In October, Upstart was worth $35 billion, according to the collective idiocy of the hype-and-hoopla stock market. Now down to $3.6 billion.

By Wolf Richter for WOLF STREET.

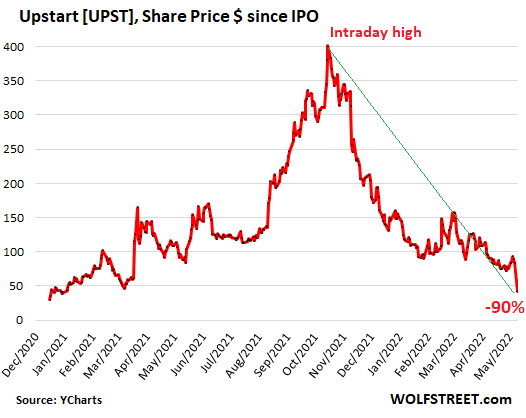

In normal times, you’d think that the 45% afterhours-plunge in the share price of a stock would look like a massive cliff dive in a chart. But these are not normal times, and the 45% dive that Upstart Holdings performed tonight after reporting earnings looks like a small-ish step down from, well, the stratosphere.

The round-trip was quite something. Following its IPO in December 2020, at $20, the shares [UPST] became a meme stock and on nothing but cloud-AI-hype-and-hoopla spiked by 1,900% in less than a year to $401 intraday on October 15, 2021, and then the hot air was let out, and the descent was brutal, and today hit $42 afterhours, down 90% from the high (data via YCharts):

The company sells cloud-based software that uses “artificial intelligence” to make consumer lending decisions. It sells this service to lenders and has attracted some smaller lenders, but not any of the big banks, which use their own systems.

Tonight, it reported that it actually made a little money, 34 cents a share, on 156% growth in revenues of $310 million. So that’s good.

But it cut its outlook for Q2 and the whole year, across the board. For Q2 is expects a month-over-month decline in revenues and net income ranging from breakeven to a loss. For the whole year, it cut its revenue forecast by 10% from its prior forecast, to $1.25 billion.

“This year is shaping up to be a challenging one for the economy,” it said in the earnings report. In the earnings call, it threw some cold water on the entire lending environment, as interest rates have started to spike.

Given the surge in interest rates, “on the margin, a whole bunch of people that would have been approved are no longer approved,” CEO Dave Girouard told analysts during the call.

“So there’s a whole bunch of loans that just never happened at all, and there’s a bunch of people that are still approved, but the interest rate is a few percentage points higher, and a certain fraction of them are going to decide that’s not the product that they want,” he said.

And delinquencies have begun to rise from the “unnaturally low” levels as the stimulus payments have faded, said CFO Sanjay Datta.

“Given the general macro uncertainties and the emerging prospects of a recession later this year, we have deemed it prudent to reflect a higher degree of conservatism in our forward expectations,” Datta said.

OK, fine. It’s getting a little tougher out there for consumer lenders. At least this member of my ever growing list of Imploded Stocks is a company that made a little money in Q1, though it may not make much or any money in Q2. But what is a company like this worth?

At the peak last October, the company was worth $35 billion, according to the collective idiocy of the stock market, 25 times the company’s expected revenues of $1.25 billion this year. It’s now worth $3.6 billion. The remaining $31 billion just vanished back into the ether from where they’d come during the hype-and-hoopla phase.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

At this point it’s like shooting fish in a barrel! I wish I was able to participate in this shooting gallery, but alas I’m just a rubber necking to get a glimpse at the car wreck.

Another IPO disaster is lightspeed commerce Inc.

I’d have a good chuckle if the fed capitulates, cuts rates and restarts QE.

At that point I’m sure these dumpster fires would shoot back up like a missle in the short squeeze of short squeeze.

If ARKK ever stops dropping for a week straight, I might pile in 20k to take that chance.

A good idea!

You might as well buy your reduced priced cars from your friendly neighborhood lot! In other words, not in your dreams Azani!

It’s like this is your guys first rodeo.

Things won’t go down forever and this time isn’t different.

I’ll probably wait for the long term treasury short squeeze, and use some of my winnings to buy arkk at all time lows just before the fed reverses course on tightening. :)

I think gold bugs suffer from such PTSD with markets going up that they have the financial equivalent of beer muscles. Lol

No one has to be a gold bug to concurrently believe ARK holds overpriced garbage. By overpriced, I’m referring to right now, not anywhere near the peak. There are no actual “disruptors” and hardly any actual “tech” in that list of holdings.

“Things won’t go down forever and this time isn’t different”

So I watched CNBC for a while and this one talking head said, “betting against the stock market is like betting against the whole human race”.

Draw your own conclusions, but I’m glad actuary tables say I’ll be dead in 5-10 years. Really sorry about those left behind with the “free market” in charge.

You sure you would want to put money into ARK?

Cathy Woods said oil was going to $12 and Bitcoin to 1 million

She might have just got lucky because of Telsa and covid.

You take Telsa returns out of the fund over the past 5 years and I am guessing the rest are negative.

I follow closely two high paying small cap dividend stocks very closely and invest in them from time to time. Both have been public around 20 years

Stock #1 Largest on-line Pet pharmacy. Q/Q and Y/Y sales and profits down.

Stock #2 Largest Outlet mall sales and earnings up Q/Q and year over year and bumped up full year guidance.

Maybe we are over supplied in on-line retailers and need a big washout.

Walmart and Target stocks are not cratering like the online retail ones are.

They’re massive ecommerce operations with massive growth in their ecommerce sales, eating into Amazon.

And they’re also massively into groceries, which are largely non-ecommerce items. Walmart is the largest grocery chain in the US.

re Big Washout

That is the nice thing about taking some time to periodically review macro stats – they provide crucial context about the sustainability of micro trends/individual stock prices.

And they usually take less time to analyze (versus 4000+ individual stocks).

They provide a reality check.

So, if the whole economy is shrinking at a 1.5% rate (despite massive money printing) and some 10 billion plus revenue company has a 40+ PE implying an earnings growth rate of XX% per year (in perpetuity), how can those two facts be reconciled?

That is the kind of analytical clarity that reviewing macro stats provides.

It is calming in its way…because it cuts through the thousand points of hype for so many individual stocks.

Cas127,

The decline in Q1 was caused by a huge spike in the trade deficit (that will likely reverse) and reduced government spending.

Consumer spending and business investment showed very solid growth.

There is a reason why I publish detailed articles about this GDP stuff:

https://wolfstreet.com/2022/04/28/gdp-sunk-by-trade-deficit-result-of-globalization-drop-in-government-spending-consumers-held-up-despite-raging-inflation/

Worth? Depends on your calculation. IMO it’s intrinsically worth $0:

A. Replacement value = $0-?

B. DCF = $0 = Net Income of ($4) to $0 million x ???

C. Comps = $3-7B

Outside of mania conditions, agree it’s worth $0.

There is nothing revolutionary about loan underwriting models. The only supposedly “revolutionary” aspect in these “fintechs” is that they are applying sub-basement underwriting eligibility criteria. That’s what the quotes in the article imply or state.

It’s not much different really than targeting the traditionally unbanked as a market opportunity. There is reason these people haven’t bene targeted, except to extract fees from them.

They are broke and usually have no money to “invest” or to gather retail deposits. They have limited or no credit history or if they don’t it’s negative.

It’s been my inference for a long time that, at least among the larger banks, most would prefer to dump the majority of their retail customer base as depositors and in many instances borrowers too because they aren’t sufficiently profitable.

They can’t because of lawsuits and bad press. An example is the media report when First National Bank of Chicago attempted to impose a $5 transaction fee (back in the late 80’s or 90’s) for teller transactions. It didn’t last long.

This is assuming no margin was harmed in the making of this Kathoomphal.

“The remaining $31 billion just vanished back into the ether from where they’d come during the hype-and-hoopla phase.”

I just saw the pets.com mascot on CNBC saying to buy the dips.

I wish there was a “Like” button.

If there was a CNBC back in 2000, I don’t doubt Pets.com would have been spending the last of their cash on CNBC ads before they went bankrupt.

Instead, the poor mascot died after being excessively exposed in Super Bowl ads.

And…it’s gone.

I am so waiting for the 4 month lag of tech stock implosions to the San Francisco housing market drippy correlation to take effect.

Fed will cut rates shortly here, so housing will just carry on as per usual

In your dreams. The FED is not cutting rates, they’ll be raising them more.

Don’t fight the fed because they fight dirty!

Depth Charge,

Maybe Peanut Gallery is spending too much time on ZH, and it’s getting to him :-]

How long will it last? At this point I think you need to bet how high the feds funds rate will get VS what the bond market already priced in before things break.

I think by end of September is when something happens.

On the bright side, maybe interest rates will stay high enough for long enough to kill off a bunch of these zombie companies.

If the fed capitulates before then, it’s game on, start up the music and fill the punch bowl and get to dancing!

Rates are going up on the long end no matter what the Fed does. Inflation will force buyers of this debt to demand a higher inflation premium on the bonds. Thats means lower prices and higher yields.

Depth Charge, that comment was solely and exactly precision-made just for you

And you bit!

…but sort of disappointed in this lackluster response. i was hoping for more

Of course housing is going to go down

IMHO housing market will be propped up by other means (other than Federal Reserve halting interest rate increases). Government has various options to prop up the housing market (increase mortgage duration to 40 or 50 years, make mortgage interest tax deductible, allow interest-only mortgages, and so on). So my bet is that Federal Reserve will continue increasing rates, and government will take some of the above listed measures to defend the housing market. This will result in the sharp declines in stock markets, stagnation of the housing market, and strengthening (in near term) of USD. Just my private opinion…

These times remind me both of 2000 and late 2018.

1) In 2000 tech stocks crashed after inflating in the DotCom bubble. It took the Nasdaq QQQ over a decade to recover to 2000 levels

2) In late 2018, stocks plunged after the Fed raised rates and were implementing QT. In early 2019, the Fed drove rates to 0 again and stocks continued their wild ride up.

In both 2000 and 2018, there was not rampant inflation.

Will the Fed save the market like they did in 2018 by reversing course and driving rates to 0? Will mortgage loans catch on fire again as house purchase demand increases causing UPST to increase 1000% again?

The Fed has a decision now:

1) Should they shut down inflation by raising rates to save the Boomers on fixed income?

2) Should they shut down the stock market drops and save the Boomer pensions which are heavily invested in stock?

I think they’ll do both. Let inflation continue at a slightly higher rate and let some of the air out of the stock and housing market bubbles.

Be prepared for higher than typical inflation and lower than typical stock and housing price increases.

I think they call this a soft landing.

2banana,

First signs are already happening. From Compass’ SF office (which they acquired), in my email today:

“Accounts of less crowded open houses and fewer offers on new listings are becoming common; some buyers are dropping out or becoming more selective; some sellers are moving listing dates forward; in many markets, declines in listings going into contract are occurring. Note that not all agents are reporting changes in client plans and motivations.”

“Absent an economic disaster event, major shifts in market conditions, especially from a superheated market, often begin very gradually. For example, an initial shift to a new listing receiving 2, 3 or 4 offers instead of 10 to 12 might not initially affect sales or sales prices, but if that changes to receiving 1 offer (no multiple-offer overbidding) or no offers, the supply and demand dynamics between buyer and seller start to shift quickly.”

” an initial shift to a new listing receiving 2, 3 or 4 offers instead of 10 to 12 might not initially affect sales or sales prices, but if that changes to receiving 1 offer (no multiple-offer overbidding) or no offers, the supply and demand dynamics between buyer and seller start to shift quickly.”

That’s the point I made in a previous article. It’s clear that stock market implosion is reducing some people’s down payment and higher interest rates will also force people out. The question is given the pent up demand and low supply, will we ever reach 1 or less.

In some ways this is like Covid’s R0 number. The initial Covid strain had an R0 estimated around 2. The latest Omicron is estimated around 12. Applying this to the housing market, the housing mania R0 may have dropped from 12 to 4 but will it continue to drop or will there be another surge?

People are WAY too impatient when it comes to RE. They want instant gratification. You’re not going to get it. It takes MONTHS for trends to become clear. But you can see signs in some of the underlying details.

“ dropped from 12 to 4 but will it continue to drop or will there be another surge?”

Nope…

The grownups are showing up….

Josh-

There is no pent up demand and low supply. That’s a canard that the real estate industry keeps peddling in order to justify the massive price increases in housing, rather than acknowledge it’s purely a function of the Fed’s monetary easing.

Wolf has had a previous post showing that the number of units constructed has exceeded household formation for the past several years:

https://wolfstreet.com/2022/04/19/a-housing-shortage-amid-a-building-boom-that-outruns-household-growth/

That means the fundamental supply / demand curve points to an *oversupply* of housing in the past few years and for the past several years moving forward. The only reason prices are still increasing is because of the Fed, and now that the Fed is reversing those policies, housing will face that double whammy of increased supply vs demand, and Fed policies being reversed.

Wait till I have a chance to post the latest population data for California and its biggest cities in 2021. I have no idea where this myth of a housing shortage comes from. Populations declined again. Amid lots of construction!

There is a shortage of affordable housing because prices shot into the sky, and there are a gazillion homeowners who bought a new home and haven’t put their now vacant old home on the market, but they will eventually, and there is the Airbnb effect…

How much of the “pent up demand” is from people wanting to buy because they think RE will go up?

And if RE stays stable or declines, how much demand will disappear? (And how much supply will appear, because RE investors think it’s the peak?)

A quick point of reference for the Bay Area housing market: A good friend of mine just put up for a sale a nice 4-1 in a very good neighborhood, only 10 minutes from downtown San Jose, and mere blocks from highway 85(largest Tech job corridor in the south bay). Two months ago this home would have sold for 1.6-1.8 million dollars, probably within the first day or two. His agent(older, very experienced) advised him to put it up for 1.5 and so he did. After 4 days on the market, he received ONE offer for 1.45 million. Apparently the family that made the offer works in Tech and is using a 5 year ARM mortgage. So if that isn’t a sign of trend change. . .Idk what is. All we’ve had in my area for the last 5 years has been absolute insane mania. The FED raises by 0.75% and it’s like boom, completely different market. Thing could shape up to be a really mess if the tech sector sees ANY layoffs.

This would get interesting once it gathers speed. Then we have got 2000+2008+the big bad man – inflation.

Will something break by end of this quarter?

Then the bulls can salivate at the printing that the Fed would do to stop this.

Another big factor affecting housing prices in cities vs suburbs and far out areas is the price of gasoline. Long commutes are suddenly a no no, and not everyone can WFH. This happened back in 1979 during the Carter era with high gas prices and gas lines. People then started moving back to the cities so as to benefit from public transportation and short commutes, bicycling or walking to work. See this scenario repeating again. The DC Swamp real Estate market, especially Condos is booming like never before in spite of the spike in interest rates.

Bingo! All the talk was about people leaving the cities blah blah blah… Back in the day I lived in the country 75 miles from my job and when gas went way up (2005-2008) I just couldn’t do it any more. People have very short memories and they think how things are NOW is how they are going to continue.

A correct NATURAL interest rate is all the intelligence a lender needs. Correct interest automatically rejects dubious or frivolous loans.

Artificial intelligence is only needed when the interest is artificially low.

This company is being put out of business by its own AI. In other words, loans to most of these current would-be borrowers suck (In my opinion, say’s Hal).

AI suggestion: Sub-Prime loans are where it’s at now.

It’s not actually artificial intelligence. That’s marketing BS. intelligence implies being alive. It’s actually “machine learning” which is the other term commonly used.

And the problem with machine learning is that it’s interpolation, e.g. it’s trained based on the past. When big things change (e.g. inflation changing the Fed’s policy), and the past data doesn’t account for that, it has the potential to blow up big time.

Its actually an automated pattern / rules matching.

Programmers (human beings) develop an algorithm of sifting through the data and picking the desired cases. Giving this algorithm (as set of rules) to human operators is inefficient because humans are very slow in processing data, and are highly prone to errors (lack of attention, emotions etc.). So algorithm is “coded” (expressed in some programming language) and given to the machine for execution. The role of the machine is not to think or learn anything but simply execute these rules at a very high speed and without any computational errors. All the intelligence that was involved into this process is human; machine just computes. There is no AI.

AK,

You said it better than I did. No, there is no learning. There will be no future “Terminator” world.

“Artificial intelligence is only needed when the interest is artificially low.”

Synonyms & Antonyms for artificial

Synonyms

affected, assumed, bogus, contrived, factitious, fake, false, feigned, forced, mechanical, mock, phony (also phoney), plastic, pretended, pseudo, put-on, sham, simulated, spurious, strained, unnatural

“AI for lending decisions”

WTGDF is that????

I can believe someone thought of it. I can believe someone wrote the goofy ass code. I can even believe that someone sold it. I just can’t believe anyone bought it.

It’s another symptom of the mania.

The whole concept of these supposed “Fintechs” is also BS.

Reminds me of the dot.com bubble when my prior employer bought this leasing company supposedly for its leasing system.

The system was a complete piece of garbage and was inferior to the credit risk infrastructure the company already had for its other lending businesses. They should have built it in-house and saved a bundle.

These “Fintech” companies are either service providers or unregulated lenders. As unregulated lenders, there is the possibility they can be more competitive versus ”

legacy” companies but given the basement lending standards already in the market now, the primary competitive “advantage” they have is to make a large volume of even lower quality loans really fast.

That’s the best way to demonstrate “growth” in a mania.

“At the peak last October, the company was worth $35 billion, according to the collective idiocy of the stock market, 25 times the company’s expected revenues of $1.25 billion this year.”

Amazing how the housing follows. Soon you will hear:

“At the peak last October, my house was worth $1.6 million, according to the collective idiocy of myself, my neighbors, and Zillow 16 times the expected yearly earnings of working families in my area.”

Yep, all this destruction in stocks foreshadows what’s coming to housing. It will take some months before the fake news media admits housing is crashing.

Housing in SF Bay Area is still hot. Overbidding by 1.5M on 3M houses in strong cities like Cupertino, Sunnyvale, Mountain View, Fremont still going on in spite of high mortgage rate and falling stocks. Inventory is building up slowly but there are no signs of any price weakness whatsoever.

Kunal,

My BS-o-meter is redlining.

From Compass’ SF office, in my email today:

“Accounts of less crowded open houses and fewer offers on new listings are becoming common; some buyers are dropping out or becoming more selective; some sellers are moving listing dates forward; in many markets, declines in listings going into contract are occurring. Note that not all agents are reporting changes in client plans and motivations.”

“Absent an economic disaster event, major shifts in market conditions, especially from a superheated market, often begin very gradually. For example, an initial shift to a new listing receiving 2, 3 or 4 offers instead of 10 to 12 might not initially affect sales or sales prices, but if that changes to receiving 1 offer (no multiple-offer overbidding) or no offers, the supply and demand dynamics between buyer and seller start to shift quickly.”

Kunal,

I have been combing through data and not seen one case of bidding 1.5 million over asking. Overbidding $400K on a 1.6 million home in Bellevue is the highest I have seen, and that was last year. Overbidding 1.5 million on a 3 million house “in spite of high mortgage rate and falling stocks” is quite the exaggeration.

BS like this does not get past Wolf.

I am still seeing houses selling here in Redmond. Sometimes you see houses listed and sold on the same day.

But not sure how long it can last.

John, in my news feed yesterday there was an article about a house that sold over $1M recently in Palo Alto. Google “sf chronicle palo alto eichler” and it should be the first result. Obviously this is just one house but it shows that there is still some nuttiness out there.

This metric of “selling over asking price” is pure BS. If you put a house on the market at an asking price of $100k to start a bidding war, well then, it’s going to sell a bunch over asking, and then the braindead reporters that are paid by the RE industry make a big deal out of it to generate hype and clickbait, and readers lap it up without thinking about it. The oldest game in town. Any headline that says “over asking,” you ignore because it’s BS by definition. Go to the articles that actually have the data.

On an Eichler, sure.

Those houses are lots of fun, and there are people in Sunnyvale, Palo Alto and Concord that are willing to pay stupid money for them.

Lawrence, don’t you have more mainstream media interviews you have to conduct to go on the offense to assure the house thumpers that the market will only level out and move up after?

Why waste time on this site to convince majority of the “doomers” here?

Here in flyover land (Ohio) seeing more “price reduced” listings and a slightly longer inventory list. Not a selling rush yet but some preliminary signs of a softening market.

Nawwww, John. The “wait spinner” (aka Halo of Patience) just stopped on the Halibut9000 LDP (Lending Decision Processor) and, apparently, my snotty nosed nephew has been approved for 1.8M on your charming and obviously undervalued bungalow.

The right equipment and the right support are tested at the new Churchill

Media Guy expense. Soon satellites will fall from the sky like the latest IPOs

Side 1, Track 4: ‘Space Junk’ from DEVO is about to spin on the ‘table. Thank you Michael!

Q: Are We Not Men?

A: We Are Devo!

Dan R.-…or all Bozos on This Bus…(Firesign Theatre).

may we all find a better day.

“It’s now worth $3.6 billion”

You make some little money in Q1 and you are worth $3.6 billion.

Still some ways to go me thinks. .

The Fed would blink if a credit event occurs. Else market seems to be on its own.

The CPI print this week will indicate from which side of their mouth the Fed speakers will sprout forth their wisdom.

Love how people disparage an innovative company just because it fell from lofty heights.

UPST has a growth rate in 50% range even with the cut to forward guidance. It is profitable with an actual P/E ratio that is far under it’s growth rate with plenty of cash in the bank. Using AI as opposed to old FICO scores to assess loans makes perfect sense if it works which is does.

Casual analysis like this is why you are a blog writer….

mike,

RTGDFA.

Since you’re new here, and likely a drive-by troll, I’ll explain it to you with the patience of the exasperated. It means: Read The G*d D*mn F**king Article.

Yes, I know it’s not your fault because you accidentally microwaved your brain this morning. Happens.

“Casual analysis like this is why you are a blog writer….”

Ouch…ohh…someone’s feeling got hurt and want to throw some shade and run to mommy..

There is no AI. Artificial intelligence implies the machine is alive which isn’t and never will be.

The PEG ratio doesn’t imply the stock is a good value. That’s nonsense.

There is nothing “innovative” about writing software that is used to make even lower quality loans that are below the sub-basement quality loans normally underwritten either.

Upstart’s stock price doubled in 18 months (when ignoring the hype static).

In the archaic transaction flow world of RE agents and lenders, this looks like a viable service which has a soft spot when lending dries up in general (i.e. market shifts).

If they can create a spinoff service of some sort and become a multi-trick pony, Upstart may indeed be able to maintain some phenomenal growth in years to come. Maybe not 50% per year type growth as they have so far, but even half that rate would be impressive.

Was Peloton already on Wolf’s list? I think it was, but anyway it just dropped 20% pre-market

Upstart may have the best technology ever developed but:

1) Their market is drying up. Lenders are drastically downsizing since rising interest rates are driving down demand for loan originations. That is their entire market.

2) What goes up 10X in 6 months can drop 90% twice as fast.

3) Fundamentals and sales never justified the price of this stock.

Their P/E was over 400 at its peak. That is extremely high even for a great product. There P/E is now 23 which is reasonable but not in a rapidly declining market.

As a side note, Cramer recommended this stock in Feb. while the housing market and refi’s were running extremely hot. He saw a good product in a hot market. He ignored the fundamentals and failed to predict the market.

It’s not rising interest rates that will tank their business prospects. Its tightening credit standards where rising interest rates are a symptom.

I don’t know how their lending models differ from their “legacy” competitors. I only that I can reasonably infer that the only competitive “advantage” they have is to facilitate the underwriting of even lower quality loans than those offered by traditional lenders.

That’s saying a lot given that in the aggregate, credit standards have never been lower.

You are probably right.

They probably had AI S/W that found a lender for anyone. Fannie and Freddie have tight standards for income but how many other lenders are out there that may charge more but have looser standards for qualifying?

ie 0% down on a Jumbo loan with no W2. The AI has to look at other assets (RE, bank accounts, stocks, beanie babies, baseball cards, Picassos (Stolen or not), bitcoin) to find the right fit with a lender.

Everyone qualifies for a price! You just have to use Upstart S/W to find them.

My son got a strange pre-approval recently that had a 5.5%, 0 point rate but the lender was willing to drop the rate to sub-4% if he paid 6 points up front. We did the math and as long as he had the cash to pay the points, he would break even with the lower payments in about 7 years and he’d have a huge tax write-off to counter all of his bitcoin gains. I had never seen that before. It made me suspect some scam or catch somewhere.

Now that there are fewer employees of mortgage brokers and lenders, they have fewer seats of their S/W that are required. Wall Street investors severely punish companies with declining users.

To deduct points on your taxes, the points cannot be more than what are typically charged in the area. You’d have a hard time defending 6 points as being typical if an audit arose.

Good point!

We had noticed this in the IRS rules.

The mortgage broker told us that it if it is offered unsolicited by a lender, then it is considered typical. If it was a special arrangement not normally offered, then it would not be considered typical.

We plan on talking with a tax advisor on this.

I have seen how these startups generate their initial business — although I have no specific knowledge of Upstart. It works like this: you are part of an ecosystem of startups that can use each others’ services. For example a car- or house-selling startup would need loan approval services. That all seems reasonable except for two things: (1) When the air goes out of the startup ecosystem their interdependence magnifies the problem. (2) The startups can have overlapping investors, meaning that they have a subtle and undisclosed additional dependence on the startup ecosystem.

Bottom line: it would be important to know how the customers from which the payments that generated $0.34 / share for the quarter are doing.

S&P 500 hit 3000 milestone September 2019. Hit 4000 in April 2021. Now it is retraced to 4000.

A line of dip-buyers was flushed out this morning and the indices quickly fell to negative mid-morning.

Meme stocks especially were trading on margin so there is a liquidity run possible across more of them. Bankruptcies for sure.

Maybe Upstart AI software got in bed with Zillow software for some AI sex and got confused between lending money and buying houses. I personally don’t need nor care about what they are peddling. Maybe AI is gonna turn into an orgy. I hope so. The results ought to be entertaing to watch.

For the sake of avoiding another housing crash, I hope the Upstart AI was better than Zillow’s AI for qualifying mortgage borrowers over the last couple of years.

I hope their AI settings weren’t set in “pity” personality mode when authorizing all of the mortgages.

DR DOOM wrote: “Maybe Upstart AI software got in bed with Zillow software for some AI sex and got confused between lending money and buying houses. ….. The results ought to be entertaing to watch.”

You can’t watch. The investment vehicle drove off with your money.

AI sex: LOL

And yet eerily relevant metaphor

What happens in the Metaverse, stays in the Metaverse.

In the old days in was the Mafia doing this kind of Pump-and=Dump on the “Pink Sheets” (with penny stocks). Now it is white shoe Wall Street firms doing it out in the open with BILLIONS of dollars in stock.

If you at closing protection letters granted year over year you can see the housing situation is getting ready to sink. See you in 3 years.

With the violent volatility going in the Fed managed ‘casinos’ only traders’ with adequate knowledge of option trading, will be able to mitigate the potential loss of NOT just the profits accumulated since ’09 but also threat to the erosion of the their capital! Fed giveth and now taking back!

MFunds are hand tied by their rules in their prspectuses, except for BEAR MFunds. A lot of investors learned the hard way during dot com and GFC!

Buy-back shares cannot stop the sliding of the mkts.

Just simple:

Without Fed there is no mkt of any kind any where in the world!

Wonder what about CPI/PPI numbers tomorrow!?

Good article and some great comments. As someone who looked at doing a refi 6 months ago I can attest that the reliance of loan processors on this “state of the art” AI or whatever, certainly makes the entire process a clu…r f..k so to speak. After numerous starts, stops and arbitrary deadlines I killed the process and took a different route.