Junk bonds are still in la-la-land though, Apocalypse but not now.

By Wolf Richter for WOLF STREET.

When investors demand higher yields on bonds, motivated sellers must lower the price of those bonds in order to sell them. And yields are now spiking and prices of bonds with longer maturities are plunging.

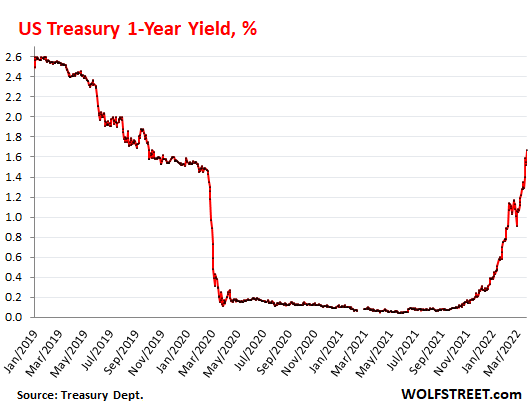

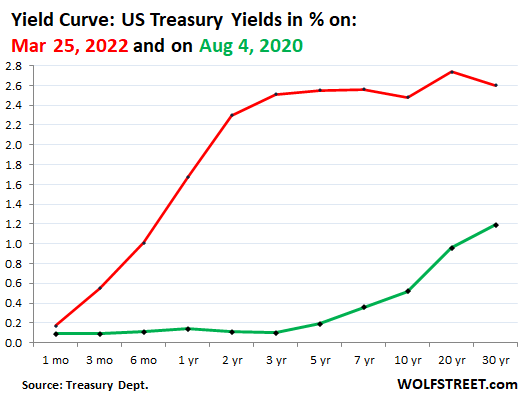

The one-year Treasury yield spiked by 38 basis points during the week, including 12 basis points on Friday, to 1.67%, the highest since October 2019. There is now a huge 150 basis point spread between the one-month yield of 0.17% and the one-year yield of 1.67%:

This is one heck of a fast-moving train. And the Fed hasn’t even done much other than one tiny rate hike and lots of talking about what it’s going to do, which is raise rates far faster and further than previously imagined, and kick off Quantitative Tightening “as soon as” May to finally crack down on inflation which is now spiraling out of control. And the credit markets got the memo.

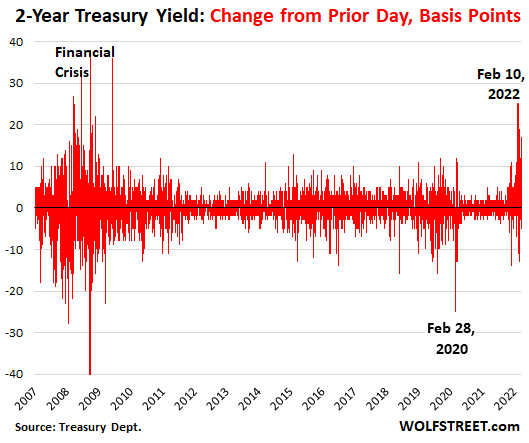

The two-year Treasury yield spiked by 33 basis point during the week, including a massive 17 basis points on Friday, to 2.51%, the highest since April 2019.

The volatility in the two-year yield is huge, the worst since the Financial Crisis, with massive spikes interrupted by some modest drops. This chart shows the day-to-day changes in the two-year yield in basis points. The biggest one-day spike in this cycle, 25 basis points, occurred on February 10:

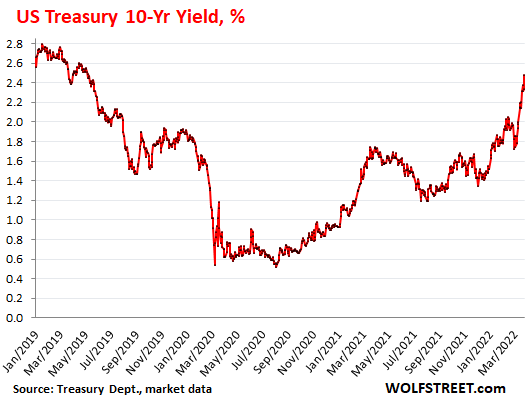

The 10-year Treasury yield spiked by 34 basis points during the week, including by 14 basis points on Friday, to 2.48%, the highest since May 2019.

The 10-year yield has been rising since the low point of 0.52% on August 4, 2020, which marked the top of the biggest bond bull market ever that had started in October 1981. At the time, the 10-year yield had peaked at 15.8%, after CPI inflation had peaked in April 1980 at 14.6%.

From October 1981, yields zigzagged lower, interrupted by big upticks in between, and since 2008 pushed down by the Fed’s interest rate repression and massive QE. Now the result is the highest inflation since 1981, with February CPI at 7.9% and worse inflation to come.

The bond massacre in dollars. Market prices of bonds with long remaining maturities get ravaged when interest rate rise.

For example, the price of the iShares 20 Plus Year Treasury Bond ETF, which holds Treasuries with maturities of 20 years and longer, fell 1.4% on Friday to $128.66. This was down 25% from the peak at the end of July 2020. The 40 years of bond bull market have lulled people to sleep about the risks of bond funds.

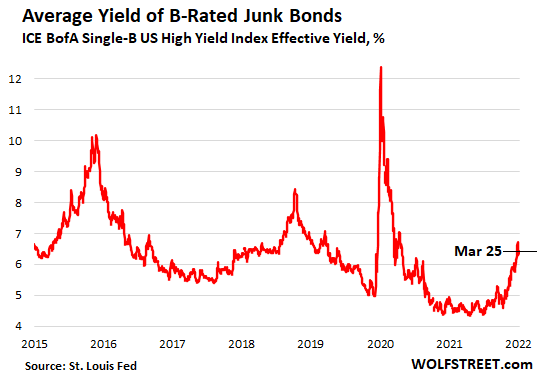

But not junk bonds yet. This massacre is playing out with Treasury securities and with investment-grade corporate bonds, particularly the highest-rated corporate bonds that closely track Treasury securities.

Junk bond yields have been slowly rising from the low point last summer, and the spreads to Treasuries have been slowly widening. But since March 15, while all heck broke loose in the Treasury market, junk bond yields have actually dropped and remain historically low, and their spreads have narrowed and are historically narrow.

This means that the market is still not paying attention to corporate credit risk – the risk of default – and the market is still chasing yield and is still giving these junk-rated companies with a significant probability of default a pass on credit risks, which is going to haunt the market when it wakes up. Apocalypse but not now.

This chart shows the average yield of B-rated high-yield bonds. A “B” rating is roughly mid-range within the junk bond spectrum (here’s my cheat sheet for corporate bond credit ratings and what they mean in plain English):

The yield curve is now very steep from the one-month yield (0.17%) through the three-year yield (2.51%). But then it flattens through the seven-year yield, inverts a tiny bit at the 10-year yield, then steepens to the 20-year yield, and then inverts again to the 30-year yield.

The yield curve still says nothing about the economy because it is still an artificial construct manipulated by the Fed: The Fed still represses the short end of the yield curve with its policy interest rates, and its obese balance sheet sits on top and squishes the long end of the yield curve. At some point QT, once it reaches critical mass, is going to start freeing the long end of the yield curve, and long-term yields will rise much further, the curve will steepen at the long end.

The chart also shows the yield curve on August 4, 2020 (green), marking the end of the 40-year bond bull market, to be cut out and taped on the fridge with a melancholic nostalgic smile:

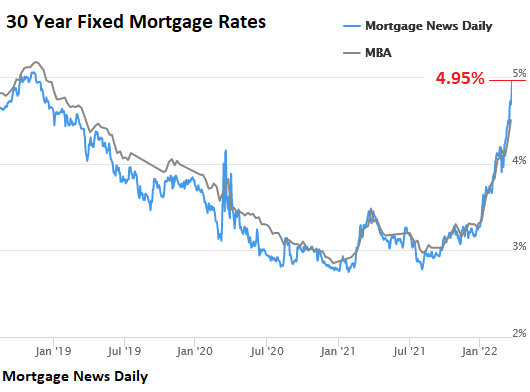

Mortgage rates, holy moly. On Friday, the average 30-year fixed mortgage rate spiked to 4.95%, the highest since November 2018, according to Mortgage Daily News. And once it goes over 5.15%, it would be the highest since before the Financial Crisis. But back then, and back in 2018, home prices were a lot, lot lower. Already, layer after layer of buyers are stepping away from the market at these mortgage rates:

But as the WOLF STREET dictum goes, “nothing goes to heck in a straight line.” It is very likely that Treasury yields will pull back some, after this run-up. And hedge funds that are short Treasuries – the most obvious no-brainer in the history of mankind – are going to get whacked around. That’s always how it is. One thing we know: it’s going to be volatile, with massive moves in both directions. And the 5% mortgage rate is sort of the sound barrier, and it will take a while to move beyond it in a significant way. But its impact on the housing market is already being felt.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Housing market already feeling this.

Any anecdotes to share?

Bloomberg:

Pending home sales down 4.1% MoM (after a downwardly revised drop of 5.8% MoM in January). That is the fourth straight monthly drop…

What will this do to the rental market? Both from an owner and a renters perspective. Any thoughts?

Jon.

Random thoughts.

Higher interest rates lead to lower housing prices, more foreclosures, more people walking away (jingle mail), more people with negative equity, longer on the market time, chasing the market down, etc.

So…

More folks will be renting out a room in their house to make ends meet

Once a home has been foreclosures or sold for less, it can be rented out for less.

Apartment buildings are in a supply/demand survey and will charge what the market can bear. Newer ones, especially over leveraged luxurious apartments, are going to go bankrupt.

Higher interest rates and high inflation means most folks have less to spend on rent or buying a house. The market can bear less.

Your thoughts?

not so sure any of those results based on both logic and last time will be exactly the same this time , 2b,,,

mainly because of the incredible increase in the crony corruption at every level, including especially USA FRB now, as opposed to it’s at least allegedly previous honest attempts to follow the policies approved by the Congress of USA…

Now, it seems surely that the now clearly corrupt FRB and the now clearly VASTLY and proven daily corrupt USA Congress are totally,, repeat, TOTALLY in the grip of the ”’ whatever”’ ,, oligarchy is a convenient meme name, but may other names apply.

AT THIS POINT IN TIME,,, it is not exactly rocket science to figure out this corruption, eh?

What may be even more complex to figure out, waaaayyy beyond rocket science is:

”Who does what, and with Which, and to Whom” per one of the ancient and always relevant dittys that started with ??? that have gone around for many generations to explain SO much formerly obscurities.

Sorry to be somewhat obscure with this comment, but do NOT want or need to involve WR with any of the current ”witch hunts.”

This is because there are no homes being listed for sale. Listings are at historic lows.

I see some opinions are moving from a slow down in home sales and an up tick in mortgage rates, and making a direct line to the financial crisis. We can have a slow down without a crisis.

Not saying that the housing market wont feel this but part of the drop is driven by inventory….

anecdotally, i know of people who have dropped out of looking for a house, the thought process is that the fact that there are no longer 3% mortgages means prices will have to come down, but that sellers haven’t yet realized it, so there will be a few months lag.

They say all real estate is local.

I wonder where houses prices will drop the most and/or the fastest?

The least?

Enlightened-

I would suggest SW Florida as one of the least, at least for 500k plus properties. My belief is based on an unscientific assumption that most sales are cash…

EL,

My bet is in central city (supposedly) gentrifying neighborhoods like in ATL where I live now. It’s not a place where people actually want to live based upon the merits but bought into anyway because the market was rising or due to close proximity to downtown and midtown.

The few I looked at with an extended price history went from something like $50K at the market bottom in 2012 to around $300K at the last sale.

Real estate may be local, but interest rates are national.

I tapped out of buying for the time being. But the Hudson Valley’s market, while dropping a tad in price, will probably stay bananas so long as NYC is overrun by criminals.

The Brooklynites are still scapping up our most affordable RE for their quaint rustic upstate getaways (gag), and their AirBnb guests still wipe out the local supermarkets’ stock every Friday like clockwork. Soon the lake beaches and state parks will be hopping.

For a lumber and worker shortage, cabins and lake bungalos seem to have no problem getting remodeled in days to weeks this month for sale or rent in anticipation of the season.

@Jake “a few months lag”:

In the 2005-2010 housing bust, the lag between peak prices and best-affordability was 3-6 years.

But what you really want to look at is the 1970s.

New listing is lower where I am but some still get over asking. I’m sitting on the fence, patiently waiting

I agree with Wisdom Seeker…it is worthwhile to hunt down real estate books from late 70’s and early 80’s, which discuss/analyze/suggest tactics for when housing prices/interest rates are exploding/imploding.

A lot of these approaches were rarely used over the last 40 years of Fed slow (sometimes fast) interest rate strangulation and a lot of the approaches look jury rigged and prone to failure, but if you bought an overpriced house in 1978 with a 7% mortgage and were trying to sell it in 1982 with 15% mortgages…you might try a lot of things…

Now contemplate how overpriced houses with phonied-up 2.5% mortgages are going to fare if mortgages go to a historical norm of 7.5% (or 15%+ if mkt integrity were ever allowed to rule again in the US…).

Homeowners don’t realize it but the Fed spends almost all its time seducing them into becoming unaware bond speculators (the inverse interest rate/bond price relationship that Wolf points out for bonds, applies identically to interest rates/housing prices.).

“ the thought process is that the fact that there are no longer 3% mortgages means prices will have to come down”

Jake W,

Someday your grandchildren will tell you they are soooooo tired of you talking about the good old days when you bought a house for $500k with a 7% mortgage :)

The thought process is wrong, I think… you may get some price reduction, but not as much as you think, depending on location and desirability of living there… as well as the circumstances of how the house was bought… one of the factors is the cost of new construction… when you had huge price drops way back when, the replacement cost wasn’t nearly as expensive as it is today which meant the difference between existing and new put a floor on pricing… I haven’t seen a chart but perhaps those who are a lot smarter than me can chime in…

John H,

I live in SW FL ( Charlotte County) where in used to be fairly rural…

The population here has doubled each of the last 10 year cycles…

The county has approved development of 6-8000 new homes coming soon in my area…

The prices here are not coming down anytime soon…

The trend here has been to sell the $500k house, take your money and go buy the 800k house…

20 years from now, when mortgage rates are at 7%, Millennial homeowners will be cursed at and accused of being the luckiest generation ever while they sit in their 2.5% mortgages and capped 2% CA Prop 13 property taxes.

Or, the Fed will change their mind and rates will go negative and the remaining Boomers will still be accused of the same.

“the replacement cost wasn’t nearly as expensive as it is today which meant the difference between existing and new put a floor on pricing”

This is a valid point, but…

It is a really interesting question as to why, when the normal pattern for most manufactured goods is to have production costs/sales prices fall (sometimes amazingly) over time, the cost for new *home* construction allegedly goes relentlessly upward.

(Allegedly, because just because homebuilders trying to sell you sometimes tell you this…doesn’t make it true).

Leaving the cost of finite supply land out of the analysis (land being maybe 15% of home costs), why is it that continuously advancing techniques and technologies in homebuilding are not resulting in *lower* (not absurdly higher) home costs?

Especially when, in the age of the internet, the dissemination of techniques and technologies (for *every* industry) has never been greater.

Sure, short term supply disruptions are responsible for some of the worst short term price spikes (lumber, labor, etc) but the home price conundrum has been going on for much longer…as long as ZIRP has been around.

Hmmm.

Ahem.

“20 years from now, when mortgage rates are at 7%, Millennial homeowners will be cursed at and accused of being the luckiest generation ever while they sit in their 2.5% mortgages and capped 2% CA Prop 13 property taxes.

Or, the Fed will change their mind and rates will go negative and the remaining Boomers will still be accused of the same.”

I’ll take neither for $1,000, Alex.

don’t know where ya get the land = 15% idea???

current SFR home land = approx. 2/3 = 66%

last one, acreage in flyover, it was more like 80%

maybe possible in apts/coops/condos?

Also, Why are the stock markets rallying over last 2 weeks with this spike in bond yields. Were they too happy that Fed raised rates by only 0.25% and postponed QT and was all Fuzzy when it will start.

Or was it because corporations love to borrow money at higher interst rates? Or is it that they love to borrow money at real negative interest rates and the got a signal that there will be a lot of Jawboning with little actual action?

Or the markets are still too rigged tl act properly? If we cannot reason with stock market moves, how do we know that these bond moves will not suddenly revert. Fed still really has a 0.25% interest rate.

Because price movements have nothing to do with any of the reasons you provided.

The only reason markets move is because of collective perception, not the event. Tracking the same or similar events over time will correspond to both advancing and declining prices.

Most recently, the US major averages bottomed on 2/24, the day of the Russian invasion. My guess is that the supposed reason given is that the war is going better than expected (for Ukraine) or there was an “over reaction) but that’s precisely the point, both are sentiment since no one has a complete picture of what’s going on there anyway and markets can rally for other supposed reasons too.

Thanks Augustus, I agree that market has more to do with perception in short term, specifically, when Fed is throwing billions at it everyday. So, market can chose to ignore the news and jump on incoming cash flows.

However, now I hear that Fed has stopped printing that money. So shouldn’t there be a recognition of fundamentals in medium term?

Raj,

Look at the disconnect between fundamentals and prices back to the late 90’s versus prior history. That’s almost a quarter century, unprecedented and why this is the biggest bubble in the history of human civilization.

Prices are higher and yields are lower than ever. and it isn’t because the environment is good or great.

The long-term fundamentals totally suck because society has been slowly falling apart. The short and intermediate fundamentals, disproportionately to completely fake due to borrowing and “printing”.

Market participants collectively rationalize current prices but that’s all it is, a rationalization.

This is also why it’s an illusion and a delusion to believe any central bank or government is in actual control of anything. The markets still have faith in both (to some degree) but this is entirely a psychological state of mind.

There is no such thing as absolute value. All financial values are relative and only exist in the mind.

That’s how actually intrinsically worthless companies, cryptos and NFTs can shoot to the moon and then suddenly collapse. This almost never happens to a market collectively, but the same principle applies.

Per Benjamin Graham (as best as ‘the experts’ can tell) …

“In the short-run, the stock market is a voting machine.

Yet, in the long-run, it is a weighing machine.”

Every older generation thinks society is falling apart.

Investors are betting on a resilient economy. Not only did we survive a pandemic, but business was booming in spite of it. With J POW at the helm, investors understand that the turbulence is temporary. It’s like we are on a ship being thrown about in a violent storm. But the captain remains steadfast at the wheel, his silver hair battered by wind, salt and sea. The storm is a perilous one. But the passengers sleep soundly in good hands knowing the captain will steer them through to calmer waters, eventually.

Jim Cramer Fan,

“With J POW at the helm, investors understand that the turbulence is temporary.”

Yes, totally, just like J POW’s mantra until recently that “inflation is temporary.”

Jim Cramer Fan seems like the type who is waiting with baited breath for the next crypto with a dog image attached so he can become a billionaire.

Well Said, Jim Cramer Fan!

Being one of those investors, I’m not sure I agree. If my investments drop enough, I may be consider JPOW more like Captain Bligh.

Not many investors would hold to this:

“The ship’s company will remember that I am your captain, your judge, and your jury. You do your duty and we may get along. Whatever happens, you’ll do your duty. ” – Captain Bligh

Otherwise, very well said, Cramer Fan!

this for bob:

quote likely true enough, and certainly reflects the actuality of a ship’s captain in Royal Navy of the time;;; however, in this current case it may be most pertinent to remember that in spite of his obvious ”little tin godness”,,,

Bligh did captain ALL his loyal crew to safety across 4000 miles in an open boat

My thinking is they rigged the markets higher so more people could pay their income tax for April 15 if they owe money.

Anecdotally, mortgage rates are 4.95%.

Wolf has given me permission to offer a bid for an authentic Wolfstreet glass mug. My current bid is $200.

In addition, Wolf has given me permission to request asking prices for an authentic Wolfstreet “Nothing Goes to Heck in a Straight Line” glass mug.

HarryHoundstooth at yahoo dot com.

Purchased my first house in Oct 1988 for a great price but at 10.5% 30yr fixed. But we got a house at 24 & 22 years old. 3 years later the hosiing market goes bust and were under water for a few years. But I was able to refinance twice down to 4.5% and ride it out. Sold the house in 2000 and pulled enough cash out to put 30% down for a house 2x the size and value. Now $50k away from paying off this house but at 3% /15yr fixed, I’m in no hurry.

Not in my experience. Our neighbor just got an offer way over asking. Rental rates are absurd and rising. Still a sellers market in Phoenix.

Yes. Hubby posted a listing on MLS last night. There are 4 showings set up for today.

This is expected behavior at the beginning of a correction. It takes time, and this correction hasn’t just barely begun. It will be collosal… much worse than the previous bubble.

Right. Everything you said about the Phoenix market is true but with the current environment, those making offers at this point and for the next 6 months to 1 year are the ones hanging out in the burning building as the others run foe the exits. There will always be those that time it wrong. With these interest rates going up as quickly as they do, there will be many riding the back end of the down curve with the housing market.

Phoenix, Denver, and Vegas, metro areas have bigger issues. On top of the pricing pressure from loan rates the inventory is going to be significantly larger than the supportable population due to water and power limitations beginning in 3-5 years in my estimation. In that case it matters not that the devaluation of the dollar by Gov borrowing and reduction in available timber caused raw material costs to rise setting a new construction replacement floor on pricing because there will be no need for new construction for years until deterioration restores balance.

Any wagers here in terms of how many months it will take to come down 20% from the recent home price highs?

I think towards the end of 2023 will be the brief air pocket where housing becomes relatively cheap

It wouldn’t surprise me to see some of the bubbliest housing markets to be down 20% from all time highs within the next few months. Of course, we won’t know that until the data comes in months later. The prices in some areas are so absurd a 20% discount would mean prices are still absolutely bonkers.

So basically selling for list price vs 20-30% over. You’re right, prices would still be way too high (for me), especially at 5%+ mortgage rates.

A lot of the houses I’ve seen on the market were staged. Meaning to me, investor owned. If BIG investors the prices may come off but in my experience the smaller the investors, the less able/willing to lower prices.

In past housing downturns were slow. Defaults and then repos take time. Lots of pain to come.

Staged doesn’t mean anything. With the prices being $800k+ in many locations, spending $3,000 to $4,000 to move out/stage isn’t a big investment for a normal seller. And realtors love it because it makes them look valuable when the house would sell anyway in 48 hours.

Currently most (at least in my area) aren’t investor owned – they’re just normal people that bought 4, 5, 10 years ago and are cashing out to move somewhere cheaper.

Last time, the best buying opportunities were in 2012, i.e. 5 years after the 2007 bubble burst. Housing prices are very sticky. Be patient.

My experience has been, at least with high end homes, is that the listing agent prefers that absolutely everything that belongs to the owner be out of the house. Then they stage the house with bland generic stuff.

They want the potential buyer to be able visualize the house with their own furniture, artwork, toys, etc.

For most buyers too much of other people’s stuff clouds their impression of the house.

At least out here in the PNW. It seems like it works.

Especially when banks are rewarded for sitting on inventory to keep prices inflated.

I’m with Bubba…when artificially inflated mkts collapse (due to Fed policy props being pulled away), prices fall very fast…because *a lot* of owners/desperate sellers have always known exactly how key those artificial props were.

Once those props are gone, it is like the end of the movie theater scene in Inglorious Basterds…all the hysterical speculators rush at the locked doors at the same time.

Look at the implosion history of Housing Bubble 1.

Impact crater, then slow crawl out.

As Jim Cramer Fan said above the “silver hair Captain battered by wind, salt and sea” cannot let housing fall too far. (20% or more).

Otherwise, the underwater homeowners and iBuyers who view a house as an investment rather than a place to live will panic and try to unload or walk away en masse. If that happens, then house prices will drop 50% and we will see a repeat of 2008. We’ve seen it before. Otherwise, at 7%-10% yearly inflation rate and flat house prices, how long before housing loses 20% of its value?

Let’s see how our courageous Captain handles being on a ship being thrown about in a violent storm. Can he avoid the recession rocks looming dead ahead? Stay tuned for the next few months. Same time, same Wolf Street Channel. “This massive ship steers very slowly”, paraphrased words of the Captain of Titanic.

“I think towards the end of 2023 will be the brief air pocket where housing becomes relatively cheap”

Boy, that’s hopeful. The housing market is seriously screwed up in a lot of ways, the most important of which appear likely to unwind any time soon. I’d put up a weighted list of them but my date is done powdering her nose and is ready to resume being entertained. She does not find finance & economics entertaining.

She finds horror movies entertaining but not economics and finance, despite the obvious similarities. Go figure.

UN-likely to unwind any time soon. Oops.

una-imagined horrors easier-nay, entertaining, even- to come to grips with than the real thing???

(Good to see your handle again…).

may we all find a better day.

My last girlfriend and I attempted to have a “conversation” about finance. Her unamused chilly response toward my interests was the moment I realized we were over. Mine wasn’t into horror movies, but lots of very new-agey stuff.

Life is too short for me to devote energies to such trifles. She was a wasting asset on a steepening discount curve. No wonder we didn’t see eye to eye anymore!

unamused — she has a GREAT horror movie coming, leaping from global finance into the powder room!

Great comments!!

Finance is far more frightening than any horror movie could be.

Horror movies have an ending.

With finance, there’s really no escape…

Powdering her nose, sitting on a powder keg.

No one will probably see this comment but you guys have me Rofl.\r

“She was a wasting asset on a steepening discount curve. ”

Still Rofl\r

Depends on job losses more than arbitrary dates. If a recession hits where many companies lay off 5% of their employees and zombie corporations actually start going under rather than receiving their current welfare checks (aka loans or “investor” funds), look out below.

Agree with you JeffD on this one. Once layoffs start up, I think that will be ground zero.

Personally I wouldn’t count on housing prices coming down in the near future. While nominal mortgage rates are rising, inflation rises at the same rate or higher, so “real” mortgage rate (= nominal mortgage rate minus inflation) remains negative, and may even be getting more negative. This provides strong incentive for people to buy homes because their mortgage debt will get inflated over time.

If inflation unexpectedly subside in the near future (as Federal Reserve apparently expects it to), then Federal Reserve will immediately go back to their habitual tricks (halt QT, and/or restart QE etc.). This will cause mortage rates to go down again.

This leaves us with the scenario when inflation stays high. In this case Federal Reserve (IMHO) will give up, and will not even try to fight inflation because they can’t rise interest rates to sufficiently high level (this would constrain US goverment’s ability to run budget deficits). So “real” mortage rates will remain strongly negative, and will provide strong incentives for people to buy homes even though prices are outrageous.

So IMHO there won’t be any sustained drop in housing prices in the near future.

maybe not ak, but reviewing one ”flyover” location recently, almost all the listings had a ”recently reduced” price, or so it said,,,

still seeing almost nothing for sale here in our hood in the saintly part of the tpa bay area on my daily perambulations

couple SFR recently gone in a day, appearing as a rental and that too gone in a day or two

Wolf, how does the latent size of the existing balance sheet surpress yields at the long end? I would have thought that the Fed’s monthly purchases, which have now stopped, would be the only thing repressing long dated yields.

you didn’t direct the question to me, but part of the reason might be that the fed owns a huge number of long maturity bonds, and is not (yet) selling. so if a large percentage of available bonds are off the market, the prices are going to be higher (and thus, the yields lower).

They have no one to buy those bonds china-Japan is out of the game

Matt,

The Fed holds 25% of all publicly traded Treasuries. It doesn’t trade, it doesn’t sell, it only buys. This is a huge amount of supply that has been removed from the market. It’s like if you remove 25% of housing stock from the market, what would home prices do? Any demand has to be met by the other 75% of holders’ selling. Same with MBS, only proportionately bigger. This is a gigantic force, and Fed governors have said as much, and have said that long term yields cannot rise properly until the balance sheet is lightened up. That’s why they want to lighten up the balance sheet.

Wolf,

“If you remove 25% of housing stock from the market, what would home prices do?”

This is exactly what just happened. Anyone who purchased their house at old prices and refinanced during covid is now stuck. 25% of the market has a house payment at x*3% interest and the market is asking for 2x*5% interest. That’s a 2.5x monthly payment w/20% down for the same house.

I wonder what the new equilibrium will be like when every refi that happened is effectively out of housing supply for the near future but no one can afford higher prices and higher interest rates.

“The Fed holds 25% of all publicly traded Treasuries. It doesn’t trade, it doesn’t sell, it only buys.”

Wolf, I thought the FED could buy and sell treasuries as part of their Open Market Operations tool? Am I incorrect here? Thanks!

They could, but currently they don’t. Enough of their bonds mature every month that they can do all their adjustments without actually selling.

Indeed, even now, the Fed isn’t increasing their total holdings, but due to tens of billions of bonds maturing every month they actually continue to buy bonds to keep their holdings steady.

When they start to tighten, ironically they’ll probably still be buying, but at much smaller amounts that don’t replace the bonds that mature, so that the overall holdings slowly shrink.

Of course if they want to tighten faster, then they can sell bonds. Those sales along with the bonds that mature every month would provide for a pretty rapid tapering.

Lune, thanks for the explanation.

The Fed can sell if it wants to, but hasn’t sold any Treasuries yet. Last year, it sold its little-bitty holdings of corporate bonds and bond ETFs (and made money doing it) — just ahead of the bond blood bath. The Fed may in the future sell Treasuries or MBS as part of QT, and if the Fed decides to outright sell Treasuries, we’ll be watching the tremors go through the market.

When owners are squeezed customers sqeeze even more

Lower rents lower housing pricing etc. Great

for those with a sharp sense of timing and opportunity.

Wolf,

Why would investors buy a Treasury bond with the 0.25% yield directly from Treasury, if there is a US10Y (2.4% yield) with potentially earlier maturity?

I feel that’s very unreasonable for a typical investor. May be someone have other motivations?

These short-term Treasury bills are used for risk-free cash management. If you have over $250,000 in cash, the excess over $250,000 is not insured by the FDIC. So a company, which might have 100 million in cash to cover its payroll and other expenses, has some of this cash in the bank, and might have some of it in Treasury bills. Short-term Treasury money market funds serve the same purpose, and they also buy those Treasury bills. No one buys Treasury bills to make money. They’re for cash management purposes.

I have been trying to explain this to people but haven’t been able to do so as succinctly as Wolf’s comment above. Treasury bills function like a billionaire’s savings account that seamlessly connects to the billionaire’s checking account. Corporations are people too.

T-bill rates also work as a barometer to tell the current weather, if you know what I mean.

Flight to “safety” and all that.

Short term notes are cash equivalent for me. Treasury Direct makes it easy. I am expecting rates to continue to rise, so I am buying short term notes, and getting better than savings account rates. This is less than 250K, but it still makes sense to me to make slightly more interest for now.

Go to the head of the class, doug. The short end of the curve, along with the long end as pointed out by Wolfmeister, have some catching up to do as the Fed gets off its butt and tightens short-term credit. Stay in the 30-day Bill range for now since the bond market yields are catching on fire. Why pay any management fees to a mutual fund money market when interest rates on Bills are at depressed levels. Even 0.3% per annum is too much in here. An enlightened investor in 2022, how refreshing, doug.

Am not going to Vegas with this bet, but my old nose smells a 50 basis point intra-meeting rate hike in April as the inflation releases burn Fed members a new one.

Isn’t that treasury direct like $10k max per year?

Moonbats, no, the 10k limit if for ibonds with that juicy 7% adjustable rate. You can have an amount in your treasury direct account.

I use it like that other reader. Anything over the limit of bank fdic insurance.

It was nice a couple of years ago when 3 month notes were yielding 1.8% . You can set it up to reinvest up to 6x without having to log in again and again.

Are treasury money market funds like VUSXX a safe place to stash cash right now?

I’m always trying to figure out where to hide and even make some money in times like this when the future looks bleak.

I am also trying to navigate investing on my own. I am starting to think I should just do the sensible thing and hire a professional. I’ve already made relatively bad choices in the name of trying to be cautious; I pulled my 401k into a non-interesting bearing Money Market fund (cash) about a year ago, expecting a big correction which started to seem like it was happening recently, but now S&P500 index is heading North again. I completely regret going to cash — and missing-out on the past year’s 20-30% growth. Now, I’m just trying to be patient, waiting for a reasonable correction to reinvest.

I’m waiting for S&P500 PE ratio (now 26, down from 37) to be in the 15-20 range, but inflation pressures might be affecting this. I see S&P500 Shiller PE (PE10) which is adjusted to inflation and uses average past 10 years of earnings is still up near the peak, second all-time high ever, 37, as S&P500 index starts to head up again.

I was wondering about the “spikey” nature of these PE peaks. The big PE spikes come down very quickly. I guess this is just the flipside nature of Irrational Exuberance: at some point, confidence just drains away and everyone is trying to get out the exits with their paper gains, or is there some correlation with Treasury yields?

Can anybody explain the discrepancy we can see presently between S&P500 PE (heading down slope quickly) and Shiller PE (still near the peak)? And, which is the better indicator (and at which value) to use as a measure of when to reinvest into the index?

Because the Schiller index looks at the trailing 10 years it takes much longer to move up and down than the s&p which is a snapshot . The Schiller gives us a reasonability test in my opinion.

I feel your pain on the cash position, I have done the same. I am looking for the s & p to get close to the Schiller average. Have decided to keep waiting: though every time I see these inflation numbers I question that decision.

The biggest mistake was to expect the Fed to stand to their duties and post.

You have alot of company and rightful so.

Last time inflation was here fed funds were over 10%, now .3

Who knew it wouldnt be this time?

Some did

My IRA is in all cash currently, and I expect there to be steady downward pressure on markets for at least another year. Like yourself, I missed out on this most recent upswing. But, I do plan on trying to put some money into the market after the next downturn that then moves upward. I’ll be conservative and only put money in for days at a time, 3-5 at most. I did this a couple of times in Jan / Feb of this year and made out nicely. My money was in the market at most 3 days.

Once I feel like we are near the bottom, which assumes we’re at the tail end of a recession, my plan is to put money into SPLG, EDOW & XLK, QS, SLDP, PLTR, TAN & QCLN. I may start dollar cost averaging about $10K into XLF over five months starting in April or no later than May, once QT starts. Banks should perform above average as long as rates are increasing.

I’m going to research the treasury bond ETFs out there and dump about $30K in them, once the FED signals rates will be cut. I know investors who dumped money into treasuries when COVID hit made a very nice profit off those bonds. I would obviously sell them once it looks like the FED down the road decides it’s time to start to raise rates again. But this could be many years, so this could be a LONG play. I’m convinced this is how you make money in the bond market. You have to be patient. The market timing isn’t hard, because the signs are the FED signals when they plan to raise & lower rates.

But, everyone has to respect the fact that ALL of this is playing out a lot faster than the FED anticipated, mostly due to the unexpected Russia war with Ukraine. So, once there’s a likely end in sight to that quagmire, be ready to put some money in the S&P500 & DOW.

Why buy a Treasury money market if you can buy the Treasuries directly from the government without middleman and without fees? And they’re perfectly safe, unlike money market funds. Very convenient, too. The site for this is treasurydirect.gov

Thanks for the reply, Wolf.

To clarify, I was talking about my 401k funds that I moved to VANG VMMR-FED MMKT which is the only cash-like option. There is no option to buy Treasuries directly in this (or any, afaik) 401k. Once your money is in the 401k it’s a kind of investing purgatory.

(I also learned a lesson about the “safe” option of bond funds when I finally noticed that bonds where getting routed day-after-day, until I came to my senses a quarter ago.)

The options in the 401k account are limited. Also, you have to be careful about selling something, e.g. FXAIX (S&P500) fund that you might want to buy in the near future, because they don’t allow you to buy (again) what you sold within the some time period — the details of which are not clear to me.

Yes, 401ks are a problem. They’re designed to generate fees. Within them, you’re not allowed to buy bonds directly from the government. I didn’t realize you were talking about a 401k.

That was a question I had. How do I directly buy bonds in my 401k?

Is it true you can’t even buy bonds thru a self directed acct in your 401k?

They way out of this is to change jobs and roll the 401(k) into an IRA. IDK if it is legal (consult relevant professionals) but a single day termination and rehire into the same position (if possible) might be enough to trigger the rollover.

Jake, you may be able to do the following: “transfer” your balance in the 401K to a brokerage, like Schwab or similar. But make sure your company’s HR department and the 401K will let you do that without: 1) bouncing you out of participation in the company’s 401K operation, either temporarily or permanently, 2) damage or eliminate your matched contribution. You may be able to do it as an IRA Rollover or similar. Don’t do it in such a way that it becomes taxable. My wife recently did this. Her 401K provider is Ascensus or somthing.

Regarding personal investing, read a lot. Get many perspectives before convincing yourself that you know what’s going to work.

Look into self directed ira in a trust. Watch out for loss of ERISA protection when moving totally out of 401k. One lawsuit could ruin the rest of your life. Just saying.

Wolf, what do you think about the Federal Thrift Savings Plan, and buying short term treasuries through its G fund? Always wanted to know the difference between the TSP and say, a Vanguard fund.

You’re asking the wrong guy.

Someone here surly works or worked for the USG and participates in the TSP, and researched it, and they might tell you about their findings.

Just google “tsp g fund.” It gives some nice little charts and stats on return. I found this particularly interesting:

“While the TSP G Fund is not guaranteed to outpace inflation, between its inception and 2010 it managed to do so, by a significant margin.

However, in recent times, things have changed. Due to historically unprecedented Fed stimulus and low interest rates, the TSP G Fund no longer outpaces inflation as of 2020.”

I just realized that information wasn’t from the actual TSP website, that was my bad. G Fund has performed worse over time (in ’88 it had a return of 8.81%), but it does appear to be a safe option.

TSP Website:

1 year 1.51%

3 year 1.47%

5 year 1.94%

10 year 1.94%

Since inception 4.70%

Wolf-i may be surly, but don’t call me shirley…(…and autocorrect will surely be the end of us…).

may we all find a better day.

VUSXX is the Vanguard Treasury Money Market fund and is their safest offering…..tossing off 0.08% annually (taxable adding insult to injury). Note that a “safe” stodgy tax exempt vehicle like VWLUX (long term muni bond fund) is down 7% YTD and sinking like a whale turd. Looks like the only safe harbor for the risk intolerant is cash or a cash equivalent.

You can buy FRN, Floating Rate Notes.

30 yr mortgages STILL way under inflation.

At least 3%….and wait till the inflation numbers in April with the Ukraine effects included….could put the difference at close to 5%!

Contrast….Last yr 30 yr mortgages close to even with inflation rate.

Inflation and thus replacement costs of housing still put buyers in the market. IMO.

As far as I know, 30 year fixed rate mortgages are not available in Canada. The typical mortgage has a fixed rate for 5 years based on a 25 year amortization schedule and then the borrowers need to renegotiate their loans with their lenders. Will the surge in interest rates finally pierce the housing bubble in high demand areas such as Toronto and Vancouver?

Anon1970: my understanding is that Canadian banks learned the hard way in the 1970’s & early 80’s about the risks of long term fixed rate mortgages in an environment of rising interest rates, and so since then have transferred interest rate risk to borrowers.

It will be interesting to see how forthcoming events answer your question about the Canadian housing bubble. The early 1980’s saw the worst stress in the housing market in Vancouver since the 1930’s. Vancouver real estate today does have more off shore demand than 40 years ago, but that may not be a positive if economies elsewhere, such as China, are also under stress.

Does the value of personal safety and a decent life weigh into the comparison between home prices and mortgage rates between US and Canada?

What???

Yes particularly when Jan 6 comes around again.

I’m confused by the High Yield chart.

Did the spike in yield to +12% happen prior to the first publicized covid cases, then come back down below 6% in early 2020? It looks like the spike occurred in late 2019.

That seems odd to me….

Yes, that was confusing. Excel put the year label in the middle of the year. I now changed that so that the year label starts at the beginning of the year. It’s a lot clearer. Thanks. I usually set it that way but in the heat of the battle today forgot to do so.

Hi Wolf,

Do you have any views on Gold through this increasing volatility ?

I’m not a buyer at these prices (gold had a huge run over the past few years), but wouldn’t sell either at these prices. In my view, gold is something you hang on to – rather than trade it. But if you buy high, you might be in the hole for years. That’s a real risk, and if you look at long term charts, you see that it happens.

The long term charts I’ve seen make gold look like a pathetic long term investment.

Hal-

If by “investment” you mean a financial vehicle that grows and pays dividends or interest, then gold is indeed a pathetic investment.

But if you think of gold not as an investment, but as a choice NOT to invest at present, then gold can be a good choice, largely due to the fact that there is no counter-party, and because it has held value for thousands of years.

If you study some of the people who recommend gold, they usually seem to recommend it as a partial hedge against those periods when both your bonds and stocks do poorly, like the 1970’s, or perhaps the 2020’s(!). That’s why the Fed holds gold as a reserve asset.

Hal 9% return a year for last 20 years damn good

Well I guess it all depends on your circumstances and probably where you live.

The Yen is currently falling like a rock as a result of increased commodity and energy prices and the BOJ action in the bond market.

The price of gold is up 23% in yen terms in the past six months and 494% over the past 20 years.

In Iran the price of gold is up 15615% in 20 years in the local currency. Probably much better than holding the paper currency of Iran.

Or how about Jamaica? They have had a problem with inflation and economic disasters for years. The price of gold there is only up 1983% in Jamaican dollars over that time.

And looking at Russia, the price of gold is up over 54% in rubles over the past six months and around 1552% in 17 years.

Turkey is even worse than Russia with the price up 106% in local currency terms over 1 year and 6923% over 20 years.

And looking at that socialist paradise down south of you guys, Venezuela, the price % figures are off the chart in local currency terms as their inflation is actually hyperinflation.

And Zimbabwe? Couldn’t find the figures.

And looking forward which one of those countries will the USA look like in a couple of years?

100%

Just to add the obvious, headwinds facing the “gold bugs,” as Uncle Lou used to refer to them, include the opportunity cost of holding a non-income producing asset in the face of unpredictably rising interest rates. Boomers need income and young whipper snappers are more enamored of digital assets. Such leaves a big hole in demand save for government hedge buyers.

“And hedge funds that are short Treasuries…”

Who lends their Treasuries to hedge funds for shorting, govt. pension funds, private holders, the fed?

Prophet…

Hedge Funds likely use the Treasury Futures market. (CME)

Ah, yes, thanks h! So, the article is somewhat misleading, although still most excellent. Hedge funds short futures contracts – a derivative, not actual Treasuries. Point being, Treasuries can’t be shorted, though I could be wrong.

In Seattle area I’m seeing lots of houses going up for sale that were purchased no more than 2-3 years ago. Many homeowners are opportunists, attempting to capitalize on quick gains. I’d say about 30% of the sales transactions fall into this category.

There is a huge investor element to this market that didn’t exist in 2007. That’s why this housing bubble could be bigger than the last bubble, and pop just as quickly. People are underestimating the impact of rising interest rates, which is what moves investors.

I see this too, at all prices in my area, the two-year tax-free flips. Many exhibit the tackiest and cheapest of modern remodeling. They are still selling, but these owners are essentially younger investors at the mercy of higher rates. There is no rental investment at these prices.

I see this happening outside the flipper market.

Some people who bought a home two years ago with an intent to live in it are now saying “let’s sell” in order to capture a quick 40% gain in Seattle. The sharp price rises have turned stable home purchasers into flippers.

Then you have other home owners who think there is a permanent supply/demand imbalance that will last forever, along with 20% annual price growth. But they will not be the ones setting the market price because they are not transacting.

I sense many homeowners are emotional and think they can keep the market high as long as they don’t decide to sell, as an individual. Human nature, I guess.

Bobber,

Here on the Eastside of Seattle there is still a very strong job market [my son-in-law just quit one tech job after 12 years for a much more lucrative one, with full work from home option] and a limited supply of land or houses.

Add to that the Eastside is a great place to live, if you can afford it, and I say that as someone who lived on the Westside of Lake Washington from 1965 til 2019.

So hard to see prices going down much, but I can sure see them flattening out. Unless all the tech jobs move to China or Texas. Might not happen with all the WFH, but there might be some pay cuts.

As for Seattle, if Boeing goes tits up and the city keeps refusing to fix quality of life issues, I can see a big drop coming.

Like I said, all real estate is local. Seattle could go down while Bellevue/Redmond keeps going up. I am not planning on going anywhere and I can ride out a drop in house value til I kick the bucket. It would just mean lower property taxes. I suspect there are a lot of homeowners in the same situation.

My recollection is that the 10YR and 30YR spiked intra-day to 0.31% and 0.66% around March 23rd, the 2020 stock market low. That’s what I see in the charts I have.

Bonds have been declining for about two years and I expect a preliminary low this year. I also expect a bond correction rally even as the FRB lifts its target rate and as QT is in process which will mystify a lot of people. The intermediate part of the yield curve has already had a noticeable run-up in anticipation of coming FOMC rate increases.

Where I live in ATL, rising mortgage rates should probably cause some buyers to lower expectations if they still qualify. Prices aren’t as inflated as the coasts or NE.

Augustus Frost,

Yes, there was a HUGE amount of volatility during that panic intraday, collapsing to 0.32% intraday on March 9 and closing at 0.54% that day and a few days later it was back at 1.22%. But these yields here are closing yields.

I covered that mayhem at the time, and this is the chart I posted back then, for people who might have forgotten all that fun:

So far the higher mortgage rates have not affected sales of Condos here in the Swamp. They are the only starter homes that are affordable and are selling in a reasonable time if priced appropriately. We are busy as heck with no letup in business. Who was that Realtor who posted a comment on this site that “No one wants condos” ? That’s why I never pay any attention to Realtors. Most of them don’t know what they are talking about.

Mortgage rates vs Inflation…..is a big consideration for those with money looking for a place to put it..

The difference between those two rates still encourages investment buying of real estate, IMO. That will eventually change, perhaps later this year.

Condos are this generations mobile home. Realtors would like to sell SFR to entry level buyers, even if they cannot afford it. (Like 75K PU trucks) This market has lift, and they are talking their book.

The only question is whether we get a mild recession or a nasty one. The train has already come off the tracks, it just hasn’t hit the ground yet.

Corporate profits are at all time highs.

Until they are not

I pay attention to the 2 year treasury yield. At 2.5% it is getting close to the utility ETF yields (XLU 2.88%). I moved much of my bond allocation into utilities the last few years as higher coupon bonds matured. Looks like it is time to consider moving from utilities into 2 year treasuries.

“The yield curve still says nothing about the economy because it is still an artificial construct manipulated by the Fed”

The market is going to prove this assertion is wrong by the end of the year.

Yancey Ward,

States, businesses, and consumers still sit on trillions of dollars from the Fed and from the government that are going to get spent. It’s mathematically almost impossible to have a recession this year.

And the consumer is shifting spending from goods to services. Tourism, plane tickets, neglected healthcare treatments, concerts, shows, ballgames, etc. Services were the laggard. They’re the biggie in this economy. And they’re now hopping.

There is a huge and real labor shortage. Businesses cannot hire enough people to grow. Even if 5 million open positions disappear, that leaves 6 million open positions which would still be historically high. For a recession (the NBER declares official recessions), you need a consistent decline in actual employment. That’s just about unthinkable now.

And watch the yield curve steepen as the Fed kicks off QT. That will push up long-term yields, which will fix your recession concerns for this year.

At some point we’re going to get a recession. We always get one sooner or later. But not this year.

Wolf-

I read somewhere a prognostication for an “earnings recession,” in 2022 due to the huge increases that many companies are experiencing.

BS, or some degree of validity?

Thanks

We’ll see :-]

Meant to say “huge cost increases”

Nov 2022 after Q3 earnings. That is when recession will start.

Fancy way of saying “after midterm elections”.

I agree, because that is when any food shortages will really start to kick in. Shortages won’t become apparent until this year’s harvests. If there is a lot less than last year then prices will really climb. If the Ukraine war is still going on (and this appears the objective of US foreign policy), I think the US will have implemented harder sanctions, and Russia harder countermeasures. And the shortages in gasoline, diesel, metals, etc. will have become more pronounced.

If current trends continue (always a most dangerous assumption), the current administration may be a lame duck after the midterms. In that event, how the Republicans decide to deal with the shortages and Ukraine is the million dollar question.

“States, businesses, and consumers still sit on trillions of dollars from the Fed and from the government that are going to get spent. It’s mathematically almost impossible to have a recession this year.”

I wholeheartedly agree with this. There is so much money sloshing around right now that it’s almost unfathomable. The spike in fuel has done nothing to even thin traffic out. I ran into a massive traffic jam today where a road was completely blocked from people turning into a plant nursery, and the problem was the parking lot was completely full so it was spilling out onto the highway.

I really don’t see any “deals” on anything happening this year. There is still way too much money chasing not enough goods and services. They overheated the economy by such a disgusting amount that this in and of itself should generate an emergency rate hike of 100 basis points. Instead, the FED is sitting back and letting this thing roar.

The Fed really should raise interest rates much quicker to incentivize saving (i.e. prevent all that cash from hitting the economy at this moment when there are supply shortages).

The whole Covid stimulus thing never made any sense to me. When you shut down the economy (i.e. produce less), you should remove money from circulation, not add more. Only add money when it is matched by higher production.

Of course prudence doesn’t win votes. Now they are talking about fuel stimmies! We are so fv$ked…

but what about the fact that 70% of spending is consumer based, and the money sloshing around is not in the hands of the average consumer? can the top 10%, who received the bulk of the “stimulus” keep us from falling into numerical recession?

No, it isn’t and can’t true, whether there is an NBER defined recession or not.

If it were true, then the US and any other country could perpetually avoid recession forever simply by borrowing and “printing”.

Augustus Frost,

Well, no, because what you get from money printing is inflation!!! Which is the specific problem we have now. Money printing works until you blow up the purchasing power of the currency, which is NOW. That’s why the Fed is now trying to undo the damage.

yushan, exactly. given that much of the economic loss was caused by government policies, it made sense for congress to make people whole who were harmed by those policies (think of it like an eminent domain taking). but it never made sense to give money to individuals who didn’t lose income, to give people “unemployment benefits” that exceeded their pre-job loss income, and to give business owners who never lost income paycheck protection welfare.

shutting down production and then dumping 4-5 times the money lost into the economy was the height of stupidity, and we’re now paying for it dearly.

augustus, wolf would be right that there isn’t a mathematical recession if gdp doesn’t contract, even if inflation means that that gdp is buying less services and goods than it did before.

that said, i’m not convinced of his thesis. while there is a lot of “stimmy” money still out there, none of it is in the hands of the lower middle and middle class, who spent two years splurging on all sorts of crap with their newfound “wealth.”

because of the “base effect,” gdp doesn’t have to drop to 2019 levels for there to be a recession. it just has to drop below the inflated number from q4 2021.

By “splurging” you mean buying food and paying medical bills?

no, apple, i mean splurging. look at wolf’s articles from the archive showing spending on consumer goods.

there’s a reason that apple and amazon had banner years, and it wasn’t due to paying rent and food.

“…while there is a lot of “stimmy” money still out there, none of it is in the hands of the lower middle and middle class, who spent two years splurging on all sorts of crap with their newfound “wealth.””

Jake – a couple things:

First, not every beneficiary of the “extra $600” in addition to their regular UE bennies blew all the money by now. Some did, but others accumulated more savings than they ever had in their lives and are still living off of it. There is no way to calculate how many people are doing this, but some of these people were earning 3x what they did on the job, and some were even working under the table for cash at the same time (construction laborers, etc.).

Even more important is the fact that we are in the most massive housing bubble in the history of the world, so the FED’s precious “wealth effect” is playing out as the sheep think they magically got rich because their house just rocketed up in value by 2x or whatever. They suddenly count this as money to play with even though they have to pay it back once they do the cash out refi. Or, they don’t borrow against it but instead borrow for a new car with the knowledge that their house went up by much more than the price of the new car so it’s “free.”

These are just a few scenarios which are part of the situation we are in right now. Remember, last housing bubble was exactly the same in terms of consumption proclivities, and this was without $10+ trillion of stimmies. This pig is so overheated it’s beyond disgusting. But Weimar Boy Powell just sits back and does almost nothing.

I’m surprised you are so sure no recession this year. What about oil/energy prices?

I think that could shut down consumer spending more quickly than people think. The impact on business would be those 11 million job openings rather suddenly disappear.

If growth slows down a little, it’ll slow from 5.7% growth last year. So maybe it’ll slow to 2% or 3% growth. Except for 2021, there hasn’t been a year of 3% growth since 2005. 2% growth is considered pretty good for the US. 2% growth is NOT a recession (all figures year-over-year inflation adjusted GDP).

That huge gap between the one month and one year Treasury yield – and the rest of the curve for that matter- shows just how out of whack the Fed’s rate policy still is … the only thing keeping short yields that low is the Fed is sitting on them.

It’s not only behind in raising short rates, it’s holding them down. For all its big talk about getting tough on inflation, its action is pulling the other way. The bond market is running out of patience.

Yes, the yeild curve is insance now. Still only 1% for the first 6 months. Then from 2 years to 30 years, you only get paid an additional 30 bp to tie up your money for 28 more years.

A lot will depend on the impact of gasoline prices if they are permanently higher. I’m sure everyone’s heard an anecdotal story or two about what folks are doing to cope. I’ve noticed a significant reduction in traffic and traffic noise in my neighborhood.

Wolf,

Regarding junk bonds still in la-la-land, could this be partly caused by the fact that a large part of the junk bond space originate from the oil & gas sector (frackers etc) that now got bailed out by the high energy prices? Or is this across all economic sectors?

It is weird because unicorn stocks have received quite a beating recently. You would expect unicorns and junk bonds to be strongly correlated.

Maybe. We know what caused the spike in junk-bond yields in 2015/2016: most of that was oil & gas that went bust, some of it was brick-and-mortar retail that went bust, and a few other industries. It was fairly narrow. I covered that at the time but don’t remember the details. And yes, the weak oil & gas players already went bankrupt, and now oil and gas prices have spiked and the survivors are making money, and their junk bonds are looking pretty good.

But there is still a chase for yield – makes sense when you think that CPI inflation is 7.9% and B-rated junk bond yield is 6.5%. Investors are trying to find a place to hide from inflation, and so junk bonds are still seen as that, and there is still strong demand for them at those yields.

Wolfburger, it seems that the bond vigilantes, a moniker penned from the Junk Bond days of Michael Milken in the 1980’s, are back in town and are selling bonds with a vengeance. The supposedly omnipotent Fed is sorely looking like a Little Rascal character with his knickers around his ankles trying to run and kick a soccer ball.

Personally, being retired and having the luxury of being able to watch the ticker tape during the day, I am waiting with baited breath to enter either a 20 to 30 year long term bond market short position, or more interesting and maybe more profitable, a long-term High Yield Bond, junk that is, very shortly. It is still the interest income investor, starved for yield in a hyper-inflating economy, that is propping up the riskiest of the risky Corporate Bonds. But I see the Four Horseman breaking the crest of the horizon and they will soon be riding into town.

Junk bond yields will have to get above the current rate of inflation going forward to continue to attract investors. Spreads over Treasuries and Investment Grade Corporates have to increase in a pre-recessionary world. And just wait until the defaults in these Shaky Eddy debt instruments start to bubble like a Fed-induced bond market bubble. Keep a close eye on the moola being lost in high-yield bonds as issuers run into all kinds of cashflow problems in a war-torn, inflation ravaged, weakening global economy. Better than a Saturday matinee serial.

”bated”,,, not baited DWY

otherwise agree

The time to short TBonds was back at the beginning of the year, or better yet even in mid 2020. This looks to me more like one of those blood-in-the-streets moments in Bond Land.

There may be another good selling opportunity somewhere ahead, but IMO it’s unlikely to be soon.

One of us is going to be wrong. I’m currently buying TLT hand over fist. I realize I’m early(ie, losing money). But to me that just means I’m buying at discount. I’m buying not because of what’s happening now but because of what’s going to happen Q2 and maybe into Q3.

The yield curve is moving towards inversion. The 5 is already inverted relative to the 10. If the feds continue to raise rates they’ll end up inverting the entire yield curve –> recession.

It would be a different matter if the Feds controlled long rates but they don’t. They can try to raise long rates to stop inversion by selling bonds (ie, QT) but whose going to buy bonds with prices dropping?

Let’s not even get into what the stock market will probably do.

VVNV-dunno, have encountered more than a few with (phew!), ‘bait breath’, and they weren’t even fisherfolk…

may we all find a better day.

Junk bonds suck. All the dividends gets reported to the IRS as ordinary income while the capitol losses which you usually get are not deductable except as long term capitol losses.

So… what’s going on with spreads these days? lol…

1) The bond massacre produced NDX dead cat bounce.

2) US 2Y @2.51- German 2Y @ (-)0.13 = 2.64. The 2Y horizontal line,

the flat accumulation area, is about equal to the vertical line. This dead cat bounce might be over.

3) The yield curve is defective, but the stock market isn’t.

4) The 2Y dead cat bounce reduced the junk bond spread.

5) Fred : high yield spread is down to 3.67 from 4.21 on Mar 15 2022.

Both are rising lately, but US 2Y jumped higher this week.

How will all of this volatility effect mortgage REITS?

AGNC lost a third of its market value in anticipation. Book value went down and earnings will eventually improve but much depends on their interest rate hedging (black Magic or charitably “rocket surgery”).

6) After reaching 99.42 USD entered a gas station.

Yahoo: US Treasury selloff sends yields racing past limits of bullish era…

Bloomberg:

With the Federal Reserve poised for an aggressive cycle of interest-rate hikes, 10-year yields have surged to nearly 2.5%, the highest since May 2019 and up more than a full-percentage point since early December. That’s a far faster and steeper increase than before other monetary-policy tightening cycles, and it has already driven the benchmark yield past a technical trend line that has effectively served as a ceiling since the late 1980s.

The 10-year yield has tested the threshold before only to snap back each time, rewarding investors who saw it as a buying opportunity and burning bears who thought it signaled the market was finally past its peak. It’s possible such a pull-back may happen again.

Six more fed rate hikes this year? Yeah, baby! (but I’ll believe it when I see it)

Why is the Federal Reserve just sitting by and not doing much of anything in terms of raising its overnight interbank Federal Funds Rate? The key significance is not that the Federal Funds Rate has any real impact on anything other than sending a message to the markets as to interest rate policy guidance by the Federal Reserve. The Taylor Rule which is still a part of Federal Reserve policy shows that the Federal Funds Rate should already be at 9.5% rather than the paltry little irrelevant level it is currently at. The timidity of the Federal Reserve never ceases to amuse and amaze. By contrast, the Russian central bank last month raised their policy guidance rate from 9.5% to 20% in a single move overnight. The Federal Reserve should try some similar moves and get the Federal Funds Rate up to 10% without any further delay.

SoCal

Agree. The Fed has either been ignorant on purpose or ignorant via wishful thinking.

The Federal Reserve can and has done good work, in the past.

BUT, in the last 15 years or so, the Fed has been “off the rails”.

They ignore their mandates of “stable prices” and “moderate long rates” by promoting ANY inflation (their 2% target rate compounded for 10 years takes the dollar purchasing power down 22%, how can that be stable prices? Add in the last year of 8% soon to be registered in double digits.)

They pounded down long term interest rates to “immoderate” all time lows!

Their own Rules for Monetary Policy, which can be read at the Cleveland Fed website…has 7 calculations for Fed Funds given GDP, employment, inflation, etc.

The MEDIAN of these 7 calculations has Fed Funds at 3.25%, with the Taylor rule (one of the calculations) as you mention.

So they ignore their mandates, they ignore their own rate guidelines.

Then, to top it off, they explode the money supply 40%….not to “meet the demands of an expanding economy” which is their charge, but to PUMP ASSETS.

In a system that boasts of “checks and balances” ….WHO CHECKS THE FED?

Exactly!

Why in the hell would you want to check the the cartel providing nearly free money crack?

The Fed lost it when they discovered celebrity politics with Greenspan…

COWG

Look at the loser he’s (Greenspan) is married to and you don’t need go no further.

where can you possibly coming from h, when the total collapse of the USD since start of FRB is AT LEAST 99%???

FRB has been THE very worsT for WE the PEONs,,, at least we savers, etc., who have been able to put our gold in the dirt in the yard before ”THEY” started the FRB to stop or slow our doing so, etc., etc.

I really thought, based on your many good relevant comments on WS that you understood what a truly criminal element FRB has been since it’s beginning, and only exacerbating that criminality recently???

Please read again

@ historicus –

“The Federal Reserve can and has done good work, in the past.”

———————————————–

read once or read twice, the above quote is what stands out

SocalBD-

First, the Fed is a failed institution with an impossible triple mandate. I’m guessing we agree on that.

But inflation is forcing the Fed’s hand to “allow” rates to rise, which they are FINALLY doing, and intend to gradually continue, at least for now.

Seems to me, though, that your suggestion to raise FFR to 10% immediately would:

a) lead to mass bankruptcies and business failures

b) create huge and immediate portfolio declines for individuals and retirement plans

c) create huge job cancelation and a spiked unemployed base

d) send the US into a repeat of the 1930’s

Not saying that the poky, deliberate and telegraphed course the Fed is following won’t still end in “a” to “d” above, but a 900 bip increase in FFR would be suicidal, IMO.

“an impossible triple mandate. ”

Disagree.

It is only when one brings in “what will it do to the markets” does it approach impossible.

But lets remember…the FED encouraged the “cattle drive” to housing and stocks by their policies. They NEVER should have done that, IMO.

Imagine if they didnt pound down interest rates, kept the yield curve positive.

Imagine if they didnt pump the money supply 40% in two years.

THEY put us in this position.

For 70 years, Fed Funds tracked inflation….usually EXCEEDING the inflation rate. Then suddenly…..no more.

2018 was the watershed. Powell had Fed Funds at 2% and inflation was 2%. But the markets (and Trump) didnt like that. That should NOT be a primary concern for the Fed. The Fed caved.

The markets should adopt to the Fed, not the other way around.

And the Fed should do their duties and stick to their guidelines, rules and mandates…all of which are part of the agreement (Federal Reserve Act 1977) that allows their existence and special powers. IMO

Not to mention the politicians in Washington FEASTING on the FREE money Buffet….and loading up the future with $21 Trillion and counting of new debt.

The use of the word TRILLION is now commonplace in Washington…..15 years ago it was only attached to national debt discussions.

$9 Trillion in debt for the first 215 years of the nation.

$21 Trillion additional in the past 12 years. (the result of free money for politicians)

Historicus-

I’m in agreement with your statements:

– “ the FED encouraged the “cattle drive” to housing and stocks”

– “ THEY put us in this position.”

– “ The Fed caved.”

But how can the Fed hope to control employment, inflation, and long term interest rates?

Furthermore, how does one measure “maximum employment,” “stable prices,” or “moderate long-term interest rates?” What the hell is a “moderate long-term rate” anyway??

Finally, actions that manipulate one mandate in a positive way effects another mandate negatively. That’s what I meant by impossible, not to mention the thousands of butterfly-wing type unintended consequences…

The real goal of the Fed is to orchestrate the command economy function, to the benefit of vote-hungry politicians and self-serving bankers.

IMO.

The Fed did not force people to buy homes. The homeless shelters are full and only allowed temporary stays. In most cases people who own their own homes retired with more wealth than those who rented.

Legislatures enacted spending programs that created budget deficits requiring expansion of the money supply. A quarter percent Fed funds rate hike will not amount to a pile of beans.

100% correct.

The Fed encouraged spending money before it depreciated due to inflation.

They caused the inflation.

They put mortgage rates at all time lows, while encouraging inflation.

They admitted they Forced investors to take more risk, thus they altered risk return ratios and PE ratios by their decisions.

Is that their job?

Why would any of that happen? The overnight increase from 9.5% to 20% in the Russian Central Bank guidance interest rate had very little impact other than to stabilize the Russian economy.

Is the Russian economy stable? I hadn’t heard…

The dust would settle within two years, and only the people who benefitted from bubble pumping would be wiped out. In other words, the ones that received the benefits of theft would be the ones to face the consequences of theft. The capital would still be there after bankruptcy and so would the human needs and wants that require a workforce to fulfill. Standard of living would be likely be lower for a decade, but maybe that’s a fair price to pay to purge rampant corruption and grift.

That’s your own theory, John H., and it sounds like some sort of nonsense the FED would burp forth.

Maybe the Fed is squeamish about public mental whiplash from another round of WTF volatilities. So much for political independence. Funny, they weren’t squeamish about the ones that posed as ultra-frothy asset prices rises. I guess they would like the intoxicated party whoopee atmosphere to continue, even as the excess cash bleeds off. It all builds toward a bigger hangover on Someday Street.

The Fed should be squeamish about holders of dollars losing 8% or more just by standing still.

What do our creditors think? I think we are about to find out.

Powell’s legacy might just be “dollar loses world reserve status”….and maybe the drive to digital currency is a deflection from this likely event.

> maybe the drive to digital currency is a deflection from this likely event.

Or maybe it is like getting desperately onto a lifeboat bound for Seattle, but not sure if Seattle is there. And that could be while being strafed by rivals.

SoCalBeachDude wrote: ” Why is the Federal Reserve just sitting by and not doing much of anything in terms of raising its overnight interbank Federal Funds Rate? ”

Everyone here seems to think only the FED RESERVE is capable of acting against inflation. The Federal Government could raise taxes on the Top 10% who benefited the most from the stimulus. Claw some of it back in that way.

But they won’t. And for the same reason the FED RESERVE is slow to raise interest rates. It would hurt the wrong people.

Manchin Wants $1 Trillion Tax Increase…

Biden to unveil new cost on billionaires…

Never happen. Dems may pass the law, but rich people have planes and they’ll have their businesses in Asia before the ink dries.

And the so called wealth tax on unrealized capital gains will be found unconstitutional.

Mass riots ,

Over what?

China warned them not to raise rates to fast ,I believe China ic new world super power in WOLfS clothing = I crack myself up

NOT A PARTICULARLY GOOD SIGN – MAD DASH FOR TRASH!

WSJ: Riskiest Bets in Stock Market Are Most Popular…

Crypto…

The WSJ article was focused on securities, mentioning investors piling into SQQQ, various inverses and short ETFs and such.

Bond losses seem more hidden than stock losses….but they are real and massive.

Read your chart. Chart don’t lie. The chart send a bearish signal, though a weak one, to be confirmed.

After Sept 11 2001 low SPX bounced back up for half a year to a lower high, until Mar 2003.

7) Ilan might send Wolfstreet to Mars.

Time for a Wolfstreet SPAC/IPO/NFT. Beer mugs to the moon!

Wolf, could you please if possible move the reply button to the left?