Junk bond yields actually fell over the past month and are historically low.

By Wolf Richter for WOLF STREET.

The yields of US Treasuries have spiked in recent months to multi-year highs, and mortgage rates have spiked, and yields of investment-grade corporate bonds have spiked, and bond funds have served up losses to their investors, and investors in conservative long-term bond funds have taken the biggest hit – for example, the price of the iShares 20 Plus Year Treasury Bond ETF [TLT] has plunged 27% since July 2020 – and all kinds of mayhem has broken loose in the bond market.

Except in junk bonds, and especially in the riskiest sections of the junk bond market, where a maniacal chase for yield continues to rage as yield-chasers don’t think that the Fed’s tightening applies to junk bonds, when in fact it applies to junk bonds a lot more than investment grade corporate bonds or Treasury securities because it will tighten financial conditions – that’s the Fed’s expressed goal – which will make it more difficult for many of these junk-rated companies to issue new debt to service and pay off existing debts, which is what keeps these companies that make up the riskier end of the spectrum from defaulting on their existing debts.

So here we go…

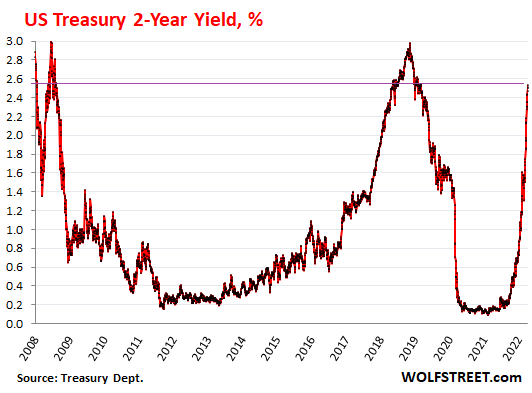

The two-year Treasury yield jumped to 2.53% by Friday, the highest since the 2018 rate-hike phase, and before then the highest since July 2008 as the Financial Crisis was beginning to fully blossom.

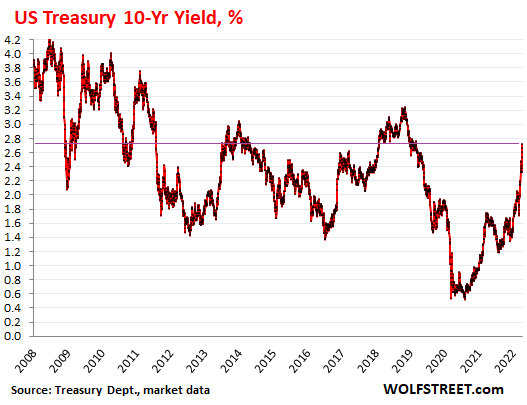

The 10-year Treasury yield spiked to 2.72% on Friday, the highest since the February-December 2018 era, and before then the highest since 2014, at the end of the Taper Tantrum:

Back in 2018, the Fed raised rates four times and was shedding assets on its balance sheet, at a pace capped at $50 billion a month. Inflation was below or at the Fed’s target. In December 2018, Powell began to buckle under Trump’s incessant attacks and reversed course.

Now inflation is nearly three times the Fed’s target and has turned into a political bitch for the White House, and the Fed is under pressure to bring it back down, which it won’t succeed in doing for a long while. But instead, the Fed will chase it higher with too-slow rate hikes and too timid Quantitative Tightening, after having committed policy error after policy error for the past two years, and after having exacerbated these policy errors starting in January 2021, when the Fed began to blow off this surging inflation. So now, there won’t be a Powell pivot to lower rates. Those rates will keep going higher, too slowly, and everyone knows it.

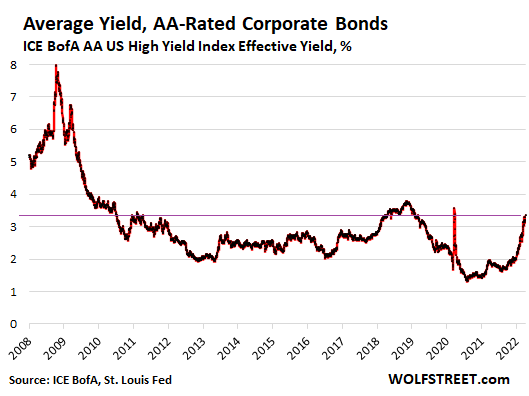

High Grade AA-rated corporate bond yields have been rising too, but since mid-March more slowly than the equivalent Treasury yield, a sign of some yield chasing, with the average yield rising to 3.37%.

During the Financial Crisis, when the 10-year Treasury yield maxed out at 4.2%, the average AA-rated yield maxed out at 8%, as financial conditions were tightening even for these companies:

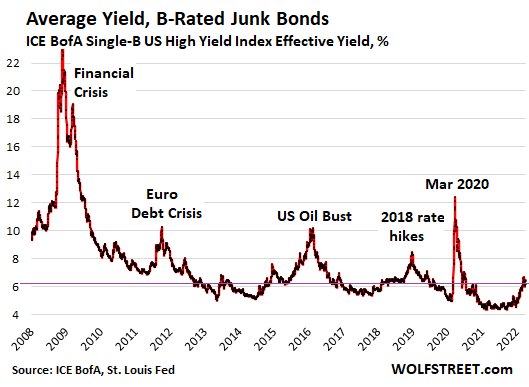

Mania at the riskiest end of the junk bond spectrum.

Single-B rated junk bonds, however, rose only modestly since September 2021, and fell since mid-March 2022, while Treasury yields were spiking. On March 15, they’d reached 6.72%. At the end of last week, they were down to 6.48%, which remains historically very low.

And this yield is still below the rate of CPI inflation! Investors are taking huge risks for still negative, but less negative, real yields.

B-rated bonds are mid-level junk bonds, considered “highly speculative.” That category is riskier than BB-rated junk bonds (“non-investment grade speculative”), according to my cheat sheet for corporate bond credit ratings.

At the risk level of BB, many companies are facing sudden downgrades and default when financial conditions tighten. And every time financial conditions tighten, there are waves of defaults, and yields spike, as noted:

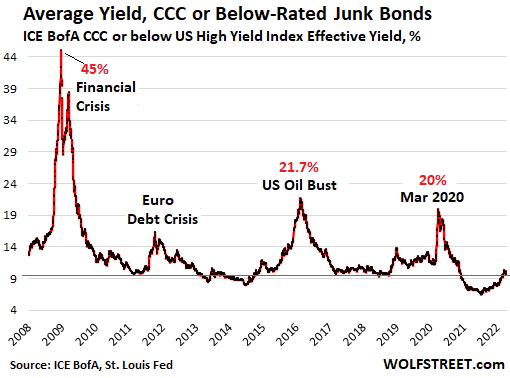

CCC-or-below-rated junk bonds comprise the highest risk category of companies, those whose cash flow isn’t nearly enough to cover debt payments, and with big losses – companies are borrowing on borrowed time, so to speak. This category of bonds ranges from “substantial risk” for CCC-rated bonds to “Default imminent with little prospect for recovery” for C-rated bonds. The next step down is D for default, according to my corporate bond credit ratings guide.

The average CCC-or-below-rated bond yield also fell from mid-March (10.36%) to 10.11% currently. Over this period, as Treasury yields spiked, the spread to Treasury yields narrowed by 81 basis points, a sign that this end of the market is in total la-la land.

This is also the category of bonds to which investors flee to get a yield that is above the 7.9% CPI inflation rate. And they’re taking huge risks to their capital, just to hedge against inflation.

The current average yield, at 10.11%, is near historic lows. Many of these bonds tend to default when the financial conditions tighten to the point where the companies run out of investors to provide new money to pay off existing investors. At that point, a debt restructuring, often in bankruptcy court, can be the consequence, with holders of these bonds taking big losses as these bonds may have been unsecured, or secured by collateral that has become nearly worthless.

What this means is that junk bonds are having some catching up to do, and these companies that don’t have enough cash flow to service their debts are going to face a new reality of tightening financial conditions, which is what the Fed has set out to do by tightening monetary policies. But for now, that segment is in la-la land where investors are still maniacally chasing yields.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What’s the best way to short junk bonds?

There are supposedly inverse bond ETFs, but I’ve never owned one.

TBT and PST

Be careful to really understand the prospectus/how the put actually operates.

A lot of inverse ETFs use mkt instruments that are only good for near term falls…if held for months, they can cause principal to erode quickly (I think it has to do with having to buy and re-buy the underlying puts…perhaps at higher prices).

Anyway, read prospectus in depth…there is a real mkt bias (especially in equities) against providing honest-to-goodness long term puts (maybe because there are few put sellers in a mkt this overvalued, for this long).

Wolf could have a *long* series of posts about the best avl puts for various mkts.

Best to steer clear – long or short. Firms like Aries who specialize in the field and know capital structures inside and out clap onto the prime cuts leaving the crap and detritus that remains to the poor retail slobs to fight over. Classic pack fighting order.

Buy puts in JNK. Perhaps few months out out-of-money puts if that fits your style. Or same with Tesla or Nvidia.

New 52-week low in junk bonds today. They just may fall of a cliff here.

SJB

Every time I invested in Junk Bond Funds I wound up with taxable income and long term capitol losses. I wouldn’t touch them with a 10 feet telephone pole. They tend to follow the preferred stocks in the stock market.

I agree. Junk bond “investors” are actually just stupid, gullible gamblers. On the other hand, I no longer trust ratings companies: they gave AAA and slightly lower ratings to their cronies’ actual junk (subprime-mortgage-based bonds) while those cronies were selling junk that they simultaneously were betting would never be repaid. See “Goldman Sachs FRAUD Charges Filed By SEC Over Subprime Mortgage Securities” in Huffington Post.

Baby Boomers will pull out of the markets rapidly starting later this year and more and more in coming years. Particularly, if there is a market correction with junk and other bonds, so that Baby Boomers’ investments go down rapidly, I suspect that more and more of them will over-react and pull all of their money out of the stock and bond markets.

Thanks for the summary on bonds. It will be interesting to see the effect of the FED rate increases and QE tightening going forward. These charts are very helpful in understanding what’s going on and what’s going to happen as the FED attempts to fight inflation.

10 year to 4.5 – 6 percent, and all hell will break loose. Like Wolf has mentioned, they have no choice if to save the dollar. The Fed will dance, jawbone, and delay tightening all they can get away with, for their fellow comrades.

Sobering quote from last summer:

“The last time junk-bond spreads were this low was in July 2007, not long before the global financial crisis totally upended the perception of risk, catapulting the high-yield premium over Treasuries above 2,000 basis points by December 2008 …”

– Reuters, U.S. Corporate Junk-bond Spread Narrows, Lowest Since 2007, June 17, 2021

When spread over an already dropping base (as treasuries themselves decline), junk bonds will experience massive corrections.

The end of the second paragraph:

“… the Fed’s expressed goal — which will make it more difficult for these junk-rated companies to issue new debts to service and payoff existing debts, which is what keeps these companies that make up the riskier end of the spectrum from defaulting on their existing debts.”

That sums things up spot on. The proverbial snowball rolling downhill and getting bigger as it rolls. But at some point the hill stops, and in time, what’s left of the snowball melts.

It took awhile, but there’s no snow left on the ground where I live.

I’m recalling an acquaintance in 2007 chasing yield by investing in subprime shadow banks. They vanished soon thereafter, and so did he.

These issuers will be first to go under, yet their spreads are NARROWING against treasuries? OMG. There may be no more bailouts in the till.

I hope, but am not optimistic that since inflation spiked so quickly, it can come down quickly. A crypto crash might help 😂.

The best solution for this entire horror show that the FED and CONgress have created would be for everything to massively crash back to reality, and sooner rather than later. Trying to prop up bubbles is a hideous waste of resources, an exercise in futility, and just delays the inevitable.

Prices down.

Salaries down.

Recession required. Just needs a precursor crash.

Can people buy these junk bonds using craptocurrencies?

Of course they can. It’s the new world reserve currency.

Craptocurrency is a just a derivative of currency/money, so just sell it for money and then buy your JNK.

Serves my theory that yields in Treasuries represent a supply issue. Before junk bonds spike in yields US treasuries will downgrade but I seriously doubt that.

I’m making 9.2%-10.85% on several hundred K of Treasury I-bonds I bought around 2000. I wish I would have maxed out my purchase limit every year back then. Who could have guessed the Fed was going to make literally crazy decisions in 2020, though.

I too bought I Bonds back then and everyone laughed at me. Now the 2000 and 2001 I bonds pay 10.8% and 10.64%; but back then I think the limit to buy per year was $60k and there was a fixed and variable % that changed every 6 months.

Today, you can buy I Bonds with $10k per person/year and current interest is 7.12%. You can cash them in after 1 year and lose 3 months interest or keep them 5 years w/o any interest loss. The new I Bonds have a 0% fixed rate (this is a negative since the older ones had about 3.5% fixed) and the variable is whatever Treasury decides – now 7.12%.

You can buy at http://www.TreasuryDirect.gov. May 1 the variable rate changes; so I guess it will increase.

Same here…and I was able to use my CC to buy them earning 1% cash back right away.

Crazy decisions in 2020?

I’m beginning to think they were all sniffing glue since before Bernanke.

Did the I bond rates go down

As inflation was low

@VB Yes and no. The fixed rate is around 3.5%, but for a few years the adjustable rates were “negative” pulling down that fixed component of the yield a little. That said, the rates can never go below a 0% floor.

Most of these junk bonds have their stock listed .

Even though almost all of these stocks have corrected sharply this year , they are still in La-la. Land . So when these companies need money all they have to do is to sell more stock instead of bonds. In doing so these companies are selling more stock far above book value , so there is no financial dilution . In a very real sense , the yields of

Junk bonds seem to reflect the vast overvaluation and speculation of many companies instead of any relationship to Treasuries

Taking one step back from the chaos created when bad economic policy is reversed, I would just like to say that capitalism is normally distributed simply because it is a system devised by a population that is normally distributed by definition.

How is this relevant, I would throw out a thought about the chaos in the interest rate market which our host commented about. Short term, again this is a dumb s**t expressing his whoefully ignorant of the intricacies of intrigue that actually determine the outcome. The Federal Reserve is willfully and seriously in failure to it’s founding and ongoing principles. The required withdrawal of the gross excess liquidity will require much faster QT and the inflation will require much higher interest rates.

Personally, I sense that Ben Bernanke’s hypothesis, suggested by Krugman’s “work”, of QE is mathematically flawed because his models were rammed through the precursor to AI, step wise multiple linear regression with a data set that didn’t include the most important independent variable, zero percent interest not too mentioned a piece of data that has become a model for no good reason, 2% inflation. Something Tony Clifton might have come up with.

I suspect that the zero interest rate model is not desirable in the long term, after 15 years experience of it, it seems to have ended exactly as the uneducated participants of our society said it would.

Someone has too pay. Certainly not the mob bosses.

Suddenly, tea in the Hampton’s is disturbed, Analysis of the miss steps of this empire of the last 80 years, under the tutelage of the least educated people, Harvard, Yale, etc

The dollar as the reserve currency is being questioned. It seems that it seems like funny money. Apparently, it has gotten so bad that bitcoin seems like a viable alternative.

Good job. Brownie Federal Reserve.

last post promise

What I mean by my snide swipes at Ivy League grads is

the are trained more than educated.

By a closed system of wealth and privilege that makes it impossible for them to make a decision that reduces their family wealth which they consider a birth right.

Just one small comment about my neighbors. They moved away, thankfully. They were such party animals that they dragged me into the shenanigans. I admit, I will miss them.

That’s the trouble with younger people they’re not reliable.

Especially in countries with aging populations. As the birth rate falls and people live longer the worst of all worlds is QE. Seniors on fixed incomes earn nothing and go broke faster.

Economic models are complete BS when it doesn’t reflect the behavior of actual human beings, just as anyone would know from common sense.

No amount of data or modeling will ever enable any central planning committee (that’s the FOMC) to “manage” an economy as complex as the US. AI won’t change the outcome. That’s a complete fantasy.

I suspect that the real reason why various economic models continue to be proposed and exist, is that folks who propose them can get their phds/publications/citations, i.e. real benefits for themselves. I came to this cynical conclusion after looking at Paul Krugman – he is a Nobel prize winner and the leading economics prof, and he always quotes bunch of “facts” in his publications, but he has about the same predictive ability as rolling dice. So I concluded that all his “works” must have been to simply achieve benefits and status for himself.

US 10 Year Note Bond Yield was 2.72 percent on Monday April 11, according to over-the-counter interbank yield quotes for this government bond maturity. source: U.S. Department of the Treasury

Imagine the only place in the bond market you can get a proper yield being a grade above default lol.

Even at that slightly above 10%, it still may be negative when you factor the real rate of inflation, and not the false government number.

On this whole tightening a rate rising spectacle; I believe it to be political theater. The Fed has to pretend they’re doing something, but these rate hikes are negligent.

From what I have read rate drops are already baked into 2023. As soon as these markets start to come down, rates will go right back to zero, and QE5 will be implemented.

There are only two paths forward. Default or inflate. My take is on inflate. The Powers that Be will not sacrifice their wealth and investments, because of the poor.

Then the issue becomes potential social and political instability.

From what I gather, your opinion is that the Fed will cave as the asset bubbles begin too buckle. The trillion dollar question.

Given the fools that are in charge of the Fed forever, one part of me says they will be like the supreme court, an arm of wealth. The other arm is warning me that my reliance to do the right thing has been misguided for a long time.

Will Brownie call for an appropriate increase in the Fed Funds Rate of 1% at the May 4 meeting. I doubt it. I expect a dillusional increase of 0.5 pct. I have no idea what these insulated fools at the Federal Reserve are likely too do. I guess that is all about the uncertainty the makes capitalism the preferred system. It’s actually democracy is the preferred system.

You can buy 3 month treasuries through a brokerage account at pretty much every reputable broker like Vanguard or Fidelity or other firms.

They are currently paying somewhere around 0.7 pct yield with an implicit guarantee of the Fed. No loss of principle and a better than FDIC guarantee while you wait to gain an understanding of what the new rules are. Ie, I don’t want to own 10 year bonds that will likely end up at 8% for a laughable 2.5% rate.

Because the powers-that-be are international in their outlook and business model. The .01% and smaller deciles view themselves as multinational players and the USA is the juiciest banana republic to stripmine and exploit. When the USA collapses they’ll retract their mandibles and find other hosts to suck dry.

“There are only two paths forward. Default or inflate. My take is on inflate. The Powers that Be will not sacrifice their wealth and investments, because of the poor.”

Those who are actually powerful do not derive their power just from their mostly fake wealth but from the geopolitical position of the country in which they reside.

None of the most powerful have their influence alone either, but as part of a similar like minded group.

Most of the supposedly powerful – the 724 US billionaires – are mostly a bunch of nobodys geopolitically or even at the national level. There aren’t anywhere near 724 actually powerful US wealthy elites.

The US needs USD global reserve currency status to maintain the Empire, as that’s where the most influential Americans derive their real influence which isn’t just derived from their mostly fake wealth.

That’s why I have repeatedly stated that when the chips are down, if necessary, the public, markets, and the economy will be thrown under the bus to save the USD from crashing in the FX markets.

There is a inverse ETF for High yield Bonds – SJB with0.95% exp ratio. Won’t recommend it for the weak hearted. It is up 8% so far

Best is to buy PUTS on JNK, HYG and LQD ( close to, or out of the money with appropriate time frames) the ‘trend and timing’ has to be on your side, otherwise you lose! Hence NOT many want to get involved, especially BTFD has been the mantra for the last 13 yrs, guranteed under the Fed’s perpetual put, which NOW, no longer operative!

Option trading is the only’ salvation’ for the retail investors during secular BEAR mkt, coming your way.

This may be a time where inverse ETF’s go upside down. The bursting of a stock market bubble, especially one of the current proportion may be breath taking like 1929. Questions of liquidity are reasonable. They operate in a world of short term variance where, I submit, we are in a world of long term variance.

Premiums are already ridiculous. Options are for hedging. Or play volatility.

Ambrose Bierce

‘Premiums are already ridiculous. Options are for hedging. Or play volatility’

EXACTLY!

B/w the Equities remain in overvalued zone! Loss 50% in S&P still puts in more than fairly valued! Long way to go. PUTs SUDDENLY are in demand. I bought my puts most of 1-2 months ago!

Puts (if properly timed and out of money) will decimate the calls in the next year or two, of course with bounces (Bear trap) all along! Lost nothing in GFC with this mode of trading. (been in the mkt since ’82)

My PUTS are happy today!!

The narrowing spread to treasuries is pretty wild. I mean it “makes sense” because stocks are rallying since mid month but someone needs to explain to me why stocks are rallying …

“Stocks are rallying” because you’re still on the sidelines. Once you buy in, that should kill it.

Seriously, not all stocks are rallying. Matter of fact, my semiconductor watchlist has been bleeding red now for over a week.

“having committed policy error after policy error for the past two years, and after having exacerbated these policy errors starting in January 2021”

TWO years? 2?? Where were you for the last decade?

Hahaha, yes, I thought someone would correct me on that. Didn’t take long :-]

I wish we could see the volume of these markets. I would imagine that it wouldn’t take much to move the Junk Bond yields one way or another.

Going forward from this point in time, there is only one relevant question As Robert Kyosaki said, “How many ounces do you have and in what form” ?

All the rest is just noise.

Gold is money Everything else is credit (J.P. Morgan).

And credit is failing (Yours truly)

Franz Beckenbauer,

Exceptionally, this one time only, I am willing to take your failing, useless, worthless, and hated “credit” off your hands and dispose of it properly. This one time only, I’d be willing to take all of it. Here is how to do it:

https://wolfstreet.com/how-to-donate-to-wolf-street/

a good one :)

The Federal Reserve assured the public there wouldn’t be a taper tantrum this time. Yet treasury yields from 2 to 30 years have spiked by 1% within a month.

This isn’t a taper tantrum. This is inflation of 8% and the market’s reaction to the Fed’s belated and too-slow reaction to this inflation.

The RRPO market is still humming along which suggests that QE hasn’t unwound at all, banks are sitting on cash, or maybe treasuries are in short supply?

Ambrose Bierce,

“The RRPO market is still humming along which suggests that QE hasn’t unwound at all,…”

The Fed would have to unwind $3 trillion of QE assets just for RRP to go to zero and for reserves to go back down to pre-Covid levels. That’s going start “as soon as” May, the Fed said. To expect this to have already happened by now is kind of silly, no?

So this is going to start in May and it’s going to go on for years. Get ready for it.

The bond market (especially the treasury market) is usually the smartest among Wall Street investors, accurately predicting the future path of the US economy.

How did they miss this one so badly? Why suddenly dump treasuries over the past month (Taper Tantrum 2) when (a) inflation has been a problem for a year & counting, (b) the Powell Pivot towards faster & earlier tightening was made almost half a year ago?

There is no “the market”, as it’s an anthropomorphic abstraction. “The market” has no collective mind.

As to the timing, it’s entirely psychological. The so-called fundamentals did not change noticeably if at all. It’s the perception that changed. This equally applies to the FRB response, as they also changed their mind about the fundamentals.

There are market fundamentals which aren’t psychologically based (such as from natural disasters and physical limits) but market pricing is always psychological, as there is no absolute value. The concept only exists in the human mind and outcomes are not mechanical. No fundamental ever bought a single share or any other tradeable asset.

Because the Fed has been setting the marginal price of Treasuries for a long time now, and that forcing function bleeds over into other bond prices.

I would strongly suggest that the Federal Reserve FOMC simply immediately raise the Federal Funds Rate to 9.5% in an emergency meeting and be done with that issue for a while and then that they take a nice Spring and Summer break and enjoy themselves. The markets can and will easily adjust just as they did when the Russian Central Bank raised their interest policy guidance rate from 9.5% to 20% in one fell swoop overnight about a month or so ago.

I can get behind this.

Would that impact US government’s ability to borrow money / run budget deficit ? Also, how would housing market handle this ?

The dip would be so deep and fast in all markets (assets, credit, labor), it would look like March 2020. The Fed would have to jump out of those lawn chairs and run back for frantic rate-cutting. Which might well not stem the tide this time, meaning impenetrable and prolonged depression. Maybe some seeming sideshow like Taiwan would suddenly jump onto the radar.

The Fed is a lot of things but they are not homicidal-suicidal.

phleep

‘it would look like March 2020’

S&P was down only by 35% and some call this ‘correction’ compared to what’s ahead!

During GFC, S&P lost nearly 60%. Would have lost if Fed had not come to the rescue. This time, yeh, it will be different, in a bad way!

“maybe some seeming sideshow like Taiwan would suddenly jump onto the radar”

This is what I am really afraid of – having determined that there is absolutely no way to avoid economic catastrophe due to the colossal debt levels etc., government will go for a full reset of the economy and society by gradually pulling the nation into a large scale war. This will absolve them of the responsibility for all of their prior errors, and will allow them to take actions that they just can’t do in peace times.

This is true. The federal government would then also be in even more of a pickle: the greater interest payments on rolled over securities would require they cancel something major, like the US army or social security or medicare.

This is the result of behavior by the banksters and their “Federal” Reserve, actually private but named to mislead, bankster cartel, which is just like the oligarchs from a certain country with its “dividends” to its oligarch owners for doing nothing, massive, QE commissons for doing little, ultra low interest rate loans to often insolvent banks of the banksters, effective guarantee of the banksters’ loans by giving them repeated “recapitalizations” (i.e., “free money” via loans at rates below the real rate of inflation, as they are now) whenever their banks go insolvent, purchase of the banksters’ hundreds of billions of mortage backed securities, which the US congress would balk at bailing out despite government guarantees, etc.

Of course, this is because the US politicians have been captured so that their ultrarich owners no longer are required to pay taxes; they are oligarchs in control of the US like oligarchs and their tyrant rule Russia via bribes direct and indirect (e.g., to relatives of politicians or judges.)

How is this supposed to happen? Through QT to cut the balance sheet by 50% overnight?

It isn’t going to make any difference on market rates by arbitrarily voting to change their target rate.

If market rates did rise to this level, the markets and economy would not easily adjust. Your comparison isn’t valid. The US financial system is loaded with debt up to its eyeballs and most people and businesses would go broke.

The current real US economic fundamentals aren’t good but mediocre to terrible, with economic “growth” since at least 2008 entirely dependent upon increased government spending and the loosest and lowest credit standards in the history of human civilization.

When we get to the point that banks don’t want to lend then things will tighten up fast. Remember during GFC when even American Express was telling their customers to get lost. No access to credit and demand will dry up within a few months.

MW: US Dollar Index hits fresh 2-year high of around 100 as yields rise; greenback also hits seven-year highs against the yen

Gold is up against a strong dollar as well which I think is not what usually happens. Gold is up 22% vs Euro year over year.

At some point it’s going to be a good time to start buying foreign assets with dollar so strong, but might be a little early.

Many manic speculative commodities are continuing their rapid descent today with oil plunging -4.60% to 93.74 with a -4.52 drop. Sure hope for the oil companies sake it doesn’t go negative again like it did a couple of years ago when it closed down $-33.00 for the day and hit an intraday low of $-40.00 back then as that’s just not good for profits!

Those were futures that went negative. Worldwide oil demand is rising due to the end of the pandemic and demand will stay healthy. It’s believed right now that supply can’t rise as fast as demand due to lack of investment in new oil during the pandemic to replace depleting wells.

What is ‘believed’ is nonsense, and the fact is that the world is DROWNING IN EXCESS OIL.

Most of the oil is in the ground. Producers only take it out when they plan to sell it. No one is drowning. Laws of supply and demand determine price action.

SoCalBeachDude

Oil price will fluctuate between Demand destruction and lack of new production b/c ESG and severe climate changes.

I bought PUTS on OIL for Dec 2022, when the oli hit $130! It will be a trade (options) between 70 and 110. Commodities like grains and fertilizers will remain in demand (with some periodic fluctuation) considering the global population current 8B going towards 10B, soon! So are the Farmlands!

Come back in a year and you’ll have some egg on your bold faced type…..

Day to day prices changes are nothing more than speculation based on whatever bs hits the news.

Shanghai lock down ends and oil will be headed back up again.

Elon Musk is now the largest shareholder of Twatter with nearly 10% of its shares and made some wonderfully constructive and helpful suggestions over the weekend. His best suggestion was to turn their Silicon Valley HQ into a homeless shelter as it wouldn’t be missed since nearly no ‘workers’ even bother to show up for work these days. Elon also mused about whether this 140 character email/web chit chat forum was dying and said that half of its accounts are bots. At the end of the weekend, Elon and Twatter reached a mutual accord that Elon wouldn’t be joining their Board of Directors, but it was a great time in the past 7 days for Elon where his stake in Twatter gained around $1 billion which is a nice gratifying return on a week of Twatter bashing!

SoCalBeachDude,

Great article. Haidt is an excellent writer.

The spread between 2-year and 10-year is almost non-existent. What does it signal? Tightening followed by wild dial back to QE?

It signals that the Fed’s obese balance sheet is sitting on top of the long end of the curve — which was the purpose of QE, to bring down long-term yields. And the Fed locked down the short end of the curve via its policy rates. And the middle was allowed up a little (2.5% yield when CPI is 8% is just a minuscule step) and move toward the yields at the long end. Enough QT will resolve this issue, with long-term yields then more exposed to market forces. Already, little by little, yields at the long end are rising despite the Fed’s $9 trillion weight on top of it.

I wish I could cut and paste individual replies.

One other factor will make the situation even worse for high yield bag (um, bond) holders: many of these junk bonds are “covenant lite.”

Creditors will not have their usual tools for at least mitigating some of the damage.

That is an important under-commented aspect. Sharpies can rush in and grab pieces of these wobbling companies’ senior debt, and throw various classes of bondholders under the bus (along with low-grade creditors like, say, employees and vendors). Some sharpies are even marketing this to companies: we’ll lend you cash now if you’ll sign deals (built around these weak covenants) to screw creditors further down the chain.

This can turn into a gold rush for a few, very quickly.

Private Equity companies are salivating to buy them with cents on the dollar, when ‘blood hits the street’!

IF one is gutsy enough, one buy those companies, now!

“Many of these bonds tend to default when the financial conditions tighten to the point where the companies run out of investors to provide new money to pay off existing investors.”

Aka ponzi bonds.

Numerous FIC players have dived right back into the break-the-economy behaviors that gets the breakers big bonuses before everything goes to hell.

There was a time when it was almost safe to invest in bonds. No, really. I would not kid you about such a thing.

Now is not the time to buy bonds anyway, not with big Fed rate increases in the pipeline and the promise of better yields in the near future.

Yields will still be too low to justify the risks, which are systematically understated these days anyway. I myself do not gamble in rigged casinos and only play games of skill, like poker.

Indymac is now Axos, btw. One has to be careful selecting ones playdates because you be crunchy and taste good with ketchup.

MW: Fed’s Evans says half-point rate hike in May could now be ‘highly likely’

Might have meant more if he’d said that a few years ago.

Inflation is not fun.

————————————

Trevor Fraser, Orlando Sentinel

Mon, April 11, 2022, 3:15 AM

Engineer Matt Swanson was working in the home office of his Baldwin Park apartment a few days ago when his wife, Katelynn, came in crying.

“She was hard sobbing, couldn’t catch her breath,” Swanson said. “I asked … ‘Did someone die?’”

It wasn’t that. Instead, the Swansons had received the renewal notice from their landlord. The monthly rent on their two-bedroom was going up by $703, from $1,747 to $2,450 — a 40% increase.

“We are essentially facing financial eviction,” said Swanson, 29.

Such sticker shock is common for Orlando renters as skyrocketing demand pushes rents to new heights, a situation experts say isn’t likely to end anytime soon.

“I wish I could tell you that we’re going to have some moderation in rents. I just don’t see it,” said Jonas Bordo, CEO of apartment listing website Dwellsy. “I think we’re going to see more aggressive price increases.”

The median asking rent in metro Orlando in March was $2,295, according to Dwellsy, a 57% increase year-over-year. Orlando ranked No. 8 on cities with the highest increase in the nation.

Tampa with a 56% increase and Jacksonville with 53% were the only other Florida cities to make the top 10. Tuscon, Arizona, took the top spot with a 139% increase.

Swanson said his rent at Azul Baldwin Park went up by $100 last year, and he had expected something similar this year. But, he added, “a hundred in a normal year would feel like a lot.”

Azul Baldwin Park did not return a request for comment.

Swanson was given 30 days to agree to the new lease. He says the search for a more reasonably priced apartment has been frustrating. “There’s not a lot of availability,” he said. “The ones that are available are the most expensive models.”

Seeing stories about rent increases, food price will go up a lot in the next year, and the white, other areas of inflation are property taxes, etc.

Maybe housing will drop some but because interest rates are rising, the monthly mortgage payment will be the same.

Add in QT.

Where else can the market go but down? Sure, there will be some winners who can price in the inflation costs, but many cannot.

Best guess as to what’s going on is that market participants believe that if the economy turns it will happen gradually enough to provide them with sufficient time to exit their positions “gracefully” before these companies start defaulting on these securities.

“Gracefully.”

Thanks! You made my day. Almost blew my lunch on the monitor with explosive dark laughter. Imagining grotesque pratfalls, still.

Yes, that’s what they thought in 2008 too.

How did that turn out?

Max power

‘happen gradually enough to provide them with sufficient time to exit their positions’

!?

Historically, Mr. Mkt NEVER accomodates the majority, in escaping the BEAR! Study the previous Bear mkts. There will be many BEAR traps for the BTFD crowd!

Excellent stuff, Wolf, as usual.

There are so many related topics that can be further addressed.

Why the (temporary?) rate compression across maturities, ratings?

Why maturity (rollover) dates might matter much, much more than all the interim years/interest service payments.

Which years have the biggest maturity walls, for which fixed income products?

What are the loss-given-default numbers for secured/unsecured bonds? They used to be 30% and 80%, but that was many, many trillions in debt ago.

So *many* topics that very few talk about…until inevitable conditions turn them into topics that are *all* anybody can talk about.

US treasury 10 year yield is up to 2.78%, I’m not an expert, but I don’t think going up .07% in one day is normal.

Nothing has been “normal” for 20 yrs…as long as the Fed has used various tools (including massive money printing) to artificially strangle interest rates for a heavily indebted gvt and nation.

What you are seeing now, is the tiniest return to a less manipulated mkt.

WOLF – you state: “….price of the iShares 20 Plus Year Treasury Bond ETF [TLT] has plunged 27% since July 2020…”

Since the price has dropped, the yield goes up – so if I buy TLT, is my annual coupon rate (yield) 27% ??

OR

Because it is an ETF (collection of different bonds) – there is no annual interest paid?

Neither

30YR futures have declined from 191 at the all-time high in 2020 to about 142 today. I don’t have the equivalent numbers for the 20 YR but 1% in change yield equals 20 points in the price.

It’s not exact because the 5YR, 20YR or 30 YR someone bought has a lower maturity depending upon when they bought it.

So, if you bought the 20YR in 2020, it’s now an 18YR.

You can check the yield every day when you look up the EFT. Today, the yield is 1.83%.

Hi Wolf, what about MBS Yield? Not sure how much as changed on the balance sheet, if it can be re-visited as well. Thank you!