Enormous churn and job hopping amid aggressive hiring, near record low layoffs, near record high job openings and quits.

By Wolf Richter for WOLF STREET.

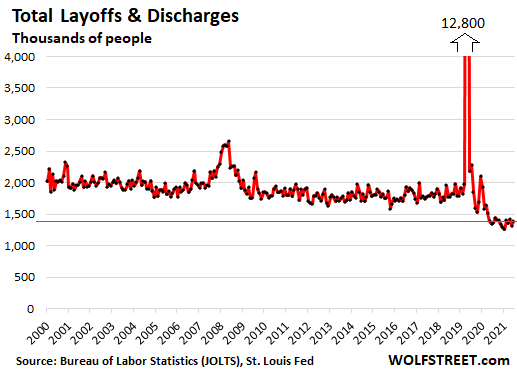

There have been numerous announcements and reports of hiring freezes at some tech companies, and layoffs at others, including in the crypto and DeFi zone that is now collapsing. But the layoff numbers were small, mostly by startup companies, or some small-scale targeted layoffs at larger companies, not mass-layoffs. And total layoffs across all industries have ticked up just a little from the record lows and remain historically low.

Layoffs in May rose by 77,000 from April, to 1.39 million layoffs, according to today’s Job Openings and Labor Turnover (JOLTS) data. But this was down by 22% from May 2019 and remains in the record low range. By contrast, in the 2011-2019 recovery, there were an average of 1.80 million layoffs per month. And in the 2000-2007 recovery, there were an average of 1.87 million layoffs per month.

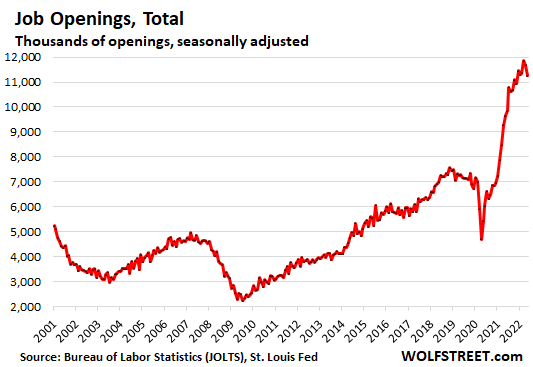

Job openings remain in the Astronomical Zone.

At the end of May, job openings dipped for the second month in a row, to 11.25 million, down 5.1% from the record in March, seasonally adjusted. But this was still way up in the astronomical zone, up by 55% from May 2019.

Note, these job openings are not based on online job postings – and therefore not influenced by fake online job postings – but are based on what companies and government entities said their hiring needs were:

This is one more indication that the “labor shortages” continued through May in an extraordinarily tight labor market, despite some small-scale layoffs and some hiring freezes, and that it will take a lot more layoffs and a lot more hiring freezes to loosen up the labor market back to anything resembling “normal.” This may come over the next few months, but it isn’t here yet.

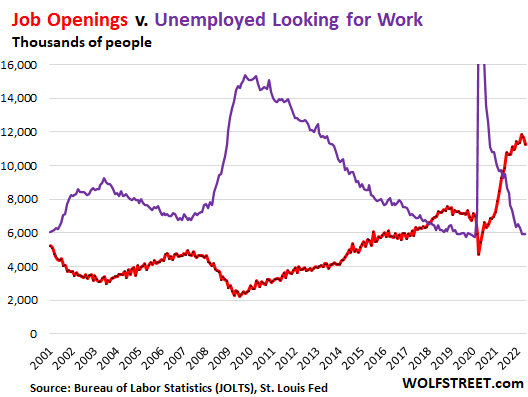

Job openings v. unemployed people looking for a job.

In the years around recessions – from 2002 to 2004 and from 2008 to 2012 – people are losing their jobs and start looking for work, and at the same time, the job openings vanish, and there is a big gap between the unemployed looking for work and actual job openings.

At the peak of the Great Recession in late 2009, there were 15 million unemployed people looking for a job, and only 2 million job openings – which is terrible math for the unemployed.

As the economy improved more job openings appeared, and more people found a slot, and unemployment fell.

Then in the already tight labor market in the years before the pandemic, job openings exceeded for the first time in the data the number of unemployed looking for work, which is what workers want. That’s the sign of a strong labor market.

Since June last year, job openings have exploded, even as the number of unemployed looking for a job has plunged, creating the biggest gap between the two – another aspect of the “labor shortage.”

That gap has been cited by Powell as well – with a historically high 11.25 million job openings and a historically low 5.95 million unemployed people looking for a job in May:

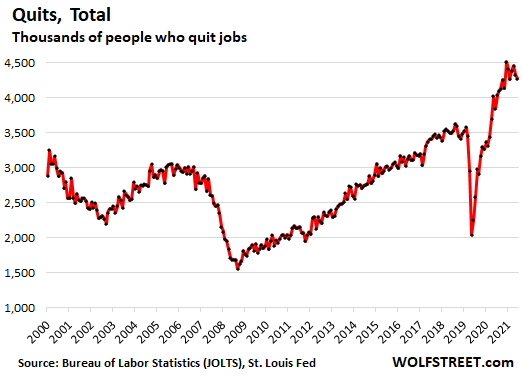

And “Quits” remained near-record highs.

The number of workers who voluntarily quit jobs in May dipped for the second month in a row, to 4.27 million, but was still up by 23% from May 2019, and remains in the astronomical zone, largely reflecting job hopping, as workers “quit” at one company to fill a job opening at another company – and thereby creating a new job opening where they left.

This is a reflection of very high churn in the labor market, as companies are aggressively hiring, offering higher pay and better working conditions, and they are recruiting people who already have jobs, while workers discovered their power in the labor market, and they’re going for the greener grass on the other side of the fence.

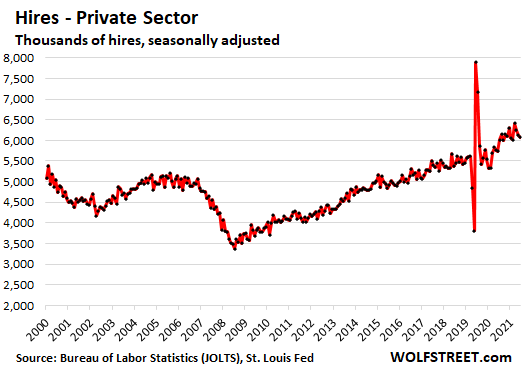

Aggressive hiring.

Private sector employers hired 6.08 million workers in May, up by 13% from May 2019, and in the same high range since June 2021. Hiring is handicapped by the ability to find qualified people to hire and to entice them away from where they’re working now:

Quits, hires, job openings, and churn.

For the past 12 months, “hires” have been running above 6 million, “quits” have been running at above 4 million, and total job openings in the 11.5 million range.

This relationship between hires, quits, and openings shows that the majority of the 6+ million a month in “hires” filled job openings that had been created by people who quit those jobs and went to work somewhere else.

When a person quits a job at Company A, this company reports it as a “quit,” and if it tries to fill that job again, it reports it as a “job opening.” And when the same person gets a new job at Company B, that company reports it as a “hire” and removes a job opening. Overall, the system reports one “quit,” one “hire,” and no change in job openings, with the opening just shifting to a different company.

That’s churn and has no impact on employment. And there is a huge amount of it now.

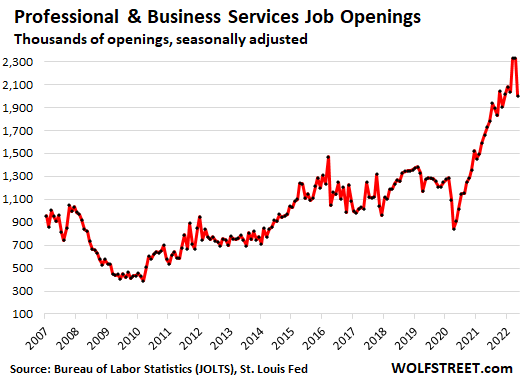

Job openings by major category: declining but still far above “normal.”

Professional and business services (includes tech and social media and is the largest category): Job openings fell by 325,000 in May from April, to 2.0 million openings.

Many of the hiring-freezes and layoffs were announced in May and are starting to be reflected in the data. But March had been a huge record for openings in the sector, and that drop leaves these job openings still in the astronomical zone, up by 57% from May 2019:

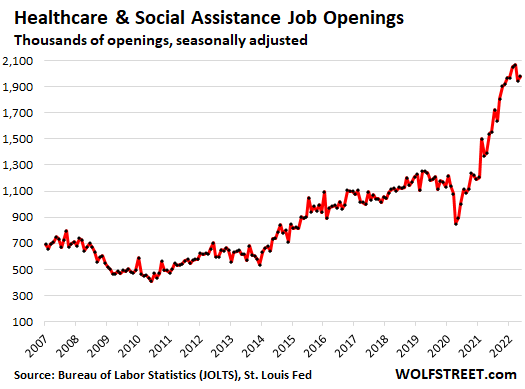

Healthcare and social assistance: Job openings ticked up a tad in May, after the big drop in April, to 1.98 million openings, up by 60% from May 2019, an indication of continued and frequently reported labor shortages, for a variety of reasons, including due to burnout, inadequate pay, and tough working conditions for nurses and other staff.

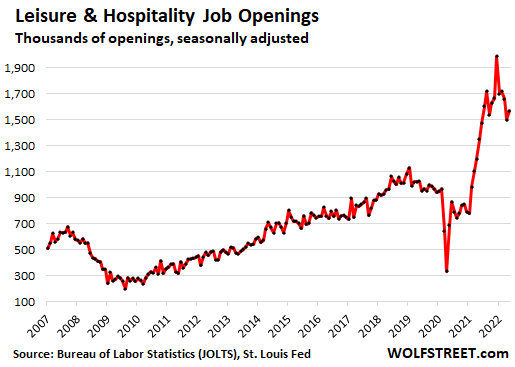

Leisure and hospitality: Job openings have backed off from the spike last year but remain very high. In May, they rose by 72,000 to 1.57 million, up by 53% from May 2019.

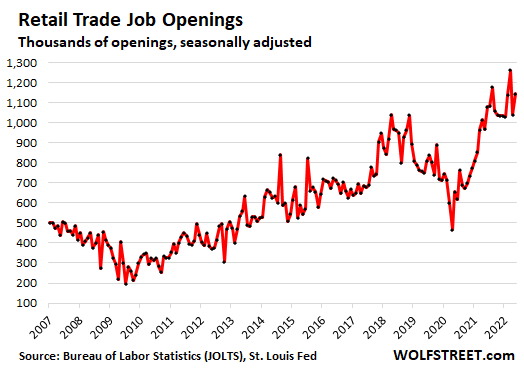

Retail trade: Job openings rose by 104,000 in May, after a sharp drop in April, to 1.14 million, up by 52% from May 2019:

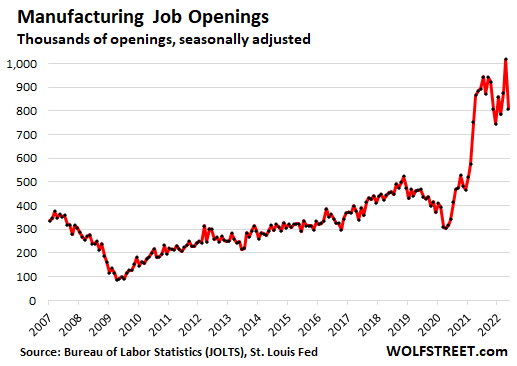

Manufacturing: Job openings dropped by 208,000 in May, to 809,000 openings, following the spike to a record in April, but they were still in the astronomical zone, up by 74% from May 2019:

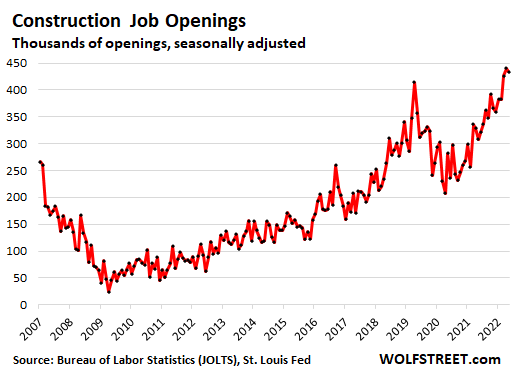

Construction: Job openings dipped by 6,000 from the record in April, to 434,000 in May, and were up by 22% from May 2019:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

looking forward to see the next rate hike from FED pointing to the inflated and hot market and economy, then all these QE fans will be shut down again.

Interestingly, if I can trust Lately Michael Burry or not, but he is pointing that the FED is not tightening enough and that FED stopped offloading MSB lately, His point is that FED is not fully determined to fight the inflation and that they are going 180 degree and will start QE aging, things are changing very fast.

Any opinion, ? Do I pay too much attention to noise?

Is Michael Burry creating noise? or he is just a little more trust worthier than other riches?

Sorry for my spelling errors, I always post my comments and then read them. :)

Who is Michael Blurry, and why do we care?

You are gonna have your ear full about the “fed not offloading”.

Side note: of course they will start printing again. It’s all they have or know.

andy,

“It’s all they have or know.”

Nope, they also have QT, and they know how to do it because they did it last time, and it allows them to keep their policy rates lower in their fight against inflation.

Enough QT and 3.5% or 4% might do, when without QT, they might have to go to 8% or 9% which would be much rougher for the real economy. QT mostly hits asset prices, not the real economy, just like QE mostly inflated asset prices, and did little or nothing for the economy.

QT is going to be a big powerful took in cracking down on inflation without hitting the real economy much.

It sounds like magic.

Here, Wolf, I’ll save you the trouble since you just posted this TODAY:

(per Wolf)

Burry is ignorant or lying – take your pick. Don’t post his BS here. And you’re don’t know nada either, it seems. So quit posting this tightening-denier BS here.

1. Since the April peak, the Fed’s balance sheet has declined by $52 billion!!! That’s QT.

2. The Treasury roll-offs occur twice a month, mid-month and end of month. In June, they occurred on June 15 and June 30. The last balance sheet was through June 29. And so the June 30 roll-off wasn’t on it. Get it?

3. I’ve said this a million times already. But you chose to not know.

4. The June 30 roll-off will be on the balance sheet to be released tomorrow, and I will make sure to cover it and I will ridicule that idiot Burry and all the other tightening-denier idiots. You chose your camp.

I’m just really tired of this tightening-denier braindead ignorant BS that people vomit into the comments here. Every day, people post this same BS here without ever reading anything, just regurgitate the same BS they saw somewhere else. And I have to waste my time shooting it down over and over again.

drg1234,

If you read my comment then you will see that I am not a QT denier , and I am looking forward to see the next rate hike. obviously we had a little mortgage rate coming down and DOW bouncing back up, but nothing goes to heck in a straight line!

And if you read my comment, you would see that those are Wolf’s words. I happen to agree with him.

Your problem isn’t your attitude towards QT. It’s that you post shit on a blog that you obviously don’t read.

😂 not really, Wolf does not talk like you did attack here. Do you think you are Wolf #2 ?

If you dont tolerate some comments, fine , dont have to respond. Your problem is your attitude towards commentators, and do you expect everyone read your comments?

I expect commenters to not hijack the comment section with BS — such as the Burry BS — that I have debunked a gazillion times.

Not convinced that QT will leave the real economy unscathed. If the market returns to setting bond prices without central bank interference, wouldn’t the 10-year Treasury pretty much fall out of bed, price-wise?

Correct me if I am wrong — just be civil about it, please — but wasn’t QE after the Panic of 2008 pretty much all about housing finance, and QE from ’20-’22 about both housing and government finance?

If QT is for real, meaning sustained at a material level, wouldn’t we see debt service be a pretty rough issue on the Treasury side of things, and wouldn’t we see a spike in mortgage rates? It seems complacent to characterize QT as benign for the real economy.

How do I have it wrong?

Wolf,

I dont care about him but what I wanted to bring up is a point. The missed point here is that whether the QT is enough or even the MBS that FED wanted to off load is enough . Obviously it is a question that FED admitted that they dont know. Everyone is arguing that with their own perspective.

What if they increased the rate but the house prices and other expenses keep going up ? Thats a scenario that I was pointing. Up to what extent they can react?

Now, If I am not patient enough to see the results , that is a different subject.

The point is that FED shows or says that it is determined to fight the inflation, but acts very late and very cautious. Seems like it wants to have train reck at the end of this movie

Good lord. It’s like folks just want to get bitch-slapped into orbit.

😂🤣😂🤣😂

drg1234,

I asked Wolf, you don’t have to waste your time! Watch your mouth.

drg1234,

but, still thanks for information .

Educated but Poor Millennial,

Burry is an ignorant idiot when it comes to MBS. He has no idea. I’m so sick of people dragging this effing BS into here. He has no idea how they work.

I’m just ridiculing this idiot.

MBS have started to drop just fine, and faster than I expected, because they take months to show up as the Fed trades them in the To Be Announced market and books the deals when they settle months late. MBS dropped by $19 billion in the last week and are down by $31 billion from the peak in April.

The “halo effect” with Burry is phenomenal. He made a big smart right short bet that hit hugely in ’08 on mortgages, and was the star of a Michael Lewis book. (Michael Lewis books seem to always have a good guy, a star, like old western movies did.) With this glittering media glow fronting every quote of him, it is as if he cannot err.

But John Paulsen made the same right bet, and later was serially wrong on a lot of things for a long time. Meanwhile he was gobbling investors’ money, based on his halo. Same for John Meriwether of Salomon and later LTCM.

Burry is a doctor.

Burry’s also a hedge fund manager, which means he’s talking his book. [ Heck, too many doctors are also getting caught “prescribing their book” – being biased by Big Pharma incentives… Not saying Burry’s not honest just that “being a doctor” doesn’t guarantee anything about anyone anymore. ]

Interestingly, in the Big Short phase of his life, he was eventually proven spectacularly right – but not before he lost most of his investors during the earlier phase when his vision hadn’t paid off and looked insane.

Well Soros also made a big short bet, and we’ve been living with that for a long time. Who’s your DA, baby?

Don’t deny real consequences. You can plan around them, but there they are.

Burry was well on his game back in the 2000’s, but the housing market is considerably different today than it was back then, as banks aren’t just handing out mortgages left and right to every Joe Blow off the street. That’s not to say housing is ridiculously overpriced, but the people driving this bubble are institutional investors like Blackrock, foreign investors paying all cash, and other wealthy investors buying homes to rent out via Airbnb and VRBO.

Read that 70% of mortgages are being done by non banks and some are going under.

One scenario is that it will not be higher rates that kill housing, but that you will not be able to get a mortgage unless your credit is pristine.

Thank you, Wolf for revealing the facts and not the BS.

I will be a life-long fan.

I will also purchase your book and read it while drinking from my WolfStreet mug when you publish.

You have been right the majority of the time I have been reading this excellent blog.

Burry is a one time wonder kid per my understanding. He made it big during GFC and people take words from his mouth as gospel.

nothing does up/down in a straight line.

EPM,

Wolf covers this a lot in his comments, but quantitative tightening absolutely is happening and it’s happening aggressively. What Burry and so many of the misinformed “experts” keep missing is that there’s a delay, a huge delay, from the time that QT moves (incl. MBS sales) are made and the time they’re settled (and show up) in the “to be announced” system. It was QE from the Fed if anything even more than ZIRP that was responsible for these dangerous US asset bubbles and raging inflation, especially the unsustainable housing bubble and all the pain that’s causing for new would be homeowners and renters, and so QT is a powerful tool. It likely won’t be enough on it’s own and more rate hikes are needed, but between interest rate increases and QT, you’d better believe that Jerome Powell and the Federal Reserve are going full Paul Volcker here. They have no choice otherwise, runaway inflation like this wrecks economics and nations, far more than a recession can.

Well said. Thank you. I hope they don’t declare mission accomplished prematurely when inflation begins to subside. There will be enormous pressure on them to do that.

The same here. Inflation really feeds on itself, and ex. the home prices we already have are unsustainable, and driving the individual rental market to rents that are crushing high for most Americans, even professionals earning a lot of money. Texas for ex. is getting slammed and while it has a lot of affordable cities and towns, they’re under threat too if prices keep rising. We’ll be facing a deep recession in 2023 and it’ll be rough, but we can ride it out to a recovery. Runaway inflation isn’t something a country can ride out though, so the Fed and the other central bankers really need to stay aggressive against it.

Higher interest rates are putting a damper on housing prices. Sales are already falling. Zillow is already showing price cuts in my area.

QT IS NOT HAPPENING AGGRESSIVELY! Had the Fed jumped in immediately and started running off $125B, then that would have borderline aggressive. But this waiting three months to go full tilt is not aggressive. It’s the same old slow poke Fed we’ve seen for the last 12 months. And don’t give me that it took them 12 months last time argument. The balance sheet is 2x bigger and the last time didn’t go all that well, a measly $650B was runoff before the Fed was forced to reverse course.

“you’d better believe that Jerome Powell and the Federal Reserve are going full Paul Volcker here.”

Same thing here. Absolutely not! Full Volcker would be selling assets outright. Running them off is about as slow poke as the Fed could possibly get. And the Fed already saw how fast interest rates were rising when they announced their plan in May, meaning a lot fewer houses being sold, meaning a lot less pre-payments to meet their $35B runoff cap in September. Heck, they may not meet their $17.5B cap in July & August, if the housing market slows enough. Again, full Volcker is outright selling MBS which, of course, would drive up mortgage rates further. At $35B, it will take many years to runoff the MBS.

The Fed’s hands are tied. They can’t sell off assets. It would cause rates to spike to untold levels, thereby significantly increasing America’s debt borrowing costs.

Does anyone really think running off the Fed balance sheet over 2-3 years, leaving about $6T, is really going to go smoothly and to full fruition? The first and only other time this ever happened, from late 2017 to Sept 2019, the 10YT rose initially then nosedived as unemployment rate continued to tick down as the FFR rose & created a yield curve inversion in May 2019. If QT this time forces yields down, then we’re screwed.

And from what I know, the Fed ended the last runoff due to the repo market freaking out from 10/2018 through summer 2019 by restarting its purchases of treasuries. So, everyone thinks this time is different and the Fed is going to be able manage FFR increases, asset runoffs so as the repo market doesn’t freak out again? And it has to manage a burgeoning RRP that’s at $2.3T and growing in order to suck cash out of the system?

All that just seems a bit too much to me.

My money is on a strong labor report Friday. IMO, the only way out of this stagflation is for the Fed to induce a significant recession (aka Larry Summers style). Otherwise, we’re in for stagflation with long-term inflation running at least 5-6%.

Thanks, Jay. You saved me a lot of time and effort pointing out how sloth-like the Fed’s balance sheet reduction plan has been and is planned to be!! When a central banker has little backbone, partially because he or she is fatally conflicted due to the swinging door out of Wall Street to the Fed, there are few operations that will put some spine in Monetary Tightening.

All should remember that Labor Market reports are lagging indicators as to the health of the economy. Have seen few companies over the last 55 years that are not guilty of hiring with both hands even as the overall economy is tipping into recession. We are at that point now, and have been so for several months now, if not quarters.

This is a grossly distorted Labor Market due to the shrapnel from Economy Shut-downs that have proven to have done little to contain the creative Chinese Bat Flu. The Quits are in for a big surprise during a severe or average recession: people inventory is relieved using the Last In, First Out method of lay-offs. Companies usually have little invested in job-hopping, new employees and act accordingly.

But the Powell Fed is hardly setting the world on fire in draining liquidity from the U.S. financial system, even with their reverse repo operations, that are overnight, not permanent liquidity drains. Get ready for several years of red hot inflation, even as the year-to-year comparisons ease, because QT and Fed Funds increases will still allow negative Real Interest Rates to be the rule and not the exception.

I’m frustrated by how slow they act, but I’m glad they are doing something. I do not know how fast they can do QT without causing a meltdown, and I doubt they have a good handle on that either. I wish they could be more dynamic, like selling into periods when demand for treasuries is high. Seems like that could be used to stabilize the yield curve, but I admit that I do not understand the repurcussions that could result from action that is not telegraphed well in advance. I share the frustration expressed here regarding the slow pace of the fed.

Agreed, can’t say better about the aggressiveness of FED

If Powell was going “full Paul Volcker” he would have done it years ago when it would have been more appropriate. Back then he tried and then chickened out. And now he is way late.

0.75%? On his way to Volcker’s 20%. It will take him 20 years. It’s all a con buying time for serious war to kick in.

It was called the Volcker Shock:

“During Volcker’s confirmation hearing in July 1979 before the Senate Banking Committee, the soon-to-be Fed chairman made his intentions clear. By then, inflation was running at an annual pace of about 9 percent. Volcker pledged to make fighting inflation his top priority, telling lawmakers the Fed would “have to call the shots as we see them.” In response to questions about his views on the money supply, Volcker responded the supply had been “rising at a pretty good clip,” and there was no evidence the nation was “suffering grievously from a shortage of money”

All that sounds really familiar, doesn’t it, JPowell, especially the 9% inflation? And BTW, the FFR, when Volcker took over in Aug 1979, was about 10.5%. +10% FFR already, and he pushed it up to 17.61% by April 1980.

But, he didn’t have $30.4T in US debt, a $9T Fed balance sheet or $11T in EXTRA spending over two years to deal with. And he probably wasn’t a proponent of managing our economy by means of MMT. JPowell can’t let the FFR or any treasury climb up to 4% nowadays. If he did, the interest on the debt will explode to at least $1T annually, and we’ll only take in low $4T this FY and revenues are already declining from the slowdown in the economy. I think revenues from the Great Recession fell by $420B. Today, that could easily jump to $800B with a nasty enough recession.

Last, the debt to GDP in 1979 was 32%. Today, it’s at least 132% depending on how the negative Q1 & Q2 growth are applied.

Miller,

Once I asked Wolf about what I should do about this inflation , and he said to raise my income and luckily I got raise lately. I would like to see more QT, and rate hikes, since house prices went so high that no one can easily afford, specially here in Los Angeles.

Everything went high so much. Items that I regularly buying are %20 to %40 higher for example my AAA just increased my annual insurance rate about $800 more for no reason but inflation!!! and it is frustrating.

I know that Wolf is informing us realities about the QT, but sometime I get distracted by some noises, which are plenty in the Media. Sorry If I contributed to the noise myself.

Seems like every article someone mentions Michael Burry this week.

I’m back in moderation? I haven’t really posted here much…

You’re fine. But you hit a trip wire, twice in a row :-]

No problem, don’t take it personally. At least those tripwires don’t set off explosives.

When it rains everybody mentions Noah

I’m coining a new recession indicator. Here it is. If you live in a fairly affluent area like me and stop off regularly at a big box gas station like RaceTrac in GA around 7 am every morning and the entire parking area & pumps are mostly filled with commercial vehicles like tree removers etc, then we’re not in a recession. We’ll call this the “RaceTrace Test” going forward.

To-date, the Fed has done absolutely nothing to induce this producer recession we’re in. Zilch. And, you can already see the Wall Street gurus clamoring for the Fed to take their foot off the peddle sooner rather than later. Without real job losses that push the unemployment rate up or above 5% for quite some time as proposed by Larry Summers, then this economy isn’t really going to slow down much. The housing market will cool, causing the 30YFRM to drop back to 4-4.5% and then it will turn around higher.

Sure, Russia could create a real oil shock and may very well do so by later this year. But save that, JPowell is going to blink sooner rather than later.

The recession indicator used by Wall Street is, whenever the Federal Reserve tightens, a recession is imminent. Whenever Congress is stuck in gridlock & cannot pass trillion-dollar binge spending bills, a recession is imminent.

If the Federal Reserve promised to stop raising rates & shrinking the balance sheet effective today, all the recession talk would immediately disappear and the S&P 500 would rocket to 5,000 overnight.

This was the first-ever bear market that started while rates were still at zero & QE was in full blast. Just the threat of future tightening at the time was enough to spark the selloff.

The only thing Wall Street cares about is free money. Like a crack addict.

Thank you. There are clearly no adults left in charge.

My money is betting Powell will do the wrong thing.

I think JP is 1-for-3.

1) He started to normalize rates in ’18 and then did the “Big Wince,” when he was arm-twisted, backtracking and dropping rates, goosing the economy as inflation threatened, pre-COVID. 1 down.

2) He revved the printer up historically (histrionically?) and spent a lot in March when COVID markets crashed. I’ll be nice and say 1 point positive.

3) he said inflation was transitory and kept revving long after it made any sense. 1 down.

That is a pretty bad average with such high stakes. Yeah, small sample, but I agree, he’ll probably blow it.

I respectfully agree with Wolf.

There is so much money still drifting around the system he can raise rates until he says uncle.

Yes they will be slow and steady but so far he has gone further than I thought he would.

Midterms are near, oil needs to be squeezed down if it can be, then we shall see what his actions say.

He’s part of the club, is responsible for this mess and hopefully continues on the hiking, QT path.

Which will be to undershoot & U Turn too early.

Mortgage rates will not necessarily decline in response to a falling housing market. I’m not even sure it’s likely for that to occur. Rates are driven by many things.

For the two years prior to this past March, mortgage rates were driven by fake demand from the Fed. IMO, the only way mortgage rates move notably higher is a scenario develops that forces the Fed to sell them out right. And I think the main driver of that would be real stagflation taking hold by early next year, forcing the Fed to raise the FFR up to 5-6%. I think we’re in for entrenched 6%+ inflation until JPowell puts on his big boy pants. My last point is that the situation we’re in right now is so unprecedented that everyone, including JPowell and his legion of analyst & data dumps, are all arm-chair quarterbacking how this plays out. Nobody really knows and JPowell is on record now admitting as mich.

C-19 created a lot of demand for housing two years ago.

Apple, yes, to a small degree, but a lot of the demand was because the Fed was effectively paying people to buy houses.

JPow isn’t going to blink, if so it would’ve done it long before this. But QT is in full swing and interest rate hikes are getting more aggressive. And, your reasoning contradicts itself, you say economy isn’t in recession (and it likely isn’t yet) but then argue the Fed would blink? If anything your reasoning suggests the opposite, we’re not yet in recession so Powell and the board members are justified in staying aggressive. And a recession wouldn’t cause the Federal Reserve to back off, a deep recession is basically inevitable in early 2023 but you’re forgetting, it’s the runaway inflation forcing the Fed’s hand here in the first place. A recession and stock market plunge (to more realistic values) wouldn’t wreck the US economy. Uncontrolled inflation OTOH would wreck the US economy, American power and the US dollar itself. And no, the housing market isn’t turning around anytime soon–it must fall since it’s far exceeding incomes, defining a bubble. The only measure that matters.

“JPow isn’t going to blink, if so it would’ve done it long before this.’

He already blinked the last time he started to raise rates and the market called his bluff.

joe2,

Last time, inflation was BELOW the Fed’s target. That’s a huge difference. The Fed tightened with inflation below its target, and then came under withering pressure from Trump.

Now it’s the opposite. It’s tightening with inflation at multiples of its target, and it’s under political pressure to crack down on inflation.

“JPow isn’t going to blink, if so it would’ve done it long before this.”

What are you talking about? We’re three months into FFR rate hikes and 1 month into asset runoff?

“QT is in full swing and interest rate hikes are getting more aggressive.”

Again, where are you getting your info? QT doesn’t go full tilt until September. A 75-basis point rise when the FFR should be at 5% to deal with 9% inflation isn’t aggressive. It’s called slow poking it.

“a deep recession is basically inevitable in early 2023”

The only thing that’s inevitable by early 2023 is JPowell still trying to figure out how to put on his big boy pants. The labor market is going nearly full steam given the slowdown purchases by Target, Walmart, etc. More to follow @ 8:30 am tomorrow.

Forecast: 300K

Stay tuned

So why do the WSJ & CNBC talking heads continue screaming about an imminent recession?

Bond traders have made trillions in bets that the Federal Reserve will soon be forced to pivot and slow/stop tightening, if not cut rates & restart QE next year.

Every time we get strong jobs or inflation reports, long-term treasury yields tick up briefly then fall back down again. What gives?

Bond traders unwound some of those bets today and the 10-year yield jumped 13 basis points.

“Enough QT and 3.5% or 4% might do, when without QT, they might have to go to 8% or 9% which would be much rougher for the real economy.”

QT doesn’t go full bore for another two months. BTW, what is enough QT? They only got to $650B last time the before the liquidity experiment had to be abandoned. Sure, they made some adjustments, but I don’t see them getting to $2-3T in the next 30 months. The Fed is raising rates WAY to slow. They should already be between 4-5%.

Jay,

“What is enough QT”

That’s is very good question. No one knows, but we’ll find out for sure. There was a lot of discussion at the Fed about this. Some of the Fed governors thought $120 billion a month would be about right. But others disagreed, and so they compromised on $95 billion a month. Markets have reacted pretty strongly to that $95 billion figure, so it may be enough.

Wolf, you owe me $0.05 : ) I referred someone to your sight today. Maybe he’ll buy a mug or two.

The dude was like, who’s Wolf Richter? I sent him the URL to this article. Told him you create great graphs and really know your stuff.

Money!

thanks!!

I’m that guy. I am looking around. Seeking facts, logic, and intelligence. Clarity helps a lot. We shall see how it goes.

Sure is funny how commodities market is getting slaughtered right before mid- term elections,this shitshow is a joke . Everything is manipulated by worlds central banks 🏦

Everything is getting slaughtered while the DXY rockets up past 107. Imagine the carnage when it hits 120! No one seems to know or care that dollar strength like this is a recipe for world wide disaster.

“ So why do the WSJ & CNBC talking heads continue screaming about an imminent recession?”

Not to be unkind, brother….

The things you read and the the things you hear are not the original thoughts of either…

Both aforementioned outlets have scripted and/ or editorialized content to get your attention…

Not tell the truth…

They’re also compromised by “recency bias” – thinking the future must be like the recent past.

But mostly their job is to gaslight you… and conceal that which you “shouldn’t” know… on behalf of their sponsors and bosses.

In addition to the other points made by other people, I think we still have a whole lotta fiat slopping about, nervously scrambling from one rat hole to another, thus causing variations in rates and indices that are no reflection on fundamentals. Crazy world.

Tech has now become so ingrained across all business sectors that it should hold up for a while. Tech drives innovation and automation so cutting tech budgets may be harder to do during this downturn.

In the past, tech was more of a ‘nice to have’ as apposed to a core need. Everyone I know in tech is in high demand right now so unless someone is rolling off a project, most are fully employed with opportunities for advancement.

WSJ today says ad revenues for big tech are expected to fall. That is the goose that lays all the golden eggs. That would explain stock price lags there.

Bingo…

Ad revenue drives the “ big tech” money…

Porn drives the innovation…

Most of those companies aren’t actually tech. AAPL is a real tech company but ad revenue while large, is a low proportion of the total.

Other companies such as Meta (FB), Google, and Amazon aren’t tech. That’s marketing BS to inflate the stock price.

The demand for technology employment is universal at any organization of any size, but that doesn’t make it a “tech” organization.

That’s partly why Meta and Google were reclassified as “Communication Services”. They’re not in the Tech-Sector ETF with the Computer Hardware and Software guys anymore, they’ve been placed with the cell phone and cable TV companies.

Frankly the official industry classification scheme is crap – these companies shouldn’t be in the same bucket – but it’s what we have been stuck with.

I use Google cloud sevices to back up my devices. Google Docs is software tech. Amazon also invested bigly in cloud services / computing. I’m not sure how significant, but the are tech companirs to some extent.

I notice the data is from the BLS, not the dept of labor. Is it informed by polls?

Umm… Bureau of Labor Statistics (BLS) is part of the Department of Labor.

Whether Federal data reports are informed by polls is a deep question, or perhaps a “Deep State” question. (Keep in mind that the initial data get “revised” a few times before they become final. The early releases CAN be “spun” a bit without compromising the historical long-term record…)

thanks

I wish people stopped talking about the ‘hot’ labor market. Labor lost 4 decades of productivity gains that were exclusively captured by capital. It’s time to claw those ill gained profits back!

Also U3 is a pathetic government created fiction. Labor force participation is at a 4 decade low.

There’s no shortage of labor at the right price point.

Yep.

Now which mouse or mice are going to put the bells on the Big Fat Cats? And how?

Not me, too old, and the rest of my generation has totally bought into the over consumption growth forever model…….but there is always some hope for the younger mice……some.

The market clearing price of labor used to be slavery, now it’s “independent contractors”.

We need a Comprehensive Green New Industry on a Climate WAR footing yesterday, plenty jobs and job training needed to do that.

The capital? Comes from the same place it did during WW2 when our backs were also to the wall……

TAXES. Roosevelt and IKE level taxes.

Lets spread this austerity around a little more.

Here in Australia there’s a lot of hand wringing about a skills shortage, leaving me incredulous regarding government stats. How does that happen without any major new projects being launched? Manufacturing is imploding, where did all those skilled workers that used build Holden’s and operate our refineries suddenly disappear to?

Retired? I notice some older people with skills are not very willing to pass on information for fear they will be replaced by younger people. Granted, I have a very limited view into that world, but it does make me wonder.

That is the opposite of what I was seeing six years ago when I retired. Millennials were actively ignoring the people with institutional knowledge and doing things the way they were taught in college. I remember one kid who I saw on four separate occasions being given exactly the same advice about a (wrong) approach he was taking to a problem and he never listened. Of course, the end results were far below standard in addition to taking far longer to complete as he continued tripping over his initial bad decision. Maybe I’m just old, but deep knowledge specialized to the business is more likely to be accurate than general knowledge preached… uh, I mean taught in college.

Listening is one of the hardest skills to conquer,always listened to grandma served me well

I could easily see that happening, but the best example I’m thinking of is a tech person who built a system no one can figure out because he pieced together antique and new equipment with old and new software and refuses to share info on it or let anyone else work on the system. He will carry any real info on it to the grave.

I see both things happening in that organization. Plenty of solid info on other things that don’t change much is re-collected because no one bothers to look for it in the filing system. People re-inventing the wheel a lot because information isn’t passed on for one reason or the other.

Lynn,

Let me ask you this: Is the assumption that this guy doesn’t know what he is doing, and it has to be changed because it is “old”, or does someone truly want to learn *why* the current system is pieced together as it is and help to maintain it. This goes back to my comment that younger people assume the older people don’t know what they are doing and want to change or “improve” it, reason for the current system, be damned. In reality, these older folks have often forgotten more about techniques that didn’t work than the younger people have even begun to know about the techniques that do. Older doesn’t mean dumber. It means they know where the mines are buried in their current field, and top level strategies for how to navigate through a new minefield they haven’t even seen yet.

As a follow up, I worked in a highly technical field, and whenever I came across something ugly or “broken”, my first assumption was always that those can came before me had a specific reason for why this horrible thing existed. About one time out of seven, the answer was, “oh yeah. I just threw that in there because I didn’t have time to find the best solution.”, but a full six out of seven times there was a goo reason, and one out of ten times, that answer was profound, because they were aware of requirements that I was not. For instance an “error” had to be introduced in the process, because five steps later, another process that was *required* and could not be worked around had a compensating error, that without the first “error” would yield an incorrect result. It turns out that if you worked out the math for the whole process, it made perfect sense. The only danger to the project is that someone who did not *care* would come into the project and assume *they knew better*. This was pervasive among the younger crowd when I retired, which is why I retired at 48 years old. I saw geniuses (that word definitely doesn’t apply to me) being ignored and treated like crap, and I couldn’t take it any more. I didn’t want to work in an environment of ignorance rather than wisdom, which was not a problem among my peers when I started.

Jeff, the first reason is basically budget constraints. That’s how the system morphed into what it is. And yes, there are a lot of work-arounds where things interface. However, most people believe the reason for him not sharing info is job security. That person has managed to retained his job for many decades while no one else has. In the past even the GM hasn’t had the passwords to a lot of systems.

He did give over web maintenance to a younger person a few years ago who just ended up tossing the entire website and rewriting it from scratch. Because he didn’t play well with some necessary info on that either I believe.

He is now retired from the organization, but still won’t share much info and works as a consultant to the organization. He maintains tech to probably 9 separate systems including the phone system. Plus a few mechanical systems which occasionally need fixing. Probably 4 or 5 of those systems interface with each other, but the others don’t.

Don’t get me wrong, he does a great job especially considering what he has to work with, but he is a miser about sharing information.

This is just one example. A lot of people work or volunteer for this organization for social status reasons. I see older people organizing events and not necessarily training younger people to organize with a bigger picture, just giving them parts and pieces. The older crowd is not able to do the things they used to but are confused as to why the younger crowd isn’t always very enthusiastic about taking incentive. I see incentive thwarted. And yes, I do also see younger people who are not willing to learn. I am older BTW. I try to stay out of it, the social status thing is like a feeding frenzy to me.

I’ve been explaining things for about 25 years to our other engineers and technicians. Young or old doesn’t matter. Most people just don’t seem to understand things that are really pretty basic, at a fundamental level. They do understand this at an “if I do this, then that will happen level” though, which is enough in a lot of cases.

I think that all circles back to people not being active listeners. For whatever reason, people’s first inclination seems to be to block out the world rather than to take it in and play with it.

A lot of people manage to squeak by in school/work by memorizing rather than thinking/analyzing.

They really don’t care that much about how/why things are the way they are …they just want to know the minimum (and adapt the least) to get by.

(Usually there are poor to no incentives to show initiative in many, many jobs – so learned helplessness and apathy grow).

If you have ever tried to implement/modify a software system in a decent sized business, you would have seen this first hand.

80%+ of workers have little to no interest/knowledge of how their own job really meshes into the broader workflows of the company.

Understanding requires thinking. Application of thinking is a bridge too far and is painful compared to a deep dive into a bag of nacho chips while playing with their devices. The good thing about them is they do not reproduce very well and the males of that group have declining sperm counts. Mother Nature will eliminate a useless appendage automatically,thinking not required.

Is all of the above “some people this and that” whining unique to people who worked on offices all their life?……Honest question……I never have worked in one so I REALLY don’t know.

Several charts – Professional & Business, Leisure & Hospitality, Retail

and Mfg – reached a climax followed by a sharp decline.

The Construction chart might be in troubles.

There is no info here about gov job opening.

State and local governments: 910,000 job openings, in the same high range for the past 6 months, up by 58% from May 2019.

That’s what we need, more government, that will fix everything……..

Lot of Baby Boomers have retired.

Jdog, that drum is getting really worn out from over use……maybe you should try another instrument…..flute, triangle?

Did you post 58%? Wow!

Yes. Nearly all of them are in education (teachers, school staff, etc.). Real teacher shortage.

Public schools vs Betsy DeVos empires. Sad. I went to all world class public schools in CA (except for a remote fund starved HS)

My daughter-in-law hung it up as a teacher after this last school year. She’s looking to the private side doing consulting with school districts and teaching teachers. COVID years for educators (and students) will only be understood fully in the years ahead. Anecdotally she estimates close to 50% of teachers in the district are at the very least seriously considering giving it up, so consistent with above number. Unbelievable some of the stories she had about conditions at schools once they opened back up. This fall will be really interesting…

@Steve This is all anecdotal, but I see many teachers where I work. I’m curious about everything, and always ask how things are going. I would say your number of 50% considering leaving is accurate. What I hear is that test scores have fallen post COVID. Admin lives and dies by test scores. Pressure on teachers is immense, and there are no additional resources. Plus the students are often still in chaos/covid mode. Mental health is a deadly serious issue for many/most kids, and is a real brake on their ability to learn. It sounds like an ugly simmering stew. These are all teachers from very wealthy suburban communities, with well-funded districts and significantly above-average salaries. Many teachers are burned out/disillusioned, and are seriously looking to leave now even at the cost of losing their pension.

I don’t see recession unless the job market starts tanking/turning.

There were still a whole lot of cars on the road going nowhere over the weekend.

Gas is expensive but not enough.

Everything is going up but people still hitting the restaurants with 18-20% tip added. Just crazy.

Telling my wife to ready for “brace, brace, brace” and stop spending too much. We will see in a few more months where all this is headed.

I am on the side that tend to worry too much.

Better to have a gun and not need it, than to need a gun and not have one, eh…

Can’t fault your logic…

Unless you are weak-minded and lack self-control, or otherwise become mentally reliant on contemplating using the gun as a crutch in situations that don’t require it.

Metaphor, my learned friend, metaphor…

Although I do carry a recent edition of the University Woke Press in my other pocket… you know, just in case… :)

I’ve stocked up on my guns, tinfoil hats, lead underwear, freeze dried food, cash under the mattress, bunker, and tons of gold buried in the backyard.

I reckon that if I need one of these, I’ll need them all.

At least temporarily until I die from the Zombie Apocalypse. Given that I’m nearly 60, I will be the first to become a Zombie anyway.

You sound exactly like me. Sure we may have a “technical” recession but if everyone is gainfully employed why does it even matter? Maybe stocks will drop a bit but who cares if everything you actually want to buy is scarce and expensive.

“if everyone is gainfully employed”

There are still about 1 million fewer people working now than immediately pre-pandemic…don’t swallow those JOLTS numbers too unquestioningly.

*Actual* monthly payroll employment increases have been like 4 or 5% of those ballyhoo’d JOLTS “openings”.

We’ll see what the latest monthly payroll adds are for June. But they ain’t going to be 10 million…the entire US payroll employment level is only about 150 million…with annual increases of 2 to 3 million during “normal”, decent years.

1 million fewer people working ….hmmmm…what could have happened to 1 million people since the pandemic??

According to the latest CDC data, 1.02M deaths in the US due to Covid since the pandemic started.

1M fewer people working? It all makes sense now.

With fewer terminations of pregnancies, we should be back to normal in 18 years.

Or we could just allow more LEGAL immigration and solve the problem immediately.

Tinfoil hat removed…

Just over half of US Covid victims so far have been 75 or older, so I’d look elsewhere for more than half of the missing workforce.

There is a difference between a statistical recession and whether the majority of the population’s economic and financial condition is improving or worsening.

According to FRED, real median household income and net worth essentially flatlined (barely increased) from late 90’s to 2019 while consumption increased. The explanation for it must be increased debt, for someone.

More recently, asset prices are declining (except for residential housing) with real incomes also declining.

So, most people are becoming somewhat poorer regardless that a recession hasn’t been declared.

It’s going to take a noticeable tightening of financial conditions before it becomes a lot more noticeable in the “real” economy. For consumers, that’s more than just rising rates. It’s also credit availability.

This isn’t a mechanical or linear process either but can happen suddenly, just as it did in 2008. I’d expect the biggest difference outside of mortgage credit. Mortgage credit is by far larger but other credit types aren’t government guaranteed.

“ According to FRED, real median household income and net worth essentially flatlined (barely increased) from late 90’s to 2019 while consumption increased. The explanation for it must be increased debt, for someone.”

Or, do you think, the items bought actually decreased in cost or were introduced at a price that provided the same utility thus requiring no more income to provide that base level without a wage increase…

.. i.e, Hyundai/ Kia, electronics, tv’s, super low airfares and hotel rooms, etc…

There was actually a time a few years ago when I looked around and said, “ Jeez, the whole world’s on sale”….

No, I don’t think so. The examples you gave should have been incorporated into the measurement of “real” income.

Most of the increase in consumption is the result of first, more government spending on entitlements which to my knowledge are not included in income data. The USG spent over $20T it didn’t have during this period and a lot of it would have shown up in the public’s ability to spend.

Second, increases in consumer debt.

Forgot to add, maybe increased tax evasion as well. I’m not sure how much the “informal” economy increased during this period and isn’t captured in the data.

“According to FRED, real median household income and net worth essentially flatlined (barely increased) from late 90’s to 2019 while consumption increased.”

“Consumption” needs to be defined to make sense of that. Is the measure of consumption in adjusted for inflation? Does it take into consideration increase in population?

I tend to think negatively about American household debt too (fueled by irresponsible spending), which is why I was puzzled to find that, according to the Fed, “Household Debt Service and Financial Obligations Ratios” (mortgage, consumer) have been at record lows the last two years or so.

What you are seeing now are the beginning of the cracks in the economy.

Retail sales down, auto delinquencies and repos up slightly, GDP decreasing, credit card balances high. All signs that at least part of the consumers are overextended.

Employment is always one of the last indicators to go. The fact that business is having problems hiring also has negative implications going forward as many are having to accept unskilled and low experience workers that will have an impact on their productivity.

Many people are on a psychological roller coaster with government giving a false sense of security by mailing them thousands in free money, and then having to deal with massive increases in inflation, quickly rising interest rates and shortages, and a falling stock market.

The big thing to watch is construction. It is the canary in the coal mine for every recession. Home builder stocks are already showing stress, and when construction goes, it begins the chain reaction which drags down the rest of the economy.

In terms of living standards for most people, it’s employment and access to consumer credit. That’s what enables so many to live beyond their means with the current consumption levels.

Employment market can change very fast and I think it will do so somewhat but not much later. I expect it to be driven by tightening credit conditions for businesses, regardless of how much or how little FFR moves. The two are not synonymous.

I look at interest rates, credit spreads and CDS premiums. I don’t have a subscription service to this data but it’s reported in the sources I read.

Since no market moves in a straight line, I expect in countertrend rally in credit (most noticeable in UST) which I think will last six months to a year. After that, I expect rates to shoot up and credit conditions to tighten drastically. The actual reason is psychological, not event driven which is what most people look to for an explanation.

Tighter credit conditions will also hit stock prices hard which will motivate C-Suite to reduce employment to prop up the stock price.

This is what it will take for consumer credit to tighten noticeably and for most people’s living standards to be impacted meaningfully. Lending standards have been so absurdly lax for so long that it’s been easy for all but the worst credit risks to borrow, even if not at cheap rates.

Millions defaulted during the GFC or filed for bankruptcy. But since the credit mania was still expanding, lenders still lent to these deadbeats because their stock prices were only penalized temporarily and they could borrow in the capital markets at (very) low rates.

It’s all contingent upon whether the credit mania did or did not end in 2020. If it did like I think, rates are destined to “blow out” in the not-too distant future and credit availability for most consumers (who are actually poor credit risks) will decrease, noticeably or drastically.

Employment is one of the first indicators, not that last.

No, employers do not begin to lay off workers until it is clear to them that sales have significantly declined, they are overstaffed, and sales will not pick back up for the foreseeable future. It would be a little oxymoronic to begin to lay off workers before sales declined…..

hmm, might be regional variation. Around where we’ve been traveling and working, there’s been a huge drop-off in the shoppers and moviegoers. Restaurants are doing OK but hardly filled, and even some of our spendthrift friends have been backing off from the high-cost entrees. A couple other friends cancelled trips to Disneyworld and Universal due to the ridiculous costs. And home-buying plans have been way scaled down in our group. Truly, gas and food costs but especially rents and medical bills are really sucking up income like crazy. It’s ridiculous that high medical bills actually add to US GDP but they make people miserable in the real world. (And this with student loans still paused.) My gut sense is there’s still decent amount of purchasing going on in some sectors, but it’s more and more thru credit cards and lines of credit. The financial media often conflates debt spending with spending of actual income and savings but the rise in the former is not a good sign, by definition it’s not maintainable.

Five hundreds years drought in Italy. The Po river look like Lake Mead.

Shortages all over the place.

Today a recruiter called me to open dialog about a 100% remote position. After politely declining I heard something I had not heard before. The recruiter quickly said wouldn’t this make a great second job.

That was the first time a head hunter had put it that way. In the past I have worked two jobs at the same time, it was grueling. Just wanted to post that on this site to see if others had heard of this being offered

WFH for the win! Just don’t be on the grid by name in both places and in any event no a conflicts of interest.

I’ve been working a 2nd part time job for almost 3 years now, mostly on an Uber style thing (work when you want to, but in tech) though I did some contract hourly work in there too. Haven’t heard of recruiters pitching a 2nd gig actively but the level of thirst out there is stunning, the pitch emails are getting crazy, and there are absolutely stories of people holding down 2 FT jobs, usually when they get busted for it, so I’m sure it’s more common than we think. I’m wondering if this was an official company position or just a hard sell, I believe recruiters are paid largely on commission.

The large tech focussed company I work for have a hiring freeze, however we have very low levels of expertise after several key people quit for higher paying jobs. Many of the “replacements” are very, very junior. Too many cooks and not enough chefs.

The shortage of genuinely good tech talent is enormous. If the Fed manage to quell tech opening they will have utterly flattened the rest of the economy.

focussed => focused, apologies.

fo-cussed

faux-cussed

pho-cussed

Phonon Physics

Boomers retired and smart x ers who don’t need the money can be more selective. Makes no sense to work in a woke corp where you are forced to sit through stupid virtue signaling meetings and deal with similarly garbage emails 30 times a day. Brain dead management that were promoted to check a few voxes and scummy HR – no thanks. With stock prices declining theres just no incentive to work for SJW inc unless youre desperate

This is the first time I’ve heard that there are not enough chefs and managers compared to cooks and waitstaff.

I can see this if senior managers/chefs are retiring with their generous RSUs leaving nobody to run the ship or train the new employees.

I have hit a ceiling being a senior cook. I need to apply for the VP Chef position. However, in my company, there are still too many chefs with generous unvested RSUs. We haven’t crashed yet and are doing well.

To be specific by “chef” I meant senior dev / lead. They are not generic “managers”, they are very competent dev who can architect systems.

I see the market is still holding up. This is great! The longer stocks can remain steady the longer Powell will keep hiking for. Each time he will see CPI is still high but that the indicators seem to be bearing up. So it’s okay to do one more.

Keep going Powell, don’t flake out like last time, ok buddy?

Yes, I wonder why folks don’t see this. If the market crashes 3 days in a row 10% each, QT and rate hikes are over. But if the market declines 50% spread over the next five years, with many ups and downs, the Fed is going to keep going until inflation is back down.

Lots of folks aren’t great with pattern recognition. The Fed has dropped interest rates during every recession on record, at least since 1954 per the FRED tool. This even held true during both of the Volcker double-dip recessions. They’ve done it in peacetime, wartime, high inflation, and low inflation environments. However, keeping in mind that the Fed has dual (more like dueling) mandates to keep inflation down while maximizing employment, I think it should be pretty clear that the key events to look for are growing unemployment and recession. If the unemployment rate starts rising and we dip into recession, the Fed will change course pretty quickly. The Fed would have to break from 70+ years of strongly established behavior to stay on the brakes beyond that point. But until then, we’ll only see interest rate hikes and QT on the menu.

I sincerely love your term, “Tightening Deniers.” These folks will be disappointed for some period of time still, but it’s also tough to think that the economy couldn’t take a quick turn and that the Fed wouldn’t be just as quick to pivot. We know the Fed has changed monetary policy quickly many times before, and we know that Powell is capable of taking lightening fast U-turns. A lot could change by the end of the year.

Well said and didn’t it take a lag if a few years to set off 2009?

The markets know this too. 2018 is calling, when is Jay going to answer?

“If the market crashes 3 days in a row 10% each, QT and rate hikes are over. But if the market declines 50% spread over the next five years, with many ups and downs, the Fed is going to keep going until inflation is back down.”

Sadly, I agree. A few years ago we were all told the Fed was independent and didn’t care about the stock market. Apparently we can’t say that with a straight face anymore. It’s repugnant that they give a rat’s ass about the stock market.

You know what will sink the real economy? Oil at 200USD. Western countries are telling Russia that the later is only allowed to sell oil at 70USD. A lot of people clearly haven’t been doing their homework. Firstly, why should Russia do as these countries say? Second, how about Saudi Arabia and other producers? So they’ll have to sell oil at that price as well on the say so of Western countries.

If the clowns at Washington continue along this path, one day oil is $100 and the next it will be at 200. Game over.

If the price of oil skyrockets, shouldn’t the United States, being a net exporter of energy, make some good coin?

“All forms of energy combined, the [United States] exported 23.0 quadrillion British thermal units of energy [during the first 11 months of 2021], which was more than the 19.6 quadrillion BTUs of energy it imported, according to the EIA’s latest monthly figures. … In 2020, the U.S. exported about 635,000 barrels per day more than it imported from other countries, “making the United States a net annual petroleum exporter for the first time since at least 1949,” the EIA has said.” And “the EIA said the U.S. continued to export more petroleum (which includes crude oil, refined petroleum products, and other liquids) than it imported in 2021.”

Probably, as happened in the past, the U.S. would jump at the chance to grab windfall profits, screwing over its allies and more vulnerable countries, in order to maintain political / military / economic dominance in the world.

No offense, but you must be one of those well qualified to run any economy into the ground.

Energy is input to EVERYTHING. That means energy is an EXPENSE item. Windfall profits to energy producers = big loss to everyone else.

The solution is easy right? Everyone can just raise their prices, but that will only work if consumers can absorb the increase, but if they can that means inflation still has ways to go, which means the Fed will keep increasing rates, which means …. please write a 10 page paper single spaced and turn it in next week.

Okay, fair enough. I didn’t mean to imply that windfall profits are a good thing.

One thing that sticks in my craw, though, is when the talking head economic news seemed to be freaking about the economy during a recent period when barrels of oil were getting so cheap.

I had always heard throughout the decades that cheap oil was good for the economy. Then, weirdly, cheap oil was deemed to be bad for the economy for some reason.

Yes, energy is input to “EVERYTHING.” But I get my energy from food and a good night’s sleep. Not petroleum products.

Cheap oil is good, but if the price is too low, it will discourage producers from investing in new fields, new processing and refining capacity etc. When that happens, everyone will be staring at 10 dollars gas.

You say you get your energy from food. If you are living in a modern society, i.e. you get your food from the supermarket, then yes, you are getting your energy from petroleum products … indirectly. Modern farms are operated using advanced machineries which run on petroleum products. Farms also use fertilizers. Guess again where that came from. Farm harvests will need to be transported to the cities. Guess what trucks use?

The modern economy can NOT run without a huge amount of surplus energy. Granted we have other sources of energy in the mix like coal, natural gas, renewables, etc, but petroleum is not going away soon.

I don’t get my main food from “modern” United States style food systems. My wife grows a lot of our food, and the local open air markets in Thailand where we get a lot of our basic foods are: 1) mainly farmers that do not depend on petroleum products, and 2) not dependent on long-haul big carbon footprint transportation.

So, the United States can take their “modern economy” and shove it where the sun don’t shine.

“if the price is too low . . . everyone will be staring at 10 dollars gas.”

Maybe you should check your calculations.

“Energy is input to EVERYTHING.”

My economy runs on fresh air and sunshine because I have solar panels and wind turbines. What I don’t have is asthma or radiation poisoning, so I’m feeling really left out here.

I have a perfectly good heavy-duty fusion reactor and can offer access licensing under very reasonable terms.

@drifterprof, next you’ll say you live in a hut without electricity and plumbing. No? So how have you been replying to me? Are you using your neighbor’s phone/computer? Either way, electricity generation in Thailand comes mainly from natural gas and coal. See? No petroleum?? But those things have to be TRANSPORTED to the power generation plant using what again? Did you say petroleum products? You are right again.

@unamused. If the price is too low …. for too long.

High prices often follow … low prices.

@SocalJimObjects

Yep I do live in a hut of sorts, with non-modern “plumbing.”

However, you’re stretching your original point (i.e., “You know what will sink the real economy? Oil at 200USD.”) into the stratosphere.

The “real economy” here where I live is not dependent on natural gas or coal generated electricity.

The electricity used to communicate with you on this forum is totally insignificant.

Yeah i’ve been seeing this claims about US gaining as an energy exporter but I’m very skeptical. If the US was such a gainer from oil and other exports in 2021, then why did we suffer such a massive trade deficit (and getting worse each year)? Not to mention that since our economy is mostly in other sectors (and the owners and stake-holders in US energy companies are overseas as much as domestic), this just means even higher feeder costs and overhead for the bulk of US economic production. Which means less productivity and higher costs, maybe one of the other drivers of this runaway inflation we’re facing.

“If the US was such a gainer from oil and other exports in 2021, then why did we suffer such a massive trade deficit…?

Not a big gainer, but not a big loser. The massive trade deficit is because U.S. capitalists decided to move their manufacturing overseas in order to maximize profits via cheap labor.

Seems like a great time to get a job or change jobs (if you need a job). It’s the silver lining in this inflationary environment I guess. Even if the new job does not catch you up to inflation, at least change can inspire personal growth and maybe a side dish of innovation from business.

1) Chip shortages might become a glut. 2) Oil shortages, after the EPA declared a war on oil and shut down seven refineries : one in Houston, two in Louisiana, NM, SD, CA and WY, might be over by Nov.

3) SPX might rise to 4,400 – 4,600 in the Q4.

4) The worse might be over for this gov by the end of the year.

This goes completely against what the industry insiders and main economists are saying. There have been efforts to tackle chip shortages but they’re way behind, hence the shortages in new cars (which need those chips). The refinery closures have nothing to do with the EPA, it’s the owners having technical problems or just making better profits with other applications (and of course from high oil prices for the refineries still open). The third and fourth points are contradicted by trend-lines in fact all the data says the opposite, the true effects of Fed tightening have barely begun to be felt. The US will likely avoid recession this year but it’s a very high probability in early 2023. So likely facing a deep recession in Q1 to Q2 2023 (though perhaps starting late in Q4 2022), then a recovery by late 2023. It’s all but inevitable with inflation like this, the Fed’s priority is knocking that down or else the whole economy implodes and we get social unrest.

Also notice where there are significant blanks in the comparative indexes that are crucial to understanding not just what is going on for the US, but the macro view. You’ll find those other indexes on the left black column.

An article on Vox reports that ‘Even bosses are joining the Great Resignation. New data shows a growing number of managers are quitting.’

I’m self-employed. When I talk to myself it’s a staff meeting.

they’re quitting because they got poached by another company with better pay and benefits. That is now everywhere.

The “Great Resignation” is really the “Great Churn.”

The company that gets poached can celebrate the loss of their employees as a cost-cutting measure and boost their stock price. Everybody wins!

It’s funny how that works. Why am I not laughing?

The number of construction job openings is higher than during the peak of the last home building boom 2006-2007. They can not hire enough cheap skilled labor. They can not build enough low priced homes due to out of control inflation.

Immigration continues to create housing demand.

Locally there is a labor shortage in construction because banks funded so many projects. Construction projects are creeping along, not getting done.

People slow down and even stop working to prolong project. Witnessed this first hand. Boss would tell people what to do, then they stopped working the moment the boss left. Boss would come back nothing done.

I was involved in one project where they accelerated the completion despite a labor shortage. It became a project from hell. The building will likely suffer “long haul COVID” as a result, for the life of the building.

I don’t know how long it will take to work through backlog of projects, or if money will run out before completion.

A building nearby had tons of red paint marking deficient block work. I don’t know if they fixed issues or painted over red paint.

“Immigration continues to create housing demand.”

Labour shortage, meet supply.

Folks from south of the border don’t know U.S. building codes or methods.

At the one building site I was at subcontractors were getting stoned and drunk on site; perhaps nothing new.

They were dry walling anything and everything and didn’t let anything get in their way. After about the 5th rework the bosses were getting a little p*ssed.

I.e. is was a money losing project long before it was done.

Don’t buy anything built during COVID, is my advice. ;-)

“Folks from south of the border don’t know U.S. building codes or methods.”

Neither did the developers of the Surfside condo and they’ve done okay. Just deregulate the industry and you’re good to go.

“At the one building site I was at subcontractors were getting stoned and drunk on site”

All such problems are management problems. This is what happens when you hire bargain-basement managers.

Romans didn’t know US building codes either but the Pantheon is still standing, and so are the pyramids. English hadn’t been invented yet so US building codes wouldn’t have been helpful.

I used to pick up folks from south of the border for day labor around 6am at 7th and Red River St in Austin in the middle eighties. They were always ready to work. Had they been skilled electricians as well as indefatigable laborers I would have been asking them for a job in bad Spanish. There’s some in front of home depot today. On a CDC laboratory (government) job in Chamblee, the non-union sheetrockers were all from SOTB. The HVAC and electrical subs were nationwide union contractors and our scale was miles ahead of what they got paid. Even with assessments and dues. But half our crew , men with families, blew off a week’s worth of work to go to Talladega. I didn’t, and noticed that the sheetrockers didn’t either. Over my time in construction I saw less people showing up for work with their head in a jug than was usual several decades ago. At least from alcohol. The painters can still hook you up with bud in the pre-legal states. Anybody doing anything more serious usually doesn’t last long in building trades where their personal problems might get someone else hurt. Even when help is scarce, drunks and pillheads aren’t trusted with anything important and always go down the road first, unless they’re somebody’s brother-in-law.

My shop steward at CDC would bird-dog my projects to make sure that as an organized-in journeyman who didn’t go through the apprenticeship program I wouldn’t work myself out of a job. Fast and efficient is undesirable in the IBEW. Enforced idleness wasn’t my thing, left after 9/11 killed road work. Nobody can coherently explain to me how that’s a good thing.

You are not living on the same planet as the rest of us. Here in Texas construction is ALL done by south of the border labor. You may see a few white guys every now and then but even they have to listen to wretched Tejano music all day. At least play some Latin pop!

E- I let my electrical licences lapse in Austin and San Antonio in ’95 when it became clear to me that indeed I did live on another planet and wouldn’t be back. Enjoy yours, I used to. You do have the best barbeque in the galaxy. Radios are usually not allowed on industrial jobsites and never on a union job. Quite agree about Latin vs tejano. Both would beat today’s hot new country hands down.

I like Mariachi. Was all we listened to on “the voice of Baja Sur” at Bahia Asuncion.

Good traditional folk music, right up there with original Cajun and Bluegrass.

High immigration is maybe not the best idea when huge inhabited sections of the US are dangerously close to getting uninhabitable from water shortages, while the worst housing bubble in US history is raging and young Americans being crushed by increased home prices and rent. Lake Mead is literally drying out–it’s now at the lowest level since they put a dam in the Colorado river and no end in sight. The Salt River in Phoenix is a mess and there’s not enough water for houses in Arizona still being posted at insane prices. A huge chunk of Texas is heading for desert status as our water sources dry up. That’s tens of millions of Americans already living in areas that may soon not be able to sustain housing or infrastructure. Low controlled levels would be fine, but maybe it would make sense not to add to these pressures (and housing bubble prices) with mass immigration? Not to mention the horrible traffic even in more medium sized US cities, wrecking quality of life and health. GDP again is worthless in measuring that, it’s all an “externality”.

But capitalism wants high (legal and illegal) immigration because it results cheap labor. So guess who is wrecking quality of life and decent health care?

‘GDP again is worthless in measuring that, it’s all an “externality”.’

Debt has been increasing faster than GDP for years, so technically you’re bankrupt anyway.

Not to worry, the government is spending billions more on water infrastructure, now that we are in a deep drought and the water is already gone.

Water right lawerys will be getting meg-rich in the coming years, while the people are drinking sand. But not the 1%.

Remember, support unlimited growth by conserving water. Everyone bought that lie hook line and sinker. Myself included until I thought about it. Environmentalists will you know what in their drawers when they figure that out.

“Not to worry, the government is spending billions more on water infrastructure, now that we are in a deep drought and the water is already gone.”

Once again, pubs create the problems and then try to prevent dems from solving them so they can blame the problems they create on dems.

The US has immigration problems because ever since the Monroe Doctrine it has enabled US corporations to ruin their countries. What goes around, comes around, I always say.

Yes, if only Democrats were always in charge, the country would be in so much better shape. We’d be living in a virtual Nirvana.

Both partiers totally suck.

Unamused,

I really have to question your claim that mismanagement of water in the south west is a party-specific issue. California has been dominated by dem legislatures for ages now. That party has supermajority control and the state easily has the resources to solve its water issues, yet the politics of environmentalism and nimbyism have prevented many projects from moving forward or slowed them significantly at great cost. A large desalination project was recently scrapped. The delta tunnels project isn’t going anywhere any time soon. A lot of our reservoirs and infrastructure are leftovers from 1930s WPA projects, and we’ve added almost no new water storage since the 70s when CA’s population was much much lower. Both parties have had plenty of time to address the elephant in the room, but neither has done so meaningfully.

As for water in the southwest in general… We can pipe millions of barrels of oil per day, billions per year around the country, but we can’t move life-giving water from wet parts of the country to dry ones? We can’t make use of already proven desalination technologies? We can’t expand existing aquaducts?