There are other types of stock market leverage, and no one knows how much leverage there is in total. Margin debt is the only reported indicator.

By Wolf Richter for WOLF STREET.

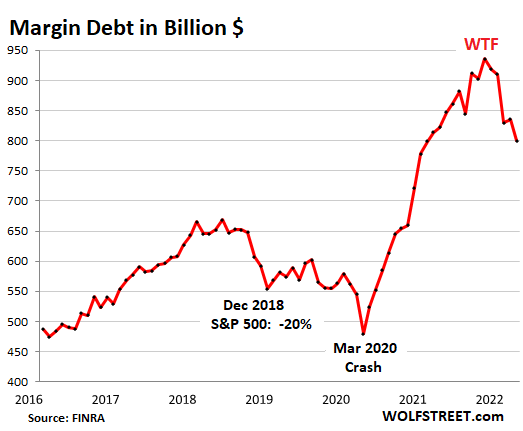

Margin debt – the only type of stock market leverage that is reported regularly – dropped by another $36 billion, or by 4.3%, in March from February, and by 12.4% over the past three months, to $800 billion, according to FINRA which collects this data from member brokers. Margin debt has now fallen below the year-ago level. But leverage is still gigantic and has a long way to go.

After peaking in October at $936 billion, margin debt started falling in November, which was also the month that the Nasdaq started falling. Margin debt has since fallen by 14.5%. The Nasdaq has fallen by 17.6%.

And many of the highfliers have collapsed by 60%, 70%, and even over 90%, some of which I track in my collection of Imploded Stocks. Stock jockeys that were margined in those trades got turned into forced sellers to raise the cash to pay down their margin debt. A margined portfolio specialized in these stocks can get wiped out.

Increasing amounts of stock market leverage provides new fuel for the market. But decreasing amounts of leverage removes that fuel.

The S&P 500 peaked on January 3, followed by a sharp sell-off and has since declined 8.8%. In the month of January, margin debt dropped by $80 billion, or 8.8%, the largest dollar-drop ever, and one of the largest percentage-drops ever.

The percentage-drops that had been higher were:

- Covid crash (March 2020: -12.1%);

- Euro Debt Crisis (August 2011: -10.4%);

- Financial Crisis (May 2010: -9.1%, November 2008: -18.1%, October 2008: -19.7%, August 2007: -13.0%);

- Dotcom crash (March 2001: -12.1%; December 2000: -11.6%; April 2000: -10.4%.)

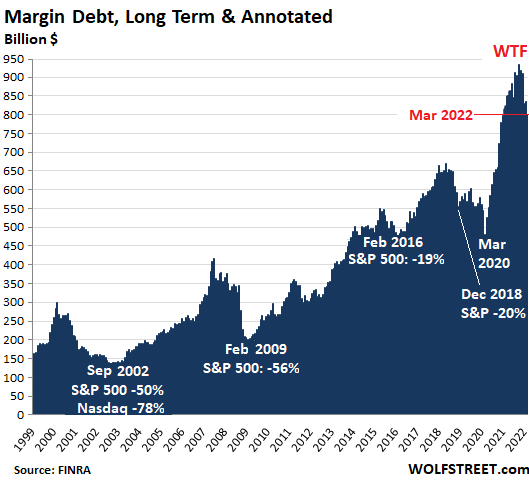

The stock market and margin debt are just about joined at their figurative hip. And drops in margin debt are associated with sharp declines in the stock market.

Margin debt is not the only type of stock market leverage. There are other types such as Securities Based Lending (SBL). Hedge funds can leverage at the institutional level. There is leverage associated with options and other equities-based derivatives, etc. No one knows how much leverage there is in the stock market.

Not even banks and brokers that fund this leverage know how much total leverage there is, or even how much leverage their own client has, which was the case when the family office Archegos, a private hedge fund, blew up a year ago and caused billions of dollars in damage to the prime brokers that had provided the leverage. The amount of leverage Archegos had used didn’t emerge until it blew up and the brokers had to sort through the debris.

But margin debt is an indicator of the direction of the overall stock market leverage. While total stock market leverage is far higher than margin debt, it likely moves in the same direction and is powered by the same dynamics as margin debt.

One thing we do know: High leverage in the stock market is one of the preconditions for a massive sell-off. In other words, a regular run-off-the-mill stock market decline can occur any time. But it’s hard to have a massive sell-off without massive leverage getting unwound, the opposite of when that leverage fueled the rally with borrowed money.

Margin debt and stock market “events.”

It’s not the absolute dollar amounts that matter over the decades because they’re skewed by the effects of inflation. What matters are the steep increases in margin debt before the selloffs, and the steep declines during the sell-offs that followed.

But no increase in margin debt was more breath-taking than the huge surge during the Fed’s $4.8 trillion money-printing binge in 2020 and 2021, neither in dollars nor in percentages, and this has now started to unwind:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If it “unwinds” a little here and a little there, no harm no foul. Massive “unwinding” in a hurry isn’t good for anyone in the market. Pension funds, 401k’s yada yada.

Frostbitefalls,

“… isn’t good for anyone in the market”

Correct. But it is good for anyone not in the market and with cash ready to deploy. This is when cash is king. There are two sides to every trade.

Interesting, isn’t it.

I wonder whether the main difficulty will be avoiding rushing in too soon.

Maybe there will be a 2 year window or so over which to observe the financial shakedown before things pick up again.

In March of 2020, I thought I might be rushing in too soon, but the truth ended up being I rushed out too early in July 2020. Making that 25% return in a couple of months was too tempting, so I cashed out early.

I honestly don’t know what to do with this market- I tried some puts over a year ago, but sold them when it was clear they weren’t going to be worth anything at expiration. I was mostly in cash/short to mid maturity bond funds since Summer of 2020. I have been lengthening the duration in the bond part slowly since January since I see nothing but recession coming before the end of the year. I am down about 5% overall this year to date after only a net 2% plus last year not discounting for the inflation losses. I would like to buy some puts, but they are just too expensive right now, which makes me think the recession isn’t coming.

Unless there is a long term bear market. Then everything is a bull trap.

No, then cash is truly king, earning interest and not losing money.

Wolf-

Could you comment sometime on what you mean by “cash?”

– Currency

– Bank savings/checking

– Money Market funds

– T-bills/Short US Treasuries

– TIPS

– Ultra-short bond funds

– Gold or silver (no heckling please!)

– Cryptos (you pick!)

– Other?

Which, if any, of these IS money, and which is ISNT?

As importantly, which might fall out of the IS category, when the next revaluation occurs in financial asset prices?

(I’m thinking back to the episode when Lael Brainard was making speeches and writing papers on the “first mover advantage” risk in money market fund land, and the imposition of gates under certain circumstances of financial panic.)

Thanks for your thought-provoking work.

John H,

Cash: Treasury bills, bank savings, CDs, money market funds, high-grade corporate paper, etc. In other words, short-term debt that is liquid and has very little credit risk.

Anything longer-term is NOT cash, including TIPS

Also not cash on your list: gold, silver, cryptos.

I would not consider an ultra-short-term bond fund “cash” because I don’t know what’s in it.

And yes, any fund has an additional risk factor: the run on the fund, which provides that “first mover advantage” Brainard was talking about. That’s why I’m on record not liking bond funds, including short-term bond funds, and money market funds.

So far, money market funds have gotten bailed out by the Fed, most recently with reverse repos and during the March 2020 blowup. That’s why Brainard and other Fed heads keep bringing them up: they don’t want to constantly have to bail them out, but it would require a fundamental change in how MM funds are structured and marketed.

What is “money” is an entirely different question that people love to debate endlessly – a debate that I don’t give a hoot about because I don’t think it matters how you define it in the modern world. There are bigger problems out there.

Thanks, Wolf. Helpful comments.

Walter

“Unless there is a ‘long term’ bear market”

Average BEAR mkt lasts around 3 yrs. But Dot com Bear lasted around 28 months. GFC Bear lasted around 18 months. Would have lasted more if Not for Fed’s intervention in March of ’09!

Ongoing Bear duration is undetermined due to CBers trying to prevent out right crash and might leak slowly(?) Fed is helpless against (or behind the curve) inflation, outside forces like Covid -Ba2, supply chain squeeze (making inflation worse, Ukraine war

and multi polar development.

No matter what long term is DOWN unless Fed engages in NPR and QEs, again! Head winds predominate over tail winds, if any!?

Wolf, let me help you out with a definition of money I first heard back in 1966.

“You see, in this world there’s two kinds of money, my friend. That which is mine and that which is not mine. You dig?”

The first kind is what I try to keep my focus on. The other kind is out of my control, so I try not to worry about it. Simple, eh?

Wolf said: “Cash: Treasury bills, bank savings, CDs, money market funds, high-grade corporate paper, etc. In other words, short-term debt that is liquid and has very little credit risk.”

——————————————-

Have to disagree. Cash is not Treasury bills. By counting treasury bills as cash you are double counting.

Define “cash” however you want. Up to you. I gave you how everyone in corporate finance and accounting is defining cash. Treasury bills and bank deposits are the ultimate “cash” on the balance sheet.

The other financial blogs say that “cash is trash” losing “7% every year to inflation”, & that the stock market always guarantee 7% returns over time, yet those who bought Doggy coin at 77 cents continue to HODL it at 15 cents.

Cash loses 8%….

and a sideways stock market loses 8% too….

and a down stock market loses the down move PLUS the 8% inflation ..

The Dystopia the Fed has created is clear.

I’m losing about 4% a year due to inflation. Not 13.8% like most people. It’s easy to save about 4% more every month without dropping my standard of living very much, to keep even.

So as Jim Morrison of the Doors once said, when

” This whole s$hithouse comes crumbling down” which it will very soon, I’ll be there to pick up the pieces.

Expressions are like, well … lets just say stupid.

“Cash is Trash”, and it rhymes. How cute.

My cash sitting in my accounts isn’t losing any money because I don’t use THAT money to buy everyday goods. And, when DEFLATION hits, THAT money “explodes” in greater purchasing power (i.e., I can buy MORE with the dollar).

“CASH IS TRASH.” And “TIME IN THE MARKET BEATS ‘TIMING’ THE MARKETS.” These are TWO of the stupidest financial expressions ever.

Yes, Swamp Creature, Americans have a lot of fat they can cut with a little effort. We can evaluate our habits and see a lot of unneeded waste going on everywhere in our lives.

Waste of water, hot water, food, electricity, natural gas, gasoline, heated and cooled unused spaces, are some of the things we have taken for granted for too long.

Now I holler at the grandkids when they are at my house: Soap up, get clean, and stop staying in the shower for thirty minutes.

There are doggy coin HODLers who too payday loans to buy it at 77 cents. I wonder how much they beat inflation?

The rich whales want bagholders in both the stock and bond markets. I don’t want to be one of them.

I also believe that storing cash in the banks with low interest rates are part of the problem. That’s why I used a credit union for my savings.

We live in interesting times, like the Chinese curse said. Peter Zeihan predicted that these symptoms of the over-availability of capital, namely the crypto coins, are going to go under when capital becomes very expensive next year and the next, until the coming, massive retirements decrease.

I predicted the same, not just due to the baby boomers’ retirement, which was Mr. Zeihan’s focus, since lots of baby boomers will have to work until they drop dead since they were defrauded by the banksters repeatedly already, but because the banksters’ Federal” Reserve will jealously protect its power to rip off Americans by creating and creating and creating US dollars until your entire salary now will only buy you a bag of fries and the banksters (who borrow trillions from their “Fed” at 2.5% per years when inflation is three times that) own whatever parts of America that have so far eluded their avaricious grasp: maybe, all remaining farmland.

Of course, a real reduction of all leverage would be good, but who knows if that is really occurring there. Famines are definitely coming: now fertilizer has become so expensive, and will become more and more expensive, that many TV personalities and politicians could be considered national treasures for their ability to spew it endlessly. LOL.

Kidding aside, the unavailability and expense of fertilizers, the inability to plant in Ukraine and China (due to the lockdowns’ direct and indirect effects), and the inability to prepare their fields in China because Chinese farmers are precluded from working outside due to Covid (LOL), will cause future, massive famines. Mark my words.

The CCP is engaging in what may be remembered in later years as V2.0 of the “Great Leap” (actually stumble) forward. That may cause Asian stock market crashes and start the world’s financial house of cards to crumbling.

I look forward to seeing the faces on the banksters who are invested in China when they, and those gullible fools whom they bamboozled into “investing” in CCP Ponzi schemes, lose their shirts. It will be epic. LOL

Maybe, the guillotines will finally start getting built or at least, maybe laws will change so banksters will actually have to pay taxes. They will be crying for their “Federal” Reserve to bail them out for the 29th time like infants with soiled diapers.

My IRA is all cash. I’ve just need the courage to put money back in. I have the stocks & ETFs all picked out. IMO, it may take a year or more for us to find the near-term bottom. Being a market timer is tough ; )

It will be Nov 2022 – not election related. Margin of error 4 months. There’s an algo predicting it back to the 1800s.

Yes, dry powder is good but will the Fed print to oblivion???

EXACTLY ”THE” question D14,,,

for each and every ”investor” of any and every kind

thanks,

and please let us on here know whenever you have any and every ”insight” to the answer

No one but Wolf consistently, accurately, and truthfully reports the fresh financial data in relevant historical context. The wisdom dispensed here daily is priceless. Wolf has done all of the heavy lifting.

Want proof? Ask all your friends and neighbors where their financial advisors have their assets. Find a single one in cash.

I am the treasurer of a fraternal organization offering my opinion that we should move out of stock and bond funds into cash. In a discussion, one member noted he had personally lost $300,000 so far in 2022 to which I immediately replied “it’s just the beginning”.(As many of you know, those of us trading SRTY and SQQQ are up nicely). I asked him in front of everyone if he was willing to lose 80% of his investment value, to which he replied yes. He countered that stocks and bonds drop, but they always come back. (Same song in 1999). I told everyone that we have just seen the lowest interest rates in 4000 years and the stock market is far more overvalued than 1929 or 2000. I asked what if it takes 30 or 40 years to get your money back?

Wolf is dead on. Having cash at the bottom is a joy.

Everyone else is saying “cash is trash”, but not Wolf… Cash is King.

Even Jeremy Grantham is afraid to time the crash now. (So it must be pretty close).

Thing is, cash can go up, as well as down. It just doesn’t show if you use the same cash unit to measure value with. A dollar is always worth a dollar, even if it gyrates all over the place.

@ Harry Houndstooth –

some have held cash “at the bottom” now for years

various FED, Government and other interventions have made that bottom hard to see. Meanwhile, money expansion (inflation 1) has continued and rising prices (inflation 2) has been continuous.

Many cash holders would have have been better off to leverage up and buy income property, with long term low interest, government subsidized loans. Enlightened Libertarian could shed some light on this.

Overall, I share your current sentiment. But the thieves and manipulators and money from nothing creators have made markets very tricky.

To my knowledge, there has never been an “orderly wind down” of “excess” stock market leverage, not even once.

The Fed will but all defaulting debt, no worries!!!

“To my knowledge, there has never been an “orderly wind down” of “excess” stock market leverage, not even once.”

Especially not from the WTF-levels seen during this latest period of Fed-&-Govt stupidity. I am always amazed by the “this time it’s different” crowd’s ability to forget the obvious signs of peak-stupid, but here we are again.

ZH has a great article on the Boise housing mkt, where I moved in late 2019. My entire life would’ve been much different if the CCP-Flu hadn’t happened to allow the Fed to lower rates to nothing and spike home-and-everything prices even more than they already were.

At least I’m not caught up trying to offload my albatross at the peak, with rabid inflation and mortgage rates shooting thru the roof!

It is hard to make a small hole in a overstretched balloon.

Slow unwinding might be good for a soft decrease of the buffer called leverage, but at the expense of the ‘real’ economy.

Hey Wolf Graham Summers says fed is still expanding balance sheet?

Thanks for letting me know who these morons are.

Maybe have the S&P on the right hand axis?

Get ready to be outraged by bailouts. This much leverage is a time bomb. We all know that.

I plan on being very patient. Wall Street would love to convice investors that the worst is over, time to climb in again. Until it’s clear that the fed is done hiking rates, nothing is over. I hope I’m wrong, but I seriously doubt they’ll do much before the election.

Harrold

This time compared to 2000 and 2008, there are head winds-external forces, over which Fed has NO control. Besides being awfully slow behind the curve against inflation, de-globalization, supply chain squeeze, multi-polar world in finance/commerce, Covid and Ukraine war. Fed cannot print/control FOOD prices, Energy, Jobs, Medical/Health care expenses or RENTS!

Yeh. This time it is different but to the WORSE side compared to GFC! By looking at the Volatility or Voilent movement of indexes, HOPIUM is still high by the BTFD crowd and a lot of bounce backs (bear traps) along the way. The later is charectric of a SECULAR Bear! Read Mkt history!

Well, Russia will probably, officially, default on the 25’th of May.

Thats when the real fun starts because who knows whats lurking in the shadows of the unregulated OTC derivatives market? Like last time, all of that will be bailed out and made hole, eventually (Maybe this time it will be “For Ukraine” instead of “For Confidence”). The next year or two will be an exciting ride.

If “The Market” surges before May 4 or 25, it will, IMO, be a perfect time to get some leveraged inverse ETF’s for the old portfolio, not more than one can abide going to Zero of course, but, like with any vice, enough to get the blood flowing again!

That is what I will be doing.

Isn’t it also tax due paying time in the USA….

It is every year in April. In March 2021, margin debt jumped by $9 billion. In April 2021, it jumped by $25 billion.

Still $800 billion, “gigantic” alright. The right side of those charts is scary. Another previous example not discussed is 1929.

Like buybacks, this could be another thing (aside from fundamentals), keeping the casino attractive, or less scary to the retail money.

“Not even banks and brokers that fund this leverage know how much total leverage there is, or even how much leverage their own client has ….”

I wonder if this factored into JP Morgan’s more downcast earnings season talk. Big selloffs creating price downdrafts is a scary thought for anyone with skin in this game — and others too. The collateral damage on Main St. could be big.

The right side of the chart would be less scary and more accurate if they were log charts.

Walter,

Yes, they would be less scary (but not more accurate). You can hide anything by manipulating the scales and adjusting data. And lots of folks would like to hide those kinds of inconvenient data by adjusting them or by manipulating the scale, such as using a log scale. Anyone in finance who uses a log scale is trying to hide something. That’s an ironclad rule.

Thank you for giving me an opportunity to point this out for the gazillionth time :-]

If you believe the dollar is going to decline at an accelerating pace then the chart will be using a log scale eventually. Log scales can be used to hide things but they are also useful to see changes in rate of increase, which is important now. If peak 1 to peak 2 is up 50% and peak 2 to peak 3 is up 75% etc then a person gets the best picture with a log scale. You should right an article about JPY and its relation to the dollar. If things continue the Chinese will be opening sweatshops in Tokyo soon. Pity to see masses of old people knitting socks in crowded cubicles to satisfy the nouveau riche Chinese.

You can prove anything with statistics as long as your audience doesn’t understand statistics.

Why would it be more accurate? Numbers are what they are.

1) Go to tradingview spx.

2) Click on ‘detailed chart’

3) Click on timeframe ‘all’

4) Compare log chart vs regular chart.

Log charts are very useful as long as they are not abised.

Another excellent example is bitcoin. If you look at the drop in November 2018, you can see that up til then everybody was trading on the log chart. People who didn’t look at the log chart up to that point were lost.

Indeed they are. As an example, if a stock price fluctuates between $42 and $48 over a year, it can be graphed in ways to give different impressions of the same numbers.

If the Y axis ranges from, say $40 to $50 over the year, the swings will look very large. Same data from $0 to $100, and it will look pretty flat. Again, same numbers.

Log charts are what I see in physics and audio gear analysis. They make sense in those realms. It takes a double-dose of watts from an amp to give a 3 dB volume increase & 10 a fold increase in power to add 10 dB. When I listen to my stereo, I try to max out at or below 85 dB. Live orchestral performances can go to the mid 90s dB level.

Sound pitch, or notes per octave work in a similar fashion. A1 =55 Hz; A2 = 110 Hz; and as you go to A6 = 1,760 Hz etc.. Intervals of the octave go up in a factor of 2 in frequency.

This smart guy named Pythagoras figured this out 2,500 years ago by studying the string lengths, at equal tension, as they vibrate to come up with a mathematical scale for musical notes.

That’s where log scales belong. Not in Wolf’s charts.

The fundamentals aren’t attractive. Whatever attractiveness appears to exist is actually the result of artificially cheap money, the loosest credit standards ever, and increased debt.

If the “the market” were actually “discounting” anything (which it isn’t since it has no collective mind), the long-term fundamentals are mediocre to awful.

It’s a mania with margin debt part of it.

Re “artificially cheap money”.

Fiat has been artificially expensive for a long time, and now commodities are returning to the market.

Unless you mean “artificially low interest rates” in which case, all a person can say is “fasten your seat belt and return your tray to the upright and locked position, and thank you for flying the 737max”

Yes, artificially low interest rates as in artificially cheap borrowing costs.

The markets aren’t expressing real valuation, but IOUs based on leverage!

We know that a fair amount of “mortgage refi” money went to buying stocks. Some of that would have been margined-up too.

S&P says that hasn’t worked out too well for most of them in the past 3 months.

And some of those who sold those stocks for that refi cash are undoubtedly waiting to buy up the over-mortgaged houses from the newly-poor margined-stock-losers when the bottom drops out of the job market…

There should be rules in place to protect people from doing too much of this – on either side…

The mutual fund locomotives continue to buy, come what may.

Google “etf outflow”. There is speculation about where the froth is coming from, one site suggesting the Fed has been buying equities.

No! Say it isn’t so! I thought this was illegal! /s

Of course the Fed buys assets, but some people suspect it goes beyond that. Read “Is the New York Fed’s Trading Floor Near the Futures Exchange in Chicago Behind the Erratic Gyrations in the Stock Market?”

‘mutual fund locomotives continue to buy’

They have to stick to the provisions of their prospectus by SEC.

But cannot the portfolio during Secular BEAR unless they bear funds.

Just study all the previous Bear mkts in 200 history of the mkt!

One can sell the ETFs during the ‘trading hours’ but not he MFunds (one has to wait until the end of day(after mkt hours) to get the NAV (net assey Value)

Or, they can be bought after the current market hours, but get tomorrow’s opening NAV?

Wolf, an interesting question is how much margin debt or cash in general is in more freely tradable NEGATIVE etf’s such as SQQQ or SDS. These products were not easily accessible / available in 1987, 1999 and even 2008/09. Though I realize is a tiny fraction of total dollars “in” the market, would be curious again as to the total amounts and your thoughts on its impact and how much influence on the current market volatility?

Margin debt cannot be used to purchase inverse ETFs. Inverse ETFs are designed such that insiders can have a portal into retirement accounts and such (cash accounts), and the ability to fleece the retailer’s cash account. Insiders monitor inverse ETFs and will come a shearn’ when enough sheep are found helplessly grazing in the grassland. Inverse ETFs are a complete scam. Why bother with inverse ETFs when there are other alternatives? One must delve deeper than the major indicies in order to find such alternatives, but they do exist. By the way, if one holds on long enough to an inverse ETF, oner might get lucky and catch a 1-for-10 reverse split. SRTY, so often cited in the comments, recently reverse split.

If one buys an inverse ETF, one is long that ETF. One is not short anything. Big difference.

In a down market, inverse ETFs move up but against a head wind.

In a sideways market, inverse ETFs drift down

In an up market, inverse ETFs crash and burn.

To each his own.

Propheticus

Most of your comments re inverse ETFs are right, but those who use invert ETFs should match ‘partially’ with long leveraged ETFs, to cut down the whiplash and the daily decay. I used them profusely during GFC and lost zilch. But afterwards when there was no longer ‘Free capitalist Mkt a different story. I also match them with Puts/Calls. The success rate is high when Secular Bear is the long term trend like late 2007 to early ’09!

Like the one, on coming BEAR!

Inverse EFTs, and particularly the 3X EFTs SRTY (triple short the Russell 2000) which I humbly recommended in Early November 2021 on this site and SQQQ (triple short the Nasdaq 100) which I recommend trading with the simple goal of ending up with more cash at the bottom of the crash. You are absolutely right that these vehicles are not to buy and hold. If you do not want to time the market, you should stay in cash. To understand why these vehicles present an egalitarian method to profit in a bear market requires some knowledge about the rigged game of shorting individual stocks: borrowing the shares, the uptick rule, broker calls requesting the borrowed shares back (their timing, not yours).

Using the strategy of buying on market rallies and selling when your account balance is going into new highs simplifies the decision making.

This might be a good time to dust off Stan Weinstein’s How to Profit in Bull and Bear Markets. The elegant simplicity of understanding the correlation between the significance of the dead cat bounce to market participant’s psychology is timely.

“If you do not want to time the market, you should stay in cash. ”

Actually, retail investors have an uncanny knack for timing the market: They buy the top and sell the bottom or they buy nearer the bottom, never to sell near the top, only to have the stock boomerang back to their initial purchase price, or worse, drop below their initial purchase price.

” requires some knowledge about the rigged game of shorting individual stocks”

Cash accounts cannot short stocks. Hence, the inverse ETF.

As far as I can tell, this isn’t the correct forum for debating inverse ETFs. Most commenters, here, seem to be interested in bonds, the “risk-free” brand, to be precise. But as they say, that’s what makes a market.

Speaking of bonds and inverse ETFs, there are a few bond- inverse ETFs that look to be relatively unmanipulated and could be candidates for longer-term buy-and-hold enthusiasts. A play like that could prove, in time, to be the biggest no-brainer in the history of the universe. Definitely not a good entry point as of today, however, as bonds are short-term oversold according to my data.

Why are we entering a feudal society where Old Money and newly created New Money get to become richer, while the working class and those engaged in labour suffer with high inflation, high cost of living and being encouraged to buy high and sell low in the stock market and doggy coins?

Let it drop!

Drop some more!

Let the doctors be paid more than an Instagram “influencer” or “doggy coin millionaire”.

It’s a speculative orgy of the FED’s making, encouraged by CONgress. Everybody is looking to get rich quick, and billionaires are posing and virtue-signaling on social media while their sycophants grovel and hope to join them when in reality they are headed for extreme poverty. It’s a veritable shit show.

In other words, money printer go brrr while an incoming recession is coming?

Better than reading stories of $100,000 homes being sold for over a million in the middle of Tennessee or Winnipeg.

Gonna need more cash to just live and get by with this level of inflation. Last thing on my mind is investing more.

There are persistent rumors that Peloton bikes, and even Tovala micro wave machines have been found hidden under non descript bags of trash on trash days at curb side lately. OMG!

Good and helpful report! Thanks. Still plenty of danger…….this is not going to end well.

Sometimes it is valuable to zoom in on chart details.

It looks like in the October to December 2000 timeframe, some entities thought it justified/wise to add $200 billion to *pre* pandemic peaks in margin debt.

A 30% increase in 2 or 3 *months*.

Just after the shock initial Covid wave.

And during the upward zoom in winter peak fatality.

Hm.

“That’s a brave call, Cotton.”

When you see things like this, you start thinking more about the semi-visible hand of opaque gvt intervention and less about the invisible hand of mkt participants (who don’t have a printing press at their backs, to cover up their high risk failures).

rehypothecation anyone?

Who was it that made the quote “He who does not learn the lessons of history are deemed to repeat it?

doomed?

The exact quote is “Those who do not remember the past are condemned to relive it.”

George Santayana. He is quoted in an introductory page to William Shirer’s “The Rise and Fall of the Third Reich”. His quote could also be applied to many American politicians of both parties. Then there is Herbert Hoover’s famous quote “Blessed are the children, for they shall inherit the national debt.”

The meek shall inherit the earth but not the mineral rights.

“Doomed” to repeat it.

Those who study history are doomed to repeat it.. Henry Ford?

i really hope what wolf has explained regarding delayed settlement of mbs explains the $30 trillion addition to the fed’s balance sheet last week. otherwise, they’re flagrantly lying to us.

Jake W,

Last week’s increase brought the total back to where it was four weeks ago, after two weeks of declines. Duh!!!

Why didn’t you come around during the two weeks of declines??

You are now officially classified as either totally clueless and too stupid to look up the chart, or a willful despicable manipulator. Either way, your comments are now condemned to permanent moderation. You don’t get to abuse my site to spread this garbage. Cheers, you did it!

Thanks for pointing this out again. There are plenty of sites out there saying that the FED balance sheet continues to increase.

Nobody really expects the Fed balance sheet to decline much before it races upwards again. Every time it starts to drop the economy starts to contract and they don’t want to be blamed for the next recession.

Ladies and Gentlemen-

Wolf has incredible tolerance of dissent, but equal intolerance of misinformation.

We are lucky to be a part of his site.

Don’t candy coat it. Tell us what you really think about Jake. ;-)

This chart?

https://fred.stlouisfed.org/series/WALCL

Where is a meaningful decline decline?

April 13th looks like an all time high

cb,

“Where is a meaningful decline decline?”

What are you talking about? QT won’t start until AFTER the MAY MEETING when the final plan is announced. There won’t be any decline until after QT starts. Don’t you people read anything on this site? Don’t you people ever listen to anything the Fed says?

@ Wolf –

I read as much as I can on the site, though you are hard to keep up with.

And as for the FED. They have proven to be a bunch of manipulative, self serving liars ……………… not to be trusted. Creators of debt slaves and benefactors to the debt masters.

And since QT won’t start until after the May meeting, why were you so quick to jump on Jake W with both feet, where you said:

“Last week’s increase brought the total back to where it was four weeks ago, after two weeks of declines. Duh!!!

Why didn’t you come around during the two weeks of declines??

You are now officially classified as either totally clueless and too stupid to look up the chart, or a willful despicable manipulator.”

Jake said that the balance sheet was still INCREASING (and at a high rate) and that the Fed was “lying” about the end of QE. His statement was total manipulative BS.

You’re talking about QT = balance sheet is DECREASING, but that won’t start until after the May meeting.

Sheesh.

cb-beware ‘baby/bathwater’ syndrome, you’ll spend an inordinate amount of time looking for the kid and/or drying your feet…

may we all find a better day.

I notice AT&T did some skydiving recently too (T down almost 20%) – to get out of their leveraged streaming services play for Time-Warner.

Spin off of Warner Media. Been planned since last year sometime.

I have decided to take Wolf’s mug off of Ebay. I don’t need the money anyway. Some dude on this site was offering $250 for the mug which is very reasonable. But with the supply chain problems, I don’t know where the glass for the future mugs will be manufactured or what the quality will be. I want the real thing and will keep the 2 mugs that I’ve got. They are irreplaceable.

Potentially inaccurate mugs though.

I’m waiting for “The Fed can make things go to heck in a straight line” special economic depression edition.

Though to be fair, I think it’ll be the Euro that does it first.

ECB for the win on heck in a straight line first!

AGREE, like totally SC:

SO,

I have decided, as a ”non collector of any ‘thing’ to put my WS mug up for auction, with the money going to support my absolutely fave website/blog, directly,,,

When the money is acknowledged by the Wolfster, I will ship the mug directly to the high bidder confirmed by WR…

Not exactly ”HIGH finance,,,” but still lots of fun for those of us old ”pre boomers” who used to enjoy and play with at least a taste now and then of the the shenanigans of HF!!

Swamp Creature-

Or anyone else holding an authentic Wolfstreet “Nothing Goes to Heck in a Straight Line” (beer) glass mug.

I do not know how I missed your listing on Ebay which I monitor. Anyone who wants $250 for a mug can post it on Ebay and drop me an email below .

Yes, I am the dude offering $250 for an authentic Wolfstreet “Nothing Goes to Heck in a Straight Line” (beer) glass mug. The current ask is $525 (which is $25 over the actual ASK which is brand new with tags) to cover shipping to me and again to the buyer, subject to the current holder’s participation.

“They are irreplaceable” … Wolf is irreplaceable. You might be surprised how high the value of these mugs could go with someone actively making a market. The intent is to benefit Wolf.

I need at least one mug to make a market.

HarryHoundstooth at yahoo dot com

HH

I’ve decided to keep both mugs for now and send Wolf a donation of $50 for the great services he is performing.

All the stopped clocks here will be very surprised when the S&P hits a new high above 4800 next month. Doubters will not have to wait long as May 2022 is just weeks away. This is the age of deliberate monetary inflation, so most the old timey metrics like margin debt, P/E ratios, price to book value, etc are not as applicable.

To get an inkling as to the effects of deliberate monetary inflation……..please examine the nominal inflation, manipulated interest rate, and equity casino charts for the most analogous era, 1942 to 1960. Note the dow casino chart for this inflationary period…..a very constant rise from 100 in 1942 to 1000 in 1960. Get it? This is the age of inflation…..your asset doubles not because you are a genius, but rather your fiat frn asswipes buy half as much. S&P between 4800 and 5000 in May after a glitch down to let the insiders get positioned..

nsa-

“…fiat frn asswipes…”

Colorful term!

I just ran across this word yesterday, that you might be able to use in future comments or communications: “PAPERASSE”

French for “paperwork”

Paperasse prononciation in French won’t make any Anglo smirk, as it sounds

Pap-rass, not

Paper-ass

Somehow this connection is not even registering on the slightly funny. It’s more of an oddity that we have a word connecting paper with -asse (I get it but really).

NB: in French a couple of words end in -asse, not too uncommon.

Up North-…’demi-tasse’ comes to mind. We all know a few who are ‘demi-tassed’ using the above alternative definition. (Now, where’d i set MY demitasse down???).

may we all find a better day.

1942 to 1960 wasn’t a mania. Comparing the present to this prior period is pure rationalization. S&P 4800 is about 10% above current levels, so yes it can happen and wouldn’t be a surprise.

There is no direct causality between “printing” and stock prices. If this existed, 1966-1982 never would have happened.

In 1942 the CAPE ratio was a very reasonable 10. I’d be all in at that level.

Today CAPE is at a nosebleed 34 as the everything bubble and massively Fed surpressed rates and QE rage on.. They didn’t have any of that contend with in that era, which makes the situation today far far more precarious.

CAPE is finally headed in the right direction, but it has a long, long way to go.

I did not include it in my prior reply, but numerous international markets refute the prior claim.

The primary one is Japan. Money “printing” has occurred on steroids since 1989, yet prices are still lower 32+ years later.

The reason the claim in the prior post is not accurate is due to human agency. People can change their minds and do, all the time.

I can answer this one (I lived in Tokyo 20 years in the financial industry and can speak / read Japanese pretty fluently).

It is because although the govt did QE, the labor market is controlled by Employer associations that control salaries of workers. This is highly pervasive and at a very level pretty much unimaginable in the USA. It is illegal as he’ll, but everyone does it, it is just the way Japan is. The labor market is not at all free and people cannot really jump around for more money.

The result is small to non existent wage hikes across the economy. No wage hikes, no inflation. The big mega corps on the other hand, they are absolutely rolling in it. Their executives (mostly) are far less prolifagate than ours though so you don’t see them building mega mansions in tokyo or taking a private helicopter to work (they ride the subway like everyone else does though some take black cabs).

Basically that’s why

A rising tide lifts all boats, but until the government admits that inflation is permanent and accelerating i.e., due to money supply, big investors will react to inflation the same way they did in the 1980s.

That 9 month leap from about $500B to about 800B is eerily similar to the 9 month leap from about $260B to about $410B in 2007.

For what it’s worth, the S&P peaked in August 2008, and bottomed out in March 2009.

Anecdotal, to be sure…

“For what it’s worth, the S&P peaked in August 2008, and bottomed out in March 2009.”

I think October of 2007 was that SP500 peak. Took about 17 months top to bottom.

Thanks, and apologies for wrong data.

Another ungraceful fall from the WTF peak.

I see a way out of all this if I can find a SPAC that will underwrite my new Icarus-coin offering.

I am considering a few “Coin” offerings.

I have an idea for a Volcano series:

Krakatoa Coin

Tambora Coin

Yellowstone Coin

Toba Coin

Vesuvius

Real neat engravings on all of them. Some can look melted or bent. Even make some look tike pieces have broken off. The “Vesuvius” can have naked chicks in a Roman hot-tub, Yellowstone can show Buffalos gasping for sulfur free air…………….you know, things that boys in the family basement like to collect……………..

The exchange can be part of my Cloud Data company: SouthSeas TuliPonzi Data (Symbol: STD).

I hope you work in your local comedy club.

They might be missing your brilliance.

Heck I was way ahead of the curve with my gambling debt back securities that I offered here on WS.

I did great. My investors, not so much. I did honor my 50% return guarantee. I refunded 50% of the money.

Two corporate hacks from Blackrock are now joining the highest levels of economic advisors, in the Biden Administration. These jobs include the Chairman of the Councel of economic advisors and his assistant. Look for them to be as crooked and incompetent and Gary Cohen and Steve Mnucian were in the Trump Administration. The more things change, the more they remain the same, no matter who is in power. ENJOY

Swamp…

Brian Dees, a former Blackrock investment exec serves on the National Economic Council. Adewal DAdeyemo former chief of staff to BlackRock’s chief executive now a top official at the Treasury Dept. Michael Pyle, former global chief investment strategist at Blackrock now chief economic advisor to Vice President Harris.

AND, going the other way, Blackrock has hired several policymakers and administrators that served in past administrations. Dalia Blass was with the SEC is now leader of external affairs at Blackrock. A Mr Thomas Donilon was national security advisor to Obama currently head of Blackrock’s research business.

All according to what I have read. But all this pales to working with the Fed, being inside the “tent” even though officially this seems to have ended.

The President and CEO of Nasdaq, Inc. sits on the board of the NY Fed as a class B director.

Class B director facts (from newyorkfed.org):

Elected by member banks;

Elected to represent the public; [LOL!]

Chosen with due but not exclusive consideration to the interests of agriculture, commerce, industry, services, labor and consumers; and

Cannot be officers, directors or employees of any bank.

Wolf, am I reading https://www.federalreserve.gov/releases/h41/20220414/ correctly the Fed did not even tighten since April 6th as Reserve Bank Credit up + $6,662 million? Still no QT?

TimmyOToole,

Everything is wrong in your statement, including that nonsense about “not even tighten since April.” Where does this BS come from? The Fed won’t tighten (QT) until AFTER its May meeting. It hasn’t even announced the final plan yet. But it will announce the plan at the May meeting. There is NOT SUPPOSED to be any QT until after the May meeting. Don’t you people pay attention to anything the Fed says? Or at least read it here? Where do you pick up this garbage about “Still no QT”? Who are the braindead morons out there that are spreading this BS that the Fed said that there would be QT by now?

“Where do you pick up this garbage about “Still no QT”? Who are the braindead morons out there that are spreading this BS that the Fed said that there would be QT by now?”

Isn’t that obvious? The gamblers who believe the Fed will always have their back so their crypto and stock investments will never go down because they Fed will never raise or tighten. They are all over ZeroHedge. This normalcy bias will be their downfall.

So it seems that there is no Quantitative Easing at the moment (expanding the balance sheet massively like they did before)–> holding pattern until May–> and then Quantitative Tightening (selling assets after May meeting).

No QT right now and mortgage rates are higher than in 2018 when Powell was reducing the balance sheet? What will happen when he starts disgorging the 9 trillion balance sheet?

If the past two months are any indication, mortgage rates will be north of 6% soon. (As before, idiots at National Association of Realtors are telling us higher rates will not affect housing at all because there is a tight supply).

I believe in free markets.

Where did it all go wrong?

Relying on price signals from the markets.

“Everything is getting better and better look at the stock market” the 1920’s believer in free markets

Oh dear.

In the 1930s, they were wondering what had gone wrong with their free market beliefs and worked out what had happened.

What had inflated the stock market to such ridiculous levels in 1929?

1) Share buybacks

2) The use of bank credit for margin lending.

The US stock market is doing really well with share buybacks and margin lending driving prices ever higher.

A former US congressman has been looking at the data.

He is a bit worried, hardly surprising really.

We didn’t realise we were making the same mistakes they made last time.

Sound, those are not mistakes, that stuff is intentional.

Sound of the Suburbs-

It is our opportunity to prosper from the same mistakes.

What I see in money flows is short to midterm money has washed out, and long term money (which includes Fed stimulus) is carrying the market. That makes sense too, for all their jawboning the Fed has done nothing and is ten miles behind the curve. That would explain margin debt dropping as well. The REPO market is bustling as well and that suggests the effects of QE are still felt, high levels of cash reserves. And REPO fails has been increasing, which is a function of collateral, but maybe supply issues in treasuries. After years of pumping fake collateral into the financial system the bill may be coming due, and inflation which puts more value on collateral, all the while bond premium is dropping. When someone said Musk would buy Twitter, one wag said, “with what?” He would have to borrow the money which is measured against stock in his company which has more liabilities than assets? Does Musk have a collateral problem? Internet AD revenue is better than auto manufacturing as a stable source of revenue? Musk guilty of reading his own press clippings? Just buy GM and save yourself. They have a great price to book number.

Wolf, you’re a data driven guy, I understand you may not want to speculate, but if you feel like it, what do you think is the real intention of the Fed for raising rates? For the record, I think the rates should be higher, QE should end, but I didn’t come up with these speculations myself, I just echoing a bunch of things I hear online, and post the question here as I really respect your opinion as well a few that are on this forum.

The multiple choices are:

1. Fed is raising rates to fight long term inflation

2. Fed is raising rates to cause short term demand destruction

3. Fed is raising rates because economy is overheated, (fight speculation, reduce margin)

4. Fed is raising rates to cause a recession (or prick a specific bubble)

5. Fed is raising rates to “reload the monetary bazooka” to be used next time (in the near future)

6. Fed is raising rates to accurately price risk and return against bonds from other world governments.

Thank you!

And also 7 (the correct choice in my uneducated opinion :-) ): the fed wants persistent inflation at an elevated level over time (years) to get the national debt/gdp ratio to something reasonable. At the same time though they do not want to crash the economy or have social unrest.

Ideal is that everyone stays employed, stocks go sideways for the next decade (but down on an inflation adjusted basis), cape ratio and interest rates eventually return to something sensible at the end of a decade of this.

Hence all the jawboning but relatively little action on the ground so far with regards to aggressive qt and rate rises (like up 8%) to kill inflation. They want the inflation and they have no intent to kill it. They do want it to be moderate though but things now have gotten a bit out of hand with the latest inflation figure, which will cause social issues soon.

Perhaps they ll wait to see if the inflation goes down on its own, other wise they’ll rates a bit faster to return to’moderate’ inflation target to get rid of national debt slowly in real terms.

That is the plan anyways, in reality this is very very hard to do.. i expect big policy screwups and runaway inflation along with a bad recession and maybe even rate cuts and qe again for a bit to try to undo the upcoming mess when they inevitably screw this up.

One of the fed chairs if I recall wrote a paper on exactly this strategy (jawboning, market and yield curve manipulation to get long term moderate inflation) they are following that playbook.

All this is essentially because politicians won’t cut spending, raise taxes (both politically unacceptable) and a debt default is even worse. Last choice on the table to get rid of debt is prolonged and intentional persistent inflation till the national debt goes down. And that’s what we got.

Disclaimer: this is only my opinion, it is also devaluing each day by inflation so take it at what’s is worth ;-)

Interesting that the stock market hasn’t fallen much yet. 14.5% drop in Margin Debt in just six months should have yielded a BIGGER drop in stock market caps that 8.8% (S&P500) and 17.6% (NASDAQ).

But as Wolf said, “High leverage in the stock market is one of the preconditions for a massive sell-off.” Margin and Market Cap will be joined at the hip until one or the other makes a big move.

“There are other types of stock market leverage, and no one knows how much leverage there is in total.”

The unregulated, unmonitored shadow finance system. Margin leverage of ~900 billion by itself is nearly 1% of the total value of US equity markets of ~94 trillion. And the rest? Who knows.

Could be dangerous. Ignorance is risk, and that’s a LOT of ignorance.

Then there’s the derivatives market, variously estimated at half a quadrillion to over a quadrillion. The 2008 crash is believed to have merely been triggered by the collapse of the housing bubble, because the real action was in OTC derivatives, according to businessinsider dot com. To quote:

Dear regulators, fix this.

Economic bubbles are not recognized by those inside of them, and the entire Western world has become quietly trapped inside the largest economic bubble in history. The global financial crisis that began in 2008 has been attributed to sub-prime mortgage lending and mortgage backed securities (MBSs), such as collateralized debt obligations (CDOs), which were revealed as toxic assets. While the root cause of the financial crisis is assumed to have been the residential real estate asset price bubble, the underlying systemic risk, and the primary reason for the “too big to fail” doctrine whereby governments were compelled to save financial institutions at any cost, lies in over the counter (OTC) derivatives. The suspension of the US Financial Accounting Standards Board (FASB) mark-to-market rule in 2009 preserved the value of bank balance sheets, i.e., of their mortgage portfolios, but what was of far greater importance was that it prevented triggering the conditions of thousands of OTC derivatives contracts, such as credit default swaps (CDS), that would have wiped out virtually all of the largest banking institutions in the world.

Unquote.

Musical interlude:

You never give me your money.

You only give me your funny paper.

To err is human. Amplifying that error requires massive mainframes running COBOL.

Thank you. I have no idea how humans long stocks or bonds sleep at night.

Wolf notes that tracking the margin debt is only looking at the portion of the iceberg above water.

I could not imagine being long going into May.

I sleep a lot better having sold all my bonds except I-bonds. The proceeds are in the “cash is trash” can waiting for the grand opportunity when there’s blood in the streets.

We’re still just doing warm-up frames at the bowling alley.

Wolf,

Could you please elaborate on what you meant by ‘high grade corporate paper’ in the comment above on the ‘what is cash’ subject? Thanks!

Try commercial paper.

I see, thank you! Learning something new every day here.