Personal Income and Spending under Red-Hot Inflation and Omicron.

By Wolf Richter for WOLF STREET.

Not adjusted for inflation, the personal income of all Americans combined, from all sources – from wages, salaries, interest, dividends, rental income, unemployment compensation, stimulus checks, Social Security benefits, etc. but not including capital gains – was essentially flat (seasonally adjusted) in January from December, fell by 2.1% from the stimulus-inflated January 2021, and rose by 11.5% from January 2020, according to the Bureau of Economic Analysis today.

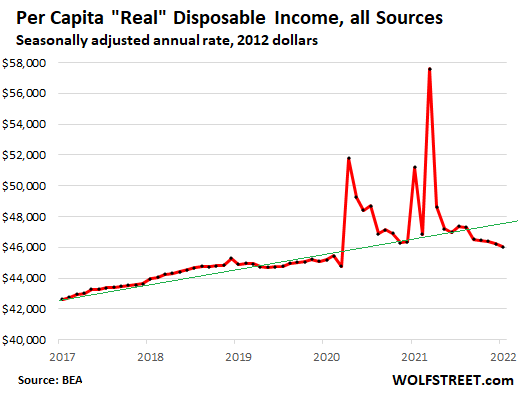

But, in “real” terms, meaning adjusted for the raging inflation, personal income from all sources fell by 0.5% in January from December, and fell by 7.7% from the stimulus-inflated January 2021 and was up only 3.7% from January 2020. But wait… this was for all consumers combined, and the population has grown.

On a per-capita basis — more people divvying up the national pie — and adjusted for inflation, minus personal taxes: The “per-capita real disposable income” fell 0.5% for the month, fell 10.1% from a year ago, and was up only 1.8% from January 2020. In other words, the red-hot inflation over the past six months ate up more than the growth in personal income and further whittled down the purchasing power of labor:

But Americans disposed of their dwindling “real” income heroically.

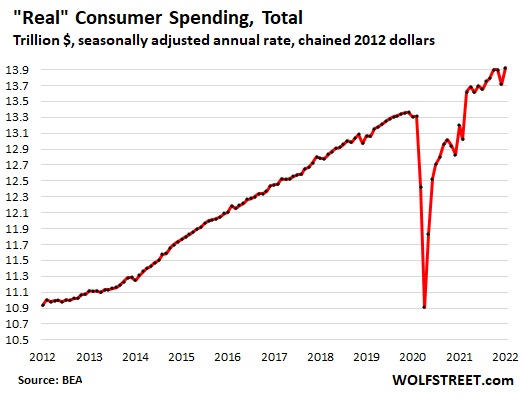

Not adjusted for inflation, consumers increased their spending by 0.8% in January from December (seasonally adjusted), and by 11.6% year-over-year, blowing money left and right in a heroic effort to keep the economy hopping.

Adjusted for inflation: “real” consumer spending in January, seasonally adjusted, bounced back from the decline in December. The decline in December and the equal bounce-back in January were likely the result of seasonal adjustments in an era when the normal seasonality was upended by the pandemic, which I discussed when it showed up in retail sales too.

Compared to January 2021, consumers increased their “real” spending by 5.4%, and compared to January 2020, by 4.6%, outspending inflation even as it ate up their income increases plus some, and despite Omicron which constrained spending on services over the past three months, as we’ll see in a moment.

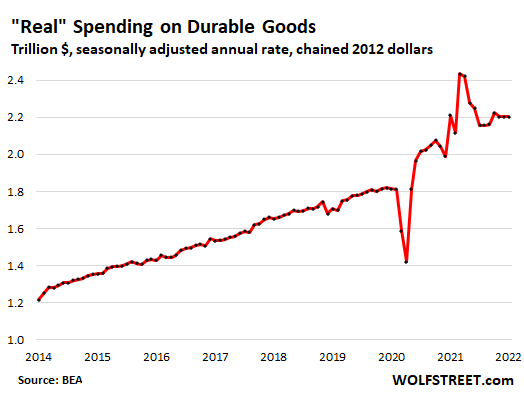

“Real” spending on durable goods – cars, cellphones, appliances, furniture, sporting goods, etc. – was flat in January and down 0.4% from January 2021, but up a whopping 21.3% from January 2020.

During the pandemic, when services such as international travels, concerts, and haircuts were hard to come by, consumers splurged on durable goods, fueled by the moneys they received from the government, and by the moneys they didn’t have to pay for mortgages in forbearance and for rents under eviction bans, and by the moneys they thought they had made in stocks, cryptos, or real estate.

So during the pandemic, there was this historic spike in spending on durable goods, even when adjusted for inflation, which was huge in durable goods (18.4% in January!), and part of the spike from the last round of stimulus checks has now unwound, but durable goods spending even adjusted for inflation remains very high – and this massive historic increase in demand is one of the factors in the shortages that have cropped up everywhere:

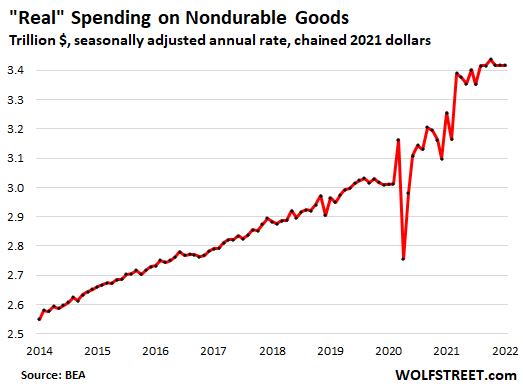

“Real” spending on nondurable goods – mostly food and beverages, all kinds of household supplies, and energy – also spiked during the pandemic, even adjusted for inflation, which was massive for nondurable goods (9.8% in January). Some of the increase during the pandemic has to do with the shift to working at home, when what used to be business spending for food, toilet paper, coffee, and other office supplies shifted to the household and became consumer spending.

In January, real spending on nondurable goods was flat with December but up 5.0% from the stimulus inflated January a year ago, and up 13.5% from two years ago:

“Real” consumer spending is adjusted for inflation on the basis of the PCE price index, which was also released today, and which runs generally lower than CPI, and which includes the “core PCE” price index, the lowest lowball inflation measure the government issues, and which therefore the Fed uses for its inflation target.

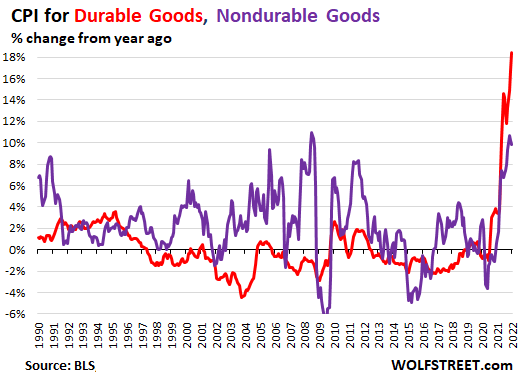

But CPI for durable goods spiked 18.4% in January, the highest on record going back to the 1950s (red line). And the CPI for nondurable goods spiked by 9.8% (purple line).

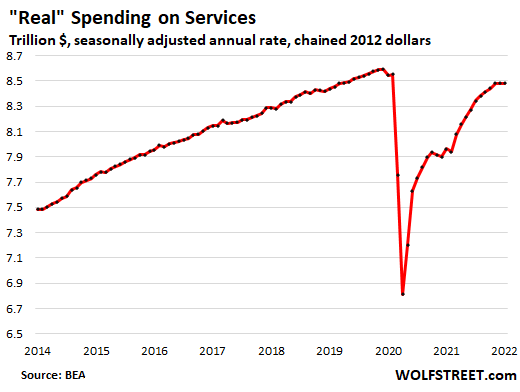

“Real” spending on services – rents, insurance, healthcare services, repairs, haircuts, lodging, air fares, rental cars, etc. – had gotten totally wiped out during the pandemic, but then mostly recovered.

In January real spending on services was flat month-over-month for the third month in a row, but at the level of mid-2019, having nearly recovered the pre-pandemic peak.

The three-month flat spot was likely caused by Omicron when some people cut back on some services, such as airline tickets and non-emergency healthcare services:

Despite Omicron, despite sour consumer sentiment, despite shortages that render some goods – such as new cars – hard to buy and often involving long waits, and despite income gains getting eaten up by inflation, consumers are still in spending mode. And households where income isn’t enough are once again charging up their credit cards, and many are using their homes as ATMs via cash-out refis. Money is still exceedingly easy, and after $11 trillion in free money from the Fed and the government, delinquencies are at record lows, and consumers are doing their jobs borrowing and consuming.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What could go wrong?

No one could see this coming…

“And households where income isn’t enough are once again charging up their credit cards, and many are using their homes as ATMs via cash-out refis. Money is still exceedingly easy…”

Come on.

There just HAS to be something that everyone else seems to have (or done) or would like to have (or do) that you NEED to HAVE or DO, too. New shit is being invented by our exceptional American entrepreneurial innovators ALL the time.

Go buy it….FIRST if you can….no fun saying, “Look, I got one too”.

There goes the neighborhood. Literally.

Keep in mind that we all expect prices in the US to go way up. Thus, if you borrow at 7% for example, but inflation over 7.5% turns that into a .5% annual gift to you from your lender, borrowing pays off, as long as you keep up the payments.

Also, finally, at long last, and only after the deaths of thousands, the EU and the US are waking up. They have two, powerful adversaries that the last US administrations, Macron, and Merkel essentially fed and supported by doing business with them and investing in them even after they initially invaded some neighbors: Crimea, Tibet, the South China Sea. Finally, they are realizing that they were feeding wild animals, which will eventually eat them and their neighbors if they keep feeding them.

Once subsidized prices from CCP-controlled, quasi-slave factories in China (where polluting the water everyone drinks is not even a consideration, much less a problem, so long as your partner is a CCP kleptocrat) are no longer available, all prices will go up. If the USA and EU are smart, what is happening now should finally make them realize that having your worst enemies be your gas/petroleum suppliers and the manufacturers of most of your goods is foolish.

It took a Russian bomb to their heads, but our leaders may finally have woken up. Thus, I have bought all that I will need for years.

Using remote work to leave NIMBY areas generates deflation at such a massive scale, it will be years at the current inflation level for me to start to feel it.

Highly recommend doing this.

Eff ’em says the Democrats.

Not our problem says the Republicans.

So so true.

The first graph is all anyone really needs to pay attention to imo. Some on here talk about how everyone is making more money than ever yet, the numbers paint the exact opposite picture. Everyone is effectively making less.

Median is more important than per capita in terms of society at large. Funny how you never see median data broken out clearly.

Funny, sad, or planned that way? You can pick any 2 but not all 3!

Median may be the best reasonable solution, not sure, but am sure that per capita misleads us quite often.

Wolf gets my respect for frequently trying to highlight economic effects on the majority of us – the middle and low income tiers.

Inflation is A RACE TO THE BOTTOM….

and the bottom is in sight.

Not SO fast hist:

NOT anywhere near the bottom IMHO, YET!!!

Going to be a ”vastly different” bottom this time,,, as it always has been since 1956,,, and probably also was before my time paying any attention at all…

Doesn’t even matter at this point what the FED does or doesn’t do,,, their efforts and, really, SCAMOLAs,,, will just add to the depths of the eventual and inevitable bottom.

So, just get ready,,, as has been the ”mantra” for some folks labeled ”preppers” or more amusingly, ”neo Luddites.”

IOWs, IF you are looking ahead now, or perhaps anytime recently, YOU can pretty well anticipate that the ”bottom” will not be clear at all, but will be the result, or at least exacerbated by the vast interference with rational markets, that will only make the eventual bottom worse and worst.

When money velocity (like water pressure) goes to zero, or negative, (like Gazproms pipe with EU) you have a liquidity problem. MV can go negative if consumers are taking money out of the economy faster than the Fed can print it, or if the Fed starts shrinking the money supply and people start hoarding cash, or buying gold, or land. MV dropped while Fed created money which sits in dead pools like MM accts. The Japanese used to “sweep up” these excesses in their economy, and everyone said WTH? The purpose of excess cash reserves and their effect, should not be dismissed. More than likely as reserves bleed off, cash gets more scarce. Net result is a greater competition for goods and bidding wars between those consumers left with assets.

Vintage…

The “race to the bottom” was in reference to inflation…and currency devaluation.

Here is one of Wolf’s charts…..and I ask….”do you see a trend here?”

https://wolfstreet.com/wp-content/uploads/2021/11/US-CPI-2021-11-10-dollar-purchasing-power-since-2000.png

Ambrose…

When the Fed pumps it usually kills MV….for money supply is the denominator in the calculation as you know.

The Fed has tripled the money supply in 14 years…

and the current Chairman Powell doesnt thing the supply of money and inflation are connected.

“• The Quantitative Theory of Money doesn’t apply according to the Chairman of the Federal Reserve……“the growth of M2 … doesn’t really have important implications for the economic outlook.” Since then, the U.S. annual inflation rate has climbed to 7.5% from 1.7%, but Mr. Powell hasn’t changed his mind…”

WSJ 2/22/2022

Wolf, I think your article here really highlighted why I think the FED will have more excuses/ammo to potentially slow QT or not go beyond .25 basis point on each interest rate hike and possible reduce the # needed this year.

With what’s going on in Ukraine and consumers are still heroically absorbing the impact of inflation, they have all the excuses they need to slow down the urgency to tame inflation. After all, why rock the market and your own personal asset value when the general public’s complaints just not red hot enough to push them into the corner.

Ukraine will be used as an excuse to not raise rates, print more money. inflation forever!

Wall Street crybabies and their promoters would certainly like that — because higher rates and QT mean lower asset prices, and they fear that more than anything. But it looks like more wishful thinking by the rate-hiker deniers and the taper-deniers and the QT-deniers.

Pure wisdom dispensed daily.

“During the pandemic, when services such as international travels, concerts, and haircuts were hard to come by, consumers splurged on durable goods, fueled by the moneys they received from the government, and by the moneys they didn’t have to pay for mortgages in forbearance and for rents under eviction bans, and by the moneys they thought they had made in stocks, cryptos, or real estate.”

Concise, true and relevant.

Friday’s “back up the truck” opportunity in SRTY and SQQQ were great! Don’t get too greedy.

Shop until you drop. We are still in the ‘shop’ part of the timeline. It’s the ‘drop’ part that’s going to hurt.

” blowing money left and right in a heroic effort to keep the economy hopping. ”

Yes we bought 3 “Dynamic Industrial Renovating Tractormajiggers”, for those uninformed… That red automated house cleaning machines from “The Cat In The Hat” book, Cartoon. I always wanted one…. Thanks to stimmy money I got 3!

.

Cobalt with weekend news round-up,

1. Gas prices are already 3.5 here in the DC swamp area. Can hit $4 soon. People with gas guzzling SUVs have to abandon them or get title loans.

2. I regularly visit a Jamaican restaurant for takeout. Although prices remain same, quality dropped. Goat, vegetables and even the whole pack weighs less…

3. If gas prices were low during ME crises, why Far-east is causing gas prices to rise?

4. Income does not matter. If prices will rise tomorrow, buy stuff today with debt. Home and bread same principle.

5. All men must enlist. There goes equality.

6. Rates will not be raised because of the situation in the east.

Gas prices in the Swamp have hit $4.19/Gallon at most Exxon stations. Heading to $5/gallon in the next month if not sooner.

I couldn’t care less.

I only put 2,200 miles on my Subaru last year. If gas goes to $7/gallon I couldn’t give a rat’s ass.

People who bought gas gusseling vehicals should have thought about this before they bought them.

My family own 3 gas guzzling vehicles. Years ago I did some rough calculations between gas guzzling, costs per mile, the additional cost per gallon, above the price for tiny, lawn mower cars.

I compared this to ALL OTHER expenses and the increase in ownership, and use, for the additional cost of getting 17 miles to the gallon, versus 28 for a sewing machine car.

The additional cost was, for my income, etc, not important. So, we own 3 gaz guzzling vehicles, and well, we like it. As long as Gazprom keeps selling us oil, going through Ukrainian pipe lines, I am fat and happy guzzling away.

I have worked my entire life, since I was 9, and I still work full time today. It is my money, my choice. I work since I LIKE gaz guzzling. I don’t waste money on sports, vacations. I “waste” it in the Suburban while others buy stupid boats, golf clubs, sport tickets, ESPN cable, alcohol, etc.

It’s the 28 miles per gallon for a smaller car, I don’t get. I know English Gallons are actually bigger but I get 60 miles to the gallon from my 2 litre car…..probably 52 from a US gallon.

Marcus,

I agree. To a large degree all consumption has the cost of energy in it. Someone can claim to be green, but if whatever you are doing costs money it’s not so green. I am sure there are a few exceptions. You can’t really have a green mansion or a green 50 foot sailboat. Even a beer and meal out can’t be green.

We can all strive to be greener. That’s very important, but a lot of green narrative is corrupt with moneyed interest looking for a new place to get a return on capital.

Anybody giving a tax credit for tossing out energy hog clothes drier and replacing with 100% efficient clothes line. Didn’t think so…no money to be made.

You think you don’t care if gas goes to 7/gal. Everything that gets transported will be paying that same 7/ga. Just because you aren’t putting it in your “Subaru” , doesn’t mean you won’t face the consequences.

I’ve had experience going out with high-earning, property owning high net worth acquaintances who live in high-income districts of Toronto, who PINCHED PENNIES quite literally.

I remember them picking out the undesirable berries and replacing it with the fresh ones in the container that was already ON SALE.

They also told me that they get discounts on clothing that were already discounted from the employees.

They OWN PRIME REAL ESTATE and EARN OVER $100,000 a year.

Meanwhile, us SERFS SPEND, SPEND, SPEND to make these 1%ers RICHER.

I think if we looked at a per unit basis not straight revenue the graph would be different.

People are spending more but is more product ending up in homes? My guess is no.

I wonder if “adjusted for inflation includes this effect?” If we buy the same amount of product but the product costs are in inflated, it appears that we are buying more. But in reality we could be buying the same amount, maybe even less, just that the total value of goods is higher due to inflation.

I know that my grocery bill has doubled but I am certainly not bringing home 2x as much groceries…. So I am not making a “heroic effort to spend,” just trying to tread water.

Frank wrote: “I wonder if ‘adjusted for inflation includes this effect?’ If we buy the same amount of product but the product costs are in inflated, it appears that we are buying more.”

Your statement seems unrelated to the graph data. The way I interpreted it, the first graph is “real” per capita disposable income which is adjusted for inflation by chained 2012 dollars. So that uses an inflation adjusted lump sum to compare the average amount per individual available to spend at each point in time.

The second graph describes “real” consumer spending using the same method (chained 2012 dollars) to eliminate inflation as a factor. Both graphs are lump sum comparative figures over time, with the inflation factor taken out, and not related to specific purchases.

The amount that specific “product costs are inflated” is irrelevant to the comparison of the lump sums, because inflation has been factored out of the sums being compared.

More interesting to me would be a further breakdown of the three categories (durable goods, nondurable goods, services) into real basic necessities vs. optional consumer items. That would take a lot of work analyzing and number-crunching. If one could do that, it would give a more complete picture of changes in per capita necessary spending (to live a somewhat reasonable life).

And also, how the proportion spent on real necessities (for roughly decent living) would change depending on region and locality as well as time. If AI starts having a hand in running the show, the data might be more readily available.

My biggest grocery luxuries are soda and muffins. Gave up brand name soda for store brand two years ago when the spread was $3 a box. Now the spread is $2 a box and I am spending what the brand name box cost two years ago anyway. The muffins have doubled in three years so I don’t buy them as often. I am spending the same amount as two years ago for lesser quality and quantity. That’s the part that doesn’t show up on any charts.

You can cut back and you are still spending more and more.

I have wondered the same thing.

I would hope all “charts and graphs” would account for this.

BUT, if the chartist is using 7% inflation, while it is 15%, then rather than an increase in spending, there would be a decrease in spending?

“Spending up” at 5%, but inflation is 7% means, spending went down 2%?

Most wealth is acquired by people who are very thrifty,don’t buy new cars ,eat off value menu,friends wife told me your rich ,told her to quit spending money ,pretty easy solution,

that used to be the case. now most “wealth” is acquired by people who were lucky enough to already own assets that the federal reserve is intent on inflating.

Fed policies also make me eat the downside of my neighbors’ mismanagement. Gee, a put, an underpriced insurance policy covering every delusional mismanager of his own personal life and spending across the whole economy. With a credit card bill on it, to send to me and my posterity. What could go wrong?

I’m so happy for those patriotic spenders. I am already in deep austerity mode for the other shoe to drop. Squeezing a dime until it screams. Well provisioned over time, so life is great.

My thinking paraphrases the Patton – George C. Scott opening speech: I will not win this war by spending and running up credit like a drunk sailor for my country (or my consumer idiocy). I will win the war by getting (or just allowing) the other sucker to do that. Meanwhile, I get my ducks methodically in a row. It’s so good to build good habits and a robust balance sheet when the necessity is not (yet) barreling down like a runaway train.

actually Jake W, all people who are wealthy are not “lucky enough” to get there: some people, many more than you realize, took the time to plan a path of financial freedom. and stick to it.

I am SO DAMN SICK of envious people whining about “the rich” as they piss away disposable income that, used wisely, would improve their lives.

and for the record, I am not financially rich myself, but have worked since age 12, navigating life the best I can, always learning from mistakes, trying not to repeat the ones that can be avoided.

btw, how do you spend YOUR day? whining & moaning about “injustice”, or doing something productive about it, the best you can!?!

aqius, i am a far right conservative. that means i value hard work and capitalism. what we have today is not that. period.

aqius,

1. Chill

2. The guy above started working at 9!

3. All those people that are envious of you are going to burn in the Lake of Fire, it’s written in stone, so don’t sweat it.

4. I started working at 8, and the rest of my siblings even younger. We got 50 cents for an A, 25 cents for a B, and zip if we got one D.

5. I think economic inequality is the worst problem (second to rendering the planet uninhabitable for humans) we have…so I’m whining and doing absolutely nothing about it…..sorry.

Mud, the “Value Menu” at our local breakfast place vanished last week and the new full value menu has seen a 20% increase across the board. For us old retirees, going out for a casual meal is becoming less frequent.

Yeah, I know, stay home and cook all your meals. But, understand that going out for breakfast every once in a while is our main entertainment these days, especially for my handicapped wife.

Anthony A.

Better keep your breakfast routine intact before someone else takes your chair.

Mud…

“Most wealth is acquired by people who are very thrifty”

Maybe 15 years ago…

SAVING IS PUNISHED….

rainy day funds or nest eggs go backwards 7%+

The formula that made us a great nation of earners/savers is gone.

Leverage and buy something…..then wait for inflation to make you rich…that is game promoted by the Fed.

Used to be you saved and scrimped to get on your financial feet, then you would gradually enter investing. That prudence is discouraged and punished…by the decisions of a cabal of unelected monetary dictators, unchecked, unmonitored.

GZ-was it Mencken who said: “…the rich ARE different from you and me, they have more money…”?

may we all find a better day.

1) QQQ stopping action was between Jan 24. The selling climax was yesterday. The response was fast. Jan 28 to Feb 24 lows : 1.65. It will be wild and volatile.

2) BCOM , Bloomberg commodity index, Buying Climax was yesterday.

The response was fast.

3) BCOM will grudgingly decline after forming a trading range. Both BCOM & QQQ will fall, but BCOM : QQQ will move up, because AAPL suck.

4) In 2008 Crude Oil futures peaked @147. From April 2020 til Feb 2022 prices were up $140 (minus 40 to 100). Crude Oil looks tired.

5) Putin dominate the East and the Middle East. He will make sure that

commodity prices will not plunge.

6) In the last decade the NG co increase production and cut prices in

order to destroy the coal and nuke industries. Raising prices will be an intolerable act to the poor and the middle class.

7) Claudia Zum indicator is up almost 50% from (-)0.37 to (-)0.20.

Avalanche of stimmies in 2020 was absolutely brutal.$11T according to Mr.Richter.

Yet Median Family Income in 2020 somehow managed to dip.

FRED:

Median Family Income in the United States (MEFAINUSA646N)

2019:86,011

2020:84,008

Skimming current MSM headlines leads me to believe that stimmies, unlike diamonds, are not forever.US Congress suddenly became quiet as a church mouse on this subject.

Let’s wait and see FRED Median Family Income data for 2021.

Unless Fed re-defines “family” I expect it to plummet even more.

Oh,and congratulations on yet another Bull Market which started yesterday around 1p.m EST

It will trickle down to the rest of us mere mortals,it always does 😀

“Avalanche of stimmies in 2020 was absolutely brutal.$11T according to Mr.Richter.”

Just to make sure we’re on the same wavelength: The $11 trillion includes $4.8 trillion in money printing by the Fed and over $5 trillion in government fiscal stimulus through borrowed money (increase of the national debt).

=same wavelength=

Mr.Richter;

I am not a broadcaster,just a humble grateful listener.

I am following Dr. Leary advice:

“Turn on,tune in to WR and DDT*”

*DDT = Drop Dead Twice from WTF charts

Your in a poker game…and the dealer says…

“Everyone break your chips in half”

and suddenly the pots get bigger…..

More accurate, the dealer takes your chips and breaks them in half.

Instead of WTF, we will start to see OMG in the near future.

Or from the old cartoon, “Help, Mister Wizard!” But what if some sunny day, Mister Wizard’s formerly deep hat of tricks and stimulating wand, even with best intentions and piles of econ degrees in the room, don’t produce any more value?

Heros from the Greek “hero” protector

Words change meaning constantly and this is a hard one to live up to

Hero maybe in the cannon fodder sense. The first in the capital structure to eat losses. A buffer offering up its flesh, so the higher capital tiers may live, hence a “protector,” even if a sucker? I think my Scotch-Irish ancestors served for that at times.

Like many and most of your comments on here ph,,, but to be very clear, it’s ”Scots” NOT ”Scotch.”

Please look it up ( and apologize to your ancestors ) IF and only if you are not clear about that, as it appears that my Scots ancestors and current cousins, etc. are NOT happy with our ancestors being confused with the wonderful whiskeys they continue to make, eh?

Scotch. Not Scot?!! That gets my tartan in a twist

No offense VVNv, but if your ancestors are Scots, they don’t make whiskey/whiskeys. It’s called whisky/whiskies.

The consumers are doing generally good if the spending dollars have not gone down a lot. It’s another thing if their dollars don’t go that far anyway.

Unless and until the spending dollars go down big time, I don’t see any red flags.

except that pending dollars have gone down. people have just loaded up on debt, from cash out refinancings, to credit cards, to “lease to own” to margin debt again stocks, and so forth.

There was an article on the increase in savings during the pandemic. If it’s accurate, the numbers are immaterial. It’s supposedly currently in the range of slightly over $1,000 to somewhat less than $10,000.

Inflation is not going to run itself out. It’s coming from the top 20%, who have stocks and RE assets at all-time highs and growing, plus huge PPP handouts and other periodic welfare for the wealthy. They’ll spend more and more as their wealth and handouts continue to grow.

The bottom half of population surely isn’t increasing it’s spending, now that fiscal stimulus has ended. They have no money.

Nothing stops this inflation train, aside from a 30% asset price crash that creates a lower wealth plateau.

The 80/20 rule…

It describes most everything. I’ve worked in sales and have experienced it first hand….

$$M1 = $20.5T. The rich are frugal, spend little, relative to their wealth, staying away from regular people. The middle class are piling up debt, buying a house, visiting HD, clicking Ikea online, eating in restaurants, paying for gas…flying, booking trails, loading c/c.

nonsense. why do you think there are year waiting lists for ferraris and porsches? why do you think rolex datejusts are now selling for 30-40% above list? that’s not the middle class causing that.

that’s the hypothetical upper middle class to rich person who has seen his stock holdings go from $5 million to $10 million in only 5 years.

this ripples through to the rest of the economy. the only way to get it under control is to crash the stock and housing markets and make people start tightening their belts. in other words, they have to induce a recession.

JW:

May just be the definition of ”middle class” that is the point here???

Years ago, when Gilbert and Sullivan were writing their wonderful light opera, it was: ”Bow, Bow you Lower Middle Classes,,, Bow, Bow you tradesmen and you Masses.”

These days, according to the graphs WR puts up frequently, it really seems that the ”middle classes” are anything and everything from us working stiffs to those making less than a couple million a year INCOME,,, eh

So, going only by income, an odious distinction to be sure, we have the rich AKA 1% on the one end, and the homeless, etc., on the other end, and everyone in between are ”middle class.”

Having worked for the ”old money” folks, and put up with their kids when I was a kid, I think the whole thing is a bunch of ”hooey.”

Jake,

I think you missed the phrase “ relative to their wealth”….

induce recession… yes. That’s why the rich piled up $20T in cash.

The rich got their nice furnished houses already. Some, when they win they might celebrate, reward themselves, show off.

Rolex is nothing for them. But many don’t spend a dime, because they hate it, they can’t. Frugality is their life style.

JW,

You should check out the number of luxury cars and watches being purchased by crypto currencies. That’s where the real purchasing power is coming from, in the luxury space. The crypto guys are trading the crypto for real goods and moving on to the next crypto scam.

Meanwhile, back at the ranch, you and I are dealing with the consequences of this mania. BTW, how do you think crypto holders are doing in the Ukraine right now?

right, but “relative to wealth” means a lot less now that wealth is so concentrated.

michael, they won’t be so quick to spend that cash if their stocks drop by 30%.

petunia, maybe from some it’s crypto, but i think a lot are just ordinary wealthy people emboldened by their paper stock gains.

How about just follow the money and tax it back where it accumulates so it can’t be spent?

What exactly is wrong with someone, who has the money, buying a Rolex or Ferrari? Really?

You can’t take it with you, right? Not the savings, nor the money, nor the Rolex, so one might as well spend it, if they’ve got it.

So many here seem to make fun of those who buy $95,000 pick-up trucks. Well, do the math. 17 million new cars sold in a year to a population of 350 Million. Of that 350 Million, how many have secure government jobs? How many did not get unemployed? How many got stimulii that didn’t need it? How many actually can afford it? How many worked for their money?

We humans have a tendency to like what we each do, think it is smart, think it is correct, and the OTHER person is the dumb one.

What if the owner of a new, loaded, F-150 likes it? Doesn’t buy the junk others buy? Want a reliable car that won’t break down? (I, being older, fear breaking down on the side of the road. I don’t keep a car for 300,000 miles like some of you brag about. That is not my priority.)

Where does your frugal used car come from? From new cars.

It is not the current new car buyer’s fault that parts come from China, and thus the Price is what the Market says. (Most of us are proud Capitalist Free Market lovers until the Market says a $45,000 F-150 is now $90,000. Free Market?). They other guy is always the dumb one, right?

I bought two of my present cars, new, in 2017, and the 3rd (new) in 2018. No regrets. None. Yeah, I’m stupid, but I know their history, their servicing, their treatment.

The most expensive watch I have ever bought was some TIMEX. Cost about $39. I only have a wedding ring. Same with my wife. She has NO jewelry. She prefers I buy Maple Leafs. She has never owned a “Coach” or LV handbag. She shops at thrift stores, garage sales, and Goodwill….See why I married her?

But, we buy new cars and dress like the Clampett’s (old reference for the old people here)

Next time I am driving in my “newer” car and I see some 300,000 mile 2004 Toyota broken down on the side of the road, I’ll wave.

marcus, what does this rant have to do with my post?

Bob-

Good points on “bottom half” buying constraints on consumption, and the separate effect of eventual asset price declines on high-net-worth consumers.

Wonder if stats are available on consumer spending that differentiate between:

~top 20% of asset holders

~bottom 80% of asset holders

….or some such division?

These groups certainly make their respective buying decisions differently, both in timing and content.

Yes, inflation as a result of rent-seeking, hadn’t quite connected it like that before. The rich buy assets upstream (like houses and oil) and charge the downstream serfs ever more for it.

When I hear the word “consumer”, I think of a creature something like the Tasmanian Devil cartoon. It ravenously devours anything within reach, with no regard to need or health or outcome.

Hahahaha, you nailed it!! That’s what economists imagine when they talk about the “consumer.”

Consumption is an old fashioned word for tuberculosis. As a nation we have decided to live in the present and completely disregard the future.

That term always irked me as well as the term “user.”

When I hear the word “user”, especially in relation to digital consumers, I think of a creature something like the junkie troll under the bridge.

When your stock trades keep up with inflation, the government taxes you for having kept pace on the treadmill.

Lots of reasons to spend now.

Maybe money’s becoming a hot potato. Buy it before the price goes up. In Weimar Germany people paid for meals in restaurants when they ordered because price could rise while they were eating.

Buy while the product is still available.

If your CC has been charging 20% interest and inflation jumps from 2% to 9% you just got a discount.

*And who / what gets to borrow at historically cheap rates with historically high inflation?

*And who / what is the largest borrower in the world?

*And who enables and empowers the Federal Reserve?

Same answer.

Same principle. Why nit pick?

20% interest on a CC is a bargain these days. Try 29% on most of them.

1) For entertainment only. IWM weekly entered a bearish territory. The monthly isn’t.

2) IWM monthly flipped in Dec 2021, two months before SPX and NDX.

3) Feb low is a lower low, a spring.

4) Mar might test Feb low, or become a spring, shortening the thrust for three months. Mar might end up in green.

5) Apr might move even higher without cancelling the countdown.

6) Mar dip might be followed by two/ three months up, in a bear market rally.

options :

7) The countdown cont.

8) The countdown will be cancelled. A new all time high.

9) A new monthly flip, a worse case scenario.

Zimanski is a smart lawyer, m+2 kids, a PM in a very successful TV show, like we got here and in other countries.

After Putin spanking and lashing he will settle, because Ukraine isn’t Afghanistan.

The Maidan sq organizer should be ashamed of himself…

Bottom line: spending more getting less.

Early stages of hyperinflation.

b

My stocks spiked yesterday. Time in the market more than timing the market.

yeah, back in the day when the economy was growing. now it’s not.

i’m really tired of people comparing stocks from 1960-2020 with what is likely coming in the next 10-20 years.

Europe, east Asia and Latin America (hey, Canada) have housed/have been our buffer states through the American Century. Long before the Fed openly became the world’s central banker and put-provider, we (Fed under Benjamin Strong, Morgan banker) were propping up the UK in the 1920s, finally in the 40s came the Marshall Plan, then propping up France in Vietnam, etc. We have been spending out the nose for a solid century to prop up our (and our brand of capitalism’s) world order, and five times now got deeper skin in the game with boots on the ground. This, through all the isolationist talk that only was a temporary fantasy and rest stop between more bouts of the same. When that stops, the world will gasp, not least of course, we will. Our internal problems have trudged on.

Interesting now is the test of financial system warfare, and cyber. Also the role of crypto as financial walls go up.

Berkshire report came out this morning. One thing that struck me was the massive earnings of Apple which has captured a lot of consumer spending. Berkshire owns biggest railroad in US and they earned record $6 billion dollars, but Berkshire owns 5.5% of Apple and that minority ownership share was roughly the same $6 billion. That’s a lot of consumer spending on high margin products.

why not? that’s what the stimulus did. it stimulated apple and amazon.

Capture consumer spending is right! I was recently forced to upgrade my iphone 5s because the major carriers are shutting off the 3g networks this year (the old iphone was still working just fine). Chose an iphone SE as an upgrade.

Well after this horrible experience I will never buy another Apple product again. I was forced to go through a convoluted, tortuous process just to transfer 8 measly GB of data from the old phone to the new phone (contacts, text messages and photos only, I don’t use apps or email on phone).

I had to synch the old phone to an old itunes account (that I hadn’t used in 10 years) on an old macbook, and then create and upload that to a new 99 cents/month icloud account (that I did NOT want), so it could be downloaded to the new phone (which was not compatible with the OS on the old macbook).

Then, since it I could not downgrade the icloud account (it simply did not work) on the phone, I had to call Apple support and wrangle with 2 different representatives for 1 1/2 hours to cancel the icloud subscription. The first rep, who was unable to cancel the account, had to transfer the call to the “IOS department”. He actually had the nerve to suggest I dispute the charge on my credit card.

Yes sure I’m going to spend another x number of hours trying to dispute a .99 monthly apple account on my credit card!

Unbelievably difficult, but I worked in IT for years, and was persistent. Otherwise I probably would have given up and paid for the stupid icloud account.

I cancelled my cell phone bill entirely. Just use wifi and voip calling now. Im not a wheeler and dealer business type needed to be connected to a phone via umbilical cord, happy saving over $400 a year on phone service. Cancelled netflix too, $120 a year, cancelled Amazon prime, another $120 a year. tired of what i call the “subscription era” of business. You will own nothing and be happy..

Perhaps one last lunge at buying perceived necessities before inflation takes them out of reach?

Are there reports that reflect both volume or units sold AND sales?. I keep thinking of the great shrinking cereal box, or candy bar.

One million tons of material “X” sold at $25 per ton in 2020 equates to $25,000,000 reported “sales”.

Yet in 2021, the exact same volume, one million tons, sold at $40 per ton equates to $40,000,000 reported “sales”.

In fact, inflation can mask reduced volumes quite easily due only to the increased price. Our little example above would allow increased sales reporting even with a significant reduction in unit or volume of sales.

Ukraine is about who gets to control the gas fields in East Ukraine. There is an pipeline the runs near there to Europe. It is in direct competition for Russian gas via NS2. Also Russia also needs bodies for their modern society. I understand they are down to 134 million bodies from 150 million last time I heard a number. That’s not enough to fill all those time zones and run a modern society. That’s why our southern border is being left open. Demographics: We all need bodies to run or societies.

Elon has it correctly. We need lots of people working very hard if we are to go to the stars. Or we become just another one planet civilization. One and done.

In the meantime I wonder where Germany will be getting its NatGas next winter. And will they be using the SWIFT system to pay for it or something else? Asking for a friend.

Andrea Merkel getting out when she did…

Why are we still buying Natural gas from Russia? I understand Russian ships are still offloading LNG at terminals in Boston.

Hydrocarbon products are a commodity and traded by brokers a lot. I spent 35 years in the oil and gas business. You would be surprised the amount of trading of ship quantities of crude oil, refined products, and LNG that goes on worldwide. I’ve seen Chinese vessels pull into a refinery here and offload gasoline.

Swamp Creature,

That region of New England is not sufficiently connected via pipeline to NG producing regions. Pipelines are in the works. I’m not updated on this, but one of them may have entered service by now. But this part of New England still doesn’t have enough NG via pipeline in the winter (peak heating). So it has oil-fired power plants on standby that kick in when needed. And it imports LNG (from wherever) when needed. In local trading, NG prices can get sky-high in the winter.

The idea the US needs more people in the lower 48 states is ridiculous.

I could get into why demographics is screwed up in this country, but it’s outside the scope of this blog.

The country doesn’t need more people to provide cheap labor for the rich or to consume more crap to generate economic “growth”. And it certainly doesn’t need it to pursue some collectivist sci-fi fantasy either.

As for Russia, they have a demographic problem but disagree the Ukraine incident has anything to do with it. I could get into that too but it’s also outside the scope of this blog.

augustus, exactly. all of our major cities are a disaster from an infrastructure perspective. in much of the west, we don’t enough water. traffic is atrocious in nearly all of our cities of any substantial size. the power grid has problems.

we were very comfortable in 1950 with 150 million people. no one has been able to explain to me why we needed to more than double our population, much less increase it even further!

JW:

1. cannon fodder

2. political power from alleged long term benefit(s)

3. servant class uprising/rising up

4. another group on which to focus negative propaganda so as to continue to divide and rule

All concepts that the oligarchy has depended on WE the PEONs for since for eva,,,

and in 1952, with the election of Ike, it just might have appeared that the oligarchs were going to have to continue to ”pay back” we peons for saving their assets from the clearly out of control fascists, rather than just get rid of them as had always been done for the previous for eva

Im sure they have explained it to you but you just never listened. Its about money. Need new ppl to pay for old ppl SS that was spent on wars. Look at Germany and most countries that import/accept immigrants.

Then why, during the 1960-1970’s, all us young people were told over and over to “go on the pill” or do other things to NOT have children, since, according to an hysterical book, we were facing a “Population Bomb”.

But, now, we open the border so we can have the grown children we were told NOT to have.

Something odd here.

Marcus-not a case of population size, it’s a case of continuing to obtainin cheap and malleable labor for those jobs that ‘Muricans’ ‘won’t do’ and ‘Muricans’ ‘won’t pay’ for.

Might have been dealt with a long time ago using verifiable and SERIOUSLY ENFORCABLE employer card check (this policy could STILL reduce the illegal immigration issue), updating the 1930’s U.S. primary/secondary education model which stressed (and in many ways, still does) general factory employee-level graduates, and appropriate tariffs on foreign goods that weren’t produced under equivalent U.S. labor/environmental regulations. Higher general costs of living? Probably. Crushingly so? Doubtful. Reduced corporate/business profits?-only in terms of not having that front-run extraction from the globalization of the national seed corn.

Global natural resources are not inexhaustable, and our tech-heavy world civilization is a vortex with an ever-increasing hunger for those resources without much apparent reinvestment in their maintenance or replacement (ref: your excellent analysis about the energy/resource footprint of your ‘gazguzzlers’ and, i salute, your thrift).

TANSTAAFL.

there may be something ‘odd’ here, but am having a lot of trouble seeing how having a lot more humans will make things any friendlier for our species going forward…

may we all find a better day.

It is hard to stop buying on a dime. For instance if you swap a pickup or SUV for a car you will be stuck buying more gas for several years… no matter what the price goes to. That is why Non-durable Goods only flatlined in 2021 on Wolf’s graph instead of plummeting the way Durable Goods purchases did.

1) BCOM, beware of March. In Mar nobody need NG.

2) BCOM reached a buying climax, because oil rigs were orders.

3) The ESG elite and their information industry might revert to nuke and coal.

4) Gold will not shine during global recession.

5) The whales will swallow the failing gold mines, which expand in the wrong time, piling debt.

6) Those which grudgingly went down, will be the winner in the next round.

7) The worst of the ME aggressors might settle their grievances, because they produce NG and oil.

Gold did just fine during the Great Depression, M.E, and we are headed for the Greater Depression as I type. It went to all-time highs in 2011 after the brief 2009 Financial Reset which really did not end until about 2013 to 2014. When citizens lose faith in their governments and domestic currencies, as we are starting to see around the globe now, hence, the misplaced popularity of Cryto-Garbage that turns out to be neither a stable safe haven, stable medium of exchange, or remotely safe from government intrusion and intervention, gold and silver do very well indeed.

Stay tuned he or she who is wed to financial assets and real estate, a perpendicular universe is about to open.

The US government fixed the price of gold, raising it from $20 to $35. It isn’t a valid comparison to any time post 1971.

Silver fell as low as 25c.

The end of the mania will produce the most chaotic financial environment anyone alive has ever seen.

It’s been bad enough trying to navigate the mania where door A is buying insanely overpriced markets versus door B where it’s Chinese water torture of negative savings rates.

Agree. In the 30s we were on a gold standard. Now, this time, for gold, it’s very different.

Okay, Augustus, then look at what happened during the most recent recession in 2009 to 2014. New high for gold, Uncle Sam not at play, in 2011 when the economic and financial system dust had yet to settle.

And the Great Depression did not end until well into World War II.

Get used to the negative savings rates: Fed has no gumption or backbone or empathy for traditional savers , so they will be dragging both feet to the Tightening Alter of Monetary Policy; I think that is called CRAWLING.

Heard a money manager say gold really was not very correlated to inflation, but performs well when real yields are negative.

I like the way you think, Mr. Young.

And there is also the possibility that Russia is kicked out of SWIFT and then replies “Russia will continue to honor all its contracts with international partners for timely delivery of oil, gas, fertilizer and other essential commodities. Payment to be accepted in Gold only.”

Bam, the central banks of China and Russia have been the two largest governmental buyers of gold over the last 20 years. I think they foresaw the loss of dominance of the U.S. Dollar in global trading with humongous Yankee debt being piled to the sky, and their necessity to develop alternative goods trading and payment systems when they inevitably fell out of favor on the world stage with a few country invasions along the way. They truly have long range planning in those fiefdoms, dictatorial as they surely are, while we do short-term planning on the back of a McDonald’s napkin.

Gold will be a buy at $1350-1500.

Against the US dollar, gold is up about 25% a year for the last twenty years. Not a bad return even it is way below some of the Markets.

Anthony-

Did you mean a different number?

25% per year compounded over 20 years would make my few holdings purchased in the 1990’s into quite a stash….

More like 9% a year

DWYoung-

The tangibility of gold (as James Grant suggests, dropping a small box of it on your foot hurts) separates it from crypto. It’s weight is significant, it’s color an luster are beautiful to the human eye, both male and female, it is infinitely divisible, and it neither corrodes nor rots.

The last two currencies recognized as sound money (i.e. un-manipulated and sustainable) were backed by gold, and their issuers, the UK and the US, were recognized as hegemonic powers of their day. For the US$, those days might end relatively soon.

At some future date, when one or several of the crypto’s lose face for whatever reason, good old gold most likely benefits based on it’s historical role and unique traits.

That said, equities offer better growth, IMO. Use metals as a currency hedge, and be wary of bonds until rates normalize.

Guessing you might agree, and eager to hear if you don’t. Thanks for your post.

You need to have a strategy in place to hold the gold. My life has been too transient, so I kept the gold in a safe deposit box. I only bought a few ounces, and did not create some elaborate scheme to hide it (e.g., moonless night, bury in mountains or dessert using GPS). Even then, someone could be tracking you and use a metal detector.

Basically I’m happy with the 31% increase in dollar value since I bought the ounces in 2015.

But because of the liquidity problem and carrying costs, I was happy to sell the ounces to one of my relatives who is a more permanent type. Nice keep such beautiful stuff in the family (PAMP Suisse gold bars).

As someone mentioned on here, coins or some other more liquid form would be the way to go if the price came down again, and if I was young enough to take a long position.

John, I strongly feel, and I am basing my investments on 4.7 decades of experience, that we are at the very end of an equities bull super-cycle that began in August, 1981. The long-term average annual gains for equities, over the last 50 years, has been 9.4% (dividends?), but there has been considerable variation annually, and that solid return cannot be extrapolated into the near future based on many facts of current economic and financial system frailties.

Fed now entering a tightening cycle, consumer confidence waning, real disposable incomes in severe decline, cost pressures mounting on corporate profit margins (only to get worse with oil supply issues), valuations well extended via most metrics, and geopolitical tensions, even Canada, not just Russia, running red hot.

One look at the chart of the S&P 500, post Pandemic collapse of 2020, shows an exponential rate of increase which has never, ever been sustainable in modern or ancient investing history. Liquidity versus fundamentally driven markets enter bear markets with regularity, esp. when the punch bowl is taken away.

Just don’t think both stocks and bonds are worth the risk at this point, and would look for substandard returns, if not actual losses, in the next several years, if not decade. Very long periods of out-performance are often followed by periods of under-performance to revert back to a more sustainable return spectrum.

While I have acquired much gold I can’t help but point out that in the USA real yields will be rising, the dollar is strengthening and soon Russia will be selling its gold to weather the storm of sanctions.

I have seen what happens when a central bank begins to sell gold, I do not think that it will be different this time. But I’ll happily be wrong here.

I see the current rise in gold as an autonomic reflex of the economic nervous system.

Compare the value of a paper dollar in 1929 to the equal amount of gold that this 1929 paper dollar could buy, with today’s equivalents.

The $1 is worth 5 cents today? And what is gold at?

Here is another way. A $20 1929 paper bill could get you one ounce of gold.

That $20 1929 paper bill is worth what (?), compared to the 1 ounce of 1929 gold today?

The Gold is about $1,800 of those paper notes, or 90 of those $20 1929. “book markers”.

Go to head of class, Marcus.

My spending is way up on things we MIGHT need. Things we know we will buy in the future, and most of it is for prepping. Yeah, we are conspiracy nut-jobs, but it is fun.

My sons and I are spending this weekend going to major stores, like Home Depot, Coscto, Bass Pro Shop, etc and walking every aisle.

We are debating anything we might need, like additional guns, more ammo, any necessary clothing (we don’t need), etc. Luckily we have most everything, but our thinking is, buy it NOW since it is cheaper NOW and before any additional shortages. We did buy another Generator and more 5 gal. gas cans.

So, with that in mind, did our spending go up? Not really. It is just that future costs will be so much higher.

I just wish I had a way to safely store about 1,000 gallons of gas.

My wife is doing the same kind of shopping with our daughter. If you will be needing and using something 2-3 years from now (?), and it can be safely stored, buy it now.

I expect at least a 20% per year increase in costs for everything, especially with the increases we will be paying for Russian and Saudi oil-gasoline. Thankfully, the present administration assured us they will be doing EVERYTHING they can to keep gas prices down. That is assuring. Everything. Good to know that.

This time it is different.

” Thankfully, the present administration assured us they will be doing EVERYTHING they can to keep gas prices down.”

I think you meant everything to keep gas prices up!

No

This time is NOT different.

I just helped a prepper move out of a long-time residence. There was a large closet full of “Patriot” branded freeze dried food in huge plastic containers that needed to be thrown away, and it likely cost $10,000 or more. Nobody wanted the stuff, not even the local food bank. That was $10,000 down the toilet.

Be careful and don’t go overboard on the prepping.

his mistake was not eating it before it went bad.

bbr:

Have read that rice found in Egypt pyramids in 19th century, apparently several thousand years old, was edible and sprouted when planted???

Modern technology is wonderful, when it works.

Suggest to all on here to make their main investment in ”open pollinated” and ”heirloom” seeds.

Seed Savers Exchange, in I owe way, is a wonderful place to start. (Disclaimer: don’t have any financial interest in that organization.)

And secondly investing in study and practice of small scale farming of locally appropriate foods, especially ”tree foods” good in your area.

The Patriot foods supposedly have a shelf life of up to 25 years. Probably still edible even after that, especially is one is starving. It also sells for good money on eBay.

The Federal Reserve Bank keeps boosting its balance sheet to new all-time highs.

https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

QE doesn’t end until “early March.” Duh.

And then it will take a couple more month to be fully reflected on the balance sheet because…

The Fed buys MBS in the To Be Announced (TBA) market, and the purchases take 2-3 months to settle, which is when the Fed books the purchases, so that what we see added to the balance sheet today was bought 2-3 months ago, at the beginning of the taper. And MBS come off the balance sheet via pass-through principal payments when mortgages are paid off or are paid down, and these pass-through principal payments speed up when rates fall, and they shrink when rates rise (fewer refis, like right now); but they’re impossible to predict. And that’s why you see the jagged line in the balance sheet.

When you look at the purchase schedule, you see the much reduced numbers in actual purchases that will be reflected on the balance sheet in about 2-3 months.

But this is in question now, they might use Ukraine as an excuse to go back on their word especially if SWIFT is disconnected Russia.

EXACTLY!

QT is NOT even started but QE will continue b/c of events in Ukraine affecting FX echanges. It may trigger a liquidity flood, tomorrow am if not tonight!

Back to square one, another Fed balance sheet-boosting crisis just like covid.

Because one guy said that the “Fed has to…”, the Fed is going to have to??? Nope.

stoneweapon,

Pozsar has recently been wrong about nearly everything, including all his BS about the Fed’s reverse repos (RRPs). That shit he prophesied never happened. But he sure gets a lot of press.

Russia’s economy is quite a bit smaller than California’s economy. If it weren’t for Russia’s energy exports, its economy wouldn’t matter on a global scale. People totally exaggerate the importance of the Russian financial system to the rest of the world.

Russia may well go into a financial crisis, as it has done many times before. Just another Russian financial crisis. SO WHAT???

LOL! That’s good, you read that stuff!

Personally I don’t take anyone’s predictions to the bank.

It’s not the size of Russia’s economy that really matters.

I’m more concerned about irrational behavior coming from the EU/NATO. I’ve been reading Alasdair Macleod’s blog and he makes a pretty good case the EU banks may be the first to go.

Considering Russia’s share of oil and gas exports to Europe and the fact that Russia’s ruling class has unanimously crossed the Rubicon and committed its military resources to take control Ukraine, this makes Russia an empire now. Without Ukraine, Russia is just a country.

The world is changing and Russia represents 20% of the worlds natural resources with a seriously advanced modern military.

Russia’s importance to China just increased 10 fold.

It’s only a matter of time before US dollar hegemony can no longer contain the price of commodities.

What’s unfolding in a very unpredictable time line is ultimately about an Eastern alliance breaking away from the US dollar.

I can only hope its rational and orderly.

I may be the most courageous of the consumption heroes today. I just bought a second overpriced home out of FOMO, while risking my retirement and kids college education, and bought a new $80k truck with 7-year financing. Now, 99% of my monthly income is going towards current consumption and loan payments. The remaining 1% is going towards Bitcoin and ARKK.

If SHTF, I deserve to be first in line for government stimulus benefits, as a reward for my courage.

sarc.

If you could use the “Way Back Machine” to go back to 1983 and tell someone (preferably an economist) that the next time inflation would be this high, interest rates would be ZERO, they would say you are crazy.

The Fed is crazy

dishonest

They could raise rates today but game the March meeting distraction

Inflation up ten 1/2 pts in 7 months (5%) and they pretend it is s delicate decision to raise one 1/2 pt

It is CRYSTAL clear the Fed serves others, rather than the citizens and their mandates

They are running the clock out. Duh

Watching an NFL game would show you it isn’t laziness, craziness or anything other than clock management. The FED has the luxury of knowing something we don’t. Only in about five years will any of us be granted permission to see or know what they did when they write a tell-all book and rewrite the history books

“. The FED has the luxury of knowing something we don’t. ”

I’m sure they do.

But we BOTH KNOW they are not doing their job, as laid out in the Federal Reserve Act…and as amended in 1977,

A tell all book? “Lords of Easy Money” is pretty close to revealing the game.

What is to be gained from knowing much later?

The Fed has been hijacked. The Fed has gone rogue. The Fed has conducted a cattle drive FORCING investors to take more RISK.

When they admitted they were FORCING investors to take more risk, they took control of the Risk/Return ratios….they forced higher PE ratios….they were so clever. And now here we are…7%+ inflation and they can not come off of zero?

Breach of duty….serving a different master than their mandates…..and crickets

1) In 2008/09, after 30 long years, gold was backing up around the 1980 peak of $800.

2) After three backbones, gold futures reached $1,911 in Sept 2011.

3) When the World Trade Ctr collapsed gold plunged. During the panic gold failed. The reaction zone lasted a year, until Oct 2012, thereafter gold prices decayed until the 2016 low..

4) Gold retracing 65% of the move from Oct 2008 low at $681 and made a new all time high.

5) Recession might send gold to $1,000, or to the 2008/09 congestion area at around $800, or even to May/ June 2006 backbone $550 – $700.

6) Others predict that recession will send gold to $2,300 – $2400, to $3,500 – $4,000 and beyond.

M.E. Gold entered the New Millennium at $290 and is currently at $1890 on the ask. Do the math, a 550% increase in these 23.2 years or a simple average return of 23.7%; get out your scientific calculator to calc compound rate of return, seat of pants about 22% per annum.

Now the ballyhooed S&P 500 closed on 12/31/1999 at 1469 and today, after a much deserved slapping around, that will turn into a real face punch before long, is at 4385 for a 199% increase or simple annual return of 8.6%. Whooooaaa, Nellie. Add about 1.4% for dividends to get a nice round 10% per annum in the New Millennium, and we will be kind enough to not mention the wipe-outs in 2000-2001, 2008, 2020, and now 2022, down 8% ytd before dividends.

That stinky old relic gold, that Russia and China have bought like drunken sailors for the last 20 years, is up a, drumroll please: 3.85%, almost a dozen percentage point better that the fleece-the-masses S&P!

Those who are so negative on Au and Ag sound like they could be Wall Streeters or their First Cousins who are merely talking their own Book.

Lastly, Michael, that ain’t no garden variety recession waiting behind Door Number One! A can of soup still may be the best investment for the next 10 years.

Wolf, heads-up, here is a canary in the consumer coal mine that would strongly disagree with those charts predicting heroic post-stimulus consumer spending to continue.

that is RCII just dropped this bomb on the market, causing their stock to plunge. I’m down 40% now. the news is very bad for the near-prime and sub-prime consumers. I wonder if the near/sub-prime car loan bubble problem prior to COVID is not going to pop post-stimulus, esp. for used cars.

https://seekingalpha.com/article/4490196-rent-center-inc-rcii-ceo-mitch-fadel-on-q4-2021-results-earnings-call-transcript

The more challenging aspects of the year primarily stem from operating in a dynamic macro environment that resulted from the lingering effects of the pandemic. This caused dramatic swings in customer behavior, especially around delinquencies and early payouts and renewal rates. For the first half of the year, the macro environment was a tailwind with government relief programs, pushing expenditures on consumer durables and favorable payment behavior to levels that were above historical averages.

In the latter portion of the year, the macro environment shifted to a headwind. Government pandemic relief programs that had supported higher rates of consumer spending ended in addition, supplies chain disruptions and a significant uptick in inflation diminished consumer’s ability to access and afford products.

We had anticipated some effect from the end of pandemic relief and implemented new tactics for decisioning and collections. However, we underestimated the speed and the magnitude of the changes in delinquencies and loss rates, especially for Acima.

…

In the fourth quarter, those external factors negatively impacted GMV growth, delinquencies and losses. We started adjusting underwriting and collections back in the third quarter to mitigate deteriorating delinquency rates and loss rates. However, as the external headwinds worsened through November and December, the deterioration in delinquencies and losses accelerated despite the additional tightening. Bottom line, despite tightening, we can now see, it was not fast enough to keep up with the changes in customer payment behaviour.

…

Skip stolen losses increased 140 basis points year over year to 4% due to the same factors affecting custom payment activity that Mitch and Jay discussed and longer term we expect it will average around the upper 3% range.

The Fed …. who doesnt have to wait for the March FOMC meeting…could raise rates at any time…

but choose not to.

I guess it is foolish to expect the Fed to stand to their post.

Not much different than watching police watch rioters burn businesses.

Duty?

“Procrastination is irresponsibility and probable deceit.”

Dietrich Bonhoeffer

Applicable to the Federal Reserve of the United States of America.

Bernanke explicitly told Scott Pelli on 60 Minutes back in 2010 that the Fed “could raise interest rates in 15 minutes, if we had to.”

It’s taking a lot longer than 15 minutes. I wonder if Bernanke regrets having said that.

I was in the markets when Volcker acted.

He was decisive and to his duties and task.

What he did put things “back in order” and our economy benefited for 20 years. Then the miscreants were set loose once again…..

Gunslinging leveragers and real estate pyramiders need not be coddled and protected.

Citizens who rely on the Fed to ACTUALLY stand to their duties, regardless of market impact , must be served, NOT HARMED as currently.

Paul Volcker was an American hero. Not many like him left anymore.