What’s good for Amazon is not good for the gander.

By Wolf Richter for WOLF STREET.

Amazon has a another huge bond deal in the works. Today, it disclosed that it would sell a pile of senior unsecured bonds, in seven parts, to add to its $50 billion in already outstanding bonds, in part to pay for the share buybacks. Moody’s said today that it rates these bonds A1, solidly investment grade, in line with its overall corporate rating for Amazon. In the Prospectus that Amazon filed with the SEC today, all amounts, maturities, interest, etc. are still left blank, to be filled in later.

But some details have emerged. Amazon would raise over $12 billion — amid huge demand from investors. As Amazon’s prior bond issues, one part of the seven parts is a 40-year bond. Its yield may be 1.55 percentage point above the Treasury yield, according to Bloomberg, citing a source. This might put the yield somewhere near 4.3%. Goldman Sachs Group, JPMorgan Chase, and Morgan Stanley are managing the bond sale.

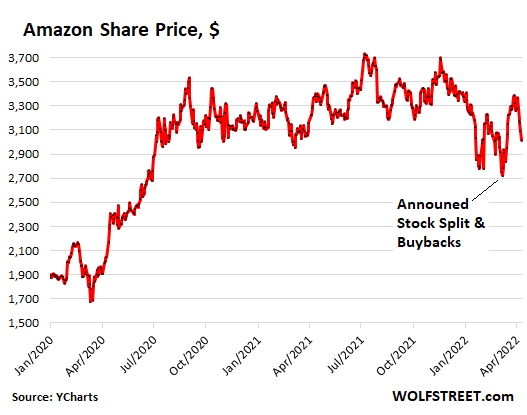

Back on March 9, Amazon announced a massive bout of financial engineering to halt its sagging share price: It would split its stock 20-1 and incinerate $10 billion in cash to buy back its own shares.

By the eve of the announcement, Amazon’s shares [AMZN] had dropped 28% from the high of $3,773 in July 2021, to $2,720 on March 8, amid endless headlines that its stock was in a “bear market.” Then on March 9, Amazon comes up with the stock split and the $10 billion cash incineration program, and WHOOSH go the shares, surging by 24% in three weeks to $3,386 by March 29, just 10% below its closing high in July. That was a very effective application of financial engineering.

Since then, the effects of this masterful financial engineering have faded and the shares have given up much of those gains and by today have dropped back to $3,015 at the moment shortly before the close, including the 2.4% drop today, down 20% from the high (data via YCharts):

Amazon’s callable 40-year bonds, buyers beware.

According to the Prospectus, at least some of the bonds are going to be callable, which can be an unpleasant surprise when interest rates drop and Amazon decides to replace this expensive debt with cheaper debt, and the bondholder just gets the face value back and loses the nice coupon payments and the capital gains. And Amazon warns about them:

“We have the right to redeem some or all of the notes prior to maturity. We may redeem the notes at times when prevailing interest rates may be relatively low. Accordingly, you may not be able to reinvest the redemption proceeds in a comparable security at an effective interest rate as high as that of the notes.

Amazon has a history of issuing callable 40-year bonds, and then calling them when it’s good for Amazon and bad for the bondholder, namely when yields have dropped and cheaper funding is available, which would normally push up the price of the bond, but Amazon pays them off at face value.

Little upside, huge downside with Amazon’s callable 40-year bonds.

The callable feature removes the upside of long-term bonds when yields fall, but leaves the holder with the downside when yields rise. So the risks are asymmetric. By contrast, bonds that are not callable provide both the upside when yields fall and the downside when yields rise, and the deal is in balance.

Little upside: For example, the $16 billion in bonds that Amazon sold in 2017 to fund its acquisition of Whole Foods also included $2.25 billion of callable 40-year bonds, with a juicy coupon of 4.25%, that Amazon then called in mid-2018 at face value. Folks who thought that they’d get the steady coupon payments of 4.25% for 40 years got instead their money back and had to kiss those nice coupons and capital gains goodbye.

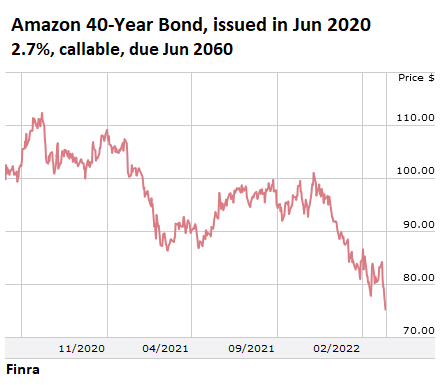

Huge downside: When yields rise, as they’re right now, the bondholders get stuck with a bond whose price is plunging, and Amazon isn’t about to call them. In June 2020, with perfect timing, Amazon sold a pile of bonds at the record-low interest rates and yields prevailing at the time. It included $2 billion in 40-year bonds, with a coupon of 2.70%. Alas, interest rates have surged since then. And inflation has exploded. The three-year Treasury yield is now 2.75%, and CPI inflation is nearly 8%, and Amazon isn’t about to call its cheapest-money 2.7% 40-year bond, which matures in 2060.

The price of that bond has plunged by 25% from 100 cents on the dollar when issued to 75 cents on the dollar today. But buyers buying the bond at 75 cents on the dollar get a yield to maturity of nearly 4% (data and chart via Finra):

Amazon is a huge and very profitable company, with a net profit of $33 billion in 2021. It’s the dominant online retailer. It bought Whole Foods in 2017 to muscle its way into grocery retailing. Amazon Web Services (AWS) is an immensely profitable provider of data centers and cloud services. Amazon has moved into advertising in a big way to compete with Google. It creates entertainment content, and has expanded into entertainment with its $8.5 billion acquisition of MGM Studios in March. Amazon has gotten so big that it can do pretty much whatever it wants to.

And surely, investors will be clamoring for its bonds, including those 40-year bonds. If it turns out that they’re also callable, their prices will drop as yields rise, which is likely in this environment; and if yields fall, and a capital gain could be in the works for those bond holders, or just the enjoyment of decades of a decent yield, well, then Amazon will call them at face value and end the fun.

But there has been a lot of yield chasing out there especially among the riskiest corporate bonds, and so why not also plow into a callable 40-year bond.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Amazon shares were a really good buy at $7 per share at the depths of the dot-com crash in Spring 2000. Not so much at any price past $700 per share, though!

stocks, bonds, wally street wonders

keep em’

unless I can control at least 51%(or 100%) I don’t want it

who did I learn from??

oh, YOU MAKE YOUR MONEY ON BUY and collect when sell

MW Breaking: Stocks end sharply lower as Treasury yields extend rise

What is “MW Breaking”?

I think it’s MarketWatch.

NIFTY PERFORMANCE BY US STOCKS TODAY TO START THE WEEK…

US MARKET UPDATES – 1:04 PM PDT 04/11/2022

Dow 34,308.08 -413.04 -1.19%

S&P 500 4,412.53 -75.75 -1.69%

Nasdaq 13,411.96 -299.04 -2.18%

GlobalDow 4,033.46 -20.27 -0.50%

Gold 1,956.50 10.90 0.56%

Oil 94.80 -3.46 -3.52%

What does your post have to do with the Amazon bond article?

I’m pretty sure most of us here get daily market updates. No need to give us interim day stats. But thanks anyway.

Also, you probably saw that the DXY hit 100 just as you predicted.

Great Information!

How many other companies will be pushing to issue bonds now, while they can still get reasonably low yields, in order to make sure they have the cash-on-hand to survive the coming financial tsunami?

Bag-holder bait. Well told, Wolf!

When Amazon turns too much to financial engineering, watch out.

MW: Bitcoin plunges below $40,000. Here are important levels to watch…[try ZERO!!!]

BitCON has been infested by billionaire “whales.” It’s nothing but a speculative gambling trinket relying upon the greater fool theory. Once the grifter Elon Musk announced that he had purchased an unknown quantity with Tesla company funds – an outrageous act for a company – it has, not surprisingly, levitated at or above that ~$36k price he bought it at. There are a lot of billionaires trying everything they can to maintain its high price.

Elon needs his attention deficit and integrity deficit meds adjusted. Maybe his legions of fanboys do too.

And I wonder what Amazon will be like in the wake of Bezos, as Bezos spirals off into whatever-land. At least Amazon’s proportion of vaporware has been relatively modest.

Elon tweeted a message that blatantly “encouraged” his TSLA share price up ($420 going private funding secured, remember?), and now tries to frontally outgun (out-spend) the SEC and twitter to cover for it all. He is the poster boy for .001-percenter hubris and folly.

Musk-scheme is the new Ponzi-scheme. It’s same, only million times larger.

“now tries to frontally outgun (out-spend) the SEC and twitter to cover for it all”

He brought a major stake of twitter (9% if I recall). So now he can exercise his “free speech” with impunity to manipulate further share price and much more. As for the SEC, well, it’s a paper tiger.

EM does walk on water, as Wolf likes to say.

CAVEAT EMPTOR!

Should be in big red letters.

It’s a very big win for Amazon and the underwriters: Goldman Sachs et.al.

SSDD!

B

Tis a gang$ter’s huckster paradise, wot it be.

Pity, those bonded cornholders …… well, not really.

Fed-Bonds-Yoelds

Recently the UST 2–year hit 2.31% compared to 1.85% on the day before the Fed’s mid-March 25bps rate hike.

The 2–year note puts the Fed 21bps more behind the curve than when it hiked rates 25bs. As anyone around in the late ‘70s knows, once the Fed gets meaningfully behind the curve, baby steps are counterproductive. Only Volcker–like action works’

There is nothing comparable in the last 60-years to the February 2022 real yield (10y) of -6.08% on a regular CPI basis. Even at the peak of the 1980s inflation blow-off the real yield only reached -4.18% and -4.70% at the top of the first oil crisis in December 1974.

This lowest real yield in 60 years is not the end of the story. It can actually be well and truly said that the biggest bond bubble in 800 years is now deflating, and that will make all the difference in the world.

The global bond market bubble is deflating at a fearsome pace. The value of global bonds dropped by another $754 billion just last week, bringing total loss from the recent all-time high in mid-2021 to a staggering $4.8 trillion or 7%.

The yields are so artificially suppressed that once it becomes evident to the speculators and front-runners in the bond pits that the central banks’ bond-buying cavalry is not coming back anytime soon, it will be Katie-bar-the-door on yields and, consequently, lights out for TINA in the stock market, as well.

h/t (David Stockman)

Message is crystal clear but Equity investors are still smoking ‘Hopium’, as usual!

I think what you are saying is that there will be no FED PUT this time when the equity market crashes. Correct?

They will let it CRASH slowly, but won’t interfere until S&P loses at least 50% from the peak. Then may be,(?) but they are already behind the curve in controling inflation.

DEBT to GDP is over 130%. Global DEBT debt to GDP is nearly 350%!

All in record territory! Mkt cap to GDP(USA) is close to 200% ,if NOT more!

Reversion to the mean, will keep long way and then some SOUTH, before Equities in fair valuation ( Not cheap, like in 1982 , when the PE (s&p) was around 7%.

Those in retirement and close to retirement will like thise who retired in 1964, when the DOW was 1000 but kept declining and never come back until 1982! 18 yrs of Bear mkt.

This could be worse this time b/c of excess debt(+leverage) unlike in human history. I hope I am wrong! Count all the HEAD winds out there!? Many won’t believe it b/c it is so UNREAL just like Bull mkt since March ’09 was so SURREAL! Time will tell. Seen it, gone throught it ( more than once) and survived! Those Nrebies 45y and under will be a witness for BEAR mkt of their time (h/t Jimmy Rogers)

You can all thank Fed and other CBers, who didn’t correct the global financial Banking in 2008 but papered over them, record CREDIT expansion and kept the ZRP, too long!

Piper is there to collect payment, due for him. Again, I hope I am wrong but our Karma won’t be!

You’re right in pointing out how negative a call feature can be for the buyer of a 40 year bond. All the downside, but very limited upside (if rates move).

Wonder if Amazon, like so many others over last few years, has removed bond covenants that 10 years ago would have been standard bond-holder protections. I’ve read of other bond issuers, mostly junkier issuers, doing that.

Fannie Mae is issuing these callable bonds as well. I almost bought one, before I noticed the call feature. I decided it was a dumb investment. If the offered rate was 6% on a callable bond, I might think about it a little harder.

Bonds with 40 years maturity ? Meh…

Diamonds and Amazon are forever !

(old wisdom updated)

Why not issue “perpetuities” ?

7% perpetuities aka consoles were often mentioned in Jane Austen novels.Income generated therefrom not only covered daily expenses but something extra was left for fox hunting etc.

Gold Standard in the 19th century.

Bingo. It worked back then, didn’t it.

Austria reportedly issued a 1000 YR bond at 1.2%. I don’t know if this is true and the amount wasn’t reportedly that high, a few billion.

Argentina issued 100YR bonds a few years ago. Heard that from many sources, including here. Several others have reportedly done likewise.

Argentina issued the 100-year bond in 2017 and defaulted on it in 2020:

https://wolfstreet.com/2020/08/04/why-wall-street-loves-serial-defaulter-argentina/

In terms of Austria’s 100-year bond, issued in 2017, I cannot look up its price easily, but by March 30, it had collapsed by 55%, according to Bloomberg. You can always hold it to maturity (2117), collect your minuscule interest till then, and then get face value. Well, not you, your heirs.

Surprised nobody jumped on the bandwagon. Probably because of the 55%, but in these times?!

Brent,

It’s not the 40 years but the “callable” feature that’s the problem.

Mr. Richter;

Strange as it may seem – perpetual bonds are STILL being issued (by GM or GE for example).

“Five High-Yielding Perpetual Bonds to add to your Portfolio”

As to “callable” contract clause, it may or may be not clearly stated, but always implied.

Both British Empire and British Consols were supposed to last forever. Then in 2015 limeys realized that their “perpetuity” is not perpetual, not perpetual at all…

Clear-cut case of “adhesion contract”, Gov vs small scattered bond holders.

My point is – Amazon needs Aura of Perpetuity more than ever and must issue perpetual bonds as a publicity stunt.

US corporate bonds, CDs, etc… if they’re callable, it is stated in the contract. If it’s not stated in the contract, they’re not callable. Bonds are contracts that the issuer has to stick to. Everything is is writing. There is nothing “implied.” If the issuer doesn’t stick to the terms of the contract (covenant), it’s a default.

However, the company can default and threaten with a bankruptcy filing, in order to push bondholders into restructuring its debts. So bond holders might agree to take 20 cents of new bonds for 100 cents of old defaulted bonds, representing an 80% haircut, if the other option would be an even bigger loss in bankruptcy court. This type of debt restructuring is a form of default and is NOT part of a callable feature.

Whether the bonds are callable or not, their price will drop if yields rise.

Yes, but if they’re not callable, you have the huge upside when yields fall. So with non-callable bonds, the deal is in balance, big upside, big downside. The callable feature removes the upside and leaves you with the downside.

I agree. It looks like you re-wrote the section related to my comment. Back in about 1988, I learned the folly of investing in high coupon bonds with anytime calls. The bonds in question were housing bonds with calls allowed from mortgage pre-payments.

Upon your comment, and a few others here, it seemed that the way I had structured the section was less than clear. So I added a summary line at the top of the section that immediately sticks out; I think people might have missed some of the more detailed explanations a little further down.

Why does Amazon have to issue bonds when it’s clearly profitable, other than financial engineering in a distorted financial system?

Possibly to cover the $10 Billion it’s going to burn to buy back stock as Wolf mentioned in the article.

It was kind of rhetorical. I was thinking, if you issue callable bonds at 4% interest, and inflation is running at 7+%, you come up on top.

Financial engineering either way.

Including for share buybacks, acquisitions, and repay callable bonds. From Amazon’s prospectus:

“The net proceeds from the sale of the notes will be used for general corporate purposes, which may include, but are not limited to, repayment of debt, acquisitions, investments, working capital, investments in our subsidiaries, capital expenditures, and repurchases of outstanding shares of our common stock.”

Thank you Wolf for the details. But let me translate that prospectus paragraph to street-speak (what I did for 43 years — street-speak).

“When we get our hands on your money, we’ll do whatever we want with it.”

Callable part of the prospectus translated:

“If and when we get the opportunity to pull the rug out from under you on this deal, we will.”

LOL, yes.

Highly profitable is highly debatable. But they do have large revenue selling/delivering $1 in products for 99 cents.

It appears that MND’s 30 year mortgage rate set a new all-time high today of 5.25%.

MND started reporting on rates almost exactly 13 years ago in April 2009.

Insane. Who was calling 7% not too long ago?

Was that also gametv?

I tip my hat to you good sir

Callable bonds should be bought by professionals only and 40 year bonds right now by nobody, lol.

I remember I once bought a 30 year bond long back. It was crazy profitable and I sold it like a fool.

“Men who can both be right and sit tight are uncommon.”

WOLF – you state:

“…..Amazon isn’t about to call its cheapest-money 2.7% 40-year bond, which matures in 2060.

The price of that bond has plunged by 25% from 100 cents on the dollar when issued to 75 cents on the dollar today. But buyers buying the bond at 75 cents on the dollar get a yield to maturity of nearly 4%…”

I have never understood bonds – but if I bought this 2017 bond with 35 years still left on it with a 2.7% coupon (interest rate), but I am only paying 75 cents on the dollar for the bond, am I not receiving a 29.7% yield (25% discount plus the original 2.7% coupon rate)?

How does it go from 2.7% to 4% when you are paying 75C on the dollar for the bond?

No, divide the 2.7% yield by .75.

That’s how you get to 4%.

because the 25% yield is in the aggregate until maturity, not each year.

Here’s my amateur understanding of Wolf’s characterization. A $100 face value bond with a yield of 2.7% pays $2.70 per year. If you purchase the bond on the open market for $75, you still get $2.70 per year, but the new yield is calculated against your purchase price, which works out to 3.6%. So Wolf is being a little generous calling this “nearly 4%.” If you want to include your purchase discount in the yield you would divide your $25 discount by 35 years remaining: $0.71 additional annual yield, for a total annual yield (coupon plus purchase discount) of 4.5% I believe there are two reasons purchase discounts are generally not figured into bond yields: first you would have to hold the bond to maturity for the calculation to be valid. Second comparing bonds would be much more difficult because every buyer of a particular bond would have a different purchase price rather than the face value. Anyone more knowledgeable than me please offer any corrections.

bond_novice,

“…which works out to 3.6%. So Wolf is being a little generous calling this “nearly 4%.”

Please see my comment below about “yield to maturity.”

Augustus Frost – Jake W – Bond Novice – John H – Wolf

Thank you. :-)

Beardawg-

Buy a Texas Instruments BA II Plus calculator with an excellent Bond Calculator function.

If you enter:

Present Value

Future Value

Maturity date

Coupon Rate

It’ll solve for yield to maturity.

(Or any combination of above to solve for the unknown variable)

And they sell them a….. Amazon!

Priceless.

Beardawg,

“Yield to maturity” – that’s the key term here.

If you buy the bond today at 75 cents on the dollar, so $750 for a bond with a face value of $1,000, you will get $27 a year in coupon interest (the 2.7% per year of the $1,000 face value). So at a cost of $750 per bond, it would be a yield of 3.6% per year. BUT WAIT…

In 2060, God willing, the bond matures and you get face value from Amazon, so $1,000. So your yield to maturity is the entire stream of coupon interest payments of $13.50 every six months until maturity PLUS the capital gain of $250 ($1,000 face value minus $750 purchase cost) spread out over the remaining years of the maturity.

Since this calculation is calendar-based and requires dates, it’s difficult to calculate by hand. Back in MBA school, in 1984, I bought an HP 12c Calculator (which I finally replaced with a new HP 12c) that would do those kinds of calculations. But it still was cumbersome. Now I just go to a yield calculator on the internet, or as in this case, I took the figure from Finra.

If you buy a bond from your broker, they will, or at least should, always give you the yield to maturity.

If you buy this in any size watch rates and when they start to drop put on a hedge. There are probably plenty of institutional buyers for this. For the retail guy it looks like the hook. Sometimes these things are convertible to stock, often preferred. Is this considered a “blue chip”?

Institutions do not care because it isn’t the fund managers money. Anything to get a few extra basis points in yield to beat their benchmark.

For the retail buyer, the math has never added up for me.

It isn’t just the credit risk though that’s usually enough of a reason to say “no”.

It’s also the after-tax yield differential. The yield spreads have been so narrow for so long that after accounting for state income taxes (which apply to corporates outside of deferred retirement accounts), there is little left on higher grade issues.

These are NOT convertible bonds. They’re callable bonds.

“ Little upside: For example, the $16 billion in bonds that Amazon sold in 2017 to fund its acquisition of Whole Foods also included $2.25 billion of callable 40-year bonds, with a juicy coupon of 4.25%, that Amazon then called in mid-2018 at face value. Folks who thought that they’d get the steady coupon payments of 4.25% for 40 years got instead their money back and had to kiss those nice coupons and capital gains goodbye.”

Therein the rub…

I buy $2 million in bonds and tie up my money expecting some return from a ”growth” company…

One year later you give me my $2 million back with no return and say thanks for playing but we used your free money well…

So basically, I have loaned you the money free fora year and have forgone anything I may have earned while you have my money… and I didn’t even get free or even discounted Prime because I don’t have an EBT card….

BTW, how much of this did Bezos buy ?

Lotsa life lesson from Forrest…

Stupid is as stupid does….

Say, are you having another offering soon ?

Asking for a friend….

New phrase for TINA this is not acceptable.hahahahaha

Amazon is a plague. Occasionally I buy something from them if I have no other choice but I and the other 22 members of my extended family are boycotting them.

IF amazon is ~2 Trillion company why does it need 0.01 trillion?

IF amazon stock gives more than 100% return in just one year, why should investor buy amazon for mere 4% return?

The market cap of $1.57 trillion now (was $2 trillion) = number of shares outstanding x share price.

This has nothing to do with the cash that Amazon actually has and needs.

Amazon stock is down 20%.

These were rhetorical questions.

“Intrinsic value is the number you get if you can predict all the cash the business can give you between now and judgement day.” – Warren Buffett

So if Amazon doesn’t even have 10B cash, I think it will never generate 1.5 trillion cash, and it’s ~1.5 trillion value is not justifiable. This is the point I am trying to make.

And if stonk went to the moon and generated 100 percent return between march 2020 dip and top , why should anyone buy bond for 4 percent return?

This bond offering suggests the fallacy of amazon market value, imo.

“These were rhetorical questions.”

I can see that now. They were funny, actually, when seen in that light. A sarc tag might have made it a little easier for me :-]

Wow…so Amazon treats its bondholders just like it treats its employees?

Amazon wants co-conspirators to finance its malice who actually like getting diddled. That way they don’t have to pay for it.

NAILED IT LOL

You literally took the words right out of my mouth. I was going to comment this exact same thing and you beat me to it.

Fool’s gold. Sadly people will buy them anyway in the hope that Amazon will be generous 🤣

This bond issue is wrong on just about every basis you can name.

– Amazon systematically abuses its market power and should be broken up as an antitrust action.

– Making a bond callable contractually enables screwing the investor.

– Share buybacks signify a crooked corporation and is only legal because of regulatory corruption.

– Doing business with Amazon supports labor abuse, tax evasion, regulatory corruption, and customer coercion.

– And so forth. Page and a half single-spaced.

If I still had an outrage gland it would detonate. Which is why I don’t go in to have the last one replaced because it detonated. Better off without one so I don’t get outraged.

So, for now, Amazon is in like a Tyrannosaur .. but like most giant behemoths, eventually it too will be kicked to Evolution’s curb, like a Dodo!

Time × circumstance = devolution

Weirdly, what you say resonates with me because I suspect that America’s flagship companies are like vaporware.

time x circumstance = devolution

Generally speaking, perhaps. Maybe

time x circumstance = age

Old people only remember lust, the sha du vua.

“I suspect that America’s flagship companies are like vaporware.”

True enough. Wall St. has long coerced corporate America to pay tribute to the Financial Industrial Complex. Or else.

As a result virtually all US corporations greater than a certain size are largely specialists in finance and financial engineering. ‘Products’ and ‘services’ are side lines, useful for maintaining pretenses. Virtually every S&P 500 listing is like that, although there are still a few exceptions in the Russell 2K.

Not everything from “flagship” companies are vaporware of course. Google’s self-driving taxis (Waymo) will likely be game-changing. ((I mention them because they seem to be the leader but autonomous vehicles in general will be game-changing.)

But it’s true that a lot of the values are placed in vaporware. There is no better example than crypto and its derivatives. Technically, it’s hardly innovation. But the amount of talent and time invested in this space is huge, and growing.

It must have something to do with “profit velocity”. Projects like Waymo will take years, if not decades to turn in a profit, while crypto ICO and NFT take merely months for their creators to meet their huge payday.

So, the bond buyer is gifting AMZN a call option on the buyer’s future gains — for free.

Phleep-

I’m guessing that if the bonds were non-callable, the bond would have yielded less… that’s the way the bond market works.

So Amazon is not “gifting” this security to anyone. It is “selling” the bond, and all the features in its indenture. And some investors (arguably a little nutty) are buying the bonds — voluntarily.

Bond buyer’s have not been “screwed” as accused by commenters above. Value, in a free market, is in the eye of the beholder.

And what is this free market of which you have spake. The one that is controlled by the Federal Reserve bank to suppress interest rates to zero.

Personally, Im not surprised that the Fed keggar turned out the way it did, having observed the reliably unfortunate outcomes of a number of keggars, in my past.

What I can attest too is that caution was never the mood of the day.

Since I was raised in a religious environment, praying that it would take, I can honestly admit that I have also prayed for salvation a number of times. So far it seems to have worked.

Dang-

I agree with your disgust with Fed’s 108 years of manipulating. That’s NOT free market. Somehow eliminating the Fed, or at least shrinking its footprint would improve the free market, as you suggest. Sadly, it’s power and tools just keep growing.

But half of what makes this article noteworthy is that the buyers of this $50 Billion bond issuance are willing to accept the terms. They are buying based on their assessments of the future. They are not victims — they are actors — and if they value the choice offered by Amazon enough to plunk down $50 large large large, then God bless ‘em. We can only hope that losses they take (if any) don’t get subsidized by taxpayers.

As for Amazon, their stock valuation is mighty rich, and always has been. Anyone who bought it since inception (except for very recently) and held has been richly rewarded. I’m not one, to my chagrin, but I respect the individuals who had more foresight (or dumb luck) than me. They were Free To Choose, and they won on this one.

Finally, corporate CFO’s are charged with making good capital allocation decisions. If I were a CFO and could raise $50 Billion at sub 5% terms, I’d sure consider it. I’d be liable to my stockholders if didn’t, wouldn’t I?

Colorful autopsy of a corporate bond play, describing in detail how everyday people are exploited every day. Financial engineering used to be referred to more honestly, grift.

I’m thinking that the cessation of the sour wind that blew the stock market bubble is likely to cause a deflation of said bubble back to the fundamental basis before the Fed did what they did.

Long term portfolios have handled 50% losses four times in my life. So, buy and hold has always been a winning strategy for young people and the source of lament for the old.

The problem with that strategy atleast for people like me who have their company 401k is choice. The 401k is usually one of the big scumbags on wall street with half a dozen investment choices. I should be able to plop my 401k money in theranos or enron or adelphia communcations if I wanted to.

Yeah, well, I know what your talking about, unable to exit the market risk because your 401K doesnt offer a vehicle or fund that is neutral.

Roll your 401k into a brokerage account and buy short term treasuries.

” There’s no point in being a grifter if it’s the same as being a citizen”- Henry Gondorf, The Sting, 1973

So who buys this stuff other than fools and big institutions that are doing a favor for Amazon?

So apparently CPI inflation numbers are going to be so bad that the BLS is leaking it ahead of time

Can’t wait to see what the numbers are tomorrow

I’m sure the markets will take it well.

I’ve never seen the markets getting prepped like this for a massive CPI print, from the White House down, which now calls it the “Putin Inflation” after having blown off the inflation all last year as “transitory inflation.” This is how we went from “transitory inflation” to “Putin inflation,” from one month to the next. So when your landlord jacks up the rent by 30%, they’ll include the phrase “due to the Putin inflation.”

Firstly, Wolf, I admire your fearless exposition of the obvious, unprecedented failure of monetary policy in my lifetime.

I expect a WTF moment tomorrow when the CPI is announced for March which I expect at > 8 pct.

The inflation print really belongs to Trump rather than Biden. While I understand the attempt of the current administrations attempts to explain a sucker punch, they were set up to take the fall.

Should they have immediately moved to stop Brownie at the Fed, maybe.

It belongs largely to the Fed. The Fed is in charge of the dollar and inflation (purchasing power of the dollar).

OK, I agree that the Fed went feral and failed, in a manner that leaves no doubt as too their incompetence but not to put too fine a point on semamtics, I question whether the incoming administration (Biden) had any idea what the former administration (Trump) had created at the Fed:

dang,

BTW, I hope you see this: You have posted 15 comments on this article with 93 comments at the moment. Of them, 8 are visible. The others I stopped, and I might let them pass as we get more comments here.

Commenting guideline #4:

4. If about 5% of the comments under one article are yours, it’s time to back off. So if the article has 80 comments and 4 are yours, it’s time to slow down. If you’re in a substantive constructive discussion with another commenter, some back and forth is OK. But once this discussion is starting to hog the comment section, or becomes argumentative, it may get blocked.

https://wolfstreet.com/2017/10/07/finally-my-guidelines-for-commenting/

Whether intentional or not, Congress, the Treasury and the Fed handed out way too much newly printed money during the Pandemic. It’s probably going to go down in history as one of the biggest financial blunders the US has made.

Dang, remember that basically team red and team blue both voted for profligate deficit spending which was monetized by the Fed, which gave us the gift of inflation that keeps giving.

Let’s keep it clean and keep it intellectual here at Wolfstreet. No partisan rabble rabble rabble please

8.4%

Surprisingly, the DOW is up 240 points this morning. With CPI inflation so high, I would have expected a negative open. But what do I know, anyway?

@Anthony A.

It could well be a bait, as if to signal the market is shrugging this off; so that suckers feel safe to get in. Then, the unloading would happen in the coming days or weeks.

Someone help me understand this… As a few folks have pointed out above, mostly institutions will by this stuff. So lets say hypothetically Silverman craps is my 401k manager and have invested my money in a pile that includes 10% bonds. Will SC be able to purchase some of this Amazon stuff and make me a holder? If amazon plays their thievery and returns the money at the worst possible time, do those losses show up on my SC 401k account (whatever % that may be).

Amazon is not committing theft if it issues callable bonds. Chances are, a lot of 401k and pension plan managers will be buying the Amazon bonds. If you work for a small employer that offers a 401k plan with high fees, I would be more concerned about the high fees of the 401k plan. If you are concerned about your retirement savings, spend more time learning about investments and less time watching TV.

Get off your high horse, not everyone has to be a finance major, people are in other professions. Sounds like you might be a money manager trolling the conversation.

You should apologize to the poster…

Ever since the advent of 401k and other retirement schemes were perpetuated upon the unsuspecting public, the responsibility for your life in your later years became YOUR responsibility…

Being ignorant of finance and investing, where to invest for the maximum gain and minimum fees and minimizing loss is the cornerstone of BUILDING a retirement scenario…

These things take many years to play out and you have to be constantly aware of how your nest egg is protected…

Unfortunately, many people don’t get serious about it until in their 50s and then it’s too late…

Had they paid attention in their 20s and 30s, it could make a difference between $500k or $5 mil…

If you did pay attention, good for you….

If you didn’t, sucks to be you cause you’re probably too late…

Sound advice above…

In other words, buying an Amazon bond is like buying an NFT with the pixelated face of Bezos. You’ll lose most of your money, but you’ll lose it in a SUPERCOOL way, which is the only thing that counts.

There are entire industries devoted to manipulating and exploiting the Neurotic Human Need to Feel Special – financially, politically, and with malice aforethought. Most people are not very good at recognizing the manipulation and avoiding the traps. One way or another most people get played rather constantly.

There are, of course, inexpensive and constructive ways to feed ones Neurotic Human Need to Feel Special without getting suckered, but your Culture of Mass Marketing naturally co-opts them to make them more profitable.

They’ll bankrupt you if they can for Fun and Profit without a second thought.

One must be careful.

1) Higher interest rates are good for small businesses, bad for the FANG.

2) Nasdaq 100 futures, NQ monthly : Nov 2021 high to Mar 2022 low is the the first stopping action. A bullish option :

3) NQ retraced 0.382 of the wave from Mar 2020 low to the top and that’s is good enough. 4) NQ monthly : the area between July 2021 close and Mar 2022 low is a “Bearish Zone”.

5) After three months in the Zone Apr might close above.

6) After a test NQ will breach Nov 2022 high and keep moving higher.

7) Recession : a round trip to the Zone in 2024/25.

or the market will decline month after month like it did in 2006. Until it was reignited by the QE1 and 2, which wasn’t enough so we added 3 and 4.

It certainly made geniuses of a whole lot of dumb people who have capitalized on their good fortune and the magnificent Federal Reserve, handing out dollars to the well to do like candy at trick or treat, depending on which neighborhood you belonged,

Why are higher rates good for small businesses?

A question, not questioning.

This kind of blatant market manipulation should be illegal.

Scott,

I don’t think it was manipulation to start with…

From the time the bond was issued, AMZN stock increased from around $800 to around $1800…

I’m not a CFO by any means, but that amount of stock price increase may have been a factor to call the bonds and eliminate the debt…

“ Buybacks are a fairly new phenomenon and have been gaining in popularity relative to dividends recently. All but banned in the US during the 1930s, buybacks were seen as a form of market manipulation. Buybacks were largely illegal until 1982, when the SEC adopted Rule 10B-18 (the safe-harbor provision) under the Reagan administration to combat corporate raiders. This change reintroduced buybacks in the US, leading to wider adoption around the world over the next 20 years.”

https://corpgov.law.harvard.edu/2020/10/23/the-dangers-of-buybacks-mitigating-common-pitfalls/

To paraphrase an old joke, a callable bond, ANY callable bond is like an umbrella the issuer wants back as soon as it starts to rain.

For the life of me I cannot understand why anyone would invest in a callable bond.

“ For the life of me I cannot understand why anyone would invest in a callable bond”

Desperation…. hoping to make some interest at a higher rate vs hoping the bond isn’t called before any interest payout…

This intrigued me so I looked it up… there was a demand of $49 billion on a $16 billion offering… AMZN could have gotten 3 times as much money but probably couldn’t have committed to that much interest expense…

As it turned out, they need not have worried about such nonsense…

Most retail investors know very little about bonds. If they were all that knowledgeable, they would always pick no-load bond funds over load bond funds. Even fund managers may have different objectives than investors. The fund managers may be under pressure from higher ups to report a higher yield for their funds to make the fund more saleable, rather than to achieve the highest total return (fund performance).

If you have ever had to review a county government pension plan, you might have noticed that the board of directors of the plan were more qualified to be union shop stewards and had little or no background in finance. As long as fund managers are in the middle of the pack, their jobs are probably safe.

I think it is for those that have too much money and need a place to park it, relatively safely. If you had 200 mil, would you put it in a bank? buy treasuries? bonds? buy gold and bury in the backyard?

I would maybe put it in bonds but not of the callable variety.

The US Dollar is doing extremely well and is now at 100.16 on the DXY.

Wolf-

Don’t MBS bonds work similarly to the callable 40 year Amazon bonds? An MBS will become a very long (tho dwindling) long hold if rates rise, heightening interest rate risk to the bond-buyer, and a built-in call feature in the form of the right to pay off if the borrower is able to refinance to lower rate, or if he moves or dies?

If they are similar, then the fact that an “A” rated tech company can issue bonds at a lower rate than an U.S. government agency-backed security speaks volumes about investor faith in the latter.

Are most MBS callable?

Pass through payment of principle is one thing, but callability is arbitrary / controlled?

PG-

They aren’t callable per se, but the borrower can repay them at any time. From a banker’s standpoint, the loan can be repaid early solely at the discretion of the borrower/homeowner.

MBS are usually backed by a collection of mortgages, so they don’t get “called” the same way as an individual bond. But when rates decline, the “average maturity” assumptions shorten up. Worse, when rates rise, the average maturity assumption extends. They call this maturity extension risk, and it played a part in the mortgage crisis, I think.

Lots more weeds to parse. This concept will resurface if and as mortgage rates rise in future years…

PG-

If you’re interested, search PSA + mortgage

John H.,

They’re similar, but very different.

MBS can get called after a lot of the underlying mortgages have gotten paid off, and the principal of the MBS has shrunk substantially.

Each time a homeowner makes a mortgage payment, or pays off the mortgage through a refi or sale of the house, the principal payment is forwarded via the servicer to the GSE (such as Fannie Mae), which then forwards those principal payments to holders of the MBS. For example, on the Fed’s MBS holdings, these pass-through principal payments exceeded $100 billion a month last year.

Each time there is a pass-through principal payment, the remaining balance of the MBS shrinks, and after a few years, the MBS is pretty small, at which time it gets called, and the remaining mortgages get packaged into new MBS.

For example, you might buy $1 billion in MBS, and the pass-through principal payments start rolling in. After 2 years, you might have gotten paid $200 million in pass-through principal payments, so you’re sitting on $200 million in cash; but your MBS holdings have shrunk to $800 million. After a few more years, your MBS holdings may be down to $300 million. And then they get called, and you get the $300 million.

Falling mortgage rates cause a tsunami of refis and pass-through principal payments.

This is one of the risks of MBS, and that’s structurally how they’re different from other bonds.

Thanks, Wolf. I didn’t remember that there was actually a call feature following significant pay down.

My point was that a couple general effects are similar to the callable long bond problems:

1. In a falling rate environment the holder gets money back that he’d rather keep invested at the called bond rate.

2. When long rates are rising, you get all of the decline allotted to a long bond holder (and then some if you get caught in the maturity extension trap).

Thanks for the stimulating subject matter and nuanced explanations!

I know this is highly off topic, but is there anyone here with knowledge on eurodollars and eurodollar lending/creation ?

I think there is a lot of focus here on WS on domestic dollar / credit expansion, but what about the foreign international markets?

Snider has a lot of fun fiction about eurodollar creation. Go over there to revel in it.

Thanks Wolf. Snider was how this topic came up.

When you say fun fiction, is that tongue in cheek or do you actually believe his stuff is nonsense?

“… or do you actually believe his stuff is nonsense?”

“Believe” is something I do in church :-]

Touche Wolf.

I can never get a GDF straight answer out of you lol

Callable bonds are not for unsophisticated investors, but there is a play here:

Amazon is known to call bonds when interest rates go down. Let’s say that Amazon prices these bonds at a 4.5% yield, which is the prevailing rate. We know interest rates are going up. But then, I predict in a year when the housing market crashes and stocks are down and wall st starts squeezing it’s paid politicians, the Fed will start lowering again (the market is pricing in 2 rate cuts in 2023).

The play here is to wait for 6 months. When interest rates are at 6%, this batch of bonds will have lost 25% of their value. Then buy them and wait for rates to go back down to 2% at which point they’ll be worth 20% over par. Amazon calls the bonds at par and you walk away with a 25% profit in a year.

IOW, yield to maturity calculations can make early callable bonds work in your favor *if* you buy them for less than face value.

The point is that callable bonds can be profitable but they’re sort of like options: timing the interest rate fluctuations is crucial.

Is in the name “unsecured bonds” they are non secured aka they are a bad investment unless you are Amazon.

It means that that they’re guaranteed by the company but are not backed by any specific collateral. So if that company goes bankrupt, bondholders are likely to just get a few cents on the dollar. If the bonds were “secured,” they would be backed by some collateral, such as real estate that the bondholders would get in the case of a default. And then they might not lose any money.

Great article! Buy I bonds instead. Easier to understand and less risky.

$10k a year limit per entity. That’s the only drawback.

Hi Wolf

Could you clarify the callable nature of these bonds.

The 2017 AMZN bond has a CUSIP of

023135BM7

Amazon.com, Inc. 4.25% 08/22/2057 Callable

The bond is “make whole” call at anytime

But the bond is callable at par (100) per:

Callable in whole or part Daily beginning 02/22/2057 with 30 days notice.

Do you have the details of the terms of the called bonds in 2018 on this bond? (or where I can find them)

Was it possibly a “make whole” call on the bonds, or were they actually called at par in 2018, prior to 02/22/2057 as stated in the article?

As you know, typically a “make whole” call is done at the treasury rate plus x basis points based on the tenor of the bond.

I did look at the prospectus linked for this particular bond issue and as you said, those terms were all blank. Is there a filled out prospectus, now that the bonds have actually been issued?

thanks

Ida Sa

Ida Sa,

You can get the most recent Amazon filings here:

https://ir.aboutamazon.com/sec-filings/default.aspx

These recent filings include the prospectus with the blanks now completed, and that may be what you’re looking for:

https://d18rn0p25nwr6d.cloudfront.net/CIK-0001018724/beae1c3e-26fc-44ce-b5eb-ed1c3f6f6d63.pdf

The CUSIP on that bond above is incorrect (that CUSIP was for the 2018 bond), but I still have the same set of questions regarding the terms of the bond. Aren’t most of the long term bonds like these only callable at par very late in the maturity cycle?

They are “make whole” callable throughout but not necessarily callable at par throughout.

I did find the original bond CUSIP AO7856195 that was called.

https://www.bondsupermart.com/bsm/bond-factsheet/USU02320AK24

Thanks Wolf.

That prospectus has the information.

Amazon.com, Inc. 4.1% 04/13/2062 Callable

CUSIP 023135CK0

If anyone is interested, the call details on the 40Y are

****Callable at par beginning 10/13/2061 (6 months prior to maturity)

Callable in whole or part Daily beginning 10/13/2061 with 10 days notice.

****Make Whole callable from settlement date (4/13/22)

Make whole call Daily beginning 04/13/2022 with 10 days notice.

Valuation based on the greater of: (valuation at discount rate of “Treasury rate” + 20 bps) OR (at par)

“plus, in either case, accrued and unpaid interest thereon to the redemption date. “