up) applies in a third country, whether China or anywhere else.

Whatever happens in China involving a non-US citizen isn’t the business of any American.

“Only American citizens should be allowed to own housing. That would solve our homeless crisis, lower rents and home prices nationwide and build more stable communities.”

1) No it wouldn’t. This is a supply issue in its entirety.

2) Your idea is fascism and profoundly unAmerican. Housing is not a right, buying housing is a transaction between consenting parties that no third party has the right to infringe on.

Very confusing objection. I think that the OP was suggesting that supply would be increased if all the foreign owned properties had to be sold, which is actually consistent with your contention that we have a supply problem. I’m not taking sides with anything here, but I am confused by the logic.

Fascist, UnAmerican? Seriously? Foreign buyers often mess up the real estate economies in cities. It would certainly have some impact on lowering home prices and would definitely build more stable communities of home owners who actually live in their homes.

@ Cytotoxic –

Why would a Nation subject it’s citizens to compete with non citizens for housing within the nations borders?

The system you defend is globalist and un American. And fascist on a globalist scale?

“If I hear ‘housing shortage’ one more time…”

I was never able to come to a logical conclusion as to how we could have a shortage. Just a decade ago, we had the biggest housing glut in history. We had overbuilt aggressively, and prices had collapsed. It’s not like the population suddenly exploded in the last 10-12 years. Sure the millennials are coming of age and forming families, but we’re largely forming smaller families, and our boomer parents are downsizing or exiting the market entirely as they walk toward the light. We never had a housing shortage, we just had a listing shortage.

“But those rate locks have expired”

This one confuses me as well. I want to be ready for whatever it is that happens with the housing market. Knowledge and preparedness are key, so I got on the phone with a loan agent for the biggest bank in the U.S. and asked him to explain rate locks to me. I was told that I could be pre-approved, but that the quoted interest rate on the pre-approval letter is nearly meaningless and that the rate-lock only occurs once a house is under contract. I talked to another loan agent with a smaller regional bank in an area that I’m keeping an eye on. Same answer. She said that Fannie and Freddie are effectively the only underwriters of conventional loans out there. She could offer personalized customer service and familiarity with the local market, but there isn’t much difference from one originator to the next. The underwriting standards are going to be the same, and you would get your rate locked in at the time that your offer has been accepted and the closing process begins. So who is allowing borrowers to lock in first and THEN put an offer on a house later shopping around for a few months? Is is the non-bank lenders? All this talk about rate locks here on Wolfstreet is not matching what I’m seeing in the real world. If a rate lock doesn’t happen until a house is under contract, then it really doesn’t matter what mortgage rates were when the loan was applied for and pre-approved, right?

No, a rate lock is not “nearly meaningless” …

You apply for a mortgage BEFORE you buy a home, so you CAN buy a home with it. You will get pre-approved for the mortgage, and there will be a rate, and the rate will be good for a set period of time such as three months (the rate lock), during which you CAN buy the home.

However, there are still some conditions to be met, and a mortgage isn’t a mortgage until it is signed by both parties and until the deal closes.

Rate locks are super-common, they’re standard operating procedures, and they hold up unless one of the conditions isn’t met.

No Sir. Those are not the terms that major lenders are offering. I am talking about 20% down on a conventional 30-year fixed rate mortgage from a bank for a borrower with excellent credit. I have now had multiple lenders, big and small, tell me that your description is not how it works. There is a quoted interest rate on my pre-approval letter, but it is subject to change. No lock-in occurs until a house goes under contract. A buyer doesn’t get to just shop around on a lower rate from a couple months ago.

Here’s the actual text in the pre-approval (not a lesser pre-qualifaction) letter from a giant lender:

“Program terms, conditions, interest rates, and points reflect today’s market and are subject to change without notice.

Contact your Home Lending Advisor for up to date rates, terms and conditions.”

It doesn’t seem possible that multiple lending agents from competing lenders of varying sizes have managed to ALL give me the same exact wrong description of pre-approval terms, and the biggest one gave me the wrong terms in writing.

To be clear, I don’t know what the non-bank fly-by-night lenders are doing (Rocket Mortgage, etc.). Also don’t know what the terms may have been in the past. But if a buyer is looking for a conventional loan underwritten by Fannie/Freddie today, then a rate-lock does not occur at the time of pre-approval.

I refinanced last year and it was as Wolf described.

No one would refinance if you were unable lock in a rate.

Using a preferred lender is different. The pre-approved letter doesn’t guarantee the rate until you go into contract. However, when using a preferred lender of a home developer, they lock in the rate until the house is built and ready to go into contract. Everyone is right.

Not Sure

You’ve made this claim about “no such thing as an interest rate lock” on several different posts here, and it’s wrong.

My wife and I were heavily searching for a house earlier this year and got pre-approved through a nationwide mortgage company. We got a 90-day lock on our interest rate without having to have a house under contract. We then went out and found a house we liked, put an offer on it, had it accepted, then realized it’s a terrible time to buy and backed out during the option period (thanks Wolf, for the data on why it’s a bad time).

During that time we wanted a comparison of mortgage interest rates and fees, so we contacted another mortgage company that was more local, and they didn’t have the ability to lock in for 90 days.

So Wolf being right and you being right don’t have to be mutually exclusive. Some companies offer a 90 day lock, others don’t.

You’re talking about two different things. Wolf is talking about a true rate lock, which is a product that is effectively an interest rate swap. In other words, you’re paying the lender to agree to cap the rate if you close before the rate lock expires. Sometimes the lender won’t actually break out the fee, and it’s just rolled into the rate you pay or the “points” they charge, but you’re paying for it one way or the other.

You’re talking about an informal “pre-approval,” which is not a contract. What that is is effectively the lender telling you “Based on our preliminary investigation of your income and credit worthiness, we will lend you $480,000 to buy a house assuming you put $120,000 down and the house appraises at $600,000 or more. Further, based on today’s interest rate, you’ll pay 5% if you get a 30 year fixed. All of this is subject to change based on further diligence and changes in market conditions.”

A pre-approval letter doesn’t bind the lender to do anything. It’s purely a tool to give you an idea about what you can afford and to let the seller’s real estate agent know you have at least pre-qualified.

On the other hand, a rate lock is a binding contract, and the lender won’t give you that until after it’s done its full investigation and deems you worthy of credit.

Apple:

But on a refinance, the property is a known commodity so it’s easy to lock in the rate.

The last time I needed a mortgage to buy a house, I did have a 90 day lock prior to purchase. I guess life changes over twenty years.

Apple: refinance application is a contract. That’s when the rate is locked. Refinance is a different animal.

Apple,

Refinancing is a different beast. Wolf’s article is talking about new mortgages for potential buyers, and so am I.

A rate lock on a pre-approval as described by Wolf suggests that a potential buyer would lock into a rate and then have some time period to look for a property to buy and then get a mortgage at the earlier locked-in rate. With a little research, it appears that Rocket Mortgage and other non-bank lenders do offer such a 90-day product, but they get theirs one way or another… In Rocket’s case you can get their “Rate Shield” product and they cook the risk into your final interest rate.

But if you’re a potential buyer today looking for a similar type of 90-day rate lock from a legitimate bank on a straightforward, traditional, conventional loan… Good luck. They’ll give you a shorter rate lock to cover the closing period once you’ve signed a purchase agreement, but that’s about it.

Not sure,

Don’t extrapolate from your mortgage to others. You may be right about your own mortgage — whatever mortgage and mortgage lender you may have. You’re wrong about it in general.

For s&g, I dug up my old pre approval letters with a local bank (3.5%, how nice) and checked the terms.

No rate lock on the local bank until after the mortgage application submitted, but I never got to the point of submitting the app due to the well-discussed nightmare of house shopping. Didn’t want to have to keep submitting apps and having my credit pulled every few months knowing full well I wasn’t gonna find anything in my range, when the prequal letter was good for 4-6 months and the rate lock was only good for 2-3 months. This was on the advisement of my mortgage lady–don’t bother submitting the app/dinging my credit again until a contract was accepted and the inspection was clean.

Rocket lost my business at the very start of my house hunt. For the prequalification letter, the mortgage agent–and I use the term generously–asked me how much I wanted him to put on the letter before I ever informed them of my finances. Basically just asked me how much I wanted to spend without any debt/income numbers provided. I explained that’s not how it works and I want a pre-approval letter, so he insisted a pre-qual and pre-approval are the same thing.

I asked to speak to the manager (such a Karen) who took my paystubs and application. He ran my credit *then* decided to tell me a Rocket pre-approval letter requires paying a $500 fee, or $1,000 fee if I wanted their 60-day rate lock product. I directed him to shove the pre-approvel letter up his nearest orifice of convenience, and walked away with the ding on my credit.

Short story long: Wolf and Not Sure are both saying correct things based on my experiences, but talking about different conditions.

Rate locks and other terms of mortgages for housing, similar to commercial, is subject to variation by lender and by location, even locations within the same state.

Similar to many biz practices that are still in the systems of the states, eh?

Seems like they, the banksters they, continue to add all kinds of small and smaller print every time we buy or sell some RE, so maybe time to just sit still till bucket kick time.

Probably not with the opportunities that appear to be coming to a home or biz near you!!!

You want plentiful affordable housing? Just go back to when they system worked.

1. 20% down payment

2. Get government completely out of the mortgage business

3. Banks eat their bad loans

4. Enforce fraud and GAAP laws

.

.

.

How dare you. You can’t buy votes that way.

But that was not the way it was.

Up until the 1930’s, house loans were interest only with ballon payments due after 5 years. 80% down payments were not uncommon.

If the bank went under, your loan was immediately due.

Why stop at pre-1930s? Let’s go to when you saved enough to buy a house outright or you accumulated enough materials to build it yourself.

What about after 1930 and before 1980? That was certainly what my parents had to do – and it seemed to work well for the middle and working classes.

This list does not address the main issue, which is zoning and other obstacles to development ie parking requirements, NIMBYs, and other insanity. Minneapolis is creeping in the right direction.

There was no ‘glut of housing’ in 2008. The “bubble” was a result of insufficient construction, and was not as big as people think it was. There’s more and more people calling out the conventional narrative of the 2008 crisis.

https://www.bloomberg.com/opinion/articles/2022-01-10/there-was-no-housing-bubble-in-2008-and-there-isn-t-one-now

Another opinion piece on Bloomberg that makes you want to not ever go back to Bloomberg again.

“Some smart economists are challenging the conventional wisdom that the Great Recession was triggered by out-of-control home prices.”

Good thing the author clarified that those economists are smart ones. Whew, otherwise I might not have believed it.

Jesus, Bloomberg should host a masterclass on Gaslighting, it’s bad enough if they sit there an argue we’re not in a bubble now but to tell us we didn’t have one in 2008….Obi Wan they are, Bloomberg mindtrick isn’t working.

The housing “shortage” came about mostly because after Implosion 1.0 new SFH construction fell maybe 65 pct and very, very slowly crawled out of that impact crater over the next 10 years.

Even with collapsing population growth, new builds from 2010 to 2015 or so we’re so low that the industry is still trying to catch up.

And greed focused supply efforts on ZIRP enabled McMansions (for McMorons) rather than affordable apts.

And ZIRP encouraged (again) rampant flipper speculation.

And Covid cut homes for sale by half…while ZIRP kept said speculation intact (key to 2021’s truly, truly stupid boom).

There is some guy whose name I’ll probably mess up… Charles Hugh Smith, I think… who claims that housing units have grown faster than the population in recent years, and that the units per capita is as high as it was during the previous bubble peak, when we were supposedly oversupplied. His data is from a source called Econimica. Is this all wrong? I’m not taking sides here. I really don’t know what is correct, but I’d like to know.

This is correct, in fact the units per capita is actually higher than we were before the HB1 burst. This is why the housing shortage narrative as a long term trend is giant dose of cow dung

PI, thanks. Seems like this is consistent with Wolf’s prediction that the supply of listings can grow significantly, which is occurring in many places.

Vacancy tax NOW!

You don’t need one in a normal housing market.

When holding costs are much greater than any sweet appreciation.

And a tax to “solve” the insanity of loose and cheap/easy monetary policy never work anyways.

‘And a tax to “solve” the insanity of loose and cheap/easy monetary policy never work anyways.’

Excess fiat needs to be destroyed. The only way to do that is by taxing the rich. It’s also the only way to get the federal deficit under control. And so forth.

It’s also way you’re going to be able control inflation, under the circumstances. And since the rich are going to fight that tooth and nail, you’re going to be stuck with a severe recession and high inflation until the coming plutocracy fails and the US devolves into the Mad Max scenario. All very predictable.

Have fun with that.

“The only way to do that is by taxing the rich.”

LOL no. The money will just be spent on nonsense. The only way to reduce fiat is tighter monetary policy.

“Excess fiat needs to be destroyed”

You are probably correct…

But how will DC’s next lie be swallowed, if the current one (printed fiat) is welshed on?

See, that is the primary problem with running government on the principle of fraud…you have to keep propping up a legacy of lies or DC burns.

Taxing the rich is the only way to get the deficit under control? LOL!

How about reducing spending? SMH

‘The US Department of Labor investigated Z&L’s Silvery Towers project in San Jose for human trafficking and found that, under a contractor, workers were “forced to work without pay” and “lived in captivity in squalid conditions in a warehouse.”’

I bet nobody from Z&L will be going to prison, and I bet nobody from Toyota will go to prison for child labor in Alabama either. Excuses will be made to allow all such firms to continue doing business and let them figure out how to get away with it in the future. In the next few years these practices will be legalized.

The US has become that sort of country.

‘It’s kind of funny actually, to put “housing shortage” into the same sentence with “such a soft market,” given that there over 40,000 vacant housing units in San Francisco, which has caused such an uproar that folks are now trying to put a vacant-home tax on the ballot.’

The most recent US census indicates that more than 16 million homes are sitting vacant across the U.S., 10.6% of all homes. This tells you there is no ‘housing shortage’. It tells you the US residential real estate market has been systematically rigged by financial predators to cause prices to skyrocket for fun and profit.

Things aren’t going to get better because the Plundering Class is expected to take over next year and pull out all the stops until the whole thing falls apart. It’s going to be ugly. After that, it gets weird ugly.

It’ll get weirder. They’ll need to figure out how to stick it only to the blue states. SALT was a strong start, but they can do so much better.

“stick it only to the blue states”

How dare you expect me to pay the full tax costs of living in a worker’s mail-in ballot paradise.

I need muh subsidies from the Federal government! Just like big oil and big solar.

Rather than enact tax laws that penalize people who live in a state that you or I don’t like for some reason, let’s get Congress to end all deductions for mortgage interest, property taxes, and sales taxes and eliminate the $500,000 exclusion of taxable gain on the sale of a house.

“Congress to end all ”

Ha ha

Confused, I’d support that. Get rid of the free $500,000 in tax free capital gain and return to the system where you could roll any gains into a new house. Otherwise, you create an absurd disincentive to downsizing, which creates the fake ‘housing shortage.”

For example, a couple buys a four bedroom house for $400,000 in 1988 to raise their kids, and sells it today for $900,000. They figure they’d always wanted to live on the beach, so they take the $900,000 in sale proceeds (let’s assume for the sake of my example that the mortgage is paid off and that there are no closing costs) and buy a two bedroom condo with a view of the ocean. If there is no tax-free capital gain, and if the gains can’t be “rolled in” to a new residence, then that couple would owe an extra $125,000-$150000 in taxes, and might not be able to afford this move.

That’s obviously a bad thing, as society is better off if the 4 bedroom house is freed up for a family that needs it.

How about we just trash the 750k pages of the IRS Code?

Gomp,

“IRS Code” is the figment of some politicians’ imagination. The actual name is “Internal Revenue Code,” and it’s written by the Congress, not the IRS. Moreover, the Code is not even close to 750k pages, even including Treasury regulations.

Confused,

Trust me, you wouldn’t want to have to carry the IRS regs (let alone Letter Rulings, etc.) up 3 flights of stairs.

Einhal – this is nuts, what government distortion has done to people’s thinking. Obviously if there was no government subsidies the prices would be lower. Get the G and the Fed out of the housing market!

Hyundai, not Toyota.

The Reuters story is about Hyundai, not Toyota.

Them eastern Asian corporations, they all look alike to me.

Racist! /sarc

I didn’t notice the Plundering Class ever leaving. If you mean party instead of class, you may have missed it, but most of the large corporate donors give to the D side of the coin, not the R side.

“but most of the large corporate donors give to the D side of the coin, not the R side.”

You forgot the /s switch, denoting sarcasm.

It’s common knowledge that pubs have been the Party of the Rich since the 19th century, which is why they’re trying to get rid of anything that helps the general population, SS and labor protections included, and whose only economic policies involve giveaways to the billionaire class.

USA Political Party confusion continues, as has been the case at least since good ol’ Abe’s time fighting slavery as a Republican.

Good bit of USA was under total domination by Democrats who were the RICH and conservatives until good ol’ LBJ did his Great Society bit 100 years after Abe.

Seeing some very likely very much more confusion coming as the democrats veer to the left; while at least at the moment, chaos seems to reign for the republicans, with movements in all directions or at least both toward the extremes and toward the center.

We ARE living in interesting times thank you very much ( for the entertainment. )

Buffett

If you think only the Republicans are the “Plundering Class,” you’re truly a delusional partisan.

You forgot the /s switch, denoting sarcasm.

It’s common knowledge that pubs have been the Party of the Rich since the 19th century, which is why they’re trying to get rid of anything that helps the general population, SS and labor protections included, and whose only economic policies involve giveaways to the billionaire class.

SS and ‘labor protections’ are an albatross around our necks.

Letting billionaires keep their money is not a ‘giveaway’. In any event, if your GOP actually existed it would be a huge improvement on the one we have which do love it punishing immigrants and imports.

Cytotoxic: “SS and ‘labor protections’ are an albatross around our necks.”

That’s because you prefer slavery and having the elderly die in alleys.

“Letting billionaires keep their money is not a ‘giveaway’.”

That’s a rationalization for how The Former Guy has been sued eight thousand times for stiffing his contractors.

Employees can sue for wage theft now. Too bad for you.

Ahh … now it makes sense. You’re the same person who asserted that deficits could only be controlled by taxing the rich – while ignoring the more obvious and effective solution: cutting spending.

Your understanding of economics leaves much to be desired.

SS and ‘labor protections’ are an albatross around our necks.

So, after working 40 years and paying into a system which will provide a portion of your retirement income, the elders should not see any income? If the old are just albatrosses, we should kill them off when they hit retirement age.

And we can remove all the labor protections then allow those 12 yr olds to keep working. Get rid of OSHA and let the worker bare the cost of injuries on unsafe job sites. Insure the employer’s right to fire you if you are pregnant or get ill or you need a week off to fly home when your dad dies.

You have lost your mind.

It’s Hyundai, not Toyota, with the child labor issues.

Newt Gingrich wants to repeal child labor laws. Ladies and gentlemen, this is the man that we need to lead us into the 18th century.

“Toyota will go to prison for child labor in Alabama either.”

I liked most of your comment, but can I get a citation on the above quote?

There is nothing inherently wrong with child labor, if done right.

Also I’m going to need a cite on the 16 million ‘vacant’ homes. And I’d like you to understand that housing is not fungible ie a vacant one in rural midwest does not mitigate a shortage in Boston ie there’s still a shortage.

“There is nothing inherently wrong with child labor, if done right.”

Do you make sure your kids have shoes before sending them into the sweat shops?

“Also I’m going to need a cite on the 16 million ‘vacant’ homes.”

Google it yourself, troll.

I started working at 12years old ,most farm kids did chores before school . Now there’s no work ethic’s because kids never learned how to work watching video games

similar to flea, i started working for money when in single digits,,, selling newspapers on a street corner

when a good day, i sold my 25 papers for 5 cents and took 40% clear ”net” into my pocket and was a very very happy and fairly ”rich” kid…

only started delivering 125 papers each and every morning when age 11 because that was lower age limit..

soon after, delivering those papers every morning, mowing every lawn i could find and my bid was accepted during the day,,, and then typing for $1 per page with NO errors or corrections..

really feel SO sorry for kids today that do NOT have similar opportunities

won’t get into if lack of opportunity due to ”politicians” of the left or right side of the aisle(s) ALL are just puppets IMHO…

Flea – I am surprised you didn’t mention your bootstraps!

Cyto,

The Census does show a pretty large number of vacant residential properties (broken into three or four groups, along the spectrum of continuous availability).

The numbers are big enough to take a lot of the wind out of the sails of the “carrying cost” argument – there are apparently enough rich property owners who can afford to sit on empty, unrented properties…until, presumably, a high enough offer comes along (or enough post ZIRP panic spreads…)

Not with rising utility and insurance costs . Plus maintenance

All these problems with Chinese owned real estate sounds vaguely familiar to the 1980’s Japanese who bought US real estate at the peak and then had to unload for huge losses.

Except and I could be wrong on this, the Japanese mostly focused on CRE not as much on residential single units. These Chinese did it on steroid, CRE, residential and even business that have nothing to do with their primary core business (i.e. HNA acquiring Ingram Micro..etc)

It’s obvious China’s economy is a disaster area. Pegging its currency to the dollar can’t be helping with its export based economy. Now ‘if’, the US dollar keeps strengthening, I wonder it there will come a time it eliminates the peg and allows its currency to float. Otherwise I expect to see the whole country become very unstable. I would not be surprised if China attacks Taiwan as a distraction. The US really seems to enjoy poking China in the eye over Taiwan.

All currencies thst peg to another currency fail pretty spectacularly.

I would bet a Chipotle dinner that Wolf probably did an article touching the subject somewhere in his archives.

There are risks and benefits, but they do not always fail.

One thing a fixed exchange rate system does is prevent the government from pursuing any independent long-term fiscal or monetary policy. You might like to consider why this is the case, and the nature of the resulting distortions.

“Permit me to issue and control the money of a nation, and I care not who makes its laws!” Attributed to Mayer Rothschild.

Cytotoxic: “Capitalism and the billionaire class did that.”

Liar. Capitalism and the billionaire class fought them every way they could and are still fighting them.

Similarly, Republicans take credit for popular social programs they lied about and voted against. Not that YOU would do such a thing. Why, that would be wrong!

You read mainstream/alternative propaganda and form your biased conclusions on false news. First, China’s economy CANNOT be a disaster because the Chinese Government owns it’s Central Bank. That is, the government prints it’s “internal money” for internal consumption….no foreign private creditors to deal with. Simply put, internal debts can be erased. Now, as for these “privately owned” Chinese Developers” (i.e. Evergrande), they are NOT part of the Chinese Government. For the CCP, if these private Millionaires/Billionaires go bankrupt, they are not bailed out (like in the USA). What the CCP cares about is “internal stability”. If ordinary citizens within China are conned/duped, then the Government will minimally compensate these people and convict the private company fraudsters. As in the case of Evergrande, some ordinary citizens were scammed so they received some compensation. However, people who invested because they were “speculating on property” and lost everything were were left out to dry. The government doesn’t protect people from greed. The American Government used to watch over it’s citizens (i.e. Glass Seagall Act) but Private Banking corrupted the law. Now US Government works for the 1% (i.e. 2008 Financial crash).

US GUV MINT always works for 1% Ron.

ALWAYS has and always will.

Get used to it, and ”play” it for your ends, even though the ”rules” are well hidden and change constantly.

“US GUV MINT always works for 1%”

Not when the government fought slavery, fought for women to have the right to vote, fought against German National Socialism and the USSR, fought to end segregation, fought to end apartheid, ended child labor and gave you the five day work week.

No wonder the billionaire class wants to get rid of the government and have themselves a free-for-all.

“gave you the five day work week.”

Capitalism and the billionaire class did that. They did all of that really.

Well…the CCP “erasing all the debt” (via money printing and Fed-like bad asset buy-ups) won’t exactly do wonders for “internal” stability (see multiple doomed US “booms”, Jan 5, and current “impossible” US inflation.)

Even central banks can’t conjure a free lunch – they can merely try and stick politically unconnected groups with the bill (inflation).

Capitalism and the billionaire class did that. They did all of that really.

A toxic troll.

Well, China is have a big enough economy to question what way the pegging work😉

The days of dumping overpriced RE on the Chinese are finished! Round eyes need to eat their $$$ mistakes, too!

Companies that serve very few customers, in a downturn

their chance of survival is low.

Chinese co targeting mostly Chinese, among the top 10%, have fewer potential customers.

Plenty of homes available? A home not for sale or rent that is unoccupied may not be available. A vacation home is unoccupied.

I used to live in SW DC a mile from the Capitol and close to the Waterfront Metro Station. I bought a studio in a high rise there in 2001. I paid $18,500. cash. I did not know it, but there had been some vandalism, robberies and murders in the neighborhood. Gun fights happened some Saturday nights in the projects across the way. Semiauto gunfire sounded like a combat zone. White people were moving out. I commuted to Bethesda and had a job as a computer application engineer. The dot com bubble burst resulted in my layoff. Back home I was robbed on my way to buy a Sunday paper. My tires were flattened. My auto paint was scratched. After four years I moved to a nicer neighborhood where people could walk without getting robbed. I sold my studio for $106,000 in 2005. Today I checked and found a studio in that complex is listed for $129,500. after a $5k markdown. Housing is available, but who would want to live there?

I could rent a condo but never own. People are too crazy nowadays. Owning a condo makes you permanently beholden to the indoctrinated kooky cancelling condo cops next door and their Current Thing.

Condo bats are also notoriously terrible at maintenance and business in general. But will assess you and place a debt on your butt to paint it all peach.

Rather live on a raft made of plastic soda bottles.

I really do marvel at the beautiful job our condo maintenance crew does on our property. I dislike the high HOA fees but I know they are doing what they can to keep our community looking great. just last weekend their was a crew here just to work on some extras around the gardens that the week day crew didn’t attend to. So don’t blame all the HOA and Condo people for being less than stellar. We have maintained yard to play ball/catch/run around on, year round pool & spa, well maintained public areas and problems resolved in a reasonable amount of time

Your paying dearly for that

Thousands of Chinese quit paying for housing they bought and started paying for 5 years ago. But the projects have not been started.

Maybe those guys would be interested in some US Condos.

Maybe Hunter can call Xi and “make a deal”?

Over 40,000 vacant housing units in SF…

The most recent US census indicates that more than 16 million homes are sitting vacant across the U.S., 10.6% of all homes. It keeps those prices and mortgage profits up by controlling supply, and that’s really all that matters, now isn’t it?

There’s no ‘shortage’ of homes. Thanks to the SCOTUS Citizens United decision there’s a severe shortage of elected officials who can stand up to the billionaires who run the country.

unamused,

People buy homes for investment, because they don’t trust the crooked stock market casino. They don’t want to put their

$1M property deep in the pocket of a tenant. An empty house/apt is good enough them. Tenants are black box. U cannot click them out, especially when u try to sell your property.

“An empty house/apt is good enough them.”

Only when prices are rising. Otherwise it’s a depreciating asset.

As if you didn’t know. Your argument is bs on many levels, intended to rationalize keeping homes off the market to keep prices up and enrich wealthy speculators.

How disingenuous can you get?

16 million of them? Who do you think you’re trying to bullshit?

One other point to take into consideration, and one that hits close to home as a Minnesotan, is that people often have two residences.

If one lives in Florida, for example, 185 days a year (and can furnish proof to the Minnesota Department of Revenue), and in Minnesota 180/181 (leap year, eh), then there is zero state income tax to be taken/paid in Minnesota.

A lot, if not most, of these homes are kept vacant, by choice of owners, for one-half of the year. State tax laws give some people financial incentives to follow this dual-ownership game plan. Life, Liberty and the Pursuit of Happiness, which is the birthright of citizens in the USA, allows them to do so.

“Life, Liberty and the Pursuit of Happiness, which is the birthright of citizens in the USA, allows them to do so.”

Numerous antebellum Southern politicians used that same argument to justify slavery, although you could use it for just about anything that makes you feel good.

Let’s see how safe their investment is when the home prices clearly trend down. I tis going down even now but the dis believers would not yet believe it.

Only time would tell but if America is not to be turned into a third world country then home prices have much to fall so that common joe can afford them.

“Numerous antebellum Southern politicians used that same argument to justify slavery”

Doesn’t matter he’s still right and you still don’t understand how housing supply works.

Jon:

Did it ever occur to you that not everyone is concerned about their housing “investment” declining in value? In Dan R’s example, these people who have two homes are taking advantage of income tax rules that determine residency (and therefore state income tax liability) by the number of days present in MN. FL has no state income tax so, if they clear the required number of days, their income tax liability is zero in MN. We see that here in AZ. Probably half of the snowbirds here are from MN. The community was developed by a MN attorney and a few car dealers several decades ago. They come in November and leave in May. Do the math.

That’s how the wealthy accumulate and maintain their wealth – not by becoming debt slaves. They work the angles and, odds are, the seasonal house has been paid for by the state income tax savings over multiple decades.

Some of the homes in the community where I now reside (that now sell in the upper hundreds of thousands to well over a million) were purchased for spit – and were passed from generation to generation.

Wow, the post by el katz makes it clear why there is so much anger in this country. I’m doing fine but I grew up in a poor area, and most or all of my childhood friends are a mess. I’m lucky, I guess. It’s awfully hard to play the angles explained by el katz when you come from a poor background. I fear that the anger could boil over at some point.

1) Some investors put gold in their vault, other accumulate real estate. Many own both.

2) Some keep kids in their apt/houses, some keep them empty.

3) Many will keep properties through downturn, because they can.

4) Speculators and B&H have one thing in common : they don’t let tenants in.

5) In a downturn, when banks call, they might transfer ownership to

their kids…

Those 16 million vacant homes are vacant because of many reasons. That number has been decreasing and was basically at 19 million in 2009 and is now 15.1 million. That is a 20% decease.

Don’t buy the myth those will all hit the market. Only 6.9 million are held off the market, the rest are most likely in a transient stages (waiting to get rented, etc)

In 2015, 7.1 million were held off the market. In 2010, 6.9 million were held off the market. In 2005, 5.9 million were held off the market. In 2004, 5.4 million were held off the market.

Now that being said, there are probably more people ever in the U.S. who own a 2nd vacation house. I know many who have some sitting vacant at a lake or they are trying to make money doing AIRbnb in Florida.

Somebody commented that in 2017, you could rent a condo on the emerald coast for just over $200 a night and now it is over $350. That higher rent is supporting higher prices. Will it continue, will it drop? I don’t know.

Owning a house is always a risk. Will the area grow in popularity or will it decline. I am guessing in the early 1950s, downtown Detroit was probably were housing was always going to go up.

It appears the actual place was California and Arizon. ;) /sarc

Euclid avenue in Cleveland was once known as millionares row, or something like that. A million back then meant something. Tours came from Europe to view the opulence. The wealth was extreme. It’s all gone now. Change happens for many reasons, and I suspect most of them are unanticipated.

Banks have repo parking lots loaded with repo cars, but they release

them slowly, to avoid flooding the market.

Michael Engel,

Hahahaha, Internet BS. Repos are up just a tad from record lows in 2020 and 2021 when folks used their stimulus funds to get caught up. But repos but remain below 2019, when they were already very very low.

I saw the article of surging repos on ZH earlier today, authored by Mish, that used MY chart of auto loans from Q2 2019, hahaha, from three years ago (!!!) to make some kind of braindead point about surging repos hitting used vehicle auctions and collapsing prices. He cannot even build his own charts, or get the actual data, or find current charts of mine, because I already posted the Q1 2022 auto-loan chart months ago. If Mish and ZH is where people get their info about repos, and if they take this garbage seriously, god help us all.

Since this article has relevance with past excesses of the Fed QE policy and without any intentional ruffling of any feathers at Wolf Street Corporate I would like to know what the head honcho’s thinking is on what the Fed balance sheet might look like in October?

Down by an additional $200 billion to $300 billion.

“It’s just that rents in San Francisco aren’t so hot at the moment either, with the one-bedroom asking rent still down about 20% from the peak in 2019 due to the “housing shortage,” or whatever, as San Francisco has lost about 6% of its population since then:”

1) Rents are still incredibly high

2) Yes, it’s a housing shortage, those 40,000 supposed vacant properties (that I will believe when I see) are a drop in the bucket of the shortage

3) The shortage and resulting insane rent prices and lack of space (people literally living in closets and bunks) is a big reason why people are leaving

“40,000 supposed vacant properties (that I will believe when I see)”

Start looking and get back to us when you’re done.

Apartment.com lists nearly 5,000 apartments for rent today in San Francisco, which is about TRIPLE the number it listed before 2019.

Inventory for sale is now also coming out of the woodwork in large numbers. There are things for sales all over the place.

But yes, agreed, rents are still way too high, and prices are still way too high, though prices have started to drop, but it will take a long time.

This (healthy and corrective) meltdown in China is along with QT/general tightening and rightening, a big reason I am bearish on the price of oil and commodities in general. I don’t see the upside.

No idea about oil and NG the wildcard is Russia. Underinvestment in oil around the world will ultimately lead to higher prices as large amounts of investment is needed to keep oil production flat. These funds will be harder to secure as the USA and EU major oil companies reduce their carbon footprint and provide less bbls. Oil has always been volatile and will continue to be so.Rhe surplus built up during Clovis took no time to disappear.

The fracking boom and bust left behind a large number of spudded wells last I heard, and last I heard these weren’t that hard or expensive to open up and costs have only fallen. Investment doesn’t have to be expensive.

Many of those drilled but not completed wells will require a costly “frac” job, testing for liquids/gas/produced water quality and spec, well head, casing and piping installation, installing several 400 -500 barrel aboveground tanks, installing separation and treatment equipment, and connection to a gas pipeline (if salable gas is produced or if one is actually nearby). Oil and produced water are almost always trucked off the well site.

So it’s not just “pop the lid off” the previously drilled well bore and go. Looking at a couple of million $$$$ on a big well. More if it’s a horizontal with several laterals.

I spent 30 years in the oilfield. Wells are more productive now than decades ago due to the advent of horizontal drilling procedures, enhanced fraccing equipment, better down-hole tooling and 3D seismic mapping.

Ben,

Seems your comment ended up under the wrong article. It should have gone here, maybe?

https://wolfstreet.com/2022/07/22/us-natural-gas-prices-re-spike-after-the-big-plunge/

Easy absolutely resource available to drill is abundant. Costs may have fallen as companies develop efficiency and longer lateral in the Hz section then approach some technical limits.

So the gains of bbls/$ spent is finite.

Access to funds ? Cost of capital ? Increasing capex? All questions. Yes oil can easily fall just two years ago was negative in May 2020. And now back to 90. Long term futures has oil at 65 which I agree with. So high price to me is above 40.

“Unpaid subcontractors have filed mechanics liens on The Oak; and Z&L owes $2.05 million in unpaid taxes on the Oak, according to the San Francisco Chronicle.”

Some commenters believe it’s just wrong to make billionaires pay their contractors and their taxes.

Apparently we owe Everything to the billionaire class and haven’t been worshipping them properly. Or making donations in proportion to their godlike benevolence.

Crytotoxic

Great point about the drilled not completed wells. You are right about the cost of those vs drilling and completing since frac cost and pipeline represent 50 percent of the cost of the well.

If a company does not complete and produce a well eventually and at the right economic time they either cannot compete economically at the current price they are fiscally irresponsible.

Oilprice.com covers the details very well if one is interested. We have a global market of oil and gas and a few wells on the margin that deplete 80 percent in the first year have no impact on the long term price of crude.

Unpaid contractors. Been associated with a group that did just that in hope that the business would role in tp pay the contractors. The intent is here to pay but rather than having the financing in place for payment the customer gets overextended as the business unravels. Prices drop and sales disappear faster than the spend rate gets paid.

If intention then fraud and should be a felony. Laws are not upheld too many times. As you say probably by the well funded 1 percent who hide behind banks and corporate legal entity.

Back in the day there was this joke …

Q – What’s the difference between a condominium and a Venereal disease?

A – you can get rid of a Venereal disease.

1) When drilling switched from vertical to horizontal each acre

produced more, much more oil. The value of land went up.

2) The price of leasing an acre went up. Early investors made a good buck selling few hundred thousands acres, keeping the rest.

3) It got wall street exited. They care about RE. They herd together, imitated each other, created a bubble.

4) When prices dropped they got out. They don’t care about oil or natgas, or whatever those acres produce, or if they are profitable, or….

If you have about an hour of time, you can check out “The china hustle” on your favorite video sharing platform. It’s not quite “The Big Short”, but it shows how the hustle just went on after 2008.

It’s from 2017. It’s not that these things were not known. But it paid off to ignore them. That’s how these things always work – until they don’t.

Which is: now.