Buyers hobbled by spike in mortgage rates and sky-high prices. Builders hobbled by shortages and worst spike in costs ever recorded.

By Wolf Richter for WOLF STREET.

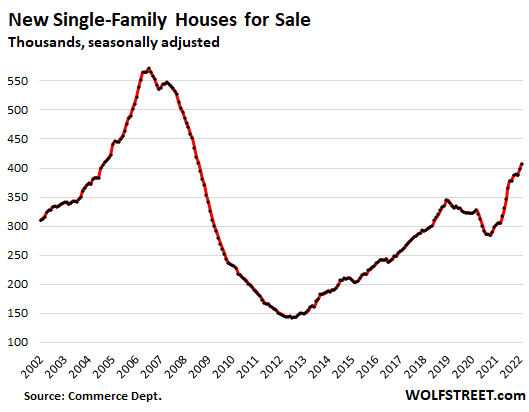

The inventory of new single-family houses for sale rose to 407,000 houses in February (seasonally adjusted), the largest unsold inventory since August 2008, up by 40% from a year ago. This represents 6.3 months of supply at the current rate of sales, according to data from the Census Bureau today.

A problematic mix. Homebuilders are facing historic spikes in costs, and they’re hobbled by shortages of materials, supplies, and labor that have been stalling construction projects and impeded the completion of projects. Potential buyers are hobbled by surging mortgage rates and prices that last year spiked into the sky. This is turning in to a problematic mix.

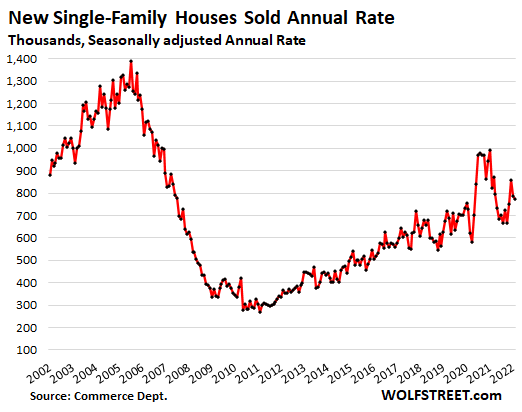

Sales of new houses in February fell to a seasonally adjusted annual rate of 772,000 houses, down 6% year-over-year. Sales remain far below the boom years of 2002-2006.

Sales of new houses are registered when the sales contracts are signed, not when deals close, unlike sales of existing homes, which are tracked when sales actually close. Trends of new-house sales tend to be an early but volatile indicator of broader home sales.

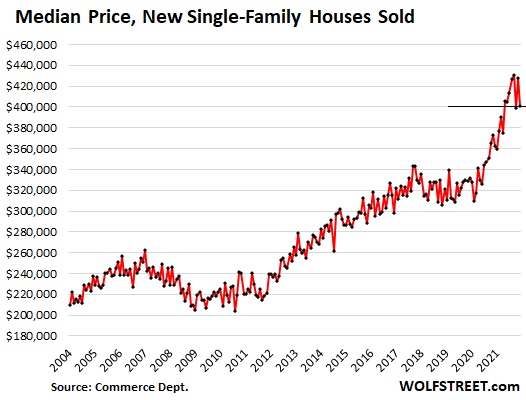

The median price of single-family houses sold, having apparently hit some kind of ceiling last year, fell to $400,600 in February, down about 7% from the peak in November 2021 ($430,300), having now bounced up and down in the same range since July 2021 ($406,000).

This whittled down the year-over-year gain to 10.7%, from the year-over-year gains of 20% to 24% that had raged last year through November.

Note the ridiculous price spike from June 2020 through July 2021, and how prices might have bumped into some sort of ceiling late last year:

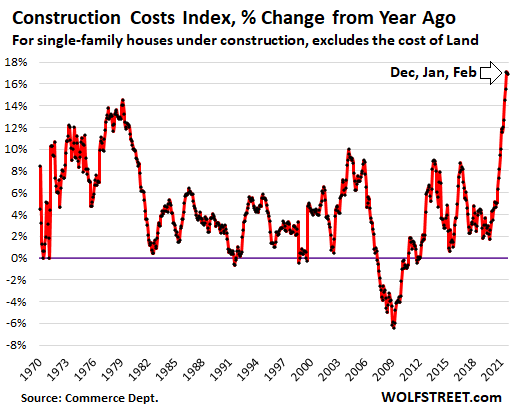

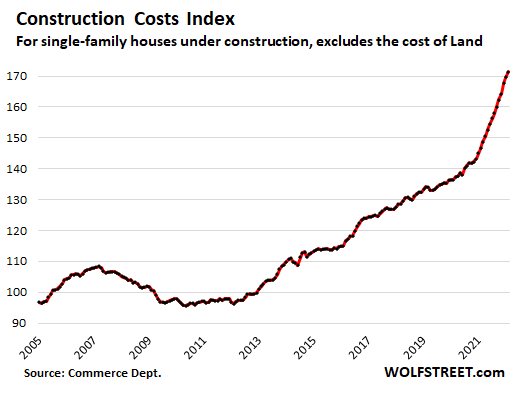

Construction costs of single-family houses – excluding the cost of land and other non-construction costs – spiked by 17% year-over-year, the third month in a row of 17% spikes, according to separate data from the Census Bureau today. These were the worst cost spikes in the data that go back to 1964, amid all kinds of shortages and delays, and with everyone being able to pass on higher prices.

This chart shows the year-over-year increases in the construction cost index of new single-family houses:

The chart below shows the actual index, with index values. Since June 2020, the index has spiked by 24%. Note what happened during the Housing Bust: Between April 2007 and February 2012, the construction cost index fell by 11%:

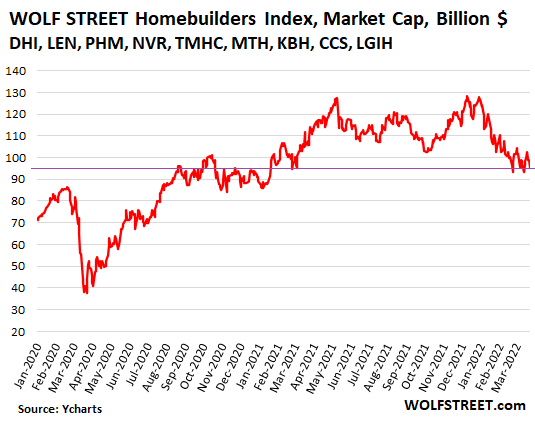

Homebuilder stocks swooned upon the news. Their stock price moves by early afternoon today:

- R. Horton [DHI]: -4.3%

- Lennar [LEN]: -3.6%

- PulteGroup [PHM]: -3.2%

- NVR [NVR]: -1.5%

- Taylor Morrison [TMHC]: -4.7%

- Meritage Homes [MTH]: -4.4%

- KB Home [KBH]: -4.5%

- Century Communities [CCS]: -4.7%

- LGI Homes [LGIH]: -7.8%

But sentiment about the homebuilders has been souring since December last year. The WOLF STREET Homebuilders Index, based on the combined market cap of the above nine homebuilders, fell 4% as of early afternoon today, is down 26% from the 52-week high last December, and is back where it had first been in August 2020:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Question: At least in my experience, the big homebuilders listed above only build on property they own. How does the land value track YoY, or does it?

They also build in the lesser-desirable areas, because that’s where the land is open for tracts.

The accumulating inventory is interesting, but I’d bet that the majority of that is in not-so-prime locations (including the regions themselves).

Not so prime areas become more attractive when that’s all you can afford.

been looking at new home prices – still 30% higher than existing

closed on one today, in escrow on 2nd and looking for 3rd

gonna be great rentals

i wouldn’t necessarily say less desirable, just older. in most places i’ve lived, the inner ring suburbs are basically fully built out, so large buildable plots only exist in the farther out suburbs or even exurbs.

but they’re not so much undesirable, just different based on what you’re looking for.

Depends on the psychology…

Many outlying areas were the boonies until becoming developed with houses, then the shopping support, then the services (docs, dentists,schools, etc)…

Until one day, magically, it became THE place to buy….

See: Northern St. John’s county FL…

Land has actually lost value the last decade. This reflects the moribund policies of most city planners. “The low cost of this land reflects the high cost of development..” Some of the high cost of building, besides being the low cost of land, is labor and materials, strict immigration laws, and better economic opportunity in countries which border the US. Inside the US tech revolution created a generation of couch potatoes. Now anyone can do the physical work needed in construction (using a 16 oz framing hammer all day) but no one is. Computers can do anything, right? So manufactured housing seems like the stock reply and more synthetic materials. Housing costs like all costs are going to come down. This burst of inflation is an antediluvian vision of Christmas past. Worse than transitory it is anti-progressive.

Some thoughts…

– Last year would have been a great time to sell a new house due to low interest rates (FOMO). In my area many homes did not finish in time due to lack of everything from windows, bathrooms, garage doors, to qualified electricians and plumbers.

– The builders of new homes cannot just sit in them like existing home owners, and will be forced to sell before rising mortgage rates make selling even harder. Perhaps the new inventory that has piled up will have to go on fire sale. This will be the first domino to fall in the housing market.

– Many existing home owners saw their home equity balloon last year, so they took out HELCOs. The variable rates will crush them in a rising interest rate environment which will increase the existing home supply.

Pick your poison Jay, do another round of QE and push inflation up to 30%, or keep rising rates and see the system fall apart. You raised to 2.5% in 2018 and saw what happened. This time it might just take 1%.

40% yoy increase in supply coupled with a 7% decline in avg price over the last qtr is a recipe for disaster. Especially if they have houses incomplete due to lingering supply chain issues.

I do hope they get all planned supply on market soon so that 40% turns into 50%, which could turn that 7% into almost 9% in decreased transaction value. Which could wipe almost $40k off purchasing price.

As rates rise, people will still need housing. Rates may limit their selection, but lower price housing might still be in their eligibility range. These might even be a smarter choice, rather than pushing the envelope on what they can afford. Waiting for the great falling asset values might be a longer period than what many can wait.

Now, if the tycoons and wannabe tycoons had rigged the markets properly this wouldn’t have happened, but then again it’s not that easy to grossly distort markets one way without grossly distorting other markets in other ways.

This is what they euphemistically call ‘free-market economics’, even though it’s well-established that there is no such thing as a ‘free market’, unless one means markets that can be freely rigged.

“Free markets you say? I’ll take two!”

The problem with all the sharp operators (as is the fashion these days) out to cheat everybody else is that everybody ends up getting cheated.

Reminds me of commercial on tv free,free,free,free mesmerizing

New builds are predominantly McMansions thanks to NIMBYs pushing zoning laws favoring larger builds, and builders profiting better off bigger homes. I’ve read actual, 2-3 BR, 1-2 bathroom, practically sized 900-1,200sq ft starter homes are < 4% of the market, and barely a blip on the radar of new builds. What's out there under 1,300 sq ft is ridiculously overpriced, over 50 years old and needs a ton of work (amid a labor and lumber shortage). Young couples are about to find out quick the cost to heat and cool the Instagram-ready open floor plan, vaulted ceiling new Starter Castles they paid over-asking on.

Sure, new builds are generally more energy efficient than a house built in '68, but most people don't need 5+ bedrooms and 2+ acres, and that's not mentioning the skyrocketing property taxes on properties both big and small.

Curious what will become of these new, 3,000+ sq ft mini palaces once the market tanks again and the foreclosures roll in.

I fully admit to being a bitter home shopper. But all I could qualify for was one of those 3% down mortgages with these prices up so high. Judge away, but down payments don't save themselves after the cost of a divorce and $175k in childcare before public school kicked in (life, yanno?). In two years I've watched a 3% down payment look increasingly like throw away of money, and then some (plus, costs of reno). And now its happening: houses in my market/price range have been dropping asking prices 6-10% in the past 2 months. Morbidly curious where it goes from here.

175k in childcare before public school? What are you feeding these kids, gold coated ribeeyes?

$175K in childcare is about right for a working single mom with 2 kids. Daycare for first 6 years at $1K/month is $144K all by itself. And in a lot of places that’s not even a high-end fancy daycare.

Lots of people got caught upside down on their mortgages last time around in the 2008 GFC. The stories from back then were hair-raising. Despite Obama’s promises, Justice wasn’t done, the wealthy didn’t feel the existential pain of losing everything like so many others did, moral hazard was allowed to fester and here we are, set up for a repeat. With extra “sauce” to boot.

$796/week for two kids under age two at the local no frills childcare center.

$796. A week.

For the ‘work harder’s out there, those were some big ol’ bootstraps to pull up. Lots of avocado toast went uneaten in those years.

In most markets, now that large houses are the norm, the only smaller houses left are in old neighborhoods. And, those, more often than not, coincide with *bad* neighborhoods. It’s just the way it is.

At least you are willing to admit all your problems are the result of your choices and actions.

There a plenty of starter homes. Problem is, for some reason, nobody wants to live there.

I do a search for homes under $200,000 in my county, and there are plenty.

MA:

The key operating words are “starter homes”. I recently read an article in one of the financial funny papers that Millennials don’t want a starter home. They want it all….. in their first home… and are shocked when they find out that it’s formica counters instead of granite and LVP instead of walnut flooring in a starter home, so then go look at McMansions and complain about how expensive they are.

Their level of expectation is different. No two bedroom one bath house on a concrete slab for them……

Marcus, I’m guessing you’re not a single parent legally bound to the NYC area which, hey, feather in your cap. Yeah my choices have been great, they got me to come from damn near rock bottom to successful, educated professional single handedly raising a full family and qualifying for a mortgage inside of 3 years while, ya know, covering daycare, in one of the most expensive areas in the country. Perspective, darling.

Natty, for the cost of childcare you’d expect at least some porterhouses but alas, not even spam in a can.

El Katz, don’t forget all the avocado toast and iPhones, or something else generationally divisive.

El Katz-

I’m not a millenial but I’ll defend them regardless. You need to look at purchases by age range. Starter homes used to be bought by 20-somethings. 20-something millenials no longer can afford to buy a house at all. Instead, they rent. Lily, those 900-1000sqf homes exist. They’re called apartments. And that’s what those 20-something millenials now live in as they try to save enough money to afford a house.

The oldest millenials are now 40 and older. Boomers and GenX were buying their second or even third home by then, and expected to get granite countertops and all that hoopla by then, because it was no longer a starter house, but their main house that they were going to live in until they retired.

The fact that millenials need to wait until their mid-30s or more in order to pay down their massive student loans and accumulate enough capital and earning power to afford the sky-high prices of today’s market means their first house, while technically a “starter home”, is not truly their starter house, but their final, pre-retirement house. So they want to get everything in it that they might need, just like anyone else.

Also, a starter house used to cost 5 digits. For that, no one expected granite countertops. But if you’re paying $500k for a brand new house, then heck yes, you expect a little bit of luxury for that.

Lune,

Back in the day (1960), the average age to get married was about 21 for women and 23 for men, and after they got married, THEN they bought a house still in their early to mid-20s. Now people get married a lot later (first marriage): 28.5 for women and 30.5 for men. If they get married at all, and many don’t get married. So the need to buy a house shows up much later, or doesn’t show up at all. Getting married has nothing to do with student loans but with people’s preferences.

With close to 300k ready for down payment and >$1MM budget, yeah, I want my “starter home” to have it all. But I’m socal I’m told I need to consider less desirable areas or attached homes with that budget. With a good income and spending power, I don’t see why I should have to move to afford a home. I’ll let this bubble play itself out.

Wolf-

Yes, average age of marriage is getting higher, but firstly, that’s also partly a symptom of young people not being financially stable enough to start a family until much older these days.

In the days when you could finish high school and get a good job at the local GM plant that would give you enough money to buy a house, a car, and your wife’s time to stay at home and raise the kids, sure, it made sense to have kids early.

I don’t deny that there are also social and personal reasons why people are delaying marriage and children but undoubtedly there’s a financial component.

Secondly, that’s all besides the point. People bought “starter homes” in their 20s because that was the beginning of their job trajectory. And when they hit peak earnings in their 40s or so, they bought another home. And since they only had ~20 years to live in it, they stayed until they retired or at least the kids moved out.

Whether you’re married or not, people still generally hit their peak earning power around their 40s. If you’re buying a house around that age, it’s not like your salary is going to double in a decade, allowing you to buy a bigger house later on. The house you buy in your 40s is probably the biggest, best, most expensive house you’re going to be able to buy. Doesn’t matter if it’s your first or second or third.

That’s my point that while technically it might be someone’s first house, it’s bought at a stage in a person’s financial life where people in previous generations would have been buying their 2nd house. So expecting the same things that people buying a 2nd house is not that unreasonable.

Marcus Aurelius said: “At least you are willing to admit all your problems are the result of your choices and actions.”

—————————————————–

That’s what I say to everyone not born rich.

There definitely is a financial component to delaying marriage, family, homes. Older millenials (or, as not to make it ‘generational’ lets say people born ’81-’87) graduated HS into a job market that demanded at least a Bachelor’s degree for entry level positions, and tuitions that skyrocketed from just 10 years prior. No sooner did we come out of school, the economy tanked and student loan interest shot up (medical jobs had hiring freezes– so I’m not talking about philosophy majors here. Half my nursing school class was still bartending 6 months after graduation, and 1st grade teachers need Masters degrees to earn $45k/year). We get on our feet career-wise over the next 6-10 years (while shovelling cash at our student loans, healthcare and childcare like a coal oven) and boom, pandemic. (Also Iraq and Afghanistan in there somewhere, for some of us).

I’m not a fan of sweeping generalizations nor excuses as every age group had their issues. I know plenty my age who were well-heeled and doing fine because of it. But despite the sanctimony discussed elsewhere in this thread, the average adult is gonna have some amout of static in their lives (medical bills, job loss, divorce, etc.) that can set them back financially. So why is this group so much worse off?

Taking away the generational cliches and strictly discussing the largest age group that’s emerging into the buyer’s market for housing, absolutely the financials have set us back and delayed our ability to start a family or purchase the quote-unquote biggest tool to personal wealth– a house. Marriage, kids, all pushed back and yeah its by choice in so much that childcare is an entire parent’s salary, healthcare is astronomical, housing is half a paycheck or more and student loans are hanging overhead like a sword of Damacles.

Our parents were on their second homes by 40, while we don’t have a healthy supply of affordable starters at the same age and negative equity from decades of renting. Its been ‘the fault of our own bad decisions’ for so long, its as if no one before us ever married the wrong person or took on student loans. Yet they emerged fine enough, so its also has to be that we’re picky and spoiled, and choosing to delay adulthood, and nothing to do with aging, limited supply housing, limited steady jobs and the largest transfer of wealth in the country’s history.

Maybe all of the above, but its undeniably the direction the cattle have been herded.

Marcus Aurelius,

I agree with you whole heartedly. What needs to be taken into consideration and doing yourself a big favor is buying properties in the $200k range.

Similar to Lily, I was a statistic of divorce with 3 kids but had bankruptcy filed prior to the divorce added to my repertoire of bad decisions. I have been watching and searching for a home since 2015 and finally purchased one that met most of my criteria last year at what I consider peak pricing. This required me to move outside of the metropolitan area.

At 50, starting all over is not easy but is possible as a single parent. My price range was $200k for the very fact that I want to retire and not be house poor.

I commend any single parent raising kids alone and attempting to rebuild their lives. It is doable, but one has to level set.

Yup. Been there. Done that. Don’t like to think about it.

Property taxes, along with other, high taxes in some states, are one factor that will put a ceiling on house prices, sooner or later. People forget that purchasers must look at all costs associated with moving into and paying for a new home.

Too many houses are now mini-mansions, often with huge HOA payments for the more modest ones, and as in 2008, we are reaching levels at which fewer and fewer Americans can afford them. CCP restrictions on the transfer of capital out of China mean that Chinese buyers will not be buying up the real estate in very desirable states anymore.

“ In two years I’ve watched a 3% down payment look increasingly like throw away of money, and then some (plus, costs of reno”

Lily,

3% down is fools errand in the high price market of today…

In a rising market, you can get away with it because the rising valuations will cover and reduce your LTV ( Loan to Value) ratio and produce a solid gain for future profit if you decide to sell…

In a declining market, the 3% is just pissed away with no hope of recovery because of the loss of any equity for your LTV ratio…

And you will have to sell at a loss of value of 40% or more… or you can pay 50% more than your neighbor for the same house…

So you can pay 3% for a house that may decline in valuation that you have to sell for a loss and declare bankruptcy or kill your credit by walking away…

Or you can keep your money in your back pocket waiting for better conditions…

I try not to make financial decisions that make me try to force a square peg in a round hole…

Sometimes the very best thing to do is…

Nothing….

COWG,

At the start of my (second) search *juuuuust before COVID hit*, FHA 3.5% was my pre qual—credit excellent, down payment hindered by aforementioned childcare–but the local market wasn’t kind to FHA requirements (Septic tank 6″ too close to the property line? No home for you!).

Tried a few Rehabs but finding contractors was impossible and the cost was never justified (in-ground oil tanks, possible leaking septic, even a busted water main soaking the front yard but that one came later…).

Moved to 3% Conventional through a first time homeowner’s program, with state grants toward down payments because what idiot turns those down. But, the market grew exponentially ridiculous and grants or no, the math never added up to take on an upside down situation. I was up against all cash offers from investment firms, idiots offering their life savings to buy over asking, cash offers from buyers who would balk when it came time to prove funding (who doesn’t demand proof of funds at offer?), or just general train wrecks of homes.

Granted, in this neck of the woods RE is a tad unique, but I’m sure my experience can’t be far off from the average schlub trying to break free from a landlord.

Now? You bet your last 3% I’m waiting it out and saving away every bottle deposit, despite every agent screaming to buy now. The last property I walked away from, has dropped price over $40k and still sitting there, with their soggy front yard and probably massive water bill.

Nothing to be ashamed of. People like yourself, and myself, have the luxury of not having to worry about losses in values, maintenance, that lack of supplies and qualified labor. We also are stuck with $300K, 400K, $500K+ mortgage on our credit reports and as a constant infestation on the weight of our conscience. No huge property tax bill knocking at our door. No expensive cracked foundations, sinkholes, asbestos or lead paint to remediate. Nothing heavy like that to saddles us down. And now that the real estate market is unraveling, we get to sit back and be entertained.

btw Lily, love your work in the 70s Blazing movie. Can’t think of the title. It will come to me though.

A wed wose. How womantic!

Bingo. All new builds around me are $500k to $700k. Average family income is $72k thus they cannot afford one of these new homes.

There is almost nothing under $300k which would be considered a starter home.

Heck, inventory is at an all time low. 1754 for a metro of 2.2 million and 594 of these homes are the new construction that start at $500k.

Sorry unamused, wasn’t trying to reply to you.

You can reply to me anytime you like, Lily. I won’t mind.

Lily I want you to make an offer on the house with the busted water main- and i want you to make it conditional on them fixing the busted water main prior to closing!

Shells, they’ll also have to fix all the fully notched joists in the basement causing the house to sink and literally sit on the corroding copper plumbing, the shifting foundation, and the roof that’s buckled in 3 spots, because the silly picky Millenial knows there is no way a contractor will get to all that before the pipes burst or the first water bill hits the mail!

Realtor(dot)com, National Association of Realtors, describes Feb 2022 new homes for sale as:

26% Not Started

64% Under Construction

9% Completed

Only 9% of these unsold inventory are finished homes.

There is a large number of homes under construction. Some of these are multifamily homes.

David Hall,

No big change from the prior month. You could have just asked me to post the charts. I often include those charts. But today I had much bigger fish to fry in my article above.

Here is New House Inventory by Stage of Construction:

And here are New House Sales by Stage of Construction:

Finished homes are near all time lows which is what matters. Finished new homes and good old homes are flying off the shelves often at 50% more than listing price.

Rae prices are not slowing down at all.

Here in South Bay Area Area market is crazy and there is literally no inventory of good homes. Interest rate, stock price, inflation or war has no effect on the housing mania. It seems like there is too much money chasing too little inventory and buyers are doing 40% down and have solid credit history and earnings so the elevated prices looks bullet proof.

Kunal,

“Finished homes are near all time lows which is what matters.”

Homebuilders cannot finish their homes because of the shortages of everything, including appliances and garage doors. Check the “under construction” category. Don’t you ever read anything I write in the articles? Do you come here JUST to troll?

Rental vacancies are the lowest they have been since the 1980’s. Housing prices are so high they would rather rent, that drives up rental prices as demand exceeds supply. People tried to escape rising rents by buying houses.

Where I live unsold home listings are a fraction of what they were in 2012 when rental vacancies were also high. In 2006 they were building too many homes, not many years later came the foreclosure crisis that may have peaked c. 2012.

David Hall,

You keep citing this BS rental vacancy number from the Census. Even the Census says it has trouble establishing what units are “vacant.” This is survey based, so the survey goes to a vacant unit. And then what? Or the landlord responds and says they’re going to remodel the unit and are waiting for permits and workers, etc. in which case the unit is NOT considered vacant because it is going to be worked on… There are a gazillion issues with this number, and Census spells this out. Get informed!!!

All it takes is selling ONE house for less than the entire development, and you’ve just repriced the entire development lower. There are going to be mass walkaways AGAIN, because nobody likes to pay for something that no longer is “worth” what they borrowed for it. All of this was avoidable. Blowing bubbles as monetary policy is reckless.

I agree with you, but for the last 10+ years they have been paying for houses not worth what they ‘paid’ for them. Consumers drove the prices up, not the builders.

The Fed drove the prices up. Since 2013, the Wall Street Banks and Hedge Funds have been borrowing from the Fed’s “Primary Dealer Credit Facility” at .25% (now raised to .5%) . That’s why up to 40% of home sales are 75k over list price and All-Cash for Grandma’s house. Tus the Fed has created the Greatest Transfer of Wealth in History. All these Elite want to be in the Rentier Class (read economist Michael Hudson) and enjoy unearned/passive rental income. The competition between these players with more billions to “invest” raises prices and eventually rents. Eventually the middle and working classes will run out of the ability to pack 4 people into a one-bedroom apt. More homelessness will occur. “Let them eat cake” the Elite will say. And then you’ll get a Bastille Day and maybe a French Revolution. It’s all part of the Great Reset: “You Will Own Nothing and You Will be Happy”.

Blah stone and other,investment companies did this with free money,winner take all

HaHa, I knew this would get some action!

Same as the stock market, except that buybacks have been keeping individual stocks up until companies can’t borrow any more to prop up their own stock.

Up to the most recent leg of this manic market starting in 2009, I was wondering where the catalyst would come for the biggest losses in US market history.

Now with gutted balance sheets, a fake economy which has inflated revenues and profits, and the end of the bond bull market dating to 1981, it’s not so difficult to see it.

Even with stocks and house prices at the most delusional levels imaginable, crypto is what really makes me laugh out loud. This is the dumbest bubble in history – people literally buying and selling “nothing” to each other. “Dogecoin?” GTFO.

DC

As bad as crypto is….NFT makes me scream even more.

Powell, and we, are really dancing on eggshells.

I pray one more unforeseen shock won’t arrive soon.

Or, intentional.

We make a serious error when we believe “they” are dumb or stupid.

Perhaps “they” know what they are doing.

Pull back your horizons and perception. If this is intentional, the question is “WHY”, and the answer becomes self evident, horrific, but self evident.

I don’t think this fumbling mess is intentional. At least, it is all tangled already in unintended consequences.

It is going to take some fancy broken field running at best, to thread through this minefield.

IDK about your assertion about walkways. We’ve all made a bad “investment” or 2. Sometimes you take your losses sometimes you stay married to it until it works out for you.

Thetes no incentive to walk away from a perfectly good home and mortgage just because you might be under water on resale value. In fact the effect of pride on a transaction where a loss is involved would IMHO more likely result in a delighting than a capitulation sale/walkway .

Your comment indicates you learned absolutely nothing from the past.

Housing is going to have to drop more than 30% before people will be underwater?

From the FED:

Housing markets have experienced positive annual appreciation since the start of 2012.

House prices rose in all 50 states and the District of Columbia between the fourth quarters of 2020 and 2021. The five areas with the highest annual appreciation were: 1) Arizona 27.4 percent; 2) Utah 27.1 percent; 3) Idaho 27.0 percent; 4) Florida 25.6 percent; and 5) Tennessee 24.1 percent.

The areas showing the lowest annual appreciation were: 1) District of Columbia 6.6 percent; 2) Louisiana 10.2 percent; 3) North Dakota 10.3 percent; 4) Maryland 10.8 percent; and 5) Alaska 11.3 percent.

How long will it be before lumber prices drop to their normal 350-450 MBF range?

When the speculators lose so much money that they don’t have enough sloshing around anymore. BTFD is alive and well.

The speculators can borrow from the Fed at .5%. It’s hard to lose money at that interest rate.

I hope there is a huge market bubble collapse and a crash in single family home prices soon. Not because I like to see people suffer, but because I want to own my own f***ing house already. I’ll be well into my 40’s before it happens at this rate.

Solidarity.

Delusion….

Houses are not liquid. It takes years for a crash to play out. The best thing you can do right now is build a massive cash position and then be able to purchase a house outright when almost nobody can qualify for a loan anymore, just like in 2012. BTW, 2012 was a fake bottom. Hopefully this time we get real price discovery. If we do, you’ll see 75% drops in many areas.

“2012 was a fake bottom. Hopefully this time we get real price discovery. If we do, you’ll see 75% drops in many areas.”

First candidate is city centrals in undesirable neighborhoods that are supposedly gentrifying. The places are actually dumps or near it.

It would take a price drop of 40-50% before we could afford anything where I live, and I’m not getting my hopes up.

DC,

It doesn’t take years for a crash to play out. I thought that in 2008, when we lost 40% equity in under 6 months. The speed of the collapse was remarkable.

Petunia – that is an astonishing rate of collapse. The areas I watched that fell 50%-65% took over 5 years peak to trough. I seem to recall you were in Florida. Let me guess – Port St. Lucie?

DC,

I was in Palm Beach County where the collapse was everywhere from Palm Beach Island to Wellington and the north and south county lines.

“The speed of the collapse was remarkable.”

That is what happens when many/most/nearly all recent home “owners” are really speculators playing a high-transaction-cost game of “guess the Fed policy”.

They know their home valuations/gains are wholly contingent upon phony low interest rates (creating ersatz affordability)…but the second the Fed allows something like honest rates (ie, not poisoned by money printing) the pool of possible buyers at nose bleed prices evaporates.

So all these speculators head for the door at the same time, generating a panicked collapse in prices.

Exactly correct in FL that time Pet,, may have been even faster in certain locations along the west coast where I listened to a clerk, while waiting to pay for gas, tell everyone how he had bought a condo the day before and sold it that morning for $$$ profit…

That development crashed so hard and fast that at least half the buildings stopped at lower floors when the folks dropped their down payments and bought something else for far less.

Saw one ad for a 3n2 ranch on a canal with sailboat water to the gulf (and no bridges) for $800K+,,, then it went to auction a few months later at $225K.

Very similar booms and busts around the cape in the early days of the space programs. Sometimes when a contract ended, you could buy houses the next week for 20 cents on the dollar or even less if not in good shape, then sell them for full price when the next contract was approved by congress…

Depth Charge,

If house prices do indeed drop – then it’s going to be interesting to see how “sticky” assessed property values are.

Cities and towns have gotten by on generous state aid packages (made possible by Federal pandemic relief). If/when that dries up – they will be extremely-reliant on property taxes for their fiscal needs because lots of small businesses did not make it through the pandemic.

If receipts from property taxes don’t keep up then it’s reasonable to expect a muni bond crash on top of everything else!

Poorlikeyou-

Your comment wishing for a crash reminded of the well-work old saying: “a recession is when your neighbor loses their job; a depression is when you lose yours.”

Not quibbling with your sentiment towards wanting lower prices, but I sincerely hope that your job is secure….

Correction: meant to say “well-worn”

Reality is when it happens to you

Jeez…

Another one who missed the “I want it now” train and doesn’t want to have to board the “I have to wait” train…

You missed it 2.5 years ago… October 2019…

What were you doing then,.. so what changed… and now you want a house soooo bad… but only on the terms that YOU think are fair… seriously?

Get over it, pull your Superman panties up and pay attention in the future…

If this sounds harsh to you, then perhaps you’ve spent too much time on Social Media and not enough time in the real world where money and finance is not a child’s game on your phone and is played by people a whole lot smarter than you…

Toughen up, Buttercup and get smarter…

You are correct. And, you are not being harsh, nor mean, nor cruel.

You are being honest, and for many, that is not nice!!!………….(Do you write Mean Tweets, too?)

Many people do not deserve to own a single family home. They didn’t earn it, work hard enough, just don’t have the “smarts” to navigate the system, or didn’t inherit it (and blew it when they did.)

Only around 65% of American Families own a home (but I am not too sure of the details).

You want a home? Go back to being 18 and start reading everything about jobs and what they pay. Pick up Atlas Shrugged and read it. Start saving your money. Find a wife who has the correct attitude. Have one job and night school, or two jobs, but don’t forget the kids.

Children are the most important thing ever, and if you never had a child, you have never lived. Plus, loving and caring for children straightens you out and forces you to think long term…assuming you love them. If you don’t, good luck, your future is pure hell.

Ask yourself, what is more important: A nice home in a “nice” neighborhood (just what does that mean????), or watching foot-ball on Saturday, Sunday, Sunday Night, Monday Night, Thursday Night……you get what you really want.

Your life today is the sum of your past choices. Yes, I know things happen to all of us, but you can always, always, make better choices, if you assume, that everything that happens to you is your fault.

“Many people do not deserve to own a single family home. They didn’t earn it, work hard enough, just don’t have the “smarts” to navigate the system, or didn’t inherit it (and blew it when they did.)”

First of all, turn into a real capitalist. Only the bottom line matters. Whatever you do, maximum profit is the goal. Saving, well with inflation at 8% and interest rate on savings are 1% I would question that advice. Work hard, just remember it is easier to get rich earning other people’s money than your own.

With some insight and thinking long term, don’t have kids. You will recognize you have placed them in a harsh place where everyone is to their own. Like those forced to fight the gladiators at circus.

Atlas Shrugged, hahahahahahahahahaha.

Tell me what John Galt would have to say about the massive government socialist enterprises known as Fannie Mae and Ginnie Mae that allow for the economically suicidal (for banks) 30-year fixed rate mortgage to come into existence.

The Federal Government now owns something like 45% of all houses in America (through owning their mortgages).

Unless you bought your house with cold, hard, cash, (and even then, I’ll happily talk government interventions that kept your house value from cratering) please stop thinking of yourself as some John Galt hero. Just stop. It’s an embarrassing look on 18 year olds who can at least be forgiven their youthful naivete. It’s really bad on old cranks lecturing others on rugged individualism.

P.S. Tell me why Ayn Rand turned to Medicare when she qualified for it. Medicare is not mandatory; you have to elect to take it, and then pay premiums. So explain what libertarian principles allowed her to accpet it, and I’ll show you the extent to which libertarians have their head stuck up their ass.

We are owners of nothing. We are stewards of everything.

Ayn Rand viewed taxes as theft. In her mind the government robbed her of her property, and she wanted it back. It would be the same as having your car stolen, only to see it a week later down the street. The thief gets out, leaves the keys in the car, and go grabs a Starbucks coffee. Do you just stroll by and chalk up your car as a loss?

SnakeEater-

Nice try, but no cigar. Medicare was passed in 1965. Rand enrolled in the mid-70s. That means at most she paid into the system for 10 years. She had lung cancer, a very expensive disease to treat even back then. I bet you she blew through whatever medicare funds were “stolen” from her with interest within the first year of treatments, if not sooner. The rest of her life, she was a dirty freeloading parasite leeching off taxpayers just like she decried.

Secondly, there’s a *huge* difference between *believing* that taxes are theft, and having the state agree with you. If I walk past Elon Musk’s car, and think “Well, I was *forced* to pay this guy $30,000 for one of his cars. That’s theft!!” And then take his car, I’ll end up in jail.

Rand can choose to believe what she wants about the taxes she willingly paid to be a resident of this country. It’s not like she didn’t know about taxes when she emigrated from Russia. But her delusions don’t magically become true just because she thinks them.

Otherwise, libertarianism becomes meaningless. Here, I’ve become a libertarian: I hereby declare that, yes, I too believe taxation is theft. Now give me all that sweet, sweet, welfare handouts, but don’t you dare call me a parasite, because, well, I *believe* I was robbed, and therefore, I’m entitled to all this, while you don’t. Do I have that right? All I need to do to receive welfare without guilt is to act like an ungracious a-hole while receiving it?

I was hoping you were actually going to link to proof that she used Medicare? I have never seen proof of that. She did take social security, and explicitly did it for her husband. She died with plenty of money from her royalties from books she wrote. I have seen other people use this same argument, I just haven’t seen evidence she ever used Medicare.

I’m not a libertarian and I don’t agree with her either, but I just fail to see the hypocrisy for someone claiming social security benefits, after spending their entire life paying into it, no matter your philosophical arguments for or against it.

“You want a home? Go back to being 18 […]”

This has to be the arrogant “let them eat cake” sentiment of home ownership

This should be quoted at every high school commencement speech (before one accumulates college debt).

COWG-

Plenty of homeowners wish for the market to go up, so they can fund their retirement, or take out a HELOC and get those jetskis they want. They have no problem loudly complaining about anything and everything that might reduce their house prices, like upzoning their neighborhood to allow more housing to be built.

If homeowners have every right to wish for asset price inflation, then future home buyers have every right to wish for asset price deflation.

Does society owe you a retirement by sitting on your ass doing nothing while your house goes up in value through no effort on your part? Pull your superman panties up, pay attention to the future, or else you have no one but yourself to blame if you end up living on cat food because the single largest asset you purchase in your life just cratered in value.

See how two can play at that game? It’s the free market, and Mr. Poor Like You can advocate for his position at your expense just as much as you can do the reverse. As for who will win that tug of war, that’s what market power is all about, so we’ll have to see.

“ See how two can play at that game? It’s the free market, and Mr. Poor Like You can advocate for his position at your expense just as much as you can do the reverse”

C’mon, Lune…

Mr. Poor Like You was pissing and moaning about the conditions of buying a house today wasn’t to his liking… and he was MAD about it… wishing pox and disaster on everybody cause someone bought a house and he didn’t…. All because he “magically” decided he wanted a house TODAY, dammit…

If he wanted a house, there were plenty, repeat plenty, of opportunities prior to trying to get in the game today …

Whiney, wah, wah, I want a house now but no one will give me one is disingenuous to many people who have worked their ass off to be successful… do not wish harm on them… to do so is to be disrespectful and so shallow and selfish of an attitude that defies credulity…

Grow up…

Finances and money is a serious subject that deserves immense respect…

Treat it as such and you ( and Mr Poor Like You) may have a chance to be successful…

Nice commentary Lune. It’s always good to see the self-righteous slapped back to their proper positions. You overlooked one point though. It’s not a free market. It is a market manipulated for special interests. It’s a market sickly distorted to bubble proportions partially due to government actions (loan guarantees, FHA, VA, Fannie Mae, Freddie Mac, down payment assistance, low income housing requirements imposed on builders, high builder fees and restrictions, etc.) and money printing and interest rate suppression by the FED. This country foments a debt society, resulting in a bunch of debt slaves.

Concentrated wealth and power is ruinous to free markets. A rentier and debt ridden society, with such things as Govt guaranteed 30 (soon to be 40?) year loans subjects it’s lower and middle classes to servitude.

I’m not worried about arguing with COWG. He doesn’t know me, or my situation, and apparently doesn’t read very carefully. NBD.

Same boat. Amen.

Yes, but plenty of folks’ incomes will not hold up in such conditions.

My place lost 40 percent of its value in 2009. And there were few buyers in sight.

If you signed a contract to buy a new build in,say, mid 2021 when mortgages were 3%, at what point can you lock the mortgage rate? Curious if the long supply chains and build times are leaving people who thought they would have a 3% loan with a 4.7% loan.

On a $500,000 loan, which is common with today’s debt junkies for a “starter home,” the difference between those two rates is roughly $400 per month – not exactly pocket change. That just made the house $145,000 more expensive over the life of the loan. Conclusion: House prices are about to crash bigly.

Why can’t you buy the home while it is under construction, and thus lock it all in: The sale, the terms, the interest rate. I would think the Bank holding the construction loan would love to get rid of that as fast as possible and not be stuck if the market turns.

What am I missing?

Apparently buyers have to read the fine print VERY carefully, as builders are putting in clauses allowing them to bag out on contracts for reasons such as materials cost exceeding 15% (blaming inflation), to turn around and sell the house higher than the buyer who first ordered it would have paid.

Can’t explain every situation but has happened enough to blow up some Reddits.

*materials exceeding 15% of the original estimate, to clarify.

Many construction loans are paid to the builder on a “draw” or completed basis…

A builder can get into severe hardship with delays in completion because the builder has to pay interest on what has been “ drawn”…

If construction has to stop because of “availability” , the interest payments on the building loan will continue…

A builder that has multiple homes under construction, can be paying a lot of interest that may have to borrowed from other sources…

Add in the builders payroll, expenses, and other obligations, he might seriously lose his shirt without an ability to recoup his pure cost, much less profit…

I would think a bank would not want to do a 12 month rate lock for cost or logistical purposes.

I don’t think you can lock till closer to the home being built. Wow would a bank lend to you at today’s rate if they know they’ll be higher in 12-18 months when the house is finished?

There have been several people shitting bricks on social media bc they’re freaking out about rates going up for their new builds.

On a related note some homebuilders won’t even start a build until they have everything on hand for it….or so I’ve been told.

This very thing just happened to my wife’s friend. They are part way through a new build and are having a hard time finding parts and labor to finish. Their rate lock was for one year. That time passed and they now have no recourse to fix it. Their interest rate went up about one percentage point before the build was finished

The thing about houses is that buyers typically like to live in them. What percentage of this new inventory is completed and ready for occupancy? If I was looking at a year-plus before the property is ready to live in, I’d be highly motivated to focus my efforts on an existing home–and probably get a much better location as well.

People might discover that inflation will demand that they will have to separate out their “wants” from their “needs”. It will be a religious experience when they realize that Starbucks is a “want” where as a pound of burger or rice or beans are a “need”. They might even be forced to settle for that “dream” home with something like my 1150sq/ft hovel I call home. I used left over 2×4 framing pieces and 5/8 in plywood for furniture and counter tops. What the hell, I was in the dry, tickled pink about that new roof over my head that I could plainly see because I had to save more money to get dry-wall for a ceiling. A true “need” is a foreign concept for the beneficiaries of the worlds reserve currency. We all had better hope that the myopic path our esteemed leaders have embarked on to kill that benefit of the reserve currency will be halted. I doubt that will be the case as they, esteemed leaders, are insulated from their own actions. I am lucky just to be alive and have my hovel I call home.

DD,

I think with todays under 40 crowd, their dictionary replaced “wants” with “deserves”…

More generational BS…is it the under 40s stacking up the impossible debt bubble that my child’s generation will have to somehow deal with. Stealing from the future to avoid bad times in the present….

Sadly, you speak the truth. I thank God every day that my millennial self was raised by fiscally conservative parents (didn’t know what they could afford but sure as heck knew I was only getting the one pair of school shoes, regardless!) and I had the benefit of a wise living gram who came of age as the Great Depression hit. I may not know the joy of my name misspelled on a latte cup, but I do know that demo and doing most of the reno myself was better therapy than any shrink’s couch could have provided.

You are delusional. Delusional! Talk to a real person under 40.

I’m not buying a house in this insane market, but believe me I’ve been keeping my eye on the starter market. And I can promise you that the starter houses that are being listed are flaming dumpster fires. My list of “wants/deserves” is absolutely bottomless. As in it’s a race for the bottom. Lead paint? Of course. 120 years old? Ok. Visible subfloor? Water damage? Rotting porches? Neighborhood with 2 murders a year? HOA in litigaton? All par for the course.

And I’ve been approved for $425k. $425k can’t get you a safe house or condo of any size. Welcome to every metropolis in the US.

More shocking is that these trash properties are seeing hundreds at their open houses and are going for $40, $50k over asking.

Like I said, I’m not buying. But for you to say that we’re entitled and picky when we are actually taking on a lot of risk for visibly subprime property, you are wrong.

*wild applause*

Where do you live?

In metro Atlanta, it’s still possible to buy decent condos or townhomes in the $00K range. That’s what I will eventually buy, hopefully at lower prices.

One is currently “pending” in a complex on my buy list for $400K right now. It’s 3BR/2 1/2 BA and 2100SQFT. Built in 2015. It’s located in a suburb about 20 miles north of midtown where my office is located, right off the interstate.

I used to laugh and wonder why my grandfather saved so many building materials in his shed. He grew up poor out of the Great Depression. The past two years have made me understand his actions a lot better. Sometimes the only way to afford getting something done is to scratch together the materials from scraps.

I recently found myself accepting large free pallet made of 2×4’s 2×6’s and 4×4’s and disassembled it for the lumber now sitting in my shed. 2/3 of which already got used on projects and saved hundreds of dollars.

Ditto here, built my own house, saved the scrap and 5 years later all used up. I did not think it would go that fast.

I’m currently painting a rental unit with paint that has been entirely scrounged from a paint drop off. Ceiling paint, wall and trim paint, latex and oil based primer, Rustoleum, latex extender, joint compound, spray paint to touch up hardware. Hundreds of dollars worth. Total cost to me: $0.

I do it not only to save money, but also to recover perfectly serviceable items from and reduce the waste stream. Many valuable materials discarded by wasteful Americans.

Well, I should correct that and say there IS a cost. My time and energy, and a bit of gas. But as a wise mentor of mine once said, “a dollar saved is worth $2 earned.” And it’s also got to be worth something to use the planetary resources in a more efficient way.

I noticed the 20 year Treasury auction went off at 2.71% which is almost exactly 2X the dividend yield of the SP500 at 1.36%. Gold at $1960 for a small one ounce coin. Half a million for a starter home. Hard to say which is a worse deal with inflation running at 8%.

I bought a 5 month pre-refunded tax free muni bond paying 1% today, for my “safe-money” account.

Ugly as it is, considering inflation, I’m excited to finally be off of the “lower bound” for my safe-money pool !!

The interest rate market is finally grinding higher, and like WR, I hope to back up the truck AND extend the maturity at some higher interest rate level.

You’ll have to be careful with longer maturities if the bond bull market dating from 1981 is over, as any surprises will be with higher rates.

With the biggest debt mania ever and far worse fundamentals than in 1981, interest rates are destined to blow past the prior highs by the time this bear market is over.

The legs on the stool have broken.

For 30 years, the economy was artificially supported with interest rate reductions. Every time the economy faltered, they just decreased the interest rate. Once they hit the zero bound, they needed some other stimulus to keep things afloat, and they got lucky with COVID and all the money printing, stimulus checks, PPP boondoggle, and the rest of it. Now that COVID has receded, and there is no more excuse to print money and increase deficit spending, what can they do to stimulate the economy?

Answer: Nothing.

In my opinion, a major asset price crash is coming within a year, or a hyperinflation scenario followed by a crash within two years.

I’ll take door #1 but it’s one or the other.

The data in this pst by Wolf would probably hold true too for that less esteemed sector of housing, mobile homes.

The only reason I mention this is that my sister and her husband wanted to buid new on a five-acre parcel, but because if the crush of orders locally, they were told that it would be a two-year wait. So they decided to buy a mobile home instead. That proved to be an even bigger problem, as these are built in a neighboring state and covid, combined with supply constraints, have added another year’s wait — on top of the year already lost.

They are currently living in the third tier of owner-occupied housing: an RV.

A few notes……I wonder if the historic Noreaster that hit the east coast in early February affected these numbers….just a slight change in a light month like February could make a difference……there was also very cold weather in the upper midwest. The 6 month level of inventory looks reasonably healthy……..rate of sale looks like its in a healthy trend, the numbers bounce up and down quite a bit………house permits and starts look like they are increasing…….on my block 10 homes that have been sold for 10 months are still waiting some construction……which will provide support for labor if a downtrend starts. The 2006 era will not be seen again for a long time, it was the peak of the baby boom buying their largest homes.

As far as a turndown in housing……maybe…..maybe not…..its going to happen but when everybody has 3-4 job offers at rich salaries…..still lots of demand…..lots of millennials (largest generation) coming into the market…….rates are important but they are still historically low. Prices are probably starting to soften things a bit and that is probably why the homebuilders have slowed their price demands.

Of course Jay P read this article and is calling an emergency meeting to restart QE…….lol.

As always Wolfe is right on top of the market. Best site on the internet.

The numbers are all seasonally adjusted, so the weather issues that are in the normal range for this time of the year are taken into account.

I wonder if this will cascade into Canadian real estate.

Fed up of foreign shell companies paying C$1.5 for a bungalow 50 miles away from the Toronto city boundaries. We don’t have fast transit like Tokyo. Takes one hour to travel from one end of Toronto the other end.

Buffalo Jerry: Say kids, what time is it?

Kids: It’s Asset Stripping Time!

It’s Asset Stripping Time.

It’s Asset Stripping Time.

Jerry Powell and Howdy too

Say Howdy Do to you.

Let’s give a rousing cheer,

Cause Howdy Doody’s here,

It’s time to start the show,

So kids let’s go!

Here I go with my stupid comment……not in SoCal apparently…still a gem of an email from RedFin this morning…still selling like hotcake or some crazy manipulation going on?

SOLD

$1,075,000 $849,999

3 Beds · 2 Baths · 1,545 Sq. Ft.

650 Highlander Ave, Placentia, CA 92870

Money laundering.

Nope. That’s just what houses go for in SoCal.

listen for keys in the mailbox

Here’s a good one for laugh…once again apparently SoCal didn’t get the memo or immune to price decline or inventory going up, cause this kind of BS is still being listed on Zillow…good times

$799,9954 bd2 ba1,743 sqft

14608 Adelfa Dr, La Mirada, CA 90638

Overview

This is a gorgeous La Mirada home at an excellent price for a cash buyer. Property has been tenant occupied for approximately 2 years, however, tenants have become uncooperative since October 2021 and, for this reason, the interior of the property is unavailable to view and only cash buyers will be considered. Price reduction is reflected for this tenant scenario.

Tenant uncooperative? Owner selling? Good luck getting them out if you’re the “winning” bidder!

Wonder if the “uncooperative tenants” poured Sakrete hydraulic cement down the toilets?

Haha, I just looked at a real beauty.. A former rental with no maintenance whatsoever done on it for 13 years. They let blackberries grow all over the leach lines for years. The septic failed and plumbing backed up but the landlord refused to admit it was septic failure. So the tenants just disconnected the tub and all sinks and let the water flow all over the floors for a while. The bathroom floor is like paper- can’t walk on it.

Then, before they left they punched holes all over the walls, tore up some subfloor, broke all windows and tore the doors off the kitchen cabinets. Now, they just keep breaking into it now and again..

Was built in the early 90’s but needs quite a few new floor joists now. Oh and it needs a new roof. And siding. And septic. any everything really except 80% of the framing and electrical. Price has been lowered but not enough. It’s going to go into foreclosure I think. Sellers are delusional.

For the lack of a nail the horse was lost. Sometimes it pays to keep those blackberries at bay.

“ for this reason, the interior of the property is unavailable to view and only cash buyers will be considered”

Meh, realtor speak for they lost the keys to the security bars…

This is a desperate SELLER that needs to unload this torn-up rental property, no questions asked, to a cash buyer because it cannot be financed, and seller is willing to CUT the price. Probably has trouble evicting the tenant too. Nightmare.

Wait, $800k for 1700sqft place is a price cut???

The truth is, they could not pay me to take this property off their hands. And I mean that quite literally: the value of this house is negative. Because, once you buy the house, you will have to spend several hundred thousand to fix it up, and more importantly, spend at least tens of thousands of dollars and several years evicting the tenants, while opening yourself up to counterlitigation that you’re not maintaining the place and violating renter protection laws.

Even if they gave away the house for free, it’s not worth risking those lawsuits and court time.

IOW, those sellers may be desperate, but they’re also still quite delusional :-)

Lune,

Seller is hoping to find one of the gazillion morons out there that will buy anything sight unseen for any price, which is quite common in this crazy market. I totally get where this seller is coming from. I wouldn’t have any mercy either with these morons that buy houses sight-unseen and waving inspections and conditions. It’s their own fault. They’re asking for it.

“IOW, those sellers may be desperate, but they’re also still quite delusional :-)”

Complete agree with all you said…sadly quite delusional seems to be running extremely rampant in SoCal or California in general but at least in central cal, you’re starting to see more cracks forming. In SoCal, this type of delusional wishful thinking is still dime a dozen and I honestly don’t know where are all these morons coming from buying these place or still overbidding on houses like RedFin or Zillow is showing.

Half of me is laughing at this insanity and waiting for the shoe to drop extra hard but the other half is opening up to the idea that that maybe this is the new normal and it will never revert back, especially SoCal is known to be #1 in FOMO and NIMBYISM so maybe the cult magic will turn a bubble into a glass dome..

Being back in the U.S. for a few weeks coincided with my property manager suggesting a rent raise for my Oregon coast house (about 8%, tenants had lived there 4 or 5 years). Nice location, but the general area has a lot of low-info poorly educated locals, and meth-lab looking houses here and there in the hills.

Tenants stupidly got angry and gave notice, but forgot they had not paid last (only first and security) and got in a jam scraping up enough for a move.

Evidently they then consulted a lawyer, and forthwith claimed the house had been “uninhabitable” for the last year because a door of a small old dilapidated metal shed (outbuilding) had fallen off. And the wife had supposedly informed the property manager (NOT). So I supposedly owed them $15,000 return of rent they had paid.

Obviously they can’t afford to pay a lawyer, and are now aware they would almost surely lose the money if they did. So “negotiations” are going on. Best case is they do a thorough cleanup in exchange for about a half of last month rent. I’m really glad I’m not directly involved.

I’m going to raise the rent about 15%, and it will be easy to find tenants. Also remove the old shed, and another very old wood outbuilding.

It’s not comfortable to be a mom & pop landlord in these times. But maybe better than most of the various asset casinos.

drifterprof,

The cap for the state of Oregon for 2022 is 9.9%.

Prophet –

Thanks for the info. Looks like I’ll be doing the max on and off in the next few years instead of trying to do my part in keeping housing costs reasonable.

“Wait, $800k for 1700sqft place is a price cut???”

In Southern California? Absolutely, yes.

I don’t think some of you understand how bad it is here. The LA metro area regularly shows up at or near the top of WR’s “most splendid housing bubbles” updates.

Wolf said: “Seller is hoping to find one of the gazillion morons out there that will buy anything sight unseen for any price, which is quite common in this crazy market.”

———————————————-

This is a side effect of a sick society, contributed to by Government and FED actions …………….. doing everything they can to create a rentier/debtor society.

Private Equity loves it.

Rental since 2020…I wonder if this landlord is a product of the tik tok/youtube passive income gravy train 🤣

I hope so. Those people will really need to be ruined financially, en masse, before sanity can be restored to the markets.

We signed up to have a house built in a nice little city on the outskirts of the bay area for about 700k. 2000+ ft, 3 bdrm, 2 ba. They are framing it now. The model we purchased has already risen in asking price 7% in the 4 months since we went under contract. There are no houses available and a big waiting list for the few that they release. We qualified at 3%. I can make the payment at 5%, but it will sting. Still the prices march upward, and the resale houses now coming on the market are junk and not really any cheaper. Rentals do not exist. I need a place to live, so here goes…

Wolf,

Thanks for information. I am looking for Los Angeles area information. Can you check the area. Some areas are going for crazi prices and once you check back later in Zillow on historical data you see that those recently solds homes are gone for over15 – 20% of asking price. It is mind boggling for me.

Me and my wife got wage increase but are still runing after way behind the train 🚂

Any idea if its the time to lay back and watch or, put ourself to catch up?

Thanks

I checked Bellevue, WA out of curiosity and noticed the same. Looks a blow-off top?

There are A Lot more houses coming on the market here in Bellevue/Redmond but don’t forget:

Tech companies plan 50k more jobs here and they have to live somewhere.

The number one place in the country tech graduates want live after college is Seattle/Bellevue.

I just can’t see a big drop in a median priced house with that kind of demand.

But bigger, more expensive homes [3 mollion+] are sitting on the market longer

We will see.

“The number one place in the country tech graduates want live after college is Seattle/Bellevue.”

Link, please, because it must be the 9 months of drizzle, low cloud cover and very little sun.

All valid explanations, but still it’s hard to believe that these factors only started to influence now. Fall 2021 the people I know had to sell the house in Clyde Hill due to their divorce, and they sold it for 3.2M – and the house was bought around 2015 for ~ 700K.

Depth Charge:

“9 months of drizzle” – Link, please :)

I can admit at most 4-5.

maybe newbies EL,,, but #1 place people moving TO in USA is Miami, followed by Phoenix and then the tpa bay area

WE have to be in the saintly part of tpa bay area to take care of mil now 92, but asap, WE will be outta here for the ‘wide open spaces’ of flyover once again, in spite of our age

Agree. I’ll also note the mix of sales is changing rapidly on the East Side of Seattle. Condo sales are skyrocketing, while single family home sales are dropping. That tells me young people are moving in for now, but what happens when they start raising families?

Will they stay in condos?

The tech companies in Seattle aren’t offering workers a permanent living situation. Perhaps that is why Amazon has such high employee turnover. When it’s time to raise a family, you need to leave Seattle, unless you want to buy a $2-3M home. Paying that much for a house isn’t going to sit well with most people, now that the financial boom appears to be topping.

Google “tech grads want to live in Seattle” and you will find quite a few articles.

BTW quite a few houses for sale in 98053 just popped, more than I have seen in 4 years looking. So perhaps the increase in inventory will drive prices down

Educated but Poor Millennial,

I’ll just say this: When people, driven by the hype and hoopla of the industry and its many organs, continue to chase house prices higher, then they’ll drive house prices higher. When they stop chasing house prices higher, then house prices stop going higher. And when enough people stop the chase, house prices go down. Simple as that. You choose.

BTW, these are new houses here. You’re not going to find them on Zillow. You need to look for the sales offices or websites of the builders.

Wolf,

I understand your point that basically no one has a crystal ball, and you don’t want to be liable to provide wrong advice. But as we know the supply and demand concept, just can’t navigate the waters to see that where we are? We are in a point of not buying a house all together since a chicken hut is like $800k and next day is $900k, need a little more information based insights , please? Maybe an article about Cali major cities, just like you where doing before? Thank you.

Look, I’m not buying anything for long-term purposes right now that I don’t have to buy — no stocks, no bonds, certainly no cars, no houses… Everything is ridiculously overpriced, though some items have come down a little.

The dust will eventually settle.

I no longer do FOMO and TINA. Been there, done that. In terms of YOLO, sure, but there are more fun things to do than chase after overpriced assets.

But that’s just me.

I understood your point, thank you

What Jerome Powell and Co., along with corrupt politicians, have done to housing prices is unforgivable. I mean it – absolutely unforgivable. I just got back from running some errands and the Walmart parking lot now resembles a new residential area of people living in their cars. It is beyond sad, it is sickeningly repulsive.

This fraudulent regime running this country – BOTH PARTIES – have turned their back on Americans and are putting the finishing touches on the coffin of the USA. Billions of dollars instantly shoot over to the Ukraine while they quietly ignore what’s happening on our own streets. When I look around, I am horrified.

While not on topic. I would agree that leadership in the financial affairs of the country have lapsed yet again. Money going out the wazoo. I suspect that several billion more will be allocated to NATO, Ukraine and dark dark budgets

Congress approved the massive FY 2022 $1.5 trillion omnibus spending package that also includes $13.6 billion in military and humanitarian aid for Ukraine on Thursday, March 11, 2022. The legislation moved at the congressional version of warp speed, passing the House late Wednesday, less than a day after it was introduced, and clearing the Senate 24 hours later. The 2,741-page bill was signed by President Biden on March 15

In jest I predicted “inflation compensation checks” to be issued….

and now the idea is being floated….and the Gov of CA is issuing gas debit cards….

IT cant get any stupider….and it can all be traced back to the reckless conduct of the Fed….who all seem to vote together (Bullard excepted)…where are the contrary opinions, the “different takes” on the matters? Where is sanity?

Have you read the Pittsburg Post-Gazette investigative reporting series on Kolomoisky laundering close to a billion dollars of Ukraine bank-fraud into 13 steel mills and commercial Cleveland RE in the US? Unbelievable stuff. They published in April 2021. Tax-breaks, no maintenance, worker injuries, OSHA and EPA intransigence, political wheel-greasing; and get this; the mills were essentially corporate shells to launder more money! They did “bust-outs”/bankruptcies on some. He’s no longer welcome in the US finally.

I’ll not buy one because of the lack of quality. Also the predator criminal banks.

Perhaps after the rude awakening l might have a change of pocket book?

?

I’ll wait kids!

The Fed is certainly more to blame for the home price surge than the people doing the buying. If prime rate were above CPI, this nonsense would stop, cold turkey.

Is there on graphs on homes completed? That might be a more telling sign of things to come

See the two charts I posted in the comments above: inventory by stage of construction (not started, under construction, completed) and sales by stage of construction (not started, under construction, completed).

We keep looking at history to gage the future. The old saying something like “Know your history to learn from past mistakes, so you are not doomed to repeat them”. We say this has the makings of a bubble. But does it? I assumed with 2020 CARES package that the inevitable recession would hit in 2021. It didn’t. Could the Fed have learned from past blunders and now has fed so much cash into the system – it simply can no longer correct. Wolf, you wrote the same sentiment that the Fed was creative and threw your timeline off. Perhaps they have more tricks up their sleeves? We are talking to younger generations that just don’t care and never had to wait on many things in their entire lives. This is their market now. Gen Z and Alpha are much worse. They are not taught the power of budgets, investing, the slow build of wealth, or patience that goes with it. The system encourages all of this with insane monetary lending practices. It may correct, but I can’t see it crashing at all. With all of that said, it is interesting that the first rumbles of the GFC took place in 3/2007. It did not make crazy noise till 9/2008. Then it did not effect Central Ohio housing until 9/2009. So, it we are now seeing 2007 behavior we have another 1.5 years if history repeats itself. With American Taxpayers holding the MBS, I doubt very much a crash will ever happen again. Thank you Frank Dodd for your wonderful housing policy.

The Fed is being pressured by more external factors this time. The war in Europe came at a bad time and relations with China seems to be deteriorating. They are being squeezed between an uncertain recovery and inflation. They surely have more tricks up their sleeve, but so does fate. Interesting times.

The Fed made their own bed.

Things were going south before Ukraine.

The inflation #s had little Ukraine impact…brace yourself for Aprils #’s.

The Fed had rates at zero with over 7% inflation….and they pretended it would go away….

Powell said he doesnt want a Volcker type reaction….but reality is a b!tch. Volcker did not want to do what he HAD TO DO. Powell, with the 40% jump in money supply and rates at record lows could only have ended just like this….how else does one create hyper inflation?

“They surely have more tricks up their sleeve, but so does fate.”

Like what? Eventually, there is no more road to “kick the can” further.

The tricks used so far have been deficit spending and “printing” to give the illusion of false prosperity. That’s all any government actually has, regardless of how it appears.

That’s the “carrot” side of things. Now there are only “sticks”. Higher taxes, higher inflation, defaulting on the “social contracts” to one degree or another, currency controls, capital controls…you get the idea.

Add it all up and it leads to the same outcome. The majority of Americans are destined to become poorer or a lot poorer.

The days of a mass aspirational lifestyle are also numbered. Mass hopes for owning large homes, luxury brand cars, (regular) international travel, dining out all the time, and early retirement are all going up in flames once there is no cheap credit with the loosest credit standards in human history, the asset mania comes to an end, and the USD loses substantial value versus countries whose GDP consists of real production instead of services.

” It may correct, but I can’t see it crashing at all.”

Your post reads like you are looking at reality linearly when it isn’t.

This is a process, not an event. Of course, since the government spent something like $5T, the US economy has “recovered”. Going by gov’t stats, most people are supposedly no worse off but going by common sense, the country has to be. You don’t partially shut down an economy, massively increase debt, and then magically emerge on the other side unscathed or better off. That’s ridiculous.

We are in the greatest asset, credit and debt mania in the history of human civilization. No other even comes close.

This mania isn’t held up by “fundamentals” since these actually “suck” and have for years but manic psychology. That’s how you get the lowest interest rates and loosest credit standards in history even as actual credit quality is worse than ever.

When the psychology behind this belief ends, the credit and asset mania will end and collapse, no matter what the FRB or USG tries to do to prevent it. I expect a deflationary asset collapse combined with price inflation, the mostly opposite from 1981-2020. But regardless of the specifics, most Americans are destined to become poorer or a lot poorer. The country has collectively lived beyond its means for decades and there is never something for nothing.

That outlook is possible, if not likely, but you also have to be prepared for a long period of hyperinflation, which could take asset prices with it. The Fed has shown no commitment to fighting inflation, aside from words.

When the next asset price drop occurs, let’s see how much money print.

I disagree with your hypothesis. All processes have standards. Cpk and Ppk come down to stability in which the FED controls with an iron grip. To many pensions sit within these assets. There will be a correction but never a crash again. This time the giant reserves sitting in the banks will be required, much like Greenspan did in the 2000’s, to bail out the Feds darling. The question is who? Correction will happen, not collapse.

One must wonder at the quality of these new houses…

with the spikes in the prices of materials, labor, etc….during construction.

Shortcuts? 3 nails to a shingle instead of 4? 1/4 inch chipboard instead of plywood, etc…

^^This. I would not buy a house built since the year 2000, EVER, unless it was a custom home and I knew the builder personally. I have seen shocking levels of garbage.

North of Houston, Texas (The Woodlands). Last night at the local watering hole, I ran across two old friends, one an active RE broker and the other a mortgage broker.

RE guy says there is no local inventory to list or sell. The lender guy says he is swamped with refi’s and cash out refi’s and it’s taking 30 days to clear both. This is in a HCOL area of 200,000 people.

Prices on houses are still nowhere near what’s going on in CA, OR, WA.

A house down the street from me (2,900 SF) is on the market for $449,900 after a 10% price drop. It started out a bit over priced. This is a 20+ year old 55+ community on SFH’s in a great area. It’s the only house for sale here out of 437 homes in the development.

The national data says refinancings are plummeting. How many beers did that guy have?