Snowflake reported earnings again, which these IPO companies should be prohibited from doing because it just kills the stock.

By Wolf Richter for WOLF STREET.

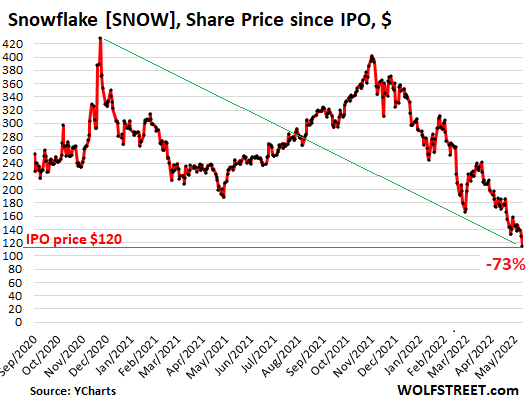

Cloud data platform Snowflake – the Buffett darling, but don’t cry for Buffett, he made plenty of money somewhere else – did another job on its stock this evening when it reported Q1 earnings, in what has become a quarterly ritual.

In afterhours trading, its already eviscerated shares dropped 13.8% to $114.41, below the IPO price of $120 a share. After it’s Q4 report three months ago, its shares kathoomphed 25% afterhours. Shares are now down 73% from the high in intraday December 2020, which shows how crazy this whole thing was back then (data via YCharts):

As part of the pre-IPO wheeling and dealing of the Wall Street hype-and-hoopla machine, Buffett’s Berkshire Hathaway bought 2.1 million shares in a private placement and 4.04 million shares from former Snowflake CEO Robert Muglia in a secondary transaction, at the IPO price of $120 a share.

On the day of the red-hot IPO, fired up by Buffett’s hype-and-hoopla backing of Snowflake, the stock soared and Buffett, thanks to his hype-and-hoopla backing, made $800 million in one fell swoop on his 6.14 million shares. The $800 million one-day gain was widely touted in the press at the time.

Given Buffett’s aversion to IPOs and tech companies in general, “it’s widely speculated that Buffett lieutenants Todd Combs and Ted Weschler orchestrated the Snowflake bet,” CNBC reported at the time.

At the high of $429 a share on December 8, 2020, Buffett’s stake was worth $2.6 billion, and he was ogling a miraculous paper profit of $1.9 billion. If Berkshire Hathaway still holds those shares tonight, all that profit has vanished into the ether whence it came, and instead, its stake is now in the hole by $37 million.

What Snowflake reported today was that it had a net loss of $165 million on revenues of $422 million. Losing so much money on this amount of revenues takes some talent. But revenues grew 84%, and that’s good. The net loss declined by 18%, and that’s good. It largely kept its guidance in line with its previous guidance, and that’s good because otherwise, there might have been another Snap tonight, which plunged 30% on Monday after hours after spooking everyone with its “The macroeconomic environment has deteriorated further and faster than anticipated.”

But even after Snowflake’s 73% shookalacking since December 2020, they still trade at a price-to-sales ratio of 24, assuming the Q1 rate of sales for a whole year.

Data providers this evening still show a price-to-sales ratio of 68, based on 12-months trailing sales through Q4.

The price-to-sales ratio was in the multiple 100s in late 2020. So it has come a long way, and it still has some way to go, and eventually, sooner rather than later, the company will have to figure out how to produce net income. Reality can be a bitch.

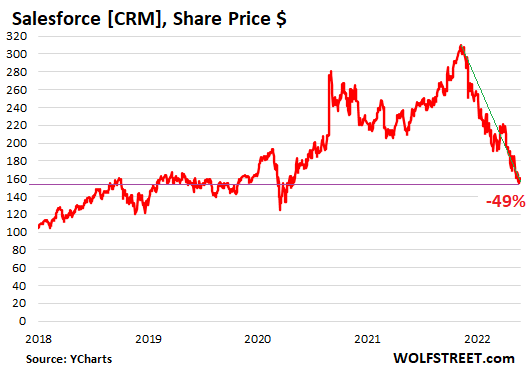

Buffett’s only IPO darling is one of the countless members of my Imploded Stocks. Not yet a member, but working on filling out the application paperwork, is another big investor in Snowflake: cloud-software provider Salesforce, which owns 6.1% of Snowflake, and this widely touted “backing” helped fuel the hype and hoopla in the runup to the IPO.

Salesforce [CRM] dripped 0.8% afterhours today, to $158.40 and is down 49% from its high in November 2021. It’s back where it had first been in September 2018 (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well at least the inevitable train wreck is, for now at least, happening in slow motion.

Better than all at once I suppose…

The Fed is doing a prescribed burn in Unicorn-land. We’ll see if the winds stay calm enough to not turn it into a full-blown wildfire.

The wildfire is coming:

1) No Fed BS runoff yet.

2) Only 75 basis points added to FFR.

3) Housing continues to try to top in terms of prices, then comes the long slide. Rents will not recede meaningfully until we’re in a recession, keeping upward pressure on inflation.

4) Treasury yields & mortgage rates haven’t peaked yet. Keep in mind that the 10YT rose 1% from 10/2017 – 9/2018 due to $50B a month in QT runoff. And only 600B was runoff before the repo market blew up. Supposedly, the Fed made adjustments that should help this time. Now, the Fed wants to double the runoff per month and is targeting $2T. So there’s 95% chance the 10YT runs up at least 1.5%, 75% chance 2% and at least 50/50 chance up at least 2.5% which would put it at upwards of nearing or above 5.5%.

5) Inflation will climb over the summer due to fuel & food prices. And for a variety of factors will remain entrenched above 5% for at least 2-3 years, unless the Fed pushes the economy into a major recession.

6) The war in Ukraine will drag on.

7) A recession probably isn’t in the cards until 1st Qtr 2023 or until housing has dropped 10%.

“Now, the Fed wants to double the runoff per month and is targeting $2T. So there’s 95% chance the 10YT runs up at least 1.5%,”

Read recently that the NY Fed owns 38% of the 10-30 year Treasuries outstanding. I don’t know the pct. of this 38% that is 30 year but it seems like a long time before these mature and disappear.

I wonder who else is buying 30 year Treasuries or if they will continue to exist.

I know Wolf puts the overall numbers in print but a breakdown of ownership by length to maturity would be interesting.

Won’t identify the site I read this in but the gist is that the massive amount of 30 year held by NY Fed is artificially depressing LT rates; which translates to depressing the 30 year mortgage rates. Which, in turn, means when these roll off new 30 year treasuries will need to come with a much higher interest coupon.

It’s not the maturity when issued that matters but the remaining maturity. For example, a 30-year Treasury with 7 years left before it matures trades like a new 7 year Treasury, and they both have the same yield.

So with that in mind, the average remaining maturity of the Fed’s holdings (based on my memory, don’t have time to look it up at the moment) is about 7 years.

Jay, if treasuries were to run up to those levels the budget line item for interest would be close to a trillion $’s. I could be wrong but that would be a budget of about $4 trillion. I don’t see how that can work, hence QE to infinity.

Just wild guessing, but is that avg skewed by a massive amount of t-bills? If so, it’d be nice to have those separated from notes and bonds, and TIPS and then avg them.

If they quit buying now, that isn’t so long before they are out of them.

I mean “most of them”.

I have stopped my pension contribution for couple decades but I resumed since March for buying monthly average on the dip. My bet is this downturn can last for couple years.

Joe

Not with out whiplashing bounces like today and yesterday!

This is Mkt for nimble traders unless you are an investor 45y or below. Then you can afford to it ride thru! B/w $ averaging works great during secular but not during the secular Bear, based on historical record!

Good Luck!

With a name like SNOWFLAKE, what could ever go wrong?

right? thought that was Wolf referring to some overpriced stock in his usual language.

They need to “pull a Meta”, and change their name to “Flake”.

Come on. That’s my favorite insult for us progressive types. Implies easy on others and fresh. I like woke, too….as in the rest are asleep or drugged…..what my buddy calls “insect consciousness”….never ever change (can’t change, actually) and get boring as hell.

A possible upcoming press release?……

“At Snowflake, we pride ourselves on spending whatever it costs to advance our mission of cloud based data storage. Unfortunately, as those of you in the West and Southwest parts of the US have noticed, there are fewer and fewer clouds in these days of long droughts and global warming. So instead of us powering our cloud system with solar energy, disruptor diodes and unicorn horns, we are forced to relocate our facilities to ground level, where fossil fuel prices are higher due to those evil Russians. It is clear to us that global warming and geopolitics are the major causes of our financial misfortune. We are confident that if we pull together and increase our expenditures 100%, we can easily improve our revenues another 84%, and continue our march to cloud data dominance.”

At Snowflake…. spending whatever it costs…

Nice healthy attitude, huh?

Next up for 80% crash is AirBnB, followed by Fortinet and Palo Alto Networks. Holding puts in all three. And Tesla of course. Sold Shopify and Snowflake puts too early (as always).

It is getting harder to find these unicorns. Plan to reload on the upcoming face-ripping rally.

Speaking of AirBnB, I am surprised that the travel companies like Expedia and Marriott are still doing so well. Expedia has dipped recently but they are both still twice as much as their low in Dec 2019. I know that consumers have been switching from goods to services but with Covid still a thing, a stock market implosion, a recession fear and inflation, I am surprised the sector is still going so well.

They will get hit soon enough. Airlines are sucking wind, no pricing power in this stagflationary environment and the same will apply to all these other travel related companies that have insane valuations.

I believe expedia owns VRBO too.

Heard some clown talk up Palo alto networks. Yeah, it’s cruising for a bruising.

Pala Alto has a market cap of $50B, 10X revenue, pays no dividend, and from CNBC doesn’t look like it has ever earned a cent or paid a cent in dividends.

It’s another company with high gross margins but outsized SG&A expenses just waiting for mass layoffs.

Iona

Top 20% of have more than enough wealth from the mkts since ’09, they will travel. Since these contribute to 35% ( of 70% consumption!), certain part of Economy can keep chuggling!

Others NOT so much!

In my area at least, hotel prices are way, way up on pre-pandemic (popular weekend destination near a large metro area). It appears lots of people are still working through their post-Covid travel fever.

I feel so bad for Jimmy Buffet. I want to send some macaroni and cheese to his Nanny.

Haha, Raman soup is more frugal.

Don’t forget he can get a payday loan from his own company or finance a trailer house. Easy lifetime predatory terms.

He prefers “Cheese Burgers in Paradise”.

With Cherry Cola!

You may be right.

Those companies are hugely profitable, if you don’t count how expensive they are to operate.

Eventually, money will flow to less complex enterprises that return actual net profit.

A new acronym: EBITDA&E, adding expenses to the list.

Now everything OK.

Yeah, that old petty cash drawer has one hell of a lot more in it nowadays. Probably needs an accountant and armed guard next to it.

I wonder when all this tech crash will cause a dent in Bay Area real estate prices, specially at the high end, on good quality homes.

Bay Area real estate (the desirable ones) is still strong and rising despite all headwinds, high mortgage rate, tech stock crash, work from home, no immigration, and now layoffs.

If it doesn’t drop in this environment then I guess it will never drop again.

May be all you need might be some patience. The Fed is trying to do a controlled demolition. If done all at once, it might bring the house down.

KPL

Mkts front ran today and yesterday, on the assumption that since 1st qtr is already contracting, Mr Powell will chicken out after 2 or(may be?) 3 hikes and turns around!

Question does the rise inflation after 40 yrs of deflation will be contained by the ‘transient’ inflation team at Eccles building?

Mortgage rates are not even close to high. Are you even familiar with rate history?

This website has chronicled the collapse of numerous individual stocks but there is no tech stock crash now either.

Look at a long-term chart of the NASDAQ or NASDAQ 100. Both are still priced in deep outer space. The overvaluation has been so insane this time (and still is now) that the dot.com bubble peak isn’t an outlier.

It would take an almost 70% decline from the November all-time high to return to the dot.com bubble peak and no, there hasn’t been anywhere near that much real growth in the intervening 20 years to make it reasonable. Remove QE and above trend deficit spending and most “growth” disappears.

Limited layoffs to this point too.

So, there is your answer. Since mortgage rates are not even close to high, there has been no tech stock market crash, and only limited layoffs to this point, this explains why Bay Area real estate isn’t weak, yet.

Wait until the NASDAQ loses 80% to 90%, minimum. It’s coming.

I’d agree with most everything you posted.

The tech stock picture gets even worse when you consider that many of the large cap stocks are leveraged plays on consumer discretionary spending.

Housing, however, remains very much a wildcard.

Non-institutional buyers have been moving to the sidelines over the past 12 months.

But I’d argue that that is being more than offset by institutional buying, and for those guys mortgage financing is a convenience rather than a necessity. Factor in an inflationary picture in which institutions want to reduce cash exposure and the introduction of european instituions onto the playing field (which I think you’re going to hear more about in the coming months) – and I really do think that continued price increases are possible in the housing market despite their being very vew buyers. And that’s despite the home construction business grinding to a near-total halt due to supply chain dysfunction.

From there there are two things (IMO) to watch in the housing market:

#1: Will institutional buying continue to be robust? I think a lot of people are already watching that.

#2: What will be the effect of increasing property taxes on housing supply entering the market? I don’t think a lot of people are yet considering this at all. The pandemic-era relief that was ultimately given to cities and towns enabled cities and towns to avoid having to increase property tax receipts (actual home valuations have increased > 25% over two years in many metro Boston locations – but nothing like that increase has been reflected in property tax bills). But with that aid ending – we could see some serious “sticker shock” in the year. Indeed, this is already affecting Texas.

Don’t be suprised if “Homeowners take out HELOCs to pay property tax bills” becomes front-page news before the next spring!

Depends upon how far out you are looking.

Institutional buyers don’t treat houses as “homes”, as there is zero emotional attachment. In practice, this means they only buy or hold as long as ROI is competitive.

Given the actual awful long-term fundamentals, they aren’t going to be able to raise rents from current levels indefinitely which their tenants can afford. Many here believe or ignore this limitation but it’s there. People will double up (or more) if necessary.

Second, if and where institutional ownership reaches enough scale, there is going to be political “blowback”, such as rent control or moratoriums. There may be one or both anyway without it, but it will be much easier to pass local ordinances with it.

After the precedent in the pandemic, I’d never be a landlord in many states and likely not in any. The government can just make up any excuse to effectively take your property.

Third, it’s likely, to some extent, institutional owners will sell to cover losses in other asset classes, especially if they use leverage or (for private equity or mutual funds) if their shareholders withdraw their money.

I assume in advance that the government will attempt to prevent falling housing prices, but don’t believe they will totally succeed. To the extent they do, longer term it will only be in a depreciating currency.

As the country becomes poorer and credit conditions tighten, prices aren’t increasing in “real” terms. This isn’t the 70’s.

Forgot to add one thing.

If you ever read Charles Hugh Smith on oftwornminds.com, he has a recent post on this topic.

I agree with him that despite my bearishness, he could be right about bifurcation. Where the local market is desirable enough and the supply is limited, it might not matter. Those who remain wealthy enough will “pay up” to “get out of Dodge” anyway.

But this doesn’t apply to the Bay Area or any city of any size in the US.

None of them are even close to desirable enough, even now.

As for later, never mind….

Augustus

Good point on how corporations treat homes. I am guessing it will be like how Simon Properties REIT has treated is commercial real estate. As long as the cash flow is positive, the value of the property does not matter too much as they depreciate it each year. So after 25 years, if the property does drop, it just lowers their basis when they sell and they do not have to pay as much taxes.

Sure it is great if the property goes up in value but it is all about the cash flow.

If the cash flow stops, they just jingle mail the keys back to the bank.

We may see some foreclosures in the future if the housing bubble does cause housing prices to drop a lot, but rent is pretty sticky. I have seen my rental property price drop 40% during housing bubble 1 but my rent I charged only dropped 10%.

Augustus Frost

Houses at 400K are in trouble, especially in the less desired locales. Competition still high at 1 M and above, in desired locations by the top 1-5%!

Honestly, I think it’s doubtful, at least for SFran. Maybe the outer Bay Area might see a bit of a dip but SF, like Manhattan, is constrained from water and California’s NIMBY culture and environmental laws will probably keep demand artificially low.

My best guess is that the second tier cities RE markets might get crushed depending on how layoffs play out. The question is whether companies in the aggregate want to continue with WFH or not. No one can say for sure yet. But if WFH is the new normal, then maybe prices go a bit flat in most markets, with some smaller declines in the first tier cities (NYC, SF, LA, etc.)

Not an expert like Wolf, but these long-term charts make me pessimistic about long term RE prices. https://www.longtermtrends.net/home-price-median-annual-income-ratio/

Either income will buck a tend for decades and actually go up a bunch, we turn into the UK’s housing market despite not living on a island, or prices will go down, somewhere.

Sorry meant to say supply artificially low

Nate,

Huge misconception about San Francisco.

#1. There are very large tracts of old industrial land that are now being redeveloped for housing. That includes the old Naval Shipyards and the Hunters Point area and Treasure Island.

#2. There are something like 70,000 housing units in the pipeline in SF. And there can be many more.

#3. Latest Census figure says that SF’s population plunged by 6.3% from about 870,000 to 815,000 by June 2021. The figures from the State gov aren’t quite as bad, but similar.

#4. Last year, over 4,000 housing units were completed in SF.

#5. Now the tech and startup and biotech sectors in SF are weakening as we speak. The layoffs are already starting. Biggies such as Uber and Twitter have imposed hiring freezes.

So: sharply declining population, labor force substantially below pre-pandemic levels, and rising housing units. You draw your own conclusion about the path of home prices.

I wouldn’t bet too hard against SNOW in the summer.

Berkshire and its friends are probably big enough to make SNOW profitable just by promoting internal adoption of SNOW’s services vs. competitors.

This made me laugh quite awhile:

“Losing so much money on this amount of revenues takes some talent.”

You see what the problem is. They’re all hung up on this outmoded idea of paying their employees. Just stop doing that, go feudal and bring in the selfdom and the corvée and they’ll be golden. If it works for Amazon and Starbucks, it’ll work for Snowflake.

Problem solved. Next!

If you work for low wages that’s on you, not your employer.

Do you think employers should be prosecuted for criminal interference in employee unionization efforts?

I have more questions than you have answers, lots more, so be careful.

Employees should be free to unionize while employers should be free to ignore and not bargain with them.

By logic and common sense, no group can have more “rights” than the individuals who compose the group.

Yes, the same principle should also apply to corporations.

So you don’t believe Corps really are “people” either?

That was a difficult concept for me to grasp, too.

“But revenues grew 84%, and that’s good”

If you are in the business of selling $20 bills for $10, you will have a massive perpetual revenue growth and an infinite addressable market – provided no one gets into the details of the foundational flaw.

Crazy how fast some of those tech stocks dropped.

I am sitting on the sidelines waiting for the Fed to stop raising interest rate before i jump back in. I may be waiting until next year. who knows?

I hope they tame inflation as sitting in cash cost me 7 or 8 % right now

Try 15-20% at least

RU82-

High oil/gas prices aid the Fed’s current quest to “tame inflation.” Same with consumer interest rates.

A Fed pause (as if they’ve made heroic efforts thus far!) could be in the cards if energy consumers finally translate high fuel/ borrowing costs into delayed gratification decisions on other stuff, including homes, cars, and all the smaller stuff. What would pause do to stock valuations in the short-run?

I find it hard to to be 100% out of the market, even though sidelines are the comfy place to be. Might be wrong, but I’m guessing you’re not 100% “out” either….

True. I am 100% out in my 401k and rollovers. There are not any good options to invest in.

I am about 75% out in my taxable accounts. I am actually up about 6% this year as I have only bought oil and commodities since January.

I figured that it was hedge against any commodity spikes / Inflation that Larry Summer kept blabbering about last fall.

But mostly I am just buying options to risk any big 25% stock drop surprises we seem to see these days.

WSJ mentioned the housing vacancy rate is at a 66 year low. They did say the “for sale” inventory is increasing, specifically for new homes. Also, Some home buyers are throwing in the towel.

What is crazy is In the article one home builder plans on building 1400 homes over the next year and plans to sell them at an average on $625k. Who has that kind of money if interest rates keep rising?

I did read another article that mentioned some companies are actually building homes for their employees. They will let the employees rent to own the homes at the cost to build. Novel approach to entice and hire new workers. By cutting out the builder and hiring contractors directly they can build affordable homes near the workplace. I guess Disney and JBL (meat packing plant) are a couple of companies doing this.

Not all that novel, my wife’s grandparents worked in a SC mill-town, the mill provided rent-to-own homes and a large plot of land to grow vegetables. When they retired they owned the home.

Company housing will be thing once again. I know of one getting started in a high housing cost area, and they only have 300 employees. So it is not just the big companies doing this.

Hiring skilled workers(not office work, but makers of real things) in a high cost living area has become very hard when there are no places to live within 30-50 miles. Interviewees like the job and the area, their spouses like the area, the salary is an increase, BUT they can’t find a place to live and turn down the offer. Rinse/repeat.

Reminds me a little of a local 1880’s lumber company who payed employees in company scrip, spendable at the company store? Creative labor solutions, but ultimately temporary — the company folded, and the scrip went the way of all paper money and is worthless.

My sheet of uncut scrip sure looks pretty framed on wall flanked by a Zimbabwe 100Trillion dollar bill and a 1Million Lirasi note, though…

PALCO?

Visited wife’s relatives at Pacific Lumber Co. in Scotia 70-72. Shacks with 2-3 bedrooms. Gravel everywhere there wasn’t a house. Inside all wood panel (natch), with Weatherby 270s along with old 30-30s, even 45-70s and 90s on the wall. Also with trophy buck heads and fuzzy pictures. Out side big 4WDs and some motocrossers.

Whistle blew, they all walked home for lunch, whistle blew, they headed back. I liked the nasty ass high-pressure water log peeler (hydraulic lifters/rollers just threw 3ft logs around like toys…noisey….fully inclosed with thick windows) and old steam donkey in front of store best. Otherwise it was just another mill, same sequence, just HUGE with a lot more people at each station.

They all seemed pretty happy, especially since most mills in Mendo had closed. Planned yearly vacation trip to Modoc, maybe even Wyoming. Not sure what wives did….watched kids and cooked, I guess.

This outfit brought logs in from the “lost coast” where they decided not to continue Hwy 1 on through. (It stops north of Ft Bragg, starts again in Eureka) even though they originally wanted it up the whole CA coast. Probably ran out of money.

Anyway that might have been your “PALCO”, sounds like it, a steam donkey is sure 1880 stuff.

Oh yeah, managers houses were on hillside behind store….you could tell rank by size, just like the Army.

I’ve been about 20 mi up that “Lost Coast”, trying to get to Shelter Cove, (on CA Rt 485?). Shelter cove has a road in from 101 and is all rich folks like the Sea Ranch, I think, airstrip, etc, but had to turn back when I hit a downhill place with huge grader ruts. (April 08?) Passed nice campground on little beach with couple campers, and several dirt roads with locked chain or bar gates.

Guess my point is it’s way better than Idaho or any other place for rich and poor preppers/survivalists. Tons of water, food, in the ocean and the hills, and no worries about freezing.

Just a real hot tip if you are one.

You move 16 tons and whaddaya get

Another day older and deeper in debt

St. Peter don’t you call me cuz I can’t come

I owe my soul to the company store…..

Company towns were like that: the owners made sure to charge you more at the company store than they paid you. A clever way around the 13 amendment, eh Sven?

Of course, nowadays they’ve scaled it up and extended the paradigm nationwide. Hey, robber barons have to eat too, don’t they? And they’ll suck out your soul for dessert.

Remarkably enough, US employees were prohibited from suing their employers in the 19th century for any reason, even for unpaid wages, and their testimony was deemed inadmissable.

My baseball cap says “Eh Sven?” Long story. Rather humorous.

Yeah, a “Company Country”…..wait till vagrancy laws are back again…..the rich have pretty much undone all the work of both Roosevelts and dumbed down Calvinistic peasants are fine with it all.

Flag with corp logos instead of stars coming soon.

Just wait till the wealthy promoters/investors of all this at this website discover they ARE NOT along for the ride.

“Flag with corp logos instead of stars coming soon.”

It’s been done. Google up File:American corporate flag.jpg.

Sold out. Sorry. Get back to work, NBay, and keep your shoes on.

I owe my soul…..to the company store!

Except in a bubble economy and manic market, SNOW isn’t going to grow to even this reduced valuation to become reasonably priced in my lifetime.

CNBC shows market cap at $41B+ as of yesterday’s close. Fiscal year 2021 revenue at $1.2B. Once again, another company losing money mostly or entirely due to SG&A, meaning it needs mass layoffs to right size.

I was reading the CNBC article on its afterhours performance yesterday which discussed the data querying software more than cloud but regardless, it doesn’t add up to a $41B market cap or anywhere near it.

If it’s primarily a cloud provider, that’s a 21st century utility.

Their revenues vastly exceed their Cost of Goods Sold, so they’re profitable there. Unfortunately their Cost of Services Sold is, ahem, in the clouds.

I can’t get misty-eyed about clouds, but maybe I’m missing something.

Hmmm. Must analyze:

Rows and floes of angel hair. Ice cream castles in the air. And feathered canyons everywhere. I’ve looked at clouds that way. But now they only block the sun. They rain and snow on everyone. So many things I could have done, but clouds got in my way.

I’ve looked at clouds from both sides now. From up and down, and still, somehow, it’s clouds illusions I recall.

I really don’t know clouds at all.

This made me smile. One of many amazing songs by Joni.

“Good afternoon ladies and gentlemen, this is your pilot. Thanks for flying SNOW Airlines today. Both engines are still on fire and we are headed for ground impact. However, there is some good news, due to the wreckage on the engines, our indicated vertical air speed has reduced from 345 MPH to 323 MPH. SNOW Airlines will issue you discount vouchers for your next flying adventure.

At least they could give you free in flight wifi…. pikers.

Saw the “stand up seats” AirBus patented well over 10 yrs ago. Have a little kinda “butt bench”. Might be better for long legged folks like me, they get real tired of people loitering around in back by the bathrooms and stewards stations.

When I was in my mid-20s, I went to the Volksoper, the famous opera house in Vienna, to see a 4-hour Wagner opera. At the time, the cheap seats (the only ones I could afford) were standup “seats” in the back. But you were not allowed to slouch with your arms on the railing in front because every time you did, the usher would come by and politely remind you not to. Not sure if they still have those standup seats, they seem too inhumane now. But standup seats have been around forever.

But let me confess: that sit-down beer afterwards sure was wonderful!

The Dow is now up 526 points at 9:04 am and oil is up $4.01 to $114.33 and profits should be great for the price gouging Dow 30 this quarter and the index may head toward 100,000 as Davos declares no recession in sight at all Happy days are here again!

Just to slightly change the subject (just for Wolf) back to stimmies…

here in the UK we are giving out stimmies (for heating) to every household of between £400 and roughly £1050 depending if you are really poor,(£1050) a pensioner(£700) or loaded (£400)

Quite a contradictory juxtaposition of headlines today in Google News:

Reuters: Global shares rally on relief after Fed minutes…

CNBC: Fed minutes point to more rate hikes that go further than the market anticipates…

Stimulus after covid in US:

“To put COVID-19 spending is perspective, the inflation-adjusted (dollar) cost of World War II for the U.S. is estimated to have been $4,100B to which we can add the inflation-adjusted $114B cost of the Marshall Plan to reconstruct Europe. That $4,214B ($4.2 trillion) spent on WW2 compares to $5,740B ($5.7 trillion) the U.S. appropriated for COVID-19 in one year Mar-2020 to Mar-2021.”

– (Barry Bannister, Stifel, Research report 5/24/22

The DOW has moved over 2,000 off the recent lows. It seems all the money is still sloshing around, just moving from one speculative asset to another. The FED should raise by 100 basis points next meeting. There is way too much speculation out there, and all the recent blather about inflation peaking is nonsense.

Think the late-in-day PPT interventions has pushed things off lows to avoid that dreaded ‘Bear Market’ moniker. Assume a lot of algos would be forced to sell, especially at the big institutional level. That’s when we would have limit-down days and the whiff of panic.

TPTB know that reckoning day/week is coming. Like the last twelve years of fake fantasyland, they kick the can again.

A couple of years ago I had a decision to make.

I had a pile of money that needed to be invested.

I picked banks thinking the future had to be better

and my advisor picked science and tech.Well banks worked out but now or sometime shortly science and tech

has a good chance of making a comeback.

Watch your charts as the truth is usually there.

Keep using that small ‘t’ in truth, cuz the larger T is that this is a Fed market and they are buyer of first and last resort. Truth in an EBITDA era is that Valuations mean nothing.

Don’t go out on the beach now. That’s not the tide out, it’s the Tsunami getting ready to come back in.

If the “truth” is just constantly getting wealthier, I’d rather pursue it as a card counter than chasing charts.

Snowflake, a cash burning cloud computing machine that couldn’t make a dollar during a period in which cloud computing volume has exploded. Peloton, a cash burning maker of exercise bikes that couldn’t make money even while everybody was ordered to stay home, gyms where shut down, and bored Americans were handed thousands in cash. Zillow, a cash burning real estate outfit that lost a huge amount of money during the hottest period of house price increases on record.

If these companies can’t make a buck under the most perfect business conditions ever experienced in their respective markets, then how are they ever going to cut a profit? Answer: They’re not going to, ever. But but but, Amazon focused on growth over profit for years, and it worked out great for them… Yeah, and there’s pretty much only one Amazon. The vast majority of their tech-bubble-era competitors disappeared.

I don’t know how much longer these zombies gorging themselves on investor cash and debt can last, but it’s clear that it won’t be pretty when the investors dry up and new debt becomes too expensive to roll the old debt into.

Mkts have zoomed (front running) today and yesterday, on assumption that Mr. Powell will chicken out after rate hikes of 2 or may be 3 and make a U turn just like in 2018! The rate at which Mkt tantrum began in 2018 was 2.75%

I doubt that Fed will be able to control spiking inflation after yrs of deflation!?

This is purely traders’ mkt with (nimble) option trading both ways with hedging!

All of a sudden I’m seeing financial articles almost declaring the end to inflation and the FED rate hikes. “Muh transitory” is alive and well, apparently. But as Wolf has pointed out, that’s not how inflation works. It takes YEARS to get it under control. It seems denial and hopium is running through the veins of all the speculators. Even housing gamblers are talking about the FED “chickening out” or some such, and that their leveraged shanty is going to turn them into the 2nd coming of Elon Musk.

I lived in Tucson in the early 90s and frequented a bar named “The Shanty.” In light of current market conditions “The Leveraged Shanty” is a much better name.

The articles I’m seeing aren’t “almost declaring the end to inflation”. They’re talking about OTHERS who think that’s possible, and are reading the carefully worded Fed minutes and looking into the tea leaves to get that. It’s just jabber.

That said, I am skeptical the Fed will clamp down very hard, and that may make markets happy as that comes to fruition. However, it will be because the Fed doesn’t want to overshoot, and because the collapse in various asset markets will convince them to pause and see how inflation comes down over more time.

If the markets are assuming Powell will chicken out shortly, then this gives the Fed a great opportunity to regain some lost credibility by continuing to fight inflation. If the Fed pivots too soon and inflation remains rampant, the loss of credibility may be impossible to overcome for a very long time. I would argue at that point a new Fed chairman will be required to fight inflation. The Fed is certainly aware of this possibility. The market is already throwing a tantrum and there is no indication the Fed is changing course. Maybe this time will be different.

I certainly agree this is a trader’s market. It’s still too high to invest for reasonable long-term returns and shorting is always risky.

Free cash flow up 500+ percent y/o/y. Such a disappointment!

500%… Wow. If “free cash flow” goes from $0 to $1 it’s up by INFINITE %, even more wow!!!

Been in management in the software industry for 40+ years. Since the GFC the industry has focused on making sure sales are accelerating at unbelievable rates and then paying their sales force and executives through stock options.

They are able to hire extremely aggressive and talented salespeople because all the sales sharks know this is the best ocean to hunt in.

But, Wall Street has been happy to accept earnings reports that do not include the value of the options granted (referred to as non-GAAP financial reporting). So, on a non-GAAP basis these companies can look profitable because they don’t include all their compensation costs, which are huge.

The poster child and originator of all this is Salesforce.com and their shady CEO, Marc Benioff.

I’ve thought for the last 10 years that the SaaS house of cards will eventually implode, but so far they have been able to keep all the plates spinning.

So their BI Platform is smoke and mirrors???

Their stock price is. And their business model is, if they cannot be profitable at this rate of sales.