Raging mania in Phoenix, stalling prices in Boston & Washington DC, dropping condo prices in San Francisco.

By Wolf Richter for WOLF STREET.

House prices spiked further in some cities, including by a crazy 32% year-over-year in Phoenix. In other cities, price increases slowed. In the Boston metro, house prices remained flat for the second month in a row. And in the San Francisco metro, condo prices fell for the third month in a row. That’s the range, according to the S&P CoreLogic Case-Shiller Home Price Index today.

The overall National Index ticked up 0.9% for the month, whittling down the year-over-year increase to a still ridiculous 18.8%, the smallest increase since June. “Slows further,” is how S&P CoreLogic described this situation. The time frame: today’s “November” data are a three-month moving average of closed sales that were entered into public records in September, October, and November.

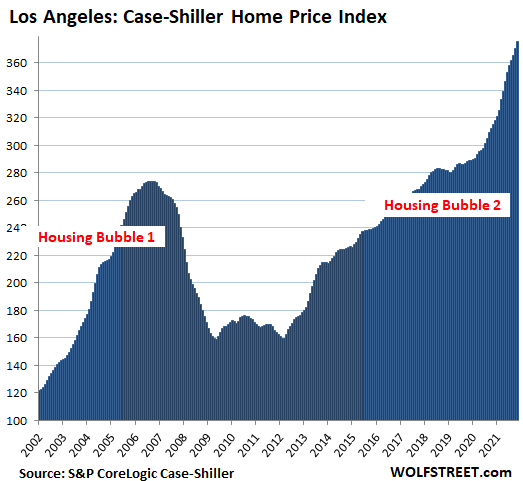

Los Angeles metro: Prices of single-family houses rose 1.2% in November from October, and by 19.0% year-over-year:

The Case-Shiller Indices were set at 100 for January 2000. The Los Angeles index value of 375 means that prices in the metro have risen by 275% since January 2000, including the Housing Bust in between. By comparison, over the same period, the Consumer Price Index (CPI) is up by 65%.

This 275% price surge since January 2000 makes Los Angeles the Number 1 most splendid housing bubble on this list. But there are other metros on this list where prices have spiked much faster on a year-over-year basis in 2021. The charts below are on the Los Angeles scale to show the relative house price inflation in each market.

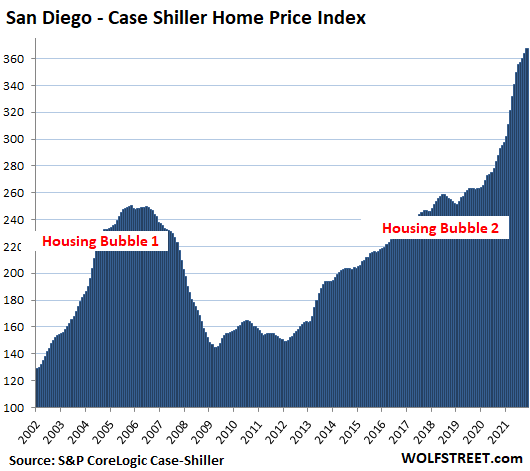

San Diego metro: The Case-Shiller Index rose 1.0% for the month, cooling somewhat from the month-to-month spikes of over 3% last spring. Year-over-year, house prices spiked by 24.4%, just a tad down from 27.8% in July. Since 2000, the index has ballooned by 268%:

The dollar is losing purchasing power with regards to houses. The Case-Shiller Index is based on the “sales pairs method,” comparing the sales price of a house when it sells in the current period to the price of the same house when it sold previously. It includes adjustments for home improvements and the passage of time since these sales pairs can be decades apart. By tracking the price of the same house, it tracks how many dollars it takes to buy the same house over time, thereby tracking the loss of the purchasing power of the dollar with regards to houses. In other words, it tracks house price inflation.

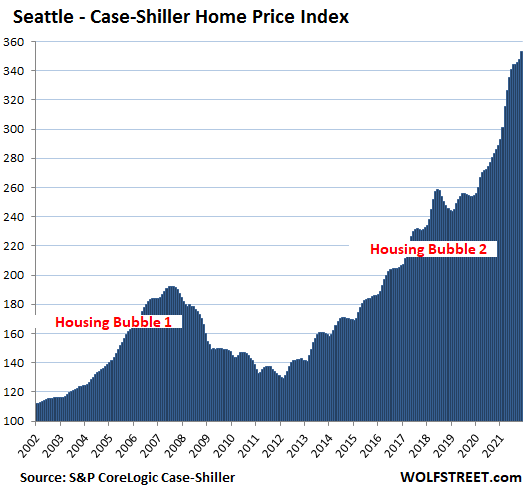

Seattle metro: House prices jumped 1.4% in November from October, and by 23.3% year-over-year, down a tad from July’s 25.5% spike. Since January 2000, the index has soared 253%:

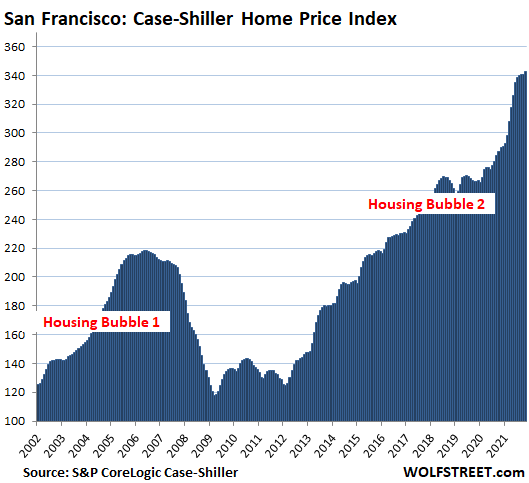

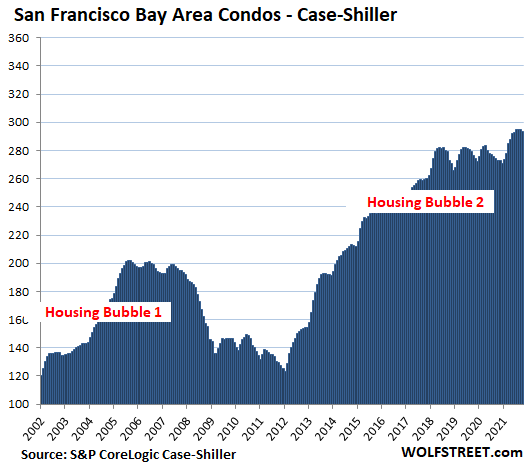

San Francisco Bay Area: House prices rose 0.6% for the month, after having stalled for three months in a row. This whittled down the year-over-year spike to 18.2%, the slowest year-over-year spike since April:

San Francisco Bay Area: Condo prices fell 0.3% for the month, the third month in a row of declines. For the past six months, prices have gone essentially nowhere. This reduced the year-over-year gain to 7.7%. Since June 2018, condo prices have risen just 4.1%:

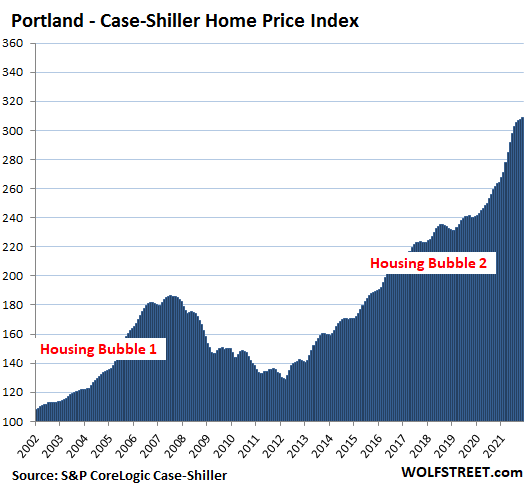

Portland metro: House prices rose by 0.5% for the month, and by 17.4% year-over-year. This is down from peak-heat in July of 19.5%:

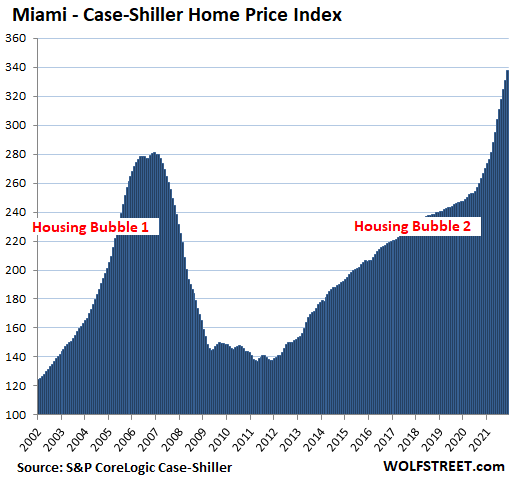

Miami metro: House prices spiked by 2.0% for the month, with no “slowing further” thingy going on here. Year-over-year, prices spiked by 26.6%, the fastest since March 2006, on the eve of the Housing Bust:

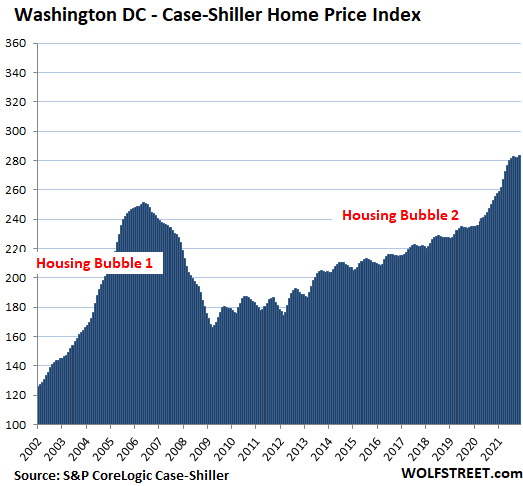

Washington D.C. metro: House prices rose 0.5% for the month, after two months of slight declines. This trimmed the year-over-year gain to 11.1%, the slowest since February, and developing a flat spot on top, the first since 2019

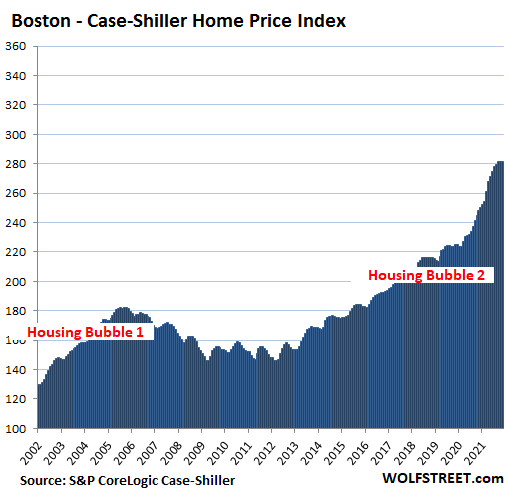

Boston metro: House prices were flat for the second month in a row, which trimmed the year-over-year gain to 13.5%, from 18.7% in July, and created the first flat spot since the second half of 2019:

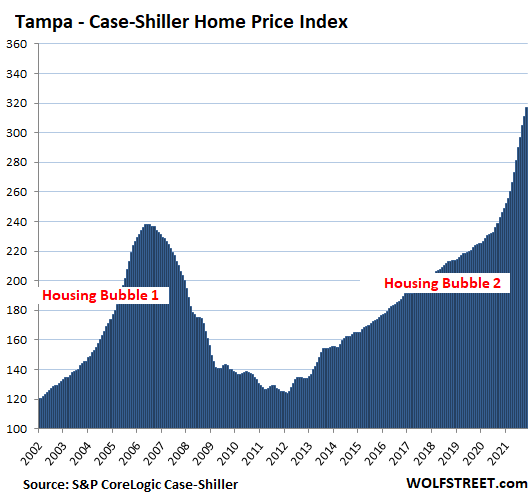

Tampa metro: +2.1% for the month, and +29.0% year-over-year, a new record year-over-year spike in this market, out-spiking the craziness during Housing Bubble 1:

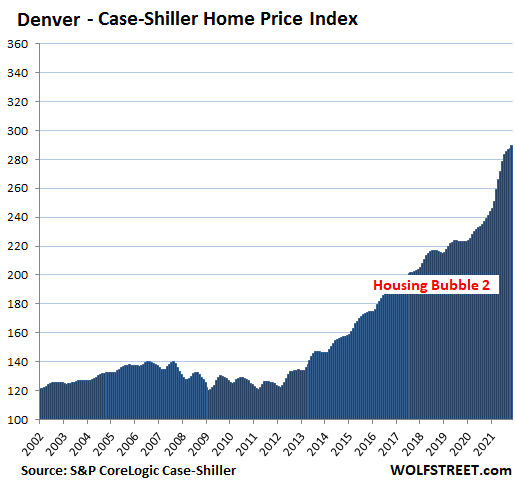

Denver metro: +0.8% for the month, which whittled down the year-over-year spike to 20.1% (from a peak of 21.5% in August):

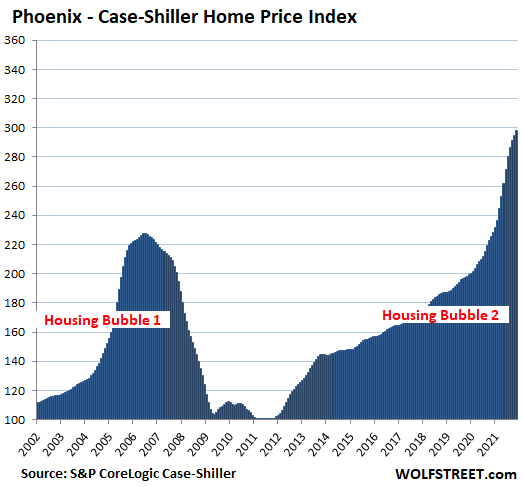

Phoenix metro: +1.2% for the month. November and October had the slowest month-to-month spikes since July 2020. Year-over-year: +32.2%, out-spiking the peak of Housing Bubble 1, and the red-hottest spike in this line-up of the most splendid housing bubbles:

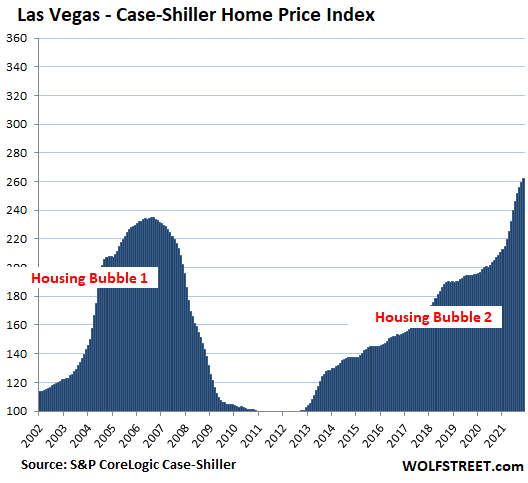

Las Vegas metro: +0.9% for the month, the slowest spike since November 2020, and down from peak-heat in June of 3.4%. Year-over-year: +25.7%.

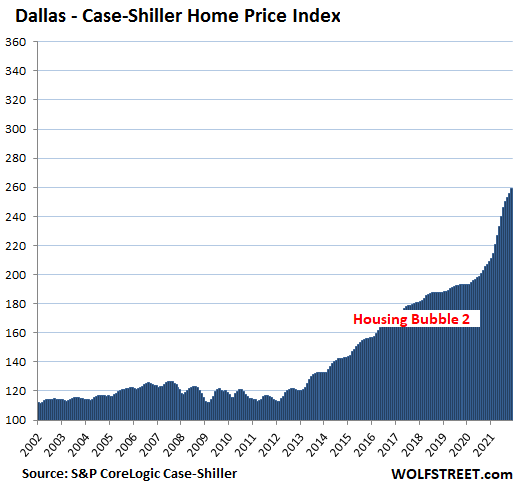

Dallas metro: +1.2% for the month, +25.0% year-over-year. .

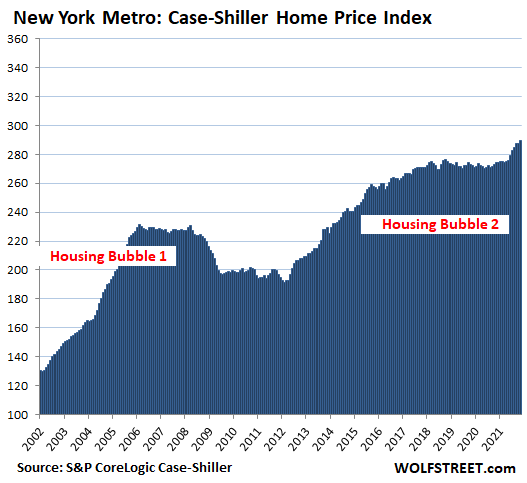

New York metro – what Case-Shiller calls the “New York Commuter” consisting of New York City plus numerous counties in the states of New York, New Jersey, and Connecticut from which people commute, or used to commute into the City.

House prices +1.0% for the month, trimming down the year-over-year gain to 13.8%, the lowest since March. The index is up 151% since 2000.

The remaining metros in the 20-metro Case-Shiller Index – Atlanta, Charlotte, Chicago, Cleveland, Detroit, and Minneapolis – have house price inflation since 2000 that has been substantially less than 150%, and so they don’t yet qualify for this list of the most splendid housing bubbles.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s really, really important to break our minds out of the realtor/media “framing” of this issue.

Low prices on good-quality houses are GOOD, not bad. They mean lower costs of living, a benefit for the majority of Americans. They mean homebuilding is more economically efficient and less wasteful. Smaller mortgages (as a share of income) means lower financial leverage, less risk for individuals, and less cost to society since fewer people will be forced to declare bankruptcy in a job loss, injury, illness or other health crisis.

The only people who think houses should be ever-more-expensive are the ones trying to sell them, and the ones hoping to trap you into debt so you can pay them interest for the rest of your life.

Wisdom Seeker,

Yes, in addition to the reasons you pointed out, high home prices are a tax on the “real economy” because people don’t have enough money left over to spend on other things.

The winners are: finance and insurance, RE brokers, and state and local taxing authorities. The losers are practically every other player in the economy.

I have tried explaining this to countless people over the years. A FLAT real estate market is ideal.

When RE continuously appreciates, you have rising prop taxes (especially outside of prop 13 CA), and a cap gain tax when you exit. That’s no fun. It’s a dead weight loss, and the longer you held it, the worse that is. After taxes, you can’t even buy back the exact same house down the street if you wanted to.

One result is that fewer people downsize, or if they do, they either give away a chunk to taxes and suck it up, or instead of moving to a smaller home nearby, they have to move somewhere else where they get more value for their sale proceeds.

Dallas was basically flat from 2002-2012.

What went wrong?

Reasonable people not bidding up home prices out the wazoo?

Denver too – flat from 2002-2012.

Why did both the Ds depart from the ideal from 2013 onwards?

What went wrong? Interest rate suppression and bailouts. Otherwise known as accountability.

Boston is EMPTY and unfortunately heading for a big reversal due to a host of issues. Wouldn’t buy a condo there for even half of some of the listing prices anytime soon.

>Boston is EMPTY…

And it’s f*cking cold there too.

It was a pleasant 68-degrees yesterday in San Diego, CA.

@Jason

Boston is empty for good reason. Why live in a cramped 100+ year old maintenance nightmare with no AC for $1m+ if you don’t have to work in the city anymore?

The Boston suburbs, however, are on absolute fire… for now.

I lived in Dallas when the market turned 2007-2013. A couple of things- the press and real estate complex started a narrative about all the companies were moving to the area (Raytheon, Toyota, etc.) and housing was tight. This was even before Toyota arrived and Raytheon was simply relocating employees within the metroplex to a new building.

Predictably folks bought into the narrative as prices started rising as the story spread.

Sanest thread I’ve ever read in a financial news site.

Thank You All.

D&C, the middle of 2012 was when global real estate investment started up, by 2013 it was going full swing. Big money started buying up good chunks in any areas that had any jobs, colleges or vacation destinations.

Jason “Boston is EMPTY ”

Took a quick look at articles on inventory levels and inventory even on condos in Boston seems to be down.

Another Ghost city developing in the US? Uninhabited investment units? Units appear to be selling fast.

Also, real estate costs are embedded into every stage of production, from warehouse costs to the wages paid to the workers.

@ Wolf –

You forgot real estate speculators and investors, many of them institutions. Of course they benefit from continually rising prices. The FED, with their interest rate suppression, which lowers interest carrying costs and pushes up prices, has greatly benefitted real estate speculators and investors ,,,,,,,,,,,, I would say at the expense of the common American, especially the working Americans.

Amen. Sadly, too many government programs to create low income houses have been “gamed” to provide many developers with tax benefits mainly. Perhaps, much higher property tax rates on homes with very high property values in a state could be used to build mini-homes like those tried out in LA for the homeless (but better ones, still mass manufactured but in many parts with better designs, which do not bring down property values in a neighborhood) may help many of our younger generations, who are living miserable lives working for miserable wages or paying off huge debts.

We must help them to amass capital, since many will not inherit much from their indebted parents or the economic consequences will not be good. Even commie economists recognized that the strength of a nation and of its economy is in the number of its skilled workers. Thus, if younger generations are largely abandoned, the US will ultimately pay for that mistake.

I could’t agree more about house price rises being a form of tax. I’m English and more or less the same things have been happening here. If interest rates a zero or close to it then all it does is encourage people to think that they can pay anything for a house as they think that they are paying very little for it each month. The lie, of course, is that they are not paying very little but an ever increasing amount as prices zoom. When you add to that increasing inflation in all the other things they have to buy in life, you can begin to sense that things may get very bad for very many people.

Just to let you know, my house in Northern England, has gone up roughly seven times since 1999, most of it in the last eight years or so. Down south, London way, it is actually worse.

The flat below mine (exactly the same size) in central Stockholm, Sweden was just sold for 12 times what I paid in 1993.

Having been a Real Estate Broker for the last 30+ years in one of the most expensive areas in the country, I have to tell you that Realtors have little to no responsibility for the escalating prices. If I had my way, I would be like to see about a 25% crash in this totally absurd market. The impact on our county has been horrific. Sometimes I even think my buyers are nuts. My question is, where are the people you actually need (teachers, nurses, etc.) going to live? However, as an individual I have no control over what people are willing to pay for a home in my area. The real causes are low interest rates, buyers with too much money, and historically (by multiples) low inventory. A buyer strike would be nice, but that won’t happen. It is a bubble, but bubbles can take a long time to bust.

Pistol said: “The real causes are low interest rates, buyers with too much money”

——————————————–

Bingo! interest rate suppression and money digitization.

But, there are other causes. FHA, HUD, VA, down payment assistance,,,,,,,,,, all the subsidized bankster supporting government programs to support “home ownership.” Scumbag politicians, both republicans and democrats who support and push these programs. Allowing non citizens to purchase real estate, etc. Tax laws such as interest deduction, depreciation, etc.

As usual, the common American is getting conned by the lending class.

Also, all the rent subsidy programs push prices. It is welfare for landlords via the tenants. A lot of it took place during covid, as well as before,,,,,,,,,,,,,,,,,, and of course will continue.

cb: how does your statement about “via the tenants” work? In my experience, the tenants stopped paying. Some landlords got money from the government, some didn’t. What they weren’t getting was money from their tenants.

@ Jeff-

rent subsidies from the government flow right through the tenant to the landlord. The tenant is just the conduit used to line the landlords pocket with government money. Welfare.

Looking at some of the housing markets they are up 3X in last 10 years which is very similar to stock market 3X value.

This is what happens when you run emergency stimulus over a 10 year period after you should have normalized rates. The Fed has used up the wealth affect arrow to keep the system going. They will try something else to help us.

Nearly everytime I see these charts I go back and read the history of Mississippi bubble and try to figure out where we are at. It was really the first central banker bubble and inflation got to 23% per month.

He thought he could soft land the bubble, but the mania quickly turned to the panic. So many lessons there about increasing crime and decreasing morals as people did anything to get rich quick. Ended very badly.

Reading history is more important than a PhD in economics.

Look at what happened in Venezuela. They printed money. That did not build houses or put loaves of bread on the store shelves. Price of lumber is up, price of copper up, price of pick-up trucks up, wages going higher, health care too expensive, etc. How unfair it is the fast food restaurant workers can not afford condos. If you want housing prices to go down, you may need to build cheaper houses. Complaining is not the same as producing more new housing completions.

I strongly disagree Pistol: Realtors have one huge responsibility for this mess: the way they talk about the market is always aimed to make people buy. The language that is used, the choice of what to highlight and what to ignore… the National Association of Realtors is absolutely famous among market-watchers for being utterly shameless, essentially lying (i.e., deliberately misleading with half-truths) the populace. The NAR is a big part of why we have had 2 huge housing bubbles in a row.

Either the industry regulates itself and comes up with a professional code of conduct – similar to fiduciary responsibility, or the doctors’ and lawyers’ professional ethics code – or someone is likely to take action.

Individual realtors are often decent people but by allowing the professional association to mislead the public about the state of the market, they betray their country.

Thats one of the reasons I don’t contribute to NAR or CAR political arms. You have been listening to/working with the wrong Realtors. What do you think would happen if I put a property on the market for far less than I think it is worth? Bingo, it sells for whatever the buying public thinks they have to pay to get the house. Would that be the Realtors fault?

Anyway, I see your points, but it still has very little to nothing to do with individual Realtors. Like all professions, there are honorable people and the others. I can talk to one for 10 minutes and know the camp.

Wisdom Seeker

We’ve used Realtors 6 or 7 times since I moved to DC. in the 1970s. In every case, unfortunately, the Realtors that we hired were lazy, unethical, dishonest, incompetent, and ignorant. I’m sure there are some good ones out there and I’ve met a few, but we were not so lucky when we really needed help. We still have to work with Realtors in our appraisal business and we are members of the NAR. That organization sends a magazine every quarter. I read it from time to time. In the last issue, I could not find a single piece of accurate or useful information in the publication. Most of the Realtors that we deal with in our appraisal business are completely incompetent and lazy to boot. They don’t even serve their clients who pay them a handsome commission. We wind up having to do a lot of their work for them

There are good ones. I keep in touch with 2- each in a different county, just in case. Both of them have talked me out of buying really really overpriced major fixers. I may not have a house but I’m not in debt with a badly leaking roof and disintegrating foundation.

At some point a house is a very bad investment.

Rising housing prices without rising salaries is wage deflation. You need more hours worked in order to afford the same SQ ft

In the aggregate, it’s those who consider housing an “investment” who think it’s great.

Wisdom Seeker

Noticed the low end of the housing market is showing some unexpected strength. People still need a place to live and cannot afford the high prices of the fancy homes that builders are putting up. So now they are taking what they can afford. This may mean moving into a neighborhood that is in a marginal area, high crime, drugs, high unemployment etc. Did one the other day which was in a townhouse development that had not even been completed, in one of the worse Ward’s of the city.

When the low-end stuff takes off, you know the bubble is in climax mode. That’s what happened in 2004-2005. When people overpay for even the least valuable properties, you know the buyers are nearing the exhaustion stage.

Wisdom Seeker

To clarify,

The houses I’m describing may be nice houses, but they are in very bad neighborhoods. They are selling at fair market value, not overpriced by any means. From a cost approach point of view you are getting a lot of house for the money. However, there is so much crime in DC since they defunded the police that you are risking your own safety by buying properties in these neighborhoods.

Wisdom Seeker

I forgot to add, in addition to the crime, litter, drug trafficking, you may have some open prostitution right in front of your $500,000 newly renovated townhouse. With gentrification this problem may go away in a few years if you can wait it out. You will be handsomely rewarded if you do this.

Do rural land next.

Iowa Farm land is up 29% in the past year. More than housing in Iowa.

So Gates is smiling.

Is the idea that the Phoenix graph somewhat resembles Monument Valley, any cause for concern?

Well X C, did you notice that hopefully ‘soon-to-be-starving’ D.C’s flattening top didn’t yet showcase those White Haus blast walls .. or that Miami’s Great Pinnacle is now probably overloaded with blu Atlan-tick Accela hypocrites galore..

edit: Accela ‘corridor’..

According to Norada Real Estate (1/22/22), the median price of a home in San Francisco County is $1,690,000.

Homelessness is a problem in San Francisco.

Homelessness is a problem in Tulsa too, where I stayed downtown a couple of months ago. They’re everywhere. Once you get out of your car and walk around, you see them. Median home price = $166,000.

Wolf said: “Median home price = $166,000.”

————————————

too high

Wolf…are you looking at the following markets – Austin, TX, Boise, ID, Salt Lake City, UT? Those may be the canaries in the coal mine!

Oklahoma oil field areas might see more cash flow as oil prices rise.

Florida was cheap 10 yrs ago. I read an article 200,000 moved to SW Florida in the past ten years. It is not cheap anymore.

Florida gets cheap every time it gets hit badly with a few hurricanes. Then a lot of people leave and after a while, everyone forgets the hurricanes, and the people come back. Same thing around other parts of the Gulf Coast.

Anthony A.

With the abnormally warm gulf water temperatures, and the shift in the path of the Atlantic storms coming off the coast of Africa, I think this problem with hurricanes in Florida is not going away any time soon. Insurance companies are going to factor this into their risk premiums. I wouldn’t buy nothin in Florida, based in this factor alone. Good place to visit but I wouldn’t want to live there.

Wolf,

Maybe you could periodically take a look at the Ntl Assoc of Realtor reports that provide median sales prices for well over a hundred metros.

Case Shiller is great but it is likely biased upward, due to its focus on mega metros (30 or so).

But there are 250 to 300 significant metros in the US and a large percentage of them provide at least a decent, lower cost alternative to the megas.

Don’t get me wrong…those additional 200+ metros are mostly significantly overvalued too…but not as badly as the megas.

And, taking a broader overview provides insight into the alternative siting options that corporations may sooner or later have to avail themselves of.

Just something to think about for a future post.

Following my tirade against the NAR further upthread: The NAR’s use of median prices, without explaining how misleading they are when the sales mix changes, is another example of how the NAR deliberately misleads the public about real estate.

If there are 10 houses sold in 1 month and they’re all $100K, the median sale price is $100K. If in the next month there are 11 houses sold and 10 are $90K but a fat cat sells his McMansion for $1.1M, the “median price” is now $200K … But HOME PRICES HAVE NOT DOUBLED!

Whenever the sales mix shifts to the wealthy side of the population, the median price “increases” and the NAR hypes that through the rafters to generate more business for their members. But it’s often total horsecrap.

cas127,

I HATE median prices. They have huge flaws. They’re very volatile, as you will see in my housing article today. Sales pairs (Case Shiller) is far better. I only use median prices when there are no sales pairs available.

“Case Shiller is great but it is likely biased upward, due to its focus on mega metros (30 or so).”

Nope, not when you’re looking at it metro by metro as I do.

“But there are 250 to 300 significant metros in the US and a large percentage of them provide at least a decent, lower cost alternative to the megas.”

Sure, you could move to Tulsa. The city will pay you $10,000 if you bring your work-at-home job with you. That’s how desperate these cities are. I used to live there. Great city. But I will never ever move back, or to a similar city. People live in big expensive cities for a reason — and they’re willing to pay for it. If not, they leave and move to Waco or Tulsa or any of the other great places around the US.

WS and Wolf,

I agree with you on the fact that sales mix can distort medians (because if only the wealthier are buying homes in an overvalued environment, then the transactional median will be biased upward) and that “matched sales” are the way to adjust for it (which is Wolf’s point) but I still believe that an exclusive focus on 30 mega metros (because that is all Case Shiller encompasses) creates its own distorted picture and ignores the potential dynamics in the system (employees/corps moving from insanely overvalued mkts to merely somewhat overvalued mkts).

Yes, the NAR uses medians, which are likely somewhat inferior to matched pairs (although perhaps not as massively as suggested – *some* lower cost transactions are still happening – and quite possibly less distortion inducing than looking at only 30 metros).

One other point – we are assuming that Case Shiller’s “metros” are identical to the big, multi-county definition that the G uses.

That may be true…but I haven’t seen it for sure. And I *am* frequently surprised by the much lower prices reported in MSA satellite cities relative to the core cities from which the MSAs take their names.

So if Case Shiller *isn’t* using some 5 or 6 county MSA definition and rather looking at just the central MSA county (or city!) that would be another possible source of upward distortion.

Just something to think about.

Another point about literally broadening perspectives…the outlying areas will quite possibly show mkt price turns *first*…and that is very valuable info to have.

I have an old issue of the magazine from the NAR dated June 2007. There is an article from a top so called expert who stated.

“while real estate has been softening lately, there has never been a better time to buy a home”

So if you follow the advice of these as$holes that write these articles, you do so at you own peril.

4 pieces of real plywood and a tarp = $30 to $300 depending on previous use. I think the NAR should include those prices in their averages of real value.

Homelessness is not the problem, it’s the consequence of other problems.

Addressing homelessness alone is like aspirin on pneumonia.

Not enough.

As long as financiers print and control money, politics, taxes, immigration, outsourcing etc… there will be more and more natives left by the side of the road.

Add drugs (legal and illegal) making money for big pharma, praying on main street..

And you have a disaster, everywhere.

If I were in a homeless situation right now (I’m not, I’m on the other side) I would go and steal some rich dude’s mansion in California.

It’s the moral thing to do.

Been there, did a ”squat” with a couple others 50 years or so ago in London; it was not fun at all, always expecting the cops, etc…

Probably better to do a ”rent strike” type of thing, with a group of adults and some children gaining a ”home” and one would think a lot of empathy.

Seen that recently in a SF bay area city, and the families involved ending up owning the house; of course it needed a lot of repairs, and that was a very good reason for the rent strike initially.

Surely doable in almost all USA cities with the lenient respect for private property dominating the news, etc.

Why?

What if the “rich dude” worked for 40 years and the homeless guy never worked at all?

I worked 50 years to get my house.

Why don’t you invite the homeless person to live with you?

It would be the moral thing to do

Anybody trying to steal my house is going to get riddled with bullets.

Enlightened Libertarian said: “I worked 50 years to get my house.”

______________________________________

Are you the same Enlightened Libertarian who in another post said …………………………..

Enlightened Libertarian

Jan 23, 2022 at 10:23 am

“Watching the RE implode will give you opportunities to buy.

Look, I know you guys hate RE but I have doubled my equity in 5 years by just letting a good property management company do all the work, plus generate 450k a year in NOI. Plus all the tax advantages. And you are 100% owner, not a minor shareholder.

It is like free money, even with the eviction moratorium. I bought in a college city with an active retirement community on a bay [lots of boating]. Smaller city with people flooding in from the big cities.

Long term loans at 4%, short term renters on their up, leases backed up by parental money, new tenants every 2-3-4 years as they move up and out, no children to destroy the place.

I am just trying to point out an opportunity that worked very very well for me and my family.”

____________________________________________

as easy as you make real estate sound, I wonder why it would take you 50 years to get a house? You must have gotten a lot smarter. Perhaps the homeless could use your training.

_____________________________________________

cb

Jan 24, 2022 at 12:30 am

An opportunity? To net $450,000 per year in real estate?

You can do that with about 10 to $12,000,000 cash in Southern California. Possibly 1/2 that in other areas. Or you can leverage, but it still takes a lot of cash for down payments.

If it is so easy, of course you will duplicate your efforts and push your collected NOI to $900,000.

You sound well intentioned, but the post rings a bit ridiculous. Of course it could be my ignorance of your methods.

All they would do if they caught you would be to slap you on the wrist and let you go after 3 days anyway.

A guy sort of did that on the very rural Cal. coast here. Broke into several empty vacation homes, hung out, stole some wine and food. Took the cops months and months to catch him. The owners were apoplectic but a good part of people here were laughing and cheering him on.

Watched the Tennessee tiny home company this week put four new 10 X 20 homes built by the Amish up for sale at 8:00 Monday night for $60,000.

This includes porch, set up, utility hookup and skirting. By 8:00 next morning 12 people were trying to be first in line to buy them. When prices go parabolic it leaves people scrambling for alternatives.

Another TN cabin company will deliver (within TN) a decent 800 sf cabin for $28k (albeit w/o interior finish).

I think that is maybe $35 psf vs. $150 psf (or higher) numbers I have seen for fully finished homes.

$115 psf for crown molding seems a bit high…

I exaggerate (there is significantly more to interior finishes) but the general point is valid…a close eyeballing of cost breakdowns in construction will reveal a lot of funny business.

It is overpriced… however, the problem with small houses is you still need the same fixtures as a larger house. Sometimes you pay more for appliances and cabinets etc because they need to be smaller and custom fit. A new very basic travel trailer is probably much more cost effective and better designed. & Lighter weight for hauling as needed. You can always swap out the flooring and countertops.

People who are buying “tiny houses” rather than travel trailers are mostly buying an added (false) status. At least someone makes good money building them.

Trailers were first marketed in the 1930’s and 40’s as “tiny houses” BTW. So ironic.

“as easy as you make real estate sound, I wonder why it would take you 50 years to get a house? You must have gotten a lot smarter. Perhaps the homeless could use your training.”

Cd:

I graduated from the UW with a degree in Philosophy and economics in 1977 and bounced around for awhile. Built boats for a few years. Got a job with USPS in 1982. Got married, had a family, bought a s all house on a double lot in 1986. Starting building houses. Had a stroke in 2005 and lost everything.started over again, now handicapped and no money.

Now I have a 3 million dollar house [which took me 50 years to work up to] and a couple of apartments generating 450k a year in NOI.

Total worth 20 mill and net worth 14 mill. 6 mil in long term low interest rate loans.

My only point is that if I could do it, on one low income and rasing a family, means that anyone could do it.

RE is a great way to make money. Not as good now as 30 years ago, but still good. My first home loan was 10.5%, compared to 3.5% today.

@ Enlightened Libertarian, who said:

“My only point is that if I could do it, on one low income and raising a family, means that anyone could do it.”

—————————————————-

It does not mean that at all. Different times, different people, different opportunities, different FED actions and beneficiaries of those actions, etc. It would be an interesting conversation.

If you were broke and handicapped in 2005, then you amassed 14 million of net wealth in 16 years, ostensibly in real estate. You should write a book, telling the Whole story. It would sell.

You acquired this fortune, continued raising a family, with the overhead of a $3,000,000 house, in 16 years? Impressive.

If you are getting $450,000 NOI yearly, then you own more than a couple of apartments.

Is it repeatable? Easy enough said, but quite another thing to repeat.

Real Estate is great way to make money, if you catch the right market, at the right time, under the right circumstances, with the right resources, and are able to and do execute. It is also a way to lose money if things move against you, particularly if you are leveraged and aren’t bailed out by the FED.

Anyway, congratulations on your success.

@ Enlightened Libertarian –

I’d bet your fortune was made near Tacoma.

A closer examination of the underlying data is warranted – especially considering the SF market:

“San Francisco Bay Area: Condo prices fell 0.3% for the month, the third month in a row of declines. For the past six months, prices have gone essentially nowhere. This reduced the year-over-year gain to 7.7%. Since June 2017, condo prices have risen just 4.1%”

Having surveyed the condo market in SF for the last 2 years before finally making a purchase last year this has certainly not been my experience.

If anything, higher quality condos are fetching exorbitant amounts. For example, a 2BR/1BA condo could previously been found in 2019 for $800,000 is now $900,000.

Well meaning idiot,

Not sure where you found that one condo you cited, but here are the median prices of condos (green) v. houses (red) through August 2021:

Wolf,

I’d like to see the same chart for Washington DC

You should be able to get that data from the local MLS. A broker has access to it (if they’re paying for it). And if you know them, they might let you have that data.

Median prices will change in response to the mix of sales.

Higher-end prices can change in a different way.

I will say that when your home’s price appreciation rate is comparable to or greater than than your annual take-home pay, you know you’re in a bubble and it can’t go on much longer…

It’s really hard to ease out of a bubble when the over priced house is leveraged 30:1. Last in are underwater over night.

“will say that when your home’s price appreciation rate is comparable to or greater than than your annual take-home pay, you know you are in a bubble..”

…so only a 20 year bubble then…(with one epic implosion…implosion 1.0)

As long as the shortage of buyable homes continues, expect home prices to keep marching higher and higher.

With inflation at 7% and rising, and increasing volatity and risk in the equity and crypto markets, not to mention worldwide political instability, I wouldnt be surprised to see prices up another 15-20% in the next 2 years, interest rate hikes or not. Rising rents continue to give RE more attractive returns than most other inflated assets.

Is RE high and overvalued? Probably, but I dont see a catalyst to turn the market any time soon, including higher mortgage rates (below 6.0%).

In my my decades in the real estate business (selling, investing, building) I’ve never seen such a shortage of properties – ever.

There are two components to prices — the ability to pay, and the willingness to pay. You’ve explained why the willingness is likely to continue. But will the ability increase 15-20%?

The ability of the average Joe will decrease, but as the rich get richer, their ability to finance more properites will increase. Why shouldn’t investors buy 40% or 50% of all homes?

Has that ever happened before?

If not, why?

Dazed and Confused, it has never happened before primarily because the rich never controlled so much of the wealth pie. Until people refuse to work unless their pay matches asset price inflation, the trend toward greater wealth inequality seems unstoppable.

Would be interesting to see what would happen if the majority of voters were renters.

Would government subsidies for homeownership (hundreds of billions of dollars per year) be repealed and replaced?

It hasn’t happened before because it’s really not easily scalable. Funds/institutions have just recently figured out how to make it reasonably scalable, but it’s still not simple.

As for individual investors or small partnerships, etc., there have historically been better investments anyway. Owning rental homes has been a modest yield play, and it took a lot of capital/risk to do it. Well, with rates squished so low, and yield crushed out of everything else, housing looks more attractive (or lookED more attractive…SFH yields are awful now).

I think the willingness to pay is a lot stronger than 2008. Hard to downsize when rents and lesser houses are sky high as well. All bets off if jobless numbers rise, however. But like Wolf said, those with high mortgage payments are going to have to examine their consumption levels for cutbacks.

There’s a theoretical argument that the Great Reshuffle has yet to run its full course – NYC banksters and Bay Area techies may have been waiting to confirm they can work remotely full-time before relocating to Miami or Phoenix.

When they do move in large numbers over the next couple of years, it will significantly boost median household incomes in those areas, at least amongst the subpopulation looking for homes to buy or rent.

Of course, this argument does not apply to the national housing market but could be made for some of the metros on the splendid list.

Not saying I agree with this but I think it’s plausible.

The third component is the availability of supply.

We need more construction, and more regulations against ownership of unoccupied properties.

When condos are as abundant as used cars, there will be plenty for everyone who might want one and prices will be decent again.

“I’ve never seen such a shortage of properties – ever”

don’t you see it as a red warning light? That an epic extreme will be followed by no less epic swing in the opposite direction?

Unless, of course, there will be a paradigm shift – which to me looks very improbable in such area as housing.

It’s The New Normal! This Time It’s Different! Buy Now or Be Priced Out Forever!

A bubble occurs when all money goes into one thing. In 2000, it was dot com stocks, in 2005, it was housing. When almost all prices go up together, it’s not a bubble, it’s a normal repricing based on currency depreciation. It’s always been this way. It’s the old normal that everyone has forgotten.

Home price are near a record low relative to the S&P 500. They are cheap!

Japan had a colossal bubble in both RE and equities in the 80s.

And no-one disputes that it was a bubble not a devaluation of the yen.

Japan in 1989 was overvalued relative to everything else. It wasn’t a case of everything going up in value, just Japan. American equities today are overvalued relative to the rest of the world and can be called a bubble, but not its real estate. Chinese real estate is overvalued relative to everything else and can be called a bubble. I think US housing has to triple to approach the price to income ratios in China.

House is now cash. You can’t put your cash in a savings account, so you put it in a house. I’m fairly sure the median house price in the US is destined to go to a million in pretty much a straight line. The only way it doesn’t happen is when people rebel by not going to work. But the employment population ratio is higher now than after the financial crisis (2010-2013). People are still going to work. So no housing bubble.

Orthodox

“It’s always been this way.”

Never has there been a spread so wide as between interest rates as set by the Fed and inflation.

Never has the Fed owned so much Mortgage paper.

Never have 30yr mortgages been 4% below inflation.

for starters…

notice, all decisions based “nevers”……not free market forces.

ie …an arrangement.

historicus, the orthodox way of looking at it is to focus primarily one thing only: does the increase in home prices roughly correspond to the increase in money supply? Money supply growth goes through great fluctuations, but over many decades it has averaged around 7%, so you’d expect it to double every 10 years. As long as home prices don’t double more than every 10 years, they can’t be in a bubble.

In 1970, the median home price was $25,000, in 1980, it was $50,000, and in 1990, it was $100,000. See, it doubles every 10 years. But in 2000, housing became undervalued as money flowed more into tech stocks. $200,000 wasn’t reached until 2005. So Bernanke was right after all. Based on historical price appreciation, there was no bubble on a nationwide basis. So I was wrong to call the 2005 period in the US a housing bubble. Probably because I was influenced by the bearish bias of many of the things I read online. I’m very sorry about that.

I see it as a bright yellow light and I’m being more cautious. I do believe we’re much closer to the top of this cycle than the bottom. Thus my comment of maybe 15-20% more upside.

That said, I don’t see a catalyst to stop prices from rising at this point. I wish I could think of one. Massive sudden oversupply? Nope. Can’t build ’em that fast. Massive drop in demand? Nope. Demographics show huge pent up millennial demand. Oversupply of rentals? Possibly, in a couple more years.

I don’t get it. Just 10 years ago, we allegedly had a huge glut of housing. Now there’s a huge shortage? I’m not sure the population, those looking for housing, has increased that much. My hunch is the truth lies in the middle — there wasn’t that big of a glut before, and there isn’t that much of a shortage now. Oh, it may FEEL like a shortage because so many people WISH to live elsewhere or on their own or whatever. But in that sense, then there’s a giant shortage of Ferraris, too.

I think it has been discussed here at length already. You envision 10-15% upside: OK, suppose it surges this much. Or more. Or less, doesn’t matter. In most probable scenario, there should be a pullback at some point. Then what?

Will those who already own N properties continue to line up to buy the N+1th one at $100K over asking? Probably not.

There’s no shortage of housing. There’s a shortage of housing for sale

No one is eager to trade a thing that is rapidly appreciating in value (real estate) for something that is rapidly depreciating in value relative to the first thing (cash).

All it takes is a change in that unusual relationship for that sentiment to transform.

Possible catalyst is severe stagflationary recession.

I wish there existed a chance that mortgage rates could return to 6% within the next 5 years. I’m afraid the peak is near. The NDX is down nearly 4% today. The second-by-second price action is like it was in late 2018 and in March 2020. One second, the index is at 14067, the next second at 14059, then back to 14064. This erratic jumping around doesn’t stop until Powell reassures markets, and he’s smart enough to know that the longer he waits, the harder it will be to get it under control. I’m convinced we’re headed for 2% mortgage rates next (before 4%). If the ten year yield goes above 2% soon, the market is basically handing out free money to investors who are willing to bet on lower yields.

Very few people are going to sell when prices keep going up 10-20 percent year over year. It beats just about any other investment especially in an inflationary environment.

As long as the shortage of buyable cars and trucks continues, expect vehicle prices to keep marching higher and higher.

With inflation at 7% and rising, and increasing volatility and risk in the equity, RE and crypto markets, not to mention worldwide political instability, I wouldn’t be surprised to see prices up another 37% in the next 2 years, interest rate hikes or not. Rising rental car rates continue to give autos more attractive returns than most other inflated assets.

Are autos high and overvalued? Probably, but I don’t see a catalyst to turn the market any time soon, including higher auto loan rates (below 6.0%).

In my decades in the car business (selling, investing, manufacturing) I’ve never seen such a shortage of cars – ever.

I see what you did there….and I like it.

I agree. After 30 years I retired because:

No affordable land to buy [unless you want to build very high end homes].

Too much unesscesary and redundant regulation.

Too much nickel and dime taxation.

The result is an incredible imbalance between supply and demand, to where houses where I live sell for $500, $600, $700 a square foot. Almost every house gets sold in days [goes pending] and for over listing price.

The building lot just around the corner from me sold in 2020 for $760,000. They will be building a 2.5-3 million dollar house. But they have waiting close to a year for a permit, while paying interest on a construction loan, paying property taxes, and watching building costs go thru the roof.

Too many people chasing too few houses.

I know a lot of single women who are house poor after a divorce. They kept the same size home as when married and are one recession away from a disaster.

I don’t really know what happens to the guys, but they seem to do something different.

Yes many many people beyond the divorced women are one recession away from disaster. Even the fabled Silicon Valley zip codes saw an average RE devaluation of 40% during the last recession. An area of staggering high incomes.

A confluence of recession/stock market bear/RE price drops are going to wreck alot of households. And eventually we will come out of it and the next bubbles will inflate. Welcome to America.

Depends completely where you are located. Stop acting like there is a complete shortage of housing all around the country. Here in the Midwest there is an over abundance in my opinion. I see new apartment building coming up by the dozen in my city that has a DECLINING POPULATION. There are no more fixer uppers, they’ve mostly been boughten and fixed up. Senior living centers are exploding to handle all of the elderly population. I’ve seen 3 news mega senior living centers just in my suburb over the last 3 years. Prices should be going down with this excess in supply. The reason they aren’t is because investors are buying up multiple properties and either sitting on them or trying to rent them for exorbitant prices. In a year or two when things go south these new studio apartments renting for $1700 in a declining rust belt city will be decimated.

Thanks for that feedback.

“By tracking the price of the same house, it tracks how many dollars it takes to buy the same house over time, thereby tracking the loss of the purchasing power of the dollar with regards to houses. In other words, it tracks house price inflation.”

So by this logic, if home prices decrease, could we say that the value of the dollar has increased? Essentially erasing that part of inflation (loss of purchasing power)? Or could we infer that with interest rates declining over time that the cost of borrowing is a key factor to consider in evaluating the purchasing power of the dollar.

MarkinSF,

“So by this logic, if home prices decrease, could we say that the value of the dollar has increased?”

Not the “value” of the dollar, but the “purchasing power” of the dollar would increase.

Interest rates are a separate item: the “cost of capital.” And yes, the cost of capital will go up. And it needs to. It’s still negative right now (far below the rate of CPI inflation).

Not the “value” of the dollar, but the “purchasing power” of the dollar would increase.

My point is that they’re synonymous (in effect). Since declining interest rates lower the cost of housing, that factor must be considered in evaluating how much the “purchasing power” of the dollar has declined. If a house was $100k 10 years ago and the rate was 10% and now it’s $300k at a rate of 4% you can’t really say the dollar has devalued proportionate to the increase of $200k.

Am I wrong?

I follow you MarkinSF. Yes, you are right.

Interest rates are the “price of money”.

Which is why the Fed should not raise rates, or it will make inflation worse…

That’s the deception of central banking. Asset values get boosted as rates decline. But that’s a one time gain, and now you have a much levered system that can not handle a 2% rate increase. It’s limited by the debt service and you are locked into a future where real asset returns can’t go up.

If you hear gentle sobs from the SW it’s just me seeing that graph sitting in my rental house in Phoenix.

They are already Az cities poaching each other’s water, be glad you can walk away without the headache of carrying a ball and chain.

Why when house prices go up media calls it “price growth “ instead of just plain old “inflation”?

Because every single person with any say over how things are described in the media owns at least one piece of real estate. Housing “price growth” is to every one of them an uncomplicatedly good thing.

Exactly… That’s exactly what I was objecting to. They frame it as “price growth” instead of “loss of purchasing power”, as if it’s a good thing to make it harder for everyone to own a place to live.

There’s some value to the notion that if your own home goes up in value, you have more equity you can cash out to pay for your last-year medical expenses, but you generally aren’t going to sell your home before then, and until that point the price of your home is irrelevant except for your tax bill. But that whole time, that high price just means your kids can’t even afford a place to live … other than your basement.

It ain’t right.

“There’s some value to the notion that if your own home goes up in value, you have more equity you can cash out to pay for your last-year medical expenses, but you generally aren’t going to sell your home before then, and until that point the price of your home is irrelevant except for your tax bill.”

My plan exactly as we did not buy expensive LTC insurance (couldn’t afford it at the time and I didn’t like the value). Our home, currently paid off, will cover LTC expenses for both of us if that is needed when the time comes. Otherwise, the value when sold is going to be part of the kid’s inheritance.

because the powers that be are gaslighting us. describe a bad thing as a good thing, using positive language, and people will start to believe it, even if it’s bad for them, and bad for society.

Jake W

Gaslighting is the correct language. Home price appreciation is mostly dollar devaluation. It does no one any good except the parisites that feed off this inflation. Even the homeowner doesn’t get much benefit. Higher property taxes, paper gain that is locked in until the property is sold, higher maintenance costs as the property ages, higher homeowners ins premiums. MY house has doubled in value since I bought it over 20 years ago. I’ve made nothing in constant dollars after adding in all the home improvements and maintenance that had to be done. All I’ve gotten is a roof over my head. That’s OK for me.

I’m wiped out, Party People. I cannot fathom another year like 2021.

I don’t know if the flattening in DC is due to prices or the lack of satisfactory inventory. There’s not a lot of appealing options on the market, but everything that’s coming up is going into 10+ offers with $100,000+ over asking.

The world’s gone mad.

Fortunately, the US is not the whole world :)

Except this is happening around the world

Not everywhere.

Italy and Spain for example.

Check out Finland. You will see why it’s rated the happiest country

@ CCCB

Only where you have money lender friendly central banks and politicians.

Melissa Terzis,

“I cannot fathom another year like 2021.” Totally agree.

Just a reminder: this data is for the metropolitan area, not just DC. The metro includes:

District of Columbia DC, Calvert MD, Charles MD, Frederick MD, Montgomery MD, Prince Georges MD, Alexandria City VA, Arlington VA, Clarke VA, Fairfax VA, Fairfax City VA, Falls Church City VA, Fauquier VA, Fredericksburg City VA, Loudoun VA, Manassas City VA, Manassas Park City VA, Prince William VA, Spotsylvania VA, Stafford VA, Warren VA, Jefferson WV

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

Things are hyper local though. Some of the areas in the list are so different than DC. We are nowhere near gloom and doom in DC, Montgomery County, Prince George’s County, Arlington, Alexandria, Fairfax.

Melissa Terzis

This information that you are putting out is either totally bogus information or only applies to a narrow area where you may work, and for a specific type of property where there may be high demand (high end buyers). We just a comparable analysis of some condos near Dupont circle (my kid owns one) and the market sales show the prices have finally recovered from the pandemic slump and riots, when everyone left DC for the country or far out suburbs. The appreciation for entry level homes is roughly in line or slightly below the overall Inflation rate. Nothing out of the ordinary. We have over 30 comps. They can’t be all wrong.

In Southeast, Washington D.C. away from Capitol Hill where we do most of our work I see some signs saying “Price Reduced”. Check out 226 Kentucky Ave SE, where a historic 4 unit was converted to a condo. I used to live there, before a fire burned the place to the ground. They did a complete renovation and are having trouble selling the units.

I like less animosity in comment replies but I will respond. Also do not appreciate being called as someone giving bogus information as I’m one of the few agents I know who tell it to people straight.

You are speaking of condos. Condos are a totally different animal. Everyone knows they fell out of favor when the pandemic hit.

This is a conversation about houses. Houses from DC to suburban Maryland to Virginia are getting 10+ offers again. If it’s in a decent area, priced remotely close to market value and offers a yard and space to WFH, it is in high demand.

Of course condos are sitting. No one wants condos right now.

Melissa Terzis

“Of course condos are sitting. No one wants condos right now.”

Condos are doing just fine in DC even with the pandemic. If they are in a decent location and are priced correctly (not overpriced) they sell within a few weeks. This is the normal market. About 4% price appreciation over the past year. I have the comps to prove it. They haven’t done as well as townhouses but that has always been the case. We’ve appraised a half a dozen in the last two weeks. We are swamped with work. We just did one that was only 400 sq feet, and sold for $385K. It was in great shape and sold in a week. Right near Dupont Circle.

If you don’t want to take condo listings, that’s your choice. But for a lot of Veterans and entry level 1st time home buyers, that’s all they can afford. They are buying Condos as starter homes. Good for them.

Update from Boston: seems like buyers came back over the last 2 weekends. Homes listed at over $1.3M have had 40 groups of people visit in a weekend of open houses. Offer of 125k over ask with contigencies declined. Listing agent resonded with “this is going for much more, honey”

In another open house (similar price range), offer accepted $175,000 over asking price. absolutely no contingencies whatsoever.

Last year, it seemed like only some people would waive all contingencies, but most would not waive inspections. This year it seems like waiving everything is what it takes to win. (which is scary for a place with almost the oldest housing inventory in the nation). Oh by the way, its never been like this in January.

Low inventory + “New Year, New goals” + FOMO with predicted interest rate hikes. In my opinion.

Johnny Provolone,

Watch the Nasdaq’s impact on the Boston housing market. I’ve tracked this for San Francisco. A Nasdaq decline of over 20% that is sustained, with IPO stocks getting annihilated and IPOs coming to a halt, will hit housing in SF with about a four month lag. Boston, like SF, has a lot of people with stock options in tech and biotech startups. SF’s housing market is more dependent on the Nasdaq than on mortgage rates – and Boston might be similar. So keep your eyes on stocks.

Definitely with the IPO and startups. i’ll keep a finger on the pulse of the nasdaq. happy to keep you updated on the Boston market as im boots to the ground in real estate here.

Case-Shiller doesn’t have Austin data but according to some other sources it’s the hottest housing market in the country with price appreciation outpacing all the ones on the “splendid” list.

One wonders if Austin like SF and Boston might also have become correlated more with tech stock prices than mortgage rates and if so what a Nasdaq bear market might do to it.

In terms of Austin, I would think now more so than ever. Tech is huge there, including from the recent influx from the Bay Area (including two of my neighbors), and yes, huge price spikes.

Too bad the CS data is not available for Austin.

Took my vacant land off the market, and told the agent to raise the price. He balked, did some comps over the w/e and agreed. The only interest the property is getting is other agents and contractors. The cost and time frame to develop a SFH is whats driving inflation. The cost of asphalt mix, and sewer line, and permits permits permits. On the other hand if you can buy a termite ridden shack, throw some stucco on the outside and double the value, the city planners will give you their blessing. For new construction even modulars are running 200 a sq ft. My logic behind raising my price is one, housing prices will rise, burnt out stock investors want real assets, or two, the price of housing actually falls, and that allows the price of land to catch up. The value of a project is constant, the variables are adjusted accordingly: land, materials and labor, and mortgage costs (still historically low). Three, any home built on this land will be a million dollar project, and raising the cost of the land 10% (land is 1/3 of the total value) is a marginal cost increase, if you have the right property that is a small premium.

i hope anyone dumb enough to put in an offer waiving inspection ends up with a house with foundation problems, black mold, and termites.

these people are the collective problem.

If you just purchased it you could literally just relist it and make more money and try again.

Jake W

Even with an inspection the home buyer can get screwed. I’m still fixing things in this house I bought 20 years ago that the inspection never uncovered. It didn’t help that the inspector worked for the listing agent’s RE company.

agreed, but you can only do so much. i’m sorry you got stuck with a bad inspector, there are a lot of scumbags out there.

but anyone who buys without one at all is an idiot. full stop.

Jake, Here’s a nightmare house to make you feel better..

I bid on a property last year and lost to cash buyers who bid much higher. Cash. The foundation was sinking, the roof was way overdue for replacement, it needed new electrical wires throughout and probably plumbing. And, lol, the cherry on top was that a corner of the original house was taken out, an addition build onto that corner AND that entire corner of the original house was being held up by only a freaking pine plank BOOKSHELF. OMG. Warped to hell of course.. Still, I figured it was a smallish shell I could work with.

& I was sort of OK with all that at a really low bid, but finally pulled back when I saw evidence that the house had been used as a pot grow room without waterproofing the floor! At first I couldn’t figure out why they used T-11 plywood as wainscotting.. Hah, the studs in the walls were rotted from the floor to about 3 feet high. Also, floor framing had to be shot. Water from a hose had gushed all over the floor 3 or 4 days a week for years. OMG, what a wreck.

Those people who bought it bid cash well over asking, over the internet within 3 days without ever stepping foot in the house. They had no time for an inspection. I doubt they had any contingencies on an “as-is” house.

So.. there you have it.

Lynn,

This confirms the old adage from banking: bad deals are made in good times. And the worst deals are made in the best times.

People should be very very careful about waiving *ALL* contingencies. There is one you don’t want to waive no matter how much experience you have. I bid on a house last year (and lost, of course) with no contingencies. I did all my homework and me and a contractor checked the house out. I have some structural construction experience.

What really really got me was while reading the bid contract I was to sign I noticed the selling agent put in *title* stuff as noncontingent!! Like- if the title had problems- too bad. If they didn’t fully own the house- too bad!! I would still have had to pay. I had him rewrite it.. Was outbid by 30% cash of the asking price, but learned a good lesson.

As I was just reading today’s Business section of the Minneapolis newspaper, the from page had this data for the Twin Cities:

In 2021, 66,319 properties closed; up 2.7% from 2020. Median sale price went up 11.4% to $339,900.

Market time was 28 days, and this was 40% faster. Big takeaway was million dollar homes sales were up more than 50% from a year ago, and they had “steep decline in market times for these properties.”

Will the Twin Cities’ high end properties keep going up as a hedge against the stock & bond markets and inflation? I would think so. But, if the market drops hard, will that take out the high-end buyer?

I just bought a house in twin cities area, probably shouldn’t have because I know they are overpriced, but my rent is going up $400. Renting a decent townhouse is well over $2,300 now, might as well buy a overpriced house.

My mortgage guy, who is also a friend, said he has 40 people lined up for houses, he has never had so many. He also stated 20% are investors where it used to be 5%. Any housing decline will be bought up by investors buying with cash. I could be wrong, time will tell. But in my point of view, if you want to own a house, time is running out. I mean I even see investors advertising that they will purchase a home for you and you can just rent it from them.

Jon,

You are putting rent money into your new home, and if inflation stays where it is — or close — for awhile, your mortgage payments will soon seem not that large (as they probably do now).

I always look at the price per square foot as my “value metric” and if inflation continues, you’ll see that price/sq-ft go up in step.

Good luck to you & all the best …

The Woodlands, Texas, north of Houston, HCOL area (for around here). There are a few houses on the market in our 437 home, 55+ community of 20 year old brick and Hardiplank homes that are for sale and prices are being slowly reduced. Maybe it’s because of the weather and the time of year?

But, these are very nicely built homes with a reasonable HOA fee ($200/month) and homes that sold recently were priced at about $175/sq. ft.

Last summer, when the craziness was in full swing, homes here were on the market one day and sold. I hear that full price offers were the norm for those sales. I have no way of knowing if offers over asking were put in.

It’s either not buy, buy, buy, madness everywhere, or somehow we got skipped over by the crazy buyers with pockets full of Benjamins.

Don’t move to Nebraska property taxes on house valued at255,000 taxed at 5100 rediculios but wife won’t move

That’s a bargain compared to Chicago.

“buy, buy, buy, madness ”

You’re starting to sound like that huckster Jim Cramer.

Yeah, I watch the show too much. I was even thinking of joining the Club, but my wife talked me out of it!

Anthony A.

Smart move

I guess the null hypothesis is that during the pandemic authorities have restricted people’s ability to do things and spend outside their homes (school, work, dining out, traveling, vacationing etc.) even confining them to their homes in some extreme cases. So people are more willing and able to spend a bigger proportion of their income on housing than prior to the pandemic. Also pandemic-induced supply problems of building materials and construction labor shortages have limited new supply.

So pandemic restrictions have increased demand and reduced supply similar to other goods like home exercise equipment, causing prices to rise.

Of course, when pandemic restrictions end, peoples’ activities and spending patterns may normalize causing these forces and prices to go into reverse. Or maybe they’ll be a new normal after the pandemic.

Is there any data that refutes the null hypothesis?

At this point, falling mortgage rates don’t explain the price changes since rates are now back to where they were before the pandemic.

And expected to go higher, hence panic buying.

yes. if that was true, then city condos would have plummeted in price. they generally haven’t anymore, after 2020. which basically means that it’s just interest rates and the “wealth effect.”

How can many who bought houses “return to normal activities” if their disposable income is now being eaten up by housing expenses.

One area gains, another loses to maintain balance.

Wait til property taxes start increasing…only then will we see damage when that reality hits.

As a construction worker/contractor for 35 years, IMO white collar people in the US have no clue. My guess is home prices will not go down, and if they do it’ll be far less than other markets. THIS is because no on in the US wants to get their fingers dirty. PBS ran a segment where a plumbing company in Seattle cannot find employees despite paying $20/hr to people learning and 6 figures to qualified plumbers. Millennials consider blue collar people as losers. The Protestant Ethic is dead in America. PLUS taxes and fees are in many cases absurd. Dream on about cheap well built homes.

My guess is over time technological advancements would make building homes very cheap. Think 3D printed homes.

I know blue collar workers may not get this but I think this is coming.

USA has no dearth of land and technology would make it cheaper.

I am a white collar worker and do a lot of handyman job on my own because of available knowledge base made possible by technology.

I don’t know about that. We used the printing technology to make engineering prototypes of pump parts at work. It took about four houses to make a part. Once design was proven the manufacturing process could make the part in 5 minutes.

Roughly 4000 hours in building a home. So you can start there with costs. If your labor costs averages $50 you are at $200,000. I bet where I live labor costs is more like $25 per hour or $100,000 labor. Lots are $30,000. Material, fees, over head run the price to about $350,000 for 1700 sq ft upscale starter or retired home.

That’s what civilians think. There are incremental advancements but there is a reason that traditional construction prevails. Lawsuits. Tried and trusted stuff is how it works. My best client can build a 10 million dollar home in 3 months… because he’s old school, no curves, no nonsense just rectangles and the best materials and subs… geodesic, PP pipe failure, steel containers… good luck building with those. People (including myself and I have a degree in design) keep trying to “improve” what I do with products that cost more and are more likely to fail… not likely in my lifetime. More likely guys like me will retire and homeowners will pay more and sue contractors more leading to higher contractor insurance.

Oh, in a few years tech workers will be a dime a dozen while plumbers [and electricians and framers and roofers and siders and concrete workers] will be driving Rolls-Royces and retiring at 45.

Somebody has to do it if you want to live in a house.

Wouldn’t be a bit surprised if ”The Pendulum” swings that way for a while EL! Seems to have already started swinging that direction to some degree many places, but especially places where housing is SO expensive.

Meanwhile, to my certain knowledge and quite opposite the opinion of many, there are plenty of skilled manual workers available in the construction industry.

The problem is that they want to receive ”fair pay”…

While ”fair pay” is an easy thing to say, even some organized labor folks are not being paid fairly by the time all the deductions are taken out of their nominal pay.

30 years ago, a young person was able to convince me that his fair pay at age 16 was almost exactly TEN TIMES what my fair pay had been at that age almost exactly 30 years previously; that was an epiphany…

far shore

U better include truck drivers ,everyone is tired of Ivy League theft of the American dream 93 million a year ludicrous

“there are plenty of skilled manual workers available” He he. When I go to a jobsite to do my job the only things I have to fix before I begin are the plumbing, carpentry, concrete and drywall. In other words everything. Time is money, its more cost effective for workers to let the next guy fix his work… when I see the stuff American’s build, like most contractors I want a Japanese truck even if they are twice as expensive.

Cost to build a house says a lot about society. It’s made with real stuff and real labor and has value. US has so many jobs that provide very little value and the cost gets spread to society as inflation.

What is the value of pumping $15,000 dollars of education in per year to a kid that doesn’t want to learn and goes out and gets himself killed trying to be a gangsta. School can’t replace a parent.

What’s the value educating someone in college if the degree is never used?

That’s why I don’t bother with ‘buying’ a house. I can’t be bothered to even deal with blue collar contractors like you. I prefer my hands clean and well manicured, and tend to my hobbies which are entirely intellectual in nature. When I need something done I just call the building management, they can deal with it while I am away. I value my time on this planet, it’s too short to waste on chores and unrewarding labor. Ciao!

I have seen the same house (kit) starting price in April of 2019 valued at 250K is now selling for 598K. It is 2200 square feet installed in the same county. That same house took 4 months to build now takes 12 months. There is no longer guarantees that it will be delivered whole. I had the house kit and installed price itemized out for tax purposes. The kit itself (wood, windows, drywall, etc) with exception of HVAC and Appliances cost 60K in total for all the supplies. It is up 12K more in supply cost. Most of that is in wood or shipping cost. That means fees and labor that 538K that is subpar at best. All because they can charge it. Hmmmm… Maybe I need to figure out how to build my own home.

Two other advantages to building your own home that I found out when I built mine was, when the house is finished, the county tax assessor (in California anyways) appraises it for what your expense was, including land, and not the value of a completed house. This can be a big savings, 20% to 30%, and because of prop 13 it stays lower comparatively.

Also when you hire someone to build it, that person has to charge you enough to not only cover his labor and expense’s, but also the income tax he pays to the state and Feds. When you build it yourself that sweat equity is not taxed.

I know a couple that thought they’d *save* money managing their own remodeling / construction project. The original budget was $200K….. He had experience as an engineer for oil pipelines in the Middle East and friends who were contractors. His wife wanted to manage the project in order to save the 20% that the GC wanted.

They spent nearly $500K before he pulled the plug on his wife because she was attempting to act as the general and didn’t understand the sequence that the trades have to complete their work. She didn’t work with their contractor friends and chose to hire her own subs.

Plumber came in…. then drywaller….. then electrician had to punch holes in the new drywall to fish wires…. then the flooring was done (hardwood) and the painters came in and scratched the hell out of them. No one did QC on the work being done (other than code inspectors) and little things like roof drains not being connected (flat roof for a view patio) caused the roof to drain into a first floor bedroom during the first rain – causing the ceiling to fall, the mattress to get soaked, and the flooring to be ruined yet again. Door swings the wrong way, causing the doors to hit one another. One of the funniest was when they spec’d out the exterior doors, including installation. Of course, they forgot to put in the bid request little things like weather stripping, door lock bores, and the like. The look on her face was priceless when she couldn’t secure the house and the door leaked when it rained. She ordered appliances that were too deep for the cabinet boxes – which required the backs of the boxes to be cut out as she used the wrong dimensions when she ordered them…..

There was more, but you get the picture.

Youtube is no substitute for real world problem solving experience. Youtube is of most value when you have a problem to solve…. not how to frame a house and properly distribute load to the foundation. Most people try to build and repair things without buying the proper tools and materials – which makes the final product appear amateurish, causes frustration (and the built in hate of DIY projects), or they hurt themselves.

Agree 100percent. In commercial/industrial work, experienced subcontractors and GC/job supers know to maintain good communication, because the lack is so costly and margins are slim, given the inherent problems in construction. In custom residential, indecisive or misinformed customers are the biggest P in the A for builders, especially electricians and trim carpenters. Or they’re just jerks, a former NFL star from around here has a record of treating contractors I know like dirt, companies turn his business down routinely. I could handle all the trades if it was my house being built, but now I know better, pay someone to let me do what I know how to do while they deal with the subs and suppliers and endless headaches.

If I was building. Now is not the time.

Here is not the place.

El Katz,

Wow, poor couple.

When I said build it, I mean actually doing the work yourselves. I did everything, except grading and HVAC, that’s how you save a lot. All this while working a 40 hour a week job.

If he just wants to be a GC, and he is an oil engineer, any engineer, and managed the project like any good engineer does by correctly budgeting and project managing, this would not have happened. Alas he let someone handle it that did not think it through.

If you can manage projects you can get a house built, yes it’s a lot of work. but its not that hard.

Although like Rick M said maybe its not a good time to do it with all the shortages and such.

Great buying opportunity!! LOL… the sheep always get slaughtered, sooner or later.

Wolf I wish you’d do a chart for the Atlanta market?

breamrod,

Atlanta doesn’t qualify for this list. The index is up “only” 100% since 2000:

Case Schiller does cover Atlanta on the FRED site.

It’s covered on the S&P CoreLogic Case-Shiller site, which I linked in the text. But to download the actual data, you need to have a login.

As long as the shortage of buyable cars and trucks continues, expect vehicle prices to keep marching higher and higher.

With inflation at 7% and rising, and increasing volatility and risk in the equity, RE and crypto markets, not to mention worldwide political instability, I wouldn’t be surprised to see prices up another 37% in the next 2 years, interest rate hikes or not. Rising rental car rates continue to give autos more attractive returns than most other inflated assets.

Are autos high and overvalued? Probably, but I don’t see a catalyst to turn the market any time soon, including higher auto loan rates (below 6.0%).

In my decades in the car business (selling, investing, manufacturing) I’ve never seen such a shortage of cars – ever.

As a matter of fact, I expect car prices to continue to go up for the next year or so too – not 37% though. And Interestingly enough, people ARE investing in rental cars. Look up turo.com. It’s like an airbnb for cars. Depreciating asset though.

And I wouldn’t be surprised to see higher rates offset by longer term loans. I never finance, but I think we’re up from 2-4 years when I was a kid to 7 years now. 50 year mortgages and 15 year car loans next?

I read where Toyota is experimenting with a car ‘refurbishing’ program. Every 3 years the car would be put back to new factory specs. This would happen again 3 years later. If the original owner was eligible, you would start on on year 7 with a mechanically new vehicle. A 15 year loan may find a place there.

Nonsense – cars are not a depreciating asset.

Used car prices increased 37% last year alone.

That’s the new normal now that the pandemic has changed everything.

Car prices will never go down again….ever

Economics 101. Government had about as bad of a policy response to the Pandemic as possible. Restrict supply and have a cash drop to raise demand. Takes about year for the insanity to work through the system.

Enjoy waiting on-line to buy over priced stuff.

The market has gone crazy here with houses so expensive, that used garbage trucks are being sold as RV’s with elevators, after retrofitting.